2-1

Environmental factors on Financial Reporting

• Presentation objectives• Understand factors influencing financial

reporting• Discuss the primary qualities of (Accounting)

financial statement information• State Alternative information sources• State Limitations of Accounting Information• Discuss the concept of Fair Value Accounting• State and discuss the steps of financial Analysis

2-2

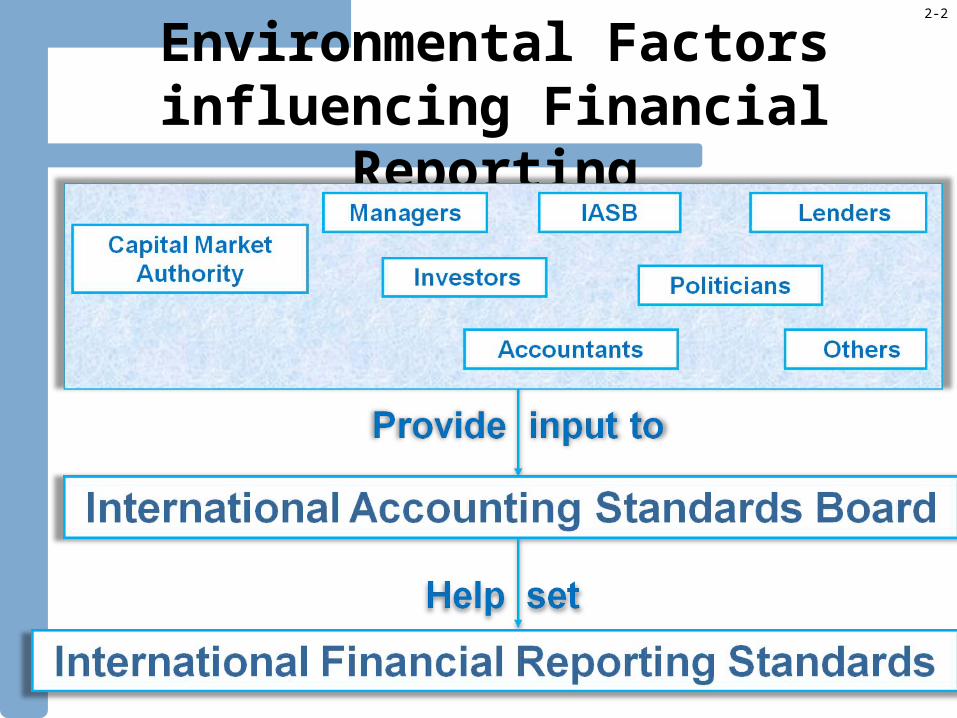

Environmental Factors influencing Financial Reporting

2-3

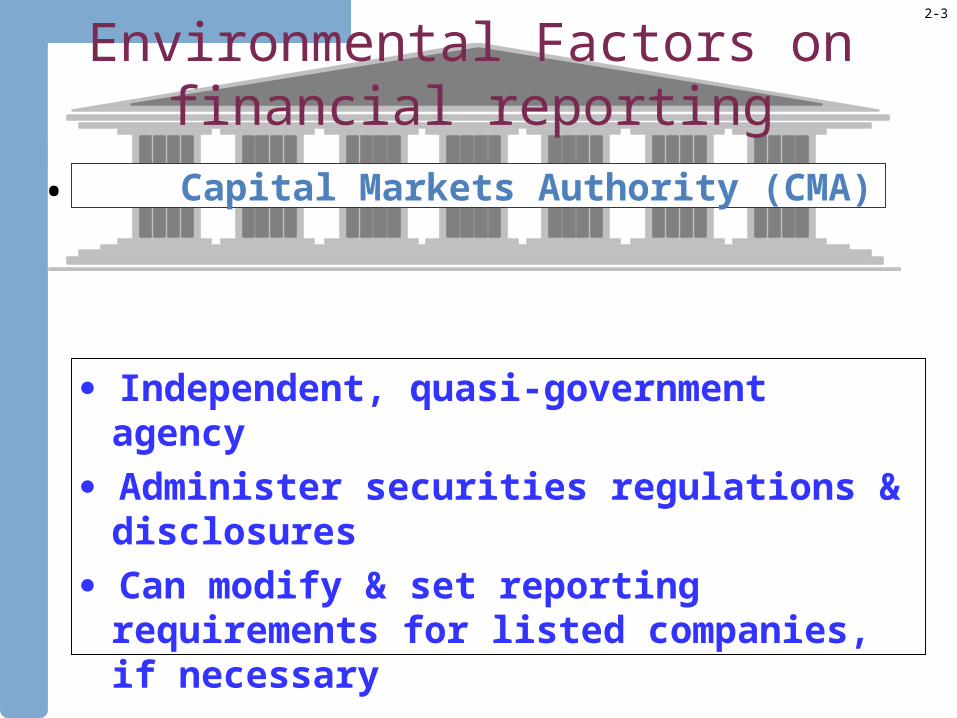

Environmental Factors on financial reporting

• . Capital Markets Authority (CMA)

Independent, quasi-government agency

Administer securities regulations & disclosures

Can modify & set reporting requirements for listed companies, if necessary

2-4

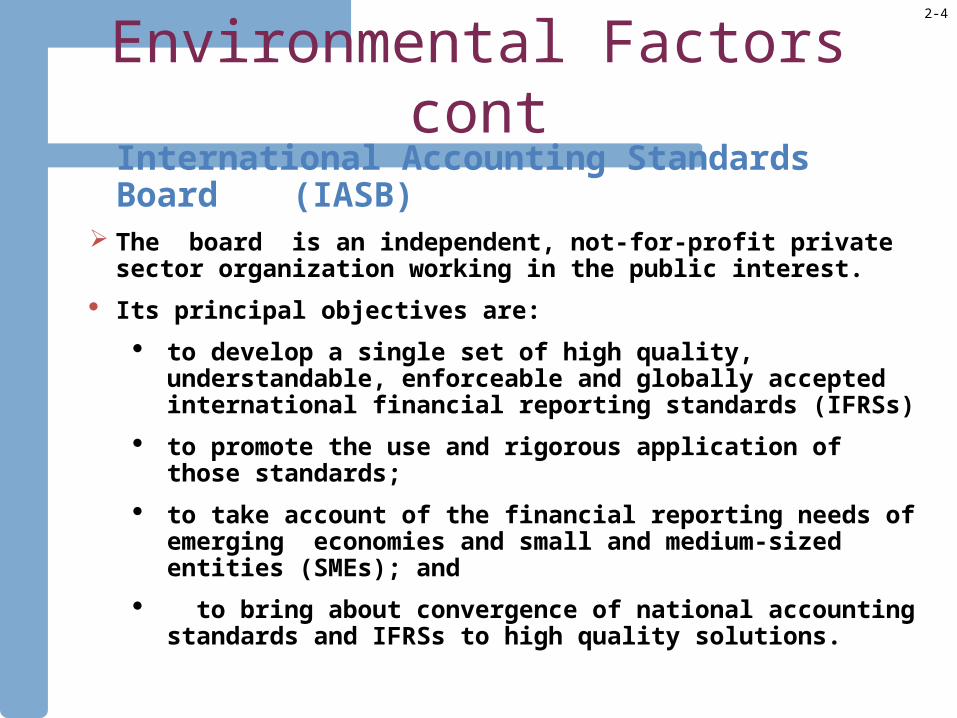

Environmental Factors contInternational Accounting Standards Board

(IASB) The board is an independent, not-for-profit private sector organization

working in the public interest.

Its principal objectives are:

to develop a single set of high quality, understandable, enforceable and globally accepted international financial reporting standards (IFRSs)

to promote the use and rigorous application of those standards;

to take account of the financial reporting needs of emerging economies and small and medium-sized entities (SMEs); and

to bring about convergence of national accounting standards and IFRSs to high quality solutions.

2-5

Environmental Factors

International Financial Reporting Standards (IFRS)

International Financial Reporting Standards (IFRS)

2-6

Environmental Factors

Managers of Companies

o Primary responsibility for fair & accurate reports

o Applies accounting to reflect business activities

o Managerial discretion is necessary in accounting

o Major lobbyist on IFRS

o Primary responsibility for fair & accurate reports

o Applies accounting to reflect business activities

o Managerial discretion is necessary in accounting

o Major lobbyist on IFRS

2-7

Environmental Factors

Auditingo CMA /Legislation requires Audit Reporto Audit opinion can be:

o clean (fairly presented)o qualified (except for)o disclaimer (no opinion)

o Check Auditor quality & independence

o CMA /Legislation requires Audit Reporto Audit opinion can be:

o clean (fairly presented)o qualified (except for)o disclaimer (no opinion)

o Check Auditor quality & independence Auditors

2-8

Environmental Factors

Corporate Governance

o Board of directors oversighto Audit committee of the board

o oversee accounting processo oversee internal controlo oversee internal/external audit

o Internal Auditor

o Board of directors oversighto Audit committee of the board

o oversee accounting processo oversee internal controlo oversee internal/external audit

o Internal Auditor

2-9

Environmental Factors

Internal UsersInternal Users External UsersExternal Users

2-10

Alternative information sources

Voluntary DisclosureVoluntary Disclosure

Economic, Industry & Company NewsEconomic, Industry & Company News

o Impacts current & future financial condition and performanceo Impacts current & future financial condition and performance

Information IntermediariesInformation Intermediarieso Industry devoted to collecting, processing, interpreting &

disseminating company information

o Includes analysts, advisers, debt raters, buy- and sell-side analysts, and forecasters

o Major determinant of IFRS

o Industry devoted to collecting, processing, interpreting & disseminating company information

o Includes analysts, advisers, debt raters, buy- and sell-side analysts, and forecasters

o Major determinant of IFRS

Motivation - Legal liability, Expectations Adjustment, Signaling, Managing expectations

Motivation - Legal liability, Expectations Adjustment, Signaling, Managing expectations

2-11

Desirable Qualities of Accounting Information

2-12

Desirable Qualities of Accounting Information cont…

o Reliability - For information to be reliable it must be verifiable, representationally faithful, neutral and reflect substance . o Verifiability means the information is confirmable. o faithfulness means the information reflects realityo neutrality means it is truthful and unbiased.o Substance over form- means information

presented in accordance with its substance and economic reality and not merely its legal form

2-13

Financial Accounting

o Historical Cost - fair & objective values from arm’s-length bargaining

o Accrual Accounting - recognize revenues when earned, expenses when incurred

o Materiality - threshold when information impacts decision making

o Conservatism - reporting or disclosing the least optimistic information about uncertain events and transactions

o Historical Cost - fair & objective values from arm’s-length bargaining

o Accrual Accounting - recognize revenues when earned, expenses when incurred

o Materiality - threshold when information impacts decision making

o Conservatism - reporting or disclosing the least optimistic information about uncertain events and transactions

Important Accounting Concepts

2-14

Financial Accounting

Relevance of Accounting InformationRelevance of Accounting Information

Relation between Accounting Numbers and Stock Prices Relation between Accounting Numbers and Stock Prices

2-15

Financial Accounting

o Timeliness - periodic disclosure, not real-time basis

o Frequency - quarterly and annually

o Forward Looking - limited prospective information

o Timeliness - periodic disclosure, not real-time basis

o Frequency - quarterly and annually

o Forward Looking - limited prospective information

Limitations of Accounting Information

2-16

Revenue Recognition – recognize revenues when

(1) Earned

(2) Realized or Realizable

Expense Matching – match with corresponding revenues

- Product costs

- Period costs

Revenue Recognition – recognize revenues when

(1) Earned

(2) Realized or Realizable

Expense Matching – match with corresponding revenues

- Product costs

- Period costs

Accruals-The Cornerstone

Foundations of Accrual Accounting

2-17

Accounting concept of income

o Based on the concept of accrual accountingo Main purpose is income measuremento Two main processes –

o Revenue recognition o Expense matching

o Based on the concept of accrual accountingo Main purpose is income measuremento Two main processes –

o Revenue recognition o Expense matching

2-18

Fair value accounting

Asset and liability values are determined on the basis of their fair values (typically market prices) on the measurement date (i.e., approximately the date of the financial statements).

Asset and liability values are determined on the basis of their fair values (typically market prices) on the measurement date (i.e., approximately the date of the financial statements).

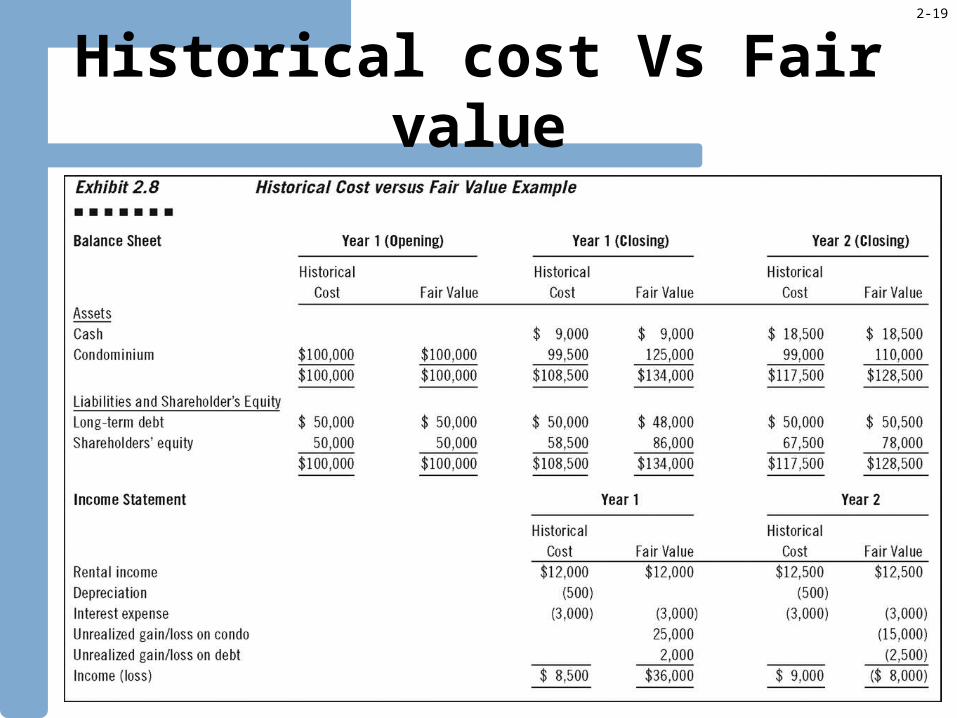

2-19

Historical cost Vs Fair value

2-20

Advantages & Disadvantages of Fair Value Accounting

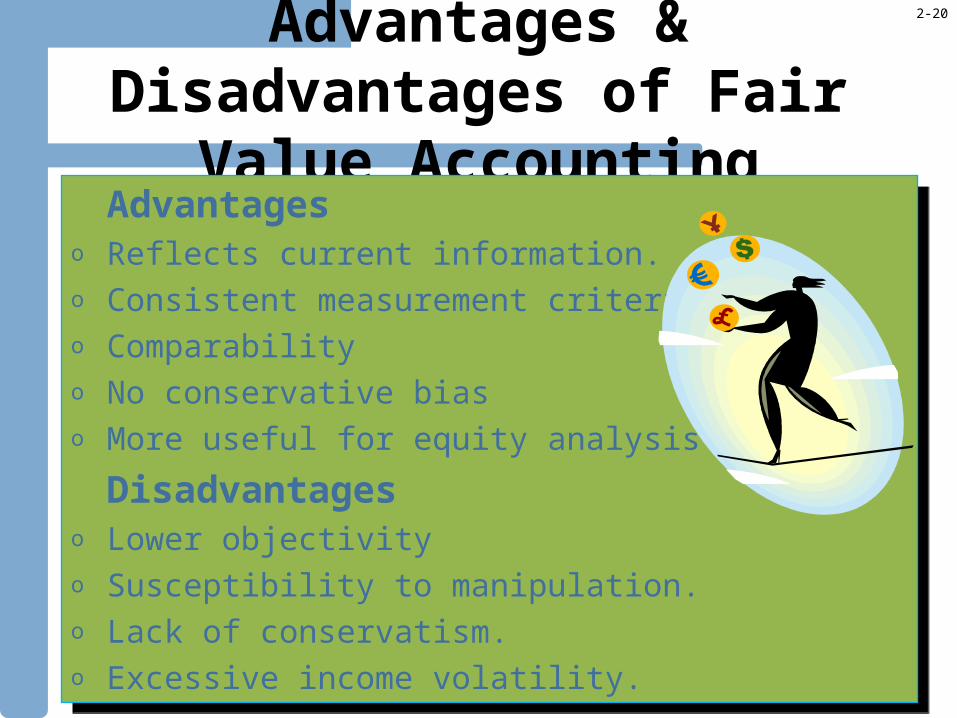

Advantageso Reflects current information.o Consistent measurement criteria.o Comparabilityo No conservative biaso More useful for equity analysis

Disadvantageso Lower objectivityo Susceptibility to manipulation.o Lack of conservatism.o Excessive income volatility.

Advantageso Reflects current information.o Consistent measurement criteria.o Comparabilityo No conservative biaso More useful for equity analysis

Disadvantageso Lower objectivityo Susceptibility to manipulation.o Lack of conservatism.o Excessive income volatility.

2-21

Implications of Fair value Accounting for Analysis

o Focus on the statement of financial position (balance sheet).

o Restating income.o Analyzing financial liabilities.

o Focus on the statement of financial position (balance sheet).

o Restating income.o Analyzing financial liabilities.

2-22

Financial Analysis Process

• Financial analysis is the process of evaluating financial and other information for decision-making.

• A six-step approach is suggested for systematic financial analysis.

2-23

Financial Analysis Process –The Steps

1. Identify purpose of financial analysis2. Corporate overview3. Financial analysis techniques4. Detailed accounting analysis5. Comprehensive analysis6. Decision or recommendation

2-24

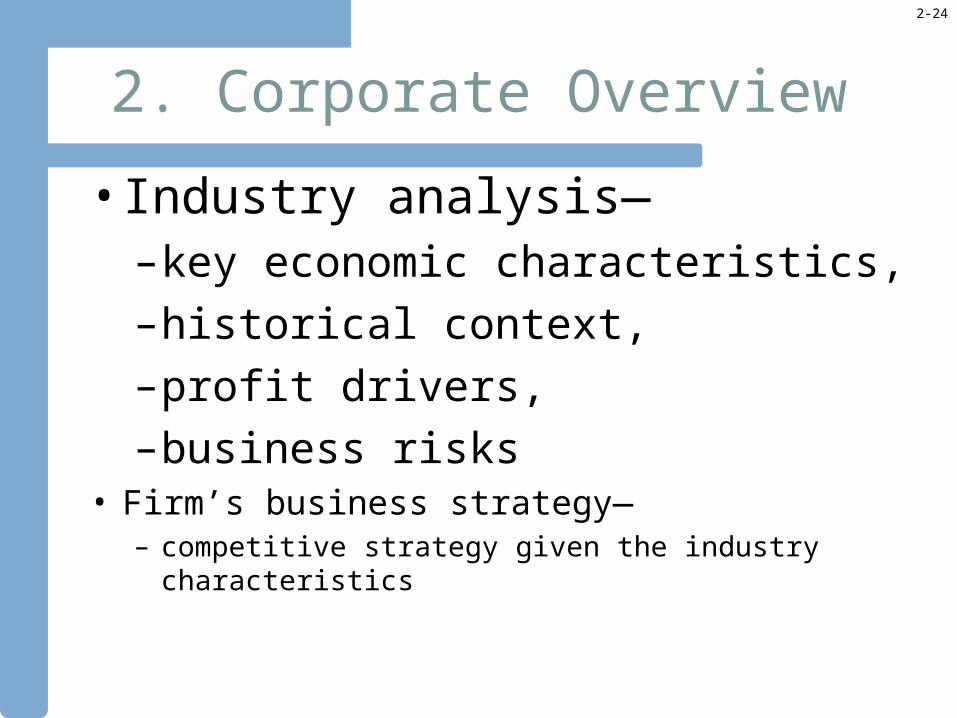

2. Corporate Overview

• Industry analysis—–key economic characteristics, –historical context, –profit drivers, –business risks

• Firm’s business strategy—– competitive strategy given the industry characteristics

2-25

2. Industry Analysis

• Competition—• Evaluate:growth rates, concentration ratios, degree of product differentiation, economies of scale relative fixed & variable costs, substitute products

2-26

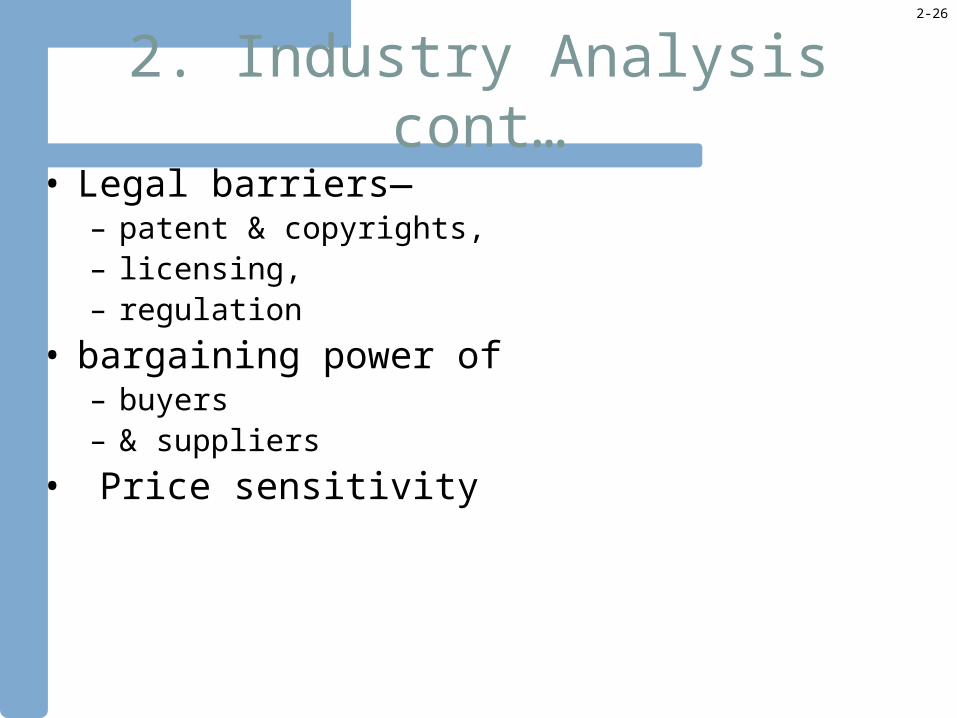

2. Industry Analysis cont…• Legal barriers—

– patent & copyrights, – licensing, – regulation

• bargaining power of – buyers – & suppliers

• Price sensitivity

2-27

2. Industry Analysis Criteria

• What is the industry?• Relative size & significance• Largest companies• Geographic presence• Business cycle effects, current

situation• Future potential

2-28

2. Business Strategy

• Cost leadership:• Achieved through: low cost producer, economies of scale, efficient production, low input prices

2-29

2. Business Strategy cont…Product differentiation: specific attributes that customers value e.g.,

quality, variety, service, delivery time,

brand nameImportance of core competencies

2-30

2. Business Strategy Criteria

• Historical perspective• Primary focus of operations• Most important strategy• Major operating segments• Corporate outlook/ forecast

2-31

Qualitative Analysis Practical Example--Dell Computer

• Industry—– primarily PCs:

• high tech, • competitive (e.g., Gateway, IBM, Apple, others), • changing products, • high growth rates,• low barriers of entry

2-32

Qualitative Analysis Practical Example--Dell Computer cont…

• Business strategy—• (1) cost leadership strategy:

– direct selling,– made-to-order manufacturing, – early on the internet, – low receivables;

• (2) product differentiation?? – IBM clones,– Intel & Microsoft components

2-33

Qualitative Analysis Practical Example--Dell Computer cont…

• Current situation—– market share; – what is the impact of the business cycle (e.g., PCs are durable

goods)?

2-34

3. Quantitative Financial Analysis

• Systematic analysis of key elements based on analysis context

• Ratios, cash flows, common-size, time series, comparative (e.g., specific firms, industry, all firms), models (e.g., DuPont, Altman’s)

• In-depth analysis for “red flag” items

2-35

3. Quantitative Financial Analysis

• Financial Statements– Common-size Analysis– Financial Ratios– Growth/trend Analysis

• Quarterly analysis• DuPont Model• Market Analysis

2-36

4. Detailed Accounting Analysis cont..

Does accounting information capture the underlying business reality?

Identify areas of “accounting flexibility” & evaluate accounting policies (choices) & disclosures; especially notes & MD&A

Evaluate earnings management potentialRecast accounting numbers when

necessary

2-37

Detailed Accounting Analysis cont..

o Adjust for accounting distortions so financial reports better reflect economic reality

o Adjust general-purpose financial statements to meet specific analysis objectives of a particular user

o Adjust for accounting distortions so financial reports better reflect economic reality

o Adjust general-purpose financial statements to meet specific analysis objectives of a particular user

2-38

Detailed Accounting Analysis cont..

Sources of Accounting Distortions

o Accounting Standards – attributed to

1) political process of standard-setting,

2) accounting principles and assumptions, and

3) conservatismo Estimation Errors – attributed to estimation errors inherent in accrual

accountingo Reliability vs Relevance – attributed to over-emphasis on reliability

at the loss of relevanceo Earnings Management – attributed to window-dressing of financial

statements by managers to achieve personal benefits

o Accounting Standards – attributed to

1) political process of standard-setting,

2) accounting principles and assumptions, and

3) conservatismo Estimation Errors – attributed to estimation errors inherent in accrual

accountingo Reliability vs Relevance – attributed to over-emphasis on reliability

at the loss of relevanceo Earnings Management – attributed to window-dressing of financial

statements by managers to achieve personal benefits

2-39

Detailed Accounting Analysis cont.. Analysis Objectives

o Comparatives Analysis – demand for financial comparisons across companies and/or across

timeo Income Measurement - demand for (1) equity wealth

changes and (2) measure of earning power.)

o Comparatives Analysis – demand for financial comparisons across companies and/or across

timeo Income Measurement - demand for (1) equity wealth

changes and (2) measure of earning power.)

2-40

Detailed Accounting Analysis cont..

Earnings Management – Frequent Source of Distortion

Earning Management strategies:o Increasing Income – managers adjust accruals to increase

reported incomeo Big Bath – managers record huge write-offs in one period to

relieve other periods of expenseso Income Smoothing – managers decrease or increase reported

income to reduce its volatility

Earning Management strategies:o Increasing Income – managers adjust accruals to increase

reported incomeo Big Bath – managers record huge write-offs in one period to

relieve other periods of expenseso Income Smoothing – managers decrease or increase reported

income to reduce its volatility

2-41

Detailed Accounting Analysis cont..

Earnings Management – Motivations

o Contracting Incentives - managers adjust numbers used in contracts that affect their wealth (e.g., compensation contracts)

o Stock Prices – managers adjust numbers to influence stock prices for personal benefits (e.g., mergers, option or stock offering)

o Other Reasons - managers adjust numbers to impact

1) labor demands,

2) management changes, and

3) societal views

o Contracting Incentives - managers adjust numbers used in contracts that affect their wealth (e.g., compensation contracts)

o Stock Prices – managers adjust numbers to influence stock prices for personal benefits (e.g., mergers, option or stock offering)

o Other Reasons - managers adjust numbers to impact

1) labor demands,

2) management changes, and

3) societal views

2-42

5. Comprehensive Analysis

• Summarize key points: what is particularly important for decision making?

• “Red flags” are particularly important• Consider a written executive summary• Consider a rating scale, such as 1-10

2-43

6. Decision• What is the recommendation or decision?• What is the key rationale for this decision?

[This is based on the specific decision: for a credit decision the key factors relate to credit risk, with particular focus on leverage and liquidity.]

• Be prepared to defend this decision.

2-44

END OF PRESENTATION

• THANK YOU

Recommended