1

REVIEW OF THE REVIEW OF THE

PUBLIC PRIVATE PUBLIC PRIVATE

PARTNERSHIP PARTNERSHIP

PRISON CONTRACTSPRISON CONTRACTS

8 November 2002

2

TASK TEAM TERMS OF REFERENCETASK TEAM TERMS OF REFERENCE

To understand output specifications, costing assumptions, project finance and risk allocation.

To identify capital and operational costs.

To identify features for re-negotiation to address DCS affordability constraints.

To establish a sound methodological basis for comparison with existing and recently constructed conventional prisons.

To report to Ministers of Correctional Services, Finance, Public Works and Portfolio Committee.

3

TASK TEAM MEMBERSTASK TEAM MEMBERSChairperson Mr NW Tshivhase CFO DCS

Secretary Mr JJ Venter ASD Financial Planning

DCS

Adv M Ndziba Minister’s Special Advisor

Mr NS Makhani Director Financial Planning

Ms J Schreiner CDC Functional Services

Ms RST Mthabela DC Offender Control

Mr J Maako Director APOPS

Mr C Basson Deputy Director APOPS

Mr CH Paxton Director Legal Services

National Treasury

Mr VH Mbethe Chief Director

Dr K Brown Director Integrated Justice Cluster

Mr W Mothibedi Acting Director DCS

Ms S Lund Senior Transaction Advisor PPP Unit

Mr W Krause SFAO DCS

DPW Mr L van Hecke Acting Director APOPS

ConsultantsMr T Williams Director Ignis

Mr P Chipindu Associate Ignis

4

TASK TEAM FINDINGSTASK TEAM FINDINGS

Part I: Existing PPP Transactions

Overview of existing PPP transactions. Options for Re-negotiation of Existing Contracts. Conclusions and Recommendations.

Part II: Future Prison Projects Illustrative comparisons of Public and PPP Prisons Future Evaluation Methodology: Feasibility

Protocol. Conclusions and Recommendations.

Part III: Recommendations for Next Steps

5

PART I PART I

EXISTING PPP PRISONS EXISTING PPP PRISONS

TRANSACTIONSTRANSACTIONS

6

1. OVERVIEW OF EXISTING 1. OVERVIEW OF EXISTING

PPP PRISONS TRANSACTIONSPPP PRISONS TRANSACTIONS

7

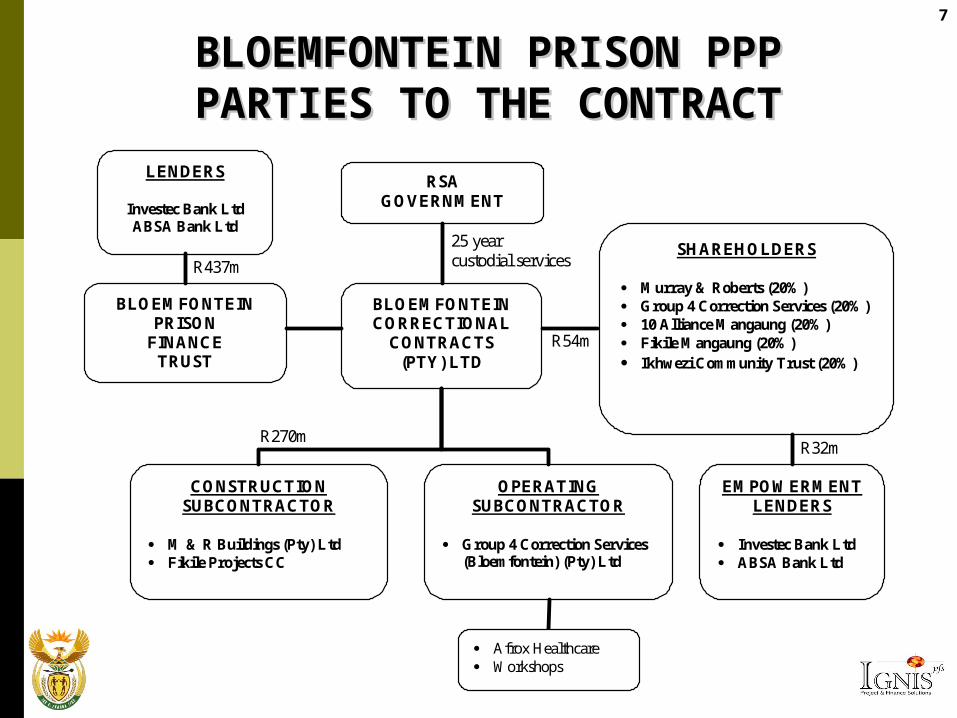

BLOEMFONTEIN PRISON PPPBLOEMFONTEIN PRISON PPPPARTIES TO THE CONTRACTPARTIES TO THE CONTRACT

RSA

GOVERNMENT

BLOEMFONTEIN CORRECTIONAL

CONTRACTS (PTY) LTD

SHAREHOLDERS

Murray & Roberts (20%) Group 4 Correction Services (20%) 10 Alliance Mangaung (20%) Fikile Mangaung (20%) Ikhwezi Community Trust (20%)

CONSTRUCTION SUBCONTRACTOR

M & R Buildings (Pty) Ltd Fikile Projects CC

OPERATING SUBCONTRACTOR

Group 4 Correction Services

(Bloemfontein) (Pty) Ltd

BLOEMFONTEIN PRISON

FINANCE TRUST

LENDERS

Investec Bank Ltd ABSA Bank Ltd

EMPOWERMENT LENDERS

Investec Bank Ltd ABSA Bank Ltd

Afrox Healthcare Workshops

R437m

25 year custodial services

R54m

R270m R32m

8

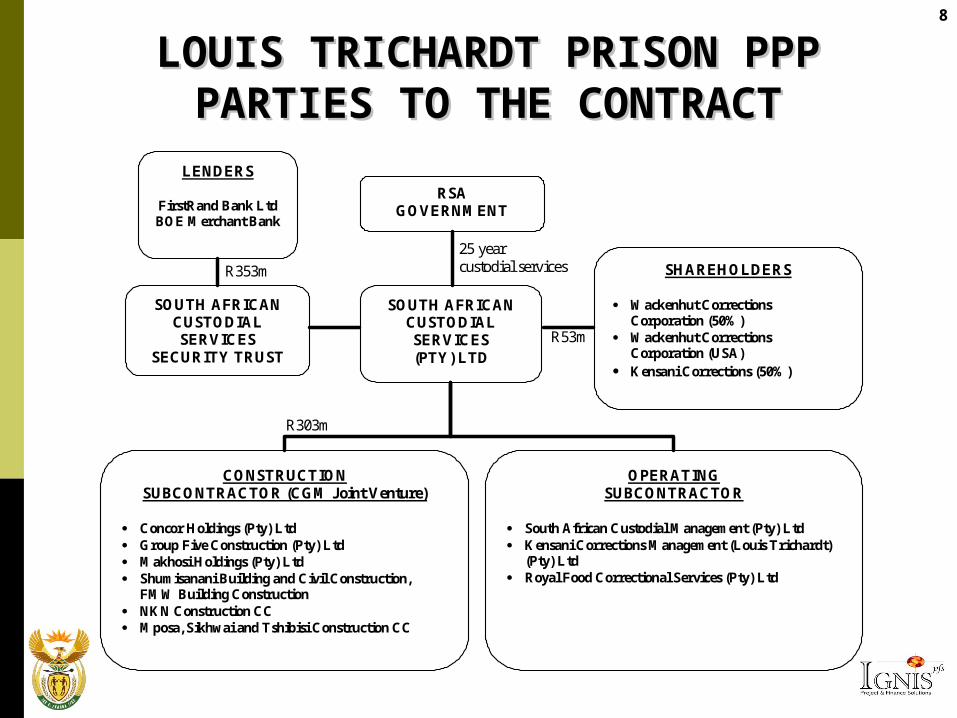

LOUIS TRICHARDT PRISON PPPLOUIS TRICHARDT PRISON PPPPARTIES TO THE CONTRACTPARTIES TO THE CONTRACT

RSA GOVERNMENT

SOUTH AFRICAN CUSTODIAL SERVICES (PTY) LTD

SHAREHOLDERS

Wackenhut Corrections Corporation (50%)

Wackenhut Corrections Corporation (USA)

Kensani Corrections (50%)

CONSTRUCTION SUBCONTRACTOR (CGM Joint Venture)

Concor Holdings (Pty) Ltd Group Five Construction (Pty) Ltd Makhosi Holdings (Pty) Ltd Shumisanani Building and Civil Construction,

FMW Building Construction NKN Construction CC Mposa, Sikhwai and Tshibisi Construction CC

OPERATING SUBCONTRACTOR

South African Custodial Management (Pty) Ltd Kensani Corrections Management (Louis Trichardt)

(Pty) Ltd Royal Food Correctional Services (Pty) Ltd

SOUTH AFRICAN CUSTODIAL SERVICES

SECURITY TRUST

LENDERS

FirstRand Bank Ltd BOE Merchant Bank

R353m

R303m

R53m

25 year custodial services

9

DCS SPECIFICATIONSDCS SPECIFICATIONS

Specifications based on inputs rather than

outputs or outcomes.

Specifications imported from UK prison –

‘ideal’ and high level.

No prior feasibility undertaken to ensure: Affordability limits

Optimal value for money

Optimal risk transfer

10

DCS SPECIFICATIONS: DESIGNDCS SPECIFICATIONS: DESIGN

Cell configuration (2-man and 4-man cells). Security. Special centres (e.g. assessment, visitors,

special treatment). Utilities. Service centres (e.g. catering, health,

religious). External works.

11

DCS DESIGN SPECIFICATIONS: DCS DESIGN SPECIFICATIONS: EXAMPLESEXAMPLES

Cell size*: 5.5m2 single or 8m2 double.

Cell height*: 2.7m.

Minimum 5 layers of security.

Telephone monitoring system.

CCTV, cameras, x-rays, etc.

* Minimum requirement according to Health and National Building Regulations.

12

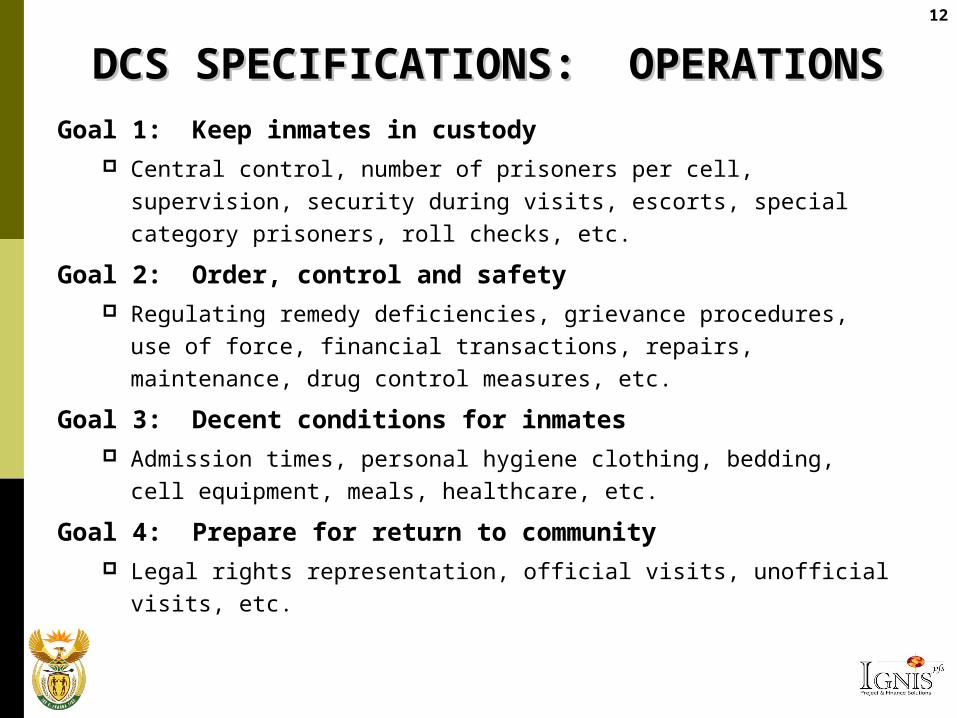

DCS SPECIFICATIONS: OPERATIONSDCS SPECIFICATIONS: OPERATIONSGoal 1: Keep inmates in custody

Central control, number of prisoners per cell, supervision, security during visits, escorts, special category prisoners, roll checks, etc.

Goal 2: Order, control and safety Regulating remedy deficiencies, grievance procedures, use of

force, financial transactions, repairs, maintenance, drug control measures, etc.

Goal 3: Decent conditions for inmates Admission times, personal hygiene clothing, bedding, cell

equipment, meals, healthcare, etc.

Goal 4: Prepare for return to community Legal rights representation, official visits, unofficial visits, etc.

13

DCS SPECIFICATIONS: OPERATIONSDCS SPECIFICATIONS: OPERATIONS

Goal 5: Structured Day Programmes Structured Day Programme, times of unlocking, activities, time

outdoors, social work services, religion, work, education training programmes, physical education library, psychologists, etc.

Goal 6: Deliver services with maximum efficiency Strategic development plans, personnel policies, equal

opportunities, drug & alcohol free work-place, conditions of service, uniforms, recruitment & selection and training.

Goal 7: Promote community involvement Community participation and vice versa, formal & informal

community development, employment to local community, local PR policy.

14

OVERVIEWOVERVIEW

Bloemfontein Louis Trichardt

Number of inmates 2 928 3 024

Total capital expenditure (R’m) 435 392

Construction (R’m) 270 303

Pre-operating interest / fees (R’m)

104 26*

Start-up costs (R’m) 58 49

Contract signed 24 Mar 00 11 Aug 00

Opening date 1 Jul 01 19 Feb 02

Full capacity date Jan 02 Sep 02

* Interest deferred in terms of financial structure.

15

FEES PAYABLE BY DCSFEES PAYABLE BY DCS

BloemfonteinR/inmate/day

Louis TrichardtR/inmate/day

Fixed Fee for Construction Debt

Base Date (1 Jan 98) 65.91 66.25

Opening 83.50 73.91

Operating Fee

Base Date (1 Jan 98) 88.50 73.06 Opening 103.97 81.51

October 2002 132.20 86.45

Total Fee

Base date (1 Jan 98) 154.41 139.31

Opening 187.47 155.42

October 2002 215.70 160.36

16

COMPARISON OF FEE STRUCTURECOMPARISON OF FEE STRUCTURE

Fee comparison complicated by: Different start dates. “K-Factor”:

Real increases above inflation. Bloemfontein: from 0.623% to 0.789% six monthly. Louis Trichardt: six monthly increases:

Years 2-3 6% Years 4-5 5% Year 6 4% Years 7-9 2% Years 10-13 1% Years 14-25 3% decrease each 6 months

Net Present Value of all fees (8% discount rate): Bloemfontein R1.3 billion Louis Trichardt R1.2 billion

17

REAL INDEXED FEE ADJUSTED FOR REAL INDEXED FEE ADJUSTED FOR “K-FACTOR”“K-FACTOR”

0

20

40

60

80

100

120

140

160

180

200

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

Operating Year

Inde

x Fee

(R

ands

)

Bloemfontein Louis Trichardt

18

BREAKDOWN OF OPERATING COSTS BREAKDOWN OF OPERATING COSTS (BLOEMFONTEIN) (BLOEMFONTEIN)

46%

11%

10%

13%

13%

8%

19

BREAKDOWN OF OPERATING COSTS BREAKDOWN OF OPERATING COSTS (LOUIS TRICHARDT)(LOUIS TRICHARDT)

27%

6%

9%38%

12%

8%

0.4%

20

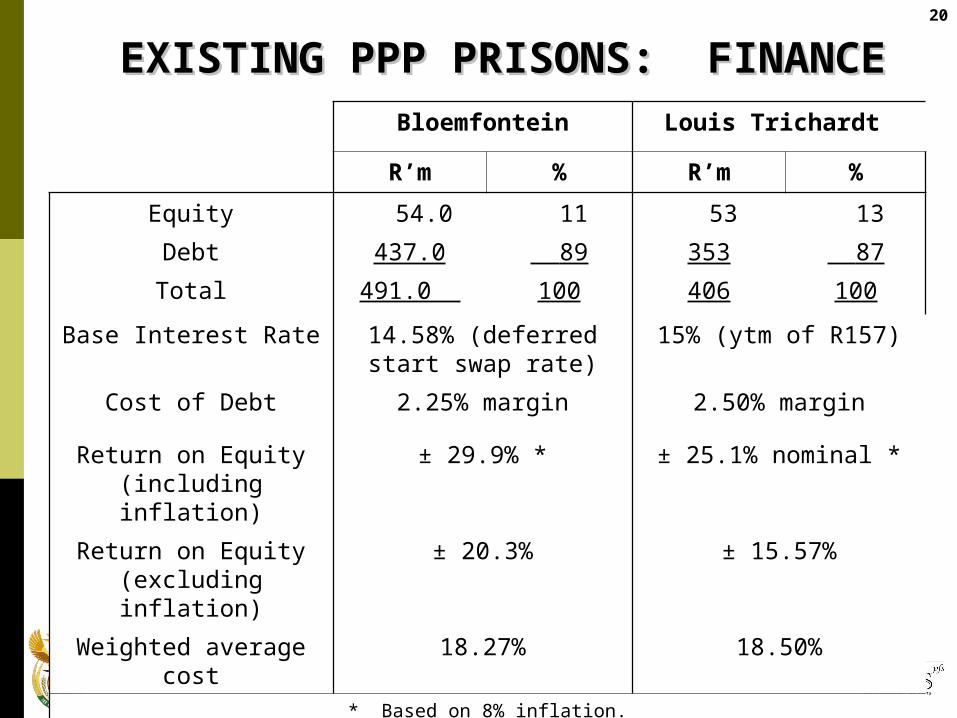

EXISTING PPP PRISONS: FINANCEEXISTING PPP PRISONS: FINANCEBloemfontein Louis Trichardt

R’m % R’m %

Equity 54.0 11 53 13

Debt 437.0 89 353 87

Total 491.0 100 406 100

Base Interest Rate 14.58% (deferred start swap rate)

15% (ytm of R157)

Cost of Debt 2.25% margin 2.50% margin

Return on Equity (including inflation)

± 29.9% * ± 25.1% nominal *

Return on Equity (excluding inflation)

± 20.3% ± 15.57%

Weighted average cost

18.27% 18.50%

* Based on 8% inflation.

21

RISK ALLOCATION:RISK ALLOCATION:TECHNICAL / OPERATIONALTECHNICAL / OPERATIONAL

Risk Type Contractor DCS

Construction – Design

Construction – Cost

Construction – Delays

Change in technology

Operating Costs

Damage to prison Force Majeure

Prison security Residual

Cell availability

Cell usage

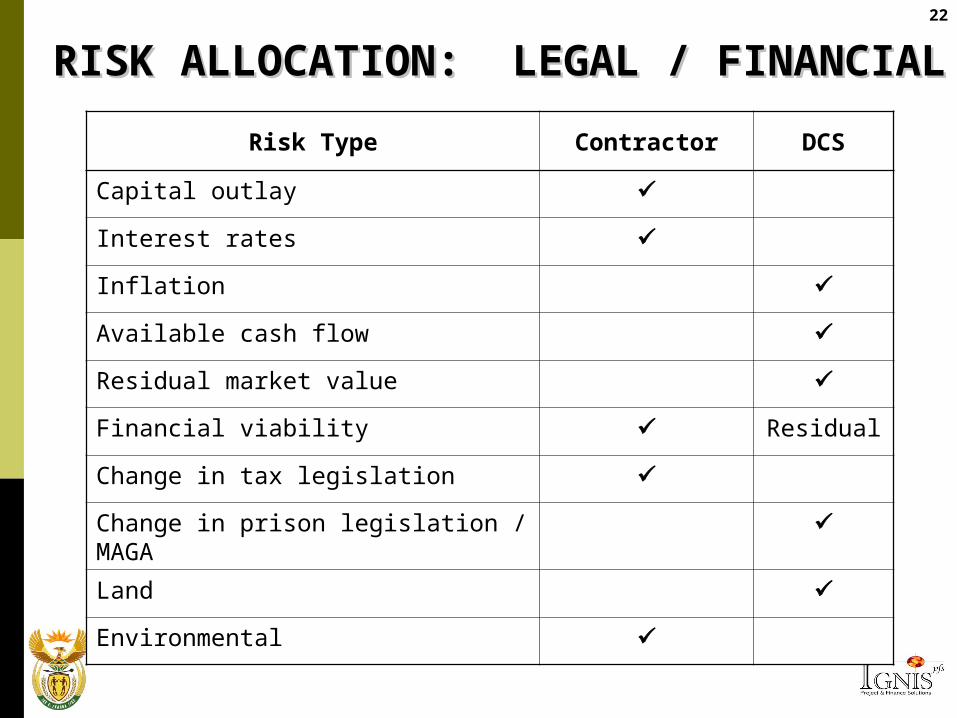

22RISK ALLOCATION: LEGAL / RISK ALLOCATION: LEGAL / FINANCIALFINANCIAL

Risk Type Contractor DCS

Capital outlay

Interest rates

Inflation

Available cash flow

Residual market value

Financial viability Residual

Change in tax legislation

Change in prison legislation / MAGA

Land

Environmental

23

2. OPTIONS FOR RE-NEGOTIATION 2. OPTIONS FOR RE-NEGOTIATION

OF EXISTING CONTRACTSOF EXISTING CONTRACTS

24

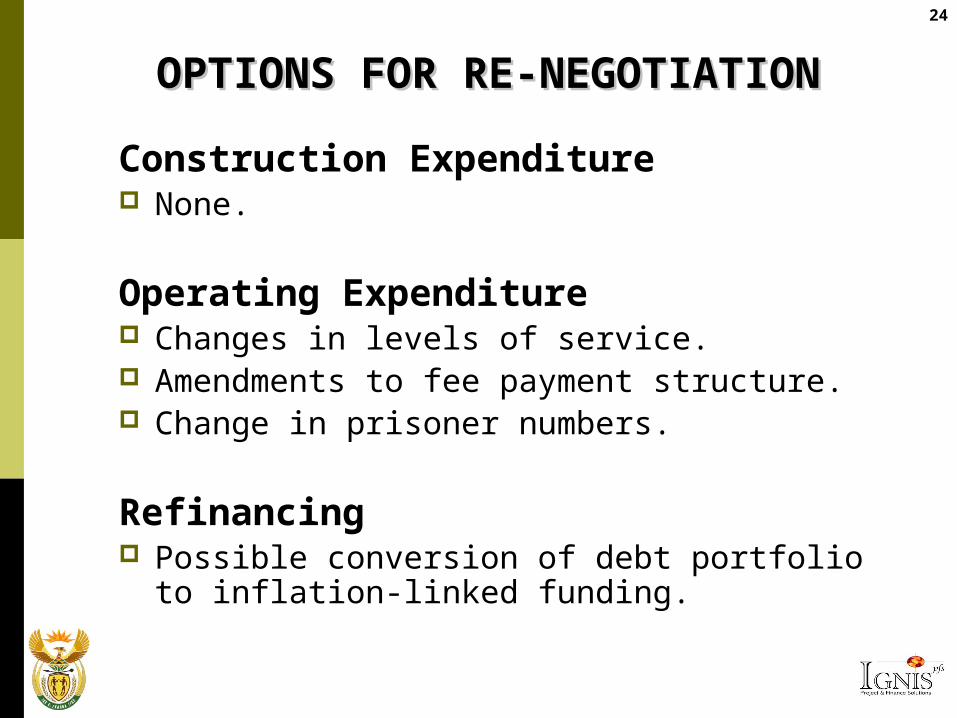

OPTIONS FOR RE-NEGOTIATIONOPTIONS FOR RE-NEGOTIATION

Construction Expenditure None.

Operating Expenditure Changes in levels of service. Amendments to fee payment structure. Change in prisoner numbers.

Refinancing Possible conversion of debt portfolio to

inflation-linked funding.

25

OPTIONS FOR RE-NEGOTIATION:OPTIONS FOR RE-NEGOTIATION:OPERATING EXPENDITUREOPERATING EXPENDITURE

Staff costs Hours out of cell. Service specifications.

Rehabilitation and Health Care Change in specifications.

Fee payment structure Amendments to “K-factor” adjustments to improve cashflows.

Change in Prisoner Numbers Bloemfontein: 2 new units. Louis Trichardt: convert 2-bed cells to 4-bed cells and use

reception/special treatment centre.

26

OPTIONS FOR RE-NEGOTIATION:OPTIONS FOR RE-NEGOTIATION:INDICATIVE FEE CALCULATIONINDICATIVE FEE CALCULATION

Bloemfontein Louis Trichardt

Current inmates 2 928 3 024

Potential additional 976 696

Potential total inmates 3 904 3 720

Capital expenditure required

Yes Limited

Current rate per day (R) 132.20 86.45

Average rate / day after expansion

112.37 73.48

Rate / day for additional inmates

52.88 17.13

27

OPTIONS FOR RE-NEGOTIATION:OPTIONS FOR RE-NEGOTIATION:REFINANCINGREFINANCING

Methodology

Net Present Value of unexpired portion of debt (settlement estimate).

Convert into new CPI-linked bond debt and calculate new repayments and NPVs.

Compare with existing payments.

28

OPTIONS FOR RE-NEGOTIATION: OPTIONS FOR RE-NEGOTIATION: RE-FINANCING ASSUMPTIONSRE-FINANCING ASSUMPTIONS

Assumptions Bloemfontein Louis Trichardt

Original value (R’m) 437 353

Current annual repayment (R’m)

83.3 68.9

Settlement estimate (R’m) 530.9 556.6

Benchmark refinance date 30 Sept 02 31 July 02

Benchmark Ref. Base Rate (R153 as at 24 Sept 02)

11.80% 11.80%

Benchmark Ref. Real Rate (assume Full Gov. borrowing)

4.50% 4.50%

Margin for refinancing (full) 2.25 2.50

Margin for refinancing (reduced)

1.75 1.75

29

OPTIONS FOR RE-NEGOTIATION:OPTIONS FOR RE-NEGOTIATION:RE-FINANCING BENEFITS RE-FINANCING BENEFITS

(BLOEMFONTEIN)(BLOEMFONTEIN)

Inflation %

Excluding Margin

Reduced Margin

Historical Full Margin

Payment 02/03 R’m

NPV R’m

Payment 02/03 R’m

NPV R’m

Payment 02/03 R’m

NPV R’m

3.00 50.9 379.3 57.2 426.4 59.1 440.3

4.50 51.6 413.5 58.0 467.8 59.9 480.0

6.00 52.4 451.5 58.9 507.5 60.8 524.0

7.50 53.1 493.7 59.7 554.9 61.7 573.0

30

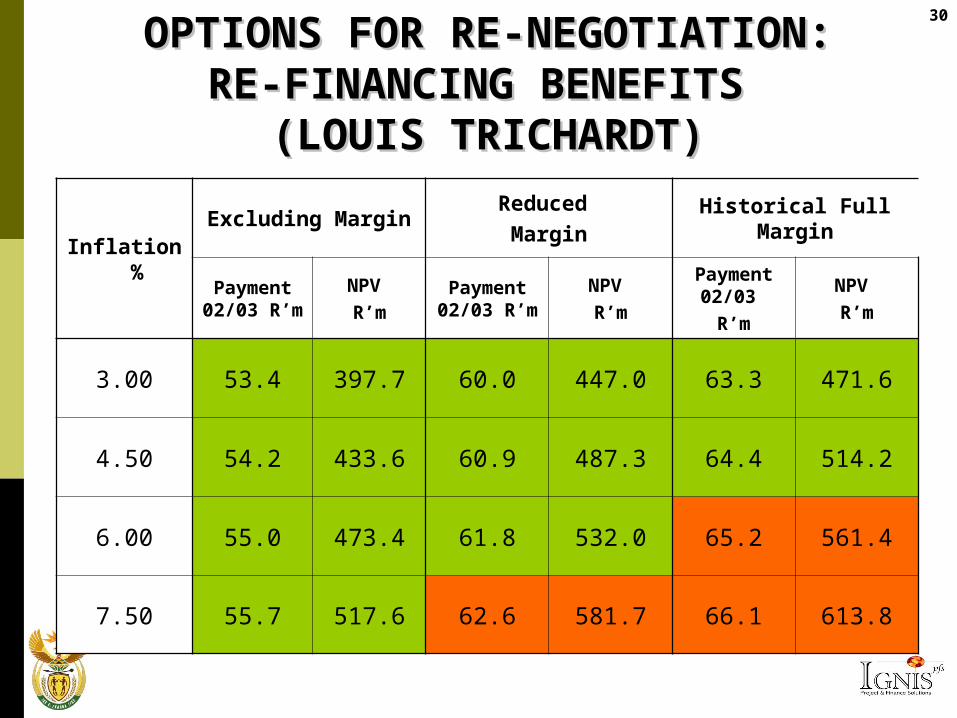

OPTIONS FOR RE-NEGOTIATION:OPTIONS FOR RE-NEGOTIATION:RE-FINANCING BENEFITS RE-FINANCING BENEFITS

(LOUIS TRICHARDT)(LOUIS TRICHARDT)

Inflation %

Excluding MarginReduced Margin

Historical Full Margin

Payment 02/03 R’m

NPV R’m

Payment 02/03 R’m

NPV R’m

Payment 02/03 R’m

NPV R’m

3.00 53.4 397.7 60.0 447.0 63.3 471.6

4.50 54.2 433.6 60.9 487.3 64.4 514.2

6.00 55.0 473.4 61.8 532.0 65.2 561.4

7.50 55.7 517.6 62.6 581.7 66.1 613.8

31

3. CONCLUSIONS & 3. CONCLUSIONS &

RECOMMENDATIONS: RECOMMENDATIONS:

EXISTING PPP CONTRACTSEXISTING PPP CONTRACTS

32

CONCLUSION: CONCLUSION: EXISTING CONTRACTSEXISTING CONTRACTS

The PPP Prison Projects delivered according to DCS’ specifications, notably achieving:

Competitive construction costs. Construction on time, on budget. Fast-track delivery (< 2years full capacity). Comparative operating costs. Significant black equity and sub-contracting Significantly higher-quality facilities. Significantly higher-levels of service. Appropriate risk allocation.

But …

33CONCLUSIONS: CONCLUSIONS: PROBLEMS WITH EXISTING PROBLEMS WITH EXISTING

CONTRACTSCONTRACTS

DCS specifications were too high (the PPP prisons

remain driven by DCS’ input specifications).

Relatively high cost of debt.

Higher than normal return on equity.

Additional budgeting pressures for DCS.

Despite overcrowding in DCS system, no ability to

over-populate PPP prisons.

34

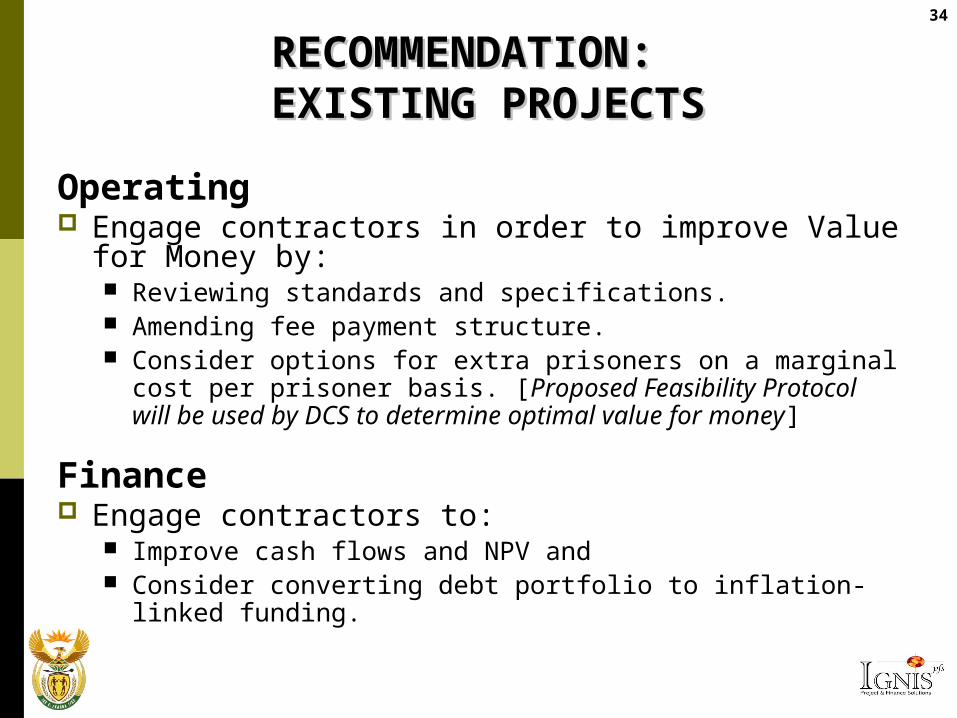

RECOMMENDATION: RECOMMENDATION: EXISTING PROJECTSEXISTING PROJECTS

Operating Engage contractors in order to improve Value for

Money by: Reviewing standards and specifications. Amending fee payment structure. Consider options for extra prisoners on a marginal cost

per prisoner basis. [Proposed Feasibility Protocol will be used by DCS to determine optimal value for money]

Finance Engage contractors to:

Improve cash flows and NPV and Consider converting debt portfolio to inflation-linked

funding.

35

PART II PART II

FUTURE PRISON PROJECTSFUTURE PRISON PROJECTS

36

1. ILLUSTRATIVE 1. ILLUSTRATIVE

COMPARISONS:COMPARISONS:

PUBLIC AND PPP PRISONSPUBLIC AND PPP PRISONS

37BARRIERS TO DIRECT COMPARISON BARRIERS TO DIRECT COMPARISON BETWEEN PPP AND PUBLIC BETWEEN PPP AND PUBLIC

PRISONSPRISONS

CAPITAL COSTS

Dates of construction Type of prison Inmates per cell Location Risk transfer Split functions: DPW/DCS Inclusion of staff housing Capacities Security levels Technology and design

OPERATING COSTS

Overcrowding Standards of facilities Standards of activities Hours out of cell Rehabilitation Health facilities Risk transfer – penalties In-house food & services Availability of information

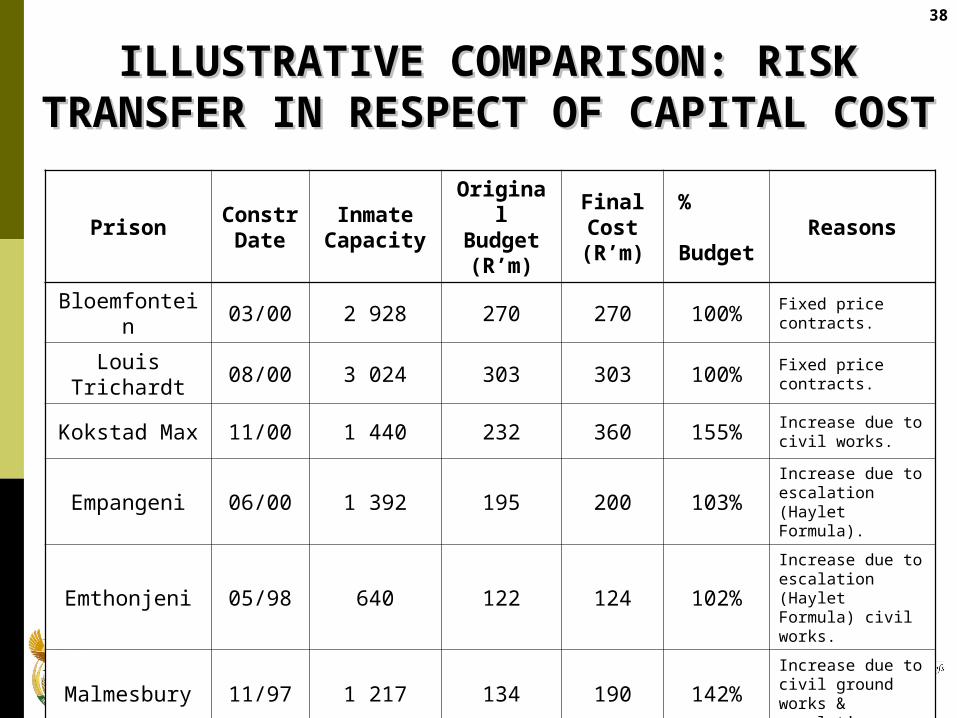

38ILLUSTRATIVE COMPARISON: RISK ILLUSTRATIVE COMPARISON: RISK TRANSFER IN RESPECT OF CAPITAL TRANSFER IN RESPECT OF CAPITAL

COSTCOST

PrisonConstrDate

Inmate Capacity

Original Budget (R’m)

Final Cost (R’m)

%

BudgetReasons

Bloemfontein 03/00 2 928 270 270 100% Fixed price contracts.

Louis Trichardt

08/00 3 024 303 303 100% Fixed price contracts.

Kokstad Max 11/00 1 440 232 360 155% Increase due to civil works.

Empangeni 06/00 1 392 195 200 103%Increase due to escalation (Haylet Formula).

Emthonjeni 05/98 640 122 124 102%Increase due to escalation (Haylet Formula) civil works.

Malmesbury 11/97 1 217 134 190 142%Increase due to civil ground works & escalation.

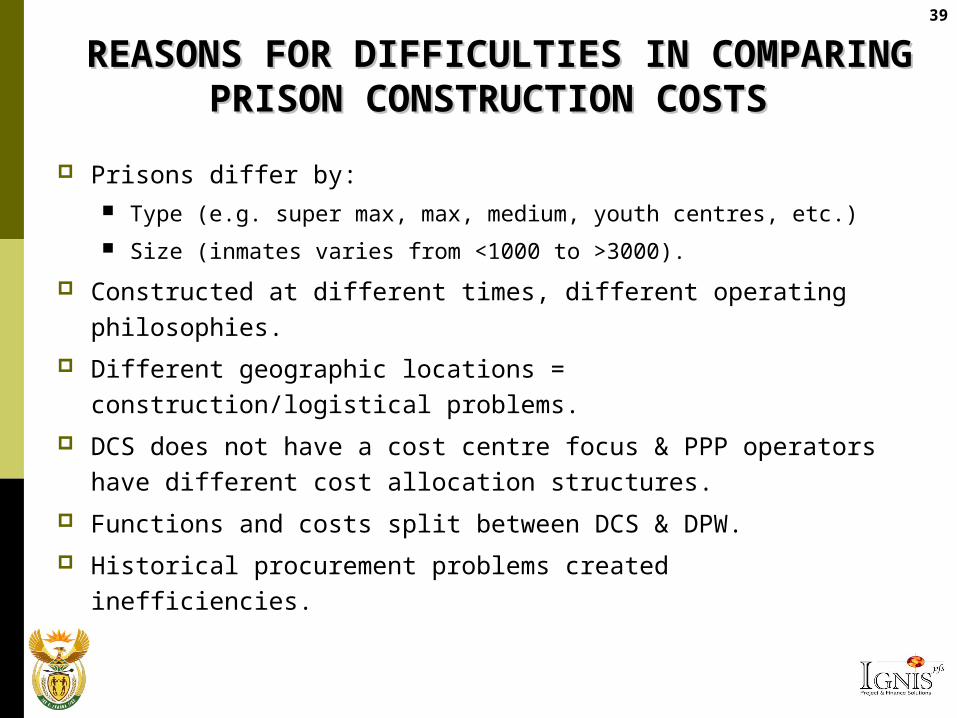

39 REASONS FOR DIFFICULTIES IN REASONS FOR DIFFICULTIES IN COMPARING PRISON CONSTRUCTION COMPARING PRISON CONSTRUCTION

COSTSCOSTS

Prisons differ by: Type (e.g. super max, max, medium, youth centres, etc.)

Size (inmates varies from <1000 to >3000).

Constructed at different times, different operating philosophies.

Different geographic locations = construction/logistical problems.

DCS does not have a cost centre focus & PPP operators have different cost allocation structures.

Functions and costs split between DCS & DPW.

Historical procurement problems created inefficiencies.

40ILLUSTRATIVE COMPARISON: ILLUSTRATIVE COMPARISON: FUNDED CONSTRUCTION COST FUNDED CONSTRUCTION COST

FORGOVERNMENTFORGOVERNMENTConstruction amount (R’m) 300

% overrun 15%

Base interest rate (benchmark government rate in 2000) 15%

Inter-government margin 1%

Debt period 15 years

Construction period 24 months

Vat Rate 14%

Number of prisoners 3 000

Results

Capital expenditure (R’m) 393

Pre-operating interest (R’m) 63

Total Debt (R’m) 456

Annual payment (R’m) 82

Cost per constructed inmate place per day (Rands) R74.70

41ILLUSTRATIVE COMPARISON: OPERATING ILLUSTRATIVE COMPARISON: OPERATING COSTSCOSTS

Cost Description

Public (R/prisoner/day)

Private (R/prisoner/day)

Budget 2002/03

Bloemfontein October 02

Louis Trichardt October 02

Staff costs - 51.54 -

Administration 35.54 - 23.18

Security / Operations 41.22 - 32.40

Health 4.24 14.14 7.76

Programmes 5.62 10.71 10.08

Facilities Management 1.80 5.72 5.45

Utilities 0.16 5.48 -

Catering 5.09 11.96 7.26

Supplies / Procurement - 8.80 0.32

Insurance - 3.67 -

Co. costs / Redemption - 20.18 -

Total 93.67 * 132.20 86.45

Total inmates172 048

(incl. 70% overcrowding)

2 928(not overcrowded)

3 024(not overcrowded)

* See comments on the effects of overcrowding (Page 44 of Report).

42 REASONS FOR DIFFICULTIES IN REASONS FOR DIFFICULTIES IN COMPARING PRISON OPERATING COMPARING PRISON OPERATING

COSTSCOSTS Overcrowding of public prisons.

Prisons differ by: Type (e.g. super max, max, medium, youth centres, etc.)

Standards of facilities (health, catering, recreation, etc.)

Standards of activities (education, vocational training, work).

Hours out of cell.

Different operating philosophies, often result of different design.

DCS does not have a cost centre focus to accounting.

PPP operators have different cost allocation structures.

Risk transfer differs.

43

2. FUTURE EVALUATION 2. FUTURE EVALUATION

METHODOLOGY: METHODOLOGY:

FEASIBILITY PROTOCOLFEASIBILITY PROTOCOL

44

PROPOSED FUTURE EVALUATION PROPOSED FUTURE EVALUATION METHODOLOGY FOR NEW PRISONSMETHODOLOGY FOR NEW PRISONS

Applicable for projects as both PPP and

conventional procurement.

Purpose is to assess all options based on clear

output specifications.

For all choices, DCS needs to demonstrate:

Affordability

Value for Money

Acknowledgement and treatment of risk

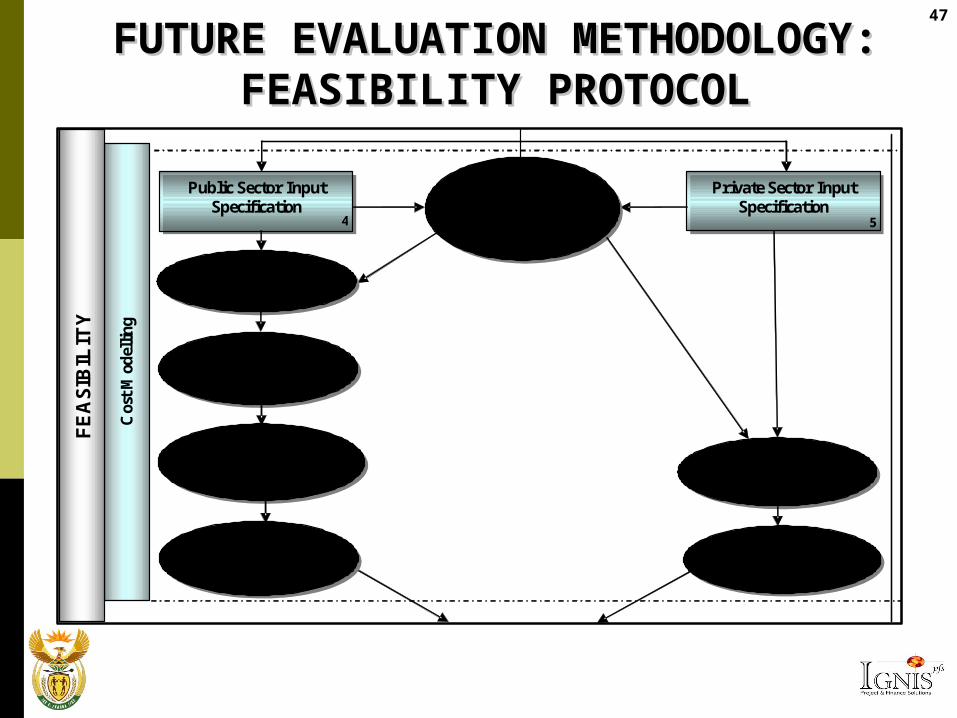

45FUTURE FUTURE EVALUATION EVALUATION

METHODOLOGY: METHODOLOGY: FEASIBILITY FEASIBILITY PROTOCOLPROTOCOL

22

21

No

Base Design and Operation Input

Specification 3

Determine Outcomes for Preferred Option

1

Determine Output Specification

2

Def

init

ion

Needs Analysis

Options Analysis

Stra

tegy

PR

E

FE

AS

IBIL

ITY

Private Sector Input Specification

5

Capital Cost Lifecycle Cost

Operating Cost 6

Unitary Payment Model

11 Unitary Payment Model

12

Public Sector Input Specification

4

Shadow Project Bid

7

Probability Risk Adjustment 10

Costed Risk Adjustment 9

Cos

t M

odel

ling

Shadow Project Bid

8

Yes

Public Sector 18

Private Sector 20

Other Procurement 19

Implementation Decision 17

Aff

orda

bilit

y an

d V

alue

for

Mon

ey

Affordable Public Sector

Project 14

Available Affordability

Budget

13

Value for Money? 16

Affordable Private Sector

Project 15

FE

AS

IBIL

ITY

46FUTURE EVALUATION FUTURE EVALUATION

METHODOLOGY: FEASIBILITY METHODOLOGY: FEASIBILITY PROTOCOLPROTOCOL

22

21

Base Design and Operation Input

Specification 3

Determine Outcomes for Preferred Option

1

Determine Output Specification

2

Def

init

ion

Needs Analysis

Options Analysis

Str

ateg

y

PR

E F

EA

SIB

ILIT

Y

FE

AS

IBIL

ITY

47

Private Sector Input Specification

5

Capital Cost Lifecycle Cost

Operating Cost 6

Unitary Payment Model

11 Unitary Payment Model

12

Public Sector Input Specification

4

Shadow Project Bid

7

Probability Risk Adjustment 10

Costed Risk Adjustment 9

Cos

t M

odel

lin

g

Shadow Project Bid

8

FE

AS

IBIL

ITY

FUTURE EVALUATION FUTURE EVALUATION METHODOLOGY: FEASIBILITY METHODOLOGY: FEASIBILITY

PROTOCOLPROTOCOL

48FUTURE EVALUATION FUTURE EVALUATION

METHODOLOGY: FEASIBILITY METHODOLOGY: FEASIBILITY PROTOCOLPROTOCOL

No Yes

Public Sector 18

Private Sector 20

Other Procurement 19

Implementation Decision 17

Aff

orda

bil

ity

and

Val

ue f

or M

oney

Affordable Public Sector

Project 14

Available Affordability

Budget

13

Value for Money? 16

Affordable Private Sector

Project 15

FE

AS

IBIL

ITY

49

3. CONCLUSIONS & 3. CONCLUSIONS &

RECOMMENDATIONS: RECOMMENDATIONS:

FUTURE PRISON PROJECTSFUTURE PRISON PROJECTS

50

RECOMMENDATION: FEASIBILITY RECOMMENDATION: FEASIBILITY PROTOCOL FOR FUTURE PROJECTSPROTOCOL FOR FUTURE PROJECTS DCS to clearly establish output specifications (for design &

operations). Establish budget constraints. Develop comparable accounting standards for both PPP and

DCS-operated prisons. Adopt clear rules for DCS staff movement during any future

PPP procurements. Comprehensive feasibility:

Cost private design, finance, build and operate, versus Risk-adjusted Public Sector Comparator.

Results: If clear distinction – Adopt. If depends on assumptions – Policy decision or pilot

comparisons.

51

PART IIIPART III

TASK TEAM’S TASK TEAM’S

RECOMMENDATIONS FOR RECOMMENDATIONS FOR

NEXT STEPSNEXT STEPS

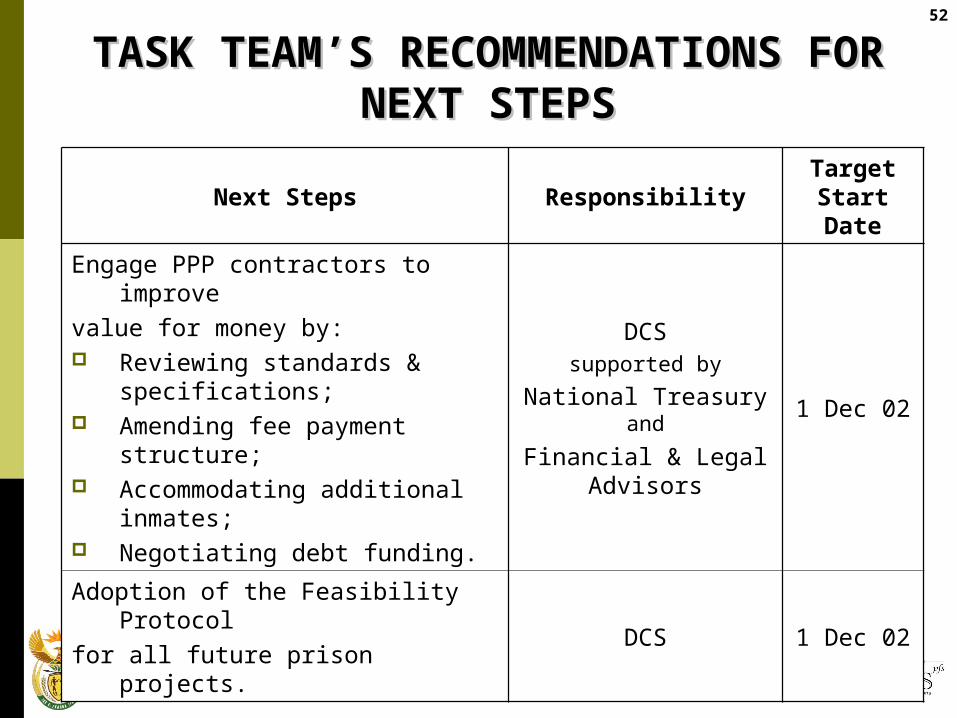

52TASK TEAM’S RECOMMENDATIONS TASK TEAM’S RECOMMENDATIONS FORFOR

NEXT STEPSNEXT STEPS

Next Steps ResponsibilityTarget Start Date

Engage PPP contractors to improvevalue for money by: Reviewing standards &

specifications; Amending fee payment

structure; Accommodating additional

inmates; Negotiating debt funding.

DCSsupported by

National Treasury and

Financial & Legal Advisors

1 Dec 02

Adoption of the Feasibility Protocolfor all future prison projects.

DCS 1 Dec 02

53TASK TEAM’S RECOMMENDATIONS TASK TEAM’S RECOMMENDATIONS FORFOR

NEXT STEPSNEXT STEPS

Next Steps ResponsibilityTarget Start Date

Setting of clear DCS policy, processes and decision-makingstructures for procurement offuture prisons.

DCSsupported by

National Treasury1 Dec 02

Setting and public announcement of DCS policy on unsolicited bids.

DCSsupported by

National Treasury1 Dec 02

Training of key DCS personnel in: DCS’s Prison Feasibility Protocol

and DCS’s Procurement policy,

methods and standards.

DCSsupported by

National TreasuryMarch 03

54

MINISTERS OF: MINISTERS OF: CORRECTIONAL SERVICES, FINANCE, PUBLIC CORRECTIONAL SERVICES, FINANCE, PUBLIC

WORKSWORKS andand

PARLIAMENTARY PORTFOLIO COMMITTEE ON PARLIAMENTARY PORTFOLIO COMMITTEE ON CORRECTIONAL SERVICESCORRECTIONAL SERVICES

REVIEW REPORT REVIEW REPORT SUBMITTED TO:SUBMITTED TO:

Recommended