- CA Rajiv Mehrotra, DISA (ICAI)

SPECIFIED DOMESTIC TRANSACTIONS UNDER I.T.ACT–

18th October, Lucknow

- CA Rajiv Mehrotra, DISA (ICAI)

Extension Of TP Laws To Domestic Transactions

Supreme Court in the case of CIT Vs Glaxo SmithKline Asia (P) Ltd. 195 Taxman 35 (SC) stated that the fair market value cannot be assigned to domestic transactions unless a specific regulation is there and suggested finance ministry should bring a proper legislation for the same.

Adjustments made by TPO’s in 7 years- Rs.1,00,000 cr.

Adjustments made by TPO’s in 2008-09 Rs.45,000 cr.

- CA Rajiv Mehrotra, DISA (ICAI)

Extension Of TP Laws To Domestic Transactions

Effective – AY 2013-14.

I.T. Return / Report due date 30th November.

- CA Rajiv Mehrotra, DISA (ICAI)

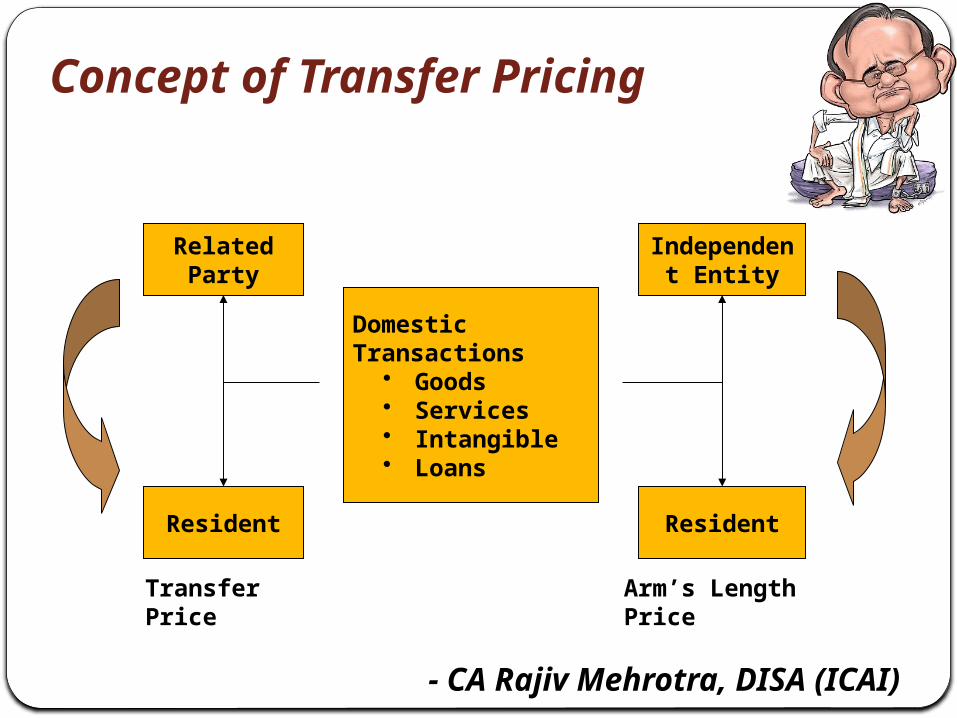

Concept of Transfer Pricing

Domestic Transactions

• Goods• Services• Intangible• Loans

Related Party

Resident

Independent Entity

Resident

Transfer Price Arm’s Length Price

- CA Rajiv Mehrotra, DISA (ICAI)

Section 92

92. (2) Where in an international transaction or specified domestic transaction, two or more associated enterprises enter into a mutual agreement or arrangement for the allocation or apportionment of, or any contribution to, any cost or expense incurred or to be incurred in connection with a benefit, service or facility provided or to be provided to any one or more of such enterprises, the cost or expense allocated or apportioned to, or, as the case may be, contributed by, any such enterprise shall be determined having regard to the arm's length price of such benefit, service or facility, as the case may be.

The following sub-section (2A) shall be inserted after sub-section (2) of section 92 by the Finance Act, 2012, w.e.f. 1-4-2013 :

(2A) Any allowance for an expenditure or interest or allocation of any cost or expense or any income in relation to the specified domestic transaction shall be computed having regard to the arm's length price.

- CA Rajiv Mehrotra, DISA (ICAI)

Section 92

92.(3) The provisions of this section shall not apply in a case where the computation of income under sub-section (1) or sub-section (2A) or the determination of the allowance for any expense or interest under that sub-section, or the determination of any cost or expense allocated or apportioned, or, as the case may be, contributed under sub-section (2) or sub-section (2A), has the effect of reducing the income chargeable to tax or increasing the loss, as the case may be, computed on the basis of entries made in the books of account in respect of the previous year in which the international transaction or specified domestic transaction was entered into.

- CA Rajiv Mehrotra, DISA (ICAI)

Extension Of TP Laws To Domestic Transactions

Section 92 amended so as to include, apart from international transactions, ‘specified domestic transactions’. New Sub section (2A) specifies that the following ‘specified domestic transactions’ may be re-computed having regard to the ALP:any allowance for any expenditure or interestallocation of any cost, expense or income

Provisions are applicable only if they are in favour of the revenue.

- CA Rajiv Mehrotra, DISA (ICAI)

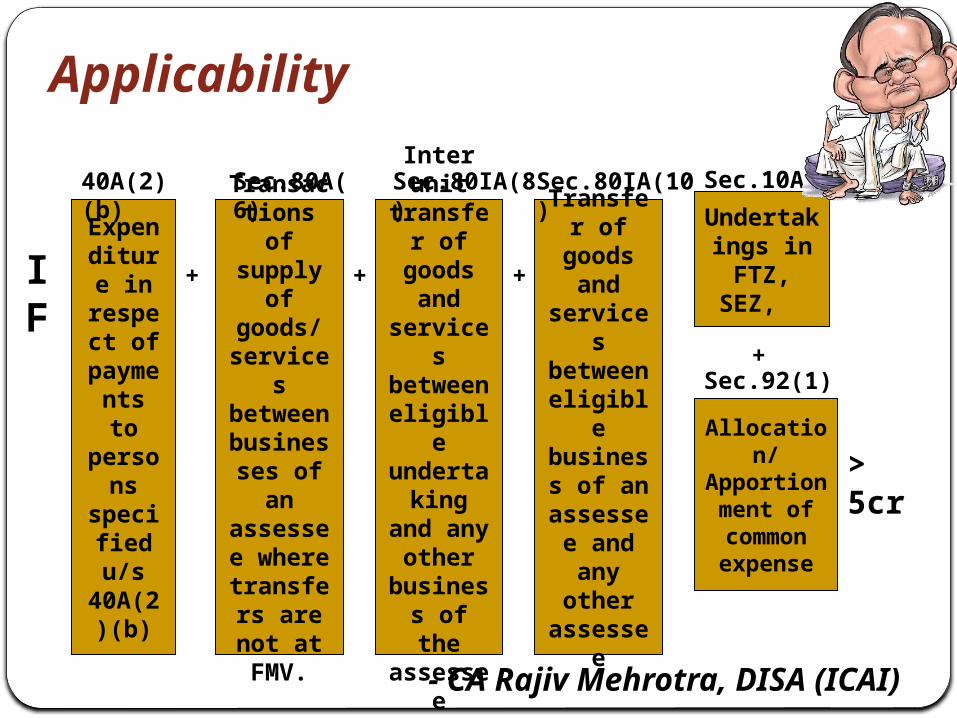

Specified Domestic Transaction

New Section 92BA: defines ‘specified domestic transaction’ as:Any expenditure in respect of which payment has been made

or is to be made to a person referred to in section 40A(2)(b). (Any time during the previous year)

Transactions of goods or services referred to in section 80A.Transfer of goods or services referred to in section 80IA(8)Transaction referred to in section 80IA(10)Transactions covered u/s 10AA.Any other transaction as may be prescribed.

Where the aggregate of such transactions entered into by the assessee exceeds 5 crore in any year.

- CA Rajiv Mehrotra, DISA (ICAI)

Applicability

Expenditure

in respect

of payments to

persons

specified u/s 40A(2)

(b)

Transactions of

supply of goods/

services between businesses of an

assessee where

transfers are not at

FMV.

Inter unit transfer of goods

and services between eligible

undertaking and

any other business

of the assessee

Transfer of goods

and services between eligible

business of an

assessee and any

other assessee

Undertakings in

FTZ, SEZ,

40A(2)(b) Sec.80A(6) Sec.80IA(8) Sec.80IA(10)

IF + + +

+

> 5cr

Sec.10A

Allocation/ Apportion

ment of common expense

Sec.92(1)

- CA Rajiv Mehrotra, DISA (ICAI)

Applicability

80IA Income from infrastructure, telecommunication, Industrial Park, Power sector etc.

80IAB Income of an undertaking or enterprise engaged in development of SEZ

80IB Income from certain industrial undertakings and housing projects

80IC Income from industrial undertaking set up in Sikkim, HP etc.

80ID Income from hotels etc. in Delhi, Faridabad and other districts

80IE Income from eligible undertakings in North Eastern States

- CA Rajiv Mehrotra, DISA (ICAI)

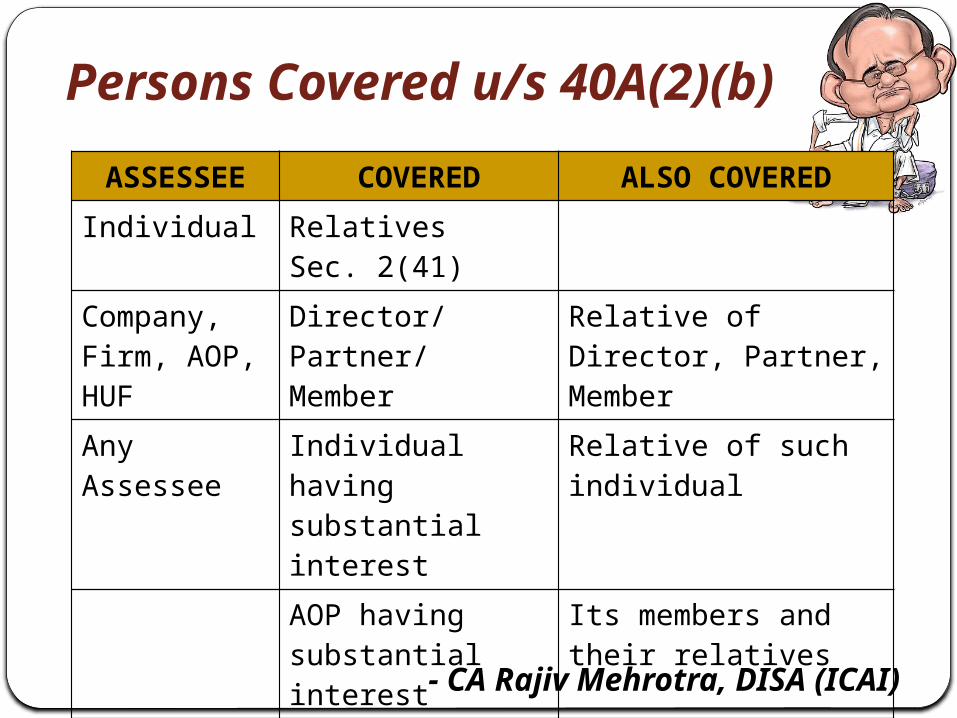

Persons Covered u/s 40A(2)(b)

ASSESSEE COVERED ALSO COVEREDIndividual Relatives Sec. 2(41)Company, Firm, AOP, HUF

Director/Partner/ Member

Relative of Director, Partner, Member

Any Assessee Individual having substantial interest

Relative of such individual

AOP having substantial interest

Its members and their relatives

HUF having substantial interest

Its members and their relatives

Company having substantial interest.

Its Directors, their relatives.

- CA Rajiv Mehrotra, DISA (ICAI)

…. Contd corporate

- CA Rajiv Mehrotra, DISA (ICAI)

…. Contd.

Section 2(41)“relative”, in relation to an individual, means the husband, wife, brother or sister or any lineal ascendant or descendant of that individual.

Relative- Chacha not included, first cousins not included, Brother in law , Nana , Mama etc. Not included.

Substantial interest => 20% . w.e.f. 01.04.13, where a company has substantial interest in

the business of an assessee, another company in which such company has a substantial interest will also be covered if any payment has been made to such company on account of any expenditure.

- CA Rajiv Mehrotra, DISA (ICAI)

Section 80IA(8) - internal transactions with more than one undertaking / units of the assessee, out of which one or more undertaking is enjoying tax holiday.

Objective of the section- Tax holiday units charge more than the market value for goods or services used by non-eligible units thus reducing tax liability.

“As per Section 80IA-(8), if the internal transfer of goods or services is not at fair market value, then profits or gains of transacting units shall be computed on the basis of ALP.”

- CA Rajiv Mehrotra, DISA (ICAI)

Section 80IA (10):As per this clause, “where it appears to the AO” when due

to close connection between assessee and ‘any other person’ or for any other reason, the eligible business of the assessee produces ‘more than the ordinary profit’, then for the purpose of deduction under this section, profit of the eligible business shall be determined by taking ALP of the transaction. Primary onus is on the taxpayer to prove that the transfer is at ALP. However, the department has to prove that the transaction is not at ALP.

- CA Rajiv Mehrotra, DISA (ICAI)

Section 80IA (10):The section starts with “Where it appears to the AO”“close connection” not defined. “Any other reason”Profits of eligible unit are higher”How will the assessee presume this.Ambiguity and lot of discretion to the AO. Against the

spirit of IT Act.All eligible units having transactions of over Rs 5 crores

from a single person and showing higher profits could fall in this.

Definitions…(an analysis)

- CA Rajiv Mehrotra, DISA (ICAI)

Company A has entered into international transactions with its A.E. aggregating to Rs.3 crores and transactions with specified parties u/s 40(A)(2)(b) aggregating Rs.3 crores. Will the “SDT” be covered under the Transfer Pricing provisions?

X ltd. makes payments to a Y ltd. (a foreign company) for imports amounting to Rs 6 cr. Y ltd. holds a 21% shares in X ltd. The transaction is not covered under IT. Whether the same would be covered under SDT?

Issues…

- CA Rajiv Mehrotra, DISA (ICAI)

Whether the same are covered?

a) Corporate guarantee to a relative will be covered?

b) Whether purchase of Capital Assets will be covered- (one case company has purchased from Directors)

c) Partners contribution as stock in trade.

d) Goods sold at lower value.

e) Interest free loan.

f) Payments for capital expenditure.

g) On incomes other than PGBP.

Issues…

- CA Rajiv Mehrotra, DISA (ICAI)

Whether the assessee who has made following payments is covered?

a) Salary to 3 directors Rs.30 lacs each.

b) Purchases from related party Rs 2 cr.

c) Sales to related party Rs. 2 cr

d) Purchase of land from related party- Rs.2 cr.

e) Interest paid to related parties Rs.1.50 cr.

f) Corporate guarantee fee charged Rs.1 cr

g) Allocation of common expenses with sister concern- Rs 50 lacs.

Issues…

- CA Rajiv Mehrotra, DISA (ICAI)

Issue

M/s Parle Products Ltd., Rudrapur, availing deduction u/s 80IC

M/s Parle Foods Ltd., Mumbai,

M/s Parle Distributors Ltd., Mumbai,

All three have Common Directors

Supply of biscuits

Manufacturing companiesMarketing company

- CA Rajiv Mehrotra, DISA (ICAI)

Issue

M/s Parle Products, Rudrapur, availing deduction u/s 80IC

M/s Parle Foods Ltd., Mumbai,

M/s Parle Distributors, Mumbai,

All three have Common Directors

Supply of biscuits

Covered by virtue of section 40A(2)(b)

Covered by virtue of sec.

80IA(10)

Not covered

Manufacturing companies Marketing company

- CA Rajiv Mehrotra, DISA (ICAI)

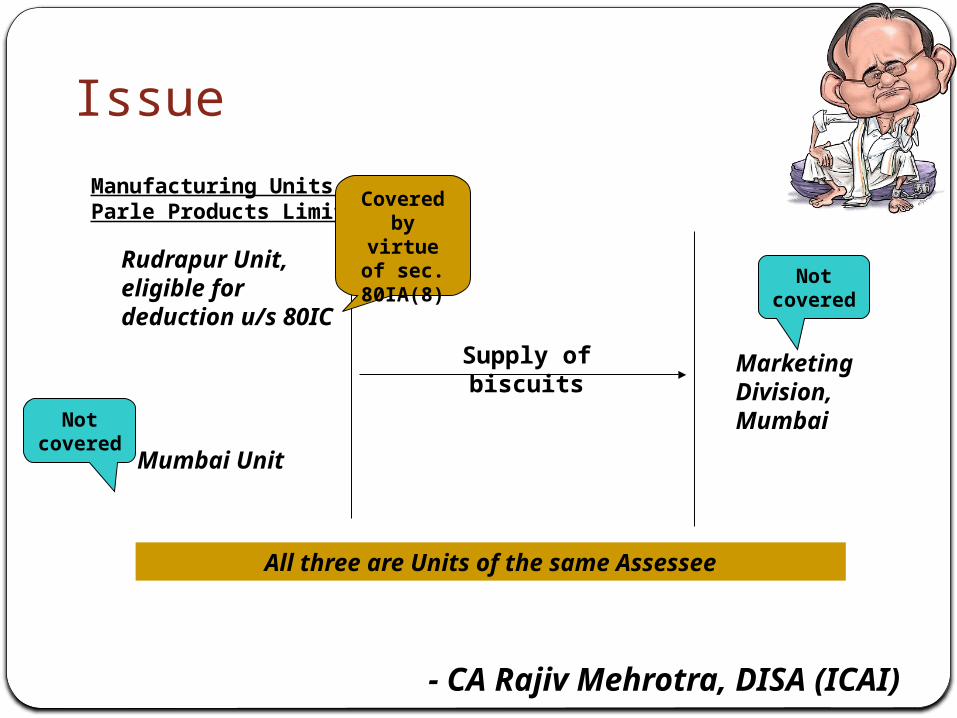

Issue

Rudrapur Unit, eligible for deduction u/s 80IC

Mumbai Unit

All three are Units of the same Assessee

Supply of biscuits

Manufacturing Units of Parle Products Limited

Marketing Division, Mumbai

- CA Rajiv Mehrotra, DISA (ICAI)

Issue

Rudrapur Unit, eligible for deduction u/s 80IC

Mumbai Unit

Marketing Division, Mumbai

All three are Units of the same Assessee

Supply of biscuits

Manufacturing Units of Parle Products Limited

Covered by virtue of sec. 80IA(8)

Not covered

Not covered

- CA Rajiv Mehrotra, DISA (ICAI)

Transactions Not Covered

Amount received by an assessee/undertaking on sale/supply of goods or services, if such entity/unit is not enjoying any tax holidays. i.e though the payer shall be covered by virtue of section 40A(2)(b), the recipient shall not be covered.

As regards units enjoying tax holidays, any transaction other than towards obtaining/providing goods or services, like financial transactions, payment for use of intangibles, etc. may not be covered for reporting purposes but can still fall under 80IA(10)

- CA Rajiv Mehrotra, DISA (ICAI)

Section Description

92 Charging section

92BA Meaning of SDT

92C Computation of ALP

92CA Reference to TPO

92D Maintenance of information & documents by parties to a SDT.

92E Report from an accountant

Consequential Amendments

Following sections to apply in relation of ‘specified domestic transactions’:

- CA Rajiv Mehrotra, DISA (ICAI)

Provisions Not Applicable

Section Description

92A Meaning of AE

92B Meaning of International Transactions

92CB Safe Harbour Rules

92CC Advance pricing agreement

92CD Effect of TP agreement

92F Definitions

- CA Rajiv Mehrotra, DISA (ICAI)

Amendments in Transfer Pricing Provisions

Section 92B: New Explanation inserted to include the following transactions within the scope of an ‘international transaction’:various transactions in tangible propertyvarious transactions in intangible property.

Not applicable to SDT

Benefit of DTAA not available to SDT thus effect of change of ALP of one assessee shall not effect the change in the other.

- CA Rajiv Mehrotra, DISA (ICAI)

…. Contd.

Section 92C: The second proviso to section 92C has been amended so as to provide that the maximum variation between the transaction price and ALP not attracting addition, shall be such percentage as may be notified, subject to a maximum of 3%.

Section 92CC & 92 CD: New sections have been inserted so as to introduce the concept of ‘Advance Pricing Agreement’. – Board to formulate a scheme. Not applicable in the cases of SDT.

- CA Rajiv Mehrotra, DISA (ICAI)

Methods for determining ALPSection 92C read with rule 10B & 10C

- CA Rajiv Mehrotra, DISA (ICAI)

Functional Analysis (FAR)

In transactions between two independent enterprises, it is essential to undertake a FAR analysis to arrive at the correct method and correct determination of ALP.

“F”- Functions to be performed Functions to be performed in respect of each

transaction.Roles of each partyStress on criticality of functions rather than number of

functions.

- CA Rajiv Mehrotra, DISA (ICAI)

“A”- Assets Used: the functional analysis should consider the type of assets used:

Plant and equipmentUse of valuable intangibles, financial assets etc.; andThe nature of assets used, such as age, market value,

location, property right protections available etc.

“R”- Risks assumedFinancial RiskProduct risk (R & D Risks, product liability risk)Market Risk

Functional Analysis (FAR)

- CA Rajiv Mehrotra, DISA (ICAI)

Methods for Computing ALPComparable

Uncontrolled Price (CUP) – it is the most preferred method as per OECD.Identify comparable

transactionsAdjust prices

charged to account for factors leading to differences in pricing between the transactions.

Internal CUP

A Ltd.

Related

External CUP

A Ltd. Related

UnrelatedB Ltd.

COMP

ARAB L E

T RAN S

AC T I ON

Unrelated

- CA Rajiv Mehrotra, DISA (ICAI)

Payments of Royalty Payments of interest. Payments of Directors Remuneration. Purchases and sales of goods in case of a manufacturing undertakings.( 80IA units).Whether payment of Directors Remn. As approved by CLB be taken as reasonable.?Whether Commission paid to Directors with no additional evidence of work done could be justified?

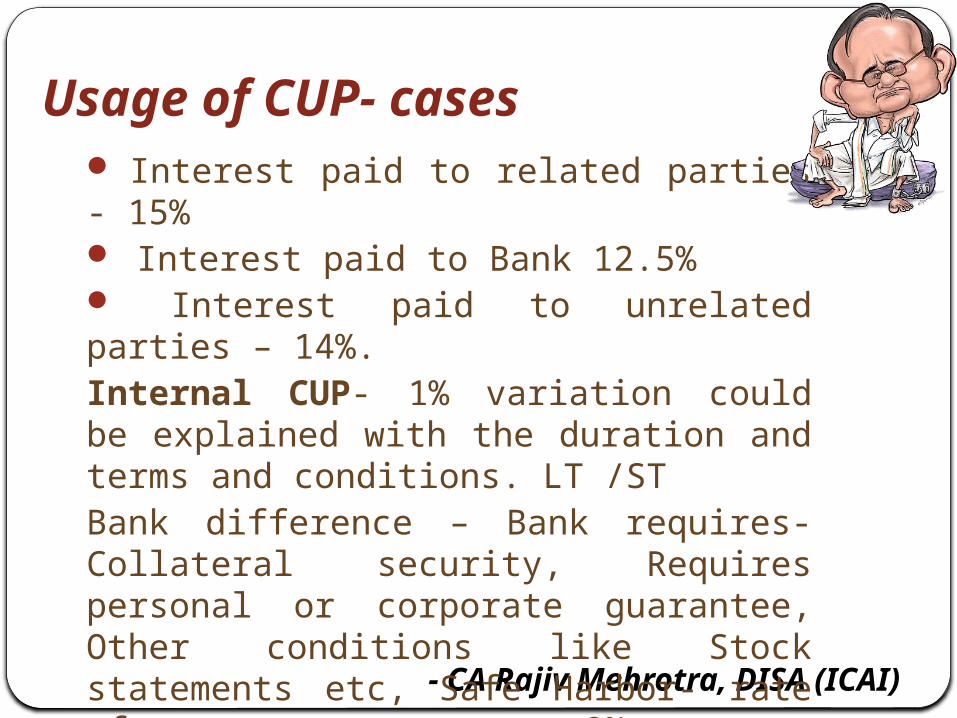

Usage of CUP- cases

- CA Rajiv Mehrotra, DISA (ICAI)

Interest paid to related parties - 15% Interest paid to Bank 12.5% Interest paid to unrelated parties – 14%.Internal CUP- 1% variation could be explained with the duration and terms and conditions. LT /STBank difference – Bank requires- Collateral security, Requires personal or corporate guarantee, Other conditions like Stock statements etc, Safe Harbor- rate of corporate guarantee- 2%. External Cup- what are those persons getting from other parties.

Usage of CUP- cases

- CA Rajiv Mehrotra, DISA (ICAI)

Resale Price Method (RPM)-

Generally applied where materials are purchased from related enterprises for re-sale to unrelated enterprises (Not reverse) (Independent Distributor etc. who makes no value addition)

Step I Identify resale price charged to unrelated party

Step 2 Deduct normal G.P. margin on similar comparable uncontrolled transaction (Either own or comparable)

Step 3 Deduct expenses on purchase

Step 4 Deduct impact of other functional differences (Risks), if any.

Step 5 The value arrived is the ALP as per RPM

Methods for Computing ALP

- CA Rajiv Mehrotra, DISA (ICAI)

Example of RSPAssessee purchases from sister concern a manufacturing

concern a T-Shirt at Rs 200 per pc. and sells the same at Rs 220 per pc.

Resale Price to unrelated party Rs 220

Gross Margin inunrelatedtransaction-10% Rs 22 (either self or market trend)

Purchase expenses incurred (say freight etc.) Rs 10

Adjustment of risks of AE say 2% Rs 4.40 (credit period/ quality/ brand/ stocking etc.)

ALP - (Rs 220- 22-10+4.40) Rs 192.40

Purchased from AE Rs 200 adjustment to be made Rs 7.60

- CA Rajiv Mehrotra, DISA (ICAI)

Cost Plus Method (C+) – A margin is added to the cost and the comparison is made between a product in a controlled environment with that in an uncontrolled environment- Best in cases of service industry or cases where semi-finished goods are sold to related parties.

Step I Identify Direct and Indirect costs in relation to production of goods/services supplied to related enterprise

Step 2 Derive normal markup in similar internal or external uncontrolled transactions

Step 3 Adjust markup for functional and other differences

Step 4 Add the markup arrived in Step 3 to the total cost

Step 5 The value arrived is the ALP as per CPM

Methods for Computing ALP

- CA Rajiv Mehrotra, DISA (ICAI)

Methods for Computing ALPProfit Split Method (PSM)- Generally where segregation

of profits between related parties in respect of eligible transactions cannot be identified (integrated) and the profit has to be allocated on the basis of functions performed. Independent data can also be helpful in analysis. Also in case where intangibles play a vital role. E.g one case where there is a concern which is doing clinical trials for its holding and final billing is same.

Services- composite service charge and functions divided between various parties. Or an entity manufacturing something to be used for manufacture by an AE of its own brand.

- CA Rajiv Mehrotra, DISA (ICAI)

Profit Split Method- ExamplePerfect Trials Ltd.(PTL) and Perfect Labs Ltd.(PLL) are

related enterprises, engaged in conducting clinical trials

- Has technical staff

- Maintains lab

- Conducts trials

- Sends reports to PTL

- Has Brand value

- Identifies projects and customers

- Supervises operations of PLL

- Bears market/product risk

Customer

PLL PTL

Charges ‘x’

margin

Charges ‘y’

margin

Total Margin = x + yTo be split on the basis of FAR and

independent commercial principals

- CA Rajiv Mehrotra, DISA (ICAI)

Transactional Net Margin Method- Here the transactions of the assessee are compared with the “tested parties” whose transactions are entered in an uncontrolled environment. Comparison with independent entities. (Similar business and similar circumstances).

Case of Granite miner selling granite.

Methods for Computing ALP

- CA Rajiv Mehrotra, DISA (ICAI)

TNMM

Step I Compute net margin realised by an enterprise from its related enterprise (margin may be N.P.Ratio, ROI.

Step 2 Similar margin realised by the enterprise from an unrelated enterprise or by other enterprises in the industry. (Internal TNMM)Or Margin of an uncontrolled party in an uncontrolled environment( comparable party).

Step 3 Adjust margin for functional and other differences

Step 4 The adjusted margin is used to calculate ALP.

- CA Rajiv Mehrotra, DISA (ICAI)

Most Appropriate Method

Such other method prescribed by CBDT- not prescribed

Most appropriate method be taken,

If more than one methods is considered appropriate and result in different values, the arithmetic mean of the values shall be the ALP.

- CA Rajiv Mehrotra, DISA (ICAI)

Most Appropriate Method- A Guideline as per guidance note of ICAI.

S.No. Method Transaction for which it is suitable

1. CUP Method Loans, Royalties, service fees, transfer of tangibles (goods etc.)

2. Resale price method

When distributor does not perform significant value addition to the project.

3. Cost plus method (i) Sale of raw materials/semi finished materials

(ii) Joint facility agreements(iii) Long term buy & Sell arrangements(iv) Provision of services

Traditional transaction Methods:

- CA Rajiv Mehrotra, DISA (ICAI)

S.No. Method Transaction for which it is suitable

4. Profit split method Provision of integrated services by more than one AE

5. Transaction Net margin Method

Transfer of semi finished goodsDistribution of finished products where resale price method appears to be inappropriate.Provision of services

Transactional Profit Methods:

Most Appropriate Method- A Guideline

- CA Rajiv Mehrotra, DISA (ICAI)

If no method can be applied and the transactions are so unique then the assessee can apply Rule 10AB a sixth method . This rule provides that

“ any method which takes into account the price which has been charged or paid, or which would have been charged or paid , for the same or similar uncontrolled transaction, with or between non-associated enterprises, under similar circumstances, considering all the relevant facts”

If transactions are unique

- CA Rajiv Mehrotra, DISA (ICAI)

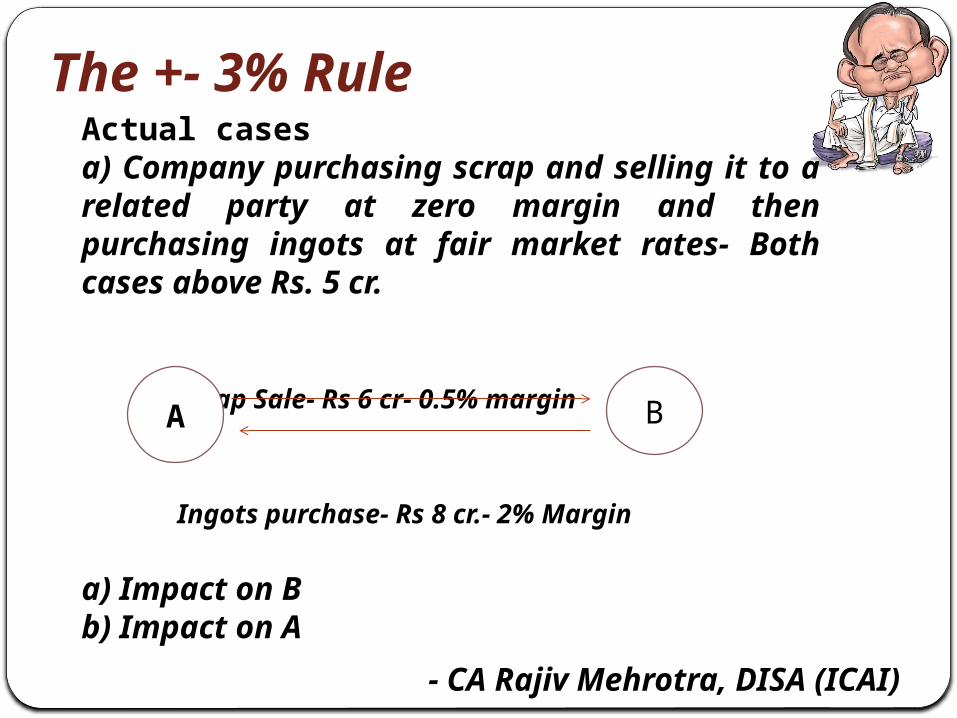

Second proviso to section 92C(2) provides that if the variation between ALP so determined and the price at which the SDT has taken place is does not excess such percentage as may be prescribed (not exceeding 3%) there shall be no adjustment made on the prices.

If “a” is Arms Length Price. “b” is price of SDT then the variation permitted would be

“a-b”/ “b” if is less than or equal to 3% then no adjustment required.

Vide notification dated 15/4/2013- rate prescribed- 1% for wholesale traders and 3% for others.

The +- 3% Rule

- CA Rajiv Mehrotra, DISA (ICAI)

Actual casesa) Company purchasing scrap and selling it to a related party at zero margin and then purchasing ingots at fair market rates- Both cases above Rs. 5 cr.

Scrap Sale- Rs 6 cr- 0.5% margin

Ingots purchase- Rs 8 cr.- 2% Margin

a) Impact on Bb) Impact on A

The +- 3% Rule

A B

- CA Rajiv Mehrotra, DISA (ICAI)

Actual cases

Company A (Indian Co.) purchases material- Oil on High Seas basis. The Value of Oil is Rs 60000 PMT. The company sells the same on High seas to its AE at a margin of Rs 500 pmt. The value of sales are Rs 100 crores.Advise the company regarding applicability of SDT and the applicability of method.

Cases:

- CA Rajiv Mehrotra, DISA (ICAI)

Issue – A company makes the following payments to Directors

as commissiona) MD- Technical Person- Rs 2 crore (Major

shareholding)b) WTD- Non Technical – class 10th passed- 1 croreOther paymentsc) Rent paid to sister concern - Rs 30 lacsd) Interest to Sister concern A - 10%- 40 lacse) Interest to sister concern B - 12%- 10 lacsf) Purchases from sister concern Rs – 1.20 cr.

Now issues of TP.Effect of disallowance by the TPO.

Issues…

- CA Rajiv Mehrotra, DISA (ICAI)

Directors remunerationa) How to benchmark ?b) More difficult if directors have substantial interest.c) Now spouses or ladies remuneration subject to more

scrutiny- Also disallowances u/s 64.d) Whether Schedule-XIII of the Companies Act could be

a benchmark? Not applicable to Pvt Ltd Co.’se) Report provides for Book Value, ALP and method of

arriving the ALP – what method and what records.f) Commission to Directors a risky proposition now.

Some judgments have also come for treating the same in lieu of dividend. (Section 36(1)(ii).)

Issues…

- CA Rajiv Mehrotra, DISA (ICAI)

A unit generating electricity and availing benefit of section 80IA- supplies power to its related concern/ its own unit at Rs 10 per unit whereas power as per the government rate is Rs 4 per unit and 80% power used is from the Government by its own unit. Issue arising out of the above. Will will lead to an

adverse inference by the AO.?Will the 80IA unit be able to show profits and take

deduction u/s 80IA.

Issues…

- CA Rajiv Mehrotra, DISA (ICAI)

Documentation required

- CA Rajiv Mehrotra, DISA (ICAI)

Rule 10D(1) - “Every person who has entered into an international transaction or SDT shall keep and maintain….”. The same has been added by the amendment in Rules on .. June 2013 where a new form has also been prescribed.

Rule 10D(1) has 13 sub-clauses (a) to (m) which are very exhaustive and elaborate and in case of each case covered under SDT the same should have been started to have been maintained.

Documentation must for all SDT covered cases.

Documentation

- CA Rajiv Mehrotra, DISA (ICAI)

Documentation- Sec.92D r.w.Rule 10D

Entity Related

- Profile of the Assessee

- Profile of Group- Profile of the

entity with whom IT/SDT is undertaken

- Broad description of Industry

Transaction Related

- Nature and terms- Nature of property

transferred and services rendered

- Quantitative & value wise details

- FAR analysis- Description &

reason for method for ALP

Price Related

• Economic & financial analysis, forecasts or other estimates prepared

• Details of uncontrolled transactions

• Comparable data and financial information

- CA Rajiv Mehrotra, DISA (ICAI)

AUDIT REPORT

- CA Rajiv Mehrotra, DISA (ICAI)

Scope of Audit

Examination of records of only those transactions which relate to SDT/IT

Not to express the True and Fair view on the Financial statements of the auditee.

Ensure maintenance of appropriate documentation as per Rule 10D & report thereon.

Not the duty of the CA to evaluate TP documentation and conclude on the Arms Length nature of the transaction.

Ensure that the method stated by the auditee has actually been used for calculation of ALP

- CA Rajiv Mehrotra, DISA (ICAI)

Scope of AuditAs per the Guidance Note of ICAI on Section 92E:Para 9.17: The accountant must limit his scope of work

and the review procedures to the extent certified in Form No.3CEB. For e.g. in the Annexure the method which has been used to determine the arm’s length price needs to be stated. In this context the accountant is only required to ensure that the method stated as being used to determine the arm’s length price by the assessee has actually been used and it is not the accountant’s responsibility to ensure that the method so used is the most appropriate method as prescribed by the Board.

- CA Rajiv Mehrotra, DISA (ICAI)

Scope of Audit

Examination and certification of particulars given in Annexure to Form 3CEB to state whether they are “true and correct”

Para 9.12 – CA should go through the records maintained by the taxpayer and match the same with documents prescribed however CA is not responsible for the content of the transactions and documentation maintained by the taxpayer.

Para 9.13 - If any document is not maintained, then the accountant should suitably qualify his report or disclose the same in his report depending upon the facts and circumstances of each case.

- CA Rajiv Mehrotra, DISA (ICAI)

Audit Report- Form 3CEB

PART APoint 1- 7 : Basic information of the assessee- same as TARPoint No.8 & 9: Details of value of IT & SDT.PART B- Reporting of International TransactionsClauses 10- List and description of AE’s for IT’sClauses 11- 20 – Reporting of Various IT’s & ALPPART-C- Reporting of SDT’sClause 21- List and description of AE’s for SDT.Clause 22-25- Reporting of Various SDT’s & ALP

- CA Rajiv Mehrotra, DISA (ICAI)

Common transaction wise information called for under above clauses:

Name and address of each AEDescription of each transactionTotal amount involved in each transaction (type)

As per BooksALP, as computed by MAM

Method used for determination of ALP

Audit Report- Form 3CEB

- CA Rajiv Mehrotra, DISA (ICAI)

Procedure of Assessment

- CA Rajiv Mehrotra, DISA (ICAI)

Procedure

Report as per form 3CEB has to filed online earlier Manual.

Now only the CA will sign and upload earlier both were signing.

Keep a signed copy of the management with us.

Revision of TP report ? Return in the respective form has to be uploaded. Case may be selected for scrutiny. The AO to complete all the routine scrutiny except provisions

relating to the report under SDT. AO if he considers necessary and expedient so to do, may refer,

SDT transactions to the TPO with the prior approval of the Commissioner- Thus the satisfaction of AO is a must. Even the approval of the Commissioner is mandatory (and should not be mechanical).

- CA Rajiv Mehrotra, DISA (ICAI)

Procedure

TPO can consider the issue under reference or any other issue relating to IT but not SDT (92CA/92CB not applicable).

TPO has power of summon u/s 131, survey u/s 133A and collecting information u/s 133(6).

No deduction (only enhancement) permissible in respect of adjustment by TPO.

Enhancement only if variation between Transaction value and ALP worked out by TPO is more than 3% or 1%.

Assessment by the TPO of SDT transactions. Same sent to AO and binding on him. No deduction u/s Chapter VI or 10A etc. on such enhancement.

- CA Rajiv Mehrotra, DISA (ICAI)

Section 144C- In case of variations noted by TPO the AO shall give a draft

order to the assessee The assessee may accept it or submit his objections The same will be referred to DRP (Dispute Resolution Panel). DRP may consider the issue referred or additional issues as

well. The DRP (of Three Commissioners) shall pass an order which

would be binding. The AO/ assessee may file an appeal against the order of the

DRP.

Dispute Resolution Panel

- CA Rajiv Mehrotra, DISA (ICAI)

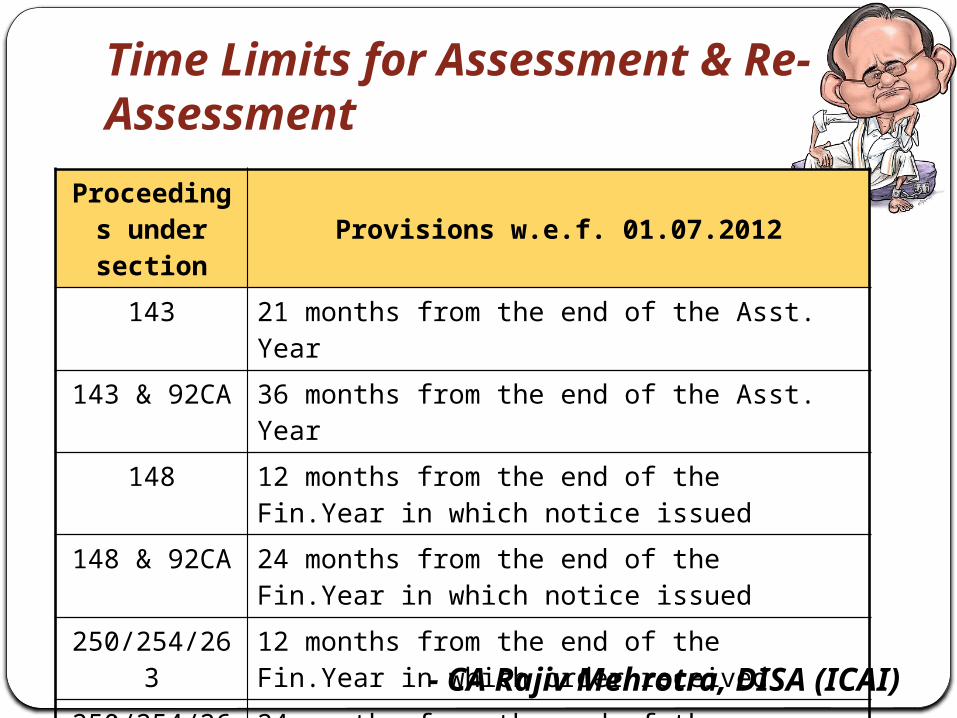

Time Limits for Assessment & Re-Assessment

Proceedings under section

Provisions w.e.f. 01.07.2012

143 21 months from the end of the Asst. Year

143 & 92CA 36 months from the end of the Asst. Year

148 12 months from the end of the Fin.Year in which notice issued

148 & 92CA 24 months from the end of the Fin.Year in which notice issued

250/254/263 12 months from the end of the Fin.Year in which order received

250/254/263 & 92CA

24 months from the end of the Fin.Year in which order received

- CA Rajiv Mehrotra, DISA (ICAI)

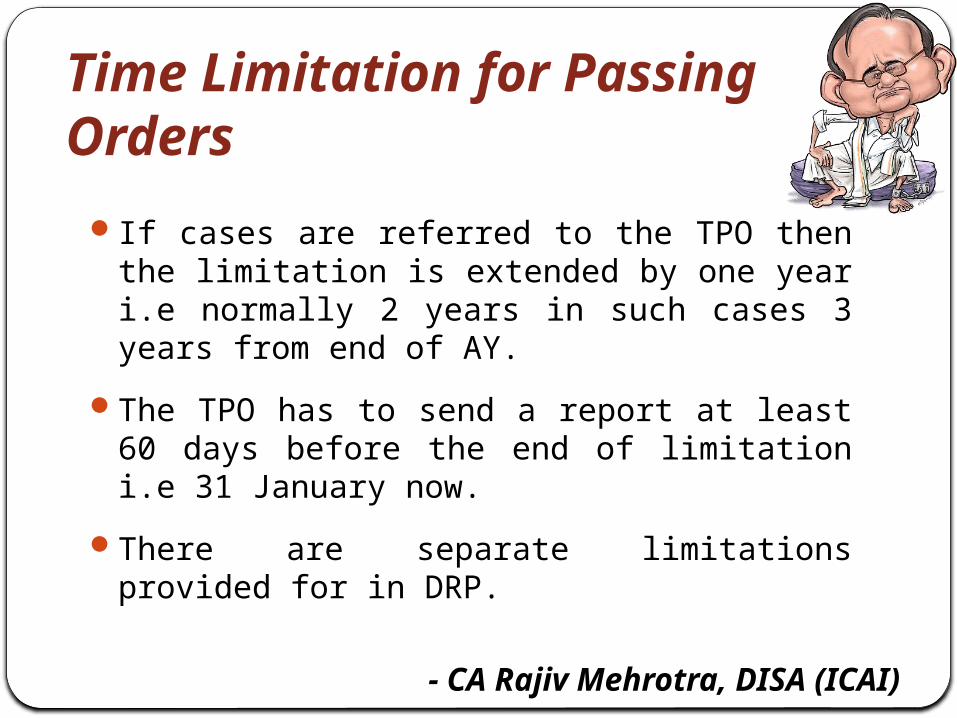

Time Limitation for Passing Orders

If cases are referred to the TPO then the limitation is extended by one year i.e normally 2 years in such cases 3 years from end of AY.

The TPO has to send a report at least 60 days before the end of limitation i.e 31 January now.

There are separate limitations provided for in DRP.

- CA Rajiv Mehrotra, DISA (ICAI)

Penalties..

Section Description Quantum

271AA failure to maintain prescribed documents or information

2% of transaction Value

failure to report any international transaction or SDT which is required to be reported,

Maintaining/furnishing any incorrect information or documents

271G Failure to furnish documents/information - - Do - -

271BA Failure to furnish report 1 lac

271(1)(c) If adjustment is made to income upon assessment

100%-300% of tax on adjustment

amount

- CA Rajiv Mehrotra, DISA (ICAI)

Recommended

![Code of Conduct for Organisations By; CA Kamal Garg [B. Com (H), FCA, DISA (ICAI)] cakamalgarg@gmail.com](https://img.dokumen.tips/doc/110x75/56649c955503460f94952c2d/code-of-conduct-for-organisations-by-ca-kamal-garg-b-com-h-fca-disa.jpg)