m - 5

5.1 INTRODUCTION

5.2 MATERIALS PLANNING AND BUDGETING

5.3 SOURCES AND SELECTION OF RAW MATERIALS

5.4 NEGOTIATING AND ORDERING PROCEDURE

5.5 CREDIT DAYS AND LIMITS EXTENDED BY SUPPLIERS TO THE SOCIETIES

5.6 RAW MATERIALS PURCHASED BY THE SOCIETIES

5.7 SOURCES OF FINANCE FOR PURCHASE OF RAW MATERIALS

5.8 SYSTEM OF REORDERING OF RAW MATERIALS

m

148

5.1 INTRODUCTION

Purchasing has come to stay as most important function of materials management.

The moment a buyer places an order he commits a substantial portion of the finance

of the firm, which affects the working capital and cash flow position. The basic

objective of the purchasing function is to ensure continuous supply of quality raw

materials, at the lowest price. For ensuring this, there is large number of well-known

parameters such as right price, hght quality, right contractual terms, right time, right

source, right materials at right place, right mode of transportation, right quantity and

right attitude. All these have to be considered jointly. A diagram indicating these is

shown in exhibit-17.

EXHIBIT-17 OBJECTIVES OF PURCHASE FUNCTION

RIGHT PLACE OF DELIVERY

PRICE COMMUNICATION

RIGHT SOURCE VENDOR RATING

PURCHASE RESEARCH

RIGHT CONTRACTS

LEGAL ASPECTS

RIGHT TRANSPORTATION COST ANALYSIS OF TRANSPORTATION

AND LOGISTICS

RIGHT MATERIAL VALUE ANALYSIS

STANDARDISATION

1 RIGHT ATTITUDE

TRAINING SWOT ANALYSIS

MATERIALS INTELLIGENCE

' 'RIGHTTIME RE-ORDER POINT'

LEAD TIME ANALYSIS

RIGHT QUALITY " REJECTIONS AND SPECIFICATIONS

. ^ - v ^ - - f,^ •?»;•<'/-; ~ r

RIGHT QUALITY EOQ & INVENTORY

MODELS

RIGHT PRICE NEGOTIATION

LEARNING CURVE

Source: Gopalakrishnan P, and Sundaresan M, Materials Management an integrated approach, New Delhi, Prentice-Hall of India Private Limited, 1996, 56-

' Gopalkrishnan P. and Sundaresan M. Materials Management an Integrated Approach. New Delhi. Prentice-Hall of India Private Limited, 1996, 55.

149

Every firm engaged in production of one or more type of goods aims at profit-

optimisation. To accomplish this objective, it tries to procure the desired material for

the operation of its activities at a low cost. In some cases, a firm can buy some raw

materials and process it in their own premises in the desired quantity at a relatively

low cost. However, in some other cases, the procurement of these materials done

from outsiders is more advantageous. In this connection, some societies may

process on own and/or they may buy the raw materials from outsiders.

The basic raw materials used by the handloom weavers' co-operative societies in the

study are cotton yarn, zari, silk, art silk, dyes, chemicals, packaging materials etc.

These materials come from various places of our country.

5.1.1 Cotton Yarn

It is the main raw material, which is in use from the time of primitive weaving. The

supply of cotton yarn is mainly from Coimbatore, and other places like Bangalore,

Gokak, Bijapur, Hulkoti and Sholapur. Cotton and mercerised cotton yarns are sold

in a bundle of 5 kilograms called muthe. This muthe consists of number of hanks.

To weave 9 yards sari it requires nearly 3-4 hanks. Un-dyed cotton hanks after

purchasing are dyed locally with direct, naphtol, vat or reactive colours.

150

5.1.2 Silk Yarn

The silk yarn is purdiased from Bangalore and it is only natural silk, which is in use.

Each packet of silk weighs about 30 kilograms and during every visit, 2-3 such

packets are purchased from Bangalore. Nearly 3-4 saris can be woven with 1

kilogram of silk. The de-gummed, bleached and dyed silk yarn is available in the

market for the use of the weavers.

5.1.3 Artificial Silk (Rayon) yarn

This is third type of yarn, which is used, in large quantity in the handloom textile

industry. This yarn is soft, pliable and have very good sheen and is used as a

substitute for pure silk. Rayon is usually supplied from Bombay and also from

Coimbatore, Kanpur and Ahmedabad. From each kilogram of this yarn nearly 3 saris

may be produced. It usually forms warp and extra warp used both in body and

border of the sari and khana. This artificial silk is manufactured at various places viz,

1. South Indian Viscose, Coimbatore,

2. National Rayon Corporation, Bombay,

3. Indian Rayon Century, Bombay,

4. Rayon from Trivancore, Cochin,

5. J.K. Rayons, Kanpur,

Rayon from different areas reaches the local market either in dyed or undyed state.

If undyed, dyeing is done locally. There are no wholesale dealers for these raw

materials. Therefore, much of the purchases are made from the market, outside the

state. However, a few whole sale dealers of some mills are in Guledgudda, where

some purchases can be made.

151

5.1.4 Zari

The other raw material required for sari is zari and is also called as brocade. It has

been in use for 15 to 20 years. This connes mainly from Surat and to some extent

from Bombay also. Zari is used in borders of rayon and silk saris. This zari is not a

pure gold or silver one but is an imitation of it.

5.1.5 Dyes and Chemicals

The attractive colours of the sari increase the value and fetch attractive prices. In

olden days only black, red and yellow colours were in use, and obtained from

vegetable ongin, namely indigo, maddar plant and turmeric roots respectively.

These dyes were used to colour the cotton yarns. Now Ciba Company dyes silk,

with acid colours, which is supplied to the nearby wholesale dealers. Cotton and

artificial silk (rayon) are dyed with naphthol, vat, procaine, direct, reactive aniline

colours supplied by Amar Dyes, Hoechst, Indokem, and AtuI company of Bombay.

These companies along with the dyestuffs they supply the necessary chemicals.

The wholesale dealers of dyes are at Bagalkot, Rabakavi, Banahatti and Sholapur

from where the retail dealers make their purchase.

In the study area raw materials like cotton yarn and art silk are used by all the

sample societies. But, materials like zari is used by 7 societies, silk by 6 societies,

dyes and chemicals by 7 societies and packing materials by 4 societies out of 15

sample societies.

152

The most important raw material for handloom is tlie yarn. It was observed that the

cost of the yarn constitutes 50 to 80 per cent of the total cost of the production

depending on the fabric woven.^ But, the handlooms consume hank yarn. There are

two kinds of hanks - Lee hank consisting of seven lees which is suitable for

bleaching, dyeing, finishing etc., and cross hank suitable for direct winding on to the

bobbins. Superior quality yarn is required for warp.

This yarn is produced both by the privately owned spinning mills, co-operative

spinning mills and composite mills. Almost entire production of yarn is in organised

mills and hence handloom sector is totally dependent on mills for their supply. The

cost of yarn has always been the cause for concern. The cost of yarn constitutes

major portion of fabric's cost.

Apart from spinning infrastructure, what needs is adequate up-gradation of dyeing

and finishing. Handlooms use about 80 per cent pre-dyed yarn. Individual weavers

dye the yarn themselves or that job will be undertaken by the society's dye-house or

sometimes that will be done from the outside jobbers also. Raw materials and other

inputs are not only made available but they must also be bought at the most

competitive prices as per the conditions in market. And they must be available when

they are needed in the right quantities and qualities.

^ Government of India, Report of the Fact-finding Committee (Handloom and Mills), Calcutta. 1942, 87.

153

The various topics deait in tills chapter are;

1. Material Planning and budgeting.

2. Sources and Selection of raw materials.

3. Negotiating and ordering procedure.

4. Credit days and limits extended by the suppliers to the societies.

5. Raw materials purchased by the societies

6. Sources of finance for purchase of raw materials.

7. Reordering system of raw materials.

5.2 MATERIALS PLANNING AND BUDGETING

The materials planning and budgeting function have a prominent place in the

integrated materials management set-up. This is so because, planning for materials

and working out a realistic budget not only helps to motivate people but also serves

as a control device. Material planning Is the way of determining the requirements of

raw materials that go Into meeting the production needs within the economic

investment policies. Factors which affect materials planning are price trends,

business cycles, credit policy, production capacity, lead times, inventory levels,

working capital, season, communication system etc. The material planning is based

on the forecast for the end products. Once the demand forecast Is made, it is

possible to go through the exercise of materials planning.

The relationship between materials planning and other major functions are shown in

exhibit-18.

154

EXHIBIT-18 MATERIAL PLANNING FUNCTIONS

PRODUCTION PROGRAM

(PER LOOM BASIS)

FEED BACK INFORMATION AND REVIEW

MATERIALS PLAN

(CONSUMPTON PER LOOM BASIS)

Source: Gopalakrishnan P, and Sundaresan M, Materials Management an integrated approach, New Delhi, Prentice-Hall of India Private Limited, 1996, 26.

Normally, material planning should be done on the basis of sales forecast and

production programme (per loom basis). It was found during field survey that, all the

weavers' co-operative societies in the study area are not planning their materials in a

scientific way. They estimate roughly not on sales forecast but on the basis of

working looms consumption and on the past experience, which is not an exact one.

They follow very rude and unscientific method of material planning.

Materials budget can be prepared based on the product requirements. Based on

that delivery schedules for materials are worked out. The process of preparing

material budget is shown in exhibit -19.

155

EXHIBIT-19 PROCESS OF PREPARING MATERIAL BUDGET

7ENT0RY

REQUIREMENTS^ OF MATFRIAI R J |

^

INVENTORY OF MATERIALS ON HAND

AMOUNT OF MATERIALS

TO BE PURCHASED

> H —

FORCAST OF PRICES &

RATES

PURCHASE RlinfiFT

ACTUAL PlIRCHASF

VARIANCE REPORTING

FOR CONTROL

Source; Gopalakrishnan P, and Sundaresan M, Materials Management an Integrated Approach, New Delhi, Prentice-Hall of India Private Limited, 1996, 31,

As shown in exhibit - 19, material procurement budget takes into account both

inventories on hand and orders on hand. Besides the budget, it may be formulated

to attain certain targeted inventory levels. This budget is formulated both in terms of

quantity and money. The materials department knows exactly its resource

availability so that they can plan its purchases in the most optimum way taking into

account price trends, market position etc. Further, material budget should be

prepared to help the financial management of materials by taking into consideration

the yearly, the quarterly and the monthly cash requirements. It was noticed during

field survey that, none of the handloom weavers' co-operative societies in the study

area were preparing the matenals budget.

156

In addition, periodic statements should be prepared and this budget should be

compared with actuals so that major variances can be highlighted for action. In the

field survey, it was found that majority of the handloom weavers' co-operative

societies do not prepare budgeted inventory report for their reference. But, societies

'A', 'B', 'F', 'G', 'H', ' I ' , 'K', 1", prepare the review of inventory report monthly,

societies 'C, 'D', 'E', 'O', quarterly, societies 'J', 'N' yearly and society 'M' was

preparing the inventory review report only on as and when necessary basis. It was

also found that, review of inventory report is prepared only by those societies who

have borrowed over draft or cash credit from District Central Co-operative Bank

(DCCB) because, they have to submit a copy of the same to them.

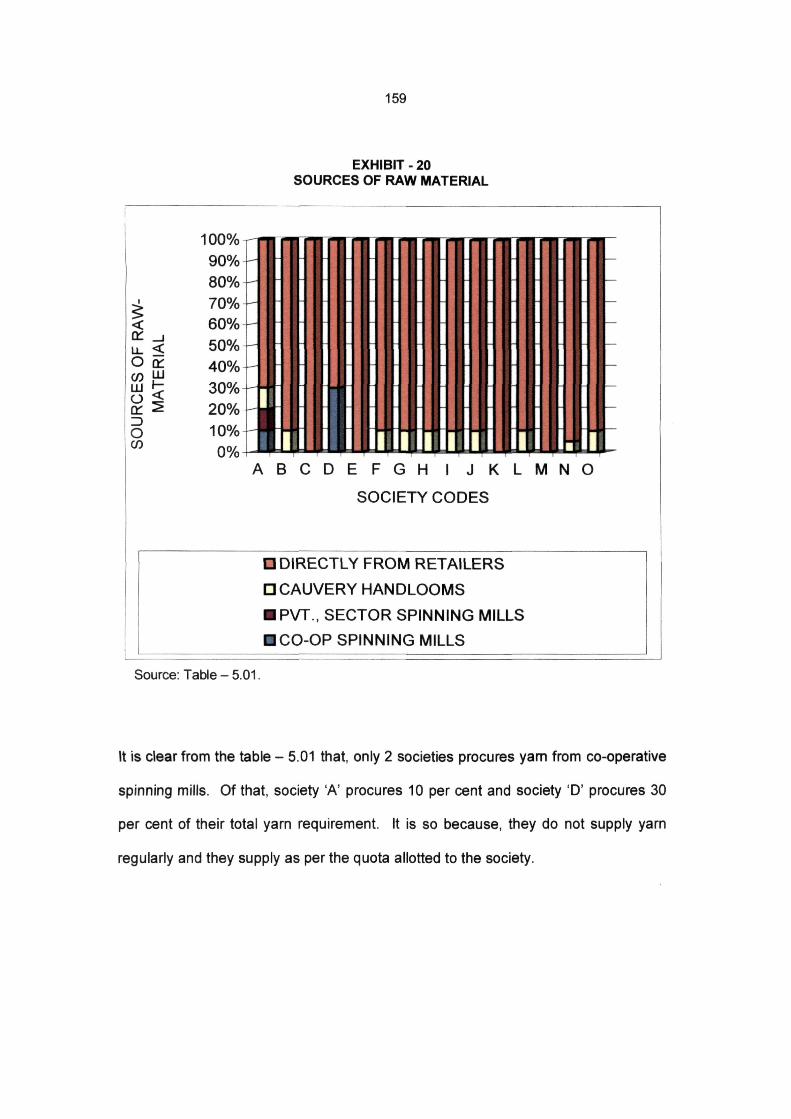

5.3 SELECTION OF SOURCES OF RAW MATERIALS

The process involved in selection of sources of raw materials are searching and

selection. Society should identify the possible sources and select such sources,

which will meet the delivery and quality requirements in the long run at competitive

price levels.

The source from which the raw material is procured should be dependable and

capable of supplying items of uniform quality. The buyer has to decide which item

should be procured from whom. Aspects such as source selection, source

development, buyer-seller relationship and vendor selection purchase decisions will

be made in weavers' co-operative societies by either secretary, Managing/Controlling

Committee or sometimes both.

157

In 3 (20 per cent) sample societies selection of sources of raw materials Secretary

takes decision alone. In these societies Managing Committee members are not

active. Further, in 7 (46.67 per cent) out of total sample, Managing Committee or

Controlling Committee take decisions. In 2 (13.33 per cent) societies, selection of

suppliers will be made jointly by both Secretary and the Chairman of the society. In

remaining 3 (20 per cent) societies. Secretary and Managing Committee members

jointly take the decision of purchasing the raw materials.

Reputed suppliers of raw materials are intangible assets to any organisation. For the

organisation they are not only suppliers of materials but they are also extremely

important sources of information with regard to market conditions, price trends and

business climate. The various sources of raw materials for handloom weavers' co

operative societies in the study area are co-operative and private spinning mills,

Cauvery handlooms (Karnataka Co-operative Handloom Weavers' Federation Ltd.,

Bangalore) and other private traders. The status of raw material suppliers has been

presented in table - 5.01.

158

TABLE - 5.01 VARIOUS SOURCES OF PURCHASE OF RAW MATERIALS

MADE BY THE SAMPLE SOCIEITIES

SL. NO.

SOCIETY CODE

SOURCES OF RAW MATERIALS IN PERCENTAGES

SL. NO.

SOCIETY CODE

CO-OP SPINNING

MILLS

PVT., SECTOR

SPINNING MILLS

CAUVERY HANDLOOMS

DIRECTLY FROM

RETAILERS TOTAL

1 A 10 10 10 70 100

2 B 0 0 10 90 100

3 C 0 0 0 100 100

4 D 30 0 0 70 100

5 E 0 0 0 100 100

6 F 0 0 10 90 100

7 G 0 0 10 90 100

8 H 0 0 10 90 100

9 1 0 0 10 90 100

10 J 0 0 10 90 100

11 K 0 0 0 100 100

12 L 0 0 10 90 100

13 M 0 0 0 100 100

14 N 0 0 5 95 100

15 0 0 0 10 90 100

Source: FIELD SURVEY.

159

EXHIBIT - 20 SOURCES OF RAW MATERIAL

< IT _, u. < O a:

o < on S Z) o CO

100% 90% 80% 70% 60% 50% 40% 30% 20% 10%

0% 1 A B C D E F G H I J K

SOCIETY CODES

L M N O

Q DIRECTLY FROM RETAILERS

DCAUVERY HANDLOOMS

• PVT., SECTOR SPINNING MILLS

• CO-OP SPINNING MILLS

Source: Table - 5.01.

It is clear from the table - 5.01 that, only 2 societies procures yam from co-operative

spinning mills. Of that, society 'A' procures 10 per cent and society 'D' procures 30

per cent of their total yarn requirement. It is so because, they do not supply yarn

regularly and they supply as per the quota allotted to the society.

160

Even though handlooms are spread all over the country, the bulk of the yarn is

produced In a few states i.e., about 65 per cent of the total installed capacity is in the

Tamil Nadu, Maharashtra and Gujarat.^ This has resulted in uneven supply of yarn to

the handloom sector. In the study area there are 3 co-operative spinning mills, out of

which only one spinning mill is active." Moreover, its yarn production is very less

when compared to the demand. Naturally, societies have to import the same from

other places. In the study area-spinning mill is located at Banahatti, local societies

get yarn on quota basis, but not for outstation societies. This source cannot be relied

on regular basis.

Further it was also found that, only society 'A' is obtaining yarn from private spinning

mills, which amounts to 10 per cent of the total procurement made by it. It is so

because, this society is running its activities successfully, its production and

consumption of material is more and it is possible for them to deal with private

spinning mills also. Moreover, they are economically sound but other societies

cannot make an attempt to deal independently or procure directly from the mills.

Third source of raw material is Cauvery handlooms, which distributes yarn and art-

silk to the weavers' co-operative societies. Its branch has been located at Ilka!

where majority of societies are concentrated. Ten societies out of 15 procure raw

material from this source that amounts to 5 to 10 per cent of their total purchase.

3 Jain L C, Handlooms Face Liquidation, Powerlooms mock at Yojana Bhavan, Economic and Political Weekly, 27 August 1983, 1521.

•• Weavers Guide, Department of Handloom and Textiles, Zilla Parishad, Bijapur, 8.

161

It is true that materials supplied through Cauvery handlooms are at subsidised rates

but they supply irregularly with limited quantity. They supply the materials against

advance demand draft, but they deliver the material 2 to 3 months later. These

societies cannot sustain this blockage of funds, since they have inadequate working

capital. Further, executives are of the opinion that, they prefer this source only when

their financial position is better. They complain that Cauvery handlooms do not

supply to the society the raw materials of required variety, in required quantity well in

time to the societies. They opt to buy the material as and when the quota is allotted

which is very rare.

The last and foremost major source of raw material in the study area comes from the

private local dealers. This source ranges between 75 to 100 per cent of the total

procurement made by the sample society. These dealers' terms of sales are

favourable i.e., credit sales and customised as per the society requirements. The

society executives are of the opinion that these private local dealers supply required

quality and quantity of raw materials to the society. Majority of these local dealers

are Marawari's; who have made their base at Guledgudda, llkal, Bagalkot, Rabakavi

and Banahatti.

162

It was observed that powerlooms and mills consume lion's share of yarn produced in

the country. This has serious implications for handloom sector, in the form of

shortage of yarn and the consequent loss of employment to weavers.̂ The overall

shortage of yarn for the handloom sector is in fact, a multi-edged murderous

weapon. Shortage of yarn affects not only output and employment, but also the price

of yarn, the competitive capacity of the handloom sector and eventually wages and

earnings of the weavers.

It was found during field survey that sample societies in the study area make their

purchases on credit to the extent of 60 to 90 per cent of their total purchase made.

Because of credit purchases, it was found that there would be price difference of 5 to

10 per cent when compared to other sources of raw materials. Further, it was noted

that, when there is scarcity in the supply of raw materials and seasonal periods they

go for cash purchase even from the private local dealers. These dealers are

preferred because they meet the requirements of the society in terms of quality and

delivery. A personal follow-up is possible to ensure speedy delivery of raw materials.

sOp. cit. 1521.

163

5.4 NEGOTIATING AND ORDERING PROCEDURE

After the preliminary screening and selection, starts the process of negotiations with

the vendors for placing orders. Negotiation is a battle of wits and an art of

embodying sophisticated tactics and manoeuvres by both the buyer and the seller.

The parameters affecting the process of negotiations of an item are; availability,

number of sources, price, delivery, penalty, discounts, packing and the

transportation. But negotiator should not adopt a strategy of hard choices and soft

options. Care should, however, be taken to adopt negotiations on a selective basis.

Further, correct and cordial relations with the vendors are essential for mutual co

operation. The vendors should be provided with the same courtesies that an

organisation expects for its own salesmen or gives to its customers. Various

aspects, including terms of delivery, price and quality are finalised during

negotiations and then the purchase orders are released.

Majority of suppliers of raw material has concentrated at places like llkal, Guledgudd,

Amingad, Sulebhavi, Bagalkot, Banahatti, Rabakavl, Jamkhandi Mahalingapur, and

Rampur where they have made their base to operate the business. IVIajorlty of

handlooms are concentrated in and around these areas. It is the practice in the

study area that representative of suppliers of raw material visit the society once a

week on regular basis and book the orders for the same. Personal contacts between

the executives of the society and the supplier often help them in maintaining a

smooth relationship.

164

The executives of the society in the study area have rated the following factors high

on the basis of priority while selecting the suppliers of raw materials, same has been

presented in exhibit - 21.

EXHIBIT - 21 RATINGS OF THE INFLUENCING FACTORS ON SELECTION OF

SUPPLIERS OF RAW MATERIAL

Source: Field Survey.

Most of the societies have rated credit terms as most important criteria, which will

influence the decision while selecting the suppliers of raw materials. Because, as it

is stated earlier that, majority of the societies face problem of liquidity of funds and

secondly, they depend extensively on borrowed funds.

165

5.5 CREDIT DAYS AND LIMITS EXTENDED BY SUPPLIERS TO THE SOCIETIES

Credit days extended by the local vendors of raw materials to the society is

presented in the table - 5.02.

TABLE - 5.02 NO. OF CREDIT DAYS EXTENDED BY THE SUPPLIERS TO THE

SAMPLE WEAVERS' CO-OPERATIVE SOCIEITIES

SL. NO.

NO. OF CREDIT DAYS

NO. OF SUPPLERS

SL. NO.

NO. OF CREDIT DAYS

UPTO 3 BETWEEN 4 & 6 7 & ABOVE TOTAL SL. NO.

NO. OF CREDIT DAYS

NO. OF SOCIETIES

% T 0 TOTAL

NO. OF SOCIETIES

% T 0 TOTAL

NO. OF SOCIETIES

% T 0 TOTAL

TOTAL NO. OF

SOCIETIES

% T 0 TOTAL

1 UPT0 15 E = 1 20.00 D,G = 2 66.67 C,K = 2 28.56 5 33.33

2 UPTO 30 L,0 = 2 40.00 A = 1 33.33 F,H, N = 3

42.88 6 40.00

3 UPTO 45 l,J = 2 40.00 Nil = 0 00.00 B,M = 2 28.56 4 26.67

4 TOTAL 5 100.00 3 100.00 7 100.00 15 100.00

Source: FIELD SURVEY.

It is clear from the table - 5.02 that, suppliers of raw materials in the study area have

extended credit to 4 (26.67 per cent) societies upto 15 days, for 6 (40 per cent)

societies upto 30 days and remaining societies have received upto 45 days. The

overall credit granted by the suppliers of raw materials to the societies is between 15

to 45 days. But, the more the credit days extended by the suppliers the more the

price charged by them to the society. In subsequent table credit limit extended by the

suppliers to the society has been discussed.

166

As majority of the societies in ttie study area depend exclusively on credit purchase

from the private local dealers of raw materials, it was felt necessary to study the

credit worthiness of the society to evaluate the credit limits extended by the suppliers

of raw materials. The credit limit extension to the concerned society is on the basis

of repayment pattern within stipulated time, scale of production, attitude and

relationship of member executives of the society.

TABLE - 5.03 CREDIT LIMIT EXTENDED BY THE SUPPLIERS TO THE

SAMPLE WEAVERS' CO-OPERATIVE SOCIETIES

SL.NO. AMOUNT IN Rs. NO. OF SOCIETIES % TO TOTAL

1 UPTO 25,000 J,0 = 2 13.34

2 25,001 - 50,000 E,F,G,H,L,M = 6 40.00

3 50,000 - 75,000 C,K,N = 3 20.00

4 75,001 - 1,00,000 D,l = 2 13.33

5 1,00,000 & ABOVE A,B = 2 13.33

6 TOTAL 15 100.00

Source: FIELD SURVEY.

167

As per the table - 5.03, 6 (40 per cent) societies have received the credit limit upto

the extent of Rs. 50,000. It is encouraging to state that 2 (13.33 per cent) societies

in each range have received credit upto 25,000, upto Rs. 75,000 and one lakh.

Further, it shows that the extent of credit limit where these societies are getting is not

sufficient. Because, they have inadequate working capital and insufficient liquidity

position on account of seasonal sales and low sales turnover. These reasons have

made them to depend exclusively on private dealers, as they do not have any other

alternatives: However, it was learnt from the analysis that society 'A' and 'B' are

getting better credit limits because of their goodwill and high turnover capacity.

5.6 RAW MATERIALS PURCHASED BY THE SOCIETIES

It was found during the field survey that none of these weavers' co-operative

societies follow the centralised purchasing policy in the study area. The purchase of

raw materials made by the societies from 1991-92 to 1995-96 has been presented in

the table - 5.04.

168

TABLE - 5.04 RAW MATERIALS PURCHASED BY THE SAMPLE WEAVERS' CO-OPERATIVE

SOCIETIES DURING 1991-92 TO 1995-96 (Rupees In Lakhs)

SL. NO.

SOCIETY CODE 1991 -92 1992-93 1993-94 1994-95 1995-96 AVG.

PURCHASES

1 A 35.34

(31 .32 ) 48.77

(36.01 ) 53.84

(32.58 ) 48.40

(29 .97 ) 41.67

(25.40 ) 45.60

(30.85 )

2 B 2.61

(2 .32 ) 5.98

( 4 . 4 2 ) 11.87

( 7 . 1 8 ) 8.50

( 5 . 2 7 ) 12.04

(7 .34 ) 8.20

(5.55 )

3 C 12.66

(11 .22 ) 13.98

(10 .32 ) 17.39

(10 .52 ) 22.53

(13 .95 ) 20.28

( 1 2 . 3 6 ) 17.37

(11 .75 )

4 D 13.97

(12 .38 ) 17.47

(12 .90 ) 21.37

(12 .93 ) 10.20

( 6 . 3 2 ) 18.11

( 1 1 . 0 4 ) 16.22

(10.97 )

5 E 12.31

(10.91 ) 10.94

( 8 . 0 8 ) 8.05

( 4 . 8 7 ) 13.74

( 8 . 5 1 ) 14.35

(8.75 ) 11.88

(8.03 )

6 F 2.88

( 2 . 5 5 ) 4.57

( 3 . 3 7 ) 4.40

( 2 . 6 6 ) 4.13

( 2 . 5 6 ) 4.41

( 2 . 6 9 ) 4.08

(2.76 )

7 G 3.94

( 3 . 4 9 ) 5.48

(4.04 ) 6.00

(3.63 ) 6.78

( 4 . 2 0 ) 7.49

( 4 . 5 7 ) 5.94

( 4 . 0 2 )

8 H 13.10

(11.61 ) 12.26

(9.05 ) 12.59

( 7 . 6 2 ) 13.11

( 8 . 1 2 ) 14.72

(8 .98 ) 13.16

(8.90 )

9 1 3.49

( 3 . 0 9 ) 3.54

( 2 . 6 1 ) 4.65

(2.81 ) 4.64

( 2 . 8 7 ) 4.25

( 2 . 5 9 ) 4.11

( 2 . 7 8 )

10 J 1.51

( 1 . 3 4 ) 1.60

( 1 . 1 8 ) 3.10

( 1 . 8 8 ) 2.90

( 1 . 8 0 ) 2.64

( 1 . 6 1 ) 2.35

( 1 . 5 9 )

11 K 2.66

( 2 . 3 5 ) 3.78

( 2 . 7 9 ) 5.77

(3.49 ) 11.38

(7.05 ) 8.09

( 4 . 9 3 ) 6.33

( 4 . 2 9 )

12 L 4.44

(3.94 ) 4.10

(3.03 ) 4.57

( 2 . 7 7 ) 5.55

( 3 . 4 4 ) 4.95

(3 .02 ) 4.72

(3.20 )

13 M 1.67

( 1 . 4 8 ) 1.05

(0.78 ) 7.04

( 4 . 2 6 ) 4.18

( 2 . 5 9 ) 4.48

( 2 . 7 3 ) 3.69

( 2 . 4 9 )

14 N 2.24

( 1 . 9 9 ) 1.85

( 1 . 3 6 ) 3.28

( 1 . 9 8 ) 3.61

( 2 . 2 3 ) 4<30

( 2 . 6 2 ) 3.06

( 2 . 0 7 )

15 0 0.02

(0.02 ) 0.08

(0.06 ) 1.35

(0.82 ) 1.85

( 1 . 1 4 ) 2.25

( 1 . 3 7 ) 1.11

(0.75 )

16 TOTAL 112.84

(100.00) 135.42

(100.00 ) 165.27

(100.00) 161.50

(100.00) 164.04

(100.00) 147.82

(100.00)

Note: Figures in parenthesis are percentages to total Source: FIELD SURVEY.

169

EXHIBIT • 22 AVERAGE PURCHASE OF RAW MATERIALS MADE BY THE

SAMPLE WEAVERS' CO-OPERATIVES

• A V E R A G E PURCHASES

Source: Table - 5.04.

The table - 5.04 reveals that average purchase of raw materials like cotton yarn,

art-silk, dyes, chemicals and packaging materials for the period of 1991-92 to 1995-

96 is Rs. 9.85 lakhs per society. For the year 1991-92 average purchase per

society was Rs. 7.52 lakhs and later by 1993-94 it has increased to Rs. 11.02 lakhs.

But, in subsequent years 1994-95, purchase of raw material has fallen down to Rs.

10.77 lakhs. The reasons for decrease in purchase is mainly due to increase in

prices and scarcity of raw materials, outdated designs and patterns, less

productivity and unfavourable market conditions.

170

5.7 SOURCES OF FINANCE FOR PURCHASE OF RAW MATERIALS

The moment society places an order it commits a substantial portion of finance of the

society, which affects the working capital and cash flow position. The secretary or

executive members are highly responsible to make payments as and when they fall

due. In order to appreciate various sources of finance for committing on purchase of

raw materials for smoothening the production process it was felt necessary to study

this.

The sales proceeds are the major source for making payments to the suppliers of

raw materials of the society. As the sales of handloom products are seasonal, they

have to depend extensively on external sources of finance for purchase of raw

materials. Those external sources of finance are Reserve Bank India (RBI) loans.

National Bank for Rural Development (NABARD) loans, members' deposits or hand

loans from the members and moneylenders who are the last resorts.

Since, the majority of the sample weavers' co-operative societies in the study area

face inadequate working capital position, this worst financial position do not permit

them to buy the raw materials on cash terms. The cash credit and/or overdraft

facility extended by the RBI or NABARD or DCC banks is not sufficient to meet their

working capital requirements. This reason has made them to rely on members'

deposits and moneylenders. The interest paid to moneylenders will be adjusted with

some other head. For making this adjustment they consult the experts, who will take

the job of manipulating and maintaining the accounts till the final accounts are

prepared and audited by the Government audit officials. They render mobile

services to various weavers' co-operative societies in surrounding areas of the study.

171

Further, it was also noticed ttiat weavers' co-operative societies are not prompt in

payments, for tliis reason,'Local vendors' association is planning to charge penalty

interest from June, 1997 at the rate of 2 per cent per month on overdue balance of

the society.®

5.8 SYSTEM OF REORDERING OF RAW MATERIALS

it was found from the study that, weavers' co-operative societies reorder for required

goods as and when the need arises. Further, it was also noticed that all societies

depend exclusively on private traders for supply of raw materials. Dealers'

representatives visit personally every week to book the orders of raw materials. So,

societies will order for required raw materials as and when necessary. The minimum

level of inventory of raw materials will be decided per loom consumption on monthly

basis. Maximum level of inventory is determined on the basis of supply conditions of

raw materials, future plan for production and price fluctuations.

In two, society's Managing Committee will take decisions connected to reordering of

materials, safety and maximum inventory level, but in remaining societies; Secretary

will take decision in consultation with the concerned clerk. Concerned clerk and/or

Secretary will control the inventory. The Secretaries of respective societies are of

the opinion that, they have safe, efficient controlling and storage facilities for raw

materials. But, they are facing the problem for storing finished goods during off

season.

' Yam Merchant Association, Guledgudda.

172

Most of the society respondents in tine study area were of the opinion that, they will

be able to get raw materials in required quantities, and qualities regularly if, the

society mal<es cash purchases and if they are in good bool<s with the suppliers. In

case, the raw materials are scarce, every dealer insists on cash terms. During such

times if society's financial condition is good they will procure raw materials by cash

otherwise they have to borrow from external sources with interest to make cash

purchase and to run the production uninterrupted. This problem was found with

every society in the study area. Further, they are of the opinion that, if the society is

making cash purchases, rates quoted by the dealers will be very competitive,

otherwise exorbitant. Moreover, if they purchase on cash terms, then they wouldn't

face the problem of inputs.

It is true that, quality of raw materials supplied and price quoted by the Cauvery

handlooms is comparatively very low. But, they supply the raw materials on piece

meal distribution, irregularly and that too against advance demand draft, which is a

big financial burden for the society. Because of these reasons, invariably weavers'

co-operative societies have to depend extensively on private suppliers. Of all the

sample weavers' co-operative societies, society 'A' is managing its purchases in

better way.

Further respondents of the societies were of the opinion that Cauvery handloom is

not reliable source of supply of raw materials. For the purpose of overcoming this

procurement of raw materials problem, all the weavers' co-operative societies in the

study area have formed Apex society at district level; which is yet to start functioning.

173

Thus, it can be seen from the above analysis that, the private dealers meet a major

part of the materials required by the weavers' co-operative societies. Other sources

meet only marginally and invariably societies have relied upon private traders. The

raw materials have to pass through the hands of the producers, wholesalers, and

retail dealers before reaching the society and its member weavers.

Recommended