Embed Size (px)

Citation preview

zargon.ca

Corporate PresentationNovember 13, 2017

Forward Looking-Advisory

Forward-Looking Statements - This presentation offers our assessment of Zargon's future plans and operations as at November 10, 2017, and contains forward-looking statements. Such statements are generally identified by the use of words such as "anticipate", "continue", "estimate", "expect", "forecast", "may", "will", "project", "should", "plan", "intend", "believe" and similar expressions (including the negatives thereof). In particular, this presentation contains forward-looking information as to Zargon’s corporate strategy and business plans, Zargon’s oil exploration project inventory and development plans, Zargon’s dividend policy and the amount of future dividends, future commodity prices, Zargon’s expectation for uses of funds from financing, Zargon’s capital expenditure program and the allocation and the sources of funding thereof, Zargon’s cash flow and dividend model and the assumptions contained therein and the results there from, anticipated payout rates, 2017/18 and beyond production and other guidance and the assumptions contained therein, estimated tax pools, Zargon’s reserve estimates,Zargon’s hedging policies, Zargon’s drilling, development and exploitation plans and projects and the results there from and Zargon’s ASP project plans 2017/18 and beyond, strategic alternatives review process, the source of funding for our 2017/18 and beyond capital program including ASP, capital expenditures, costs and the results therefrom. By their nature, forward-looking statements are subject to numerous risks and uncertainties, some of which are beyond our control, including such as those relating to results of operations and financial condition, general economic conditions, industry conditions, changes in regulatory and taxation regimes, volatility of commodity prices, escalation of operating and capital costs, currency fluctuations, the availability of services, imprecision of reserve estimates, geological, technical, drilling and processing problems, environmental risks, weather, the lack of availability of qualified personnel or management, stock market volatility, the ability to access sufficient capital from internal and external sources and competition from other industry participants for, among other things, capital, services, acquisitions of reserves, undeveloped lands and skilled personnel. Risks are described in more detail in our Annual Information Form, which is available on our website. Forward-looking statements are provided to allow investors to have a greater understanding of our business.You are cautioned that the assumptions, including, among other things, future oil and natural gas prices; future capital expenditure levels; future production levels; future exchange rates; the cost of developing and expanding our assets; our ability to obtain equipment in a timely manner to carry out development activities; our ability to market our oil and natural gas successfully to current and new customers; the impact of increasing competition; our ability to obtain financing on acceptable terms; and our ability to add production and reserves through our development and acquisition activities used in the preparation of such information, although considered reasonable at the time of preparation, may prove to be imprecise and, as such, undue reliance should not be placed on forward-looking statements. Our actual results, performance, or achievement could differ materially from those expressed in, or implied by, these forward-looking statements. We can give no assurance that any of the events anticipated will transpire or occur, or if any of them do, what benefits we will derive from them. The forward-looking information contained in this presentation is expressly qualified by this cautionary statement. Our policy for updating forward-looking statements is that Zargon disclaims, except as required by law, any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.Barrels of Oil Equivalent - Natural gas is converted to a barrel of oil equivalent (“Boe”) using six thousand cubic feet of gas to one barrel of oil. In certain circumstances, natural gas liquid volumes have been converted to a thousand cubic feet equivalent (“Mcfe”) on the basis of one barrel of natural gas liquids to six thousand cubic feet of gas. Boes and Mcfes may be misleading, particularly if used in isolation. A conversion ratio of one barrel to six thousand cubic feet of natural gas is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. Given that the value ratio based on the current price of crude oil as compared to natural gas is significantly different from the energy equivalency of 6:1, utilizing a conversion ratio on a 6:1 basis may be misleading as an indication of value. The estimates of reserves and future net revenue for individual properties may not reflect the same confidence level as estimates of reserves and future net revenue for all properties, due to the effects of aggregation. Estimated reserve values disclosed in this presentation do not represent fair market value. Discovered Petroleum Initially-In-Place (“DPIIP”) is that quantity of petroleum that is estimated, as of a given date, to be contained in known accumulations prior to production. The recoverable portion of discovered petroleum initially in place includes production, reserves, and contingent resources; the remainder is unrecoverable.The aggregate of the exploration and development costs incurred in the most recent financial year and the change during that year in estimated future development costs generally will not reflect total finding and development costs related to reserves additions for that year.

2

Third Quarter 2017 Highlights

Production has improved in each core area (due to Q3 and Q1‐Q3 capital programs of $1.77 and $6.41 million). Announced fully funded “low‐growth” H1 2018 budget focused on waterfloods and oil well optimizations.

Compared to Q2 2017:• Oil production improved to 2,037 bbl/day from 1,921 bbl/day in Q2 2017 ( 6% increase)• Total production increased by 128 boe/d to 2,628 boe/d from 2,500 boe/d in Q2 2017 ( 5% increase)• Operating costs declined to $20.17/boe from $22.49/boe in Q2 2017 ( 10% decrease)• G&A costs declined to $3.68/boe from $4.89 in Q2 2017 ( 25% decrease)

3

0

500

1,000

1,500

2,000

2,500

Jan‐16 Apr‐16 Jul‐16 Oct‐16 Jan‐17 Apr‐17 Jul‐17

Alberta (excluding ASP)

North Dakota

Little Bow ASP

Oil Prod

uctio

n (bbl/d)

Zargon Operated Oil Production Zargon’s oil properties are pressure supported by waterfloods, tertiary recovery schemes or natural aquifers. Base corporate oil production decline is less than 10% per year. Stable (or low growth) production volumes can be delivered with low cost, exploitation (plumbing type) capital programs focused on waterflood and other enhancements.

Third Quarter Summary

Pro Forma BalanceSheet

4

Operations Trends in Q3 2017:

Slowly improving oil production volumes coming from low cost oil exploitation programs.

Cash costs (operating, transportation, G&A and interest) are declining or are stabilized, thereby resulting in lower costs on a $/boe basis.

ASP production volumes (rate and oil cut) continue to improve.

Q3 2017 Results

Zargon’s capital structure provides stakeholders significant time to realize Zargon’s substantial option value relating to higher oil prices.

Bank debt – $nil

Working Capital – Positive $5.2 million

Convertible Debentures – $41.9 million

Net Debt – $36.7 million

Q1 2018 Hedges: 1,000 bbl/d @ $70.15 Cdn./bbl (WTI)

Q2 2018 Hedges: 500 bbl/d @ $71.00 Cdn./bbl (WTI)

OperationsTrends

Balance Sheet

Zargon’s Q3 2017 results:

Q3 production volumes of 2,628 boe/d, a 5% quarter over quarter gain. Nine month 2017 production of 2,569 boe/d is 3% higher than 2017 guidance of 2,500 boe/d

Q3 funds flow of $1.76 million ($0.06/share)

Q3 field cash flow of $3.27 million

$1.77 million Q3 capital program focused on waterfloods and well reactivations

Zargon Key Investment Highlights

5

Oil Exploitation Focus

• Zargon is an oil‐weighted company focused on the exploitation of mature oil properties.• Following 2012‐16 divestment programs, Zargon’s remaining operated oil reservoirs continue to be

characterized by significant oil‐in‐place, low recovery factors and low oil production declines.• Over its history, Zargon has raised $210 million of equity capital and paid out $367 million in dividends and

distributions.

Low Decline Oil Production• Zargon’s low corporate oil decline of less than 10% per year is enabled by reservoir pressure support from

natural aquifers, waterfloods and tertiary floods. Consequently, stable oil production can be delivered through relatively small capital programs focused on waterfloods, reactivations and facility modifications.

Oil Exploitation Opportunities

• Zargon’s properties provide waterflood optimization opportunities plus exploitation drilling opportunities that enable improved reservoir recovery factors in existing pools.

• The McDaniel reserve report books 12 P+P exploitation locations with average per well parameters of 63 Mbbl oil reserves, 47 bbl/d initial rate and $0.93 MM all‐in costs.

Control of Properties &Key Infrastructure

• Very high working interest and operatorship across core operating areas, batteries and facilities.• Majority of batteries and facilities have been upgraded in the last five years.• An actively managed abandonment and reclamation program. Alberta LMR is 1.36 (November 2017).

Little Bow ASP Project• At higher oil prices, the existing ASP infrastructure can be utilized to resume AS injections in high‐graded areas

and for multiple other ASP phases and Polymer only projects seeking a 10 percent incremental oil recovery on over 80 million barrels of working interest oil‐in‐place.

Other Corporate Attributes• Zargon holds ~$192 million of high quality tax pools (Sept. 30, 2017), includes $148 million of non‐capital losses.• Zargon has retained a TSX listing, plus strong operating, accounting, land and finance capabilities, and can readily

manage additional assets with minimal additional costs.

Zargon is a Canadian (and North Dakota) oil and gas producer that provides exceptional torque to higher oil prices, in addition to offering a variety of attractive oil exploitation opportunities including oil exploitation horizontal infill drills and a long term Southern Alberta tertiary recovery project.

H1 2018 Budget / Outlook

H1 2018Projections

6

H1 2018 production volumes are forecast at 2,600 boe/d, a four percent increase from 2017 production guidance of 2,500 boe/d and a six percent increase from 2016 Q4 production volumes of 2,449 boe/d.

The budgeted capital programs are fully funded by corporate cash flows at WTI oil prices of $68.50 Cdn./bbl, or better.

Without hedges, Zargon’s price sensitivity for every $5 Cdn. per barrel (WTI) increase in oil price is an annualized $3.3 million ($0.11 per share)

Zargon will continue to focus on cost control and low cost “plumbing type” oil exploitation projects that efficiently add oil production and oil reserves.

Recognizing that Zargon’s assets are comparatively inexpensively priced and provide significant unrecognized oil price option value, Zargon will continue with its strategic alternatives process focused on unlocking this upside. The process may result in a sale of all or part of the company, a financing, merger or other business combination.

H1 2018 Next Steps

H1 2018 Capital Budget

Zargon has announced a $3.7 million H1 2018 capital budget allocated $2.0 million to reactivations, recompletions and waterflood modifications, $1.0 million for Little Bow polymer chemical purchases and $0.7 million of land retention and other costs.

Zargon’s H1 2018 site reclamation and abandonment budget is set at $1.0 million. These expenditures are expected to maintain compliance with the Government of Alberta’s Directive 13 and Inactive Well Compliance programs, while delivering small improvements in our corporate Alberta Liability Management Ratio.

zargon.ca

Cash Flow Projections & Valuations

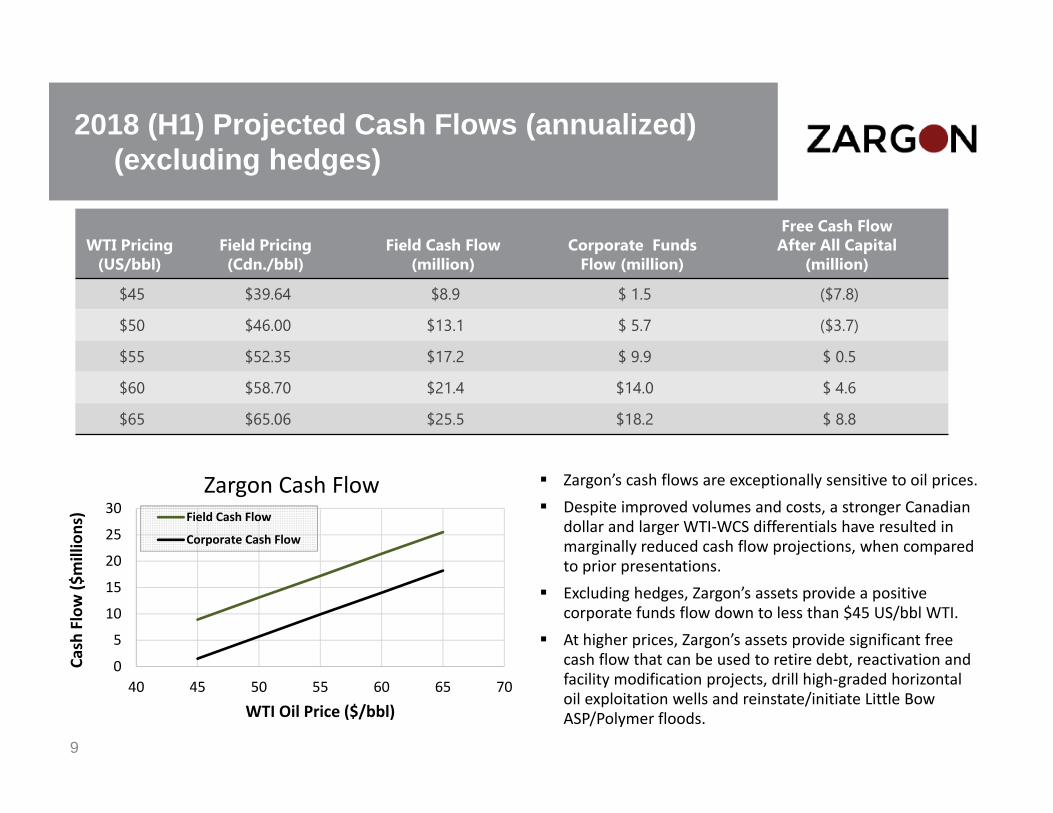

2018 (H1) Cash Flow Parameters (excluding hedges)

Oil 2,050 bbl/d Gas 3.30 mmcf/d Equiv. 2,600 boe/d (79% oil and liquids). Royalties 9% Alberta, 24% North Dakota (includes state and severance taxes)

Oil Prices WTI – WCS diff.: $13.32 US/bbl (avg. of prompt month and 2017 avg.)Field price: WCS less $0.60 Cdn./bbl (from 2017 averages)

Gas Prices $2.05/mcf Alberta average field price (AECO strip less $0.25/mcf adj.) Exchange 0.787 $US/$Cdn (Nov. 3, 2017 forward strip) G&A Costs $2.0 million (improved annualized rate of $4.0 million) Interest $1.7 million – revised debenture cost, no interest on cash balances

Production

2018 (H1) Costs & Capital

Other Parameters

8

Operating $9.6 million (annualized run rate of $19.2 million) Abd. & Reclam. $1.0 million (meets regulatory obligations while improving LMR) US Taxes $ nil ASP Capital $1.0 million chemical costs (status quo polymer only) Main. Capital $0.7 million non‐discretionary land and other costs Exploit Capital $2.0 million (Bellshill optimizations, Little Bow non‐ASP waterfloods and

recompletions, North Dakota waterflood optimizations); no wells to be drilled

9

WTI Pricing(US/bbl)

Field Pricing (Cdn./bbl)

Field Cash Flow (million)

Corporate Funds Flow (million)

Free Cash Flow After All Capital

(million)

$45 $39.64 $8.9 $ 1.5 ($7.8)

$50 $46.00 $13.1 $ 5.7 ($3.7)

$55 $52.35 $17.2 $ 9.9 $ 0.5

$60 $58.70 $21.4 $14.0 $ 4.6

$65 $65.06 $25.5 $18.2 $ 8.8

Zargon’s cash flows are exceptionally sensitive to oil prices. Despite improved volumes and costs, a stronger Canadian

dollar and larger WTI‐WCS differentials have resulted in marginally reduced cash flow projections, when compared to prior presentations.

Excluding hedges, Zargon’s assets provide a positive corporate funds flow down to less than $45 US/bbl WTI.

At higher prices, Zargon’s assets provide significant free cash flow that can be used to retire debt, reactivation and facility modification projects, drill high‐graded horizontal oil exploitation wells and reinstate/initiate Little Bow ASP/Polymer floods.

2018 (H1) Projected Cash Flows (annualized)(excluding hedges)

0

5

10

15

20

25

30

40 45 50 55 60 65 70

Cash Flow ($

millions)

WTI Oil Price ($/bbl)

Zargon Cash FlowField Cash Flow

Corporate Cash Flow

10

WTI Pricing (US/bbl)

Field Cash Flow (million)

4.5 Times Field Cash Flow

(million)

ZargonNet Debt (million)

Attributed to Zargon Shares

(million)

Calculated Zargon Value

(per share)

$45 $8.9 $ 40.0 $ 36.7 $ 3.3 $0.11

$50 $13.1 $ 59.0 $ 36.7 $ 22.3 $0.72

$55 $17.2 $ 77.4 $ 36.7 $ 40.7 $1.32

$60 $21.4 $ 96.3 ($ 5.2) $101.5 $1.58

$65 $25.5 $114.7 ($ 5.2) $119.9 $1.86

Above valuation based on 4.5 times property multiple and, • $5.24 million of positive working capital as of Sept. 30, 2017, $41.94

million of remaining debentures and 30.75 million shares outstanding.

• for the $60 and $65 cases, $41.94 million of remaining debentures are assumed to convert into Zargon shares at a $1.25 conversion price (33.55 million shares) taking the total outstanding shares to 64.30 million.

Zargon’s long‐life oil reserves provide investors with exceptional torque (both operational and financial leverage) to future increases in oil prices.

A corporate valuation based on a 4.5 times property cash flow multiple suggests that significantly higher share prices may be realized at prices of $50 US/bbl or better.

Valuation using 2018 (H1) projected (annualized) field cash flows

0.00

0.50

1.00

1.50

2.00

40 45 50 55 60 65 70

Share Price ($/sha

re)

WTI Oil Price ($US/bbl)

Zargon Share Value4.5 Times Property Cash Flow

Key Considerations

Zargon’s Board and management believe that Zargon’s share price has not been reflective of the fundamental value inherent in the Company.

Zargon continues to seek a strategic alternatives solution that will enable Zargon stakeholders to participate in Zargon’s exceptional torque to higher oil prices.

Strategic Process

Deep Discount to NAV

11

Zargon’s H1 2018 corporate budget is forecast to deliver 2,600 boe/d of production, a four percent improvement from 2017 guidance levels. This forecast (including liability management) can be completely financed from corporate cash flows at oil prices of $68.50 Cdn./bbl (WTI) or better.

With a sustainable 2018 business plan, investors are able to wait for materially higher oil prices (and the substantial upside to Zargon share price) without erosion of the underlying asset base.

Exceptional Torque to Higher oil Prices

Sustainable 2018 Corporate Model

Investors buy Zargon at a discount to the proved developed producing net asset value when evaluated at prices at (or above) current strip.

Zargon’s long‐life oil reserves provide investors exceptional torque to higher oil prices: Financial – Although improved, Zargon’s balance sheet remains over‐levered where small changes in

underlying corporate value result in large inferred changes in share price. Operational – Zargon’s production tends to be from mature low‐decline, low‐rate wells with relatively

higher operating costs. Small improvements in oil prices result in significantly improved cash flows. Exploitation – Zargon’s larger scale exploitation opportunities are significant, but generally require

higher prices.

zargon.ca

Conventional Properties

Alberta Exploitation Core Areas

13

Bellshill Lake

TaberLittle Bownon‐ASP

Little Bow ASP

Excluding the Little Bow ASP project, the Alberta core areas are mature operated oil properties, with low decline rates and waterflood and pressure supported exploitation opportunities.

• Recent base annual oil production declines of less than 10 percent have been more than offset by oil exploitation projects (waterfloods, reactivations, and facility modifications).

• Similar projects and results are forecast for the upcoming quarters.

13

Alberta Plains (excluding Little Bow ASP)

14

• Q3 2017 production of 1,726 boe/d

– No drilling in 2015‐17 due to capital allocation decisions; less than 10% annual decline is offset by waterflood and reactivation expenditures.

– Multiple exploitation and development opportunities have been identified throughout Zargon’s asset base.

– 3D seismic coverage supported booked and un‐booked locations

– 8 booked infill and exploitation drilling McDaniel locations.

– 67% liquids‐weighted (16 – 32o API) and ~98% operated.

Q3 2017Prod

% Liquids API OOIP

Recoveryto Date

Gross UndevelopedLocations

(boe/d) (%) ( ⁰ ) (MMbbl) (%) McDaniel Additional

Bellshill Lake 437 95% 27 16 32% 5 1+

Taber 449 92% 16‐24 27 15% 3 5+Little Bow (Conventional) 304 65% 21 82 25% ‐ tbd

Alberta Other 536 21% 18‐32 n.a. n.a. ‐ 2+

Total 1,726 67% 16‐32 125+ 24% 8 8+

0

250

500

750

1,000

1,250

1,500

Jan‐16 Apr‐16 Jul‐16 Oct‐16 Jan‐17 Apr‐17 Jul‐17

Oil Prod

uctio

n (bbl/d)

Waterflood and reactivation projects stabilize production (no wells have been drilled since 2014)

Liquids(Mbbl)

Total(Mboe)

PV 10%($MM)

PDP 2,889 3,541 47.6

TP 3,124 4,032 50.2

P+PDP 3,713 4,563 59.0

P+P 4,453 5,850 70.2

McDaniel Reserves Summary (December 2016)

0

100

200

300

400

500

600

Jan‐15 Jan‐16 Jan‐17 Jan‐18 Jan‐19

Bellshill Lake History

McDaniel 2016 YE Fcst

Oil Prod

uctio

n Ra

te

Alberta Plains – Bellshill Lake

Bellshill Lake produces low‐decline rate 27 API oil with remaining infill drilling potential.• Zargon operated, high working interest.− 100% working interest in all Dina production.

• Areally extensive Dina sand with aquifer pressure support. − Addi onal ver cal wells in par ally drained localized closures can be drilled when funding is available− Q4 2017 water handling expansion will provide mul ple for mul ple low‐risk, low‐cost well pumping optimization projects in H1 2018.

Liquids(Mbbl)

Total(Mboe)

PV 10%($MM)

PDP 910 955 13.5

TP 910 972 13.5

P+PDP 1,185 1,246 17.4

P+P 1,382 1,489 20.9

McDaniel Reserves Summary (December 2016)

McDaniel has recognized 5 P+PUD locationsZargon has defined 4 additional locations

15

Proved Developed Producing Oil Rate Profile

Reported oil volumes show flattening decline trends that exceed McDaniel YE 2016 proved developed producing production forecasts.

Alberta Plains – Taber Mannville

• Sunburst development is seismically defined − 30 horizontal wells drilled since 2007 − 25 on produc on, 5 on injec on

• North pool receives pressure maintenance from two vertical flank water injectors − Es mated recovery to date ~ 16% and forecast ul mate P+PDP recovery ~ 21.7% based on estimated OOIP of 6.7 MMbbl

• South pool oil rates are stabilizing due to waterflood effects (vertical well historical production was negligible due to higher density oil) − Es mated recovery to date ~10% − Ul mate forecasted P+PDP recovery ~18% − Es mated OOIP of 15.5 MMbbl

The Taber property offers low‐decline production with remaining development potential

Liquids(Mbbl)

Total(Mboe)

PV 10%($MM)

PDP 1,068 1,089 19.4

TP 1,182 1,204 20.4

P+PDP 1,416 1,442 24.0

P+P 1,634 1,663 26.9

McDaniel Reserve Summary (December 2016)

16

Proved Developed Producing Oil Rate Profile

0

100

200

300

400

500

600

700

800

900

Jan‐15 Jan‐16 Jan‐17 Jan‐18 Jan‐19

Taber History

McDaniel 2016 YE Fcst

Oil Prod

uctio

n Ra

te (b

bl/day)

Reported oil volumes show flattening decline trends that exceed McDaniel YE 2016 proved developed producing production forecasts.

North Dakota Properties

• Long life conventional oil properties, average of 27 API gravity oil‐ Stable production, large OOIP, more than 15 MMbbl oil produced. ‐ Infrastructure and water disposal in place.‐ Infill drilling potential at each property (very low drilling density).

• Established waterflood and unitized production − Ongoing waterflood modifications and reactivations are increasing production.

• North Dakota Williston Basin geology is directly analogous to the offsetting Southeast Saskatchewan Williston Basin geology, however activity levels are substantially lower and the properties are less developed.

Q3 2017Production OOIP

Recoveryto Date Decline

Gross UndevelopedLocations

(boe/d) (MMbbl) (%) (%) McDaniel Additional

Haas 201 51 23% 3% 1 5+Mackobee Coulee 80 17 12% 12% 3 7Truro 117 30 4% 11% None 2

Total 398 98 15% 7% 4 14+17

Proved Developed Producing Oil Rate Profile

0

50

100

150

200

250

300

350

400

450

500

Jan‐15 Jan‐16 Jan‐17 Jan‐18 Jan‐19

North Dakota History

McDaniel 2016 YE Fcst

Oil Production Rate (bbl/day)

Liquids(Mbbl)

Total(Mboe)

PV 10%($MM)

PDP 1,644 1,644 17.9

TP 1,974 1,974 20.9

P+PDP 2,143 2,143 21.6

P+P 2,560 2,560 26.2

McDaniel Reserve Summary

(December 2016)

Reported oil volumes show flattening decline trends that exceed McDaniel YE 2016 proved developed producing production forecasts.

zargon.ca

Little Bow ASP (Tertiary EOR)

Little Bow ASPEOR in a mature Southern Alberta Waterflood

Zargon constructed an Alkaline Surfactant Polymer (“ASP”) facility at Little Bow, Alberta, which enables the injection of dilute chemicals in a water solution to flush out undrained oil in existing reservoirs.

At higher oil prices, the existing ASP infrastructure can be utilized for multiple ASP and Polymer only projects seeking a 10 percent incremental oil recovery on over 80 million barrels of working interest oil‐in‐place.

19

Zargon W.I.(%)

W.I. OIIP(mmbbl)

ASP Phase 1 (‘I’ Pool)North and Central 100 15

Southern Area 100 8Future Potential Phases

Remaining portions I&P Pools 97 16U&W Unit (D8D/H9H Pools) 97 26

G Unit (B8B Pool) 95 10MM Unit (E8E Pool) 100 5

C8C / X8X Pool 100 9Total 89

ASP Facility & Gas Plant

Zargon Battery site

ASP Central Facility

Future ASP Phase

Future PolymerProject

ASP Phase 1

ASP Phase 1 ConformanceRemediation & Extension

ASP Modified Phase 2 Area

Liquids(Mbbl)

Total(Mboe)

PV 10%($MM)

PDP 1,750 1,891 18.8

TP 2,054 2,209 21.2

P+PDP 2,504 2,685 30.7

P+P 4,167 4,496 35.9

McDaniel Reserve Summary (December 2016)

0

100

200

300

400

500

600

Jan‐15 Jan‐16 Jan‐17 Jan‐18 Jan‐19

Little Bow ASP History

McDaniel 2016 YE Fcst

Oil Prod

uctio

n Ra

te (b

bl/day)

Little Bow ASP Project

20

Zargon’s Little Bow ASP project has shown good oil banking, but the combination of low oil prices and Zargon’s weakened financial condition forced Zargon to “idle” the project in a manner that preserved future recoveries when reactivated.

• Phase 1 Alkali and Surfactant (“AS”) injections were suspended in Q1 2016, to reduce capital outflows during a very low oil price period. In September 2016, high water cut Phase 1 producers in AS under‐treated areas South (Phase 1) were suspended, thereby bypassing the untreated reservoir and permitting full AS recoveries upon reactivation.

• With higher oil prices, AS injections can initially be resumed in high‐graded Phase 1 areas followed by a refined Phase 2 area and then ultimately the U&W Unit.

Production plot shows Fall 2016 rate reduction to preserve long term re‐start optionality and also shows recent positive oil banking in the Central area.

Forecast Q4 2016 Op. cost of $1.0 million

Upper Mannville P Pool

North Extension

North

CentralN.E. Spur

South (Phase 1)

South (Phase 2)

Proved Developed Producing Oil Rate Profile

Reported oil volumes show improving rates that exceed McDaniel YE 2016 proved developed producing reserve forecasts.

ASP Enhanced Oil Recovery Process

Dilute concentrations of chemicals (Alkali, Surfactant and Polymer) in water are injected into an existing oil pool to “scrub” out oil that waterflooding alone will not recover.

Surfactants: Detergent; mobilizes trapped oil.

Alkali: Increases surfactant effectiveness.

Polymer (Thickener): Thickened water helps sweep oil from the reservoir.

21

1) ASP InjectionA blend of Alkali,

Surfactant & Polymer mobilizes trapped oil

2) Polymer “Push”Polymer displaces

mobilized oil to producing wells

3) Terminal WaterfloodReturn to waterflood to

complete oil displacement

OIL BANK ASP POLYMER WATER

Husky/CNRL Taber Mannville “B” ASP Husky/Whitecap Gull Lake ASP

Analog ASP Performance (The Prize)

The Taber Mannville B and Gull Lake ASP projects are good analogs to our Little Bow ASP project. Successful ASP projects provide stable production volumes for many years after the first three years

of cost intensive AS injections are completed. With higher oil prices, and the reactivation of AS injections in phase 1 and subsequent phases, we

continue to foresee the potential for many years of production growth followed by many years of free cash generating stable production for our Little Bow property.

22

zargon.ca

Additional Information

Zargon Statistical OverviewCapitalization(1)

Share Price (Nov. 10, 2017) $0.455 Basic Shares Outstanding 30.75 Market Capitalization $14.0 Net Debt(2) $36.7Option Proceeds ‐

Entity Value $50.7

52‐Week High $0.88 52‐Week Low $0.405

Net Debt Summary(2)

Bank Debt $nil Convertible Debs ( Dec. 2019) $41.9 Working Capital ($5.2) Net Debt $36.7

Other Company Details

Employees 15 Office 5 Field

Head Office Calgary, Alberta, Canada Primary Exchange Listing TSE Reserve Evaluators McDaniel

24

(1) All numbers in $millions except per share values

(2) Net debt calculated as convertible debentures plus net working capital as at September 30, 2017

Four Qtr. Comparisons Q4 2016 Q1 2017 Q2 2017 Q3 2017 Total/Avg. Change Q3‐17 over Q4‐16

Oil Prod. (bbl/d) 1,952 2,016 1,921 2,037 1,984 +85 +4.3%

Gas Prod. (mmcf/d) 2.98 3.38 3.47 3.55 3.35 +0.57 +19.1%

Equiv. Prod. (boe/d) 2,449 2,579 2,500 2,628 2,539 +179 +7.3%

Revenue & Hedges ($ million) 9.24 9.72 9.37 9.51 37.84 +0.29 +2.9%

Royalties ($ million) 1.02 1.00 1.11 1.13 4.26 +0.11 +10.7%

Op. Costs ($ million) 4.87 5.11 5.12 4.88 19.98 +0.01 +0.2%

Property Cash Flow ($ million) 3.35 3.61 3.14 3.50 13.60 +0.15 +4.4%

G&A Costs ($million) 1.33 1.16 1.11 0.89 4.49 ‐0.44 ‐33.1%

Interest & Other ($ million) 1.16 0.95 0.89 0.85 3.85 ‐0.31 ‐26.7%

Corp. Funds Flow ($ million) 0.86 1.50 1.14 1.76 5.26 +0.90 +104.6%

Capital ($ million) 1.43 2.51 2.13 1.77 7.84 +0.34 +23.8%

Abd. & Reclaim ($million) 0.05 0.14 0.55 0.55 1.29 +0.50 +1000%

In Q3 2016, Zargon sold significant assets in order to eliminate bank debt. Since then, production and financial results have steadily improved:

Production volumes have increased 7.3% (after replacing base declines), by virtue of a $7.84 million (four quarters) oil exploitation capital program.

Revenue has increased by 2.9%, operating costs were stable, G&A has declined substantially.

Consequently, corporate funds flow has increased by 105%.

Zargon Production and Financial Statistics (since Q3 2016 property sales)

McDaniel Reserves YE 2016 Review (based on McDaniel Dec. 31, 2016 Pricing)

NAV Calculation (Dec 31, 2016 Reserves)Proved + Prob. McDaniel Est. (BT DCF 10%) $ 132 million

Undeveloped Land (Seaton Jordan evaluation) $ 2 millionDeduct Net Working Capital & Conv. Deb. (unaudited) ‐ $ 34 millionNet Asset Value $ 100 million

Zargon Proved + Prob. Net Asset Value $3.27 per share

Reserve Category McDaniel PVBT 10% ($ million)

Net Asset Value ($ million)

Net Asset Value –no deb. conversion

($/share)

Net Asset Value –with deb. conversion

($/share)

PDP 84 52 1.70 1.48

Total Proved 93 61 1.99 1.62

P+PDP 111 79 2.58 1.90Proved & Prob. 132 100 3.27 2.23

(30.61 million shares at Dec 31, 2016)

25

Property GroupPDP

RLI (yrs)PDP

DeclineP+PDPRLI (yrs)

P+PDPDecline

Alberta (excl ASP) 6.7 12 % 8.7 10 %

Little Bow ASP 11.0 n/a 15.7 n/a

W.B. (ND) 12.9 9 % 16.8 7 %

Zargon 8.8 8 % 11.7 5 %

McDaniel Oil Reserves & Production CharacteristicsRLI (yrs) & 2017 Decline Rate (%/yr)

zargon.ca

Corporate PresentationNovember 13, 2017