Embed Size (px)

Citation preview

IR – January 2017

Yara International ASA SEB Nordic Seminar

Petter Østbø, EVP Production

11 January 2017

IR – January 2017

14.1% 14.4%

14.1%

16.1%

22.8%

8.5%

17.4%

20.9%

17.3%

12.6% 13.3% 14.0%

10.7%

0

20

40

60

80

100

120

140

160

0

0

0

0

0

0

2004 '06 '08 '10 '12 '14 L4Q

Yara avg. gross investment, 12M rolling

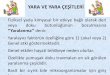

Strong growth and profitability track record

1) Share price appreciation (end December) plus dividend payments

2

Cash return on gross investments

above the Yara CROGI target of 10% Average annual shareholder return of 23%1

10% target

0

50

100

150

200

250

300

350

400

NOK/share

L4Q 15 14 13 12 11 10 09 08 07 06 05 IPO

2004

Book equity

Accumulated cash dividend payments Average annual share price

Share price end December

IR – January 2017

Safe operations is our first priority

3

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

1) TRI: Total recordable injuries, lost time (absence from work), restricted work and medical treatment cases per one million work hours

2) OFD and Galvani included in statistics from January 2016

IR – January 2017

Market

IR – January 2017

2,000

2,100

2,200

2,300

2,400

2,500

2,600

07 08 09 10 11 12 13 14 15 16E 17F

Million tons

Steady growth in grain consumption

5

Source: USDA December 2016

Steady growth in grain consumption, and pick-up in food prices

Source: FAO, November 2016

100

120

140

160

180

200

220

Jan-14 Jun-14 Nov-14 Apr-15 Sep-15 Feb-16 Jul-16

Index

FAO food price index increase L12M

IR – January 2017

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

Lower urea prices and higher input cost have reduced Chinese

urea production and exports…

6

Urea price Black Sea

USD/t

Source: BOABC, CFMW

0

100

200

300

400

500

600

Kilotons

0

200

400

600

800

1,000

1,200

1,400

1,600

Chinese urea exports

IR – January 2017

…but on-going capacity additions elsewhere are in excess of trend

consumption growth

7

2.8

3.5

2.1

2013 2019

4.1

2018

4.5

2017

7.4

2016

6.9

2014 2015

2.0

2020

~3 Mt = 10 year historical trend

consumption growth

Gross projected capacity additions, excl. China

(mill. tonnes urea1)

Source: CRU, gross capacities, September 2016 1) Assuming 50% operating rate in new plants’ first year of production

Indonesia 0.7

Egypt 0.6

Malaysia 0.6

Saudi Arabia 0.5

Bangladesh 0.2

USA 1.7

Algeria 1.2

Nigeria 0.7

Iran 0.5

Russia 0.3

India 0.7

Malaysia 0.6

Indonesia 0.5

Mexico 0.5

Bolivia 0.3

Bangladesh 0.3

Canada 0.1

USA 2.5

Nigeria 0.7

Iran 0.5

Russia 0.3

USA 0.9

India 0.7

Brazil 0.6

Turkmenistan 0.6

Mexico 0.5

Azerbaijan 0.4

Indonesia 0.3

Bolivia 0.3

Canada 0.1

Iran 0.5

Russia 0.3

India 0.7

Brazil 0.6

Turkmenistan 0.6

Azerbaijan 0.4

Indonesia 0.3

Russia 0.4

Nigeria 1.3

Algeria 1.2

Russia 0.1

Nigeria 1.3

India 0.6

IR – January 2017

Yara

IR – January 2017

Integrated business model creates value through scale, flexibility

and value chain presence

9

IR – January 2017

Differentiated product portfolio represents a key source of

competitive edge

21%

36%

24%

19% Standard products

(Urea, UAN,

Ammonia)

Differentiated products

(CAN, AN)

Specialty

(CN, Compound NPK,

Fertigation)

NPK blends

Fertilizer product portfolio (2015/16 season volume)

10

IR – January 2017

10.4

6.9

3.5

7.2

15.0

7.6

9.2

6.45.9

4.6

13.6

8.48.0

6.66.36.86.4

7.8

3.63.74.5

5.3

1.9

6.8

K&S Mosaic Agrium CF PCS Yara

2015 2014 2013 L4Q

11

Yara return on assets more stable and resilient than commodity-

oriented players

Source: Thomson One

IR – January 2017

Yara has invested for the long term in Brazil; Bunge acquisition

brought critical mass in distribution

12

0

1

2

3

4

5

6

7

8

9

10

19 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

Acquisition

Acquisition

Divestment

Acquisition

Acquisition 60%

99

Volume

(MM tons)

IR – January 2017

Yara Brazil today: unrivalled market presence and farmer-centric

strategy

> 20,000 growers using Yara solutions

> 200 Yara agronomists and 600 sales

representatives

> 55% of Yara deliveries are direct to farmer

> 55,000 interactions with growers p.a.

Unrivalled presence: 28 sites in 11 states Farmer-centric strategy drives growth

Galvani (fertilizer

production, mining

and port operation)

Yara (offices,

production, blending

and distribution of

fertilizers, port

operation)

13

IR – January 2017

Crop Value Index – a key guide to our approach What is CVI:

Crop revenue

Fertilizer costs

Low value - High volume

Limited price premiums for quality

Nutrient use efficiency is key

+1200 USD/ha = 50% yield increase

CV

I

Global area grown (ha)

High value, Low volume

Double price premium for high quality

2% yield increase= +1200 USD/ha

Optimal cost position for lower value segments

Low level of differentiation

Build positions for crop with both value and scale

Yield, quality and productivity

Take the position in cash crop – but not enough scale

Key parameters: Quality and yield

14

IR – January 2017

Brazil: focus on premium products and solutions drives growth

15

Source: ANDA, Yara

1,518

2007 2008 2009 2010 2011 2012 2013 2014 2015 L4Q

+43%

Yara Brazil premium product deliveries (kt)

IR – January 2017

Outlook and strategy

IR – January 2017

Sustaining profitable growth and competitive edge within three

focus areas

17

Organic growth and

market development

Operational improvement

Profitable step growth

1

2

3

Shape the markets where we are

present, and grow our positions

Improve productivity and returns

through company-wide program

Drive growth through M&A, as

well as capacity expansions and

new builds

Implications of market outlook Strategic response

• Increased relative strength of integrated

business model

• Reduced trade liquidity; market positions

are key

• Timing of investments is critical

• Pressure on commodity crop margins

• Significant fertilizer market growth

opportunities in emerging markets

IR – January 2017 18

OFD

CN/NPK expansion Porsgrunn

NPK expansion Uusikapuunki

Expand premium products sales and

supply

Bunge (Crop Nutrition)

Freeport ammonia JV (newbuild)

Pilbara (acquisition of remaining 49% stake)

New ammonia vessels

Expand commodity scale based on

attractive full-cost growth opportunities

Act on attractive opportunities to grow

industrial sales and supply

Galvani

Dallol1 Structurally secure P and K supply

OFD

Pilbara – TAN (newbuild)

Köping – TAN

Small-scale TAN

LeHavre

Environmental solution bolt-on

Greenbelt Fertilizers

West Sacramento import

terminal

1) Not yet committed

Strategic growth with financial discipline:

brownfield expansions, acquisitions and occasional divestments

Divestments Fosfertil

CO2 business

GrowHow UK

Pilbara TAN

IR – January 2017

Yara growth project pipeline adds ~5 NOK earnings per share by

2020 at current market prices

19

CN/NPK expansion Porsgrunn (2H 2017)

NPK expansion Uusikaupunki (2H 2016)

Urea 8 Sluiskil (2H 2017)

Rio Grande expansion (2H 2020)

Expand premium products

sales and supply

Freeport ammonia JV (4Q 2017)

New ammonia vessels (2016)

Babrala urea asset (2H 2017)

Expand commodity scale

based on attractive full-

cost growth opportunities

Act on attractive

opportunities to grow

industrial sales and supply

Galvani, Salitre (mining: 2H17, chemical 1H18) Structurally secure P and K

supply

Pilbara – TAN (4Q 2016)

Köping – TAN (1H 2018)

Profitable growth through expansions and M&A Incremental earnings at current prices1 (NOK/share)

0.5

1.8

4.0

5.3

2017 2018 2019 2020

Impact2 of +100 USD/t price change (NOK/share)

0.8

1.2 1.5

Urea Ammonia DAP

1 Urea fob Yuzhny 190 USD/t, Ammonia fob Yuzhny 170 USD/t, DAP fob Morocco 345 USD/t 2 At full capacity (2019 for urea and ammonia, 2020 for DAP) 3 Phosphate-driven price change, equivalent to 138 USD/t phosphate rock (72 bpl)

3

IR – January 2017

Yara Improvement Program: significant progress during second

half towards full program launch first quarter 2017

2Q 2016 presentation • All units working to establish and detail

improvement initiatives

• Several large-impact initiatives have started

execution, with positive results so far

• Work so far gives confidence Yara will deliver at

least USD 500 million EBITDA improvement by

2020

• Baseline for measurement will be 2015

• Full target, description and timeline to be launched

in connection with 4Q results

20

IR – January 2017

Plant productivity improvement and portfolio optimization

will make our upstream position more robust

• Implement global best practices

• Improve maintenance execution

• Reduce energy consumption

• Enhance product quality

• Further strengthen safety

culture

• Improve capex efficiency

• Optimize asset footprint

Intensive rollout with up to three parallel groups of

implementations for the next 2.5 years, starting with

Sluiskil

Systemic assessment across Yara Production

organization identified a number of improvement areas

across all sites

21

IR – January 2017

Acquisition of Tata Chemicals’ fertilizer business in India provides

footprint to accelerate premium product growth

22

Integrated world scale urea plant in Babrala, Uttar Pradesh

• ~0.7 million tons ammonia production

• ~1.2 million tons urea production

• Commissioned in 1994

World-class operations and energy efficiency

• Workforce is committed to high HESQ standards; solid safety track

record

• Energy consumption below 21 mmbtu/t, on par with Sluiskil

Significant distribution footprint

• Warehouses: 4 own and approx. 100 third-party operated

• Salesforce: 50 own, and approx. 600 on contract

Acquisition provides footprint to accelerate premium product growth

• Yara India 17% p.a. growth in premium product sales since 2010

• Yara Brazil premium products growth provides reference case

IR – January 2017

Strong rationale for creating value through further growth

23

We are positioned to grow

Strong balance sheet

Global presence

We can grow profitably

Strong track record of profitable growth

through synergies, timing and capital

discipline

We should grow

More opportunities available

Sustain and grow competitive edge

Expand premium product sales and supply

Expand commodity scale based on attractive

full-cost growth opportunities

Act on attractive opportunities to grow

industrial sales and supply

Structurally secure P and K supply

IR – January 2017

IR – January 2017

Earnings before interest, tax, depreciation and amortization

(EBITDA)

25

4,184

4,039 3,318

1,858

3,591

4,227

3,964

4,625 4,794 5,179

7,884

3,504

5,055

5,489

3,004 4,149

4,103

3,223 2,363

3,830 4,185

4,002 4,528

5,742

5,055

4,614

3,508

5,050

3,958

2,968

2013 2015 2014 2016

NOK millions

EBITDA excluding special

items

NOK

millions 13,399 16,407 21,361 13,548

Annual

IR – January 2017

Decline in nitrogen fertilizer prices since 2014, but improvement in

4Q 2016

26

0

100

200

300

400

500

600

700

4Q13 2Q14 4Q14 2Q15 4Q15 2Q16 4Q16

USD/t

Nitrogen upgrading margins1 (monthly publication prices)

CAN (46% N) NH3 CFR (46% N) Urea Egypt CFR proxy

Yara EU gas cost *20

Nitrate

premium

above urea

Value above

ammonia

Value

above gas

0

10

20

30

40

50

60

70

80

90

100

4Q13 2Q14 4Q14 2Q15 4Q15 2Q16 4Q16

European nitrate premium2 (quarterly Yara realized) USD/t

2) Yara European realized nitrate prices (excl. sulphur grades)

compared with urea publication prices (Egypt CFR proxy) with

1 month time lag. All numbers in USD per tonne of CAN equivalents. 1) All prices in urea equivalents

IR – January 2017

Weighted average global

premium above blend cost

0

100

200

300

400

500

600

700

3Q13 1Q14 3Q14 1Q15 3Q15 1Q16 3Q16

USD/t NPK premium over blend1

Value above

raw material

0

100

200

300

400

500

600

3Q13 1Q14 3Q14 1Q15 3Q15 1Q16 3Q16

USD/t Phosphate upgrading margins

DAP, fob USG

Lower commodity phosphate margins, stable compound NPK

premiums

27

1) Export NPK plants, average grade 19-10-13, net of

transport and handling cost.

Rock, fob North Africa *1.4

NH3, fob Black Sea *0.22

DAP, CIF inland Germany

MOP, CIF inland Germany

Urea, CIF inland Germany

Nitrate premium, CIF inland Germany

IR – January 2017

19.5

2.8

16.7

14.8

2.4

17.2

0

5

10

15

20

25

Pro

duction

Exp

ort

Do

mestic

Do

mestic

Exp

ort

Pro

duction

Million tons

5.0

5.2

5.4

5.6

5.8

6.0

6.2

6.4

6.6

6.8

7.0

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun

Million tons

Source: CFMW

16/17

Domestic Chinese supply by reduced by 11% so far in the 2016/17

season

Chinese urea production Domestic urea balance

Jul-Sep 15/16 Jul-Sep 16/17

-11% 14/15

15/16

IR – January 2017

Strategic growth with financial discipline: Profitable growth through brownfield expansion and M&A, while maintaining credit rating

OFD (Latin America)

CN/NPK expansion Porsgrunn (Europe)

NPK expansion Uusikapuunki (Europe)

Greenbelt Fertilizers (Africa)

West Sacramento import terminal (USA)

Expand premium products

sales and supply

Bunge (Crop Nutrition) (Brazil)

Freeport ammonia JV (newbuild in USA)

Pilbara (acq. of remaining 49% stake)(Australia)

New ammonia vessels

Expand commodity scale

based on attractive full-

cost growth opportunities

Act on attractive

opportunities to grow

industrial sales and supply

Galvani (Brazil)

Dallol1 (Africa) Structurally secure P and K

supply

OFD (Latin America)

Pilbara – TAN (newbuild in Australia)

Köping – TAN (Europe)

Small-scale TAN

Le Havre (Europe)

Environmental solution bolt-on (Europe)

1 Not yet committed

Net debt / EBITDA evolution

0.96

0.35

0.07 0.29

0.72 0.63

0.0

0.5

1.0

1.5

2.0

2.5

2010 2011 2012 2013 2014 2015

Net debt/EBITDABBB

rating

≤~ 2x

GrowHow UK (50% stake)

European CO2 business Divest non-core

businesses

Dividend and share buy-backs, share of net income

2015

57%

51%

6%

2014

53%

47%

6%

2013

64%

48%

16%

2012

47%

35%

12%

2011

23%

17%

6%

2010

19%

18%

1%

2009

41%

34%

6%

2008

21%

16%

5%

2007

26%

19%

7%

2006

48%

18%

30%

2005

48%

23%

25%

2004

32%

25%

7%

Dividends Share buy-backs Target range 40-45%

29

IR – January 2017

Strong growth pipeline

30

1) Yara’s share of capex

1.3

2017

16.2

5.4

6.2

3.3

1.3

2016

14.2

5.5

7.0

0.4 1.4

2015

14.4

6.0

4.2

3.3

0.9

2018

9.0

5.6

2.1

Maintenance

Committed growth

M&A

Cost&capacity improvements NOK bn

Capex plan1

2) Finished fertilizer and industrial products, excl. bulk blends. Including Yara share of production in

JVs. 2015 numbers excl. Growhow UK (~300 kt)

3) Committed projects only. TAN Pilbara: 160 kt, Porsgrunn: 250kt, Glomfjord: 185kt, Uusikapunki:

250kt, Köping: 90kt, Sluiskil: net 160kt, Galvani (Salitre - 60% of ~ 1 mill.tons)

4) Excl. Growhow UK (~200 kt). Including 100% ownership in Pilbara NH3 plant

5) Rio Grande expansion ads 0.5 million tons SSP and 1 million ton blends by 2020

Production growth 2015 - end 20185

Finished fertilizer Ammonia

Mill.tons

0.8

1.2

1.7

Production

end 2018

22.7

Committed

growth3

Babrala Regularity

improvement

Production

20152

18.9

0.7

0.7

9.0

7.20.5

Production

end 2018

Babrala BASF JV Regularity

improvement

Production

20154

IR – January 2017

Earnings per share*

31

8.04

6.69 5.66

0.23

6.40

8.26

6.18 6.74

2.65

10.59

14.56

1.58

10.22

11.23

3.00

8.52

7.97

5.62

2.65

7.03 7.74 7.62

8.17

10.51 9.58

7.41

3.97

9.14

6.37

3.46

NOK 20.67 27.59 29.38 24.46

Annual 2013 2014 2015 2016

*Average number of shares for 3Q 2016: 273.2 million (3Q 2015: 275.1 million).

EPS excluding currency and

special items

IR – January 2017

Lower prices mainly impact Production segment

32

1,519 1,502

432 403

6,221

894

1,534 1,502

432 403

2,937

857

3Q15 3Q16

EBITDA

(NOK millions)

EBITDA excluding special items

Crop Nutrition Industrial Production

IR – January 2017

EBITDA development

33

3,233

2,641

857

3,004

7,884

EBITDA 3Q16 Other

241

Currency

translation

156

Energy costs Price/Margin Volume

223

EBITDA 3Q15 Special

items

NOK millions

IR – January 2017

2015 Highlights

Crop Nutrition creates resilience in earnings…

Share of fertilizer volumes by product

Offers the industry’s most comprehensive product portfolio and

has a strong position in value-adding crop solutions.

Increased market presence in Africa and North America by

signing agreements to acquire the Greenbelt Fertilizer and the

Sacramento Terminal

Continued investments in solutions for precision farming and

water scarcity. Investments in 2015 amounted to a total of NOK

1.5 bn

Key financials

Fertilizer volumes by region

(NOKm) 1H 2016 1H 2015 Change YE 2015

Revenue and other income1 37,760 41,950 (4,190) 80,189

EBITDA 3,108 3,415 (307) 6,188

Operating income 2,476 2,854 (378) 4,973

% margin 6.6% 6.8% N/A 6.1%

CROGI (12-month rolling avg.) 16.3% 17.9% N/A 17.5%

0

5,000

10,000

15,000

20,000

25,000

2013 2014 2015

Europe Latin America North America Asia AfricaKilotons

26,317 26,544 23,668

0%

20%

40%

60%

80%

100%

2013 2014 2015

NPK OTHFER UREA CN NITRA UAN

1 External revenue and other income

34

IR – January 2017

… by adding distribution and agronomic competence

Time

Mark

et depth

Sell what we produce

• Place new capacity

• Manage seasonality

Build product

reputation

• High quality products

• Viking ship brand

Farmer centric solutions and

tools

• Our next strategic step to

build Yara’s knowledge

margin

Asset

Product

Crop

Farmer

Build crop

solutions

• Crop knowledge

• Product portfolio

• Application competence

Evolved focus and aspiration

35

IR – January 2017

2015 Highlights

Industrial segment reduces cyclicality and seasonality…

Significantly expansion of terminal and logistics network in North

America and Brazil to better and more efficiently serve the

automotive Nox abatement markets with respectively DEF (Diesel

Exhaust Fluid) and Arla 32 reagent

Increased deliveries of air pollution abatement products by 20% and

achieved strong growth parameters for Nutriox business (waste

water treatment) and increasing demand for related services and

monitoring technologies

Agreement to sell European CO2 business

Key financials

(NOKm) 1H 2016 1H 2015 Change YE 2015

Revenue and other income1 9,085 8,520 565 17,233

EBITDA 2,116 749 1,367 1,489

Operating income 2,030 602 1,428 1,174

% margin 22.3% 7.1% N/A 6.8%

CROGI (12-month rolling avg.) 43.6% 18.8% N/A 22.0%

1 External revenue and other income 2 Including Yara share of production in equity-accounted investees 3 Including share of JVs

Industrial sales by product2

Kilotons

6,255 6,593 7,030

0

1,500

3,000

4,500

6,000

2013 2014 2015

Environmental products Base ChemicalsMining Applications Animal NutritionCO2 and feed phosphates

36

IR – January 2017

…by securing stable off-take from production plants and the

unseasonal nature of its businesses

Chemical applications for

food, feed, automotive, space,

pharmaceutical and

construction industries

Abatement of emissions from

heavy duty vehicles

NOx and SOx abatement for

maritime sector

Solutions to the Civil explosives

industry

Based on Technical nitrates for

mining and construction

CO2 as gas, liquid and Dry ice

CN for Industrial Applications

Animal nutrition

Key product and

service offering

EBITDA 2013- 20151

(NOKm)

Market drivers GDP growth Legislation, GDP growth GDP growth, infrastructure

projects, supply security GDP growth, standard of living

Strategic fit Optimization of Upstream

assets

Utilize technology, logistic

advantage and infrastructure

footprint

Handling, storage and

economies of scale Monetize secondary products into

primary markets applications

Geographical market Europe Global Global Global

Four business lines with focused strategy and operations

Base Chemicals Environmental Solutions Mining Applications Gas and Industrial

applications

2015

515

2014

533

2013

426 303

2014 2013

237 447

2015 2014 2015

147 223

2013

225

2015

513

2014

492

2013

337

1 EBITDA not adjusted for eliminations between Business Units

37

IR – January 2017

2015 Highlights

Production segment has plants and mines across the globe which

provide scale and flexibility…

In the US, Yara and BASF started construction of a world-scale

ammonia plant in Freeport. In Australia, Yara secured full ownership of

the Pilbara ammonia plant and increased ownership in the Pilbara TAN

plant. Construction started on the project to increase the capacity of

value-added production in Sluiskil, the Netherlands. Yara sold its 50%

stake in GrowHow UK.

Total production ended at 26.5mm tons, ammonia production

decreased by 1% and finished fertilizer and industrial products

increased by 2%

Gas consumption by region in 20152

1 Including Yara share of production in equity-accounted investees; 2 Including share of JVs

22

Europe

159

RoW Canada

109

Million MMBtu

Key financials

Production volumes by product2

(NOKm) 1H 2016 1H 2015 Change YE 2015

Revenue and other income1 22,881 28,266 (5,385) 55,812

EBITDA 4,965 6,017 (1,052) 14,414

Operating income 2,132 4,364 (-2,232) 8,842

% margin 9.3% 15.4% N/A 15.8%

CROGI (12-month rolling avg.) 11.0% 11.4% N/A 12.1%

26,009 25,924 26,259

0

5,000

10,000

15,000

20,000

25,000

30,000

2013 2014 2015

Ammonia Urea Nitrate NPK CN UAN SSPKilotons

38

IR – January 2017

Net interest-bearing debt development

39

3,1462,836

Net debt

Sep 16

10,390

Other

32

Foreign

currency

translation loss

114

Net operating

capital change

26

Yara dividend

and share

buy-backs

210

Investments

(net)

Cash earnings* Net debt

Jun 16

9,698

* Operating income plus depreciation and amortization, minus tax paid, net gain/loss on disposals, net interest expense and bank charges

NOK millions

IR – January 2017

Value-added and distribution make up larger part of Yara’s contribution

40

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

1Q15

Trade

Upgrade & distribution

Commodity Europe

Commodity overseas

3Q10 3Q11 1Q12 3Q12 3Q16 1Q16 1Q11 3Q15 3Q14 1Q10 1Q14 3Q13 1Q13

Total Yara contribution

IR – January 2017

Production

41

0

500

1,000

1,500

2,000

2,500

Kilotons

2016 2015 2013 2014

Ammonia1

1) Including share of equity-accounted investees

0

1,000

2,000

3,000

4,000

5,000

6,000

Kilotons

Urea Nitrates NPK CN UAN SSP - based fertilizer

2015 2013 2014 2016

Finished fertilizer & industrial products1

IR – January 2017

Yara 3Q fertilizer sales by market and product

42

2,085

2,930

582 526 577 235

2,100

3,190

619 427 591 322

Europe Brazil Latin America North America Asia Africa

3Q15 3Q16

1,101

1,603 1,415 998

1,347

236 234

1,419 1,750

1,448

913 1,210

229 279

Nitrate Urea Other products UAN CNCompound NPK1 Blend NPK

1) Yara-produced compound NPK and third party sourced (Total NPK minus blend NPK)

Kilotons

IR – January 2017

Fertilizer deliveries

43

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500

6,000

6,500

7,000

Europe Outside Europe

Kilotons

2012 2009 2010 2011 2013 2014 2015 2016

IR – January 2017

Fertilizer deliveries by product and source

44

1,415 1,448

1,101

1,419

1,603 1,750

998 913

236 229

1,582 1,488

3Q15 3Q16 3Q15 3Q16 3Q15 3Q16 3Q15 3Q16 3Q15 3Q16 3Q15 3Q16

Yara-produced deliveries Joint venture & third party sourced

NPK compounds NPK blends Urea UAN Other

Kilotons

Nitrate

IR – January 2017

YaraMila (compound NPK) and YaraBela (nitrate) deliveries

45

0

200

400

600

800

1,000

1,200

1,400

1,600

3Q12 3Q13 3Q14 3Q15 3Q16

Yara-produced YaraMila deliveries

-

200

400

600

800

1,000

1,200

1,400

1,600

3Q12 3Q13 3Q14 3Q15 3Q16

Yara-produced YaraBela deliveries Kilotons

Outside Europe Europe Outside Europe Europe

Kilotons

IR – January 2017

Strong premium product deliveries

46

1) YaraBela, YaraMila and YaraLiva deliveries

0

500

1,000

1,500

2,000

2,500

3,000

3,500

3Q12 3Q13 3Q14 3Q15 3Q16

303

231

148

41

84

305

250 236

37

85

300

499

302

128

84

Asia Brazil LatinAmerica excl.

Brazil

Africa NorthAmerica

Value-added fertilizer deliveries1 Value-added fertilizer deliveries1

CAGR

8%

Outside Europe Europe

3Q16 3Q15 3Q14

IR – January 2017

Industrial volume development

47

893889847829815

892859864852849

816866

819

572571538

577541540

482511

438456432

207242

308328

385364333346

380361339367364

3Q13

374

3Q16 2Q16 1Q16 4Q15 3Q15 2Q15 1Q15 4Q14 3Q14 2Q14 1Q14

382

4Q13

Other Environmental products Industrial N-chemicals

Kilotons

IR – January 2017

AdBlue deliveries

48

0

50

100

150

200

250

300

350

400

450

500

3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16

Kilotons

IR – January 2017

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Urea Nitrates Compound NPK Other

Yara stocks

49

Kilotons

Finished fertilizer Bunge Fertilizer

included from 3Q 2013

IR – January 2017

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

3Q11 3Q12 3Q13 3Q14 3Q15 3Q16

Domestic production Imports

Normal start to the European season, slow in the US

50

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

3Q11 3Q12 3Q13 3Q14 3Q15 3Q16

Domestic production Imports

West Europe US Million tons N Million tons N

-13% +2%

Source: Yara estimate for fertilizer deliveries to selected West European countries.

Total nitrogen deliveries based on TFI, US Trade Commission, Blue-Johnson and Yara estimates

IR – January 2017

European producers’ nitrate stocks

51

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun

16/17 10/11 11/12 12/13 13/14 14/15 15/16

Source: Fertilizers Europe, Yara estimate for September

Index

June 2007 = 1

IR – January 2017

Energy cost

52

4.0 4.4

4.0

2.8

3.7

5.2 4.6

3.9 3.8

2.9 2.7 2.7 2.1 2.0 2.1

2.8 2.8 3.3

3.6

4.8

5.7

8.2 8.0 8.0 8.1

6.9

6.1 6.5

5.9 5.7 5.3 5.2

4.1 4.0 4.3

4.9 4.7

6.6

9.2 9.4

10.5 9.8

7.6 7.0

8.1

7.0 6.8 6.5

5.4

4.2 4.4 4.2 5.1 5.3

6.6

7.6

10.7 11.0 11.4 11.3

9.2

7.5

8.5

7.6 7.5 7.0

6.2

5.0 4.6 4.9

5.2 5.8

2009 2010 2011 2012 2013 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17

US gas price (Henry Hub) Yara Global TTF day ahead (Zeebrugge 2009-2012) Yara Europe

Yearly averages 2009 – 2013, quarterly averages for 2014-16 with forward prices* for 4Q16 and 1Q17.

*Dotted lines denote forward prices as of 13 October 2016 Source: Yara, World Bank, Argus/ICIS Heren

IR – January 2017

Increasing coal prices

53

CIF ARA1 December 2016 ($/mt)

1) Amsterdam, Rotterdam, Antwerp

China anthracite prices November 2016 (RMB/mt)

Source: CME Group, China Fertilizer Market Weekly

IR – January 2017

Global grain balance

54

1,950

2,000

2,050

2,100

2,150

2,200

2,250

2,300

2,350

2,400

2,450

2,500

2,550

2,600

07 08 09 10 11 12 13 14 15 16E 17F

Million tons

Consumption Production

Grain consumption and production Days of consumption in stocks

55

60

65

70

75

80

85

90

95

07 08 09 10 11 12 13 14 15 16E 17F

Days

Source: USDA October 2016

IR – January 2017

Non-commercials’ net long position in corn

55

-200

-100

0

100

200

300

400

500

Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16

Thousand contracts

Source: US Commodity Futures Trading Commission

IR – January 2017

Weak grain production economics, affecting particularly P and K

demand

56

0

50

100

150

200

250

300

1/2006 1/2007 1/2008 1/2009 1/2010 1/2011 1/2012 1/2013 1/2014 1/2015 1/2016

Index FAO price index

Cereals Price Index Cereals 5 year avg. Food Price Index Food 5 year avg.

Source: FAO

IR – January 2017

Key value drivers – quarterly averages

57

268 250 207 198 183

281 270 233

208 193

3Q15 4Q15 1Q16 2Q16 3Q16

Urea prilled fob Black Sea (USD/t)/Urea granular fob Egypt (dotted line, USD/t)

257 255 249

197 166

3Q15 4Q15 1Q16 2Q16 3Q16

CAN cif Germany (USD/t)

2.7

2.1 2.0 2.1

2.9

3Q15 4Q15 1Q16 2Q16 3Q16

US gas price Henry Hub (USD/MMBtu)

6.4

5.5

4.1 4.3 4.2

3Q15 4Q15 1Q16 2Q16 3Q16

TTF day ahead (USD/MMBtu)

8.2

8.5

8.7

8.3 8.3

3Q15 4Q15 1Q16 2Q16 3Q16

NOK/USD exchange rate

388 355

270 274

210

3Q15 4Q15 1Q16 2Q16 3Q16

Ammonia fob Black Sea (USD/t)

Source: Fertilizer Market Publications, CERA, World Bank, Norges Bank

IR – January 2017

10-year fertilizer prices – monthly averages

58

0

200

400

600

800

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

USD/t Urea prilled fob Black Sea/Urea granular fob Egypt

Average prices 2006 - 2015

0

200

400

600

800

1,000

1,200

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

USD/t DAP fob US Gulf/MOP granular fob Vancouver

0

100

200

300

400

500

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

USD/t CAN cif Germany

0

200

400

600

800

1,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

USD/t Ammonia fob Black Sea