Embed Size (px)

Citation preview

Yangzijiang Shipbuilding (Holdings) Ltd.

Roadshow Presentation25th April 2008

1

Agenda

Operation update

Our Presence & Our Shipyards

Market outlook

Q & A

Strong order book and increasing of production capacity

Sustaining profit margins

Consideration and Strategies

2

Our Presence

♦ Old shipyard is located in Jiangyin City

♦ New shipyard is located in Jiangjiang city with new facility to produce more ships

Our shipyards ♦ 2nd largest non-state-owned shipbuilder in terms of production

capability

Our Core Business ♦ Producing wide range of commercial vessels

Our Products

♦ Containerships

♦ Dry bulk carriers, and

♦ Multi-purpose cargo vessels

Our Customers

♦ Peter Dohle (Germany)

♦ Rickers Reederei (Germany)

♦ Tomas Schulte (Germany)

♦ Hansa Shipping (Germany)

♦ Carisbrooke (UK)

♦ Seaspan (Canada)

♦ Formosa (Taiwan)

♦ Canadry (Italy)

♦ D’amato (Italy)

♦ IMS Shipping (Italy)

♦ Cosco (China)

Our Presence & Our Shipyard

3

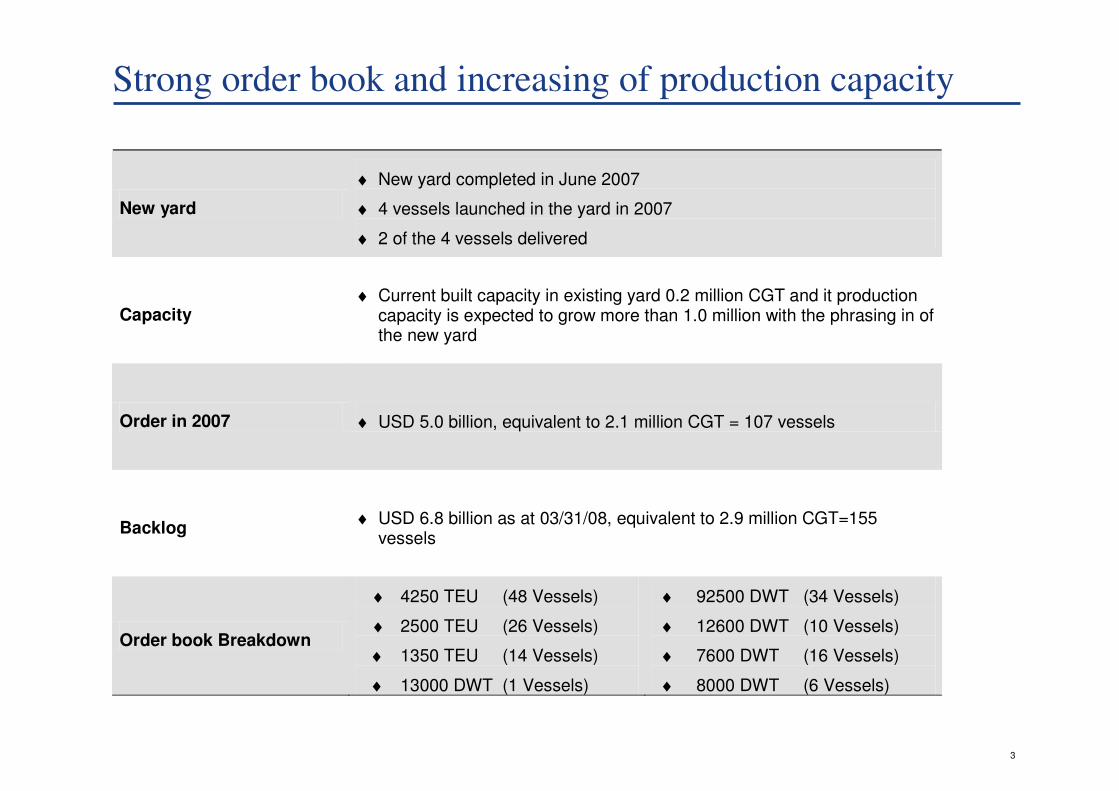

New yard

♦ New yard completed in June 2007

♦ 4 vessels launched in the yard in 2007

♦ 2 of the 4 vessels delivered

Capacity ♦ Current built capacity in existing yard 0.2 million CGT and it production

capacity is expected to grow more than 1.0 million with the phrasing in of the new yard

Order in 2007 ♦ USD 5.0 billion, equivalent to 2.1 million CGT = 107 vessels

Backlog ♦ USD 6.8 billion as at 03/31/08, equivalent to 2.9 million CGT=155

vessels

Order book Breakdown

♦ 4250 TEU (48 Vessels)

♦ 2500 TEU (26 Vessels)

♦ 1350 TEU (14 Vessels)

♦ 13000 DWT (1 Vessels)

♦ 92500 DWT (34 Vessels)

♦ 12600 DWT (10 Vessels)

♦ 7600 DWT (16 Vessels)

♦ 8000 DWT (6 Vessels)

Strong order book and increasing of production capacity

4

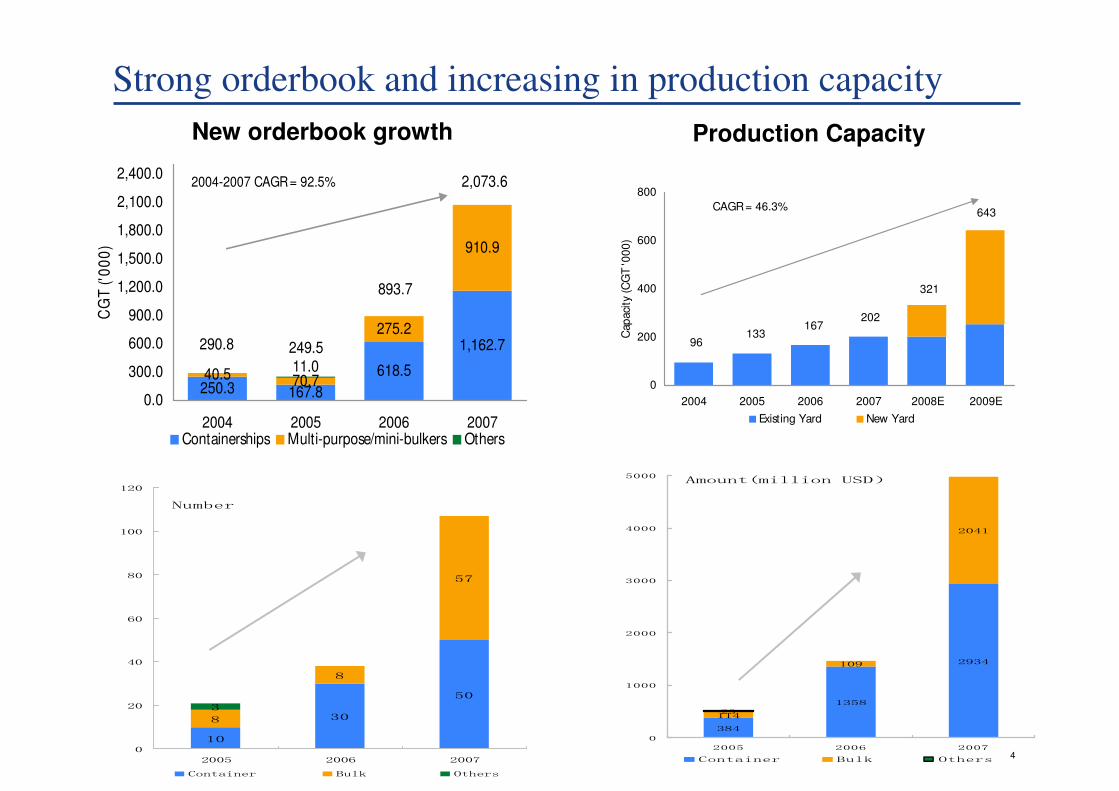

Strong orderbook and increasing in production capacity

Number

10

30

50

8

8

57

3

0

20

40

60

80

100

120

2005 2006 2007

Container Bulk Others

Amount(million USD)

384

1358

2934

114

109

2041

23

0

1000

2000

3000

4000

5000

2005 2006 2007

Container Bulk Others

250.3 167.8

618.5

1,162.7

40.5

275.2

910.9

70.711.0

0.0

300.0

600.0

900.0

1,200.0

1,500.0

1,800.0

2,100.0

2,400.0

2004 2005 2006 2007

CG

T (

'00

0)

Containerships Multi-purpose/mini-bulkers Others

2004-2007 CAGR = 92.5%

290.8 249.5

893.7

2,073.6

0

200

400

600

800

2004 2005 2006 2007 2008E 2009E

Cap

aci

ty (

CG

T '

00

0)

Existing Yard New Yard

CAGR = 46.3%

96133

167202

321

643

New orderbook growth Production Capacity

5

Strong orderbook and increasing in production capacity

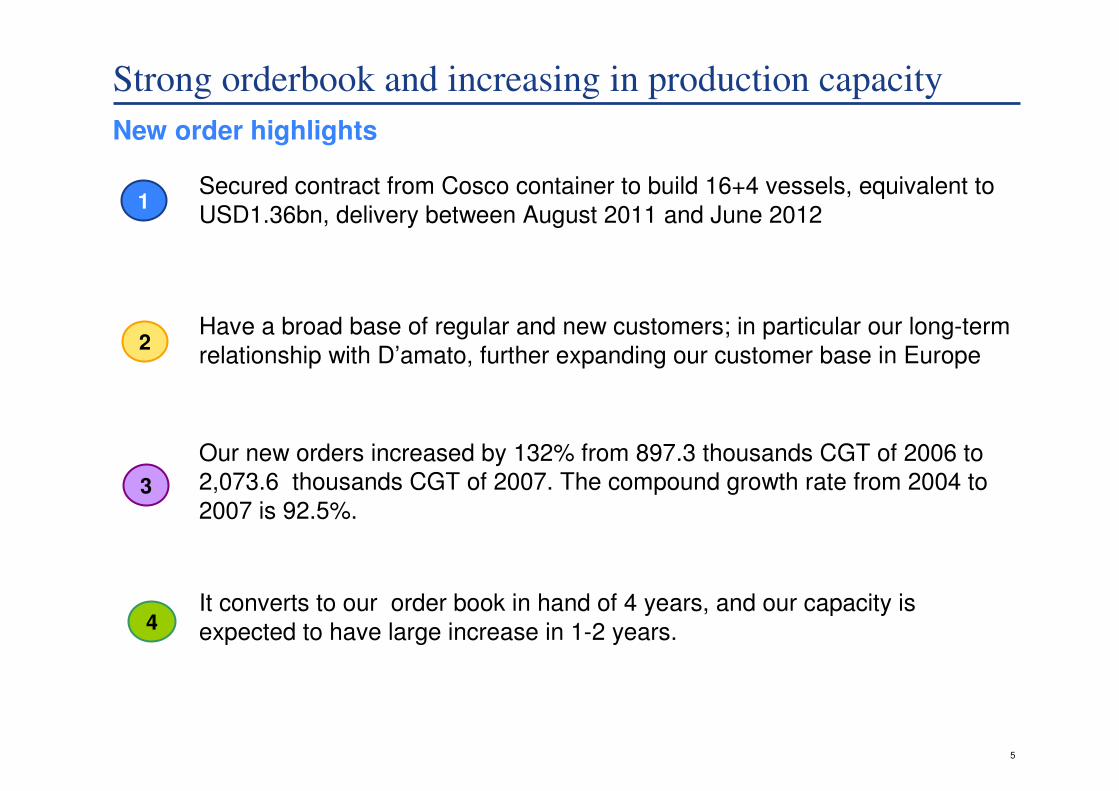

New order highlights

1

2

Secured contract from Cosco container to build 16+4 vessels, equivalent to

USD1.36bn, delivery between August 2011 and June 2012

Have a broad base of regular and new customers; in particular our long-term

relationship with D’amato, further expanding our customer base in Europe

Our new orders increased by 132% from 897.3 thousands CGT of 2006 to

2,073.6 thousands CGT of 2007. The compound growth rate from 2004 to

2007 is 92.5%.

It converts to our order book in hand of 4 years, and our capacity is

expected to have large increase in 1-2 years.

3

4

6

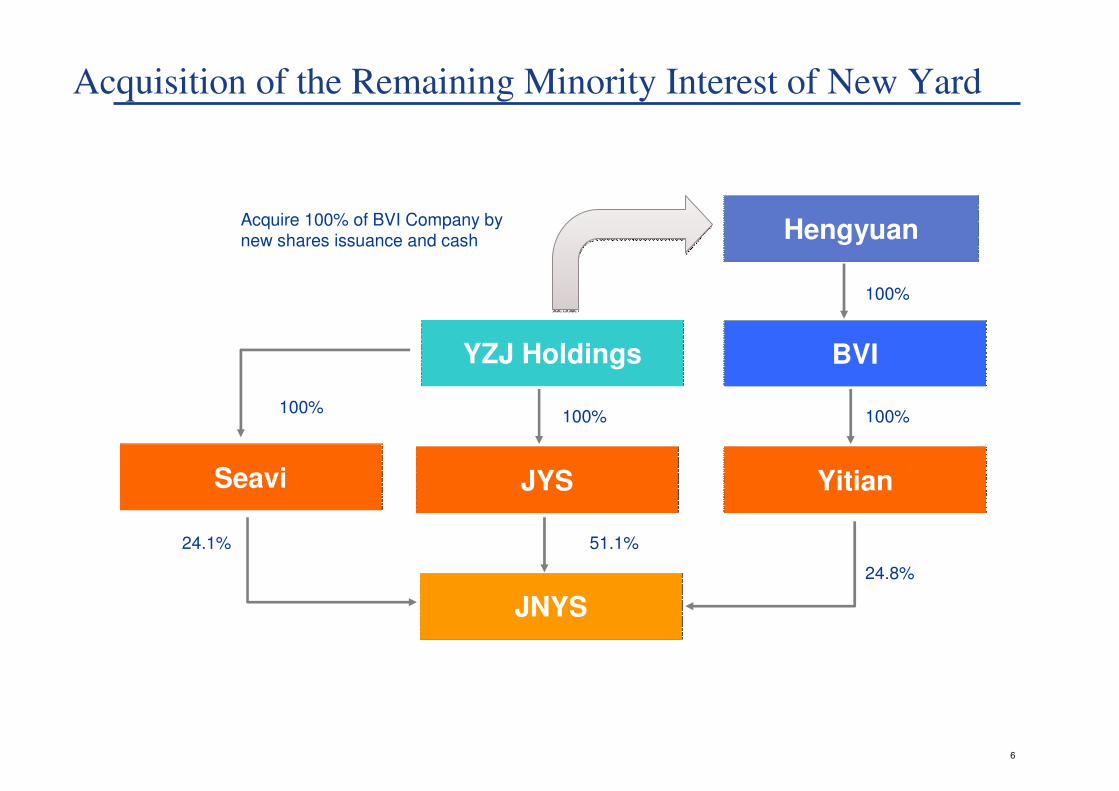

Acquisition of the Remaining Minority Interest of New Yard

Seavi

JNYS

24.8%

JYS Yitian

YZJ Holdings BVI

100%100%

51.1%24.1%

100%

Hengyuan

100%

Acquire 100% of BVI Company by new shares issuance and cash

7

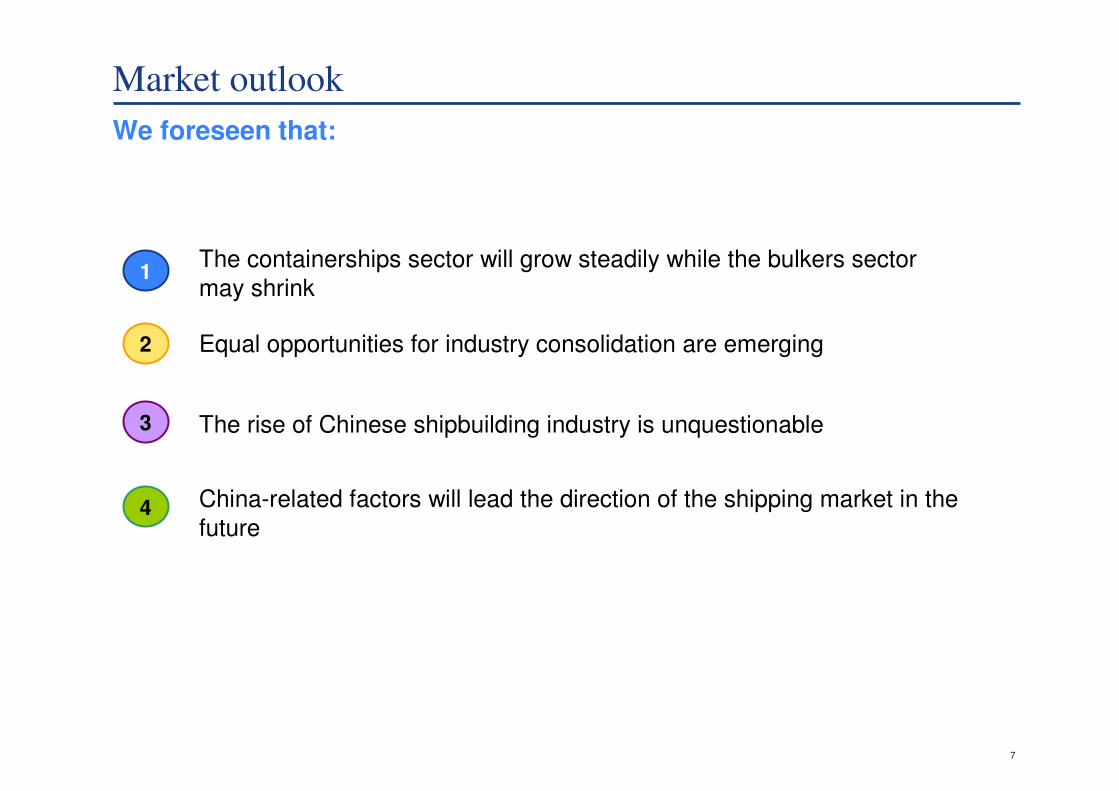

Market outlook

We foreseen that:

1

2

The containerships sector will grow steadily while the bulkers sector

may shrink

Equal opportunities for industry consolidation are emerging

The rise of Chinese shipbuilding industry is unquestionable

China-related factors will lead the direction of the shipping market in the

future

3

4

8

Rising steel prices

Steel Price is expected to increase in 2008, which in turn will increase the raw

material cost;

The enlarged production capacity by steel mills in 2005 may take away some of

the heat from the raising steel price towards the second half of 2008;

Demand for steel will decrease with tight fiscal policy implemented to cool the

economic;

Rapid increase in steel price push CPI further; we believe the Chinese

government will freezing certain prices within the economy in order to help keep

inflation under control;

9

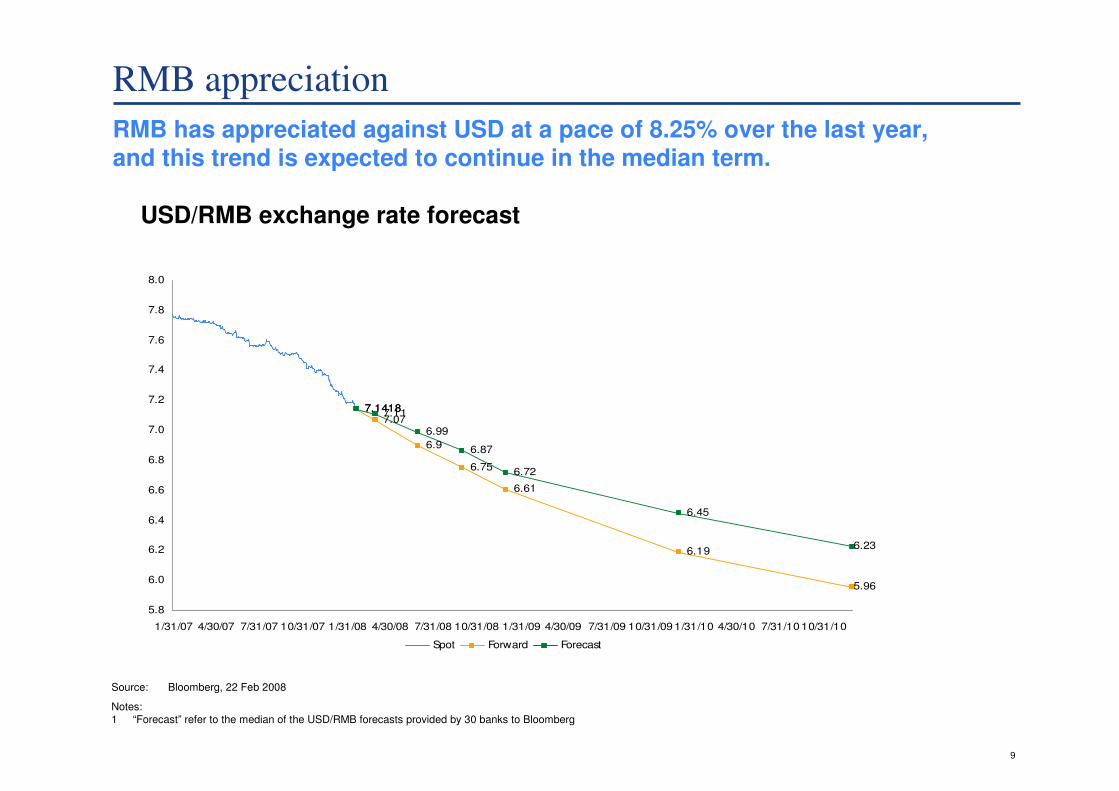

7.14187.07

6.9

6.75

6.61

6.19

5.96

7.14187.11

6.99

6.87

6.72

6.45

6.23

5.8

6.0

6.2

6.4

6.6

6.8

7.0

7.2

7.4

7.6

7.8

8.0

1/31/07 4/30/07 7/31/07 10/31/07 1/31/08 4/30/08 7/31/08 10/31/08 1/31/09 4/30/09 7/31/09 10/31/091/31/10 4/30/10 7/31/1010/31/10

Spot Forward Forecast

RMB appreciation

RMB has appreciated against USD at a pace of 8.25% over the last year, and this trend is expected to continue in the median term.

Source: Bloomberg, 22 Feb 2008

Notes:1 “Forecast” refer to the median of the USD/RMB forecasts provided by 30 banks to Bloomberg

USD/RMB exchange rate forecast

10

About the New Orders:

♦ To a certain extend the boom of shipbuilding industry in 2007 had cause a temporary over tonnage situation.

♦ On average most shipyards have more then 4 years’ of orders in hand. When only 2 years’ order conventionally, their desires to accept orders are not very strong. Any new order, will have to live with a longer then normal delivery time.

♦ In terms of uncertain judgment of cost increase/exchange rate and ship market, ship yards are not willing to accept an order easily.

♦ The decreased of new ship orders are deem to be a blessing in disguise as it can help to sustain the high price of new ships, especially for containerships. The appreciation of price in 2007 are consider to be reasonable.

♦ Our focus on containerships, good track record and our ability to build a wide range of ships will mitigate any serious impact to our profitability while allowing the market to find it own equilibrant.

♦ Our cautions and steady management strategy ensure the least possibility of contracts cancellation.

11

Industry cycle and our competitiveness

We foresee that industry cycle and the introduction of new yards will intensify the competitiveness of the industry.

1

2

Our sustainable operating policies ensure the continuity of new orders

while the industry troughs

Relevant training program for all level of staffs are in place.

Timely & efficient application of capital markets to consolidate the

industry

Rewarding systems to keep talent and to inspire creativity

3

4

12

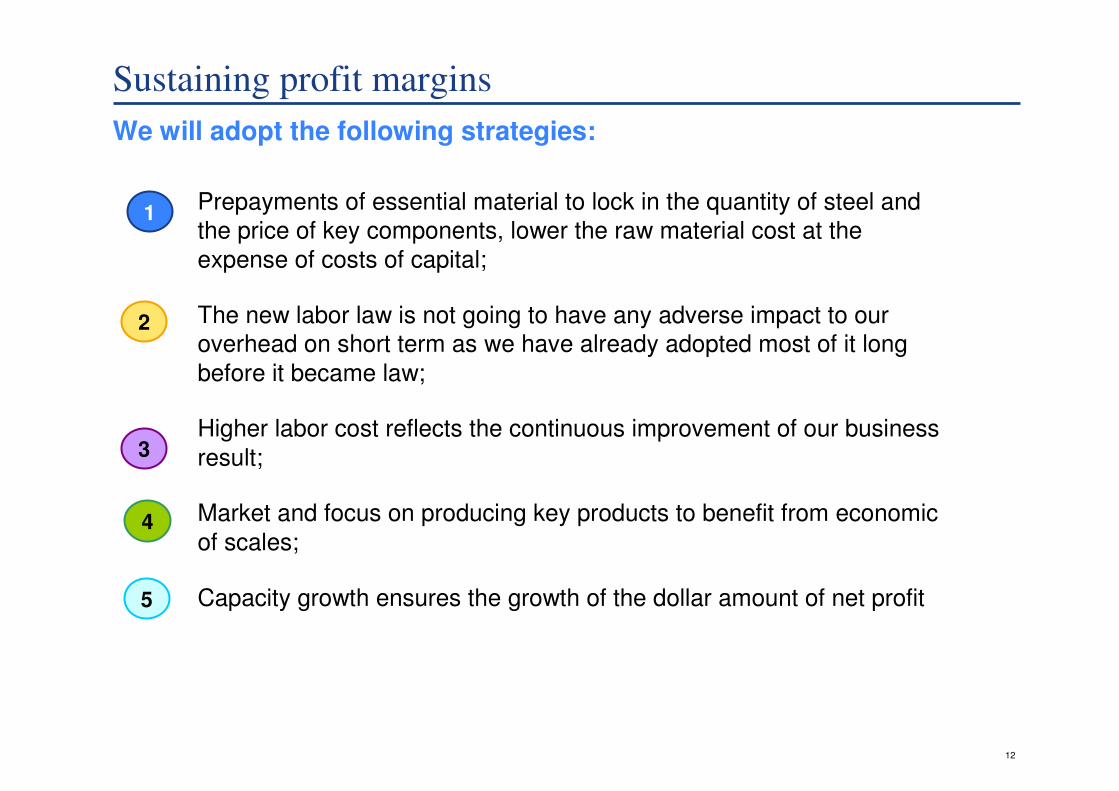

Sustaining profit margins

We will adopt the following strategies:

1

2

Prepayments of essential material to lock in the quantity of steel and

the price of key components, lower the raw material cost at the

expense of costs of capital;

The new labor law is not going to have any adverse impact to our

overhead on short term as we have already adopted most of it long

before it became law;

Higher labor cost reflects the continuous improvement of our business

result;

Market and focus on producing key products to benefit from economic

of scales;

Capacity growth ensures the growth of the dollar amount of net profit

3

4

5

Appendix

Q & A