Embed Size (px)

Citation preview

Page 1 International Trade Centre

WTO NAMA Negotiations

Challenges and opportunities for Pakistan

September 2007

WTO NAMA Negotiations

Challenges and opportunities for Pakistan

September 2007

This publication has been produced with the assistance of the European Union (EU) as part of an EU-funded Trade Related Technical Assistance (TRTA) programme with the Government of Pakistan. The International Trade Centre (ITC) is implementing the programme. The designations employed and the presentation of material in this publication do not imply the expression of any opinion whatsoever on the part of the EC, ITC, UNCTAD or WTO concerning the legal status of any country, territory, city or area or of its authorities, or concerning the limitation of its frontiers or boundaries. ITC has not formally edited this report.

Written by: Prof. Sam Laird, International trade and public policy expert, Geneva, Switzerland With initial inputs by: Ms. Huma Fakhar, Chairperson, MAP Services Group and Partner, Fakhar Law International, Lahore, Pakistan

© International Trade Centre (UNCTAD/WTO) Palais des Nations, 1211 Geneva 10, Switzerland Email: [email protected] http://www.intracen.org Publication No. BAS/TS/PAK/E/07/02/rev.1 Distribution: Unrestricted September 2007

ITC: Your Partner in Trade Development The International Trade Centre is the joint technical cooperation agency of the United Nations Conference on Trade and Development (UNCTAD) and the World Trade Organization (WTO) for business aspects of trade development. ITC’s mission is to contribute to sustainable development through technical assistance in export promotion and international business development. ITC’s strategic objectives are:

Enterprises – Strengthen the international competitiveness of enterprises.

Trade support institutions – Develop the capacity of trade service providers to support businesses.

Policymakers – Support policymakers in integrating the business sector into the global economy

Acknowledgements

This publication was originally prepared as a discussion draft for the seminar on the ‘WTO NAMA Negotiations: Challenges and opportunities for Pakistan’ held in Karachi on 3 & 4 November 2006. The seminar was organized as part of the European Union (EU) Trade-related Technical Assistance (TRTA) programme for Pakistan. The TRTA programme aims to enhance awareness among government officials, the business sector and civil society about the implications of WTO Agreements on the economy of the country, and to assist Pakistan in building the necessary capacity to address issues resulting from its participation in the WTO.

The seminar was designed to deepen the understanding of the commercial and economic implications of the WTO Non-Agricultural Market Access (NAMA) negotiations, and of the emerging multilateral trading system. Discussion was designed to bring out the new market access opportunities and threats for business through discussion with international and national experts, business leaders, academicians and trade policy analysts and negotiators.

The seminar allowed public and private sector decision-makers to anticipate changes that the Doha Development Agenda (DDA) will bring about and to position themselves within the new multilateral trading environment. The enhanced knowledge is expected to equip business leaders to play a more meaningful advocacy role with the Government, with a view to contributing to the completion of the DDA negotiations.

The report was finalised and published following the seminar, and revised and updated following the release of the modalities text by the Chair of the NAMA Negotiating Group in July 2007.

The report focuses on four of Pakistan’s major non-agricultural export sectors – namely textiles and clothing, leather goods, chemicals and electrical goods and appliances – in light of the WTO NAMA negotiations.

Abbreviations

ABI Argentina, Brazil & India [tariff cut formula] AOA Agreement on Agriculture DDA Doha Development Agenda DVD Digital video disc EPB Export Promotion Bureau EU European Union FTA Free Trade Agreement GATS General Agreement on Trade in Services GATT General Agreement on Tariffs and Trade GDP Gross Domestic Product GSP Generalised System of Tariff Preferences GSTP Global System of Trade Preferences among Developing Countries ITC International Trade Centre LDCs Least Developed Countries MFN Most-favoured-nation [status] MINFAL Ministry of Food, Agriculture & Livestock NAMA Non-Agricultural Market Access NTBs Non-tariff barriers NWFP North West Frontier Province PC Personal computer PKR Pakistan Rupees PRSP Poverty Reduction Strategy Paper R&D Research & development REGS Rapid Export Growth Strategy T&C Textiles & clothing TDAP Trade Development Authority of Pakistan TRTA Trade Related Technical Assistance TV Television UAE United Arab Emirates UK United Kingdom UNCTAD United Nations Committee on Trade and Development US United States WTO World Trade Organization

Table of contents

Executive summary .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1

I . Pakistan’s economic and polit ical situation, and prospects .. . . . . . . . . .5 Traditional low value-added industries ............................................................6

Textiles and clothing................................................................................................6 Leather goods...........................................................................................................8 Chemicals...............................................................................................................10 Electrical goods and appliances .............................................................................12

I I. Pakistan’s export and import regimes ... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13 Exports..........................................................................................................13

The renaissance of export development.................................................................13 The non-diversified export basket..........................................................................14 Strategic elements in export development .............................................................15

Imports ......................................................................................................1617 Policy support for economic development.....................................................17

Rapid Export Growth Strategy...........................................................................1718 Trade Development Authority of Pakistan ............................................................18

I II . Analysis of Pakistan’s export and imports .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19 Textiles and clothing .....................................................................................19

The importance of the EU’s GSP...........................................................................20 Will the EU’s regional cumulation for SAARC countries help Pakistan’s exports? ..................................................................................................................26

Leather and leather goods ............................................................................26 Chemicals .....................................................................................................27 Electrical goods and appliances....................................................................28 Other sectors of note.....................................................................................28

IV. NAMA negotiations – substantive issues and process ... . . . . . . . . . . . . 29 The state of play of the negotiations – Doha to Hong Kong ...........................29

The Doha mandate .................................................................................................29 Background to the negotiations..............................................................................30 Hong Kong Declaration .........................................................................................32

Formulae for tariff reduction ..........................................................................34 Tariff rationalization of industrial goods in South Asia ...................................38

Bangladesh .............................................................................................................39 India .......................................................................................................................39 Nepal ......................................................................................................................39

Sri Lanka................................................................................................................ 39 Pakistan.................................................................................................................. 40

V. Pakistan’s preferential trade pockets .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41 Agreement on South Asian Free Trade Area................................................ 41 FTA with Sri Lanka ....................................................................................... 42 FTA with China............................................................................................. 42

Early Harvest Programme...................................................................................... 43

VI. Conclusions and recommendations .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

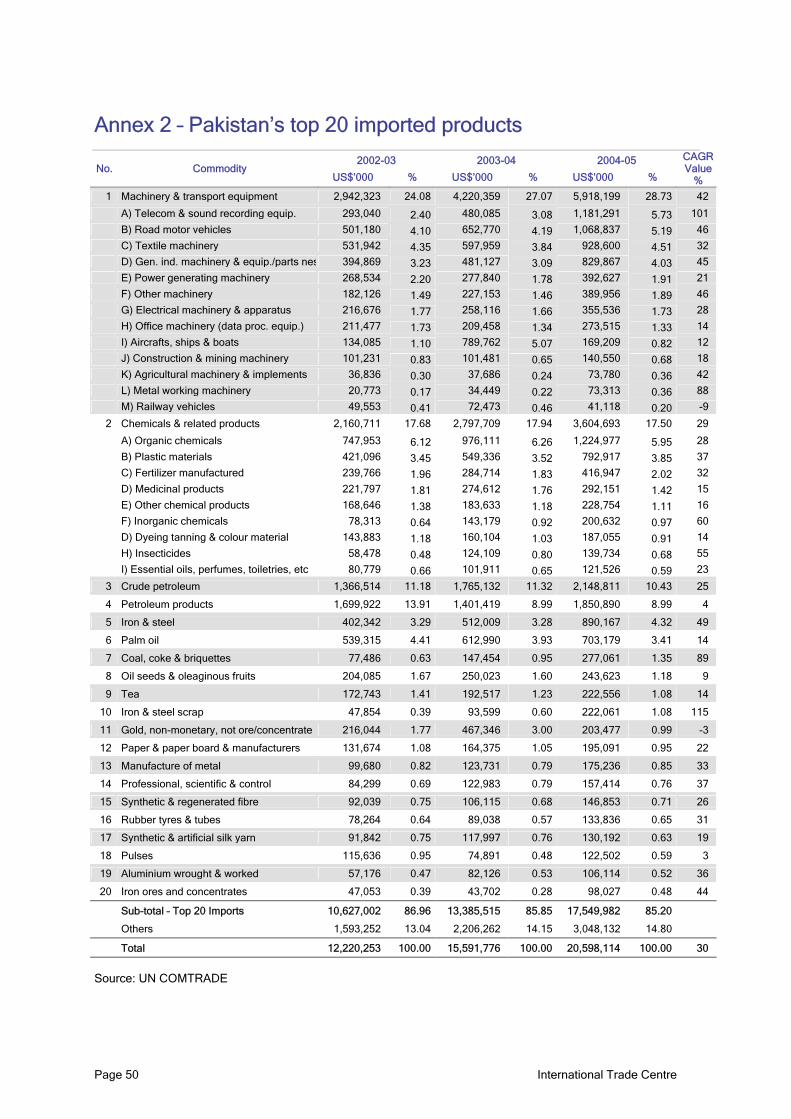

Annex 1 – Pakistan’s top 20 exported products .. . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

Annex 2 – Pakistan’s top 20 imported products .. . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

Annex 3 – Pakistan’s NAMA proposal . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51

References ... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56

List of Tables Table I.1: Overview of Pakistan’s textiles and clothing industry .......................................... 7 Table I.2: Structure of Pakistan’s textiles and clothing industry, 2003 ................................ 8 Table I.3: Pakistan’s major leather products, 2002-03 ........................................................ 9 Table I.4: Overview of Pakistan’s leather industry, 2002-03 ............................................... 9 Table II.1: Cross country comparison – growth rates (%) and (share of exports (%)) ........ 14 Table II.2: Product diversification – Number of equivalent products .................................. 14 Table III.1: Key products in Pakistan’s export basket (Million PKR).................................. 19 Table III.2: Pakistan’s exports of textiles and clothing to the EU....................................... 25 Table III.3: Pakistan’s exports of textiles and clothing to the EU....................................... 25 Table VI.1: Initial and final rates after application of Swiss formula with selected

coefficients ................................................................................................................. 36

List of Figures Figure III.1: Contribution of the textiles and clothing sector to Pakistan’s economy

(2005-06)....................................................................................................................20 Figure III.2: EU trade with Pakistan in 2004 ......................................................................21 Figure III.3: Growth of Pakistan bed linen as a GSP-covered product, 1996-2003

(Euros) .......................................................................................................................23 Figure III.4: EU textiles and clothing imports from Asia (2002-04) ....................................24 Figure III.5: EU textiles and clothing imports from Pakistan ..............................................24

International Trade Centre Page 1

Executive summary

Pakistan is a developing economy with a population of 156 million, the world’s sixth largest. Pakistan’s Gross Domestic Product (GDP) in 2006 was estimated at approximately US$404.6 billion. Pakistan ranks 55th worldwide in factory output. Pakistan’s industrial sector (non-agricultural goods) accounts for about 24% of GDP. The manufacturing sector grew at an average rate of 8% from the 1960s to the 1980s, but growth fell to 3.9% during the 1990s. The manufacturing sector has shown impressive recovery in recent years, growing at a compound rate of 10.9% per annum during 2001 and 2005, with large-scale manufacturing growing even faster.

The food, textiles and clothing (T&C), and leather industries heavily dominate (over 50%) Pakistan’s manufacturing sector. Cotton-based textiles alone contributed 46% of total manufacturing, 60% of total exports and employed 38% of all industrial workers.1 The textile industry’s share of the economy, along with its contribution to exports, employment, foreign exchange earnings, investment and value added, makes it Pakistan’s single largest manufacturing sector. The leather industry is the second largest foreign exchange earner after textiles. It is one of the established indigenous manufacturing sectors to have developed reasonably well. Leather exports have increased at an average rate of 11% per annum. At present, the industry contributes at least 5% to manufacturing GDP, 7% to total exports and provides direct employment for more than 200,000 people.

The chemical processing industry contributes 21% to value added of Pakistan’s manufacturing sector. It is capital-intensive, and its share in employment is 9%. Pakistan’s electronics industry has grown rapidly in recent years, with nearly 1 million television (TV) sets, 300,000 personal computers (PCs), and 250,000 digital video disc (DVD) units produced in the country in 2004. As an indication of this growth, only 60,000 TV sets were produced in 2000. Several local brand names have also appeared.

Exports from Pakistan increased at an annual compound rate of 5.6% during the 1990s. However, from 2000-01 these started to increase at a faster pace, with annual compound growth of almost 16% between 2002 and 2006. Exports were expected to reach US$18.6 billion in 2007, an increase of 12.9%.2 Pakistan’s exports are highly concentrated in a few items, namely, cotton, leather, synthetic textiles and sports goods. Despite the overall fast growth of exports, exports of textile manufactures only grew by 6.2% – a disappointing performance. Prominent among these exports are knitwear (growing at 13.9%), readymade garments (6.8%), made up articles (8.9%), cotton yarn (4.6%), and towels (2.6%). Exports of other textile materials registered a high double-digit growth of 17.2%. Export of raw cotton, cotton cloth and bed wear on the other hand registered a decline. Pakistan’s exports are also highly concentrated in a few countries.

The World Trade Organization (WTO) Non-Agricultural Market Access (NAMA) negotiations aim at binding and reducing tariffs not just on industrial products, but also on products like fish and fishery products, which also fall outside the purview of the Agreement on Agriculture (AOA). This agreement is important for developing countries, because the products and sectors

1 Ministry of Finance Economic Survey 2006-07, available at

http://www.finance.gov.pk/survey/survey.htm. 2 Ministry of Finance Economic Survey 2006-07 (op. cit.).

Page 2 International Trade Centre

that fall under its ambit are of vital importance to the industrial development of these countries and to the livelihoods of their people.

Since the Hong Kong Ministerial Conference in December 2005, attention has focused on variations of the so-called Swiss formula by which higher tariff rates are reduced to a proportionately greater extent than lower rates, and the maximum rate for a country’s rates is set at a level determined by the “a” coefficient. Pakistan’s proposal is for a Swiss formula with two “a” coefficients of 6 and 30 – in effect setting future maximum rates – to be applied by developed and developing countries, respectively. These coefficients are similar to the existing unweighted averages of bound tariff lines for these groups of countries. This approach would also have the effect of compressing or “harmonising'” tariff levels within each of the two groups of countries, bringing down high tariffs that prevail in some other key developing country markets. The idea of having two Swiss coefficients, one for developed and another for developing countries, is also favoured by Canada, the European Union (EU) and the United States (US) but with coefficients of 10 and 15 for developed and developing countries, respectively. These proposals for dual Swiss coefficients, by Pakistan, Canada, the EU and the US, would lead to greater harmonisation of rates within the developed and developing country groups, respectively.

In a draft text put forward by the Chairman of the NAMA Group in July 2007, it is stated that there is “an almost unanimous view that a simple Swiss formula with two coefficients should be adopted”.3 The Chairman then suggests a compromise in which the rates coefficient for developed countries would lie in the range of 8-9, while that for developing countries would be in the range 19-23. In either case, the agreed approach would be supplemented by the possibility of the elimination of tariffs (on a voluntary basis by developing countries) in some sectors, said to be of export interest to developing countries. There would also be the flexibility of keeping a certain percentage of tariff lines unbound or of applying no or less than formula cuts.

However, the Chairman’s July 2007 text is not yet an agreed position, and no other proposal has been formally withdrawn. For example, Argentina, Brazil and India (ABI) made a proposal, largely based on an earlier proposal by the first Chairman of the NAMA Negotiating Group, Ambassador Girard of Switzerland, by which the “a” coefficient for each country would essentially be based on its existing average bound rates, so that with the application of the formula the average rate would become the maximum rate.4 A group of developing countries, the so-called NAMA 11,5 further suggested in June 2007 that consideration might even be given to returning to another early proposal in which linear or straight percentage cuts were the key element. A number of other proposals by individual countries and groups have largely been overtaken by subsequent proposals from the same countries or groups in which they participate.

The application of the formulae, supplementary modalities and flexibilities makes the outcome difficult to evaluate, and the impact would also vary across sectors depending on the initial levels of tariffs. In the major developed country markets, the formula itself is critical but the possibility of the elimination of tariffs in sectors of interest to developing countries could be 3 WTO document JOB(07)/126 of 17 July 2007. 4 Under this proposal the “a” coefficient could be multiplied by a second, “b”, coefficient which, if greater

than unity, would lessen the tariff-cutting effect. 5 The NAMA 11 consists of Argentina, Bolivarian Republic of Venezuela, Brazil, Egypt, India, Indonesia,

Namibia, Philippines, South Africa and Tunisia.

International Trade Centre Page 3

very important. Whichever formula is used, the effects on Pakistan’s exports to other developing country markets would depend on the extent to which Pakistan’s key exports were excluded from the tariff reductions by use of the “flexibilities” available to such countries. There is some concern that other forms of protection, such as anti-dumping, could replace tariffs, negating the effects of the formulae cuts. Pakistan has every reason to be concerned about this possibility, having been subject to such actions in developed countries in the past.

The Doha Ministerial Declaration requires “less than full reciprocity” in tariff reduction commitments for least developed and developing countries, but this is not defined. Some (mostly developed) countries argue that establishing a higher “a” coefficient for developing countries under the Swiss formula meets this requirement. However, in previous rounds of negotiations, “less than full reciprocity” (a term taken from GATT Article XXVIII bis) has been manifest in a lesser percentage cut in tariffs by developing countries. On the basis of the full range of coefficients currently under consideration, there would be a higher percentage cut in bound rates by developing countries.

In the work carried out under this project,6 tariff cut simulations for Pakistan’s four major non-agricultural export sectors (T&C, leather, chemicals and electrical goods) show that the various formulae under consideration would provide improved market access opportunities for Pakistani exports. These simulations of tariff cuts cover 33 major industrial export products (15 top export products from T&C, 4 from leather, 10 from chemicals and 4 from electrical goods).

This analysis suggest that an objective for Pakistan in the NAMA negotiations should be to eliminate the tariff peaks of developed countries as they are hurting its exports, especially in the T&C sector which constitutes about 70% of its exports, and all of the formulae being considered should largely achieve this objective, with varying degrees of success. Some previously privileged T&C exporters with greater preferences than Pakistan are also seeking special provisions that would reduce the value of formula cuts or extend the implementation periods in this area, and, while this has been successfully resisted till now, no doubt such proposals would be welcomed in competing industries in major markets. This is obviously an area where Pakistan needs to be particularly attentive.

At the same time, Pakistan needs to consider how best to pursue a defensive approach that provides an adequate cushion against the potential negative impact of rapid adjustment to external shocks. For example, Pakistan may avail itself of the flexibilities to exclude certain sectors from tariff reductions or protect them from the full depth of formula cuts. The dual Swiss formula with coefficients of 10 and 15 (or 8-9 and 19-23, as now proposed by the Chairman of the NAMA Group) could prove difficult for some areas within Pakistan’s industrial sector. Therefore, the main question for Pakistan will be to decide on which variation of the flexibilities to adopt. Here it has the choice of excluding up to 5% of tariff lines from any formula reduction (provided that does not exceed 5% of imports), or applying half of the formula cuts to 10% of tariff lines (not exceeding 10% of imports). The ultimate choice

6 See WTO NAMA Negotiations: Challenges and opportunities for Pakistan – NAMA formulas – Tariff cut

scenarios, ITC, February 2007. However, it should be noted that the main work for the simulation study was carried out on the basis of 2005 tariff structures, when Pakistan’s unweighted bound average MFN rate was some 35% (the corresponding applied MFN rate was 14%). However, early in the negotiations, Pakistan extended its binding coverage to close to 99% of tariff lines, raising the overall unweighted average MFN rate to 55% in 2006. This means that the Pakistan coefficient in the ABI formula would rise from 35 to 55, implying even less cuts of bound tariff rates for Pakistan than those shown in that study.

Page 4 International Trade Centre

depends on how many sensitive sectors would be affected under the alternatives, but given the width of Pakistan’s industrial base, it may be tempting to adopt the second of these two approaches.

This same choice of flexibilities is also being faced by other developing countries and this could have implications for Pakistan’s prospects for increasing its exports to other developing countries. This seems to be less of a problem in the Gulf States where rates are quite modest but could be important in other developing markets. In those cases, Pakistan may wish to consider deepening its ties within Asia to take advantage of the high growth of some markets in the region.

Overall, the alternative formulae options, the possibility of elimination of tariffs in some key sectors (with voluntary participation by Pakistan), and the flexibilities for exclusions or less than formula cuts all raise some difficult questions for Pakistani policy-makers in relation to the pace and depth of its ongoing reforms, as well as in relation to the policies to be pursued in promoting nascent industries to diversify and expand Pakistan’s production and trade base. Too deep cuts and too rapid reforms could have negative effects on sensitive sectors in the short term, including for employment and tariff revenues. On the other hand, maintaining high levels of industrial protection may involve longer-term welfare costs and could have negative effects on the export drive by raising the costs of material inputs.

In conclusion, Pakistan should continue its active participation in the NAMA negotiations and keep pressing for better market access in developed countries through steep reductions in their tariff levels. Pakistan needs to work together with other developing countries to maintain solidarity in the NAMA negotiations and better press its position. It should also seek to deepen regional ties with fast growing markets in the Asian region.

International Trade Centre Page 5

I. Pakistan’s economic and political situation, and prospects7

Pakistan is a developing economy with a population of some 156 million, the world’s sixth largest. Pakistan’s GDP in 2006 was estimated at approximately US$404.6 billion, larger than that of Saudi Arabia and a little smaller than that of the Philippines. The economic scenario at present is robust with GDP growth of over 6% for the fourth consecutive year and much-improved macro-economic indicators. With a per capita income of over US$900 and foreign exchange reserves hovering around US$13 billion, there has been a significant increase in foreign direct investment. The country’s Eurobonds received a favourable international response last year. There has been significant growth in the socio-economic infrastructure of the country, a much better implementation of economic reforms and, despite some difficulties, the privatization process is moving ahead.

On the other hand, Pakistan’s stance in the global fight against terrorism since the events of 9/11 has led to better treatment in some markets, contributing significantly to the achievement of Pakistan’s economic objectives. However, the re-profiling and write-off of its debt portfolio, the assistance of multilateral lending agencies, the upsurge in remittances by expatriate Pakistanis, and the trade incentives given by EU countries may not be available in coming years. Pakistan is facing a tough international environment, especially with the elimination of restraints under the WTO Agreement on Textiles and Clothing, and recent events have highlighted the domestic economic challenges, too. In the face of negative fiscal developments and a widening external account gap, the authorities have increased interest rates in a move that could presage an increase in the real effective exchange rate with possible negative effects on exports.

Pakistan ranks 55th in the world in factory output. Pakistan’s industrial sector (non-agricultural goods) accounts for about 24% of GDP. Cotton textile production and apparel manufacturing are the country’s largest industries, accounting for about 64% of total exports. Other major industries include leather, cement, fertilizer, edible oil, sugar, steel, tobacco, chemicals, machinery, and food processing. Pakistan is currently privatizing large-scale parastatal units: the public sector accounts for a declining proportion of industrial output, while growth in overall industrial output (including the private sector) has accelerated. Current industrial policy is aimed at diversifying the country’s industrial base and bolstering export industries.

The manufacturing sector (non-agricultural goods) grew at an average rate of 8% from the 1960s to the 1980s, but growth fell to 3.9% during the 1990s mainly because of a reduction in investment levels due to a lack of policy continuity and consistency. Political instability, the law and order situation in the major industrial centres, transport bottlenecks, as well as unreliability and inadequate availability of power supply at affordable rates, were also responsible for the deceleration in growth during the 1990s.

The manufacturing sector has shown impressive recovery recently, growing at a compound rate of 10.9% per annum from 2001 to 2005, with large-scale manufacturing growing even faster. However, while strong growth has been maintained, this has slowed slightly to 9.9% in 2006 and 8.45% so far this fiscal year. Political and macroeconomic stability, utilization of tariffs, increased investments, improved utilization of productive capacity, and growth in demand for manufactured products, resulting from higher exports and consumer spending 7 The data for this section are taken from the Ministry of Finance, Economic Survey 2006-07, available at

http://www.finance.gov.pk/survey/survey.htm.

Page 6 International Trade Centre

(fuelled by increased remittances), have been the major factors leading to this growth. The share of manufacturing in Pakistan’s GDP is currently 18.2%, and production costs have come down because of higher production volumes and economies of scale. The Government has made important efforts to reduce the costs of production in Pakistan. In this regard, it has reduced tariffs on raw materials in order to ensure low cost inputs in most sectors for cost effective production. The positive effects of these changes have been most marked in the electronics and heavy engineering sectors.

The food, T&C, and leather industries heavily dominate (over 50%) Pakistan’s manufacturing industry. The share of textiles and its derivatives in exports was as large as 67% in 2003-04. Other major segments in manufacturing include chemicals and pharmaceuticals (15.2%), basic metal industry (7.7%), non-metallic mineral products (5.1%), machinery (4.6%), cement (4.4%), and automobiles (4.4%). Automobiles, electronics, cement, fertilizers and textiles have all showed cumulative double-digit growth during the last three years. The share of high technology goods in Pakistan’s export basket is less than 1%, whereas engineering goods made up 63% of world trade in 2003, with electronics contributing nearly half of this value. Thus, Pakistan appears to be underperforming in this sector.

Tradit ional low value-added industries

Pakistan’s manufacturing sector still revolves around traditional low value-added industries, whose share in world trade is either declining (resource based and low technology goods) or nearly constant (medium technology goods). An efficient, world standard supply chain, which is critical for local industry to develop, is missing, partly due to insufficient scale economies and partly to bundling of raw material, parts and modules by multinationals in their assembly-oriented companies, which discourage a local vendor industry.

Textiles and clothing

T&C holds the biggest share of Pakistan’s manufacturing sector as well as its exports, contributing 10.5% to GDP, 68% to exports and employing 38% of all industrial workers in 2003/04. The T&C industry – with its share of the economy, and its contribution to exports, employment, foreign exchange earnings, investment and value added – is Pakistan’s single largest manufacturing sector.

With exports reaching about US$8.6 billion in 2004-05, Pakistan is one of the world’s largest textile exporters. T&C trade is classified into two broad categories, i.e. textiles, which includes yarn, fabric and made-ups; and clothing, which represents ready-made garments. The variety of products ranges from cotton yarn to knitwear. Made-up garments and bed wear are the most important export products, with an export value of about US$1.35 billion each. Knitwear, ready-made garments and cotton yarn also have important shares in total exports.

Overall, the US and EU are Pakistan’s largest trading partners accounting for a 25% and 20% share of Pakistani exports, respectively. Other major importers include China (yarn), the Untied Arab Emirates (UAE) and Saudi Arabia.

Table I.1 gives an overview of Pakistan’s textile industry.

International Trade Centre Page 7

Table I.1: Overview of Pakistan’s textiles and clothing industry

Total number of units (2005)

Ginning 1,221

Spinning 445

Weaving Large 140 Small 425 Power looms 20,600

Finishing Large 106 Small 625

Garments Large 600 Knitwear 700 Towels 400

Total capacity

Ginning More than 10 million bales

Spinning 1,900 million kilograms yarn

Weaving 5,600 million square metres of fabric

Finishing 3,500 million square metres

Garments 650 million pieces

Knitwear 350 million pieces

Towels 55 million kilograms

Major economic contribution by textile sector during 2002-03

Exports 68% of total exports (US$7.4 billion)

Manufacturing 46% of total manufacturing

Employment 38% of total industrial workers

GDP 10.5% of total GDP

Investment 31% of total investment

Taxes PKR 101 billion per annum

Interest PKR 44 billion per annum

Salaries & wages PKR 4.5 billions per annum

Contribution to R&D PKR 148 billion per annum

Bank financing US$1 billion during 2002 and 2003

Investment in last 4 years US$4 billion

Source: Digest of Industrial Sectors in Pakistan & Pakistan Investment Guide

At present, the T&C sector consists of a large-scale organized sector and a highly fragmented, cottage/small-scale sector. The organized sector comprises integrated textile mills, i.e. spinning units with shuttle-less looms. The downstream industry (weaving, finishing, garments, towels and hosiery), with great export potential, is mostly in the unorganized sector.

Table I.2 depicts the structure of Pakistan’s T&C industry.

Page 8 International Trade Centre

Table I.2: Structure of Pakistan’s textiles and clothing industry, 2003

Sector Sub-sector No. of units

Size Production

Spinning 403 9.2 million spindles 147,852 rotors

1,500 million kgs

Composite units 50 9,876 looms 384 million m2

Total 453

Independent weaving units

124 23,600 shuttle-less looms

Finishing units 10

Large-scale mill sector

Garment units 50 5,000 sewing machines

Independent weaving units

453 50,000 looms 3,600 million m2

Power looms 20,600 175,200 looms

Total 21,053 225,200 looms

Finishing 625 Cotton Synthetic

2,700 million m2 760 million m2

Terry towels 400 7,602 looms 53 million kgs

Garments 2,500 300,000 sewing machines

600 million pieces

Cottage/small-scale sector

Knitwear 600 12,000 knitting machines

400 million pieces

Source: Pakistan Investment Guide (Experts Advisory Cell)

Pakistan’s T&C sector is suffering due to high costs of production and Pakistan’s negative image relating to terrorism. The way forward is to concentrate on competitiveness and niche products. Concentration on high-end yarns, woven fabrics, and home textiles (including towels) should be a priority. At the same time, investments should not saturate a particular product line: denim fabric is a good example. In light of reduced numbers of key players in this sector globally, a level of regional co-ordination in South Asia and China remains of prime importance.

Preferential market access is important for this sector. However, for countries like Pakistan with few preferential pockets, the multilateral NAMA negotiations are the sole solution. Tariff reduction at the multilateral level will surely increase trade in this sector and Pakistan should encourage consensus with other developing countries to pursue this aim. The fact that the T&C sector engages 38% of the total workforce of the country and accounts for 68% of its total exports makes this an important goal for the Government.

Leather goods

Pakistan’s leather industry also contributes substantially to GDP: it is the second largest foreign exchange earner after T&C. Leather exports have increased at an average of 11% per annum. At present, the industry contributes around 6% to manufacturing GDP and 7% to total exports, and provides direct employment for around 250,000 people. There are more than 2,500 tanneries and footwear-manufacturing units, mainly located in Karachi, Lahore, Sialkot and Kasur.

International Trade Centre Page 9

Pakistan is well known internationally for very high quality, and a wide-range, of finished leather garments (sports jackets) and gloves (working and industrial). However, Pakistan’s contribution of leather goods (handbags, purses, suitcases, key chains, belts, etc) and footwear is very small. The major leather products manufactured by the sector include footwear, leather garments, leather gloves, handbags, purses, key chains, wallets, etc.

The comparative position of value addition in leather and leather made-ups is given in Table I.3.

Table I.3: Pakistan’s major leather products, 2002-03

Item Quantity Value

(US$ million)Conversion

rates Quantity

(million ft2) US$ / ft2 of

leather

Finished leather 12.61 million m2 177 10.76 135.58 1.31

Leather garments 7.1 million pieces 295 45 ft2 / piece

35 ft2 / piece

30 ft2 / piece

25 ft2 / piece

322.20

250.60

214.80

179.00

0.92

1.18

1.37

1.68

Leather gloves 19.38 million pieces 26 1.0 ft2 / piece

1.5 ft2 / piece

2.0 ft2 / piece

19.38

29.07

38.76

1.34

0.89

0.67

Leather footwear 2.75 million pieces 23 1.75 ft2 / pair

2.0 ft2 / pair

2.5 ft2 / pair

4.13

5.50

6.88

5.57

4.18

3.34

Source: Ministry of Food, Agriculture & Livestock (MINFAL)

Around 80% of leather production is exported. The share of leather products in total exports declined from 9.1% in 1990-91 to 5.3% in 2003-04. Leather products – like jackets, shoes and gloves – account for more than two-thirds of leather exports with tanned unfinished leather accounting for the remaining third. Exports of leather from Pakistan are normally finished leather, mostly used in footwear, goods and upholstery. Of total leather exports from Pakistan, 53% is of skin leather. This is opposite to the world trend where skin leather constitutes only 11% of total leather exports.

Table I.4 below provides an overview of Pakistan’s leather industry.

Table I.4: Overview of Pakistan’s leather industry, 2002-03

Total number of units

Tanneries 725

Leather garments/apparel 461

Leather footwear 524

Leather gloves 384

Leather goods 142

Leather sports goods 160

Page 10 International Trade Centre

Total capacity

Tanned leather 90 million m2

Leather garments/apparel 7 million pieces

Leather gloves 10 million pieces

Leather footwear 200 million pieces

Export growth (1991 to 2001) 1.11%

Contribution to total growth 7%

Source: Pakistan Tanneries Association (PTA)

More than 80% of the leather industry’s units are located in Karachi and Lahore. There are numerous tannery units in the unorganized sector, producing leather on a cottage basis with negligible use of machinery and present day technology. The industry is also flourishing in Hyderabad, Multan, Sahiwal, Kasur, Sheikhupura, Gujranwala, Sialkot and Peshawar. The growing capacity for tanning in the country has given a fillip to the development of the footwear and leather goods manufacturing industries, which produce gloves, garments bags and other products.

The leather sector is facing similar problems to those of the T&C sector, in terms of high production costs and Pakistan’s brand image problems. In addition, a main problem is that the majority of Pakistan’s exports are of skin leather rather than products, which is opposite to world trends.

There is a need to encourage and improve the production and export of leather gloves and leather footwear, rather than exporting the skin leather to be used by importing countries themselves to make footwear and other leather goods. Pakistan’s footwear exports are currently minimal compared to its finished leather exports. Footwear production and export should be encouraged in order to capitalize on available raw material and to promote downstream value-added goods. Leather product manufacturers should also begin developing local brand loyalty of their products. Venturing into the local market and creating a consumer base at home is a good start before moving gradually into high-end goods for export.

Chemicals

The chemical processing industry contributes 21.2% to Pakistan’s manufacturing value added. It is capital-intensive and its share in employment is 8.9%. Pharmaceuticals, fertilizers, synthetic resins and petroleum refining and products constitute the bulk of the sector’s value added.

The chemical industry is significant: the global chemical market is worth US$1.8 trillion and its trade volume is US$600 billion. Over the last two decades the industry has grown at a rate of 1.5 times the world GDP growth rate. The Asia-Pacific region chemical industry has grown faster than the global chemical industry and adds US$30 billion of output every year. As much as 45% of the total chemical products produced in the region are bulk organic chemicals, which also form a major component in the export basket from the region. This region commands a 30% share of the global chemical market and is fast emerging as a key player in the global chemicals business.

International Trade Centre Page 11

Petrochemical and chemical products constitute approximately 40% of Pakistan’s total imports. Pakistan has no facilities to produce basic petrochemicals – like ethylene, propylene, butadiene, etc. – and they are imported in bulk. Total production of chemicals in Pakistan is around US$3 billion. Imports of chemical-related products constitute 20%, or around US$2 billion, of total imports. Thus, there is a vast potential for development of this sector through import substitution and self-reliance.

Locally available natural gas, petroleum and coal resources are being used mainly to meet the energy requirements of the country. They have not been utilized in the manufacture of chemicals where, in some cases, value-addition can be ten-fold. The only exception is the use of natural gas to produce fertilizers. There exists vast potential to manufacture chemicals from reserves of indigenous natural gas, coal and minerals.

Some organized chemical sectors are well developed. A few basic chemicals – like sulphuric acid, caustic soda, soda ash and chlorine – have sufficient installed capacity to meet local demand. Most raw materials and intermediates for dyes and pigments, paints and varnishes, pesticides, and plastics and plasticizers are being imported. These raw materials and intermediates mainly belong to or are derived from petrochemicals, which have no base in Pakistan.

Dyes and pigments are being produced locally but only partially meet local demand. Most of these raw materials are imported. Active ingredients used in pesticides and insecticides are not produced locally, but about 30 units are involved in formulations based on imported raw materials. There is a strong need for domestic production of some active ingredients. Numerous units are involved in the production of soaps and detergents. However, there is heavy dependence on imported tallow for soaps and alkyl benzene, and sulfonic acid for the production of detergents. The plastics, plasticizers and polyester downstream industries are well developed but, again, depend on imported petrochemical raw materials, i.e. olefins, poly olefins and benzene, toulene and xylene (BTX).

Development of the petrochemical sector has been neglected, in spite of numerous recommendations over the last three decades to setup a naphtha or hydro cracker. No appreciable progress is possible in the chemical sector without the indigenous production of petrochemical building blocks, like olefins (ethylene, propylene, butadiene) and basic aromatics, like BTX. In view of the importance of basic petrochemicals, the setting up of a petrochemical complex is strongly recommended.

Major issues for the chemical sector include the inadequate supply of energy and other inputs as well as their high cost, an obsolete technology base, limited research and development (R&D) and quality control, environmental problems, and the large investments required to diversify into other processes with higher scales of production. However, this would likely require greater levels of import protection or support than are presently available and any such increases would run counter to the Government’s liberalisation strategy. So far, investment in this industry is estimated to be PKR 360 billion.

This sector also faces serious threats from Chinese exporters, who have had a history of dumping chemicals in the Pakistani market. The Government may need to take effective measures to safeguard this sector against such activities.

Page 12 International Trade Centre

Electrical goods and appliances

Pakistan’s electronics and electrical goods industry is basically a consumer product industry, involved in the manufacture of electric light bulbs, tubes, air conditioners, fans, refrigerators, freezers, television sets, radios, and other electrical appliances. The home appliance sector has grown phenomenally in the last five years: production of refrigerators grew by 20% and air conditioners by 31% from 2001 to 2005. Consistent production growth over this period was due to robust growth in the economy. This, coupled with improved quality, has lead to a preference for local products and gradual development of brand loyalty. Additionally, a low tariff regime has encouraged price competitiveness.

Pakistan does not produce picture tubes, deflection yokes, etc., which are vital components for a number of electrical goods being assembled and manufactured locally. Hence, there is demand for spare parts and various accessories, which are presently being imported. Growth in this sector is being hampered by lack of availability of local raw materials, capacity constraints due to low investment, high financial and infrastructure costs and relatively low technology levels. However, despite the above factors, Pakistan’s exports in the home appliance sector remain competitive.

Adequate market access could open doors for Pakistan’s electronic exports to a US$72 billion annual world trade in appliances. The Government should consider granting a degree of protection and incentives to this growing sector, particularly with the Chinese Free Trade Agreement (FTA) expected to come into force in 2007. It is also important that Pakistan continues its efforts to curtail the smuggling of electronic goods into the country via Afghanistan. The northern areas (Punjab & NWFP) are especially affected by the influx of such smuggled products. Increasingly, used television sets and picture tubes are also being smuggled into the country from China.

Larger production volumes have also resulted in the development of a vibrant vendor industry, with major opportunities in sub-assembly and modules. There is enormous scope for indigenous development and manufacturing of switching equipment, computers, modems and routers, and broadband Internet services. The Government plans to assist development of an international quality indigenous supply chain, and to raise the share of electronics in the output of the manufacturing sector from under 3% at present to 10% in 2010 and 20% in 2020.

International Trade Centre Page 13

II. Pakistan’s export and import regimes

In 1947, only 5% of the large-scale industrial facilities in British India were located in what became Pakistan. The country started with virtually no industrial base and no institutional, financial, or energy resources.

The pace of industrialization in Pakistan since independence has been rapid, although it has fluctuated in response to changes in government policy and world economic conditions. During the 1950s, manufacturing expanded at about 16% annually. During the first half of the 1960s it expanded at around 11% a year, but this pace slowed to under 7% a year in the second half of the 1960s. Between 1970-71 and 1977-78 the index of manufacturing output increased on average by only 2.3% a year, but this rose to an average of 9.9% a year between 1977-78 and 1982-83. Growth averaged 7.7% during the Sixth Five-Year Plan (1983-1988) and 5.4% from 1989-90 to 1992-93. In 1993-94, manufacturing accounted for 17.3% of GDP, of which large-scale manufacturing accounted for 61% and small-scale manufacturing for 39%. Manufactured goods accounted for 64% of all exports by value in 1993-94; the bulk of these exports came in the relatively low-technology areas of cotton textiles and clothing.

In the early 1990s, food processing and textiles dominated the manufacturing sector. Provisional figures for 1992-93 indicated that sugar production was 2.1 million tons, vegetable ghee 819,000 tons, cotton yarn 862,000 tons, and cotton cloth 234 million metres. Other industrial products included motor tyres (647,000 units), cycle tyres (2.2 million units), cement (6.1 million tons), urea (1.4 million tons), soda ash (147,000 tons), bicycles (364,000 units), and paperboard (13,000 tons).

Exports

Exports from Pakistan in 2005-06 were US$16.47 billion, an increase of 14.4% over the previous fiscal year. During the period from 1999 to 2003 world exports increased by 31%. During the same period, Pakistan’s exports grew by 43% reflecting an improvement in its world share. By comparison, Singapore’s exports increased by 26%, Malaysia 19%, Indonesia 25%, UAE 5%, and the Philippines 1%.

Pakistan’s main exports are textiles and related products. The world textile trade is currently estimated to be worth around US$300 billion. Pakistan’s share of current trade volume is around 3%. Pakistan’s non-textile exports are negligible.

The renaissance of export development

Exports from Pakistan had annual compound growth of 5.6% during the 1990s. However, from 2000-01 exports started to increase at a faster pace, with an annual compound growth rate of 9.1% during the period 2001 to 2004. Exports reached US$12 billion in 2003-04.

Over time, there has been a shift in the composition of exports with the share of primary commodities falling and that of manufactured goods increasing. The share of primary commodities decreased from 19% in 1991 to 11% in 2002-03; the share of manufactured goods increased from 57% to 78% during the same period. This increased share of manufactured goods has lessened Pakistan’s export vulnerability to fluctuations in the international price of primary commodities. Pakistan’s principal exports are cotton yarn, cotton

Page 14 International Trade Centre

fabrics, ready-made garments, synthetic textiles, hosiery, other textile made-ups, fish products, leather and leather garments, sports goods, surgical goods and carpet. The T&C sector alone has been the backbone of the export sector.

Pakistan is not a major player in international trade. In fact, it is under-represented as a trading nation based on its share of world exports and imports when compared with other developing countries: it accounted for merely 0.12% of world exports in 2004. In addition, its share in world exports has declined from 0.26% in 1960 to 0.12% in 2004, whereas the share of other developing countries has increased manifold. For example, Korea has increased its share of world exports from 0.1% during the 1960s to 2.06% in 2000.

Table II.1 below explains the share of world exports over time.

Table II.1: Cross country comparison – growth rates (%) and (share of exports (%))

Region / Country 1960s 1970s 1980s 1990s 2000s

World 8.8 20.1 6.8 6.6 7.2

Asia 4.5 23.8 10.9 8.3 5.4

China 0.04 (1.31) 22.1 (0.2) 14.3 (1.39) 13.7 (2.72) 21.0 (3.5)

India 4.1 (0.91) 14.4 (0.55) 10.0 (0.48) 9.2 (0.58) 14.0 (0.58)

Korea 39.4 (0.10) 37.4 (0.63) 17.2 (1.56) 9.8 (2.27) 7.7 (2.06)

Malaysia 4.1 (0.68) 23.3 (0.53) 8.6 (0.74) 11.5 (1.27) 1.3 (1.16)

Pakistan 0.3 (0.26) 20.1 (0.13) 8.1 (0.15) 5.9 (0.12) 12.2 (0.12) Source: International Trade Centre

The non-diversif ied export basket

It has been widely acknowledged that Pakistan’s export base is extremely narrow; the cotton group alone contributes 63% of export earnings. Not only is Pakistan’s export base relatively undiversified, it is also concentrated in relatively low value added products. This combination represents a serious issue for Pakistan. Unfortunately, there has been little progress in increasing the number of products; only 34 new products have been added since 1998.

Table II.2 below explains Pakistan’s diversification vis-à-vis all other countries and South/Far Eastern countries.

Table II.2: Product diversification – Number of equivalent products

2002 average 1998 average

Products Pakistan All countries

South / Far east countries

Pakistan All countries

South / Far east countries

Fresh food 9 15 19 13 14 16

Processed food 2 14 15 12 10 11

Wood products - 15 15 - 13 13

Textiles 30 37 43 11 20 25

Chemicals 4 4 66 - 43 5

Leather products 5 8 3 8 5 6

Basic manufacturers 14 53 60 6 42 47

Non-electronic machinery - 31 29 - 25 26

International Trade Centre Page 15

2002 average 1998 average

Products Pakistan All countries

South / Far east countries

Pakistan All countries

South / Far east countries

IT/consumer electronics - 7 8 - 7 8

Electronic components - 19 17 - 15 14

Transport equipment - 9 9 - 7 6

Clothing 13 30 33 10 1 20

Miscellaneous manufacturers 6 2 36 3 5 19

Minerals 3 4 4 4 5 5

All categories 86 318 362 52 239 24 Source: International Trade Centre

Strategic elements in export development

To capture a larger share of world trade, Pakistan needs to continue its efforts to make a strategic shift in the composition of its exports. This entails promoting exports of products whose share in world trade is increasing and reducing those with a lower or declining share.

Manufacturing goods constitute 63% of global trade (with electronics at 40%), whereas textiles’ share is nearly 6%. This is reversed in Pakistan: textiles constitute 63% and the engineering sector only 3% of total exports. Pakistan is yet to enter the hi-tech exports sector as virtually no hi-tech items are manufactured for export. Most of Pakistan’s exports have low technological content. As the role of technology increases in world trade, Pakistan will need to make concerted efforts to boost the production of its hi-tech industries and include its products in its export categories.

Exports were targeted at US$18.6 billion in 2007, up 12.9% over the previous year. However, this growth rate is somewhat less than the previous few years, partly due to the decline of exports of rice due to weather conditions which kept the domestic price higher and made it more profitable to sell on the home market) and fruits by 2.6% and 14.3%, respectively. Pakistan's exports are highly concentrated in a few items namely, cotton, leather, rice, synthetic textiles and sports goods. These five categories of exports account for 77.2% of total exports during the first nine months of 2006-07 with cotton manufacturers alone contributing 61.5%, followed by leather (4.5%), rice (6.6%), synthetic textiles (3.0%) and sports goods (1.6%).8

In the first 10 months of 2006-07, exports of textile manufactures grew by 6.2%: prominent among these were exports of knitwear (13.9%), ready-made garments (6.8%), made-up articles (8.9%), cotton yarn (4.6%), and towels (2.6%). Exports of other textile materials registered a high double-digit growth of 17.2%. Export of raw cotton, cotton cloth and bed wear on the other hand registered a decline. Exports of engineering goods increased by 6.7% while exports of petroleum products declined by 2.7%. In other manufactures’ categories of exports, all items including carpets, rugs & mats, sports goods, leather products, surgical equipments and chemical & pharmaceutical products registered negative growth. Exports of most of these items have been on the decline for quite sometime. In absolute terms, overall exports posted an increase of US$452.1 million in the first ten months of the current fiscal year over the same period last year. Of this increase, 114.1% or US$516.1 million was contributed by textile 8 Ministry of Finance, Economic Survey 2006-07 (op. cit.).

Page 16 International Trade Centre

manufactures while ‘all other items’ increased by 64.8% or US$293.2 million. This increase of US$809 million was offset by a decline of exports of rice (US$59.3 million) and other manufacturers (US$296.6 million) leaving a net increase of US$452 million.

The Government of Pakistan attributes the less than satisfactory export performance of textile manufacturers to a variety of factors.9 First, it appears that Pakistan’s textile exporters are having difficulties in competing with their traditional competitors. Second, the discriminating and tied-dumping duty of 5.8% on bed linen exports also affected Pakistan’s competitiveness. Third, the poor quality of cotton, due to the contaminated cotton issue, has also adversely affected exports of the spinning industry. Fourth, the rise in the prima cotton price (a genetically modified version), which is imported from the US and is a critical input for producing higher quality bed wear and fabrics, has made these items less competitive in the international market. Pakistan’s export industry also appears to be suffering a need to install new equipment that would lift quality and productivity, shifting away from low value added and poor quality products that fetch low international prices. According to the Government, the issues mainly need to be addressed by the private sector, with the Government playing its role of facilitating and providing some financial support on a temporary basis. Pakistan’s exporters spend little money on R&D, and exporters lack the capacity to meet bulk orders or consumer demands in terms of fashion and design.

Pakistan’s exports are also highly concentrated in a few countries. Seven countries – namely the US, Germany, Japan, UK, Hong Kong, Dubai and Saudi Arabia – account for 50% of its exports. The US, at 27% of total exports, is Pakistan’s single largest export market, followed by the United Kingdom (UK), Dubai, Germany and Hong Kong. Japan is fast losing significance as an export destination, with less than 1% of Pakistan’s exports entering Japan.

Pakistan needs to diversify its exports, not only in terms of commodities but also in terms of markets. Heavy concentration of exports in few commodities and few markets could cause serious export instability.

Imports

Pakistan’s imports continue to be pushed higher by the unprecedented rise in oil prices and continued strength of non-oil imports owing to buoyant domestic demand. Imports were projected to grow by 4.25% for the fiscal year 2005-06. In the first 9 months (July-March), imports were up by 43.2% – rising from US$14.5 billion to US$20.7 billion over the same period the previous year.

Disaggregation of total imports suggests that food imports grew by 35.9% – up from US$990.7 million to US$1.4 billion. Major contributors included wheat, sugar and pulses, which together contributed 93% to the substantial rise in food imports.

Imports of petroleum products have played a key role in taking Pakistan’s imports to a new height. Emerging as the single largest item in the country’s import bill, petroleum group imports amounted to US$4.6 billion during the first 9 months of 2005-06, an increase of 64.5% over the same period in the previous year. Although the quantities of imported crude and petroleum products are down by 2.3% and 5.8%, respectively, the prices of these two items rose by 76.6% and 62.9%, respectively, compared with the previous year, causing imports of

9 Idem.

International Trade Centre Page 17

these two items to rise by 64.5% in value terms. Despite quantity being down, Pakistan was forced to pay US$1.9 billion more to import crude and petroleum products.

Major contributions to 2005-06 incremental imports came from the petroleum group (29%), and raw materials and machinery (almost 35%). These three items alone are responsible for 64% of the increase in imports and for 27.6% of the 43.2% growth in total imports over last year.

Consumer durables, including cars, contributed only 6.4% to the increase in total imports and 2.8% of the 43.2% growth in total imports over last year. Within this category of imports, electrical machinery and appliances contributed a mere 1.7%, and cars only 4.7%.

Like exports, Pakistan’s imports are highly concentrated in a few items, namely machinery, petroleum and petroleum products, chemicals, transport equipment, edible oils, iron and steel, fertilizer and tea. These eight import categories accounted for 72.5% of total imports during 2005-06: machinery, petroleum and petroleum products, and chemicals together accounted for 53.4% of total imports. The concentration of imports remained, by and large, unchanged over the last decade, with the exception of 2000-01.

Pakistan’s imports are highly concentrated from few countries: over 40% of imports originate from just seven countries, namely, US, Japan, Kuwait, Saudi Arabia, Germany, UK and Malaysia. Saudi Arabia is emerging as a major supplier, followed by the US and Japan.

Policy support for economic development

The present multilateral trade negotiations on the Doha Development Agenda (DDA) in the WTO are likely to result in further liberalization of industrial trade and give rise to new opportunities for exporters. However, optimum benefit from these opportunities can only be achieved if sound sector strategies are prepared and succeed in generating exportable surpluses that are competitive both in terms of price and quality. With this in mind, the Prime Minister of Pakistan has asked the Planning Commission to develop sectoral development strategies for traditional or core industrial sectors, as well as developmental sectors with good potential.

Rapid Export Growth Strategy

In order to facilitate a quantum jump in the level of exports, the Trade Policy 2005-06 announced a Rapid Export Growth Strategy (REGS) based on the following five pillars:

1. Resort to trade diplomacy to increase market access.

2. Regional diversification of export markets.

3. Strengthening of the trade promotion infrastructure.

4. Skill development.

5. Early provision of modern infrastructure.

Within the REGS framework, Pakistan planned to focus attention from 2006-07 on the export promotion of a few selected product groups, with a view to facilitating annual exports of each of these products to a level in excess of US$1 billion within 3 years. The product groups

Page 18 International Trade Centre

selected for this purpose include leather products, engineering goods, chemicals and pharmaceuticals, towels, denim, and services.

Trade Development Authority of Pakistan

In view of the rapidly changing international trading environment, the Government has established the Trade Development Authority of Pakistan (TDAP) with the objective of achieving a quantum jump in Pakistan’s exports. The Authority’s mandate has been expanded to include trade development rather than just export promotion. The President signed the Ordinance bringing the TDAP into operation in November 2006. The Authority replaces the Export Promotion Bureau (EPB), which was responsible for trade promotion for the previous 43 years.

The TDAP will be equipped with the necessary resources and autonomy so that it can effectively exploit opportunities for increasing Pakistan’s prosperity through enhanced trade. A Policy Board, chaired by the Commerce Minister and with members representing both the public and private sectors, will supervise the Authority. Highly qualified professionals, paid market-based salary packages, will staff the TDAP. The transition from EPB to TDAP will take approximately 18-24 months.

International Trade Centre Page 19

III. Analysis of Pakistan’s export and imports

Pakistan’s exports during 2004-05 were US$14.4 billion, compared with US$12.3 billion in 2003-04 and US$11.2 billion in 2002-03. This reflects an increase of 16.9% and 28.9%, or achievement of Pakistan’s export targets by 101.7% and 107.3%, respectively.

Following is an analysis of four of Pakistan’s important export sectors. Data on Pakistan’s top 20 exports and imports are attached as Annex 1 and Annex 2, respectively.

Texti les and clothing

The T&C sector contributed 62% to Pakistan’s exports in 2004-05, increasing in value to US$8.9 billion, up 8% over 2003-04. Major categories registering an increase over the previous year were: cotton cloth (9%), knitwear (hosiery) (12%), ready-made garments (10%), towels (29%) and textiles made-ups, including bed wear (6%). There was also a decrease in some items, such as yarn (6%), synthetic textiles (36%) and tents and canvas (11%).

Five categories of goods – cotton yarn, garments and hosiery, cotton cloth, raw cotton and rice – account for 80% of the country’s export earnings. Table III.1 below shows Pakistan’s core export basket.

Table III.1: Key products in Pakistan’s export basket (Million PKR)

Period Raw

cotton Cotton fabrics

Cotton yarn& thread

Knitwear Bedwear Woollen carpets

1999-2000 3,760.8 56,757.2 55,551.4 45,913.1 36,757.1 13,200.4

2000-01 8,072.5 60,485.6 62,954.8 53,201.6 43,649.8 16,424.7

2001-02 1,502.1 69,296.9 57,165.3 52,089.6 56,383.6 14,976.9

2002-03 2,872.6 78,665.4 54,342.0 67,033.7 77,633.0 12,689.8

2003-04 2,741.5 98,542.2 64,868.0 84,014.8 79,666.0 13,173.4

2004-05 6,549.3 110,578.7 62,805.6 96,879.8 86,063.9 16,216.9

Source: www.statpak.gov.pk

A basic analysis of Pakistan’s T&C sector underlines its importance to the social and economic welfare of the country. The sector accounts for more than 69% of total exports, while its share in total manufacturing is 46%. Total textile exports are worth US$8.4 billion, and account for 8.5% of GDP. Substantial investment in the T&C sector over the 5 years from 1999 to 2004 amounted to US$4.5 billion.

Importantly, the sector also accounts for 38% of the country’s employment.10 The clothing sector is the single largest source of industrial employment in the country, employing mainly men (87%) as sewers, with women working in trimming and packing (23%)11. The sector’s

10 Textile Commissioner’s Organization, Ministry of Textile Industry, Government of Pakistan.

11 There is no specific source of these figures and numbers vary distinctly from different sources. The above reflects a mean analysis of the situation determined through industry interviews.

Page 20 International Trade Centre

labour costs are among the lowest in the world, but quality and productivity are also generally low.

Figure III.1 below shows the contribution of the T&C sector to Pakistan’s economy.

Figure III.1: Contribution of the textiles and clothing sector to Pakistan’s economy (2005-06)

Source: Pakistan Textile Commissioner’s Organisation.

Pakistan has an established industry, which adds value at all levels from cotton to made-ups. A broad policy framework – Textile Vision 2005 – aims to make Pakistan a more viable, stronger and more competitive textile industry, especially at the value added stages. For this, over US$2 billion has been invested over the last 3 years on the restructuring of the textile industry as a whole. Emphasis is being laid on increasing the share of downstream industry in overall textile exports, meaning greater value addition. Vertically integrated units or specialized mills both demand consistent quality across huge volumes of single items of clothing, which can only be produced with a skilled workforce.

Despite the high number of units and employment opportunities in the clothing sector, investments here are lowest at 4.8%, compared with spinning, which attracted investment of 47%.

The importance of the EU’s GSP

From 2002 to 2004 Pakistan gained substantially from the special incentive for drugs. From 1999 to 2004, Pakistan experienced a fall in exports of raw cotton, whereas exports of fabrics, knitwear and bed wear, including garments, increased tremendously as a result of the EU’s Generalised System of Preferences (GSP) scheme. (Figure III.2 below gives a profile of EU trade with Pakistan in 2004.) However, this steady growth from 2001 to 2004 decreased in the first quarter of 2005. While there was growth of more than 11% in yarn and fabrics, knitwear and bed wear exports fell by 10%–15%.

11% 9%

67%

8%31% 38% 27% 16%

89% 91%

33%

92%69% 62% 73% 84%

0%10%20%30%40%50%60%70%80%90%

100%

GDP

Value A

dded

Expo

rts

Marke

t Cap

italiz

atio

n

Fixed

Ass

ets

Emplo

ymen

t

Emplo

ymen

t Cos

t

Indire

ct Ta

xes

Textile Others

International Trade Centre Page 21

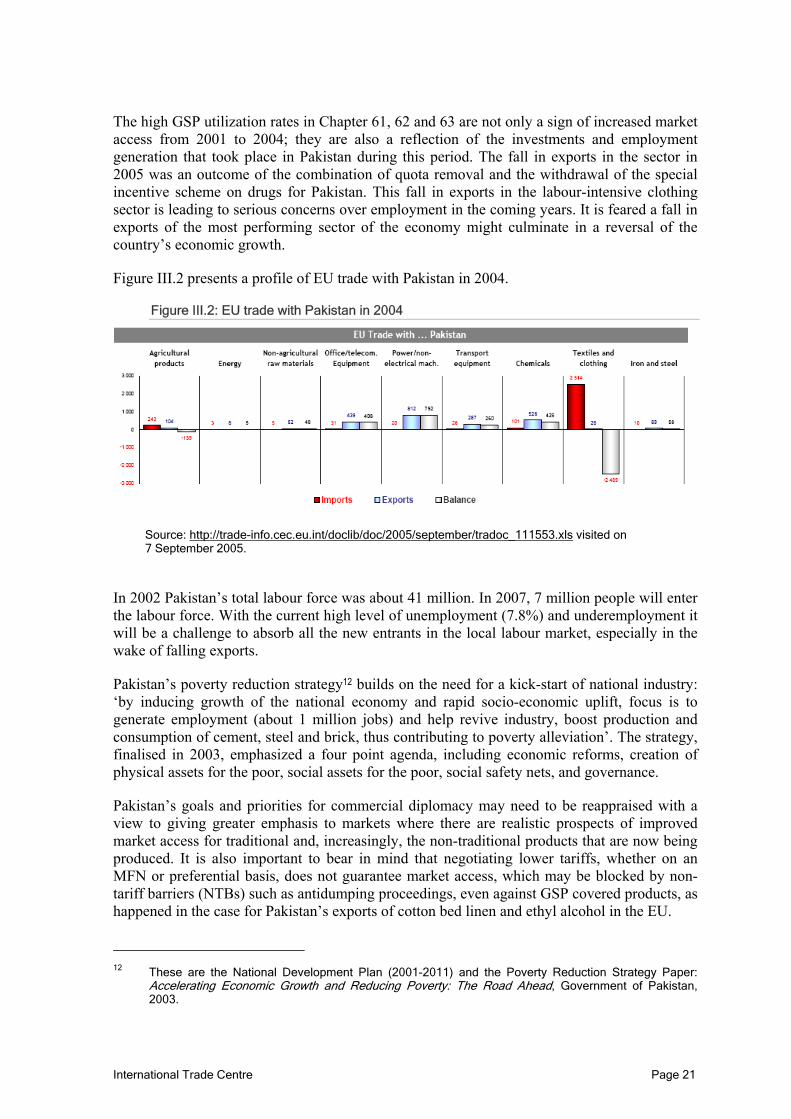

The high GSP utilization rates in Chapter 61, 62 and 63 are not only a sign of increased market access from 2001 to 2004; they are also a reflection of the investments and employment generation that took place in Pakistan during this period. The fall in exports in the sector in 2005 was an outcome of the combination of quota removal and the withdrawal of the special incentive scheme on drugs for Pakistan. This fall in exports in the labour-intensive clothing sector is leading to serious concerns over employment in the coming years. It is feared a fall in exports of the most performing sector of the economy might culminate in a reversal of the country’s economic growth.

Figure III.2 presents a profile of EU trade with Pakistan in 2004.

Figure III.2: EU trade with Pakistan in 2004

Source: http://trade-info.cec.eu.int/doclib/doc/2005/september/tradoc_111553.xls visited on 7 September 2005.

In 2002 Pakistan’s total labour force was about 41 million. In 2007, 7 million people will enter the labour force. With the current high level of unemployment (7.8%) and underemployment it will be a challenge to absorb all the new entrants in the local labour market, especially in the wake of falling exports.

Pakistan’s poverty reduction strategy12 builds on the need for a kick-start of national industry: ‘by inducing growth of the national economy and rapid socio-economic uplift, focus is to generate employment (about 1 million jobs) and help revive industry, boost production and consumption of cement, steel and brick, thus contributing to poverty alleviation’. The strategy, finalised in 2003, emphasized a four point agenda, including economic reforms, creation of physical assets for the poor, social assets for the poor, social safety nets, and governance.

Pakistan’s goals and priorities for commercial diplomacy may need to be reappraised with a view to giving greater emphasis to markets where there are realistic prospects of improved market access for traditional and, increasingly, the non-traditional products that are now being produced. It is also important to bear in mind that negotiating lower tariffs, whether on an MFN or preferential basis, does not guarantee market access, which may be blocked by non-tariff barriers (NTBs) such as antidumping proceedings, even against GSP covered products, as happened in the case for Pakistan’s exports of cotton bed linen and ethyl alcohol in the EU.

12 These are the National Development Plan (2001-2011) and the Poverty Reduction Strategy Paper:

Accelerating Economic Growth and Reducing Poverty: The Road Ahead, Government of Pakistan, 2003.

Page 22 International Trade Centre

Ant i-dumping dut ies on GSP-covered products

Pakistan’s two key products – cotton bed linen and ethyl alcohol – performed exceptionally well in the EU market under the GSP preferential regime. However, this performance has been curbed and restricted by recent anti dumping investigations.

Textile exports from Pakistan in general, and value-added textile exports in particular, suffered a drastic set back as a result of the tragic events on 11 September 2001 in the US. The decision by Pakistan to join the international coalition in the fight against terrorism was based on principles other than its immediate consequence on the economy of the country. However, in order to enable Pakistan to play its role effectively, both the EU and the US offered aid packages.

Under the EU package all value-added exports from Pakistan, i.e. ready-made garments, finished fabric and knitwear, were exempted from import duty with effect from 1 January 2002. Pakistan’s export quota for T&C was increased by 15% with effect from 1 December 2001 and the anti-dumping duty of 6.4% levied on imports of bed linen from Pakistan was terminated. The package made Pakistan eligible for the new GSP scheme applicable to countries combating drugs, removing tariffs on T&C. As a result, Pakistan improved its access to the EU market. The applicable tariffs on T&C were reduced to 5%, 15% and 25% from the beginning of 2002 – a 5% reduction across the board compared with 2001 tariffs.

EU Trade Commissioner, Pascal Lamy, while presenting the package to the EU Council of Ministers and the European Parliament, declared:

We have made these negotiations a top priority because Pakistan is in an exceptional situation. We have targeted those areas where Pakistan can benefit most, namely clothing and textiles. Trade is a weapon of peace. Through trade, and the fostering of greater economic ties with Pakistan, the EU can contribute to alleviating in some measure its current difficulties.

As a direct result of these concessions, there was a surge in bed linen exports to the EU. The value of bed linen exports to the EU increased to approximately 26.5% of the value of total exports of bed linen from Pakistan in the year 2002-03. Exports of bed linen were 18% of the total textile exports of the country in 2003, up from 8% in 1996. Figure III.3 below highlights the steady growth in bed linen exports, which doubled in value from €245,505,650 in 1996 to €533,532,900 in 2003.

However following this increase, and in the wake of Commissioner Lamy’s affirmation that Pakistan was in an ‘exceptional situation’ and that the EU would contribute to alleviating its difficulties through the lifting of import duties, the EU imposed a 13.1% anti-dumping duty on Pakistani bed linen effective from 18 March 2004. In addition, Pakistan also failed to qualify for the EU’s new GSP plus scheme, inter alia also losing the 12.8% benefit of the special drug incentive. In total, the booming bed linen exports suffered a duty of approximately 25%.

The investigation of the EC bed linen case gave rise to some important questions about the EU GSP. In addition to being a GSP-covered product, the increase in imports of bed linen from Pakistan during the investigation period was much less than those of other countries into the EU. For example, imports from Poland increased by 99% (from 4,677.4 to 9,307.7 tonnes), from Turkey by 65% (from 13,412.2 to 22,082.7 tonnes), from Romania by 62% (from 3,179.9 to 8,342.7 tonnes) and from the People's Republic of China by 58% (from 2,842.1 to 4,479.6

International Trade Centre Page 23

tonnes). Moreover, EU market share held by Pakistani producers/exporters (21%) was much lower than the overall increase in market share of imported bed linen (46.3%) or the increase of the market share of Romania (116.3%) or Poland (64%).

Figure III.3: Growth of Pakistan bed linen as a GSP-covered product, 1996-2003 (Euros)

Source: Trade Development Authority of Pakistan (previously Export Promotion Bureau).

While the increase in exports of bed linen from Pakistan was considered dumping, third country exports of bed linen into the EU were not accounted for. The EU also rejected the calculations of Pakistani manufacturers relating to production costs, as well as the price of bed linen in the local Pakistani market. Bed linen export prices were based on calculations of a deemed profit margin of only 3.5%, while a profit margin of 6.5% was taken for the EU industry. This issue was challenged in the reply to the injury statement but was not upheld during the proceedings.

The surge in imports of bed linen from Pakistan during 2002 was helped by the EU concession granted to Pakistan to benefit from duty-free access under the anti-drug GSP special regime. Therefore, the increase was not due to dumping but to the application of lower, preferential rates of duty. Curiously, most of the complainants in the EC investigation were buyers of bed linen from Pakistan that did not seem to be suffering any loss of profitability. Indeed, most complainants boasted of stable results, e.g. Dewerchin: ‘the company is enjoying even greater success and its bed linen is now positioned at the top end of the range’.13 While such promotional statements cannot constitute formal evidence, it is clear that the steady growth in production of developing country T&C product lines was not at odds with the high-end products manufactured by most of the complainant companies.