Embed Size (px)

Citation preview

World Ethanol & Biofuels 2016

US Ethanol Industry Market Dynamics, Policy Developments and Future Outlook

Neil Koehler, CEO Pacific Ethanol, Inc.

Brussels, BelgiumNovember 8, 2016

2

o 8 strategically located bio‐refineries located in the U.S.

o Production capacity of 515M gallons/yr.

o Current run rate of 1 billion gallons/yr. of marketing volume

o Co‐product production capacity of over 1.5M tons/yr. (dry matter basis)

o Positioned to access 48 states and export markets with ethanol production and

marketing

Mission: To be the leading producer and marketer of low‐carbon renewable fuels

Feedstock procurementEthanol & co‐

product productionMarketing, transportation

& logisticsDistribution & customer

services

Pacific Ethanol, Inc.

History: Founded in 2003, public in 2005 as the first pure‐play ethanol company

Stock Profile a 11/04/16:

• Nasdaq: PEIX

• Trading at $7.25

• Market cap of $313M

3

HQPacific Ethanol PlantsMarketing Partner PlantsTerminals

Pekin, IL100mmgyWet Mill

Pekin, IL60mmgyDry Mill

Aurora, NE110mmgyDry Mill

Boardman, OR40mmgyDry Mill

Burley, ID60mmgyDry Mill

Stockton, CA60mmgyDry Mill

Madera, CA40mmgyDry Mill

Aurora, NE45mmgyDry Mill

Serving Multiple Markets

Recent Highlights:

• Initiated ethanol production from

corn fiber generating D3 cellulosic

RINs in Stockton CA.

• Installing industry first 5MW solar

electric system

• Started up industry first membrane

system to improve efficiency of

dehydration process

4

Fundamentals Support Continued Demand

Gasoline demand in the US market has hit record highs with lower fuel prices, an increase in large vehicle sales

and a strong summer driving season

Source: NYMEX, CBOT, EIA

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

0.00

100.00

200.00

300.00

400.00

500.00

600.00

700.00

800.00

900.00

WTI [USD

/BBL]

CORN [USC/BSH

]

Corn vs. Crude Oil

CBT CORN First Month [USC/BSH]

NYMEX Light Sweet Crude Oil (WTI) Futures Pit (Front Month) [USD/BBL]

8.0

8.2

8.4

8.6

8.8

9.0

9.2

9.4

9.6

9.8

10.0

2‐Jan 2‐Feb 2‐Mar 2‐Apr 2‐May 2‐Jun 2‐Jul 2‐Aug 2‐Sep 2‐Oct 2‐Nov 2‐Dec

Millions BBls per Day

U.S. Motor Gasoline Demand Based on 4‐Wk Average

5‐Year Range 2014 2015 2016

5

Lower Gasoline Prices Increase Demand for Ethanol

Source: INTL FCStone

6

US Largest and Fastest Growing Global Producer of Ethanol

‐ 5.0 10.0 15.0 20.0 25.0 30.0

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Global Ethanol Production (billion gallons)

US Brazil ROW

0

2,500

5,000

7,500

10,000

12,500

15,000

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

p

Million Gallons

The Rapid Growth of US Fuel Ethanol Production

o 211 operating ethanol plantso Installed capacity of 15.7 BGYo 2015 production = 14.7 BGo Estimated 2016 production =

15.2 BGo Producing over 40 million

metric tons of high protein feed per year

o Producing approximately 3 billion lbs. of corn distillers oil

60%

65%

70%

75%

80%

85%

90%

95%

100%

105%

110%

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

2008 Commodity Bubble

2012 U.S. Drought

Record ethanol exports; tax credit expiration

Quarterly Average U.S. Fuel Ethanol Nameplate Capacity Utilization Rates

US Ethanol Market Moving Beyond the “Blend Wall”

9

10

o Export levels are on track to exceed 2015 levels with expectations of nearly 1 billion gallons of exports in 2016

o Global demand is growing 2‐3% annually as global markets incorporate environmental and performance benefits

o Approximately 30 countries have renewable fuel standards or targets

o US ethanol producers supply the world with low‐cost ethanol while sugar prices surge

Source: EIA, Department of Commerce

Exports Create Growing Opportunity

99.6

(100.0)

(50.0)

‐

50.0

100.0

150.0

200.0

Jun‐11 Sep‐11 Dec‐11 Mar‐12 Jun‐12 Sep‐12 Dec‐12 Mar‐13 Jun‐13 Sep‐13 Dec‐13 Mar‐14 Jun‐14 Sep‐14 Dec‐14 Mar‐15 Jun‐15 Sep‐15 Dec‐15 Mar‐16 Jun‐16 Sep‐16

MM Gallons

U.S. Ethanol Export and Import

Import Export Net Export

11Source: EIA

Top Markets for U.S. Ethanol in 2015

Canada249 (30%)

Mexico34 (4%)

Brazil116 (14%)

Oman33 (4%)

Philippines

72 (9%)

Tunisia26 (3%)

Rest of world 12% Total 2015 Export 844 million gallons

India47 (6%)

China 71(8%)

S. Korea 60 (7%)

Netherlands

34 (4%)

Top Markets for U.S. Ethanol in 2016

12

0

20

40

60

80

100

120

140

160

180

200

Brazil Canada China India Korea Mexico Netherlands Peru Philippines UAE ROW

US Ethanol Export by Country (mm gals)

Sum of 2015 Jan‐Sept

Sum of 2016 Jan‐Sept

Source: EIA, Department of Commerce

2016 YTD Export at 694mm gals

Corn Lower Cost than Sugar for Ethanol Production

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

$/lb

CBOT CORN ‐ Sugar Equivalent [USD/LBS] NYMEX No. 11 Sugar First Month [USD/LBS]

13Source: CME

Record Corn Crop Expected in 2016

13,829 14,216

13,601

15,057

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

00‐01 01‐02 02‐03 03‐04 04‐05 05‐06 06‐07 07‐08 08‐09 09‐10 10‐11 11‐12 12‐13 13‐14 14‐15 15‐16 16‐17(P)

Million Bushels

U.S. Corn ProductionFour largest corn crops in history in last four years

Source: USDA, July 2016 WASDE14

171.0

168.4 173.4

50

60

70

80

90

100

110

120

130

140

150

160

170

180

190

75‐76

76‐77

77‐78

78‐79

79‐80

80‐81

81‐82

82‐83

83‐84

84‐85

85‐86

86‐87

87‐88

88‐89

89‐90

90‐91

91‐92

92‐93

93‐94

94‐95

95‐96

96‐97

97‐98

98‐99

99‐00

00‐01

01‐02

02‐03

03‐04

04‐05

05‐06

06‐07

07‐08

08‐ 09

09‐10

10‐11

11‐12

12‐13

13‐14

14‐15

15‐16

16‐17(P)

Bushels/Acre

U.S. Average Corn Yield Continues To Increase

15Source: USDA, July 2016 WASDE

Corn Stocks Projected to Hit 29‐year High

4882

2114

821

12321731

1706

2409

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

75‐76

76‐77

77‐78

78‐79

79‐80

80‐81

81‐82

82‐83

83‐84

84‐85

85‐86

86‐87

87‐88

88‐89

89‐90

90‐91

91‐92

92‐93

93‐94

94‐95

95‐96

96‐97

97‐98

98‐99

99‐00

00‐01

01‐02

02‐03

03‐04

04‐05

05‐06

06‐07

07‐08

08‐ 09

09‐10

10‐11

11‐12

12‐13

13‐14

14‐15

15‐16

16‐17(P)

Million Bushels

U.S. Corn Ending Stocks

Stocks over 2.4 billion bu. for first time since 1987‐88

16Source: USDA, July 2016 WASDE

Corn Prices Projected to Hit 10‐year Low in 2016‐17186

198 232 250

205

200

304

420

406

355

518

622

689

446

370

360

315

0

100

200

300

400

500

600

700

800

00‐01 01‐02 02‐03 03‐04 04‐05 05‐06 06‐07 07‐08 08‐09 09‐10 10‐11 11‐12 12‐13 13‐14 14‐15 15‐16 16‐17(P)

Cen

ts/Bushel

U.S. Season Average Corn Prices

17Source: USDA, July 2016 WASDE

18Source: NYMEX, CBOT, EIA

Ethanol Days of Supply & Spot Margin

Historical crush margin is calculated using formula: OPIS Chicago – (CBOT Corn)/2.8*(1-co product return)-0.2* NYMEX NG

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

15.0

17.0

19.0

21.0

23.0

25.0

27.0

29.0

$/gal

Days of Supply

Days of Supply Crush Margin $/gal

19Source: Renewable Fuels Association.

o Breaching the blend wall

o Only Federal fuels policy to reduce greenhouse gas (GHG) emissions

o Need regulatory certainty to secure development of cellulosic ethanol projects

Renewable Fuel Standard

‐

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Billion Gallons

RFS‐ Conventional Biofuel RFS ‐ Advanced Biofuel Installed Capacity

Industry Production Total Demand Incl. Net Export blend ratio @ 10%

blend ratio @ 15% Domestic Ethanol Demand

RFS: 2017 RVO Proposed Rule

15.00 14.80

1.503.00

2.00

0.69

5.50

0.31

12

13

14

15

16

17

18

19

20

21

22

23

24

Statutory EPA Proposal

Billion Gallons (EtOH Equiv)

2017 RVOs: Statutory Volumes vs. EPA Proposal

Renewale Fuel (D6) Biomass‐based Diesel (D4) Advanced Biofuel (D5) Cellulosic Biofuel (D3)

o In May, EPA released its proposed rule for 2017 Renewable Volume Obligations (RVOs)

o EPA reduced “conventional” renewable fuel to 14.8 BG based on “distribution constraints” andno carry‐over RINs

o Reduced total advanced biofuels to 4.0 BG based on inadequate supply

o Proposed BBD requirement is 2.0 BG (3 billion RINs) vs. 1.0 BG (1.5 billion RINs) required by statute

Total = 18.80

Total = 24.00

20Source: Renewable Fuels Association.

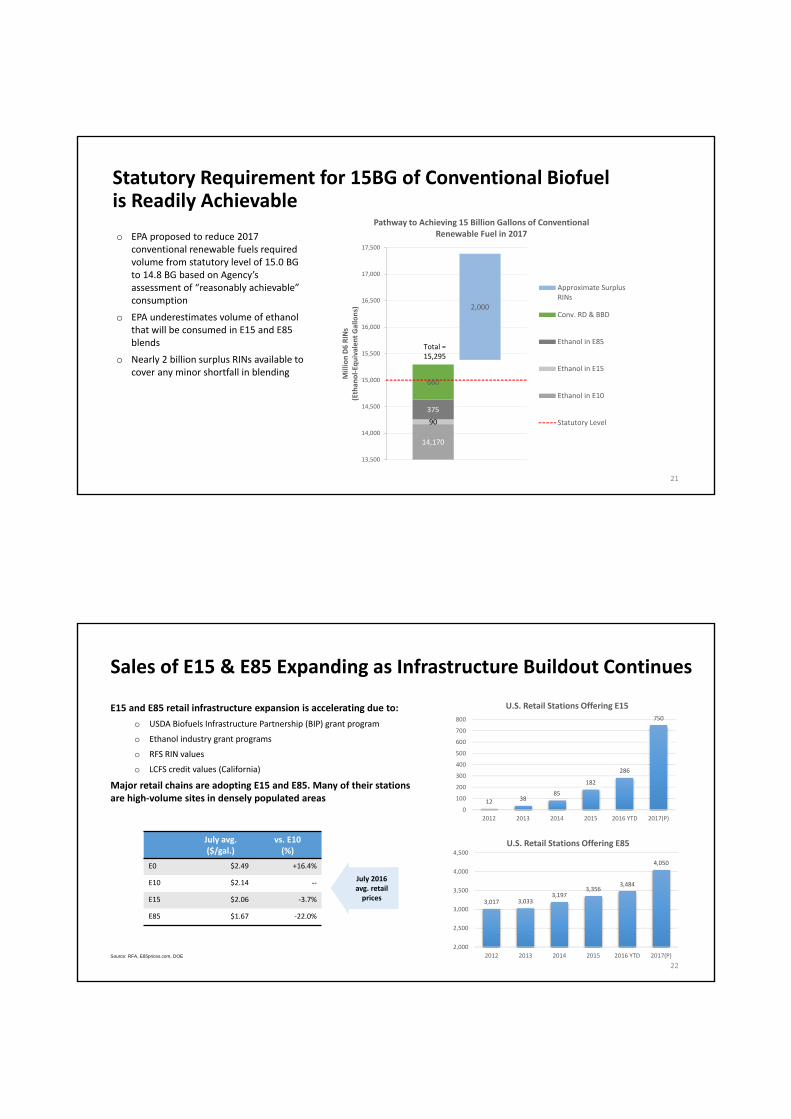

Statutory Requirement for 15BG of Conventional Biofuel is Readily Achievable

o EPA proposed to reduce 2017 conventional renewable fuels required volume from statutory level of 15.0 BG to 14.8 BG based on Agency’s assessment of “reasonably achievable” consumption

o EPA underestimates volume of ethanol that will be consumed in E15 and E85 blends

o Nearly 2 billion surplus RINs available to cover any minor shortfall in blending

21

14,170

90

375

660

2,000

13,500

14,000

14,500

15,000

15,500

16,000

16,500

17,000

17,500

Million D6 RINs

(Ethan

ol‐Eq

uivalen

t Gallons)

Pathway to Achieving 15 Billion Gallons of Conventional Renewable Fuel in 2017

Approximate SurplusRINs

Conv. RD & BBD

Ethanol in E85

Ethanol in E15

Ethanol in E10

Statutory Level

Total = 15,295

Sales of E15 & E85 Expanding as Infrastructure Buildout Continues

12 3885

182

286

750

0

100

200

300

400

500

600

700

800

2012 2013 2014 2015 2016 YTD 2017(P)

U.S. Retail Stations Offering E15

3,017 3,0333,197

3,3563,484

4,050

2,000

2,500

3,000

3,500

4,000

4,500

2012 2013 2014 2015 2016 YTD 2017(P)

U.S. Retail Stations Offering E85

E15 and E85 retail infrastructure expansion is accelerating due to:

o USDA Biofuels Infrastructure Partnership (BIP) grant program

o Ethanol industry grant programs

o RFS RIN values

o LCFS credit values (California)

Major retail chains are adopting E15 and E85. Many of their stations are high‐volume sites in densely populated areas

Source: RFA, E85prices.com, DOE

July avg.($/gal.)

vs. E10(%)

E0 $2.49 +16.4%

E10 $2.14 ‐‐

E15 $2.06 ‐3.7%

E85 $1.67 ‐22.0%

July 2016 avg. retail prices

22

84

85

86

87

88

89

Octane (R+M

)/2

Estimated Hydrocarbon Octane and Octane Boost from Oxygenates in U.S. Refinery‐Produced Gasoline

Pool Octane

Octane Boost from Ethanol

Hydrocarbon Octane

Octane Boost from MTBE

23Source: MathPro

Octane Boost from Ethanol

24

o Slate of crude oil supply and higher demand for premium fuel create octane shortage

o Auto companies calling for higher octane fuels to power next generation of increasingly efficient engines

o Higher blends of ethanol necessary to meet future octane needs

o Opens up new export opportunities as world markets are increasingly octane short

Ethanol Lowest Cost and Cleanest Source of Octane

Source: OPIS

0.00

0.50

1.00

1.50

2.00

2.50Octane Value

((93 Premium ‐ 87 Regular)/6)* (113‐87)

0.00

0.01

0.02

0.03

0.04

0.05Ethanol vs. Alkylate

Gulf Ethanol per Octane Point Gulf Alkylate per Octane Point

0%

5%

10%

15%

20%

25%

Premium Share (%)

Reported 50% Premium 40% Premium 30% Premium

If 30% of premium required or recommended vehicles are fueled with premium

If 50% of premium required or recommended vehicles are fueled with premium

25Source: MathPro

Projected Market Share of Premium Gasoline Resulting from Increased Turbocharging

Internal Combustion Engine (ICE) to Remain as most Dominant Propulsion Technology

26

Table ES‐3 and Figure 3.11 from TAR suggest compliance with 2025 standards will be largely enabled by accelerated

deployment of advanced ICE technologies, along with modest increases in HEV, PHEV, and EV technology.

Draft Technical Assessment Report (TAR) for CAFE/GHG Mid‐term Review Suggests Internal Combustion Engine (ICE) will Remain as most Dominant Propulsion Technology through 2025

Table ES‐3 – Selected Technology Penetrations to Meet MY2025 Standards1

* Data through 2015 includes all turbocharged vehicles, not specifically turbo‐downsized engines

High Octane and Low Carbon Make Ethanol an Attractive Component of Future Fuels

A fuel like E30 “…could help manufacturers who wish to raise compression ratios to improve vehicle efficiency as a step toward complying with the 2017 and later GHG and CAFE standards.”

E20‐E30 offers “ridiculous power and good fuel economy.”

“…a mid‐level ethanol‐gasoline blend (greater than E20 and less than E40) appears to be attractive as a long‐term future fuel for automotive engines in the U.S.”

In optimized engines, E20‐E40 can achieve the same or better

fuel economy as E10

27Source: RFA

28Source: OPIS

o The California Air Resources Board (CARB) re‐adopted the LCFS with the revised program effective Jan. 2016

o Oregon LCFS initiated Jan. 2016 for a 10% reduction in carbon intensity by 2025

o RFS is successful carbon policy at the national level

Pacific Ethanol currently receives a $0.08 per gallon premium over standard Midwest ethanol on each CA

production gallon sold into the CA market

Low‐Carbon Fuel Standards

‐

0.020

0.040

0.060

0.080

0.100

0.120

California Ethanol premium $/gal (CI 69.6)

1%2.0%

3.5%5.0%

7.5%

10.0%

[VALUE]??

0%

5%

10%

15%

20%

25%

2015 2016 2017 2018 2019 2020 2030 E

California LCFS ProgramReduction in Carbon Intensity

Agronomic Improvements Further Reduced Energy Intensity and Carbon Impacts of Feedstock Production

Energy Inputs per Bushel of Corn Produced

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

1991 1996 2001 2005 2010 2015

BTU

/Bushel

Total Energy Use per Bushel of Corn Produced

18.5

12.7

10

12

14

16

18

20

1980 2011

Lbs. CO2e/Bushel

GHG Emissions per Bushel of Corn Produced, 1980‐2011

>40% reduction since 1991

31% reduction between 1980 and 2011

Source: Field to Market 2012 Environmental and Socioeconomic Indicators Report; : Gallagher et al. (USDA, 2016); 2015 extrapolated29

0.0

0.5

1.0

1.5

2.0

2.5

1991 1996 2001 2005 2010 2015

Cu. Ft./Bushel

Natural Gas

0.00

0.02

0.04

0.06

0.08

Gallons/Bushel

Liquid Petroleum Products

0.0

0.2

0.4

0.6

0.8

kwh/Bushel

Electricity

Steady Gains in Ethanol Production Efficiency

30%

7%

32%

8%

0%

5%

10%

15%

20%

25%

30%

35%

40%

2006 2016

Process Technology and Thermal Energy Feedstock Changes, 2006‐2016

Coal Share of ThermalEnergy

Wet Mill Share of TotalCapacity

24

73

0

10

20

30

40

50

60

70

80

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Million Gallons Per Year (m

gy)

Historical Average Ethanol Plant Capacity

20,000

22,500

25,000

27,500

30,000

32,500

35,000

37,500

40,000

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

BTU

/gallon (LH

V)

Thermal Energy Use for Ethanol Production

0.50

0.60

0.70

0.80

0.90

1.00

1.10

1.20

1.30

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

kWh/gallon

Electricity Use for Ethanol Production

New technologies adopted by grain ethanol producers

o Combined heat & power (co‐generation)

o Corn oil extraction

o Selective milling

o Fiber separation

o Advanced enzymes

o Low‐temp fermentation

o Variable frequency drive for valves, fans, pumps

o Membrane separation

o Molecular sieve economizers

o Heat exchangers/transfer

o CO2 capture

o Differential temperature control for DG dryers

o Process water recovery and recycling

o DG cooling enhancement

o 93% natural gas or biogas for process energy

30

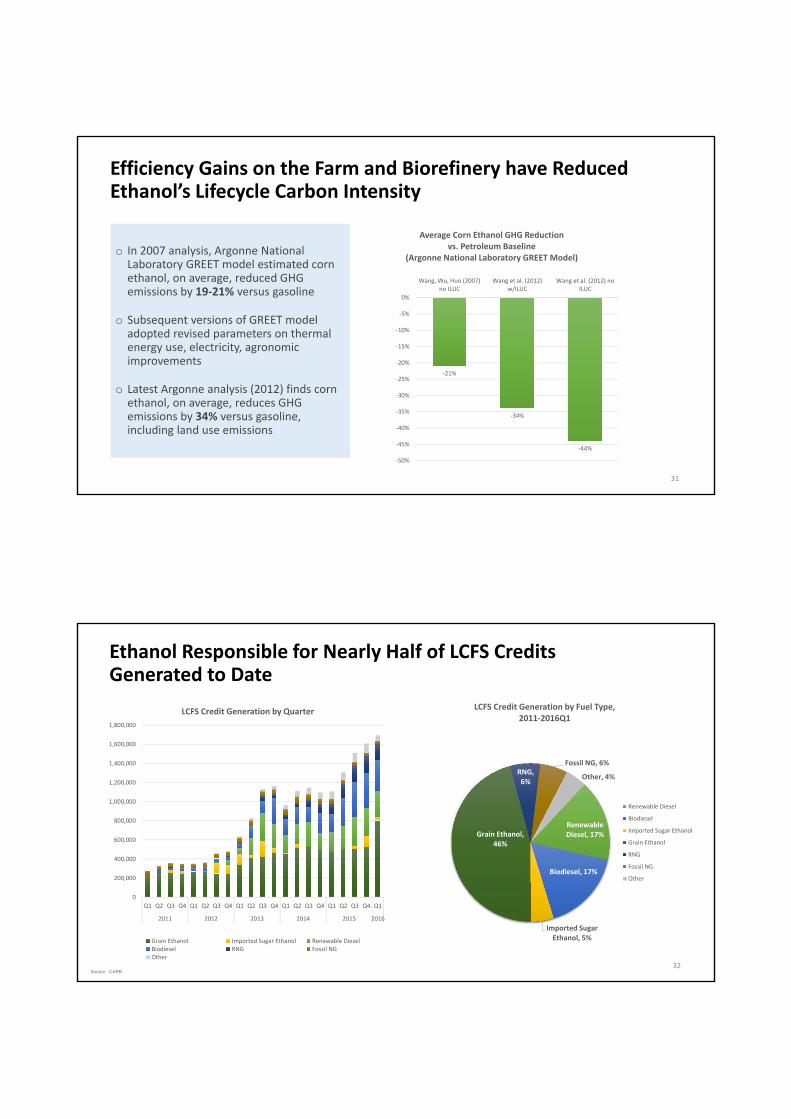

Efficiency Gains on the Farm and Biorefinery have Reduced Ethanol’s Lifecycle Carbon Intensity

‐21%

‐34%

‐44%

‐50%

‐45%

‐40%

‐35%

‐30%

‐25%

‐20%

‐15%

‐10%

‐5%

0%

Wang, Wu, Huo (2007)no ILUC

Wang et al. (2012)w/ILUC

Wang et al. (2012) noILUC

Average Corn Ethanol GHG Reduction vs. Petroleum Baseline

(Argonne National Laboratory GREET Model)o In 2007 analysis, Argonne National Laboratory GREET model estimated corn ethanol, on average, reduced GHG emissions by 19‐21% versus gasoline

o Subsequent versions of GREET model adopted revised parameters on thermal energy use, electricity, agronomic improvements

o Latest Argonne analysis (2012) finds corn ethanol, on average, reduces GHG emissions by 34% versus gasoline, including land use emissions

31

Ethanol Responsible for Nearly Half of LCFS Credits Generated to Date

Renewable Diesel, 17%

Biodiesel, 17%

Imported Sugar Ethanol, 5%

Grain Ethanol, 46%

RNG, 6%

Fossil NG, 6%

Other, 4%

LCFS Credit Generation by Fuel Type, 2011‐2016Q1

Renewable Diesel

Biodiesel

Imported Sugar Ethanol

Grain Ethanol

RNG

Fossil NG

Other

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2011 2012 2013 2014 2015 2016

LCFS Credit Generation by Quarter

Grain Ethanol Imported Sugar Ethanol Renewable DieselBiodiesel RNG Fossil NGOther

32Source: CARB

Conclusions

o Lower oil prices increasing ethanol demand

o High Octane Low Carbon benefits driving growth

o Industry continues to innovate to improve efficiencies and meet environmental performance standards

o US exports support market growth globally

The Future Has Never Been Brighter

THANK YOU

34

![Liquid Fuel Supply (Ethanol and Other Biofuels Mandate ... · PDF file[s 4] Liquid Fuel Supply (Ethanol and Other Biofuels Mandate) Amendment Bill 2015 Page 6 petrol does not include](https://img.dokumen.tips/doc/110x75/5a9dd4a27f8b9ae0108c27e2/liquid-fuel-supply-ethanol-and-other-biofuels-mandate-s-4-liquid-fuel-supply.jpg)