Embed Size (px)

Citation preview

- 1 5900* October 4, 1996

w. " The World Bank

Bangladesh

~~~~~~~ _

... - 0 j I - 1 1 ' 1 ' 4 '

TRADE POLICY REFORM m4"

IMPROWING THE INCENTIVE : 1 c-

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

BANGLADESH

TRADE POLICY REFORM

FOR IMPROVING THE INCENTIVF, RFGIMF

OCTOBER 4, I '96

Private Sector Development and Finance DivisionCountry Department 1South Asia RegionReport No. 1 5900-BD

LIST OF ACRONYMS

BOP - Balance of PaymentsBSIC - Bangladesh Standard Industrial ClassificationCIF - Cost Insurance FreightCD - Customs DutyCL - Control ListCEM - Country Economic MemorandumCV - Coefficient of VariationDEDO - Duty Exemption and DrawNback OfficeEPB - Export Promotion BureauEPZ - Export Processing ZoneGATT - General Agreement on Tariffs and TradeGDP - Gross Domestic ProductGOB - Government of BangladeshHS - Harmonized SystemIDA - International Development AssociationIPO - [mport Policy OrderNBR - National Board Of RevenueNPR - Nominal Protection RateNT'B - Non-Tariff BarrierL/C - Letter of CreditLF - License F'eeMFA - Multi-Fibre ArrangementOTS - Operative Tariff SchedulePBW - Private Bonded WarehousePSI - Pre-Shipment InspectionQRs - Quantitative RestrictionsRMG - Ready-made GarmentsSBW - Special Bonded WarehouseSD - Supplementary Excise DutySITC - Standard Internationial Trade ClassiFicationSRD - Statutory Rate of DutyTOT - Terms of TradeTV - Tariff ValuesUNCTAD - United Nations Commission for Trade and DevelopmentVAT - Value Added Tax

BANGLADESHTRADE POLICY REFORM FOR IMPROVING THE INCENTIVE REGIME

Table of ContentsPage No.

Executive Summary .................................................................. i-ix

CHAPTER 1. WHY TRADE REFORM? ........................................................................................... 1

CHAPTER II. THE CURRENT TRADE REGIME AND ITS IMPACT

Since 1992 import liberalization has reduced statutory levels of protection ........ ........ 3Efforts to streamnline import clearances have been less successful .... . ........................... 6Despite policy changes, smuggling persists ................................................................. 7High effective protection keeps incentives focused on production

for the domestic market and perpetuates inefficiencies ...................................... ....... 9Export promotion schemes provide an enclave setting for the production of exports.. 11Compared with other reforming countries, trade policy reform

in Bangladesh has a way to go .................................................................. 14

CHAPTER III. THE REMAINING AGENDA

Complete the process of trade liberalization ................................................................. 17The fiscal cost of tariff reform can be mitigated

by improving tax administration ................................................................. 2 1Take advantage of the World Trade Organization Framework ............. ....................... 22Follow an effective export promotion strategy ............................................................. 24Reestablish macroeconomic stability ................................................................. '7

CIIAPTER IV. POLICY RECOMMENDATIONS FOR AN EXPORT - ORIENTED ECONOMY

Import liberalization is the most effective wax to promote trade,especially for cxports ................................................................. 28

Adequate infrastructure facilities must be available to reducethe costs of doing business ................... .............................................. 29

Access to trade finance is crucial to spur export diversification,and increase value added in exports ..................... ............................................ 30

Use the WTO to lock in trade reforms . ................................................................. 30Substantial modification of investment incentives and the regulatory environment

can intensify the effect of trade policy reform ......................................................... 31Bangladesh should act quickly to consolidate the gains from policy reform ........ ....... 31

Page No.ANNEXES

1. Trends in Nominal Protection, 1990/91 to 1995/96 ..................................................... 322. Effective Protection Rates: Corden Method FY95/96 ..................................................... 333. Import Composition FY91/92 to FY95/96 ..................................................... 374. The Uruguay Round Agreement: Main Features and Potential Gains .................................. 385. Bangladesh: Schedule of Commitments for WTO ..................................................... 406. List of Participants in Workshop on the Report ..................................................... 43BIBLIOGRAPHY

List of Tables, Figures and BoxesText Tables

2.1 Trends in Nominal Protection, 1990/91 to 1995/96 ..................................................... 52.2 Main Items in Illegal Cross-Border Trade Between Bangladesh and India ........................... 82.3 Bangladesh: Indicators of Effective Protection, 1992-1996 ................................................ 102.4 Competitiveness of Import-Substituting Industries, 1992/93 .............................................. 112.5 Export Processing Zones at a Glance ..................................................... 122.6 Share of Major Exports and their Contribution to Growth .................................................. 132.7 Nominal Protection in South Asia ..................................................... 152.8 International Comparisons of Tariff Rates ..................................................... 162.9 International Comparisons of Nominal Tariffs in Manufacturing ....................................... 16

3J.1 Bangladesh: Customs Duties ..................................................... 213.2 Share of World Exports, Selected Countries, 1972 and 1994 .............................................. 25

Figures

2.1 The Structure of Tariffs. 42.2 Export Diversification: 1982/83 to 1994/95 .14

Boxes

3.1 The Impact of High Tariffs on Exports .18

3.2 Textiles and Garments: Differing Policy Regimes .20

3.3 Using the World Trade Organization as a Precommitment Device .24

This report was prepared by Sona Vanna (Task Manager). Contributing to the report were Charles Draper(SAIPF), Khurshid Alam (SA1BG), Zaid Bakht, Kamil Yilmaz (Consultants), and Zaidi Sattar (Advisor, NationalBoard of Revenue). Surveys on illegal trade were conducted jointly by the Bangladesh Institute of DevelopmentStudies. Dhaka, and the National Council of Applied Economic Research, New Delhi. Meta de Coquereaumont ofAmerican Writing Corporation was the principal editor. Madeline DeVan (SAIPF) also assisted with editing.Tercan Baysan and Charles J. A. Draper provided valuable comments. The report was processed by AnthonyStanley and Soon-Won Pak. The Director is Mieko Nishimizu and the Division Chief is Marilou Uy. PeerReviewers were Messrs. Bernard Hoekman and Neil Roger. The draft report was discussed in a Workshop held inDhaka on August 29, 1996, participated by GOB and IDA officials, Business Leaders, and Academics (Listattached at Annex 6). The Report was subsequently revised by Tercan Baysan and Khurshid Alam taking intoaccount the some of the recommendations from the Workshop.

Executive Summary

1. Many factors--inadequate infrastructure, a poorly-functioning financial system, lack ofskilled labor, amongst others--constrain efficient allocation of resources and increase the cost ofdoing business in Bangladesh. At the same time, the current trade policy regime, characterizedby a highly-dispersed and anomalous import tariff structure, creates an incentive system that isfar from being neutral. The resulting relative prices still maintain a significant anti-export bias,while providing protection to highly inefficient import-substituting activities. An open traderegime resulting from trade reforms helps enhance domestic market competition, reduces pricedistortions arising from projectionist polices so as to bring the domestic relative prices into closeralignment with the international trend prices, induces resource shifts toward activities that showcomparative advantage efficiency in resource allocation, and encourages innovation anddiversification. It also paves the way for the development of a far more diversified and strongexport-base. In short, the trade policy choices Bangladesh's policymakers make will have animportant influence, along with all other pending economic policy and institutional reforms, onthe success of the country's rapid economic growth strategy.

2. While other important and unfinished structural reforms are not covered in detail in thereport, it should be emphasized up-front that the trade policy reforms alone cannot realize the fullextent of gains expected from improvements in the allocation and use of resources. Tradereforms will help enhance domestic market competition, bring domestic relative prices intocloser alignment with the international trend prices, and induce resource shifts toward activitiesthat show comparative advantage. However, dynamic adjustments will be difficult and costlier ifconstraints on supply response are not addressed. Accordingly, acceleration of reforms in otherkey areas such as infrastructure, banking sector, legal and judicial structure, and public enterprisesector are also very crucial.'

3. This report focuses on Bangladesh's foreign trade policy. It reviews the recent reformactions, evaluates the current trade regime and its impact on the economy, and makesrecommendations for a phased, pre-announced reform strategy to push forward with incompletetrade reform. The remaining trade policy reforms pertain to further liberalization of the importregime, mostly involving the elimination of remaining protection-related non-tariff barriers andfurther rationalization of the tariff structure towards low uniform rates. These steps,accompanied by a flexible exchange rate policy, will help foster domestic competition andstrengthen Bangladesh's export-base. Simplifying and reducing the costs of importing will alsohelp boost the confidence of investors, both domestic and foreign.

A detailed coverage and discussion on the pending economic and institutional reform agenda in Bangladesh's keysectors can be found in the following Bank documents: Bangladesh: An Agenda for Action. June 1996;Bangladesh: Government that Works - Reforming the Public Sector. July 1996; Annual Economic Update:Recent Economic Developments and Mediuim-Term Reform Agenda. July 1996.

- 11 -

4. Trade reformn has been an important part of the comprehensive stabilization and reformprogram that Bangladesh has been implementing since 1992. In contrast to the piecemealreforms of the 1 980s, significant steps have been taken during the 1 990s to liberalizeBangladesh's trade regime. In the late 1980s, prohibitive tariffs and quantitative restrictionsresulted in underinvoicing and smuggling. Most tariffs were not binding, and there was a highincidence of "water in the tariff' - tariff redundancy which results from smuggling andprohibitively high tariff rates. In some cases, "statutory" levels of protection were higher than theobserved levels of protection, as measured by the difference between world and domestic prices(for most goods, domestic prices were lower than the tariff-adjusted world prices). And in manyothers, competing imports were of higher quality than their domestically manufacturedsubstitutes since domestic producers often compromised or. quality to keep their prices belowthat of competing imports .

What Has Been Done So Far

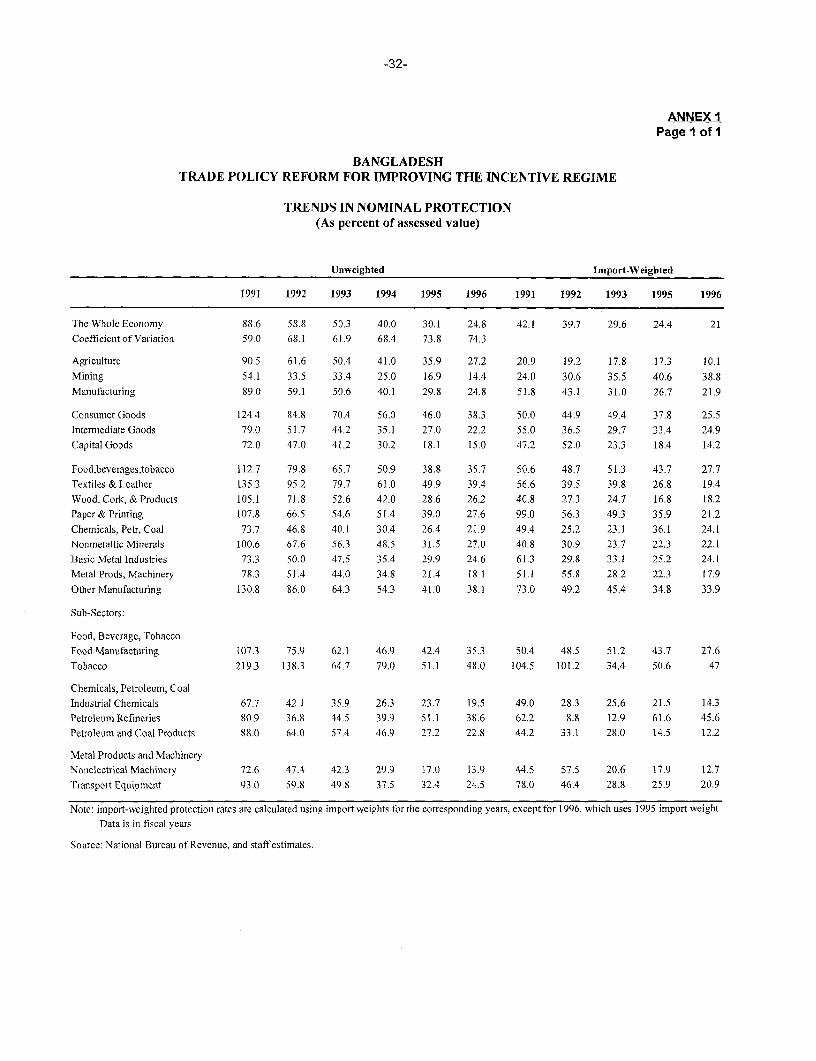

5. A large part of the trade reform effort so far has resulted in reducing the water in thetariff and bringing statutory levels of protection closer to observed levels.2 It has also reducedthe average tariff burden on imports. Average nominal protection, measured as the average of allimport duties and protective taxes, has fallen from 89 percent in 1990/91 to 25 percent in1995/96 (Table 1). However, nominal protection, as measured by import-weighted averageprotection rates, has declined since 1990/91, but by much less (21 percentage points) than thedecline in unweighted average protection rates (64 percentage points). The practice of grantingtariff concessions and exemptions based on end-use has slowed the move toward simplificationof the tariff schedule.

6. Other reforns have steadily dismantled a complicated structure of import controls,though a crucial industry, textiles, remains protected. A voluntary preshipment inspectionscheme supplements the use of rigid tariff values for import valuation.

7. As a result of such reforms, effective protection has decreased for most industries since1992. But because effective rates of protection for the steel and engineering and food and dairyindustries increased significantly, aggregate effective protection fell only 15 percent between1992 and 1995. When steel and engineering and food and dairy are excluded, the aggregateeffective protection rate shows a 48 percent decline. Observed average effective protection ratesindicate that trade policy reform has not shifted incentives firmly towards the production ofexportables.

2 As indicated by the difference between world and domestic prices.

- 111 -

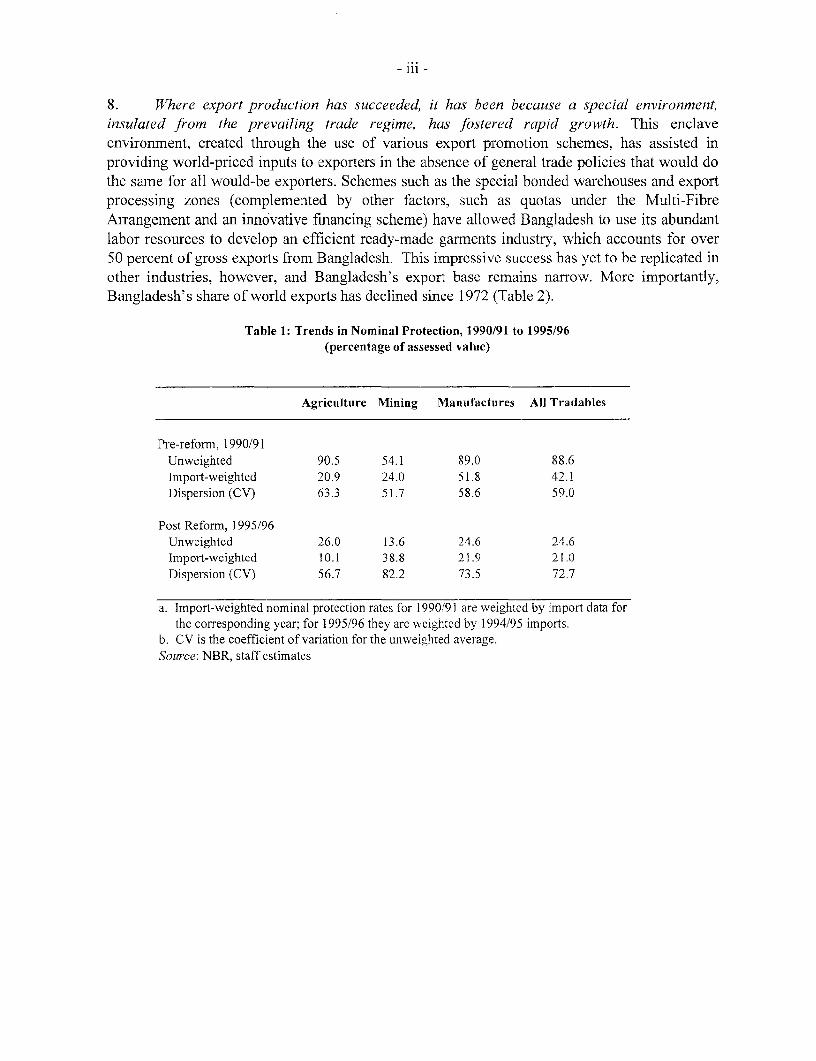

8. WVhere export production has succeeded, it has been because a special environment,insulated from the prevailing trade regime, has fostered rapid growth. This enclaveenvironment, created through the use of various export promotion schemes, has assisted inproviding world-priced inputs to exporters in the absence of general trade policies that would dothe same for all would-be exporters. Schemes such as the special bonded warehouses and exportprocessing zones (complemented by other factors, such as quotas under the Multi-FibreArrangement and an innovative financing scheme) have allowed Bangladesh to use its abundantlabor resources to develop an efficient ready-made garments industry, which accounts for over50 percent of gross exports from Bangladesh. This impressive success has yet to be replicated inother industries, however, and Bangladesh's export base remains narrow. More importantly,Bangladesh's share of world exports has declined since 1972 (Table 2).

Table 1: Trends in Nominal Protection, 1990/91 to 1995/96(percentage of assessed value)

Agriculture Mining Manufactures All Tradables

Pre-reform, 1990/91Unweighted 90.5 54.1 89.0 88.6Import-weighted 20.9 24.0 51.8 42.1Dispersion (CV) 63.3 51.7 58.6 59.0

Post Reform, 1995/96Unweighted 26.0 13.6 24.6 24.6Import-weighted 10.1 38.8 21.9 21.0Dispersion (CV) 56.7 82.2 73.5 72.7

a. Import-weighted nominal protection rates for 1990/91 are weighted by import data forthe corresponding year; for 1995/96 they are weighted by 1994/95 imports.

b. CV is the coefficient of variation for the unweighted average.Source: NBR, staff estimates

- iv -

Table 2: Falling Behind... Bangladesh's Share in World Exports,Selected Countries (percent)

Country 1972 1994

China 0.95 2.81Indonesia 0.46 0.94Thailand \a 0.28 0.87Mexico 0.43 0.81Turkey \a 0.23 0.36Sri Lanka 0.09 0.08Bangladesh 0.09 0.06Ghana \b 0.11 0,02Kenya 0.09 0.04Nepal'\a 0.01 0.01Philippines 0.28 0.45Vietnam \b 0.00 0.04a\ 1993b\ 1989Source: IMF, International Financial Statistics

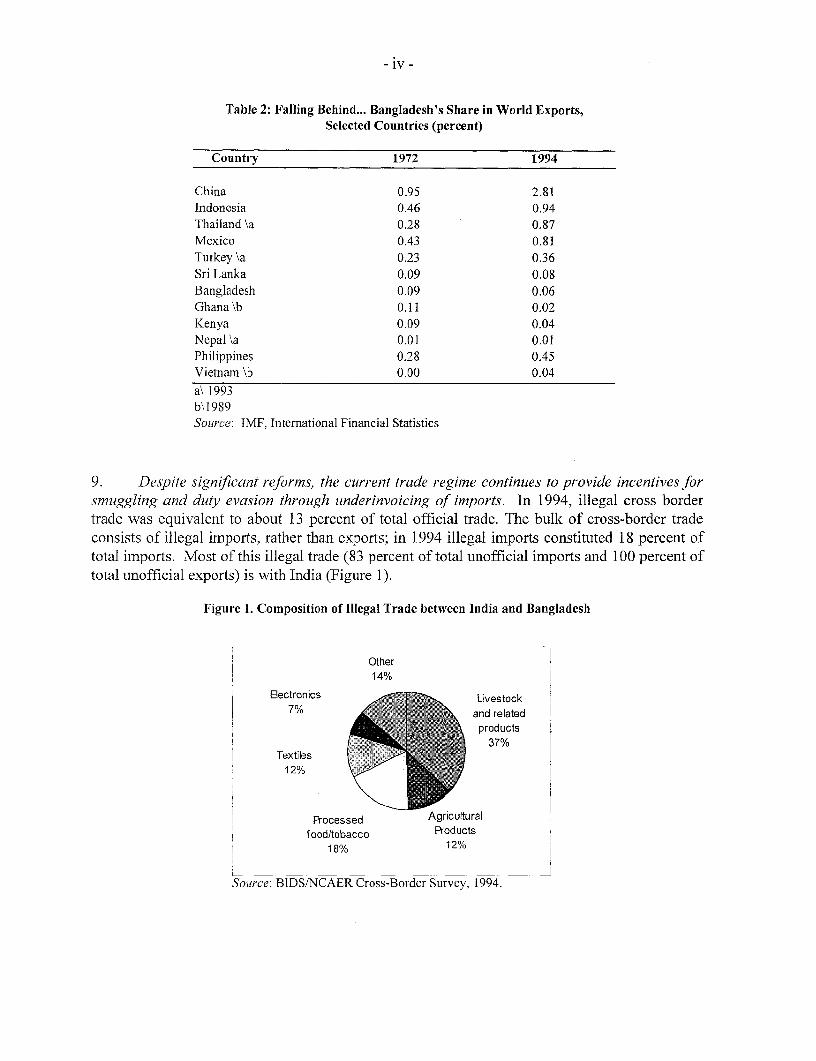

9. Despite significant reforms, the current trade regime continues to provide incentives forsmuggling and duty evasion through underinvoicing of imports. In 1994, illegal cross bordertrade was equivalent to about 13 percent of total official trade. The bulk of cross-border tradeconsists of illegal imports, rather than exports; in 1994 illegal imports constituted 18 percent oftotal imports. Most of this illegal trade (83 percent of total unofficial imports and 100 percent oftotal unofficial exports) is with India (Figure 1).

Figure 1. Composition of Illegal Trade between India and Bangladesh

Other14%

Electronics Livestock7 %and related

37%Textiles

Processed Agriculturalfood/tobacco roducts

18% 12%

Source: BIDS/NCAER Cross-Border Survey, 1994.

- v -

10. Compared with other reforming countries, Bangladesh has a long way to go in its tradepolicy reform. In South Asia, Sri Lanka has compressed tariffs into three bands and plans tomove to a low, uniform tariff soon. In Latin America and the Caribbean in 1993, Chile had auniform tariff rate, the Central American countries had only four rates, Jamaica had five, andUruguay had three. Most East Asian economies have also significantly reduced tariffs in an effortto boost exports. In Africa, Ghana adopted a three rate regime in 1993 (Table 3).

Table 3: Many Reformers have Lower Tariffs than Bangladesh(average unweighted tariffs, percent)

Bangladesh (1996) 25Sri Lanka (1995) 10.3 \aArgentina (1992) 12.2Chile (1991) 1 iPeru (1992) 17Malaysia (1993) 14Ghana (1993) 17a\ Denotes tariff collection rateSource: World Bank staff estimates

What To Do Next

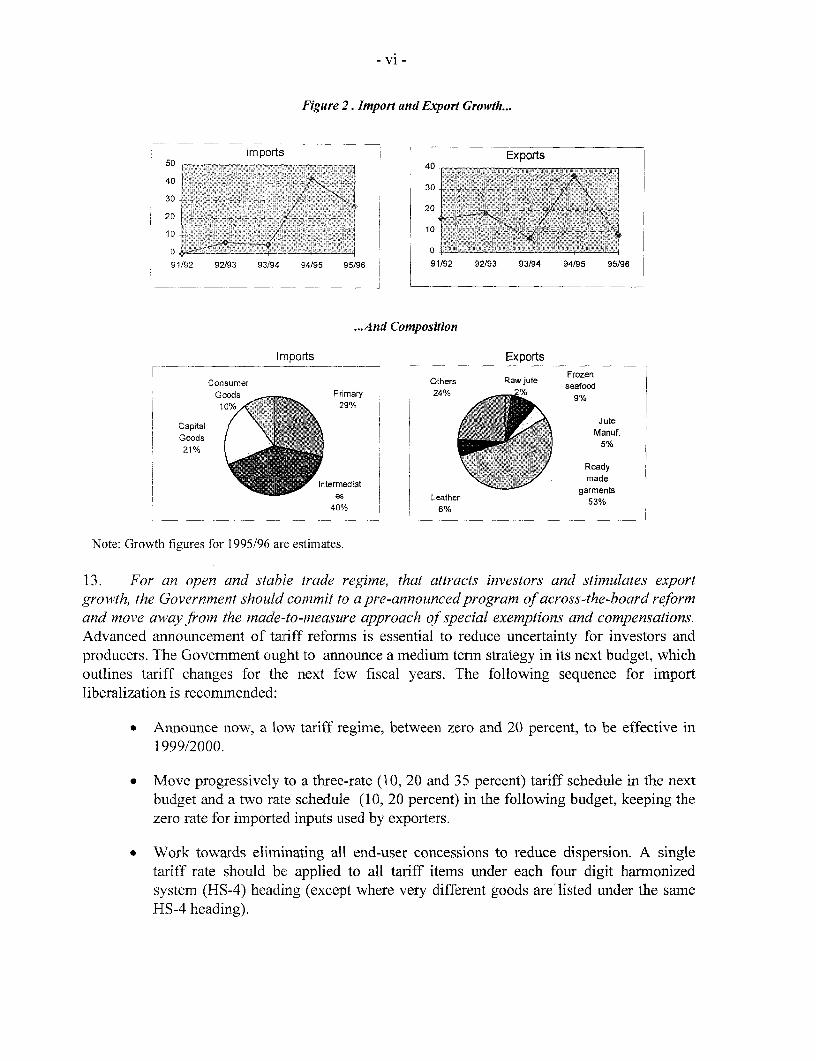

11. Bangladesh has made a good start. Significant export and import growth in 1994/95,suggest that trade reforms, coupled with relative macro stability and overall growth in theeconomy, may be evoking a supply response from the private sector (Figure 2). To sustain andstrengthen this response, Bangladesh should complete the crucial remaining items on the tradereform agenda. This agenda should focus on import liberalization, while maintaining theefficiency of current export promotion schemes. To signal private investors of Bangladesh'ssteadfast commitment to a liberalized trade regime, Bangladesh should adopt many provisions ofthe recently concluded Uruguay Round agreement.

12. Import liberalization is the most effective way to promote trade, especially of export, andtariff reform is the most critical element of import liberalization. The Government has madegood progress in reducing tariffs. Now progress is needed in establishing more uniform rates ofprotection, by compressing the number of tariff rates to reduce dispersion and simplify theregime. A major source of tariff dispersion is the continued use of tariff concessions for end-users, which should be phased out.

- vi -

Figure 2. Import and Export Growth...

Imports I Exports50- 40SD 1 40

40 t 1- 0 9 j ; 9 ,, 9 9

- ~~~~~~~~~~~~3030 -- 20

20

0 0 1

91/92 91/92 92/93 93/94 94/95 95/96

...And Composition

Imports Exports7 Frozen

Consumer Others Raw jute seafoodGoods ~~~Primary 24% % 9%

Capital J uteGoods sr.cmtap-n cdoa Manuf.21% 5/

¶~~~f ~~Readypdtermrediat T made

liberalization isreco:garmentsLeather ~~~53%

400/ 6%

Note: Growth figures for 1995/96 are estimates.

13. For an open and stable trade regime, that attracts investors and stimulates exportgrowth, the Government should commit to a pre-announced program of across-the-board reformand move away from the made-to-measure approach of special exemptions and compensations.Advanced announcement of tariff reforms is essential to reduce uncertainty for investors andproducers. The Government ought to announce a medium term strategy in its next budget, whichoutlines tariff changes for the next few fiscal years. The following sequence for importliberalization is recommended:

* Alnnounce niow, a low tariff regime, between zero and 20 percent, to be effective in1999/2000.

* Move progressively to a three-rate (10, 20 and 35 percent) tariff schedule in the nextbudget and a two rate schedule (10, 20 percent) in the following budget, keeping thezero rate for imported inputs used by exporters.

* Work towards eliminating all end-user concessions to reduce dispersion. A singletariff rate should be applied to all tariff items under each four digit harmonizedsystem (HS-4) heading (except wvhere very different goods are listed under the sameHS-4 heading).

- vii -

Unify the statutory rates of duty and the operative rate to avoid complicating theschedule, and also to avoid any chance of backsliding on the reforrrm process.

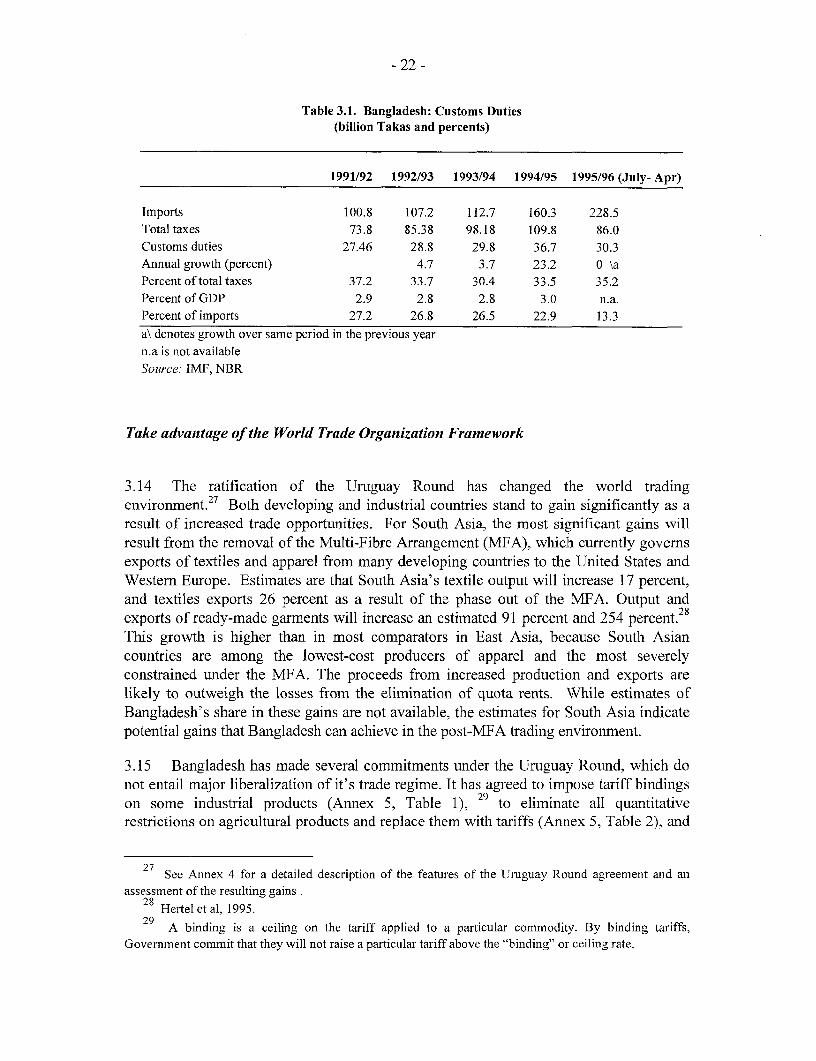

14. Fears of large tax revenue losses have been key factors in holding up rapid reductions intariffs. This is an understandable concern in Bangladesh given the importance of tax revenuescollected on imports. Currently, customs duties account for over 33 percent of NBR-administered taxes, with VAT and supplementary duty collected on imports accounting for 23percent and 3 percent, respectively. Obviously, it is important to speed up the unfinisheddomestic tax reform, focusing on the expansion of VAT and income tax nets, while intensifyingefforts aimed at strengthening the NBR. Improvements on the domestic tax front, includingefficiency of the tax machinery, need to be achieved both to pave the way for further importtariff liberalization as well as to strengthen Government's fiscal base. However, it should also beadded that import tax revenue collections also depend, in addition to the tax/duty rates, onshort/long-term price and income elasticities of imports, economic growth and technologychanges - given international prices and abstracting from shocks. All these factors could morethan offset the effect of tariff cuts on tax revenue collections. Indeed, this has been the case inBangladesh in recent years. When tariffs were reduced in 1994-95, imports increased 39 percentin dollar terms, and that import tax revenue increases more than compensated for lower tariffs.And the surge in imports and customs revenue continued into 1995/96, despite congestion at theport of Chittagong and a difficult political situation. As a rough estimate, reducing import-weighted tariffs to half their present level could potentially reduce customs duties by Taka 19billion. If macroeconomic stability is maintained and the economy continues to grow, revenuelosses from further tariff reductions should be offset by increased volume of imports.

15. Quantitative restrictions, especially on textiles, are preventing the development ofbackward linkages with the ready-made garment sector. If these restrictions are removed,protection due to nontariff barriers will virtually disappear in Bangladesh. This would spur thedevelopment of a textile sector that could potentially supply the needs of the ready-made garmentindustry, which now imports more than 90 percent of its textile inputs. Bans on import of sugar,salt, and some other commodities are somewhat meaningless because large amounts of thesecommodities are imported illegally from India. Removing these restrictions would expose theseindustries to greater competition, generate tariff revenues, and benefit consumers by reducingprices.

16. The trade liberalization agenda will not be complete without strengthening importvaluation and clearance. Tariff values, used in import valuation should be phased out; a welldesigned pre-shipment inspection scheme can be used until Bangladesh can rely on invoiceprices as accurate measure of value. Mandatory pre-shipment inspection avoids a number ofproblems being currently faced by the voluntary system. The Govcrnment recently introducedcomputerized customs assessment using the UNCTAD-developed SPEED system at Chittagongport and Dhaka airport, but design and implementation problems have kept the system fromfunctioning smoothly. A review and adjustment of the system, to get it operating correctly, isnecessary to complete computerization of import clearance. The Operative Tariff Scheduleshould be published regularly to ensure transparency of the tariff regime.

- viii -

17. The program for import liberalization should take top priority in the Government'sstrategy for trade reforn. Until this liberalization process is complete, however, exportpromotion schemes must be made as effective as possible to reduce disincentives for exporting.The following measures are recommended:

* Overcome the obstacles to making special bonded warehouses available for mosttypes of export industry and further develop the scheme so that it can be used byestablished firms serving both home and domestic markets.

- Consolidate the progress made in developing export processing zones to ease theireventual integration with the regular economy. Private investment in new estates canplay a useful role.

* Resumne improvements in the functioning of the Duty Exemption and DrawbackOffice, produce new and revised flat rates for duty rebates, make partial, occasional,and indirect exporters eligible for duty rebates, and implement the recent decision toinvolve banks in paying the rebates.

* Remove implementation bottlenecks of export promotion schemes reflected ingovernment's policy declaration, e.g. that of allowing export oriented industry to sellpart of their product (I 5-20 percent) in the domestic market after paying of all taxesand duties.

18. Adequate infrastructure facilities should be available to reduce the costs of doingbusiness. Production activities are hampered by Bangladesh's pervasive infrastructurebottlenecks. Unless addressed urgently, these problems will continue to be serious constraint torapid economic growth. Infrastructure facilities are satisfactory only in export processing zones,encouraging export development in enclaves. For sustained growth in exports, all prospectiveexporters must have access to power, telecommunications, and other infrastructure, and toimproved port facilities that expedite the clearance process for both imports and exports. Thefollowing measures are recommended:

* Set up an inland container depot at Chittagong and expand Mongla port. Considerprivate participation in the inland container depots, private container stuffing anddestuffing centers, and the leasing of container berths to private operators.

* Lift the air cargo monopoly currently enjoyed by Biman to bring competition intothe air cargo industry and improve services.

19. Access to trade finance is crucial to spur export diversification, and increase value addedin exports. In the long run, the development of an efficient banking system will relieveconstraints in trade finance. Over the short run, however, a few steps can be taken to increaseexporter's access to trade finance. They are:

- ix -

* Discontinue such outdated practices as the compulsory back-to-back usance importletters of credit; let exporters be free to choose between them and other forms offinancing.

* Continue a dollar line of credit at Bangladesh Bank to isolate pre-shipment exportcredit from thc inefficiencies of the banking system.

* Remove the interest rate ceiling on export loans, which have denied small-scaleexporters access to finance.

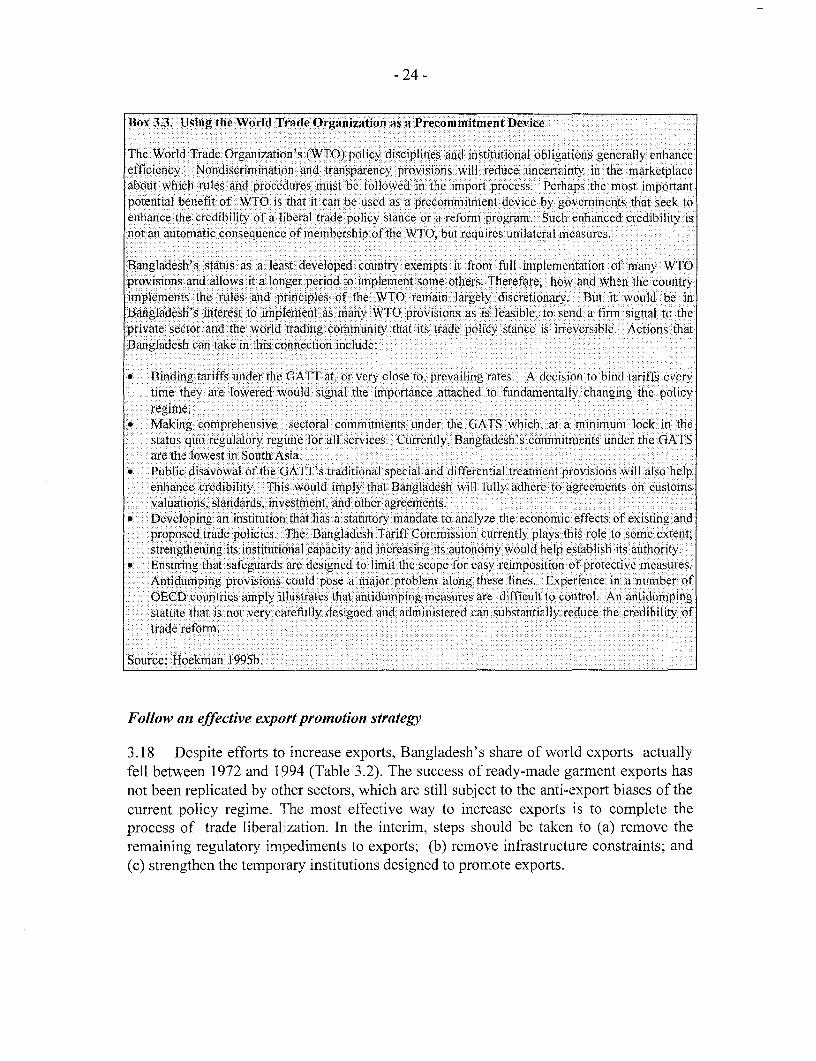

20. The Government can use the WVorld Trade Organization to facilitate and lock in tradereforms. Bangladesh's commitments at the WTO can serve as a precommitment device for futurepolicy change and will be useful for achieving credibility with investors, both domestic andforeign. To this end, Bangladesh should:

* Bind its tariffs at operative rates.

* Further develop the Tariff Commission as a transparency institution that advises ontariff policy changes.

* Ensure that safeguards mechanisms are designed to minimize the scope for an easyreimposition of protection.

21. Substantial modification of investment incentives and the regulatory environment canintensify the effect of trade policy reform. The current corporate tax system, the remnants of pastcontrols on investment and foreign exchange, and inadequacies in the legal framework increasethe cost of doing business in Bangladesh, and also reduce the incentives for foreign investment.These shortcomings can be remedied relatively quickly, particularly compared with the time itwill take to improve inefficient utility services and inadequate infrastructure. By clearing mostof the policy hurdles the Government will be able to provide incentives for investment that canbalance the additional costs due to the deficiencies in infrastructure.

22. Bangladesh should act quickly to consolidate the gains from policy reform and forgeahead. International experience demonstrates that successful trade reforms proceed on a well-paced, pre-announced schedule, give priority to the reduction of tariff and nontariff barriers toimports, and are accompanied by flexible exchange rate management and prudentmacroeconomic policies. Bangladesh has largely followed this path. While the pace of changehas been slow, policy reform has picked up momentum in the last few years. Early results showthat these changes have elicited a significant supply response. Bangladesh must act quickly toremove the remaining hurdles to trade, in order to move the economy firmly onto the path ofoutward-oriented development and rapid economic growth.

- 1 -

1. WHY TRADE REFORM?

Trade policy reform is essential for efficient resource allocation and an outward-orienteddevelopment strategy

1.1 Bangladesh has adopted an export-oriented strategy of growth. If implementedsuccessfully, this strategy would increase domestic investment, attract much-needed foreigninvestment, create millions of jobs, and reduce poverty. Many factors--inadequateinfrastructure, a poorly-functioning financial system, lack of skilled labor, amongst others--constrain efficient allocation of resources and increase the cost of doing business in Bangladesh.At the same time, the current trade policy regime, characterized by a highly-dispersed andanomalous import tariff structure, creates an incentive system that is far from being neutral. Theresulting relative prices still maintain a significant anti-export bias, while providing protection tohighly inefficient import-substituting activities. An open trade regime resulting from tradereforms helps enhance domestic market competition, reduces price distortions arising fromprojectionist polices so as to bring the domestic relative prices into closer alignment with theinternational trend prices, induces resource shifts toward activities that show comparativeadvantage efficiency in resource allocation, and encourages innovation and diversification. It alsopaves the way for the development of far more diversified and strong export-base. In short, thetrade policy choices Bangladesh's policy makers make will have an important influence, alongwith all other pending economic policy and institutional reforms, on the success of the country'srapid economic growth strategy.

1.2 While other important and unfinished structural reforms are not covered in detail in thisreport, since focus here is primarily on Bangladesh's foreign trade policy, it should beemphasized up-front that the trade policy reforms alone cannot realize the full extent of gainsexpected from improvements in the allocation and use of resources. However, dynamicadjustments will be difficult and costlier if constraints on supply response are not addressed.Accordingly, acceleration of reforms in other key areas such as infrastructure, banking sector,legal and judicial structure, and public enterprise sector are also very crucial.l

1.3 Trade policy reform has been an important part of the comprehensive stabilization andreform program that Bangladesh has been implementing since 1992. Early reforms resulted incommendable macroeconomic stability and internal and external balance. All macroeconomicindicators showed marked improvement between FY1990 and FY1994: the fiscal deficit wentfrom 7.7 percent in FY1990 to 5.9 percent in FY1994, the current account deficit from 6.9percent of GDP to 1.4 percent, and foreign exchange reserves from 1.9 months of imports to 8.2

A detailed coverage and discussion on the pending economic and institutional reform agenda in Bangladesh's keysectors can be found in the following Bank documents: Bangladesh: An Agenda for Action. June 1996;Bangladesh: Government that Works - Reforming the Public Sector. July 1996; Annual Economic Update:Recent Economic Developments and Medium-Term Reform Agenda, July 1996.

months. There has been some deterioration during FY1995 and FY1996, however, largely due toeconomic disruptions resulting from political tensions.

Macroeconomic stability alone cannot ensure rapid growth

1.4 Though an essential foundation for growth, macroeconomic stability alone will not resultin faster growth, as Bangladesh's recent experience demonstrates. To achieve sustained increasesin economic growth, macroeconomic stability must be complemented by effective structuralreforms in such areas as the financial sector, legal reform, infrastructure, and energy. Most ofthese reforms are difficult and politically sensitive. Trade policy reform, the bulk of whichconsists of liberalizing imports, is perceived to be relatively easier to implement.2 By reducingthe bias against exports, trade policy reform should be very effective in spurring investment, bothdomestic and foreign, in export-oriented sectors. A large share of investment in Bangladesh willcome from foreigners looking to produce exports for the world market. The Government canstrengthen the confidence of these investors by accelerating trade policy reform and announcingin advance the schedule of policy changes so that new investors can select projects sensibly andenterprises can plan any necessary restructuring.

1.5 This report reviews and analyzes trade policy reform in Bangladesh since 1992 andattempts to put into perspective the major policy issues affecting trade. It evaluates the currenttrade regime and its impact on the economy, and makes recommendations for a phased pre-announced near-term reform strategy, to accelerate completion of the remaining trade reformagenda, remove distortions in the import regime, and enhance export competitiveness. Theremaining trade policy reforms pertain to further liberalization of the import regime, mostlyinvolving the elimination of remaining protection-related non-tariff barriers and furtherrationalization of the tariff structure toward a single and low uniform rate. These steps,accompanied by a flexible exchange rate policy, will help foster domestic competition andstrengthen Bangladesh's export-base. Simplifying and reducing the costs of importing will alsohelp boost the confidence of investors, both domestic and foreign.

Though trade reform prescriptions are perceived to be relatively easier to implement, in Bangladesh it may berestrained by the perception prevailing in some quarters of the government and the business community thatBangladesh has already liberalized faster than its neighbors, thereby increasing ratio of risks to returns forindustries here.

-3 -

2. THE CURRENT TRADE REGIME AND ITS IMPACT

2.1 By the late 1980s, despite some efforts at reform, Bangladesh's trade policies hadresulted in a trade regime with prohibitively high tariffs and quantitative restrictions that fosteredsmuggling, particularly along the long, porous border with India. As a result, most tariffs werenot binding, as is evidenced by the fact that domestic prices for most goods were lower than thetariff-adjusted world prices.3 A 1992 survey revealed that in some cases "statutory" protection,calculated from the tariff regime, was higher than the observed protection measured by thedifference in world and domestic prices. And in many others, competing imports were of higherquality than their domestically manufactured counterparts since domestic producers oftencompromised on quality to keep their prices below that of competing imports.

Since 1992 import liberalization has reduced statutory levels of protection

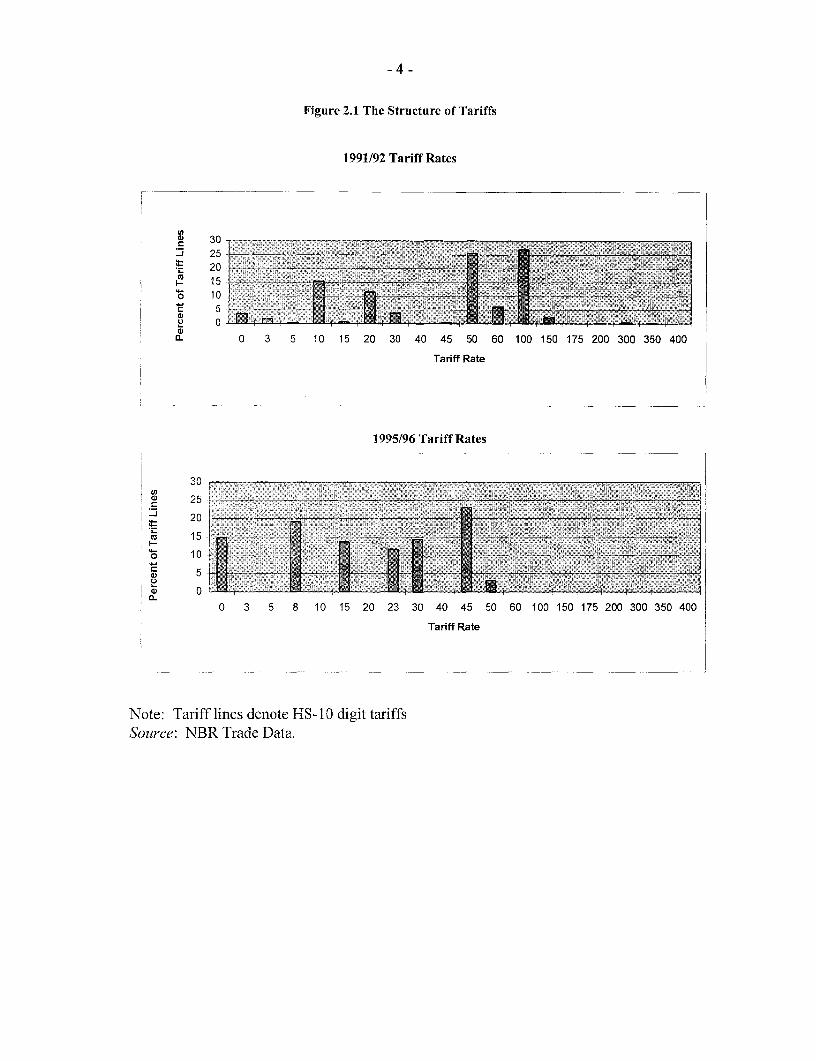

2.2 In contrast to the piecemeal and partial reforms of the 1980s, significant steps have beentaken since 1992 to liberalize Bangladesh's trade regime. The reforms have reduced the "water inthe tariffs", bringing statutory levels of protection closer to observed levels. The import-discriminating, multiple rate sales tax was replaced by a 15 percent value added tax levied onboth imports and domestically produced goods. Regulatory duties and surcharges on importswere replaced by a supplementary excise duty, a trade-neutral consumption tax. Tariffs werereduced in each successive budget, and some exemptions based on end-use were eliminated,resulting in some compression of the tariff structure (Figure 2. 1).5

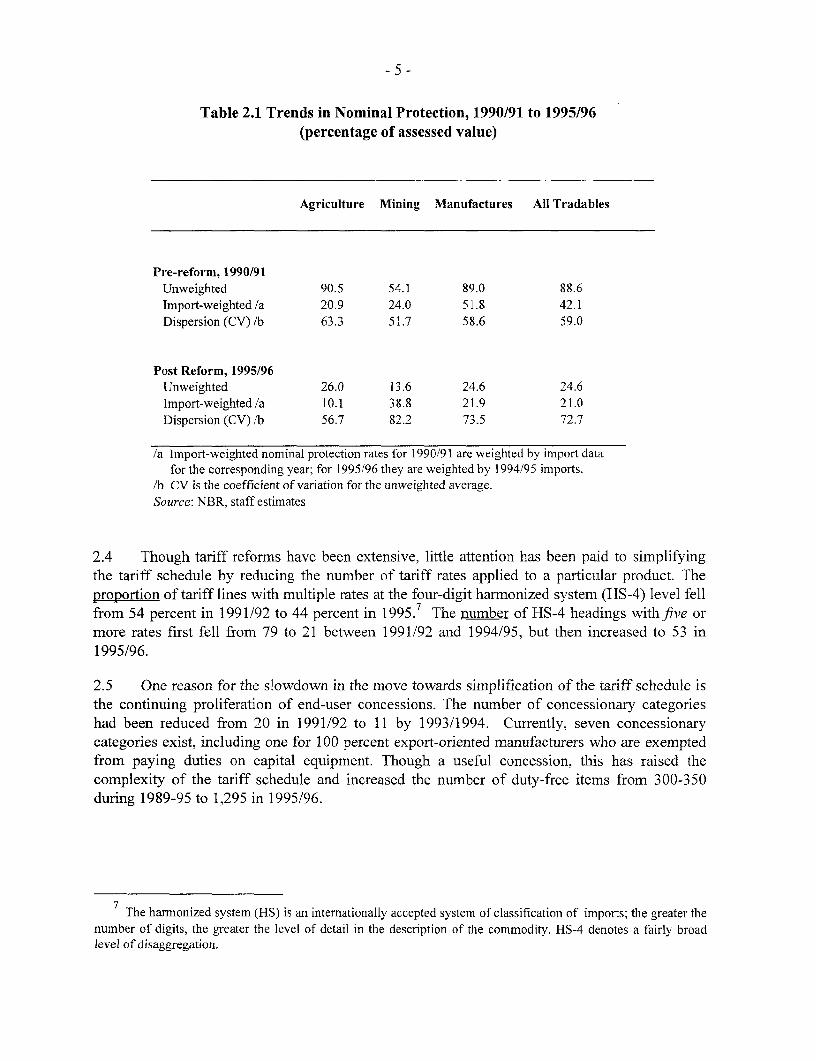

2.3 As a result of these sustained efforts, average nominal protection, including all importduties and protective taxes, fell from 89 percent in 1990/91 to 25 percent in 1995/96, a drop of 64percentage points (Table 2.1). The import-weighted average protection rate, fell by 21 percentagepoints. The import-weighted average protection rate for the manufacturing sector fell even morethan the overall average--about 30 percentage points--the rate rose for mining-- by 15 percentagepoints--mainly because tariffs on petroleum, oil, and lubricants were changed from specific ratesto ad valorem rates in 1993/94. 6 (For a more detailed breakdown of nominal protection rates, seeAnnex 1).

3 See Bakht, 1995.

Tariff redundancy resulting from smuggling and prohibitively high tariff rates.

Unlike many other countries, end-user exemptions are listed in the Bangladesh tariff schedule

6 Prior to 1994195, petroleum, oil and lubricants were taxed at Taka 5,000 per metric ton, in 1993/94, thisspecific rate was replaced by an ad valorem tariff of 45 percent of import value.

- 4 -

Figure 2.1 The Structure of Tariffs

1991/92 Tariff Rates

30 c=> 25 -

20i-D 15

u 0

IL 0 3 5 10 15 20 30 40 45 50 60 100 150 175 200300 350 400

Tariff Rate

1995d96 Tariff Rates

Source: N 77r77777Data.

20

0 10

0 3 5 8 10 15 20 23 30 40 45 50 60 100 150 175 200 300 350 400

Tariff Rate

Note: Tariff lines denote HS- I 0 digit tariffsSource: NBR Trade Data.

- 5 -

Table 2.1 Trends in Nominal Protection, 1990/91 to 1995/96(percentage of assessed value)

Agriculture Mining Manufactures All Tradables

Pre-reform, 1990/91Unweighted 90.5 54.1 89.0 88.6Import-weighted /a 20.9 24.0 51.8 42.1Dispersion (CV) /b 63.3 51.7 58.6 59.0

Post Reform, 1995/96Unweighted 26.0 13.6 24.6 24.6Import-weighted /a 10.1 38.8 21.9 21.0Dispersion (CV) /b 56.7 82.2 73.5 72.7

/a Import-weighted nominal protection rates for 1990/91 are weighted by import datafor the corresponding year; for 1995/96 they are weighted by 1994/95 imports.

/b CV is the coefficient of variation for the unweighted average.Source: NBR, staff estimates

2.4 Though tariff reforms have been extensive, little attention has been paid to simplifyingthe tariff schedule by reducing the nurnber of tariff rates applied to a particular product. Theproportion of tariff lines with multiple rates at the four-digit harmonized system (HS-4) level fellfrom 54 percent in 1991/92 to 44 percent in 1995.7 The number of HS-4 headings with five ormore rates first fell from 79 to 21 between 1991/92 and 1994/95, but then increased to 53 in1995/96.

2.5 One reason for the slowdown in the move towards simplification of the tariff schedule isthe continuing proliferation of end-user concessions. The number of concessionary categorieshad been reduced from 20 in 1991/92 to 11 by 1993/1994. Currently, seven concessionarycategories exist, including one for 100 percent export-oriented manufacturers who are exemptedfrom paying duties on capital equipment. Though a useful concession, this has raised thecomplexity of the tariff schedule and increased the number of duty-free items from 300-350during 1989-95 to 1,295 in 1995/96.

The harmonized system (HS) is an internationally accepted system of classification of imports; the greater thenumber of digits, the greater the level of detail in the description of the commodity. HS-4 denotes a fairly broadlevel of disaggregation.

- 6 -

2.6 Thus tariff dispersion, as measured by the coefficient of variation, has remained high.8 (Ingeneral, the greater the number of tariff rates per item, the higher the coefficient). The majorreduction in import taxes in 1991/92 actually resulted in an increase in the coefficient ofvariation from 59 to 68 percent. In 1992/93 the compression of customs duty rates and theremoval of two concessionary categories reduced the coefficient of variation to 62 percent. By1995/96, however, the coefficient of variation had risen to 74 percent because low tariff rates,rather than high rates, were decreased.

2.7 Progress has also been made in reducing quantitative restrictions. A complicated structureof import controls has been steadily dismantled, although a crucial subsector, textiles, remainsprotected and reductions have occurred unevenly across commodity groups and sectors. Ingeneral, restrictions on domestically produced goods have been removed more slowly than thoseon other goods, and restrictions on manufacturing goods have been lifted more slowly than thoseon agricultural goods. In manufacturing, controls on consumer goods have been more stringentthan those on intermediate and capital goods. Currently, the textiles sector enjoys the heaviestprotection from quantitative restrictions; almost 25 percent of all eight-digit harnonized systemlines in textiles are under quantitative restrictions. By comparison, barely two percent of tarifflines overall are now subject to trade-related quantitative restrictions. Import bans are in place onall woven fabrics, and gray cloth imports are restricted to the ready-made garment industry. Thisprotection has reduced the competitiveness of the local textile industry and has encouragedsmuggling of foreign textiles and domestic leakages of textiles and garments from bondedwarehouses, whose stocks are restricted to be used for ready-made garment exports.

Efforts to streamline import valuation have been less successful

2.8 The Government has set tariff values that are to be used in place of the invoice pricedeclared by the importer in assessing the import value of some imports. In many cases, the tariffvalues are set higher than world prices, thus increasing the protection provided by tariffs. Areview of import transaction data in 1993/94 reveals that tariff values can increase protection byas much as four to seven percent (for basic metal products and textiles). In certain cases, the tariffvalue has inadvertently been set below the CIF invoice price. The recently completed TextilesStudy revealed that the tariff value on a certain quality of polyester yam was below its CIF price,thcrefore actually undercutting the intended protection. 9

2.9 To improve the import valuation system, the Government introduced a voluntary pre-shipment inspection scheme in its 1993/94 budget. In 1994/95 the system was amended to allowpre-shipment inspection values to override fixed tariff values. This improvement increased theusage of the pre-shipment inspection scheme, in 1995/96 it covered approximately 25 percent of

8 The coefficient of variation (CV) is calculated as the ratio of the standard deviation (SD) to the mean,multiplied by 100. The SD has fallen from 54 to 16 percent between 1990/91 and 1995/96. Although the SD iswidely used as a measure of dispersion, it a weaker measure than the CV, since it is scale dependent (depends on thevalue of the mean). The CV rise, despite the fall in SD, occurred because the SD did not fall as much as the meanduring the process of tariff reduction.

See Bangladesh Tariff Commission, Textiles Sector Study Project, Final Report on the Textile Spinning Sub-sector, pp. 16.

all imports. Other improvements in import clearance include publication of the tariff schedule,and installation of a computerized customs appraisal system at Dhaka and Chittagong.

Despite policy changes, smuggling persists.

2.10 Reforms have not eradicated the strong incentives for smuggling, especially across theporous Indian border, and duty evasion continues through under-invoicing of imports. A recentsurvey reveals that illegal cross-border trade, most of it imports, was equivalent to about 13percent of total official trade in 1994. Illegal imports constituted approximately 18 percent of

1(0total imports into Bangladesh. The bulk (83 percent) of unofficial imports are from India. Thistrade has been facilitated by the different pace of trade liberalization in the two countries.Bangladesh has liberalized its import regime faster than India, but border price differentials arestill significant enough to ensure the profitability of illegal trade. The survey found that onaverage, the prices of illegal imports of Indian goods were 31 percent higher in Bangladesh thanin India. While this price differential has fallen since 1990, when it was 74 percent, it is still highenough to make smuggling worthwhile. The onerous import clearance procedures in bothcountries make the use of unofficial channels for trade even more appealing.

2.11 The survey of cross-border flows between India and Bangladesh found that illegalimports from I'dia into Bangladesh ($519 million) greatly exceeded exports from Bangladesh toIndia ($126 alulion). The Indian survey estimated total cross-border trade between the twocountries at a lower $450 million. I l

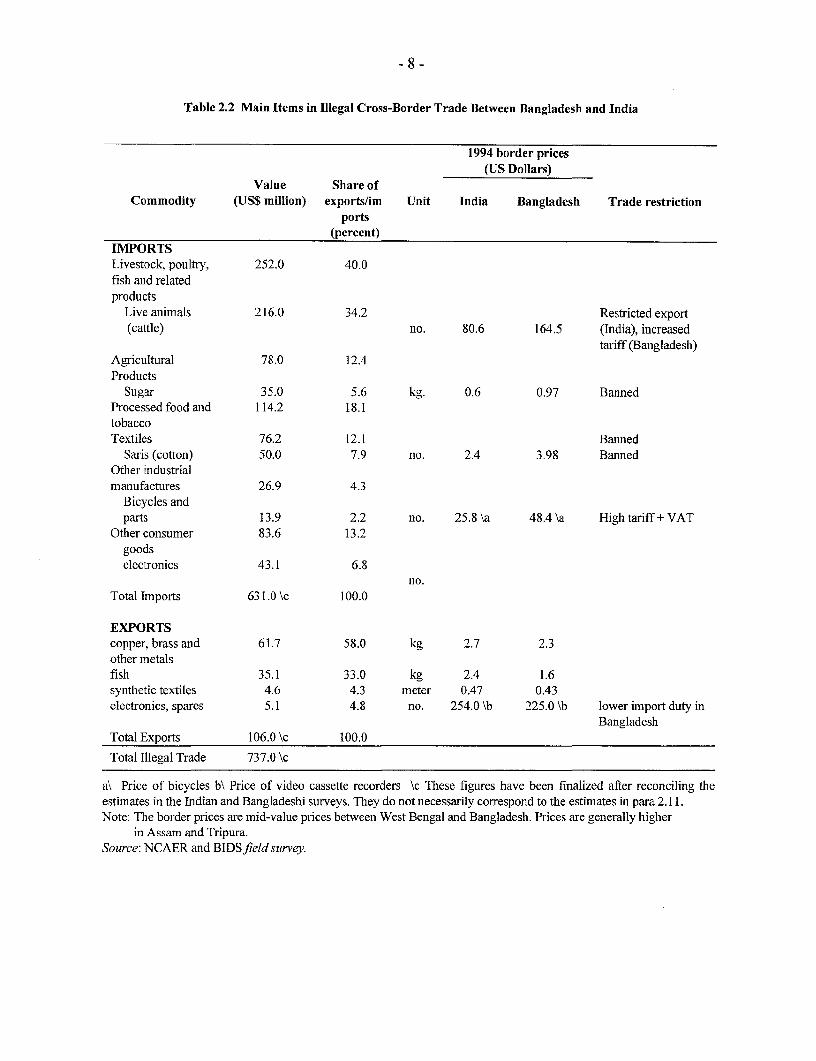

2.12 Food, agricultural products, and livestock account for the bulk of illegal imports - morethan 70 percent. Cattle alone account for one-third of illegal imports (Table 2.2). 12 Textiles,especially cotton saris, make up another 12 percent, and sugar, pulses, powdered milk, spices,salt, and bicycles are also illegally imported in large volume. Most illegal exports to India arefirst legally imported into Bangladesh, where tariffs are lower, and then exported to India. Thevolume of this "legal import-illegal export" trade has fallen significantly since the tariffdifferentials between India and Bangladesh became smaller, with India's liberalization ofimports. Important items illegally exported to India include copper and brass products, synthetictextiles, VCRs, calculators, and used clothing. Some indigenous items (fish, jute, synthetic fabricwoven of imported yarn) are also exported illegally to India.

0 These estimates are based on a 1994 survey, which estimated the volume of illegal trade between India andBangladesh. All numbers are approximations and should be used with caution.

The field survey was conducted simultaneously at the Indian and Bangladeshi borders, using a commonquestionnaire and methodology. The "Delphi technique" a method of estimation based on successive interviewswith knowledgeable persons, was used to assess the magnitude of the flows.

12 Approximately 1.7 million cows are estimated to cross the border into Bangladesh each year; accounting for20 percent of the hides and skins.

- 8 -

Table 2.2 Main Items in Illegal Cross-Border Trade Between Bangladesh and India

1994 border prices(US Dollars)

Value Share ofCommodity (US$ million) exports/im Unit India Bangladesh Trade restriction

ports(percent)

IMPORTSLivestock, poultry, 252.0 40.0fish and relatedproducts

Live animals 216.0 34.2 Restricted export(cattle) no. 80.6 164.5 (India), increased

tariff (Bangladesh)Agricultural 78.0 12.4Products

Sugar 35.0 5.6 kg. 0.6 0.97 BannedProcessed food and 114.2 18.1tobaccoTextiles 76.2 12.1 Banned

Saris (cotton) 50.0 7.9 no. 2.4 3.98 BannedOther industrialmanufactures 26.9 4.3

Bicycles andparts 13.9 2.2 no. 25.8 \a 48.4 \a High tariff+ VAT

Other consumer 83.6 13.2goodselectronics 43.1 6.8

no.Total Imports 631.0 \c 100.0

EXPORTScopper, brass and 61.7 58.0 kg 2.7 2.3other metalsfish 35.1 33.0 kg 2.4 1.6synthetic textiles 4.6 4.3 meter 0.47 0.43electronics, spares 5.1 4.8 no. 254.0 \b 225.0 \b lower import duty in

BangladeshTotal Exports 106.0 \c 100.0

Total Illegal Trade 737.0 \c

a\ Price of bicycles b\ Price of video cassette recorders \c These figures have been finalized after reconciling theestimates in the Indian and Bangladeshi surveys. They do not necessarily correspond to the estimates in para 2.11.Note: The border prices are mid-value prices between West Bengal and Bangladesh. Prices are generally higher

in Assam and Tripura.Source: NCAER and BIDSfield survey.

-9 -

High effective protection keeps incentives focused on production for the domestic market andperpetuates inefficiencies

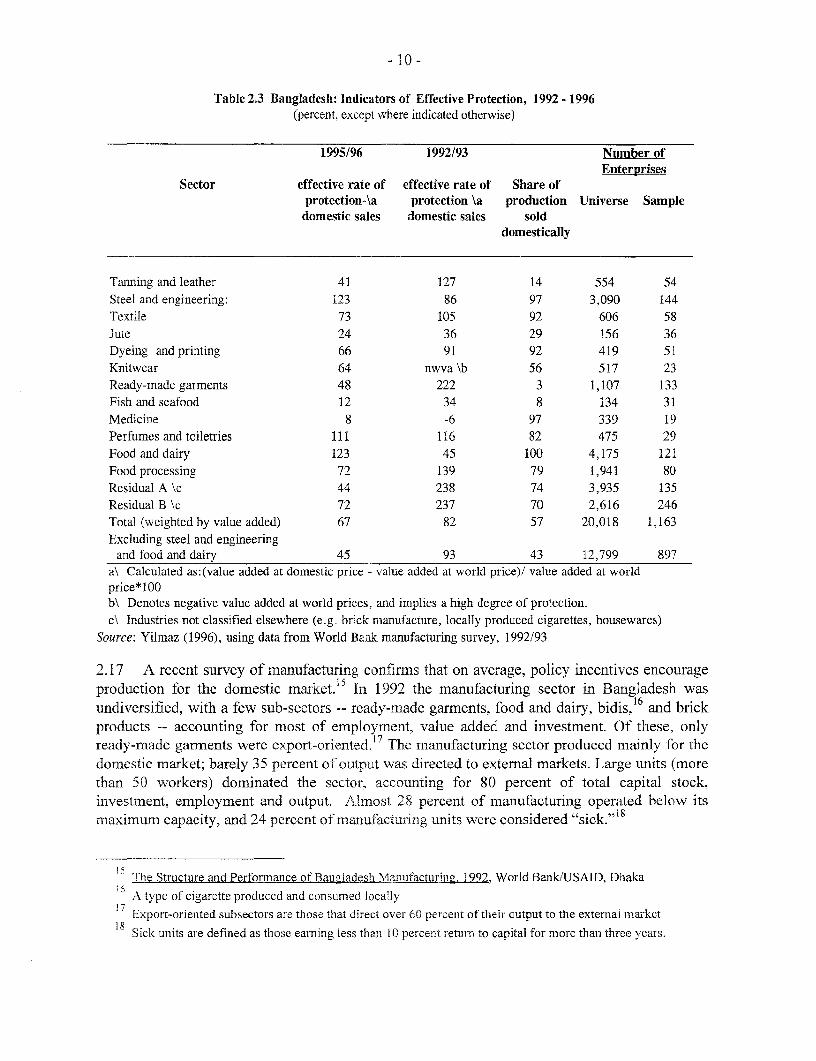

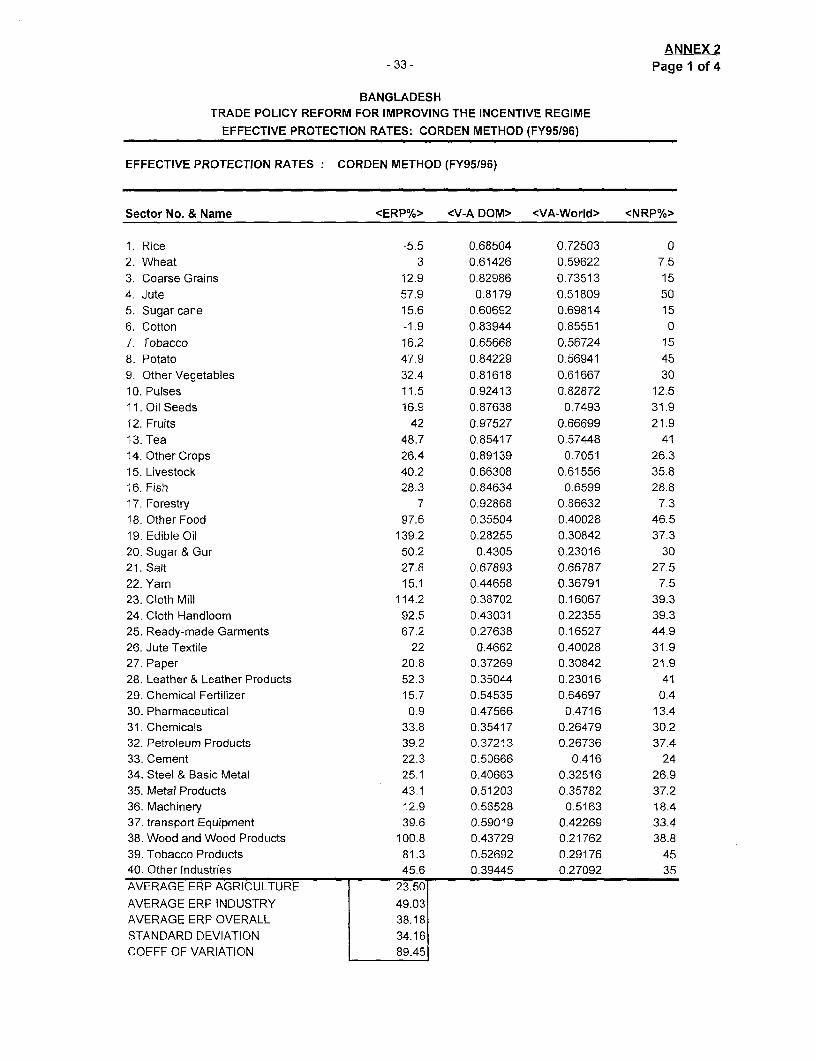

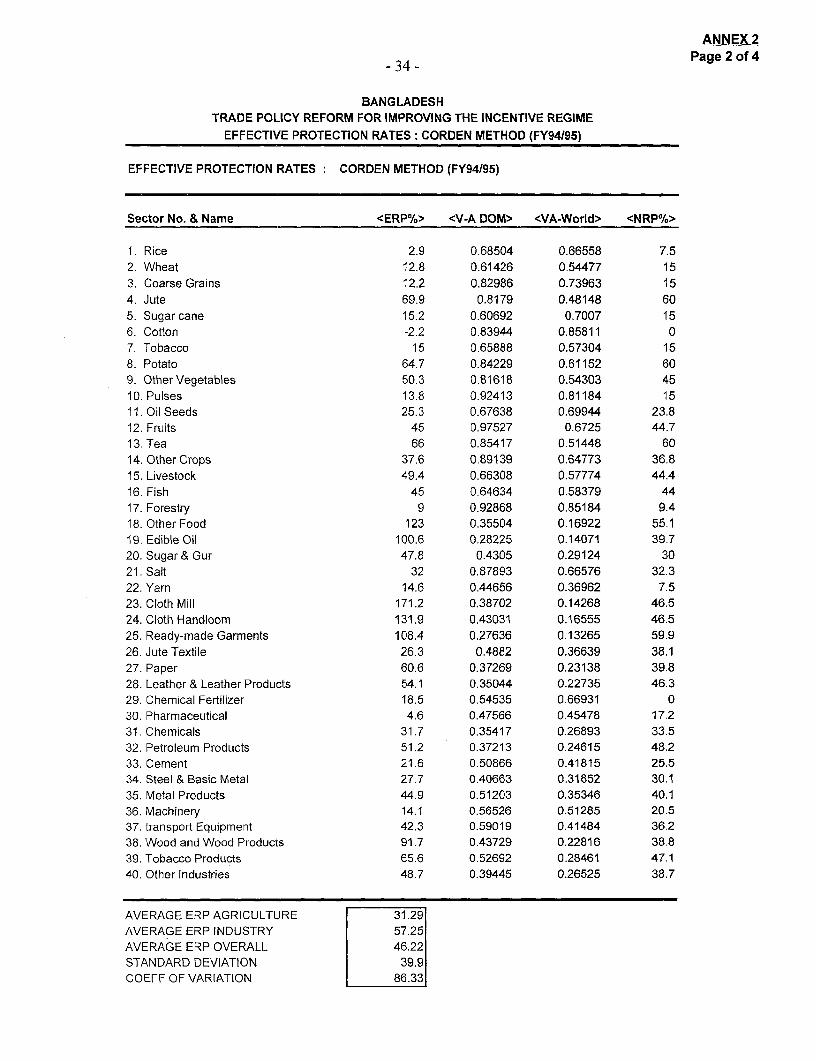

2.13 Effective protection, which measures protection to net value added, tends to be a bettermeasure than nominal protection since it takes into account protection on traded inputs.Effective protection rates for domestic sales of manufactured goods demonstrate that industry inBangladesh was highly protected at the start of tariff refonn in 1992 (Table 2.3). 13 Textiles andcertain consumer goods produced mainly for domestic consumption had particularly higheffective rates of protection.

2.14 Sustained trade reform since 1992 has reduced levels of effective protection in mostindustries (Table 2.3), 14 but because effective rates of protection rose significantly for the steeland engineering and food and dairy industries, aggregate rates fell only 15 percent. If theseindustries are excluded, aggregate effective protection declined by 48 percent between 1992/93and 1995/95.

2.15 These trends are corroborated by independent analysis performed by the BangladeshTariff Commission (Annex 2). The analysis showed that effective protection fell from 46 percentin 1992/93 to 24 percent in 1995/96 in agriculture, and from 120 to 49 percent in industry. Theanalysis also found that for certain sub-sectors (edible oils, mill cloth, and wood and woodproducts), effective protection rates are higher than nominal protection.

2.16 Though differences in methodology make it difficult to match up the World Bank resultsin Table 2.3 with those of the Bangladesh Tariff Commission, both studies indicate that tradepolicy reform has not shifted incentives towards the production of exportables. High effectiveprotection has hampered productivity and efficiency growth among import substitutingindustries. Where export production has flourished, as in ready-made garments, its rapid growthhas been fostered not by the overall policy environment, but by a special environment(availability of MFA quotas, an innovative financing scheme, and export promotions schemes)insulated from the prevailing trade regime (paras 2.20 -2.26).

3 Effective protection was calculated using firm-level data on value added. Due to lack of disaggregated worldprice data, the input-output tariff structure was used to estimate world prices. There are problems with this approach,and these results must be treated as approximations. Specifically, most tariffs are not binding, and there is a highincidence of "water in the tariff' in Bangladesh. This is a situation under which protection accorded by the levied tariffsis undermined by smuggling, domestic competition , and related factors. Therefore there may be a significant differencebetween the statutory protection levied by the tariff structure and the "observed" protection that results.

14 Effective rates of protection for 1995/96 have been calculated using the same firm level data but with the1 995i96 tariff rates.

- 10-

Table 2.3 Bangladesh: Indicators of Effective Protection, 1992 - 1996(percent, except where indicated otherwise)

1995/96 1992/93 Number ofEnterprises

Sector effective rate of effective rate of Share ofprotection-\a protection \a production Universe Sample

domestic sales domestic sales solddomestically

Tanning and leather 41 127 14 554 54Steel and engineering: 123 86 97 3,090 144Textile 73 105 92 606 58Jute 24 36 29 156 36Dyeing and printing 66 91 92 419 51Knitwear 64 nwva \b 56 517 23Ready-made garments 48 222 3 1,107 133Fish and seafood 12 34 8 134 31Medicine 8 -6 97 339 19Perfumes and toiletries 111 116 82 475 29Food and dairy 123 45 100 4,175 121Food processing 72 139 79 1,941 80Residual A \c 44 238 74 3,935 135Residual B \c 72 237 70 2,616 246Total (weighted by value added) 67 82 57 20,018 1,163Excluding steel and engineering

and food and dairy 45 93 43 12,799 897a\ Calculated as: (value added at domestic price - value added at world price)/ value added at worldprice*100b\ Denotes negative value added at world prices, and implies a high degree of protection.c\ Industries not classified elsewhere (e.g. brick manufacture, locally produced cigarettes, housewares)

Source: Yilmaz (1996), using data from World Bank manufacturing survey, 1992/93

2.17 A recent survey of manufacturing confirms that on average, policy incentives encourageproduction for the domestic market.i In 1992 the manufacturing sector in Bangladesh wasundiversified, with a few sub-sectors -- ready-made garments, food and dairy, bidis, 6 and brickproducts -- accounting for most of employment, value added and investment. Of these, onlyready-made garments were export-oriented.17 The manufacturing sector produced mainly for thedomestic market; barely 35 percent of outpl't was directed to external markets. Large units (morethan 50 workers) dominated the sector, accounting for 80 percent of total capital stock,investment, employment and output. Almost 28 percent of manufacturing operated below itsmaximum capacity, and 24 percent of manufacturing units were considered "sick."

V The Structure and Performance of Bangladesh Manufacturing. 1992, World Bank/USAID, Dhaka

A type of cigarette produced and consumed locally1 Export-oriented subsectors are those that direct over 60 percent of their output to the extemal market

8 Sick units are defined as those earning less than 10 percent return to capital for more than three years.

- I1 -

2.18 The export-oriented sectors-garments, knitwear, tanning and leather, jute, fish andseafood-performed better than the rest of manufacturing in labor productivity (fish and seafood,tanning and leather), capital productivity (ready-made garments, knitwear, fish and seafood),capacity utilization (knitwear, ready-made garments), and highest returns to capital (ready-madegarments, knitwear, and fish and seafood).

2.19 A number of import substituting industrie-s (except for the bidi industry) were inefficientat current capacity. This is indicated by a domestic resource cost of greater than 1 (Table 2.4).19Profitability was positive, but lower than the manufacturing sector's average of 15 percent (ascalculated in the 1992 survey); the bidi industry was the most profitable in the sample. Theseindustries were more competitive than the tariff structure and resulting statutory levels ofprotection would indicate, however. Observed levels of nominal and effective protection werewell below statutory levels in the soap and detergent industry and the cotton spinning andweaving industry, indicating a high degree of tariff redundancy.

Table 2.4 Competitiveness of Import-Substituting Industries, 1992/93(percent, unless otherwise indicated)

Cotton Soap and Iron and MetalIndicator Bidi spinning and detergent steel re- furniture &

weaving rolling mills fixtures(3143) (3211) (3533) (3713) (3814)

Nominal protectionfrom tariff 51 51 65 66 75observed 41 25 50 n. a. n. a.

Effective protectionfrom tariffs 21 151 110 33 57observed n. a. 52 81 n.a. n.a.

Domestic resource cost (Ratio)at current capacity 0.9l 1.16 - 1.27 1.37 - 1.50 1.00 1.19at full capacity 1.00 1.15 - 1.26 1.34 - 1.47 1.30 1.30

Profit as percent of output 11.7 10.3 8.0 9.9 4.8Note: Numbers in parenthesis are Bangladesh Standard Industrial Classification codes

n.a. denotes not available

Source: Bakht (1995)

Export promotion schemes provide an enclave setting for the production of exports

2.20 Until trade policies can ensure better incentives, export promotion schemes provideexporters with access to world-priced inputs. They have made a significant contribution to theboom in garment exports, particularly the special bonded warehouses and export processingzones.

2.21 Special Bonded Warehouse Scheme. Bonded warehouses allow firms producingexclusively for export to import and stock duty-free inputs. Used mainly by garment exporters,

19Domestic resource cost is the opportunity cost of domestic resources used to save or earn one unit of foreignexchange. DRC calculations use shadow prices, whereas ERP calculations use market prices.

- 12 -

the scheme is monitored through the use of import and export passbooks and pre-set input-outputcoefficients (for example, the fabric-gannent conversion factor to check inventory of fabric).Special bonded warehouses, which create a free trade environment for these exporters, have beena critical factor in the development of ready-made garments exports, and related intemational anddomestic subcontracting.

2.22 Until 1993, special bonded warehouses were only available to 100-percent exporters inthe garment industries using back-to-back lines of credit, and to suppliers that sell 100 percent oftheir output (e.g. zippers and buttons) to garment exporters.20 In August 1993, special bondedwarehouse status was extended to all 100-percent exporters and "deemed exporters." So far, onlya few leather anid toy exporters have joined the ready-made garments firms that are the main usersof the facility. The National Board of Revenue has not promoted the use of special bondedwarehouses because of the absence of a system for monitoring duty free imports into specialbonded warehouses for industries other than garment firms. The Govemment recently established a

21facility for jewelry exporters. Approximately 2,065 special bonded warehouses are in operation.

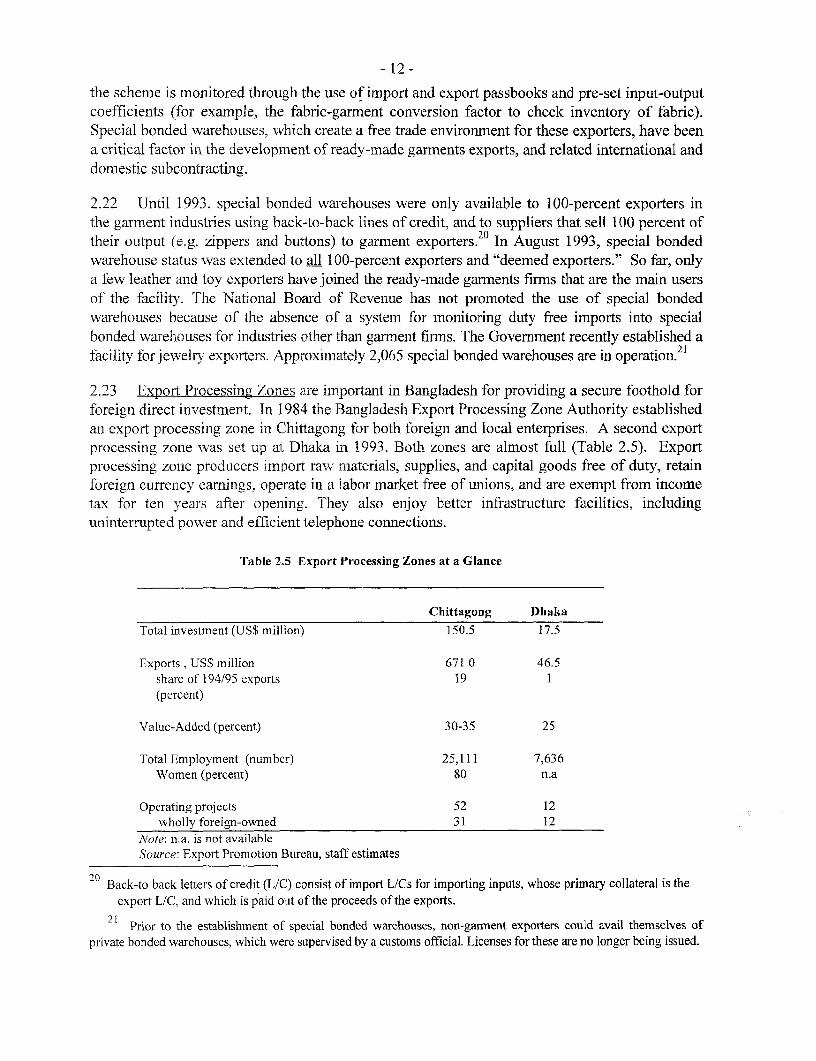

2.23 Export Processing Zones are important in Bangladesh for providing a secure foothold forforeign direct investment. In 1984 the Bangladesh Export Processing Zone Authority establishedan export processing zone in Chittagong for both foreign and local enterprises. A second exportprocessing zone was set up at Dhaka in 1993. Both zones are almost full (Table 2.5). Exportprocessing zone producers import raw rnaterials, supplies, and capital goods free of duty, retainforeign currency earnings, operate in a labor market free of unions, and are exempt from incometax for ten years after opening. They also enjoy better infrastructure facilities, includinguninterrupted power and efficient telephone connections.

Table 2.5 Export Processing Zones at a Glance

Chittagong Dhaka

Total investment (US$ million) 150.5 17.5

Exports, US$ million 671 0 46.5share of 194/95 exports 19 1(percent)

Value-Added (percent) 30-35 25

Total Employment (number) 25,111 7,636Women (percent) 80 n.a

Operating projects 52 12wholly foreign-owned 31 12

iVote: n.a. is not availableSource: Export Promotion Bureau, staff estimates

20 Back-to back letters of credit (L/C) consist of import L/Cs for importing inputs, whose primary collateral is theexport L/C. and which is paid out of the proceeds of the exports.

21 Prior to the establishment of special bonded warehouses, non-garment exporters could avail themselves ofprivate bonded warehouses, which were supervised by a customs official. Licenses for these are no longer being issued.

- 13 -

2.24 Duty Drawback schemes were introduced in 1970 to provide rebates of duties and taxesfor exporters. The Duty Exempticn and Drawback Office, established in 1988, is responsible forhandling import-policy-related and technical tasks affecting the import of inputs used in theproduction of exports. The system is not open to partial and/or occasional exporters. Over theyears the scheme has been modified to require the use of a standard schedule of ilat rates forcertain imports. It has been extended to indirect exporters using the inland let-er of credit system.and now exempts direct and indirect exporters from import restrictions.

2.25 The use of the duty drawback scheme has increased as a result of the application ofstandard rates to a growing number of products and the streamlining of procedures. Leatherexporters use them extensively. Some Taka 1.4 billion (about US$35 million), in dutydrawbacks was paid in 1994/95, but the scheme has not been as successful as the special bondedwarehouses.

2.26 This enclave environment, combined with the avaiability of M-FA quotas, alliovcdBangladesh to use its abundant labor resources to develop an efficient ready-i ade garmer.tsindustry. Garment exports account for over 50 percent of gross exports from Bangladesh. Mostof the 15 percent average annual growth in exports between 1982/83 and 1994/95 was driven lythe growth of ready-made garments (Table 2.6). Other industries have not replica ed thi.simpressive success, however, and Bangladesh's export base remains narrow despite the rapidgrowth in frozen seafood and leather exports (Figure 2.2).22

Table 2.6: Share of Major Exports and their Contribution to Growth. 1987-94(Dercent)

Annual average Share of total Contribution togrowth exports, 1987 - 1994 growth

(1) (2) (3)Raw Jute -2 5 0Jute Goods -2 16 0Leather 3 9 0Tea 4 2 0Frozen Food 8 1i INaptha 5 1 0Garments 24 49 12Total 12 100 12Note: (3) = (1)*(2)Source: Bangladesh Bank export statistics

22 Frozen seafood exports have increased 251 percent over the last decade to USS 306 million in 1994/95;leather exports have increased 189 percent over the iast decade to US$ 202 million in 1994/95. Together theyaccount for 15 percent of total exports, ready-made garment accounts for 53 percent in 1994/95 (Source: ExportPromotion Bureau).

- 14 -

Figure 2.2 Export Diversification: 1982/83 to 1994/95

1982/83 1994/95Frozen

seafoodLeather &91/ utleather Others Raw jute Othiers Raw jute Manufact

products 19% 16% 24% 2%Frozen Leather & ures

8% ~~~~~~seafood leather M 5Ready 11% productmade 6%

garments2% Jute Ready

Manufact madeures md ur4s garment

44% ~~~~~~~~54%

Note: Numbers represent gross exports.Source: Export Promotion Bureau

2.27 After a surge in merchandise export receipts to US$34.5 billion in 1994/95, a growth of36.5 percent in dollar terms from 1993/94, export performance is expected to be below potentialfor 1995/96. Recent political tensions and frequent strikes have been very damaging for industryin general, and the export sector in particular. Foreign purchasers lost confidence in the ability ofBangladesh's garment exporters to deliver on time and canceled orders. Prospects for otherexports are also bleak. Export growth in 1995/96 is expected to be no more than 10 percent, wellbelow the outstanding performance of 1994/95.

Compared with other reforming countries, trade policy reform in Bangladesh has a way to go

2.28 Comparison with South Asia. A comparison of tariff data for Bangladesh, India, Nepal,Pakistan, and Sri Lanka shows that Bangladesh's maximum tariff is the same as India's, buthigher than Sri Lanka's (Table 2.7). Import-weighted tariffs are, however, higher in Bangladeshthan in India, Nepal, and Sri Lanka. India's trade regime was more protectionist in the past, butsignificant reforms have narrowed the difference between India and Bangladesh. Compared withIndia and Pakistan, Bangladesh has moved faster to reduce quantitative restrictions and exportrestrictions--in India, consumer good imports is still virtually banned, and some 200 agricultural,mineral, and metal items are under export restrictions. However, most South Asian countries aremoving quickly to remove the remaining barriers to trade.

2.29 Sri Lanka is a good comparator for trade reform. Since 1977, Sri Lanka has been steadilyliberalizing its trade regime. Tariffs have been compressed into three bands with standard rates of

- 15 -

10, 20 and 35 percent. Export taxes have been abolished,23 and quantitative restrictions areapplied primarily for non trade reasons.24 Sri Lanka is also moving away from a reliance onimport duties for revenue: in 1995 custom duties were only 21 percent of total revenue(compared with 33 percent in Bangladesh) and 9.7 percent of imports (23 percent inBangladesh). Although Sri Lanka's trade regime does have some drawbacks (the granting of dutywaivers and exemptions and the application of surcharges and markups in import valuation), themove to the three-band tariff system has made Sri Lanka's economy the most open in SouthAsia. Sri Lanka has announced plans to move to a two- band regime (10 and 20 percent) soon,and to a uniform tariff shortly thereafter.

2.30 Comparison with the Rest of the World. Although Bangladesh's tariffs are low comparedwith those of other South Asian countries, they are higher than the average tariffs prevailing in anumber of countries that have undertaken or are undertaking trade reform in Latin America andEast Asia (Indonesia, Malaysia, South Korea). as well as those in Ghana and Morocco (Table2.8). However, aiter Colombia, Bangladesh has made the largest reductions in average tariffsover its reform period, as measured by the ratio of average tariffs after reform to those beforereform.

2.31 Capital goods enjoy low- protection in Bangladesh (Table 2.9), while consumer goods aresubject to relatively high protection. Protection of capital goods in Bangladesh is similar to thatof countries in Europe, Latin America, and the Middle East. while protection of intermediate andconsumer goods compares with protection of these goods in Africa. These comparisons suggestthat despite significant progress, further tariff reduction is necessary before Bangladesh'seconomy is as open as the economics of rapidly industrializing nations around the world.

Table 2.7: Nominal Protection in South Asia(percent)

Year Maximum tariff Unweighted average Coefficient of Import-weightedvariation average

Bangladesh 1995 50 25 73 211991 509 89 59 42

India 1995 50 41 61 191991 400 128 25 87

Nepal 1994 100 20 n.a. 10

Pakistan 1994 70 50 27 n.a.Sri Lanka 1995 35 n.a. n.a. 10 \aa\ denotes collection rateNote: n.a. is not availableSource: India: Issues in Trade Reform. Volurne 1, 1994, staff estimates

23 Some export cesses and "royalties" remain on items such as coconut products, tea packets and bags, rawhides and skins and rubber.

24 Exception are some agricultural products, certain used transport vehicles, and certain diesel engines.

- 16 -

Table 2.8: International Comparisons of Tariff Rates

Country Average Before Average After Tariff Ratio \areform reform

Bangladesh (1989, 1995) 94 25 0.27

Cote'd Ivoire (1984, 1989) 26 33 1.27Nigeria (1984, 1990) 35 32.7 0.93Ghana(1983, 1991) 30 17 0.57

Argentina (1988, 1992) 29.4 12.2 0.41Brazil (1987, 1992) 51 21 0.41Chile (1984, 1991,1\b 15 11 0.73Colombia (1984, 1992) 61 12 0.20Costa Rica (1985, 1992) 53 15 0.28Mexico (1986, 1991) 22.6 13.1 0.58Peru (1984, 1992) 27 17 0.63Venezuela (1989, 1991) 37 19 0.51

China (1986, 1992) 38.1 43 1.13Indonesia (1985, 1990) 27 22 0.81South Korea (1984, 1992) 24 10.1 0.42Malaysia (1985, 1993) NA 14

Egypt (1989, 1993) 47 34 0.72Jordan (1987, 1994) 33.4 30.5 0.91Morocco (1983, 1990) 36.1 23.4 0.65Tunisia (1987, 1990) 32.5 28.5 0.88a\ tariff ratio is calculated as post-reform tariff/pre-reform tariff, i.e. Column 2/Column 1b\ denotes uniform tariff after reformsSource: Hoekman 1995b, Dean et al 1994.

Table 2.9: International Comparisons of Nominal Tariffs in Manufacturing

Country/ Region Capital goods Intermediates Consumergoods

Bangladesh 12 19 35Thailand* (1985) 22 14 25Turkey (1988) 31 16 35Philippines (1985) 22 23 38Indonesia* 12 7 27Argentina 24 21 13RegionsAfrica 24 26 50Europe and Central Asia, 19 15 31Middle East and North AfricaLat.n America 19 18 33* denotes il:)ort weighted tariffs, all others are arithmetic averagesSource: India: Issues in Trade Reform, Volume 1, 1994

- 17 -

3. THE REMAINING AGENDA

3.1 Moves to liberalize the trade regime, coupled with relative macroeconomic stability andoverall growth in the economy, resulted in significant import growth in 1994/95. After years of3-5 percent average import growth, imports grew 39 percent in dollar terns between 1993/94 and1994/95. Primary commodities, the largest component of the increase, grew 60 percent. Capitalgoods, the second largest component, grew 50 percent (Annex 3). There is also evidence of apickup in private sector activity; total credit to the private sector grew 24 percent in 1994/95, amarked increase from the average growth rate of 6 percent between 1990/91 and 1993/94. Thiswould imply that investment activities, including construction, were on the rise in Bangladesh.These major changes in import and credit growth rates indicate that the reform program mayfinally have begun to evoke a supply response.

3.2 Chapter 2 indicates, however, that the present policy regime provides high effectiveprotection to domestic industries, maintains incentives for smuggling, and facilitates exportgrowth only under enclave arrangements. While tariffs have been reduced steadily, there is stillevidence of "water in the tariff'. Such a regime is not conducive to the growth of an efficientmanufacturing sector. Moreover, current incentives focus manufacturing production on thelimited domestic market in Bangladesh and are inconsistent with the Government's export ledgrowth strategy. A significant growth in exports would require a fundamental shift in the currentincentive structure, as well as growth in productivity and efficiency of enterprises. Completingthe remaining agenda for trade liberalization can help shift the incentive structure towards theproduction of exports.

Complete the process of trade liberalization

3.3 The recent growth in trade indicates that trade reforms may be evoking a supply response.To sustain this response, Bangladesh must complete the reforms it has begun. Its reform agendashould focus on import liberalization to remove price distortions, while maintaining theefficiency of its current export promotion regimes. By adopting the provisions of the recentlyconcluded Uruguay Round agreement, Bangladesh could send a strong, positive signal to privateinvestors at home and abroad.

3.4 Tariff reduction. Tariff reform is the most critical element of trade policy reform. Itdeserves top priority in an export-oriented development strategy. Tariffs constitute a hidden taxon exporters, and are an impediment to streamlining trade procedures and increasing backwardlinkages (Box 3.1). All these factors directly affect export competitiveness.

- 18-

3.5 The Government has made commendable progress in tariff reduction, but a small,critical part of the agenda remains incomplete. A key objective of tariff rationalization isto move toward uniformity in nominal rates, and thereby in effective protection, whilereducing the average rate. Reducing the maximum tariff rate will not only increasetariff uniformity, but also bring about the largest efficiency gains. A second objective isto reduce tariff dispersion, to reduce the bias implied by different rates. A major source ofdispersion is the continued use of tariff concessions for end users. These concessionalrates of duty should be phased out, and the higher tariff rates should be reduced to bringtariffs closer to neutrality.

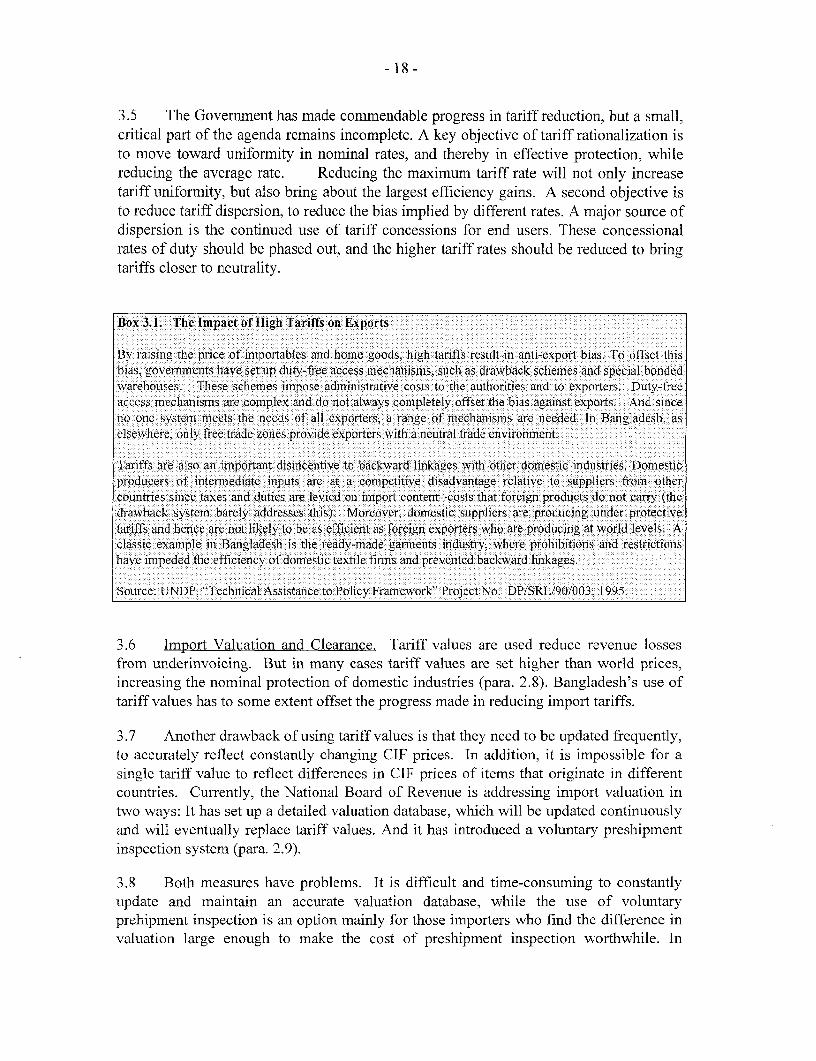

Box 3.. The Mpact of Hih Tarffs on Eprt

By raisin gthe price of importables and homfe: goods,: high tariffs result inanti-exportf bias., To offset thisbias, lgovernments:.have set up duty-free access mechanisms, such assdfrawback schemes and special bonded

dwarehouses.0 These schemes impose admrinistrative costs tothe: authorities: and to exporters. .D uty-freeaccess meChanisms are :complext anid do notfalways comp letely offset the bias against6exports.$ And since.no, one system meets the needs :of all exporters, a f 0mechanisms are needed. In Bangladesh, aselsewhere, only free trade zones provide exporters witha neurtral trade environment.

Tariffslare} also an important disincentive dto backward linkages with other domestic iMdustries. Domesticprodciers of:intermediate inputs areiat a competitive disadvantage relative to suppliers, frmo:: 6thercountries since taxes and: duties are levied on import content--osts that foreign products do not carry (lthe.drawback system barely addresses this)i. Mi Moreover, domrestic t suppliers are producing under protectivetariffs and hence are notlJik elyto be as efficient as gforeign exporters who areproducing at world levels.: Alclassic:i example in Bangladesh is the ready-made garments industry, twhere prohibitions and restrictionshavek impeded theiefficiency of domestic textile firrns and prevented backward linkages

Soure:. lUNDP:,"erhnical: Assistanc to PolicyFram!ework" ProjctgN6o. DP/SRL/90/O3D0J1995.

3.6 Import Valuation and Clearance. Tariff values are used reduce revenue losses

from underinvoicing. But in many cases tariff values are set higher than world prices,increasing the nominal protection of domestic industries (para. 2.8). Bangladesh's use oftariff values has to some extent offset the progress made in reducing import tariffs.

3.7 Another drawback of using tariff values is that they need to be updated frequently,to accurately reflect constantly changing CIF prices. In addition, it is impossible for asingle tariff value to reflect differences in CIF prices of items that originate in differentcountries. Currently, the National Board of Revenue is addressing import valuation intwo ways: It has set up a detailed valuation database, which will be updated continuouslyand will eventually replace tariff values. And it has introduced a voluntary preshipmentinspection system (para. 2.9).

3.8 Both measures have problems. It is difficult and time-consuming to constantlyupdate and maintain an accurate valuation database, while the use of voluntaryprehipment inspection is an option mainly for those importers who find the difference invaluation large enough to make the cost of preshipment inspection worthwhile. In

- 19-

addition, there have been significant discrepancies recently between the preshipmentinspection value and tariff values, which has caused some conflicts between NationalBoard of Revenue and the preshipment inspection agencies. As a result, the NationalBoard of Revenue has temporarily banned the use of preshipment inspection certificatesfor 12 items.25 The WTO now requires that customs valuation be invoice-based. Tocomply with this, Bangladesh would need to phase out its system of tariff valueseventually.

3.9 In the long run, the best solution to valuation and clearance problems is acomplete reform of customs. As tariff rates are compressed, the incentive to underinvoicewill be reduced, and Bangladesh wvill be able to rely on invoice prices as an accuratemeasure of import value, as many countries now do. Until then, a well-functioning PSIsystem is a useful transitional tool to reduce revenue losses through underinvoicing. Arecent review of such systems found that the "design and content of PSI contracts...merits careful attention if the full benefits of the service are to be realized".26 Wherethey have proved disappointing, especially on the revenue side, it has been largelybecause of the "lack of serious monitoring and follow-up of information generatedthrough pre-shipment inspection and the absence of a satisfactory system for ex-postreconciliation". This finding is particularly relevant to Bangladesh, whose voluntaryscheme cannot deliver the results that could be explicitly mandated in Government-agency contracts, such as accountability to principals, trade facilitation, and routines forconflict resolution. Thus the system needs to be properly designed.

3.10 The trade liberalization agenda will not be complete without improving importclearance procedures. As tariff reform has progressed, the need to improve the efficiencyof import clearances has become even more urgent. The Government recently introducedcomputerized customs assessment using the UNCTAD-developed SPEED system atChittagong port and Dhaka airport. Design and implementation problems have kept theSPEED system from functioning smoothly, however, there are no immediate plans tointroduce it at other customs stations. Review and adjustment of the SPEED system areneeded to complete the process of computerizing the assessment of imports.

3.11 Quantitative Restrictions and Other Barriers. Quantitative restrictions, especiallyon textiles, are preventing the development of backward linkages with the ready-madegarnent sector (Box 3.2). Removing these restrictions would eliminate virtually allremaining protection due to non-tariff barriers in Bangladesh. More important, that wouldprovide an impetus to the development of a textile sector that could potentially supply theneeds of the ready-made garments industry, which now imports over 90 percent of itstextile inputs. Bans on imports of sugar, salt, and some other commodities are virtuallymeaningless because significant amounts of these commodities are imported illegallyfrom India. Removing these restrictions would increase the efficiency in these industries

25 These include cars, dry cell batteries, air conditioners, filament lamps, fluorescent light tubes, GItubes, soda ash and caustic soda, cigarettes, powdered milk, cumin seed and black pepper.

26 See Low , Patrick "Preshipment Inspection Services", World Bank Discussion Paper No. 278.

- 20 -

by exposing them to competition, generate tariff revenues, and benefit consumers by

reducing prices.

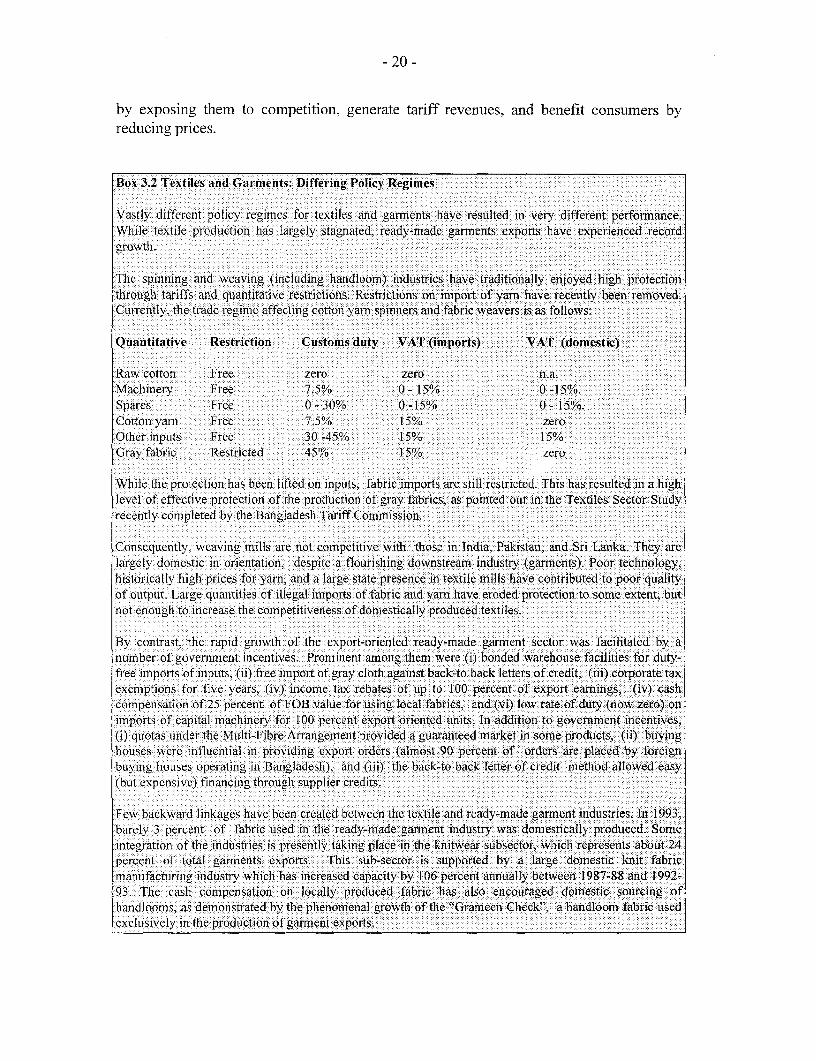

Box 3.2 Textiles ~and Garments: Differing PolicyR,egimes

Vastly ifferen poicy regimes, fort txiles: And ~garments: hAve resuledi ver ifren perfrmance.Whiile textile production has~ largely stagniated, ready-ima de garments iexports have experienced record

The spinnin ad wain (including: hanidloom) industries: have tanditionally enjoye hIghpoeto

through: tariffs ~and ~quantitative restrictions.: Restrictilons oQn iprt o ff yrnhaeirecently been, removed.~Currently, the trade regime affectincotnymsier adbfabic Weavers sa oI

Quantitative Restriction CEustoms.duty.:1 AT (imports) VAT (oetc

Raw cotton Free i i1zeroI zero n.a.Machinery~:~ Free '7.5% :0. 15% 0-5%spares Free 0~-30% >0 15% 15NoCotton yarn Free 7.5% 5% zeroOther inputs Free' 30 -45%. 15%i 15%Gray fabric Restricted :,45% ~ ~ 15% i zero

While thie ~protection: has beeni I 'fted on inputs fabricA imports are still: retrited hshsrslenahg