Embed Size (px)

Citation preview

RET br�n lorvl T 1! CIRCULATING COPY

I REPOPTS nF7SZI BE RETURNED TO REPORTS DESK LA-5WITHIN IN CENTRAL FILES

| ONE '.'EK-- {i

f Thl; ranort wins nrenared for use within the Bank and its affiHintatd nrganizatinns.I. They do not accept responsibility for its accuracy or completeness. The report may

n not be published nor mnv it kb qontetd nc renreentinn their viws

INTEIRATIONAL BANK FOR RECONSTRUCTION AND DE'VELOPMENT

INTERNATIONAL FINANCE CORPORATIONAs- ' T I V T>T" rTTT r T 1 R TTT I e l IT k t "T

UN 1 £MK1NA I I1VAAL D r- V 1Z~r'V1IiNl 1 iD'Vi1-A 1 l)J.N

APPFRATSAT. OF THE

iN '%~r n Tmr 7 -, -r T yrr~ f ,'% r Yr C-rFAL CON BRID G E DU %JI.Jf NICKrEJ .LJ PRJE TLA-

DOMINICAN REPUBLIC

i.uri

November 25, 1969

IFC - Department of Investments

Latin Anierica, Europe and Australasia

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

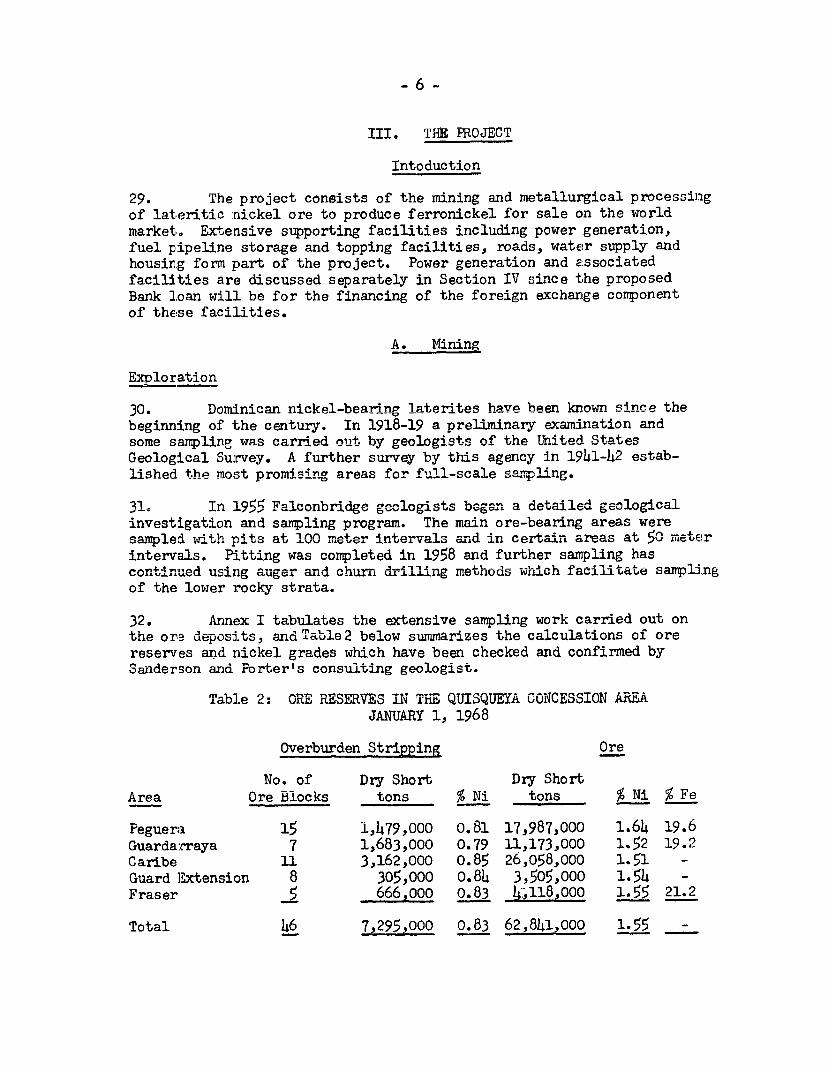

lic D

iscl

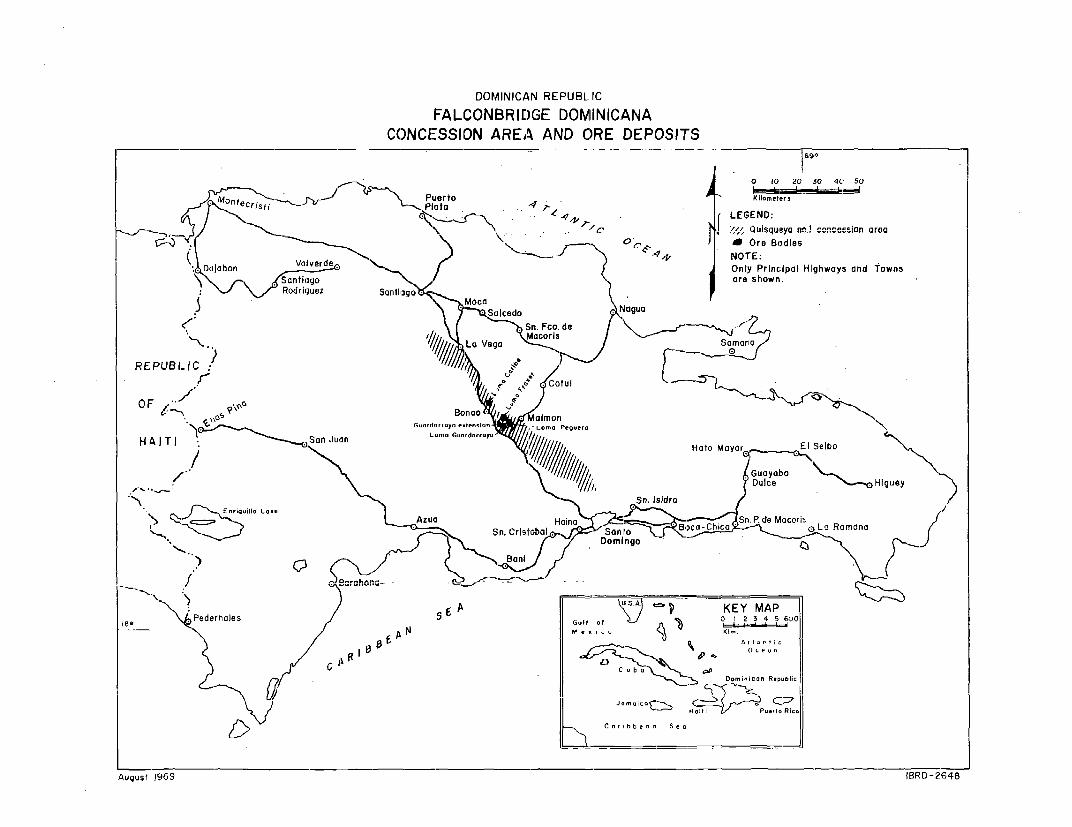

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

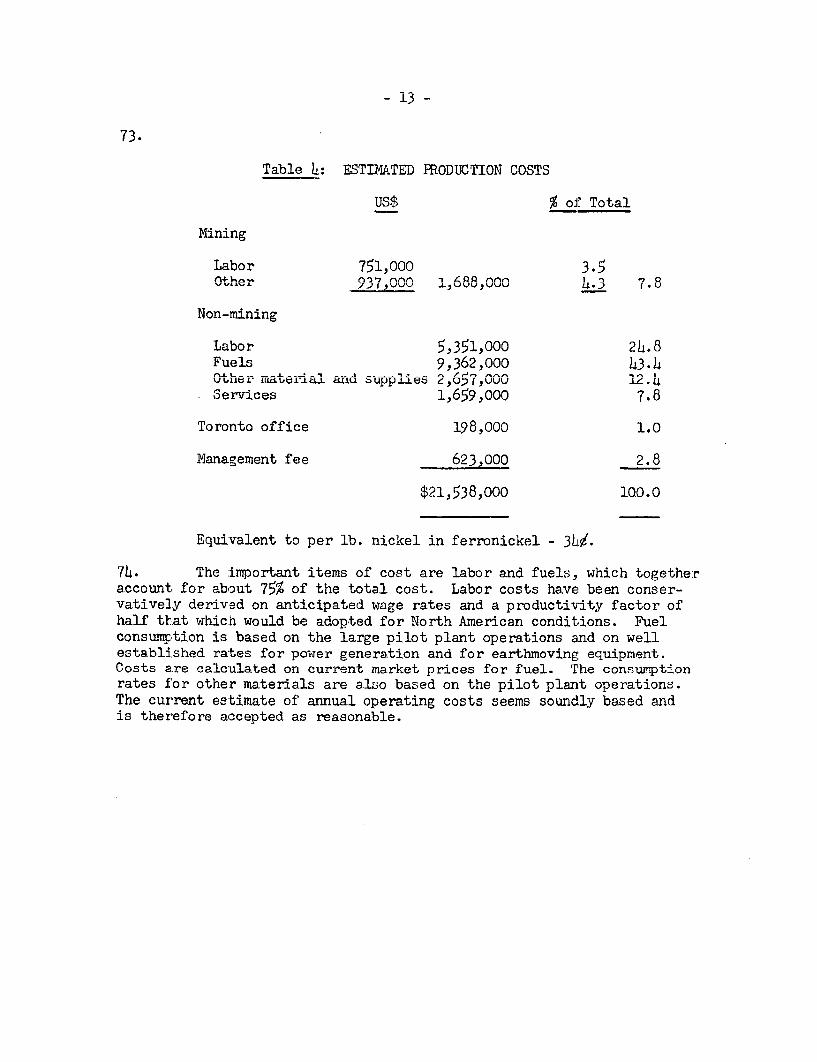

APPRAISAL OF THE

FALCONBRIDGE NICKEL PROJECT

DOMrINICAN REPUBLIC

TABLE OF CONTENTS

Paragraphs

I. Introduction 1 - 7

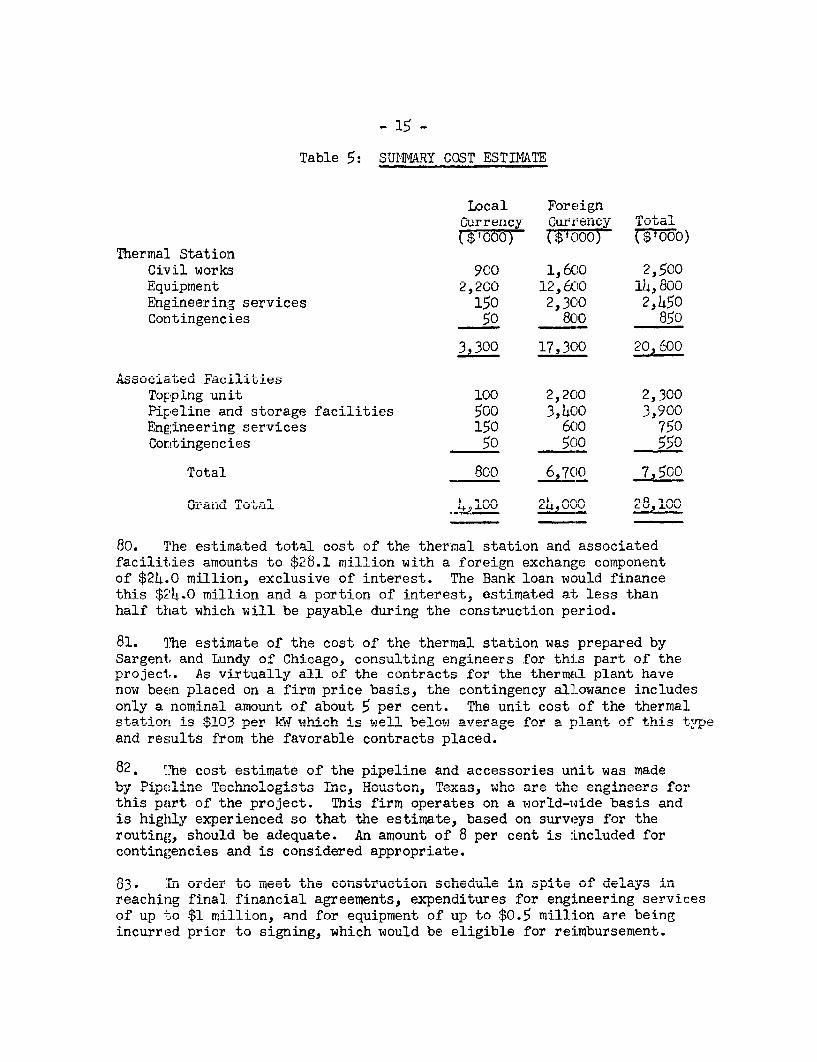

II. The Borrower and Sponsors 8 - 28

A. Falconbridge Dominicana C por A 8 - 12B. Falconbridge Nickel Mines Limited 13 - 16C. Armco Steel Corporation 17 - 20D. Management Arrangements 21 - 28

III. The Project 29 - 74

Introducticn 29A. Mining 30 - 40B. Processing 41 - 49C. Water Supply 50 - 52D. Transport 53 - 55E. Townsite 56F. Project Cost Estimate 57 - 62G. Engineering and Construction 63 - 67H. Procurement 68 - 69I. Personnel 70 - 71J. Production Cost Estimates 72 - 74

IV. Bank Financed Facilities 75 - 90

A. Description of Facilities 75 - 78B. Cost Estimates 79 - 84C. Operating Cost - Thermal Plant 85 - 86D. Pomer Reauirements 87E. Engineering, Procurement & Construction 88 - 90

V. The Market 91 - 117

A. General 91 - 95R- Connsmrtio rn 96 - 102C. SuLpply 103 - 108D. rPenPi for Ferronickel 109 - 113E. Marketing and Price 114 - 117

Paragraphs

VT. Financing Plan and Financial Prospects 118 - 161

A. Pronosed Financing Plan 119 - 131B. Financial Prospects 132 - 138G. nehbt Servicing ruarantee 139 - 1c)6

D. Concessions and Incentives 157 - 161

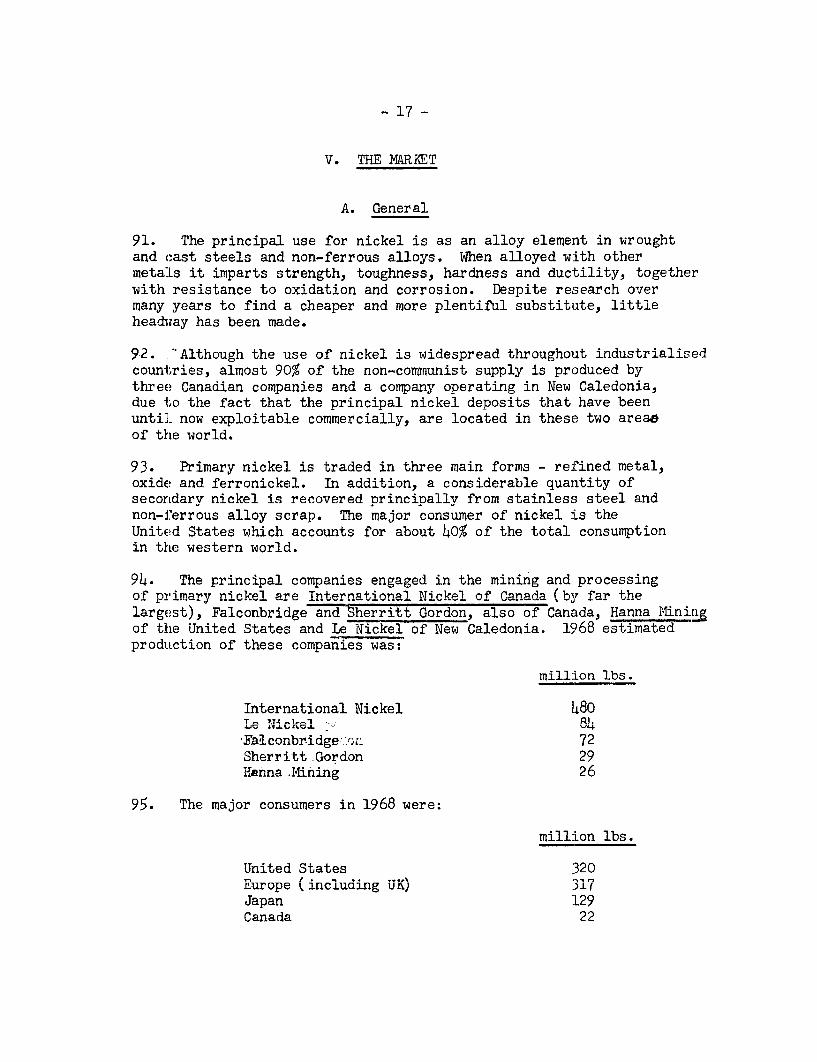

VII. Economic Benefits 162 - 174

Gains in Foreign Exchange 164 - 167Fiscal Ben.efits 168 - 17'0Indirect Benefits 171 - 174

VIII. Protective Arrangements 175 - 181

IX. Conclusvon 182

List of Annexes and ilaaps

Annex 1 - Historical Sampling Program

Annex 2 - Ore Preparation and Processing

Annex 3 - World Nickel Production

Annex 4 - Future Production of Nickel

Annex 5 - World Ferronickel Production

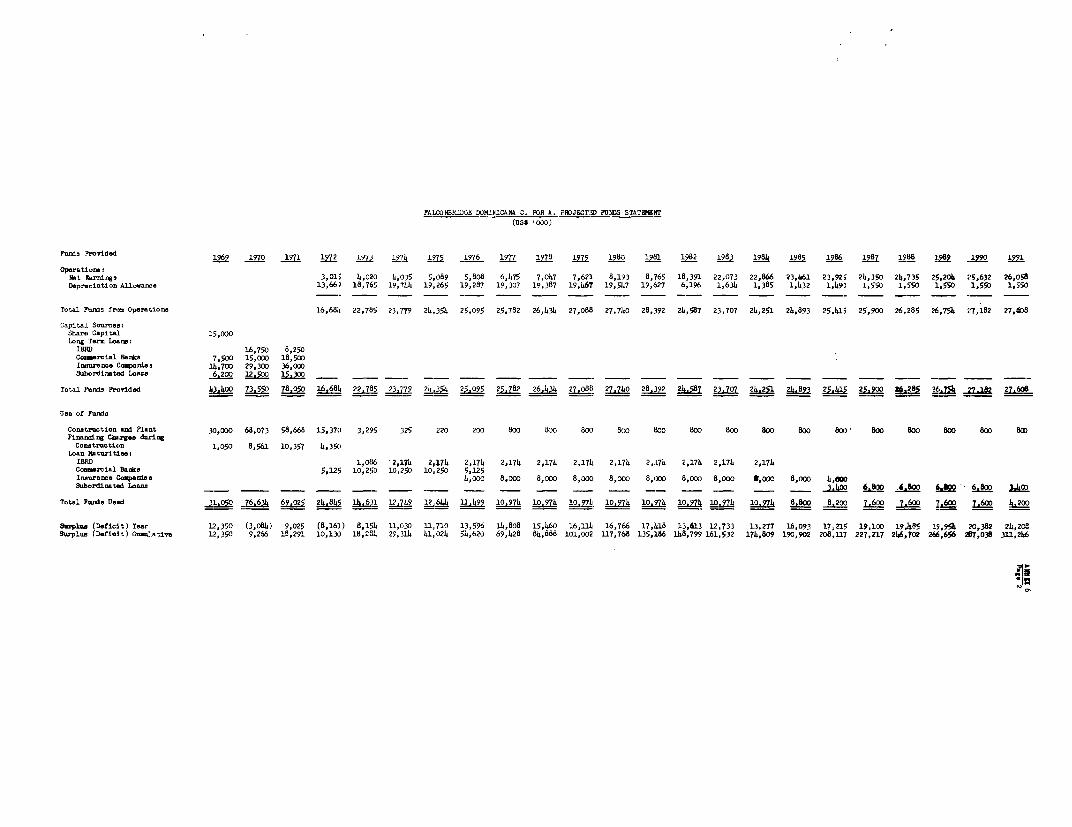

Annex 6 - Financial Statements of Falconbridge DominicanaC por A

Annex 7 - Financial Statements of Falconbridge NickelMines Limited

Annex 8 - Financial Statements of Armco Steel Corporation

Annex 9 - Economic Data

Maps - Dominican Republic

Mining Area of Falconbridae Dominicana

APPRAISAL OF THEFAiCONMBRIDGE Ii-1Cn-, PROjECT

DOIVINICAN REPUBLIC

SUMMARY AND CONCLUSIONS

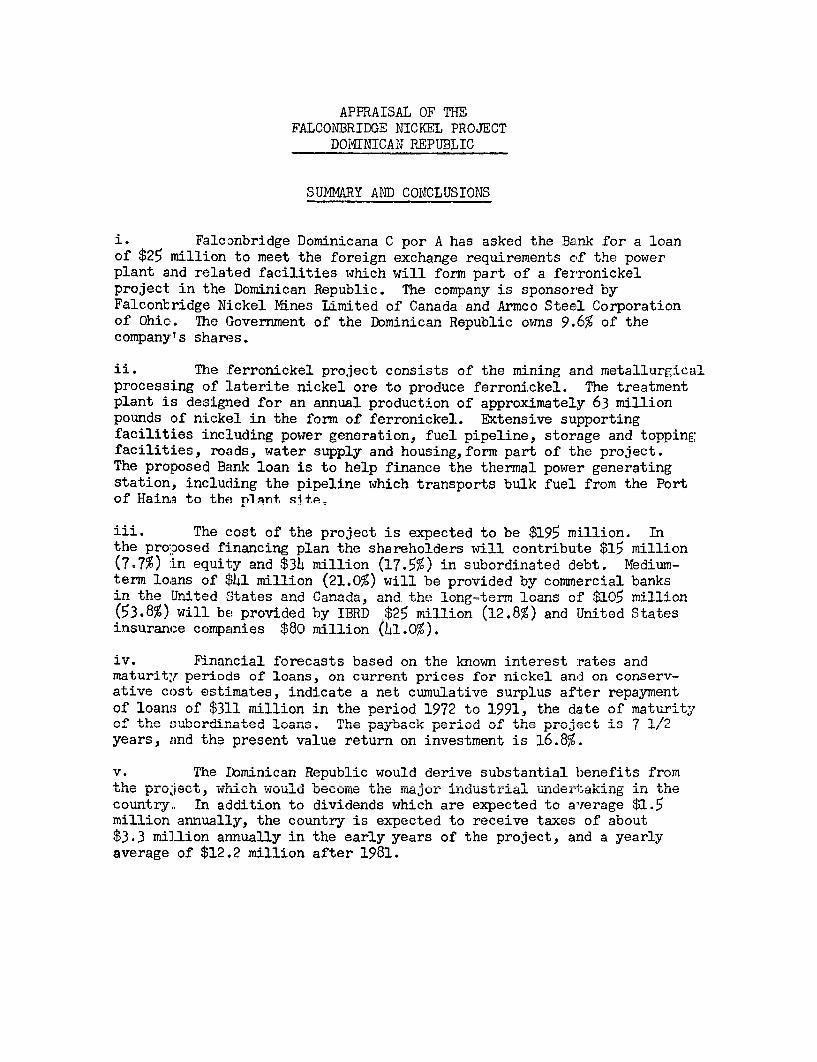

i. Falconbridge Dominicana C por A has asked the BEInk for a loanof $25 million to meet the foreign exchange requirements of the powerplant and related facilities which will form part of a ferronickelproject in the Dominican Republic. The company is sponsored byFalconbridge Nickel Mnes Limited of Canada and Armco Steel Corporationof Ohic. The Government of the Dominican Republic owns 9.6% of thecompany'-s shares.

ii. The ferronickel project consists of the mining and metallurgicalprocessing of :Laterite nickel ore to produce ferronickel. The treatmentplant is designed for an annual production of approximately 63 millionpounds of nickel in the form of ferronickel. Extensive supportingfacilities incLuding power generation, fuel pipeline, storage and toppingfacilities, roads, water supply and housing,form part of the project.The proposed Bank loan is to help finance the thermal nower generatinestation, including the pipeline which transports bulk fuel from the Portof Haina to the nlant site,

iii. The cntt. nf t.he prorjerct i. Pvnrnri +.ns hed to be lQ9 m:illion. Tnthe proposed financing plan the shareholders will contribute $15 million(7.7%) -in equit;y and $3i million (17 .5%) in subordinated debt. Mdiu.-term loans of $141 million (21.0%) will be provided by commercial banksin the United 'tates anrd Canada, and the long-erm- loans of $105 mi"ion(53.8%) will be provided by IBRD $25 million (12.8%) and United States

insurar.e- cpies 80 11milion (11 .0W%

Av. Tr n I; .IanciaJl forecasts buaseud o, thLIile IL Lnown interest .ates andUmaturity periods of loans, on current prices for nickel and on conserv-ative cost estimates, indicate a net cumu-lative surplu a.fter r.paym.entof loans of $311 million in the period 1972 to 1991, the date of maturityof the subordir4-.ate~d loCans. MIe payback perio 4of th prjcti 7 '1/2

years, and the present value return on investment is 16.8%.

v. The Dominican Republic would derive substantial benefits fromULMe pro;ject u, whIJch woUU uid IA Uleom v i±ajUlr indusvi1rial ±utrIUerai.U1g in Wietcountry. In addition to dividends which are expected to average $1.5million annUually, the coUntr1'y iS exAPected tO recei-ve taxes of about$3.3 million annually in the early years of the project, and a yearlyaverage of $12.2 million after 1981.

- 2 -

vi. Present nickel consumption in the non-Communist world is about800 million lbos. per annum. Consumption has been limited by short supplyin recent vea-rs. but a P'rowth in consumntion at an averaee annual rateof 6p is expected. Although rapid growth is anticipated in the produc-tnrn of f orrmni nkel- i4t Si prn-'bhle that Apmned will1 eointinue to exceedavailable supply. Falconbridge Canada, which has an international salesorganization- T.I11 sll +.hea fr-rniek.1l vrndiive in the niminican Re-public and it has already received purchasing intentions for about 80%oof th poecedotpt

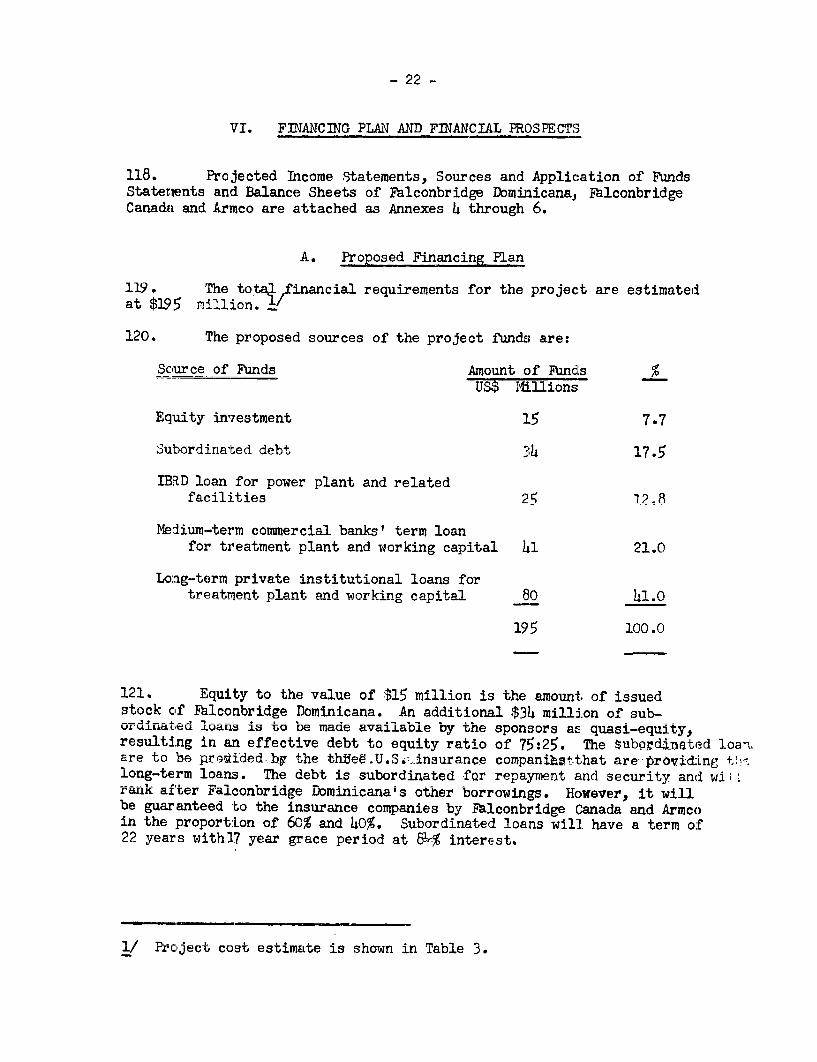

'4 4-~~,~11 & 1-~ T'L,,,4,4^nnv 11%414?' 0vii Fal;,or,bridAge Do,,in ----- W -1 pa ohen, 4ria" eubnV.LJ. .L 0. L%.%JXLLJ.L LJU V IL" L'C.LLa. VV.L..L.&. FCX 'JJ VILU~LJl .C.~

fee of 1½-% of the outstanding Bank loan in return f'or guaranteeing theloan.

Viii.. TIhe sponsors hi[ave agreteu t provieu a'' uJ add uuUitior.al fU. neU--

ed for any project cost overrun, subject to a time limitation which isdescribed in the Completion Agreement. The hRBD loan will be premLat-urdshould the project be abandoned before completion.

ix. The loan will have a term of 15 years with a grace period ofSt years. Repayment will be made in 23 equal semi-annual maturitiesof principal.

x. Subject to protective trrangements the proposed project wouldbe a suitable basis for a Bank loan of $25 million.

APPRATIAT OF rPH

FALCONBRIDGE NICKEL PROJECTnnMAMTt.TT,AU DDTrDTTf'~J'JL_J.I'd.LWZ"1.' L6UA .UJ..U.L~L

I. INTRODUCTION

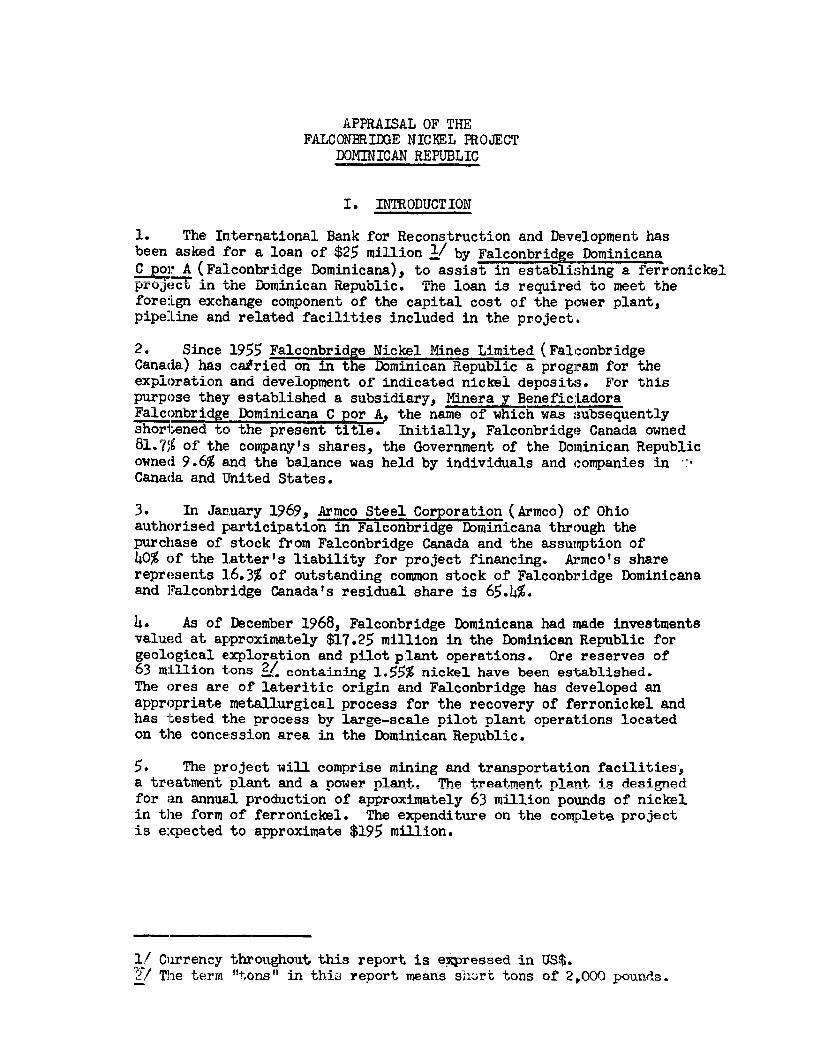

1. The International Bank for Reconstruction and Development hasUeen asked Lor a "loan of $2 mlillon 1/ Dy Falconbridge DominicanaC por A (Falconbridge Dominicana), to assist in establishing a ferronickelproject in the Dominican Repuolic. The loan is required to meet theforeiLgn exchange component of the capital cost of the power plant,pipe:Line and. related facilities included in the project.

2. Since 1955 Falconbridge Nickel Mines Limited (FalconbridgeCanadla) has catried on in the Dominican Republic a program for theexploration and development of indicated nickel deposits. For thispurpose they established a subsidiary, Minera y BeneficiadoraFalconbridge Dominicana C por A, the name of which was subsequentlyshortened to the present title. Initially, Falconbridge Canada owned81.7, of the company's shares, the Government of the Dominican Republicowned 9.6% a.nd the balance was held by individuals and companies inCanada and United States.

3. In January 1969, Armco Steel Corporation (Armco) of Ohioauthorised participation in Falconbridge Dominicana through thepurchase of stock from Falconbridge Canada and the assutmption of40% of the latter's liability for project financing. Armco's sharerepresents 1.6.3% of outstanding common stock of Falconbridge Dominicanaand Falconbridge Canada's residual share is 65.4%.

4. As of December 1968, FalconbridRe Dominicana had msade investmentsvalued at approximately $17.25 million in the Dominican Republic forgeological exploration and pilot Dlant operations. Ore reserves of63 m:Lllion tons 2/ containing 1.55% nickel have been established.The ores are of lateritic origin and Falconbridge has developed anappropriate metallurgical process for the recovery of ferronickel andhas tested the process by large-scale pilot plant operations locatedon the concession area in the Dominican Republic.

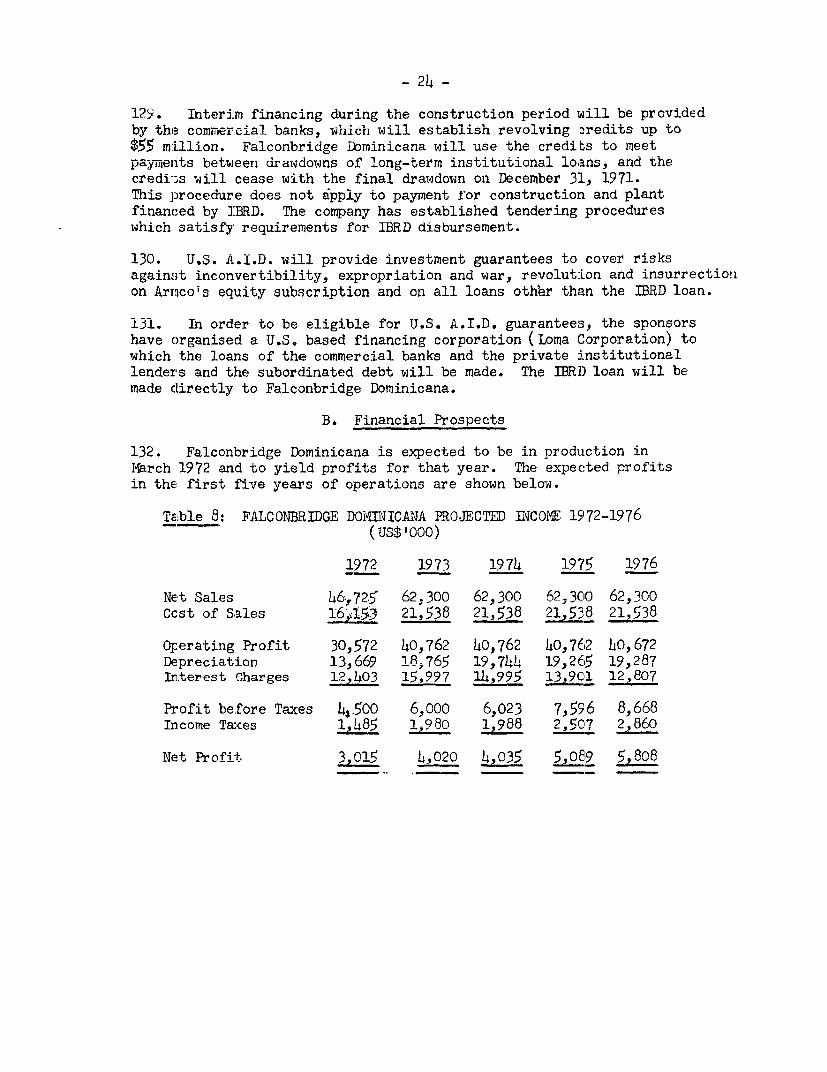

5. The project will comprise mining and transportation facilities,a treatment plant and a nower plant. The treatment plant is designedfor an annual production of approximately 63 million polnds of nickelin the form of ferronickel. The exmendit.ire on the eomnlete oroiectis expected to approximate $195 million.

1/ Culrrency throughout this report is expressed in US$.~/ The term "%tons"t in this report means short tons of 2 nOOv pounds.

- 2 -

6 Th.e GOvernen of the Donmnican Republic has 4-n lica *tssupport for the project and is prepared to guarantee the proposed loan.TI wever, the - -- sec rity for loar9 t-o F--1 'obie ^. na wil be£1~JW ~ ULM J 1 .JX C .¶LLA OV%.4L .LVY L%JJ L u IJ. JAJ"±~ I~LL~ --

the talce or pay clauses of the Sales Agreement between Fa]LconbridgeDro r,i-iL"cana "alconJ-idge C- adand A---oUVI5 X~~ £L ~ULALUU±Ur IAUtwu ut JLU A111kv.

7. Information on the project was s-upplied by raiconbridge Canada,Dillon Read and Co. Inc. of New York who are financial advrisors toFalconbridge, and by various technical consultants. at; thre request oIthe prospective U.S. institutional lenders, Sanderson and Porter Inc. ofNew York, a leading firm of engineering consultantss, made a comprehensiveexaminr&tion of the Dominican project and of the managementi9 technicaland firtancial ability of FiLconbridge Canada. During 1968 and 1969,several IBRD/IFC missions carried out field investigations in Canada andthe Dominican Republic.

II THE BORROWER AND SPONSORS

A. Falconbridge Dominicana C por A

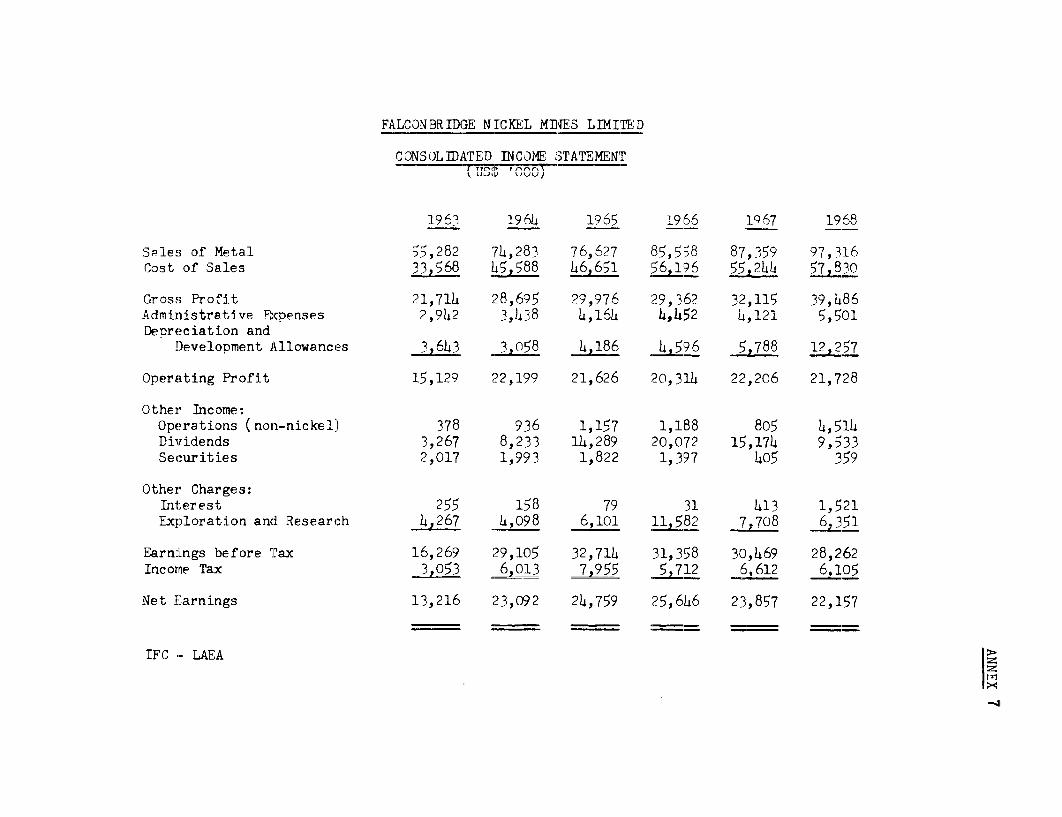

8. Falconbridge Dominicana is registered in the Domiinican Republicwith the head office in Santo Domingo. The issued capital consists of1,4,99,CGO shares of a par value of $10 each.

9. The shareholdings in Falconbridge Dominicana are:

Table I: FALCONBRIDGE DOMINICANA SHAREROLDfIG

F§lconbridge Canada 65.4Armco l/ 16.3Dominican Government 9.6Private U.S. and Canadian holdings 8.7

100.0

10. The history of the Dominican proiect commenced in 1955 whenthe Concession Quisqueya No. 1 (the Concession) was granted to Minera yReneficiadora Dominicana a nor A (Minera. . a cormanv controlled at thattime by citizens of the United States, who souglt associates to carryouit. thp nRnRsa.nrv investiotiatin and nPrnlnration. A nontrant wascompleted between Falconbridge and Minera, and a new company was createdunder the name of Minera y B neficJadoralFnnonhridnge Tominit-na G nor A.

lX Tr. 96 wbc..rih de Dmnm.ricar.a made a 1 for 2 Qhne isueapar' ($10). Falconbridge Canada purchased all of the shares

off'ered to the v-te aau.. ofP thea 1V y4.icr. P*pubic;4. l+ +aten

Government has the right to repurchase such shares at $10 perShI...a TI- 4ip o +h-e +I-. f411 v.a4man wil d +nhi. by supply=

t .4 Lu .LO v&WJ.k..so;NJ W,AL~ u uust W'-' ot;.*w,t u avj..&A. a-4% uns.j. Li JA YI.

ir,g services to Falcorbridge Dominica^a dluring he constructionperiJodl 4vo, +1fl 1,e v* Vr- o.fl l p' 3f C,fe s.-; A- 4-'Ž

L tI.. v Z V". Q.LAX '.Jl VIOIJ. L4AJ*~A J.~aa2t L& . .

- 3 -

which subsequently acquired the Concession from Minera. Later the nameof Minera y Beneficiadora Falconbridge Dominicana C por A was changed toFalconbridge I)ominicana C por A (Falconbridge Dominicana).

11. The Concession was orioginfl1v granted to Xhnera for a term of30 years, i.e., through January 15, 1986. In accordance with the provi--slonns -of the Minineg Lw a550 o,-' f 1056, w inera subs-qun"tly declared to tilet:> ~ ., ~, 0 - .1 -- -- ¾ --

authorities that the Concession would be governed by said new law:Falconbridge and the Do.mnrnicaJn G-overernment state that this declaration hasthe effect of making the Concession run for an unlimited period of timea-vd a notatio.- to- this effect is esntered into th be Plegistry. -W'ith Vileapproval of the Dominican authorities Minera assigned its rights to the

~~Lk)JI Uk)V LkV L3ure AJAI k).1 (i U)'LIUV.L4 .LJ. VIL iUk;tWIUUConcess-ion to vValconbri`ge Domin,cana on 'eceri-bier 14, 96 r eeb24, 1956, Falconbridge Dominicana and the Dominican Republic signed anagreement (vhe Basic Contract) determi-nig the respective rights andduties of the two parties with respect to the Concession. This agree-ment was sup] Lemented ani'd amended by a further agreement 'between theparties dated September 26, 1969 (the Supplementary Agreement).

12. Falc:onbridge Canada has been the technical sponsor from theinception of Falconbridge Dominicana. In January 1969, 20% ofFalconbridge Canada shares in Falconbridge Dominicana were sold to Armcc.Aitnou;n Armco will not participate inthe technical operation ofFalcon'bridge Dominicana, the company has distinct financial responsibil-ities which are described together with the financial prospects ofFalcon'bridge Canada and Armco in Section VI. The corporate backgroundsof the two companies are given below.

B. Falconbridge Nickel Mines Limited

13. Falconbridge Canada which owns 65.4% of FalconbridgeDominicana's issued stock is responsible for putting together the finan--cial package and will assume technical and commercial management of theproject.

14. Falconbridge Nickel Mines Limited was incorporated in 1928under the laws of the Province of Ontario, Canada. Since 1930, thecompany has been continuously engaged in the production of nickel andcopper, and has mining and smelting facilities in the Sudbury Districtin Ontario. It also has refining facilities at a wholly-owned plant inKristiansand, Norway. The company maintains general offices in Toronto,Canada.

15. The company is the third largest producer of primary nickel inthe western world and in addition has extensive shareholdings in othermining enterprises which produce copper, gold, silver, iron ore, magnesium,lead, zinc and some industrial minerals. However, the company's principalsource of revenue is the operations in the Sudburv Basin. Consolidatedrevenue for 1968 was $97 million.

- 4 -

16. Falconbridge Canada is a public company whose shares aretraded on the Toronto, Mbntreal and Vancouver Stock Exchange. Approxi-mate2v 80% of the outstanding shares are registered in Canadian names.McIntyre Porcupine Nines Limited, a Canadian company, owns approximately37% of Falconbridce. The chief shareholder of McIntvre is Superior OilCoMmpcny of Houston, Texas, which directly and through its subsidiary,Can-ar rn pintrrnr Oil TimitptA nwnq nnnrnximqstPlv '9t of McTntvre. The

gst single shareholding in Superior Oil Company is held by the Keclkfa m iJy Mb= HowTT R. .A- Keck iS a director And chief PcyrutivP offf7ieer ofSuperior. In Fbbruary 1969, following the death of Mr. Horace Fraser,the pres±dent of Prrnd, Tvfe Mmrch A. Gooper- fnrmrilv Presidentof McIntyre, became President of Falconbridge. Subsequently, Mr. Keck

~ ~ ,4rns+ ,.P U-T-+,- -,A - --,m4, n~+reA r'1-n4 ,.m_,i nv' nf4,'n,+.evr,* mfb Is. 4. s -- dera' of ,a-t.bye -.J was nomina*ed rJ.a4r,.n of Directors o Falconbridge.

C. l tIIoJ Ste Iel Corporation

stock. The company will undertake financial liabilities to FalconbridgeAoju in1cana for part oI the subordinated aeot, Tone overrun UULFWJiIJUMUb"Zand the take or pay clauses of the Sales Agreement, but will have nopart in the m:nanagement of operations.

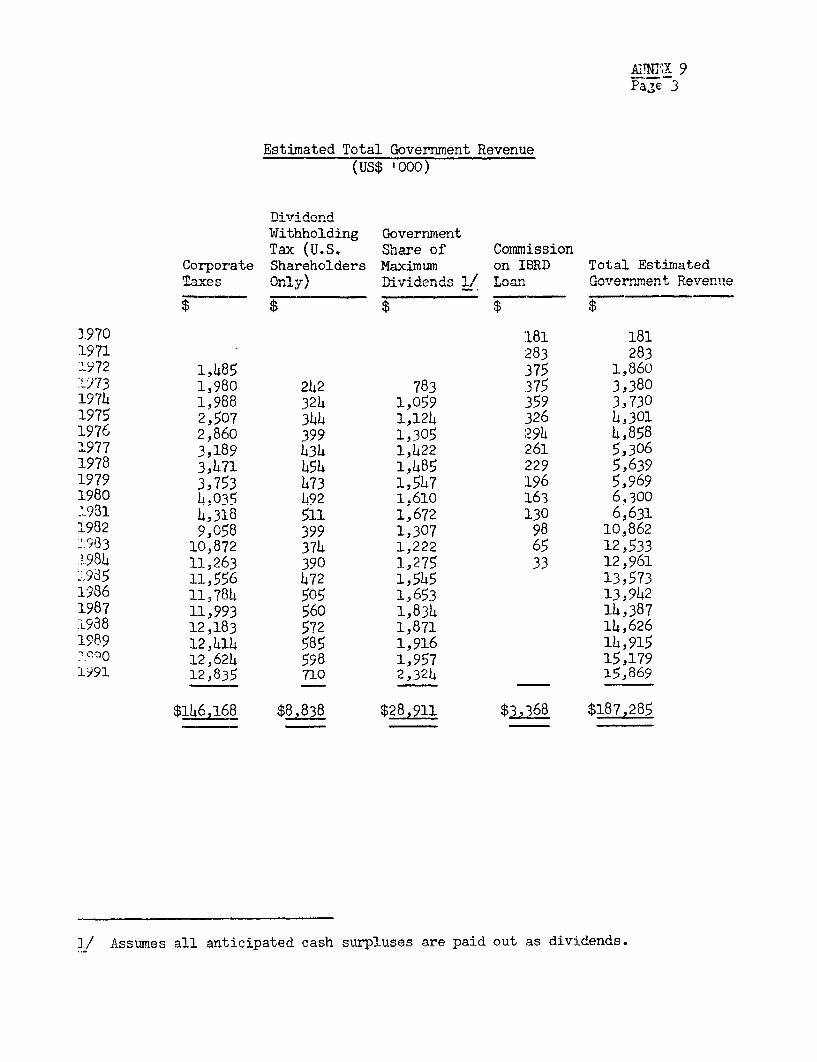

i8. Armco Steel Corporation was incorporated in Ohio in 1917 asthe American Rolling Mill Co. The present title was adopted in 1948.The corporation is an industrial complex that includes 9 steel-producingplants in the United States, 37 specialized manufacturing operations inNorth America and 24 manufacturing plants elsewhere in the world. Armcois listed on the New York Stock Exchange. l/

19. Armco is the fourth largest steel company in terms of salesin the Unitedl States. Its activities range from mining to the product-ionand fabrication of steel. The company manufactures various metalproducts, such as steel buildings, equipment for oil and gas drilling madrainage prodlucts. It has specialized in new steels, alloys and advancedmaterials for the aerospace and hydrospace industries.

20. The company uses nickel and ferronickel in its productiveprocesses, but the Sales Agreement will make explicit, FalconbridgeCanada's obligation not to give preference or price concessions to Armcoin selling ferronickel from the project.

D. Management Arrangements

21. Falconbridge Dominicana is incorporated in the DominicanRepublic, but the meetings of the Board of Directors and the annualmeetings of the company have been held in Toronto, Canada. At presentthe Board is lareelv comDrised of Falconbridge personnel. The President

1/ Total sales of Armco - $1.138 million in 1967. S1.375 million in 1963.

- 5 -

and Chairrmn of the Falconbridge Dominicana Board (Mr. Marsh A. Co=oer).is also Presicdent of Falconbridge Canada. The Vice President, (Mr. E. L.Healy) is Ryecutive Vice President of Fa1reonhrir1e and is a member ofboth Boards of Directors. Falconbridge Dominicana's General Manager andTreasu:rer are both from Facrbig aaa

22. T l alconbriLdge Dominicana .ntr.int

Technical Services Agreement with Falconbridge Canada. Under this Agree-4.en F,al c onb ridL-ge Canalda tWi12l manage a~n'd sne)ii h cosrcinanrd

operation of the project facilities.

23. The management fee payable to Falconbridge Canada is US$500,00'Jper annum, comi,,ier.cing from the date of ll-e general conssruc ontract.

After production commences, the fee will be 1% of the revenue ofra±LonUi±L1'gLUge JU lullUaIZA lr irvi wie Ca±e U1 pIoUUcuts Uer-±veu IUSIJ UXL>

Quisqueya No. 1 Mining Concession, with a minimum annual fee of US$500,000.IFC staff considers that this fee is reasonable for the services to berendered.

2b. Falconbridge Canada and Armco will enter into a Sales Agreementwith Falconbridge Dominicana whereby the entire output of ferronickelwill be sold by Falconbridge Canada.

25. Falconbridge Dominicana will transport the ferronickel tostorage facilities at the Port of Haina and will load the metal intoships provided by Falconbridge Canada, which assumes title to and riskof loss once loading is completed.

26. Falconbridge Canada is to sell the metal at competitive worldprices and deduct transport costs and a sales commission of 1 1/2%. Theobligation of the sponsors to obtain fair prices is made explicit inthe Sales Agreement. The proceeds of the sales will be paid in foreigncurrencyr to a T'rustee (a U.S. Bank) appointed under a Current AccountsTrust Agreement between Falconbridge Dominicana, the Central Bank of theDominican Republic and Loma Corporation (a U.S. corporation through whichloans, other than from IBRD are to be channelled). IBRD w,ill be partyto the Trust Agreement.

27. The Trustee will make payments for all obligations of FalconbridgeDominicEina including authorized payments to lenders, trade creditors andshareholders.

28. The Sales Agreement and the Management and Technical ServicesAgreement are to remain in existence until all loan obligations byFalconbridge Dominicana to IBRD and Loma Corporation lenders are ful-filled. Falconlbridge Canada will then have the option to review thesections of the agreements dealing with production, sales and othercommercial matters.

- 6 -

III. THE PROJECT

Intoduction

29. The project consists of the mining and metallurgical processingof lateritic nickel ore to produce ferronickel for sale on the worldmarket. Extensive supporting facilities including power generation,fuel pipeline storage and topping facilities, roads, water supply andhousing form part of the project. Power generation and atssociatedfacilities are discussed separately in Section IV since the proposedBank loan will be for the financing of the foreign exchange conponentof these facilities.

A. Mining

Exploration

30. Dominican nickel-bearing laterites have bee-n knowmn since thebeginning of the century. In 1918-19 a preliminary examination andsome sanpling was carm-ied out hv geologists of the United StatesGeological Su;rvey. A further survey by this agency in 1941-42 estab-lished the most pro-mising areas for fullscale

31_ In L!955 Falconrbridge geologists began a detailed geolopicalinvestigation and sampling program. The main ore-bearing areas were

saw le ;,rhpits a 100 eer 'Iaras and in -tain a.-eas at, 50 SmsetErintervals. Pitting was completed in 1958 and further sampling has^-nliriUeA us4Ing auger arda churn wu-u d-lng rLi fhUUb wruch fi iJaLte samplJngof the lower rocky strata.

32. Annex I tabulates the extensive sampling work carried out onthe ore deposits, and Tablel2 below summarizes the calculations of orereserves and nickel grades which have been checked and confirmed bySanderson and Porter:s consulting geologist.

TL-able 2; ORE RESMVES IN TIE QUISQuEM CONCESSION AKmA

JANUARY 1, 1968

Overburden Stripping Ore

No. of Dry Short Dry ShortArea Ore Blocks tons % Ni tons % Ni % Fe

Peguera 15 1479,000 0.81 17,987,000 1.64 19.6Guardarraya 7 1,683,000 0.79 11,173,000 1.52 19.2Caribe 11 3,162,000 0.85 26,058,000 1.51 -Guard Extension 8 305,000 o.84 3,505,000 1.54 -Fraser 5 666,000 0.83 4,118,000 1.55 21.2

Total 46 7,295,000 0.83 62,841,000 1.55 -

- 7 -

33. The company's estimate of ore reserves as at JaLnuary 1, 1968~i3 bhefelt1oI O63 iiLl on dry sIhoLtb uu Uof ore avera1r L..5)5 ickl,

this is considered acceptable. These reserves are sufficient for about25 yez.rs at the proposed level of extraction, and continnuing explordtionwork indicates that additional reserves of commercial value are likelyto be proven.

Geology

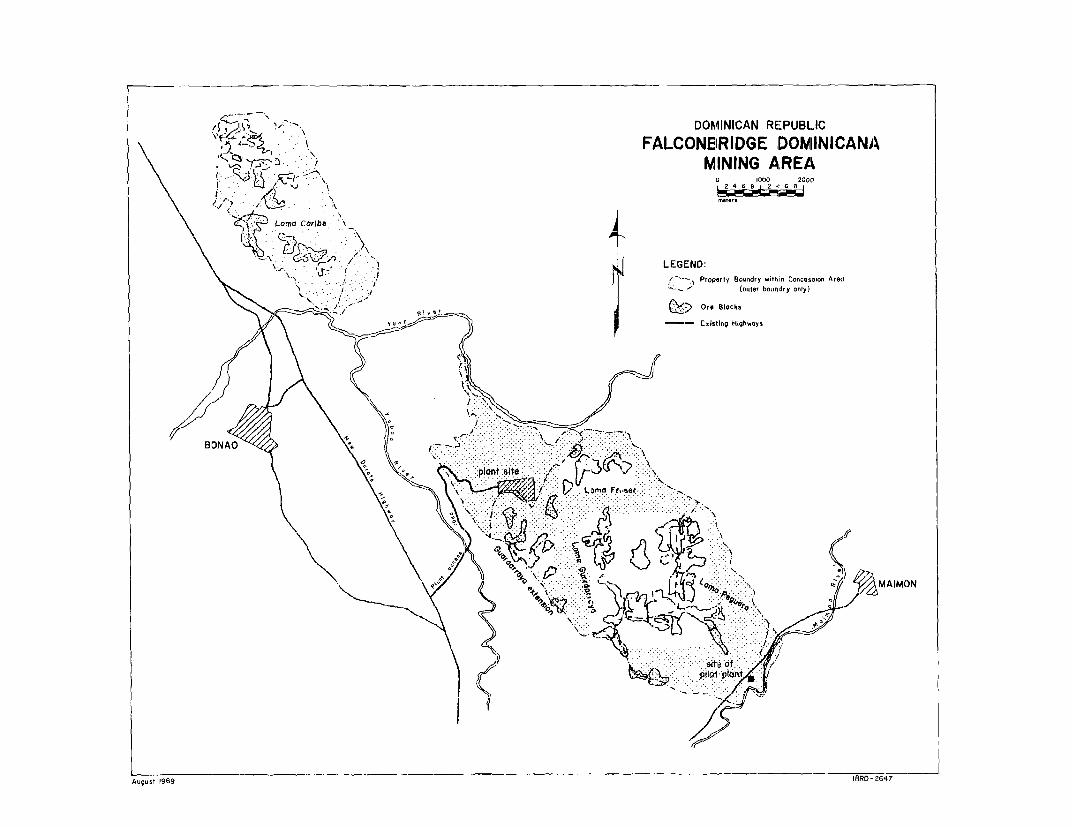

34. The ore deposits are dispersed over the length of FalconbridgeDominicana's concession area extending in a narrow zone from sierraPrieta about :L2 km. north of Santo Domingo some 100 km. northwest toLa Vega (see Maps). The deposits of commercial value occur midway inthe length of the Concession on the area.s of high ground where weatherirnghas prDduced a lateritic capping on the ridges and plateaux. In placesunder this capping secondary enrichment has taken place.

35. There are two general types of material carrying economicconcentrations of nickel: the overlying layer of laterite containing35 - 50% iron and 0.6 - l.h% nickel distributed relatively homogeneouslythroughout; and the underlying layer of rock at various s-tages ofalteration, which is heterogenous in character with iron varying from5 - 30% and nickel from about 0.8 up to b% in pockets of :Local enrich-ment.

36. The depth of ore varies from 1 meter up to 55 meters, but theaverage depth is around 10 meters on the main deposits.

Minine Plan

37. The variable nature of the denosits reouires the adontion ofa flexible mining system, which will take into account the dispersionof the ore bodies the lnrge nnd rapid e-hanges in the plet'.tinn of theterrairi and the variations in the physical and chemical constitution of

38. Minino, will he oarrieRd oit hb rnonventionnl strin mining methodn

using large bulldozers equipped with riDpers. No drilling and blastingwill be necessary other thnn to lear occasional la.rge rock int- uions.The ore will be loaded into trucks by L4 yd. diesel electric shovelsfrom a. nu..ber Oe"4 face s u s to provide fo bPg Because

of the large drop in elevation between most of the mining areas and ther.l nv~+.Cc4 +- m +-,^,.r.r -.,4+1&, -, , ,, .

411 1,k. -,,A 4.-. W1,-

US,VW s W U%.-Ltd n . UW 6 ,lSaJ ; V WL n...,4,6

WUL.J J U VWS L-U.A

ore from the various faces to the ore dump at the plant.

39. Becauise of the wide dispersion of the ore deposits and theneesit t o work a nsum,ber of ore bodies _1m'nosy,asbttane~cessJ.-- J4J W.L~ A . LL tULIJL %.J U.~ UUU.LVO O.LMIU.L LK-LUMULU,.)L~y 9 , 0UJ ~UU I Usd L±j.LdJ

road building program will be an important part of the min:ing operationsover the first Lew years.

40. The mining rate required for a plant output of 63,hoo,000 lbs.per year of nickel in ferronickel is about 16,000 short tons of run-of-mineore per day. Two shifts per day will be adequate to handle this tonnageusing the proposed equipment.

B. Processing

hi. The Falconbridge process for the extraction of ferronickelfrom laterite ores was developed by Falconbridge Canada specifically totreat Dominican ores but also with a view to general application else-where. Certain aspects of the process are the subject of patent applica-tions by FalconbridPe Canadaj buit. Falconbridge Dominicana is to haveaccess to the process without payment of royalties.

42. Pilot plant work was initiated in 1959 on a site adjacent tothe m,ain ore bodies. Progressive experimentation established 1-mprovedplant designs and operating techniques until the stage was reached wherea sa'is kr p r- es s h,a d 'been. developed. ihes imrovements were in-corporated in a large-scale pilot plant which was commissioned in early-196,' and operatLled on a continuous "-as-'s unt-i1 thI'e er.d of 'gu 1968,

when it was closed down, having successfully fulfilled its objectives.

43. This pilot plant was visited in July 1968 by engineering staffof International Finance Corporation, who subsequently concluded thata satisfactory technical process had been developed to produce ferro-nickel from the Dominican laterites.

44. The Falconbridge process has a number of attractive featuresincluding: all of the ore deposit can be treated without the need forselective mining; the flow sheet is relatively simple,and marketaDieferronickel is produced without any refining steps; and the productionof atmospheric pollutants has been minimized and there are no harmfuleffluents to pollute rivers.

45. Processing consists essentially of three successive stages -ore preparation, selective reduction, and electric melting. These aredescribed in detail in Annex 2.

46. The ore is upgraded and blended by autogenous milling undercontrolled conditions. Milled and screened ore is stockpiled and formsthe prepared feed for the metallurgical plant. Ore preparation is carriedout on a two-slhift per day basis; the other operations of the plant willbe continuous, three shifts per day.

47. Ore from the stockpiles is fed to briquetting presses which inturn feed the reduction furnaces. Carefully controlled conditions inthe furnaces produce the required degree of reduction of the briquetteswhich are then transferred to electric arc furnaces for melting andseparation into slae and ferronickel. The ferronickel is cast intopigs for shipment.

- 9 -

48. IThe overall recovery of nickel from run-of-mine ore toferr-onickel. is of the order of 81.5% and indicates an efficient process.

49. The plant site is located mid-way in the Concession area,about 90 kilometers northwest of Santo Domingo near the town of Bonao.These locations are illustrated in the annexed maps.

C. Water Supply

50. The entire water requirements of the plant and supportingfacilities are drawn from the nearby Yuna River which has a minimumflow of 60,000 U.S. gallons per minute. The company proposes to erecba cc,ntrol structure in the form of an earthwork or concrete dam whichwill direct a sufficient flow of water into an old channel of the riverthat runs alongside the plant site. This plan is being studied byAqueductos y Alcantarillados, S.A., a DoTminican company experienced inthis work.

51. A pumping station will be installed On thhe. old chan-nel witth apumping capacity of 12,000 gallons per minute, and storage capacity for800,000 galLons is provided. A water treatment plant filters and treatswater for the plant and power stations, and a separate treatment unitprovides dlrkinkig water. The pumping station and water treatment plantwill be included in the facilities to be financed by the Bank loan.

52. The make-up water requirements are about 6,00o gallons perminut o f W.hi rh about 4,000 are required for the power i'lant and thebalance for the process plant.

Ai. Transpor-t

53. Tit!o methods of traSr.port are used. The large 4' -' 0l of,eloil Xor the power plant and processing plant are transported by pipelinefrom a tanker unloading dock at the Port of Haina to storage tanks atthe site. Ihe port will have to be dredged from 25ft to 31ft alongsidepnie r t+o b e capabl, 1e o f b,e r thirn. g a '20nw,000A (4 4on ntan-r

54. Dieel oilsgasoline and ,,.iscellaneous s-upplies9 are 'ranspor'Le'dfrom Haina by road, and ferronickel is transported to Haina by road.

55.- The main road from Haina and Santo Domingo passes close to thesite, and a connection by a new access road and bridge over tne YuboaRiver is part of the project. The main road will be more than adequateto hasndLe thge additional traffic resulting from the proJect.

- 10 -

E. Townsite

56. It has been decided that accommodation at the plant site shouldbe limited to a lodge, some single quarters and hospita]L facilities.Tne main housing for expatriate staff is to be provided by an urbanisationschenme at the local township of Bonao (about 6 kilometers distant), andsome 75 family homes and 38 single apartments are required. Negotiationsbetween the Government and Falconbridge Dominicana on the provision oftownsite facilities and housing are in progress, and it is anticipatedthat the company will contribute approximately $2.5 million.

F. Project Cost Estimate

57. Table 3 summarises the latest estimate of the capital cost of theproject:

Table 3: PROJECT COST ESTIMATE

US$ million

Mining and mine road building 4.0Producltion and service facilities 47.0Power plant 17.3Pipelirne fuel storage and topping facilities 6.2Access road and bridge 1.4HousingP 2.5Port facilities 0.2Freieht 3.7Engineering and construction costs 28.0Proiect administration 4.0

Spares 3.3_ont.inoenr 12.1Escalat,ion 13.3

Total construction cost i4.

Pre-prc,duction expenses 1[tInterest and financing charges Working capital 10-4 52.0

Total project cost 195.0

58 ApproYiLmately 3 millinn of' t.he tota.jl nipronc conq+ will bepexpencled in the Dominican Republic.

59. The estimate for the process plant and service faciLlities, preparedby,. he -consu14ti -n, -eers A^.1,Av UH+cUh ar.d Asocaia+e,s~ To"ror.+o is

based on quotations received for the supply of major iterms of equipment;bthee reaA.aindher ofn thee equip aaent costs plu3s installatior. and cors"+ructon

costs were established in accordance with sound engineering practice,

- 11 -

using pertinent information obtained from supplies and contractors and theirpast experience with the construction of the two pilot plants. Estimatesfor mining and mine road building were determined in a similar way byFalconbridge. The cost of the access road and bridge into the plant sitE!was estimated bv the Comnanv's (onsultants. Marshall Macklin Monaphan Limitedof Don Mills, Ontario. The power plant estimate is described in Section IV.

60. 0bher installations were defined by company personne'l in accordancewith erperiencej cuirrent data where available and normal sond practice

61= The general corntingency allcnaence of $12. 1 million is' approxirmately10% of -the installed cost of the plant and other facilitieis. Price

eim4J.'l L -sL- h,as be et,n.atied at 4 - _per an.u.. givin4a total of $13.3 million from 1968 through 1971.

62. The detailed build-up of this capital cost estimate has beeniscusse d andU e.va]uated w £ U1 lc11dg i officials, an d4 4 -l;e .l - s

accepted as reasonable. Sanderson and Porter have also reviewed- lconbridgtjt U±, CoLiS c ruc Lu±u Costs aniu liave CuHIirujeu Laemm

to withiLn 1%.

G. Engineering and Construction

63. TLe primary responsibility for the engineering and supervisionof the project will lie with Falconbridge Canada's general engineeringdepartment. Up to the present they have contracted out the major workin design and engineering to a number of consulting engineers.

64. The mining aspects of the project have been the responsibilityof Falconbridge Canada. The production and service facilities have beencontracted to Atkins, Hatch and Associates of Toronto. Uther consultantspresently involved in the project are:

Scrgent and Lundy of Chicago - power plant

Pipe Line Technologists Inc of Houston - pipelines

Marshall Macklin and Monaghan of Toronto - access,road and bridge

William Trow Associates of Toronto - s6il testing

ILternational Water Supply Co. of London, Ontario - water supply

Ac[ueductos y Alcantarillados of Santo Domingo - water supply

All of these consultants are well qualified in their fields.

- 12 -

65. Engineering work is at present about 2,5% " c0 pleted ar.d a num.beof bids for the major plant items have been received and evaluated.The a,ctual construction will be performed by a general contractor assistedas necessary by the various consultants. The main contractor,Brown and Root Inc of HoIuson Texas was selected fom bids receivedfrom four leading companies all with experience in the Caribbean area.I is expected tuba utie contracuor will ut on s±te wiJ.IALI nex

three months and in anticipation, clearing and drainage works havecommenced. The contractor will be paid on a cost plus fixed Lee basls.

66. Tne construction of the access road and bridge has been let toa local contractor, and is well advanced.

67. The project is scheduled to start up in March 1972.

H. Procurement

68. The procurement of the Bank financed facilities is beingcarried out according to usual Bank procedures (see Section IV).

69. The procurement of most of the remaining plant and equipment istied up with the proposed United States Agency for InternationalDevelopment (U.S.A.I.D.) guarantee of the other lenders and consequent]ybids are beirng obtained mainly from U.S. and Canadian suppliers. It isprobable that about 10% of machinery and equipment will come fromCanadian sources.

I. Personnel

70. The total number of persons employed in the Dominican Republicwill 'be 1,15C); an additional staff of 9 will be required in the HeadOffice in Toronto. Of this total, expatriate technicians or administrcativepersonnel wi]l number 81. Of the remaining 1,069 Dominicans, 411 willbe classified as unskilled although some may be doing work above thatof lalborer.

71. No diff'iculty is anticipated in obtaining the required number ofDominicans and Falconbridge will provide or recruit the necessaryexpatr,iate personnel. The pilot plant operations have provided anucleus of key personnel for the start up of the commercial operation.

J. Production Cost Estimates

72. The production program envisbges start up in March 1972 andadditional expense during the running-in period until June 1972 has beencapitalised. Cost estimates shown in table 4 are based on a normalyear.; oneration.

- 13 -

73.

Table 4: ESTIMATED PRODUCTION COSTS

US$ % of Total

Mining

Labor 751,000 3.5O+her 93.-7 180 , 7.8

T 11 nf%^~~~~~' ~r' nVA'I~ 0Labor 5,35,0 2l4.UFuels 9,362,000 43.4M SL _- _ /.I -- _ I OUl1the rmater-ial anU supplies 2,67,000uu .4Services 1,659,000 7.8

Toronto office 198,000 1.0

Management fee 623,000 2.8

$21,538,000 10.0.0

Equivalent to per lb. nickel in ferronickel - 3l&.

7T. The important items of cost are labor and fuels, which togetheraccount for about 75% of the total cost. Labor costs have been conser-vatively derived on anticipated wage rates and a productivity factor ofhalf that which would be adopted for North American conditions. Fuelconsumption is based on the large pilot plant operations and on wellestablished rates for power generation and for earthmoving equipment.Costs are calculated on current market prices for fuel. T'he consumptionrates for other materials are also based on the pilot plan,t operations.The current estimate of annual operating costs seems soundly based andis therefore accepted as reasonable.

- 1, -

IV. BANK FINANCED FACILITIES

A. Descrintion of Facilities

75. The proposed Bank loan will be to finance the foreign exchangeportioris of the thermal power generating station, a ninnln to tasport crude oil from the Port of Haina to the plant site and a toppingnit at the site, to convert +e crde in+o appropriate -ractions. A

portior, of interest and other charges on the loan due during constructionwoll-ld be irncluded as well.1 The_ power -sttir 4s to be 4integral p-4t-, ~ ~ W~.&.A* *J~ PWMZ Ud ~UJ.LL .LW O d IA U CLI~ ."1.± C.J_ jJOJ.u

of the project designed to provide power only for the ferronickel process-i.g5 pl-a.+.' and. ar,cl..L al e '.Jhe pJowe.Lr statCLo.L WLl opeat Uat'.LdAd' did

the same frequency as the domestic electrical power system, so that inter-conn.ection in uthe fu uwe is nou preci l j LUUde.

76. The thesrma1Ll pUower b ation with a capacity of 198 iVTw will consistof three 66 IAW turbo-generators, boilers and associated ecuipment, in-cludiung water supply and treatment plant. Ine generators are of conven-tional design, operating at a voltage of 13.d kV, 0.85 power factor,three phase, sLxty cycles and hydrogen cooled.

77. Each boiler, of the fully outdoor type, has a capacity of 600,000lbs. of steam per hour, 9500F, 1,250 psi, and is fired with heavy fueloil. Condenser cooling water is recirculated and cooled in heat exchangertowers. The overall heat rate of the thermal plant is estimated at10,750 BTU/kwnh, based on the boiler and turbine contracts. The outputof the power p:Lant will be transformed to 34kV for primary mine distribu-tion and operation of the smelter furnaces.

78. The pipeline has a diameter of b", is 44 miles in length and hasthe capacity to transport up to 5.0 million barrels of oil per year.The topping unit converts crude oil into fuel oil and higher petroleumfractions by volume ratio of 60 percent and 40 percent respectively,giving an annual fuel oil capacity of 3 million barrels, compared withan estimated fuel oil requirement of 2.5 million barrels, includingabout 300,000 for the ore drying kilns. Adequate storage facilitiesat Haina and the plant site would be provided.

B. Cost Estimates

79. The est;imated capital cost of the thermal station and associatedfacilities is shown in table 5 below:

*1!El- 15 -

iabe-u- 5: WnnIl CUDI linIirl

Local Fore!ignCurrency Gurr.ency Total($'000) 77-075) ($1000)

Tnermal StationCivil works 900 1,600 2,500Equipment 2,200 12,6100 lh,OuuEngineering services 150 2,300 2,450Contmingencies 50 80c0 _ 850

3,300 1,3,, O,u

Associated Facii'vitiesToFping unit 100 2,200 2,300Pipeline and storage facilities 500 3,400 3,900Engineering services 150 600 750Corntingencies 50 500 550

Grn -T /. 1U, ocvu 28,1

UVL1±ud mU £LL,UU\.) eU .LUU

80. I'he es-timated total cost of the thermal station and associatedfacilities amounts to $28.1 million with a foreign exchange componentof $2h.0 million, exclusive of interest. The Bank loan would financethiS Z'lt.O million and a nortion of interest; estimated at less thanhalf that which will be payable during the construction period.

81. The estimate of the cost of the thermal station was prepared bySargent and Taindy of rhicago c-nsuling engineers for this part of theproject. As virtually all of the contracts for the thermal plant havennw beehn placed on a firm. price basis the -onntingencyv allowance includesonly a nominal amount of about 5 per cent. The unit cost of the thermalstatioin is $103 per kie uohich is w-el below average for a plant of this t rpeand results from the favorable contracts placed.

82. T7he cost estimate of the pipeline and accessories uslit was madeby PplreTecbnol ogi4sts T-c, Houton Teas - h - re vh. nineso

this part of the project. This firm operates on a world-wqide basis andi;s hi.;g}'y -Aeie e so 4that 4-he estimate,- based on s veys fPor theik.L~ ~~LLj y experiencied.L~ ov b1m.v U1 th .LJL&V. , ~O ' iJLA 01U g.Y V .1 'J lU11

routing, should be adequate. An amount of 8 per cent is :included for

03nting ordcer to meet th schaedule in Spite of delaysaireaching final financial agreements, expenditures for engineering servicesof -up lo $1 million, and for equipment of -up to $0.5 mill:on are beingincurred prior to signing, which mould be eligible for reimbursement.

84. Disbursements would be for the CIF cost of imported materialsand equipment required for the project ana for the Iforeign exchange cos tof civil works and engineering services, together with up toUS$1,Ci00,000 for interest and other charges. if, at such time as projectconstruction is sufficiently advanced to indicate there may be surplusfunds to any of these requirements, consideration woula at that timebe given to disbursing them for other categories.

C. Operating Cost - Thermal Flant

85.. Crude oil (Bunker "C") is estimated to cost $1.70 per barrel($Il.5O per ton) CIF Haina, with an additional $0.05 per barrel,repreEsenting the operation cost. The total delivered cost of fuel oilto the thermal plant amounts to about $0.28/million BTU and is reasonablylow priced.

86. The cost of fuel will amount to about 3 mills/kWh and operationand ma.intenance charges will add a further 1 mill.

D. Power Requirements

87. The metallurgical plant comprises three electric meltingfurnaces (Annex 2) taking a total of 120 MS under normal operatingconditions and a holding furnace and ore preparation facility requiringan additional 30 MI. The estimated peak demand is 172 MI. Total annualenergy consumption is estimated at 1.22 billion kWh giving a load factorof 81 per cent.

E. Engineering, Procurement and Construction

88. Economic and other considerations dictated that the thermal plantshoulcd be located at the site of the production plant and the fueltransported by pipeline.

89. Equipment and materials for the thermal plant and associatedfaciliLties are being purchased on the basis of international competitivebidding excent in the case of minor items for which such bidding wouldbe impractical. The general construction contract has been awarded toSociedad Venezolana de Electrificacion G.A. of Venezuela. followinginternational competitive bidding. There are separate contracts forthe nurchase of other maior comnonents of' ele.trinal eqpmrnent, for thefabrication and construction of the pipelines and of the topping unit.

90. The schedule calls for the placing of most orders during 1969and full-scale operation of the pnwer plant by the end of 1971It is likely that most, if not all contracts, for the thermal plant,

as this was necessary to meet the schedule.

- 17 -

v. THE MAR KeT

A. General

91. The principal use for nickel is as an alloy element in wroughtand cast steels and non-ferrous alloys. When alloyed with othermeta:Ls it imparts strength, toughness, hardness and ductility, togetherwith resistance to oxidation and corrosion. Despite reSearch overmany years to find a cheaper and more plentiful substitute, littleheadway has been made.

92. Although the use of nickel is widespread throughout industrialisedcountries, almost 90% of the non-communist supply is produced bythree Canadian companies and a company operating in New Caledonia,due to the fact that the principal nickel deposits that have beenuntil. now exploitable commercially, are located in these two area9of the world.

93. Primary nickel is traded in three main forms - reiined metal,oxide and ferronickel. In addition, a considerable quantity ofsecondary nickel is recovered principally from stainless steel andnon-ierrous alloy scrap. The major consumer of nickel is theIJnit.ed States whieh anrniints fnr about )40% of the total nonsumotionin the western world.

9h. The principal companies engaged in the mining and processingof nrnima'ry nickepl nre Tn+.trnati ona1 Niclekel of anndai (bh faqr the

largest), Falconbridge and Sherritt Gordon, also of Canada, Hanna Miniagof the TTni+edQn+ Stte an Te NNick01 ofP New rCaledonia. =5)6 estimate

produLCtion of these companies was:

million lbs.

International Nickel lt80TLe IEJ;1.UIi.kel 8Fa-Lconbridge: ;; 72

Henna Mining 26

95. The major consumers in 1968 were:

milliLon lbs.

United States :320Europe (including UK) :317Japan 129Canada 22

- 18 -

B. Consumition

96. Nickel has many import-ant and vnried nses hit by fnr the largestquantities are used for the production of ferrous and non-ferrous alloys.Table 6S shows the distrhiuti+n of' Pnd-ge averaePd fr fr +nh neriod 1998-67.

Table 6: DISTRIBUTION OF END-USE OF NICKEL

b. Alloy-steel - wrought 13.0c. Ir-on and steel cast-ings 11.1

d. Electroplating 15.6e. NiJ.cke.l al.loy ''.94

f. Copper alloys 4.0g. OJhE' Wr tuses 79.

Y9. The nicKel consumed for tne various end-uses can ce dividedfrom the application aspect into two product classes. Class I includeselectrolytic nickel and other pure forms of nickel and nickel salts;Class rI includes ferronickel and nickel oxide.

98. End-use categories d, e, f, and much of g, require Class Imaterialis for reasons of production technology. Categories a, b and c,which account for about 57% of total consunmption, can use either ClassI or GLass II but are tending to swing to the latter since the unitcost is lower.

99. Most of the above uses have good growth prospects. For example,the use of stainless steel is increasing steadily in important manufac-turing industries, including automobiles, aircraft, domestic appliancesand building. The use of low and mediumn alloy constructional steels isincreasing at a rate of growth considerably above that for steel as awhole. Space-age superalloys also promise an increasing requirement fornickel. The excellent corrosion-resistant properties of nickel electro-plate should aLso assure a steady, if not spectacular, growth area.

100. Because of the relative scarcity and high cost of nickel, metal-lurgists have for many years carried out research with a view to develop-ing alLoy compositions in which nickel could be replaced by cheaper andmore p:Lentifu]. elements. So far however, only limited success has beenachievted. In some applications such as high temperature alloys for gasturbines, substitute materials impair performance; in othiers such asalloy steels, the possible substitute elements like molybdenum,vanadilm or chromium may be in even more limited supply. In certainstainlless steel compositions, the technology is proved for substitutingabout half of the nickel content by manganese; however, a real incentiveto make the change has so far been lacking. At this point it does notseem likely that substitution of this kind will result in any seriousrp.,ine1t.-inn ir, tl:p. 4,-_mqnri fnr ninkpl.

- 19 -

101. World conRumntion of nrimarv nickel has grown eLt an averagerate cf 6% per annum over the period 1947-68. Total consumption whichr_ehd npe of Sin million Ihb in 196h. fell to 810 million lbs. in1967, and was expected to reach about the same level in 1968. Thisapnnrtmntlu q-..ntie- th?-pp_vpy.r nprid was nrofoiinidlv affected bvydficiencles

of supply and in 1967, 40 million lbs. was made available from the U.S.stoc4rrile- W<lcon.hridge Canadn, on the basis of nvnilahlpe market inform-ation, forecast that consumption will continue to increase by approximately6 = 7% anr.nually to about 1.2 billion lbs. b'y 1Q75 This estimate gnsumnsthat the utilization of secondary nickel will increase proportionately.

102. Taking into account the dynamic nature of the end-usingM =Q4 W 1.L. '.f VLF U V I .L 'i UAL~ 6 U ~C'V ~ 'v -

rate cf growth is a reasonable assumption.

J * o UIJ,J.,y

103. lnnex J gi-ves details of the historical pattern of supplyover the period 1955-67 in terms of mine production of recoverablenickel, and FalconDridge's forecast of possible future production forthe period 19,68-75.

104. The following points should be noted with regard to thesefigures. First nickel production over the period 1955-67 has beenconsistently Less than reported nickel consumption. The reasons for thediscrepancy !ie in purchases and disbursements by the U.S. stockpile;imports from Communist countries; and changes in consumers' inventories.Thus past experience shows no indication of over-supply of nickel,even for short periods.

105. Secondly, in many cases, the ore mined is semi-processed at athe mine site and refined at another location. For example, some of thematte ! produced by International Nickel, and all produced by Falconbridgein Canada, is refined in England and Norway respectively, and matte fromLe Nickel in New Caledonia is refined in Canada, France and Japan.

106. Thirdly, there is considerable difficulty and uncertainty inattempting to forecast future changes of nickel production, since notonly the deveLopment of existing mines is involved, but also the open-ing up of undeveloped newly-discovered or as yet undiscovered deposits.

107. The forecast is based on many published trade reports, informa-tion obtained from Government departments and other sources of intelli-gence concerning the development of nickel deposits around the world. Ethas to be recognized that plans to develop deposits may change betweennow and 1975 but this is not calculated to influence unduly the supplypicture. W,hat might upset the balance later is the exploitation ofdeposits not yet discovered or proved. However, this factor could notbe expected to make a serious impact before 2975. Annex f briefly

1/ Unrefined nickel sulphide

- 20 -

descri.bes the naJor developments that have been taken into considerationin making the forecast.

108. Over the last few years the picture has consistently been ofa supply shortage that may well have restricted potential] consumption.Consicderation of the probable future supply/demand position indicatesthat sun approximate balance is likely to be- achieved up t, 1975;especially if it is assumed that mine production will not exceed 90% ofprojecrted capacity. IyWTevertheless1 delays in opening new deposits - anot unlikely possibility - may mean a continuation of the tight supplysituation for a year or ta,i w. In d virtiua In trol of nickel

mining rests with three or four large producers, which suggests that newipr-.flJ wilI be developeA at a rate wV"Lnjch.,L wllj aVoid a se-riou9orer=

supply situation.

UD Prospects Lor £Ferronicke.LLA.

.LU7 r* .L "e broad pictUare oJ spply anu GENU,an f'or nickel, the

particular case of ferronickel is of special importance.

ULO. The development of ferronickel production for the years 1955-1967 is shown in Annex n.. Growth which has been rapid and relativelyconsistent over the period, averaged 15% per annum. This is more thantwice the rate of' increase of total nickel consumption for the sameperiod.

111. TabLe 7 below shous Falconbridge's forecast of world productionof the different types of nickel product.

Table 7: PRODUCTION OF NICKEL

1966 1970 1975

Class II

Ferronickel 19 19 29Nickel oxide _5 20 17

34 39 46

Class I

P1ure nickel and salts 66 61 54

100 100 100

- 21 -

112. The sharn increase in the nronortion of ferronickel hetween1970 and 1975 is due to the unit cost advantage of ferroriickel as com-pared with pure nickel. and to the intrrPa'dr1 avniuI ility of ferro-nickel. Whereas it is forecast that 39% and 46% respectively of totalnickel produced *in 1Q70 and 1Q7n 711will be Motas TT m*rin, thepotential maximum consumption from the technological aspect is of the corder

11~~ TI-*+~I.AA1. ------ A 1.v

IFC, that the supply and demand situation for nickel up to 1975 will bereasonably Jir. ---- baarc ar.d -4-4 poe.tia der,,JLL&PJCLJ%~ LAAULL PJWA.C4 LUan.d fPor fLerronicAc'sl mlay,

perhaps exceed the available supply.

E. Il.r11ybketing ald Price

1'w.4 ralconbridge Canada will contract with Falconbridge Dominicanato purchase the entire output of ferronickel. Falconbridge Canada hasa worldwide saues network in nickei and other metals and is experiencedin this business, so that it can be reasonably assumed that the salesorganization vill be adequate. During the period 1964 - 1968 the pilotplant :Droduction of ferronickel has been sold to a large number of steelmakers in North -nerica and Europe in order to test acceptance. WIrittenoffers have been made to a number of consumers undertaking to deliverspecific quantities starting in 1972. Favorable verbal and writtenrespon3es have been received, and within the limitations cf the deliveryand purchasing intentions expressed, it may be said that 150 millionlbs. amnually (or about 80% of the projected output) has lbeen tentativelyaccepted on the market.

115. Unde!r the terms of the iCanada will take delivery of the ferronickel, FOB vessel Port of Haina.The realized value of each shipment will be the CIF sellinlg price ofnickel contained in the ferronickel received from buyers in the UnitedStates and Europe. Under this Agreement the estimated ne-b FOB priceused in financial projections of this report is 98.26 cents per lb.after deducticns for sales commissions of 1.5% of the market value lesstransportation costs.

116. Sales will be made according to competitive commercial terms,without special concessions for any purchaser including AiRMCO.

117. The price for cathode nickel in the western wor:Ld has risensteadi]y over the last 10 years from $0.7h per lb. in 1959 to $l.03 in1969. There is little reason to expect a decline in the f!uture in viewof the rising costs of production in Cnnadrin mines and the fct that.serious over-supply is unlikely for the next 5 years.

- 22 -

VI. FICINGi P-LAN AND FINANCIL PROSPEClT,

118. Projected Income Statements, Sources and Application of FundsStater,lents and Balance Sheets of Falconbridge Dbmini cana, FalconbridgeCanada and Armco are attached as Annexes 4 through 6.

A. Proposed Financing Plan

119. The total,financial requirements for the project are estimated1at $195 million. _

120. The proposed sources of the project funds are:

Source of Funds Amount of Fund.s %US$ Millions

Equity investment 15 7.7

Subordinated debt 34 17.5

IBRD loan for power plant and relatedfacilities 25 12.8

Medium-term commercial banks' term loanfor treatment plant and working capital 41 21.0

Long-term private institutional loans fortreatm.nt plant and working capital 80 41.0

195 100.0

121. Eq-uiuy u ue vai-ue OI 5,5)5 miiilon is tne amount, or issuedstock of Falconbridge Dominicana. An additional $34 million of sub-ordinated loans is to 'be made available by the sponsors as quasi-equity,resulting in an effective debt to equity ratio of 75:25. The subprdi.neted loan,are to be preided by the three.U.Si-insurance companist%that are-provd:Lng t:,?-long-term loana. The debt is subordinated fQr repayment and security and wirank after Falconbridge Dominicanais other borrowings. However, it willbe guaranteed to the insurance companies by Falconbridge Canada and Armcoin the proportion of 60%u and 4u$. Subordinated loans will, have a term of22 years withl? year grace period at 81-% interest.

.L PrCject cost estimate is shown in Table 3.

- 23 -

122. IBRD has been asked to provide a loan of $25 milli:on towardsfinancing the foreign exchange costs of the power generation facilities,pipeline and other ancillary services, which are estimated to cost$33 million. The loan which will rank equally with the senior loansfrom banks and institutions, will be senior in security to the subordi-nated debt and will be made directly to Falconbridge Dominicana. Theterm of the loan is 15 years with a St years period of grace.

123. Falconbridge Dominicana proposes to repay the IBRD loan withsemi-annual equal-payments of principal which returns thet bulk of theloan funds to IBRD earlier than the normal level line met-hod.

124. Long-term loans of $80 million will be provided by the followingcompanies in the proportions shown:

M4etropolitan Life Insurance Company - 60%Equitable Life Assurance Society - 20%Nlorthwestern Mutual Life Insurance - 20%Company

125. The repayments on the principal commence in 1976 and the loansmature on June 15, 1986. The interest rate is &A%, payable semi-annual:Ly, and, the commitment fee is ½6_ of 1%. The loans will rankpari passu with the IBRD loan.

126. Medium-term loans totalling $h1 million are being provided bytwo banks; the First National City Bank will lend $21 mil:Lion and theCanadian Imperial Bank of Corinerce $20 million.

127. Repayment of the commercial bank loans commence in 1972 andthe loans reach maturity on June 15, 1976. The rate of initerest is8% and the commitnment fee is ½ of 1%= The nommPercial bank loans willrank pari passu with the IBRD loan and. the $80 million loans from theinsurance companies, and will have a term of 7 years including 21½ yeargrace period.

128. Falconbridge Canada and Armco also agree to provide all additionalfunds needed to com-plete the nroieAt in the event of cost overruns.Such additional funds will be provided on the same 60% to 40% basis and.there i.s no liimit to the amount un to a time limit of JanLarv 1, 1974.In case completion is not feasible or the sponsors decide to abandont+he project the sponsors undertake to repay pro rata the unnaid balanceof the Bank's loan.

- 24 -

129. Interim financing during the construction period wAill be providedby the co-mmercial banks, which will establish revolving credits up to$55 million. Falconbridge Dominicana will use the credi-ts to meetpayments between drawdowns of long-term institutional loans, and thecredits will cease with the final drawdown on December 3:l, 1971.TLhis procedure does not apply to payment for constructioni and plantfinanced by ]:BRD. The company has established tendering procedureswhich satisfy requirements for IBRD disbursement.

130. U.S. A.I.D. will provide investment guarantees to cover risksagainst inconvertibility, expropriation and war, revolution and insurrectionon Arrnco's equity subscription and on all loans othler than the IBRD loan.

131. In order to be eligible for U.S. A.I.D. guarantees, the sponsorshave organised a U.S. based financing corporation (Loma Corporation) towhich the loans of the commercial banks and the private institutionallenders and the subordinated debt will be made. The IBRI) loan will bemade clirectly to Falconbridge Dominicana.

B. Financial Prospects

132. Falconbridge Dominicana is expected to be in production inMarch 1972 and to yield profits for that year. The expected profitsin the first five years of operations are shown below.

Table 8: FALCONBRIDGE DOivIfICANA PROJECTED INCOME 1972-1976- - ~~~~~(uss'ooo)

1972 1973 197h 1975 1976

Net Sales h61-72-r 62.300 621300 62 3cio 62?300Ccst of Sales i6'i53 21,538 21,538 21,538 21,538

Operating Profit 30,572 40,762 40,762 40,762 40,672Depreciation 13,669 18,765 19,744 19,265 19,287Interest Charges 12,403 15,997 1h,995 13,901 12,807

Profit before Taxes 4h-500 6,ooo 6,023 7,596 8,668Income Taxes 19485 9980 1,988 9,50r7 2,80n

Net Profit n - c1 4 5

- 25 -

133. The financial projections (shown in full in Annex 6) indicatethat the net profits will be about $4 million in the early years of theproject and w ll have grown by 1980 to more than $8 million. Depreciationallowances (10% per annum on $180 million of the investment and5% per annum on remaining $15 million) will be substantially exhaustedby 198L and subsequent annual net profits range upwards from $18 milliorn.These profits are estimated to exceed $25 million annually after 1989.

134. The yield of the investment to the company is the after taxprofits plus the interest on the subordinated debt for each particularyear on the total of the equity and quasi-equity. For the first fouryears of operations the yield averages 16.1%. The yield in 1976 is18.3% and increases in 1981 to 24.3%. Th re mainr dpnrecia-tion allowancescease in 1982 and yield in that year is 44.0%.

135. The discounted present value of the investment is 16.8%.

136. In each year income from operations and depreciation allowancescreate sufficient funds to meet the debt servicing requirements of thecompany. In 1973 the portion of debt due for repayment in that year iscoverer- 2.01 times b,ty available funds, and in the three subsequentyears the projected coverage averages 2.1 times. The repayments of thelsrncei"nnr-m co..panies loans - 4.nCp in 1076 and av-Iable f'u.nds in the

five subsequent years are expected to cover debt repayments 2.6 times.ine fAne ox fu6. ds statement which re"ates to debt repaments is s ,win Annex 6.

- 26 -

137. The flow of funds indicates T+at the period !Th(in w h +he costsof the entire investment are returned to the sponsors is 71½ years from

I ?.T0 A4-,p4n - A Ann,, 4-l

that, apart from an unspecified reserve and minor reinvestment, all sur-pls iAunds whue oVII LrtL1d.Lng, fLro, operationsLLS or fror,. de,preciation,

allowc.nces would be distributed as dividends. The tables showing returnsto %1 JtJUe! L±L1L.cdaL UUV;tuLlUtI hacLve biteei UcldaULUtedU Uon f,his- basis.

C. Debt Servicing Guarantee

139. Alth-ough Falconbridge Canada and Armco are assured of A.I.D.guarantee against inconvertibility, expropriation, and war, revolutionand insurrection and have the protection of force majeure clauses, itmay become necessary for them to assume debt servicing (see Section VIII).Their ability to do so is demonstrated below.

Falconbridge Canada

140. In the period 1964 - 1968 the annual sales of FalconbridgeCanada have increased from $74 million to $97 million, which is anannual growth rate of 7%. Gross profit on sales have averaged 39% overthe period (see Annex 7).

141. Annual net earnings after tax of the company have ranged from$22 million to $25 million over the 5 year period with an annual averageof $23.9 million. Net earnings after tax in 1968 represented 22.7% pro-fit margin on sales.

142. Since 1965 Falconbridge Canada has spent $100 million on majorexpansion and modernization projects in Canada and Norway. Furtherexpenditure of' $180 million will be made on plant and mines in theperiod 1969 - 1975.

143. In its investment program Falconbridge Canada has seldom usedloan funds. Short-term loans from banks in December 1968 were $25 millionbut there werei no substantial long-term debts. The short-term creditwill be retired in 1969 while a small continuing mortgage relates to thefinance of company housing. Capital required for expansion after 1970 isgenerated entirely from internal sources. The debt to equity ratio wasat a peak of 17:83 in 1968 and is expected to be 0.1:99.9 in 1970.

144. The company expects increases in profit of about 30% annuallyun to :1970 as new projer-ts hPeGOm onprative Higher depreciationcharges lower the net profit after 1970, but total funds provided fromorprn+a:nnL nare, conicstz+.en+.tl abnhaver tA T4nmllieonn in ^ vaor frrom 1970-

- 27. -

145. Falconbridge Canada's projected funds are sufficient to coveriL US 0 li/O aCLULLiyU Fa U.L Mconbridge £LL1irc bL1 y '4.) t,.ir,,es in L79J7 adIU LJ'y

2.0 times for the whole of the first six years of operations. In addition,over the sa!t( period, the comJpa-ny canLLaintain the payrt,eat of dividendULat the current rate.

146. The :Loan potential of Falconbridge is considerable as borrowingsare negligible after 1970. The company nas tne financiali capacity toborrow4 and service up to $260 million, which is $150 million in excessof the whole of the company's 60% liability to Falconbridge Dominicana.

147. It can be concluded that Falconbridge Canada has the financialability to meet its part of the debt service guarantee included in theSales Agreeme!nt.

148. In the Ancillary Agreement between First Nationa:L City Bank(acting as Trustee for Loma Corporation), Falconbridge Canada and Armco,a deblt limit of 45% of consolidated net tangible assets :is to be imposedon Fa:Lconbridge Canada. This is a debt:equity ratio of about 31:69,and this restriction is more than adequate to protect al:L lendersincluding IERD.

Armco Steel Corporation

1)49. Since 196)4 Armco's annual sales in the U.S. and Canada haveexceecled one billion dollars. Sales outside these countries are madethrough subsidiaries. whose profits are included only as dividends paidto Arnmco. Sales in 1968 were $1.4 billion and 10% higher than salesrecorded in 1967. Gross Drofit on sales averaged 23% from 1964 through1967, but declined to 21% during 1968. With extensive modernisation thecomparny expects a substantial lowering of production costs and increasedproUtits from 1969.

150. Annual net earnings of the Corporation have averaged $83.8 millionsince 1964. In 1968 net earnings increased to $88.9 million, and were$17.L4 million higher than the previous year. This conforms to thepattern of increased sales and higher cross Drofit recorcled for the vear.The nEt earnings figure for 1968 represents 6.h% profit margin on salesafter n1llow2nre fnr tn-r

11. In 196A4 the cormpany e.mnbark.ed npnn an fl+ensi-v expanqion nrlmodern,isation program which to date has cost $650 million. In additionloca'l ;mini-rn1 i+.1in m- =v,rnr.dinr7 53 mrillifn or. fan 1cili+tie whlic-h are

to be leased to the company upon completion in 1969.

152. Long-term debt of Armco at the end of 1968 was $241 million,while current leasing arrangei,,ents with the Ohio .m,unicip-1ites addeda

contingent liability of US$199 m,illion. The long-term debt:equity ratio.LS )L41 Ur. UrLen' "liabl es are h L±U iigh anA 4the total debt:eq-uity raio

is 41:59. These liabilities are well covered by current assets and the±iI4uidiU±t ratio waC.U 2 t. bUItnU Ue of1U96, aLUILUugli preJL'tViUUs ye

- 28 -

it was in excess of 3.0. The ratio of debt to equity has been risingeach year since 1964 with the increased borrowings for the heavy invest-ment program, but is expected to decline after 1969.

153. Armco future nlanning is based on a 5 year financial plan,(shown in Annex 8) which extends to 1972 and estimates beyond this dateare not available.. The coiupann predifts a ilC increase in earnings eachyear w:hich together with depreciation of the new equipment, create arapidl;y incre-sing, cash flowTT. Cpital expenditure is to continue at ahigher rate but only in 1969 is extensive recourse made tio loan financing.Bevond 1969 c-ash flow is sufficient for ca t>al expenditure, repa,Trent sfloans and dividends and should still yield a large surplus. The cumul-ative surplus in 19 ic e.ected to be four tim.es Amco'^s contingentliability for 40% of Falconbridge Dominicana's debts.

154. On the assumption of a 50:50 debt:equity, Armco has a currentborrowing capacity of nearl US$1 billlon, which is $300 ri-llion hithan the present level of total debt. Annual earnings are sufficient toser vice debt Increases of this magnitude. I necessary, Artco has thecapacity to raise sufficient loans to service its liability toF ' ~LconvDr-' dge Vomr,Linicana.

155. It is apparent that Armco has the financial abiiity, in bothearnings capacity and loan potential, to meet the 40% debt; servicingguarantee, should it become necessary.

156. The institutional lenders to Falconbridge Dominicana have notimposed. debt restrictions on Armco, but the parties have agreed thatreasonable debt covenants will be applied should Armco take over itsshare cf the senior debt in the event of default by Falcon.bridgeDominicana.

D. Concessions and Incentives

157. Concession arrangements between the Government of the DominicanRepublic and Falconbridge Dominicana were re-examined recently andagreement was reached in June 1969. A memorandum of agreed stipulationswas signed on June 15, 1969 by President Balaguer and M4r. Marsh A. Cooper.

158. The efi.ective tax rate on profits of Falconbridge Dominicanais to be 33% with no reduction for depletion.

- 29 -

159. Depreciation on the $15 million equity investment is to beallowed over 20 years and depreciation on the remaining costs of fixedassets is allowed over 10 years. However deDreciation will not becharged in any year if it reduces the taxable profits below $6 million.Depreciation disallowed in one year can be charged fully or partlyin any subsequent year, subject to the taxable prof'its in that yearbeinge above the minimum.

160. An income tax of 18% is to be withheld from dividends paidto any foreign shareholder of FaLconbridge Dominicana, subject to thetax being allowed as .redi t or deducti on against the shareholder'staxation in his home country. At the moment this tax wouLd probablyapolv to Uriited States sharehol ders. hut not to Ganadian.

161. Falcoribridge Dominianan will n2v an anniiua fee of 114on the outstanding balance of the IBRD loan to the Govermnent of thenominic-an Republic for guaranteeing the loan.

- 30 -

VII. ECONOMIC BENEFITS

162. The proposed project would be the most important industrialundertaking in the Dominican Republic and would represent the largestexternal invesftmPnt in any singRle nroiect to date including those whichare currently under consideration. It would tap a potential source ofnati ona:1 weal; which hit±herto has nott hbn e,xnloitefi and because ofthe nature of the ore cannot be economically exploited without specialProcess1n g whno ch reqTTires considernhle outlay and t.echnic1 expnerience.neither of which could be supplied from domestic sources. The projectrwvould prode+. +bni tth ncnorm o,f' tfhe. coirntrv in vuarious fields.

1- ----- -…- 1 - - Lo . -h - e- n -V

163. qhe GNP of the Domini can Republic inl,63 was aToundl U$ 1.1 billion,of which about $187 million represented gross investment. The operationsw . C L E O .L | us; Qt >wu % > u V~4. y IiI y.LU1L s I ws L' JA 1 , J U U A i5

the construction period, increasing total investment above the 1963i baseby some 12 p~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~erer.. ThL'e viarious ecor.omic benefits e.x ete to accu to

the country ares briefly discussed in the following under three aspects:Ia) gains in .oriL± idLa,, (b) fiscal bets; (c ---JployII,ent a.I.

other indirect benefits which cannot be easily estimated at this time.

Gains iL Foreian Exchanr-e

164. Tables in Annex 9 estimate the net generation of foreiign exchange,which consist amainly of construction costs (both ori,4inai aWnd subseL-ueU.-),

operatin; costs, corporate taxes and dividends on shares held by Gov-ern-ment. Construction and operatingr costs incLude the costs o^ purchasingland, local materials and employment of local labor. The corporate taxie;)resents 33 percent on the tax-able income of Falconbridge Jo-nicana.The latt;er is affected by depreciation over 13 years *if the tutal costof fixecL assets and over 2, years of the pre-operating expenses. Di-Videndswould be received by the Gcvernment on its hcldings of 9.6 percent of thetotal outstandin7 com-cmon shares of Falconbridge D,minicana.

6. Durin- the period 1966-1966, the value of exports from the Do.mnicanR.epublic averasedi P152 iaillion. The average annual value of exports offerronicKel, beJinning in 1972, would be $462.4 million.

Lo6. Total net foreian exchange generated by the project range from 44.3-rillion to over $11.7 million a year from 1969 through 1981, except for1970, the year of most intensive construction work, when it will bearound $16.5 million. From 19d2 onwards, i.e., after the tenth year ofoperatio:a when the depreciation allowance comes to an end and the cor-,:orate tax increases substantially, total net foreign exchange receiptswill ranige from $16.0 million to over $21 million. The grand total offoreign exchange generated between 1969 and 1991, i.e., over a 23 yearperiod, :Lncluding 20 years of operations, is estimated at $325 million.

- 31 -

167. From the point of view of foreign exchange benefits, the 23years covered by the estimates can be divided into three periods.During the construction period (1969-1971) there will be a largeinflow of foreign exchange, concentrated, according to present plans,around 1970. This neriod will be followed by 13 relatively "lean"years when depreciation and interest payments cut deeply into taxableinnnom!s. Finally; from 1982 onwards; taxes ani cnonsoillentTv foreignexchange receipts will pick up considerably.

Fiscal. Benefits

160. Annual fiscal revenue of the Dominican Government since 1905 has'~tTlflOn 1 71. ' ll p- nnn, n e n,

4n no o-, 4r A n c ,n. n o

0.e e $1,705 '-L 9. l;on. -L aS-.er.ts or.J ncome %.L V .J.A.a.. genera+ed

by the project would add between 1972 and 1961, an average of $3.3mill4on per annum , and ng. thAe subseq-ent I 1 years, a yearly a-r-rageof $12.2 million. The grand total of tax receipts from the project up4.A ±1 7±' WUU±U. U' V4J± - -1-i±±±±UtIo 1991 wouldU bue $1,5 r,illuio.

169. In adoit;ion, there woUld be dividends accr-i ng to the GoverriUfe±.tas shareholder of Falconbridge Dominicana. Between 1972 and 1991 annual.dividends would range from $0.6 million to $2.3 million and would average$1.5 million. Total dividends would amount t.o over $2d.9 million. In theestimated Total Government Revenue, shoam in Annex 9, dividends are cal-culated on the assumption that all cash surpluses are dec:Lared as dividendsduring the twenty year production period. Moreover, nickel prices areunlikeLy to remain constant during the period under consideration and anincrease would. probably exceed labor cost increases as the project employslittle labor relative to its size.

170. IL mnall amount of annual revenue is gained through the guarantee feefor the IBRD loan which is calculated at 1 1/2 percent of the outstandingamount of the loan. The annual amount is initialAy about $0.4 million,but decreases as repayments are made, and amounts to $3.7 million overthe term of the loan.

Indirect Benefits

171. There would arise from the project a number of further quiteimportant benefits to the country which, however, cannot be very wellestimated at this time. They are briefly summarized as follows.

- 32 -

172. The project would help to diversify the local economy which islargelr agricultural. In the field of mining. at nresent the onlv maioroperat-Lon is the export of bauxite by Alcoa, although several othermining onnes, ions have been granted and some prosnpeting is goine on.Apart from being the largest mining and industrial venture, the projectwouldf r st+.imil na+t +.the rowt7rF.h of' smanl l Pr subshci Hi ary i nrd1u.stri e3s nsuch ascement,, woodworking, etc., as well as service industries in the projectarea T+ It vld thus lead +o an econom c upr ng of a . dn ofthe couLntry in wihich multiplier effects of the new employment would be

.L~..L W.

J17 . For aL %coUL1 Lt.Y sU.L.LVf L f1ro L .LVII. LA4oJ.LA' unJA e..p lSl--

employment, between 1,500 and 2,500 new jobs during the constructionpe-Loud andu arounu 1,000 em voyees thereafterv a±re of consiLcera'D'e -mport-

ance. Apart from the generation of income for those immediately con-cerned, this additional employmen wo-uld also lead 4o various revenuesfor the central and local government from income and businLess taxes.

174. Finally, there will be in the country an increase in technicalSKills due to the training of Dominican staff as geologica3L, cnemical,mining, electrical, administrative, etc. operators.

VIII. PROTECTIVE ARRANGEMENJTS

175. The protective arrangements for the financing of FalconbridgeDominicana eccur at two levels; protection of the loans an,d protectionof onerational cemmitments._ The Bank has to be satisfied in relation toboth arrangements.

176. The loan from IBRD is to be guaranteed by the Government oftbha D1min-iicnn. Paroiinr- TLons from other :n,1rrqes will be guaranteed bvU.S.A.I.D. against specific risks mentioned previously.

177. Loans from IBRD, the commercial banks and $80 million of loansfrom the insura nce onmnniPs will rank equally and will be senior to the$34 million of subordinated loans supplied by the insurance companiesand guaranteed by Flor.nbiridge Canada and A-rmeco against eommercial. butnot political risks. The senior loans will be secured pari passu by(i) a mortgage and mining hyroth.ec on F.teOnhrirge nomininana's fixedassets, (ii) an assignment by Falconbridge Dominicana of its rightsag-ainst Fr , ^nn d-A CAar.d nA A?mr-. iiunrdr +t-.' Rnles Agreement and ofits rights against Falconbridge Canada under a license agreement, and(iii) a pledge by F- conbridge Can--ada- and AAw'^ +their sharp_s ofstock of Falconbridge Dominicana.

178. Falconbridge Dominicana will enter into contractual arrangements-wt 'aconlbrdge CftnaWda a-nd A-'t-C th1rough a Sa-les ^g.reer.en hc gaaW-Iitl r aicoribriug UU arU RIaMUiu tlAIUU'll CZ Oa.Lv JMr,I~U l~

tees the payment to Falconbridge Dominicana of sufficient funds to servicethe companyis debts. Tne sales contract waii require Fdlconbuiudge Canada

- 33 -

to purchase the whole of the production of Falconbridge Dominicana andto pay full market price for the metal, less transportation costs and aselling commission of 14. Falconbridge Canada is obliged to apply thediligence of an agent in obtaining the best available price for themetal or obtain the market price if such price for ferronickel becomesestablished.