Embed Size (px)

Citation preview

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No. P-4056-PAK

REPORT AND RECOMMENDATION

OF THE

PRESIDENT OF THE

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

TO THE

EXECUTIVE DIRECTORS

ON A

PROPOSED LOAN

IN AN AMOUNT OF US$178.o MILLION

TO THE

ISLAMIC REPUBLIC OF PAKISTAN

FOR AN

ENERGY SECTOR LOAN

May 6, 1985

This dxocment has a reticted distributio and may be used by recipients y in the perf rmwneeoftheidr official duties. ItS contentsma nuot othenrwie be disclosd witbuut World Bbnk nsohorinizn.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

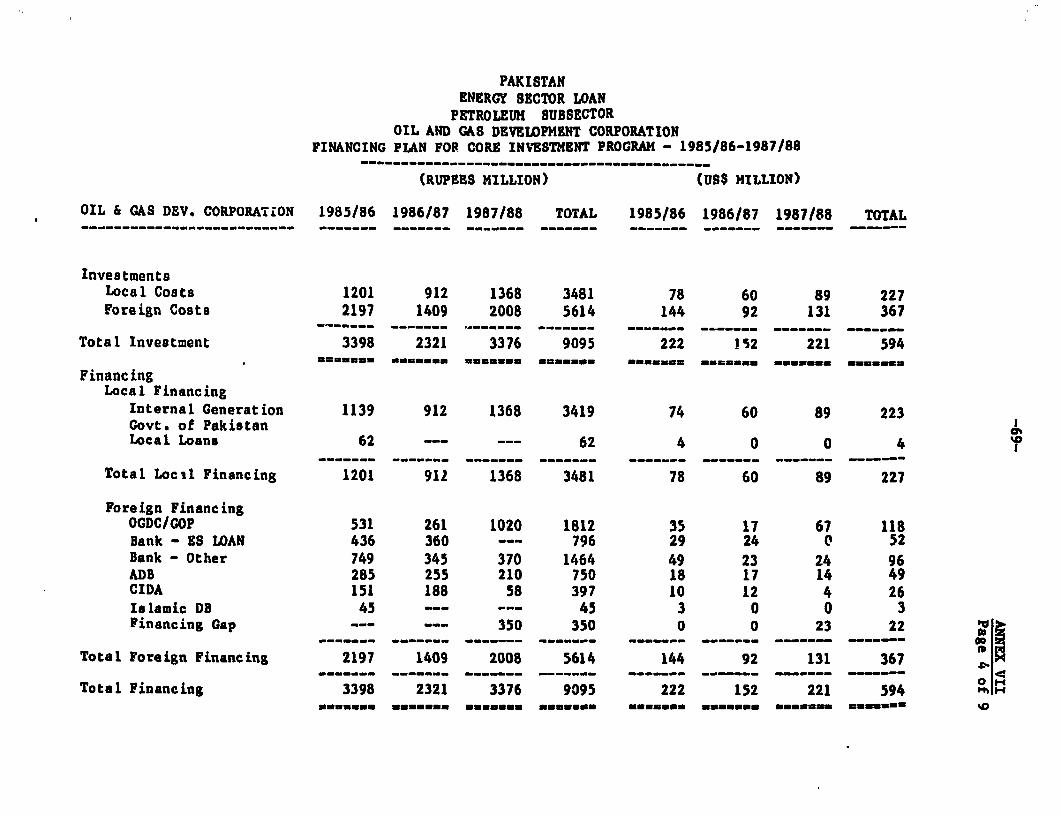

rized

Pub

lic D

iscl

osur

e A

utho

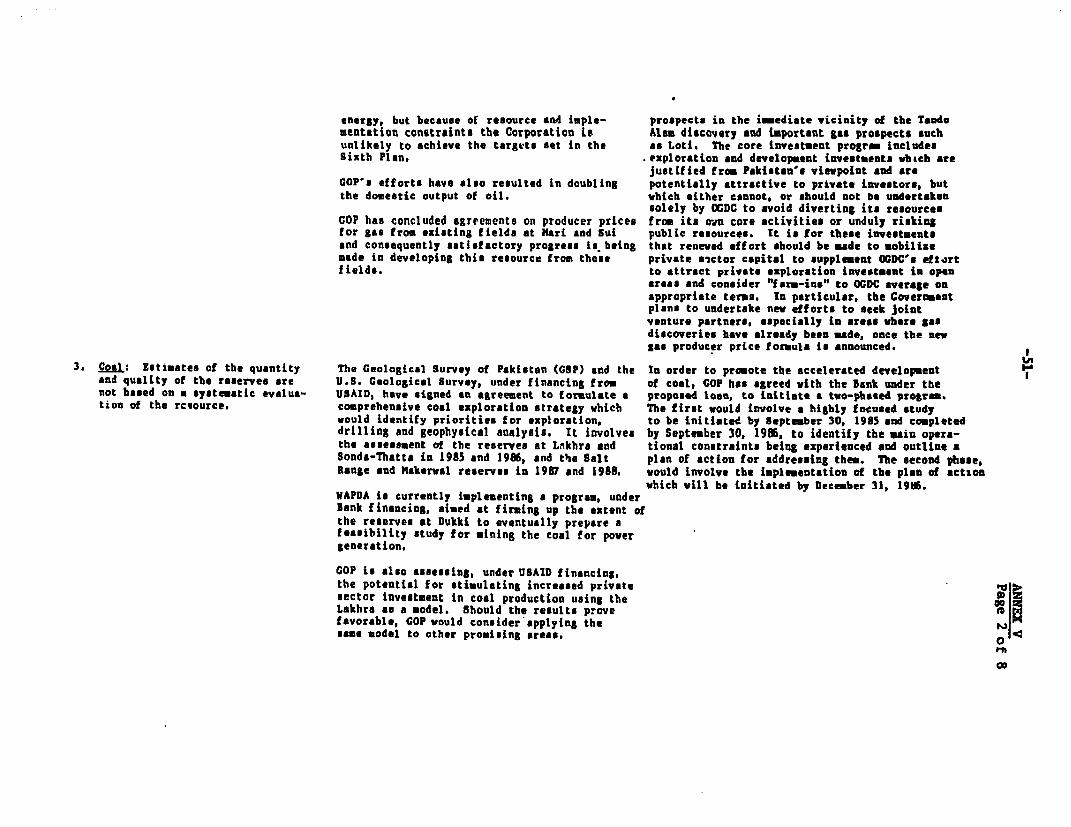

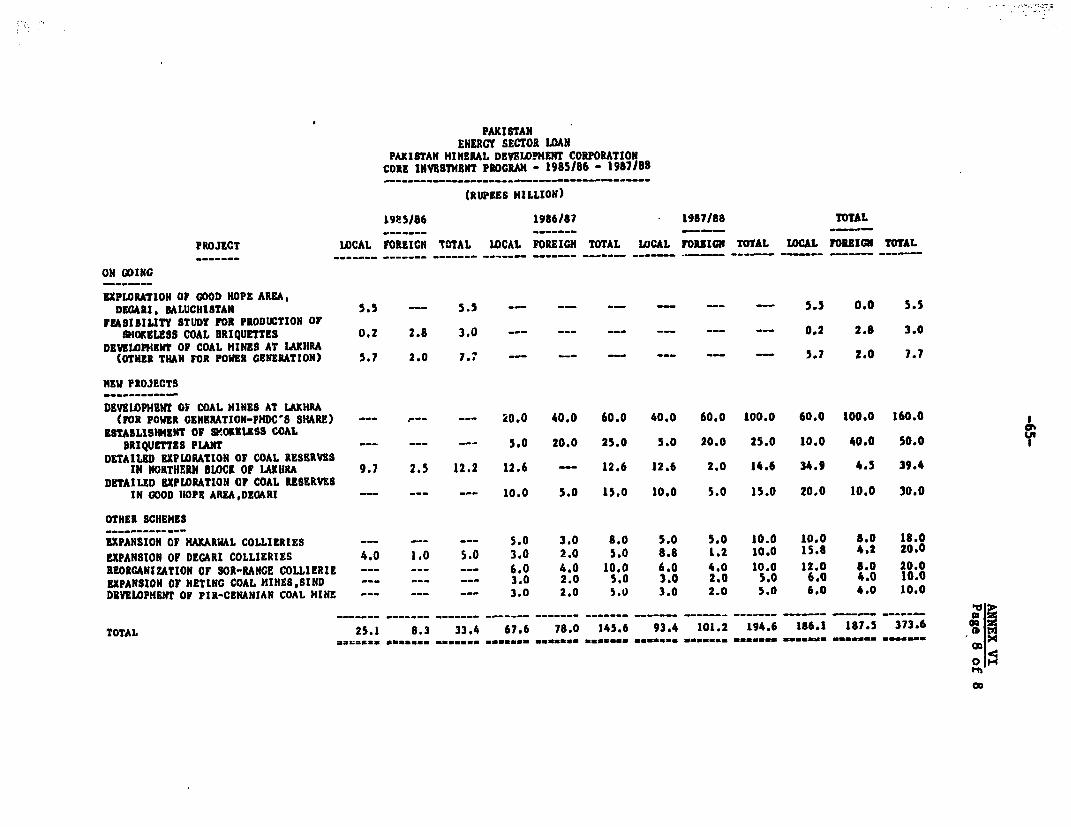

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

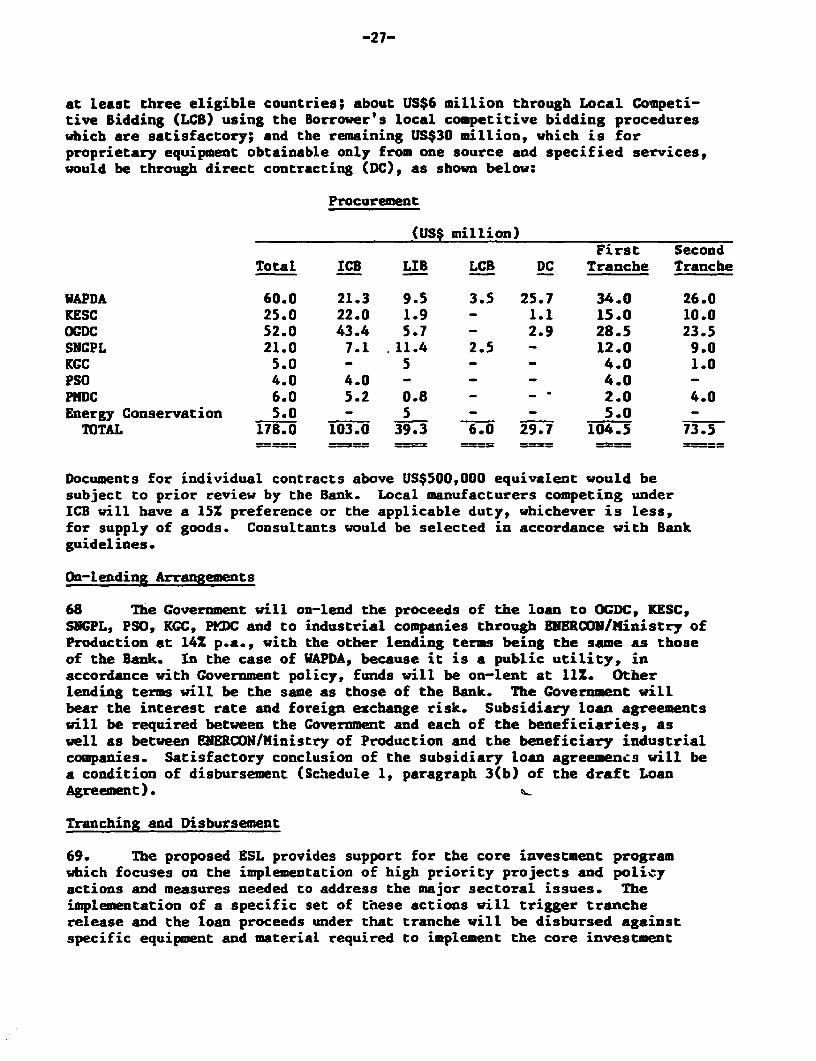

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

Currency Unit = Pakistan Rupee (Rs)US$1.00 = Rs 15.3

FISCAL YEAR

July 1 - June 30

ABBREVIATIONS

ADB - Asian Development BankCIDA - Canadian International Development AgencyENERCON - National Energy Conservation CenterENERPLAN - Office of Energy PlanningESL - Energy Sector LoanCSP - Geological Survey of PakistanKESC - Karachi Electric Supply CorporationKGC - Karachi Gas CompanyNRL - National Refinery LimitedOGDC - Oil and Gas Development CorporationPHDC - Pakistan Mineral Development CorporationPSO - Pakistan State OilSNGPL - Sui Northern Gas Pipeline LimitedUSAID - United States Agency for International DevelopmentWAPDA - Wa-er and Power Development Authority

FOR OMCIAL USE ONLY(i)

PAKISTAN

ENERGY SECTOR LOAN

Loan and Project Summary

Borrower: Islamic Republic of Pakistan.

Beneficiaries: WAPDA, OCDC, KESC, PSO, SNGPL, KGC and PHDC.

Amount: US$178 million.

Terms: Repayable in 20 years, including five years of graceat the standard variable interest rate.

Onlending Terms: From the Government of Pakistan to WAPDA at llX p.a.and to all other beneficiaries at 14Z p.a., with theother lending terms being the same as those of theBank.

Project Description: The Loan would support the Government's reformprogram in the energy sector, as outlined in theattached development policy letter from theGovernment to the Bank, and assist in theimplementation of the Government's core energyinvestment program for the period FY86-87. Thereform program consists of a number of significantimprovements in the areas of: development andinvestment; pricing and demand management; andinstitutional development. The core investmentprogram takes into account the inter-linkages amongenergy subsectors and the implementation andfinancing capabilities of the Government.

The Loan has been designed through extensiveanalysis and discussions on key sector issues betweenthe Government and Bank staff. The reform programand care investment program constitute an integratedand comprehensive policy and investment framework forthe efficient development of Pakistan's energysector.

The Loan would finance imports of equipment andmaterial required by priority projects included inthe core investment program, as well as for theefficient operation of existing facilities. The mainrisk relates to possible political events which mayimpede the implementation of the program. The riskis considered minimal.

Thidcuent has a restcted distributon and may be used by recipients only in the performance ofir offiia dutes. Its contents may not otherwise be discosed without World Bank authorizaton.

(ii,

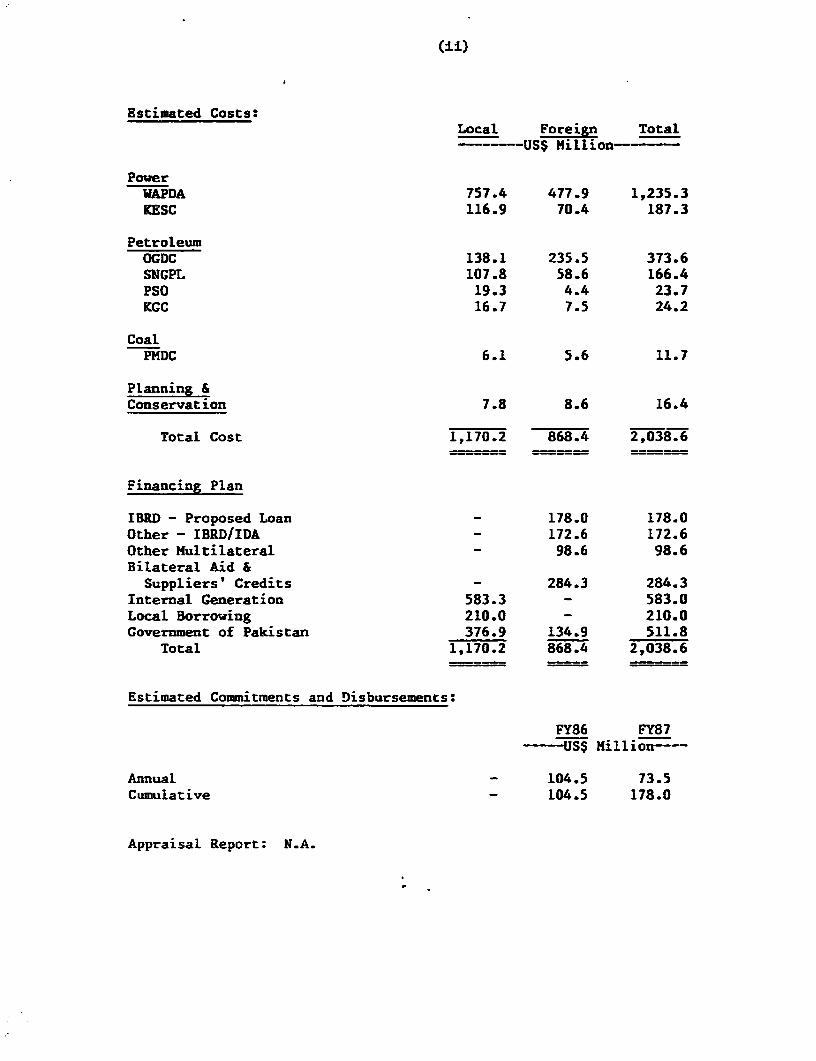

Estimated Costs:Local Foreign Total------ US$ Million ---

PowerWAPDA 757.4 477.9 1,235.3KESC 116.9 70.4 187.3

PetroleumOGDC 138.1 235.5 373.6SNGPL 107.8 58.6 166.4PSO 19.3 4.4 23.7KGC 16.7 7.5 24.2

CoalPMDC 6.1 5.6 11.7

Planning &Conservation 7.8 8.6 16.4

Total Cost 1,170.2 868.4 2,038.6

Financing Plan

IBRD - Proposed Loan - 178.0 178.0Other - IBRD/IDA - 172.6 172.6Other Multilateral - 98.6 98.6Bilateral Aid &

Suppliers' Credits - 284.3 284.3Internal Generation 583.3 - 583.0Local Borrowing 210.0 - 210.0Government of Pakistan 376.9 134.9 511.8

Total 1,170.2 868.4 2,038.6

Estimated Commitments and Disbursements:

FY86 FY87-- US$ Hillion----

Annual - 104.5 73.5Cumulative - 104.5 178.0

Appraisal Report: N.A.

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

REPORT AND RECOMMENDATION OF THE PRESIDENTTO THE EXECUTIVE DIRECTORS ON A PROPOSED ENERGY SECTOR LOAN

TO THE ISLAMIC REPUBLIC OF PAKISTAN

1. I submit the following report and recommendation on a proposed EnergySector Loan of US$178 million to the Islamic Republic of Pakistan. The loanwould have a term of 20 years, including five years of grace, at the standardvariable interest rate.

PART I - THE ECONOMY

2. The most recent economic report "Pakistan: Recent Economic DeveLop-ments and Structural Adjustment" (No. 5347-PAK, dated March 20, 1985) wasdistributed to the Executive Directors on April 4, 1985.

3. The steadily improving performance of recent years was interruptedin FY84 due to an unexpected downturn in agriculture and migrant remittances,and the carry-over of inflationary pressures from FY83. GDP growth slowed to3.5% as a result of a 6.2Z fall in agricultural value added caused by adverseweather and pest attacks. Manufacturing grew by 8.3% and services by 6.2%.Fixed investment rose by 6.5%, while private investment increased by 11.5%.National savings fell to 12.1% of GNP as a result of a drop in privatesavings. Public savings remained low reflecting reduced Federal and Provin-cial budget surpluses. Excess liquidity from FY83 (generated largely byforeign exchange inflows), increases in world prices and reduced agriculturaloutput, contributed to inflation above 9%, as against 5.2Z in FY83.Budgetary policies continued to be prudent. Current revenues increased by20-, largely through improved tax administration, but current expenditur^salso increased reflecting higher allocations for economic and social serv-ices. Considering the economic importance of agriculture, the achievement ofcreditable growth in FY84 points to a considerable resilience of Pakistan'sunderlying economic structure, which is partly the result of recent Govern-ment efforts to begin removing structural imbaLances in the economy.

4. The balance of payments deteriorated in FY84, relative to the markedimprovement in FY83. The current account deficit at US$1 billion was almostdouble that in FY33. Stagnant exports and lower remittances were the maincontributing factors. With cotton and yarn exports much reduced by the poorcotton crop, exports rose by only 1.6%, while imports increased by 6.9%.Remittances, which declined for the first time in FY84, fell by 5.1%.Moreover, recent projections suggest a decline in net migration, which isLikely to lead to lower remittances over the medium term. The higher currentdeficit, together with lower net capital flows, led to a reserve drawdown ofUS$113 million. Gross official gold and foreign exchange reserves wereUS$2.4 billion at end FY84, equivalent to 3.8 months of imports of goods andservices.

-2-

5. Since 1980, the Government has moved gradually to eliminate interestfrom the economy and has announced that the process will be completed by July1985. All transactions will be based on new financing modes consistent withIslamic principles. Existing interest-based commitments will be honored andtransactions with foreign governments and financial institutions will not beaffected. At this stage, it is difficult to determine with any certaintythe potential costs of Islamization. Undoubtedly, there will be some costsin converting the system, but whether long-run efficiency is affected willdepend on how the system is applied. To date, the Government has proceededcautiously and, while fully committed to the elimination of interest, hasstressed that new financing modes will be applied flexibly and developmentsmonitored closely.

6. The slowdown in economic growth in FY84 marked a departure from theimproved performance achieved during the Fifth Plan period (FY79-83). Growthin national output (6.5%), agriculture (4.2%), manufacturing (10.42), exports(11%) and private investment (6.7Z), though beLow Plan targets, was wellabove rates achieved during FY70-78 and very respectable compared to otherLDCs. Growth during this period - coupled with increased remittances -benefited large segments of the population. Improved performance took place,despite a number of adverse factors: (a) a world recession; (b) a 30% declinein the external terms of trade after 1979; and (c) the Afghanistan crisiswith its attendant requirements for increased defense and refugee assistanceexpenditures.

7. Fiscal performance and the balance of payments improved significantlyduring the Fifth Plan. The overall budget deficit and Government bank bor-rowing, which stood at 8.8% and 4.3% of GDP in FY79, fell to 6.4% and 1.7%,respectively by FY83. Reduced levels of Government borrowing from banks,together with overall credit restraint, led to lower money supply growth andlessened inflationary pressures; inflation dropped from 8Z to 5% by the endof the Plan period. The improved fiscal performance was largely the resultof expenditure restraint rather than better revenue performance. Real expan-sion in current expenditures on economic and social services barely kept pacewith population growth and development expenditures declined relative to GDP.Government revenues remained constant at 16% of GDP and public savings,having risen in the first half of the Plan period from 1% to 3.8% of GNP,dropped to 1.6% by FY83. Assisted by remittances, but also strong exportgrowth, the current account deficit tell from 5% of GNP to 2% by the end ofthe Plan period. Gross reserves increased from 3.5 to 4.5 months of importsof goods and services.

8. In addition to improving economic management through fiscal andmonetary policies, the Government took measure- to improve performance inthe commodity-producing sectors. In agriculture, all major crops reachedrecord output levels, with wheat and sugar achieving self-sufficiency. Sub-sidies on pesticides were virtually eliminated, while fertilizer prices wereraised eo reduce the subsidy burden. Crop procurement prices were adjustedto bring them closer to world prices. Provincial allocations for operationsand maintenance in irrigation were increased, along with water charges.

-3-

Encouraged by improved poLicies and incentives, private manufacturing invest-ment grew by 10.9% p.a. Areas open to the private sector were widened, mostagricultural processing units were denatioralized and sanctioning limitsincreased. A flexible exchange rate policy adopted in 1982 was instrumentalin encouraging manufactured exports, while import Liberalization increasedthe availability of raw materials and capital goods. In energy, measureswere taken to accelerate the development of domestic resources, rationalizeprices, and improve policy formulation and energy planning capabilities.

9. The developments in Pakistan's economy since FY78 represent welcomesteps toward the solution of problems which are essentially structural andlong-term in nature. Notwithstanding these improvements, furtherwide-ranging measures to address structural issues are necessary. Two issuesare critical to Pakistan's long-term growth prospects: (a) the need toincrease the level and efficiency of public investment; and (b) the need toencourage export expansion and efficient import substitution. To sustainhigh economic growth, Pakistan is faced with the urgent need to make majorinfrastructure investments, upgrade existing facilities and strengthen itsneglected social base. The latter has fared badly as a result of resourceconstraints and is reflected in Pakistan's social indicators which lagseriously behind these of other LDCs at comparable levels of development.Increases in public investment and recurrent alLocations will not be possiblewithout a major domestic resource mobilization effort. Although reform ofindirect taxation through the introduction of a broad-based sales tax shouldreceive priority, greater reliance on user changes, curtailment of subsidiesand increased self-financing by public enterprises will also be required.Civen the more constrained outlook for official assistance and the likelihoodof lower remittance flows, sustained improvements in both export expansionand efficient import substitution will be necessary to support high growthwith sustainable external capital requirements. Improved trade performancewill require a continuation and strengthening of the structural adjustmentprocess in the key sectors of agriculture, industry and energy. Bothagriculture and industry have considerable potential for increased exportsand some degree of efficient import substitution. In energy, the accelerateddevelopment of Pakistan's underexploited resources can make a major contribu-tion to the reduction of energy imports.

10. In agriculture, high growth has been Largely the result of increasedacreage; average yields remain low by world standards and those of progres-sive farmers within Pakistan. Increasing agricultural productivity anddiversification will require strengthened institutional support, appropriatepricing policies, and the identification and implementation of the coreinvestment program. More effective institutional support should be soughtthrough improvements in the quality and quantity of services to farmers. Inparticular, strengthening the seed program requires more efficient seedmultiplication and dissemination, increased efficiency in public sectorplants and a greater role for the private sector. The delivery of agricul-tural credit needs to be improved to ensure it actually reaches small farmersand tenants, whose credit needs are greatest. Marketing costs need to bereduced together with a strengthening of research and extension services.Agricultural pricing policies should ensure appropriate incentives tofarmers, while minimizing subsidies. Multi-crop approaches to pricing should

-4-

complement the single crop, cost-of-production approach currently used.Finally, a core investment program in agriculture and water is needed toreduce the possibility of distortions in investment priorities. Programsthat are low-cost and yield quick returns should be emphasized along withcritical infrastructural investments that raise farm productivity. Greateremphasis on the complementarity of investment programs, especially betweenagriculture and water would ensure that priority is accorded to programs thatincrease agricultural productivity rather than merely augment the supply ofphysical infrastructure.

11. Increasing and diversifying Pakistan's manufactured export base andencouraging efficient import substitution will depend, to a large extent, ona rationalization of industrial incentives to reduce both the level anddispersion of effective protection rates. The objective should be toincrease the efficiency of the industrial sector by exposing protectedproducers to greater foreign competition and to reduce the antiexport biasinherent in the present incentives system. In addition, reform of Governmentregulations affecting investment sanctioning and cost-plus pricing is alsorequired. The Government should limit sanctioning to a few cases ofstrategic importance, leaving most investment decisions to the private sec-tor, which is better able to assess investment opportunities. Cost-pluspricing arrangements, which provide insufficient incentives to minimize costsor alLocate capital efficiently, should be replaced by market-orientedapproaches which better reflect supply/demand conditions and provide adequateincentives for reinvestment and operational efficiency.

12. In the energy sector issues need to be addressed in three broadareas: (a) investment and development; (b) pricing; and (c) institutionalstrengthening. To date, the Government's power generation program, as wellas other investments in the sector, have not been based on a long-termleast-cost development plan. Given the likelihood of domestic resourceconstraints and persistent power shortages, the Government should ensure thatfuture investments conform to such a plan and that a core investment programis insulated from uncertainties inherent in the budgeting process. Thepresent gas producer pricing formula for new discoveries should be adjustedto provide adequate incentives to attract private sector exploration. Con-sumer gas prices, which were maintained artificially low to encourage thesubstitution of gas for imported oil, have resuLted in a considerable distor-tion of relative prices and uneconomic use of gas. The Government's policyis to increase gas prices to reach two-thirds of fuel oil parity by FY88 andsince 1982, price increases have averaged 15% p.a. in dollar terms. TheGovernment needs to meet its FY88 objective and move to full parity as soonthereafter as possible. Electricity tariffs, which are currently belowlong-run marginal cost, should be adjusted to reflect this cost, not only toensure efficient use of electricity and encourage energy conservation, butalso to mobilize additional funds to meet the substantial resources requiredby the power investment program. Finally, the Government should considerincreasing the autonomy of public enterprises in the energy sector to improvetheir efficiency and should continue efforts'to strengthen energy planningand policy coordination.

-5-

13. The Six:h Five-Year Plan (FY83-88) articulated a pragmatic strategyfor Pakistan's continued rapid development which incladed an expanded rolefor the private secLor, increased public development expenditures andincreased allocations for energy, agriculture, irrigation and the socialsectors. Although the size and composition of the Plan are appropriate,because of insufficient domestic resource mobilization, development expendi-tures during the first two years of the Plan will be 9Z lower than theamounts projected. Although this would not appear overly large, the way inwhich sectoral shortfalls have been distributed contradicts Plan priorities.Education, energy, health and agriculture. received considerably lowerallocations than called for in the Plan. Furthermore, without a predefinedcore investment program, there is a tendency to distribute shortfalls evenlyover a large number of projects within a sector; too many projects areinitiated and projects that should receive priority are underfunded. Inorder to address this issue, the Government has announced the reintroductionof a Three-Year Priority Investment Program (FY86-88). The Government hasemphasized that the adoption of a rolling medium-term program does not meanplan strategies and priorities are being revised, or that shortfalls areconsidered inevitable. The Program will identify sectoral core investmentprograms which will be given priority in formulating annual plans. Byprotecting priority investments, especially in key areas, the effectivenessof the public investment program would be enhanced and priorities sharpened.

14. Despite the temporary setback in FY84, the improved performance andpolicy framework set in motion during the Fifth Plan, which the Governmentintends to continue during the Sixth Plan, have improved Pakistan's credit-worthiness for a blend of Bank and IDA borrowing and commercial borrowing.At the end of calendar year 1983, Pakistan's external public debt (excludingthe undisbursed pipeline) stood at US$9.8 billion, of which US$4.7 billionwas owed to bilateral members of the Pakistan consortium, US$1.3 billion toOPEC, US$2 billion to multilateraL agencies, and the balance, to otherbilateral and private lenders. In 1983, the Bank Group's share in Pakistan'sexternal public indebtedness was 15.3% and in external debt service was 7.0%.Bank projections indicate that, provided recent policy improvements aresustained and structural issues addressed. Pakistan's debt service wouldremain below 15% during the remainder of the 1980s, even with somewhat higherlevels of commercial borrowing.

PART II - BANK GROUP OPERATIONS IN PAKISTAN 1/

15. The cumulative total of Bank/IDA commitments to Pakistan (exclusiveof Loans and Credits or portions thereof which were disbursed in the formerEast Pakistan) now amounts to approximately US$3.2 billion. During its longassociation with Pakistan, the Bank Group has been involved in most sectorsof the economy. This has included its involvement with other donors, over a20-year period, in the major program of works to develop the water resources

l/ Part II is substantially the same as that in the President's ReportP3940-PAK (Fourth WAPDA Power Project), dated February 13, 1985.

-6-

of the Indus Basin. Approximately 30% of total Bank/IDA conmitments toPakistan have been for agriculture and irrigation; 28% for industry, includ-ing import program credits; 18% for transport, telecommunications and publicutility services; 14% for energy, including power, gas pipelines andpetroleum; 5% for social programs in education, population and urban develop-ment; and 5% for structural adjustment lending and technical assistance.

16. In the current period, the Bank's assistance strategy is to supportthe Government's efforts to formulate and implement policy reforms in threesectors--energy, industry, agriculture-which shape the structural adjustmentprocess in Lhe economy. At the same time and in order to ensure that thegains from adjustment are sustained in the long term and shared more broadly,the strategy also includes investments in physical infrastructure and thesocial sectors (education, population, etc.) which have been neglected inPakistan's development efforts. To succeed, this strategy requires aflexibLe deployment of the full range of traditional instruments of Banksupport - sector work and active policy diaLogue, policy and project-basedLending, technical assistance and aid coordination. The Bank Group's lendingprogram has two components. The larger project-based component supportsspecific high priority investments in productive sectors and physical andsocial infrastructure. The smaller but strategic component focuses on policyreforms in the key secturs of agricuLture, industry and energy, relyingheavily on high quality economic and sector work. The strategy includes aseries of technical assistance credits to finance studies and formulateaction programs for policy reform. The experience with the first of thesehas been extremely positive. Through the annual Country Economic Memorandum,we aim to foster a greater understanding among Consortium members of theGovernmentts structural adjustment program and aid requirements which,coupled with increased co-financing, should enhance the policy relevance andeLfectiveness of other official aid and help attract additional resources toPakistan from nonconcessional sources.

17. Historically, the Bank Group has placed special emphasis on lendingfor agriculture which is the mainstay of the Pakistan econoiy. The Bank andthe Government are in agreement on the main elements of a strategy whichunderpins lending in the sector. In recent years, the objective has leen toincrease agricultural productivity through improvements in the efficien- ofthe irrigation system and supporting agriculturaL services. Among the issuesbeing addressed are: the balance between short-gestation projects andlonger-term expenditures, rationalization of input and output prices, market-ing, improvements in operation and maintenance, cost recovery, and a widerrole for the private sector. Projects in the sector have ranged from irriga-tion/drainage to agricultural inputs, research and extension and haveincluded institution building components. OveraLl, progress in agriculturehas been satisfactory.

18. In industry, the strategy has two complementary aspects: tostrengthen and broaden the process of structural adjustment in Pakistan'sindustrial sector and to support the Government's efforts to revitalize theprivate sector through the provision of industrial finance. The industrialreform program is designed to improve the competitiveness of the sector inorder to promote export expansion and efficient import substitution. Issues

-7-

being addressed include trade and industrial incentives; deregulation;efficiency of public enterprises; pricing decontrol; and improvements in thecredit delivery system. Projects have included lines of credits to DFCs andother financial intermediaries which has been mainly for the private sector,totaling US$488.5 million. Direct lending for industry has also includedassistance to three large fertilizer plants and a refinery engineering loan.As of September 30, 1984, IFC has made investments in 15 Pakistan enterprisestotaling US$174.21 million of which US$163.24 million was by way of loans andUS$10.97 million by equity participation (these are shown in Annex II).While individual operations have generally achieved their objectives, theagenda for overall reform in industry remains formidable.

19. Following progress on a number of major sector issues as a resultof the Structural Adjustment Loan (SAL) process in 1981/82, our lendingprogram in cneg is expanding rapidly. The overall objective is to expanddomestic-supply from all energy subsectors, while simultaneously increasingthe e'ficiency of energy use through appropriate pricing, conservation andother demand management measures. No less central have been efforts tostrengthen key institutions in the sector. In power the Bank has assistedboth the Karachi Electric Supply Corporation (KESC) and the Water and PowerDevelopment Authority (WAPDA) in both power generation and transmission; thesector has also been assisted by the construction under the Indus BasinDevelopment Program of Mangla and Tarbela Dams. In oil and gas, the Bankhas financed operations which support a sound expLoration and developmentprogram and has assisted in the development of the extensive gas transmissionsystem. Smaller operations, mostly of an engineering and technical assis-tance nature, have supported coal exploration, energy audits and oil refin-i_g. Despite much progress, however, the Bank will need to continue itsparticipation in institution building in concert with efforts to assist theGovernment to mobilize adequate funds for energy investments through tariffs,co-financing, and greater private sector participation.

20. Bank Group lending for transport and communications has focused bothon new capital investments and on improving the efficiency of existingassets. Operations have also focused on strengthening the institutionsresponsible for these services, especially the Karachi Port Trust, PakistanRailways, the Telephone and Telegraph Department and federal and provincialhighways agencies. However, recent analysis has identified transportinfrastructure as a critical constraint to overall growth due, in largemeasure, to a running down of infrastructure stock. In the future, thebalance between new investments and operation and maintenance and amongvarious modes will need to receive greater attention.

21. With an overall literacy rate of only 252, a population growth rateof about 3%, and rapid urbanization, Pakistan faces a formidable developmentagenda in the social sectors. The Bank has supported the Government'sprogram in education through five credits totaling some US$62.5 milliondesigned to upgrade primary, postsecondary and higher technical and agricul-tural education, middle-level training of primary teachers and agriculturalextension agents. The focus has and will continue to be on the lower end ofthe education system (primary, secondary, technical and nonformal education,including literacy). A first population project designed to expand demand

-8-

for population control services was approved in FY83. In the urban and watersupply sector, the Bank has financed four projects. Besides providing urbanservices, these operations are addressing, among other issues, improved localresource mobilization and cost recovery; improved planning and efficiency ofresource utilization; and urban management, especially at the ProvinciaL andMunicipal levels.

22. 'Jith respect to policy-based lending, a SAL operation was approvedin June 1982. The SAL program consisted of a number of significant reformsin Government development planning and in policies and programs in theagriculture, energy and industrial sectors. The loan was fully disbursed atthe end of FY83 and achieved significant progress in the above areas. Intne next few years, continuing support to the structural adjustment processis envisioned under sector loans.

23. Annex II contains a summary statement of Bank Loans and IDA Creditsas of September 30, 1984. Credit and loan disbursements have been generallysatisfactory. Some projects have experienced initial delays due toprotracted Government procedures for project approval, which are beingaddressed, and to slowness in the procurement of goods and services. Rapidturnover of managerial and technical staff, in part dueL to migration to theMiddle East, and budgetary constraints have been probLems in the case of someprojects.

24. A number of operations are currently under preparation or are beingappraised. These incLude projects for power transmission and generation;oil and gas exploration and development; coal development; lines of creditfor industrial finance for the private sector; industrial subsector restruc-turing, balancing and modernization; irrigation/drainage, agricultural inputsand services; primary and informal education; urban development and watersupply. In addition to the proposed loan, two sector loans which wouldsupport further structural adjustment in industry and agriculture are alsobeing discussed with the Government. Where successfuL, these sector loanswould provide a policy umbrella for projects in those sectors. To assistthe Government to finance agricultural and other high priority projects whichhave a low foreign exchange component, financing of some local expendituresin.specific cases is justified.

25. In addition to lending, economic and sector work provides the basisfor continuing a dialogue between the Bank Group and the Government of Pakis-tan on development strategy, the sector loans now being prepared, and for thecoordination of external assistance within the Pakistan Consortium. The workprogram emphasizes resource mobilization, structural adjustment in the threekey sectors, and physical and social infrastructure.

-9-

PART III - THE ENERGY SECTOR

A. Setting of the Sector

26. The development of Pakistan's resource potential in the energy sectorand measures to limit the growth of energy demand will be critical for sus-taining high economic growth over the long run. Pakistan's commerciallyexploitable domestic energy resources consist, in order of importance, ofhydropower, natural gas, oil and coal. In addition, the country has a sub-stantial nonconventional energy resource base, consisting mainly of fuelwood,agricultural and animal waste, and solar and wind energy. By and large,these resources have remained underutilized and their development hasprogressed at a substantially slower pace than is warranted by the size ofreserves because of inappropriate policies and resource constraints. Aspolicies to contain consumption of energy were inadequate, the country'sdependence on imported energy increased, which, together with increases inoil prices since 1973, contributed to the rapid growth of imports and exter-nal payments deficits. The import bill for oil increased from US$63 million,amounting to 8Z of total imports in FY73, to US$1,496 million representing23% of total imports in FY84. In order to buffer the consumers from thehigher cost of imported energy, the Government encouraged the increased useof domestic energy products such as natural gas and electricity by maintain-ing the price of these products at levels substantially below their economiccost of supply. As a result, by FY78, when the Fifth Five-Year Plan waspromulgated, the economy was experiencing severe resource constraints andrapid growth in energy consumption.

27. In order to address these shortcomings, the Fifth Plan (FY78-83)emphasized the accelerated development of domestic energy resources andrationalization of energy prices. However, the shortages of local and for-eign resources, as well as the unanticipated increases in outlays for ongoingprojects impeded the achievement of the supply targets for all energyproducts except natural gas for whicn over 99% of the output target wasrealized. The largest shortfall was in the power subsector where, betweenFY78 and FY83, only 60% of the forecast generating capacity was commissionedand 85Z of the primary and 53Z of the secondary transmission lines wereenergized. The shortfall was no less pronooaced in tie petroleum subsector,where only 36% of the output target for oil was achieved. These shortages,together with the rapid growth of consumption, precipitated by the delayedand incomplete adjustment to higher world energy prices, resulted in acuteshortages of natural gas and electricity during the last two years of theFifth Plan period. This, in turn, raised the demand for liquid hydrocarbonsand further increased the country's dependence on imported energy. Theadjustments in the prices of petroleum products were initiated in 1978, fiveyears after the first round of increases in the international price of oil,and by FY83 the weighted average price was about 1502 of the border price.By contrast, prices of gas and electricity were not increased until 1980 andeven then at a substantially slower pace than for petroleum proJucts. As ofFY83, the price of natural gas was about 39Z of the border price of fuel oiland electricity was about 63% (WAPDA) and 98% (KESC) of the average long-runmarginal cost for the combined system.

-10-

28. Severe shortages of natural gas and electricity, and the resultantincreases in imports of liquid hydrocarbons ushered the economy into theSixth Plan. The industrial and household sectors were particularly affectedby these shortages, which are increasingly becoming a major impediment tomaintaining the economy's growth momentum. In recognition of the possibleadverse impact of increased dependence on imported energy and of continuingshortfalls in energy supply, the Government accorded high priority torestructuring the energy sector during the Sixth Plan. The objectives of theSixth Plan are to: (a) accelerate the development of domestic energy resour-ces to reduce the country's dependence on imported oil; (b) promote theefficient and rational use of energy to meet the future demand at least-costto the economy; (c) adjust energy prices to reflect their economic costs;(d) streamline the organizations and institutions in the sector to promotetheir efficient operation and management; and (e) develop mechanisms forincreasing private sector participation. The Sixth Plan allocated Rs 116.5billion (US$8.6 billion) to public sector energy programs, representing anincrease of about 120% in real terms over the Fifth Plan and amounting to 38%of total public sector outlays.

29. In addition to increasing the allocation for the energy sector, theGovernment has taken several important policy initiatives to promote theachievement of Sixth Plan objectives. These initiatives, which are discussedin detail below, have addressed some of the constraints that impeded theachievement of the Fifth Plan targets and underscore the Government's commit-ment to restructuring the energy sector. Despite these efforts, the SixthPlan's supply targets are not likely to materialize fully, particularly forelectricity, domestically refined petroleum products and natural gas. Theshortfall in the supply of elecrricity stems primarily from the Government'sinability to mobilize domestic and foreign financial resources which inducedit to scale down subst.ntially the investment program for the power subsec-tor, where actual expend:tures during the first two years of the Plan periodare expected to be only 60Z of the original targets. The shortfall in supplyof domestically refined petroleum products is due to the Government's deci-sion to delay the implementation of projects called for under the Sixth Plan.This decision was prompted by the uncertairty regarding the economic andtechnical viability of these projects in meeting the future demand at leastcost. As for natural gas, strict rationing is expected to continue,primarily because the Government's pricing policies have failed to induce theprivate sector to accelerate exploration and development and contain growthof demand.

B. Strategy for the Development of the Energy Sector

30. The setbacks experienced in the implementation of the investmentprogram for the energy sector during the first two years of the Sixth Planand the high likelihood that existing resource constraints will continue intothe immediate future have prompted the Government to implement a comprehen-sive development strategy to address the issues impeding the development ofthe major sectors of the economy. The energy sector strategy for theproposed loan, which is outlined in the Letter of Development presented inAnnex IV, involves a two-pronged approach. The first focuses on minimizing

-11-

the shortfalls in energy during the remaining three years (FY86-88) of thecurrent Plan period and on ensuring that the slippages in investment that areexpected to occur do not become a major impediment to the implemeiztation ofthe Seventh Plan. Hence, it concentrates on the implementation of: (a) acore program of high priority projects; and (b) policy actions and institu-tional reforms needed to mobilize sufficient revenues for executing theseprojects, restrain the growth of demand for energy and enhance planning andproject implementation capabilities in the sector. The second calls forstudies that would provide the inputs needed to promote the integrateddevelopment of the sector over the Seventh and Eighth Plans. The Govern-ment's development strategy for the energy sector is described in detailbelow and summarized in Annex V under the following three headings: invest-ment and development; pricing and demand management; and institutionaldevelopment.

C. Investment and Development

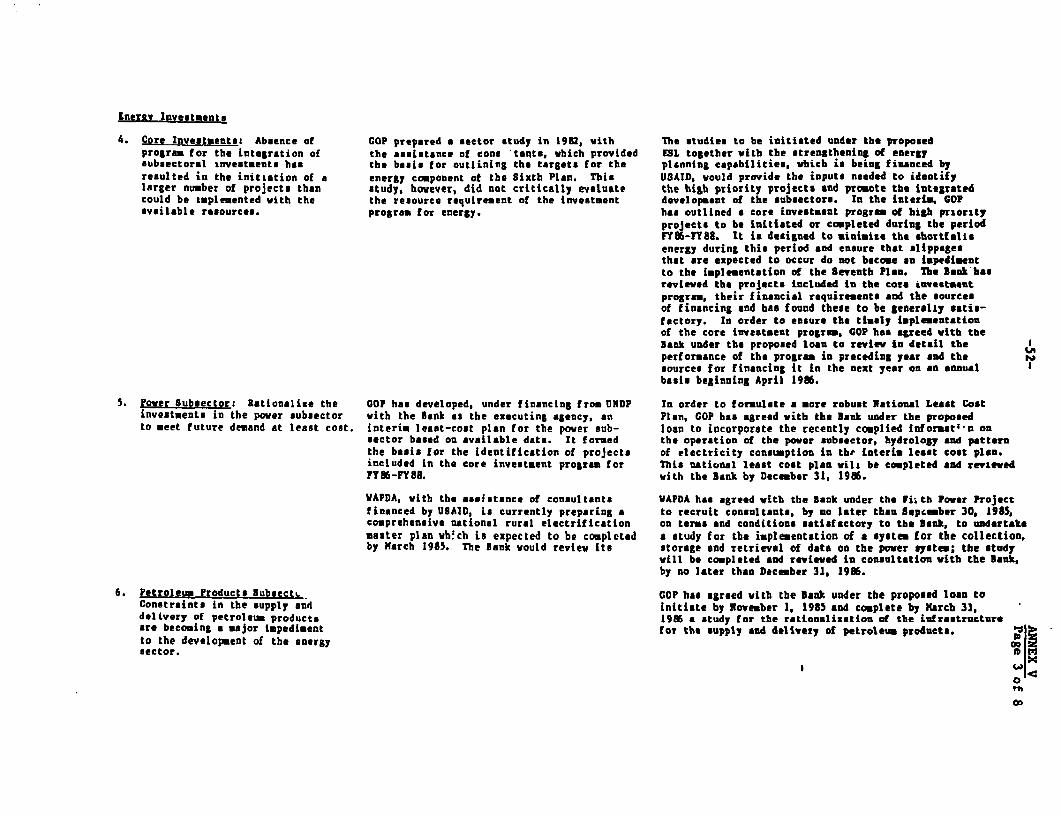

Euergy Investments

31. Core Investment Program: Pakistan's investment plans for thedevelopment of primary and secondary energy have been progressing in apiecemeal fashion, dictated primarily by the availability of financialresources. Moreover, the planned cargets have been ambitious relative tothe availability of financial resources. This divergence between actual andplanned investment has not only precluded the achievement of the supplytargets, but has also resulted in the distribution of limited resources amonglow and high priority projects. Pakistan's energy plans also suffered fromthe absence of a core investment program which would receive priority in theallocation of resources and from insufficient attention being given to theinterdependence of projects and the subsectoral interlinkages (coal, elec-tricity, etc.). The core investment program for energy, which was formulatedby the Pakistan Energy Working Group with assistance from the Bank, wasadopted to address these shortcomings.

32. The Government's core investment program covers the remaining threeyears (FY86-88) of the Sixth Plan and includes ongoing and new projects aswell as the rehabilitation and maintenance of existing facilities whoseeconomic operation is critical to the achievement of the revised targets.The core investment plan takes as its point of departure a demand projectionfor energy, disaggregated by product, for the period 1985-1993. It wasderived on the basis of a detaiLed review of the developments in the energysector and in the major energy consuming sectors of the economy. Theprojects included in the core investment plan were matched with the forecastdemand for energy. The projects were then ranked on the basis of theirexpected rates of return and selected in a descending order to ensure that,when aggregated within and across sectors, they would meet this demand atleast cost to the economy. The financial requirements in terms of foreignexchange and local costs were ascertained for each project in each subsectoron an annual basis. This provided the total investment required in theenergy sector for FYs 86, 87 and 88. The financial projections of eachimplementing agency as well as the projecced annual allocations by theGovernment were reviewed to assess the adequacy of the financial resources

-12-

for the implementation of the proposed projects. The investment requirementswere then matched through an iterative process with the sources of financing.This culminated in the core investment program which is achievable in termsof both implementation capability and availabiLity of financial resources.

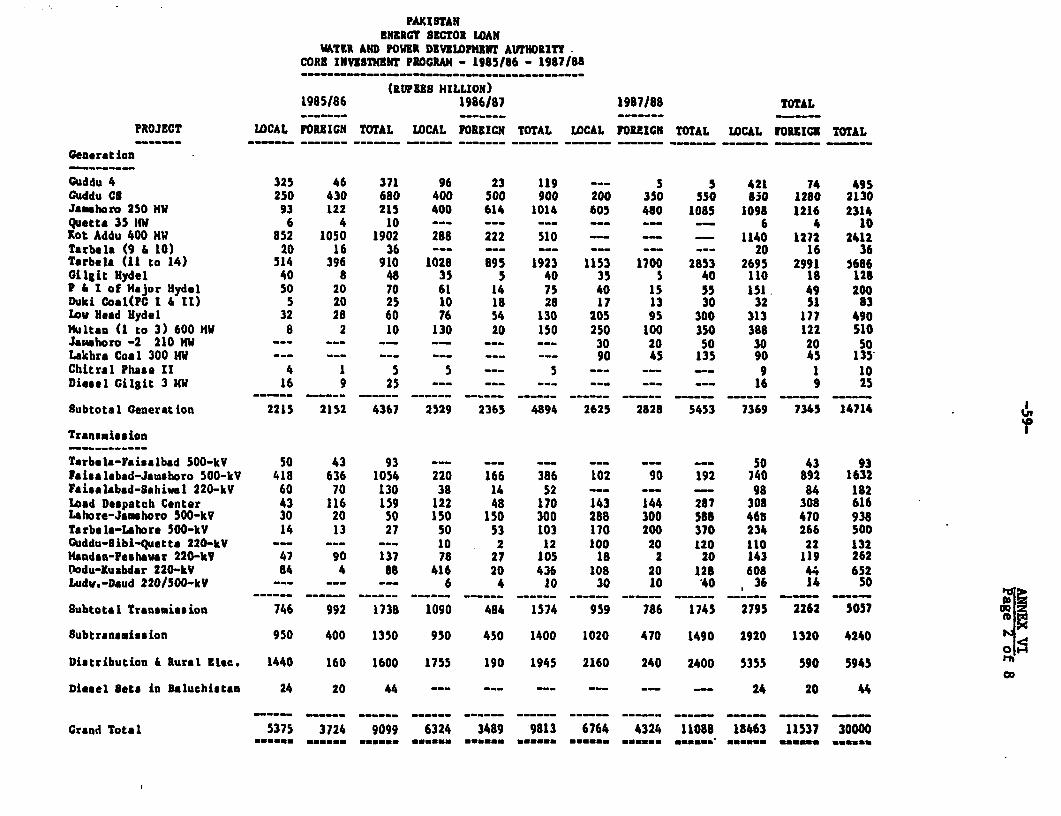

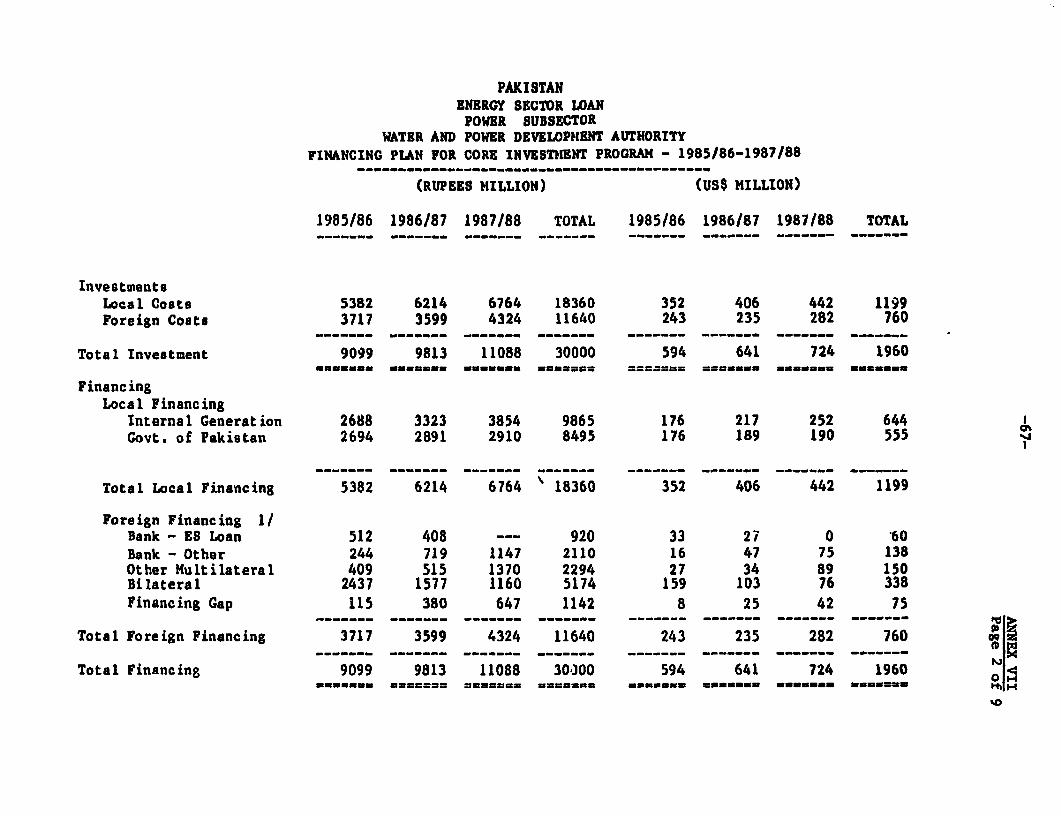

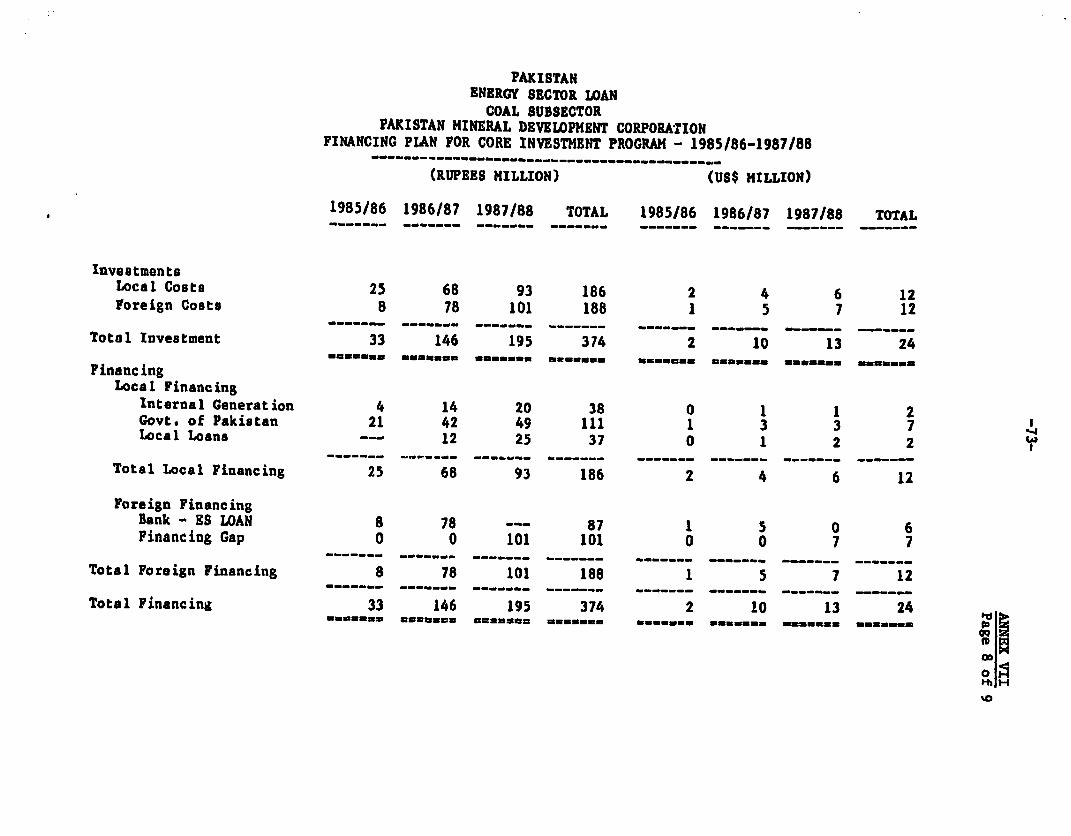

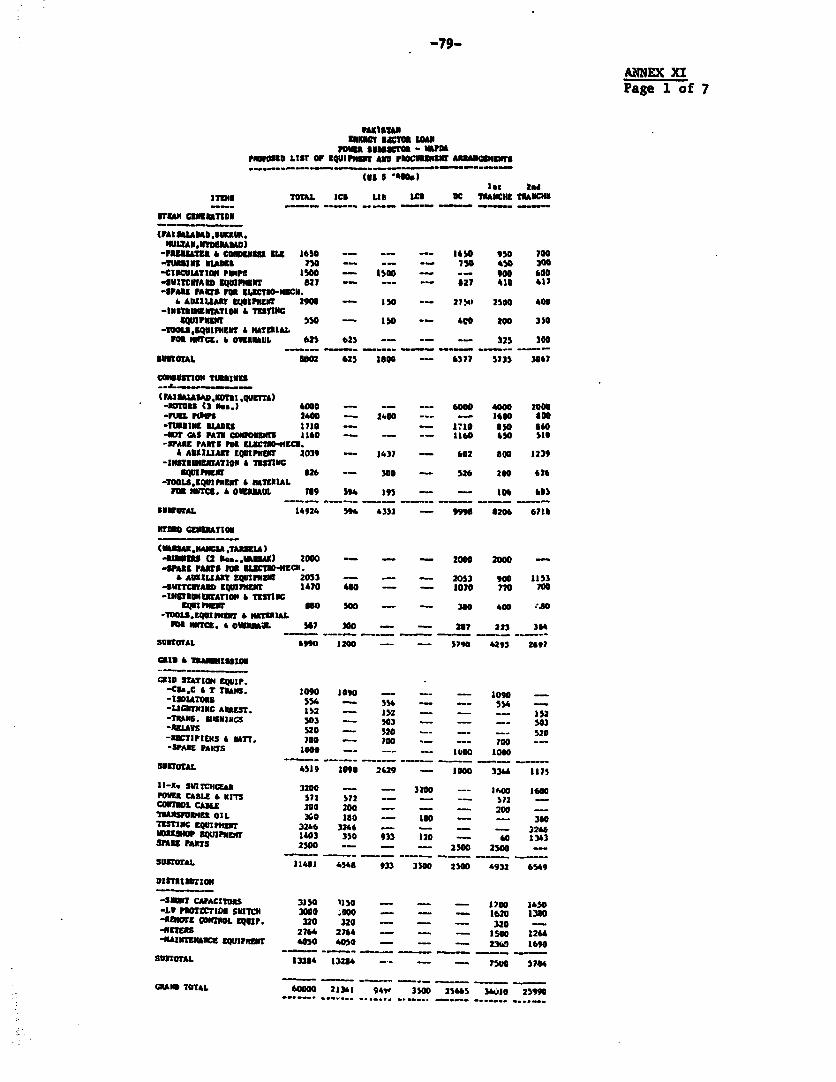

33. The core investment program encompasses high priority projects to becompleted or initiated during the next three years (FY86-88) by OCDC, WAPDA,KESC, Pakistan State Oil (PSO), Sui Northern Gas Pipeline Ltd. (SNGPL),Karachi Gas Company (KGC) and Pakistan Mineral Development Corporation(PMDC). It also includes the services of consultants for energy audits andfeasibility studies as well as instrumentation purchases for energy conserva-tion. The financial requirements of the core investment program amount toabout Rs 50 billion (US$3.2 billion) to be allocated over the next threeyears as follows: Rs 16.0 biLlion (US$1.0 billion) for FY86; Rs 16.0 billion(US$1.0 billion) for FY87 and Rs 18.0 billion (US$1.2 billion) for FY88. Ofthe financial resources earmarked for the core investment program, Rs 36.5billion (US$2.3 billion) would be absorbed by the power subsector; Rs 13billion (US$0.8 billion) by the petroleum subsector; Rs 0.4 billion(US$24 million) by the coal subsector; and Rs 0.2 billion (US$17 million) byenergy planning and conservation activities. The details relating to thecore investment program for each entity are presented in Annex VI. The scopeof the programs to be implemented by OGDC and WAPDA, which are expected toabsorb about 78% of the core investment program outlays, is described below.

34. OGDC's core investment program consists of three main elements: thefirst covers the appraisal and development of fields to be undertaken by theCorporation using its own internally-generated funds and Government alloca-tions; the second covers exploration and development activities to be under-taken under existing joint ventures; and the third involves new joint ven-tures in prospective areas for which further efforts would be made by Govern-ment to mobilize private sector participation. OGDC would concentrate itsefforts on the following: the development of oil and gas fields at Toot,Pirkoh, Dakhni and Tando Alam, smaller investment projects such as Rhodo andSari/Hundi in strongly gas-prone areas, and a modest-sized explorationprogram which gives priority to potentially high-yielding prospects in thevicinity of the Tando Alam discovery and important gas prospects such asLoti. The joint venture components of the core investment program aredesigned with a view to supplementing OGDC's technicaL capabilities andmobilizing resources for exploration and development. The component of thecore investment program covering the existing joint ventures would involveOGDC's non-operating interest as minority partner in Badin and North Potwar,with financing provided by the Corporation and the Bank under the proposedPetroleum Resources Joint Venture Project to cover OGDC's foreign exchangeshare. The component covering the new joint ventures are yet to be firmedup; however, resources have been earmarked under the proposed PetroleumResources Joint Venture Project to finance OGDC's share of any prospectiveagreemeun.s. The implementation of this core investment program would fullyabsorb the Corporation's technical, managerial and financial resources. Theprogram i's viewed as the most effective strategy for enhancing OGDC's perfor-mance and for minimizing the risk to public resources.

-13-

35. WAPDA's core investment program for generation incLudes essentially:the extension at TarbeLa, with completion of units 9 and 10 (2x175 MW) andinitiation of units 11 to 14 (4x406 KW); the completion of a steam unit (210MW) and a combined cycLe group (450 MW) at Guddu; the compLetion of a combus-tion turbine station (4x100 MW) at Kot Adu; the completion of a firstfuel-fired unit (250 MW) at Jamshoro and the initiation of a second unit (210MW); the initiaticn of a fuel-fired station at Multan (3x210 MW) and of theLakhra coal-fired station (300 MW). For power transmission, it includes thecompletion of the first 500-kV scheme Tarbela-Faisalabad- Jamshoro and theinitiation of a second 500-kV scheme Tarbela-Lahore- Jamshoro. The 220-kVnetwork and subtransmission systems will also be expanded to ensure theirintegrated and coordinated development with the 500-kV grid. The distribu-tion system will be reinforced and expanded in order to add about one milLionconsumers. The only major investment not included in the core program is theKalabagh generation project, for which, because of its size, special finan-cial arrangements will be required. However, its exclusion is consistentwith the methodology of formulating the core program, because the projectwould not, in any event, come onstream during the period for which demand isprojected.

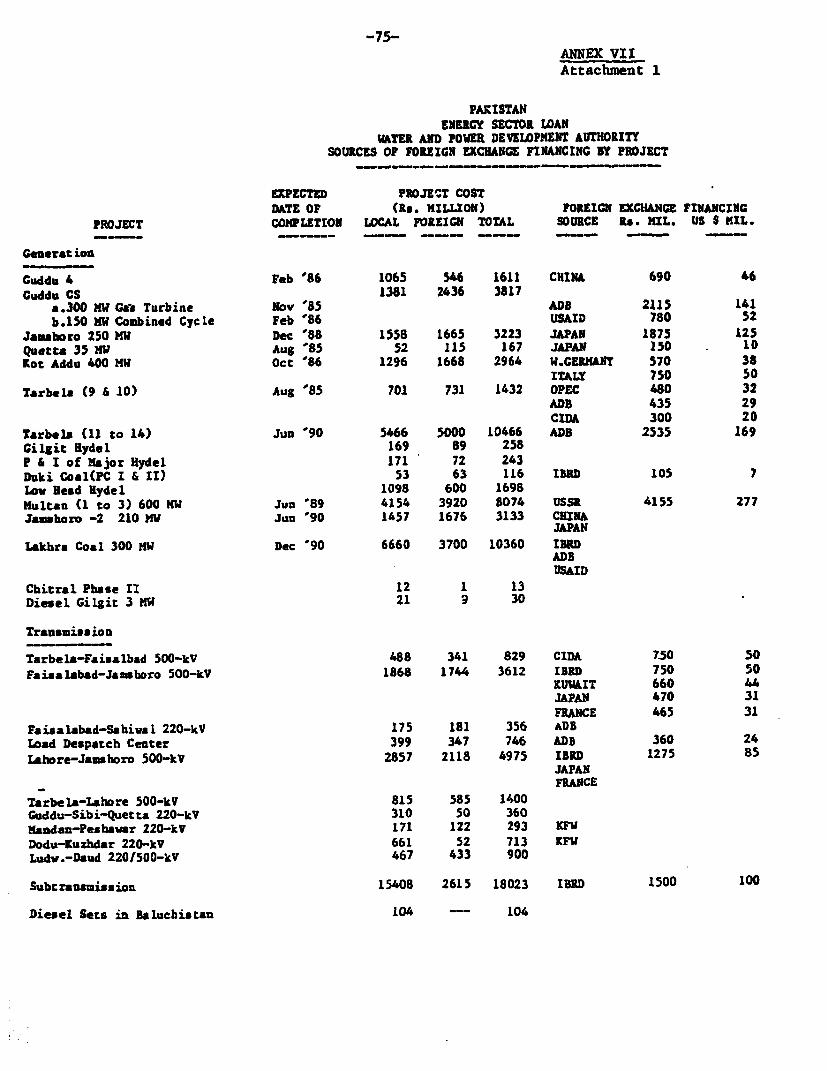

36. To finance the core investment program, the Government would con-tribute Rs 10.5 billion (US$0.7 billion) from the Annual Development Plan andthe contribution of the entities from their internally-generated funds wouldamount to Rs 14.7 billion (US$0.9 billion). The remaining Rs 24.6 billion(US$1.6 billion) would be in the form of loans, grants and suppliers'credits. The sources of financing for the core investment program arepresented in Annex VII. In order to ensure that resources are made availablefor the timely implementation of the high priority projects included in thecore investment program, the Government has agreed under the proposed loan toreview with the Bank in detail the performance of the program in the preced-ing year and the sources for financing it in the next year on an annualbasis, beginning April 1986 (Schedule 4, paragraph (b) of the draft Loar.Agreement).

Energy Development

37. Hydropower: Hydropower is Pakistan's most important source of energywith the potential estimated at about 30,000 MW. Of this, only 2,897 MS hasbeen developed and 1,928 MW are under consideration/construction. Another3,600 MW will be added when the site at Kalabagh is fully developed.Detailed engineering has been completed and preparations are underway forinitiating the implementation of this scheme during the Seventh Plan(FY89-93). The Government has also completed a study for ranking hydropowersites on the Indus River whose potential is greater than 200 MW. Of thesesites, Basha and Dasu, whose potential is estimated at about 2,500 MW and2,700 MW respectively, are ranked first and second, after KaLabagh, fordevelopment. The Government's long-term plans call for developing the sitesat Kalabagh, Basha and Dasu by the year 2020. Detailed cost estimates arerequired for integrating the development of these sites with the program forthermal generation and determining the optimal timing for their implementa-tion and commissioning. So far, cost data are only available for Kalabaghand only a feasibility study has been completed, with the assistance of

-14-

consultants financed by CIDA, for Basha. Therefore, in order to ensure thatthe hydrosites following Kalabagh are exploited and commissioned at theoptimal time, minimal cost, and in full integration with thermal generation,the Government has agreed under the proposed Loan to recruit consultants byDecember 31, 1986 to initiate the preparation of detailed site investigation,engineering and cost estimates for Basha (Schedule 5, paragraph 1 of thedraft Loan Agreement). The Government would also initiate in due coursesimilar work for Dasu.

38. Hydrocarbons: Natural gas is Pakistan's main commercially exploitedhydrocarbon resource. Its knLown reserves are estimated at about 340 milliontoe, consisting of 271 million toe of proven reserves and 69 million toe ofprobable reserves. Proven reserves of oil, by contrast, are modest,estimated at about 13 million tons. In addition to the proven reserves,probable oil reserves at known fields are estimated at 3 million tons andpossible reserves at about 6 million tons.

39. In recognition of the prospects for increasing the domestic outputof hydrocarbons, particularly gas, the Government has actively promoted theinvolvement of public and private sector enterprises in exploration anddevelopment of oil and gas over the past two years. As a result, explorationand development have accelerated. In 1984, a record number (46) ofexploratory and development wells were spudded or drilled and four new oiland two new gas fields were discovered. Although there was a significantimprovement in the drilling performance of the Oil and Gas Development Cor-poration (OGDC) in 1984 compared to the Fifth Plan, it was unable to achievethe targets set in the Sixth Plan, due to resource and implementation con-straints. Seismic surveys in the offshore areas, undertaken with the assis-tance of Norway, have identified four promising structures for drilling andfurther evaluation. The Government has finalized negotiations for offshoredrilling of oil-bearing structures located in the Tndus basin. Agreement hasalso been concluded with the private sector on producer prices for gas fromexisting fields at Mari and Sui, which has resulted in satisfactory progressbeing made in the development of this resource.

40. Despite this progress, the exploration and development program needsto be expanded to minimize the anticipated shortfalls in gas supply andachieve the Government's objectives of reducing Pakistan's dependence onimported energy. This requires a national policy aimed at increasing thelevel of foreign and local private equity investment and balancing the invol-vement of the public and private sector in expLoration and development. Sucha policy requires the delineation of the scope of exploration and developmentprogram to be undertaken by OGDC over the next three years (FY86-88). This,in turn, makes possible a parallel delineation of the need for, and theapproach to be followed in attracting private sector participants, bothforeign and local. The Government has identified a core investment programfor OGDC which focuses its activities on high priority projects(paragraph 34). The core investment program includes OGDC-implementedprojects and exploration and development invesements for which furtherefforts would be made to mobilize private sector management and capital tosupplement OGDC's efforts. The Government intends to continue its efforts toattract private exploration investirent in open areas and consider "farm-ins"

-15-

to OGDC acreage on appropriate terms. In particular, the Government plans toundertake new efforts to seek joint venture partners, especially in areaswhere gas discoveries have already been made, once the new gas producer priceformula is announced (paragraph 47).

41. Coal: Coal and lignite reserves are estimated at about 835 milliontons, of which only 107 million tons are proven. Of the total reserves,about 80Z are held by the private sector and the remaining 201, amounting to165 million tons, are held by Pakistan Mineral Development Corporation(PMDC), a Government-owned entity. The size of the proven reserves in theprivate and public sectors is believed to be substantially lower than thecountry's potential; however, as yet, very little is known of the geology ofcoal in Pakistan.

42. The Government has decided to undertake a systematic program for theformulation of a comprehensive coal expLoration strategy. The GeologicalSurvey of Pakistan (GSP), and the US Geological Survey have signed an agree-ment to undertake joint work, under USAID financing, to identify prioritiesfor exploration drilling and geophysical analyses. The first phase of thiswork involves the assessment of the reserves at Lakhra and Sonda-Thatta in1985 and 1986 and the Salt range and Makerwal reserves in 1987 and 1988.This work would identify the concessions, private and public, where furtherexploration is justified. In addition, WAPDA is currently implementing aprogram, under World Bank financing (1355-PAK), aimed at firming up theextent of the reserves at Dukki in Baluchistan and to eventually prepare afeasibility study for mining the coaL for power generation. The Governmentis also assessing, under USAID financing, the potential for stimulatingincreased private sector investment in coal production using the work onLakhra as a model. Should the results prove favorable, the same model couldbe applied to other promising reserves. In addition, the Government hasagreed under the proposed loan to initiate a two-phase program to promotethe accelerated development of coal. The first phase would involve a highlyfocused study to be completed by September 30, 1986, to identify the mainoperational constraints being experienced and outline a plan of action foraddressing them. The second phase would involve the implementation of theplan of action which will be initiated by December 31, 1986 (Schedule 5,paragraph 6(a) of the draft Loan Agreement).

43. Long-Term Development Plan for the Power Subsector: The power sub-sector accounts for almost two-thirds of the overall investment in energy andone-fifth of the public investment. Despite its size and relative impor-tance, the development of the power subsector has not been dictated by aleast cost program which identifies priority projects and the scale andtiming of investments to ensure that resources are earmarked for theirimplementation. This, together with the Government's inability to mobilizeresources, resulted in the commissioning of only 60% of the forecast gener-ating capacity, 85% of the primary transmission lines and 53% of the secon-dary transmission lines during the Fifth Plan. For essentiall*y these samereasons, the targets of the Sixth Plan for the power subsector' al'so are notlikely to materialize fully. In fact, as was noted (paragraph 29), actualexpenditures in the power subsector during the first two years of the current

-16-

Plan period are expected to be only 60% of the original targets. The short-falls in implementing the investment program for the power subsector and thesupply constraints ensuing therefrom have also prompted the Government toassign higher priority to increasing the country's generating capacity thanto the reinforcement and rehabilitation of the transmission and distributionnetwork. This, in turn, has kept the losses at the transmission and dis-tribution networks inordinately high compared to other system with a similarconfiguration, theteby necessitating further load-shedding. In recognitionof the possible adverse impact of excessive load-shedding, the Government hasdecided to improve the efficiency of and rationalize investments in the powersubsector. In order to improve the efficiency of the system, the Governmentis currently being assisted by USAID in reducing the losses in the distribu-tion network (paragraph 51) and by the Bank in expanding and reinforcing thetransmission network. As for rationalizing investments, an interim leastcost plan was formulated jointly by WAPDA and Argonne Laboratory (USA), underUNDP financing with the Bank as the executing agency, for the period1985-2005. It provides the umbrella for the long-term development of thepower subsector. A subset of the least cost plan, covering the period1985-1993, was identified. The front-end of this plan provides a list ofongoing and new generation, transmission and distribution projects that areto be initiated or completed by WAPDA between 1985 and 1993. These con-stitute the core investment program for WAPDA (paragraph 35). In order toreaffirm its commitment to rationalizing investments in the power subsector,the Government intends to finalize the interim least cost plan for whichextensive information on the operation of the power subsector, hydrology andpattern of electricity consumption is currently being prepared. The Govern-ment has decided to use these data and complete the formulation of thenational least cost plan and review its results with the Bank by December 31,1986.

44. Long-Term Development Plan for the Petroleum Products Subsector:Constraints in the supply and delivery of petroleum products are becoming amajor impediment to the deveLopment of the energy sector. Inadequate porthandling facilities for the delivery of oil and petroLeum products, shortagesof storage facilities throughout the country, and a serious imbalance betweenthe production of and demand for petroleum products, particularly up-country,are expected to become more pronounced, unless major investmetLs are under-taken to ensure that future demand is met at least cost. The Government hasagreed under the proposed loan to complete by March 31, 1986 a study for therationalization of the infrastructure for supply and delivery of petroleumproducts (Schedule 5, paragraph 9 of the draft Loan Agreement). The purposeof the study is to outline a least cost development plan for the petroleumsubsector which takes into account the plans for the increased use of bothdomestic and imported coal for power generation; the new mid-country powerplants to come on stream and the prospects for increasing the production ofdomestic oil and natural gas.

Pricing and Demand Management

45. Consumer Gas Prices: Since the discovery of natural gas in Pakistanin 1952, its consumption has increased rapidly. By 1981, consumption startedto surpass supply. As a result, the Government decided to introduce measures

-17-

aimed at restraining the growth of demand and stimulating increased produc-tion. On the supply side, a new cost-plus formula was adopted to inducegreater participation by the private sector in exploration for gas. On thedemand side, the Government agreed with the Bank under SAL I to the gradualincrease in the domestic price of natural gas to reach two-thirds of theborder price of fuel oil by FY88. Consumer price of gas has increased inrupee nominal terms by 125% between 1981 and 1984, which brought the averagedomestic price of gas in December 1984 to 392 of fuel oil parity. TheGovernment will continue to increase the price of gas to achieve the FY88target. Thereafter, the Government has agreed under the proposed Loan toreview with the Bank the general strategy and the measures for inducingconsumers to use this scarce resource more rationaLly and mobilize resourcesfor the development of the subsector (Section 3.06 of the draft Loan Agree-ment).

46. In 1981 the Government commissioned, under Bank financing, a gasstudy aimed at outlining a strategy for baLancing the forecast demand andsupply. This study was completed in 1982 and was used to set a frameworkfor the Gas Development Plan which resulted in increased development includ-ing four projects that received Bank financing. Significant new gas resour-ces are now likely to be available from Pirkoh, Dhurnal, the Badin concessionand Dakhni and the results of drilling on the Loti gas prospect will be knownsoon. Accordingly, the Government has agreed under the proposed loan toinitiate by no later than December 31, 1985: (a) a study to revise the GasDevelopment Plan to determine the optimal supply and utilization pattern forthe next five years; and (b) a study to outline a demand management policyaimed at improving the efficiency of gas supply and consumption. The resultsof these studies would be reviewed with the Bank by December 31, 1986(Schedule 5, paragraph 2 of the draft Loan Agreement).

47. Gas Producer Prices: As stated above, the Government introduced in1981, a cost-plus formula for setting producer prices aimed at stimulatingthe interest of foreign and local firms in accelerating exploration anddevelopment activity in Pakistan. This formula, however, has not eLicitedthe response hoped for from international oil companies. As a result, theGovernment has outlined a new framework for gas producer prices to stimulatethe interest of the private sector. The key elements of this framework are:(a) the price paid to the producer for pipeline quality gas will equal 66Z ofthe international price of fuel oil at main consumption centers, adjusted forthe transport cost of gas from the field to main consumption centers, less apercentage discount; (b) the magnitude of the discount is to be negotiatedand agreed in Concession Agreements before commencing exploration. Thediscount will vary from area to area and will take into account, among otherthings, the geological risk and location of the concession, anticipatedexploration and development costs, oil market conditions and cost of produc-tion. It is the Government's intention to negotiate discounts with the basicobjective of stimulating accelerated exploration by private investors; and(c) the new price formula will apply to all non-associated gas from newconcessions signed on or after September 30, 1985. The Government has agreedunder the proposed loan to make an announcement of the new policy by June1985, and widely publicize it within oil industry circles (Section 3.07 of

-18-

the draft Loan Agreement). The Government intends to keep the operation ofthis formula under review.

48. Electricity Pricing: WAPDA's resource mobilization through tariffshas not been as high as planned by the Government. This, together with thereduction in the budgetary allocation precipitated by resource constraintsexperienced over the past few years, resulted in substantial reductions inthe development program of the Authority. To address this shortcoming,future increases in tariffs would now be directly linked to the three-yearcore investment program, set at Rs 30 billion, according to the formulaagreed with the Bank in the loan agreement for the Third WAPDA Power project.The Government has agreed with the Bank under the Fourth WAPDA Power Project(P3940-PAK), henceforth to adjust tariffs to ensure that at least 40% of theinvestment expenditures called for under the core investment program arefinanced from WAPDA's internal sources (Schedule 4 of the draft Loan Agree-ment).

49. Coal Pricing: Coal prices, unlike other energy products, are notset by the Government but are determined by market forces. However, becauseof its size and the institutional structure governing the tendering proce-dure, PKDC acts as the price setter. As PMDC's costs of production aregenerally higher than those of the private sector, this approach results inhigher prices for domestically produced coal. Despite this distortion, theaverage ex-mine price of PMDC coal of US$84/toe in Baluchistan, US$74/toe inPunjab and US$48/toe in Sind compares favorably with the cif price ofUS$90/toe for imported coal.

50. Since the coal produced in Pumjab and Sind, which accounts for aboutone-half of the country's annual production, is consumed locally, transportcosts add, on the average, only about US$12/toe to the price paid by thefinal consumers. However, the other half, which is produced in Baluchistan,is consumed largely in Sind and Punjab. The transportation costs for thiscoal which, on the average, amount to US$70/toe, add substantially to theprice paid by the consumer. These inordinately high transportation costsare attributable to the bottlenecks in the rail transport system which neces-sitates transporting coal from Baluchistan by trucks to Punjab and Sind. Inrecognition of the fact that the economic value of the fuel used by thetrucks far exceeds that of the coal they carry, the Government has decided toaddress the structural imbalance between the sources of supply and locationof final consumers. As a first step, the Government has initiated aprefeasibility study for the expansion of the infrastructure for coal han-dling around Karachi, aimed at meeting the demand fcr coal in Punjab andSind. When implemented, this development would allow for the importation ofcoaL for these two provinces which would be more economic than the coal fromBaluchistan. In addition, in order to create an expanded market for importedcoaL, the Government has agreed under the proposed loan to allow its use forpower generation in the Karachi area (Schedule 5, paragraph 3 of the draftLoan Agreement). A prefeasibility study is already underway for a powergenerating complex around Karachi. As for Baluchistan, a program is cur-rently underway to firm up the reserves at Dukki (paragraph 42) which couldset the stage for expanding the local coal market by leading to the estab-lishment of mine-mouth power plants. In addition, in order to improve the

F

-19-

efficiency of PHDC, and in turn, reduce its cost of production, the Govern-ment has agreed under the proposed loan to complete by November 30, 1986 astudy that would: (a) outline a strategy for corporate restructuring andtechnical improvements to promote the more efficient operation of mines inthe public sector; and (b) provide a basis for reviewing the role of thepublic sector in coal mining (Schedule 5, paragraph 6(b) of the draft roanAgreement). In the incerim, through its ongoing work in the encrgy sectorthe Bank will continue to monitor the performance of PMDC as well as domesticcoal prices relative to the costs of imported coal.

51. Demand Management: In keeping with the objective of the Sixth Plan,the Government has already taken several important initiatives to rationalizeenergy consumption including: (a) steps to enhance the energy efficiency ofthe NRL refinery, a major energy consumer; (b) a survey of energy consumptionin public sector industries to be followed in 1986-87 with some 20 energyaudits and assessments in the cement, steel, fertilizer, chemical, and otherindustries in the public sector which are designed to define the potentialfor energy conservation, leading to investments resulting in substantialreductions in industrial energy consumption; (c) studies designed to reducelosses in the power transmission and distribution networks; (d) the iden-tification of thermal power plants whose efficiency could be improved throughrehabilitation and retrofitting; (e) the formulation of a least-cost develop-ment plan for the power subsector that would set priorities for investmentsin generation, and ensure the optimal use of primary energy resources;(f) upward adjustments in the consumer price of gas; and (g) the release ofgas from cement industries and the power subsector for higher value uses.The Bank has supported the Government's policy initiatives through SAL I(2166-PAK), the Fourth WAPDA Power Project, a Refinery Engineering Project(2218-PAK), a project for Fertilizer Industry Rehabilitation (2172-PAK) andTechnical Assistance. UNDP, with the Bank as the executing agency, isfinancing the formulation of the least cost plan for power. USAID is assist-ing the Government in implementing its program for reducing losses in thepower subsector at the distribution level (paragraph 43). UNIDO is currentlyfunding a program of audits of a number of smaller textile, metal-working andother plants. Although important, these initiatives are but a first step inthe formulation of a comprehensive strategy for rationalizing the consumptionof energy. If the objective of energy conservation is to be achieved, a moreintegrated and comprehensive strategy is needed. Toward that end, theGovernment has agreed under the proposed loan to establish by December 31,1985, mainly with the assistance of USAID, an Energy Conservation Center(ENERCON) in the Ministry of Planning (Schedule 5, paragraph 8 of the draftLoan Agreement).

Institutional Development

52. Operational Autonomy: The two most important agencies in the energysector, WAPDA and OGDC, need considerable strengthening and greater fiscaland managerial autonomy. The possibility of separating distribution ofelectricity from WAPDA and assigning WAPDA with the responsibility for gener-ation and transmission of electricity for the entire country will beexamined. This would include looking into the possibility of taking over thegeneration and the primary transmission of KESC by WAPDA and restricting the

-20-

KESC operation to bulk purchase from WAPDA and distribution in the Karachiarea. Additionally, the possibility of handing over distribution to privatesector/provinces in the rest of the country would be considered along withthe possibility of creating a separate authority for power distribution. Inorder to assist WAPDA in formulating a plan for the reorganization of itsdistribution department, consultants have been recruited under USAID financ-ing. The Government has agreed under the proposed loan to review with theBank the means and the timetable for reorganizing the power subsector by June30, 1986 (Schedule 5, paragraph 7(a) of the draft Loan Agreement).

53. The Sixth Plan envisages an expanded role for OGDC whose investmentactivity is expected to triple as compared to the Fifth Plan. OGDC's finan-cial position is expected to improve considerably in FY85 as a result of:(a) the Government's decision to allow OGDC to retain a larger share of itsearnings and the setting of oil and gas prices similar to those available tothe private sector in adjacent areas; and (b) anticipated increases inproduction from the Pirkoh gas field and the Tando Alam oil field. Not-withstanding the improved self-financing outlook for OGDC, the key con-straints to OCDC's expanded activities will be directly related to itsability to recruit and retain qualified professional staff and to operate asa commercial concern. The Government intends to take further steps tostrengthen OGDC's managerial and technical capabilities and to move towardsfinancial self-reliance. Accordingly, the Government has agreed under theproposed loan to review with the Bank by June 30, 1986, the measures neededto move OGDC toward that objective and the timetable for their implementation(Schedule 5, paragraph 7(b) of the draft Loan Agreement).

54. Energy Planning: In recognition of the increasing importance of theenergy sector in sustaining the country's growth momentum, the Government hasdecided to strengthen its energy planning capability. Toward that end, anoffice of Energy Planning (ENERPLAN) has been established in the Ministry ofPlanning and Development under financing from USAID to address substantivepolicy issues. It is mandated to coLlect, compile and analyze, on an ongoingbasis, all relevant data on the energy sector and integrate them with thecountry's development plans to enable the Government to identify priorities,evaluate resource requirements, support effective policy formulation andinvestment planning. ENERPLAN, which is divided into two groups, one fordeveloping an energy data system and the other for data analysis, is headedby a Managing Director who was recently appointed. It will be administeredby an interministerial Energy Policy Board. ENERPLAN will be staffedentirely by Pakistani personnel who will be assisted during the first fouryears by consultants financed by USAID. In order to ensure that ENERPLAN'sactivities would provide the input needed for effective policy decision, andintegrated energy sector and macroeconomic planning, the Government hasagreed under the proposed loan to review, on an annual basis, beginning April30, 1986, its scope of work jointly with the Bank, USAID and ADB (Schedule 5,paragraph 5 of the draft Loan Agreement).

55. Energy Conservation: There is an increasing awareness in Governmentcircles and, to a lesser extent, in the private sector of the potentialbenefits of energy conservation. According to a recent study by USAID con-sultants, in the industrial sector alone, energy conservation investments of

-21-

about US$330 million could yield annual savings of about US$200 million. Asmentioned (paragraph 51), a number of conservation activities have beenundertaken in the recent past. However, as one would expect in the initialstages of development of such a program, these efforts are proceedingpiecemeal. To be effective, conservation activities need to be coordinated;therefore, the establishment of ENERCON will be a critical first step. TheCenter will serve as the focal point for all conservation activities and itsmain responsibilities will be to formulate comprehensive and integratednational energy conservation programs covering industry, power, transport,agriculture, households, and commercial and residential buildings; plan andinitiate energy conservation actions; outline policy guidelines; develop adata base; support training activities and private research; undertakedevelopment and demonstration, as well as public information activities; andmonitor the implementation of conservation programs of various public andprivate entities. ENERCON would also mobilize resources to finance invest-ments in energy conservation measures such as energy audits, feasibilitysLudies, instrumentation purchases, retrofitting, fuel substitution andtechnological changes, and support these with fiscal and other incentives.InitialLy, the Center would focus on energy audits in the industrial sectorand the power subsector. A detailed action program for ENERCON is currentlybeing prepared with the assistance of the Bank and USAID. The Center isexpected to formulate a comprehensive national conservation program withinabout one year. Tl. Government has agreed under the proposed loan to reviewthe activities of ENERCON jointly with the Bank and USAID on an annual basisto ensure that these are consistent with the national conservation program(ScheduLe 5, paragraph 5 of the draft Loan Agreement). Administratively,ENERCON will work in close collaboration with ENERPLAN. The Center will beheaded by a Director and manned with long and short term expatriate advisersand Pakistani professional and support staff. The work program of ENERCONwill be guided by a Supervisory Board composed of representatives of Federaland Provincial governments and the private sector. The core activities ofENERCON are expected to be financed by the Government and USAID. The Bankwould co.ntribute to the financing of public and private sector industrialenergy audits, feasibility studies and purchases of instrumentation. As afirst step, the Government has agreed under the proposed loan to ensure thatENERCON identifies by December 31, 1985, on the basis of a private sec-tor-wide energy consumption survey, at least 15 of the largestenergy-consuming plants in the private sector industries for audits to beperformed by local and foreign consultant firms. All efforts will be made tocomplete these by December 31, 1987 (Schedule 5, paragrap'. 4(a) of the draftLoan Agreement). The Government has also agreed to initiate a program ofaudits by November 1, 1985 in at least 20 of the largest energy consumingplants in the public sector industries to be performed by local and foreignconsultant firms and completed by June 30, 1987 (Schedule 5, paragraph 4(b)of the draft Loan Agreement).

56. Manpower Development: To ensure that Pakistani personnel are ableto continue the recently initiated energy planning and conservationactivities, the Government has implener.eed a sectoral manpower developmentprogram. With the assistance of consultants financed by USAID, the Govern-ment will conduct a manpower needs assessment to determine: (a) the range oftechnical, management, and analytical skilLs needed to accomplish the goals

-22-

of energy programs; (b) the present capabilities of local institutions tomeet these needs; (c) the priorities to increase skills to meet these needs;and (d) the actLons necessary to improve existing programs, together with thecost and time requirements. Based on the results of the needs assessment,ENERPLAN would organize and conduct in-country short courses and seminars onselected topics, utilizing highly qualified professionals drawn from thepublic and private sectors; identify further options for overseas training;and pursue strategies to upgrade and enhance training programs in Pakistanfor improving the planning, management, and technical implementation ofenergy sector policies.

PART IV - THE PROJECT

History

57. The proposed loan is the continuation of a process of Bank Groupassistance for long-term structural reforms initiated under the first Struc-tural Adjustment Loan (SAL I) to Pakistan (Loan 2166-PAK; Credit 1255-PAK).The SAL program for energy was wide-ranging, and included: strengthening ofOGDC; accelerated exploration of OGDC concession areas; increased privatesector participation; progressive rationalization of gas consumer prices; andcompletion of a number of detailed studies needed for long-term energy plan-ning. Although overall progress was highly satisfactory, it is clear thatreform of the energy sector in Pakistan will be a long-term process in whichcontinued Bank Group support can play a useful role. This sector loanprovides a comprehensive long-term framework for policy actions and, there-fore, will be the basis for our expanded lending for specific energy invest-ments for the next several years. The policy framework also will serve as abasis for more effective coordination of all external financing for thesector. This approach, a sector loan in support of an agreed long-termpolicy framework followed by lending for specific investments, has substan-tially enhanced our dialogue with the Government, fostering intensive andfocused discussions on issues which cut across energy subsectors and whichotherwise would have been treated, if at all, in a piecemeal and uncoor-dinated fashion through project lending. In the energy sector, the policydialogue has focused on identifying issues constraining the development ofthe energy sector and the actions and measures needed to address them. Theseactions and measures constitute an integral part of the Government's coreinvestment program whose implementation is the basis of this loan. Theproposed loan was appraised in two phases. In Phase I, which was completedin mid-December 1984, policy actions on which agreement was being sought werereviewed with the Government. Phase II, which was completed in February1985, focused on a detailed review of the investment priorities, the equip-ment and material to be covered under this loan and on issues such astimetable for the preparation of procurement documents, disbursements andconditions for tranche releases. Technical discussions and negotiations tookplace in Washington from April 15 to April 22, 1985. The Pakistani delega'tion was led by Mr. Ejaz A. Naik, Secretary General, Economic Affairs Divi-sion, Ministry of Finance.

-23-

Project Objectives