Embed Size (px)

Citation preview

Document of

The World Bank

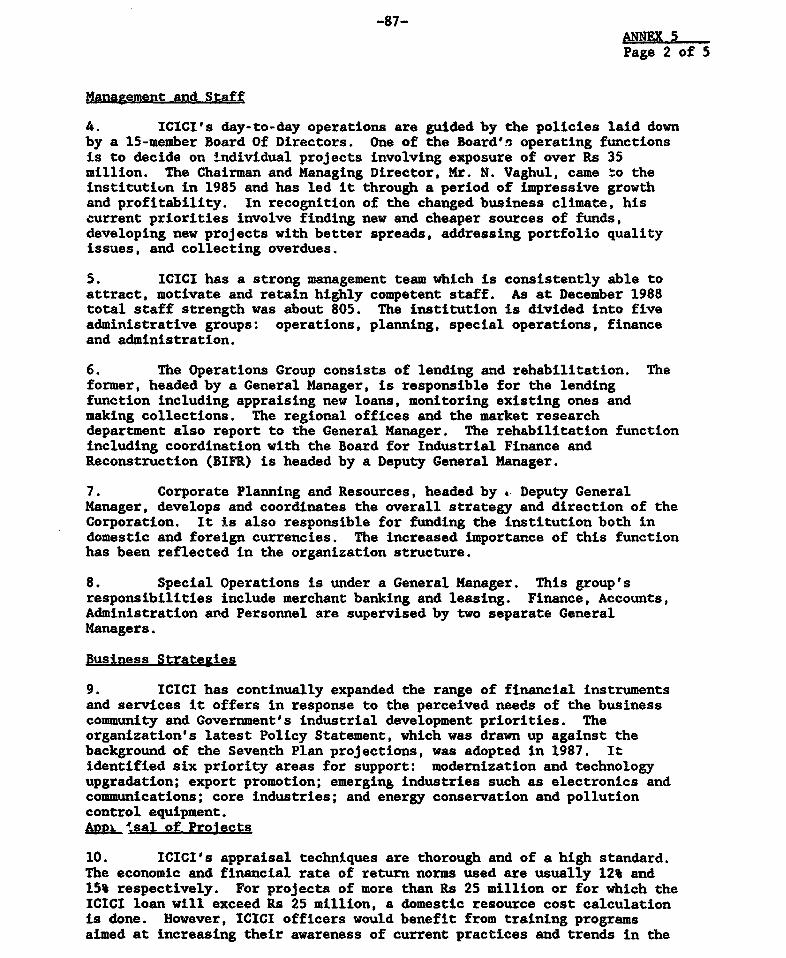

FOR OFFICIAL USE ONLY

t-N 3e093-/'V4.A/~~4

-3 o e S- /A Report No. 7704-IN

STAFF APPRAISAL REPOI'T

INDIA

ELECTRONICS INDUSTRY DEVELOPMENT PROJECT

MAY 24, 1989

Asia Country Department IV (India)Industry and Finance Operations Diviqion

This document has a restricted distribution and may be used by ecipients only in the perfonmnace oftheir officral duties. Its contents may not otherwise be disclosed without Wodd BDnk author4oo. 0

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

29& =Y EOUIVALENTS

Rs 1 - US$0.067Rs 15 - US$1.00

FISCAL YEI=

Government of India - April 1 - March 31IDBI - April 1 - March 31ICICI - April 1 - March 31

ABBREVIATIONS AND ACRONYMS

ASIC - Application Specific Integrated CircuitsCAD/CAM - Computer Aided Design and ManufacturIngCEDT - Center for Electronics Design and TechnologyDFI -Development Finanice InstitutionEPABX - Elect.onics Private Auxiliary Branch ExchangeERAS - Exchange Risk Administration SchemeEximbank - Export-Import Bank of IndiaFERA - Foreign Exchange Regulation I,tGOI - Government of IndiaIC - Integrated CircuitICICI - Industrial Credit and Investment Corporation of IndiaIDBI - Industrial Development Bank of IndiaIIT - Indian Institute of TechnologyJGF - Japan Grant FacilityLSI - Large Scale IntegrationMES - Minimum Economic ScaleMODVAT - Modified Value Added TaxMRTP - Monopolies and Restrictive Trade Practices ActOGL - Open General LicensePIU - Project Implementation UnitPMP - Phased Manufacturing ProgramPSE - Public Sector EnterpriseRBI - Reserve Bank of IndiaREP - Import ReplenishmentSCL - Semiconductor Complex Ltd.SDC - Swiss Development CooperationSFC - State Financial CorporationSSI - Small Scale IndustryVLSI - Very Large Scale Integrated Circuit

FOR OFCIAL USE ONLY

~PA

ELECTRONlICS INDUSTRY DEVELOPMENT PROJECT

STAFF APPRAISAL REPORT

Table of Contents

Page No.

IAN AND PROJECT SUMMARY ....................................T i

I. INTRODUCTION ................................................. 1

II. SECTOR BACKGROUND ............................................ 2

A. Electronics Industry Structure and Performance ........... 2B. Assessment of Competitiveness ........................... 4C. Potential and Prospects for Development .................. 5D. Policy Environment ....................................... 6E. Policy Constraints ....................................... 10F. Manpower Constraints ..................................... 11G. The Financial Sector.. ....... ,... 12

III. THE BANK'S ROLE IN INDUSTRY .................................. 18

A. Previous Bank Lending to Industry ........................ 18B. T"s Bank's Future Lending Strategy ....................... 19C. Electronics in Bank's Lending ............................ 19

IV. THE PROPOSED PROJECT ......................................... 2.

A. Project Objectives ....................................... 21B. froject Description .. 21C. Term Credit to Expand and Upgrade Electronics Capacity... 22D. Manpower Development and Training . . 23E. Technical Assistance .. 25

(i) Software Capability Devrelopment .................... 25(ii) Seminar Program .................................... 26(iii) Training and Technical Assistance for the DFIs ..... 26

F. Project Cost ......................... 27G. Financing Arrangements .................... 28

This report is based on the findings of an appraisal mission to India inJanuary 23 - 'larch 8, 1989. Mission members were Messrs. G. Gowen (SeniorEconomist), K. Arichandran (Senior Financial Analyst), J. Bredie (TechnicalEducation Specialist), Arnold Miller (Consultant), B. Wadia (Consultant),A. Bhojwani (Consultant), P. Reymond (Consultant), J. Delisle (Consultant,Swiss Development Cooperation), and A. Pittet (Consultant, SwissDevelopment Cooperation). The report was prepared by Messrs G. Gowen,K. Arichandran, and J. Bredie.

This document has a restricted distfibution and may be used by recipients only in the performanceof their official duties Its contents may not otherwise be disclosed without World Bank authorization.

- ii-

Pag-e No.

V. THE PARTICIPATING FINANCIAL INSTITUTIONS ..................... 30

A. Industrial Development Bank of India (IDBI) .............. 30B. The Industrial Credit and Investment Corporation

of India Limited (ICICI) ............................... 31

VI. THE PROPOSED LOAN ........................................... 33

A. Terms and Conditions ..................................... 33B. Administrative Procedures ................................ 34C. Project Benefits and Risks ............................... 37

VII. AGREEMENTS AND RECOMMENDATIONS ............................... 39

A. Agreements ................................... 39B. Recommendation ................................... 40

ANNEXES

1. Electronics Production 1980-87

2. Manpower Development

3. Technical Assistance

4. The Industrial Development Bank of India (IDBI)

5. The Industrial Credit and Investment Corporationof India Limited (ICICI)

6. Documents in Project File

INDIA

ELET=RONICS INDUSTRY DEVELOPMENT PROJECT

Loan and proiect Summary

B kiorrowers (a) India, acting by its President.(b) Industrial Development Bank of India (IDBI);(c) Industrial Credit and Investment Corporation of

India (ICICI).

Guarantor of theLoans go IDBIand iCI i India, acting by its President

Loan Amounvts : US$210 million equivalent to be lent as follows:(a) US$8 million equivalent to India;(b) US$101 million equivalent to IDBI; and(c) US$101 million equivalent to ICICI

Terms Twenty years, including 5 years of grace, at theBank's standard variable interest rate.

Relending terms : Development Finance Institutions (DFI) CreditComponent. The loans to IDBI and to ICICI forfixed assets and permanent working capital would berelent in foreign exchange at the Bank's standardvariable interest rate plus 2% to provide a spreadto the DFIs, or in rupees at the prevailingExchange Risk Administration Scheme (ERAS) rate(presently 15% with a cap rate of 18%). This ratewould be adjusted according to ERAS terms to coverthe foreign exchange and interest rate risks.

ProiectXDescription : The project would include the following components:

(a) private and joint sector investment (US$420million) in fixed assets and permanent workingcapital with Bank financing through IDBI and ICICI(US$202 million) us a new "single window"mechanism for financing of both term and workingcapital requirements of sub-borrowers; (b)improvement of skilled man-power development andtraining capacity of selected education andtraining institutions (US$26.8 million) throughgrants from DOE (financed by US$8.0 million fromthe Bank, $16.2 million grant funds expected fromthe Swiss Development Cooperation and US$2.6million from GOI) for equipment, training and otherassistance; and (c) technical assistance (US$3.0million) for: (i) development of the computersoftware industry studies, seminar, and projectidentification; (ii) support of electronics policy

.11-

development through seminars and studies; and (iii)upgrading the capability of financial institutionsto screen and appraise electronics projects(financing of US$2.7 million expected from JapanGrant Facility, $0.2 million from GOI and US$0.1million from the DFIs. The total cost of theproject would be US$450 million.

Risks : The credit component would provide longterm financeto about 30 subprojects, resulting in totalinvestment of about US$420 million and employmentof about 12,000 people. It would initiate reformin the system for financing industrial investmentsin the direction of increased institutionalflexibility. The manpower and training componentwould result in an upgraded capability to produce4000 middle and higher level technical andprofessional staff annually in the fields ofelectronics and computer software. The major riskof this project is that the Government willimplement further needed reforms too slowly. Thiswould commensurately reduce the pace at which theindustry achieves lower costs and increasedefficiency, which in turn would lead to less thanexpected efficiency of subsequent users throughoutthe economy. Recent policy reforms provide asufficient basis for the project, and the Bank andGovernment will continue to discuss further reformsboth in the context of macro-economic and sectorwork and the proposed project. ERAS scheme is newand will require close monitoring to ensure thatrelending rate adjusts properly to marketconditions, and the needs of financial institutionsand sub-borrowers for some predictability in theirfinancial planning. Finally, with respect to themanpower component there is a potential risk ofdelays in implementation because the organizationalset up is new, and the institutions are notfamiliar with Bank procedures. Additionalsupervision at start up will help reduce this risk.

-lii-

Estimated CGosts:

Local Ensign Total------- (US$ million) ------

Credit Line for ExpansionFixed Assets 144.1 150.0 294.1Working Capital 74.1 52. 1261.

Sub-total 218.2 202.0 420.2

Manpower Development 19.3 7.5 26.8Technical Assistance & Stvt.ies 0.6 ,2.4 3,0

Total 238.1 211.9 450.0

Financing Pla:

Bank 0.5 209.5 210.0GOI 2.8 -- 2.8Development Finance Institutions 50.7 -- 50.7Subproject Sponsors & others 167.6 167.6Swiss Development Cooperation 16.2 16.2Japan Grant Facility 0.3 2.4 2.7

Total 238.1 211.9 450.0

Estimated -Lsbursements:

Bank FY 91 22 i3 2& 95 96----------------- (US$ million)--------------

Annual 19.6 60.5 71.2 41.4 14.7 2.2 0.3Cumulative 19.6 80.2 151.4 192.8 207.5 209.7 210.0

Economic Rate of Return: Subprojects financed by the FinancialIntermediaries would have a minimum economic rateof return of 12%.

INDIA

ELECTRONICS INUSTRY DEVLPNE PROJE

STAFF APPRAISAL REPORT

I. INTRDUCION

1.01 India has the potential to develop a competitive electronicsindustry of international stature based on its large pool of high levelscientific and technical manpower, its growing and potentially vastdomestic markets, and the significant existing industrial base with itslarge pool of capable managers and entrepreneurs, including Indians nowresident abroad. After several decades of following restrictive regulatorypolicies and an inward looking trade regime, the Government, in recentyears, has enacted a far-reaching program of policy reform, which forelectronics goes further than for almost any other industry. It provides asound initial basis to try to realize this industry's immense potential forincreased production and employment and as a source of productivityimprovements throughout the economy.

1.02 The proposed Electronics Industry Development Project would assistthe Government in its further efforts to foster this industry's sounddevelopment with the objective of eventually reaching a level ofinternational competitiveness. First, it would provide technical andfinancial support to the two largest development finance institutions toimprove their capability to identify, appraise and finance economicallysound projects in this sector. Second, it would help to improve thequality of medium and high level technical and professional manpower neededfor the industry's rapid and efficient growth. Third, it would lay thebasis for expanding capacity in the most promising area, computer sofhrare,by identifying projects and measures to provide needed infrastructure.Finally, the project would provide an important basis for on-goingdiscussions between the Government and the Bank on policies for theelectronics sector and for industry as a whole.

-2-

II. SECTOR ACKGRO

A. Electronics Industry Structure and Performance

2.01 The world electronics industry reached an estimated worldvidkproduction of nearly US$500 billion in 1987, its rapid growth spurred bytechnological advances that have lowered the cost of information processingby more than 20S per year for more than four decades. It now accounts forabout 108 of worldwide manufacturing and its impact, through communications,broadcasting, and information technology reaches to every corner of theworld economy. The Indian electronics industry, established almost 25 yearzago, accounts for only about 0.6% of international electronics production.Relatively stagnant during the 1970s with an annual growth rate of 10% inreal terms, it has begun to catch up, its growth rate accelerating to 18%per annum in the first half of the eighties and to nearly 25% per annum in1985-87. Gross output reached a level of Rs 47.2 billion (US$3.6 billion)in 19e7. The industry now comprises more than 5% of manufacturing valueadded in India and is expected to continue its rapid rate of expansion.

2.02 The subsector is domestically oriented. Total exports in 1987(including free zones) reached only Rs 3.1 billion (US$240 million) andaveraged less than 7; of output, of which 42% originate from the oldest andmost active export processing zone on the outskirts of Bombay. Except forChigia, this share is low for developing countries that have significantelectronics subsectors. Imports meet only 25% to 30% of the demand forfinal products. However, except for such traditional consumer goods asradio receivers and black-and-white television sets (B&W TVs), whose inputsare mostly produced locally, the subsector imports about half of therequired materials and components.

2.03 Public sector enterprises (PSEs) account for about 40% on averageof the subsector's output, ranging from 104 in consumer goods to nearly 100%in communications and aerospece and defense. Most of the 3,000 or soelectronics firms are small-scale industries (SSIs), which produce about 25%of total output and are especially important in consumer electronics.Medium and large private enterprises account for about 35% of total output;many of the large private firms have had long-standing associations withmultinationals.

-3-

2.04 Electronics production in 1987 was as follows:

USS billiU *

Consumer electronics 1.42 38.6Industrial electronics .54 14.5Data processing &office supplies .30 7.9

Communications .56 15.0Aerospace and defense -24 6.4

Sub total 3.04

Components .55 14.8Export processing zones .10 2.8

Grand total 3.69 100.0

Source: Depa-tment of Electronics

Expansion in consumer electronics, particularly color televisionproduction, has helped to accelerate the subsector's recent growth. Thissegment now accounts for nearly 40% of total electronics output. Althoughthe production of data processing equipment has grown rapidly because ofGovernment-sponsored modernization programs in industry and in banking,output in this segment only reached about 46,000 units in 1987 (mostlymicrocomputers), representing 8% of India's electronics subsector comparedwith a 20% share ir. other countries. The industrial, telecommunicationsand components segments each command about 15% of the subsector's totaloutput. In telecommunications, two large PSEs dominate: Indian TelephoneIndustries and Hindustan Cables Limited. Industrial electronics, whichincludes several large PSEs, is concentrated in industrial process controlsand power electronics. In this segment, several firms with internationalties have been able to export worldwide. A breakdown of electronicsproduction, 1980-87 is given in Annex 1.

2.05 The structure of the components segment is highly fragmented, witha few very large firms at one end and many small producers at the other.Production is largely for use in radio and television sets. Semiconductors(mostly discrete devices) account for only 12% of India?s components outputcompared with 30% to 50% in industrialized countries. Small- and medium-scale integrated circuits (ICs) are produced by a single PSE, BharatElectronics Ltd. A second PSE, Semiconductor Complex Ltd., was producinglarge-scale integration (LSI) ICs partly from imported wafers until itsplant was destroyed by fire in early 1989 (para 2.15). Very large-scaieintegration (VLSI) ICs are still imported. In total, locally produced ICsmeet less than 10% of demand and account for only 3% component productioncompared with a much larger share worldwide.

.4-

B. Assessment of Competitiveness

2.06 India's electronics subsector has developed in an environmentprotecting it from both domestic and international competition andinsulating it from technological progress. As a result, processtechnologies are generally outmoded (8 to 20 years behind); producttechnologies are 5 or 6 years behind; and Indian electronic goods generallyhave very high production costs and prices. For example, for 10 majorelectronics products, India's factory prices in 1986 exceeded world pricesby 20% to 170% and many were of inferior quality. Products with pricesnear or below world prices, such as in printed circuit boards (PCBs) andcomputer software, are rare.

2.07 Several important factors account jor the high production costsand prices. Production scales are substantially smaller than internationalminimum economic scales (MES) of leading multinationals by factors of 20 to100 in some product lines, which affects raw material prices, capacityutilization and other costs. Indian electronics industries also bear highcustoms duties on imported components inputs and several other indirecttaxes so that total indirect taxes comprise 20% to 40% of the sales price.As scales are small most firms pay 15% to 40% above world prices obtainablethrough bulk purchase of materials and components. Profit margins for welloperated Indian firms are high by international standards for electronicsindustries (from 18% to 40% of factory prices), reflecting lowercompetitive pressures and short term profit horizons. Other factors whichhurt competitiveness include the following: India's relative isolationfrom world markets, which limits exposure to product trends and changingtechnologies; the related problem of supply uncertainties stemming fromreliance on imported raw materials, components and other needs as well asdelays due to customs administration (all of which result in costlyinventories); the lack of suppliers, precision services, ii-id otherindustrial and service "infrastructure" of adequate technologicalcapability and re'liability; limited and unreliable communications services;and Government regulation and controls. In addition, Indian electronicsfirms face shortages and interruptions of power, communications, and inputsupply (which contribute to costly inventories), and labor regulations thatlead to inflexibility and encourage overstaffing.

2.08 Although the subsector is generally inefficient by worldstandards, a few firms in India now produce competitively with domesticprices that, if adjusted for indirect taxes and international profit norms,would approach world prices. These firms are typically found in productareas (such as B&W TVs) characterized by relatively simple and maturetechnologies that have been fully assimilated, and by domestic marketslarge enough to allow economies of scale. In addition, product areas thatrequire a significant level of skilled labor such as PCBs, individualelectronics products with a high design content, and above all, computersoftware, perform well. In most product areas, however, even the mostefficient firms are uneconomic, exhibiting one or more of the followingcharacteristics: production is highly capital Intensive; technology isdifficult and has not been mastered because of inadequate technologytransfer arrangements; the market is too small to allow adequate scale, orelse the technology appropriate for the size of the market is obsolete; and

high protection allows "kit assembly" from foreign sole-source sipplierswith resultant very high raw material costs.

C. Potential and Prospects foX Development

2.09 India has the potential to develop a competitive electronicsindustry. Its main advantageo are its unusually large pool of high levelscientific and technical manpower whose average wages are a tenth those ofthe U.S. and Western Europe- its growing and potentially vast domesticmarkets; and the significant industrial base -- including a long-standingelectronics industry -- that has already developed with its pool of capableand experienced managers and entrepreneurs. Also, a large number of non-resident Indians with technical and managerial experience are a source ofentrepreneurship and of assistance in developing collaborative arrangementswith foreign sources of technology and finance.

2.10 These advantages need qualification, however. Skilled manpowerlacks training and exper'.ence -- constraints which this project will helpto address (paras. 4.07-4.13). Markets are not as large as India's vastpopulation would suggest because low incomes coupled with high pricesexclude much of India's population from them; in absolute size they arecomparable to Turkey or the Philippines. The industrial base and itsmanagement evolved under a highly protected environment that until recentlytended to stifle competition, allowed survival (indeed, prevented exit),despite outmoded or obsolete technical practices and limited scales ofoperations, and fostered inefficient managerial practices. As discussedbelow (paras. 2.17-2.23), there have been major improvements in this policyframework.

2.11 The Bank prepared a study of this sector,J/ submitted to theGovernment in July, 1987, which indicates that overall demand forelectronics equipment is expected to expand In real terms at 18-20% overthe medium term. Exports will grow even faster but will remain at lessthan 10% of total production. The study identified a number of productgroups which are already competitive or can become so. The most promisingexhibit many of the following characteristics: high need for engineeringand skilled manpower in design, production, sales and installation, andservicing; a domestic market large enough to allow production at sufficientscale; the technology required for production can be assimilated,effectively used, and kept up to date given the present levels oftechnology and supporting infrastructure in India; relatively low intensityin use of capital and materials; high transport costs relative to productvalue; and local availability of critical inputs and experience atreasonable costs.

2.12 The most promising product groups for the domestic industry, whichwill be the primary focus of the industry's development in the next decade,are in the professional electronics segments of industrial electronics,computers and data processing including software, and te3ecommunicationsequipment. These segments include many product groups with prospects of

1/ India - Development of the Electronics Industryl A Sector ReRort, No.6781-IN, (June 26, 1987), (Project File, No. 1).

-6-

becoming competitive (e.g. in instruments, process controls, EPABXs)because they are skill intensive, have relatively low capital and rawmaterials needs and do not require high volumes and large scales.Attempting products which are technically very difficult, such as state-of-the-art mainframe computers and integrated circuit testers, may be verycostly because their technologies are closely held, fast changing andrequire a hlgh level of R&r to assimilate as well as strong supportingtechnical and industrial service infrastructure.

2.13 Computer software, though still a tiny industry (estimated valueof production in 1987 was about US$160 million), is particularly promisingbecause of its high degree of skill intensity. Exports reached US$57million in 1987 and are estimated to have grown to US$70 million in 1988.Though the industry is dominated by two firms, which account for about 60%of total exports, there are dozens of smaller firms whose potentialcontribution to both domestic production and exports is constrained by lackof access to marketing expertise, software productivity tools and hardwareneeded for software development, and risk capital to finance costs ofproduct development and marketing. A technical assistance component of theproject addresses these issues (paras. 4.15-4.16). There is a moregeneralized constraint from lack of specially trained manpower as discussedbelow (paras. 2.27-2.28) which the project will also address (paras.4.07-4.13).

2.14 With regard to consumer electronics, domestic demand can supportproduction at reasonable scale of some major *onsumer items (radios, black-and-white and color TVs) as well as major inputs for these products such ascolor picture tubes and glass shells that are used in color picture tubes.Export of some consumer items to other developing countries has begun andcan be expanded to many consumer products, such as black and white TV,which are at the lower end of the technology scale and whose production isbeing relinquished by producers in more developed countries where thedemand has stagnated or declined.

2.15 In the critical area of integrated circuit production,particularly at very high levels of technical difficulty such as VLSIchips, Indian producers face much the same difficulties as for "high tech"professional electronics products: closely held, fast-changingtechnologies, and a requirement for a high level of R&D capability which inturn requires the availability of high-tech supporting services, andincreasingly costly investment due to rising scales and capitalintensiveness. India has been trying to develop a microelectronicscapability, particularly for large scale integrated circuits throughSemiconductor Complex, Ltd. (SCL), the DOE-administered wafer fabricationplant in Chandigarh that was completely destroyed by fire in February,1989. Though in production for more than four years and capable ofexporting simpler ICs such as clock chips, it had not begun to achievecompetitive efficiency. The Government is now assessing how best toreplace this loss.

D. Policy Environment

2.16 Past Policy Framework. The very high prices and variable qualityof electronic products have largely been the result of the industrial and

-7-

trade policies followed until recently. These policies, which were anintegral part of the industrial policy framework that emerged in the latesixties and early seventies, emphasized self-sufficiency, indigenoustechnological development with minimal recourse to foreign technology,reservation of key products to the public sector, concessions to small-scale producers and pressure for the regional dispersion of production.These policies in electronics, resulted in a capability to produce a largenumber of products in each of the electronics segments. However, theyimposed major constraints on the development of an efficient electronicssubsector:

- The industrial licensing system severely regulated entry andrestrained growth of the most efficient producers. Larger firms,especially those subject to the Monopolicies and Restrictive TradePractices Act (MRTP) and Foreign Exchange Restrictions Act (FERA)were inhibited from expanding. Some 24 product areas includingsome that needed scale for efficiency (especially in consumerelectronics and components) were reserved to SSIs. Exit ofinefficient firms was discouraged by a combination of laborregulations, restrictions on asset transfer and bank lendingpractices. These policies and procedures, together with thoselimiting total domestic production capacity to the perceived sizeof the market, restrained domestic competition in importantproduct areas.

- The reservation of some segments to the public sector(telecommunications and defense) eliminated private-sectorcompetition and allowed inefficient monopolies to develop;

- The emphasis on technological self-sufficiency led to backwardnessin processes and products. The policy climate did not encourageforeign collaborations and many joint ventures involved technologysufficient to enter production but not to update thereafter.Restrictions on royalty payments and other limitations did notprovide sufficient incentives to encourage foreign firms to enterintc joint ventures especially those firms with proprietarytechnology in the more sophisticated areas;

- The trade and protection policies, which resulted in extremelyhigh levels of effective protection (d&te to high tariffs and thebanning of competing imports), prevented alternative sources ofpotential competition from developing and discouraged exports,which could have exposed the industry to international trends andcompetition;

- The high level of indirect taxes contributed to higher productioncosts, and the complicated structure of these taxes hampered thedevelopment of exports because it was difficult to identify theindirect taxes to be rebated or otherwise offset; and

- By encouraging geographic dispersal, the Government policieshindered concentration of the industry, which was vital todeveloping a strong supporting infrastructure.

-8-

2.17 Recent Pollcy Reforms. The Government has recognized theimportance of electronics--not only for its direct contribution toindustrial output and employment but also as a source of productivitylmprovements in manufacturing and other sectors--and has singled out thissubsector for policy changes to achieve efficient growth. A series ofmajor policy changes dealing with different electronics segments commencedwith the Policy on Electronics Components in 1981, and led up to theIntegrated Policy Measures in Elee.tronics (March, 1985), which consolidatedprevious pronouncements and made additional fiscal and licensing reforms.A major reform in computer software followed with adoption in December,1986, of the Policy on Computer Software Export, Software Development andTraining. Incremental improvements have continued to be made since then.Electronics has also benefitted from the series of discrete policy actionsinitiated since 1985 applylng to all industries which cumulatively havesignificantly improved the policy environment for all industries. Thesereforms have been complemented by some liberalization of the financialsector, especially in capital markets (paras. 2.31-2.33).

2.18 Of the policy reforms affecting electronics, most important forelectronics has been the gradual liberalization of the regulatory system tolift restrictions on entry and enterprise growth. Components and consumerelectronics have been specifically delicensed, which has meant that theycould undertake new investments without having to go through complex andtime consuming Government procedures to obtain an investment license.Other electronics segments benefit from the recent increase in the generallicensing minima from Rs. 50 million (US$3.3 million) to Rs. 150 million(US$10 million). For industrial projects generally, delicensing wasextended to units importing up to 30% of input needs, up from 15% in thepast. In areas still subject to licensing, more flexibility has been glvento adjust both output mix and capacity. Licensing procedures have beensimplified. DOE introduced "single point" scrutlny of project applicationsin computers and industrial products in 1984, and computer software in1986. Access to imported capital goods for electronics has been assured byplacement of much of the specialized equipment used by electronics firms onopen general license (OGL), which has meant these items can be im.portedwithout prior clearance from the Government. Reservation of productsreserved for small scale industry, which included many types of components,has been virtually eliminated.

2.19 The product areas open for investment to electronics firms subjectto the MRTP Act (which subjects them to different types of anti-monopolyregulation) has expanded from components to include all segments exceptconsumer electronics. Electronics has benefited from the general increasein the threshold level for a firm to be classified as monopolistic. 2./Telecommunications equipment formerly the exclusive preserve of the publicsector, was opened in 1984 to the private and joint sector for manufactureof equipment at subscribers premises (i.e. telephone handsets, EPABXs) andin 1988 was broadened further to include some of the remainder, includingrural exchange and transmission equipment (for public sector firms withState Government ownership greater than 50%).

2/ The level of a firms total assets at which it is considered to be amonopollstic for the purpose of Indlan regulatory laws was lncreased ln1985 from Rs. 200 million (US$13.3 million) to Rs.l billion (US$66.7million).

-9-

2.20 Domestic deregulation has had a major impact in increasingdomestic competition in electronics as evident from the ex-factory pricedrops in some of the major products. Color TV set prices have fallen by60% since 1984 when large scale production began. Microcomputers priceshave dropped by nearly 50% in just the last two years. Intelecommunications equipment the large public sector firms have improvedmarginally and partly due to competition from newly established privatesector firms. Pressure on domestic profits as a result of competition hasalso helped to increase the incentive to export (see para. 2.22). Inparallel with deregulation has come improved access to foreign technology,critical to electronics which now accounts for 20% of foreigncollaborations. Restrictions have been lifted entirely on foreignownership if equity is less than 40%, and greatly reduced on the types oftechnology firms are U.llowed to import. These measures have dramaticallyincreased foreign co'laborations, which reached 173 in 1985 and grew to 260in 1987 compared with an average of 10-15 a year in the mid-1970s. Foreigncollaborations have become more attracti -t ioreign partners because ofthe 1987 increase of the royalty ceiling From 5% to 8%.

2.21 In the area of trade policies, quantitative restrictions (QRs)have been greatly reduced for components, which are now mostly on OGL toactual users and have been eliminated entirely in the case of software.The July, 1988, action to allow all industrial items on "limitedpermissible" to be purchased under Import Replenishment (REP) license hasessentially eliminated this category as a quantitative restriction to userswilling to pay the additional premium, currently around 20%, which accruesto REP license sales. The import duty structure has been largelyrationalized, with raw materials generally at 45%, processed parts at 60%,components and peripherals at 80% and final products ranging from 90% to150,.

2.22 The incentive to export has recently grown as a result of threefactors: overcapacity in a number of products, especially in passivecomponents (carbon film resistors, for example) following deregulation;improvement of export policies and administration which began in 1986; i/and the adoption of a more flexible and realistic exchange rate policyleading to a real effective exchange rate that has depreciated more than30% since the end of 1985. In response exports of electronics productsfrom the domestic tariff area (i.e. excluding free zones), which hadstagnated by 1984 have more than tripled in value since then, growing from2.7% of total production in 1984 to 3.9% in 1987. With regard to the taxsystem, GOI has reduced and simplified corporate taxes; implemented amodified value added tax (MODVAT) that eliminates the cascading effect ofindirect central government taxes for most products and facilitatesindirect tax deduction for exports, and rationalization of tax incentivesfor small scale industries.

2/ A detailed review of recent changes in export policies andadministration are given in India: Export Development Proiect StaffAnoraisal Report. Report No. 7603-IN, paras. 2.09-2.19.

-10-

2.23 As a result of the pioneering improvements in electronics policyframework which began in 1981 and the more recent general policyimprovements that date mostly from 1985 onwards, production and investmenthave greatly increased, especially from the private and joint sectors.Electronics production, which had grown in real terms at nearly 13% between1975-80 increased to more than 18% from 1980-85, and to 25% from 1985-1987.Electronics investment, as measured by the commitments of the two majorall-India financial institutions, the Industrial Development Bank of India(IDBI) and the Industrial Credit and Investment Corporation of India(ICICI), which provide about 80% of project term financing for medium andlarge firms in this segment, had increased in the period 1983-85 to morethan six times the level of a 1977-79, and in 1986/87 to more than doublethe rate of 1983-85. Noreover, the composition of electronics financinghas changed: private and joint sector investment, which was less than halfthe total commitments of these institutions in 1977-79 is now more than80%.

E. Policy Constraints

2.24 The policy improvements to date are encouraging a more efficientindustry that has promise in many areas of becoming internationallycompetitive. Despite the improvements discussed above, however, additionalreforms will be needed to ensure that cost competitiveness and quality ofIndian electronics products will approach international standards. TheJune, 1987, Electronics Sector Report (Project File, No. 1) provided anagenda for further change to achieve these objectives. The recommendationsincluded: progressively eliminating quantitative restriction on importsand at the same time gradually reducing customs duties to compel dormesticfirms to upgrade their products, improve efficiency and lower price:3 tomeet world price and quality standards; simplifying and eventuallyeliminating domestic content requirements under phased manufacturingprograms (PNPs); eliminating the remaining disincentives that restrictaccess to foreign technology leaving firms free to choose technologiesappropriate for production and market conditions, with minimum Governmentinvolvement; extending capacity delicensing to industrial electronics,computers and telecommunications; and removing remaining HRTP clearancerequirements for product groups where scale is needed for efficiency.

2.25 The study also emphasized the need for an easement of industrialexit restrictions to complement the measures taken to improve entry. Whilerecognizing that the changes for this purpose are needed in banking, laborregulations, and bankruptcy procedures that go well beyond the electronicsindustry the study suggested that the electronics industry might beselected for priority treatment. The study underlined the importance inthe longer run of extending MODVAT to a more comprehensive value-added taxsystem; the need to persuade the states to harmonize state level taxes withthe VAT system and to eliminate discrimination between local and out-of-state production which have become an important source of distortion thatis fragmenting capacity in this industry. The study also pointed out theneed to lift or reduce restrictions on location to allow economies ofagglomeration to be realized.

-11-

2.26 Though this is a large agenda for change, there has been steady.though incremental progress in implementing it, even since the SectorReport was issued. It has taken the form both of broad industrial measuresthat affect electronics, and specific measures concerning only electronics.These include: reiucing further the licensing restrictions on MRTP firms;raising the threshold on the imported materials percentage that subjects afirm to licensing; extending delicensing to microcomputers, peripherals,and monitors; rationalization of the tariff structure for computers andcomputer peripherals; reduction of the indigenization objectives of thephased manufacturing program for all industries from 90% to 708; andelimination of QRs on a broad range of products for firms willing to pay anadditional premium. As a result of the sector study and projectpreparation, dialogue has been established with DOE and other Governmentagencies on policies for this sector that is contributing to the changethat is taking place. A Bank loan to support this industry's furtherdevelopment is well justified on the basis of improvements made before andduring the project preparation period. The project will provide a contextfor a continuing dialogue with DOE and other Government agencies on anumber of fronts as the results of project financed technical assistanceand studies are discussed. These concern the key areas of software andmanpower development as well as a range of specific issues (paras.4.19-4.20) involving import tariff levels, indigenization, standardization,dissemination of information technology, etc.

F. Manpower Constraints

2.27 Skill requirements for electronics are far higher than forindustry as a whole. Nearly 30% of the electronics work force possesstechnical degrees at bachelor level or higher; in the case of computersoftware, about 90% of the work force are engineers. The most importantbasis for Indian competitiveness is the potential availability of higherlevel skilled, technically trained manpower at low cost. Indianelectronics experts have proved their competence abroad, and in India theircosts are less than most other developing countries with significantelectronics industries. However, except for a few top-level institutionssuch as the five Indian Institutes of Technology and the Indian Instituteof Science, which export about 30% of their graduates, and the DOE managedCenter for Electronics Design and Technology (CEDT), Bangalore, the qualityof training that is being provided for middle and higher levelprofessionals is seriously deficient in practical application, iwith theresult that extensive training, often of a year or more, must be providedby individual firms before higher level technical staff can be usedproductively. The lack of quality of instruction is rooted in a number ofdifferent factors: theoretical bias of curricula, shortage of teacherswith practical experience, lack of opportunity to receive industryexperience during the formal training period, lack of funds for well-equipped laboratories and workshops, and the lack of linkage with existingindustry.

2.28 In the computer software industry, where India's potentialcompetitive advantage may be greatest, the industry faces an absoluteshortage of staff as well as an upgrading problem which is clearly evidentfrom discussions with firms in the industry. DOE estimates that the

-12-

programmers. systems analysts, computer engineers, and similar types ofspecialties needed by the end of the Seventh Flve year plan period willhave reached more than 33,000 compared with an output from formal traininginstitutions during that period estimated at little more than 9,000. TheGovernment's software export policy (para. 2.17) recognizes thisconstraint and has recommended not only an expansion of public educationalinstitutions and establishment of three new CEDTs, but also new incentivesto upgrade the private-sector training and educational institutions. Theproject includes a component to support the Government's objective ofimproving the quality of the output of middle and higher level manpower,focused primarily on upgrading the electronics and computer scienceprograms at a carefully selected group of engineering colleges (theprincipal source of higher level technical engineering manpower) andpolytechnic institutes (the main source of middle-level technicians such asprogrammers, factory technicians, and repairmen). See paras 4.06-4.12.

G. The Financial Sector _/

2.29 Historically, India has followed relatively conservative monetaryand financial policies. The main objectives have been to mobilize domesticsavings on a large scale, contain inflationary pressures and achieve apattern of investment conforming to the Government's economic and socialpriorities. These oLjectives have been pursued through several mechanisms.First, interest rates have been administered through the Reserve Bank andthe interest rates paid on commercial bank deposits and other savingsinstruments as well as the lending rates have been kept positive in realterms. Second, the commercial banking system's scope for credit creationhas been tightly circumscribed. Third, a system of quite rigid creditallocation guidelines has been used to direct funds to earmarked industriesand social sectors. Within this policy framework, the financial system hasgrown rapidly over several decades and the nation's traditionally highsavings rates have been accompanied by significant financial deepening.Savings rates have risen steadily from about 168 of GDP in the late sixtiesto an average of 23% since 1980. However, this success on the resourcemobilization side contrasts with the more mixed results in resourceallocation both in terms of their impact on economic efficiency and thefinancial condition of lending .,.nstitutions. The evidence suggests that inconjunction with restrictive industr4al policies, the credit allocation andinterest rate policies encouraged inefficient patterns of investment inindustry.

2.30 As of December 1986, commercial bank credits of Rs 49 billion wereofficially classified as being extended to "sick industries" which havenegative net worth. Outstanding credit to sick industries alone are about15.7% of commercial banks' credit to industry and 8.1% of their totaloutstanding credit. The situation in the DFIs is similar; in 1985 IDBI'soutstanding loans to sick industries were about 11% of its portfolio. Inaddition to the sick industry problem, the collection ratios on other

A/ World Bank, India: Credit and Capital Markets Study, ReportNo. 6661-IN (February 27, 1987), provides a comprehensive analysis ofthe Indian financial sector.

-13-

industrial and agricultural lending have been decreasing. The problems arebeing further exacerbated by increased competition faced by many industriesresulting from the ongoing industrial liberalization. Together withdeteriorating portfolio quality, the operating spreads of financialinstitutions have narrowed as recent interest rate adjustments haveresulted in lower average lending rates and higher funding costs. Thusthere is a need to rationalize the system of financial sector controls andimprove the institutions' operational flexibility and profitability. Inrecognition of these problems the Government has since 1985 set up severalcommittees to study the various financial markets and recommend ways ofimproving the working of the financial sector and their reports areproviding a basis for an ongoing process of reform. 5/

2.31 In the last few years, the Government has encouraged thedevelopment of new and more appropriate funding instruments and markets tofinance industry; thus, it has encouraged a shift away from bank loans tomore capital market funding of both private and public sector industrialfirms. First, restrictions on the purposes for which companies could issuesecurities were progressively relaxed to allow flotation of debentures tofund new companies, mergers/acquisitions and working capital. Second, thequantitative limit for issues exempt from capital issues controls wasdoubled to Rs 10 million and listing requirements were eased. Third,smaller firms were given improved access to the non-convertible debenturemarket by the raising of the interest rate ceiling on their issues to 15%from 13.58. Fourth, in an effort to encourage public sector firms to raisefunds on the capital markets, these firms were given the freedom toundertake public debenture issues even though their shares may not belisted.

2.32 Measures to diversify the markets and improve the attractivenessof issues by start-up firms have included the introduction of newinstruments such as Cumulative Convertible Preference Shares (CCPS). Thesesecurities count as equity, carry a 10% dividend and are convertible intostraight equity after three to five years. Also liquidity hasincreased--particularly in the debt markets--with the major public sectorinvestment institutions playing an important role in maintaining secondarymarkets. Finally, the Government has introduced legislation to protectinvestors and boost confidence in the markets, and new institutions such asa stock holding corporation have been set up to simplify the purchase ofsecurities. The introduction of further capital market reforms is expectedsoon.

2.33 In response to the various changes in regulations and fiscalincentives the capital markets have grown rapidly in the 1980s, andparticularly since 1985. The equity market took off in 1980/81 when theamount issued rose 242% to Rs 2 billion as a result of FERA legislationwhich indigenized ownership of foreign firms. Since then the primary

1/ These are the Chakravarty Committee to Review the Working of theMonetary System (1986); the Patel Committee on the Operations of theStock Exchange (198_; the Vaghul Working Group on the Money Mark-cs(1987) and the Hussain Committee on the Carital Markets (1988).

-14-

market has grown fat. The volume of equity issued (including rights andpreference shares) quintupled to Rs 8.8 billion in 1986 from Rs 1.77billion in 1982. The debenture market also grew significantly over thesme period when the amount isaued more than doubled to Rs 5.9 billion fromRu 2.4 blllon. In general, the relaxation of guidelines controllingdebenture issues brought down financing costs to companies, especially thecost of working capital, in comparison to bank loans. At the same time theyields to investors on these securities were higher than those paid oncomparable bank deposits. These capital market developments haveencouraged financiai. institutions to expand their activities to leasing,mutual funds, credit cards and other higher income earning activlties tocompensate for the declining marglns on their basic lending activities.

2.34 Th Baking Syste. The Indian financial system is highlysegmented with different roles clearly earmarked for the variousinstitutions. The Reserve Bank of India (RBI) has a wide-reaching role int!,e system. In addition to traditional central banking functlons, it hasbroad regulatory and policy implementatlon functions. The financial systemis overwhelmingly in the public sector. There are currently about 30private sector Indian banks and about 20 foreign banks which togethercomprise the private banking system. However, these banks are dwarfed bythe huge public sector ones, both in terms of size and geographic spread.The private sector banks and foreign banks account for only about 4.3% and4.5% respectively of total commercial bank assets. The remaining 91.2% isaccounted for by 28 public sector commercial banks.

2.35 In spite of the increased role of the capital markets, thefinancial sector is still dominated by the banking system. Commercialbanks have the lead role in resource mobilization and together with theDevelopment Banks, they are the biggest source of funding for industrialinvestments. As of June 1987, the Scheduled Commercial Banks §/ had totaldeposits of over Rs 1 trillion.

2.36 The Commercial Banks' scope for creating credit is strictlylimited by reserve and liquidity ratio requirements which currently channelabout 51% deposits into compulsory investments in the securities ofGovernment and public sector institutions at below-market rates.Furthermore they have limited discretion over the direction of theirlending as RBI credit allocation guidelines account for about 77% of totaldeposits.

2.37 Under this system, the commereial banks are a major source offunds for the public sector through their purchases of securities issued bythe central and state governments, public sector companies and all-Indiafinancial institutions, which satisfy Statutory Liquidity Ratio (SLR)requirements set by RBI. The strict control of bank operations has hadsome unintended effects. Apart from promoting inefficient resourceallocation and fostering rigidities, the system has had a negative impacton commercial banks' profitability, because the net interest income they

fJl There are currently 50 Scheduled Commercial Banks and they account forabout 95% of gross bank credit.

-15-

receive Is only slightly more than their administrative costs. In fact thecommercial banks' profits are therefore largely derived from unfunded itemssuch as fee income on international trade, foreign exchange commissions andgains on portfolio trading activities. The comercial banks have beengiven greater flexibility as a result of reforms announced in October andNovember 1988. These reforms have: (a) removed the Interest rate ceilingon working capital loans; (b) given customers the freedom to change banks;and (c) effectively removed the restrictions previously imposed on the sizelimit of working capital and term loans the commercial banks are able toprovide. As a result 04 the new freedom to set interest rates, the bankshave been able to lower the interest cost to the most credit worthycustomers to 16', while slightly increasing the rates charged relativelyweaker credits.

2.38 As a consequence of the Chakravarty Committee recommendations, RBIhas been adjusting the interest rate structure by increasing the interestrates paid on public sector bonds held by commercial banks as SLRrequirements bring public sector borrowing rates closer to market rates.While this rationalization does not appreciably affect the profitability ofthe comercial banks, it significantly increases the costs of thedevelopment banks which raise resources through selling their bonds to thecommercial banks. Given this, and for other reasons, it would beappropriate to extend the same flexibility to set rupee lending rates,which has been given to the commercial banks, to the development banks.

2.39 The Indian developmen1t finance system comprises national andstate level development banks and investment institutions. At the nationallevel the predominant development banks are Industrial Development Bank ofIndia (IDBI), The Industrial Credit and Investment Corporation of IndiaLimited (ICICI) and Industrial Finance Corporation of India. In additionthe Export-Import Bank of India (Eximbank), was set up in 1982 to provideworking capital and term finance for exports, having taken over thosefunctions from IDBI; the Industrial Reconstruction Bank of Indiaestablished in 1984 has replaced the Industrial Reconstruction Corporationof India with responsibility for rehabilitating sick units. The nationalor All-India investment institutions are Life Insurance Corporation ofIndia (LIC), Unit Trust of India and General Insurance Corporation ofIndia. At the state level, funding is provided by the State IndisstrialDevelopment Corporations and State Financial Corporations. Thesedevelopment finance institutions (DFIs) are the major source of termlending to industrial firms, and the vast majority of their lending is toprivate sector firms. As at March 1987, these institutions 2/ haddisbursed about Rs 290 billion, 75% of which was to the private sector.Annual sanctions and disbursements were Rs 81 billion and Rs 56 billion,respectively, up from Rs 66 billion and Rs 49 billion in the previous year.

2.40 The three main all-India DFIs (IDBI, ICICI and IFCI) accounted for75% of total disbursements by the development finance institutions in1986/87. They follow a consortium approach to project financing in whichthe institutions periodically meet in order to co-ordinate matters of

Z/ Eximbank data not included.

-16-

policy, business, procedures, processing applications, appraisal andfollow-up of projects. One institution is assigned responsibility AS "leadinstitution" for project financing. The lead institution appraises theproject, discusses wit,, other participating institutions, arranges forconsortium financing (which is governed by pre-agreed rules concerningsize), provides assistance on behalf of all participating institutionsagainst single documentation, supervises the end-use of assistance, andmaintains follow-up as long as loan balances are outstanding. This systemlimits competition between the DF-s but greatly facilitates projectadministration.

2.41 The industrial term lending institutions have, in recent years,been faced with an increasingly riskier lending and investment environment.The state-level institutions have been weakened over time by poorcollection performances. The direct lending portfolios of all developmentbanks, state level and all-India, have come under increasing pressure astheir borrowing costs have risen along with the rise in administereddeposit and public bond rates. Their financial conditions havedeteriorated as their clierts have had to adjust to a less regulated andmore competitive environment, and steady depreciation of the exchange rate.At the all-India level these adverse developments have been partiallyoffset by the leasing business and other higher-yielding activitiesundertaken by these institutions and more recently improvements incollection rates so that so far, their profitability has been maintained.

2.42 Exchange Risk Administration Scheme (ERAS). The DFIs previouslyon-lent their foreign currency borrowings, on a back-to-back basis, with amark-up of 1.5% to cover costs of administration and risks, with theinterest rate and foreign exchange risks borne by the sub-borrowers. Giventhe steady depreciation of the rupee and volatility of foreign exchangerates in the last few years, sub-borrowers have borne extremely high, andoften highly unpredictable, effective repayment rates. The absence of awell developed foreign exchange currency market in India has meant thatprivate sector borrowers have limited means to protect themselves againstsuch risks. As a consequence, these firms' debt-servicing capacities havebeen impaired, which in turn has negatively affected the foreign currencyloan portfolios of the lending institutions. By 1987, the demand forforeign currency loans had fallen dramatically; foreign currency sanctionsby ICICI fell an estimated 34% in that year.

2.43 The Government, in conjunction with the major DFIs (IDBI, ICICI,and IFCI), has responded to the situation with the development of anExchange Risk Administration Scheme (ERAS) which commenced April 1, 1989,under the management of IDBI. Under ERAS, the DFIs will move to a currencypooling system for their foreign commercial borrowings. Sub-borrowerswill pay a rupee-denominated rate made up of: (a) the weighted averageinterest cost of the DFIs foreign borrowings; (b) a premium in respect ofthe estimated foreign exchange risk; and (c) the DFI's intermediationspread of 2.0%. The scheme has commenced with an initial rate of 15%, 1Iabove the present term lending rate of the DFIs. The rate will be reviewedevery six months and adjusted as necessary to cover the foreign andinterest rate costs, based on international interest rate and currency

-17-

movements, subject to an lnitial cap of 18%. Thus, each sub-borrower wouldhave a floating rate sub-loan, subject to the cap. The actual ERAS rateaffecting loans already made, and tne initial rate on new loans and theceiling rate for new loans will be adjusted quarterly. ERAS will beoptional and sub-borrowers will have the right to borrow in a givencurrency and assume the attendant foreign exchange risks. The Governmenthas agreed that the rate will be adjusted as necessary to cover the foreignexchange and interest rate risks. It has also agreed that if due to largefluctuations the fund runs into a deficit in the short run, the Governmentwill make advances into the fund and be repaid when the fund is in surplus.

2.44 Financing Electronics Firms. The sharp division in the presentfinancial system between the provision of working capital financing, whichis the responsibility of the commercial banks, and project financing, whichincludes fixed assets but only 25% of permanent working capital, frequentlyleads to delays and occasionally to liquidity crises because the commercialbanks us8e quite different, more conservative and sometimes less flexiblefinancing norms. For electronics firm these problems tend to be moresevere because of their financing characteristics. First, electronicsfirms in India on average require almost 50% more gross working capital forthe same level of fixed assets as manufacturing firms as a whole(reflecting dependence on imported materials, and low fixed capitalintensiveness) and are therefore more likely to be hurt by delays orshortages in working capital finance. Second, imported raw materials areroughly twice as important an element of working capital as all of industry(reflecting that many components and most raw materials cannot economicallybe produced locally) which requires access to a higher level of foreignexchange to finance working capital that is often more difficult to obtainthan local currency. Finally, electronics firms have been much fastergrowLig because of rapidly expanding domeetic markets; thus commercial bankcredit limits tend to be quickly outgrown. Electronics firms juststarting up, that comprise more than 85% of the value of investmentfinanced by the DFIs, are hit especially hard as they often face teethingproblems in start up due to the need to assimilate new technologies andadjust to the unce'tainties of fast-changing markets.

2.45 The project proposes to address these financing difficulties bylodging the responsibility for ensuring adequate financing for both fixedassets and permanent working capital for clients of this project with theDFIs until a project is operating at capacity (see para. 4.04). Thisreduction in financial institution specialization, approved by RBI on apilot basis for this project, could have a liberalizing impact on theindustrial finance structure as a whole, if RBI thereafter introduces thechange more widely.

-18-

III. THE BANK'S ROLE IN INDUSTRY

A. Previous Bank Lending to Industry

3.01 The Bank has made 19 developw-nt finance loans amounting to US$1.4billion through financial intermediaries, (mainly ICICI and IDBI), foronlending to private and joint sector firms engaged in all aspects ofindustry. Fourteen operations concerned ICICI alone. Three (Credit356-IN, and Loans 1511-IN and 1260-IN) were channelled through IDBI toState Financial Corporations (SFCs) and State Industrial DevelopmentCorporations (SIDCs) for relending (Loan 2928-IN the Industrial Finance andRestrt'cturing Project) approved in 1988, uses both intermediaries. TheBank'= experience with IDBI and ICICI in implementing past projects hasbeen discussed in recent Project Completion Reports (PCRs) and theconclusions have been taken into account in project preparation.

3.02 The first development finance project in India specifically topromote exports, Industrial Export (Engineering Products) Project, (LoansNo. 2629-2930-IN), for US$250 million approved in September 1985, wasdesigned to support the growth of exports of engineering products throughprovision of term finance through ICICI (US$160 million) and partieipatingcommercial banks (US$90 million) and the creation of productivity andmarketing funds for exporters. As of January 31, 1989, about 72% of theloan to ICICI had been sanctioned. The slow performance has been dueprimarily to the reluctance of sub-borrowers to bear the currency poolforeign exchange risk at relatively high interest rates. The fact thatexports of engineering exports have expanded much less rapidly thanprojected at appraisal is also contributing to rlow disbursements. InFebruary 1988, the project was modified to allow GOI to bear the foreignexchange risk for a fee and relending these funds in local currency. As aresult of this modification, the remaining funds are expected to becommitted by ICICI ly August, 1989.

3.03 The most recent DFI project under implementation, the IndustrialFinance and Technical Assistance Project (Loan 2928-IN), which becameeffective in August, 1988, provides US$310 million in financial andtechnical assistance support to IDBI (US$205 million) and ICICI (US$105million) to help them meet their requirements for long term foreignexchange resources and to strengthen their capacity to appraise projectseffectively in a less regulated environment, cope with the more difficultportfolio management problems stemming from the adjustment process, andmobilize resources through new financial instruments in more competitivefinancial markets. The project also provided US$50 million to the majorGovernment steel company, SAIL, for technical assistance to upgradetechnology and improve efficiency. The project is proceeding smoothly.

3.04 The Bank Group has also provided US$3.2 billion for projects inthe fertilizer, cement, and petrochemicals subsectors where opportunitiesexisted for the Bank to support policy reforms at the subsectoral level andto finance economic investment. Implementation of these projects has been

-19-

generally satisfactory with all projects currently under implementatione.pected to have satisfactory rates of economic return and, despite someinitial delays, to be fully disbursed by the respective closing dates.

B. The Bank's Future Jending Strategy

3.05 The Bank has had an active industrial sector work program andprepared a number of sector reports on such subjects as industrialregulation, tetbhology policy, export promotion, public enterprisemanagement and credit and capital markets .nd a number of subsector reportsincluding electronics, automotive products, steel, capital goods andfertilizer. The 1987 CEM, IMnia: An Induatrializing conomy in Tr iti /also focused on the development of the industrial sector and supplied thebroad outlines of a reform program. Many of the issues in these reportswill continue to be discussed with the Government in the context of futureoperations.

3.06 The future lending program for industry is primarily based on thesector work and will thus include:

(i) industrial finance projects which will serve as a focal point forevaluating and discussing with Government overall progress onindustrial and financial policy reform as well as addressing issuesin the financial institutions;

(ii) export, technology and industrial energy conservation projectswhich will serve as a focal point for evaluating and discussingwith Government overall progress and improve the policy, financialand institutional support for activities in these key areas; and

(iii) subsector projects which will provide policy, technical andfinancial support for economic investments in areas where improvedefficiency will have implications for the growth of the wholeindustrial sector (e.g., petrochemicals, electronics, cement andcapital goods).

3.07 In all of these areas, loans are basically linked to the policyreforms that are being undertaken either in designated policy areas such asexports, technology, etc. or in the policies that affect a specificsubsector. The basic criterion that determines the decision to go aheadwith a loan is whether the policy environment is conducive to efficientinvestments in the area or subsector that is being supported. Thus, thelending strategy involves supporting investments in areas where policyimprovements have already been undertaken, consistent with the conclusionsof the previous sector work.

1/ Report No. 6633-IN (March 13, 1987).

-20-

C. Electronics in Bank's Lending

3.08 Electronics has been included among the subsector projects in theBank's industrial program for India because it has already reachedsignificant size, has good potential for rapid growth and efficiency andwill have significant impact on other sectors throughout the economy. Forthese reasons, the Government has given electronics high priority in theSeventh Five Year plan and in the Eighth Five Year plan now underpreparation. It has shown a willingness to make major policy changes,greater than for almost all other industrial sectors, to foster theindustry's sound development with the objective of eventually reaching alevel of internationally competitive production.

3.09 The project will complement two other contemporary projects whichdeal with related issues. The Industrial Technology Development project (aFY90 project whose appraisal mission returned early April, 1989) addressestechnology issues that will impact upon electronics in the areas of riskfinancing and R&D infrastructure. The Export Development Project which wasapproved by the Board on May 12, 1989 2/ includes financing of technicalassistance in promising export areas, including software development forexports.

2/ See Staff Appraisal Report No. 7603-IN, April 20, 1989.

-21-

IV. THE PROPOSED PROJECT

A. Project Objectives

4.01 A major goal of the Government's program of policy reform is tofoster an industry that will become internationally competitive. Thisproject is intended to initiate a long term relationship with India tosupport this goal and the specific objectives set for the project reflectthis. The project would: (a) provide technical and financial support toassist the two largest DFIs improve their capability to identify, appraiseand finance sound projects as well as to improve performance of existingfirms in this sub-sector; (b) assist in upgrading the training of mediumand high level technical and professional manpower needed for the rapid andefficient growth of the industry; (c) help to lay the basis for long termcontinued improvement in the policy environment for electronics; and (d)help to shape India's strategy, and prepare projects to support, softwaredevelopment.

B. Project Descrigtion

4.02 The project would comprise:

(i) A credit component for investment in electronics industryexnansion and ugnrading of about US$420 million under a new"single window" approach providing both fixed investment andpermanent working capital which will allow each firm to deal withonly one financial institution to ensure adequate total projectfinancing;

(ii) Skilled manMower development and training of US$26.8 million forprovision of equipment, training, and related assistance throughDOE as grants to selected engineering colleges, polytechnicinstitutes and Centers for Electronics Design and Technology(CEDTs) to upgrade preparatory training of electronics andsoftware engineers and technicians, and for industry training toupgrade engineers already employed; and,

(iii) Technical assistance of US$3.0 million for (a) a study, semina:csand project identification for the development of the computersoftware industry including software exports; (b) a program ofseminars and studies to expose Government and industry leaders toworldwide developments in electronics and help to establish astronger factual basis for addressing future policy and investmentissues; and (c) training and consultancy assistance to the DFIs toupgrade project preparation and implementation capalbility in thisindustry.

-22-

C. Term Credit to Expand and U12rade Electronics Capacity

4.03 Under this component, the Bank will finance US$202 million inlines of credit to cover estimated foreign exchange costs of both fixedassets and permanent working capital to viable projects in electronics andrelated areas involving estimated total investment of $420 million in boththe private and joint sectors for medium and large scale projects. It willuse two major financial institutions as intermediaries, IDBI and ICICI,which provide 70%-80% of the term financing to projects of this size inthis sub-sector.

Single Window Credit Line

4.04 To ameliorate the problems for electronics projects under thepresent system of divided responsibility for financing term loans forprojects and working capital (para. 2.44), sub-projects financed under thisproject would be provided with both fixed asset financing which is about70% of the total, and the incremental permanent working capitalrequirehents which constitutes the remaining 30%, through a singlefinancial institution, up to the time that a firm reaches full capacityproduction. This approach would eliminate the inconvenience of dealingwith several financing agencies. It would also reduce the risk that afirm's working capital needs are not taken care of because of differingapproaches in assessing and monitoring those needs. Because firms wouldreceive term loans for permanent working capital, however, receivableswould be excluded because they can be conveniently handled separately bycommercial banks under the present system of overdraft facilities and billsdiscounting. Exclusion of receivables is in line with RBI's long termpolicy that eventually they should be financed only by way of billdiscounting. The DFIs have agreed, that they would use the subsidiary loanfrom GOI to finance working capital (see para 6.02) only when part of aBank financed investment project for fixed investment. The "single window"approach to project financing, though commonplace elsewhere in the worldbecause of the trend away from Government mandated specialization, is newfor India. RBI l is confirmed to the DFIs its willingness to permit itsintroduction to India on a pilot basis, restricted to the electronicssector under this project. RBI would consider broadening its application toother industrial sectors after the experience from this project can beevaluated in terms of the benefit of improved project financing against thecosts in terms of loss of control in meeting other objectives.

4.05 A credit line of the size proposed can be committed within threeyears. The '-otal demand for electronics investment in projects presentedto the DFIs ..ached US$233 million equivalent in 1986 climbed to aboutUS$250 million in 1987 and reached US$290 million during 1988. Thecombined foreign exchange requirements for those three years reached US$340million. Investment has kept pace with, if not exceeded, increases inproduction which is expected to grow steadily at 18% - 20% over the nextfour to five years. The DFIs have completed an analysis of projects likelyto be submitted over the next three to four years and have identified some40 possible projects involving investment of about Rs.10.4 billion (US$691million) with a foreign exchange requirement for fixed assets alone of

-23-

Rs.464 million (US$309 million). These estimates appear reasonable. Underpresent projections, the Bank loan would finance 46% of the estimatedforeign exchange requirements for investment and working capital ofelectronics sub-projects over the next three years.

D. Manoower Development and Training

4.06 Though middle and high level skilled technical manpower isgenerally available in India, skilled technical and engineering manpowerwith specific, relevant, practical training in electronics, computers,programming, systems engineering and related skills is a serious constraintto expansion in the potentially most competitive segments, especiallycomputer software (para 2.28). To help alleviate this constraint thiscomponent would aim: (a) to improve the quality of pre-service training ofmiddle level skilled manpower (technicians) and higher level skilledmanpower (engineers) in electronics and computer software; (b) to improvethe quality of engineers and technicians already employed; and (c) tostrengthen the links between pre-service training centers and industry.

4.07 To achieve these objectives this component would have thefollowing main elements:

(a) Improvement of electronics and computer software training programsat a selected group of 14 engineering colleges (ECs), which arethe principal source of high level technical manpower for thisindustry, a selected group of 12 polytechnic institutes (PI) whichprovide mid-level technical manpower such as rupair andmaintenance technicians, and programmers, six Centers forElectronics Technology and Design (CETD). This element would (i)develop up-to-date learning materials in areas such as productdesign, computer science and software development, etc. where suchmaterials are lacking; (ii) introduce hands-on product design anddevelopment exercises and training; (iii) modernize teachingfacilities and equipment; and (iv) provide practical training forteachers that have no industry experience. Base costs are US$18.0million.

(b) Upgrading of practicing engineers and technicians through (i) theconduct of state-of-the-art seminars for middle and higher leveltechnical employees of small and medium scale firms and (ii)support of continuing engineering education programs. Deliveryinstitutions for this element would be the Indian Institutes ofTechnology (IIT) at Bombay and Delhi and the Indian Institute ofScience, Bangalore. A fourth institute satisfactory to the Bankwill be selected later. It is also expected that the specialexpertise in training technicians of the Nettur Electronics Center(NEC) in Bangalore will be utilized. Base costs are US$2.0million.

(c) Strengthening of links between industry and the ECs through (i) aprogram of industrial attachment for students; and (ii) theprovision of part-time teachers from industry. Base costs areUS$1.7 million.

-24-

4.08 This is a pilot project dealing with a relatively small number ofinstitutions. In the case of the strengthening of pro-service training(para. 4.07 (a)), which is the largest single element, a smail group ofqualified institutions were identified by Bank consultants from amongapproximately 300 ECs and 600 PIs on the basis of crlteria which emphasizeclose proximity to clusters of computer and other electronics firms, thecapacity of the institution to implement the project and the strength oflinks between the institute and industry. All ECs are associated withautonomous universities; the PIs are state government institutesadministered by State Ministries of Education. The institutions that DOEhas identified to participate in the project, limited to 32 (14 ECs, 12 PIsand 6 CEDTs) have been reviewed and are satisfactory. Agreement wasreached that the institutions finally selected must be satisfactory to theBank.