Embed Size (px)

Citation preview

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No. 6405-MAG

STAFF APPRAISAL REPORT

MADAGASCAR

ENERGY I PROJECT

March 31, 1987

Eastern and Southern Africa Projects DepartmentEnergy Division

This dument has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

Currency Unit - Malagasy Franc (FMG)US$1.0 = FKG 750

(as of July 1, 1986)

WEIGHTS AND MEASURES

1 kilometer (km) 3 0.621 miles1 square kilometer (km2) - 0.386 square miles1 kilovolt (kV) 1,000 volts1 megawatt (MW) - 1,000 kilowatts1 megavolt ampere (MVA) - 1,000 kilovolt amperes1 gigawatt hour (GWh) 1 million kilowatt hours1 ton of oil equivalent (toe) - 10)500,000 kilocalories

bbl = barrel MJ - megajoulecm = centimeter Hm 3 million cubic metersGW - gigawatt m3 - cubic meterhs = hectare MWh - megawatt hour-ie = kilotonnes of oil equiv. od - oven dry:, kWh - kilowatt, kilowatt hour sv = solid volume

LPG 3 liquified petroleum gas t - tonneN = million TCF - trillion cubic feetmcwb = moisture content tpa, tpy - tonnes per annum, per year

wet basis twe = tonnes of wood equivalent

GLOSSARY OF ABBREVIATIONS

BADEA Banque Arabe de Dgveloppement Economique en AfriqueBNI Banque Nationale pour l'IndustrieCCCE Caisse Centrale de Cooperation EconomiqueCIDA Canadian International Development AgencyCIMA Kalagasy Cement ManufacturerDEE Department of Electricity and WaterDEF Department of Fishery and ForestryDGP Planning DirectorateEEK Electricitg et Eau de MadagascarESMAP Energy Sector Management Assistance ProgramFAC Fonds d'Assistance a la CooperationFANALAMANGA Malagasy Industrial Wood Plantation AuthorityFAO Food and Agriculture OrganizationFED Fonds Europeen de DdveloppementGOM Government of MadagascarICS Interconnected System serving Antananarivo RegionJIRAMA Malagasy Electricity and Water CorporationMIEM Ministry of Industry, Energy and MinesMPAEF Ministry of Animal Production, Fisheries and ForestsMPARA Ministry of Agricultural Production and Agrarian ReformOMNIS Military Office for National and Strategic IndustriesPIU, PMU Project Implementation Unit, Project Management UnitPSIP Public Sector Investment ProgramRIP Reference Power Sectot Investment ProgramSEM Soci6tf d'Energie de MadagascarSOLIMA Malagasy Petroleum Refinery CompanySOMAGI Government-owned Data Processing CompanyUNDP United Nations Development ProgramUSAID United States Agency for International DevelopmentZE Major Power Production Zones Outside of ICSZI Small Isolated Power Systems

GOVERNMENT OF MADAGASCAR FISCAL YEAR = CALENDAR YEAR

IVOR OML6 S NYMADAGASCAR

ENERGY I PROJECT

Credit and Project Summary

Borrower: Government of Madagascar

Amount: SDR 19.8 million (US$25 million equivalent)

Beneficiaries: The Malagasy Electricity and Water Corporation (JIRAMA);the Ministries of Industry, Energy and Mines, ofAgricultural Production and Agrarian Reform, and of AnimalProduction, Fisheries and Forests; public enterprisesinvolved in the boiler program; local private charcoalers;and the Industrial Wood Plantation Authority(FANALAMANGA).

Terms: Standard. 1/

Project The project would help the Government strengthen energyObjectives: policy formulation, planning and investment programming,

and institutional development. It would assist theGovernment and JIRAMA in improving the efficiency ofresource utilization in the power subsector bystrengthening financial management, planning and manpowerdevelopment. and by rehabilitating existing deterioratedsubsector infrastructure, improving financial andoperational performance of JIRAMA, and stimulatingcommercial utilization of low cost hydropower resources.It would help the Government develop least-cost plans toexpand the supply of electric power and household energyproducts and by correcting distortions in their prices.Finally, it aims to encourage increased and moreeffectively coordinated flow of resources from donors tothe power and household energy subsectors.

Project The project comprises the implementation of the highestDescription: priority projects, comprised mostly of rehabilitation

works, included in JIRAMA's investment program for theperit,d 1987-1992, technical assistance for power systemplanning and investment programming, and assistance in theestablishment of modern methods and tools for utilityfinancial management and administration. The projectcomprises technical assistance for strengthening energyplanning and management in MIEM, and for major policy andplanning studies on biomass fuels supply and marketing andresource assessment, and household energy demand. Theproject would support initiatives to improve householdcooking efficiency, to develop production of charcoal frompine plantation thinnings and residues; and to test pilot

1/ Onlending terms are 8% Interest rate, repayment periods of 10 to 20years after grace period of 2 to 5 years.

Thi documnt b a estited distdbution and may be used by reipints only in the perfonmceof te officil dutbs Its contonts may not otherwi be diclosed without Wodd Bank authodutlon.

- il -

production of rice husk briquettes. Finally, the projectincludes installation of electrical boilers which woulduse surplus power in the Interconnected System (ICS).

Project Risks: Risks are minimal as the project concentrates onrehabilitating existing generation, transmission anddistribution systems. Also, JIRAMA has a sound record forsafe engineering practice. Benefits arising from theproposed electric boiler program may be reduced due todelays in implementation or reduced demand. The risk thatJIRAMA may be overwhelmed administratively by the volumeof required rehabilitation works is to be minimized by theappointment of consultants to assist with the design,prioritization and implementation of the rehabilitatinprogram. Foreseen improvements In the financial viabilityof JIRAMA may be jeopardized by delay In tariff adjustmentalthought this risk is to be minimized by linking theachievement of financial performance criteria to therelease of the first and second phases of investment.

Madagascar Public Power Stations and Transmission Lines,October 1986, IBRD 18816R

MADAGASCAR

ENERGY I PROJECT

STAFF APPRAISAL REPORT

Table of Contents

Page No.

I. THE ENERGY SECTOR IoOOOoOOOOOooooOOOooOeOOOOOOOOeOOooOOOOOooOoo 1Introcjction 00I00000006009000000000090000000090000000000000000 1Bank Particepation in the Sector .............................. 2Reasons for IDA's Involvement in the Energy Sector ............. 4Energy Resources 4.....0.0.00...........*ooooooooooooooooooo 4Hydropower .. ooooo.ooooooo.ooo.oooooooooooo.oooo 000000000 4Petroleum ............................... 4Coal, Lignite and Peat ................... 5........... 5

Biomass 5FoergDests .d.o...000000*000000*00000000000000000000000000000000 5

Energy Balances and Trends .............0.00.0o.0...0.0..o. 5Energy Supply oooo. .o .ooo.000 **.**0.000..0*.00** 6Electric Power ee6oooooo*oooooo*oooooooooo.oo*00000o000o 6Petroleum and Petroleum Products *7**ooo*#o*** ooooooooo 7Biomass Fuels B000000000****o*****o**oooooo.eo*oooo 8

II. THE POWER SUBSECTOR *000000000 ooooo00ooo0o0oo0oooOooooo000o*o 8Organization 0000000000000*00 eee**.e**0*0**00..*4.0oo0o00 8Sector Fatilities *000000000000-00000000000000000--00000 9Access to Service 10Pattern cf Electricity Consumption 10Power Subsector Planning 11Power Subsector Objectives 12Power Subsector Strategy *oo.ooooooo*o......................... 12Aid Inflow and Coordination in the Sector 12

ITI. THE BORROWER AND THE IMYLEMENTING AGENCIES ...... 13JIRAMA 0 00 13Organization and Management 13Planning 14Engineering and Design ..... 14Operations and Maintenance 14Data Processing 15Billing and Collection 15Accounting and Audit 15

This report is a result of a mission which visited Madagascar betweenJune 2 and June 19, 1986. The mission leader was Ken Newcombe (SeniorEnergy Specialist) and included Juergen Franz (Senior Financial Analyst),C. H. A. Killoran (Power Engineer, Consultant), W. Pacheco (Power Engineer,Consultant), and J. R. Mercier (Energy Planner, Consultant).

Insurance and Taxes ...................................... 15Personnel and Personnel Management 16Training 16Management Information System (MIS) 16Performance Indicators 17

IV. THE MARKET 17Electricity Market 17Historical Market ...... ..oe ........................ 17Demand Forecast for Electricity in the Main ICS 17Generation and Capacity Balances in the Interconnected Systeu 18Demand Forecast for Electricity in the External Zone 19Demand Forecast for Electricity in the Isolated Zone 19

Household Fuels Market , 19Cooking Fuel Supply and Demand: Antananarivo #.............. 20Household Fuels Marketing ....... .20

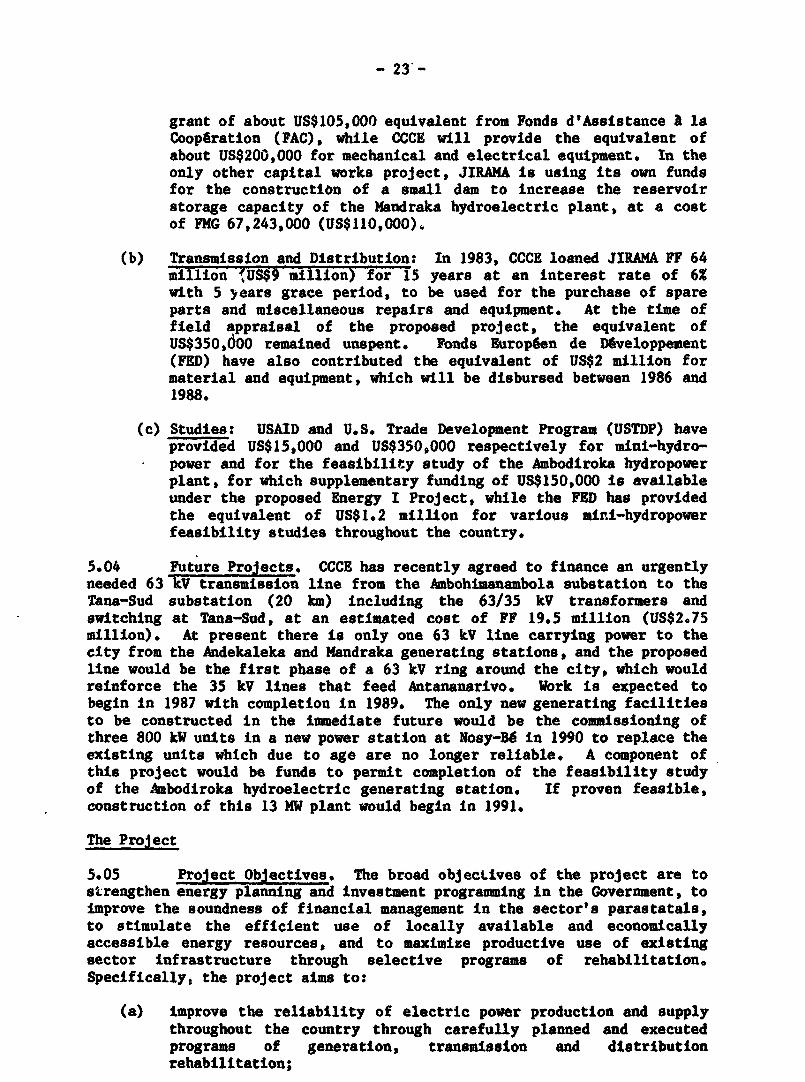

V. INVESTMENT PROGRAM AND PROJECT 21Power Subsector Investment Program (PSIP) s.................... 21The Program ...................u. 22Works in Progress 22Future Projects 23.......... * 00 23

The Project 23Project Objectives 23Project Preparation 24Project Description 25Power Components 25Energy Components 25Electric Boilers ................... o. 26

Project Costs ... o........ ** 26Project Implementation 27Implementation of Power Components 27Implementation of Energy Components 28Implementation of Boiler Program ............................ 29

Consulting Services .ee*. * . 000.0.......... 30Procurement ................ 30Advance Contracting and Retroactive Financing ...... 32Financing Plan 32Disbursement 33Special Account,; 33Environmental Aspects ....................... 00 34Project Risks 34

VI. FINANCIAL ANALYSIS .... 3 5 ........... 35Introduction 35Financial Position and Past Operating xesults of JIRAMA 35Tariff Structure and Policy ...... 36Financial Restructuring of JIRAMA 38Future Financial Position and Operations of JIRAMA 40Project Phasing and Financial Covenants 41

VII. ECONOMIC JUSTIFICATION 42A. Power Subsector Economic Analysis 42

Average Incremental Cost Analysis 42

Return on Power Subsector Investment .......................... 42Economic Analysis of Volobg Hydropower Plant Rehabilitation ... 43Electric Boller Prograu ....................................... 43Economic Analysto of Antananarivo-Anstirabe Transmission Line . 44Economic Viability of New Household Power Supply Connections .. 44Economic Viability of Rehabilitation Programs ................. 44

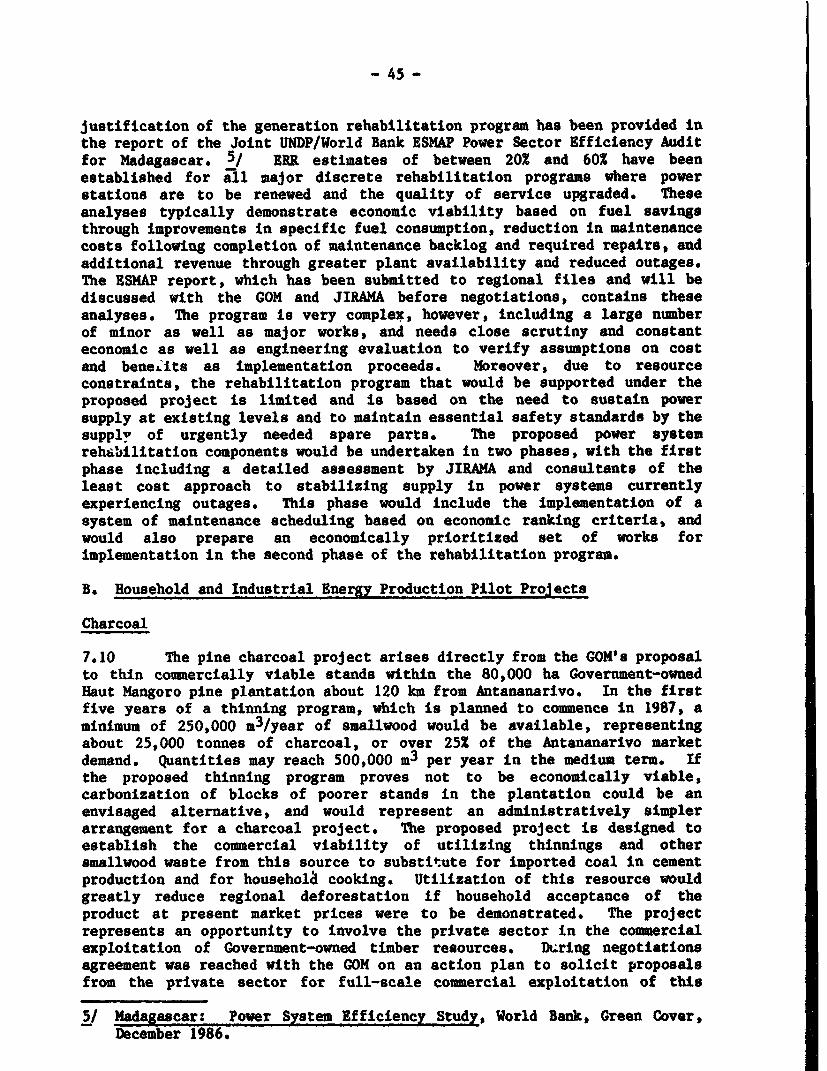

B. Housebold and Industrial Energy Production Pilot Projects ..... 45Charcoal ....................... 45Rice Husk Briquettes .... ...................................... 46

VIII. AGREEMENTS TO BE REACHED AND RECONMENDATIONS .................. 46Agreements ....................... 46Conditions for Effectiveness .................................. 48Conditions of Disbursement ............ *00e***O**.............. 48Recommendation .... O.......OO@C OCOCOC.. 49

LIST OF ANNEXES

1.1 National Energy Balance, 19831.2 Energy Sector Information Flow sad Decision Making Process and

Administration of Household Energy Planning Program

2.1 Installed Generation Capacity

3.1 Organization and Functions of the PMU, Project ManagementOrganization, and JIRAMA Organization Chart

3.2 Selected Performance Indicators

4.1 Methodology and Assumptions for Load Forecasts4.2 JIRAMA ICS Sales and Generation, Actual and Projected FYSO-954.3 JIRAMA ICS Peak Demand, Actual and Projected FY80-954.4 JIRAMA ICS Energy and Capacity Balances FY86-954.5 Isolated External Zone Centers Sales Forecast4.6 Projected Supply-Demand Balance for Household Energy, Antananarivo

Faritany4.7 Description of the Charcoal "Filiare"; Present and Possible Fhiture

Situation

5.1 Reference Power Subsector Investment Plan Sumary, 1987-19915.2 Project Description5.3 Project Cost Summary5.4 Summary of Implementation Schedule5.5 Electric Boiler Project - General Contract Terms & Conditions5.6 Financing Plan5.7 Estimated Scbedule of Disbursements

6.1 JIRAMA Reform Measures6.2 JIRAMA Income Statements 1983-19926.3 JIRAMA Balance Sheets 1983-19926.4 JIRAMA Sources and Uses of Funds 1984-19926.5 Assumptions Used for Financial Analvsis6.6 Phase II Investments

7.1 Economic Cost of Electricity and Economic Rate of Return on PowerSubsector Investment Program

7.2 %conomic Analysis of VolobG Hydropower Generating Plant7.3 Economic Analysis of the Antananarivo Region Electric Boiler Program7.4 Economic Analysis of Antananarivo-Antsirabe Transmission Line7.5 Comparative Economic and Financial Cost of Rice Rusk Briquettes,

Madagascar, 1986

8.1 Documents entered Into the Project File

MAP: Madagascar Public Power Stations and Transmission Lines, October1986, IBRD 18816R

MADAGASCAR

ENERGY I PROJECT

STAFF APPRAISAL REPORT

I. THE ENERGY SECTOR

Irtroduction

1.01 Madagascar is the fourth largest island in the world with a landarea of 597,000 km2. Its estimated 1986 population Is 10.1 million.Despite a favorable resource endowment, Madagascar's economic performancehas been disappointing and its present estimated GDP per capita is onlyabout US$240/capita, 1/ whiech is 252 below that of the early 19708 andstill declining. The lialagasy economy remains predominantly agriculturalwith 81% of the population being rural and agriculture contributing aboutone third of GDP. Economic recovery is predicated on more efficient use )fresources in the face of severe foreign exchange constraints, rehabilite-tion of infrastructure and productive capacity and resumption and growth inagricultural exports.

1.02 Total gross energy consumption was about 2 million toe, or 214kgoe per capita in 1983 of which 82X was fuelwood used very largely forhousehold cooking (Annex 1.1), whereas final energy use was 1.65 milliontoe. Energy demand is forecaet to reach 2.44 million toe by 1995, a growthof 3.3% per annum, though woodfuels used in the household sector will stillexceed three-quarters of final energy consumption. 2/

1.03 Madagascar's main commercial energy resources are hydropower,petroleum and coal. Hydropower is estimated at 7 GW, coal at one billiontonnes and heavy oil at 5-20 billion barrels; however, the economicallyrecoverable quantities are not known as physical and technical accessi-bility is generally difficult. Other forms of petroleum, lignite, and-despite regional shortages-forests and woody biomass are all available insignificant quantities though commercial access is presently limited.Uranium and geothermal steam are also known to occur.

1.04 The Ministry of Industry, Energy and Mines (MIEM) has the mandateto formulate energy policy and to undertake energy planning and investmentprogramming, although the (ffice Militaire pour les Industries Nationaleset trategiques (OMNIS) has played an important role in this sphere untilrecently. The other major energy agencies are JIRAMA and SOLIMA, thenational power and petroleum supply and refining companies, respectively.Both of these companies report through the Direction de l'Energie et del'Eau (DEE) of MIEN, to the Minister of Industry, Energy and Mines.Increasingly, other Government agencies are being drawn into energy supplyactivities, especially for woody biomass fuels. These include the

1/ Preliminary revised Atlas figure.2/ Madauascar: Issues and Options in the Energy Sector, World Bank (July

1986), Report No. 5700-MAG.

- 2 -

Departement des Eaux et ForOts (DEF) of the Ministere de Production desAnimaux, Eaux et Forgts (MPAEF), the parastatal timber producer,FANALAMANGA, linked to MPAEF, in respect to woodfuels, especially charcoal,and the MinistAre de Production Agricole et Revolutioin Agraire (MPARA) withrespect to agricultural residue fuels. A schamatic representation of thenew arrangements for energy administration of the Government and for theenergy planning administration itself, is pre3ented in Annex 1.2. Thesearrangements were agreed with IDA during project preparation and are beingimplemented.

1.05 Interaction for the purposes of energy policy formulatlon,planning, and investment programming between government agencies, even forthose under the umbrella of MIEM, has not been strong. There is nocoherent national energy policy, though in certain contexts, such asGovernment sponsored conferences on the nation's energy resources, nationalgoals and objectives have been enunciated. In the course of IDA's ongoingdialogue with the GOM ill the energy sector, and with the benefit of therecent joint UNDP/World Bank Energy Sector Assessment and preparation forthe proposed Credit, the GOM has confirmed the central role andresponsibility of MIEM for energy policy and planning. Thus IDA wouldprovide technical assistance and other means of support to MIEM to elevatethe status and effectiveness of energy planning and to broaden the horizonsof energy strategy formulation to include the household energy subsector:specifically, supply and demand management aspects of energy used forhousehold cooking, lighting and other household end-uses. The size ofIDA's proposed support for the energy administration and household energyplanning has been adapted to the absorptive capacity of the Government.

1.06 Public sector investment programming is the responsibility of theDirection G6n6rale du Plan (DGP), which has limited skilled staff andresources, and no staff assigned to, or well informed with respect to$ theenergy sector. Currently, DGP compiles the energy sector components of thePublic Sector Investment Plan (PSIP) directly from the plans and programsof the various agencies active in energy production and supply. However,there is no explicit energy sector investment program prepared as part ofthe PSIP. Instead, woodfuel production, power supply, petroleumexploration, and petroleum refining and distribution are treated indisaggregated fashion with no attempt to prioritiz% within the sectorconsistent with least-cost among competing solutions to serve particularenergy demands. Thus sound technical, economic and financial analysis andjudgment of sector priorities is lacking and there is an ongoing risk ofinefficient resource utilization in the sector. Under the proposed credit,IDA would seek to alleviate this problem by strengthening energy planningand investment programming both within MIEM and JIRAMA, as well asencouraging coordination between all other energy-related agencies towardseffective energy planning and project implementation.

Bank Participation in the Sector

1.07 The Bank Group has provided funds for three energy sectoroperations and two forestry projects which have subsequently createdimportant energy supply options. The first energy sector project was forthe power subsector through assistance with financing the AndekalekaHydropower Project with a credit of US$43 million (Credit 817-MAG, May

1978). This credit closed on September 15, 1986. The project included theconstruction of a dam and power plant with two 29 MW generating units,engineering services, technical assistance, and training. The projectachieved its objective of exploiting an Important hydropower resource toeconomically displace thermal power in the main interconnected power supplyzone (ICS). In the process JITAMA staff increased their competence inmajor project design and implementation. The project achieved theestablishment of a planning unit, the provision of computer facilities andimproved management practices and organization. However, plarningmethodologies, investment programming, and the successful adaptation ofcomputer technology for consumer billing and accounts and for planning andengineering design are still needed. Lessons learned from the projectinclude the need for improved demand forecasting techniques and marketanalysis to reduce the risk of premature investment. Failure to predictmore accurately future power demand at the time of designing the Andekalekaproject has led to large surpluses of hydroelectricity in the ICS (para.4.03). Similarly, a stronger and ongoing dialogue is required duringproject supervision between JIRAMA, the Government and IDA in order tostrengthen planning and management capability. Under the seeend energysector project, the Petroleum Exploration Promotion Credit of 1980 (Credit1016-MAG), the GOM established the legal and fiscal framework for explora-tion and promotion and assembled the required data. Since 1981 fourcontracts have been signed with major oil companies and more than US$90million has been spent on drilling activity. The third energy sectorproject, the Tsimorora Heavy Oil Exploration Project of 1982 (Credit1298-MAG) has further defined the Tvimorora resource, and though notproving up recoverable resources, showed possible extension of thereservoir, thereby justifying further seismic analyses lu 1985, and shallowdrilling in 1986. In the forestry sector, two operations have contributedto energy sector development by generating large quantities of charcoalfeedstock in the form of thinnings and smallwood. These are the first andsecond Mangoro Forestry projects (Loan 1065-MAG and Credit 525-MAG, 1974-1981 and Credit 1661-MAG, 1982) which helped the Government to complete theestablishment of about 80,00U ha of pine plantations at Haut Mangoro.

1.08 Under the Joint UNDP/World Bank Energy Assessment Program and atthe request of the Government of Madagascar, the Bank conducted in 1984 anenergy sector assessment of Madagascar. The final report (No. 5700-MAG) ofthe mission was published in January 1987 after detailed review by theGovernment, and concludes that the sector issues which roquire the mosturgent action are: (i) the increasing shortage and rapidly growing r.: 1prices of woodfuels for household cooking and the deforestation andenvironmental deterioration related partly to woodfuel scavenging; (ii)the urgent need for rehabilitation of distribution, transmission andgeneration systems in the power sector; (iii) the gross under-utilizationof hydropower available from the Andekaleka hydroelectric generatingstation in the Interconnected Zone; (iv) the general weakness of energypolicy, planning and investment programming in Government, exacerbated bythe lack of a single effective focus for energy planning and poor coordina-tion between agencies active in the ener,v sector; (v) the future form ofpetroleum products supply and the viability of and options for refineryrehabilitation and operations; (vi) the inadequate definition in physicaland economic terms of the major resources with energy potential, includingin particular hydropower and woody biomass.

-4-

Reasons for IDA's Involvement in the Energy Sectort

1.09 IDA's goals in Madagascar are to assist the Government with theformulation and implementation of policies and programs which will improvethe efficiency of the public sector and stimulate private sector productionof goods and services. leading to increased resource mobilization, andincreased production and exports of agricultural produce and manufacturedgoods where Madagascar has a comparative advantage. In supporting theenergy sector, IDA is seeking the formulation of comprehensive energypolicies leading to rational energy prices, import substitution, economicuse of indigenous energy resources, energy efficiency improvements andenhancement of the role of the private sector in energy management anddevelopment. Consistent with these objectives, IDA sought and reachedagreement with the Government on the strengthening of energ sectorinstitutions through the development of a single effective energy planningagency, and the preparation of least cost production and supply plans formajor subsectors of the energy economy. Another important objective is theimprovement of reliability of supply and efficiency in the power sectorthrough rehabilitation of deteriorated generation, transmission, anddistribution facilities, and the financial rehabilitation of sectorparastatals (especially JIRAMA), leading to uniformly high technicalstandards of service and financial autonomy.

Energy Resources

1.10 Hydropower. The hydropower resources of Madagascar aresubstantial but poorly defined and frequently economically inaccessible topotential demand centers. Stream gauging and hydrological analysis hasbeen only intermittent in the major catchment zones. JIRAMA estimates thatthere are 339 known sites with a firm power potential of 7,055 MW capableof an annual production of about 60,000 GWh. Thirty-three sites withestimated power outputs tabove 50 MW account Eor 6,330 MW, or 90% of theknown total. There are 72 sites identified in the 1-5 MW range, and atleast 200 sites below 1 MW. Only 105 MW, corresponding to 1.6% of knownpotential, has been developed. The greatest barrier to efficientdevelopment of the hydropower resource is the lack of precise informationon the potential to economically displace existing diesel generation withmini or micro-hydropower installations, the lack of a comprehensive leastcost development plan, and the poor coordination between potential donoragencies. The proposed project will strengthen hydropower resourceassessment and development planning (see para. 5.07(e)).

1.11 Petroleum. Two sedimentary basins, Morondava in the west andMahajunga in the north, are potential sources of oil and gas. Their totalland-area is 170,000 ki2, with a further 80,000 km2 offshore at depths upto 200 m. The deep water area between 200-2,000 m covers a further 50,000km2, offering prospects for oil and gas in the 'onger term. Most explora-tion has been in in the Morondava basin where evidence of tar sand andheavy oil have been found. Following the 1979 increase in oil prices, theGovernment, with IDA assistance, was able to attract major oil companies toinvest heavily in oil exploration. The four major oil companies nowactive-Mobil, AGIP, Amoco and Occidental-will have spent more than US$100million by mid-1988. There are also tar sand and heavy oil deposits inwestern Madagascar. The Bemolanga tar sands are estimated to contain 5-20

billion barrels of oil equivalent. However, studies financed by IDAindicate that their exploitation is not presently economic. The heavy oildeposits at Tsimorora are also being reviewed with IDA assistance in orderto establish their potential foe commercial exploitation, though onceagain, market conditions do not suggest early production from thisresource.

1.12 Coal, Lignite and Peat. The area of greatest interest for coal isthe Sakao basin with estimated reserves of 1,000 million tonnes andmineable reserves wltt. moderate ash, medium volatile steam coal estimatedat 173 million tonnes, of which 82 million tonnes are recoverable byunderground methods, and 23 million tonnes by open pit methods. Theprincipal lignite resources occur in the Anteirabe region of the centralhighlands. Recent estimates indicate proven reserves of 11 million tonnesand possible reserves of 32 million tonnes. Lignite is not of sufficientquality to justify mining hence there appears to be no foreseeable economicfuture for the resource. On the other hand, peat occurrences are commonand it is used widely for brick making. Peat resources have not beeninvestigated though there is potential for significant discoveries.

1.13 Forests. The contiguous natural forest cover is estimated at12.3 million ha. Plantations add a further 265,000 ha. On the assumptionthat only 20X of the natural forest is economically accessible underenvironmentally sound management practices, the estimated sustained annualyield is about 2 million toe, compared with a gross annual consumption ofabout 1.7 million toe. Unfortunately, there are regional imbalances whichrender meaningless the apparent surplus of 0.3 million toe. In fact,demand for woodfuels is concentrated in the central highlands, in thehinterland of Antananarivo, Antsirabe and Fianarantsoa, where there is asbortfall between accessible sustainable production and regional demand ofabout 0.6 million toe (1.9 million tonnes of wood) per annum. Productionsurplus to demand in other regions cannot be economically transported tothe central highlands demand centers.

1.14 Other Biomass Resources. Madagascar's main agricultural crop isrice which generates annually cellulosic residues of about 4.6 milliontonnes. Some 500,000 tonnes of these residues are rice husks which arelargely disposed of as wastes, except in the Lac Aloatra region where abouthalf are used for fueling boilers to provide shaft power for rice milling.The remainder there and in the immediate hinterland of major cities couldbe briquetted for household fuel production, and used as a substitute forfirewood and the low quality charcoal presently marketed. Sugar cropresidues are another potentially economic source of industrial andhousehold fuel, or for the production of electricity surplus to sugar millneeds for regional sale in public distribution systems. Bagasse and canefield residues offer long term potential for power and energy production ofabout 90,000 toe annually. Other crop residues are judged not to beeconomically accessible in the foreseeable future.

Energy Demand

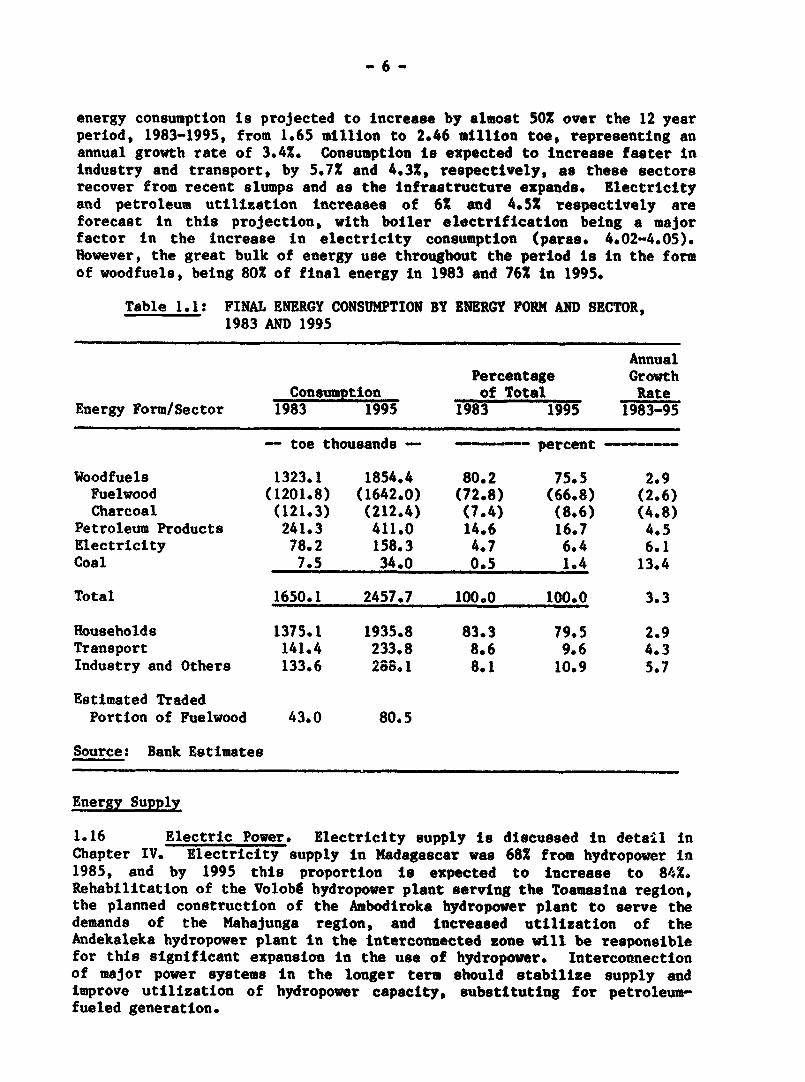

1.15 Energy Balances and Trends. A national energy balance forMadagascar for 1983 is provided in Annex l.1. Table 1.1 provides a summaryof this Annex with projections of demand for all fuels through 1995. Total

- 6 -

energy consumption is projected to increase by almost 50% over the 12 yearperiod, 1983-1995, from 1.65 million to 2.46 milllon toe, representing anannual growth rate of 3.4%. Consumptlon is expected to Increase faster inindustry and transport, by 5.7% and 4.3%, respectively, as these sectorsrecover from recent slumps and as the infrastructure expands. Electricityand petroleum utilization increases of 6X and 4.52 respectively areforecast in this projection, with boiler electrification being a majorfactor in the increase in electricity consumption (paras. 4.02-4.05).However, the great bulk of energy use throughout the period is In the formof woodfuels, being 80% of final energy in 1983 and 76% in 1995.

Table 1.1: FINAL ENERGY CONSUMPTION BY ENERGY FORM AND SECTOR,1983 AND 1995

AnnualPercentage Growth

Consumption of Total RateEnergy Form/Sector 1983 1995 1983 1995 1983-95

- toe thousands - - percent

Woodfuels 1323.1 1854.4 80.2 75.5 2.9Fuelwood (1201.8) (1642.0) (72.8) (66.8) (2.6)Charcoal (121.3) (212.4) (7.4) (8.6) (4.8)

Petroleum Products 241.3 411.0 14.6 16.7 4.5Electricity 78.2 158.3 4.7 6.4 6.1Coal 7.5 34.0 0.5 1.4 13.4

Total 1650.1 2457.7 100.0 100.0 3.3

Households 1375.1 1935.8 83.3 79.5 2.9Transport 141.4 233.8 8.6 9.6 4.3Industry and Others 133.6 2 8.1 8.1 10.9 5.7

Estimated TradedPortion of Fuelwood 43.0 80.5

Source: Bank Estimates

Energy Supply

1.16 Electric Power. Electricity supply is discussed in detail inChapter IV. Electricity supply in Madagascar was 68% from hydropower in1985, and by 1995 this proportion is expected to increase to 84%.Rehabilitation of the Volob6 hydropower plant serving the Toamasina region,the planned construction of the Ambodiroka hydropower plant to serve thedemands of the Mahajunga region, and increased utilization of theAndekaleka hydropower plant in the interconnected zone will be responsiblefor this significant expansion in the use of hydropower. Interconnectionof major power systems in the longer term should stabilize supply andImprove utilization of hydropower capacity, substituting for petroleum-fueled generation.

- 7 -.

1.17 Petroleum and Petroleum Products. Madagascar is entirelydependent on imports for Its petroleum supply, both crude and refinedproducts. Net petroleum Imports were 31% of total merchandise imports in1983 and absorbed 52% of non-energy export revenues, 3/ up from 13% and15% respectively in 1978, in spite of a decline in petroleum ilport volumesduring this period. In 1983 crude oil cost US$82.7 million and refinedproducts cost US$63 million. Preliminary indications for 1985 imports areUS$15 million for crude and US$41 million for refined products: asubstantial reduction due both to reductions in the price of refined andcrude products and to reductions in absolute volumes imported and stockreductions. Madagascar obtains its crude oil through a Government-to-Government arrangement with the Soviet Union and precise details of thisarrangement remain confidential. It is believed that the indicative pricewas about US$22/bbl in mid 1986, considerably above world market prices,but credit and foreign exchange requirements are softened by virtue ofspecial payment terms and conditions. Refined product needed to supplementrefinery production in meeting Madagascar's demand is procured on the openmarket at CIF prices more than 25% above those available if foreignexchange were not a constraint. At present, SOLIMA, the State-ownedpetroleum parastatal, is forced to buy late and short, because it does nothave a sufficient credit rating to permit it to engage major suppliers incompetitive bidding, based on optimal procurement and transport packages.The proposed project includes a study to review the options to minimize thecost of petroleum products, including procurement of crude and products.

1.18 Imported crude is refined at the port of Toamasina, at theGovernment owned refinery operated by SOLIMA, the company formed by theGovernment in 1976 to take over petroleum supply, refining, distributionand marketing from local affiliates of a number of major foreign oilcompanies. The refinery has a capacity of 16,800 bpd (750,000 tpy) and isequipped with a new 350,000 tpy visbreaking unit, a 165,000 tpy gas oilhydro-sulfurization unit and a 20,000 tpy bitumen unit. The refinery is ina deteriorated condition as a result of a long period of operation withoutadequate spare parts and a subsequent fire in the topping furnace in 1983,after which it was temporarily shut down, and more recently, operated belowfull capacity. The GOM plans a major program of refinery rehabilitationpending the availability of required foreign exchange financing, in whichCCCE has expressed an interest to participate, though no firm arrangementshave been made. Although petroleum products are still widely available,port handling, storage, coastal transport and inland distribution systemsare in a badly deteriorated condition due to lack of spare parts andsuboptimal storage and handling arrangements, leading to large productlosses through multiple handling and evaporation. The study of petroleumimport options included in the project would also review the future role ofthe refinery and include preparation of a master plan for petroleumdistribution, expansion, and rehabilitation, and the organization andincentive system to effectively distribute petroleum products throughoutthe country.

3/ Fuel oil surplus to country requirements is re-exported from theToamasina refinery.

-8-

1.19 Petroleum prices remain above border prices; e-en with recentdevaluation, though the relationship between prices and economic costs ischanging rapidly due to exchange rate and global petroleum price varia-tions. Government policy is to discriminate in pricing against high-incomeusers in favor of low-income and productive end-uses. However, it isunlikely either that families using kerosene for cooking are low-income, orwhat heavy discrimination against gasoline is economically productive atthe margin. Diesel-engined vehicles are more expensive, and the policycurrently leads to the use of kerosene in blends with gasoil and gasoline,resulting potentially in higher engine wear and serious loss of fueleconomy. A review would be made by the Direction of Energy and Water,MIEM, as part of proposed petroleum planning studies, of possiblealternative pricing policies which might avoid the worst aspects of thepresent distortion while maintaining tax revenues and achieving economi-cally sound policy objectives.

1.20 Biomass Fuels. Declining physical accessibility of woodfuels ofacceptable quality over the past decade is strongly reflected in pricetrends in the open market. Prices of firewood and charcoal in Antananarivoappear to have increased by 50X and 30%, respectively, in real terms overthe 1973-1984 period. Since 1984, the Bank has monitored firewood andcharcoal prices at selected retail outlets in Antananarivo and had foundthat firewood prices have risen 13-15%, and charcoal about 5% per annum, inreal terms, during the past two years. However, recent IDA time seriesanalyses, which applied more accurate inflation data, cast doubt thatpricet have actually been increasing significantly in real terms. Detailedwoodfuels supply-demand projections were made by the Joint UNDP/World BankMadagascar Energy Assessment. Without a series of possible interventionsidentified by IDA, sbme of which are supported through this project, thedeficit between sustainable supply and demand in the hinterland ofAntananarivo will grow from 1.3 million to 2.2 million tonnes of woodequivalent over the next decade. The supply demand imbalance projectedwill lead to loss of oome 1.5 million ha of natural forest cover by 1995,some 12% of present contiguous forest cover. It is neither a conceivablenor a feasible option to reforest at a rate to avoid potentially seriousnegative effects of anticipated deforestation, although a combination ofimproved forest management, community or agroforestry, recovery of fuelquality residues surplus from wood processing, logging and existingindustrial wood plantations, as well as growing use of modern fuels andhigher cooking efficiency, could greatly ameliorate impending problems. Asa component of this project, IDA would support the utilization of thinningsand other residues from the Haut Mangoro pine plantation, commercial trialsof rice husk briquetting, improvements to traditional carbonizationefficiency, improved household energy planning, and interventions toimprove cooking efficiency through the use of improved stoves and theintroduction of electric rice cookers, all as private sector initiatives.

II* THE POWER SUBSECTOR

Organization

2.01 JIRAMA is the sole agency in Madagascar responsible for elec-tricity production and supply, and is also responsible for potable watersupply. Until 1973, responsibility for power supply was vested with two

-9-

major companies, privately owned Electricit6 et Eau de Madagascar (EEM) anda company in which the Government had a majority share-holding: Soci4t6d'Energie de Madagascar (SEM), which operated supply mainly in therespective municipalities. These two major companies also operated publicwater supplies in their service areas. In 1973 the Government took overSEM and EEM, managing the combined entity temporarily under the Soci6t6d'Interft National pour l'Eau et l'Electricite, and then in 1975,established the autonomous Malagasy Electricity and Water Corporation(JIRAMA), to own and operate all electricity and water supply. Finally, onJanuary 1, 1977, JIRAMA took over the assets and liabilities of the formerentities, in addition to the long term debt to Government in respect to thecompensation of related foreign interests. JiRAMA was at first responsibleto the Ministry of Economy and Commerce, but in the early 1980s became theresponsibility of the Ministry of Industry, Energy and Mines. Chapter IIIcontains further details on the management and origin of JIRAMA and itslinks with Government.

Sector Facilities

2.02 The major electric power facilities have been constructed tointernational standards. However, serious lack of foreign exchange for theprocurement of spare parts has led to severe deterioration of physicalplar- and increasingly frequent and economically disruptive outages.Sustained power supply in several major towns and cities is now seriouslyjeopardized. This problem has been further exacerbated by recentcyclones. Cyclone Kamisy caused severe damage to central highlands andwest coast facilities, especially in the Mahajunga supply zone, in 1984,and in March 1986 cyclone Honorina caused damage to distribution, transmis-sion and generation facilities. The majority of funding proposed for thepower subsector in the proposed project is for rehabilitation of diesel andhydropower generation, and for transmission ane distribution facilitieswith the objective to improve reliability of supply and to create a soundbasis for later power system expansion (para. 5.07).

2.03 Although the public power supply system is managed by JIRAMA,private sector captive supply is significant with 23% of total installedcapacity, a sizeable proportion of which is within the sugar industry.Table 2.1 indicates the ownership of power plants. In the region of thecapital of Antananarivo, supply is through a large interconnected systempresently responsible for over 63% of public electricity sales. The totalinstalled capacity in Madagascar is 267 .AW, if which 105.5 MW ishydropower, about 139 MW is diesel and 22.4 MW is steam turbine drivengenerators. Supply is divided into three groups as per Table 2.2 (IBRD Map18816).

Table 2.1: GENERATING CAPACITY BY OWNERSHIP IN 1985

Hydro, Thermal and Diesel TotalMW % MW % MW %

Public Supply 105.5 51.5 99.4 48.5 204.9 76.8Private Supply 62.1 62.1 23.2

Total Country 105.5 51.5 161.6 60.5 267.0 100.0

- 10 -

2.04 The main electric power generating facilities are listed in Annex2.1 and summarized in Table 2.2.

Table 2.2: GENERATING CAPACITY IN MADAGASCAR, 1985

Hydro Diesel Thermal TotalUnits MW Units MW Units MW Units MW

Interconnected Zone 16 92.4 13 34.5 - - 29 126.9External Zone 12 13.0 135 63.1 - - 147 76.1Isolated Zone 2 0.1 21 1.8 - - 23 1.9Public Sector 30 105.5 169 99.4 199 204.9

Private Sector - - 64 39.5 6 22.4 70 62.1

Total Country 30 105.5 233 138.9 6 22.4 269 267.0

Access to Service

2.05 All urban centers are served by electricity from public supply.The urban population is estimated to be 19% of the total of 10 million(1986). However, less than one-third of the urban population is actuallyconnected to electricity, wbich represents about 6% of the totalpopulation. Extension of supply within the ICS and other low cost supplyzones is a high priority component under the proposed IDA project. Percapita consumption of electricity from the public supply system was about33 kWh/year which, given substantial private sector production, is anunderestimate of the true national average. Madagascar's consumption is ofthe same order as that of Tanzania, and above that of the poorer countriesof the region, such as Ethiopia and Uganda. However, it is about one-halfand one-third of that for Malawi and Kenya, respectively, lndicating thatthe relative level of electrification is very low by regional standards,despite the availability of low-cost indigenous power resources.

Pattern of Electricity Consumption

2.06 Public electricity consumption by major system and consumercategory is shown in Table 2.3. In the ICS consumption was about 204 GWh,or about 64% of the total in 1985.

Table 2.3: MADAGASCAR: PUBLIC ELECTRICITY CONSUMPTION BYCONSUMER CATEGORY, 1985

ICS External Z. Isolated Z. TotalCategory GWh % GWh Z GWh Z GWh X

Residential 61.1 30.0 20.3 18.0 0.8 41.5 82.2 25.8Commercial 44.2 21.7 18.1 16.0 0.8 41.5 63.1 19.8Industrial 98.3 48.3 74.6 66.0 0.3 17.1 173.2 54.4

Total 203.6 100.0 113.0 100.0 1.9 100.0 318.5 100.0

- 11 ~-

Power Subsector Planning

2.07 Power system development planning has been carried out by JIRAMAwithout the assistance of consultants. Any development plans prepared byJIRAMA are presented to the Department of Energy and Water, MIEM, reviewedthere and then discussed with the DGP before being incorporated in thePublic Sector Investment Program (PSIP). However, the company has notroutinely undertaken comprehensive power system planning as it lackssuitably trained and experienced personnel and until recently was notstructured to facilitate systematic planning for power supply developmentand management. As a result there has never been a comprehensive leastcost expansion plan as the basis for review annually, or more frequently,as a regular part of management review and budgeting. Similarly, loadforecasts have been, for the most part, simple linear projections based onhistorical performance. The proposed project would include technicalassistance and training to strengthen the new Direction of Economic Studiesand Planning and the Direction of Electrical Equipment, which is thedivision responsible for the final feasibility study and implementationmanagement for major power system development. The proposed project wouldalso fund the first national power sector master plan and relatedinvestment programming and tariff studies, projecting the needs for systemdevelopment beyond the year 2000, and laying the foundation for rollingannual review and revision of plans and investment programs by JIRAMA.

2.08 In part as a result of planning weaknesses, and in part throughdirect Government intervention, there has been both overinvestment incapacity and overestimation of demand, leading to a dramatic oversupply ofgeneration capability in certain regional centers and little otilization ofavailalle hydropower in the main ICS. This has led, in turn, to lower thanexpected revenue, resulting in poor financial performance for the utility.Perhaps the most serious problem arises from the large surplus in hydro-power capacity contributed by the Andekaleka Hydropower plant (2x29 MW) inthe ICS feeding the Antananarivo region. Load growth in the ICS did notgrow as anticipated during the economic evaluation of the Andekalekaproject in the late 1970s, largely because the economy has been stagnant todeclining in comparison with the moderate growth foreseen at the time. Inparticular, a large number of planned industries did not materialize. In1985 only 180 GWh of the 500 GWh average annual availability of this hydro-power plant was utilized. The GOE and JIRAMA are revising commercialpolicies for electricity connections to promote the use of electricitywherever financially and economically attractive. Such measures would besupported by the proposed project. Furthermore, there is a need forcomprehensive power system rehabilitation. However, apart from the absenceof a planning framework for system expansion, there is no economicallysound methodology being practiced by JIRAMA to establish priorities forrehabilitation in the face of ongoing scarcity of equipment and materials.Modern maintenance scheduling and planning for decision-making onpriorities for implementation of the proposed major rehabilitation programare addressed in detail in the proposed project. The initial review phaseleading to rationalization of diesel generation facilities would alsoassist with a revaluation and computerization of the asset base and theestablishment of computerized spare parts inventory.

- 12 -

2.09 During appraisal, agreement was reached on reasonable loadforecasts, and an indicative or "Reference Power Sector Investment Prograu"(RIP) for the 1986-1992 period, was established in advance of more detailedload forecasting and system expansion planning which would be undertaken aspart of the proposed project. Agreements were obtained during negotiationsthat: (i) JIRAMA would not, until the completion of the project, undertakeany major change in the Government's RIP agreed with IDA unless JIRAMAshall have furnished evidence satisfactory to IDA that such major projector program is economically and technically justified and, (li) the RIP,which would cover at least five years, would be reviewed annually by March31, or as needed, and revised as required. Major changes would be thoserequiring capital expenditure which would exceed 1X of JIRAMA's grossrevalued assets in operation in any fiscal year, or two million dollars,whichever is the lower.

Power Subsector Objectives

2.10 The main objectives of the power subsector arising from discus-sions between JIRAMA, the Government and IDA are: (i) to improve thereliability of production and supply of electricity throughout the countryin accordance with agreed national economic and social objectives; (ii) toensure that electricity supply is provided at least cost; (ili) to increasethe use of indigenous sources of electricity wherever economicallyjustified; (iv) maximize the utilization of existing low cost sources cisupply from existing production capacity.

Power Subsector Strategy

2.11 The following strategy represents the position of the GOM andJIRAMA in attempting to fulfill the main power sector obJectives: (i) todevelop indigenous energy resources, such as hydropower and biomassresidues, for electricity generation in place of more expensive importedfuels; (ii) to interconnect supply zones to make more efficient use ofexisting and prospective major hydropower plants and to stabilize andminimize the cost of power supply; (iii) to increase system reliability andreduce power losses through improving operation and maintenance andrehabilitating existing facilities; (iv) to regulate tariffs and take otherfinancial measures necessary to meet financial objectives; (v) to promotethe utilization of electricity where economically and financiallydesirable, through increasing the number of consumers and designingprograms of interfuel substitution in industry for electrifying heat andsteam production; (vi) to undertake least-cost power system expansionplanning and to carry out detailed feasibility studies for economicallyattractive major power developments.

Aid Inflow and Coordination in the Sector

2.12 Bank participation in the sector has been substantial, thoughlimited to one major hydropower project: Andekaleka. To finance thisproject a substantial cofinancing effort was made leading to a financingpackage which included the Abu Dhabi Fund, Banque Arabe de D6veloppementEconomique en Afriq-¶e (BADEA), Caisse Centrale de Cooperation Economique(CCCE), Canadian International Development Agency (CIDA), Kuwait Fund, andthe Saudi Development Fund. However, despite the number of donors involved

- 13 -

in financing Andekaleka, CCCE is the only donor which has continued tosupport power subsector development consistently with several small loans,the most recent of which being considered is for US$2 million equivalentfor the proposed Tana Sud 63 kV transmission ring. Aid flow has otherwisebeen modest and JIRAMA has had to resort to short term suppliers' creditsto finance recent diesel power plant expansion, which was itself, in retro-spect, a low priority use of foreign exchange. Hence, foreign assistancehas been inadequate to meet subsector requirement; a limitation whicb hasbeen further exacerbated by natural disasters, including floods andcyclones. Finally, weaknesses in planning and overt Government interven-tion in investment decision making has led to an imbalanice in investmentbetween generation expansion and rehabilitation of existing facilities,which continue to deteriorate rapidly.

III. THE IMPLEMENTING AGENCIES

3.01 The implementing agencies would be JIRAMA for the power components,FANALAMANGA for the pine carbonization project, and the five ProjectImplementation Units (PIUs) under the coordination of the PMU in the MIEMfor the energy components of the project. Implementing agencies and theinstitutional arrangements are presented in Annex 3.1.

JIRAMA

3.02 JIRAMA is an entirely state-owned corporation, created in 1975 toown and operate all public electricity and water supply facilities. Inthat context JIRAMA may undertake all relevant activities, including theacquisition of other water and power companies in the country, and thecreation of subsidiaries. This flexibility has enabled JIRAMA to absorb,consolidate, and merge into one company the numerous independent utilitiesin existence prior to its own creation.

3.03 Organization and Management. JIRAMA has an eighL-member Board ofDirectors, which is appointed by the Government and includes four membersfrom the Ministries of Energy, Interior, Labor, and Agriculture and non-government appointees. A Director General, also appointed by the Govern-ment, is responsible for day-to-day management. Although it is under theformal supervision of MIEM, JIRAMA has reasonable autonomy to conduct itsday-to-day affairs without undue interference by Government. However,Government has directed JIRAMA to make investments in power supply formajor projects which have not materialized or which will not use power atthe planned level, leading to serious overinvestment in generationcapacity. The company is also subject to tight controls regarding foreignexchange allocations which require the approval of MIEM, the Ministry ofFinance, and the Central Bank. The Government further exercises strictcontrol over electricity tariffs, and tariff changes require cabinetapproval. JIRAMA has recently undergone a reorganization, wherebyresponsibilities have been more suitably regrouped by function rather thanon the previous basis of geographical areas. Also, a greater decentraliza-tion of day-to-day management within reinforced regional administrativeentities is envisaged with respect to personnel, customer management andinventory control. Furthermore, all planning activities and economicstudies, previously dispersed in seve:al departments, have been consoli-dated within a single Department of Economic Studies and Planning, for

- 14 -

which a technical assistance program is proposed under the project (para.5.07(e)). Managerial efficiency of the company continues to be constrainedby infrastructural and logistical shortcomings. For example, management inAntananarivo is dispersed in 17 buildings, telecommunications equipment atthe local level is limited and obsolete, communications between the regionsand the center are difficult, and the situation of the vehicle fleet iscritical. Programs for the modernization of the vehicle fleet and of thetelecommunications system are part of the proposed project (para.5.07(d)). In order to overcome present deficiencies ii the relationshipbetween the Government and its wholly-owned parastatal, JIRAMA, which untilrecently have implied ongoing financial dependency, limited tariffmanagement autonomy and increasingly costly and poor quality service, it isappropriate for the Government and tIRAMA to consider a complete review andreform of their commercial and administrative relationship. The GOM hastaken important steps towards such a reform package through the measures tobe adopted for financial restructuring of JIRAMA in parallel with theprocessing of the proposed Credit. Building on these financial reforms, itis appropriate for the GOM to develop and adopt a more all-embracingcompact defining specific objectives, mutual responsibilities andobligations that would lead JIRAMA not only to financial autonomy, but alsoto a greater degree of management autonomy based on a commitment toGovernment to achieve certain minimum performance criteria consistent withincreasingly reliable and high quality service at least cost. Atnegotiations, Government and JIRAMA would agree to prepare and present forIDA review by December 31, 1987 such a compact or "contract plan".

3.04 Planning. Due to a shortage of suitably experienced and qualifiedstaff and a lack of data processing equipment and computer software, JIRAMAhas been unable to prepare appropriately detailed load forecasts and asystem expansion plan and investment program. These deficiencies will bealleviated under the proposed project (see paras. 2.07, 5.07 andAnnex 5.2).

3.05 Engineering and Design. Although JIRAMA has a number of qualifiedengineers on its staff, to date its design activities have been limited tothe distribution and sub-transmission level, with assistance fromconsultants on major projects. During construction of the Andekalekaproject, JIRAMA construction crews satisfactorily completed the erection ofthe 175 km, 138 kV transmission line to Antananarivo, with guidance fromconsultants. Installation of all distribution facilities was completedwithout outside technical help. However, because of the large volume ofengineering work required, JIRAMA should employ consultants to assist inprocurement and supervision in order to ensure successful projectcompletion, and funds have been included in the proposed project for thispurpose,

3.06 Operations and Maintenance. The electric power facilities are notwell maintained primarily because of the lack of funds for spare parts butalso due to the lack of training in modern preventive maintenance programs.In consequence, supply outages in the ICS and External Zone (ZE) areincreasingly frequent and disruptive of industrial and commercial activity,and a large proportion of diesel electric generating plant is unservice-able. This is a particular problem with diesel engines which, withoutroutine maintenance, become unreliable long before their expected service

- 15 -

life. Thus, a component of this proposed project includes not only theprovision of spare parts, but also the training of maintenance personneland the establishment of equipment monitoring and repair techniques.

3.07 Data Processing. At present JIRAMA does not have any internaldata processing equipment such as micro-computers for basic statisticalanalysis and management information reporting. Data processing is carriedout by SOMAGI, a public enterprise for computer services. However, therole of SOMAGI in the evolution of computerization of data processing inJIRAMA is to be reviewed as part of the proposed project and incoordination with CCCE technical assistance to JIRAMA. SOMAGI performscustomer billing, financial accounting and analytical accounting. With thedecentralization of management on a regional basis, additional equipment ofsufficient capacity to handle (i) inventory control; (ii) maintenancemanagement; and (iii) regionalized computerized customer billing, isproposed under the project (para. 5.07(d)). The proposed equipment wouldbe micro-computers and communication with the center would be viadiskettes.

3.08 Billing and Collection. Meters are read once a month. Thereadings are sent to SOMAGI, where batch programs issue the bills on the20th of each month. Ten to fifteen percent of the customers pay directlyto the collector distributing the bill, 6.5% by automatic withdrawal from abank account, 13% by check, and the rest in cash at JIRAMA's registers.Enforcement of payment for private consumers is quite strict. Customersthat do not pay within 8 days of receipt of a special delivery reminder,which in turn is sent 8 days after the original bill has been issued, aredisconnected. As a result, accounts receivable from private and industrialcustomers are satisfactorily low. JIRAMA on the other hand has not beensuccessful in collecting from Government agencies and municipalities.Accounts receivable represent betweer 12-14 months of sales to theseconsumer groups. The proposed project requires that the totality ofarrears be settled half by June 31, 1987, and half by September 31, 1987,(Table 6.3).

3.09 Accounting and Audit. JIRAMA !aintains its books in accordancewith Malagasy accounting codes and regulatiou. Many accounting functionsare computerized through SOMAGI; notable exceptions include asset andinventory control, which will be addressed under the proposed project(para. 3.09). The auditor's report for the 1984 accounts contained severalqualifications relating to and recommending (i) improvement of theinventory of assets and their valuation; (ii) reducing accounts receivablein the Isolated Systems; and (iii) upgrading inventory valuation. JIRAMAhas been taking corrective actions in these areas and the audit report forthe 1985 accounts contained only a qualification regarding the upgrading ofinventory valuation. Agreement was reached during negotiations that JIRAMAwill continue to evploy qualified auditors and will send audited accountsto IDA within six months after the end of the fiscal year.

3.10 Insurance and Taxes. JIRAMA has satisfactory insurance coverageof its plant and equipment against the risks of fire, theft, liability, andaccident. Breakdown of machinery Is insured in some instances. JIRAMA issubject to a 36% tax on its net income as well as custom tariffs, importduties, vehicle taxes, and a business tax. Prom its customers the company

- 16 -

collects for the Government an added value tax of 15% and a consumptioncharge of FMG 5 per kWh (0.6 US¢/kWh). JIRAMA is thus a rather highlytaxed utility. While it generates significant revenues for Goverrment, thetax regime results in tariffs which are considerably higher than elsewherein the Eastern and Southern Africa Region. Different consumer categoriespay different taxes and base tariffs for the same conFlumer groups varyarbitrarily due co the historic tariff structure (para. 5.01(f)). Reduc-tion in the number of tariffs, and simplification of the application oftaxes through the billing structure, offer the potential for considerableimprovement in administrative efficiency and cost reductions. Agreementwas reached during negotiations with JIRAMA and the Government that theresults of the tariff reform study will be jointly reviewed with IDA beforeSeptember 1988 and that the new tariff structure would be implemented notlater than January 1, 1989.

3.11 Personnel and Personnel Management. As of mid-1986, JIRAMA hadabout 4,100 employees of which about 325 or 8% were top and middle levelmanagers and professional staff, about 900 or 22% were lower level managersand middle level staff, and the remaining 2,875 or 70% were lower levelemployees. These numbers represent overall employment including the watersupply staff. Considering that about half the staff are concerned withelectricity affairs, the staffing levels represent one employee per 58customers which is a satisfactory ratio by regional standards, thoughreduction to 65-70:1 should be sought and will be monitored by JIRAMA overthe next decade. JIRAMA's salaries are reasonably competitive and thecompany is generally able to attract suitable staff as necessary, althoughJIRAMA is currently recruiting in a captive market. Most of the company'sprofessionals are graduates from the local university system and only veryfew have been trained abroad. A new evaluation system was introdaced inAugust 1986 for all higher and medium level staff. Based on performanceplans and subsequent evaluation reviews merit increases are allocated.Individual training schedules are being established as precondition for thenext promotion step, and in the future managerial positions will be filledfrom a company-wide pool of candidates. Personnel administration will bedecentralized as standardized recruitment, probation, promotion, andrelated procedures are implemented.

3.12 Training. JIRAMA's training activities are well organized. Anorientation group chaired by the Director General deternines the annualtraining objectives. A training committee and specialized subcommitteessubsequently design specific training curricula. Most of the training isprovided through the in-house training facility; external trainingrepresents 5%. In 1985, 518 staff received 592 staffweeks of training,equivalent to an average of about 0.5 staffweeks per eligible employee(managers, professional and middle level staff). Training a- oad has beenseverely restricted due to lack of foreign exchange, and while JIRAMA'sstaff is technically competent, it has to some extent been isolated fromthe latest techniques. Therefore the project supports additional overseastraining based on an agreed training program.

3.13 Management Information System. JIRAMA needs an appropriateManagement Information System which will help managers to identify problemareas early and to take corrective action. Such a system would bedeveloped and implemented under the proposed assistance to JIRAMA's

- 17 -

planning department (para. 5.07(e)). It would establish a number oftechnical and financial performance indicators to be reviewed and agreedwith IDA in the course of the project.

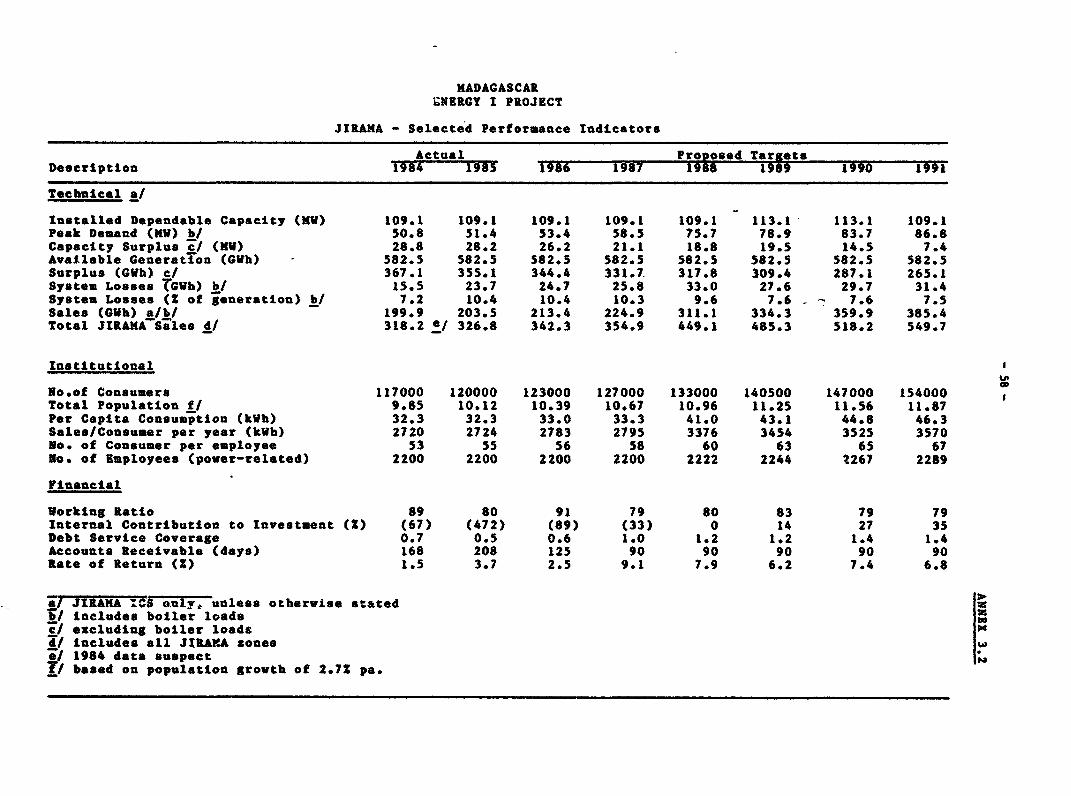

3.14 Performance Indicators. An indicative set of performanceindicators is provided in Annex 3.2. It will be used while the MIS isdefinied and implemented. These indicators are necessarily tentative asthey have been defined on the basis of preliminary estimates.

IV. THE MARKETElectricity Market

4.01 Historical Market. Electricity sales have grown sporadicallyduring the 1970s and 1980s. Nationwide sales grew on average by 4.4% peryear between 1973-83, from 203 GWh to 313 GWh, though year to year growthrates varied from 14% in 1979 to -1% in 1982 (Table 4.1). The largeincrease in 1979 was due to a 17% growth in industrial electricity consump-tion as a result of a 13% increase in industrial output. Similarly, theperiod of virtually zero growth in 1980-82 was caused largely by a sharpdecline in industrial output. Growth in ICS sales was only about half thatof the other systems after 1983: 3.4% compared with 6.4%. Capacity demandgrew more rapidly than energy demand for the 1973-83 period, from about 30MW to 45 MW, or 4.1% per annum.

Table 4.1: ELECirrY aIpexq, 1973-83

1973 1976 1979 1980 1981 1982 1983 1973-76 1976-79 1979-83 1973-83- Growth Rate (M)

ics a/Sales, G)h 138.2 146.6 172.6 180.0 182.0 180.2 192.3 2.0 5.6 2.7 3.41mdmn Dend, MW 30.2 32.5 38.0 40.0 41.5 44.6 45.3 2.5 5.4 3.6 4.1Other AreasSales, GWh 65.1 82.4 106.4 115.6 120.8 119.8 120.6 8.2 8.9 3.2 6.4Total Sales, GWh 203.3 229.0 279.0 295.6 302.8 300.0 312.9 4.0 6.8 2.9 4.4

So: JER

4.02 Demand Forecast for Electricity in the Main ICS. During prepara-tion and appraisal of the proposed project, IDA missions undertook adetailed review of power and energy demand for the main ICS and severalregional supply centers. Subsequently, IDA and the Government have agreedon a load forecast for the the ICS, between 1985-1995, wherein demand isexpected to grow by 5.1% p.a. excluding the foreseen electric boiler load,and by 7.5% per annum including boiler electriflcation (see para. 5.07).It is acknowledged by JIRAMA that electric boiler loads made possible bysubstantial surpluses of hydropower from the Andekaleka Hydropower Projectare not to form part of the justification for expansion of generationcapacity in the ICS in the longer term. Demand growth is expected to occuras a result of the project through the provision of additional distributionequipment and materials, and more flexible financing arrangements forconnections, to begin to meet the large backlog of consumer demand for

- 18 -

electricity supply service, as well as through a modest pilot program toexamine the market for electric rice cookers. There is a cumulativeregister of 10,000 applications for electricity supply, including 200commercial undertakings, for whom connection has not been possible due toshortages of distribution materials. Assumptions on which the ICS demandforecast was based are provided in Annexes 4.1, and the detailed forecastitself is in Annex 4.2. The pattern of demand growth in 1980, 1985 andprojected for 1995 is presented in Table 4.2. The composition of demanddid not change greatly between 1980 and 1985, though major changes areexpected over the next decade. As a result of boiler electrification theindustrial share of electricity demand will grow disproportionately to 62%of the total; household demand will also continue to grow strongly,maintaining its share of the market, while the share of commercial demandis expected to decline.

Table 4.2: JD0MA ICS: PATIERN OF MDMD, AC1ULAN) AM ECRED BY aOMii CAM1'RY, 1980-9

Goth Rate Growh RateFM8 mF5 FYBD-F85 FY95 FY85-FY95

Category GWh h X GWh h h h GJh b h

Residential 46 26 61 30 5.7 115 26 6.5ormercil 40 22 44 22 2.2 55 12 2.2IndustralBoilers (0) 0 (0) (0) 0 (0) (97) 35 (22)Other Industry (94) 100 (52) (98) 100 (48) 0.9 (177) 65 (40) 6.0Total industry 94 100 52 98 100 48 0.9 274 100 62 10.8Overall Tbtal Sales 180 100 204 100 w4 100

Total No. Qstomers 75,499 86,882 129,000 (est.)(in the ICS)btal JInMa 119,888 138,416 2D5,000 (est.)

4.03 Generation and Capacity Balances in the Interconnected System.Actual and forecast peak demands in the period 1980-1995 are provided inAnnex 4.3. Peak demand is expected to grow at the rate of about 7% peraanum during the 1985-95 period due largely to the electric boiler program,but also due to renewed growth. Apart from the backlog of domesticconnections, there are important opportunities to substitute electricityfor imported LPG in commercial cooking and for storage water heating. Theproject itself, and new JIRAMA connection financing policies, willstimulate growth in the domestic sector demand for electricity. Capacityand energy balances for the ICS are provided in Annex 4.4. Present firmavailable capacity has been confirmed from operational records for theplant concerned. The hydropower dominated system has experienced highgenerating reliability to date, and the proposed project would provide forspare parts and other works to maintain this record. Hence, a reservemargin established with the biggest unit out of service (22 MW firm) shouldprove acceptable. With this reserve margin, corresponding to about 19% ofcapacity reserve, capacity is sufficient up until 1995, although newcapacity would be required at the latest during 1995. Apart from slightcapacity expansions through efficiency improvements in existing hydropower,this will require investment in new generating plant, interconnection with

- 19 -

other systems then in surplus, or both. A least cost expansion plan studyto be financed under the proposed project would form the basis of decision-making regarding expansion of supply to the ICS. In the interim period, atleast until 1993, there is surplus capacity, and there are very substantialenergy surpluses-always in excess of 40% of demand--through 1995. Theproject seeks to promote means of utilizing these surpluses, as describedabove, without catalyzing untimely and expensive new investments incapacity.

4.04 Demand Forecast for Electricity in the External Zone. TheExternal Zone (ZE) includes other major highlands centers as well as thecoastal towns. The largest are Mahajunga and Tollary on the west coast andToamasina on the east coast, the main port. Between them, these centerscomprise almost 80% of demand in the ZE which, in turn, comprises about 36%of total demand in the public supply system. Demand is expected to growmodestly, averaging about 4% per year, in these major towns, due to thedepressed state of the small regional economies which have only moderateprospects for industrial production and exports (Annex 4.5).

4.05 Demand Forecast for Electricity in the Isolated Zone. TheIsolated Zone (ZI) is comprised of numerous very small do'wand centresserved by diesel plant and lies within the general supply area of the ICS.In the longer term, as demand in these centres expands they will beconnected to the main grid, thus the ZI will always remain comparativelysmall, and is presently about 0.5% of total public sector demand, growingat about 10% per annum (Annex 4.5).

Household Fuels Market

4.06 Household energy comprised 83% of final energy consumption in 1983and is projected to remain close to 80% of end-use through 1995 (see Table1.1). The estimate' composition of household energy consumption in 1979and 1983, and that projected for 1995 is presented in Table 4.3.

Table 4.3: HOUSEHOLD ENERGY CONSUMPTION, ACTUAL AND PROJECTED, 1979-95

1979 1983 1995Energy Source ktoe % ktoe % ktoe %

Firewood 1074.8 87.4 1201.8 87.4 1688.8 84.6Charcoal 99.8 8.1 121.3 8.8 212.8 10.7Electricity 17.0 1.4 21.7 1.6 37.6 1.9LPG 4.2 0.3 1.7 0.1 4.0 0.2Kerosene 34.5 2.8 28.6 2.1 51.4 2.6

Total 1230.3 100.0 1375.1 100 1994.6 100

Firewood for household cooking dominates the household portion of nationalenergy demand and, including charcoal, woodfuels serve 96% of nationalhousehold demand in final energy terms. This situation is unlikely tochange over the next decade except that, with the rapid urbanization beingexperienced, charcoal is projected to supply a greater proportion of finalcooking energy demand, reflecting the preference of a growing lower-middleto middle income urban population. Similarly, while remaining a small

- 20 -

proportion of total household energy demand, domestic use of electricity isexpected to expand as a result of recently revised commercial policiesdesigned to stimulate connection of consumers presently within the ICSregion, and through expanded use of electricity for cooking, both of whichare encouraged by the proposed project. Except where hydropower surplusesexist, the use of petroleum fuels for household cooking is expected torecover and exceed historical levels assuming more stable and efficientoperation of the refinery, or reduced petroleum product costs CIF, makingkerosene and LPG available at lower real prices during this period.

4.07 Cooking Fuel Supply and Demand: Antananarivo. Antananarivo is byfar the largest marketplace for traded household cooking fuels and that forwhich future supply portends the greatest economic burden on the country.As noted in paragraph 1.20, sustainable supply of woodfuels to the Faritanyof Antananarivo is far less than demand, implying continued harvesting ofaccessible prime forest with unknown but possibly serious environmental andeconomic consequences for the sustained productivity of agriculturalecosystems in its hinterland. Annex 4.6 provides estimates of actual andprojected supply and demand to the Faritany of Antananarivo, dominated bythe city i self, for the period 1980-1995. Woody fuels from aging fuelwoodplantations, natural forest and residues meet 96% of present demand in thisregion, though with well planned utilization of other untapped andpotentially sustainable sources--such as residues from industrial pinewoodplantations, wood processing and logging operations, improved forestmanagement and woodfuel tonversion and end-use and expanded use of surplushydroelectricity-the rate of deforestation can be stabilized. Theproposed project is supporting this objective through assistance forproduction of charcoal from pine plantation thinnings and for expandedelectrification of cooking, and through a cooking efficiency program aimedat designing and disseminating efficient wood and charcoal stoves.

4.08 Household Fuels Marketing. Marketing of woodftsels is essentiallycontrolled by the private sector. Similarly, despite publication andpurported regulation of official charcoal prices by the Government,firewood and charcoal prices respond dynamically to the forces of supplyand demand in the open market. The only active interface betweenGovernment and private sector traders is through licensing by themunicipality concerned of urban retail outlets for charcoal and firewood.Even so, substantial numbers of retailers appear to escape regulation,licensing and the associated fees, which are charged per unit floor areaof the retail outlet. The market price reflects the full cost of supply(excluding the full economic cost of primary woodfuel production), plus anyprofit taken at each stage in the supply chain. Generally, fees charged bywoodlot owners to firewood gatherers or charcoalers are well below thereplacement cost of the resource. A graphical representation of thetypical supply chains feeding charcoal and firewood to the urban householdmarket of Antananarivo is provided in Annex 4.7. The woodfuels business isundertaken by a variety of entrepreneurs, from individuals engaged inoccasional production and marketing in the off-crop, season to medium-sizedorganized charcoal production and trading compsaies. The business ishighly competitive and evidence that the number of retail outlets forcharcoal has more than doubled in the 19809 in Antananarivo suggests thatit is expanding rapidly. IDA missions have been monitoring prices in aselection of retail outlets in Antananarivo over the past two years; the

- 21 '-

results show that there is marked seasonality in prices, and nominal priceshave increased sharply, though the underlying trend in real price increasesis observed by relatively poor data on inflation experienced by thecharcoal consuming group.

4.09 The project would provide for the production and marketing of atleast 5,000 tpy of charcoal from pine thinnings in the Haut Mangoro Pineplantation and 1,500 tpy of experimental rice husk briquettes from ricehusks wastes of local milling plants. The marketing of these fuels wouldeither be under contracts negotiated between private sector producers ormanagers of the production process and industrial consumers, such as thecement manufacturer, CIMA, in Antsirabe, or through the regular wholesaleand retail trade described above. There are almost certainly opportunitiesto reduce costs for present private sector traders and to improve theefficiency of supply and marketing arrangements, such as through improvedaccess to credit for transportation and woodfuels production and conversionequipment and materials, and through final effective deregulation of retailmarketing. Thus, the project includes a detailed and comprehensive reviewof the woodfuels business in the Antananarivo region, and for Toliar andMahajunga, three important though quite different supply and tradingenvironments. This component, which is part of a wider household energyplanning program IDA would finance (para. 5.07 (i)), modelled on a similar,successful IDA-supported planning program in Ethiopia, would also establisha regular network of market price monitoring for selected major centers.Recommendations are expected to arise from this review on means to assistthe private sqctor to improve the efficiency of the business and to reducewoodfuel costs.

V. INVESTMENT PROGRAM AND PROJECT

Reference Power Subsector Investment Program (RIP)