Embed Size (px)

Citation preview

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No. 47916-PH

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

INTERNATIONAL FINANCE CORPORATION

MULTILATERAL INVESTMENT GUARANTEE AGENCY

COUNTRY ASSISTANCE STRATEGY

FOR

THE REPUBLIC OF THE PHILIPPINES

FOR THE PERIOD FY 2010-2012

April 2, 2009

Philippines Country Team, World Bank

East Asia and Pacific Region

International Finance Corporation

East Asia and Pacific Department

Multilateral Investment Guarantee Agency

East Asia and Pacific Department

This document has a restricted distribution and may be used by recipients only in the performance of

their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

The last Country Assistance Strategy (CAS) Report No. 32141-PH was discussed by the Board on May 17, 2005, and the last CAS Progress Report No. 40085-PH was dated June 21, 2007 World Bank IFC MIGA Vice President James W. Adams Rashad-R. Kaldany

Karin Finkelston Izumi Kobayashi

Country Director/ Resident Representative

Bert Hofman Jesse Ang Frank Lysy

Task Team Leader Co-Task Team Leader

Lada Strelkova Andrew Parker

Magdi Amin Conor Healy

CURRENCY EQUIVALENTS

Currency unit: Pesos (Php) as of April 2, 2009

US$1 = Php 48.27

FISCAL YEAR

January 1 – December 31

This Country Assistance Strategy (CAS) was prepared under the guidance of Bert Hofman, IBRD Country Director, and Jesse Ang, IFC Resident Representative, by a team led by Lada Strelkova, Task Team Leader (TTL) and Andrew Parker, co-TTL. The IFC team integral to the development of this CAS was led by Magdi Amin, Principal Strategy Officer. MIGA participation was led by Conor Healy, Risk Management Officer. Nigel Twose provided overall guidance on the joint IFC-IBRD strategy development.

The CAS Core Team included: David Llorito, Leonora Gonzales, Lilanie Magdamo, Maribelle Zonaga, Maryse Gautier and Yolanda Azarcon and the following Working Group Leaders: Ben Eijbergen, Carol Figueroa-Geron, Eduardo Banzon, Eric Le Borgne, Jehan Arulpragasam, Josefina Esguerra, Karl Kendrick Chua, Kim Henares, Maria Loreto Padua, Mukami Kariuki, Swati Ghosh, and Yasuhiko Matsuda. Core team support was provided by: Cynthia Manalastas, Grace Borja, Maria K. Hermoso, Maria Liberty Cardenas, Ludy Anducta, and Necitas Garcia from IBRD; Andrey Manalo from IFC; and Yoshine Uchimura, and Zafar Ahmed (consultants).

The following CAS Working Group members and other colleagues have also made important contributions to this strategy: Agnes Albert-Loth, Cecille Vales, Christopher Pablo, Fabrizio Bresciani, Florian Lazaro, Hamid Alavi, Hiroshi Tsubota, Josefo Tuyor, Felizardo Virtucio, Jr., Iain Shuker, Jonas Bautista, Lynnette Dela Cruz Perez, Mark Woodward, Mario Suardi, Mary Judd, Ma. Bella Tumaliwan-Belizario, Matthew Stephens, Maya Villaluz, Miguel Navarro-Martin, Rashiel Velarde, Rayah Sarah Judy Padilla, Rey Ancheta, Rosechin Olfindo, Salvador Rivera, Sameer Goyal, Sheryll P. Namingit, Simon Gregorio, Maria Theresa Quinones, Timothy Johnston, Ulrich Lachler, Victor Dato, and Zahid Hasnain from IBRD; and Aileen Ruiz, Ali Naqvi, Colin Taylor, Deepa Chakrapani, Euan Marshall, Gerlin Catangui, Julie Bayking, Lulu Baclagon, Matthew Gamser, Patricia Wycoco, Rafael Dominguez, Val Bagatsing, Will Beloe, and William Haworth from IFC. Other members of the Bank-wide Philippines Country Team (including IBRD, IFC and MIGA) have also contributed.

Special thanks are extended to the Government of the Philippines counterpart team and World Bank Group development partners for their contributions.

ACRONYMS AND ABBREVIATIONS

AAA Analytical and Advisory Activities

ADB Asian Development Bank

AIDS Acquired Immune Deficiency Syndrome

ARCDP2 Agrarian Reform Communities Development Project 2

ARMM Autonomous Region in Muslim Mindanao

AusAID Australian Agency for International Development

BSP Bangko Sentral ng Pilipinas (Central Bank of the Philippines)

BEIS Basic Education Information System

BIR Bureau of Internal Revenue

BOC Bureau of Customs

BTr Bureau of Treasury

CALABARZON Cavite, Laguna, Batangas, Rizal and Quezon provinces

CAS Country Assistance Strategy

CCT Conditional Cash Transfer

CDD Community-Driven Development

CDS City Development Strategy

CGAC Country Governance and Anticorruption

CIDA Canadian International Development Agency

CMU Country Management Unit

CLT Country Leadership Team

COA Commission on Audit

CPBD Congressional Planning and Budget Department

CPI Consumer Price Index

CSOs Civil Society Organizations

DBM Department of Budget and Management

DBPLID Development Bank of the Philippines/ Local Infrastructure Development

DENR Department of Environment and Natural Resources

DepED Department of Education

DFIMDP Diversified Farm Income and Market Development Project

DILG Department of Interior and Local Government

DOE Department of Energy

DOF Department of Finance

DOH Department of Health

DPL Development Policy Loan

DPWH Department of Public Works and Highways

DRM Disaster Risk Management

EAP East Asia and Pacific

ECSLRP Electric Cooperatives System Loss Reduction Project

EC European Commission

FDI Foreign Direct Investment

FIES Family Income and Expenditure Survey

FM Financial Management

FSAP Financial Sector Assessment Program

JICA Japan International Cooperation Agency

GAD Gender and Development

GDP Gross Domestic Product

GFDRR Global Facility for Disaster Reduction and Recovery

GFIs Government Financial Institutions

GIFMIS Government Integrated Financial Management Information System

GNP Gross National Product

GOCC Government Owned and Controlled Corporations

IBRD International Bank for Reconstruction and Development

ICT Information and Communication Technology

IEG Independent Evaluation Group

IFC International Finance Corporation

IMF International Monetary Fund

INT Department of Institutional Integrity

FY10-12 Country Assistance Strategy for the Philippines April 2, 2009

ii

IPs Indigenous Peoples

ISRs Implementation Status and Results Reports

IRA Internal Revenue Allotment

KALAHI-CIDSS Kapit Bisig Laban sa Kahirapan-Comprehensive and Integrated Delivery of

Social Services

LGC Local Government Code

LGUs Local Government Units

LISCOP Laguna De Bay Institutional Strengthening and Community Participation

MDFO Municipal Development Fund Office

MDGs Millennium Development Goals

MIGA Multilateral Investment Guarantee Agency

MILF Moro Islamic Liberation Front

MIMAROPA Mindoro, Marinduque, Romblon, and Palawan provinces

MRDP2 Mindanao Rural Development Project 2

MMURTRIP Metro Manila Urban Transport Integration Project

MTEF Medium Term Expenditure Framework

MTF-RDP Mindanao Trust Fund-Reconstruction and Development Project

MTPDP Medium-Term Philippines Development Plan

MTPIP Medium-Term Philippines Investment Plan

MWSS Metro Water Sewerage Systems

NAPC National Anti-Poverty Commission

NCR National Capital Region

NEDA National Economic and Development Authority

NER Net Enrolment Rate

NG National Government

NGO Non-Governmental Organization

NPS National Program Support

NPL Non Performing Loan

NRIMP2 National Roads Improvement Management Project 2

NSCB National Statistical Coordination Board

NTC National Telecommunications Commission

ODA-GAD Official Development Assistance-Gender and Development

PCN Project Concept Note

PDF Philippines Development Forum

PEFA Public Expenditure and Financial Accountability

PEM Public Expenditure Management

PFM Public Financial Management

PGAT Philippines Governance Advisory Team

PIDP Participatory Irrigation Development Project

PPP Public-Private Partnership

PSP Private Sector Participation

RPP Rural Power Project

SME Small and Medium Enterprise

SOCCSKSARGEN South Cotabato, Sarangani, North Cotabato, and Sultan Kudarat provinces

SSLDIP Support for Strategic Local Development and Investment Project

TA Technical Assistance

TB Tuberculosis

TF Trust Fund

UN United Nations

USAID United States Agency for International Development

UT Urban Transport

VAT Value Added Tax

WBI World Bank Institute

WBG World Bank Group

WDDP Water District Development Project

WHO World Health Organization

WGI World Governance Indicators

WPA Work Program Agreement

JOINT IBRD/IFC/MIGA

COUNTRY ASSISTANCE STRATEGY (CAS) FOR

THE REPUBLIC OF THE PHILIPPINES

TABLE OF CONTENTS

EXECUTIVE SUMMARY ............................................................................................ I

I. INTRODUCTION ................................................................................................ 1

II. PHILIPPINES CONTEXT AND DEVELOPMENT AGENDA ............................. 1 Social and Political Context ........................................................................................................................... 1 Recent Economic Developments .................................................................................................................... 3 Macroeconomic Prospects .............................................................................................................................. 4 Poverty Profile and Trends ............................................................................................................................. 6 Philippines Development Challenges and Opportunities ............................................................................... 9 Updated 2004-10 Medium-Term Philippines Development Plan (MTPDP) ............................................... 11

III. BANK GROUP ASSISTANCE STRATEGY FOR THE PHILIPPINES .............. 12

A. Lessons Learned from FY06-09 CAS and Stakeholder Feedback ......................................................... 12 Lessons from FY06-09 CAS Completion Report......................................................................................... 12 Findings from Recent IEG Evaluations ........................................................................................................ 12 World Bank FY09 Client Survey and Multistakeholder Consultations ....................................................... 13

B. Proposed World Bank Group Assistance Strategy ................................................................................. 14 World Bank Group Assistance Strategy Overview ...................................................................................... 14 World Bank Group Program Integration ...................................................................................................... 17 Strategic Objectives and Results Areas ........................................................................................................ 18 - Strategic Objective 1: Stable Macro Economy .......................................................................................... 18 - Strategic Objective 2: Improved Investment Climate ................................................................................ 20 - Strategic Objective 3: Better Public Service Delivery ............................................................................... 22 - Strategic Objective 4: Reduced Vulnerabilities ......................................................................................... 24 Cross-Cutting Theme: Good Governance .................................................................................................... 27

C. Implementing the FY10-12 Country Assistance Strategy ....................................................................... 29 Operationalizing Governance ....................................................................................................................... 29 Managing the Program ................................................................................................................................. 31 Fostering Stronger Partnerships ................................................................................................................... 34 Mainstreaming Gender ................................................................................................................................. 36

IV. MANAGING RISKS ......................................................................................... 37

FY10-12 Country Assistance Strategy for the Philippines April 2, 2009

ii

TEXT TABLES

Table 1: Medium-Term Macroeconomic Framework

Table 2: Poverty by Urban-Rural Areas and Sector of Employment, 2003 and 2006

Table 3: Estimates of Growth Elasticity of Poverty

TEXT BOXES

Box 1: Key Messages from Multistakeholder Consultations

Box 2: World Bank Group’s Response to the Global Economic Crisis

Box 3: One Bank Group: IFC-IBRD Integrated Programs

Box 4: Enhancing Conflict Sensitivity

Box 5: Governance Filters

Box 6: CAS Results Monitoring

TEXT FIGURES

Figure 1: Poverty Reduction in the Philippines versus East Asian Neighbors

Figure 2: Poverty Incidence versus Magnitude of Poverty, 1985 and 2006

CAS ANNEXES

Annex 1: Poverty, Inequality and Progress toward the MDGs

Annex 2: Governance Challenges, Opportunities and Risks

Annex 3: FY06-08 Country Assistance Strategy Completion Report

Annex 4: World Bank FY09 Client Survey and CAS Multistakeholder Consultations

Annex 5: FY10-12 Country Assistance Strategy Results Framework

Annex 6: Indicative World Bank Group (WBG) Program by Results Area

Annex 7: Official Development Assistance (ODA) Programs in the Context of the CAS

Annex 8: World Bank Group-Managed Trust Funds in the Philippines

Annex 9: Philippines Harmonization Agenda

Annex 10: Country Financing Parameters for the Philippines

CAS STANDARD ANNEX TABLES

Annex A2: Country At-A-Glance

Annex B2: Selected Indicators of Bank Portfolio Performance and Management

Annex B3: IFC Investment Operations Program

Annex B3 IBRD Indicative Financing Program, FY10-12

Annex B4 IBRD Indicative Program of Analytical and Advisory Activities, FY10-12

Annex B5: Philippines – Social Indicators

Annex B6: Philippines – Key Economic Indicators

Annex B7: Philippines – Key Exposure Indicators

Annex B8: Operations Portfolio (IBRD and Grants)

Annex B8: IFC Committed and Disbursed Outstanding Investment Portfolio

MAP OF THE PHILIPPINES (IBRD NO. 33466R3)

FY10-12 Country Assistance Strategy for the Philippines April 2, 2009

i

EXECUTIVE SUMMARY

i. The Philippines’ Development Challenges. In recent years, the Philippines’ economic

growth has rebounded on the back of fiscal consolidation, macroeconomic stability and a strong

international economic environment. Higher growth has, however, not translated into less poverty: the

share of the population below the poverty line is the same as it was a decade ago and has increased

between 2003 and 2006. Income inequality remains high, and the country risks missing MDGs on

education and maternal health. Weak governance is a recognized constraint to sustained growth and

poverty reduction. The country’s main development challenge, therefore, is to achieve more inclusive

growth. In the short- and medium-term, the external environment for the Philippines is likely to

deteriorate, and the country may face slower growth and renewed fiscal pressures. Furthermore, the

elections in 2010, typical of such elections, may slow down decision-making and program

implementation. At the same time, an incoming administration can be expected to engage with the

World Bank Group on the policies and initiatives it gives priority to.

ii. The World Bank Group Strategy. The updated 2004-10 Medium-Term Philippines

Development Plan (MTPDP) provides the framework for the Bank Group’s CAS for the Philippines.

The MTPDP focuses on economic growth and job creation; energy; education and youth opportunity;

and anticorruption and good governance. It highlights the need for agriculture sector modernization to

raise farmers’ incomes and to upgrade rural welfare; supports sustained investments in infrastructure;

and gives priority to protecting the poor through more employment opportunities, shelter, health

insurance, microfinance, low-cost medicines, and cash transfers. Over the CAS period, the World

Bank Group will contribute to achieving more inclusive growth by supporting the Philippines to (i)

maintain macroeconomic stability and cope with increased macroeconomic uncertainty through a

stronger revenue base, improved expenditure efficiency and targeting, and responsive financing; (ii)

improve the investment climate through an enabling business environment that promotes

competitiveness, productivity and employment, especially for sectors of particular importance to the

poor, such as agriculture and fisheries, and developing better models of infrastructure finance and

management; (iii) increase access to better public services for the poor by deepening the reform

agendas in key public services sectors and expanding basic service delivery directly to the poor; and

(iv) reduce vulnerabilities by expanding and rationalizing the country’s social safety net, improving

disaster risk management, piloting climate change adaptation measures and expanding climate change

mitigation programs. In line with the Bank’s country governance and anticorruption framework

(CGAC), the Bank Group will promote good governance as a cross-cutting theme by supporting more

capable and accountable government at the national, local, and agency level to strengthen core

governance systems in public financial management, procurement and decentralization.

iii. The World Bank Group Program. The Bank Group's program focuses on core results areas

through engagements at the national, local, and private sector level. The CAS proposes an IBRD

lending program in the order of US$700 million-US$1 billion per year, which would reverse the recent

trend of negative net transfers and could increase IBRD exposure to the Philippines from US$2.7

billion in FY08 to US$3.9 billion in FY12. The proposed lending plan is indicative as IBRD’s

capacity to lend can change over time. There is higher degree of certainty for the lending plans for the

earlier years of the CAS period. The IFC investment program is expected to be in the order of

US$250-300 million per year, while advisory services will be supported by funding of approximately

US$3 million per year. The Bank Group will support efforts to counter the effects of the global

economic crisis by financing faster-disbursing poverty alleviation programs such as the conditional

cash transfers (CCT), the community driven development (CDD) project KALAHI-CIDDS, the

national program support (NPS) for health and education, additional financing to ongoing operations,

and repeater projects. The Bank has committed to support a possible government program for

increasing revenues and fiscal transparency in calendar year 2009. Beyond current commitments for a

development policy loan (DPL) with a possible draw-down option to mitigate the impact of the global

economic crisis, the Bank will use development policy operations in support of disaster risk

FY10-12 Country Assistance Strategy for the Philippines April 2, 2009

ii

management and in the context of a strong reform program in government financial management. The

World Bank Group will also continue to support increasing local government access to finance

through more diversified financial instruments. IBRD investment loans and IFC investment and

advice will support the development of new models of financing and management for critical

infrastructure. IFC’s response to the global crisis will also include access to four financing facilities.

The World Bank Group, in collaboration with other development partners, will increasingly emphasize

knowledge cooperation and formalize a rolling knowledge program with the Government and in

partnerships with consortia of think tanks and universities. A central aim of the program for the CAS

period is to provide input into the MTPDP (2011-15) to be approved after the 2010 elections.

iv. One Bank Group. The Philippines CAS pilots deeper integration of IBRD and IFC efforts by

building on lessons of successful World Bank Group integration, such as a shared assessment and a

shared strategy developed jointly by a mixed IBRD and IFC team. IBRD and IFC will pursue joint

programs in three areas: infrastructure, agribusiness, and financial sector. MIGA will also continue to

offer its guarantee products, ensuring consistency with the overall Bank Group goals.

v. Implementing the Program. The World Bank Group will organize its Philippines program

and its country team along the lines of the four strategic objectives, one cross-cutting theme, and

eleven core results areas. For each of these, the Bank Group will organize, budget for, and monitor an

integrated program of AAA, lending, trust funds and partnership activities. The Bank will flexibly

adjust resource allocation among results areas depending on progress and emerging opportunities in

those areas. IFC’s resources will be integrated in the results areas that will be jointly pursued. The

Philippines Governance Advisory Team (PGAT) will prioritize activities in governance reforms, and

will advise task teams on governance improvements in specific activities, including through use of

―Governance Filters‖. The World Bank Group will strengthen existing partnerships with civil society

and academe and with other development partners within the overall framework of the Government-

led Philippines Development Forum, which the Bank co-chairs. In delivering the program, the World

Bank Group will pay special attention to strengthening the portfolio, improving lending efficiency,

furthering the knowledge agenda, and leveraging its resources through strategic partnerships and trust

funds. The Bank has identified, and agreed with the Government, a set of early ―Readiness Filters‖

that will be used to screen projects during the regular programming discussions.

vi. Managing Risks. There are considerable risks, both internal and external, that may affect

the implementation of the Philippines CAS. Political risks stem from the upcoming national elections

and associated transitions, which may influence commitment to ongoing and planned programs. The

World Bank Group will maintain dialogue with the administration to ensure continuity in its programs

and help inform the development agenda of the incoming government. The ongoing global recession

and financial turmoil is expected to affect negatively the Philippines, particularly through reduced

remittances, exports, and possibly, lower revenues. The World Bank Group, together with the IMF

and other partners, will assist the Government to manage fiscal and financial sector risks and external

vulnerabilities through policy advice and monitoring of economic and social developments including

through support for improved statistics. In case of a sharper-than-expected deterioration in the

economy, the World Bank Group stands ready to use IFC crisis facilities, and IBRD financing for

quick disbursing budget support within the broad parameters of the CAS lending range. The World

Bank Group support will proceed once there is clarity on agendas and commitments, and projects meet

the Bank’s processing filters. Commitment to governance reforms is a major focus of these filters,

including at the decentralized level.

Suggested Items for Board Discussion

(i) Is the CAS adequately positioned to help the Philippines cope with emerging global

uncertainties and likely shocks to economic management and prospects?

(ii) Is the proposed indicative program and choice of instruments appropriate, considering the

country circumstances and the Bank's comparative advantages?

(iii) Is the CAS approach to operationalizing governance sufficiently strong?

FY10-12 Country Assistance Strategy for the Philippines April 2, 2009

1

I. INTRODUCTION

1. The current World Bank Group CAS for the Philippines covers the period up to June

2009. It was discussed by the Bank’s Board in May 2005 and was originally planned to cover the

period FY06-08. The turn-around in the country’s fiscal position in the two years that followed the

preparation of the CAS opened a window of opportunity for broader policy reforms for the

Philippines. In 2007, the World Bank Group, in agreement with the Philippine Government, decided

to extend the CAS to June 2009. The CAS Progress Report prepared in June 2007 reaffirmed the

relevance of the CAS theme of Supporting Islands of Good Governance in national government

agencies, local governments, and dynamic sectors in the Philippines that demonstrate how improved

accountability and service delivery can lead to better economic and social outcomes. The Progress

Report also anticipated more Bank lending based on the increased fiscal space and government

demand for more Bank assistance.

2. Beyond the institutional requirement, the period of political transition lying ahead, the

rapidly deteriorating external economic environment, and the emerging shifts in the Bank

Group strategy provide the rationale for moving ahead with a new CAS. Launching a new CAS

in the first half of calendar year 2009 will allow the Bank Group one year of implementation before

the May 2010 elections, and would provide an opportunity to contribute to the new MTPDP 2011-15,1

the Government’s main guide for development policy. A CAS Progress Report in FY2011 would

allow the Bank Group to align priorities with those of the incoming government. At the request of

Government, the subsequent Bank Group CAS will be synchronized with the new MTPDP. Other

development partners have been closely involved in developing the CAS, and some expressed interest

in a joint Partnership Strategy beyond 2012.

3. The proposed strategy is grounded in the EAP Regional Strategy and the Bank Group’s

strategic themes. Many of the Bank Group’s current strategic priority agendas are relevant to the

Philippines. The country’s middle-income country (MIC) status, yet continuing high rates of poverty

and inequality; struggles with the effects of climate change; challenges to bring peace to areas of

enduring conflict; and requests for the Bank to bring to bear the best global knowledge all provide

clear links to the Bank’s strategic priorities and the core areas of EAP’s strategy, such as MIC agenda,

fragile/conflict states, global public goods, and the knowledge agenda.

II. PHILIPPINES CONTEXT AND DEVELOPMENT AGENDA

Social and Political Context

4. The Philippines is an archipelago of 7,107 islands located in Southeast Asia. With a

population of about 89 million in 2007, the Philippines is the world’s 12th most populous country. The

Philippines is the fastest urbanizing country in East Asia: fueled by in-migration and natural

population growth, the urban population has already passed the 50 percent mark and is expected to rise

to 75 percent of the country’s population by 2030. The country is divided into three island groups:

Luzon, Visayas, and Mindanao. Metro Manila, the capital, is the 11th most populous metropolitan area

in the world. A per capita GDP of US$ 1,624 in 2007 ranks the Philippines as a low-middle income

country.

5. The Philippines has a strong potential for development in terms of natural and human

resources, but overall development outcomes have fallen short of potential. The Philippines is

considered to be one of the most biologically rich and diverse countries in the world, with substantial

mineral, oil, gas and geothermal potential. Its human resource base is strong, with many leaders in

1 The Philippines National Economic and Development Authority (NEDA) has requested Bank Group inputs

into the next MTPDP, which will be completed after the 2010 elections.

FY10-12 Country Assistance Strategy for the Philippines April 2, 2009

2

Government, industries, and academe possessing world-class talents. The country has a vibrant

private sector and an active civil society, which are both important partners in development. Modern

productive sectors such as electronics manufacturing, business processing operations and

telecommunications have experienced rapid growth in recent years. The value of the country’s

English-speaking work force is reflected in the rapid growth of the business process outsourcing and

other services in the country, as well as in the international demand for its labor force and the resulting

high level of overseas employment.2 As of December 2007, around 8.7 million Filipinos, about 10

percent of the total population, were permanent residents or temporary residents/workers overseas,

with annual remittances reaching US$14.4 billion, or more than 10 percent of the country’s GDP.

However, the country has seen a relative decline in its income per capita compared to its neighbors

since the 1950s, when it was second only to Japan. Compared to its ASEAN neighbors, the

Philippines has exhibited higher unemployment rates and greater income inequality.

6. The next Philippine general elections are scheduled to be held on May 10, 2010. At the

national level, the presidency, vice-presidency, half the Senate seats, and all House seats are up for

election. In addition, all provinces, cities and municipalities (including 41,995 barangays), will also

hold elections. Current President Gloria Macapagal-Arroyo came to power in 2001 after she, as then

vice president, replaced then-President Estrada who was forced to leave his post amid popular protests

and pending impeachment procedures against him on the grounds of alleged corruption. He was later

convicted of plunder, and subsequently pardoned. The current president was elected in 2004 in a

victory that has been contested by some parties and civil society coalitions. President Arroyo faced

two attempted military coups, several impeachment attempts, and repeated widespread popular

protests against her rule, but she retains strong support in the House of Representatives and among a

majority of governors and mayors. Several high-profile corruption cases involving political figures

remain unresolved. A debate on possible changes in the constitution for several reasons, including a

possible second term for a president and a change to a parliamentary system of democracy, is a

recurrent theme in Philippine politics.

7. Weak incentives embedded in the country’s political institutions may continue to

hamper reforms. The fragmented political structure and politicization of the government

bureaucracy is seen as one of the constraints to promote and implement reforms. In recent years, a

number of reforms to strengthen the institutional capacity of the state have been launched, often with

strong support from civil society. The work of civil society, both in advocacy and in project

implementation and monitoring, has contributed to the successful promotion of specific reforms,

especially in the fields of procurement, textbook delivery, budget transparency, community

infrastructure, etc.

8. Weak governance has long been recognized as a key constraint to sustained growth and

poverty reduction in the Philippines. In the MTPDP 2004-10, the Government diagnosed various

governance challenges, ranging from the lack of independence, capacity and integrity of government

institutions, and regulatory capture, to built-in checks and balances that allegedly tended to slow down

policy-making and policy implementation. The Plan attributed the limited effectiveness of the

government bureaucracy to the pernicious influence of vested interests and a system of patronage.

Recognizing these challenges, the Government embarked on reforms on a number of fronts, including

anticorruption efforts and bureaucratic reforms. Similarly, a variety of civil society organizations have

engaged in advocating and/or supporting governance reforms of various kinds. At the local level,

some commentators have observed the prevalence of patronage politics, with consequent implications

for poor provision of public services. At the same time, a growing number of local leaders have

2 Some would argue that the large number of migrant workers is a mixed blessing. On the one hand, their

remittances bring in much-needed foreign exchange, but on the other they reflect the incapability of the domestic

economy to generate sufficient number of jobs, their remittances keep the real exchange rate high, so export

oriented industries develop more slowly, and their absence from home delays the formation of a domestic middle

class that in other countries is considered to be instrumental in developing stronger governance.

FY10-12 Country Assistance Strategy for the Philippines April 2, 2009

3

demonstrated good governance and effective management. The challenge is how to expand these

innovations and scale them up to benefit more people across more local governments.

Recent Economic Developments

9. Philippine economic growth during 2000-08 averaged around 5.1 percent. Economic

growth picked up gradually from 2002 to 2007 when it peaked at 7.2 percent—the highest growth in

three decades—and slowed down to 4.6 percent in 2008 as the twin shocks of the food and fuel crisis

and global slowdown took their toll on the economy. Notwithstanding the improved growth

performance, the Philippines growth has been noticeably below other developing East Asian countries,

which grew at an average of 8.7 percent during 2000-08. With population growth at more than 2

percent per annum in the Philippines, growth in per capita income has also been lower relative to most

of its neighbors.

10. Growth during the period was driven by private consumption and the services sector.

Demand growth was largely driven by consumer spending, with public sector expenditures more

recently providing an extra boost. In recent years, around 70 percent of the growth can be attributed to

private consumption, supported in part by growing overseas Filipino workers’ remittances. The

services sector comprises more than half of GDP and employs more than half of the workforce. The

contribution of private investment to GDP growth, at around 5 percent during 2004-08 has been

relatively weak. During 2004-06, the Government focused on fiscal consolidation and reforms which

entailed a cut in public investment expenditures, and the contribution of the public sector to growth

was around negative 3.6 percent. Since then the significant progress made in fiscal consolidation,

together with hefty privatization receipts, permitted the Government to increase spending.

11. In 2008, growth slowed down to 4.6 percent as higher oil and food prices and the onset of

the financial crisis reduced real incomes and slowed the growth of private consumption,

investments, and exports. In the first half of 2008, public sector spending lagged, and contracted in

real terms. In May, the Government announced that, in response to the increases in oil and food

prices, it intended to postpone its balanced budget goal to allow for higher spending on infrastructure,

social protection, and subsidies to the poor. Public spending, in particular infrastructure spending,

accelerated in the second half and buoyed overall growth. The relatively weak demand has resulted in

slower growth of the services sector. Inflation, which had been falling over the past few years and

averaged only 2.8 percent in 2007, rose sharply in the first half of 2008, peaking at 12.5 percent in

August 2008, but receded almost as quickly to 7 percent in January 2009. However, the inflation

faced by the poor, especially the urban poor, is estimated to be about 2 to 3 percentage points higher

given the high share of food in their consumption basket (up to 70 percent). Food prices rose sharply

through 2008—rice prices, in particular, rose by almost 50 percent.3

12. The balance of payments position weakened, following several years of strong

performance, but remained in surplus. The higher oil and food prices in 2008 increased the import

bill, while the global slowdown began to take its toll on exports. Remittances, however, still remained

robust in 2008, keeping the current account in moderate surplus. Direct investment inflows have

diminished but remain positive. Portfolio investment was more adversely affected by the financial

market turmoil and global risk aversion. Nonetheless, the overall balance of payments remained in

surplus in 2008 and enabled the country to continue to accumulate international reserves.

13. As in other emerging markets, the Philippines has seen a decline in stock market and

asset prices, higher spreads on its international bonds, and a depreciation of the currency

against the US dollar. Following the strong appreciation of the peso in 2007, the currency

depreciated by about 15 percent against the US dollar during 2008, despite interventions by the central

3 It is estimated that the food crisis may have pushed up the poverty incidence by 3.2 percentage points and is

equivalent to 2.7 million more poor people during the height of the food crisis. Lower inflation since September

of last year is likely to have reversed some of this increase.

FY10-12 Country Assistance Strategy for the Philippines April 2, 2009

4

bank. Stock market prices have nearly halved since the end of 2007, a decline comparable to that in

other East Asian economies. Meanwhile, spreads on international treasury bonds issues increased by

around 500 basis points. Nevertheless, the Philippines successfully issued a US $1.5 billion

international bond in January 2009, as the first Asian country to return to the international markets

after the September 2008 crash, giving off an important signal of confidence in the country and the

region.

14. So far the impact of the global financial turmoil on domestic financial markets has been

relatively contained. The Philippines’ direct exposure to distressed credit products appears to be

limited. Overall exposure to structured products is estimated at about 2 percent of banking sector

assets and a sizable portion have provisions for loss. A key vulnerability to the turmoil in the global

financial markets arises from its still relatively high stock of public sector debt. About one-third of

Philippines foreign currency denominated debt is held by domestic banks, which makes them

vulnerable to global re-pricing of risks and interest rate increases. However, the banks appear to have

appropriate cushions to weather the shocks—with reported capital adequacy ratios of over 14 percent

as of the first half of 2008 and declining non-performing loan ratios. Moreover, recent changes in

accounting rules cushion the impact on capital of bank losses on their investments. Nevertheless, bank

profits, though positive, have fallen significantly.

Macroeconomic Prospects

15. Macroeconomic prospects for 2009 and 2010 have clearly become less favorable than the

preceding CAS period. Overall, the economy is in a stronger position than before to weather the

uncertainties brought about by the recent turmoil. The fiscal reforms and current account surpluses of

the last few years have served to improve investor confidence and boost the level of international

reserves. Nevertheless, the Philippines will be affected by the projected slowdown in the global

economy and growth is likely to slow considerably given the country’s high degree of trade and

capital openness. Weaker domestic demand due to lower real income, rising unemployment and

underemployment, slowing remittances, and falling exports of key products such as electronics are

expected to limit growth severely in 2009 with only a very gradual recovery in sight in 2010 (see the

base-case projections in Table 1). At this stage, risks for further slowdown remain real.

16. Over the medium- to long-term, economic growth is projected to recover to around 5

percent. Its sustainability, however, will depend on further progress in structural reforms. In

particular, turning around low investment and productivity are essential for sustaining economic

growth. Domestic investment as a share of GDP is expected to fall in 2009 due to tighter global credit

and financing conditions, followed by a gradual recovery in response to future improvements in

governance and the investment climate.

17. The current account of the Balance of Payments is projected to remain in surplus in the

near term. Under the current assumption that the global economy may take up to two years to

recover, exports are expected to contract significantly before improving while the import bill would

also contract given the high content of electronics parts and falling commodity prices. Slower exports

and imports would lead to a lower trade deficit in the near-term followed by an increase in the trade

deficit as imports pick up again. Exports of manufactured goods, dominated by highly cyclical

electronics, remain vulnerable to global demand conditions. While the growth in remittances is

expected to slow significantly, remittances are nonetheless expected to remain relatively strong,

because a sizable share of the migrants is employed in sectors (such as health care) that may be less

vulnerable to cyclical downturns. This is expected to help keep the current account in surplus. A

current account deficit might arise in the long-term however, should export competitiveness lag,

commodity prices increase, and growth in remittances declines further.

18. The global uncertainties and risks will continue to pose threats to net investment inflows. Net inflows of direct investments are expected to be minimal this year and next. Over the medium

term, attracting significant inflows of FDI will depend on further improvements in the investment

FY10-12 Country Assistance Strategy for the Philippines April 2, 2009

5

climate. Consistent with global financial volatility, net portfolio investments are expected to be

minimal as well. The net outflow in 2008 could be reversed if the interest rate differential rises in the

coming months and if global prospects become less pessimistic. Overall, though, the combined

strength of the current, and capital and financial accounts would still contribute to further reserve

accumulation in the medium-term.

Table 1: Philippines – Key Macroeconomic Indicators and Projections

(As percentage of GDP, unless indicated otherwise)

2005 2006 2007 2008 2009 2010 2011 2012 2013

Est.

Output and Prices

GDP growth (% Δ) 5.0 5.4 7.2 4.6 1.9 2.8 4.0 4.5 5.0

CPI Inflation (ave, % Δ) 7.6 6.2 2.8 9.3 4.5 4.0 4.0 4.0 4.0

REER (% Δ, + = apprec.) 5.9 11.8 8.8 7.6 … … … … …

Savings and Investment

Gross Domestic Investment 14.6 14.5 15.3 15.3 14.9 15.1 15.5 15.8 16.1

Gross National Savings 16.6 19.0 19.7 17.7 16.9 16.4 16.6 16.7 16.6

Balance of Payments

Current Account Balance 2.0 4.5 4.4 2.4 2.0 1.3 1.1 0.9 0.5

Trade Balance -7.9 -5.7 -5.7 -6.4 -6.9 -7.2 -7.4 -7.6 -7.8

Exp. (merchandise fob) 40.7 39.6 34.2 28.4 25.8 25.4 25.1 25.2 25.7

Imp. (merchandise cif) 48.6 45.3 40.0 34.8 32.7 32.5 32.5 32.9 33.4

Foreign Direct Investment 1.7 2.4 -0.4 0.6 0.1 0.3 0.6 0.8 1.0

Public Sector Finances

Consolidated Pub. Sec. Balance -1.9 0.2 0.6 -0.5 -1.5 -2.0 -1.9 -1.9 -1.8

National Government balance -2.7 -1.1 -0.2 -0.9 -2.3 -2.3 -2.2 -2.0 -1.9

Primary balance 2.8 4.1 3.8 2.7 2.7 1.6 1.6 1.7 1.8

Total Revenues 15.0 16.2 17.1 16.0 15.0 15.0 15.0 15.2 15.4

o/w Tax revenues 13.0 14.3 14.0 14.0 13.3 13.4 13.6 13.9 14.1

Total Expenditures 17.7 17.3 17.3 17.0 17.2 17.3 17.2 17.2 17.3

Net Interest 5.5 5.1 4.0 3.6 3.9 3.9 3.9 3.8 3.8

Debt

Non-Financial Public Sector Debt 85.9 73.9 61.1 63.3 64.1 63.1 61.7 60.7 59.0

External Debt 1/ 62.4 51.3 45.7 39.9 42.3 40.3 38.1 36.6 35.1

Memorandum item:

Nominal GDP (billions of US$) 98.8 117.6 144.1 168.6 161.3 167.4 177.5 189.3 202.9

Soures: Government of the Philippines and World Bank staff calculations

1/ Based on The World Bank's definition

----------Actual---------- -------------------Projected-------------------

19. In response to the global economic slowdown, the Government has prepared an

economic resiliency plan to stimulate the economy. In February 2009, the Government announced

a stimulus package of Php330 billion of which about Php200 billion is estimated to come from a 15

percent increase in national government spending and from previously scheduled tax cuts. This is to be

complemented by about Php100 billion in contributions from government financial institutions, social

security institutions (SSIs), and private banks to fund additional infrastructure projects. The balance of

about Php30 billion is to come from the Social Security System in the form of new and temporary

extra benefits to members. The Plan indicates the Government’s intention to: (a) front load spending;

(b) shift resources from slow to fast-moving projects; and (c) implement/upscale quick-disbursing high

impact projects. Implementing agencies are expected to spend 60-80 percent of their calendar year

2009 discretionary budget totalling 1.2 percent of GDP in the first half of 2009.

20. The public sector’s fiscal position is expected to remain manageable, but fiscal risks

could materialize. For 2009, the Government projects a deficit of about 2.1 percent of GDP. Tax

FY10-12 Country Assistance Strategy for the Philippines April 2, 2009

6

collections this year will be more challenging because of several policy measures already taken4 and

lower oil prices. In the absence of new measures, tax revenues as a share of GDP are projected to

decline well below the ratio achieved in 2008. Under these circumstances, reforms to improve tax

administration will be critical for keeping the deficit within sustainable levels. A further source of risk

is the gross financing needs of the non-financial public sector, which are large and rising, thereby

generating significant rollover risk (18.5 percent of GDP in 2009 and 19.7 percent of GDP in 2010).5

With considerably higher and more volatile interest rates in the domestic and international capital

markets, financing such large amounts could become more challenging.

21. The public sector debt-to-GDP ratio is projected to continue to fall over the medium-

term, in spite of the global financial turmoil. Non-financial public sector debt fell from over 100

percent of GDP in 2003 to about 62 percent of GDP in 2008. This ratio is projected to fall further over

the coming years, albeit at a markedly slower pace. While the projected pace of decline is sensitive to

various macroeconomic parameters, especially GDP growth and the exchange rate, the overall trend of

a declining debt burden is broadly robust to various scenarios.

Poverty Profile and Trends

22. The Philippines has made significant progress in the fight against poverty over the last

two decades. The share of the population living below the national poverty line, which almost reached

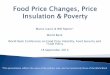

50 percent in the mid-1980s, was brought down to less than a third in recent years (Figure 1)6. Poverty

measured using the international benchmark shows a similar trend. The proportion of the population

living below US$1.25-a-day declined from 34.9 percent in 1985 to 22.6 percent in 2006, or a reduction

of about 2 percent per year over the two decades. While significant, these gains are lower than those

recorded in some neighboring countries, particularly Indonesia, Thailand, Vietnam, and China.

Moreover, the absolute number of the poor based on the $1.25/day poverty line increased from 18.5

million poor people in 1985 to 19.7 million in 2006.

Figure 1: Poverty Reduction in the Philippines versus East Asian Neighbors

Phil

Phi Off'l

Indo

Rural China

Viet

Thai

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

mid-1980 mid-1990 early-2000 2006 (latest)

Povert

y I

ncid

ence (

%)

Note: Figures refer to the proportion of the population with income per capita below the new

international benchmark of US$1.25 a day in 2005 Purchasing Power Parity, except Philippine official

poverty incidence which is based on national poverty lines.

Sources: World Bank and NCSB

4 These included the 5 percentage point reduction in the corporate income tax rate, a full year impact of the

personal income tax threshold increase, and tax exemptions arising from personal equity and retirement account. 5 IMF Article IV Consultations 2008.

6 Data used in the analysis reflect the latest government and Bank staff estimates and may differ from Annex A2

and Annex B5, which present data from the DECDG database and other standard sources.

FY10-12 Country Assistance Strategy for the Philippines April 2, 2009

7

23. Income poverty hardly fell in recent years. The latest estimates show that between 2003

and 2006 income poverty as measured against the country’s own poverty line increased from 30

percent to 32.9 percent, back to its level in 2000. The incidence of poverty based on alternative

measures of the poverty line also show similar increases during that period, consistent with the official

statistics. Between 2003 and 2006, the US$1.25-a-day poverty increased from 22 percent to 22.6

percent7, and consumption-based poverty estimates increased from 26 percent to 28.1 percent

8.

Furthermore, self-rated hunger indicators showed steady increase since 1998 and rose to an all-time

high of 19 percent by the end of 20069.

24. Non-income dimensions of poverty and welfare are lagging behind, specifically in health

and education. The latest statistics show that the Philippines has made good progress in reducing

child mortality, combating tuberculosis and other diseases, improving access to water and sanitation,

and protecting the environment, but has done poorly in achieving universal primary education and

maternal health (see further analysis of progress in achieving MDGs in Annex 1).

25. Regional poverty rates vary significantly. Although the national poverty rate increased

between 2003 and 2006, official estimates of poverty declined in four of the country’s 17

administrative regions. Poverty declined in three regions in Mindanao: Zamboanga from 49.2 percent

to 45.3 percent, Caraga from 54 percent to 52.6 percent, and Northern Mindanao from 44 percent to

43.1 percent. Poverty in Western Visayas also declined from 39.2 percent to 38.6 percent. In contrast,

poverty headcounts in the other 13 regions increased in 2006 compared to 2003. In particular, poverty

in conflict-affected Autonomous Region of Muslim Mindanao (ARMM) swelled by almost 10

percentage points (to 61.8 percent).

26. Poverty remains predominantly a rural phenomenon in the Philippines, but urban

poverty is on the rise. In 2006, about three-quarters of the poor resided in rural areas (Table 2).

Estimates also show that rural poverty increased (although marginally) between 2003 and 2006 and

that poverty among agricultural households is about three times higher than poverty in other sectors.

While rural poverty remains more than double that of urban poverty, the share of urban poor to total

poverty has been increasing since 2000 due to rapid urbanization and inequitable income distribution.

Between 2003 and 2006, the share of the poor population living in the urban areas increased from 23.2

percent to 28.8 percent. With rural-urban migration and rapid population growth, this trend can be

expected to continue over time unless rapid urbanization is accompanied by better income distribution.

Table 2: Poverty by Urban-Rural Areas and Sector of Employment

Poverty Headcount (%) Share to Poverty (%) Share to population (%)

2003 2006 2003 2006 2003 2006

Area

Urban 14.2 19.3 23.2 28.8 49.1 49.3

Rural 45.5 46.2 77.0 71.2 51.0 50.7

Sector of Employment of the Household Head

Agriculture 53.6 55.5 66.5 59.4 37.4 35.3

Industry 23.1 28.8 11.9 12.7 15.5 14.4

Services 14.2 18.8 16.3 20.2 34.7 35.4

Not Employed 13.1 17.1 5.4 7.7 12.5 14.9

Total 30.0 32.9 100.0 100.0 100.0 100.0 Source: World Bank staff estimates based on official poverty lines for 2003 and 2006; FIES 2003 and 2006.

7 Chen, S. and M. Ravallion (2008). ―The Developing World is Poorer than We Thought, But No Less

Successful in the Fight Against Poverty.‖ 8 Balisacan, A. (2008). "Poverty Reduction: What We Know and Don't?" University of the Philippines

Centennial Lecture Series. 9 Social Weather Stations (July 2008). Report on Self-Rated Poverty and Hunger.

FY10-12 Country Assistance Strategy for the Philippines April 2, 2009

8

27. High levels of inequality partly explain why growth translated into limited poverty

reduction. The country’s Gini coefficient remains high relative to its neighbors in the region (45.8

percent in 2006), and large variation in economic opportunities persist at the sub-national level.

Geographically, the National Capital Region and two adjacent regions, which account for more than

half of GDP, have above average per capita income and have seen the fastest decline in poverty

headcount. In contrast, per capita incomes in the poorest regions (ARMM and Caraga), are only 50-60

percent of the national average. Estimates suggest that the Philippine's growth elasticity of poverty is

greater than unity, but has been declining in recent years (Table 3)10

. Between 1985 and 2000 when

growth averaged 3 percent per year, poverty declined by about 2.2 percent annually. In the period

2000-2006, when the country posted about 5 percent growth per year, the pace of poverty reduction

dropped to 0.1 percent per year.

Table 3: Estimates of Growth Elasticity of Poverty

Data Years World E. Asia CHN INDO PHL THA VNM

Besley and

Burgess (2003)

Varies by country

(1980-1998)

-0.73

(0.24)

-1.06

(0.25)

-0.60

(0.14)

-1.12

(0.38) -0.70

(0.12)

-1.72

(0.48)

World Bank

(2008)*

1990-2000

-2.12

(0.42)

-1.20

(0.14)

-2.60

(0.74) -1.85

(0.21)

-5.15

(0.46)

-2.13

(0.10)

World Bank

(2008)*

2000-2006

-2.19

(0.34)

-1.29

(0.07)

-1.85

(0.36) -1.27

(0.45)

-4.55

(0.81)

-3.04

(0.18)

* Fujii and Velarde (forthcoming)

28. High population growth may have slowed poverty reduction efforts over the past two

decades. While the trend in poverty incidence has generally been downward over the years, the gains

in poverty reduction may have been affected by the country’s high population growth, which averaged

about 2.2 percent, compared to less than 2 percent in neighboring countries like Indonesia, Vietnam,

and Thailand. Rapid population growth puts high demand on education and health services, and on

the economy’s capacity to generate jobs. Recent growth has generated more jobs, but not enough to

absorb the increase in the working-age population. Consequently, even though the share of population

living in poverty declined from nearly half of the population in 1985 to only one-third in 2006, the

absolute number of poor increased from 26.2 million to 27.6 million (Figure 2).

Figure 2: Poverty Incidence versus Magnitude of Poverty, 1985 and 2006

27,61726,231

32.9%

49.3%

-

20.0

40.0

60.0

1985 2006

Inci

den

ce (%

)

-

10,000

20,000

30,000

40,000

Mag

nitu

de

('000

)

Magnitude of poor population

Poverty incidence of Population (%)

Note: Figures refer to official poverty estimates that are not directly comparable across time

but they give a consistent trend with the $1.25/day poverty estimates.

Source: NSCB

10

See also Ravallion, M. (2001). ―Growth, Inequality, and Poverty: Looking Beyond Averages.‖ World

Development, 29: 1803-15; and Cline, W.R. (2004). "Technical Correction" in Trade Policy and Global Poverty,

Institute of International Economics, Washington DC.

FY10-12 Country Assistance Strategy for the Philippines April 2, 2009

9

29. It is estimated that 45 percent of Filipinos are vulnerable to poverty11

, and that half of

poor households became poor because of an income shock12

. For example, the sharp increase in

food prices between July 2007 and July 2008 is estimated to have increased poverty incidence by 3.6

percentage points, an additional 3 million people. Household spending patterns shed light on their

degree of vulnerability to shocks. An average household spends 41 percent on food, making them

highly susceptible to falling into poverty with sudden increases in food prices, and only 2.9 percent on

health and 4.4 percent on education of its total expenditures. The poor, meanwhile, spend even more

on food (60 percent) and less on health (1.4 percent) and education (1.7 percent) making them more at-

risk to future shocks and less equipped to exit poverty. Some of the factors that drove the increase in

poverty in recent years are further discussed in Annex 1.

Philippines Development Challenges and Opportunities

30. The proposed new CAS for the Philippines will be addressing many of the same

development challenges that the country has been struggling with for decades. The country’s

main achievement over the past years has undoubtedly been the hard-fought improvements in the

country’s fiscal position and resulting macroeconomic stability and higher growth rates. Yet, poverty

is proving to be relatively insensitive to growth in the Philippines and has even drifted upwards in

times when the highest economic growth in three decades was recorded. Indeed, in absolute numbers,

the Philippines now has more people in poverty than three decades ago. While public investments

have started to increase again, supported by growing fiscal space, private investment continues to be

lackluster in an investment climate that many consider as weaker than that of most of its neighbors.

And while rising budget allocations to and recent progress in reforms in the social sectors promise

better services, for now the Philippines is at risk of missing its targets on basic education and maternal

health. Many observers in the Philippines see weak governance as an underlying cause in all of these

development challenges, even though some notable progress has been made in this area—progress,

which was on occasion overshadowed by headline grabbing corruption scandals.

31. Ensuring sustainable growth in the Philippines will require addressing the key

challenges to progress on critical structural reforms. Recent improvements in macroeconomic

management, especially fiscal consolidation, will need to be put on a sustainable and permanent

footing by improving tax administration and tax policy on the revenue side, as well as by improving

expenditure management and the management of fiscal risks. Underinvestment in infrastructure, and

the poor quality and maintenance of services, transport in particular, limit overall competitiveness,

increase the cost of doing business, and adversely affect trade-related transactions. Private sector

development is further impeded by a constrictive policy and regulatory environment, particularly in

areas such as rice trade where policies favor the public sector; inter-island shipping and port services;

land administration and management; and access to credit. Strengthening the investment climate,

improving the policy and regulatory framework, and creating a more competitive financial sector will

provide opportunities for enhancing productivity and ensuring sustainable and broad-based longer-

term growth. Given the decentralized nature of the country, much of the reforms (including revisions

of local fiscal and revenue authority, and the Local Government Code) and improvements will need to

be at the local government level, in particular, in the large and expanding urban areas.

32. While considerable progress has been made in human development outcomes, achieving

some of the key Millennium Development Goals (MDGs) remains a major challenge. The

country is on track to halving poverty by 2015 (the proportion of the population living below the

national poverty line is down to a third), and has made good progress on reaching the MDGs on

nutrition, gender equality, reducing infant and child mortality (infant mortality fell to 23 per thousand

live births in 2006 from 57 in 1990; under-five mortality in 2006 fell to 31 per thousand live births

from 80 in 1990), water supply and sanitation, and combating AIDS and other diseases. However, the

11

NAPC and NSCB (2005). "Assessment of Vulnerability to Poverty in the Philippines." 12

Reyes, C. (2002) "The Poverty Fight: Have We Made an Impact?"

FY10-12 Country Assistance Strategy for the Philippines April 2, 2009

10

net enrolment rate (NER) for elementary education has been falling, and that for secondary education

is stagnating at a low 58-60 percent, whereas completion rates at both levels were declining until 2006.

Despite a decline from 209 per hundred thousand live births in 1990 to 162 in 2006, maternal

mortality remains high. Achieving the MDGs for primary education and maternal mortality remain

major challenges and are increasingly unlikely to be met. The incidence of malnutrition is also an

issue. There are significant opportunities to improve the efficiency of increasing budgets in the social

sectors, as well as further raising allocations as efficiency and fiscal space improve.

33. There are significant inequalities in the access to basic infrastructure and social services

by regions and income groups. Income disparities at the sub-national level translate into

significantly lower access to vital infrastructure services such as electricity, water supply, paved roads,

and telephone service. Less prosperous regions, mostly in Mindanao, have much lower levels of

access. Gaps are also largest in urban areas where many poor households often lack access to services

due to their informal status. There are also persistent gaps in educational and health outcomes, as well

as access to good quality schools and health services and inputs, between poor and non-poor areas, and

between poor and non-poor families.

34. A key feature of the recent Philippines’s economic story has been the weak response of

poverty reduction to income growth and persistent vulnerability. Official estimates show that

nearly half of the population is vulnerable to falling into poverty as a result of shocks, including rising

prices. Analyzing and understanding the causes and nature of poverty are critical to responding to the

challenge of how the poor can better benefit from growth. Factors for the disconnect between growth

and poverty reduction include the impact of cumulative inflation on real incomes of households; the

compression of public expenditures, including both infrastructure and social spending, in the face of

unsustainable budget deficits in the early years of this decade; the quality of growth which accrued

largely to the corporate sector compared to households; and, insufficient job creation for low skilled

labor with growth favoring the services sector. Poverty is also driven through the nexus with the

environment and climate change, as well as with natural disasters. A poorly coordinated and

inaccurate social protection system further reduces the effectiveness of poverty targeting programs.

35. The overarching and cross-cutting challenge of weak governance remains a key

constraint to sustainable growth and poverty reduction. The Government recognizes this

challenge and there has been considerable progress in strengthening the overall framework for good

governance. Governance reforms have encompassed anticorruption drives, bureaucratic reforms,

strengthening of public procurement and fiduciary processes, promotion of local government

oversight, and the engagement of strong civil society groups, communities, and lawmakers in

providing checks and balances. For example, following up on the findings of an INT investigation of

the first phase of the National Roads Improvement Program, the Government and the World Bank

designed for the second phase of the project a battery of stringent anti-corruption measures and

governance mechanisms, such as the use of independent procurement evaluation, tighter procurement

controls, building the agency’s capacity for internal audit, and independent monitoring by a civil

society group. An example of the Government’s recent administrative reform efforts is Oplan

Kandado (Operations Padlock) launched in January 2009 and aiming to strictly enforce administrative

sanctions for noncompliance by taxpayers. However, governance challenges continue to overshadow

these achievements. Key challenges include the need to further strengthen public institutions and make

them more accountable and transparent; intensify the demand and political impetus for reforms; and,

consolidate and expand the engagement of the vibrant civil society. See further analysis in Annex 2.

36. Finally, the conflict-affected areas in Mindanao pose a particular challenge. The

decades-long intermittent conflict between government forces and separatist groups have resulted in

loss of life and displacement of people, destroyed infrastructure, slowed development, below-average

human development, and stagnating economic outcomes far below potential in the affected regions.

This potential is somewhat evident in the island’s growth centers where there is relatively better

economic performance. The World Bank Group, along with many other development partners, has

FY10-12 Country Assistance Strategy for the Philippines April 2, 2009

11

been supporting development activities in Mindanao, but the various short-term initiatives need to be

better coordinated to result in improved outcomes and more sustainable longer-term development.

37. Addressing the country’s development challenges is likely to become more demanding in

the coming CAS period. As for most developing countries, the external environment for the

Philippines is deteriorating rapidly and is likely to be less benevolent in the coming years. Although

better prepared than in the past, and better prepared than some other middle income countries, the

Philippines is likely to face slower growth in the years ahead, and renewed fiscal pressures are already

emerging. The country needs to manage these additional pressures in times of political change. The

elections scheduled for May 2010 offer risks as well as opportunities: on the one hand, elections in the

Philippines traditionally slow down decision making, reform initiatives and program implementation.

On the other hand, though, the upcoming elections offer an opportunity for a renewed political

mandate for the incoming administration, the potential for new policy directions, and new coalitions

for needed reforms. The baseline expectation therefore is that the CAS will operate in a rapidly

changing and often challenging political environment.

Updated 2004-10 Medium-Term Philippines Development Plan (MTPDP)

38. With a fresh mandate in 2004, the Government outlined the country’s MTPDP for the

period 2004-2010 with a macroeconomic framework designed to maintain economic stability. Starting in 2005, the Government implemented crucial reforms to improve tax collection, increase

revenues and prudently manage expenditures. Fiscal reforms resulted in stabilized public finances,

large prepayments and lesser dependence on external borrowings. Consequently, the budget deficit

was contained, in turn resulting in lower interest rates. Record levels of overseas remittances coupled

with increasing export earnings led to an improvement in the country's credit outlook. These further

attracted foreign investments and boosted the peso's strength. Hence, an economy once struggling to

recover after the Asian crisis began to show a turn-around in 2007. However, the momentum receded

by mid-2008 in the wake of global shocks: soaring food and fuel prices, and a downturn in the U.S.

economy.

39. The MTPDP was updated in 2008 to review past performance, attend to remaining

commitments in the Plan, and reformulate policies to address the new challenges. The update

was undergoing final review during the CAS preparation time. The updated MTPDP focuses on the

areas of: economic growth and job creation; energy; education and youth opportunity; and

anticorruption and good governance. It highlights the need for the agriculture sector to become more

competitive in view of the liberalized global economy and stresses the need to decentralize

development by decongesting Metro Manila through the establishment of new centers of government,

business and housing in Luzon, Visayas and Mindanao. It aims for the nation to become more self-

reliant in its energy mix, becoming a world leader in renewable energy. It puts new emphasis on

science, technology, and innovation, and speaks of boosting the outsourcing industry and establishing

regional ICT centers. The MTPDP supports sustained investments in infrastructure, pursuing an urban

rail-based mass transport system, and linking the islands via more Roll-on-Roll-off ports. It highlights

actions to manage inflation, as well as to address the relatively high rates of unemployment and

underemployment. The Plan gives priority to protecting the poor through more shelter, health

insurance, microfinance, low-cost medicines, and cash transfers.

40. The overall goals of the MTPDP provide the country framework for the Bank’s CAS for

the Philippines. The CAS will be broadly aligned with the themes under the updated MTPDP, and

will serve as early input to the next MTPDP that is to be approved by the incoming government after

the 2010 elections. At the Government’s request, the Bank will provide input in the preparation of the

new plan that is expected to start in the coming year. Given the possibility of a shifting focus with the

change of administration after elections, the alignment will be measured in terms of adequate

responsiveness to changing client requests, within a selective framework that focuses on areas in

which the Bank can best serve the country’s development and poverty reduction goals.

FY10-12 Country Assistance Strategy for the Philippines April 2, 2009

12

III. BANK GROUP ASSISTANCE STRATEGY FOR THE PHILIPPINES

A. LESSONS LEARNED FROM FY06-09 CAS AND STAKEHOLDER FEEDBACK

Lessons from FY06-09 CAS Completion Report

41. The FY06-09 CAS Completion Report (Annex 3) presents an assessment of the strategy

that aimed to achieve fiscal stability, generate economic growth, ensure social inclusion and

improve governance. The following lessons have been learned that have implications for the design

and implementation of next FY10-12 CAS:

The overall strategic direction of the CAS was sound. Sound fiscal management and

improved governance will continue to be critical for ensuring sustained economic growth and

poverty reduction. The next CAS will need to ensure that the gains made in revenue

generation, public expenditure management, and procurement are sustained while pursuing

further improvements in governance. Continued focus on implementing the project portfolio

will be critical to success during the next CAS. Going forward, the Bank will need to

understand better the factors explaining the relationship between the country’s economic

performance and lack of poverty reduction, and ensure that Bank-supported operations

emphasize the needs of the poor.

Continued engagement is a critical element for success, but at the same time the Bank

needs to develop criteria for strategic and selective engagement. The Bank has a long

history in the Philippines and has been able to develop relationships and trust with many

government agencies, which has enhanced the Bank’s effectiveness. The Bank would need to

build on these relationships with counterparts in pursuing results during the next CAS.

However, the Bank, jointly with the Government, would need to be strategically selective and

develop criteria to determine when the Bank should disengage given the extent of current

engagements and Bank resource constraints.

Monitoring (and evaluation) of AAA needs to be strengthened. Knowledge transfers are

an important part of the Bank engagement with the Philippines. But the Philippine program

has not been adequately monitored and the possible impact of its AAA program has not been

assessed. There also needs to be a stronger link between the Bank’s AAA program with that

of the priority analytical study needs of the Government.

The CAS results framework needs to be strengthened. The FY06-08 CAS results

framework has not proven useful in monitoring, managing and evaluating the CAS. The Bank

can make the results framework into an effective CAS management, monitoring and

evaluation tool by clearly stating the expected CAS outcomes, including specific, measurable,

achievable, relevant and time-bound indicators to allow for better monitoring, and making

explicit the link between expected CAS outcomes and Bank instruments. Linking CAS

monitoring and operational (including AAA) monitoring would facilitate data collection.

Closer strategic monitoring of progress towards CAS strategic objectives should facilitate

decisions on engagement. These lessons have been reflected in the new results framework.

Findings from Recent IEG Evaluations

42. The Independent Evaluation Group (IEG) prepared a country brief for the Philippines

in April 2008. IEG’s country brief provides the following highlights:

The main challenges identified in the Philippines have been the Bank’s late response to

clients’ demands for more programmatic lending and the lack of synchronization with the

FY10-12 Country Assistance Strategy for the Philippines April 2, 2009

13

budget process. Going forward, government officials were optimistic that the new

programmatic loans which started in 2006 would allow for appropriate flexibility.

Clients appreciated the Bank’s high-quality knowledge work. At the same time, they lamented

the lack of applicability and appreciation of country dynamics.

At the project level, a weak regulatory framework for Local Government Unit (LGU) finance

and private sector participation has hampered participation of LGUs in Bank projects.

43. Overall Value of the Bank. More specifically, IEGs’ 2006 Development Results in Middle-

Income Countries (MIC) report indicated that Philippine partners value the Bank for its longstanding

relationship and consider the Bank to have an intimate knowledge of the country. Appreciation was

universally high for the Philippine Development Forum and the Bank’s role in it; this relationship

helped assure the relevance of the Bank’s strategy.