Embed Size (px)

Citation preview

Workplace Pensions SeminarWednesday 29 January 2014

Automaticenrolment.

What are we learning from stagers?

A wise man learns from other’s mistakes

Phil Risbridger – Account Manager

January 2014

The slides are authorised for use by accredited Scottish Widows staff in

corporate pensions presentations to employers, trustees and UK financial

advisers and should not be relied upon by any other person.

2

Learning Outcomes

•Re-cap on some of the Auto-enrolment rules and how they are being interpreted in practice

• Gain an understanding of key learning points from those firms that have already staged

• Look at Qualifying Schemes

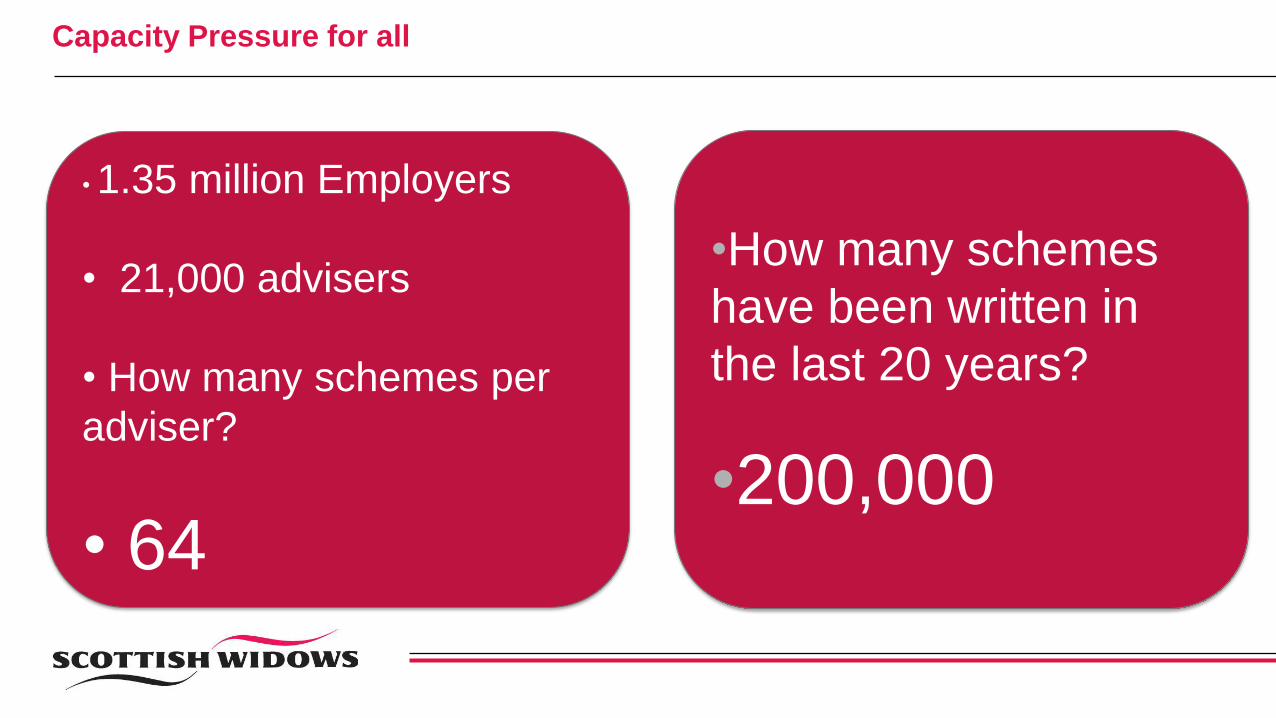

Capacity Pressure for all

• 1.35 million Employers

• 21,000 advisers

• How many schemes per

adviser?

• 64

•How many schemes

have been written in

the last 20 years?

•200,000

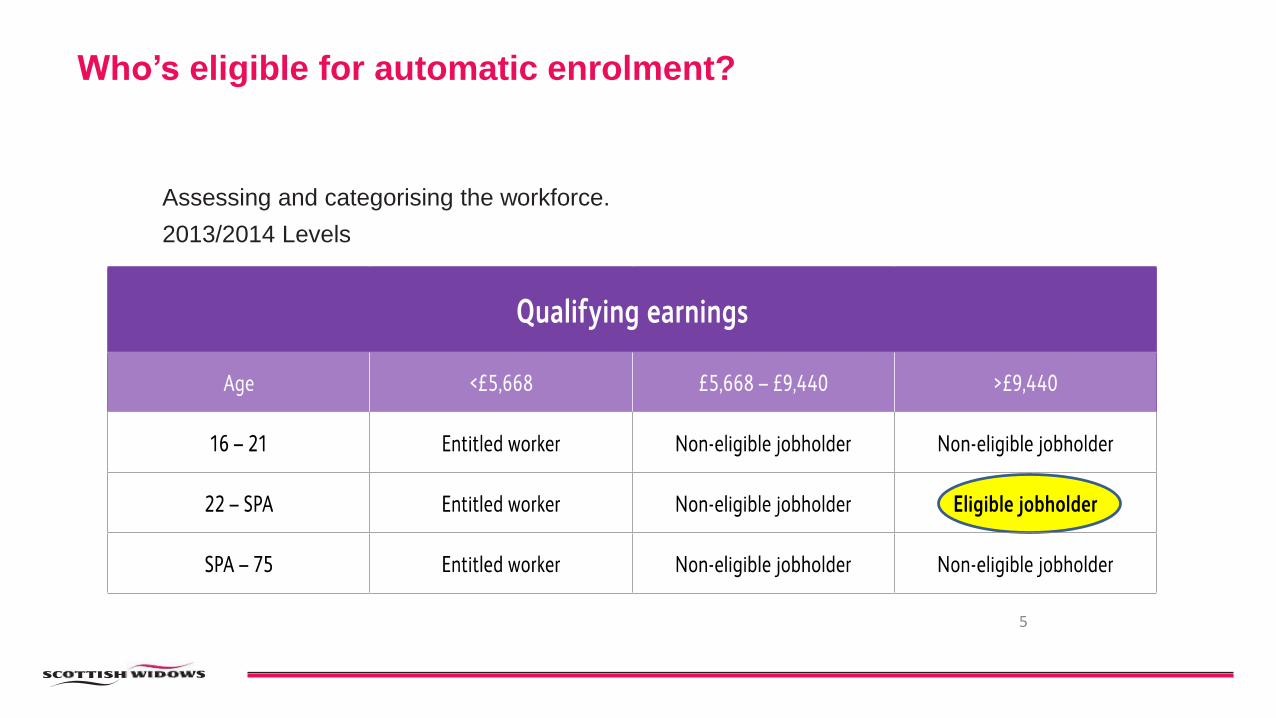

Who’s eligible for automatic enrolment?

Assessing and categorising the workforce.

2013/2014 Levels

5

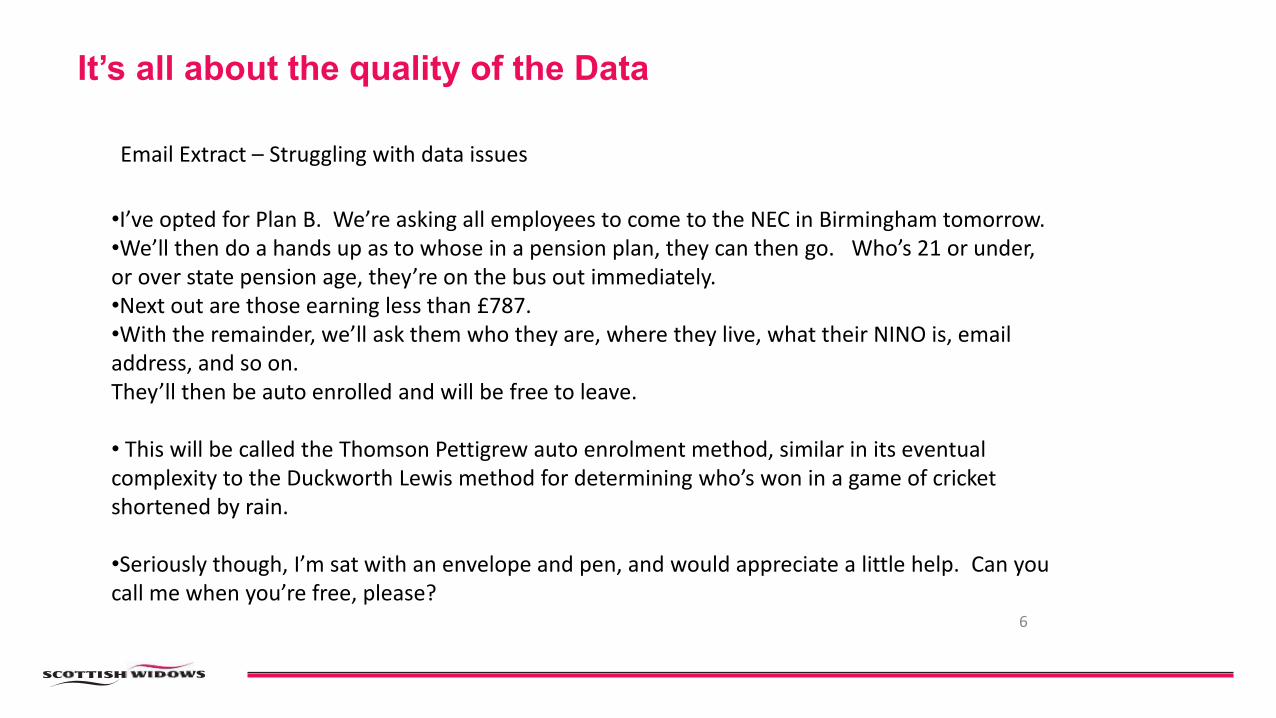

It’s all about the quality of the Data

6

•I’ve opted for Plan B. We’re asking all employees to come to the NEC in Birmingham tomorrow.•We’ll then do a hands up as to whose in a pension plan, they can then go. Who’s 21 or under, or over state pension age, they’re on the bus out immediately.•Next out are those earning less than £787. •With the remainder, we’ll ask them who they are, where they live, what their NINO is, email address, and so on.They’ll then be auto enrolled and will be free to leave.

• This will be called the Thomson Pettigrew auto enrolment method, similar in its eventual complexity to the Duckworth Lewis method for determining who’s won in a game of cricket shortened by rain.

•Seriously though, I’m sat with an envelope and pen, and would appreciate a little help. Can you call me when you’re free, please?

Email Extract – Struggling with data issues

Contributions – phasing in.

7

Simplified certifications options.

Employer industry and demographic will drive decisions.

Qualifying Earnings Definition (2013/14) – P60 income from £5,668 to £41,450.

8

Opting out.

Default ‘re-enrolment date’ is 3rd anniversary of employer staging date.

Opting outEngage your

workforce

Review

Engage your

workforce

1 month

window

1 month

window

Opt out

notice

Opt out

notice

Fill in

notice

Fill in

notice

Every 3 years

Refund

worker

Refund

worker

Inform

provider

Inform

provider

Refund

employer

Refund

employer

9

To date opt- out rates have been lower than expected – sub 10%

Governance requirements.

Checklist

All employers will have additional regulatory requirements.

• Employers prohibited from incentivising opt outs.

• Register with TPR to show they are meeting their duties.

• Payments will be monitored by administrators orscheme trustees who need to report failures.

• Must keep records for six years.

• Must retain opt in and opt out notices for four years.

10

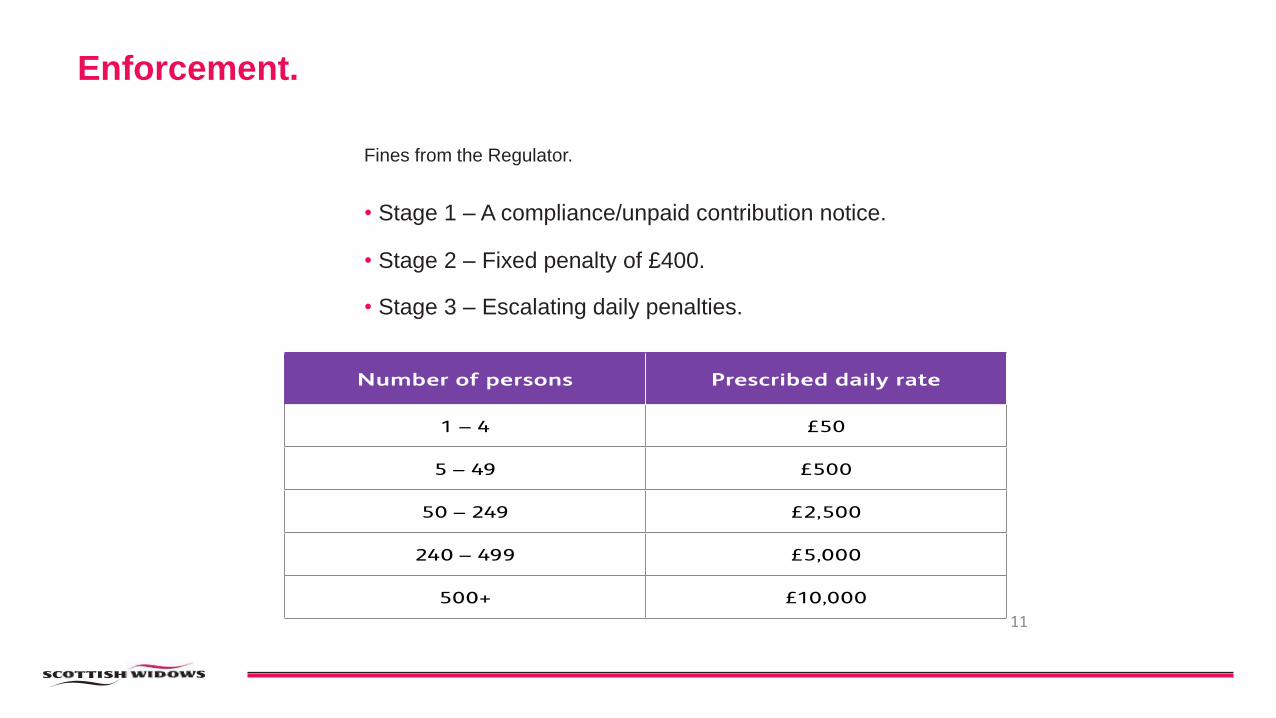

Enforcement.

Fines from the Regulator.

• Stage 1 – A compliance/unpaid contribution notice.

• Stage 2 – Fixed penalty of £400.

• Stage 3 – Escalating daily penalties.

11

”

Enforcement.

*Source: The Pensions Regulator interviewed in Corporate Adviser, September 2012.

Where employers don’t get there, that means employees

won’t get the contributions to their pension that they

are legally entitled to. The most important thing is that

employees do not lose out and where people are liable for

a fine for not meeting a duty then we have to fine them

because if we don’t then we are penalising those people

who have made investments in getting there on time.*

“

12

Employers – who deals with automatic enrolment issues?

Large

Medium

Small

Pensions Department /Human Resources

Payroll

Owner

13

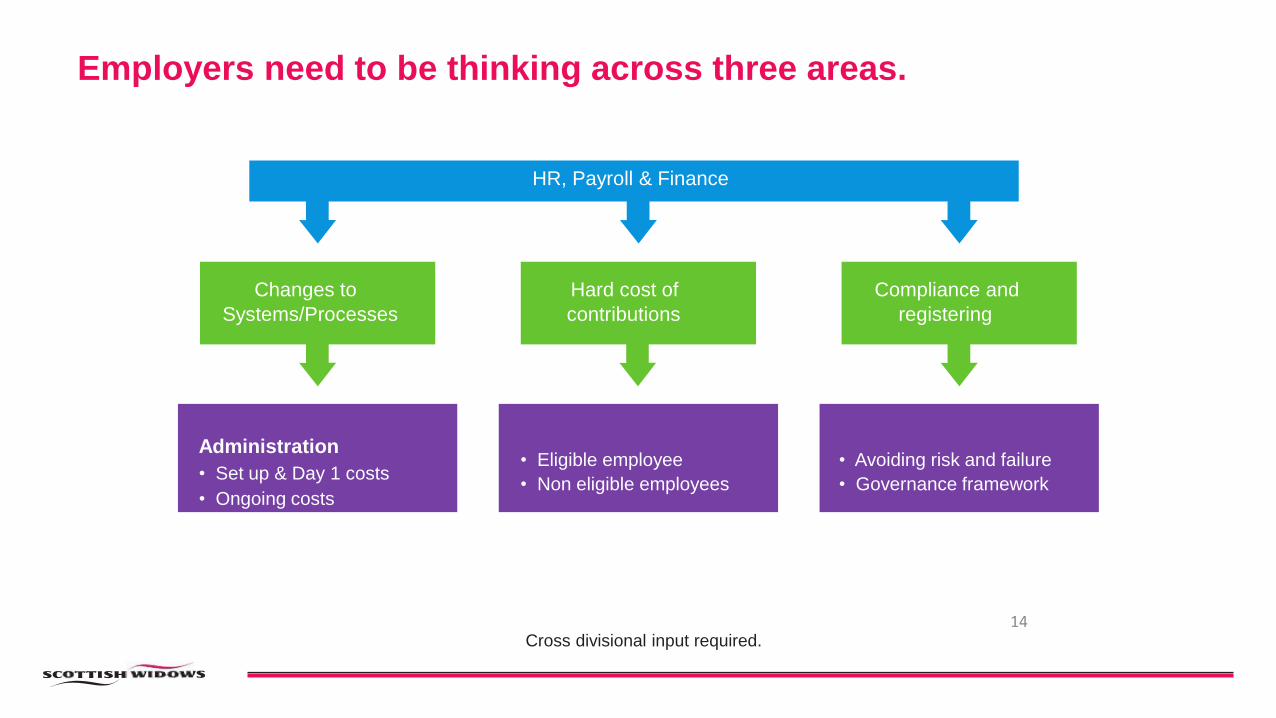

Employers need to be thinking across three areas.

Hard cost of

contributions

• Eligible employee

• Non eligible employees

Cross divisional input required.

Changes to

Systems/Processes

Administration

• Set up & Day 1 costs

• Ongoing costs

Compliance and

registering

• Avoiding risk and failure

• Governance framework

HR, Payroll & Finance

14

How much will AE cost businesses?

“UK businesses will pay fees of between £8,900 and £28,300 to meet their auto-enrolment obligations,according to research from economic consultancy Centre for Economic Business Research.

Size of Employer Estimated Set Up Cost for AE

1- 4 Employees £8,900

100 Employees £12,600

250 Employees £15,600

500 Employees £22,300Source: Finding your way out of the auto enrolment maze, A report by Cebr September 2013

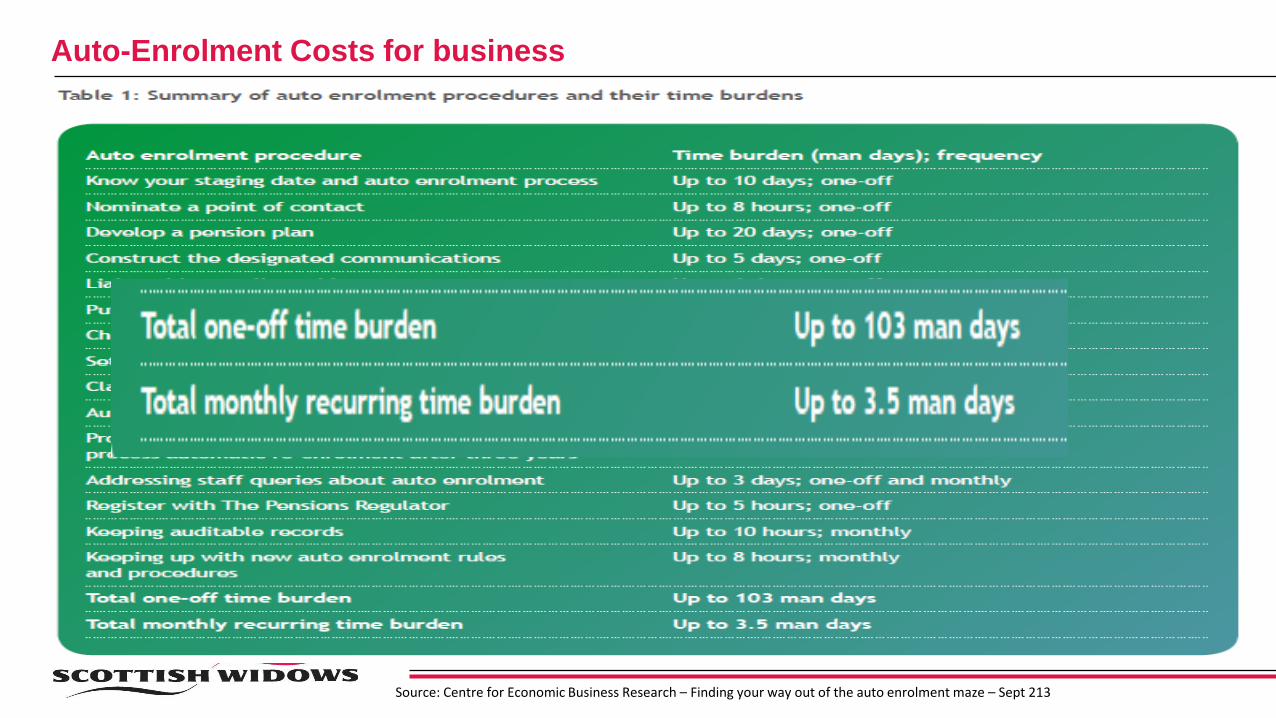

Auto-Enrolment Costs for business

Source: Centre for Economic Business Research – Finding your way out of the auto enrolment maze – Sept 213

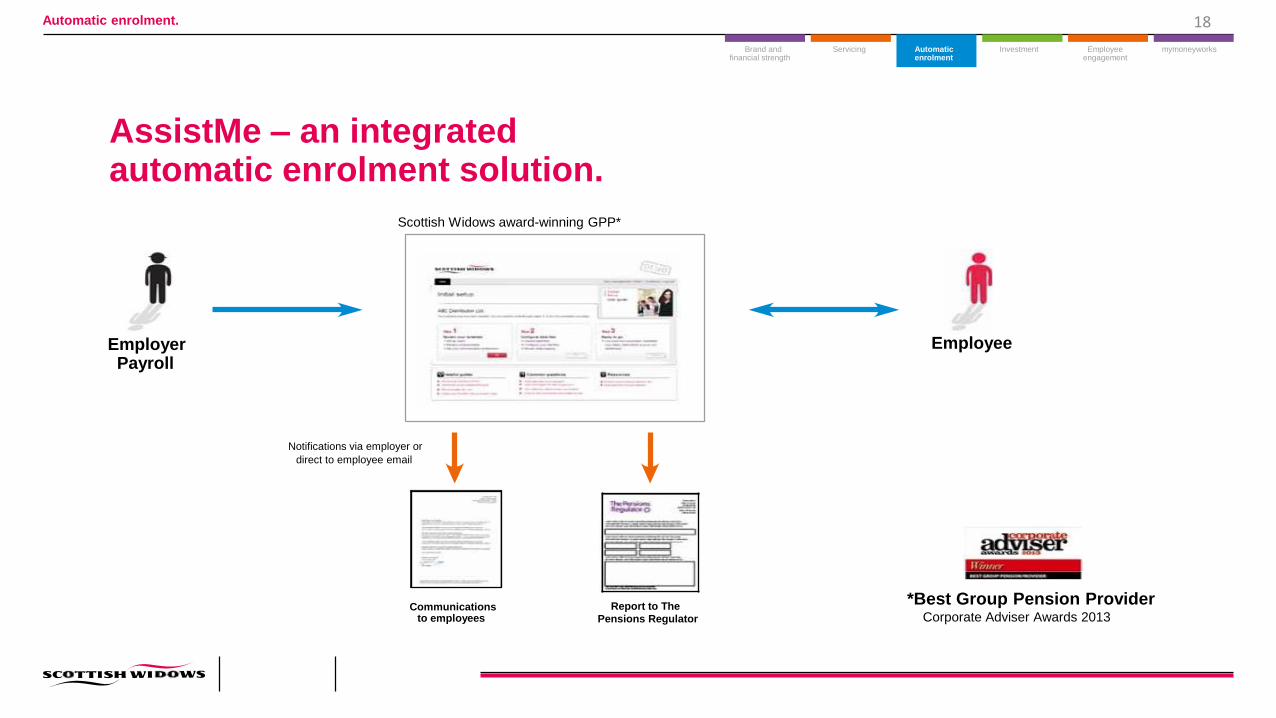

Assessing Auto-enrolment solutions?

EmployerPayroll

Report to The

Pensions RegulatorCommunications

to employees

Notifications via employer or

direct to employee email

mymoneyworksEmployeeengagement

InvestmentAutomaticenrolment

ServicingBrand andfinancial strength

Automatic enrolment.

Employee

*Best Group Pension ProviderCorporate Adviser Awards 2013

AssistMe – an integratedautomatic enrolment solution.

Scottish Widows award-winning GPP*

18

Experience of our early staging clients.

We’ve read the theory, but what’s the reality?

• Enthusiastic and resourceful.

• Preparation is key.

• Understanding your needs.

• It’s all about the data and governance.

• Automatic enrolment as an opportunity – not a threat.

19

The Good

Experience of our early staging clients.

We’ve read the theory, but what’s the reality?

• Late decision making

• No one appointed as project manager.

• No communication with Pay Roll Provider.

• Poor quality of data.

• Last minute panic

20

The Not So Good

TPR Timeline

21

What can you expect from your pension provider?

What providers can do to help you make

automatic enrolment a success.

• Benefit of experience.

• Technology to meet your needs.

• Robust communications.

• Education and employee engagement.

22

Guiding you through Auto-enrolment

TPR Plan Your PlanMaking it happen with

Scottish Widows

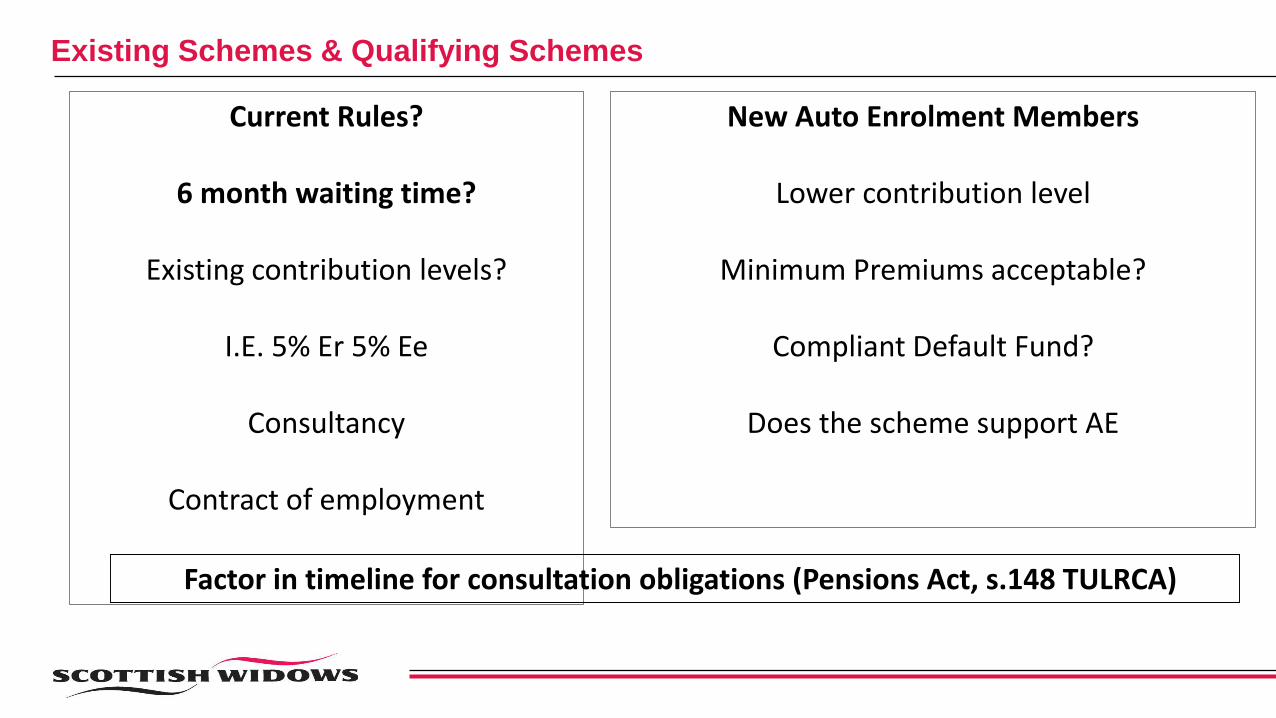

Existing Schemes & Qualifying Schemes

Current Rules?

6 month waiting time?

Existing contribution levels?

I.E. 5% Er 5% Ee

Consultancy

Contract of employment

New Auto Enrolment Members

Lower contribution level

Minimum Premiums acceptable?

Compliant Default Fund?

Does the scheme support AE

Factor in timeline for consultation obligations (Pensions Act, s.148 TULRCA)

Email [email protected] | Tel 01823 446 210

www.pardoes.co.uk

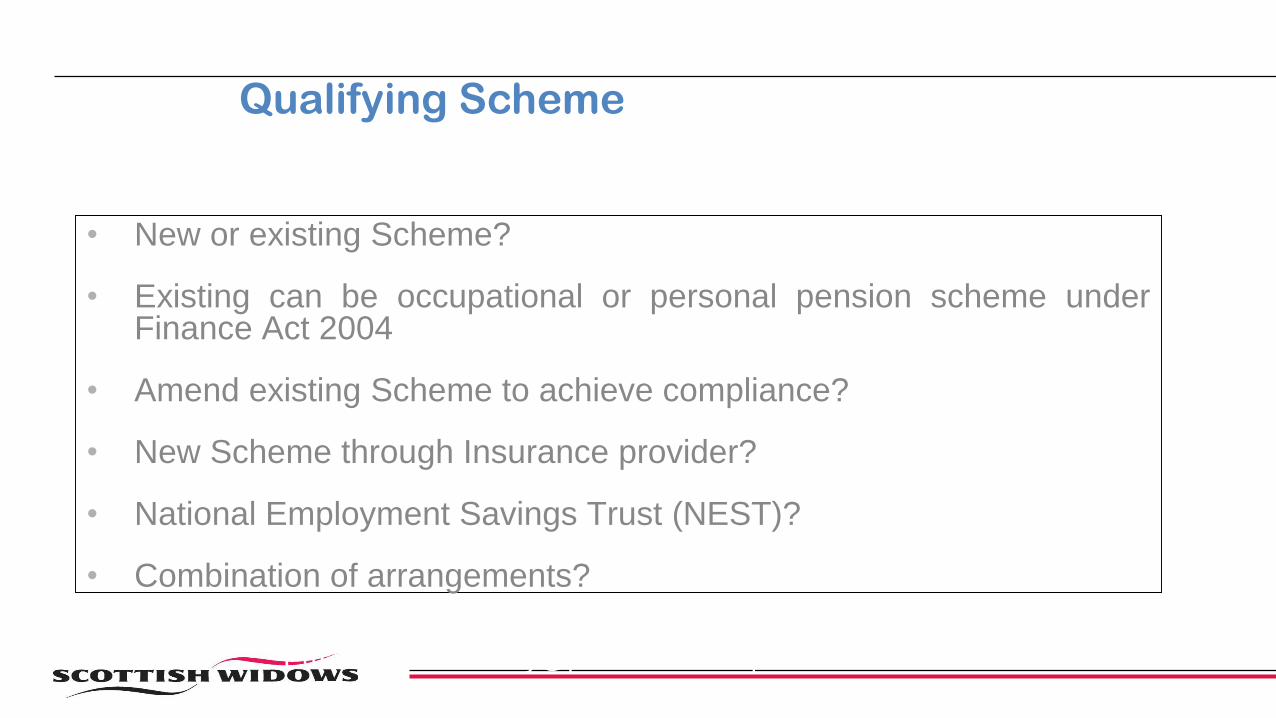

• New or existing Scheme?

• Existing can be occupational or personal pension scheme underFinance Act 2004

• Amend existing Scheme to achieve compliance?

• New Scheme through Insurance provider?

• National Employment Savings Trust (NEST)?

• Combination of arrangements?

Qualifying Scheme

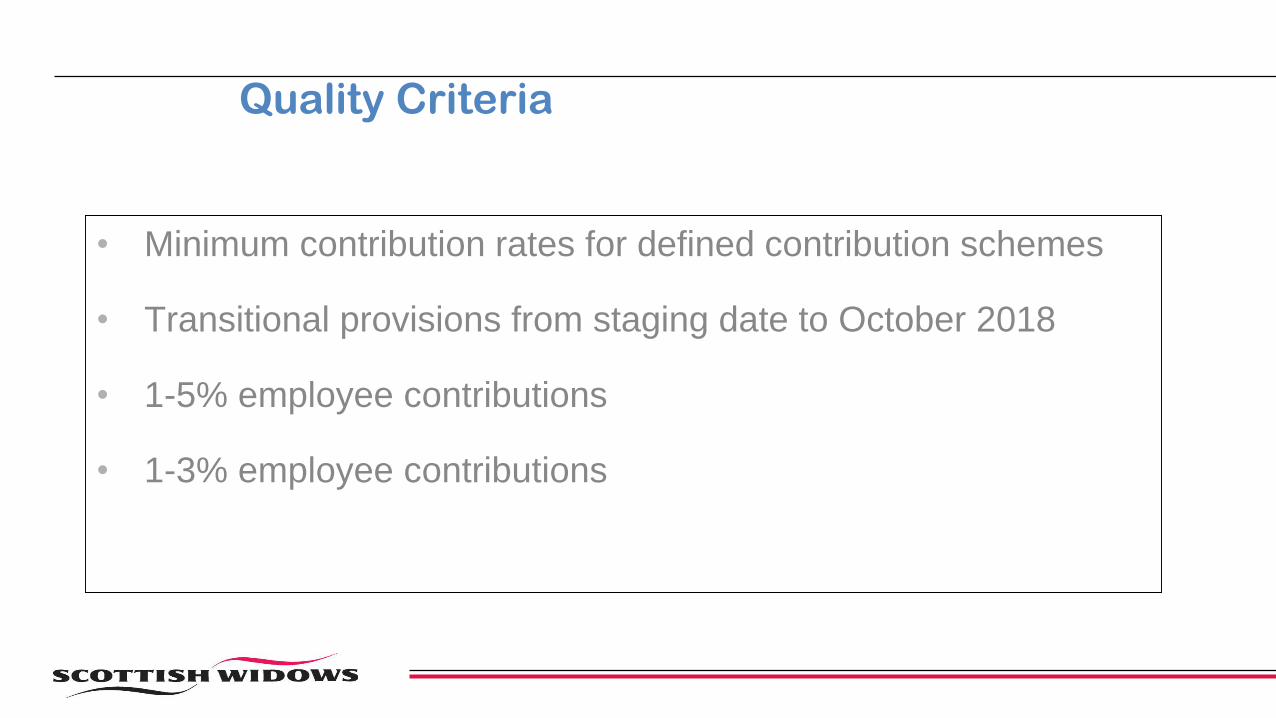

• Minimum contribution rates for defined contribution schemes

• Transitional provisions from staging date to October 2018

• 1-5% employee contributions

• 1-3% employee contributions

Quality Criteria

Email [email protected] | Tel 01823 446 210

www.pardoes.co.uk

Must be no provision in Scheme

•Preventing auto-enrolment of eligible job holders

•Requiring eligible job holder to express a choice in any matter (e.g.investment of funds)

•Requiring eligible job holder to provide information in order to remain anactive member

Quality Criteria

Email [email protected] | Tel 01823 446 210

www.pardoes.co.uk

• Are changes needed to existing Scheme to be auto enrolment compliant?

Contribution levels?

Pensionable salary?

Eligibility?• If so, do these trigger 60 day consultation period required under

Pensions Act 2008?

Practical Steps

Email [email protected] | Tel 01823 446 210

www.pardoes.co.uk

• Any conduct that encourages opting out

• Statements or questions in recruitment that encourage opting

out

• Inducements to opt out (flexible benefits?)

Prohibited Conduct

Email [email protected] | Tel 01823 446 210

www.pardoes.co.uk

• Obligation to maintain records documenting compliance for 6 years

• Record eligible job holders – changes in pay and age

• Record details of contributions payable

• Re-enrolment every 3 years for all eligible job holders and go through opt

out procedures

Monitoring

Email [email protected] | Tel 01823 446 210

www.pardoes.co.uk

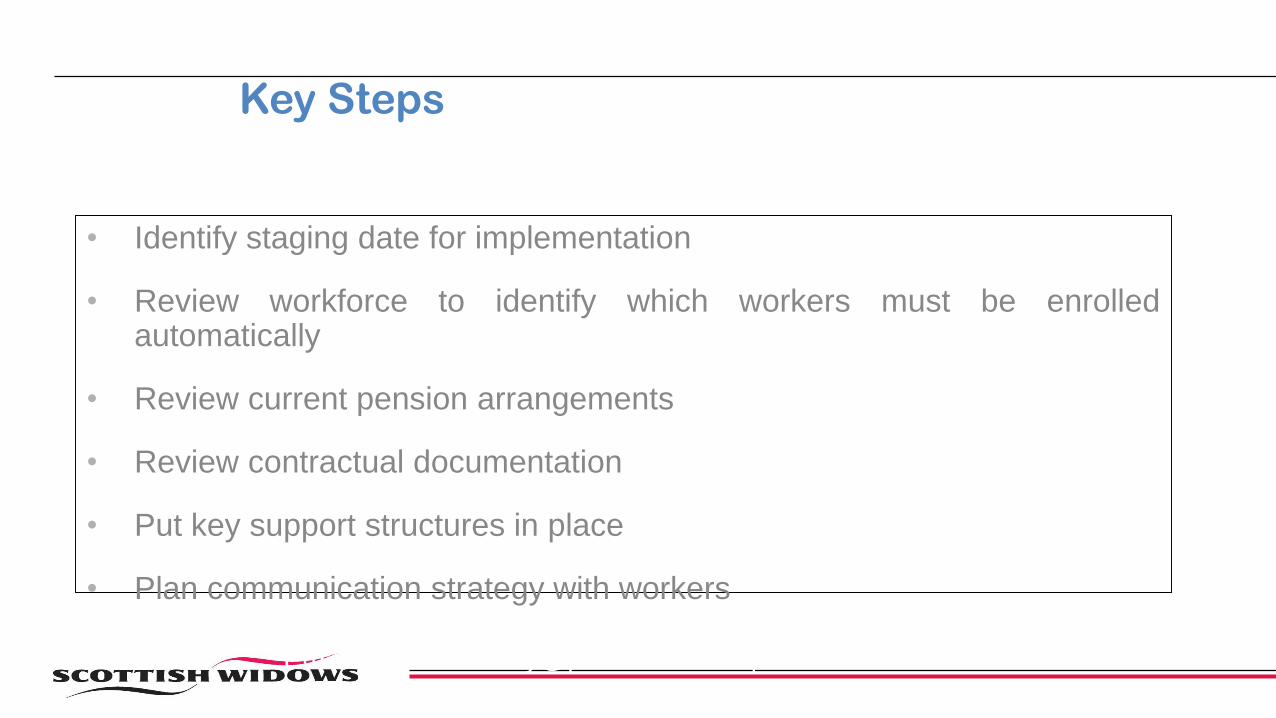

• Identify staging date for implementation

• Review workforce to identify which workers must be enrolledautomatically

• Review current pension arrangements

• Review contractual documentation

• Put key support structures in place

• Plan communication strategy with workers

Key Steps

• Contracts

Entrenched pension promises

Eligibility criteria for pension membership

Collective Agreements

Handbooks• Interview and recruitment processes

• Flexible benefits

Review Documentation

• Changes to terms and conditions

By agreed variation or

New contracts for old on contractual notice• Consult staff

Meeting and letter setting out proposed changes and consultation process

1 to 1 meetings as required

Factor in timeline for consultation obligations (Pensions Act, s.148 TULRCA)

Implement Changes Required

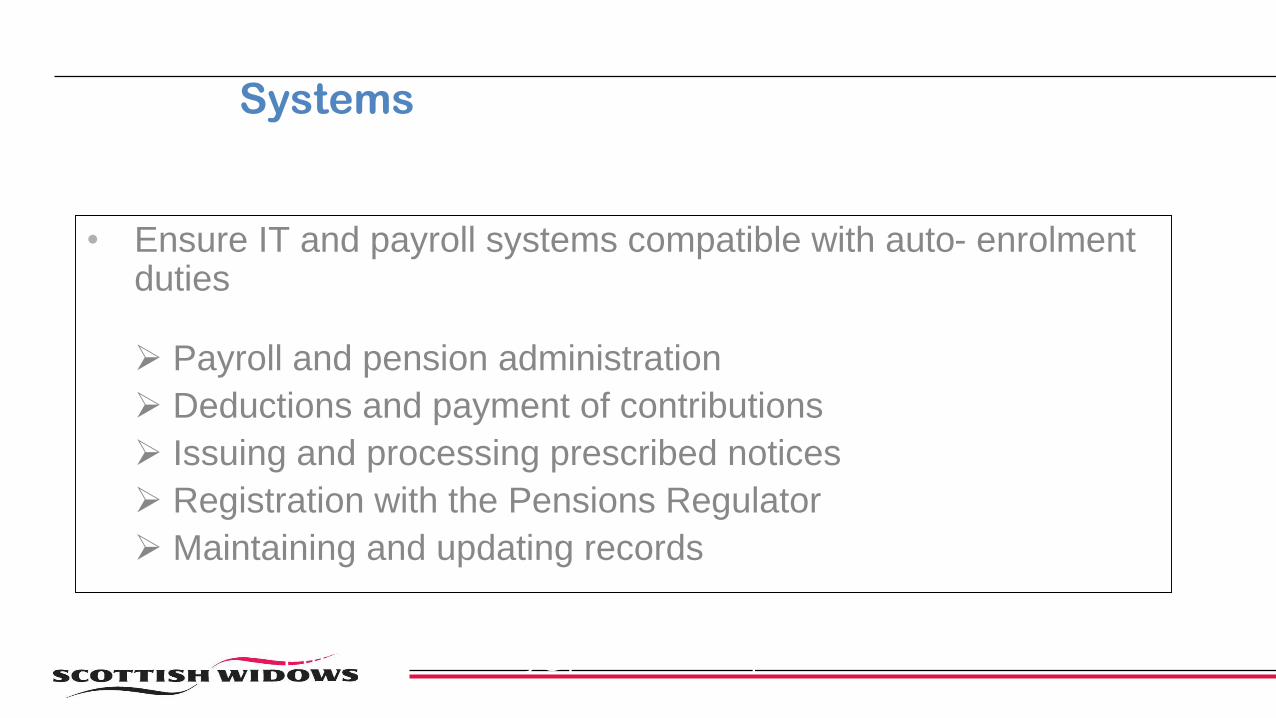

• Ensure IT and payroll systems compatible with auto- enrolment duties

Payroll and pension administration

Deductions and payment of contributions

Issuing and processing prescribed notices

Registration with the Pensions Regulator

Maintaining and updating records

Systems

Email [email protected] | Tel 01823 446 210

www.pardoes.co.uk

• Plan timeline and communication strategy

• Factor in any consultation periods

• Notify workforce of auto-enrolment policy and opt-out rights

(Intranet, Newsletters)

• Letter templates on TPR website

• Department of Work and Pensions Toolkit

Communication

Email [email protected] | Tel 01823 446 210

www.pardoes.co.uk

• www.thepensionsregulator.gov.uk

Template letters

Opt out forms

Useful Contact Details

• www.dwp.gov.uk Toolkit

Key facts booklet, facts and myths, case studies

These slides represent a summary of the legal issues referred to in them and are not intended to provide or be relied upon as specific legal advice

nor are they intended to be comprehensive

If you require advice on a specific issue please contact your solicitor

Disclaimer

Email [email protected] | Tel 01823 446 210

www.pardoes.co.uk

What next?

• If you have employers staging with Scottish Widows over the next 12 months you will be invited to a comprehensive seminar to help ensure as smooth a process as possible

• Download the Auto Enrolment Factsheets from our website http://www.scottishwidows.co.uk/extranet/financial-planning

•Watch out for our continuing suite of support for advisers dealing with auto-enrolment

Learning outcomes

• Re-cap on some of the Auto-enrolment rules and

how they are being interpreted in practice

• Gain an understanding of key learning points from

those firms that have already staged

• Share alternative employer fee models

Follow us on twitter. Join our adviser group on Linkedin

@SWidowsAdviser

Scottish Widows Adviser Forum

Disclaimer.

This presentation represents Scottish Widows’ interpretation of current and proposed legislation

and HM Revenue & Customs practice as at the date of publication – these may change in future.

This material is for use by UK Financial Advisers only. It is not intended for onward transmission

to private customers and should not be relied upon by any other person.

Scottish Widows plc. Registered in Scotland No. 199549. Registered Office in the United Kingdom at 69 Morrison Street, Edinburgh EH3 8YF. Telephone: 0131 655 6000.Authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. Financial Services Register number 191517.

24417 07/1340

![Cap. 173] Pensions CHAPTER 173. PENSIONS. 173.pdf · Pensions, etc., to cease on bankruptcy. 14. Pensions, etc., may cease on sentence to term of imprisonment. 15. Pensions, etc.,](https://img.dokumen.tips/doc/110x75/5f32c41fe2aa25713c052446/cap-173-pensions-chapter-173-173pdf-pensions-etc-to-cease-on-bankruptcy.jpg)