Embed Size (px)

Citation preview

Workers Compensation Update

Karen Ayres, FCAS, MAAANCCI

Casualty Loss Reserve SeminarSeptember 12, 2005

Workers Compensation Results

31.0 31.3

26.3 25.2 24.2 23.3 22.325.0 26.1

29.331.1

34.5

29.130.529.8

0

10

20

30

40

50

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004p

WC Net Written Premium ($ B)

Workers Compensation PremiumContinued to Rise in 2004

Private Carriers$ Billions

Calendar Yearp Preliminary

Source: 1990-2003, A.M. Best Aggregates & Averages; 2004p, NCCI

117123 122

109102

97 100 101107

115 118122

111 109105

0

20

40

60

80

100

120

140

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004p

Loss LAE Underwriting Expense Dividends

1.9% Due to September 11Percent

WC Calendar Year Combined Ratio Continued Its Modest Decline in 2004

Private Carriers

p Preliminary

Source: 1990-2003, A.M. Best Aggregates & Averages; 2004p, NCCI

Calendar Year

13.014.0

18.116.7

14.4

16.817.6

20.421.3

20.519.5

14.0

10.7 10.4 10

0

5

10

15

20

25

1990* 1991* 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004p

Percent

Low Workers Compensation InvestmentReturns Continued in 2004

Investment Gain on Insurance Transactions to Premium RatioPrivate Carriers

Calendar Yearp Preliminary* Adjusted to include realized capital gains to be consistent with 1992 and afterInvestment Gain on Insurance Transactions includes Other IncomeSource: 1990-2003, A.M. Best Aggregates & Averages; 2004p, NCCI

7.5

12.8

19.717.9

19.8

13.9

5.2

1.5 1.0

5

0.0

-7.5

-3.4

-8.7

-4.2

-15

-10

-5

0

5

10

15

20

25

1990* 1991* 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004p

Percent

Calendar Yearp Preliminary* Adjusted to include realized capital gains to be consistent with 1992 and afterOperating Gain equals 1.00 minus (Combined Ratio less Investment Gain on Insurance Transactions and Other Income)Source: 1990-2003, A.M. Best Aggregates & Averages; 2004p, NCCI

2004 Workers CompensationResults Improved Over 2003

Pre-Tax Operating Gain Ratio—Private Carriers

28.427.0 25.9

28.5

32.0

37.5

42.0

46.0

25.0

0

10

20

30

40

50

1996 1997 1998 1999 2000 2001 2002 2003 2004p

25.2 24.2 26.129.2 31.1

34.5

23.3 22.325.0

0

10

20

30

40

50

1996 1997 1998 1999 2000 2001 2002 2003 2004p

State Funds ($ B)

Private Carriers ($ B)

$ Billions

p PreliminarySource: 1996-2003 Private Carriers, A.M. Best Aggregates & Averages; 2004p, NCCI

1996-2004p State Funds: AZ, CA, CO, HI, ID, KY, LA, MO, MT, NM, OK, OR, RI, TX, UT Annual Statements

Workers Compensation PremiumVolume Continues to Grow

Private Carriers and State Funds

Calendar Year

100 101

107

115118

122

111 109105

112

119

143147

144

115 114 116 118119

128

141144

136

116 117

103 101

80

90

100

110

120

130

140

150

1996 1997 1998 1999 2000 2001 2002 2003 2004p

Private Carriers NCCI Affiliated State Funds State Funds

Percent

Calendar Year

Workers Compensation Calendar YearNet Combined Ratios

Private Carriers and State Funds

p PreliminarySource: 1996-2003 Private Carriers, A.M. Best Aggregates & Averages; 2004p, NCCI

1996-2004p State Funds: AZ, CA, CO, HI, ID, KY, LA, MO, MT, NM, OK, OR, RI, TX, UT Annual Statements

Workers Compensation

Accident Year Results

And

Reserve Estimates

p PreliminaryAccident Year data is evaluated as of 12/31/2004 and developed to ultimateSource: Calendar Years 1995-2003, A.M. Best Aggregates & Averages;

Calendar Year 2004p and Accident Years 1995-2004p, NCCIIncludes dividends to policyholders

Accident Year Combined RatioAnother Underwriting Profit in 2004

Workers Compensation Calendar Year vs.Ultimate Accident Year – Private CarriersPercent

97100 101

107

115118

122

111109

105

100

106

120

131

139135

126

106

98

94

90

100

110

120

130

140

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004p

Calendar Year Accident Year

p PreliminaryReported Loss and LAE reserves from Schedule PSource: 1995-2004p, NAIC Annual Statement insurance data

Workers Compensation AccidentYear Loss & LAE Ratios

Private CarriersPercent

Accident Year

78 7779

8184

83 83

7577

69

73

85

94

10098

86

7673

74

65

70

75

80

85

90

95

100

105

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004p

At First Report

As of 12/31/2004

15

18

2021

18

15

12

2

5

10

0

5

10

15

20

25

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004p

$ Billions

Workers Compensation Reserve Deficiencies Continue to Decline

Private Carriers

Loss and LAE Reserve Deficiency Through Year Endp Preliminary

Difference between NCCI estimated ultimate losses and LAE as of 12/31/2004 and reported in Schedule P

$5 billion of the Reserve Deficiencyin 2004 is due to Tabular Discounts

Workers Compensation

Premium Drivers

12.1

7.4

10.0

2.9 3.5

1.2

4.9

6.6

-0.9

-6.4

-3.2

-6.0

-8.0

-5.4

-2.6

-6.0

-10

-5

0

5

10

15

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005*

Cumulative 1990-1993

+36.3%

Cumulative 1994-1999

-27.8%

Average Approved BureauRates/Loss Costs

History of Average WC Bureau Rate/Loss Cost Level ChangesPercent

Cumulative 2000-2003

+17.1%

Cumulative

2004-2005

-6.8%

Calendar Year* States approved through 04/15/2005Countrywide approved changes in advisory rates, loss costs and assigned risk rates as filed by the applicable rating organization

-5.1-3.0

-2.0 -1.8-1.5-1.3 -1.1-1.0-0.7 -0.3

0.0 0.1 0.61.7 2.0 2.2 2.3 2.4 2.5 3.4 3.9 4.9 5.3 5.5 6.3 6.5

8.8

12.0

11.2 11.4

-20.2

12.1

-6.5

-25

-20

-15

-10

-5

0

5

10

15

20

RI CONV

FL HI SD DC AR MO IA GA AL CT OR IL MS KS NC ME LA AZIN

NH MD TN NEVA

ID OK KY VT NM UT SC AK MT

Current NCCI Voluntary Market Approved Rate/Loss Cost Changes

Excludes Law-Only FilingsPercent

States approved through 04/15/2005

-7.1 -7.5 -7.0-8.5

-10.4

-14.6

-17.7

-22.6

-19.2

-14.2

-4.00.2

-23.2

-1.7

-25

-20

-15

-10

-5

0

5

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004p

Rate/Loss Cost Departure Schedule Rating Dividends

Percent

Impact of Discounting on Workers Compensation Premium

NCCI States—Private Carriers

p PreliminaryNCCI benchmark level does not include an underwriting contingency provisionDividend ratios are based on calendar year statisticsBased on data through 12/31/2004 for the states where NCCI provides ratemaking services

Policy Year

Workers Compensation

Loss Drivers

$9

.7

$9

.4

$9

.1

$9

.6

$9

.7

$1

0.3

$1

1.1

$1

2.1

$1

3.3

$1

4.7

$1

6.1

$1

6.5

$1

7.2

$1

7.9

+4.2%+4.6%

+2.4%+9.0%

+11.2%

+9.9%

+8.5%+7.7%

+5.9%+1.7%+4.9%

-2.8%-3.1%+1.0%

5

7

9

11

13

15

17

19

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004p

IndemnityClaim Cost (000s)

Annual Change 1991–1995: +0.3%Annual Change 1996–2003: +7.4%

2004p: Preliminary based on data valued as of 12/31/20041991-2003: Based on data through 12/31/2003, developed to ultimateBased on the states where NCCI provides ratemaking servicesExcludes the effects of deductible policies

The Growth in WC Indemnity ClaimCosts Has Eased in Recent Years

Lost–Time Claims

Accident Year

Indemnity severity 2004p: Preliminary based on data valued as of 12/31/2004Indemnity severity 1995-2003: Based on data through 12/31/2003, developed to ultimateBased on the states where NCCI provides ratemaking services, excludes the effects of deductible policiesSource: Calendar year Current Population Survey, Economy.com; Accident year indemnity severity, NCCI

2.8 2.8

4.04.7

4.24.9

4.2

2.2 2.01.7

5.9

7.78.5

9.9

11.2

9.0

2.4

4.64.2

2.2

0

2

4

6

8

10

12

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004p

Change in CPS Wage Change in Indemnity Cost per Lost-Time Claim

Percent Change

Workers Compensation Indemnity Severity Is Outpacing Wage Inflation

Lost–Time Claims

Year

Annual Change 1991–1995: +3.9%Annual Change 1996–2003: +9.3%

WC Medical Claim Cost TrendsDouble-Digit Growth Continued in 2004

Lost–Time ClaimsMedicalClaim Cost (000s)

Accident Year

$8

.0

$8

.2

$8

.0

$8

.7

$9

.1

$9

.8

$1

0.8

$1

1.6

$1

2.8

$1

3.9

$1

5.5

$1

6.8

$1

8.7

$2

0.6

+10.5%

+10.9

+8.4%

+11.9%

+8.5%+9.9%

+7.6%+10.1%

+7.4%+5.1%+9.0%

-2.1%+1.3%+6.8%

5

7

9

11

13

15

17

19

21

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004p

2004p: Preliminary based on data valued as of 12/31/20041991-2003: Based on data through 12/31/2003, developed to ultimateBased on the states where NCCI provides ratemaking servicesExcludes the effects of deductible policies

4.53.6

2.83.2 3.5

4.14.6 4.7

4.0

5.1

7.4

10.1

7.6

9.9

8.5

11.9

8.4

10.9 10.5

4.4

0

2

4

6

8

10

12

14

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004p

Change in Medical CPI Change in Medical Cost per Lost-Time Claim

Workers Compensation Medical Severity Has Been Growing Much

Faster Than the Medical CPILost–Time ClaimsPercent Change

Medical severity 2004p: Preliminary based on data valued as of 12/31/2004Medical severity 1995-2003: Based on data through 12/31/2003, developed to ultimateBased on the states where NCCI provides ratemaking services, excludes the effects of deductible policiesSource: Calendar year Current Population Survey, Economy.com; Accident year medical severity, NCCI

Year

3.2 3.54.1 4.6 4.7

7.6

9.9

8.5

11.9

8.4

12.9

15.1

12.4

14.9

11.1

0

2

4

6

8

10

12

14

16

18

20

1998 1999 2000 2001 2002

Change in Medical CPIChange in Medical Cost per Lost-Time ClaimChange in Rx Drug Costs per Lost-Time Claim

Percent Change

Drug Costs Are Increasing More Rapidly Than Total WC Medical Costs

Year

Medical severity: Based on data through 12/31/2003, developed to ultimateBased on the states where NCCI provides ratemaking services, excludes the effects of deductible policiesSource: Calendar year Current Population Survey, Economy.com; Accident year medical severity, NCCI; Accident year

Rx Drug Costs, NCCI estimate based on sample data provided by carriers

Workers Compensation Medical Losses Are More Than Half of Total Losses

All Claims—NCCI States

44%56%

1984

MedicalIndemnity

1994

51% 49%

Indemnity Medical

2004p

43% 57%Indemnity Medical

2004p: Preliminary based on data valued as of 12/31/20041984, 1994: Based on data through 12/31/2003, developed to ultimateBased on the states where NCCI provides ratemaking servicesExcludes the effects of deductible policies

-4.2 -4.4

-9.2

-6.3

-4.2-3.7 -3.4

0.3

-6.5

-4.5

0.5

-3.9

-2.3

-4.5

-10

-8

-6

-4

-2

0

2

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004p

Cumulative Change of –42.0%(1990-2003)

Percent Change

Workers Compensation Lost-Time Claim Frequency Continues Its Decline

Lost-Time Claims

Accident Year2004p: Preliminary based on data valued as of 12/31/20041991-2003: Based on data through 12/31/2003, developed to ultimateBased on the states where NCCI provides ratemaking servicesExcludes the effects of deductible policies

Workers Compensation Frequency for Selected Classes

Policies Expiring in 2003 Policies Expiring in 1999

Payroll ($M)Lost-Time

Claims FreqLost-Time

Claims FreqFreq

Change

Clerical 526,085$ 29,402 0.056 28,974 0.060 -8%Salesperson - Outside 117,728$ 8,688 0.074 9,964 0.089 -17%College Professional 67,230$ 6,531 0.097 7,385 0.108 -10%Physician 59,364$ 4,568 0.077 4,173 0.080 -4%Retail Store 32,183$ 16,555 0.514 15,626 0.513 0%Hospital Professional 28,806$ 7,665 0.266 8,343 0.313 -15%Attorneys 26,717$ 938 0.035 1,064 0.047 -25%Auditors/Accountants 25,334$ 408 0.016 431 0.017 -5%Caterer 22,642$ 15,357 0.678 19,459 0.887 -24%Auto Service/Repair 16,593$ 10,414 0.628 11,484 0.703 -11%Architect/Engineer 15,189$ 1,655 0.109 1,619 0.129 -16%Electrical Wiring 11,754$ 7,219 0.614 8,602 0.779 -21%Fast Food Restaurant 10,985$ 6,931 0.631 7,643 0.821 -23%Convalescent/Nursing Home 10,093$ 9,239 0.915 12,701 1.249 -27%Plumbing 9,927$ 7,150 0.720 8,065 0.892 -19%Total - Largest Classes 980,630$ 132,720 0.135 145,533 0.160 -16%Total - All Classes 1,568,658$ 529,404 0.337 633,235 0.422 -20%Mix-Adjusted Total -16%

Countrywide Class

Frequency = Lost-time claims/payroll. Payroll adjusted for inflation Claim count determined at first report

NCCI states only

-24%-21%-15%-22%-8%

-70

-60

-50

-40

-30

-20

-10

0

10

20

Fatal PermanentTotal

PermanentPartial

TemporaryTotal

Medical OnlyPe

rce

nt

Ch

an

ge

in L

os

t-T

ime

Cla

im F

req

ue

nc

y

Smallest 1/3 of Claims within Injury Type

Middle 1/3 of Claims within Injury Type

Largest 1/3 of Claims within Injury Type

Percent Change Between Policies Expiring in 1999 and 2003

Change in Lost-Time Claim Frequency By Injury Type and by Size of Loss Group

Loss Size Adjustments: 4.2% Indemnity, 7.4% MedicalFrequency = Lost-time claims / payroll; Payroll adjusted for inflationClaim count determined at 1st report. NCCI States only, excluding Texas

$1

2.1

$1

3.3

$1

4.7

$1

6.1

$1

6.5

$1

7.2

$1

7.9

+4.2%+4.6%

+2.4%+9.0%+11.2%

+9.9%+8.5%

5

7

9

11

13

15

17

19

21

23

1998 1999 2000 2001 2002 2003 2004p

IndemnityClaim Cost (000s)

Workers Compensation Indemnity Claim Costs

Lost–Time Claims

Accident Year

Annual Change Before Adjustment for Claim Size, 1998-2002: +8.1%

2004p: Preliminary based on data valued as of 12/31/20041998-2003: Based on data through 12/31/2003, developed to ultimateBased on the states where NCCI provides ratemaking servicesExcludes the effects of deductible policies

$1

2.1

$1

2.9

$1

4.0

$1

4.8

$1

4.7 ? ?

? ?

+4.2%+4.6%

+2.4%+9.0%+11.2%

+9.9%+8.5%

5

7

9

11

13

15

17

19

21

23

1998 1999 2000 2001 2002 2003 2004p

IndemnityClaim Cost (000s)

Annual Change Before Adjustment for Frequency by Size, 1998-2002: +8.1%Annual Change After Adjustment for Frequency by Size, 1998-2002: +5.1%

Impact of Changes in Claim Size Distribution on Indemnity Claim Costs

Lost–Time Claims

Accident Year2004p: Preliminary based on data valued as of 12/31/20041998-2003: Based on data through 12/31/2003, developed to ultimateBased on the states where NCCI provides ratemaking servicesExcludes the effects of deductible policies

$1

1.6

$1

2.8

$1

3.9

$1

5.5

$1

6.8

$1

8.7

$2

0.6

+10.5%

+10.9%

+8.4%+11.9%

+8.5%+9.9%

+7.6%

5

7

9

11

13

15

17

19

21

23

1998 1999 2000 2001 2002 2003 2004p

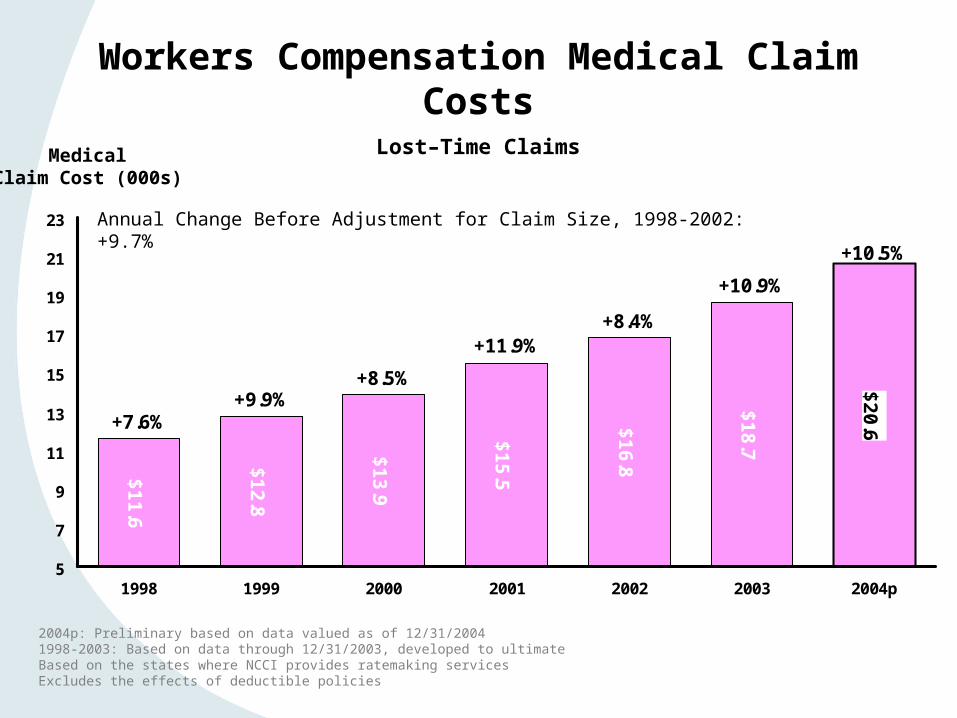

Workers Compensation Medical Claim Costs

Lost–Time Claims

Accident Year

Annual Change Before Adjustment for Claim Size, 1998-2002: +9.7%

MedicalClaim Cost (000s)

2004p: Preliminary based on data valued as of 12/31/20041998-2003: Based on data through 12/31/2003, developed to ultimateBased on the states where NCCI provides ratemaking servicesExcludes the effects of deductible policies

$1

1.6

$1

2.5

$1

3.4

$1

4.6

$1

5.6

??

?

?

+7.6%+9.9%

+8.5%

+11.9%+8.4%

+10.9%

+10.5%

5

7

9

11

13

15

17

19

21

23

1998 1999 2000 2001 2002 2003 2004p

Annual Change Before Adjustment for Frequency by Size, 1998-2002: +9.7%Annual Change After Adjustment for Frequency by Size, 1998-2002: +7.7%

Impact of Changes in Claim Size Distribution on Medical Claim Costs

Lost–Time Claims

Accident Year

MedicalClaim Cost (000s)

2004p: Preliminary based on data valued as of 12/31/20041998-2003: Based on data through 12/31/2003, developed to ultimateBased on the states where NCCI provides ratemaking servicesExcludes the effects of deductible policies

0

5

10

15

20

25

30

19261930

19341938

19421946

19501954

19581962

19661970

19741978

19821986

19901994

19982002

20062010

Model Projection Period

Injury Rates

Trend Line

Historical Bounds

Patterns in Historical Labor Statistics Underlie a Possible Modest Upturn

Calendar Year

Source: NCCI analysis of Bureau of Labor Statistics injury rates from 1926-2002

ManufacturingInjury Rates

Workers CompensationResidual Market

1.2

2.12.6

2.8

3.54.0

4.44.8

4.1

3.1

2.0

1.00.6

0.3 0.3 0.40.6

1.11.4 1.5

0

1

2

3

4

5

6

Workers Compensation Residual Market Premium Volume

NCCI-Serviced Workers Compensation Residual Market PoolsAs of December 31, 2004

$ Billions

Policy Year

* Excludes Maine Residual Market Pool** Incomplete Policy Year Projected to Ultimate

Workers Compensation Residual Market Shares Continue to Rise

Workers Compensation Insurance Plan States* Premium As a Percent of Direct Written Premium

9

1618 17

2224

2629 28

24

17

11

8

4 3 3

13

5

1112

0

5

10

15

20

25

30

Percent

Calendar Year

p Preliminary* NCCI Plan states plus DE, IN, MA, MI, NJ, NC

176

164168 166

159

143

127

112103

98 94 98 102

115119 118 116114 115 113

80

100

120

140

160

180

200

19851986

19871988*

1989*

1990*

1991*

1992*

19931994

19951996

19971998

19992000

20012002

20032004**

Workers Compensation Residual Market Combined Ratios

NCCI-Serviced Workers Compensation Residual Market Pools As of December 31, 2004

Percent

Policy Year

* Excludes Maine Residual Market Pool** Incomplete Policy Year Projected to Ultimate

-922

-1,361

-1,777-1,883

-2,063

-1,687

-1,190

-553

-141-14 -50 -53 -63

-240-85 -164 -174

71 11816

-2,500

-2,000

-1,500

-1,000

-500

0

500

Workers Compensation Residual Market Underwriting Results

NCCI-Serviced Workers Compensation Residual Market PoolsAs of December 31, 2004

$ Millions

Policy Year

* Excludes Maine Residual Market Pool** Incomplete Policy Year Projected to Ultimate

Residual Market ProgramsMitigate the Burden

Pricing Programs:– Differential/Surcharge

– ARAP/SARAP

– Removal/Reduction ofPremium Discount

– LSRP

– Two point or greater underwriting

contingency provision

Depopulation Mechanisms:– Take-Out Credit Program– Voluntary Compensation Assistance Program

Improved Controls:– Paid Loss Ratio Incentive Program– Heightened carrier audit process

Improved Efficiency:– Servicing carrier bid process

ARAP: Assigned Risk Adjustment ProgramSARAP: Simplified Assigned Risk Adjustment ProgramLSRP: Loss Sensitive Rating Plan

Impact of TRIAOn Workers Compensation

• TRIA’s direct financial impact is limited to infrequent extreme events

• TRIA is not triggered under approximately 98% of the modeled scenarios

• TRIA enables the P/C market to function effectively with minimal financial exposure to taxpayer funds

When Does TRIA Make a Difference?

2% 2% 4% 6%12%

20%

68%

0

50

100

150

200

250

9/10 3/4 1/2 1/4 1/20 1/25 3/100 1/50 1/100 1/500 1/1000

Industry Loss with TRIA Federal Contribution Excess of TRIA Limit

Under Most Scenarios TRIA Is Dormant, but When TRIA Is Triggered It Is Vital

P/C Underwriting Loss With and Without TRIA Support

Chance of an Event

Total Loss as % of P/C Surplus

U/W Loss ($ B)

Source: EQECAT, NCCI

In Summary

Negatives

• Low investment returns continue to put pressure on underwriting results

• Medical severity continues rapid growth

• Calendar year results lag behind other lines

• Uncertainties surrounding TRIA extension

Positives

• Results are improving

• Frequency continues to decline

• Industry making progress on reserve deficiency

• Residual Market burden still manageable

End of Presentation

Thank You