Embed Size (px)

Citation preview

i

WISCONSIN INTERNATIONAL UNIVERSITY COLLEGE

AN ASSESSMENT ON THE PERFORMANCE OF ALUWORKS LIMITED USING

FINANCIAL RATIOS FROM 2014 – 2016.

(A CASE STUDY OF ALUWORKS LIMITED GHANA)

BY

AGBO JOSHUA FORSON

(WIUC/03/5796)

&

MICHAEL ALIMO

(WIUC/03/6022)

A research work submitted to the Department of Business Studies of the

Faculty of Banking and Finance, Wisconsin International University College,

in the partial fulfillment of the requirements for award of Bachelor of Arts

Business Studies Degree in Banking and Finance.

JUNE, 2018

ii

DECLARATION

We hereby declare that this project work is the result of our own original research and that no part

of it has been presented for another degree in this university or elsewhere.

................................................. ..…………………………………….

AGBO JOSHUA FORSON (WIUC/03/5796) DATE

(STUDENT)

……………………………… ……………………………………….

MICHAEL ALIMO (WIUC/03/6022) DATE

(STUDENT)

Supervisor’s Declaration

I hereby declare that the preparation and presentation of the project work were supervised in

accordance with the guidelines on the supervision of the project work laid down by Wisconsin

International University College.

Supervisor’s Signature: …………………………. Date: ………………………

Name: Mr. Elias Megbetor

iii

ACKNOWLEDGMENT

First, we would like to thank our supervisor Mr. Elias Megbetor for his unreserved supervision

which led to the completion of this paper. In addition, our thanks go to the management and staff

members of Aluworks Limited especially to Wallace Dankwah, Human Resource Manager, for his

support to provide data for the study. Last but not least, we warmly acknowledged the contribution

of the late James Oblie for his effort to bring this study into reality.

iv

DEDICATION

We dedicate this project to our parents because they are the reason why we strived to make this

work a success.

v

ABSTRACT

This study attempts to look at the usage of financial ratios to assess the performance of

Aluworks Limited. The objectives of this study are to determine the performance of the company

with respect to profitability, liquidity and efficiency. The method employed involved the

conducting of interviews with management and some key employees. The financial statements

were used to compute the categories of ratios, analysed and presented. The key findings the study

revealed include the following; Inconsistency in the performance of Aluworks under the

profitability ratios, liquidity and especially for the return on capital employed. It also showed that

the company had a poor creditor’s collection period. The study brought to light that the company

was not liquid when comparing the current ratio performance to the standard current ratio.

Lastly, the interviews revealed that the company’s cost of sales and expenses were more than the

revenue generated.

vi

TABLE OF CONTENTS

DECLARATION .......................................................................................................................................... ii

ACKNOWLEDGMENT .............................................................................................................................. iii

DEDICATION ............................................................................................................................................. iv

ABSTRACT .................................................................................................................................................. v

CHAPTER ONE ........................................................................................................................................... 1

1.1 Introduction ............................................................................................................................................. 1

1.2 Statement of the Problem ........................................................................................................................ 1

1.3 Objective of the Study ............................................................................................................................ 2

General Objectives ........................................................................................................................................ 2

The Specific Objectives are: ......................................................................................................................... 2

1.4 Research Questions ................................................................................................................................. 2

1.5 Significance of the Study ........................................................................................................................ 2

1.6 Definition of Terms ................................................................................................................................. 3

1.8 Limitation of the Study ........................................................................................................................... 3

1.9 Organization of the Study ....................................................................................................................... 4

CHAPTER TWO .......................................................................................................................................... 5

LITERATURE REVIEW ............................................................................................................................. 5

2.0 Introduction ............................................................................................................................................. 5

2.1 Theoretical Review ................................................................................................................................. 5

2.1.1 Definition of Financial Ratios .............................................................................................................. 5

2.1.2 Ratio classification and analysis .......................................................................................................... 6

2.1.2.1 Activity ratios .................................................................................................................................... 6

2.1.2.2 Liquidity Ratios ................................................................................................................................ 7

2.1.2.3 Cash flow ratios ................................................................................................................................ 7

2.1.2.4 Debt/leverage ratios .......................................................................................................................... 8

2.1.2.5 Profitability ratios ............................................................................................................................. 9

2.2 Empirical Review of Literature............................................................................................................... 9

CHAPTER THREE .................................................................................................................................... 14

METHODOLOGY ..................................................................................................................................... 14

3.1 Introduction ........................................................................................................................................... 14

3.2 Research Design .................................................................................................................................... 14

3.3 Population ............................................................................................................................................. 14

vii

3.4 Sample size ........................................................................................................................................... 15

3.4.2 Primary Sources of Data .................................................................................................................... 15

3.4.3 Secondary source Data ....................................................................................................................... 16

3.5 Technique of Selection ......................................................................................................................... 16

3.6 Data collection Instrument .................................................................................................................... 16

3.7 Data Collection Procedure .................................................................................................................... 16

3.8 Data Analysis ........................................................................................................................................ 17

3.8.1 Profitability ratio ................................................................................................................................ 17

3.8.2 Efficiency ratio ................................................................................................................................... 17

CHAPTER 4 ............................................................................................................................................... 19

DATA ANALYSIS, RESULTS AND DISCUSSIONS ............................................................................. 19

4.0 Introduction ........................................................................................................................................... 19

4.1 Performance of Aluworks limited with respect to profitability. ........................................................... 19

4.2 Performance of Aluworks Limited with respect to efficiency. ............................................................. 22

4.3 Performance of Aluworks Limited with respect to Liquidity. .............................................................. 27

CHAPTER 5 ............................................................................................................................................... 29

SUMMARY, CONCLUSIONS AND RECOMMENDATIONS ............................................................... 29

5.1 Introduction ........................................................................................................................................... 29

5.2 Summary of Findings ............................................................................................................................ 29

5.3 Conclusion ............................................................................................................................................ 30

5.4 Recommendations ................................................................................................................................. 30

REFERENCES ........................................................................................................................................... 32

APPENDIX ................................................................................................................................................. 34

viii

1

CHAPTER ONE

An Assessment On the Performance of AluWorks Limited Using Financial Ratios From

2014-2016

1.1 Introduction

Measuring the performance of firms helps in assessing, evaluating and forecasting on what to do

next in the nearby future. (American Institute of Certified Public Accountant, 1994). Assessing a

firm’s performance using financial ratios has been a traditional yet powerful tool for

decision-makers, including business analysts, creditors, investors, and financial managers.

Financial ratio analysis can help stakeholders analyze the financial health of a company. Using

these financial ratios, comparisons can be made across companies within an industry, between

industries, or within a firm itself. Such a tool can also be used to compare the relative performance

of different size companies. Accounting and finance textbooks generally organize financial ratios

into classes including liquidity, profitability, long-term solvency, and asset utilization or turnover

ratios. Liquidity ratios evaluate the ability of a company to pay a short-term debt, whereas

long-term solvency ratios investigate how risky an investment in the firm could be for creditors.

Profitability ratios examine the profit-generating ability of a firm based on sales, equity, and

assets. Asset utilization or turnover ratios measure how successfully the company generates

revenues by utilizing assets, collecting receivables, and selling its inventories.

1.2 Statement of the Problem

Most organizations and businesses have some knowledge about how financial ratios are applied,

analyzed and translated. Despite companies putting in a lot of promising investments, the

ineffective application of financial ratios by some companies has led to the failure of their

investments. (Adegoke, 2007). Ratio analysis is a useful management tool that improves the

2

understanding of financial results and trends over time, and provides key indicators of

organizational performance. However, the ineffective use of financial ratios affects the company

in terms of assessing whether the company is performing well or not. As a result of this

phenomenon, this study focused on assessing the performance of AluWorks Ghana Limited using

financial ratios, analyzing and interpreting them.

1.3 Objective of the Study

General Objectives

The general objective of the study is to assess the performance of AluWorks Limited a 3year

audited financial statement.

The Specific Objectives are:

To evaluate the profitability performance of AluWorks Limited through the profit and

loss statement.

To evaluate the efficiency ratio of AluWorks limited in the course of the study.

To evaluate the performance of AluWorks Limited in relation to liquidity ratio.

1.4 Research Questions

What is the performance of AluWorks Limited in the terms of profitability ratio?

What is the performance of AluWorks Limited in terms of efficiency ratio?

What is the performance of AluWorks Limited in terms of liquidity ratio?

1.5 Significance of the Study

The importance of the study is to improve the financial performance of AluWorks Limited by

3

assessing their financial statements over a 3-year period. Furthermore, the findings from this study

will help us make relevant suggestions and recommendations that have the potential to improve

the performance of AluWorks. Financial ratios help the management in understanding the past and

present financial state of the company. These also provide a useful idea about the existing strength

and weaknesses of the company over a specific period of time. This knowledge is vital for the

management to plan and forecast the future of the company. Finally, applying financial ratios

properly helps to provide adequate information on efficiency and profitability of the company.

1.6 Definition of Terms

Financial ratios: A financial ratio is a relative magnitude of two selected numerical values

taken from an enterprise's financial statements.

Profitability ratio: It is the ratio that focuses on the profitability of the firm. Profit margins

measure performance with relations to sales. In other words, it indicates how well a firm is

performing in terms of its ability to generate profit.

Efficiency ratio: This measurement of how well a company can manage income and

expenses.

Liquidity ratio: It is the ratio that measures a firm's ability to meet its short-term financial

obligations on time.

Leverage ratio: this measures the relative contributions of stockholders and creditors and

of the firm's ability to pay financing charges.

1.8 Limitation of the Study

The study is expected to experience certain challenges in achieving its aims and objectives. This

4

includes limited time within which the study may be completed. The researcher will try as much as

possible to work within the specified time frame. Information on the financial report, books and

materials will be hard to get and the information may not be sufficient. The researcher will try as

much as possible to get all the information on the company's website.

1.9 Organization of the Study

This study is structured into five chapters.

Chapter one gives a brief description of the subject of study. It starts by presenting the background

of the study. It continues by providing the statement of the problem of the study, the aims and

objectives, research questions, definitions of the key concepts, the significance of the study, the

limitations of the study and finally, the structure of the study.

Chapter two discusses the theoretical positioning of the study as well as empirical studies on the

subject matter. The focus will be on theories and concepts on the subject matter.

Chapter three presents the study’s methodology and discusses the procedures used to obtain the

data, the reason for using the methods, the validity of the study, sampling procedures and

procedures for analyzing data. It will also provide statistical analysis of the study of findings.

Chapter four will focus on the analysis and discussions of the overall data gathered on the study

and the presentation of results.

Finally, chapter five will include discussions on the findings, conclusions and recommendations.

5

CHAPTER TWO

LITERATURE REVIEW

2.0 Introduction

This chapter reviews the theoretical and empirical literature relating to financial ratios.

2.1 Theoretical Review

'A financial ratio is a two or more line items from financial statements joined by a mathematical

operation. (Bailey 2012). Financial statements are the balance sheet, the income statement, the

statement of retained earnings and the statement of cash flow.

Financial statement analysis allows analysts to identify trends by comparing ratios across multiple

time periods and statement types. These statements allow analysts to measure liquidity,

profitability, company-wide efficiency and cash flow. There are three main types of financial

statements: the balance sheet, income statement and cash flow statement. Ratios are extracted from

financial statements to enable analysts to assess the strengths and weaknesses of a company.

The balance sheet is a snapshot in time of the company's assets, liabilities and shareholders' equity.

Analysts use the balance sheet to analyze trends in assets and debts. The income statement begins

with sales and ends with net income. It also provides analysts with gross profit, operating profit

and net profit. Each of these is divided by sales to determine gross profit margin, operating profit

margin and net profit margin. The cash flow statement provides an overview of the company's cash

flows from operating activities, investing activities and financing activities.

2.1.1 Definition of Financial Ratios

The quantitative relation between two amounts showing the number of times one value contains or

is contained within the other. (Patrick 2006)

6

2.1.2 Ratio classification and analysis

Financial ratios are generally classified into the categories discussed below:

2.1.2.1 Activity ratios

Activity / Turnover Ratios are a set of financial ratios used to measure the efficiency of various

operations of a business. Activity ratios measure the efficiency of the firm in using its resources/

assets. Those Ratios include:

• Accounts receivable turnover which is equal to net credit sales/average accounts

receivable.

• Accounts receivable period (the number of days’ purchases in receivables) which is equal

to 360 days/accounts receivables turnover.

• Inventory turnover which is equal to Cost of goods sold/ average inventory.

• A number of days inventory which is equal to (inventory/cost of goods sold) *360.

• Accounts payable turnover which is equal to the cost of goods sold/average accounts

payable.

• Accounts payable period (the number of days’ purchases is payables) which is equal to 360

days/accounts payable turnover.

• Assets turnover which is equal to net sales/ average total assets (Delta, 2006:64).

Delta (2006) says that in the absence of information on whether sales or purchase are made on

credit or cash, an assumption can be made that all sales and purchases are on credit basis.

7

2.1.2.2 Liquidity Ratios

Liquidity ratio refers to the ratio between the liquid assets and the liabilities of a bank or other

institution. This includes:

• The current ratio is an indicator of a firm's ability to meet short-term financial obligations.

It is the ratio of a current asset to current liabilities. Though every industry has a range of

acceptable current ratios, a ratio of 2:1 is considered desirable in most sectors. Since

inventory is included in the current asset, acid test ratio is a more suitable measure where

salability of inventory is questionable. The current ratio is equal to current assets/current

liabilities.

• Quick (acid-test) ratio is a key measure of a firm's liquidity. It answers the question " can

this firm meet its current obligations from its liquid asset if suddenly all sales stop?".

Usually, an acid test ratio of 1.0 or higher is considered satisfactory by lenders and

investors. Acid test ratio is equal to (current assets - inventory)/current liabilities.

2.1.2.3 Cash flow ratios

Cash flow ratio is a measure of how well current liabilities are covered by the cash flow generated

from a company's operations. The operating cash flow ratio can gauge a company's liquidity in the

short term. Cash flow ratio is a measure of how well current liabilities are covered by the cash flow

generated from a company's operations. The operating cash flow ratio can gauge a company's

liquidity in the short term. This includes:

• Cash flow to average total current liabilities;

8

• Cash flow and bank to total assets;

• Cash flow and bank to current liability;

• Cash flows from operating activities/operating income;

• Cash flows from operating activities/net income;

• Cash flow return on assets which is equal to (Cash flows from operating activities +

interest paid + taxes paid)/average total assets; and

• Cash flow return on equity which is equal to (Cash flows from operating activities -

preferred dividends paid)/average common stockholders' equity (Delta Publishing,

2006:117).

2.1.2.4 Debt/leverage ratios

A leverage ratio is any kind of financial ratio that indicates the level of debt incurred by a business

entity against several other accounts in its balance sheet, income statement, or cash flow statement.

• Debt ratio which is equal to average total liabilities/average total assets.

• Debt to equity ratio which is equal to total liabilities/stockholders' equity.

• Equity to total assets which is equal to shareholders' equity/total assets.

• Times interest earned which is equal to income before interest and taxes (EBIT)/interest

expense (Delta Publishing, 2006:76).

9

2.1.2.5 Profitability ratios

Profitability ratios are a class of financial metrics that are used to assess a business's ability to

generate earnings compared to its expenses and other relevant costs incurred during a specific

period of time. These ratios include:

• Gross profit margin is a measure of a company's profitability that is expressed as a

percentage of gross profit. It is calculated by dividing gross profit by revenue which is

equal to gross profit/net sales.

• Net operating income which is equal to operating income/net sales.

• Return on total assets (ROA) which is equal to net income/average total assets.

• Return on equity (ROE) which is equal to net income/shareholders’ equity.

• Return on investment (ROI) which is equal to net income/average total assets.

Earnings per share (EPS) which is equal to net income available to common

shareholders/weighted average number of common share outstanding (Delta Publishing, 2006:84).

2.2 Empirical Review of Literature

Adegoke in the year 2007 conducted a research in Nigeria about the relationship between financial

ratios and corporate profitability. The researcher applied financial ratio analysis to assess the

performance of some firms in Nigeria. The researcher found out that some promising investment

in Nigeria has turned out to be a failed investment due to the lack of inadequate use of financial

ratios. He also found out that in developing countries like Nigeria, few studies have been carried

out with respect to the corporate profitability of the Oil and Gas Industry.

10

Fraser & Ormiston in the year 2004 conducted a research in Texas USA on a measure of short-run

solvency. The researcher applied financial ratios to determine the short run solvency of the

company. The researcher found out that the available cash resources came primarily from cash or

the conversion of a current asset to cash. Fraser & Ormiston defined current ratio as the ability of a

firm to meets it debts requirement as they come due.

Clausen in the year 2009 conducted a research in Kenyatta University Cisco Networking Academy

Kenya, about the profitability ratio analysis of income statement and balance sheet. He applied

financial ratios as a measure of assessing university’s financial statement. He found out that both

the income statement and balance sheet are two important reports that can be used to assess the

performance of the firm considering profitability, activity ratio, ROE and ROA. He also indicated

that income statement shows the net profit of the company by subtracting expenses from gross

profit (sales – the cost of goods sold). He said that the balance sheet does not report profits alone

but also looks at the relationship between assets and profit.

Capkun et al in the year 2009 conducted a research in Poland to study on the relationship between

inventory performance, both total inventory (INV) and its discrete components (Raw Material

(RMI), Work-in-Process (WIP) & Finished Goods (FGI)) and financial performance of

manufacturing companies. The researchers applied correlation method to know the relationship

between inventory performance and the financial performance of the manufacturing industry. It

was found out that, there was a positive relationship between inventory performance and the

financial performance of the manufacturing industry.

Mohammadzadeh et al in the year 2013 conducted a research in Iran to study the relationship

between the profitability of pharmaceutical companies in Iran and the capital structure. Net profit

11

margin was expressed as an indicator of profitability and capital structure. It was found out that

there was a negative relationship between capital structure and profitability of the company.

Anjum in the year 2013 conducted a research in Pakistan in cement industry to study the

relationship between working capital management and profitability of the cement industry.

Regression analysis was used to determine the relationship between working capital management

and profitability of cement industries. It was found out that, there was an inverse and positive

relationship between working capital management and profitability of cement industry in Pakistan.

Sayeed and Hogue in the year 2009 conducted a research in Bangladesh on the impact of asset and

liability management; a study on the public versus the privately owned commercial banks in

Bangladesh. This study examined how inflation rate, the degree of market concentration could

impact the profitability of selected commercial banks in Bangladesh. The study adopted a

regression model. The regression results showed that the use of total income the dependent

variable for private and public banks was evidenced that asset had a significant contribution to the

total income of private banks.

Dave in the year 2012 conducted a research on the relationship between financial management and

profitability of the Indian Pharma sector for a period of 10years. The study adopted ratio analysis

to establish the link between financial management and profitability of Indian Pharma sector. It

was found out that, Total Asset to Sales Ratio and Creditors Velocity are the core variables

improving the profitability of the company.

Vanitha. S and Selvam. M in the year 2007, conducted a research in India on how a company’s

financial performance can be analyzed through ratios, t-test, mean and standard deviation.

Financial ratios standard deviation, t-test and mean were applied to the study. The findings pointed

12

out that the overall financial performance of merged companies in respect of various variables was

not significantly different from the expectations.

Antoniou et al in the year 2007 conducted a research on the relationship between leverage ratio and

a physical asset on the firm’s performance in Oman. Financial ratios were used to determine the

relationship between leverage ratio and physical asset. The finding pointed out that there was a

positive influence of leverage ratio and physical assets on the firm’s performance. The researchers

also argued that leverage ratio which positively affects firm performance is also influenced by

conditions that are driven by market forces within the business environment.

Amato and Burson in the year 2007 conducted a research on service industries with respect to their

size and profitability. The study was conducted in a Malaysian financial sector on 172 firms. The

study applied financial ratios to do the comparison. The findings pointed out that regardless of the

size of firms, it can still attain higher profit.

Jonsson in the year 2007 conducted a research in Iceland on the relationship between size and

profitability of the firms operating in Iceland. Financial ratios were used for the study to determine

the relationship between profitability and size of the firm. The findings pointed out that, larger

firms have a higher profitability as compared to smaller firms.

Manyo et al in the year 2013, conducted a research in Nigeria on the effect of the number of days’

account receivables on return on asset of some selected Nigerian firms from 2000-2009 by the use

of regression analysis. From the study, it was found out that the days’ accounts receivable had a

negative relationship with the profitability which was measured by the return on assets. The study

concluded that profitability increased with a decrease in day’s accounts receivable.

13

Gill, Biger and Mathur in the year 2010, conducted a research in the USA on the relationship

between working capital management and the profitability of 88 companies listed on the New

York Stock Exchange from 2005-2007. The study applied regression analysis for the study. The

findings pointed out a strong association between the cash conversion cycle and profitability,

hence concluding that profits can be boosted by properly handling the cash conversion cycle and

optimizing debtors’ level.

14

CHAPTER THREE

METHODOLOGY

3.1 Introduction

This chapter provides an account of how the research was designed and conducted. This study

seeks to evaluate the performance of Aluworks Limited using financial ratios. This chapter

discusses the research design, the population of the study, sample size, sample techniques,

procedure of data collection, data reliability and finally, data analysis.

3.2 Research Design

In order to evaluate the performance of Aluworks Limited, quantitative research was adopted for

the study. Quantitative research attempts to establish why it is that way or how it came to be. The

purpose of this research design is to assess Aluworks performance with respect to profitability,

efficiency, liquidity and also take action to improve future performance in an essential element of

quality management. The study also adopted quantitative research which seeks to emphasize

objective measurement and analysis of numerical data collected.

3.3 Population

A study population is the entire mass of observations, which is the parent group from which a

sample is to be formed (Singh, 2006). Korb in the year 2012 defined a population as a group of

people that the researcher wants to draw a conclusion on once the research study is finished. The

average population for the study was eight (8) employees. Asiamah et al in the year 2017 indicated

that, more often than not, the general population included people who are not eligible to be a part

of the population because they do not possess certain characteristics which are in the researcher’s

interest. In this regards, certain criteria were set to scrutinize the population to get a desirable

population. The researcher’s criteria index included:

15

The individual must be a recognized staff of Aluworks Limited

The individual must be a permanent worker

The individual must be an administrative staff who has worked with the company for

relatively a longtime.

3.4 Sample size

Sample size is the act of choosing the number of observations or replicates to include in a

statistical sample. The sample selected were three of the population size. In the sample design, the

researcher used purposive sampling where there were defined characteristics of the persons to be

included in the sample. These were those dealing in financial and strategic management areas and

how financial planning can help in improving financial performance. For this purpose, the

population had predetermined characteristics. The three (3) respondents had more knowledge

about the performance of the company.

3.4.1 Sources of Data

The study used both primary and secondary data.

3.4.2 Primary Sources of Data

Primary data was used for study. Primary data refers to the firsthand collection of data for a

particular purpose. The data was collected through interviews from employees of Aluworks

Limited, Tema.

16

3.4.3 Secondary source Data

Secondary data refers to data that was collected by someone other than the user. Data was

collected from the company’s website in the form of financial report and annual report from 2014

to 2016.

3.5 Technique of Selection

The technique adopted for the selection was a purposive sampling. The reason for this technique is

that the respondents had more knowledge pertaining to the company’s performance and were in

the best position to clarify issues pertaining to the company’s performance.

3.6 Data collection Instrument

McNamara in the year 1999 defined interviews as a qualitative research technique which involves

conducting intensive individual interviews with a small number of respondents to explore their

perspectives on a particular area. Interviews were picked as information gathering methods in light

of current circumstances. Interviews serves as a means of verifying information obtained through

application form and test. The interview questions designed by the researcher were open ended

questions. The questions were to seek respondent view on the performance of Aluworks Limited.

The researcher gave the respondent the opportunity to express themselves without interruptions

and to clarify all information asked on the subject matter.

3.7 Data Collection Procedure

This sub-section of the methodology explains how data was collected for the study. Central to the

data collection aspect of research design, secondary data were also collected such the company’s

financial statement and annual report from 2013 to 2016. The method that was adopted for the

17

collection of secondary data was through Aluworks Limited Website. Prior to the data collection,

the researchers sought permission to carry out the research from Aluworks Limited. An

introductory letter from the Department of banking and finance under the Faculty of Business

Studies would be sent to Aluworks limited, Tema indicating that the research is for academic

purposes only. Upon approval, the researcher was given the green light to conduct the interviews

and issues that needed clarifications were discussed dispassionately and reached a conclusion.

3.8 Data Analysis

Data analysis is a procedure of assessing, purifying, changing, and demonstrating information with

the objective of finding valuable data, proposing conclusions, and supporting basic leadership. In

this study, data was analyzed and shown in a tabular form to ease contrasting and to appreciate the

findings from the study. Data was analyzed using financial ratio. Financial ratios are relationships

determined from a company’s financial information and used for comparison purposes. Some of

the ratios used for the study included profitability ratio, net profit margin ratio, efficiency ratio,

and liquidity ratio.

3.8.1 Profitability ratio

The profitability ratio consisted of gross profit margin and net profit margin. Gross profit margin is

calculated as gross profit/sales*100. The net profit margin is calculated as profit before interest

and tax/sales*100.

3.8.2 Efficiency ratio

Efficiency ratio is typically used to analyze how well a company uses its assets and liabilities

internally. An efficiency ratio can calculate the turnover of receivables, the repayment of

18

liabilities, the quantity and usage of equity, and the general use of inventory and machinery. This

ratio can also be used to track and analyze the performance of companies.

An efficiency ratio measures a company's ability to use its assets to generate income. For example,

an efficiency ratio often looks at aspects of the company, such as the time it takes to collect cash

from customers or the amount of time it takes to convert inventory to cash. This makes efficiency

ratios important, because an improvement in the efficiency ratios usually translates to improved

profitability.

These ratios can be compared to peers in the same industry and can identify businesses that are

better managed relative to the others. Some common efficiency ratios are accounts receivable

turnover, fixed asset turnover, sales to inventory, sales to net working capital, accounts payable to

sales and stock turnover ratio.

It is calculated as a company’s Expenses / Revenue. However, interest expense is not included in

this formula.

19

CHAPTER 4

DATA ANALYSIS, RESULTS AND DISCUSSIONS

4.0 Introduction

Under this section the researchers presented and analyzed the data which have been gathered from

the company’s secondary and primary data sources. Hence the data presented here have been

presented in the form of tables (as per annexed) and figures, they are expressed in percentages. The

data which have been presented and analyzed on the figures have also been interpreted in words

for answering the research questions. The researcher applied selected financial ratios from a

framework of different researchers of various studies related with financial performance

evaluation of a company.

4.1 Performance of Aluworks limited with respect to profitability.

Table 1. Computation of Profitability Ratio Result from 2014-2016

Source: Field survey 2018

Gross profit margin measures a company’s profitability that is expressed as a percentage of gross

profit. It is calculated by dividing gross profit by revenue.

From the table, the gross profit of Aluworks limited increased by 14.98% in 2014. In the year

2015, it was 12% and then declined in 2016 by 11.88%. From the table above, it can be seen that

Ratios 2014 2015 2016

GROSS PROFIT

MARGIN

14.98% 12% 11.88%

NET PROFIT

MARGIN

-2.1% -0.1% -4.2%

20

Aluworks limited was better off in 2014 than in the previous year (2015 and 2016). This means

that, Aluworks limited had no control over the cost of sales and also, when expenses is more than

sales, it can lead to a decrease in gross profit.it is important to note that more expenses can cause

expenses to go up.

Source: Field survey 2018

The bar graph above depicts a graphical representation of the Gross profit margin of AluWorks

Limited. Gross profit shows how cost was controlled in manufacturing aluminum products. From

2014-2016, the costs of manufacturing these products were not controlled and as result of that,

gross profit declined. In the graphical representation above, gross profit increased in

2014(14.98%) and then declined in 2015(12%) and 2016(11.88%).

From this observation, it means that 2014 recorded the highest gross profit margin of 14.98%,

which tells us that AluWorks Limited had more cash flow to spend in its operations. In 2016, the

14.98%

12% 11.88%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

2014 2015 2016

Gross Profit Margin

21

company recorded the worst gross profit margin of 11.88%. This means that the company was

unable to control cost to some degree. The only drag on gross profit margin is the cost of goods

sold.

Net Profit Margin from 2014-2016

Source: Field survey 2018

Net Profit Margin looks at the percentage of revenue left after all expenses have been deducted

from sales. From the table above, Aluworks limited recorded a loss from 2014 to 2016. Thus,

-5.72%, -18.8% and -27.8% respectively. This occurs when cost exceeds revenue. From the report

on Aluworks website, the Company incurred a net loss for the year ended 31 December 2016 of

(GH¢ 19,314,000), (2015: GH¢14,810,000), (2014: GH¢ 4,400,000) and as of that date, its current

liabilities exceeded its current assets by GH¢ 29,182,000 (2015: GH¢ 27,751,000) and (2014:

GH¢27,751,000). From this point of view, Aluworks Limited had continued to make losses

consistently from 2014-2016. This was as a result of Aluworks limited having an overdraft facility

-2.10%

-0.10%

-4.20%

2014 2015 2016

Net Profit Margin

Net Profit Margin

22

of GH¢ 5million with Ecobank Ghana Limited to finance the purchase of raw materials stocks,

spares and other operational tools at an interest rate of 6% per annum and also had an overdraft

facility of GH¢ 2.1 million with Societe Generale Ghana Limited. This overdraft facility was used

to finance working capital. Aluworks limited also obtained a facility of $ 10 million from Social

Security and National Insurance Trust to finance the acquisition of second cold rolling under the

terms of a six-year convertible bond with two years moratorium. Therefore, Aluworks limited has

not been performing well with respect to profitability ratio.

4.2 Performance of Aluworks Limited with respect to efficiency.

Table 2

Source: Field survey 2018

Return on capital employed is a type of measurement where by capital investments made by a

company are then measured concerning profitability as well as their overall efficiency. In other

words, return on capital has to do with efficiency. That is the full utilization of the assets. From the

table, Return on Capital Employed was -2.6%, -0.3% and -3.1% respectively. This indicates that

Efficiency Ratio 2014 2015 2016

Return on Capital

Employed

-2.6% -0.3% -3.1%

Debtors Collection

Period

22 days 25 days 12 days

Creditors Collection

Period

119 days 125 days 142 days

Asset Turnover 0.53times 0.58 times 0.35times

23

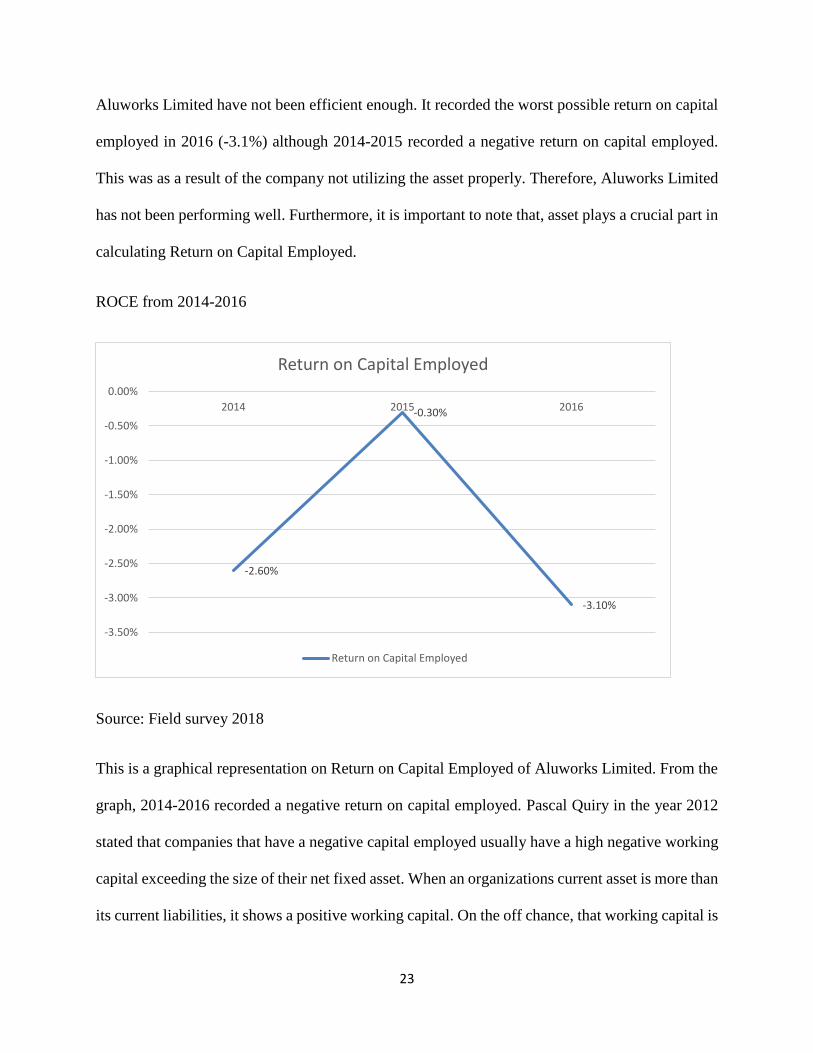

Aluworks Limited have not been efficient enough. It recorded the worst possible return on capital

employed in 2016 (-3.1%) although 2014-2015 recorded a negative return on capital employed.

This was as a result of the company not utilizing the asset properly. Therefore, Aluworks Limited

has not been performing well. Furthermore, it is important to note that, asset plays a crucial part in

calculating Return on Capital Employed.

ROCE from 2014-2016

Source: Field survey 2018

This is a graphical representation on Return on Capital Employed of Aluworks Limited. From the

graph, 2014-2016 recorded a negative return on capital employed. Pascal Quiry in the year 2012

stated that companies that have a negative capital employed usually have a high negative working

capital exceeding the size of their net fixed asset. When an organizations current asset is more than

its current liabilities, it shows a positive working capital. On the off chance, that working capital is

-2.60%

-0.30%

-3.10%

-3.50%

-3.00%

-2.50%

-2.00%

-1.50%

-1.00%

-0.50%

0.00%

2014 2015 2016

Return on Capital Employed

Return on Capital Employed

24

incidentally negative, it regularly demonstrates that the organization had acquired a huge money

expense or a considerable increment in its records payable because of an extensive buy of items

and administrations from its sellers. In the annual report of Aluworks limited, it stated that its

current asset was less than the current liabilities. In the financial statement of Aluworks limited,

2014’s current asset was less than its current liabilities. Thus, GH¢ 22,626,000 as against GH¢

51,809,000. The same goes for 2015 and 2016 having its current asset less than its liabilities. In the

light of event pertaining to a negative return on capital employed, Aluworks limited performance

has been poor consistently from 2014-2016.

Table 3: Debtor Collection Period from 2014-2016

Source: Field survey 2018

Debtor collection period looks at how organizations are able to collect their debt from people who

owe the company. In other words, it is the period taken by an organization to collects its money

owed to it by its debtors.

The table above shows the performance of Aluworks Limited under the efficiency ratio category.

Debtors ratios showed the following result from 2014-2016; 22, 25 and 12 all in days respectively.

Based on the calculation on debtors’ collection period, Aluworks limited did well in collecting

their debt on time. In the year 2016, its debtors’ collection period was 12 days, which means that

the company has been making sure that debt owed is paid back on time. With respect to 2014 and

2015, debtors’ collection period was poor as against 2016. This indicates that its debtors’

collection policy has improved. In the annual report pertaining to credit risk, the company

Debtor Collection Period 2014 2015 2016

Days 22 25 12

25

established a credit policy under which a new customer is assessed before credit is issued to the

customer. The company generally trades with pre-defined and selected customers. Credit exposure

on trade receivable is covered by guarantee from well-established banks. Therefore, from this

observation, Aluworks limited has a good credit policy.

Table 4: Creditors Collection Period from 2014-2016

Source: Field Survey 2018

Creditors’ collection period is an indication on how a company is able to pay off its debt. It

actually gives information about the payment habit of a company and whether the company is

taking full advantage of paying off its debt. The table above shows the performance of Aluworks

Limited under the efficiency ratio category. Creditor’s collection period showed the following

result from 201-2016; 119, 125 and 142 all in days respectively. Based on the calculation con

creditors’ collection period, Aluworks limited did not perform well as expected of them. In the

year 2014, the company used 119 days to pay off its debt and used 125 days to pay off its debt. In

the year 2016, the company used 142 days to pay off its debt. This means that, the company has not

been performing well lately.

Creditors Collection Period 2014 2015 2016

Days 119 125 142

26

Table 5: Total Asset Turnover from 2014-2016

Total Asset

Turnover

2014 2015 2016

Number of times 0.53 0.58 0.35

Source: Field survey 2018

Total asset turnover indicates how a firm is in utilizing its assets and in generation of sales revenue.

In other words, it shows how many times the company is able to sell of its assets to meet their debt.

Total asset turnover is calculated sales/total asset. It can often be used as an indicator of efficiency

when a company is deploying it asset in generating sales. With respect to Total Asset Turnover, a

higher ratio is considered desirable, but what is considered high in one industry may be low for

another. Total Asset Turnover is equal to sales divided by total asset. From the table above, figure

4.2.3, Total Asset Turnover ratio were as follows, 0.53, 0.58 and 0.35 all in times.

Based on the analysis above, 2015 recorded the highest turnover ratio and then declined in 2016 by

0.35. There had been a steady increase in asset turnover from 2014-2015 and then declined in 2016

by 0.35 times. This means that, Aluworks Limited turned over their asset 0.35times or one-third

during the year. In other words, for every cedi that was invested in asset, the company generated

GH₵ 0.32 of net sales in 2016. This means that Aluworks Limited was not efficient enough in

utilizing its asset.

27

4.3 Performance of Aluworks Limited with respect to Liquidity.

Table 6: Computation of Liquidity Ratio results from 2014 to 2016

Liquidity Ratios 2014 2015 2016

Current ratio 0.63:1 0.46:1 0.44:1

Acid test 0.22:1 0.13:1 0.07:1

Source: Field survey 2018

Liquidity ratio has to do with the company’s available cash and marketable securities against

outstanding debt. This ratio measures the company’s ability to pay off its short term debts. A

higher ratio indicates a company with a low risk of default. The table above shows the performance

of Aluworks Limited under the liquidity ratio category. Liquidity ratio comprises of current ratio

and acid test. Current ratio is calculated as current asset/current liabilities. From the table above,

Aluworks limited can meet its short term financial obligations as and when they fall due from 2014

to 2016 are as follows; 0.63, 0.46 and 0.44. Though every industry has its own range of acceptable

current ratio, a ratio of 2:1 is considered desirable in most sectors. In other words, the company has

a good financial background and below that will mean that the company is in financial crises.

Aluworks limited recorded the highest current ratio of 0.63 and then declined in 2015 and 2016.

This however is below the industry standard and that we can say that Aluworks limited is in

financial crises. Therefore, the company has not been performing well as expected.

Acid test ratio measures the firm’s liquidity and it answers the question” can this firm meets its

current obligations from its asset if suddenly all sales stop?” Acid test is calculated as current

asset –inventory/current liabilities. From the table above, acid test was as follows; 0.22, 0.13 and

0.07 all in tines. From this analysis, 2014 had the highest acid test ratio and then declined in 2015

and 2016 respectively. Usually an acid test ratio of 1.0 is considered desirable by lenders and

28

investors. Therefore, the company’s acid test ratio is less than the industry standard. Therefore,

Aluworks limited has not been performing well in meeting its current obligation if suddenly

all-sales stops.

29

CHAPTER 5

SUMMARY, CONCLUSIONS AND RECOMMENDATIONS

5.1 Introduction

This chapter covers the summary of the findings, the conclusions and recommendations that were

made by the researchers.

5.2 Summary of Findings

It was found out that there was no consistency in the performance of the company under the

profitability ratio. Table 1 shows, for example that the profitability of the company in 2014 was

14.93% which was then decreased to 12% in 2015, and lastly, decreased to 11.88% in 2016.This

shows inconsistency in the profitability level of the company. This was as a result of a decline in

operating profit and a decline in sales. From 2014-2016 sales declined and there was an operating

loss. However, it’s possible to increase your sales revenues and suffer a profit decrease.

1. The efficiency ratio from table 2 revealed a good debtor’s collection period. According to

the annual report Aluworks limited had a credit collection policy to which credit is given to

the consumer. The company established a credit policy under which a new customer is

assessed before credit is issued to the customer. The company generally trades with

pre-defined and selected customers.

2. The study showed that the performance of Aluworks limited under the efficiency ratio,

revealed a poor creditors collection period. It is poor when the company delays in paying of

their debt. That is to say that Aluworks limited have not been paying of their debt on time.

3. It was found out that, with respect to total asset turnover, there has been a steady increase

from 2014-2015 and then later declined in 2016. This means that for every cedi that was

invested in asset, the company generated GH₵ 0.53 of net sales in 2014, 0.58 in 2015 and

30

0.35 in 2016. This means that Aluworks Limited was not efficient enough in utilizing its

asset.

4. It was found out that the current ratio of Aluworks Limited was less than one. This was

below industry level. The industry standard for current ratio is one (1). This was as a

result of liabilities exceeding total current asset.

5. It was found out that return on capital employed for 2014 which was -2.6% decreased and

increased to -0.3% in 2015 and later on decreased to -3.1% in 2016. This shows

inconsistency in the return on capital employed.

6. It was found out that Acid test ratio of Aluworks Limited was also less than one, which

means that the company do not have enough liquid asset to pay their current liabilities and

should be treated with caution. Therefore, the company’s current asset is highly dependent

on inventory.

5.3 Conclusion

Based on the discoveries of the investigation it can be inferred that financial ratios can help

organizations to decide their financial strength. It can likewise push investors and forthcoming

investors or prospective shareholders to settle on cool headed choices to hold shares, buy more

share or to sell off the shares. In addition to that, it likewise indicates how management are

performing based on the investors or speculators inputs.

5.4 Recommendations

From the findings and conclusions, it can be recommended that, much effort should be put in by

management towards its to continue to have either constant increase in their performance under the

31

profitability ratio, liquidity ratio, and efficiency ratio especially for return on capital employed

(ROCE).

Secondly, the company should come up with a policy to tackle the problem of creditor’s collection

period. As such, the company should pay off their debt on time in order to build a good repute for

the company. This will give the company a good name and will turn increase efficiency.

Thirdly, it is recommended that the company can improve its asset turnover by focusing on

increasing revenue. Also, obsolete and unused assets should be liquidated. This means that, assets

that are not used frequently should be analyzed to see whether there is a sense in retaining those

assets.

It is also recommended that the company should assess their overhead cost and see if there are any

opportunities to decrease overhead cost such as rent, indirect cost, indirect labor etc. Decreasing

overhead cost can have a direct impact on profitability.

32

REFERENCES

Adegoke. (2007). Innovation types and innovation management practices in service companies",

International Journal of Operations & Production Management, Vol. 27 Issue: 6,

pp.564-587.

Amato, L. H. (2007). The effects of firm size on profit rates in the financial services. Journal of

Economics and Economic Education Research, Vol. 8, Issue 1, pp. 67 – 81.

Antoniou A, G. Y. (2008). The Determinants of Capital Structure: Capital Market Oriented versus

Bank Oriented Institutions.

Capkun, V. A. (2009). On the relationship between inventory and financial performance in

manufacturing companies. International Journal of Operations & Production

Management, 29(8): 789-806.

Dave, A. (2012). . Financial management as a determinant of profitability: A study of Indian

pharma sector. South Asian Journal of Management, 19(1): . 124.

Frase, L. &. (2004). Understanding Financial Statements. New Jersey: Pearson Prentice Hall.

Gill, A. N. (2010). The Relationship between Working Capital Management and Profitability:

Evidence from the United States. Business Economics Journal.

James, C. (2009). Accounting 101 – Income Statement: Financial Reporting and Analysis of Profit

and Loss”, Journal of income statement.

James, C. (2009). Accounting 101 – Financial Statement Analysis in Accounting: Liquidity Ratio

Analysis Balance Sheet Assets and Liabilities”, Journal of financial statement.

Lee, S. (2008). Ownership Structure and Financial Performance: Evidence from Panel Data of

South Korea. Corporate Ownership and Control, 6(2), 1-30.

Manyo. (2010). The effect of accounts receivable on return on assets of selected Nigerian firms.

International Journal of Current Research Vol. 5, Issue, 12, pp.3767-3772.

Rehman MU, A. N. (2013). Determination of the Impact of Working Capital Management on

Profitability: An Empirical Study from the Cement Sector in Pakistan. Asian Economic and

Financial Review3 (3): 319-332.

Sayeed. M. A. and Hogue, M. S. (2009). Impact of Assets and Liability Management on

Profitability: A Study of Public vs Private Commercial Bank in Bangladesh.

33

Vanitha, S. a. (2007). Financial Performance of Indian Manufacturing Companies during Pre and

Post Merger “International Research Journal of Finance and Economics, Page

No12:7-35.

34

APPENDIX

Wisconsin International University College Ghana

Department of Banking & Finance

These questions for interview are being used to collect information on the ‘The performance of

Aluworks Limited’. You will be contributing greatly to this study if you could objectively respond

correctly to these questions. Please, the responses will be treated confidentially, because the study

is for academic purpose only.

Interviews Schedule

1. Why has Aluworks limited been recording loss for the past four years?

2. Has Aluworks limited been efficient enough in utilizing its asset?

3. Does the company go for loans to finance their operations?

4. What is Aluworks’ credit policy?

5. What is the performance of the company with respect to liquidity?

6. Has the company’s debtor’s collection period improved overtime?

7. Has the company’s creditors’ collection period improved overtime?

35