Embed Size (px)

Citation preview

1

Wireless Internet Code

NETWORK: AVCCODE: B0850965C7

2

Chair’s Welcome

John Higgins CBE,Director General, Intellect

Keynote Address

Jon Fredrik Baksaas,President and CEO,Telenor

3

Jon Fredrik BaksaasPresident and CEO

Keynote address

FT World Telecoms Conference, London, 3rd November 2008

Home and away | Long-term commitment

2007Exit Austria

1994Russia

2000ThailandMalaysia Denmark

Exit IrelandExit Germany

2006Serbia

1998Ukraine

GermanyRussia (VIP)

1996Austria

Bangladesh

1993Hungary

1997Greece

2005SwedenPakistan

2004Exit Greece

1995Ireland

Montenegro

2008India

Coming out of the 1987

financial crisis

Financial crisis (Russia, Asia..)

Present crisis

dotcom crash/UMTS

licensing

• 12 mobile markets at present with 159 million subscriptions• Expected service launch in India mid 2009• More than 15 years in CEE and 12 years in Asia

4

Source: Markets with highest number of net additions, reported and calculated data (Wireless Intelligence, 30.10.08)

Number of net mobile additions Q308

Market penetration Q208

Rank

72 %

84 %

91 %

67 %

125 %

27 %

124 %

41 %

55 %

57 %

88 %

51 %

72 %

26 %

44 %

2,314,960Philippines15

2,364,136Turkey14

2,630,294Thailand13

2,872,984Mexico12

3,177,721Germany11

3,341,965Bangladesh10

3,721,134Russian Federation9

3,874,825Nigeria8

3,906,242Iran7

4,161,447Vietnam6

5,843,062USA5

5,929,503Pakistan4

5,977,965Brazil3

22,072,094India2

25,697,739China1

Present position | In high growth markets

Financial services

Innovation | In all markets

Insurance

Community services

Health services

M2M

Mobile services play a wider role in low income countries than in high income countries

5

Opportunities | Broadband and new services

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

4 500

5 000

2000 2002 2004 2006 2008 2010 2012

Mill

?Total internet subscriptions

Mobile voice subscriptions

Fixed broadband household subscriptions

Mobile

Inte

rnet

Pers

onal

Inte

rnet

Access to the Internet will have the same deep changing impact on people’s lives as the mobile phone

During my 15 minutes, another 17 000 people world wide have connected to a mobile network…

Closing words | Is the boom over?

6

Emerging Markets – Is The Boom Over Or Is It Just Beginning?Doug Richard, Founder, Cambridge Angels, and Chairman & CEO,

Trutap

Michael O'Brien, Director and Senior Analyst, Standard and Poor’s

Carlos Winzer, SVP and Senior Analyst for the Telecoms Sector, Moody’s Investors Service

Bashar Arafeh, COO East Africa Region, Zain

Rating ConsiderationsFor a Home and Away Strategy

Carlos WinzerSenior Vice President

Presentation at

FT World Telecoms Conference

3 November 2008

Presentation at

FT World Telecoms Conference

3 November 2008

7

Home and Away common strategy

Maintain a strong position in the domestic market, despite of a challenging environment in both segments

Focus on broadband

Strict cost control

Growth from existing international operations

Seek for opportunities in emerging markets

Increasing contribution from international diversification

Criteria to identify an opportunity in an emerging market:

1) High growth potential

2) Forward looking telecom policy

3) Investment friendly climate

4) Regulation that permits an acceptable ROR on investment.

5) Acceptable political and economic situation

In Moody's experience, penetration grows faster than

expected, number of subscribers is very high, but Arpu is

lower than planned and capex higher.

8

Options companies have

Stand still and continue to search for attractive opportunities (Belgacom).

Try to acquire an existing company with broad emerging market exposure (FT/TeliaSonera).

Acquire a target company in emerging markets.

Acquire a license and start from scrach

For those already exposed, continue to enhancethe footprint through either bolt-on acquisitions, adjacent ones or in different and non relatedmarkets.

International Diversification Increasingly in Focus

Substantial investments in the past

Contributor to revenue growth

Risk profile is greaterRevenue and cash flow mix changing

Increasing contribution from international diversification

Revenues split

0.0%

25.0%

50.0%

75.0%

100.0%

Telenor

TEF DT FTOTE

Magya

r

Belgac

om

Domestic International

9

What to look for when an acquisition is proposed

Is a consistent strategy being followed ?

Is the price “fair” ?

Funding structure

Liquidity and refinancing strategy. Change in ownershipcovenants. Recourse Vs Non recourse debt of target

Shareholder agreements/dividend policy

Integration risk/Synergies

Corporate structure and cash up-streaming mechanism

Growth potential in emerging marketsWireless Penetration Comparison with China

41.4%

20.3%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

China IndiaWireless Penetration

Subscriber Addition Comparison (1)

0.41.5 1.7

2.8

5.45.44.7 5.2 5.5

4.95.6

7.2

0.4 0.81.5

3.24.3

2.2 1.70.5 0.5 1

1.6 1.7 1.21.8

0.2

6.9

0

2

4

6

8

10

2001 2002 2003 2004 2005 2006 2007

Net

Add

s- S

ubs

(mm

)

India China Rusia Brazil

Source: NL Research, Global Wireless Matrix 24 Dec 2007(1) Average net adds per month

Subscriber Addition Growth has accelerated in last 2 years

10

Growth potential in emerging markets

Sub Sahara African subscribers will reach 400 million by 2017; Penetration 45%+

0

50

100

150

200

250

300

350

400

450

2006 2007 2008e 2009e 2010e 2012e 2017e

Mob

ile S

ubsc

riber

s (m

m)

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

50.00%

Pene

tratio

n(%

)

Source: Morgan Stanley Research

The Challenge is to increase ARPU in low GDP regions

0

10

20

30

40

50

60

US South Africa Brazil Russia China India

CY03 CY04 CY05 CY06 CY07

India has the lowest ARPU among Large Telecom MarketsARPU inMill $

Source:NL Research, Global Gíreles Matriz 24 Dec 2007

11

In Summary

Since 1993 we have seen a wave of feverish expansion into the emerging markets.

Companies are benefiting today from that international diversification.

Further acquisitions are expected.

Emerging markets continue to show growth and opportunities remain.

Key to balance shareholder remuneration, creditorprotection and strategyc M&A.

Valuations today range from 7x to 13x Ebitda.

Q&A

12

Bashar T. ArafehCOO Zain Group for East Africa region

FT World Telecoms Conference, 3&4 November 2008

Emerging Markets – Is The Boom Over Or Is It Just Beginning?

FT World Telecoms Conference | 3&4 November 2008| Zain Limited © | FT World Telecoms Conference | 3&4 November 200824

Zain is an emerging telecoms player operating in 22

markets in the Middle East and sub-Saharan

Africa

Introduction to Zain Group and Zain’s 2008 performance

50.7 (+58%)

6.7 (+26%)

2.8 (+19%)

Customers (Million)

Revenues (USD Billion)

EBITDA (US$ Billion)

Group results (year ending June 2008)

Source: Zain investor relations

13

FT World Telecoms Conference | 3&4 November 2008| Zain Limited © | FT World Telecoms Conference | 3&4 November 200825

• Zain (formerly MTC) started off in 1983 in Kuwait as the region’s first mobile operator

• Thanks to its 3 x 3 x 3 strategy, Zain evolved from a national player into MEA player in only 4 years

• Today Zain is present in 22 countries– 7 operations in the Middle

East– 15 operations in Africa– Population under license: 546

M

Zain’s historical growth based on the 3 x 3 x 3 strategy

FT World Telecoms Conference | 3&4 November 2008| Zain Limited © | FT World Telecoms Conference | 3&4 November 200826

Spearheading Zain’s future growth: ACE strategy

• Accelerate growth in all operations

• Consolidate existing assets through

– Group-wide synergies

– Performance improvements

• Expand into adjacent markets

• Expand into adjacent businesses

Accelerate Consolidate Expand

Become one of the top 10 mobile and lifestyle operators of the world by 2011

14

FT World Telecoms Conference | 3&4 November 2008| Zain Limited © | FT World Telecoms Conference | 3&4 November 200827

Asia1,250M 46%

Australia20M 104%

Source: Euromonitor and Informa (WCIS); Delta Partners analysisNote: Mobile penetration is weighted average

“Emerging markets”“Growing markets”“Saturated markets”

Population

2007

Penetration

Africa features with China and India among the world’s most attractive markets in terms of room for growth…

Africa

964M 27%

India

1,140M 19%

China

1,322M 41%

Russia142M 122%

Europe667M 111%

North America335M 62%

South America573M 66%

East Africa

130M 20%

FT World Telecoms Conference | 3&4 November 2008| Zain Limited © | FT World Telecoms Conference | 3&4 November 200828

… in terms of speed of growth, Africa’s is expected to continue growing at a fast pace

36

260

440

2002 2007 2012E

Source: Informa (WCIS)

2002 2007 2012E

4%

+650%

27%

+70%

41%

Mobile subscriber (M) and penetration (%) growth

15

FT World Telecoms Conference | 3&4 November 2008| Zain Limited © | FT World Telecoms Conference | 3&4 November 200829

African players will have to face many challenges - the overall challenge being to grow profitably

Growth

MoUs and ARPU decrease

• Untapped market potential growth will be driven by low income segments

I • More players to enter (Indian, European operators)

• Further push from fixed wireless solutions

• Player take-over/M&A

Competition increase

Price drops & margin erosion

II

Addressablemarket saturation

Churn increase

• Even assuming more moderate growth rates, saturation of the addressable market could soon be reality

III

Profitable growth

Today

FT World Telecoms Conference | 3&4 November 2008| Zain Limited © | FT World Telecoms Conference | 3&4 November 200830

So far, other players have been implementing tactical bits & pieces to address the immediate challenge to grow…

ULCH and micro-

financing initiatives

(cost of entry reduction)

FMCGdistribution

model(to push numeric

distribution)

Payphones

(entry product for rural areas)

Validity for life,per second billing, price adjustments

(cost of ownership reduction)

Network expansion into

rural areas(e.g. via low cost hybrid solutions)

Electronic Recharge Vouchers(to add flexibility,

reduce logistics and cost)

Promotional activities

(create customer

excitement)

16

FT World Telecoms Conference | 3&4 November 2008| Zain Limited © | FT World Telecoms Conference | 3&4 November 200831

Pan-regional governance & partnerships

Corporate social responsibility

… while Zain has focused on building a sustainable emerging market business model to achieve profitable growth

Focus on loyalty and retention

One brand and one experience Seamless cross-border network

Cost (CAPEX and OPEX) synergies

EMERGING MARKET BUSINESS MODEL

leveraging on the pan-regional footprint

Customized value proposition for

low ARPU segment

FT World Telecoms Conference | 3&4 November 2008| Zain Limited © |

Thank you

17

Networking Coffee Break

We will resume at 11:00

Innovation – What Can Emerging Markets Teach Us?Michael Joseph, CEO, Safaricom

Chris Gabriel, Chief Executive, Celtel International

Michael Hecker, VP, Strategy and Corporate Development, Mobile TeleSystems OJSC

Sanjay Gupta, Chief Marketing Officer, Airtel

18

Michael Joseph

CEO Safaricom Limited

3rd November 2008

Emerging Markets; Emerging Markets;

KenyaKenya

* Source of Data: EIU Country Report Feb 2008

GDP Growth Rate …

GD

P G

row

th

6.3%

4.1%

6.1%5.7%5.1%

2.9%

1.2%1.2%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

2000/1 2001/2 2002/3 2003/4 2004/5 2005/6 2006/7 2007/8

Official GDP excludes the Informal Sector – which is a large % of the Economy

19

+370%+97%

+77%

+64%

+57%

+54%

+68%

+32%

2,513,154

3,944,007

6,081,950

10,231,554

13,500,565

1,528,420864,347

439,78493,4750

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

2000/1 2001/2 2002/3 2003/4 2004/5 2005/6 2006/7 20007/8 20008/9

Num

ber o

f Sub

scrib

ers

Subscriber Growth Rate…

* Source of Data: EIU Country Report Feb 2008

Year

Rural Expansion … Revenue Growth

0

500

1,000

1,500

2,000

2,500

2000/1 2001/2 2002/3 2003/4 2004/5 2005/6 2006/7 20007/8 20008/9

Site

s

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

Rev

enueSites Ongoing Revenue

Expansion to Rural Areas hasResulted in Revenue Growth

20

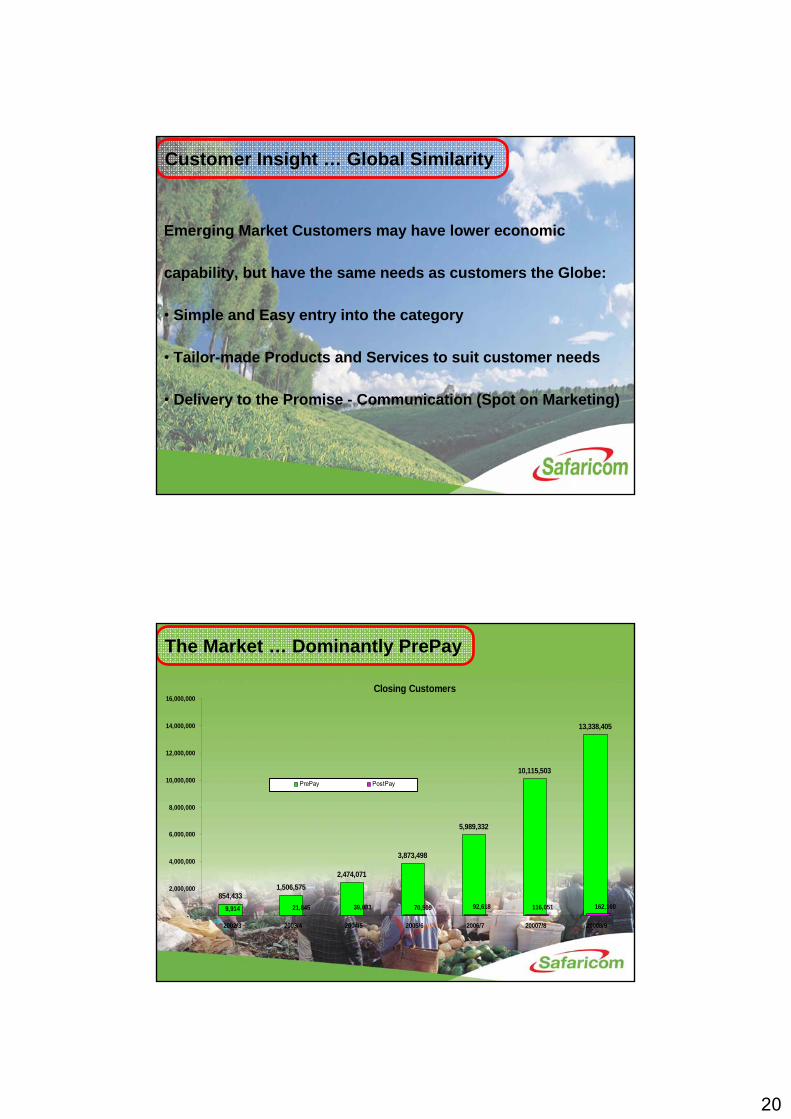

Customer Insight … Global Similarity

Emerging Market Customers may have lower economic

capability, but have the same needs as customers the Globe:

• Simple and Easy entry into the category

• Tailor-made Products and Services to suit customer needs

• Delivery to the Promise - Communication (Spot on Marketing)

Closing Customers

854,4331,506,575

2,474,071

3,873,498

5,989,332

10,115,503

13,338,405

9,914 162,160116,05192,61870,50939,08321,845-

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

2002/3 2003/4 2004/5 2005/6 2006/7 20007/8 20008/9

PrePay PostPay

The Market … Dominantly PrePay

21

0.1%

0.2%

1%

6%

7%

11%

22%

52%

74% of top-ups are in low denomination

Cards

Top-Up … Lower Entry Point

6.25

3.125

0.25

MPESA

SAMBAZA

12.5

1.25

0.625

USD

Total

12,785,843

1,628,359

1,671,962

2,563,012

1,395,034

1,810,282

3,717,194

Key No of Subs

Revenue … Spend Bands

<0.0125

0.0125 - 1.25

1.26 - 2.50

2.5 - 6.26

6.26 - 12.5

>12.5

29%

14%

11%

20%

13%

13%

19%

% Revenue

14%

NA

1%

3%

62%USD

22

• We have over 3800 Prepay customers to date • Affordable device – BlackBerry 7130: Distribution expansion and sales through dealers

Launch of PrePay BlackBerry Performance

Tailor-Made Products … To Customer needs

0100020003000400050006000700080009000

Dec-07 Jan-08 Feb-08 Mar-08 Apr-08 May-08 Jun-08 Jul-08 Aug-08 Sep-08

Cumulative Device Sales

Cumulative APN activations

Embracing New Technology….

Distinct Data Users

337,068

1,046,083

200,000

400,000

600,000

800,000

1,000,000

1,200,000

Aug

-07

Sep-

07

Oct

-07

Nov

-07

Dec

-07

Jan-

08

Feb-

08

Mar

-08

Apr

-08

May

-08

Jun-

08

Jul-0

8

Aug

-08

Sep-

08

Launch of 3G

23

*Source – Finaccess national survey 2006

Kenya’s Mobile Market Banked Population

Only 19% of Kenyans have bank accounts but many more have access to a mobile phone … the gap is widening

M-PESA …. Fulfilling a Need

45%

27%

27%

No Access Friend/Family Own

81%

19%

Unbanked Banked

M-PESA … Fulfilling a Need4.1 Million Subscribers registered as at September 30th

Average of 10,000 new registrations per day

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

Jul-0

7

Aug

-07

Sep-

07

Oct

-07

Nov

-07

Dec

-07

Jan-

08

Feb-

08

Mar

-08

Apr

-08

May

-08

Jun-

08

Jul-0

8

Aug

-08

Sep-

08

24

Thank YouThank You

Zain: Strategies For Emerging Markets

Chris GabrielChief Executive Zain Africa

A wonderful world

FT World Telecoms ConferenceLondonNovember 3, 2008

25

Zain is an emerging telecoms player operating in 22 markets in the Middle East and sub-Saharan Africa

$1,500--------------------average GDP

per capita

500,000+--------------------point of sales

16,000/102--------------------

staff/nationalities

165 million +--------------------SMS per day

15,500+--------------------base stations

754 million+--------------------call attempts

per day

600 million--------------------

population under license

$630 billion--------------------

total GDP

15m sqm--------------------

geographic coverage

18%--------------------

average penetration rate

26

Changecontent and/or context?

• Historical context• Industry perception and forecasting as recently as 2005 was based

on two major fallacies and led to severe underestimation of market potential

• Assumptions regarding size of addressable market • The equity of mobile calls in developing countries

• The African and Indian market experiences confirmed our thoughts

Identifying untapped potential in developing countries

27

History of the telecom industry• Monopoly

• State Controlled

• Heavily Regulated

• Engineering-led utility

• Zero Marketing

• What Brand?!!!

• Command & Control

• Captive Customer

Build ScaleBuild Scale

Strategy

Leverage very high growth market

Leverage very high growth market

Create a global brand

Create a global brand

28

The fury of execution:1.Managing strategic challenges when

solidifying competitive position

2.Leveraging size and diversity

3.Building strategic capabilities

4.Balancing financial profitability & growth – lower ARPU/rural penetration

The fury of execution:5.Operationalizing synergies

6. Leveraging emerging technologies

7. Alternative energy sources

8. Building the learning capability

9. Vitalizing the role of domestic/local operations and actively creating & executing the vision

29

IntroducingOne Network

Telecom service of the year

CommsMEA award &

Global Telecom Business Award

2008

September 27, 2006

One Network was introduced in East Africa

Kenya Tanzania Uganda

One Network expanded to

June 08, 2007

DRC Congo B Gabon

One Network roll-out expanded service to

End 2007 and 2008

SudanMalawiChad Burkina FasoNigerNigeria

One Network roll-out

Pha

se 1

Pha

se 2

Pha

se 3

Bahrain Iraq Jordan Saudi Arabia

30

Introducing Me2U

60

Send virtual money to

Friends and family

Send money from Me2U

money account to bank account Deposit cash

Receive virtual money

Pay bills, pay for

goods and services

Send money from your bank

account to Me2U Money account

Top up yours or someone else

airtime account

Withdraw cash

Me2U

31

61

Secure Secure

–– No need to carry cash No need to carry cash

–– Safe way send money to friends and family Safe way send money to friends and family

–– Password is needed for each transactionPassword is needed for each transaction

–– State of the art security applicationState of the art security application

Convenient Convenient -- available to you 24/7available to you 24/7

Simple Me2U style menuSimple Me2U style menu

Easily accessible from your phone menuEasily accessible from your phone menu

Me2U

Global Brand = Global Company

Why the Zain brand?

32

PassionBrandspreach a better world

“making life better”

“A wonderful world”

Giving Back to the community

33

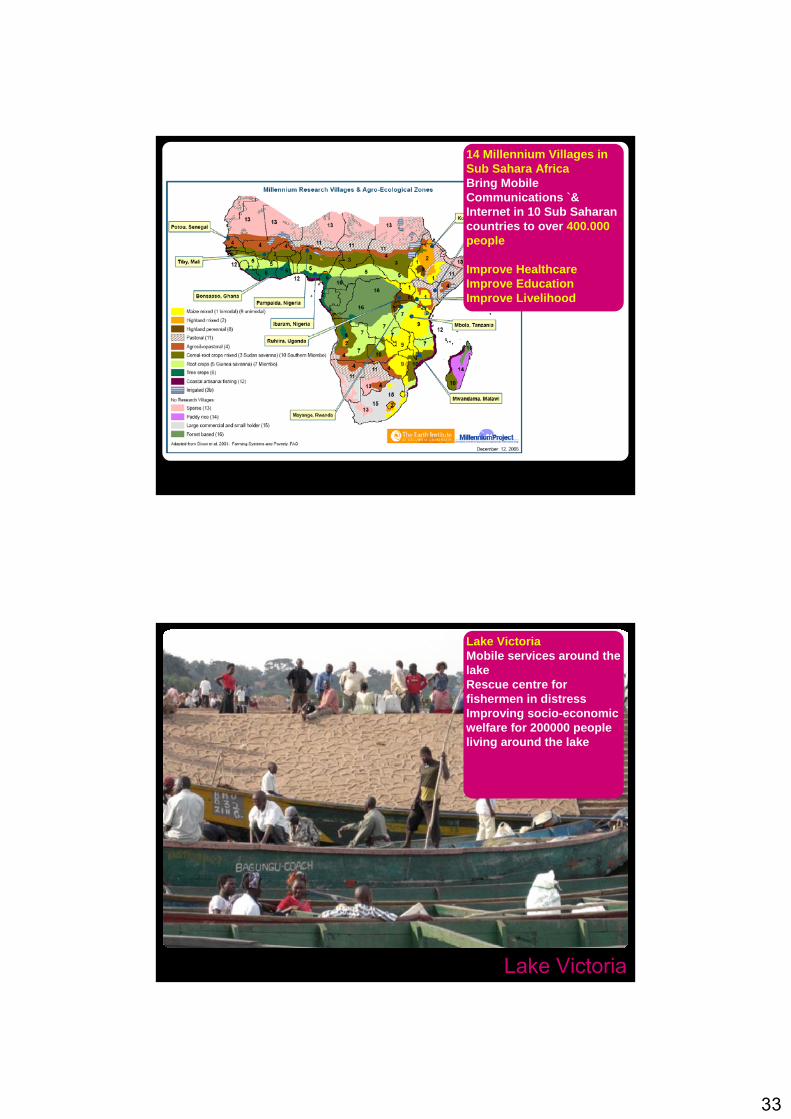

14 Millennium Villages in Sub Sahara AfricaBring Mobile Communications `& Internet in 10 Sub Saharan countries to over 400.000 people

Improve HealthcareImprove EducationImprove Livelihood

Lake Victoria

Lake VictoriaMobile services around the lakeRescue centre for fishermen in distressImproving socio-economic welfare for 200000 people living around the lake

34

Zain challenge and aspirationThe first Middle Eastern - African company to be global

The first telecom company to join the top 100 brands in the world.

Thank youFor more information please contact:

Christopher A. GabrielChief ExecutiveZain Africa

35

MTS Group – Strategy Forward

Financial Times World Telecoms Conference November 03/04 2008, The Landmark, London

Dr. Michael Hecker, VP Strategy and Corporate Development, MTS Group

Safe harbor

Some of the information in this presentation may contain projections or other forward-looking statements regarding

future events or the future financial performance of MTS, as defined in the safe harbor provisions of the U.S. Private

Securities Litigation Reform Act of 1995. You can identify forward looking statements by terms such as “expect,”

“believe,” “anticipate,” “estimate,” “intend,” “will,” “could,” “may” or “might” the negative of such terms or other similar

expressions. We wish to caution you that these statements are only predictions and that actual events or results may

differ materially. We do not intend to update these statements to reflect events and circumstances occurring after the

date hereof or to reflect the occurrence of unanticipated events. We refer you to the documents MTS files from time to

time with the U.S. Securities and Exchange Commission, specifically, the Company’s most recent Form 20-F. These

documents contain and identify important factors, including those contained in the section captioned “Risk Factors,”

that could cause the actual results to differ materially from those contained in our projections or forward-looking

statements, including, among others, potential fluctuations in quarterly results, our competitive environment,

dependence on new service development and tariff structures; rapid technological and market change, acquisition

strategy, risks associated with telecommunications infrastructure, risks associated with operating in Russia and the

CIS, volat i l i ty of stock pr ice, f inancia l r isk management, and fu ture growth subject to r isks.

36

MTS Group Overview - Facts & Figures

Total Subscribers 1,38 mlnMarket share 74%Market place 1 Revenue (only 3Q, 4Q) $ 67 mlnOIBDA 56,5%

Total Subscribers 0,36 mlnMarket share 88%Market place (revenue) 1 Revenue $ 168 mlnRevenue growth (vs. 2006) +58%OIBDA 55,5%

Total Subscribers 2,8 mlnMarket share 54%Market place 1 Revenue $ 248 mlnRevenue growth (vs. 2006) +66%OIBDA (2007) 63,5%

Total Subscribers 57,43 mlnMarket share 33%Market place (revenue) 1Revenue $ 6181 mlnRevenue growth (vs. 2006) +29%OIBDA 2007 51,0%

Total Subscribers 3,8 mlnMarket share 53%Market place (subscribers) 1

Total Subscribers 20,0 mlnMarket share 36%Market place (revenue) 2 Revenue $ 1608 mlnRevenue growth (vs. 2006) +6%OIBDA 48,6%

MTS Armenia, 2007

MTS Turkmenistan, 2007

MTS Uzbekistan, 2007

MTS Russia, 2007MTS Belarus (49%), 2007MTS Ukraine, 2007

RUSSIABELARUS

UZBEKISTAN

TURKMENISTAN

UKRAINE

ARMENIA

MTS is the leading mobile operator group in the CIS

MTS Revenue in 2007 $8,25 bln. 2008 forecast*

• Revenue Growth > 25%

• OIBDA > 50%

* - in local currencies Source: MTS

74,9%

Russia19,5%

Ukraine

3,0%

Uzbekistan

2,0%

Turkmenistan

0,8%

Armenia

MTS 3+2 Group Strategy: Growth + Efficiency

EFFICIENCY

GROWTH

Delivering best customer experience

Expansion in CIS and Developing Markets

Cost efficiency

Driving data &content services

MTS Group development

Delivering superior quality at all touch points

Increasing customer lifetime value

Driving demand stimulation

Market consolidation in existing CIS presence

Enlarging CIS footprint

Realizing growth opportunities outside CIS

Continuous cost & process efficiency focus

Exploiting synergies within CIS operations

Optimal technology solutions

Compelling Internet user experience

Innovative services & attractive content portfolio

Broad and rapid infrastructure deployment (3G)

Efficient Group organization and processes

Build-up of best-in-class workforce andcapabilities and attractive corporate culture

Active corporate and social responsibility

1

3

2

+1

+2

+

Leading communi-

cation brand in CIS

Exceptional shareholder

returns

Source: MTS

37

MTS Growth Strategy: “Waves of Growth”:

2002 2006 2010 2014

Single-Digit Growth

Double-Digit Growth

Wave 1:Subscriber growth

Wave 2:ARPU growth*

Wave 3:Multiple growth components

Network coverage Usage stimulation Data & Content services

Distribution roll-out Brand Mobile BB infrastruct. (3G/4G)

Acquisition campaigns Quality M&A in/outside CIS

Key Growthdrivers

Data & Content

M&A in CIS

M&A outside CIS

.. = Focus of this presentation

* esp. Russia and UkraineSource: MTS

-13%

2%12%

23%33%

44%50%55%

73%

93%

405%

<30

147%

30 -60

60 -100

100 -150

150 -200

200 -250

250 -300

300 -400

400 -600

600 -800

800 -1000

>1000

MOU growth rate*

Fixed subs groups with MOUin April 2007 in range of :

11 12 13 13 10 7 6 8 9 4Share of subs in the group

among all subs % 2 4

Key growth segments: today’s low ARPU subscribers

Mass Market Russia

*Based on large random sample of subs from April 2007 till March 2008

Sustainable demand growth strategy: “Go 600”

Source: MTS

38

MTS Data & Content strategy: “Mobile makes more”

Data

Home Office

Voice

Home Office

Voice + Data + Content

W-Europe

Fixed

Russia& CIS

-

Well-developedofferings

Low-developedofferings

Mobile

Home + Office + On the move

Capturing, Substitution &

Completionby mobile

Source: MTS

In the future mobile BB will play a similar strong role that mobile voice has taken in the CIS in the past

Aggressive Mobile Broadband infrastructure roll-out at MTS

Network deployment to stimulate demand, drive data and content usage and increase overall customer lifetime value

2010

+ 40 cities

20092008

+ 24-27 cities

14 cities

Full commercial HSPA-enabled networks launched:

St. Petersburg, May 2008

Kazan, June 2008

Sochi and Yekaterinburg, July 2008

Nizhny Novgorod, August 2008

Novosibirsk, Norilsk and Vladivostok, September 2008

Add’l 6 cities until the YE 2008

2010: HSPA-enabled networks launched in all regions of Russia

2008: Commercial launch by YE in Tashkent, Uzbekistan

2009: Armenia

2007: CDMA-450 EV-DO Rev A launch in Ukraine

18 cities covered to date

3G Russia

Source: MTS

39

“Red Brothers” – MTS and Vodafone partnership agreement

Increasing performance and innovation from mutual enrichment of two leading operator groups

▪ Advantageous procurement terms

▪ Products, services and devices from Vodafone

exclusive to CIS markets

▪ Joint Product Development

▪ Joint Global Key Account management

▪ Best Practice and Knowledge Sharing

Benefits for MTS

▪ Increased scale from MTS

▪ Joint Global Key Account management

▪ Delivering best customer experience for Vodafone

customers in the CIS

▪ Best practice and Knowledge Sharing

▪ Extension of footprint to cover an additional population of

240 million

Benefits for Vodafone

Source: MTS

Critical success factors for emerging market operators

Management focus on execution

Playing regional differences

Exploiting the Brand Power

Seizing the Mobile BB Opportunity

Benefit from “Lessons learned” in developed markets

Source: MTS

40

Thank you for your attention !

Mobile Services

Innovation – What can Emerging Markets teach us?

41

Mobile Services

Emerging World vs Developed World

Source: https://www.wirelessintelligence.com database

Next 2 Billion to go mobile in Emerging World are in Rural

Mobile Services

PartnersOutsourcing Deals

– IBM Daksh - Nortel– Mphasis - Aegis– Hinduja TMT - Teleperformance

CRM outsourcing

Information Technology

NetworkOutsourcing &Maintenance

Passive Infrastructure Bharti Infratel, Indus

Airtel Innovation in Business Model - Outsourcing

Core Outsourced. Create “Minute Factory” to lower cost / minute

42

Mobile Services

Creating Profitable Low Cost Business

Reducing Costs. Increasing Penetration. Creating Scale.

Source: https://www.wirelessintelligence.com database

0%

10%

20%

30%

40%

50%

60%

0.00 0.05 0.10 0.15 0.20 0.25 0.30

China Mobile

Bharti Airtel

Celcom Malaysia

AT&T Cingular

TIM Brazil

O2 UK

O2 Germany

NTT DoCoMo

Developed world

Emerging world

EBIT

DA

Mar

gin

(%)

OPEX/Min (USD)

Mobile Services

Pervasiveness

130 Mn TV Sets 40 Mn PCs 300 Mn Mobiles

A Ubiquitous Medium to Reach Out

Source: IRS, TRAI, AUSPI, COAI

43

Mobile Services

Profiling

Customer Location Billing Leg

ARPU Bank Music Movie Games Demogs Insurance

Airtel √ √ √ √ √ √ √ √ √Device Mfr √ √Banks/NBFCs √ √ √ √FMCG

A Smart Medium to Know a Person

Mobile Services

Price

Cost / Transaction Bank Branch $ 1.20

A Cheaper Medium to Sell & Serve

Cost / Transaction Bank ATM $ 0.40

Cost / Transaction Net Banking $ 0.008

Cost / Transaction Mobile $ 0.004

44

Mobile Services

What will Emerging Markets innovate on?

Rural Consumer

Reach, Care & Services

Mobile AdvertisingPervasivenessProfile

Banking & Commerce Education Health

PervasivenessPrice

Will Drive Pervasiveness

45

Mobile Services

Innovation – The Virtuous Cycle

Consumer pocket

50% MobilePenetration

100% MobilePenetration

Innovation Continues...in an EMERGING WAY!!

Cost towards ZERO

Innovation LedNew Business ModelFor Allied IndustriesPays for Next set of Customers going

Mobile

ConsumerPocket

Networking Lunch

We will resume at 14:00

46

Convergence – Opportunity and DisruptionJosh Silverman, President, Skype

Joachim Horn, CTO, T-Mobile International

Marc Selby, VP Industry Collaborations, Nokia

Andrew Gilbert, EVP and President, MediaFLOTechnologies and Qualcomm Europe

92

Enabling Broadband in Emerging Markets.FT World Telecoms Conference 2008London, 03.11.2008 Joachim HornChief Technology OfficerT-Mobile International AG

47

Mobile will bring broadband to emergingmarkets.

0%

40%

60%

80%

100%

Africa & Middle East

Asia Pacific

LatinAmerica

Central & Eastern Europe

North America

Western Europe

Fixed BB subscriber lines / HHMobile BB subscriptions / pop

Source: Pyramid Research

20%

120%

20072007

20132013

Mobile and Fixed Broadband Penetration by Region 2007 & 2013

Mobile drives economic growth in emerging markets.

0%

20%

40%

60%

80%

100%

120%

140%

0 1000 2000 3000 4000 5000 6000 7000 8000 9000

GDP per Capita ($US)

Mob

ile P

enet

ratio

n

Source: Pyramid Research

Mobile Penetration vs. GDP per Capita in Emerging Markets 2007

48

New technologies allow to increase efficiently mobile broadband penetration in emerging markets. Example: Superior Efficiency

Carrier Capacityin Mbit/s

LTE

33

EDGE0.3

UMTS

0.8

HSPA

3

GPRS0.1

WiMAX

11

Increased spectral efficiencySimplified network architecture Re-use of existing assets

Mobile WiMAX TDD mode (10MHz); LTE FDD mode (20MHz paired sp

Example: Green Power

Alternative power … help to provide mobile communication services to people in remote off-grid regions

15000050000 100000

South Asia

East Asia & Pacific

Europe & Central Asia

Latin America & Carribean

Middle East & North Africa

Sub Sahara Africa

Annual Growth in BTS in Developing Regions

2007 - 12

Off-gridOn-grid

Project „Green power for Mobile“

New Services

Affordable devices promote mobile communication and facilitate new services in emerging markets.

“With its ubiquity, relatively low cost and high penetration in nations around the world, mobile phone services have the potential to vastly improve access to funds for people in developing markets”

Low Cost Devices

Availability of low cost devices will drive mobile broadband penetration

ts „3G for all“, „Mass Market 3G Notebooks“, „Mobile Broadband“ Project „Mobile Money Transfer“

Example:

Financial Services

49

Convergence affects the entire value chain.

“Convergence Stack”Our Understanding of Convergence

“Bringing together my communications, information, media and transactions, on any of my devices, in a cost effective way in order to manage and engage in my personal, social and business life anywhere.”

“Create superior user experience & simplicity in a convergent world”

Integrated Tariffs

Technologies & Architectures

Sales Bundles

Products and Applications

Customer Centricity

Devices

Net

wor

k P

rodu

ct s

Sal

es &

Ser

vice

Internet

@ WorkMobiledevice

Photo Music

VideoVoice/

Messaging

Photo Music

Video

Mobiledevice

Laptop

TV

“I can access specific services from many

different devices and screens.”

“I can access all my services from a single

device”

Convergence at the application side enables customers in emerging markets to have access to all services.One service on all screens One screen for all services

50

Performance of NGMN will enable fixed broadband experience on mobile.

Fixed and Mobile CapabilityFixed vs. Mobile Performance

Fixed Mobile

1992 1996 2000 2004 2008…

ISDN ADSL VDSLFTTH

10 Mbit/s

1 Mbit/s

100 kbit/s

10 kbit/s

100 Mbit/s

1 Gbit/s

NGMN3G2G9,6 k

384 k

> 100 M

128 k

50 M

384 k

1988 2012 … 2020

large screen nomadic

small screen on the move

very large screen

@home/ @work

higher bandwidthno mobility

lower bandwidth

high mobility

Co-existenc

e

Fixed

Mobile

Devices BandwidthDemand

Access

Conclusions.

Mobile drives economic growth in emerging markets.Mobile will bring broadband to emerging markets. New efficient technologies and affordable devices allow to increase mobile broadband penetration and facilitate new services in emerging markets.Convergence affects the entire value chain. In emerging markets convergence at the application side enables customers to have access to all services.

51

Thank your for your attention.

Financial Times Emerging Markets November 3rd 2008

102

Current State of the World: Digital Divide Exists

For every 100 people worldwide, only 41 have a mobile phone. Far fewer have Internet access.

41% 15.7%17.4%

Source: World Telecommunication/ICT Indicators Database online 11th edition, 2007. Retrieved November 13, 2007, from http://www.itu.int/ITU-D/ict/statistics/ict/index.html

Global MOBILE Penetration Global INTERNET Penetration

41%

17%

52

Financial Times Emerging Markets November 3rd 2008

103

Why Wireless Connectivity Matters

Mobile Penetration:1% increase 4.7% increase in average per capita income

Internet Penetration:1% increase 10.5% increase in average per capita income

Source: Telecommunications Management Group, Inc (TMG) and ITU World Telecommunications Database Statistics; 2007

Financial Times Emerging Markets November 3rd 2008

104Forecasted to Grow to 1.6 Billion 3G Subscribers by 2012

Source: Wireless Intelligence

3G

Over 3 Billion Cellular Subscribers Including More Than 625 Million 3G Subscribers

53

Financial Times Emerging Markets November 3rd 2008

105

Regional TrendsAsia Pacific & Emerging Markets Forecast to Lead Growth

0

200

400

600

800

1000

1200

1400

1600

2006 2007 2008 2009 2010 2011 2012

North America Latin America Asia Pacific Europe Africa/Middle East

Glo

bal A

nnua

l Han

dset

Sal

es

9741,105

1,2051,291

1,3561,411 1,452

(In m

illio

ns)

Source: Informa Telecoms & Media, October 2007

Financial Times Emerging Markets November 3rd 2008

106106

Rank Operator Country Total Subs (M) QIII Net Adds (M) QII Net Adds (M)(Aug'08) (Jul,Aug) (Apr,May,Jun)

1 China Mobile China 428.9 14.3 22.4 GSM2 China Unicom China 171.8 1.1 3.7 GSM,CDMA 1X3 Bharti India 74.78 5.4 7.4 GSM4 AT&T (Cingular) USA 74.72 1.8 1.5 GSM,WCDMA/HSPA5 Verizon Wireless USA 70.5 1.9 1.5 CDMA 1X,EVDO/RevA6 Mobile TeleSystems Russia 62.2 0.8 1.5 GSM, WCDMA/HSPA7 America Movil - Telcel Mexico 54.5 1.7 1.3 GSM,WCDMA/HSPA,TDMA8 Reliance Comm India 54.3 3.5 5.0 CDMA 1X, GSM9 Telkomsel Indonesia 54.0 1.5 1.1 GSM,WCDMA/HSPA10 NTT DoCoMo Japan 53.8 0.15 0.24 GSM,WCDMA/HSPA,PDC11 Vodafone Essar India 52.8 3.6 5.1 GSM12 Sprint USA USA 51.0 0.07 -0.92 CDMA 1X, EVDO/RevA,IDEN13 Vimpelcom Russia 43.173 0.7 0.4 GSM, WCDMA/HSPA14 BSNL India 43.171 1.2 1.2 GSM, CDMA 1X15 Vivo Brazil Brazil 41.7 1.3 1.1 GSM,WCDMA/HSPA,TDMA,

CDMA 1X,EVDO16 T-Mobile Deutschland Germany 39.4 1.0 1.29 GSM/WCDMA17 Megafon Russia 39.3 1.07 1.21 GSM18 TIM Italy Italy 36.2 0.44 -0.13 GSM/WCDMA19 Vodafone Germany Germany 36.1 0.79 0.88 GSM/WCDMA20 Turkcell Turkey 36.0 0.64 0.3 GSM28 Idea Cellular India 29.3 2.6 3.2 GSM29 Tata India 28.4 2.0 2.0 CDMA 1X

Note:

Source:

Operator ranking is based on total subscriber across all technologies in the country

Wireless Intelligence 25/9/2008, TelecomWatch August 2008, www.Telco.comUS subscriber numbers are esimated based on last quarter announcement by carriers

3G Impact - Global Top 20 Wireless Operators (Aug 2008)

54

Financial Times Emerging Markets November 3rd 2008

107

Russia India

0

5

10

15

20

25

2006 2007 2008 2009 2010 2011

DSL connections (m)3G connections (m)

DSL vs 3G connections

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

2006 2007 2008 2009 2010 2011

Fixed penetration (%)Wireless penetration (%)

Fixed vs wireless penetration

0

20

40

60

80

100

120

140

160

2006 2007 2008 2009 2010 2011

DSL connections (m)3G connections (m)

DSL vs 3G connections

0%

10%

20%

30%

40%

50%

60%

2006 2007 2008 2009 2010 2011

Fixed penetration (%)Wireless penetration (%)

Fixed vs wireless penetration

Financial Times Emerging Markets November 3rd 2008

108

WCDMA HSPA HSPA+ (HSPA Evolved)

Rel-99 Rel-5 (HSDPA) Rel-6 (HSUPA) Rel-7 Rel-8 Rel-9 & Beyond

1R8 will reach 42 Mbps by combining 2x2 MIMO and HOM (64QAM) in 5MHz, or by utilizing HOM (64QAM) and multi carrier in 10 MHz. 2R9 and beyond may utilize combinations of multi carrier and MIMO to reach 84 Mbps peak rates. Similarly, uplink multi carrier can double the uplink data rates. 3Peak rates for 10 and 20 MHz FDD using 2x2 MIMO, the standard supports 4x4 MIMO enabling peak rates of 278 Mbps. TDD rates are a function of up/downlink asymmetry

Enhanced capacity and data rates

2x data and up to3x voice capacity

Broadbanduploads, QoS

Broadbanddownloads

DL: 384 KbpsUL: 384 Kbps

DL: 1.8 - 14.4 MbpsUL: 384 Kbps

DL: 1.8 - 14.4 MbpsUL: 5.7 Mbps

DL: 28 MbpsUL: 11 Mbps

DL: 42 Mbps1

UL: 11 MbpsDL: 84 Mbps2

UL: 23 Mbps2

2009 2010 2011+20082007

LTE

DL: 71- 143 Mbps3

UL: 37- 75 Mbps3

Complements 3GLeverages wider bandwidth

Rel-8 Rel-9

Wireless Technology Evolution Path

55

Financial Times Emerging Markets November 3rd 2008

109

Enabling New Mobile Internet & Mobile Computing Devices

MARKET OPPORTUNITY FOR POCKET COMPUTINGDEVICES

Pow

erC

onsu

mpt

ion

Dev

ice

Size

Cos

t

MoreFeatures

MoreFeatures

Financial Times Emerging Markets November 3rd 2008

110

Sub $30 CDMA handsets in India

Classic 361Huawei

Classic 203ZTE

Classic 204ZTE Huawei

C2900

Haier2010

HuaweiC2601

56

Financial Times Emerging Markets November 3rd 2008

111

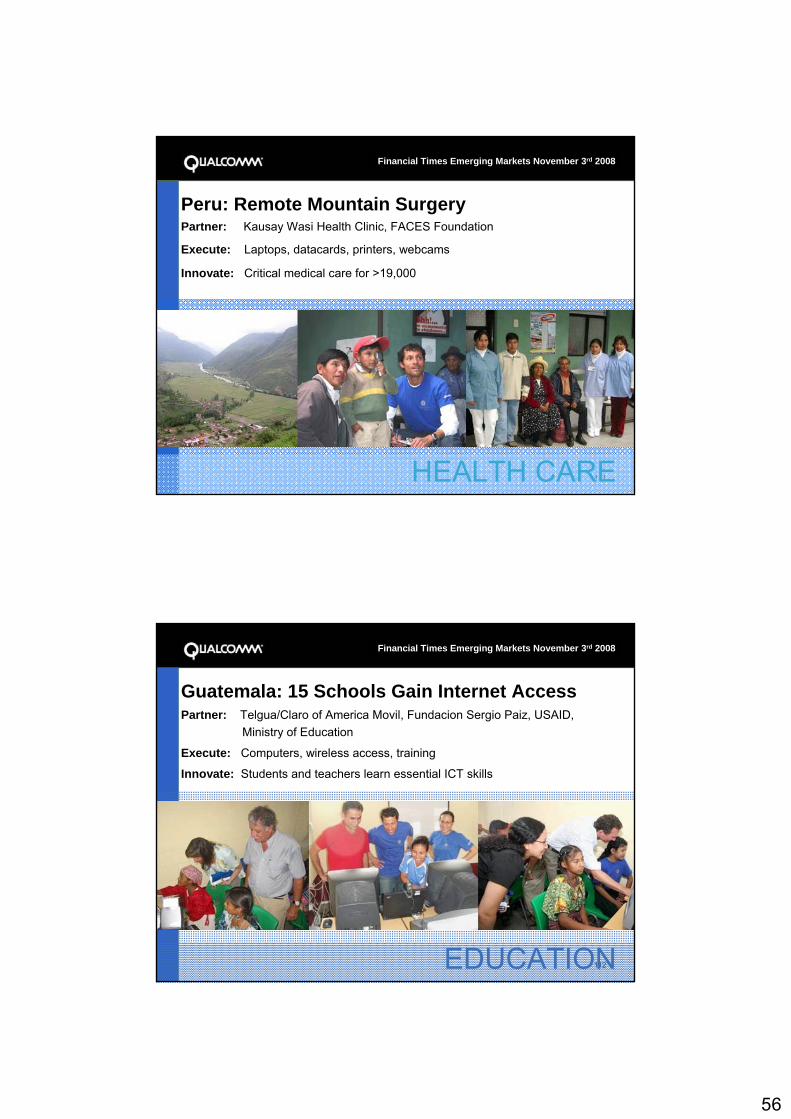

Peru: Remote Mountain SurgeryPartner: Kausay Wasi Health Clinic, FACES Foundation

Execute: Laptops, datacards, printers, webcams

Innovate: Critical medical care for >19,000

HEALTH CARE

Financial Times Emerging Markets November 3rd 2008

112

Guatemala: 15 Schools Gain Internet AccessPartner: Telgua/Claro of America Movil, Fundacion Sergio Paiz, USAID,

Ministry of Education

Execute: Computers, wireless access, training

Innovate: Students and teachers learn essential ICT skills

EDUCATION

57

Financial Times Emerging Markets November 3rd 2008

113ENTREPRENEURSHIP

Sri Lanka: 45 HSDPA Easy Seva CentersPartner: USAID, Dialog Telekom, SSG, NDB, Infoshare, LOLC

Execute: Microfinance loans, business in a box, training

Innovate: Entrepreneurs build businesses providing ICT services in rural

communities

Financial Times Emerging Markets November 3rd 2008

114

Convergence of Devices & Services3G & Beyond 2G 1G

PHONE EVOLUTION

MobileCommunication Information Entertainment / CE Rich

CommunicationUser Generated Content/

Social Networking Computing

+ + + + +

PC EVOLUTION

User Generated Content/ Social

NetworkingComputing Simple

Communication Information EntertainmentRich

Communication

+ + + + +

CONVERGENCEOF DEVICES & SERVICES

Connected ApplicationsRich ContentComputing ApplicationsHigh-Speed Access

Connected DevicesBluetooth HeadsetsMulti-Function CEMobile Computing

58

Financial Times Emerging Markets November 3rd 2008

115

Wireless Reaches the parts that other communication doesn’t!

Networking Coffee Break

We will resume at 15:40

59

Emerging Markets Leadership Panel

Boris Nemsic, CEO, Telekom Austria Group and mobil austria

Kjell Morten Johnsen, Head of Telenor Russia and Snr Vice President, Telenor CEE

Jose Maria Alvarez-Pallete, Managing Director, Telefónica, Latin America

Cenk Serdar, Deputy CEO, Turkcell

Kjell Morten JohnsenSenior Vice President, Central and Eastern Europe

Emerging markets leadership panel

FT World Telecoms Conference, London, 3rd November 2008

60

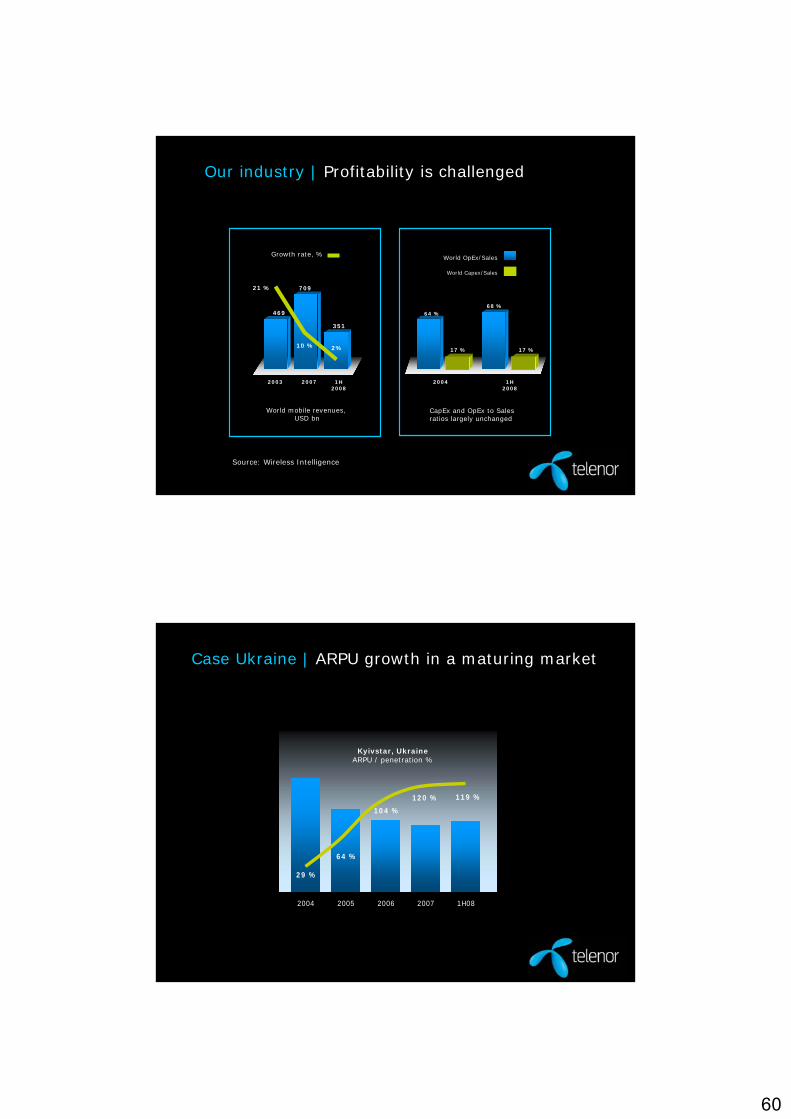

Growth rate, %

CapEx and OpEx to Sales ratios largely unchanged

469

709

2003 2007

21 %

2%

1H 2008

351

10 %

World mobile revenues, USD bn

2004

64 %68 %

1H 2008

17 % 17 %

World OpEx/Sales

World Capex/Sales

Our industry | Profitability is challenged

Source: Wireless Intelligence

Case Ukraine | ARPU growth in a maturing market

119 %

64 %

104 %

120 %

29 %

2004 2005 2006 2007 1H08

Kyivstar, UkraineARPU / penetration %

61

Case Pakistan | Greenfield success

Market share

Ufone

Warid

Mobilink

Zong

0 %

10 %

20 %

30 %

40 %

50 %

60 %

1H05 2H05 1H06 2H06 1H07 2H07 1H08 2H08E

Instaphone

Summary

• Operational efficiency

• Global scale – local drive

• Innovator position

• Deploy Telenor concepts

• Customer experience and brand preference

62

Telefónica Latinoamérica

José María Álvarez-PalleteGeneral Manager, Telefónica LatinoaméricaLondon - November 3, 2008

The Opportunity of Emerging Markets:

Telefónica Latinomérica

FT World Telecoms Conference

Telefónica Latinoamérica

Today Latin America is a young, urban, and multicultural society with great growth potential

México DF POP 23 m

São Paulo POP 19 m

Buenos AiresPOP 15 m

Source: Telefónica

Poverty rate evolution in Latin America (% Pop)

Homes by socioeconomic level

In Brazil, in the next four years, 10% of the current homes (5.5 m) will become middle–upper class

More than 40 million people have escaped poverty since 2003

More than 74 million people have improved their economic status, 3 times above population growth in this period

Maximum level in Social Public Expenditure per capita ($ 850)

6 Cities among 21st Century megalopolis80% of Urban population

Only 8% > 65 years old (2015e)

Río de JaneiroPOP 12 m

LimaPOP 9 m

BogotáPOP 9 m

Source: Banco de Santander; Report:“A emergência da classe média no Brasil”

42,0 39,8 36,5 35,144,0 44,2

2002 2003 2004 2005 2006 2007

42.0 39.8 36.5 35.144.0 44.2

2002 2003 2004 2005 2006 2007

236 MM236 m

196 MM196 m

-7 pp

B

Dec05 Dec10E

A

E

C

D

42% 37%

12%17%

12%

15%17%

23%19%

8%B

05 10E

A

E

C

D

42% 37%

12%17%

12%

15%17%

23%19%

8%

63

Telefónica Latinoamérica

0,0

2,0

4,0

6,0

8,0

10,0

12,0

2006 2007 2008 2009

GDP Latin America100% = € 3,400 bn *

* Source: IMF 2007 78% Regional GDP in Brazil, Mexico, Colombia, Chile and Peru

BBB+

AA

BBB+

A+

BBB+

BBB+

AA

BBB+

A+

BBB+

The region has averaged 5% growth during the past five years, with the region's seven main economies growing at the same time.

Real GDP growth (%)2006 – 2009e

Source:. IMF October 2008 Regional Overview

Despite global economic conditions, the region will keep growing and consolidating international confidence...

>75% of GDP Investment grade

Investment Grade countries in 2008

Latin America average for 2008 at around 4.6%

IMF - World Economic Outlook

Telefónica Latinoamérica

The recent slowdown of the world economy takes place after a solid expansion of economic activity in the region, based on the increasing integration of emerging economies.

The advantageous economic conditions of the past years place the region in a better position to deal with the current situation.

…driven by sound economic policies that will be needed for future challenges

2001 2002 2003 2004 2005 2006 2007 2008

x 3,5 71%58%

45%36%29%25%22%21%

Reserves/External debt Latam*

Higher than Poland (39.3%), Czech Republic (46.6%), Hungary (20.4%)

*Includes: Argentina, Brazil, Chile, Colombia, Venezuela, México and Peru

60%

2000

45%

2007

- 15 pp

Less dependency

on the US

% Exports to the US vstotal

Source: McKinsey

Source: IMF

IMF - World Economic Outlook (WEO)Current Account Balance

The region faces a new environmentFall of commodity pricesDifficult external conditionsInflationary pressures

Source:. IMF October 2008 Regional Overview

-4,0-2,00,02,04,06,08,0

10,012,014,016,0

2006 2007 2008 2009

Argentina Brazil Chile Colombia Mexico Peru Venezuela

64

Telefónica Latinoamérica

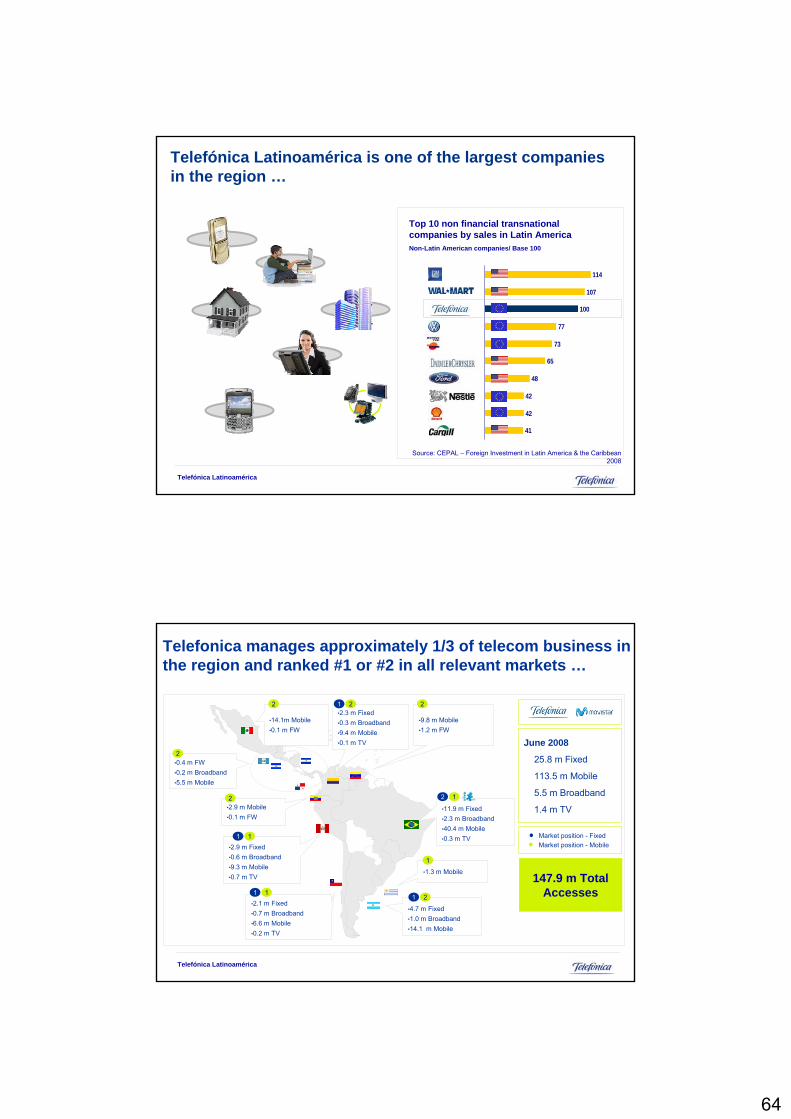

Top 10 non financial transnational companies by sales in Latin America Non-Latin American companies/ Base 100

Source: CEPAL – Foreign Investment in Latin America & the Caribbean 2008

41

42

42

48

65

73

77

100

107

114

Telefónica Latinoamérica is one of the largest companies in the region …

Telefónica Latinoamérica

June 2008

25.8 m Fixed

113.5 m Mobile

5.5 m Broadband

1.4 m TV

Market position - FixedMarket position - Mobile

•1.3 m Mobile

•4.7 m Fixed•1.0 m Broadband•14.1 m Mobile

•2.1 m Fixed•0.7 m Broadband•6.6 m Mobile•0.2 m TV

•2.9 m Fixed•0.6 m Broadband•9.3 m Mobile•0.7 m TV

•14.1m Mobile•0.1 m FW

•2.9 m Mobile•0.1 m FW

•9.8 m Mobile•1.2 m FW

•0.4 m FW•0.2 m Broadband•5.5 m Mobile

•11.9 m Fixed•2.3 m Broadband•40.4 m Mobile•0.3 m TV

•2.3 m Fixed•0.3 m Broadband•9.4 m Mobile•0.1 m TV

2

2 21 2

2

11

1121

1

12

147.9 m Total Accesses

Telefonica manages approximately 1/3 of telecom business in the region and ranked #1 or #2 in all relevant markets …

65

Telefónica Latinoamérica

Dec-98 Dec-99 Dec-00 Dec-01 Dec-02 Dec-03 Dec-04 Dec-05 Dec-06 Dec-07

+4 m +5 m

+10 m+9 m

+27 m

+20 m

+16 m

+19 m

+4 m

Jun-08

+4 m

20 24 2833

4352

79

99

115

134

Dec

+4 m+4 m +5 m+5 m

+10 m+10 m+9 m+9 m

+27 m+27 m

+20 m+20 m

+16 m+16 m

+19 m+19 m

+4 m+4 m

-08

+4 m+14 m

148

Dec-98 Dec-99 Dec-00 Dec-01 Dec-02 Dec-03 Dec-04 Dec-05 Dec-06 Dec-07

+4 m+4 m +5 m+5 m

+10 m+10 m+9 m+9 m

+27 m+27 m

+20 m+20 m

+16 m+16 m

+19 m+19 m

+4 m+4 m

Jun-08

+4 m+4 m

20 24 2833

4352

79

99

115

134

Dec

+4 m+4 m +5 m+5 m

+10 m+10 m+9 m+9 m

+27 m+27 m

+20 m+20 m

+16 m+16 m

+19 m+19 m

+4 m+4 m

-08

+4 m+14 m

148

… thanks to a sustained growth since 1998

Telefónica has reached 150 MM accesses, more than a year

before our commitment for 2009

Telefónica Latinoamérica

With a strong, long-term commitment to the region that also makes us the largest private foreign investor in Latin America

56%24%

7%

6%4% 3%

Latin America

East Europe

Asia (Southeast)

Asia (South)

Middle East & North Africa

Africa Sub-Saharian

FDI in Telecommunications, by region1990-2005 Main investment recipient

(US$ 120bn in the period 1990-2005)

Telecommunications CAPEX in Latin America*1990-2007

Telecommunications CAPEX Aprox. 130 Bn€ for the period 1990-2007

Telefónica has invested around 30% of the total CAPEX in Latam

* Telefónica´s estimations

Telefónica´s investment in Latin America 1990-2007 (m Euros)

Latin America has experienced an important investment flow in the past years

Telefónica has been the leader thanks to our permanent investment commitment, which started more

than 15 years ago

Telefónica has committed infrastructure investments in Latin America of € 14-16,000 m for the period

2007-10

83,24737,643

45,604

FDI Total

83,24737,643

45,604

Infrastructure Total

66

Telefónica Latinoamérica

For the future we expect significant top line growth potential, capitalising on our unique integrated approach…

Further penetration increase

Data potential

Voice usage upside

WIRELESS

Accesses expansion (Broadband, TV, fixed wireless)

Further Broadband development (upselling through 2P & 3P)

Traffic bundles+

WIRELINE

Customer &ARPU expansion

T. Latam2007-10E

Over 55/60 million additional mobile accesses in 2007-10E with a 1-3% 06-10E CAGR ARPU increase (ex-fx)

Over 4/5 million additional BB accesses

3G will be launched by Q1 09 across all

our operations

Telefónica Latinoamérica

Client demandsBandwidth demandHomogeneous experience despite access/deviceService Bundling (Duos & trios)

Competitive environmentNew companies (ASP, CSP) that use our network capacity for

new business models

Efficiency requirementsMore competitive pressure with an impact on margins

Technology evolutionTechnological evolution offers powerful tools in terms of service efficiency New technologies with shorter life cycle

1995 2001 2003 2006 20101995 2001 2003 2006 2010

GSM

GPRS

UMTS

HSxPA

LTE

0,0096 Mbps

0,08Mbps

0,384Mbps

14,4Mbps

100Mbps

Mobile Broadband width evolution(Mbps)

Fixed Broadband width evolution(Mbps)

Focusing on technological evolution and its positive impact on business and society…

1982 85 88 92 96 2000 02 04 10 12 2014

Moore's Law x

2every

2 years

Copper Fiber

ADSLADSL2+

VDSL

FTTH0.033

0.0560.128

0.2570.512

22

0.00240.0012

0.0003

0.0280.0144

0.0096

1

6 8

0.0001

0.001

0.01

0.1

1

10

100

1000

08

67

Telefónica Latinoamérica

Fostering innovation, dedicating resources and promoting new ideas…

Technological innovation– Telefónica Group1

(m Euros)

20072006

4,3844,301

*Source: Annual Corporate Responsibility Report 2007

R&D investment

Equipment 61%

R&D 14%

Acquisition of other knowledge 13%

Design and Planning 10%

Training & Marketing 2%

Telefonica has innovation centers all over the world…

(1) Technological Innovation according to the definition of OECD (&Spanish INE)

>190 international R+D projects in collaboration with 920 institutionsFund dedicated to entrepreneurial initiatives with 18 on-going, including a project in China

Strategic minority participation - Venture Capital

International Remittances

Speedy Zero

Telefónica Latinoamérica

Developing new products and services for the benefit of our customers…

1st Operator to launch digital TV in the region

17%

6%

13%

3 years 1 year 1 year

Spain Czech RepublicChile

Innovative products

VPN VPN Pasarela Residencial“Llena tu casa de

vida”

IP CardSmart TV

Digital TV market share obtained since launch

Tele-presence

Video-surveillance

i-phone launch

throughout the region

October 2008 -Digital TV

launched in Venezuela

68

Telefónica Latinoamérica

Develop a direct channel for institutional relations with key government / industry Explore business opportunities in China and elsewhere in AsiaEstablish contacts with major telecommunications manufacturers in China to optimize purchasing processes.

Latin America has become a key supplier of raw materials for China

And strengthening our partnerships in other key markets

Exports from Latin America to AsiaPercentage of total exports

05

10152025303540

ChileBras

il

Colombia

Argen

tina

PerúLata

m*

Uruguay

Venez

uela

20%

In 2005, Telefónica opened its permanent representative office in Beijing

* Enero -noviembre 2004 acumulado , excepto para Brasil (año completo)Fuente: basado en estad ísticas nacionales

Telefónica reaches an agreement with the Chinese ZTE to bring 3G to Latin America

20/10/07Telefónica opens the Hispanic market to the largest Chinese equipment manufacturerThe Spanish telecom operator has signed a framework agreement with Huawei, the second largest manufacturer of equipment for Internet access via ADSL in the world

20/10/0718/10/04

Telefónica Latinoamérica

1,5%

1,3%

1,6%

2,0%

1,3%

0,9%

Venezuela

Colombia

Chile

Peru

Argentina

Brazil

% Revenues / GDP in relevant markets 2007 – Telefónica, Corporate Responsibility Report

8,1398,139

1,8251,825

2,3682,368

1,5061,506

1,5851,585

2,4302,430

Telefónica´s revenues 2007 (m €) Fixed + Mobile

But Telefónica also assumes its responsibility as a cornerstone for the development of communities…

Direct employees

Telefónica Latinoamérica 2007Telefónica, Corporate Responsibility Report

164.231

12.216

16.859

2.288

6.369

14.613

14.554

21.493

75.839

TOTAL

Rest

Mexico

Venezuela

Colombia

Chile

Peru

Argent ina

Brazil

In the markets where Telefónica operates, revenues are equivalent to 1-2% GDP

In addition, Telefónica generates 239.000

indirect jobs

69

Telefónica Latinoamérica

… and has brought ICT´s to all of society, proving to be a global leader in corporate responsibility

"INTÉGRAME" recognized by the UN as one of the most important projects

Viernes, 30 de Mayo 2008

We collaborate with more than 400 municipalitiesthroughout the country, from advisory services to the installation of all the telecommunications infrastructure

“We aim at enhancing people’s lives, business performances and the progress of the communities in which we operate, by delivering innovative services based on information and communication technologies.” Spirit of Progress

“Intégrame”

Children

Schools

240

2005 2007 may 08 2008e

>100,000

~1,700

Program launched in collaboration with more than 100

prestigious NGO´s in the region

“CiudadesDigitales”

11,540 52,08273,023

1,1181,531

Telefónica Latinoamérica

1

2

3

4

6

Latin America will still be one of the regions with solid growth potential and it is prepared to deal with the current economic environment.

Latin American society is young, dynamic and has great potential. The region’s significance in the world will increase in the coming years.

Telefónica is proud to lead telecommunications investment in Latin America over the past 18 years, strengthening the sector and bringing our services to all of society.

Telefónica has a significant role in the development of the region, and maintains a strong social and economic commitment with the countries in which operates.

Telefónica is one of the largest companies in Latin America, the leading integrated telecommunications operator in the region, and plays a key role in the Telefónica Group.

Summary

5 In the future, we fill focus on technological evolution, fostering innovation and developing new products and services for the benefit of our customers.

70

Telefónica Latinoamérica

CENK SERDARChief VAS Officer

TURKCELL

71

DemographicsYoung and Growing Population%40 of population is under 22.

Telecom MarketMobile is growingMobile Subs: 63.7mMobile Penetration: 90%Fixed Subs: 17.8mThe world’s highest mobile service taxes!

Population:71 Million

Turkey in a nutshellTurkey in a nutshell

Source: DİA & 3rd party market researches

Recent Developments3G licensing in Q4 2008

MNP implementation in November 2008MVNO licenses in Q1 2009

EconomyStrong Economic Conditions

GDP (2007): $657bGDP per Capita (2007): $9305

CPI % (Oct 2008): 11.13

Turkey

Kazakhstan

Azerbaijan

Georgia

Moldova

Northern Cyprus

Belarus

Ukraine

Turkcell GroupTurkcell Group

*Turkcell is holding a 41.45% stake in Fintur and trough Fintur holds interest in AzerCell, K’Cell, GeoCell and MoldCell. The subscriber number according to our percentage ownership is 48.8 million as of Q2 2008.

Operations in 8 countries

58 M subscribers in total

35.4 M in Turkey

2

3

3

1

1

1

12

72

Turkcell’s Key FiguresTurkcell’s Key Figures

• Europe’s 3rd and the world’s 13th largest operator in terms of subscribers

• Biggest operator in Turkey with 56% market share. ($14.3 ARPU and 83.1 min MoU in 2007)

10%

35%

11%

30%

Revenue ($b)

Net Income ($b)• 25th position in Businessweek Infotech 100 list.

• First and only Turkish company listed in the New York Stock Exchange

• Mobile Payment

• Mobile Signature

• Mobile Education

• Mobile Health

• Mobile Advertising

•Mobile‐ fixed substitution

•Mobile as only access method in certain areas

INCREASE PENETRATION

MOBILE BROADBAND

PLATFORM DEVELOPMENT

GROWTH DRIVERS

•Turkcell footprint countries • Acquisitions in emerging markets

TOTALCOMM.

PROVIDER

• Fixed + Mobile + Internet

Growth will come from four areasGrowth will come from four areas

73

Increase in mobile penetration in footprint countries will drive revenuesIncrease in mobile penetration in footprint countries will drive revenues

Selected Turkcell footprint countries

A sample list of Western European countries

Delta will create significant revenue

stream

Avg: 69%

Avg:132%

Mobile Broadband Is Gaining MomentumMobile Broadband Is Gaining Momentum

•“47% of all broadband subscribers in Europe will access the Internet through mobile networks by 2013”

Mobile‐fixed broadband substitution

Source: Analysys Mason, October 2008 ; McKinsey

74

Total Communication Solution ProviderTotal Communication Solution Provider

Voice, Data, VASPSTN, Fiber, Cable, ADSL, ...

Voice, Data, VAS

GSM, 3G, HSDPA

Software, Hosted Solut

ions

IP, IMS, Seamless NW

FIXED

IT SERVICES

ServicesServices

ConvergedConvergedPlatformPlatform

Voice, Data, Voice, Data, VASVAS

MOBILE

Mobile Games

Mobile Education

Mobile Healthcare

Mobile Internet Telemetry

Applications

Mobile Banking & Payment

Mobile SignatureMobile

Navigation

Mobile Marketing

Creating New Business PlatformsCreating New Business Platforms

75

Example > Mobile SignatureExample > Mobile Signature

• 50K+ users• 2 mn signatures

• 35 applications

• 50K+ users• 2 mn signatures

• 35 applications

Finance Public Sector Corporate

e‐Commerce

Universal Authentication for Digital Transactions!

Mobile Payment

Transportation

Parking

Digital Goods

Service Delivery

• Launched in July 2008• Started with internet players/parking• Launched in July 2008• Started with internet players/parking

Example > Mobile PaymentExample > Mobile PaymentMicropayments charged to your bill

76

Example > Mobile WalletExample > Mobile Wallet

• NFC transactions are predicted to account for 50 per cent of the global mobile payment market by 2013

• Active role in NFC standards and business models

• Largest NFC pilot in the world with 3K access points

• NFC transactions are predicted to account for 50 per cent of the global mobile payment market by 2013

• Active role in NFC standards and business models

• Largest NFC pilot in the world with 3K access points

Touch & Pay

= + +

Credit Card Security / ID Transportation

+

Simcard based NFC!

Example > Mobile MarketingExample > Mobile Marketing

• “Permission Database”: 7.2 mn subscribers

• 100% yoy revenue growth• Leader in MM via Rich and Innovative Services

• 31 different sectors, 154 brands, 323 mobile marketing projects (H1 08)

• Ad‐funded content through sponsorships

• Launched TonlaKazan, the world’s first mobile RBT advertising platform

• “Permission Database”: 7.2 mn subscribers

• 100% yoy revenue growth• Leader in MM via Rich and Innovative Services

• 31 different sectors, 154 brands, 323 mobile marketing projects (H1 08)

• Ad‐funded content through sponsorships

• Launched TonlaKazan, the world’s first mobile RBT advertising platform

77

SummarySummary

OpportunitiesOpportunities ThreatsThreats

• Penetration increase through acquisitions in emerging markets

• Mobile Broadband

• Platform Development to gain market share/loyalty

• Total Communication Solution Provider

• Penetration increase through acquisitions in emerging markets

• Mobile Broadband

• Platform Development to gain market share/loyalty

• Total Communication Solution Provider

• Fast decrease in Voice revenue

• New players in town

• Fast decrease in Voice revenue

• New players in town

Growth For Emerging Markets In Short Term: Strong potential for further penetration.In Long Term: Non‐voice business will gain momentum as in WE.

Growth For Emerging Markets In Short Term: Strong potential for further penetration.In Long Term: Non‐voice business will gain momentum as in WE.

THANK YOU . . .

www.turkcell.com.tr

78

Chair’s Closing Remarks

John Higgins CBE,Director General, Intellect

Networking Drinks Reception