Embed Size (px)

Citation preview

D Lindley: Energy 2100. 08.05.06 1

Wind and Tidal Energy

- a vision of the future ??

Dr David Lindley: Ocean Power Delivery Ltd

Energy 2100: The Royal Academy of Engineering: 8 May 2006

World wind energy capacity (MW)

0

10000

20000

30000

40000

50000

60000

70000

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Cumulative

Annual

D Lindley: Energy 2100. 08.05.06 2

% electricity produced by wind energy

0

2

4

6

8

10

12

14

16

18

Denmar

kSpa

in

German

y

Portu

gal

Irelan

d

Greec

e NL

Austri

aIta

ly

Luxem

bourg

Latvia UK

Sweden

Estonia

Norway

EU25

D Lindley: Energy 2100. 08.05.06 3

The sixteen leading wind countries

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

German

yUSASpa

inIndia

Denmar

kChin

aIta

ly UK NLPor

tuga

lAus

tralia

Canad

aAus

tria

Franc

eGre

ece

Sweden

D Lindley: Energy 2100. 08.05.06 4

Wind Energy as a % of total installed capacity

-2.000.002.004.006.008.00

10.0012.0014.0016.0018.0020.00

1975 1980 1985 1990 1995 2000 2005 2010

Spain USA Germany UK

D Lindley: Energy 2100. 08.05.06 5

The largest owners of wind farms

D Lindley: Energy 2100. 08.05.06 60

500

1000

1500

2000

2500

3000

FPLIberdrolaEHNPPM SPEurusShellEndesaEnergi E2NuonAlliantElsamENEL

D Lindley: Energy 2100. 08.05.06 7

Current Practice and Future Trends

Offshore wind (Round II) c.7GW

Wind - 2020?

Existing wind farms c. 890MW to date

IrelandGB

Applications for connection c. 18GW

Also 1GW offshore (Round I)plus onshore in England and Wales

UPDATE: As of May 2006 operational wind farms ~1400 MW and 1100MW under construction

^

^̂^

^

^

^^

^ ^ ^

^

^

^^

^^Lely

Emden

Blyth

Nysted

Samsoe

VindebyHorns Rev

Tuno KnobUtgrunden

Arklow Bank

Bockstingen

Scroby Sands Irene Vorrink

Middelgrunden

Frederikshaven

North Hoyle

Yttre Stengrund

Existing Offshore Wind farms: 2004

606.6 MW

D Lindley: Energy 2100. 08.05.06 8

^

^̂

^̂

^

^

^̂

^^

^

^̂^

^

^

^^

^ ^ ^

^

^

^^

^^Lely

Emden

Blyth

Nysted

Samsoe

VindebyHorns Rev

Tuno KnobUtgrunden

Arklow Bank

Bockstingen

Scroby Sands Irene Vorrink

Middelgrunden

Frederikshaven

Q7

Lynn

BarrowButendiek

Robin Rigg

Borkum West

Thornton Bank

Inner Dowsing

Kentish Flats

North Hoyle

Yttre Stengrund

Nordzeewind

Gunfleet Sands

Offshore Wind Farms : 2009 ?

>2000MW

D Lindley: Energy 2100. 08.05.06 9

Offshore turbines will be “different”

5m per annum

15 MW205 m

316 kW per annum 170m10 MW

2004 …………20201990

D Lindley: Energy 2100. 08.05.06 10

Wind Energy Development Trends

0

500

1,000

1,500

2,000

2,500

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

kW

1,000

10,000

DKK/

kWh

Average rated power of w ind turbines installed (kW) Specific price of w ind turbines (DKK/kWh) relative to 2000 prices

Until 1985– Concept

development– Unit size < 100kW– Single units

1985-1995– Many small companies,

strong competition– Unit size quadruples in 10

years– Small w ind farms c.10MW

1995-today– Average unit size grows >

1MW, w ind farms up to c.100MW

– Growth of offshore wind, business consolidation

Future– Unit size grows >

5MW, w ind power plants up to c.1000MW

– Market diversif ied geographically

– Continued expansion of offshore w ind

Cumulative global capacity1,000MW 2,000MW 5,000MW 18,000MW 60,000MW 75,000MW

0

500

1,000

1,500

2,000

2,500

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

kW

1,000

10,000

DKK/

kWh

Average rated power of w ind turbines installed (kW) Specific price of w ind turbines (DKK/kWh) relative to 2000 prices

Until 1985– Concept

development– Unit size < 100kW– Single units

1985-1995– Many small companies,

strong competition– Unit size quadruples in 10

years– Small w ind farms c.10MW

1995-today– Average unit size grows >

1MW, w ind farms up to c.100MW

– Growth of offshore wind, business consolidation

Future– Unit size grows >

5MW, w ind power plants up to c.1000MW

– Market diversif ied geographically

– Continued expansion of offshore w ind

Cumulative global capacity1,000MW 2,000MW 5,000MW 18,000MW 60,000MW 75,000MW

D Lindley: Energy 2100. 08.05.06 11

Capital Costs of existing offshore wind farms

5

2

5

17

3

4

1040

160

23

60158

6090

10

200

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

1990 1995 2000 2005

Cap

ital c

ost [

£m/M

W]

Onshore wind farms

Onshore wind farms

D Lindley: Energy 2100. 08.05.06 12

D Lindley: Energy 2100. 08.05.06 13

Marine Renewables - Wave & Tidal Power

Tidal Power Barrage• Use of a Barrage to Impound the Tide & extraction of the

Potential Energy to drive Turbines (similar to Hydropower)

Marine Current (Tidal Stream)• Extraction of the Kinetic Energy in Tidal Currents

Wave Power• Extraction of Energy from Wave motion

Tidal Barrage PowerProven Technology: La Rance in France has generated

tidal power reliably for nearly 40 years

D Lindley: Energy 2100. 08.05.06 14

Operational and proposed Marine energy projects worldwide

D Lindley: Energy 2100. 08.05.06 15

D Lindley: Energy 2100. 08.05.06 16

Severn Tidal Barrage

• UK potential mainly from Severn Estuary

• 17TWh = 5% of UK electricity supply

• Rated at 8640MW• 7p/kWh (incl. financing &

grid upgrade)• Estimated capital cost

=£14 billion (2006)• Constraints

- Project financing- Environmental issues

Tidal Power Barrage operation

D Lindley: Energy 2100. 08.05.06 17Tidal Power Barrage Operation

Severn Barrage Layout (1989 Report)Severn Barrage Layout (1989 report)

• 216 Turbines 40MW each

• 166 Sluices

• Ship Locks

• Small Locks

• Public Road

• Railway (possibly)

•216 turbines (40MW each)

•166 sluices

•Ship locks

•Small locks

•Public Road

•Railway (possibly)

D Lindley: Energy 2100. 08.05.06 18

Mersey Barrage Proposal 1992700MW capacity & 1.45TWh/year output

Mersey Barrage Proposal 1992700 MW capacity & 1.45 TWh/year output

Estimated Capital cost (1992) = £900 million

D Lindley: Energy 2100. 08.05.06 19

Tidal Stream Resource (Black & Veitch - for Carbon Trust - 2004-5)

Location Total TWh/year

ExtractableTWh/year

EconomicTWh/year

UK 90 18 ~12

?

?

Europe(excl. UK)

90 17

Worldwide(remainder)

600 ? 120 ?

D Lindley: Energy 2100. 08.05.06 20

Tidal Stream Sites around the UK

• Tidal Streams around the UK with Spring Tide > 2 m/s

• Water 800 times denser than air• Water flow of 1m/s carries the

same energy density as a wind flow of 9m/s

• Constraints- Technology at an early stage- Best sites are remote ( e.g Orkneys

and Channel Isles)- Costs uncertain at present

>9p/KWh for first farmsD Lindley: Energy 2100. 08.05.06 21

D Lindley: Energy 2100. 08.05.06 22

2004

UK Tidal Currents at Mean Spring TideFrom Atlas of Marine Renewable Energy Resources – Dti 2004

UK Tidal Current at Mean Spring TideFrom Atlas of Marine Renewable resources – DTI 2004

Tidal Current Device Types

• Horizontal axis Turbines

• Vertical axis Turbines

• Oscillating Hydrofoil Devices

• Venturi Devices

•Vertical axis Turbines

•Oscillating Hydrofoil Devices

•Venturi devices

•Horizontal axis Turbines

D Lindley: Energy 2100. 08.05.06 23

Tidal Stream Development

Seagen – 1MW deviceMarine Current TurbinesProposal -Approved 2006 for installation in Strangford LoughNorthern Ireland

D Lindley: Energy 2100. 08.05.06 24

D Lindley: Energy 2100. 08.05.06 25

Lunar Energy – seated on the seabed – 1MW Prototype planned for 2006/7

Lunar Energy – seated on the seabed – 1MW Prototype planned for 2006/7

Buoyant device, moored at mid water depth

TidEl by Hydrovision –Buoyant device, moored at mid water depth

Summary of Constraints to Development of Marine

RenewablesFor Tidal Barrages• Environmental Consents• Financing & lack of long term market• Construction risk & cost consequences

For Tidal Stream & Wave• The need for successful demonstration projects• Need to reduce costs • Costs of grid connection• Need for additional support (ROC’s + ) after

Demonstration projects and during Development stageD Lindley: Energy 2100. 08.05.06 26

D Lindley: Energy 2100. 08.05.06 27

Integration of Intermittent energy

sources and Forecasting

The “Virtual” Power System –Challenges of managing a distributed Power System

Source: EWE, Germany D Lindley: Energy 2100. 08.05.06 28

Wave & Wind Energy are intermittent but not unpredictable.

Tidal energy is predictable

D Lindley: Energy 2100. 08.05.06 29

The “Virtual “ Power system -A challenge to manage integration of intermittent sources

D Lindley: Energy 2100. 08.05.06 30

D Lindley: Energy 2100. 08.05.06 31

Range of findings related to additional reserves with increasingpenetration of intermittent supplies

D Lindley: Energy 2100. 08.05.06 32

Source: UK Energy Research Centre: “The costs and impacts of Intermittency - an assessment of the evidence”March 2006

Range of findings on the cost of additional reserve requirements

D Lindley: Energy 2100. 08.05.06 33

Source: UK Energy Research Centre. “The costs and Impacts of Intermittency – an assessment of the evidence”March 2006

Range of findings on capacity credit of intermittent generation

D Lindley: Energy 2100. 08.05.06 34

Source: UK Energy Research Centre: “The costs and Impacts of Intermittency – an assessment of the evidence”. March 2006

Aggregate costs of Intermittency for 20% wind penetration

•Short –run balancing costs = £2 to £3 /MWh

•Maintaining a higher system margin = £3 to £5 /MWh

•Total costs = £5 to £8 /MWh

•This is to be compared with direct costs of wind generation of between £30 to £55/MWh. If shared between all consumers the impact of intermittency on electricity prices = 0.1 to 0.15p/kWh.

Source: UK Energy Research Centre: The costs and impacts of intermittency. March 2006

D Lindley: Energy 2100. 08.05.06 35

D Lindley: Energy 2100. 08.05.06 36

EU and IEA reference scenarios for wind energy

D Lindley: Energy 2100. 08.05.06 37

The 1999 Commission base scenario projections for wind, solar and geothermal was 9.4 GW in 2000, 16 GW in 2005, 23 GW in 2010, 34.4 GW in 2015 and 46.2 GW in 2020.

•The 2015 figure had already been reached at the end of 2004 by wind alone.

In 2003 the Commission Baseline scenario projections for wind and solar were 28.6 GW in 2005, 74 GW in 2010, 92.6 GW in 2015, 105.3 GW in 2020, 126.4 GW in 2025 and 149.4 GW in 2030

•Between 1996 and 2003, the Commission’s estimate of how much wind power would be built in 2010 was increased ninefold.

In 2004 the Commission Baseline scenario projections for wind and solar were 28 GW in 2005, 73.2 GW in 2010, 91.7 GW in 2015, 104.1 GW in 2020, 125.2 GW in 2025 and 149.2 GW in 2030.

300 (2003)

Future forecasts for wind power in Europe(IEA, EU and EWEA_

D Lindley: Energy 2100. 08.05.06 38

What is possible in 2100• 20% of electricity from Wind power ( cf. Energy White

paper/Innovation review target of 10% from renewables by 2010-which would require ~ 7500MW of new wind capacity and 15% by 2015.)

• 6% of electricity from Tidal Power ( Severn Tidal Barrage and Mersey barrage =9340MW)

• 1% of electricity ( 4TWh) from Tidal streams Energy (ref: Kerr: Proc ICE.Nov 2005). Realisable potential 22TWh. ( ref. UK Marine Renewables Atlas. The Carbon trust)

D Lindley: Energy 2100. 08.05.06 39

Note: At the end of 2004 renewables contributed 3.7% of UK electricity. Currently about 2500MW of wind farms are operational or under construction ~about 1600MW more than existed at end of 2004

Conclusions:A “New” paradigm –”Joined up thinking” is required.

Government Renewables Aspirations will not be met unless:-Government Aspirations will not be met unless:--• A commitment is made now to

invest to remove grid constraints• A mechanism is put in place to deal

more efficiently with the planning process

• A mechanism is put in place to deal with connection applications.

• The “Funding Gap” is closed for New and emerging technology Pathfinder projects”appropriate to their technical and commercial status [viz; Use Marine Fund ASAP] to enable UK companies to take advantage

of current lead ; create IPR value, new industries and jobs

• An augmented or “double ROC”mechanism is put in place to support early Pathfinder Marine RenewablesProjects

• THEN:-• Wind energy could contribute 20% of

UK electricity before 2030• Tidal barrages could contribute 6% by

2030 but need Govt. support for long term ROC type contracts

• Other tidal could contribute 1% by 2030

D Lindley: Energy 2100. 08.05.06 40

D Lindley: Energy 2100. 08.05.06 41

David Lindley thanks you for listening –any questions??

D Lindley: Energy 2100. 08.05.06 42

Meeting the challenge – Opportunities and Barriers

D Lindley: Energy 2100. 08.05.06 43

• Transmission constraintsif real and not fixed this is major constraint to meeting Govt. aspirations

• 13GW of connection applications –needs a prioritisation mechanism [£??]

• Planning –needs a prioritisation mechanism or more resources and greater acceptance of national priorities

• Emerging technologies [e.g marine] - need to lower generation costs via Pathfinder projects

• Offshore SEA could be a “killer blow” to the marine renewablesindustry

• Pathfinder projects need financial support from Marine fund ASAP. Funding should be appropriate to the commercial readiness of the technology

• “Augmented” ROC mechanism or “double ROC’s” needed for early marine projects

Tidal Stream Prototypes

D Lindley: Energy 2100. 08.05.06 44

Seaflow – 300kW at 2.7m/sMarine Current Turbines - installed

2003 in Bristol Channel

Stingray – 150kW at 2m/sThe Engineering Business –

installed 2002 in Shetland Isles

Stingray – 150kW at 2m/s.The Engineering Business –installed 2002 – Shetland Isles

Time history for April@ a 6 hour forecast horizon

GH Forecaster Hourly Power EvaluationForecast Horizon T + 6 hrs

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

13-Apr 18-Apr 23-Apr 28-Apr 03-May 08-May

Date - Time

Pow

er (%

of c

apac

ity)

GH ForecasterActual

D Lindley: Energy 2100. 08.05.06 45

Power: 3 month time history @ a 12 hour forecast horizon

GH Forecaster Hourly Power EvaluationForecast Horizon T + 12 hrs

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

13-Feb 23-Feb 04-Mar 14-Mar 24-Mar 03-Apr 13-Apr 23-Apr 03-May 13-May 23-May

Date - Time

Pow

er (%

of c

apac

ity)

GH ForecasterActual

D Lindley: Energy 2100. 08.05.06 46

Capacity penetration (normalised by MD): Future

D Lindley: Energy 2100. 08.05.06 47

System MD Wind capacity anticipated

Germany 75 GW 2012: 29.4 GW (39%)Spain 37 GW 2010: 20 GW (54%)RoI 4.5 GW 2010: 1.1 GW (24%)GB 62 GW 2010: 8 GW (13%)Scotland 5.9 GW 2020: 6 GW (100%)Alberta 7.9 GW 2008: 0.8 GW (10%)Québec 37 GW 2012: 2.2 GW (6%)

D Lindley: Energy 2100. 08.05.06 48

Relationship between capacity credit and reliability cost, GB relevant capacity credits and system characteristics

D Lindley: Energy 2100. 08.05.06 49

Source: UK Energy Research Centre: “The costs and Impacts of Intermittency –an assessment of the evidence”March 2006

Reliability costs of intermittent generation = Fixed costs of energy equivalent thermal plant minus the avoided fixed costs of thermal plant that is displaced by the capacity credit of wind

D Lindley: Energy 2100. 08.05.06 50

Tidal Barrage Projects & ProposalsCountry Location Power

MWEnergy TWh/yr

France La Rance 240 0.5

3.3

2.5

31.0

1.4

3.9

1.1

1.8

18.5

Canada Bay of Fundy – Cumberland basin 1,400

China Various 1,000

Russia Mezan Bay & Tugur 28,000

Korea Siwha & Garolim 740

India Khambat 1,800

Australia Secure Bay & Cape Keraudren 600

Argentina San Jose / Nuevo 600

UK Severn & Mersey 9,300

Tidal Barrage projects and proposals

Proposed elevation and plan of the 16km long Severn Barrage

D Lindley: Energy 2100. 08.05.06 51

Proposed plan of the 2km long Mersey Barrage

D Lindley: Energy 2100. 08.05.06 52

Proposed location of the UK’s 8640 MW Severn Tidal barrage

D Lindley: Energy 2100. 08.05.06 53

Barrage Construction

Caissons built at deep water sites around the UK (& Europe) and towed to the site

Turbine Generators installed at the site with heavy lift crane

Barrage ConstructionCaissons built at deep water sites around the UK(& Europe) and towed to site

Turbine Generators installed at the site with heavy lift crane

D Lindley: Energy 2100. 08.05.06 54

D Lindley: Energy 2100. 08.05.06 55

Ebb Generation (preferred)

Flood Generation

Two-way Generation

Ebb Generation

(preferred)

Flood Generation

Two way Generation

Tidal Barrage Generation

Tidal Barrage Generation

e Proposal 2005 West coast of KoreaFlood generation scheme – to keep basin water levels low & to alleviate pollution in the lake

Siwha Power Barrage proposal 2005 West coast of KoreaFlood generation scheme to keep water levels low & to alleviate pollution in the lake

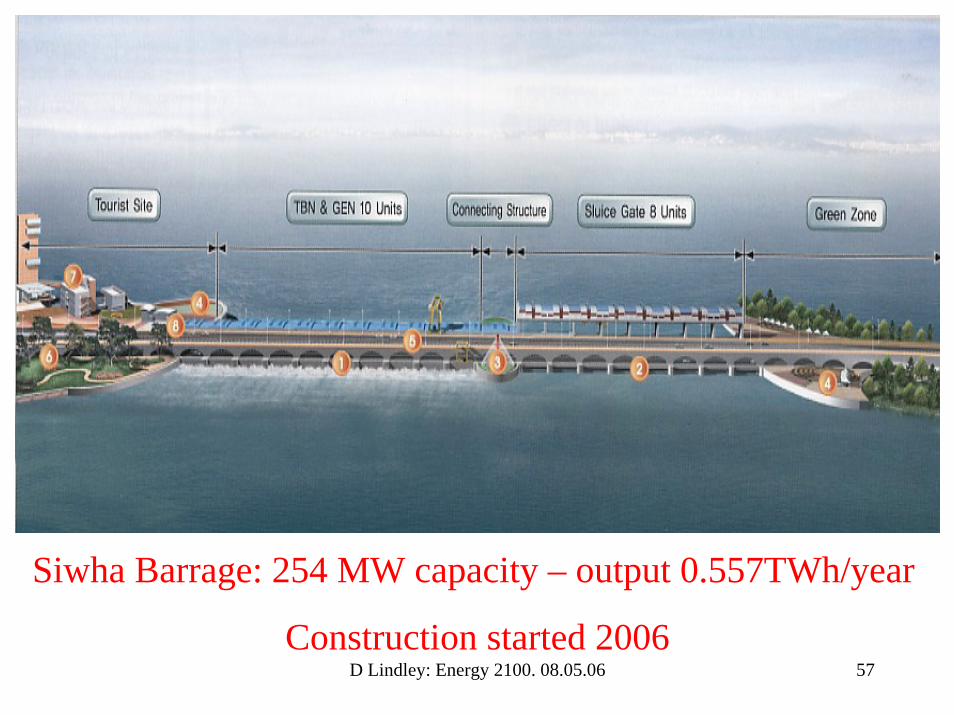

D Lindley: Energy 2100. 08.05.06 56

D Lindley: Energy 2100. 08.05.06 57

Barrage: 254MW capacity - output 0.55TWh/yr

Construction started 2006

Siwha Barrage: 254 MW capacity – output 0.557TWh/year

Construction started 2006

Proposed location of the UK’s 700MW Mersey Barrage

D Lindley: Energy 2100. 08.05.06 58

Offshore wind farm project size

D Lindley: Energy 2100. 08.05.06 59

020406080

100120140160180200

No.

of u

nits

Bly

th

Mid

delg

rund

en

Utg

rund

en

Yttr

e St

engr

und

Hor

ns R

ev

Sam

so

Nys

ted

N H

oyle

Ark

low

Ban

k

Scro

by S

ands

2010

?

Offshore wind farms : Maximum depth

D Lindley: Energy 2100. 08.05.06 60

0

5

10

15

20

25

30

35

HM

WS

[m]

Bly

th

Mid

delg

rund

en

Utg

rund

en

Yttr

e St

engr

und

Hor

ns R

ev

Sam

so

Nys

ted

N H

oyle

Ark

low

Ban

k

Scro

by S

ands

2010

?

Offshore wind farms : Distance offshore

D Lindley: Energy 2100. 08.05.06 61

0

5

10

15

20

25

30

35

40D

isct

ance

offs

hore

[km

]

Bly

th

Mid

delg

rund

en

Utg

rund

en

Yttr

e St

engr

und

Hor

ns R

ev

Sam

so

Nys

ted

N H

oyle

Ark

low

Ban

k

Scro

by S

ands

2010

?

D Lindley: Energy 2100. 08.05.06 62Current Practice and Future Trends

Wind - 2005

IrelandGB

Existing wind farms c. 890MW to date

Future of Offshore Wind Power in UK

• Capital Costs• Construction Risk• Operations costs and

risks• Contracting• Other technical issues

D Lindley: Energy 2100. 08.05.06 63

g

D Lindley: Energy 2100. 08.05.06 64

The Barrage impounds the tide, then the water is released through a bulb turbine to generate electricity

Tidal Barrage – Typical cross sectionTidal Barrage – Typical Cross SectionThe barrage impounds the tide, then the water is released through

bulb turbines to generate electricity

Overview

D Lindley: Energy 2100. 08.05.06 65

L

Output• Power Forecast

Inputs• Numerical Weather Prediction• SCADA System• Site Measurements

Weather Service

D Lindley: Energy 2100. 08.05.06 66

MW added in 2005

D Lindley: Energy 2100. 08.05.06 67

0

500

1000

1500

2000

2500

German

yUSA

SpainIndia

DenmarkChina

Italy UK NL

Portugal

Australia

Canada

AustriaFranceGreec

eSweden

D Lindley: Energy 2100. 08.05.06 68Source: UK Energy Research Centre: The costs and Impacts of Intermittency” March 2006