Embed Size (px)

Citation preview

Canadian Public Policy

Will the Bankruptcy Reforms Work? An Empirical Analysis of Financial Reorganization inCanadaAuthor(s): Timothy C. G. Fisher and Jocelyn MartelSource: Canadian Public Policy / Analyse de Politiques, Vol. 20, No. 3 (Sep., 1994), pp. 265-277Published by: University of Toronto Press on behalf of Canadian Public PolicyStable URL: http://www.jstor.org/stable/3551954 .

Accessed: 14/06/2014 11:58

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

.

University of Toronto Press and Canadian Public Policy are collaborating with JSTOR to digitize, preserveand extend access to Canadian Public Policy / Analyse de Politiques.

http://www.jstor.org

This content downloaded from 185.44.77.82 on Sat, 14 Jun 2014 11:58:23 AMAll use subject to JSTOR Terms and Conditions

Will the Bankruptcy Reforms Work? An Empirical Analysis of Financial Reorganization in Canada TIMOTHY C.G. FISHER Department of Economics Wilfrid Laurier University and JOCELYN MARTEL CRDE, Universit6 de Montrial*

Les recentes modifications a la Loi sur la faillite poursuivent deux objectifs: (i) accroitre le nombre de reorganisations financibres au detriment des faillites et (ii) assurer une protection accrue aux travailleurs d'entreprises en faillite. Sur la base d'une banque de donn6es unique comprenant 338 propositions de reorganisation d'entreprises soumises au Canada au cours de la p6riode 1978-1987, nous 6valuons l'efficacit6 de la r6forme & atteindre ces objectifs. L'estimation d'un modble logit de la probabilit6 d'acceptation d'une proposition par les creanciers non-garantis nous amine A la conclusion que cette probabilit6 d'acceptation augmentera d'environ 7 points de pourcentage suite aux modifications apportdes la loi. Ceteris paribus, cela devrait se traduire par la sauvegarde d'environ 120 emplois par annee. Donc, bien que nous puissions anticiper une augmentation du taux d'acceptation des propositions par les cr6anciers, I'impact r6el de la r6forme sera plut6t faible.

The new Bankruptcy Act has two clear aims: (i) to increase the number of firms opting for reorganization over liquidation, and (ii) to increase protection for wage earners at bankrupt firms. The paper examines a unique micro data set of 338 commercial financial reorganization proposals filed in Canada during the period 1978-87 to determine whether these aims are likely to be met. Estimates from a logit model of reorganization plan acceptance indicate that the new Act will result in a roughly 7 percentage point increase in the number of reorganization plans that creditors accept. Everything else being equal, these changes are estimated to save about 120 jobs per year in Canada. Thus, while the new Act will increase the rate at which creditors accept reorganization plans, the actual impact of a higher acceptance rate will be quite small.

I Introduction

n June 1992, parliament passed legisla- tion to reform the bankruptcy process in

Canada. Bill C-22, which became law December 1, 1992, represents the first sub- stantial changes to the Bankruptcy Act since 1949. According to government pro- nouncements at the time, the new law is aimed specifically at two areas of the bank- ruptcy process. The principal aim of the new Bankruptcy Act is to encourage finan- cial reorganization in order to save the jobs

that would be lost in the event of liquida- tion. At a press conference announcing the tabling of the Act, then Minister of Con- sumer and Corporate Affairs, Pierre Blais, stated: 'We are changing the rules of the current Act to make it easier for businesses that are experiencing financial difficulties to reorganize their affairs and thus improve their chances of survival and save jobs'.' A secondary goal of the new Act is to increase the access of workers to funds for the pay- ment of wages owed by bankrupt firms by making the payment of overdue wages a

Canadian Public Policy - Analyse de Politiques, XX:3:265-277 1994 Printed in Canada/Imprim6 au Canada

This content downloaded from 185.44.77.82 on Sat, 14 Jun 2014 11:58:23 AMAll use subject to JSTOR Terms and Conditions

condition of reorganization. Other key changes to the Bankruptcy Act that affect financial reorganization include changes to the voting procedure, the stay of proceed- ings, and changes affecting secured credi- tors, Crown claims, and wage claims.

In some sense, the main goals of en- couraging reorganization and increasing protection for workers are inconsistent. Forcing reorganizing firms to pay overdue wages increases the financial burden on the firms and, hence, makes reorganization more difficult. Nonetheless, on balance, the new Act may increase the frequency of re- organization as long as the effect of com- pulsory wage payments is offset by changes elsewhere. Thus, the ultimate affect of the new Act is an empirical matter. This paper analyses a micro data set of 338 financial reorganization proposals filed in Canada during the period 1978-87 in order to deter- mine whether the stated goals of the new Act are likely to be met. In the past, aggre- gate data have been used to analyse bank- ruptcy issues.2 However, the new Act will affect the bankruptcy process at the levei of individual firms and, therefore, it is impor- tant to have micro data.

The fundamental structure of the finan- cial reorganization process remains un- touched by Bill C-22. For a firm to reorgan- ize, two things must happen. First, the management or owners of the bankrupt firm must decide to reorganize, as opposed to liquidate, the firm's assets.3 Second, if reorganization is chosen, unsecured credi- tors must decide whether to accept the terms of the firm's reorganization plan. Given the structure of the reorganization process, an increase in financial reorgani- zations may be accomplished in two ways: an increase in the number of firms opting for reorganization over liquidation, or an increase in the number of plans that unse- cured creditors accept. The data in this paper allow us to estimate the impact of the bankruptcy reforms on the unsecured cred- itors' decision. We return to the impact of the reforms on the firm's decision in the final section of the paper.

The paper proceeds as follows. The next section uses the data to provide an overview of the financial reorganization process in Canada. Section III discusses specific re- forms to the Bankruptcy Act and explains how, in principle, the reforms are expected to affect the process of reorganization. Sec- tion III also presents preliminary empirical evidence on the effects of the reforms. Sec- tion IV uses logit analysis of the creditors' reorganization decision to determine whether the new Act will indeed result in an increase in the frequency of reorganiza- tion.

II An Overview of Reorganization

The micro data set comprises information on 338 firms that filed for financial reor- ganization under the jurisdiction of the 1949 Bankruptcy Act during the period 1978-87.4 Table 1 contains some facts about the firms and their reorganization plans. The firms in the sample are quite small, having average liabilities of $4.0 million and average assets of $2.4 million.5 In terms of numbers, there are more unse- cured creditors (ordinary creditors and pre- ferred creditors) than secured creditors but, in terms of debt, secured creditors have a relatively larger presence. Preferred claims average $96,100 and are made up mostly of Crown claims, which average $79,600; wage claims average only $9,300. As may be expected from financial data, the variables are skewed, which is clearly seen by comparing mean and median values. Two variables are of particular interest to unsecured creditors voting on a reorganiza- tion plan: the pay-off rate they are offered in the plan and the pay-off rate they can re- ceive if the firm's assets are liquidated.6 As indicated in Table 1, reorganization plans offer ordinary creditors an average of 44 cents on each dollar of debt and the firms have an average liquidation value of 30 cents per dollar of ordinary claims.

Table 2 indicates the fate of the 241 firms in the data whose cases have been officially closed by the bankruptcy court.7 Creditors

266 Timothy C.G. Fisher and Jocelyn Martel

This content downloaded from 185.44.77.82 on Sat, 14 Jun 2014 11:58:23 AMAll use subject to JSTOR Terms and Conditions

Table 1 Summary statistics for financial reorganization plans

Variable Mean Median Standard Minimum Maximum deviation

Financial variables:a Secured claims 1,890.5 222.3 11,920.0 0.0 189,460.0 Ordinary claims 1,324.7 342.8 6,185.5 0.0 92,852.0 Preferred claims 96.1 17.9 337.3 0.0 4,415.2

Crown claims 79.6 11.0 326.5 0.0 4,415.2 Wage claims 9.3 0.0 44.1 0.0 661.1

Total liabilities 3,971.7 791.6 18,228.0 16.0 247,620.0 Total assets 2,372.1 299.6 10,955.0 0.0 122,100.0

Creditor variables: Number of secured creditors 2.6 2.0 3.7 0.0 42.0 Number of ordinary creditors 80.4 41.0 173.0 0.0 2,487.0 Number of preferred creditors 13.6 2.0 55.8 0.0 827.0

Number of wage creditors 11.0 0.0 55.0 0.0 819.0

Pay-off rate variables:b Liquidation pay-off rate 28.7 10.3 35.3 0.0 100.0 Reorganization pay-off ratec 43.6 32.3 83.5 0.0 101.0

Other variables: Number of amendments 0.4 0.0 0.6 0.0 3.0 Number of days between filing and voting 52.5 24.0 113.6 11.0 1,682.0

Notes: The sample size is 338 plans. aFinancial variables are reported in thousands of December 1993 dollars, deflated by the CPI. bPay-off rate variables are reported in percent. CThe reorganization pay-off rate is based on the 284 plans for which the information is available.

Table 2 Fate of reorganization plans

Total plans 241 - Rejected plans 59 = Accepted plans 182 Acceptance rate 182/241 = 75.5% - Defaulted plans 34 Default rate 34/182 = 18.7% = Completed plans 148 Success rate 148/241 = 61.4%

Note: The sample is restricted to 241 firms whose cases have been officially closed by the Bankrupcty Court.

voted to accept 182 of the 241 Vlans for an acceptance rate of 76 per cent. Of the 182 firms with accepted plans, 34 subsequently defaulted on the terms of their proposals and were liquidated for a default rate of 19 per cent. The remaining 148 firms success- fully completed the terms of their pro- posals. The overall success rate of reor- ganizing firms is, therefore, 61 per cent. For the firms that reorganize successfully, the average time to complete the reorganiza-

tion process is slightly under three years.

III Changes in the Bankruptcy Act

The new Act relaxes the voting criteria that determine whether a reorganization plan is accepted. Under the 1949 Act, a creditors meeting was called to determine the fate of a reorganization plan. Provided that (1) a majority of the unsecured creditors at the meeting voted in favour of the plan, and (2)

Will Bankruptcy Reforms Work? 267

This content downloaded from 185.44.77.82 on Sat, 14 Jun 2014 11:58:23 AMAll use subject to JSTOR Terms and Conditions

the claims of those voting in favour repre- sented at least three-quarters of the total claims of all creditors at the meeting, the plan was deemed to be accepted. Under the new Act, criterion (2) is changed so that the claims of those voting in favour only have to cover two-thirds of the total claims of creditors at the meeting. Obviously, the new criterion will increase the number of plans that are accepted. This is clearly de- monstrated in the micro data. Examination of the 119 closed files from Montreal and Toronto reveals that 21 proposals were re- jected because the claims of creditors voting in favour of the plan accounted for less than three-quarters of the total claims of voting creditors, implying an acceptance rate of 82 per cent (98 of 119). Had the new voting cri- teria been in effect, the number of rejected proposals would have fallen from 21 to 15. Thus, ceteris paribus, the acceptance rate would have been 87 per cent (104 of 119) under the new criteria, an increase of five percentage points. The new Bankruptcy Act will affect four other aspects of financial re- organization.

Secured Creditors Secured creditors were not bound by the 1949 Bankruptcy Act. As long as a firm was in default, secured creditors could demand immediate repayment of loans or petition to have a receiver appointed to protect their assets. This power essentially enabled a se- cured creditor to terminate any reorganiza- tion plan that was not in its interest. Secured creditors are given a more explicit role in the new Act. First, to provide reor- ganizing firms with some 'breathing space,' the claims of secured creditors who have not started enforcing their security are now stayed for a period of 30 days upon the fil- ing by the debtor of a notice of intention to make a proposal. Second, debtors are al- lowed to include secured creditors in reor- ganization plans. If a secured creditor votes in favour of the plan, the creditor is bound by the terms of the plan. If a secured cred- itor votes against the plan, the creditor is not bound by the terms of the plan and may,

in the event of default, claim its security from the firm.9 A secured creditor that is not included in the plan may also, in the event of default, claim its security after giving the firm ten days notice.

The view of bankruptcy theorists (Bulow and Shoven, 1978; White, 1989) is that se- cured creditors hinder financial reorgani- zation. The intuition for this view is as fol- lows. An insolvent firm is revealed to be a non-viable enterprise, so continuation of the firm's existence will only deplete the value of the assets held as collateral by the secured creditor. Thus, it is in the interest of the secured creditor to prevent reorgani- zation. This view appears to have been partly adopted by policy-makers. However, by allowing debtors to include secured cred- itors in reorganization plans, policy-mak- ers have also recognized that there may be room for negotiation between debtors and secured creditors.

According to the data, 85 per cent of the proposals in the sample have some secured claims. Thus, the new provisions covering secured creditors could potentially affect most reorganization plans. Nonetheless, the 30 day stay on secured creditors is likely to have only a minor impact. As pointed out by Martel (1991), secured creditors have al- ways played a key role in the reorganization process. In practice, the informal approval of secured creditors was a necessary condi- tion for any successful reorganization plan under the old Act. Under the new Act, se- cured creditors can still terminate reor- ganization after 30 days, so firms reor- ganizing without the support of secured creditors will be unable to extend their life appreciably. Firms reorganizing with the support of secured creditors can, under the new Act, include the creditors in the terms of the plan, but this is just a formal recog- nition of a process that implicitly existed under the old Act. Therefore, we expect the amendments affecting secured creditors will have little real impact.

Stay of Proceedings According to the old Act, a stay of proceed-

268 Timothy C.G. Fisher and Jocelyn Martel

This content downloaded from 185.44.77.82 on Sat, 14 Jun 2014 11:58:23 AMAll use subject to JSTOR Terms and Conditions

ings covering all unsecured creditors auto- matically came into effect when a firm filed a reorganization plan. The stay elapsed when the plan was rejected by the creditors or when the terms of the plan were completed. Under the new Act, the claims of unsecured and secured creditors are stayed for 30 days as soon as the firm files a notice of intention to make a proposal. After 30 days, a firm may either present a plan to its creditors or apply to the court to extend the stay (in 45-day segments) up to a maximum of five months. The extended stay applies to all creditors. Either way, once the proposal is submitted to the cred- itors, a further 21 days elapses before the creditors vote. Firms are allowed to ask the creditors for an extension of the 21-day pe- riod. Thus, the new Act stays the claims of all creditors for a minimum of 51 days and a maximum of six months.

There were no explicit time limits under the old Act, so the new law apparently im- poses constraints on insolvent firms. However, according to our discussions with an expert in bankruptcy law at Consumer and Corporate Affairs Canada (CCA), even though there was no legislated limit under the old Act, there was an informally recog- nized limit on the time between filing and voting of 21 days. According to the micro data, the mode of the time between filing and voting is 21 days, giving some evidence to support the expert's claim. Additional evidence to support implicit time con- straints under the 1949 Act takes the form of so-called 'holding' proposals. A holding proposal, of which there are 55 in the sample, is an interim document submitted by firms that require extra time to prepare a complete proposal.10 If there were no im- plicit limits on the time between filing and voting under the old Act, firms could take all the time they needed to prepare plans and hence, according to the law, there was no need for firms to file holding proposals in the first place. Thus, the very existence of holding proposals suggests that time limits were implicitly observed under the Bankruptcy Act of 1949.

In our view, the new time limits on the stay of proceedings simply formalize an im- plicit 21-day limit present in the old Act. In addition, the provision that allows firms to extend the stay of proceedings is a formal recognition that some firms may take sig- nificantly longer than others to sort out their financial affairs. Table 1 shows that the mean elapsed time between filing and voting under the old Bankruptcy Act was 53 days. Yet almost 80 per cent of the pro- posals took 51 days or less to be submitted for the creditors' vote, suggesting that the majority of reorganizing firms will not re- quire the minimum stay provided by the new Act. On the other hand, just over 5 per cent of the proposals in the sample took longer than six months between filing and voting, so the maximum stay of six months under the new Act would not have been long enough for a few firms in the sample. On balance, it is not obvious how the new restrictions on the stay of proceedings will affect the mean time between filing and voting. It is even less clear how the restric- tions will affect the likelihood of reorgani- zation. In the next section, we investigate whether the length of time between filing and voting has any impact on the accep- tance rate of reorganization plans.

Crown Priority Under the 1949 Act, federal and provincial governments were given Crown priority, which placed their claims ahead of other unsecured creditors. Crown claims had to be paid in full as a condition for the bank- ruptcy court's approval of the plan. Under the new legislation, Crown priority is abolished, with the exception of 'source de- ductions,' which comprise income taxes, Canada Pension Plan contributions, and Unemployment Insurance premiums. Moreover, firms have up to six months to repay source deductions to the Crown. The new rules will improve the cash flow of re- organizing firms and, hence, raise their chances of successfully completing reor- ganization. This should lead to an increase in the proportion of plans accepted.

Will Bankruptcy Reforms Work? 269

This content downloaded from 185.44.77.82 on Sat, 14 Jun 2014 11:58:23 AMAll use subject to JSTOR Terms and Conditions

Information from 128 closed files from Montreal and Toronto indicates source de- ductions represent just under half (48%) of Crown claims. Thus, the new Act transfers slightly more than half of Crown claims into the ordinary claims category. On aver- age, Crown claims account for roughly 4 per cent of total claims against firms in the sample. This may not seem to be a signifi- cant amount, but recall that Crown claims had to be repaid in full under the old Act. In other words, cash-poor reorganizing firms were burdened with immediate pay- ments amounting to 4 per cent of their total debt. The new Act cuts these immediate payments in half. Given that Crown claims occur in 80 per cent of the proposals in the sample, this amendment is expected to have a significant impact.11

Wage Earners Under the 1949 Act, employees with wage claims were fourth on the list of preferred claims after funeral expenses (in the case of a deceased debtor), administration costs and trustees fees, and the levy of the super- intendent of bankruptcy. After these claims were paid, each employee claim for wages, vacation pay, and expenses - for services rendered up to three months prior to the re- organization filing date - ranked as a pre- ferred claim for up to $500 for wages and $300 for expenses; any additional amounts ranked as an ordinary claim. Under the new Act, the maximum amount for an em- ployee preferred claim has been raised to $2,000 for wages and $1,000 for expenses and the period for which claims may be made has been extended from three to six months prior to the filing date. Reorganiza- tion plans must also provide for the imme- diate and full repayment of the preferred claims of employees in order for the plan to proceed. In addition, wage earners are no longer permitted to vote on the reorganiza- tion plan along with other unsecured cred- itors.

The effect of these changes will likely be exactly the opposite to the change affecting Crown claims. That is, raising the amount

of preferred claims that reorganization plans must satisfy, reduces the cash flow of firms and, hence, lowers their chances of successfully completing reorganization. Furthermore, taking away the voting rights of wage earners will reduce the ac- ceptance rate of proposals because most workers probably vote in favour of reor- ganization in order to preserve their jobs.

Only 79 plans (23%) involved some wage claims. In the full sample, there is an aver- age of 11 wage claims per plan. In the sample of 79 plans with wage claims, there is an average of 47 wage claims per plan and the average claim per worker is $653 (1981 dollars). Therefore, the previous coverage of $500, was, on average, not high enough to provide full protection to wage earners in 1981. Translating to December 1993 dol- lars, the average wage claim per worker is $1,123. Thus, increasing the $500 protec- tion to $2,000 should be enough to cover most wage claims today. Notice that the new level of coverage is still lower, in real terms, than the coverage originally pro- vided in the 1949 Act; $500 protection in 1949 is equivalent to protection of $3,568 in December 1993.

In summary, the relaxed voting criteria and the removal of Crown priority will likely increase the number of plans credi- tors accept; increased protection for wage earners will probably decrease the number of plans accepted. The effect of revisions af- fecting secured creditors and the stay of proceedings is uncertain. On balance, therefore, it is not clear a priori how the new Act will affect the proportion of firms successfully reorganizing. In the next sec- tion we estimate a model of the creditors' decision to try to determine the overall ef- fect of the revisions to the Bankruptcy Act.

IV Estimation and Results

To determine how the changes to the Act will affect the number of plans accepted by unsecured creditors, we estimate a reduced form model of the incidence of proposal ac- ceptance, i.e. the proposal acceptance

270 Timothy C.G. Fisher and Jocelyn Martel

This content downloaded from 185.44.77.82 on Sat, 14 Jun 2014 11:58:23 AMAll use subject to JSTOR Terms and Conditions

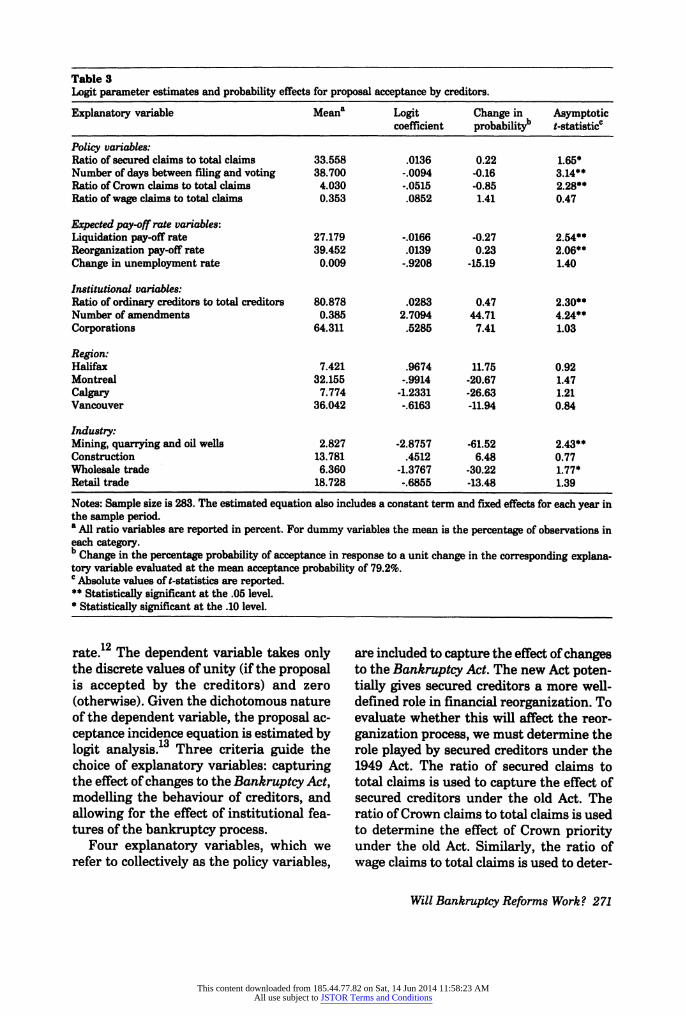

Table 3 Logit parameter estimates and probability effects for proposal acceptance by creditors.

Explanatory variable Meana Logit Change in Asymptotic coefficient probabilityb t-statistice

Policy variables: Ratio of secured claims to total claims 33.558 .0136 0.22 1.65* Number of days between filing and voting 38.700 -.0094 -0.16 3.14** Ratio of Crown claims to total claims 4.030 -.0515 -0.85 2.28** Ratio of wage claims to total claims 0.353 .0852 1.41 0.47

Expected pay-off rate variables: Liquidation pay-off rate 27.179 -.0166 -0.27 2.54** Reorganization pay-off rate 39.452 .0139 0.23 2.06** Change in unemployment rate 0.009 -.9208 -15.19 1.40

Institutional variables: Ratio of ordinary creditors to total creditors 80.878 .0283 0.47 2.30** Number of amendments 0.385 2.7094 44.71 4.24** Corporations 64.311 .5285 7.41 1.03

Region: Halifax 7.421 .9674 11.75 0.92 Montreal 32.155 -.9914 -20.67 1.47 Calgary 7.774 -1.2331 -26.63 1.21 Vancouver 36.042 -.6163 -11.94 0.84

Industry: Mining, quarrying and oil wells 2.827 -2.8757 -61.52 2.43** Construction 13.781 .4512 6.48 0.77 Wholesale trade 6.360 -1.3767 -30.22 1.77* Retail trade 18.728 -.6855 -13.48 1.39

Notes: Sample size is 283. The estimated equation also includes a constant term and fixed effects for each year in the sample period. a All ratio variables are reported in percent. For dummy variables the mean is the percentage of observations in each category. b Change in the percentage probability of acceptance in response to a unit change in the corresponding explana- tory variable evaluated at the mean acceptance probability of 79.2%. C Absolute values of t-statistics are reported. ** Statistically significant at the .05 level. * Statistically significant at the .10 level.

rate.12 The dependent variable takes only the discrete values of unity (if the proposal is accepted by the creditors) and zero (otherwise). Given the dichotomous nature of the dependent variable, the proposal ac- ceptance incidence equation is estimated by logit analysis.13 Three criteria guide the choice of explanatory variables: capturing the effect of changes to the Bankruptcy Act, modelling the behaviour of creditors, and allowing for the effect of institutional fea- tures of the bankruptcy process.

Four explanatory variables, which we refer to collectively as the policy variables,

are included to capture the effect of changes to the Bankruptcy Act. The new Act poten- tially gives secured creditors a more well- defined role in financial reorganization. To evaluate whether this will affect the reor- ganization process, we must determine the role played by secured creditors under the 1949 Act. The ratio of secured claims to total claims is used to capture the effect of secured creditors under the old Act. The ratio of Crown claims to total claims is used to determine the effect of Crown priority under the old Act. Similarly, the ratio of wage claims to total claims is used to deter-

Will Bankruptcy Reforms Work? 271

This content downloaded from 185.44.77.82 on Sat, 14 Jun 2014 11:58:23 AMAll use subject to JSTOR Terms and Conditions

mine the effect of wage claims under the old Act.14 Lastly, to see whether time affects the creditors' decision, the number of days between the filing and voting on the plan is added to the policy variables.

In deciding how to vote, we assume that unsecured creditors compare the pay-off rate under liquidation to the expected pay- off rate under reorganization, voting for the option with the higher pay-off. The ex- pected pay-off in reorganization depends on the pay-off rate that the firm is offering in the plan and the probability that the firm will successfully complete the plan. The probability that the firm will complete the plan is hypothesized to depend on the ex- pected state of the business climate which we proxy by the change in the unemploy- ment rate between the quarter when the proposal is filed and the previous quarter. The creditors' expected pay-off variables are thus: the liquidation pay-off rate, the reorganization pay-off rate, and the change in the unemployment rate. Everything else being equal, the acceptance rate should in- crease with the reorganization pay-off rate and decrease with the liquidation pay-off rate and the change in the unemployment rate.

To capture institutional features of the reorganization process we use a dummy (0- 1) variable for corporations (as opposed to unincorporated businesses). As a proxy for bargaining between the creditors and the firm, the number of amendments to pro- posals is added as an explanatory variable. White (1989) argues that firms with rela- tively large numbers of ordinary creditors may be more likely to favour reorganiza- tion, because ordinary creditors are the only group likely to benefit from financial reorganization. The ratio of ordinary cred- itors to the total number of creditors is used to control for the effect of ordinary credi- tors. Lastly, industry, region, and year dummy variables are used as controls.

Table 3 contains the estimation results for the logit model. The logit coefficients measure the effect of changes in the expla- natory variables on an unobserved variable

that may be interpreted as the propensity for creditors to accept a reorganization pro- posal. For our purposes, it is more useful to determine the effects of the variables on the probability for creditors to accept a reor- ganization proposal. Because the prob- ability effects differ for each observation, they are calculated at the means of the data and displayed in the 'Change in probability' column of Table 3. For the dummy (0-1) ex- planatory variables, it is inappropriate to calculate a marginal change, according- ly we calculate the effects of discrete changes.15 Owing to a lack of information on key variables, the 55 holding proposals are deleted from the sample resulting in a sample of 283 plans.

Secured Creditors Contrary to the conjecture of Bulow and Shoven (1978) and White (1989), results in Table 3 show that secured creditors do not have a negative impact on the reorganiza- tion process. A 1 per cent increase in the ratio of secured claims to total claims in- creases the acceptance probability by 0.22 per cent and the estimate is significant at the .10 level.16 As a result, it does not ap- pear that the fact that debtors may include secured creditors in the terms of a reorgani- zation plan under the new Act will reduce the frequency of plans accepted by credi- tors.

The positive correlation between the presence of secured creditors and the accep- tance rate is consistent with our view that secured creditors play an informal role in reorganization. Because secured creditors could usually terminate a plan at any time under the old Act, it is likely that most re- organizing firms had the support of secured creditors. In other words, our sample is likely to be made up largely of firms having secured creditors that favour reorganiza- tion. It is also likely that secured creditors are better-informed than unsecured credi- tors about the financial prospects of the firm. Thus, unsecured creditors may inter- pret the relative size of secured claims as a signal of a firm's viability. Accordingly, un-

272 Timothy C.G. Fisher and Jocelyn Martel

This content downloaded from 185.44.77.82 on Sat, 14 Jun 2014 11:58:23 AMAll use subject to JSTOR Terms and Conditions

secured creditors interpret a high ratio of secured debt to total debt as a signal of a vi- able firm, and, as a result, the unsecured creditors vote to accept the reorganization plan.

Stay of Proceedings The probability of a proposal being ac- cepted decreases with the length of time be- tween filing and voting. An extra day between filing and voting decreases the ac- ceptance probability by 0.16 per cent and the effect is statistically significant at the .05 level. An interpretation is that, under the old Act, creditors interpreted delays in the reorganization procedure as evidence of a weak firm. Everything else equal, longer delays imply weaker firms and, hence, cred- itors are less likely to favour reorganiza- tion. Hence, under the old Act, it seems that firms were implicitly constrained in how long they could draw out the reorganization process. The result suggests that attempts by firms to postpone the vote under the new Act could backfire because creditors inter- pret delays as a sign of weakness. This being the case, the provisions of the new Act that conditionally allow firms to lengthen the period between filing and voting may have no effect because it is not to the bene- fit of firms to use the longer time.

Crown Priority Results indicate that proposals with a higher ratio of Crown claims to total claims are significantly less likely (at the .05 level) to be accepted. A 1 per cent increase in the ratio of Crown claims to total claims decreases the acceptance probability by 0.85 per cent. This is consistent with the view that the statutory nature of payments to the Crown in the old Act were perceived by unsecured creditors as a burden on the cash flow of firms. At the margin, the re- quirement in the old Act for firms to repay the Crown in full as a precondition for ac- ceptance of the proposal did prevent some firms from reorganizing. As noted in the last section, the amount of Crown claims

that firms have to repay immediately is about 50 per cent lower in the new Act which would lower the average ratio of Crown to total claims from 4 per cent to 2 per cent. Our results indicate that the 2 per- centage point drop in Crown claims will in- crease the acceptance rate of proposals by 1.7 per cent.

Wage Earners Although the new Act offers greater protec- tion to wage earners, it could impose a larger burden on debtors and possibly re- duce the chance of a successful reorganiza- tion. The results in Table 3 reveal that proposals by firms with proportionately larger wage claims have a higher prob- ability of acceptance.17 This result seems at odds with the hypothesis that wage claims are a burden on reorganizing firms, but re- call that wage earners were allowed to vote on reorganization under the old Act. Thus, a higher proportion of wage claims may simply mean more votes in favour of reor- ganization. If this is the case, taking away the voting power of wage earners, as under the new Act, may reduce the acceptance rate of proposals. Having said this, the coefficient on the wage term is not statisti- cally significant, so the estimates imply that the provisions of the new Act regard- ing wage claims will not have a substantial impact on proposal acceptance rates.

In conclusion, our results indicate that had the firms in our sample been subject to the new Bankruptcy Act the acceptance rate of reorganization plans would almost cer- tainly have been higher. Removing the pri- ority of Crown claims will certainly have a positive impact on the acceptance rate. Pro- visions affecting secured creditors and wage claimants are not estimated to have a significant impact on the acceptance rate. The effect of the longer stay of proceedings under the new Act is hard to judge, because the stay may be extended by the firm. However, if firms are rational, then they are likely to be fairly selective about when they extend the proceedings.

Will Bankruptcy Reforms Work? 273

This content downloaded from 185.44.77.82 on Sat, 14 Jun 2014 11:58:23 AMAll use subject to JSTOR Terms and Conditions

The joint significance of the policy vari- ables may be interpreted as a statistical test of whether the bankruptcy reforms will have an impact on acceptance rates. A likelihood-ratio test that the coefficients on the policy variables are jointly equal to zero yields a X2 test statistic of 17.64 with four degrees of freedom and a probability value of 0.0015. Therefore, there is statistically significant evidence at the .01 level that the new Bankruptcy Act will have an impact on acceptance rates. Quantitatively, however, the changes to the Act are estimated to have only a small impact on acceptance rates.

Several other results in Table 3 are note- worthy. First, as expected, plans offering unsecured creditors higher pay-off rates are more likely to be accepted and firms with higher liquidation pay-off rates are less likely to have plans accepted. Second, the coefficient on the unemployment varia- ble indicates some weak evidence that pro- posal acceptance rates are procyclical; fal- ling when the unemployment rate is rising and rising when the unemployment rate is falling. Third, as conjectured by White (1989), plans with proportionately more or- dinary creditors are more likely to be ac- cepted. Fourth, there is a positive correla- tion between the number of amendments to the plan and the acceptance rate, indicating that there is bargaining occurring between firms and creditors. Fifth, there is no sig- nificant difference between the acceptance rates of corporate plans over plans made by owner-operated businesses. The coeffi- cients on the region variables indicate that there is very little variation in acceptance rates across regions. The coefficients on the industry variables indicate that the mining, quarrying and oil wells industry and the wholesale trade industry have significantly lower acceptance rates compared to other industries. Together, the control variables are only marginally significant: a likeli- hood-ratio test of the hypothesis that the coefficients on the industry, region and year dummy variables are jointly zero gives a x2 test statistic of 27.21 and a probability value of 0.075.

V Conclusion

The relaxed voting criteria is estimated to raise the acceptance rate of reorganization plans by 5 percentage points and the change in Crown priority is estimated to in- crease the acceptance rate by 1.7 percent- age points. If the other changes to bank- ruptcy law have no effect on the acceptance rate, as the estimates suggest, our results indicate that the acceptance rate would have been 6.7 percentage points higher had the new Act been in effect over the period 1978-87. Because 1,985 reorganization at- tempts were made over the sample period, a 6.7 percentage point higher acceptance rate translates into an extra 133 accepted plans over 1978-87. Given a default rate of 19 per cent, 108 firms that would not have reorganized under the old Act would have successfully reorganized under the new Act, everything else being equal. Based on an average of 11 workers per reorganization attempt, the new Bankruptcy Act is esti- mated to save 1,188 jobs over a ten-year pe- riod, or roughly 119 jobs per year in Canada. Thus, while it is true that the changes to the Act are estimated to increase the accep- tance rate of reorganization plans, one of the principal aims of the new legislation, we anticipate that the actual effect of these changes will be quite small.

Having said this, the paper has focused on the effects of the new Act on the accep- tance rate of reorganization plans. The new Act could also increase the frequency of fi- nancial reorganization by encouraging more firms to choose reorganization over liquidation. Without more data, it is im- possible to do more than conjecture about the effect of the new Act on the liquidation- reorganization decision of an insolvent firm. However, because the acceptance rate of proposals will very probably increase, it is reasonable to expect that the new Act will lead more firms to choose reorganization over liquidation. If this effect is sufficiently large, the number of jobs saved by bank- ruptcy reform could be significantly higher than 120 per year.

274 Timothy C.G. Fisher and Jocelyn Martel

This content downloaded from 185.44.77.82 on Sat, 14 Jun 2014 11:58:23 AMAll use subject to JSTOR Terms and Conditions

Finally, it is worth pointing out that the new Act is based on the assumption that raising the frequency of financial reorgani- zation is a desirable goal. But this is not necessarily the case. In a world of perfect information, there would be little need for a financial reorganization procedure. Firms that were not financially viable would have their assets liquidated; viable operations in financial distress would be given extra time to pay their bills. Imper- fect information should, therefore, be con- sidered the rule rather than the exception in financial reorganization. This being the case, some financially viable firms will be refused reorganization, because, for ex- ample, they are unable to convince credi- tors of the firm's viability. Likewise, some firms that are not financially viable may at- tempt to reorganize at the expense of cred- itors who are not fully informed of the firm's financial state.18 This second 'ineffi- ciency' is demonstrated by the data: 19 per cent of reorganization plans accepted by creditors enter into bankruptcy before the terms of the plans are completed.19 By rais- ing the number of reorganizations, the new Bankruptcy Act will raise the number of firms that will default on reorganization plans. Therefore, a cost of the new Act will be the burden on creditors and the bank- ruptcy system resulting from firms default- ing on proposals that would not have been attempted under the old Act. It is not ob- vious that the benefits of the new Act, measured in terms of the additional jobs saved, will more than offset these higher costs.

Data Appendix

Every reorganization proposal made under the Bankruptcy Act is filed with one of 15 regional bankruptcy offices of CCA, the fed- eral government department that is ulti- mately responsible for the administration of Canadian bankruptcy law. The data used in the present study are taken from these files, which were kindly made available to the authors by the Bankruptcy Branch of

CCA.20 For the study, attention is limited to the

approximately 1,985 commercial reorgani- zation proposals filed at the largest offices in each of five regions of the country (Hali- fax, Montreal, Toronto, Calgary, and Van- couver) during the period 1978-87.21 Using a master-list of proposal file-numbers kept by CCA, a random sample of 499 proposals is selected from the 1,985.22 The sample is chosen to be 'balanced,' that is the sample is representative of the regional distribu- tion of proposals filed each year over the sample period.

Because the study focuses on commer- cial reorganization proposals, consumer proposals are omitted from the sample, re- ducing the sample by 55 proposals to 444.23 Owing to insufficient data and missing or incomplete files a further 105 proposal files are deleted from the sample. The final sample has 338 proposal files, of which 241 are officially closed and 97 are active.24 The sample is regionally divided as follows: Halifax, 22 proposals (6.5%); Montreal, 120 proposals (36%); Toronto, 67 proposals (20%); Calgary, 23 proposals (6.8%), and; Vancouver, 106 proposals (31%).

We have the following information for each proposal: the office where the proposal is filed; the industry of the business submit- ting the proposal; the filing date of the pro- posal; the filing dates of the amendments to the proposal, if applicable; the creditors' proposal decision, i.e. accept or reject the proposal; the date of the vote on the pro- posal; the value of unsecured, secured, pre- ferred, and Crown claims against the debt- or; the number of unsecured, secured, and preferred creditors; the percentage pay-off to unsecured creditors as specified in the proposal; the value of wage claims, either unsecured or preferred, against the debtor; the number of wage claimants; and, whether the proposal is a 'holding' pro- posal. The liquidation pay-off rate is calcu- lated as the ratio of the firm's gross liqui- dation value divided by the claims of ordinary creditors. The gross liquidation value of the firm is defined as the total as-

Will Bankruptcy Reforms Work? 275

This content downloaded from 185.44.77.82 on Sat, 14 Jun 2014 11:58:23 AMAll use subject to JSTOR Terms and Conditions

sets of the firm minus secured and pre- ferred claims.

Notes

* We would like to thank the Bankruptcy Branch of the Department of Consumer and Corporate Af- fairs (now called the Department of Industry and Science) for making available the data used in the study. We would also like to thank John Chant, Henri Massue-Monat, Frangois Vallaincourt, and an anonymous referee for helpful comments. Er- rors and omissions are the responsibility of the authors.

1 Canada. Consumer and Corporate Affairs, News Release, June 13, 1991.

2 See Martel (1991) for an example of a bankruptcy study using aggregate data in Canada.

3 Reorganization and liquidation only apply if the firm chooses the protection of bankruptcy law; there are other options available outside bank- ruptcy law, like informal workout agreements, walk-aways, etc.

4 The data set is described briefly in an appendix. For a more detailed description of the data see Fisher and Martel (1994).

5 Except where noted, all dollar figures in the text are December 1993 dollars.

6 See the appendix for details on how the pay-off rates are calculated.

7 For the remaining 97 firms in the data set, bank- ruptcy proceedings were still under way when the data were collected.

8 For the full sample of 338 firms, the acceptance rate is 77% (259 of 338 plans).

9 Note that if all secured creditors vote against a plan, the plan does not stop, as would happen if unsecured creditors voted against it. The vote of each secured creditor really represents a decision whether to opt into the plan.

10 According to the data, the time between filing and voting is, on average, three times longer for hold- ing proposals than it is for the rest of the sample.

11 Obviously, switching all, rather than a portion, of Crown claims to ordinary status would have re- sulted in an even greater impact on the likelihood of successful reorganization. See Martel (1991) for further discussion.

12 For a theoretical analysis of the creditors' decision whether to accept a proposal see Martel (1994).

13 See Maddala (1983). Estimation was performed using Version 7.0 of SHAZAM (White, 1988).

14 In each case, we use ratios, rather than another measure of claims such as dollar values, in order to reduce the sensitivity of the estimates to ex- treme values in the sample.

15 See Gunderson, Kevin and Reid (1986) for details. 16 See Hoshi, Kashyap and Scharfstein (1990) for a

detailed discussion on the positive role of banks in mitigating information asymmetries during fi- nancial distress.

17 Other measures of wage claims - a dummy varia- ble for the presence of wage claims and the total value of wage claims - were also insignificant.

18 Given that it is costly for creditors to gather infor- mation about the financial viability of a firm (e.g., to pay for an independent audit), it may be rational for creditors not to be fully informed about the firm's financial state.

19 There are no data in the case of viable operations that are refused reorganization, because these firms are liquidated.

20 For a detailed discussion of how the data were col- lected, see Fisher and Martel (1992).

21 The filing system of the Bankruptcy Branch groups commercial proposals together with con- sumer proposals and bankruptcies. The figure 1,985 refers to the total number of files and, thus, is an upper limit on the number of commercial proposals.

22 Random sampling is carried out using the System- atic Random Sampling Procedure recommended by Statistics Canada.

23 Commercial proposals are those with more than 50% of total debts represented by business debts, which is the definition used by CCA.

24 Because reorganization may take several years, there is no guarantee that the plans were completed when the data were collected in 1990.

References

Bulow, Jeremy I. and John B. Shoven (1978) 'The Bankruptcy Decision,' Bell Journal of Economics, 9:437-56.

Canada (1985) Bankruptcy Act (Ottawa: Queen's Printer).

- (1991) 'Notes for a Statement by the Honourable Pierre Blais, M.P., P.C., Minis- ter of Consumer and Corporate Affairs Given at a Press Conference Announcing the Ta- bling of the Bankruptcy and Insolvency Act.' Speech S-10444/91-13 (Ottawa: Consumer and Corporate Affairs), June.

(1992) An Act to amend the Bankruptcy Act and to amend the Income Tax Act in con- sequence thereof (Bill C-22) (Ottawa: Queen's Printer).

Fisher, Timothy C.G. and Jocelyn Martel (1992) 'Characteristics of Canadian Firms in Finan- cial Reorganization.' Discussion Paper 92- 001. Department of Economics, Wilfrid Laurier University.

- (1994) 'Financial Reorganization in Canada,' Canadian Business Economics,

276 Timothy C.G. Fisher and Jocelyn Martel

This content downloaded from 185.44.77.82 on Sat, 14 Jun 2014 11:58:23 AMAll use subject to JSTOR Terms and Conditions

2:54-66. Gunderson, Morley, John Kervin and Frank

Reid (1986) 'Logit Estimates of Strike Inci- dence from Canadian Contract Data,' Jour- nal of Labor Economics, 4:257-76.

Hoshi, Takeo, Anil Kashyap and David Scharf- stein (1990) 'The Role of Banks in Reducing the Costs of Financial Distress in Japan,' Journal of Financial Economics, 27:67-88.

Maddala, G.S. (1983) Limited-dependent and Qualitative Variables in Econometrics (Cam- bridge: Cambridge University Press).

Martel, Jocelyn (1991) 'Bankruptcy Law and the Canadian Experience: An Economic Ap-

praisal,' Canadian Public Policy - Analyse de Politiques, XVII:1:52-63.

- (1994) 'The Behaviour of Firms and Credi- tors in Financial Reorganization.' Unpub- lished manuscript. Department of Eco- nomics and CRDE, University of Montreal, Montreal.

White, Kenneth J. (1988) 'SHAZAM: A Compre- hensive Computer Program for Regression Models (Version 6),' Computational Statis- tics and Data Analysis (August):102-4.

White, Michelle J. (1989) 'The Corporate Bank- ruptcy Decision,' Journal of Economic Per- spectives, 3:129-51.

Canadian Employment Research Forum

The Canadian Employment Research Forum (CERF) is a non-profit corporation whose objects are: (i) to improve the level of employment policy analysis and debate in Canada by encouraging policy-related empirical research; and (ii) to improve interaction among researchers and policy-makers from governments, universities, business, labour and other communities concerned with employment issues. Since its inception in 1991, CERF's main activities have been the organisation and funding of applied research, through conferences, workshops and supporting research projects of particular relevance to the policy community. Future events in planning include: * International Conference on the Impacts and Effects of Unemployment Insurance.

Citadel Inn, Ottawa, Ontario, October 14-15, 1994; * Workshop on Policy Responses to Displaced Workers, Universit6 du Qu6bec A

Montr6al, Montr6al, Qubbec, December 2-3, 1994; * Workshop on Sustainable Development and the Labour Market, University of Ottawa,

Ottawa, Ontario, April 1995; and * Workshop on Retooling the Workforce: Focus on New Brunswick, Summer/Fall 1995.

If you have further questions or would like to become more actively involved, please contact: W. Craig Riddell (Academic Co-chair) Ging Wong (Secretary) Economics Department Strategic Policy, Human Resources University of British Columbia Development Canada, 112 Kent St., 22nd Fl. Vancouver, B.C. V6T 1Z1, (604) 822-2106 Ottawa, Ontario KIA 0J9, (613) 954-7709

Will Bankruptcy Reforms Work? 277

This content downloaded from 185.44.77.82 on Sat, 14 Jun 2014 11:58:23 AMAll use subject to JSTOR Terms and Conditions