Embed Size (px)

Citation preview

Why Do Managers Avoid EPS Dilution?

Rong Huang Assistant Professor

Baruch College, CUNY

Carol Marquardt Associate Professor

Baruch College, CUNY

Bo Zhang PhD student

Baruch College, CUNY

We thank John Graham, Brian Bushee, and Jeffrey Wurgler for providing data on marginal tax rates, institutional ownership, and investor sentiment, respectively. We also thank Mary Ellen Carter, Aloke Ghosh, Armen Hovakimian, Amy Hutton, Peter Wilson, and participants at the Boston College, Lehigh University, and The Hong Kong University of Science and Technology accounting workshops and the 2008 American Accounting Association Annual Meeting for helpful comments and suggestions.

Why Do Managers Avoid EPS Dilution? ABSTRACT: Survey and empirical evidence reveals that managers prefer to avoid earnings dilution, though financial theory suggests that it is irrelevant in firm valuation. We explore contracting and behavioral explanations for this apparent paradox. Using a large sample of debt/equity issuers, we report evidence that managers only avoid earnings dilution when their bonus compensation explicitly depends upon earnings per share (EPS) performance; we further find that this effect is increasing in the magnitude of EPS-contingent bonus compensation. Our results are robust to controlling for endogeneity in compensation contract design, behavioral explanations including clientele and investor sentiment theories, and corporate governance policies. Our findings provide new evidence on the implications of the contracting role of accounting in firm decision-making. Keywords: earnings per share, dilution, executive compensation, leverage, agency theory Data Availability: Data are available from the sources described in the text.

I. INTRODUCTION

A half century of corporate finance theory suggests that earnings dilution should be

irrelevant in firm valuation (see Modigliani and Miller 1958; Brealey et al. 2007), yet survey

evidence presented by Graham and Harvey (2001) and Servaes and Tufano (2004) reveals that

CFOs regard earnings dilution as the single most important factor in determining whether to

issue equity.1 To quote Graham and Harvey (2001, p. 229):

“The popularity of this response is intriguing. It either indicates that executives focus more than they should on earnings dilution (if the standard textbook view is correct), or that the standard textbook treatment misses an important aspect of earnings dilution.” In this paper, we propose and test potential resolutions for this apparent paradox, with a

focus on a contracting explanation for managers’ preoccupation with earnings dilution. In

particular, we note that executives’ bonus compensation contracts are frequently based on

earnings per share (EPS) performance (see Morgenson 2008; Healy 1985), a situation which

creates strong incentives for executives to fixate on reported EPS. We therefore begin our

analysis by examining whether the use of EPS as performance metric in executives’ bonus

contracts helps to resolve the ‘dilution puzzle’ but also explore whether behavioral explanations,

including clientele and investor sentiment theories, might also provide a rationale for managers’

professed aversion to EPS dilution.

Our research question also extends the previous literature that has demonstrated a link

between firms’ financing activities and their financial reporting objectives related to EPS. For

example, Hand (1989) finds that smoothing reported EPS is a primary motivation behind firms’

1 “Earnings dilution” typically refers to the reduction in earnings per share (EPS) that occurs through the issuance of additional common shares or the conversion of convertible securities. We use the terms “earnings dilution” and “EPS dilution” interchangeably throughout the paper.

2

decisions to undertake debt-equity swaps; Marquardt and Wiedman (2005) document that firms

structure convertible bonds to increase diluted EPS figures; and Bens et al. (2003) and Hribar et

al. (2006) show that firms use stock repurchases to meet EPS benchmarks.2 However, to our

knowledge there is no extant research that examines how financial reporting incentives related to

EPS performance might affect what is arguably the firm’s most basic financing decision – the

choice between debt and equity.

We employ a standard two-stage model to examine firms’ debt-equity issuance decisions.

In the first stage, we estimate target leverage ratios for a large sample of firms with the necessary

Compustat, CRSP, and ExecuComp data over the period 1993-2005.3 In the second stage, which

is our main focus, we include our EPS dilution, contracting, and behavioral variables of interest

along with previously documented determinants of debt-equity choice.

To estimate EPS dilution, we follow prior research and create an indicator variable that

equals one whenever equity financing will result in greater dilution than debt financing, i.e.,

whenever the issuing firm’s E/P ratio exceeds its after-tax cost of debt. To examine the role of

compensation contracts, we hand-collect data from firms’ proxy statements filed with the

Securities and Exchange Commission (SEC) to ascertain whether EPS performance is explicitly

mentioned as a determinant of executives’ annual cash bonuses.4 If contracting incentives apply,

we expect managers’ aversion to EPS dilution to be intensified when their bonus compensation is 2 On a related note, prior research has also found that firms’ financing choices are associated with the management of balance sheet effects. For example, Imhoff and Thomas (1988) show that the choice between lease and non-lease financing depends upon balance sheet disclosure requirements; Engel et al. (1999) find that the decision to issue trust preferred stock is linked to its balance sheet classification; and Mills and Newberry (2005) find that firms’ contractual debt covenants influence their use of off-balance sheet and hybrid debt financing. 3 Our methodology is related to the two-stage analyses by Hovakimian et al. (2001); Fama and French (2002); Frank and Goyal (2003); Kayhan and Titman (2007); and Byoun (2008). 4 We obtain this information from the “Report of the Compensation Committee” within firms’ proxy statements. This report typically outlines the general compensation philosophy and provides details about the CEO’s compensation more specifically.

3

explicitly linked to EPS performance.

We provide strong empirical evidence consistent with the contracting argument. After

controlling for known determinants of debt-equity choice, we find that firms are significantly

more likely to favor debt over equity financing when debt has a relatively smaller dilutive effect

on EPS and when executives are explicitly compensated on EPS performance; i.e., managers are

more likely to avoid EPS dilution when their pay depends on reported EPS. We also find that the

likelihood of a debt issue is increasing in the interaction between EPS dilution and the magnitude

of executives’ bonus compensation for the subsample of firms that explicitly reward executives

on EPS performance; we document no such relation for the firms that do not use EPS as a

performance metric in their annual bonus contracts.

Because there is potential endogeneity with regard to firms’ compensation structure

choices, we supplement our main analysis with a Heckman (1978) estimation procedure in which

the decision to compensate executives on EPS performance is first modeled as a function of

observable firm characteristics. As there is no established model for this decision, we draw upon

prior findings in the compensation literature in developing our own. We relate the use of EPS as

a performance metric in bonus contracts to firm size, market-to-book ratios, leverage, tax rates,

the relative noise of earnings to returns, and corporate governance measures. We then include

the Inverse Mills Ratio (IMR) from this analysis as a control variable in our main analysis; our

results are robust to controlling for endogeneity in compensation structure choice.

While our evidence strongly suggests that managers’ preoccupation with EPS dilution is

linked to their annual bonus compensation, we also explore whether clientele or investor

sentiment theories might also play a role in explaining the phenomenon. We use transient

4

institutional ownership and Baker and Wurgler’s (2006) investor sentiment index as proxies for

short-term investment horizons and investors’ propensities toward speculative investments,

respectively. Although both variables are significant determinants of debt-equity choice, the

estimated coefficients on interaction terms between EPS dilution and these measures are not

significantly different from zero. We thus are unable to provide evidence that behavioral effects

explain managers’ aversion to earnings dilution, though we caution that we cannot entirely rule

out this explanation. Finally, our results are qualitatively unchanged after controlling for

managerial entrenchment and for executives’ stock and option holdings beyond those granted as

compensation in the current period.

We contribute to several streams of literature. First, we contribute to the literature linking

financial reporting incentives to firms’ financing decisions. While this literature has examined

the role of reporting incentives in firms’ decisions to undertake debt-equity swaps (Hand 1989);

contingently convertible debt issues (Marquardt and Wiedman 2005); and stock repurchases

(Bens et al. 2002; Bens et al. 2003; Hribar et al. 2006; Myers et al. 2007; Yang and Young 2009),

to our knowledge no extant research has examined the role of financial reporting in determining

the firms’ most fundamental financing decision – whether to issue debt or equity. Our paper

addresses this void in the literature.

Second, we contribute to the executive compensation literature. A long literature links

financial reporting choices to bonus compensation (e.g., Healy 1985; Holthausen et al. 1995;

Gaver and Gaver 1998), employee stock option activity (Cheng and Warfield 2005), and

executive retirement benefits (Kalyta 2009). Our evidence suggests that the use of EPS as a

performance metric in bonus compensation contracts creates an incentive for managers to avoid

5

EPS dilution, thereby significantly affecting firms’ financing choices. We thus extend this line of

research by providing new evidence on the implications of the contracting role of accounting.

Third, our results provide a plausible explanation for managers’ “puzzling” avoidance of

EPS dilution that has been documented both in survey and empirical findings within both the

accounting and corporate finance literatures. For example, Bens et al. (2003) question the

appropriateness of managers’ apparent fixation on EPS dilution documented in their work,

observing: “Executives’ myopic focus on short-term EPS in our study may sound implausible to

readers steeped in the neoclassical Arrow-Debreu framework.” This sentiment is further echoed

by both Guay (2002) and Larcker (2003), who note the absence of an equilibrium incentive

structure to support executives’ concern regarding EPS dilution. If, however, managers are

compensated on EPS, then their concerns about earnings dilution are not puzzling at all, but a

well-founded and rational consideration, given their incentives.

Lastly, our results contribute broadly to the corporate finance literature. This literature

has generally tended to on two competing models to explain firms’ financing decisions – the

traditional tradeoff model, in which firms identify optimal leverage by weighing the costs and

benefits of additional debt, and Myers’ (1984) pecking order model, in which financing decisions

are driven by internal financial deficits. However, both the tradeoff and pecking order theories

assume that shareholder wealth maximization is the corporate objective and typically ignore

agency costs that might affect capital structure decisions. Our findings suggest that explicitly

6

incorporating the agency costs related to executive compensation may be necessary if a unified

theory of corporate financial policy is to ultimately emerge.5

The remainder of this paper is organized as follows. In Section II, we discuss prior

literature and develop our hypotheses. We describe our methodology and variable construction

in Section III and our sample data in Section IV. We discuss our results in Section V and present

sensitivity tests in Section VI, and Section VII concludes.

II. PRIOR LITERATURE AND HYPOTHESIS DEVELOPMENT

EPS Dilution and Valuation

In this subsection, we briefly present a numerical example of Modigliani and Miller’s

“conservation of value” argument, adapted from Brealey et al. (2007), to illustrate the ‘standard

textbook view’ on EPS dilution and firm valuation. Suppose a company has no leverage and all

the operating income is paid as dividends to the common shareholders. Expected operating

income is $1,500, and there are 1,000 shares outstanding each with a market price of $10.00 per

share; expected EPS is thus $1.50. The expected return on the share is equal to the earnings-

price ratio, 1.50/10.00 = 0.15, or 15%.

The company’s president wonders if shareholders would be better off if the company had

equal proportions of debt and equity and proposes issuing $5,000 of debt (at an annual rate of

interest of 10%) and repurchasing 500 shares. Expected EPS under the new scenario is expected

operating income of $1,000 ($1,500 less $500 of interest expense) divided by 500 shares

outstanding, or $2.00, and the expected return on the share is now 20%. It would now appear

5 Fama and French (2005) and Barclay and Smith (2005) have both expressed a need for a unified framework of capital structure.

7

that the firm is better off issuing debt.

However, shareholders have the alternative of borrowing on their own account. For

example, suppose an investor borrows $10 and invests $20 in two unlevered shares. The payoff

on this investment is $2.00 ($3.00 in earnings, less $1.00 in interest charges on the $10 that is

borrowed), yielding exactly the same expected return of 20% as the investor would get by buying

one share in levered company. Therefore, a share in the levered company must also sell for $10.

Leverage increases expected EPS but does not affect the share price, and EPS dilution related to

the choice between debt and equity financing is irrelevant in firm valuation.6

Hypothesis Development

Despite the supposed lack of a theoretical link between EPS dilution and firm value,

survey and empirical evidence show that EPS dilution does affect financing decisions. Graham

and Harvey (2001) report that EPS dilution is the single most important factor affecting CFOs’

decisions to issue equity, with over two-thirds of CFOs citing it as a “very important” or

“important” factor in their decision. Hovakimian et al. (2001) empirically find that firms are less

likely to choose equity over debt financing when an equity issue will dilute EPS, noting that

compensation policies might explain the result.

We explore the compensation contracting argument more fully. Jensen and Meckling

(1976) articulated the implications of the agency problem between a firm’s shareholders and its

managers, which arises due to the imperfect observability of managerial effort and costly

contracting. Watts and Zimmerman (1986) further theorized that contracting considerations

6 This example may be generalized to incorporate the effects of taxes. See Miller (1977).

8

affect managers’ accounting choices in the presence of agency costs and information asymmetry,

and a large empirical literature suggests that the determination of accounting income and

selection of accounting methods are affected by compensation contracts (e.g., Healy 1985;

Holthausen et al. 1995; Cheng and Warfield 2005; Bergstresser and Philippon 2006; Kalyta

2009).

We extend this line of inquiry by considering the effect of compensation contracts that

explicitly link executives’ annual cash bonuses to EPS performance. When compensation is

contingent upon EPS performance, managers have an incentive to influence their pay not only

through the operating and reporting decisions that affect net income, but also through financing

decisions that affect the number of shares outstanding used in EPS calculations, and previous

literature documents that financing decisions to undertake debt-equity swaps (Hand 1989),

contingently convertible debt issuances (Marquardt and Wiedman 2005), and stock repurchases

(Bens et al. 2002; Bens et al. 2003; Hribar et al. 2006; Myers et al. 2007; Yang and Young 2009)

are influenced by EPS reporting incentives. Because the choice between debt and equity

financing differentially impacts reported EPS, managers who are rewarded explicitly on EPS

performance may be motivated by self-interest in making this decision. This leads to our first

hypothesis:

H1: Managers are more likely to avoid EPS dilution related to debt-versus-equity issues when their bonus compensation is explicitly linked to EPS performance.

We also explore whether the magnitude of EPS-based compensation affects managers’

financing decisions. We predict a positive association between the amount of bonus

compensation and managerial preferences for higher levels of reported EPS when bonus

9

contracts are explicitly linked to EPS performance. Stated formally, our second hypothesis is as

follows:

H2: Managers’ aversion to EPS dilution is increasing in the magnitude of bonus compensation explicitly linked to EPS performance.

Evidence consistent with H1 and H2 provides one rational explanation for managers’

previously documented aversion to EPS dilution. However, it does not necessarily imply that

managers’ financing decisions are suboptimal. Prior research shows that incentive compensation

is often used to induce managers to take on greater levels of debt because managers often tend to

under-leverage to reduce firm risk and protect their under-diversified human capital (Fama

1980). Mehran (1992) finds that firms’ leverage ratios are positively associated with the

percentage of executives’ total compensation in incentive plans, and Berger et al. (1997) report

lower leverage levels in firms where executive compensation plans are less sensitive to

performance. Evidence relating compensation contracting to managerial aversion to EPS

dilution would be consistent with the predictions of agency theory.

We also note that in developing our hypotheses above we assume that compensation

policies are exogenous. However, Smith and Watts (1992) and Skinner (1993) argue that the use

of accounting information in compensation and debt contracts should be viewed as endogenously

determined. Therefore, in our empirical tests, we allow for endogeneity in compensation

structure by using a two-stage Heckman model to control for firms’ decisions to use EPS as a

performance metric in their annual bonus contracts when choosing between debt and equity

financing.

10

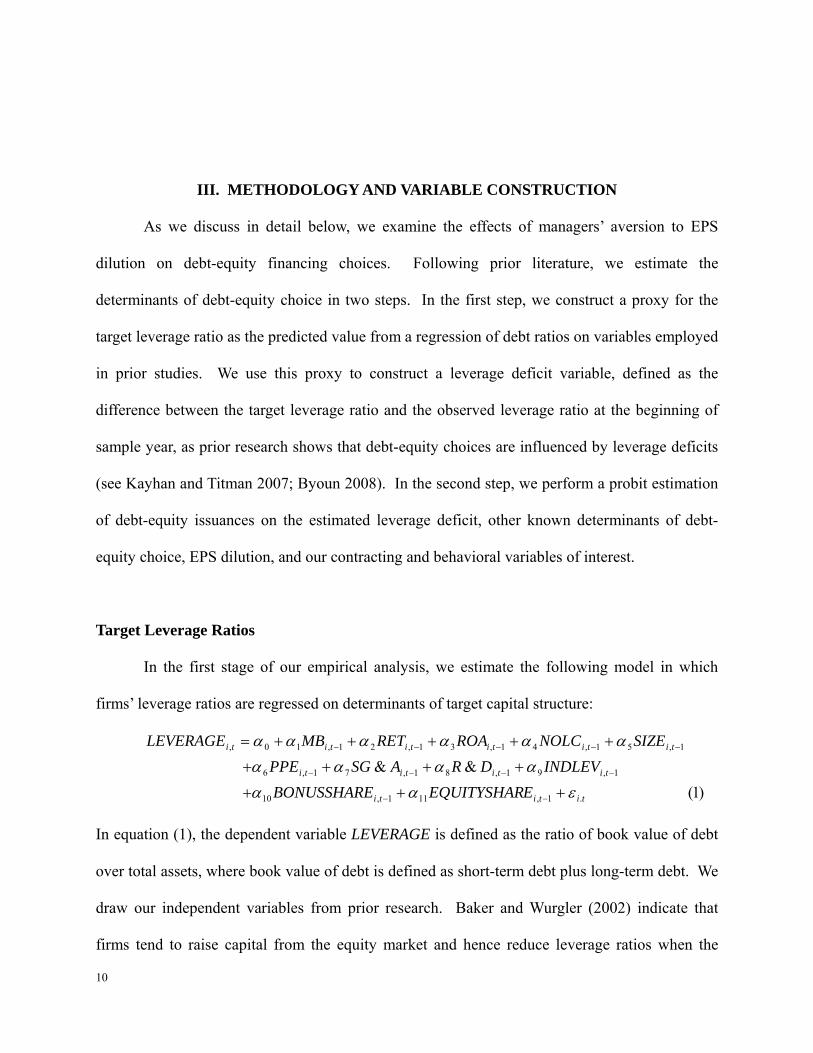

III. METHODOLOGY AND VARIABLE CONSTRUCTION

As we discuss in detail below, we examine the effects of managers’ aversion to EPS

dilution on debt-equity financing choices. Following prior literature, we estimate the

determinants of debt-equity choice in two steps. In the first step, we construct a proxy for the

target leverage ratio as the predicted value from a regression of debt ratios on variables employed

in prior studies. We use this proxy to construct a leverage deficit variable, defined as the

difference between the target leverage ratio and the observed leverage ratio at the beginning of

sample year, as prior research shows that debt-equity choices are influenced by leverage deficits

(see Kayhan and Titman 2007; Byoun 2008). In the second step, we perform a probit estimation

of debt-equity issuances on the estimated leverage deficit, other known determinants of debt-

equity choice, EPS dilution, and our contracting and behavioral variables of interest.

Target Leverage Ratios

In the first stage of our empirical analysis, we estimate the following model in which

firms’ leverage ratios are regressed on determinants of target capital structure:

)1(&&

.1,111,10

1,91,81,71,6

1,51,41,31,21,10,

tititi

titititi

titititititi

EEQUITYSHARBONUSSHAREINDLEVDRASGPPE

SIZENOLCROARETMBLEVERAGE

εαααααα

αααααα

+++

++++

+++++=

−−

−−−−

−−−−−

In equation (1), the dependent variable LEVERAGE is defined as the ratio of book value of debt

over total assets, where book value of debt is defined as short-term debt plus long-term debt. We

draw our independent variables from prior research. Baker and Wurgler (2002) indicate that

firms tend to raise capital from the equity market and hence reduce leverage ratios when the

11

equity market is perceived to be more favorable, i.e., when the market-to-book ratio is high.

Following Baker and Wurgler (2002), we use the market-to-book ratio (MB) to capture this

market timing effect, where MB is defined as (total assets – book value of equity + market value

of equity) / total assets. Welch (2004) shows that leverage ratios are negatively related to past

stock returns, consistent with the notion that firms tend to issue equity following stock price

increases. We use stock return (RET) to capture this effect, where RET is defined as the split-

and dividend-adjusted raw return over the previous two fiscal years. We control for past

profitability using average return on assets for the previous three fiscal years (ROA) and for tax

benefits using net operating loss carryforwards (NOLC). Firms with better past profitability tend

to have lower debt ratios (Titman and Wessels 1988) because profitable firms are able to pay off

debt, and firms with NOLCs are able to better utilize the tax shield that debt financing provides.

We control for SIZE to capture the fact that small firms are more likely to become financially

distressed as they tend to have more volatile cash flows (Rajan and Zingales 1995). We define

SIZE as the log of net sales. We also include PPE (net property, plant, and equipment scaled by

total assets) to control for tangible assets. Titman and Wessels (1988) show that firms with large

amounts of tangible assets tend to have high target leverage ratios because their bankruptcy costs

are low. In contrast, firms with high intangible assets and unique products (high R&D expenses

and high selling expenses) tend to have low leverage ratios because their bankruptcy costs are

high (Titman 1984). We use R&D deflated by sales and SG&A costs deflated by sales to capture

the level of intangible assets and unique products. We include the industry median debt ratio

(INDLEV) to mitigate potential omitted variable problems, where the industry median leverage

ratio is calculated for firms within the same 3-digit SIC code for the same fiscal year

12

(Hovakimian et al. 2001).

We also include incentive compensation variables, as both Mehran (1992) and Berger et

al. (1997) find that incentive compensation tends to increase observed leverage ratios.7

However, in contrast to prior work, we separate incentive compensation into its bonus and equity

components. We expect bonus compensation, which is significantly more sensitive to EPS

performance than is equity-based incentive compensation (Core et al. 2003), to be more

positively associated with leverage ratios if managers are concerned with EPS dilution. We

define BONUSSHARE as the average ratio of annual cash bonus over shareholders’ equity for the

top five executives and EQUITYSHARE as the average ratio of the value of new grants of stock

options and restricted stocks over shareholders’ equity for the top five executives.

Since leverage ratios fall between zero and one, OLS estimation of equation (1) is likely

to produce biased estimates (e.g., Greene 2000, pp. 927-933; Maddala 2001, pp. 333-336).

Therefore, we estimate equation (1) using a Tobit model with fixed year effects, where the

predicted value of the leverage ratio is restricted to be between zero and one (Hovakimian et al.

2001; Kayhan and Titman 2007). The predicted value from the Tobit estimation is the estimated

target leverage ratio.

Debt-Versus-Equity Issuances

We use the following probit model to investigate whether earnings dilution and EPS-

based bonus contract affects the debt-versus-equity choice.

7 Our results are robust to whether incentive compensation is included in the target leverage ratio estimation.

13

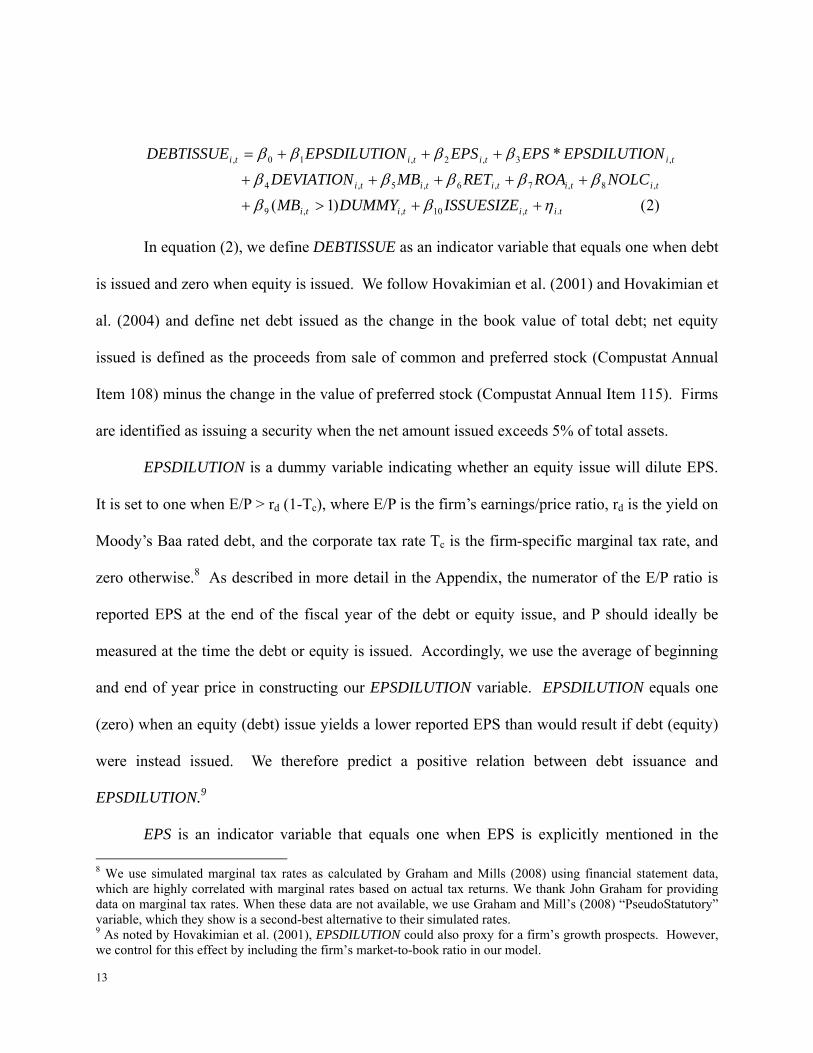

)2()1(

*

.,10,,9

,8,7,6,5,4

,3,2,10,

titititi

tititititi

titititi

ISSUESIZEDUMMYMBNOLCROARETMBDEVIATION

NEPSDILUTIOEPSEPSNEPSDILUTIODEBTISSUE

ηβββββββ

ββββ

++>+

+++++

+++=

In equation (2), we define DEBTISSUE as an indicator variable that equals one when debt

is issued and zero when equity is issued. We follow Hovakimian et al. (2001) and Hovakimian et

al. (2004) and define net debt issued as the change in the book value of total debt; net equity

issued is defined as the proceeds from sale of common and preferred stock (Compustat Annual

Item 108) minus the change in the value of preferred stock (Compustat Annual Item 115). Firms

are identified as issuing a security when the net amount issued exceeds 5% of total assets.

EPSDILUTION is a dummy variable indicating whether an equity issue will dilute EPS.

It is set to one when E/P > rd (1-Tc), where E/P is the firm’s earnings/price ratio, rd is the yield on

Moody’s Baa rated debt, and the corporate tax rate Tc is the firm-specific marginal tax rate, and

zero otherwise.8 As described in more detail in the Appendix, the numerator of the E/P ratio is

reported EPS at the end of the fiscal year of the debt or equity issue, and P should ideally be

measured at the time the debt or equity is issued. Accordingly, we use the average of beginning

and end of year price in constructing our EPSDILUTION variable. EPSDILUTION equals one

(zero) when an equity (debt) issue yields a lower reported EPS than would result if debt (equity)

were instead issued. We therefore predict a positive relation between debt issuance and

EPSDILUTION.9

EPS is an indicator variable that equals one when EPS is explicitly mentioned in the 8 We use simulated marginal tax rates as calculated by Graham and Mills (2008) using financial statement data, which are highly correlated with marginal rates based on actual tax returns. We thank John Graham for providing data on marginal tax rates. When these data are not available, we use Graham and Mill’s (2008) “PseudoStatutory” variable, which they show is a second-best alternative to their simulated rates. 9 As noted by Hovakimian et al. (2001), EPSDILUTION could also proxy for a firm’s growth prospects. However, we control for this effect by including the firm’s market-to-book ratio in our model.

14

firm’s proxy statement as a determinant of executives’ annual bonus compensation, and zero

otherwise. We expect a positive relation between debt issuance and EPS, as managers with EPS-

based bonus schemes are likely to prefer debt over equity financing, on average, because debt

financing generally results in higher reported EPS (see Modigliani and Miller 1958; Brealey et

al. 2007).

Our main variable of interest is EPS*EPSDILUTION, which is the interaction term

between EPS and EPSDILUTION. A positive estimated coefficient on this variable would

indicate that managers are more likely to be concerned with EPS dilution related to debt/equity

issuances when their compensation depends upon reported EPS, consistent with H1.

We also include additional control variables that affect debt-equity financing decisions.

Trade-off theory suggests that firms choose the form of financing to offset deviations from their

target leverage ratios (Fama and French 2002; Kayhan and Titman 2007). We therefore include

the DEVIATION from target leverage, defined as the difference between the observed leverage

ratio and the predicted ratio from equation (1), as a control variable; we expect a negative

relation between DEVIATION and DEBTISSUE. Following Hovakimian et al. (2001), we also

include the market-to-book ratio (MB), raw stock returns (RET), return on assets (ROA), and net

operating loss carryforwards (NOLC) in the model, along with an indicator variable,

(MB>1)DUMMY that is set to one if the market-to-book ratio exceeds one and zero otherwise,

and ISSUESIZE. The (MB>1)DUMMY variable indicates whether an equity issue will dilute the

firm’s book value per share, and issue size equals the sum of the net debt and net equity issued.

We use a probit regression to estimate equation (2) since the dependent variable is binary.

To test whether managers’ aversion to EPS dilution is increasing in the magnitude of their

15

EPS-related bonus compensation (H2), we use the following probit model, which is estimated:

)3()1(

**

.,12

,,11,10,9,8

,7,6,,5

,,4,3

,2,10,

titi

tititititi

titititi

tititi

tititi

ISSUESIZEDUMMYMBNOLCROARET

MBDEVIATIONNEPSDILUTIOEEQUITYSHARNEPSDILUTIOBONUSSHARENEPSDILUTIO

EEQUITYSHARBONUSSHAREDEBTISSUE

ηβββββ

βββββ

βββ

++

>++++

+++

++

++=

To simplify the interpretation of interaction effects, we estimate equation (3) separately

for firms that reward executives explicitly on EPS performance versus those that do not. We

incorporate the magnitude of incentive compensation by including both BONUSSHARE and

EQUITYSHARE as potential determinants of the debt-equity choice. We expect both

BONUSSHARE and EQUITYSHARE to be positively related to DEBTISSUE, as prior research

has shown that incentive compensation induces managers to take on greater debt levels.

However, if executives’ concerns about EPS dilution are related to compensation structure, we

expect that a dollar of bonus compensation will be more positively associated with the likelihood

of a debt issuance than will an equal amount of equity compensation. In addition, as in equation

(2), we expect EPSDILUTION to be positively associated with DEBTISSUE.

Our main variables of interest are the interaction terms, BONUSSHARE*EPSDILUTION

and EQUITYSHARE*EPSDILUTION. Consistent with H2, we expect the interaction between

BONUSSHARE and EPSDILUTION to be positively associated with DEBTISSUE for the

subsample of firms that reward executives on EPS performance, but have no such expectation for

the subsample that does not. Furthermore, we do not expect the interaction between

EQUITYSHARE and EPSDILUTION to be a significant determinant of DEBTISSUE in either

group of firms, as reported EPS should not play a strong role in determining equity-based

16

incentive compensation (Core et al. 2003).

Controlling for Endogeneity in Compensation Structure

The above analysis assumes that firms’ decisions to explicitly condition annual bonus

compensation on EPS performance is exogenous. However, as observed by Smith and Watts

(1992) and Skinner (1993), it is possible that compensation structure and financing policies are

jointly determined. We address this potential endogeneity issue using a two-stage Heckman

(1978) model. In the first stage, we model the firm’s decision to explicitly reward executives on

EPS performance, relying on prior finding in the compensation literature in choosing our

dependent variables. Our model is as follows:

)4(.1,6

1,51,41,31,21,10,

titi

titititititi

ENTRENCHEDTAXRATELEVNOISEMBSIZEEPS

ξγγγγγγγ

++

+++++=

−

−−−−−

EPS is an indicator variable equal to one for firms with bonus compensation contracts

that are explicitly based on EPS, and zero otherwise. We include firm size (SIZE), as defined

earlier; we expect a positive coefficient on SIZE because large firms are more likely to use

compensation contracts that are sensitive to earnings performance (Kole 1997). We use market-

to-book (MB) ratio to control for investment opportunities and predict a negative coefficient on

MB, as firms with high investment opportunities tend to rely less on accounting-based

performance and more on market-based performance (Smith and Watts 1992). NOISE is the

ratio of time-series variance of ΔEPS to time-series variance of stock returns over our sample

period. We predict a negative relation between EPS and NOISE as firms with relatively more

noise in earnings tend to use less earnings-based compensation (Bryan et al. 2000). We control

17

for the existing level of leverage and expect a positive coefficient on LEV as highly leveraged

firms may provide more earnings-based cash incentives to avoid earnings-related debt covenant

violation (Watts and Zimmerman 1986). TAXRATE represents estimated marginal tax rates as

calculated by Graham and Mills (2008) using financial statement data. We expect a positive

coefficient on TAXRATE as firms with high tax rates tend to rely more on performance-based

cash compensation in order to preserve the tax deductibility of their executives’ bonus

compensation under Internal Revenue Code Section 162(m) (see Bryan et al. 2000).10 Finally,

following Davila and Penalva (2006), we include a corporate governance measure that captures

managerial entrenchment, ENTRENCHED, which is a weighted index of the following four

variables: anti-takeover protection; the proportion of executives that serve on the board of

directors; an indicator variable that equals one if the CEO is also the chairman of the board; and

the number of board meetings. We predict a positive coefficient on ENTRENCHED, as Davila

and Penalva (2006) find that entrenched managers tend to negotiate compensation contracts that

depend more on accounting-based rather than market-based performance. We obtain the inverse

Mills ratio from estimating equation (4) and add it as an additional dependent variable in both

equations (2) and (3). A significant coefficient on the inverse Mills ratio indicates the presence

of endogeneity.

IV. SAMPLE AND DATA

We obtain financial data from Compustat 2007, stock price information from CRSP 2007,

10 Under Internal Revenue Code Section 162(m), cash bonuses in excess of one million dollars are only deductible for tax purposes if the bonus is based on the achievement of financial performance goals that have been put in place by the firm’s compensation committee and approved by shareholder vote.

18

and compensation data from ExecuComp 2007. We exclude firms in financial industries (SIC

codes 6000—6999) since their financial reporting and capital structure are likely to be very

different from those of other firms (Hovakimian et al. 2004; Kayhan and Titman 2007).11 We

restrict our sample to firm-years with total assets above $10 million. Because ExecuComp is

available from 1992 and we require one-year lagged data for some our variables, we restrict our

sample from 1993 to 2005. The final sample contains 5,980 firm-year observations from 1993 to

2005.

We track debt issuances from the change in total debt reported in Compustat. Equity

issuances are identified from the statement of change in cash flows reported in Compustat. After

merging with our sample containing nonmissing financial variables, stock return variables, and

executive compensation variables, we obtain a sample of 2,397 firm-years with security (debt or

equity) issuances.

To identify firms with bonus compensation contracts that are explicitly based on EPS, we

access the proxy statements of the 2,397 firm-years with security issuances via SEC Edgar and

search for the description of bonus compensation contracts. We collect a sample of 614 firm-

years whose bonus contracts are explicitly based on EPS. Another sample of 1,188 firm-years

did not mention EPS in their description of their annual bonus plans in proxy statements filed

with the SEC. The remaining 595 firm-years either did not file a proxy statement or did not

report a bonus plan in their proxy statements. We thus use a total of 1,802 (614 plus 1,188) firm-

years in our examination of debt/equity issuances.

11 Graham and Harvey (2001) note that avoiding EPS dilution seems to be particularly important to CFOs working in regulated industries. We omit financial institutions to ensure consistency with prior research; however, we may be reducing the power of our tests if these firms are more likely than other firms to reward executives on EPS performance.

19

V. RESULTS

Target Leverage Ratios

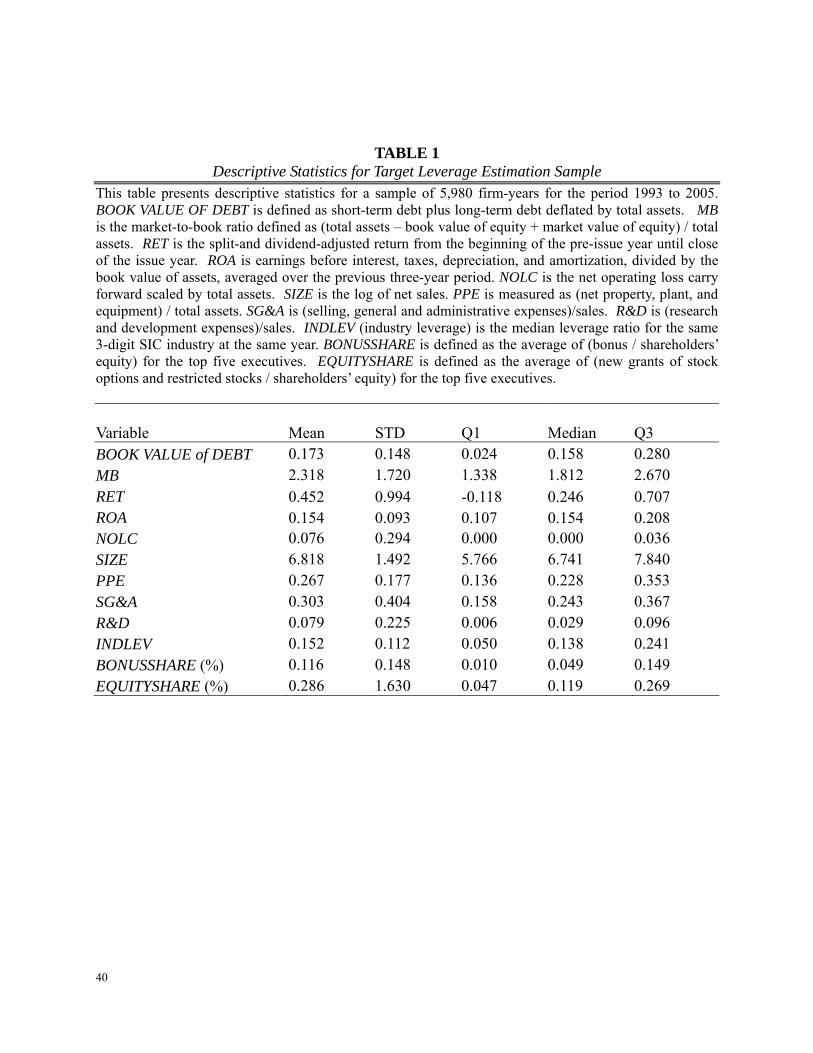

In Table 1, we provide descriptive statistics on firm characteristics of the initial sample

used to estimate target leverage ratios. BOOK VALUE of DEBT is book value of long-term and

short-term debt, deflated by total assets. The mean (median) leverage ratio is 17.3% (15.8%),

which is slightly lower than figures reported by Byoun (2008), who reports mean (median) ratios

of 0.2051 (0.1782) in 1993 and 0.1834 (0.1741) in 2003. The mean (median) values of 2.318

(1.812) for MB, 0.452 (0.246) for RET, and 0.154 (0.154) for ROA indicate that most firms in

this sample are profitable and financially healthy, consistent with their inclusion in the

ExecuComp database. In addition, the statistics for NOLC, SIZE, PPE, SG&A, and R&D

indicate that our sample firms have few tax loss carryforwards, high sales levels, and are

relatively asset-intensive. They are also more highly levered that the average firm in their

industry, as indicated by mean (median) values of INDLEV of 0.152 and 0.138. The mean

(median) value of bonus compensation as a percentage of shareholders’ equity is 0.116%

(0.049%) per executive, while the mean (median) value of equity compensation as a percentage

of shareholders’ equity is 0.286% (0.119%) per executive.12

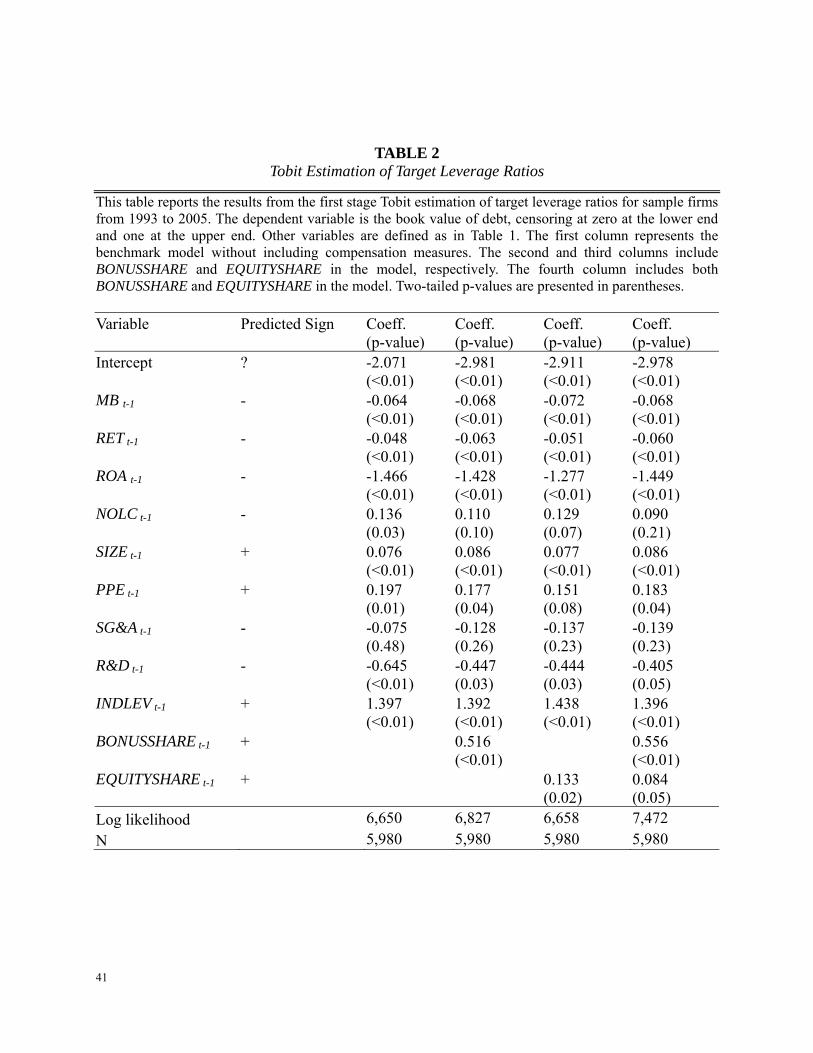

Table 2 reports the results from the first stage Tobit estimation of target leverage ratios.

The first column presents the benchmark model without including compensation measures to

provide a comparison with prior studies (Hovakimian et al. 2004). Consistent with prior 12 Prior literature has noted that bonus compensation frequently represents a smaller proportion of total compensation than does equity compensation (Hall and Liebman 1998; Murphy 1999) and questioned its ability to create incentive benefits (Bushman and Smith 2001). Hoppe and Moers (2008) argue that corporate boards use bonus contracts to communicate how performance will be evaluated and thus signal the measures relevant in CEO termination decisions; they also present empirical evidence consistent with their argument.

20

research, we generally find that the determinants are associated with leverage ratios in the

predicted fashion. MB, RET, ROA, SG&A, and R&D are negatively related to leverage ratios,

while SIZE, PPE, and INDLEV are positively related to leverage ratios.13 These results suggest

that our sample is comparable to the samples used in prior studies, and all the documented

determinants in our sample generally behave in the predicted fashion.

The second and third columns include BONUSSHARE and EQUITYSHARE in the

regression, respectively. The estimated coefficient of 0.516 on BONUSSHARE is significantly

positive with a two-tailed p-value of less than 0.01. Similarly, the coefficient of 0.133 on

EQUITYSHARE is also significantly positive (p-value = 0.02), albeit much smaller in magnitude.

When both BONUSSHARE and EQUITYSHARE are included in the model, the estimated

coefficients are both still highly significant. These results are consistent with the prediction that

both bonus and equity compensation are positively associated with target leverage ratios. We

also perform an F-test (not tabulated) to determine whether the estimated coefficient on

BONUSSHARE is significantly larger than the coefficient on EQUITYSHARE; the F-statistic of

116.88 is highly significant (p-value < 0.001). In addition, we find that all the control variables

have the predicted signs, though SG&A and NOLC fail to reach conventional levels of

significance.

While we do not rely on the results from Table 1 as formal tests of H1 and H2, the results

are nonetheless consistent with our hypotheses. We find that a dollar of bonus compensation has

a significantly greater impact on leverage ratios than does a dollar of equity compensation.

13 Although NOLC is predicted to be negatively associated with target leverage, we find a positive relation, consistent with Hovakimian et al. (2001), who note that a positive relation may reflect the fact that firms with accumulated losses in the past tend to be over-levered relative to their targets.

21

Bonus compensation may be more effective in raising leverage ratios than equity compensation

because it is more sensitive to EPS performance than equity compensation and because debt

financing typically results in higher reported EPS levels than would result from equity financing;

hence, managers tend to choose debt over equity when bonus compensation is larger.14 We

proceed, however, with more formal hypothesis tests in the following section.

Debt-Versus-Equity Issuances

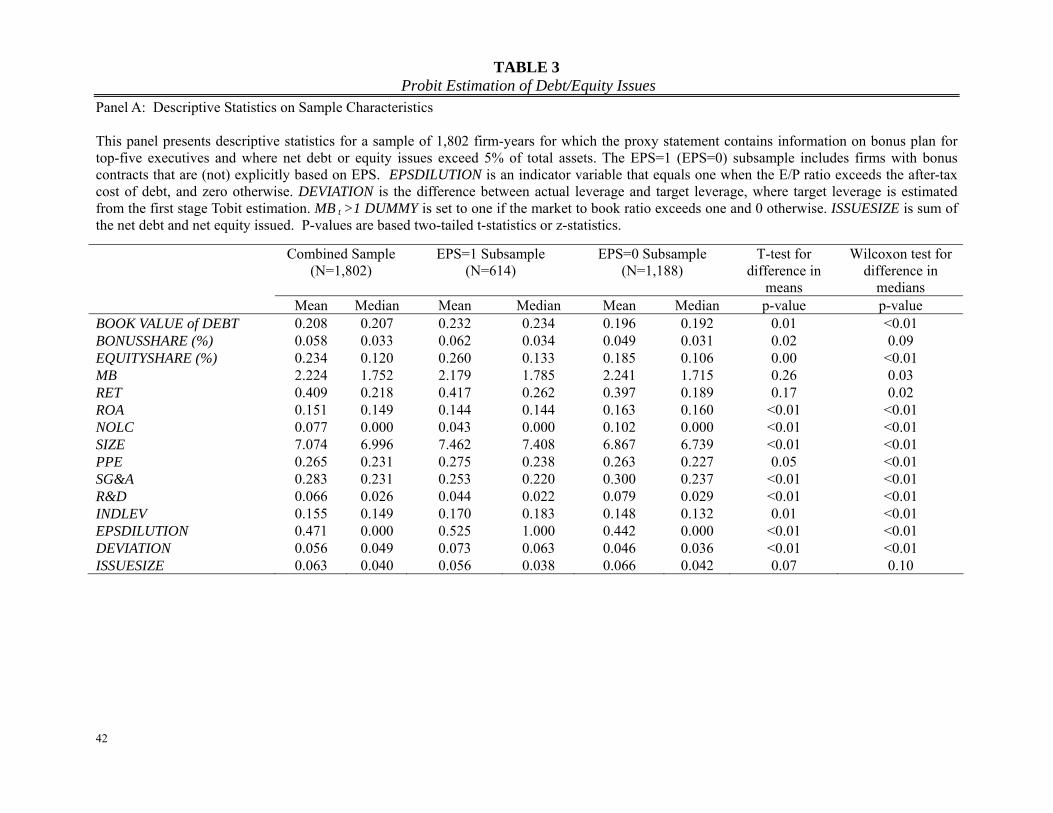

Panel A of Table 3 presents descriptive statistics for the sample of debt and equity issuers.

We present statistics for the combined sample, as well as for the two subsamples that are

conditioned on whether EPS is used as an explicit performance metric in firms’ bonus plans.

Firms that reward executives explicitly on EPS performance (EPS=1) are significantly more

levered than firms that do not (EPS=0): mean (median) book leverage is 0.232 (0.234) for the

EPS=1 subsample versus 0.196 (0.192) for the EPS=0 group. The EPS=1 firms also use more

incentive compensation. Both BONUSSHARE and EQUITYSHARE are significantly larger for

firms that reward EPS performance, with BONUSSHARE means (medians) of 0.062 (0.034) and

0.049 (0.031) and EQUITYSHARE means (medians) of 0.260 (0.133) and 0.185 (0.106) for the

EPS=1 and EPS=0 groups, respectively.

In addition, the EPS=1 firms are relatively larger than the EPS=0 firms (mean SIZE of

7.462 versus 6.867, p<0.01), have fewer tax loss carryforwards (mean NOLC of 0.043 versus

0.102, p<0.01), more fixed assets (mean PPE of 0.275 versus 0.263, p=0.05), and smaller SG&A 14 It is also possible that the estimated coefficient on BONUSSHARE is higher than that of EQUITYSHARE in Table 1 because the use of equity-based incentive compensation (especially nonqualified incentive stock options) can reduce marginal tax rates and the desirability of debt financing (Graham et al. 2004). We discuss this possibility in more detail in section VI.

22

and R&D expenses (means of 0.253 versus 0.300 and 0.044 versus 0.079, respectively, both

p<0.01), and are in more highly-levered industries (mean INDLEV of 0.170 versus 0.143,

p<0.01). Equity issues are also more likely to dilute EPS in the EPS=1 subsample: mean

EPSDILUTION is 0.525 for this group versus 0.442 (p<0.01) for the EPS=0 firms. The EPS=1

subsample is also more over-levered relative to their target debt ratios: mean DEVIATION is

0.073 versus 0.046 for the EPS=0 subsample (p<0.01)

Panel B of Table 3 presents the estimation results from our probit estimation models of

debt vs. equity issuances. The leftmost column presents results from estimating equation (2) for

the combined sample. The estimated coefficient of 0.256 on EPS is positive and significant (p-

value < 0.01). This finding is consistent with our expectation that managers with EPS-based

bonus plans are more likely to issue debt than equity. The estimated coefficient on

EPSDILUTION is also positive and significant (p-value <0.01), consistent with Graham and

Harvey’s (2001) survey evidence revealing that CFOs regard EPS dilution as a key factor in

determining whether to issue equity. More importantly, we find that the interaction term

EPS*EPSDILUTION has a positive coefficient of 0.159 (p-value<0.01). This finding confirms

our prediction that managers are more likely to issue debt when their bonuses are based on EPS

and when earnings will be diluted with an equity issue, consistent with H1.

We also find that, as expected, the estimated coefficient on DEVIATION is negative and

significant (p-value < 0.01), which supports the trade-off theory that firms choose the form of

financing to offset deviations from their target leverage ratios. In addition, MB, RET, ROA and

ISSUESIZE are significantly negatively related to the likelihood of debt issues.

We next investigate whether managers’ aversion to EPS dilution is increasing with the

23

magnitude of bonus compensation. The middle columns present results from the estimation of

equation (3) for the subsample where bonuses are explicitly based on EPS performance.

Consistent with our expectations, the estimated coefficients on BONUSSHARE and

EQUITYSHARE of 0.159 and 0.123, respectively, are significantly positive, indicating that

incentive compensation induces managers to choose debt over equity financing, consistent with

previous findings. EPSDILUTION continues to be positively related to the likelihood of a debt

issue, as expected, with an estimated coefficient 0.672.

Our main variables of interest, however, are BONUSSHARE*EPSDILUTION and

EQUITYSHARE*EPSDILUTION. The estimated coefficient of 0.476 on

BONUSSHARE*EPSDILUTION is positive and significant (p-value=0.02), consistent with H2.

Furthermore, the estimated coefficient of 0.122 on EQUITYSHARE*EPSDILUTION is not

significantly different from zero (p = 0.53). These results provide support for the argument that

the concern over EPS dilution in debt/equity financing decisions is related to compensation

contracting.

Finally, in the rightmost columns, we present results for the subsample where EPS is not

an explicit determinant of executives’ bonus compensation. Here we find that EQUITYSHARE is

significantly positively associated with the likelihood of a debt issue, but BONUSSHARE is not.

In addition, as expected, neither BONUSSHARE*EPSDILUTION nor

EQUITYSHARE*EPSDILUTION is a significant determinant of financing choices for firms that

do not explicitly reward executives on EPS performance. Finally, the estimated coefficient on

the EPSDILUTION variable is not significantly different from zero (0.138, p-value=0.23). It

appears that the ‘dilution puzzle’ presented by Graham and Harvey (2001) only applies to firms

24

that explicitly reward their managers on EPS performance, consistent with agency theory.

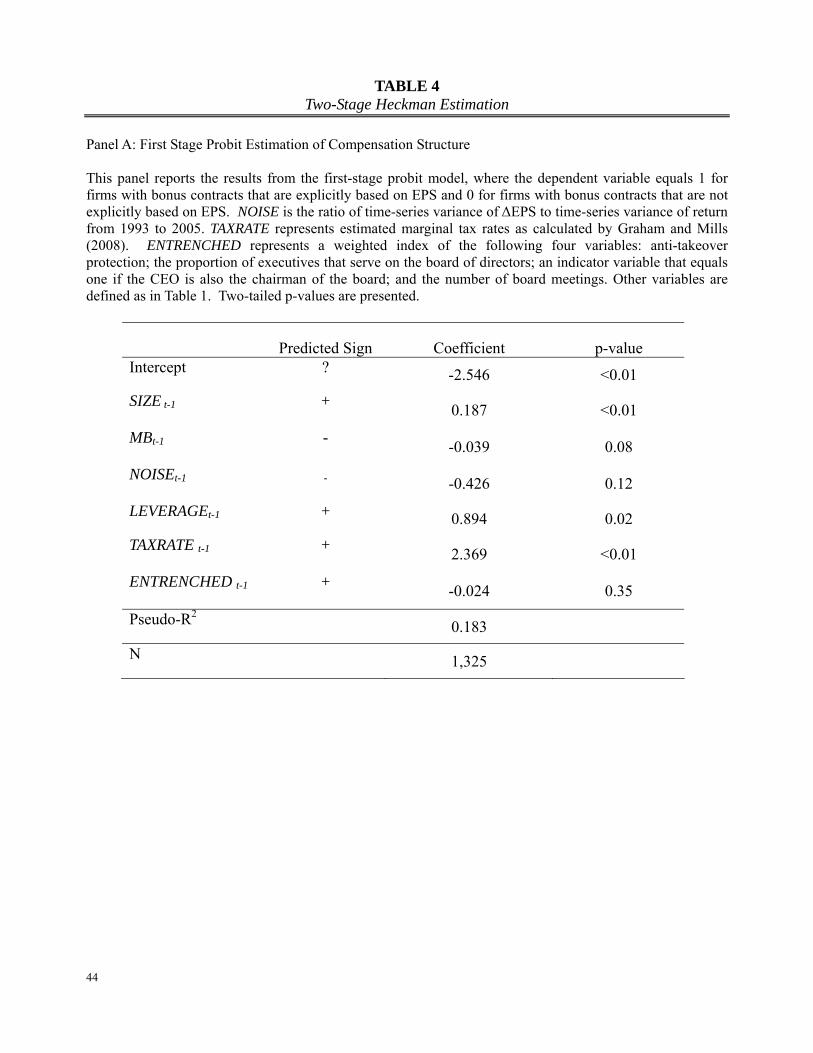

Controlling for Endogeneity in Compensation Structure

Our analysis thus far assumes that compensation structure is exogenously determined. In

this subsection, we present results of a two-stage Heckman (1978) model that controls for

endogeneity in compensation contract design.15 We present the results of the first stage

estimation of equation (4), a probit model of the decision to base executive annual bonuses on

EPS performance, in panel A of Table 4. Consistent with our expectations, we find that the

coefficient of 0.187 on SIZE is positive and significant (p-value = 0.01), suggesting that large

firms are more likely to use EPS-based bonus compensation. We use the market-to-book ratio

(MB) to control for investment opportunities. MB is marginally negatively associated with the

probability of EPS-based bonus scheme, indicating that firms with high investment opportunities

use less accounting-based performance measures in their compensation contracts, as accounting

performance tend to be noisy for these firms. In addition, we find that, as expected, firms with

high leverage and high tax rates provide more EPS-based cash incentives. Finally, the

coefficients on NOISE and ENTRENCHED are negative but insignificant.

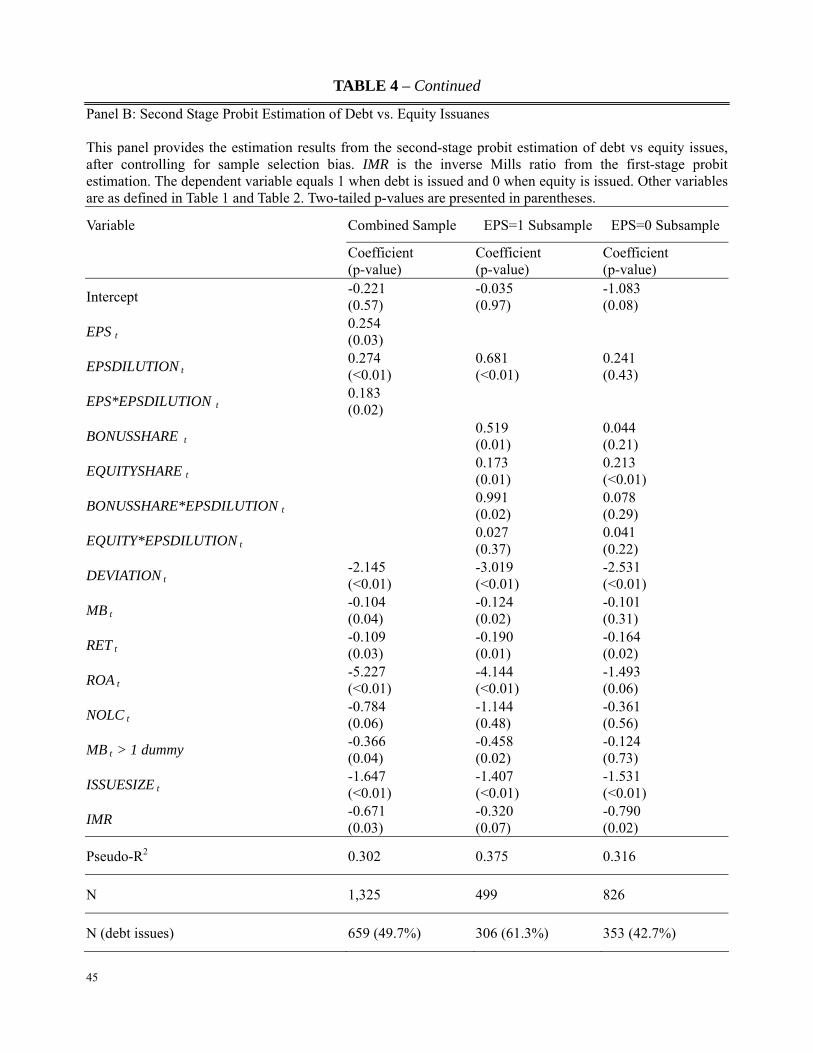

In the second stage, we perform a probit estimation of the decision to issue debt by

adding the inverse Mills ratio as an additional explanatory variable. The leftmost column of

panel B shows that after controlling for endogeneity in compensation structure, the coefficients

on EPS*EPSDILUTION, EPS and EPSDILUTION are still positive and significant. This finding

confirms our prediction that managers with EPS-based bonus schemes are more likely to issue

15 Note that the sample size in Table 4 drops to 1,325 observations, as we require corporate governance data to estimate equation (4).

25

debt when an equity issue will dilute EPS. Note that the estimated coefficient on the inverse

Mills ratio of -0.671 is negative and significant, indicating that there is evidence of endogeneity

between compensation structure and financing choices, consistent with Smith and Watts (1992)

and Skinner (1993).

The middle and rightmost columns report results of the second-stage probit model for the

EPS=1 and EPS=0 subsamples, respectively. As before, we find that debt issuance is positively

associated with EPSDILUTION, BONUSSHARE, and BONUSSHARE * EPSDILUTION only in

the subsample where bonus is based on EPS performance. For the subsample where bonus is not

based on EPS, these three variables are not significant determinants of debt/equity choice,

although EQUITYSHARE remains a significant determinant for this group. In addition, the

estimated coefficients on IMR are negative and significant for both subsamples, providing

evidence of endogeneity between compensation structure and financing choices. However, our

results are robust to this concern.

VI. SENSITIVITY TESTS

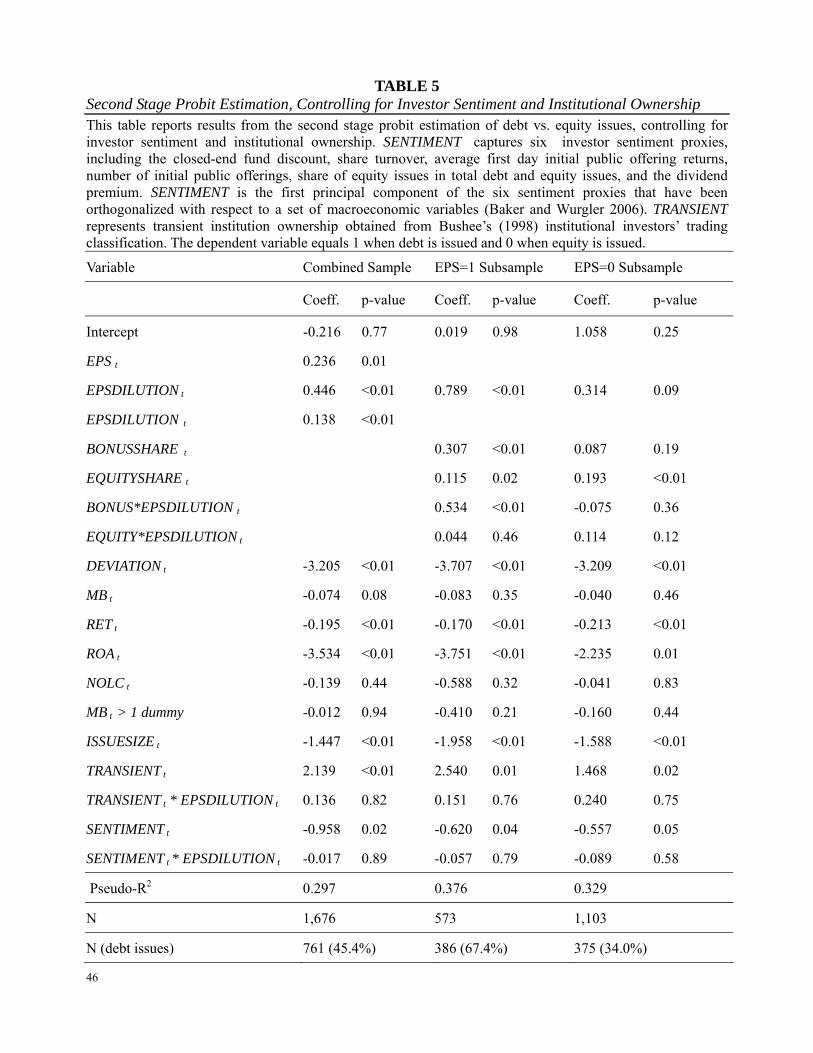

Clientele Effects and Investor Sentiment

Agency theory provides one potential explanation for managerial concern over EPS

dilution, and our empirical evidence strongly supports this view, but other explanations might

also apply. In this subsection, we explore whether behavioral theories related to clientele effects

and investor sentiment might also play a role in the phenomenon. That is, it is not that managers

per se are concerned about EPS dilution; it is rather that they are catering to investor demands

for higher reported EPS performance.

26

One might reasonably expect investor concern with EPS dilution to vary both cross-

sectionally and over time. For example, prior research has documented that transient

institutional owners tend to overvalue current earnings in pricing securities (Bushee 2001), and

high levels of transient institutional ownership has been linked to myopic financial reporting

behavior by managers. Bushee (1998) reports evidence that firms with high levels of transient

institutional ownership are more likely to cut R&D to reverse an earnings decline, and

Matsumoto (2002) finds that firms with high transient ownership are more likely to meet or

exceed earnings expectations. Thus, managers of firms with high transient institutional

ownership may have relatively stronger preferences to avoid earnings dilution than other firms.

Similarly, prior research shows that investor sentiment – a phenomenon that biases

investors’ expectations of future firm performance – affects firms’ investing and financing

decisions (see Baker et al. 2007). When market sentiment is low, investors are pessimistic about

future prospects and undervalue the firm. Managers may be particularly reluctant to dilute

earnings at these times, as investors already have a negative view of the firm’s outlook. In

contrast, when sentiment is high, earnings dilution will be less likely to concern investors, as

they view the firm’s long-term prospects as good. We therefore expect managers to have

stronger preferences to avoid earnings dilution during times of low investor sentiment.

We control for both transient institutional ownership (TRANSIENT) and investor

sentiment (SENTIMENT) in our analysis of debt/equity issuances and interact both measures

with EPSDILUTION. If clientele effects and investor sentiment are related to the dilution

puzzle, we expect a positive coefficient on TRANSIENT*EPSDILUTION and a negative

coefficient on SENTIMENT*EPSDILUTION. We define TRANSIENT using Bushee’s (1998)

27

investor trading classification scheme and SENTIMENT using the investor sentiment index

developed by Baker and Wurgler (2006).16

Our results, reported in Table 5, show that after controlling for these two factors, the

estimated coefficients on EPS (0.236), EPSDILUTION (0.446), and EPS*EPSDILUTION

(0.138) remain positive and highly significant for the combined sample. The estimated

coefficient on SENTIMENT (-0.958) is negative and significant (p-value = 0.02), indicating that

managers tend to issue debt when the investor sentiment is low, while the coefficient of 2.139 on

TRANSIENT is significantly positive, suggesting that managers tend to issue debt when there is a

large proportion of transient institutional investors. However, neither interaction term is

significant, which suggests that behavioral explanations are not driving managers’ concerns

regarding EPS dilution.

Results for the EPS=1 and EPS=0 subsamples are also qualitatively unchanged after

adding the TRANSIENT and SENTIMENT variables, although we note that the EPSDILUTION

variable in the EPS=0 subsample is now marginally significantly positive. Overall, we are

unable to find support for a behavioral explanation for managers’ aversion to earnings dilution.

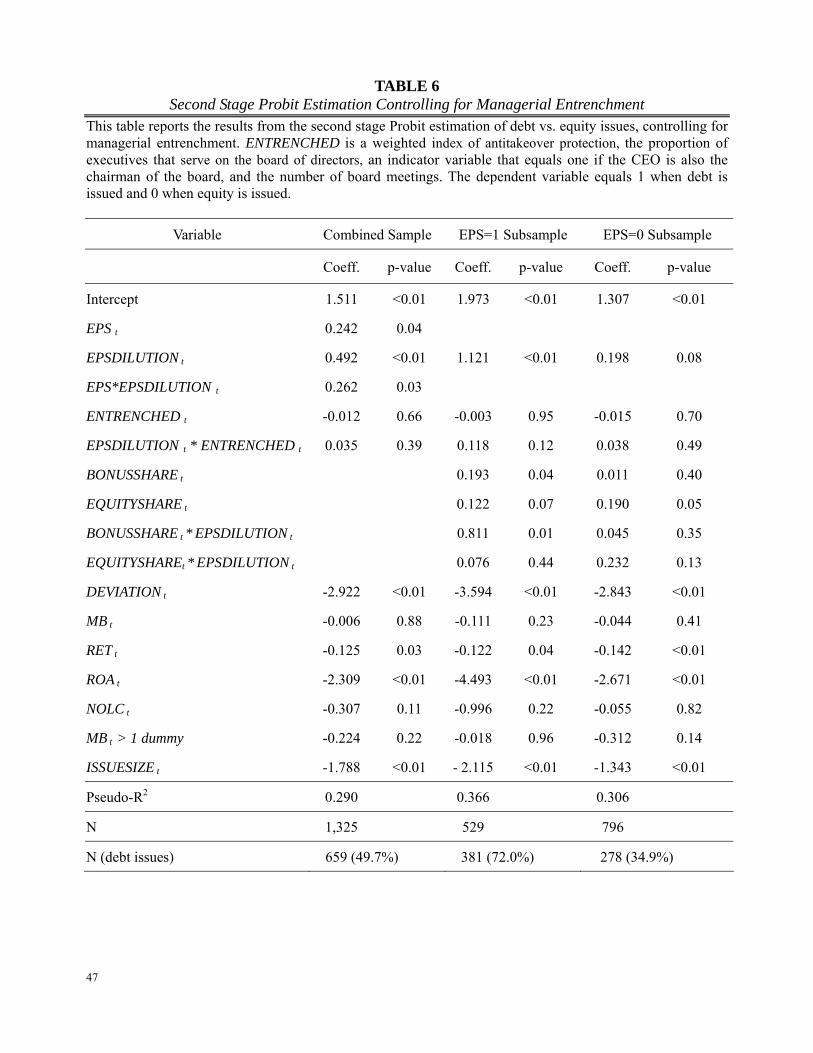

Managerial Entrenchment

Managerial preferences for avoiding EPS dilution may vary cross-sectionally with

corporate governance mechanisms and levels of managerial entrenchment. On the one hand, an

16 We thank Brian Bushee for providing transient institutional ownership data. The Baker and Wurgler (2006) index captures six investor sentiment proxies, including the closed-end fund discount, share turnover, average first day initial public offering returns, number of initial public offerings, share of equity issues in total debt and equity issues, and the dividend premium. SENTIMENT is the first principal component of the six sentiment proxies that have been orthogonalized with respect to a set of macroeconomic variables. We obtain this data from the following website: http://pages.stern.nyu.edu/~jwurgler/

28

entrenched manager may be better able to influence compensation levels than a less entrenched

manager (see Core et al. 1999), suggesting that a lower reported EPS figure may have little

impact on executives’ pay packages. On the other hand, Davila and Penalva (2006) find that

entrenched managers tend to have compensation contracts that employ accounting-based rather

than market-based performance measures, as accounting-based measures are presumably easier

to manipulate. This latter finding suggests that entrenched managers may benefit relatively more

from avoiding EPS dilution than other managers.

In this subsection, we explore whether managerial entrenchment might affect our results

linking managers’ aversion to EPS dilution to compensation contracts. We add the same

ENTRENCHED variable defined in Section III to our first and second stage regressions and also

add the interaction term ENTRENCHED*EPSDILUTION to the second stage analysis. As

shown in Table 6, the estimated coefficients on these variables are insignificantly different from

zero in every specification, although we note that for the EPS=1 subsample, the estimated

coefficient of 0.118 is approaching significance with a two-tailed p-value of 0.12. Overall,

however, our main findings are robust to controls for managerial entrenchment.

Executives’ Existing Stock and Option Holdings

In addition to the new grants of options and restricted stock that comprise our

EQUITYSHARE variable, executives’ existing holdings of stock and stock options might also

affect target leverage and debt-equity financing decisions, as they also help in aligning

executives’ interests with shareholders (Mehran 1992; Berger et al. 1997). As noted earlier,

option holdings could also affect our results if their exercise is used as an alternative tax shield to

29

debt financing.17 We estimate EQUITYHOLDING using the methodology outlined in Core and

Guay (1999) and Yermack (1995). Our results in both the first and second stage analyses are

robust to its inclusion as an additional control variable (results not tabulated). For the EPS=1

subsample, the estimated coefficients on EPSDILUTION (1.665), BONUSSHARE (0.183), and

BONUSSHARE*EPSDILUTION (0.878) are still significantly positive, and the coefficient on

EQUITYSHARE*EPSDILUTION is not significantly different from zero. In addition, neither

EQUITYHOLDINGS nor EQUITYHOLDINGS *EPSDILUTION are significant determinants of

debt/equity choice for this subsample. For the EPS=0 subsample, EQUITYSHARE remains a

significant determinant of financing choices, with an estimated coefficient of 0.280 (p-

value=0.03), but BONUSSHARE, the interactive terms BONUSSHARE*EPSDILUTION and

EQUITYSHARE*EPSDILUTION, and the new regressors EQUITYHOLDINGS and

EQUITYHOLDINGS*EPSDILUTION are all insignificant. Our main findings are thus robust to

the inclusion of executives’ equity holdings.

VII. Conclusions

In this paper, we examine whether the use of EPS as a performance metric in executives’

annual bonus contracts explains managers’ supposedly irrational tendency to avoid EPS dilution.

Using a large sample of debt and equity issuers with the necessary Compustat, CRSP, and

ExecuComp data over the period 1993-2005, we find that firms are significantly more likely to

favor debt over equity financing when debt has a relatively smaller dilutive effect on EPS and

17 Graham, Lang, and Shackelford (2004) find that the exercise of nonqualified stock options substantially reduces the marginal tax rates of Nasdaq 100 firms, but has little effect on the tax rates of S&P 100 firms. The median marginal tax rate for our sample firms is 0.35, which suggests that the widespread use of employee stock options as a non-debt tax shield is unlikely for our sample firms.

30

when executives are explicitly compensated on EPS performance; i.e., managers are more likely

to avoid EPS dilution when their pay depends on reported EPS. We also find that the likelihood

of a debt issue is increasing in the interaction between EPS dilution and the magnitude of

executives’ bonus compensation for the subsample of firms that explicitly reward executives on

EPS performance; we document no such relation for the firms that do not use EPS as a

performance metric in their annual bonus contracts. These results are robust controlling for

endogeneity in compensation contract design, behavioral explanations including clientele and

investor sentiment theories, and corporate governance policies. Overall, our results provide

compelling evidence that managers’ professed aversion to EPS dilution is related to

compensation contracting concerns, a finding consistent with agency theory.

While our findings suggest that contracting concerns are the most likely explanation for

managers’ tendency to avoid EPS dilution, we have no evidence that managers’ financing

choices are suboptimal, as incentive compensation is often used to encourage executives to

increase firm leverage. We consequently do not examine whether compensation committees

adjust executive pay for “opportunistic” financing choices, as we have no reason to believe that

an association between EPS-based bonus contracts and managerial preferences to avoid EPS

dilution represent a non-optimal contracting outcome. Future research might seek to address

whether there are instances of suboptimal leveraging decisions related to the use EPS-related

compensation contracts.

There are limitations to our analysis. First, because our EPSDILUTION variable depends

on firms’ E-P ratios, it could potentially capture growth or market timing effects. However, we

control for both of these effects by including the market-to-book ratio and stock price

31

performance in our analysis. It is also possible that the EPSDILUTION variable could also be

capturing differences in the relative cost of debt to equity, if the E-P ratio is viewed as a rough

proxy for the cost of equity capital. Firms will simply prefer to issue debt when it is relatively

cheaper than equity, i.e., when the EPSDILUTION variable is equal to one. While we

acknowledge that this is one possible interpretation of the EPSDILUTION variable, if this

construct is mainly capturing relative costs of debt versus equity financing, we would not expect

different results across our two subsamples, nor would we expect differences in the significance

of the interaction terms involving EPSDILUTION. In addition, our use of target leverage ratios

in the first stage analysis should also serve as an implicit control for the relative costs of debt

versus equity. Nonetheless, the results should be interpreted with this caveat in mind.

Second, we dichotomize our sample into firms that explicitly reward executives on EPS

performance and those that do not, based on information provided in proxy statements filed with

the SEC. It is possible that firms do use EPS in determining bonus compensation, but do not

disclose this information in their proxy statements. On a related note, we assume that bonus

compensation mainly reflects earnings and EPS performance. While this assumption is well-

supported in prior research, bonus compensation could potentially be affected by stock price

performance, as well as by non-financial measures of performance. To the extent that either or

both of the above situations apply, the power of our tests will be reduced.

The relatively small magnitude of bonus compensation relative to other components of

executive pay also has implications for our study. We implicitly assume that bonus

compensation is sufficiently large enough to impact managerial decision making. The strength

of our results suggests that this assumption is justified, and we further note that current trends in

32

incentive compensation may eventually render this potential concern as moot. Citing a survey of

350 large U.S. companies, Dvorak (2007) observes that as many firms are abandoning stock

options due to the new expensing requirements and other problematic issues, the percentage of

performance-based incentive pay has increased dramatically from 12% to 31% of total incentive

compensation over 2002−2006. The importance of bonus contract design in firm decision-

making is likely to grow in the near future.

On a final note, given the significant impact that EPS-based bonus contracts have in our

setting, it is likely that the use of EPS as a performance metric in determining executive pay

affects other firm decisions as well. For example, the Office of Federal Housing Enterprise

Oversight’s (OFHEO) now-famous 2006 report on the Fannie Mae accounting debacle sharply

criticizes Fannie Mae’s over-reliance on EPS in determining executive pay. According to the

report, “Fannie Mae tied major portions of executive compensation to EPS, a metric easily

manipulated by management.” The report also states, “Fannie Mae’s executives were precisely

managing earnings to the one-hundredth of a penny to maximize their bonuses while neglecting

investments in systems internal controls and risk management,” and Fannie Mae’s reaching of

announced targets for EPS each quarter “were illusions deliberately and systematically created

by senior management with the aid of inappropriate accounting and improper earnings

management.” Future research might address whether the use of EPS-based compensation

contracts has played a similar role in the recent financial crisis.

33

REFERENCES

Baker, M., and J. Wurgler. 2002. Market timing and capital structure. Journal of Finance 57 (1): 1-32.

———, and ———. 2006. Investor sentiment and the cross-section of stock returns. Journal of

Finance 61(4): 1645-1680. ———, R. Ruback, and J. Wurgler. 2007. Behavioral corporate finance: A survey. Handbook of

Corporate Finance: Empirical Corporate Finance. Barclay, M., and C. Smith. 2005. The capital structure puzzle: The evidence revisited. Journal of

Applied Corporate Finance 17(1): 8-17. Bens, D., V. Nagar, and F. Wong. 2002. Real investment implications of employee stock option

exercises. Journal of Accounting Research 40 (20): 359-393. Bens, D., V. Nagar, D. Skinner, and F. Wong. 2003. Employee stock options, EPS dilution, and

stock repurchases. Journal of Accounting and Economics 36 (1-3): 51-90. Berger, P., E. Ofek, and D. Yermack. 1997. Managerial Entrenchment and Capital Structure

Decisions. Journal of Finance 52 (4): 1411-1438. Bergstresser, D., and T. Phillippon. 2006. CEO incentives and earnings management. Journal of

Financial Economics 80 (3): 511-529. Brealey, R., S. Myers, and F. Allen. 2007. Principles of Corporate Finance. McGraw-Hill, New

York, NY. Bryan S., L. Hwang, and S. Lilien. 2000. CEO stock-based compensation: An empirical analysis

of incentive-intensity, relative mix, and economic determinants. Journal of Business 73(4): 661-693.

Bushee, B. 1998. The influence of institutional investors on myopic R&D investment behavior.

The Accounting Review 73(3):305-333. ———. 2001. Do institutional investors prefer near-term earnings over long-run value?

Contemporary Accounting Research 18 (2): 207-247. Bushman, R., and A. Smith. 2001. Financial Accounting Information and Corporate Governance.

Journal of Accounting and Economics 32 (1-3): 237-333. Byoun, S. 2008. How and when do firms adjust their capital structure toward targets? Journal of

Finance 63(6): 3069-3096.

34

Cheng, Q., and T. Warfield. 2005. Equity incentives and earnings management. The Accounting

Review 80 (2): 441-476. Core, J., and W. Guay. 1999. The use of equity grants to manage optimal equity incentive levels.

Journal of Accounting and Economics 28 (2): 151-184. ———, ———, and R. Verrecchia. 2003. Price versus non-price performance measures in optimal

CEO compensation contracts. The Accounting Review 78 (4): 957-981. ———, R. Holthausen, and D. Larcker. 1999. Corporate governance, the executive officer

compensation, and firm performance. Journal of Financial Economics, 51 (3): 371-406. Davila, A., and F. Penalva. 2006. Governance structure and the weighting of performance

measures in CEO compensation. Review of Accounting Studies 11(4): 463-493. Dvorak, P. 2007. Theory and practice: Tweaking the stock option grant – Firms rework terms to

keep plans’ benefits and minimize problems. Wall Street Journal (April 30): B3. Engel, E., M. Erickson, and E. Maydew. 1999. Debt-equity hybrid securities. Journal of

Accounting Research 37 (2): 249-74. Fama, E. 1980. Agency problems and the theory of the firm. Journal of Political Economy 88

(2): 288-307. ———, and K.R. French. 2002. Testing tradeoff and pecking order predictions about dividends

and debt. Review of Financial Studies 15 (1): 1-33. ———, and ———. 2005. Financing decisions: Who issues stock? Journal of Financial Economics

76 (3): 549-582. Frank, M., and V. Goyal. 2003. Testing the pecking order theory of capital structure dividends

and debt. Journal of Financial Economics 67 (2):217-248. Gaver, J. J., and K. M. Gaver. 1998. The relation between nonrecurring accounting transactions

and CEO cash compensation. The Accounting Review 73 (2):235-253. Gompers, P., J. Ishii, and A. Metrick. 2003. Corporate governance and equity prices. Quarterly

Journal of Economics 118 (1): 107-155. Graham, J., and C. Harvey. 2001. The theory and practice of corporate finance: Evidence from

the field. Journal of Financial Economics 60 (2-3):187-243. ———, M. Lang, and D. Shackelford. 2004. Employee Stock Options, Corporate Taxes, and Debt

35

Policy. Journal of Finance 59 (4): 1585-1618. ———, and Mills, L. (2008). Using tax return data to simulate corporate marginal tax rates.

Journal of Accounting and Economics 46 (2-3): 366-388. Greene, W. 2000. Econometric Analysis. Upper Saddle River, NJ: Prentice-Hall. Guay, W. 2002. Discussion of “real implications of employee stock option exercises.” Journal

of Accounting Research 40 (2002): 395-406. Hand, J. R. 1989. Did firms undertake debt-equity swaps for an accounting paper profit or true

financial gain? The Accounting Review 64 (4): 587-623. Hall, B., and J. Liebman. 1998. Are CEOs really paid like bureaucrats? Quarterly Journal of

Economics 111(3): 653-661. Healy, P. M. 1985. The effect of bonus schemes on accounting decisions. Journal of Accounting

and Economics 7(1-3): 85-107. Heckman, J.J. 1978. Dummy endogenous variables in a simultaneous equation system.

Econometrica 46 (4): 931-60. Holthausen, R., D. Larcker, and R. Sloan. 1995. Annual bonus schemes and the manipulation of

earnings. Journal of Accounting and Economics 19 (1):29-74. Hoppe, F., and F. Moers. 2008. Bonus contracts, private information, and CEO turnover.

Working paper, Maastricht University. Hovakimian, A., G. Hovakimian., and H. Tehranian. 2004. Determinants of target capital

structure: the case of due debt and equity issues. Journal of Financial Economics 71 (3): 517-540.

———, T. Opler., and S. Titman. 2001. The debt-equity choice. Journal of Financial and

Quantitative Analysis 36 (1): 1-24. Hribar, P., N. Jenkins, and W. B. Johnson. 2006. Stock repurchases as an earnings management

device. Journal of Accounting and Economics 41(1-2): 3-27. Imhoff, E., and J. Thomas. 1988 Economic consequences of accounting standards: The lease

disclosure rule change. Journal of Accounting and Economics 10 (4): 277-310. Jensen, M., and W. Meckling. 1976. Theory of firm: Managerial behavior, agency costs and

capital structure. Journal of Financial Economics 3 (4): 305-360.

36

———, and K. Murphy. 1990. Performance pay and top-management incentives. Journal of

Political Economy 98 (2): 225-264. Kayhan, A., and S. Titman. 2007. Firms’ histories and their capital structures. Journal of

Financial Economics 83 (1): 1-32. Kalyta, P. 2009. Accounting discretion, horizon problem, and CEO retirement benefits. The Accounting Review (forthcoming). Kole, S. 1997. The complexity of compensation contracts. Journal of Financial Economics 43

(1): 79-104. Larcker, D. 2003. Discussion of “employee stock options, EPS dilution, and stock repurchases.”

Journal of Accounting and Economics 36 (1-3): 45-49. Maddala, G. 2001. Introduction to Econometrics. Chichester, England: Wiley. Marquardt, C., and C. Wiedman. 2005. Earnings management through transaction structuring:

Contingent convertible debt and diluted earnings per share. Journal of Accounting Research 43 (2): 205-243.

Matsumoto, D. 2002. Management’s incentives to avoid earnings surprises. The Accounting

Review 77(3): 483-514. Mehran, H. 1992. Executive incentive plans, corporate control, and capital structure. Journal of

Financial and Quantitative Analysis 27 (4): 539-560. Miller, M.H., 1977. Debt and taxes. Journal of Finance 32 (2):261-275 Mills, L. and K. Newberry. 2005. Evidence of off-balance-sheet financing from book-tax

differences. Journal of Accounting Research 43(2): 251-282. Modigliani, F., and M. Miller. 1958. The cost of capital, corporation finance and the theory of

investment. American Economic Review 48 (3): 261-297. Morgenson, G. 2008. If the pay fix is in, good luck finding it. The New York Times (September

07): BU1. Murphy, K. 1999. Executive compensation. In Handbook of Labor Economics, Vol. 3b, edited

by O. Ashenfelter, and D. Card, Chapter 38, 2485-2563. New York, NY: North-Holland.

Myers, S. 1984. The capital structure puzzle. Journal of Finance 39 (3): 575-592. Myers, J., L. Myers, and D. Skinner. 2007. Earnings momentum and earnings management.

37

Journal of Accounting Auditing and Finance 22 (2): 249-284. Rajan, R. G., and L. Zingales. 1995. What do we know about capital structure? Some evidence

from international Data. Journal of Finance 50 (5): 1421-1460. Servaes, H., and P. Tufano. 2006. The theory and practice of corporate capital structure.

Corporate Capital Structure, Deutsche Bank, ed. James Ballingall and Adrian Crockett (January).

Skinner, D. J. 1993. The investment opportunity set and accounting procedure choice:

Preliminary evidence. Journal of Accounting and Economics 16 (4):407-445. Smith, C., and Watts, R. 1992. The investment opportunity set and corporate financing, dividend,

and compensation policies. Journal of Financial Economics 32 (3): 263-292 Titman, S. 1984. The effect of capital structure on a firm’s liquidation decision. Journal of

Financial Economics 13 (1): 137-151.

———, and R. Wessels. 1988. The determinants of capital structure.” Journal of Finance 43 (1): 1-19.

Watts, R., and J. Zimmerman. 1986. Positive accounting theory. Prentice-Hall Welch, I. 2004. Capital structure and stock returns. Journal of Political Economy 112 (1): 106-

131. Yang, J., and S. Young. 2009. Stock repurchases and executive compensation contract design:

The role of earnings per share performance conditions. Working Paper, Towers Perrin, Lancaster University.

Yermack, D. 1995. Do corporations award CEO stock options effectively? Journal of Financial

Economics 39 (2-3): 237-269.

38

APPENDIX

EPS Dilution and Debt vs. Equity Issues

The relative effect of a debt versus an equity issue on reported EPS depends on the

relation between the firm’s E/P ratio and the after-tax cost of debt. To illustrate, assume that at

the beginning of the year the firm finances a project by issuing either debt or equity, where the

amount of financing equals the stock price at the beginning of the year, Pt-1, times the number of

shares issued, N.18 In the case of a debt issue, reported EPS at the end of the year may be

expressed as 1

1

−

−−

t

td

SharesNPrE

where E is annual earnings before interest on the debt issued, rd is the

after-tax interest rate on the debt, and Sharest-1 equals the number of common shares outstanding

at the beginning of the year. In the case of an equity issue, reported EPS at the end of the year is

simply NShares

E

t +−1

.

Reported EPS will be higher when debt financing is used instead of equity financing

whenever the following holds:

.11

1

NSharesE

SharesNPrE

tt

td

+>

−

−−

− (A.1)

Algebraic manipulation yields the following relation:

.1)( 11

dtt

rPNShares

E>

+ −−

(A.2)

Note that the first term, NShares

E

t +−1

, is reported EPS assuming an equity issue. Equation

(A.2) indicates that an equity issue will result in lower reported EPS, relative to a debt issue, 18 The example can be easily generalized to allow the financing event to occur at any time during the fiscal year.

39

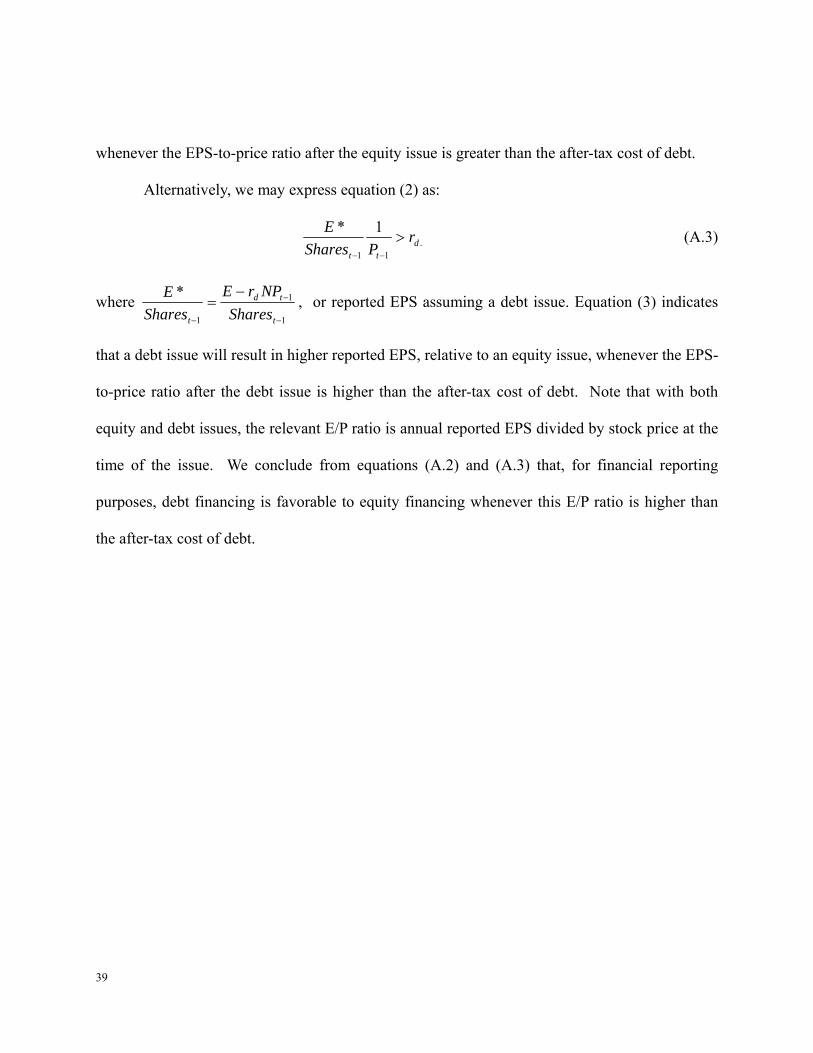

whenever the EPS-to-price ratio after the equity issue is greater than the after-tax cost of debt.

Alternatively, we may express equation (2) as:

.11

1*d

tt

rPShares

E>

−−

(A.3)

where 1

1

1

*

−

−

−

−=

t

td

t SharesNPrE

SharesE , or reported EPS assuming a debt issue. Equation (3) indicates

that a debt issue will result in higher reported EPS, relative to an equity issue, whenever the EPS-

to-price ratio after the debt issue is higher than the after-tax cost of debt. Note that with both

equity and debt issues, the relevant E/P ratio is annual reported EPS divided by stock price at the

time of the issue. We conclude from equations (A.2) and (A.3) that, for financial reporting

purposes, debt financing is favorable to equity financing whenever this E/P ratio is higher than

the after-tax cost of debt.

40

TABLE 1 Descriptive Statistics for Target Leverage Estimation Sample