Embed Size (px)

Citation preview

WHITE YOUNG GREEN PLANNING REGATTA HOUSE CLIPPERS QUAY SALFORD QUAYS

MANCHESTER M50 3XP

TEL 0161 872 3223 FAX 0161 872 3193

ST HELENS RETAIL CAPACITY STUDY

Final Report

Prepared by

WHITE YOUNG GREEN PLANNING

On behalf of

ST HELENS COUNCIL

MAY 2005

CONTENTS __________________________________________________________________________ Page

1 INTRODUCTION 1 2 BACKGROUND TO RETAIL AND LEISURE 4 3 PLANNING POLICY FRAMEWORK 18 4 ASSESSMENT OF VITALITY AND VIABILITY 24 5 ORIGINAL MARKET RESEARCH 47

6 POPULATION AND EXPENDITURE 57 7 RETAIL CAPACITY ASSESSMENT 73 8 SUMMARY 85

Appendix A - Defined Catchment

Appendix B - MapInfo methodology

Appendix C - Household Survey Results

Appendix D - In Street Survey

Appendix E - WYG Convenience Model

Appendix F - WYG Comparison Model

Appendix G - Business Survey Results – St Helens

Appendix H - Business Survey Results - Earlestown

Appendix I - GOAD Town Centre Map

Technical Appendices are bound under separate cover.

1 INTRODUCTION Objectives of the Study 1.01 White Young Green Planning was commissioned by St Helens Metropolitan Borough

Council in 2004, to undertake a retail study for the Borough (2005 to 2015). The

study seeks to up-date the findings of 2001 Retail & Leisure (2000-2016) Study

undertaken by MVM Planning and provide new evidence on the need for further retail

development.

1.02 The aim of this study is to provide baseline evidence that will inform the development

of future plan strategy including the emerging Local Development Framework.

Therefore, this report specifically focuses on the ‘need’ for future retail and leisure

uses rather than seeking to review local policy at this stage. In response to the

requirements of Consultant’s Brief, the report considers the following.

(1) To provide an of Update of the need assessment set out in the 2001 Retail and

Leisure Study;

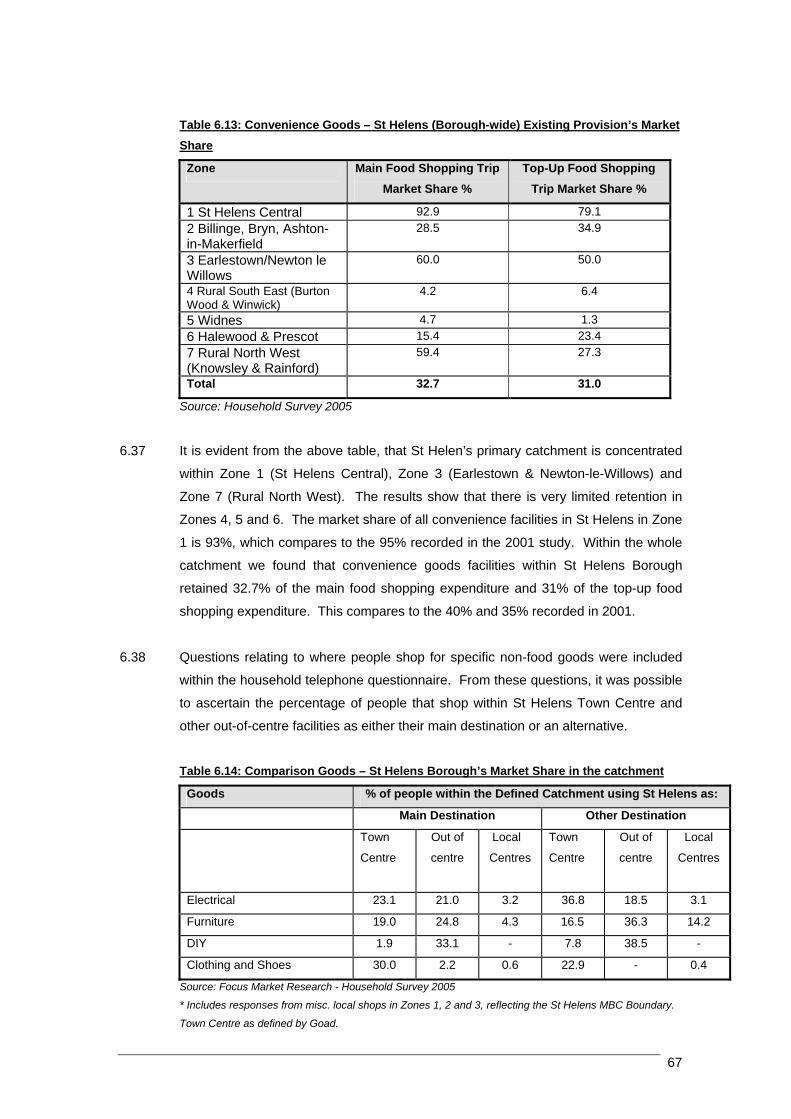

(2) To compare and contrast results between the 2001 and 2005 studies;

(3) To identify capacity to accommodate additional retail growth by sector over the

period to 2015; and

(4) To review sub-regional trends in the retail market and advise on the actions

necessary for St Helens to maintain it’s competitive position.

1.03. The methodology adopted for the study has been informed by the recently published

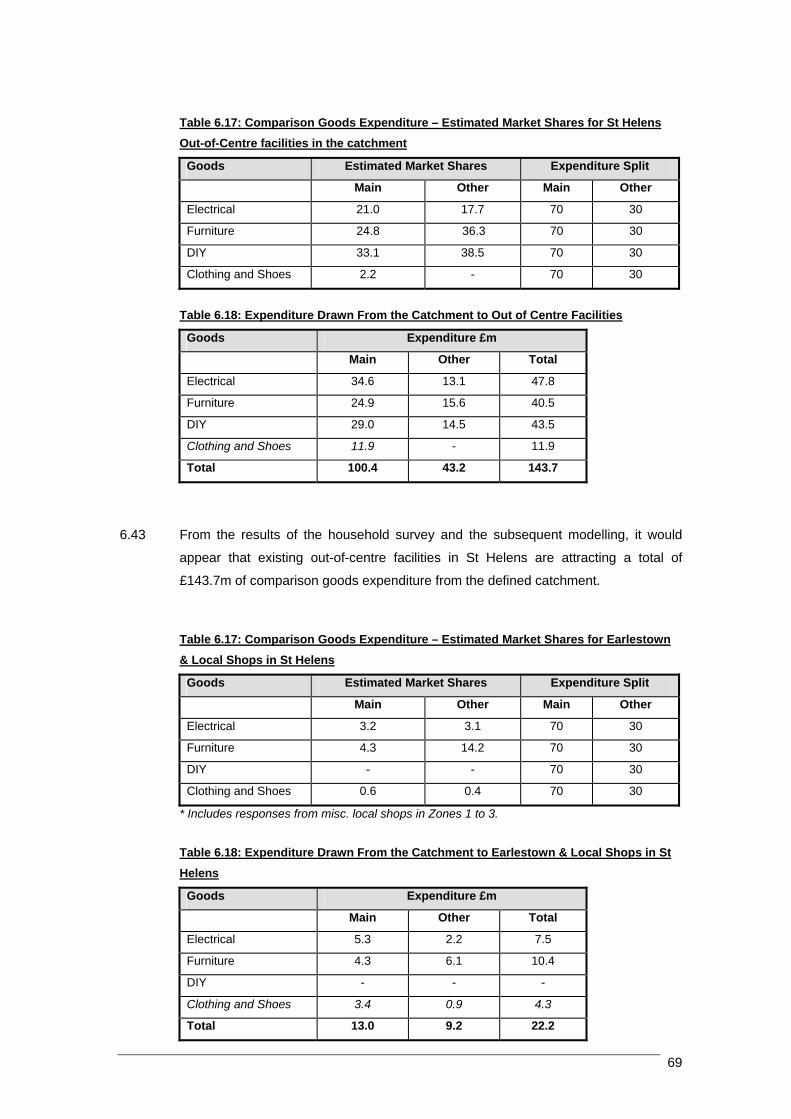

Planning Policy Statement 6 (PPS6) which deals with town centre and retail

development. The study has also taken into account the findings of key documents

produced by the Local Planning authority, most notably their annual ‘St Helens Town

Centre Health Check’.

Original Market Research

1.04 In order to up date the 2001 study, new empirical research has been completed.

This includes:

A telephone survey of 1,000 households (compared to 750 in 2001) in St

Helens and the surrounding area in order to ascertain general patterns of

shopping and leisure activity in the sub-region. The same catchment was

used as in the 2001 study in order to compare changes in market shares. A

plan showing the extent of the catchment area is provided below;

1

Figure 1.1: The Defined Catchment Area

An on-street survey of 300 visitors to St Helens and Earlestown Town

Centres in order to gauge customer perceptions of each centre and following

the same methodology adopted in the 2001 study.

A postal survey of 600 retail and services businesses within St Helens and

156 within Earlestown town centres in order to assess retailer’s views of the

strengths and weaknesses of each town as a shopping and leisure

destination and to understand their future plans for investment within the

centres.

Report Structure

1.05 The report is set out as follows:

Section 2: considers recent and future trends in the retail market and the

implications on land use planning.

Section 3: provides an overview of the current and emerging planning legislation

in respect of retail development.

Section 4: provides an assessment of the vitality and viability of both St Helens

and Earlestown Town Centres, in line with the guidance set out in

PPS6, comparing these to the results of the 2001 MVM study.

Section 5: reviews the findings of the original market research that underpins the

study, including an examination of the household survey, in street

2

survey and business survey, comparing the results to the previous

2001 study.

Section 6: undertakes an assessment of expenditure growth in convenience and

comparison goods within the defined catchment area and identifies the

market shares for a variety of goods for St Helens.

Section 7: Identifies the retail capacity for additional convenience and comparison

floorspace within St Helens Borough.

Section 8: Sets out the study’s principal findings and recommendations for any

future policy formulation.

3

2 BACKGROUND TO THE RETAIL AND LEISURE INDUSTRY Forecast Changes in Consumer Expenditure

2.01 The latest figures recorded by MapInfo for retail consumer expenditure in 2003

reached an all time high of £4,346 per head per annum (2000 Prices). This

represents over 80% growth in expenditure since 1983 when average retail

expenditure per head stood at £2,382. This represents a compounded average

annual growth rates for all retail goods of 2.8% per annum.

2.02 However, when the headline figures are examined in more detail, it is evident that

much of the impressive growth recorded in the past twenty years has been achieved

in the ‘non-food’ goods sector.

Convenience Goods

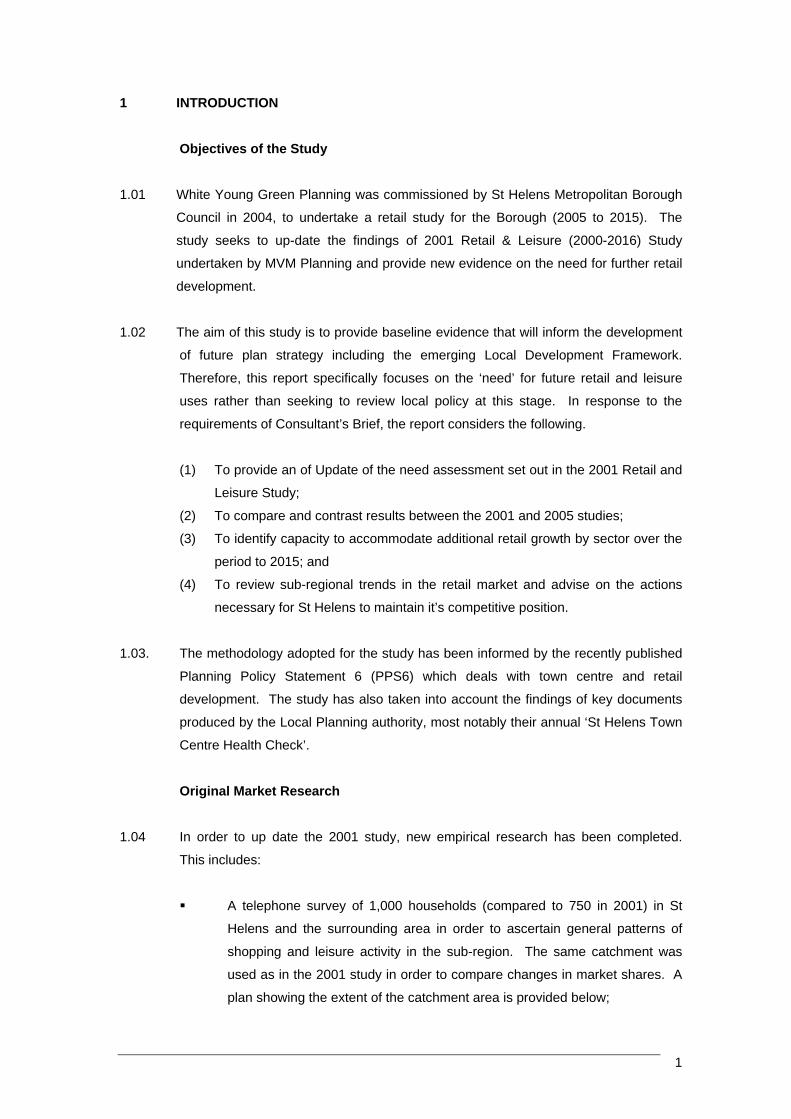

2.03 In 1983, the average spend on convenience (food grocery) goods was £1,483 per

head per annum. By 2003 the average spend per head was £1,584 which

represents a growth of just 12% or 0.5% per annum compound. As can be seen from

figure 2.1 below, the pattern of growth over the twenty year period has been

inconsistent with expenditure declining during six of the twenty years. It is evident

that expenditure per capita on convenience goods has fluctuated within a narrow

band with no real trend growth over the past 40 years as a whole. Whilst expenditure

steadily declined in the 1970’s the trend since then has been slightly upwards.

Figure 2.1: Retail Expenditure Growth

UK Average Consumer Retail Expenditure by Goods Type (2000 prices)

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

Year

GB

P

Convenience GoodsComparison GoodsAll Goods

4

2.04 There is a widely held theory that consumers will only purchase the convenience

goods that they need to ensure that they eat regularly. Therefore, the likelihood of

witnessing any major growth after inflation is limited. In addition, as society in

general becomes more affluent and our standard of living increases, we will have a

greater tendency to eat out more frequently thereby reducing the need to spend as

much on food goods in the supermarket.

2.05 However, more recent evidence on growth has shown that the opposite is actually

occurring with convenience goods expenditure per capita increasing at 1.0% per

annum between 1998 and 2003. This is double the rate of growth recorded over the

past twenty years. Much of this growth could be attributed to the increase in

popularity of more expensive organic produce and luxury items. The major

supermarket operators have responded to consumer’s increasing demands for high

quality produce with the release of brands such as Sainsbury’s ‘Taste the Difference’,

Tesco’s ‘Finest’ and Asda’s ‘Extra Special’. However, it must be noted that the

increases that have been recorded in the short term are likely to reflect the strong

economic growth over the past five years and general increases in household

disposable income.

.06 If the economy was to enter into a recessionary period in the future then this growth

may not be as significant given that spending on luxury items would be the first to be

hit. In fact between the recession in 1980 and 1984 expenditure on convenience

products fell by 6%. During the next recession in 1991 and 1995 convenience

expenditure also fell by just over 2%. This would appear to suggest that recessionary

periods may have an influence on the overall level of growth recorded in convenience

goods shopping.

.07 MapInfo recognise that it is inaccurate to focus on short term growth which may not

reflect the true periods of growth and decline. They state that at present the most

tatistically robust estimate for growth in this sector is for the period 1993 to 2003

.08 In 1983 the average spend on comparison (non-food) goods was just £913 per capita

nd

2

2

s

when the annual growth rate averaged 0.9%. MapInfo suggest that the strong

growth recorded recently appears to be unsustainable in the longer run similar to the

boom in the 1980’s which was then followed by a period of slower growth.

Comparison Goods

2

per annum. This represented just 38% of total retail expenditure and was well behi

average expenditure on convenience goods. However, there has been significant

5

growth in comparison goods expenditure since 1983 which now means that

comparison goods expenditure represents 64% of retail expenditure.

In 1992, more was spent on comparison goods than convenience goods for the first

time since records began in 1964. By 2003, the average expenditure on compa

goods had reached £2,762 per capita. This represented a growth of over 200% in

just 20 years. This equates to an annual average growth of 5.0% compared to

0.5% recorded in com

2.09

rison

the

parison goods.

h

the

.11 However, despite the peaks and troughs recorded, the most important fact is that in

2.12

tres such

as Cheshire Oaks and The Trafford Centre. In fact, all of the major supermarket

the future growth in retail expenditure will be primarily

focused on non-food goods. Therefore, we have witnessed the shift in emphasis

Asda

Implications of Future Growth

2.14

t

2.10 Similar to convenience goods, the growth recorded over the twenty year period

reflects the general economic performance and growth in disposable income. At the

height of the economic boom in the mid to late 1980’s growth was recorded as hig

as 8.3% in 1986. By 1991 growth had fallen to just 0.1% reflecting the onset of

recession and increasing interest rates. By the mid to late 1990’s growth had

recovered significantly with the latest high recorded in 2000 with 8.2% growth.

2

the last 20 years growth on non-food expenditure has trebled. In fact, spending in

2003 on comparison goods per capita at constant prices was over four times larger

than spending on the same basis in 1964.

With this in mind, it is not surprising to discover that major retail development has

been driven by non-food retail development including regional shopping cen

operators now recognise that

within larger supermarkets seeking to provide more space for the sale of comparison

goods. This has been most successfully achieved within Asda whereby the growth of

the Asda George brand has now resulted in the development of stand alone Asda

George stores selling non-food goods only. One such example is the recent

George store at Manchester Fort Retail Park.

2.13 MapInfo recognise that the strong growth recorded recently will be unsustainable

particularly as the economy begins to slow. Despite this, it is anticipated that the

average rate of growth recorded through to 2016 will still be between 3.9% and 3.4%

per annum.

In order to examine the potential implications of future expenditure growth, MapInfo

have provided forecasts for UK consumer spending which are based partly upon pas

6

trends but also on expected changes on other economic variables. The forecasts

recognise that the short-term growth trends for all goods, especially compariso

goods are unsustainable and that some correction is necessary. However, MapI

n

nfo

expect price falls to continue for products such as electronics and clothing which will

2.15

Figure 2.2: Average Annual Forecast Growth Rates

continue to boost sales.

On this basis, MapInfo have provided forecasts which are set out below.

Convenience Comparison Total 2004-2006 1.1% 3.9% 2.9% 2004-2011 1.2% 3.5% 2.7% 2004-2016 1.2% 3.4% 2.7%

2.16

mparison goods expenditure. In

fact, in the next twenty years, expenditure on comparison goods is set to double

ctual and Forecast Expenditure Per Capita per Annum

If we project these forecast growth rates through to 2021, it is evident that growth will

still be significantly focused on comparison goods. From Figure 2.3 below, it is

evident that by 2021, total expenditure will have increased by 61% to £7,005 per

capita per annum. The anticipated growth recorded for convenience goods will be

24% compared to the 83% growth recorded in co

based on current forecasts. This has important implications for the modelling of

future retail ‘needs’ which is set out in detail later on in this study.

Figure 2.3: A

2003 2011 2016 2021 Convenience £1,584 £1,743 £1,850 £1,963 Comparison £2,762 £3,609 £4,266 £5,042 Total £4,346 £5,352 £6,115 £7,005

The Retail Market

The retail market has been the subject of some profound changes over the recent past. The mix of social and economic conditions which prevailed in the 1980’s and 1990’s triggered the arriv

2.17

al of a much more discerning consumer driven not just by value for money but also increased selectivity and a demand for higher quality

entury where value for money is increasingly important. These conditions continue to

e consumer loyalty has become a ital ingredient in the success to retailers. Increasingly, successful shopping facilities

h ve to fulfil t stination l ge part thi s providing a w f nd leisure fa able to attract and the interest of the entire fam return such schem nefit not only from wider

shopping environments. This trend has continued through the turn of the C

impinge on the nature of today’s retail market wherva he role of a de ocation. In lar s meanide range o shopping a cilities retain

ily. In es be much

7

catchment areas, but also from substa longer shopping trips. Effectively, shopping is fast becoming the nation’s key leisure activity. However, the consumer is

one

2.18 e

n rising

stand alone food superstores, accounted for another 8.9 million sq. m or 15% of the

2.19 Other shopping malls in off-ce ocations ed about 0.8 million sq. m in 2000

c only 0.1 million sq. m in 198 f town reTrafford Centre eshire ompris than 80,the period but incre n sq. m by the end of 199 . Furthermore, with the high rate of residential construction during the 1980’s, local district centres expanded to an estimated 6.6 million sq. m in 1998.

.20 The decline of the traditional high street, however, should not be assumed to mean

town

e in

2.21

r that

2.22

There is increasing evidence that polarisation of centres is occurring across the UK, whereby large, more dominant

ilarly, the more attractive and accessible town centres are likely to

ntially

still keen to experience increases in choice and conveni9nce. This has led to the development of large format stores which seek to offer a wider range of goods inconvenient location supported by free parking.

As a result, over the last twenty-year period, the retail property landscape across thUK has changed dramatically. Since 1980, the rise of out of town retailing was unparalleled, and by 2000, the amount of retail park space had grown to 4.6 milliosq. m, representing 7.5% of all the UK retail stock. Superstores, mainly comp

total retail stock.

ntre l providompared with 0. Out o gional malls such as

and Ch Oaks c ed less 000 sq. m at the start of ased to nearly 1 millio 8

2

the decline of overall town centre trading. New shopping schemes in centres or onthe edge of town centres have brought not only more efficient space into the retail hierarchy, but introduced a quality of managed shopping environments, which couldnot be created within the context of the high street. Managed shopping malls incentres totalled 6.5 million sq. m at the beginning of the 1980’s. In 2000 they comprised over 10.5 million sq. m, a 60% rise. As a result 18% of all retail spacthe country is now to be found in shopping malls located within town centres.

As a whole therefore, the amount of retail space in town centres including both traditional and new space has not declined. On the contrary it has risen from around35 million sq. m in 1980 to nearly 39 million sq. m by 2000, a rise of 11% oveperiod.

However, much of this activity has taken place in higher order centres where largescale redevelopment schemes have been driven by high street national multiples seeking to increase representation and market share.

retail markets (both in terms of town centres and out of town malls) have continued to outperform more average locations in retail growth terms. The reduction in the amount of new floorspace coming through the out of town development pipeline (as more restrictive planning policy bites) is likely to further inflate rents in the best retail parks and prime locations, adding further to the divide between prime and secondaryretail property. Sim

8

perform better than the less attractive centres. Town centre expansion however will allow new opportunities to develop within the heart of towns which could dilute saleand rental performance in some locations, whilst encouraging it in others. The effectsof such development on existing business need to be carefully monitored.

In the next twenty years the retail landscape will cont

s

2.23 inue to evolve. Taking the

anticipated rise in the volume of retail sales, the expected trend in sales productivity, .

2.24

on

names are becoming increasingly vulnerable to takeovers. The merger and

n

d to

2.26

an

increasing number of outlets for specialist or niche goods, rather than rely on

to

space.

2.27 approach to new

investment for many key national retailers. Marginal locations within centres, and

as well as the retail schemes already in the development pipeline, it is reasonable toexpect further increases in total retail floorspace in major retail locations in the future

Certainly, future policy needs to be based on creating a balance between accommodating the dynamism of the market place, its increasing competitiveness and the widening gulf between differing shopping locations.

Trends in Non-food Retailing

2.25 As highlighted above overall, expenditure on non-food goods is increasing year

year, providing a stable platform for the domestic industry to grow. International

market conditions and price deflation in some key sectors mean that many high street

consolidation of companies could lead to fewer national multiple outlets competing i

the market place during the course of the local plan review. It will make those

retailers still in the market increasingly location-sensitive. This will increase demand

from multiples for prime and ‘super-prime’ pitches, but reduce the attractiveness of

other areas. The net result may be an increased occupation of secondary town

centre shopping units by non-retail uses. Planning policy has already responde

this trend by providing more flexible policy stances relating to secondary retail activity

and changes of use.

Key retailers, such as Marks & Spencer and the Arcadia Group, are reducing the

distribution of their operations and others, such as C&A, have left the domestic

marketplace altogether. This is a result not only of price deflation, but also of

changing shopping patterns. Many consumers are now prepared to shop in

household names, as was the case previously. The decision by Asda and Tesco

stock clothing has also had a major impact on this core area of high street trade. As

demand from these major anchor retailers decreases for representation in smaller

town centres, more lower-order retailers and food/drink uses will occupy town centre

Increased sensitivity over future viability will mean a cautious

9

prime locations within smaller town centres, will be increasingly rejected. Many

investment decisions will be influenced by the scale of commitment from other

2.28

. The

of between 2,500 and 5,000 sq. m. Demand is weakest in

the size range where supply is greatest (of about 1,000 sq. m).

2.29

rder to

.30 In addition, the DIY market has grown in strength considerably, in line with the

ween

ed

e

n, at

tlet Centres has subsided considerably, suppressed

by increasing planning restrictions. However, these and other successful regional

se

retailers; developers will increasingly need to promote large town centre

redevelopment schemes if they are to attract high quality retailers.

Retail Warehousing

In terms of retail warehousing, the market is becoming increasingly sensitive to

quality and location. Many retail warehouse operators will now only accept units on

major mixed-use retail parks, leading to a decline in the popularity of free-standing

units and older retail parks that are located away from the regional road network

market is now dominated by the likes of Homebase, Ikea, Big W and B&Q, seeking

units of 10,000-12,000 sq. m; and Matalan, Comet, Currys, Decathlon and Focus

seeking flagship stores

Many retail parks are unable to accommodate this new demand owing to the

configuration of the existing units. In the context of low demand for the smaller ‘bulky

goods’ units, many investors are seeking to create greater flexibility by incorporating

mezzanine levels into existing outlets, and to remove restrictive conditions in o

increase the number of ‘non-bulky’ goods operators able to utilize the space.

Because more fashion wear retailers are experimenting with lower cost warehouse

formats, many developers are seeking to provide fashion-led out-of-centre retail

parks (‘shopping parks’).

2

expanding DIY and home improvement culture. The market grew by 51.2% bet

1996 and 2000 and in 2000 alone consumer spending in the market sector increas

by 2.2%. However, the Keynote Market Review (August 2001) anticipates that

growth in the DIY market is slowing and more gradual growth is predicted for th

period 2001 to 2005. Despite this, spending is forecast to reach £11 billio

current prices, by 2005.

2.31 The demand for new Factory Ou

shopping centres, such as Merry Hill, are under pressure to extend and to increa

their overall attractiveness by introducing complementary non-retail uses.

Growth in Restaurant, Bars and the wider Café Culture

10

2.32 er

over the world.

Japanese sushi, Spanish tapas and Indonesian restaurants have joined the more

t

2.33 y Note found that in 2004 the usage of traditional branded

chains continued to decline despite their high profile in the market. Usage of the

t

r fast

ed

the UK’s and the world’s largest restaurant chain announced

that it would stop offering super size meals to help tackle obesity. Given these

n

• Busier working lifestyles - and the rising number of dual income families are

. As a result, eating out

has become a regular feature rather than a luxury of the working week. In fact,

f

ure

diversification - menu diversification and changes are now almost regular

features of most branded chains. Pub restaurants in particular have started to

In the UK the choice of restaurants is characteristically broad as a result of consum

willingness to adapt to new styles of eating and drinking from all

traditional curry houses. In addition, French, Italian and Greek restaurants can be

found in the majority of British towns. Frequent usage of restaurants is closely

correlated to social grade and income, with 83.6% of As and Bs visiting restaurants in

the evening in the last 12 months. Another important factor is whether both partners

in the household are working, which makes it practical and affordable to eat ou

regularly.

Research conducted by Ke

leading restaurant brand, Pizza Hut, decreased by 6 percentage points like mos

other chains, Brewer’s Fayre, Harvester, Little Chef, Beefeater etc recorded a lower

penetration than three or four years earlier. Since 2001, growth in the restaurant

meals market has been relatively slow as a result of the slow down in demand fo

food. This is due partly to market saturation, the obesity debate and the rise of

healthy eating values. Fast food chains are remedying this problem with improv

menus, and McDonalds,

initiative and rising consumer demand for eating out, Key Note forecasts that

between 2006 and 2008, growth in the restaurant meals market will remain betwee

5% and 5.9%. Key factors impacting upon growth in the future will include:

undoubtedly reducing the time available for hoe cooking

restaurants are targeting these cash rich/time poor customers

• Eating out as a leisure activity - for many customers, eating out is now part o

the leisure experience. The location of restaurant outlets has encouraged this

trend, for example it is common for these outlets to be situated close to leis

venues and cinema complexes. Eating out associated with travel is also on the

increase.

• Menu

introduce broader base menus and more frequent menu changes as a means of

maintaining customer interest in this increasingly competitive market.

11

• Greater choice of restaurants - new types of restaurant emerge regularly in

UK and often profit from the open minded nature of British with regard to food

and drink. Many cities and large towns now offer a wide range of culinary st

Key Note states that in 2004 the total UK restaurant meals market was worth £12.4

billion, a rise of 3.3% on 2003. Overall the market is expected to grow by 23%

between 2004 – 2008 to £15.25 billion. Between 1999 and 2008, Key Note for

that the value of the UK restaurant meals market will have grow by 49.2%. At 23%,

the growth forecast for the 5 years between 2004 – 2008 is faster than the in

the

yles.

2.34

ecast

crease

experienced in the previous five years, 17.4%.

2.35 Ano

alco

hote distinction

between a pub and a restaurant or café is likely to become even more blurred. For

ord e.

Ano

unli

rest US than in the UK, might use a new more liberal licensing regime to

move into the drinks market that is currently dominated by pubs

2.36 For

eati

As f young

adults aged between 18 and 35 have no problem finding employment and both

mor

cha

and eating out concepts such as tapas or sushi bars. This is partly derived from

for the

n

ther profound change taking place in the UK is the licensing of outlets selling

hol. This is likely to change the character of many outlets, such as pubs and

ls, which already play a major role in the eating out market. The

example, a pub could well consider moving into the market for take away food, in

er to provide customers with the option of having a drink and taking a meal hom

ther possibility is that the fast food majors which have traditionally been

censed in the UK, historically being attributable to alcohol being even more

ricted in the

ecasts for continuous growth in the restaurants market is based on the fact that

ng out has become a major element in the lifestyles of the younger generations.

a result of nearly a decade of economic growth in the UK, the majority o

partners are increasingly likely to work full time. This makes the eating out option

e attractive than ever. Restaurants in the UK will also continue to benefit from a

racteristic of the British – a willingness to experiment with new foods and drinks

foreign travel which is also increasing and expanding to new countries, making it

possible to introduce new styles of cuisine. This clearly has major implications

expansion of the restaurant and café industry within St Helens which has witnessed a

dramatic increase in the past five years.

The Growth in Electronic Commerce

2.37 Many consumers who previously shopped in town centres and retail parks are now

using the Internet for some of their purchases. This trend is set to continue, although

the exact impact that e-commerce will have on the high street has yet to be

established accurately. In 2001, total on-line sales in the UK were estimated at £4b

12

(Key Note, ‘E-Commerce’ September, 2002) which could rise by up to £7.5bn by

2005, an increase of 75%.

The most popular on-line purchases are currently books, CD’s, travel, food and

groceries, and computer products (Key Note, 2002). Technology is currently being

developed by companies such as Amazon that will allow on-line b

2.38

rowsing of books

which is likely to result in this sector making further in-roads into the on-line market.

2.39

2.40

etail units than before, as more is directed

to e-commerce. The effect of this will be to reduce spending growth and expenditure

e

2.41

of

tailing.

e

The clothing market has been slow to see the benefits of e-commerce with most

people still preferring to try on clothes prior to purchasing. Security concerns are also

still a major issue affecting all sectors of the market, with recent surveys suggesting

that 24% of people do not feel comfortable giving credit card out details over the

internet (Key Note, 2002).

The food and grocery market is also growing fast and some estimates suggest that

around 25% of the grocery market will be sold on-line by 2008 (The Institute of

Grocery Distribution, 2001).

As access to the Internet increases through digital televisions and mobile telephones,

proportionally less money will be spent in r

capacity. In turn, this will:

• Affect the investment decisions of existing retailers, and over time, further reduc

the demand for retail premises; and

• Lead to the creation of new ‘sui generis’ retail collection centres on the edges of

major conurbations. Experiments with 10,000 – 20,000 sq. m units are already

underway.

National Trends in Retail Trading Formats and Investment Planning policy has reduced out-of-centre development in recent years although

recent trends indicate an upsurge in retail warehouse development. Indeed, the

amount of retail warehouse park floorspace in the development pipeline at the end

2003 reached 2.7 million sq m. This was an increase of some 930,000 sq m the end

of 2000, although is almost 20% below the peak level in the 1990s. However, it is

significant to note that national planning policy (PPS6) intends to challenge the

format driven approach to re

2.42 However, the demand for retail warehouses remains strong although it is considered

that obstacles in obtaining planning permission restricted development in the lat

13

1990’s. Despite this, current completion levels are anticipated to remain at an annual

level of between 300,000 sq m (gross) to 350,000 sq m (gross). Figure 2.4 illustrates

e Parks in the Pipeline 1992-2003

the recent uplift in the amount of retail warehouse park floorspace that has been

coming forward.

Figure 2.4: Retail Warehous

0

0.5

3

3.5

1.5

2

2.5

1

Floo

rspa

ce (m

illio

n sq

m)

Proposed

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Year

With Planning ConsentUnder Construction

The total amount of floorspace in the shopping centre development pipeline reac

just over 5.4 million sq m (gross) by th

2.43 hed

e end of 2003. Town centre located schemes,

at 4.1 million sq m (gross), accounted for 75% of this total. This marks a significant

increase on the 1993 proportion, when town centre located schemes accounted for

just 64% of the development pipeline (Figure 2.5).

14

Figure 2.5: Change in Location of New Shopping Centre Floorspace 1992-2003

Figure 2: Change in Location of New Shopping Centre Floorspace, 1992-2003

67.964.2

67.7 70.4 73.382

85.991.8 90.4 90

85.8

75.4

32.135.8

32.3 29.6 26.718

14.18.2 9.6 10

14.2

24.6

0

10

20

30

40

50

60

70

80

90

100

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Year

Prop

ortio

n of

Tot

al S

hopp

ing

Cent

re

Deve

lopm

ent P

ipel

ine

(%)

Town CentreOut of Town Centre

However, it is significant to note that the proportion of out of town floorspace at the

end of 2003 (25%) is significantly higher than the low of only 8% at the end of 1999.

Clearly, Figure 2.5 highlights that a greater proporti

2.44

on of shopping centre

development is proposed/constructed at out of town locations, which is similar to the

position prior to 1996.

2.45 Therefore, both Figure 2.4 and Figure 2.5 indicate uplift in out of town development,

after a period where out of town development saw a downturn in development, most

notably between 1997 and 1999.

The St Helens Perspective

2.46 In order to understand the trends that have occurred in St Helens we have reviewed

information provided by Promis who examine retail development performance

throughout the UK. Figure 2.6 below illustrates the type of retail development that

has occurred in St Helen’s since 1993. From this information it is not surprising to

discover that St Helen’s has seen significant development in the retail warehouse

sector particularly since the turn of the century. In fact since the last study was

prepared, there has been significant development primarily focused at the

Ravenhead Retail Park, which is currently being extended.

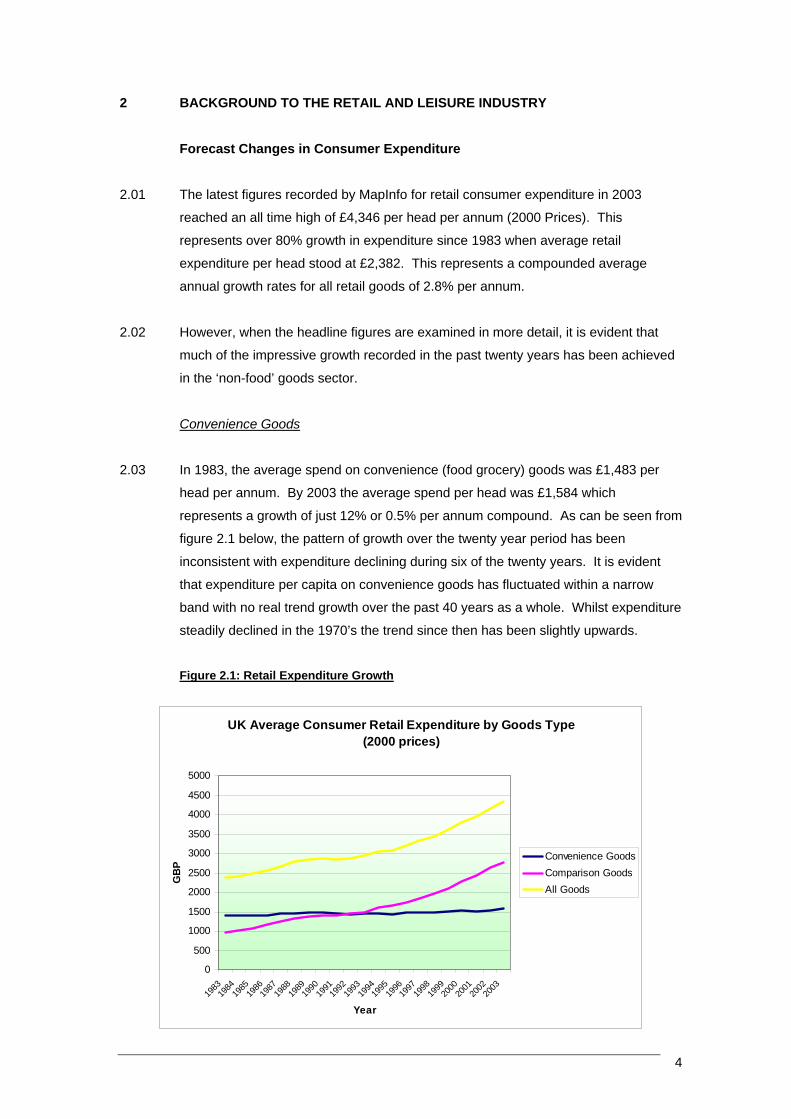

2.47 In 1993 St Helens Town Centre comprised approximately 80,825 sq m (870,000 sq

ft) of town centre floorspace (according to Promis). However, by 2004 this had

15

increased by 9,384 sq m (or 101,000 sq ft) to 90,209 sq m (or 971,000 sq ft)

representing an increase of 11.6%.

Figure 2.6: St Helens Comparison Floorspace (1993-2004)

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Sq.

ft (0

00's

)

Retail Warehousing

Tow n Centre

Source: Promis 2005

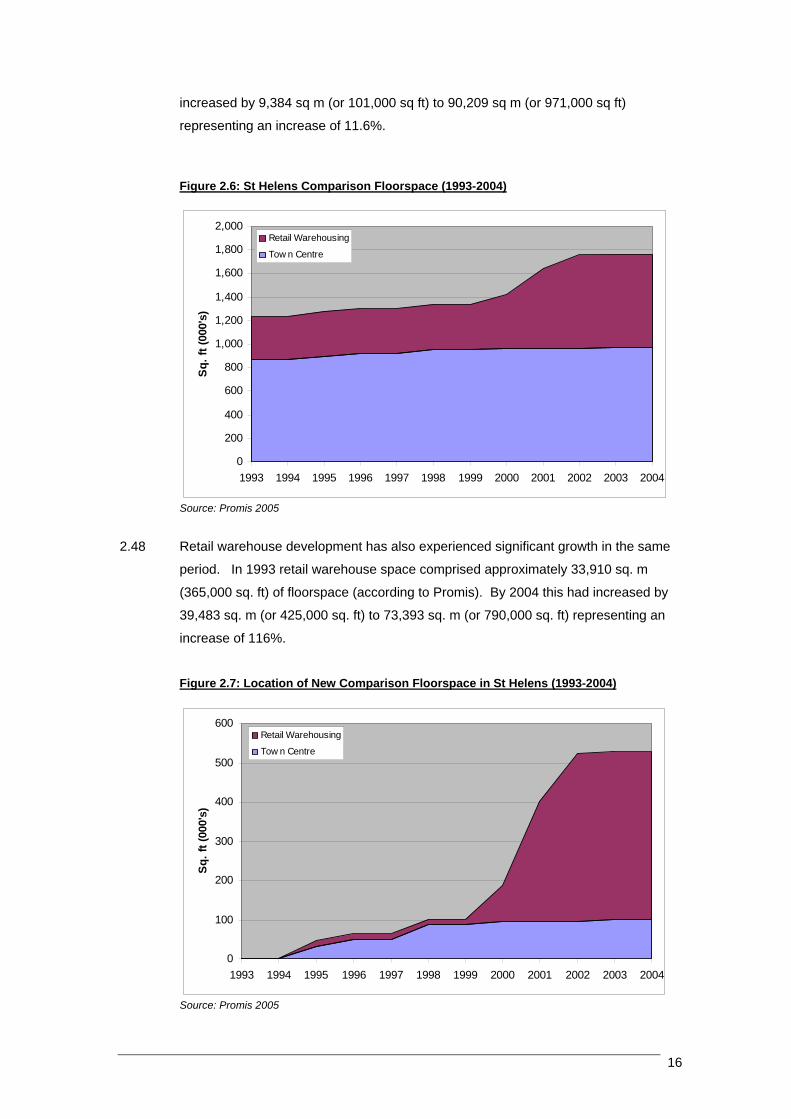

Retail warehouse development has also experienced significant growth in the same

period. In 1993 retail w

2.48

arehouse space comprised approximately 33,910 sq. m

(365,000 sq. ft) of floorspace (according to Promis). By 2004 this had increased by

igure 2.7: Location of New Comparison Floorspace in St Helens (1993-2004)

39,483 sq. m (or 425,000 sq. ft) to 73,393 sq. m (or 790,000 sq. ft) representing an

increase of 116%.

F

0

600Retail Warehousing

Tow n Centre

100

200

300

400

500

Sq. f

t (00

0's)

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Source: Promis 2005

16

2.49 of the

ver, by 2004 this had risen to 45%, an increase

of 50%. Therefore, it is not surprising to discover that 81% of all comparison goods

on-food) retail development that has occurred since 1993 has been retail

ionally and nationally.

In 1993 the total provision of retail warehousing in St Helen’s represented 30%

total retail floorspace provision. Howe

(n

warehousing confirming the trends that have occurred reg

17

3 PLANNING POLICY FRAMEWORK Introduction

Given that this study seeks to provide important background evidence that will a

in fu

3.01 ssist

the ture development of the LDF process, it is important at this stage to reflect

upon key policy advice and how the national guidance may impact upon the

development of policies locally. The key texts, which have been considered as part of

our study, include:

• Planning Policy Statement 6 ‘Planning for Town Centres’;

• Existing and emerging Regional Planning Guidance for the North West;

• The St Helens Unitary Development Plan

Planning Policy Statement 6 – Planning for Town Centres (March 2005) 3.02 Paragraph 1.3 of PPS6 notes that the Government’s key objective for town centres is

to promote their vitality and viability by:

• Planning for the growth and development of existing centres; and

• Promoting and enhancing existing centres, by focusing development in such

centres and encouraging a wide range of services in a good environment,

accessible to all.

These other objectives should be taken into account in the context of paragraph 1.3

these include:

• Enhancing customer choice by making provision for a range of shopping, leisure

and local services, which allow genuine choice to meet the needs of the entire

community, particularly social excluded groups

• supporting efficient, competitive and innovative retail, tourism and other sectors,

with improving productivity

• improving accessibility ensuring that existing or new development is or will be

accessible and well served by a choice of means of transport

3.03 In order to deliver the Government’s objectives, paragraph 2.1 notes that

development should be focused in existing centres in order to strengthen and, where

appropriate, regenerate them.

3.04 A positive and proactive approach to planning is encouraged by the guidance, with

paragraph 2.16 noting that local planning authorities should work in conjunction with

18

s ess the need for new floorspace for

re and other main town centre uses, taking into account both quantitative

tions.

ns. In deprived areas which lack access to a range of services will be clear and demonstrable benefits in identifying sites for

appropriate development to serve communities in these areas, additional weight should

3.06 tail development when preparing its

development plan documents, paragraph 2.34 notes that a local planning authority

ses of goods to be sold, within the broad ries of comparison and convenience goods…;

3.07 In tecon al planning department will be to provide for consumer choice by nsuring that:

vitality and viability of town centres and the application of the sequential approach, to improve accessibility for the whole community; and

3.08 The ragraph 2.36 that in addition to the above, other

s

be o

nsure

tion of the centre and its catchment. Appropriate

development should be located in the right type of centre to ensure that it fits and

takeholders and the community to, inter alia, ass

retail, leisu

and qualitative considera

3.05 In assessing the need and capacity for additional retail and leisure development,

paragraph 2.33 notes that: ‘local planning authorities should place greater weight on

quantitative need for additional floorspace for the specific types of retail and leisure developments. However, local planning authorities should also take into account of qualitative consideratioand facilities, and there

be given to meeting these qualitative deficiencies.’

In assessing quantitative need for additional re

should assess the likely future demand having a realistic assessment of:

• Existing and forecast population levels;

• Forecast expenditure for specific clascatego

• Forecast improvements in productivity in the use of floorspace.

rms of qualitative need, the guidance states at paragraph 2.35 that “a key

sideration for a loce

• An appropriate distribution of locations is achieved, subject to the key objective of promoting the

• Provision is made for a range of sites for shopping, leisure and local services, whichallow genuine choice to meet the needs of the whole community, particularly the needs of those living in deprived areas.”

guidance further states at pa

con iderations may be taken into account including the degree to which shops may

vertrading.

3.09 The guidance in paragraph 2.04 states that Local Planning Authorities should e

when selecting suitable sites for development that the scale of opportunities identified

are related to the role and func

compliments its role and function.

19

3.10

o consider a indicative upper limit for the scale of

development likely to be miscible in different types of centres.

3.11

ly

r

opment in

relation to the role and function of the centre; and then

e given to sites that are or will be well

• are or will be well served by

a high

likelihood of performing links with the centre.

3.12

propriate range of sites to allow the accommodation of the

ed, it also recognises that Local Planning Authorities should be flexible

operators. It is also re

term

3.13 n considering potential sites for allocation either in edge of centre or out of

ld

ment. In addition Local Planning Authorities should ensure that

locations are accessible when selecting appropriate sites for allocation. These

of

d

d congestion.

In terms of local centres, given their characteristics the guidance considers that it

would be inappropriate as a location for large scale new development. Therefore

Local Planning Authorities are t

PPS6 adopts the sequential approach to site selection whereby Local Planning

Authorities should select appropriate sites for allocation within identified centres

where identified need is to be met. All options in town centres should be thorough

assessed before less central sites are considered for development for town centre

uses. Paragraph 2.44 sets out the sequential approach required. A development

should be considered in the following order:

• First locations in appropriate existing centres where suitable site or buildings fo

conversion are, or are likely to become, available within the development plan

document period, taking account of an appropriate scale of the devel

• edge of centre locations with preferenc

connected to the centre; and then

out of centre sites with preference given to sites that

a choice of means of transport and which are close to the centre and have

When considering sites Local Planning Authorities should in consultation with

stakeholders identify an ap

identified ne

and realistic when drawing up such sites and should discuss this with developers and

cognised that Local Planning Authorities should have

appreciation for business models and should take into account business models in

s of scale, format, car parking provision and the scope for desegregation.

Whe

centre locations the statement also suggests that Local Planning Authorities shou

assess the impact that that potential development could have on identified centres

within the catch

should be

• Whether the site is or will be accessible or well served by a choice of means

transport, especially public transport, walking and cycling, as well as by car, an

• the impact on car use traffic an

20

Regional Planning Guidance for the North West (March 2003)

Regional Planning Guidance RPG13 (now RSS) for the Nort

3.14 h West provides the

broad development strategy for the period to 2016. Published in March 2003, the

uality

3.15 ich

tre management initiatives and other

strategies should “recognise the continued need to protect, sustain and improve the

io Cen

3.16 Poli within and on the edge of

st

3.17 commerce, residential, retail, helps redu

hemes

3.19 he

Retailing Chapter of the adopted UDP. The overall strategic approach which is

opping centre as shown on the Proposals Map and listed in Schedule 2 will be permitted, subject to there being no conflict with other Plan Proposals and

li

I. eak flows of traffic, including heavy

goods vehicles;

guidance seeks to develop the region in a sustainable way to ensure that the q

of life for residents, the business community and visitors will be maintained and

enhanced.

Policy EC8 relates to town centres, retail, leisure and office development, wh

states that development plans, town cen

reg n’s town and city centres, including the role of Manchester City and Liverpool Citytres as regional shopping centres”.

cy EC8 also notes the need to “encourage new retail…

exi ing defined town and city centre boundaries (primary shopping areas)”.

It is also noted in paragraph 5.40 that “incorporating mixed uses like business and

leisure and culture into developments in central areas to keep them alive both day and night, contributes to urban regeneration and

ces the need to travel”.

3.18 However, it states further that it is important: “that edge-of-centre mixed use sc

with a strong commercial element do not undermine the vitality or viability of nearby centres or the shopping facilities in rural areas”

The St Helens Unitary Development Plan

Policies relating to town centre developments and retailing are contained within t

identified in Policy S5 of part 1 of the UDP seeks to concentrate new retail

development within existing centres, an approach advocated at both the national and

regional level. In dealing with such development, Policy RET1 states that:

Retail development and associated service uses in, or immediately adjacent to, an established sh

Po cies and provided that, in particular, the following criteria are satisfied:

The site enjoys good access to the highway network and is capable of satisfactorily accommodating the estimated p

21

II. the layout provides adequate car parking, cycle parking and servicing tly located in

relation to public transport and pedestrian routes;

II

3.20

and Earlestown Town Centre. Fifteen other local shopping centres are

also identified within Schedule 2.

3.21

Any proposal for large scale retail development outside an existing centre will be

improvement of the urban areas and does not undermine the plan strategy;

the diversion of trade and/or deterrence of investment;

wn centre sites are available, followed by edge-of-centre sites, district and local centres;

nmental effects or undue loss of amenity to neighbouring residential areas and the surrounding locality;

g

.22 Whilst Policy RET2 requires the developer/applicant to apply a sequential approach

ore

recent advice set out in PPS6 highlighted above.

arrangements that comply with Policy GEN9 and is convenien

I. and the scheme will not result in harmful environmental effects or undue of loss of amenity to local residents.

In dealing with Policy RET1, the two main shopping centres identified are St Helens

Town Centre

Whilst the plan seeks to promote further retail and service development within

established centres, Policy RET2 provides a criterion based policy dealing with future

out of centre retail development. The policy states that:

considered against the following criteria:

I. it makes a positive contribution to the economic and environmental

II. it is not located within the Green Belt; III. it will not cause significant harm to the viability and vitality of any shopping

centre identified in Schedule 2 and shown on the Proposals map, or in adjacent authority areas, through

IV. it is readily accessible by both public and private transport; V. evidence that a sequential approach to site selection has been adopted which

demonstrates firstly, that no suitable to

VI. there is no significant harmful enviro

VII. the proposal will have good access to the highway network capable of satisfactorily accommodating the estimated peak flow of traffic, includinheavy goods vehicle, and provide adequate car parking and servicing (GEN9)l and

VIII. the effect on overall traffic patterns

3

to site selection, it is evident that the policy does not specifically require a

demonstration of ‘need’. Therefore, any future update of core policies relating to out

of centre retail development would have to include a criteria which reflects the m

22

3.23 rontages

and s as

they w .

3.24 Policy ps, restaurants and cafes and sets out a number

3.25 and vehicle hire services and again provides

3.26

ment in St Helens

can be improved in the future and that existing features of quality are retained. As

etween the security needs of the industry and the need to protect amenity. The

policy il will

require de

doors

3.27 In summa vel

will have t

importantly, PPS6 now requires local authorities to define a Primary Shopping Area

which is likely

UDP. Ho

reflect the In addition, it will also be

impor is a

clear disti

defin

Policy RET3 deals with amusement centres in the secondary and primary f

tates that whilst such centres are generally accessible in the secondary are

ill not be permitted in the primary shopping areas

RET4 deals with hot food sho

of criteria that have to be satisfied relating to local amenity, hours of opening and

traffic issues.

Policy RET5 deals specifically with taxi

a series of criteria that will need to be satisfied.

Finally Policy RET6 seeks to deal with the design of existing shop fronts and new

developments. The policy seeks to ensure that the built in environ

part of the policy, the Council recognise that there needs to be a balance struck

b

also deals with access for those with special needs whereby the Counc

signs to incorporate appropriate measures such as ramps, automatic

, hand rails etc. to facilitate access.

ry, it is evident that the development of future plan policy at the local le

o be updated to reflect the recent guidance issues in PPS6. More

to reflect the existing defined Central Shopping Area in the adopted

wever it will be important that the boundary of this area is reviewed to

definitions set out in Table 2 of annex A in PPS6.

tant to review the extent of the Prime Shopping Area to ensure that there

nction between the primary frontage and the primary shopping area as

ed in PPS6.

23

4. SSESSMENT OF VITALITY AND VIABILITY

his section of the report assesses the vitality and viability o

A 4.01 T f St Helens and Earlestown

town centres with reference to the indicators in PPS6, chapter 4.

T

.02 Town centres have an important role to play in any Borough. They form a focal point

fo

w ure, education and transport.

P e

im

lo

st

id

T .04 It is important that St Helens and Earlestown remain competitive with their neighbours

a

ce sses

an

m

ef

4.05 T

im

• They help to asses the success of retail policies in the existing St Helens Unitary

Development Plan and will assist in the formulation of appropriate policies in the

Unitary Development Plan when the plan is reviewed.

• They provide a starting point for any retail strategies that may be produced and will

assist with retail planning in St Helens and Earlestown;

• They provide useful base data that will facilitate a process of monitoring that can be

undertaken each year to asses how the town centres are performing over time;

• They allow positive and negative aspects of the town centres to be identified and

appropriate action taken;

he Importance of Town Centres

4

r the community and provide a wide range of services that are accessible to the

hole population including retail, employment, leis

4.03 lanning Policy Statement note 6 “Planning for Town Centres” (2005), emphasises th

portance of maintaining a “healthy” town centre as it helps to foster civic pride and

cal identity and can contribute towards the aims of sustainable development. It also

ates that by monitoring town centres on a regular basis, signs of decline can be

entified early on and remedial action can be taken.

he Purpose of the Health Check

4

nd continue to attract shoppers, visitors and businesses. To achieve this, the town

ntres must continually strive to build on their strengths, alleviate their weakne

d continually improve the facilities they provides to the community. Simply

aintaining the status quo is not an option. Successful town centres must respond

fectively to the changing needs and demands of its users.

he town centre health checks for St Helens and Earlestown serve a number of very

portant functions:

24

• They provide data that can be used to compare the performance of St Helens and

ers’ perception of the towns they allow schemes

and strategies to be drawn up to help improve the town centres for their users.

4.06

information gained on the key indicators that PPS6 ‘Planning for Town Centres’

-

• Retailer representation and intention to change representation;

• Proportion of vacant street level property;

4.07 een informed by a combination of desk top research, ‘on the

town centres and original survey work.

St Helen

4.08 athered as part of this study

riefly examined the findings of the Council’s previous St Helens Town Centre

a

that the town centre wa destination in the sub-

region, both in terms of its function and size. The Council consider its main competitors

b

4.09 The main conclusions of the 2001 report confirm that St Helens town centre shows sign

re

follo 1.

Earlestown town centres to other neighbouring centres in the region and therefore

to ensure that they remain competitive;

• By looking at retailers’ and shopp

These health checks, while focusing specifically on economic factors, also examine

other issues such as transport provision and the environment. They incorporate

suggest should be used to asses the health of town centres. These include:

• Diversity of uses;

• The amount of retail, leisure and office floorspace in edge-of-centre and out-of

centre locations,

• Shopping rents;

• Commercial yields on non-domestic property;

• Pedestrian flows;

• Accessibility;

• Customer views and behaviour;

• Perception of safety and occurrence of crime; and

• State of the town centre environment quality

The assessment has b

ground’ observations of the

s Town Centre Health Check 2001 and 2004

r to compare previous research with the evidence gIn orde

we have b

He lth Check undertaken in 2001 and reviewed in 2004. Overall, the Council found

s an important comparison shopping

to e Wigan and Warrington.

of latively good vitality and viability. In respect of some key indicators we note the

wing conclusions from 200

25

er of vacant units within the Central

Shopping Area, which had been vacant previously for three consecutive

%)

in the number of shops in the town centre, whilst there has been a rise in the

has

• Pedestrian surveys within the town centre indicate a relatively healthy volume

stributed around the town centre similar to patterns in previous

mained constant since 1994;

% since 1996 and

s in Wigan, Widnes, Runcorn and Salford;

eriod 1999/2000 to 2000/20001 by 15%;

hin the town centre by 20% between

espite robbery and violent crime against the person

ng spaces within the town centre has increased;

e has remained constant.

.10 Where possible comparisons have been made with the St Helens Retail and Leisure

.

T HELENS TOWN CENTRE

t Helen’s position within the Regional Hierarchy

4.11

oring system which takes account of each location’s

provision of multiple retailers and anchor store strength.

• Between 1999 and 2001 the Council found there had been a decline in the

number of vacant properties in the town centre by 26%;

• The Council found a fall in the numb

surveys;

• Between 1999 and 2001 the Council found that there has been a decline (-4

financial and professional services, food and drink establishments, private

offices and public buildings;

• The Council found that the number of multiples stores in the town centre

increased from 47 in 1996 to 59 by 2001;

of shoppers di

studies;

• Yields have re

• Zone A rent values for the town centre have increased by 43

outperform rent

• Increased planning application in the p

• Decline in the theft from motor vehicles wit

1999 and 2001, d

increasing;

• The total number of car parki

• The number of bus routes out of the town centr

4

Study 2000-2016 undertaken by WYG (previously MVM Planning Ltd) in March 2001

S

S

Table 4.1 below illustrates St Helens’s position within the hierarchy of town centres in

the surrounding area, by reference to the Management Horizons Europe’s UK

Shopping Index (2003/2004). This rank the top 1,672 shopping venues in the UK,

including town centres, stand alone malls, retail warehouse parks and factory outlet

centres, through a weighted sc

26

Figu 4re .1: The Sub-Regional Shopping Hierarchy

Ce rent Rank 2003-2004 Rank 2000-2001 Change in Rank

Manchester 2 3 +1 Liverp 14 13 -1 ool Southport 62 77 +15 W inarr gton 83 91 +8 St Helens 92 111 +19 Wigan 111 121 +10

Manageme

4.12 It can be se

ranked 92 it within the top 6% of all UK

sho

that the

Genera

4.13 St Hele ot Road), the A570

(Co r

4.14 The cen et,

Hardsh Barrow Street. The prime shopping frontage in addition to the

Chu

of B g y

two department stores, Marks and Spencer and T J Hughes. The Church Square

long Baldwin Street, Claughton Street, Westfield Street and Duke Street. These

st the

in

lpful as comparisons can be

made with other centres as well as national averages.

nt Horizons Europe: UK Shopping Index (2003/2004)

en that out of the 1,672 shopping venues surveyed nationally, St Helens isnd in the 2003-2004 period, which places

pping venues. During the 2000-2001 periods, St Helens was ranked 111th showing

centre has improved over the last two years.

l Description of St Helens Town Centre

ns Town Centre is formed at the junctions of the A58 (Presc

rpo ation Street) and the A571 (College Street/ King Street).

tre is focused on the pedestrianised area of Church Street, Market Stre

aw Street and

rch Square and Hardshaw Centre includes Church Street, Ormskirk Street and part

rid e Street. The Hardshaw Centre consists of a single storey mall anchored b

Shopping Centre comprises four interlinked arcades, which is anchored by Boots and

BHS and also contains a large indoor market. The centre extends further to the south

a

areas perform a more secondary role.

Diversity of Uses

4.15 Tables 4.2 and 4.3 below illustrate the retail composition of St Helens town centre at

2004 and 2000 in terms of outlet numbers and floorspace and compare it again

respective UK national averages for town centres. This is based on GOAD, the

boundary of which is attached in Appendix I. We note that the boundary is different

that previously adopted by Promis and will not also reflect the town centre boundary

the adopted UDP. However, the GOAD information is he

27

ntre, 2004Table 4.2: Retail Composition of St Helens Town Ce xperian Goad (2004)

Sector No. of Outlets

% of Outlets Floorspace (sq. m)

% of Floorspace

GB GB

Source: E

St Helens St Helens Convenience 38 10.6 9.3 21,024 23.2 16.9 Comparison 178 49.6 48.0 48,180 53.1 53.1 Service 110 30.6 31. 14,344 15.8 20.7 1 Miscellaneous 4 1.1 1.4 641 0.7 1.4 Vacant 29 8.1 10.3 6,494 7.2 7.9 TOTAL

Table 4.3: Retail Composition of St Helens Town Centre, 2000

359 100 100 90,683 100 100

Source: Experian Goad (June 2000) updated by MVM Planning (November 2000)

particularly strong. It

resented, with the proportion of

bove the national average (48.0%) and the proportion

ng at the national average. This has, however,

4.18

ared to 31.1% and

service floorspace amounts to 15.8% compared to 20.7%. The service sector in St

Sector No. of Outlets

% of Outlets Floorspace (sq. m)

% of Floorspace

St Helens Change 00-04

St Hele0

ns Change 0-04

Convenience 34 9.3 +1.3 15,190 17.1 +6.1 Comparison 192 52.6 -4.6 51,600 58.2 -5.1 Service 109 29.9 +0.7 15,120 17.1 -1.3 Miscellaneous 2 0.5 +0.6 290 0.3 +0.4 Vacant 28 7.7 +0.4 6,419 7.2 0 TOTAL 365 100 - 88,610 100 -

It can be seen that at 2004 the convenience sector in St Helens is4.16

has an above average number of units having 10.6% compared to the national average

of 9.3%. The proportion of convenience floorspace (23.2%) is also above the national

average (16.9%). Indeed, the centre has two large edge-of-centre foodstores: an Asda

at Kirkland Street and the former Safeway (now Tesco), at Chalon Way West along

with a Lidl which is located on the King Street Retail Park. Table 4.2 shows that the

convenience sector in St Helens has strengthened since 2000 in terms of both the

number of units (by 4 units or 1.3%) and the amount of floorspace (by 5,824 sq m or

6.1%).

The comparison sector at 2004 is also well rep4.17

comparison units (49.6%) being a

of comparison floorspace (53.1%) bei

declined since 2000 in terms of both the number of units (by 14 units or 4.6%) and the

amount of floorspace (by 3,420 sq m or 5.1%). This trend was identified by the Council

in the latest health check, where they found that the town centre had experienced a

decline in the number of shops between 1992 and 2002/03 of 15% (however, this did

not differentiate between food and non-food).

In contrast to the above, the proportion of service units and floorspace in St Helens is

below the national average. Service units amount to 30.6% comp

28

Helens has increased marginally since 2000 in terms of the number of units (by 1 unit

ce (by 776 sq m or 1.3%).

.19 erall, the retail t incr d from 365 units or 88,6 f

000 to units or 90,683 sq m in 2004.

.20 pected with a town of St Helen ze, the cen upports a b

s in add to retai St Hel as a num ultural ve

s rs from further afield. These

r Street, which comprises

a cinema, Chicago Ro ge and Pizza

Kirkland Street, the f Glass museum and art gallery a he Hilton Hotel at

art ib t. The centre also p

inistrat le as th cation for governmen gs and C l. In

s C occup large rtion of the central area.

.21 In light of the compa ith the ious MVM dy abo h examin e

s lso examined more

detailed information also be Experian in respect of key service facilities which were not

4.22

4: Service Composition of St Helens Town Centre, 2004

or 0.7%), but has declined in terms of the amount of floorspa

4 Ov sector in S Helens has ease 10 sq m o

floorspace in 2 359

4 As would be ex s’ si tre s road

variety of use ition ling. ens h ber of c nues

erving local residents in addition to attracting visito

include an entertainment complex on the Chalon Way / Wate

ck Café, Yates Wi

World o

ne Lod Hut, along with the

nd t

Lidl at

Linkway West, library and gallery on L rary Stree erforms an

important adm ive ro e lo t buildin ounci

addition St Helen ollege ies a propo

4 rison w prev stu ve, whic ed th

ummary data provided by Experian in 2000 and 2004, WYG have a

previously examined in St Helens in 2000.

The results set out in Figure 4.4 clearly show that when compared to the national

average St Helens is well provided for at 2004. The only identifiable deficiency is the

number of restaurants in the town centre. This contrasts with the fact that the town

centre is very well provided for with bars and public houses, with an above average

representation.

Table 4.

4.23

Sector No. of % of Outlets Floorspace (sq. Outlets m)

% of Floorspace

St Helens GB St Helens GB Fast Food Restaurants

19 4.35 4.61 1,347 1.17 2.22

Restaurants 12 2.75 4.24 2,192 1.91 3.26 Clubs 2 0.46 0.89 548 0.48 1.51 Cafes 10 2.29 2.66 957 0.83 1.28 Hotel and Quest Houses

4 0.92 0.52 3,400 2.96 1.62

Bars and Wine Bars

20 4.58 1.45 5,788 5.03 2.09

Public Houses 19 4.35 3.36 4,199 3.65 4.45 Retail Banks 11 2.52 2.74 3,437 2.99 3.41 TOTAL 97 21,868

When we compare these figures to the position at 2000 (Figure 4.5), it is evident that

the town centre has seen a marked increase in the number of fast food restaurants,

29

bars and wines bars and public houses.

Table 4.5: Service Composition of St Helens Town Centre, 2000

.24 This appears to support the conclusion reached by the Council whereby between 1992

other

4

and 2002/03 there was considerable growth in the number of food and drinking

establishments.

Retailer Representation

4.25 Table 4.6 illustrates the scale of St Helens retail offer at 2004 relative to

competing centres. Table 4.6: Scale of Retail Offer

Centre Convenience Floorspace (sq m gross)

Comparison Floorspace (sq m gross)

Service (sq m gross)

Total

Manchester 13,025 139,085 77,193 229,303 Liverpool 13,081 3 1108,61 29,840 51,534 Southport 22,548 70,318 27 120,830 ,964 Warrington 16,044 49,1 17,6 9 92 8 82,925 St Helens 21,024 48, 1 8180 4,344 3,548 Wigan 10,461 57,888 12,876 81,225

Source: Experian Goad (2 ). Notes: Total floorspa tes to con compariso servicee only, and exclud iscellane orspace cies and oth s.

4.26 tes that the size e retai or as a w St Helen reate

t and an, but han M ster, Live uth It can

b ver, t the co nce s in St Helens is particul strong

h rop n of floorspace tha st centre only exce being

Southport.

al

the

004 ce rela venience, n and floorspac es m ous flo , vacan er use

This table indica of th l sect hole in s is g r

han Warrington Wig less t anche rpool and So port.

e seen, howe hat nvenie ector arly

aving a higher p ortio n mo s, the ption

4.27 The presence of multiple retailers can greatly enhance the appeal of a centre to loc

consumers and investors. Other retailers in a centre can also benefit from

Sector No. of Outlets

% of Outlets Floorspace (sq. m)

% of Floorspace

St Helens Change 00-04

St Helens Change 00-04

Fast Food Restaurants

15 3.06 +1.29 1,208 0.9 +0.27

Restaurants 20 4.08 -1.33 2,796 2.09 -0.18 Clubs 0 0 +0.46 0 0 +0.48 Cafes 4 0.82 +1.47 836 0.62 -0.14 Hotel and Quest Houses

0 0 +0.92 0 0 +2.96

Bars and Wine Bars

8 1.63 +2.95 1,830 1.37 +3.66

Public Houses 16 3.27 +1.08 4,162 3.11 +0.54 Retail Banks 11 2.24 +0.28 3,948 2.95 0.04 TOTAL 74 100 14,780

30

increased pedestrian traffic generated by the presence of national multiples. However,

multiples also provide strong competition for rivals and over concentration may threaten

and local identity. An

approp alance bet en multiple ependents i e

national average fi the proportion of national multip n town centres is 34%

which is a useful benchmark in However, it should th

l are ex ed to c n a h than ave ortion ultipl

r lower o centres acteris lower lev footfall an ch ar

therefo e less attractive to ‘footloose’ multiple retailers.

.28 ere 1 multiple retailers (d as being f a netwo ine o

m outlets) in St Helens, occupying 46% of the total number of units in the centre

( d, 200 This inc 18 ‘k actors’ i. e retailers t likely

to improve the cons al of a cen cause strong br ding or

comprehensive product mix. These include: BhS, Boot the Chemist, Marks and

4.29 St Hele also has a good representation of independent units. The majority of these

ndary areas.

ness survey of St Helens found that 68.2% of retailers had plans to make

ithin the next year. Of those who were looking to make

changes, 7.5% noted that they were looking to relocate within the town centre, 12.5%

noted that they were lo te o 2.5 ooking to extend

floorspace, 15.2% were urbis rsp roportion

( that they were looking to clo noted t had no to

m ges to their .

4.31 T iness survey also indicated that most retailers in St Helens were tr ell

and just 7.7% felt that they were trading poorly. The survey further revealed that 52.2%

4.32

day/ tourist visitors (16.4%), high rents/ overheads (15.5%), lack of footfall

outside premises and poor security (9.5%), competition from other traders in St Helens

the independent sector in a town, undermining diversity

riate b we

gure for

s and ind s therefore d

les i

sirable. The

for compar g centres. be noted at

arger centre pect ontai igher rage prop of m e

etailers than rder char ed by els of d whi e

r

4 In 2004, there w

ore

66 efined part o rk of n r

Experian Goa 4). ludes ey attr e. thos mos

umer appe tre be of their an

Spencer, WH Smith, Woolworths, Mothercare, Next, New Look, McDonalds and

Superdrug.

ns

are located within the seco

Intentions to change Representation

4.30 The busi

changes to their businesses w

oking to reloca ut-of-centre, 1

h existing floo

% were l

looking to ref ace, and a small p

2.5%) noted se. 45% hat they intentions

ake chan business

he bus ading w

(41%) or moderately (41%). 10.3% of respondents felt that they were trading very well

of retailers felt that the performance of their businesses had improved over the last 5

years (52.2%), 17.5% had stayed the same, and 27.5% had declined.

The main threats felt by businesses were noted to be inadequate customer car parking

and lack of

(6.9%), poor quality of town centre shopping environment (6.0%), inadequacies of

31

current pitches and competition from other town centres (5.2%) and poor location of

premises (4.3%).

Retailer Requirements

Table 4.7 sets out retailer requirements within St Helens town centre as derived from

the Focus Database (October 2004).

4.33

lens Town Centre, 2004Table 4.7: Summary of Retailer Requirements within St He

Number of Minimum Maximum

Requirements Floorspace (sq. m)

Floorspace (sq. m)

Convenience 4 385 627 Comparison 21 5,605 11,436 Service 11 2,095 4,171 TOTAL 36 8,085 16,234

4.34

n in St Helens, with a total of 36 requirements listed. Retailers with

r simply not being actively marketed. Conversely a

Source: Focus Report (October 2004) - uses falling within specific retail trade categories from Experian Goad definitions It can be seen that there is a healthy level of demand from businesses seeking

representatio

current requirements include La Senza, Carphone Warehouse, Hobbycraft, Peacocks

stores.

Street Level Vacancies

4.35 The number of vacant units within a town centre can provide a good indication of how

the town centre is performing. However, care should be taken when interpreting

figures. Vacancies can occur for positive as well as negative reasons e.g. the opening

of a new retail centre elsewhere in a town may draw retailers from older properties or

more peripheral areas of the town. Vacant units will be found in even the strongest

town centre and are simply an indicator of the level of demand in a centre. For

example some properties may lay vacant because they are poorly maintained, unsuited

to modern retailing requirements o

low vacancy rate does not necessarily mean that a centre is performing well. For

example, if there is a proliferation of charity shops and other uses nor usually

associated with a town centre it may be a sign of decline, particularly where these uses

are located in prime locations. Despite these issues, it is still a useful indictor of

performance.

4.36 In 2004 there are 29 vacant units or 8.1% in St Helens town centre, which is

significantly below the national average of 11.3%. As a proportion of total floorspace,

vacancies account for 6,494 sq m or 7.2% which is also below the national average of

7.9%. Vacant units have increased marginally by 0.4% since 2000 when there were 28

vacancies amounting to 7.7%. Vacant floorspace has, however, increased only

32

moderately between 2000 and 2004. This is especially notable in the context of

previous reports undertaken by the City Council (2004), where the Council found that

during the period between 1992 to 2002/03 the number of vacant buildings increased

uld be noted that the Council’s definition of the town centre is

wider than that defined by Goad, as in 2002/03 the Council identified 69 vacant units,

.37 Table 4.6 below compares the vacancy count in St Helens town centre with other

tion of

s within the su

cancies in St Helens and other n y centres

by 188%. However, it sho

compared to Goad’s 29 in 2004.

4

nearby centres. It can be seen that St Helens town centre has the lowest propor

vacant unit b region.

Table 4.8: Va earb

Centre Vacant Units % Units Manchester 200 17.1 Liverpool 71 10.4 Southport 60 8.8 Warrington 46 11.6 St Helens 29 8.1 Wigan 80 18.0

Commercial Rents and Yields

.38 Zone A rents (the rental value of the first six metres depth of floorspace in retail units

4.39 town

Source: Experian Goad (2004).

4

from the shop window) reflect retailers’ perception of the town centre. As retailers

consider rent to reflect the margin between turnover and operational costs (plus

profit), the better the trading prospects the higher the rent that the operator will be

willing to pay.

Table 4.9 below records the changes in prime pitch Zone A rents in St Helens

centre over the period relative to other centres in the sub-region.

Table 4.9: Prime Pitch Zone A Rents (£/ sq m)

Centre June ‘96

June ‘97

June ‘98

June ‘99

June ‘00

June ‘01

June ‘02

June ‘03

June ‘04

Manchester 1,938 2,153 2,960 3,231 3,231 3,014 3,014 3,231 3,231 Liverpool 1,668 1,884 2,045 2,691 2,691 2,691 2,853 2,960 2,960 Southport 1,023 1,023 1,076 1,184 1,184 1,076 969 915 861 Warrington 1,023 1,130 1,130 1,184 1,399 1,507 1,560 1,560 1,560 St Helens 753 807 914 969 1,076 1,076 1,076 1,076 1,076 Wigan 753 753 753 753 807 915 915 969 969

e

4.40

s a

Source: Focus Town Centre Reports, October 2004 based on Colliers CRE’s opinion of open market ZonA rents

It can be seen that Zone A rents in St Helens have increased steadily between June

1996 and June 2000 increasing from £753/ sq m to £1,076/ sq m. This indicate

33

strengthening of the perceived trading prospects of the centre. Since this time,

levels have remained static reflecting the relatively stable position in terms of the

town centre.

Rental levels in St Helens at June 2004 are higher than Southport and Wigan, but

lower than Manchester, Liverpoo

rental

4.41