Embed Size (px)

Citation preview

When $#@! happens

Tim Sanderson – Senior Technical Manager

November 2014

This presentation is given by a representative of Colonial First State Investments Limited AFS Licence 232468, ABN 98 002 348 352 (Colonial First State). Colonial First State Investments Limited ABN 98 002 348 352, AFS Licence 232468 (Colonial First State) is the issuer of interests in FirstChoice Personal Super, FirstChoice Wholesale Personal Super, FirstChoice Pension, FirstChoice Wholesale Pension and FirstChoice Employer Super from the Colonial First State FirstChoice Superannuation Trust ABN 26 458 298 557 and interests in the Rollover & Superannuation Fund and the Personal Pension Plan from the Colonial First State Rollover & Superannuation Fund ABN 88 854 638 840 and interests in the Colonial First State Pooled Superannuation Trust ABN 51 982 884 624.

The presenter does not receive specific payments or commissions for any advice given in this presentation. The presenter, other employees and directors of Colonial First State receive salaries, bonuses and other benefits from it. Colonial First State receives fees for investments in its products. For further detail please read our Financial Services Guide (FSG) available at colonialfirststate.com.au or by contacting our Investor Service Centre on 13 13 36.

All products are issued by Colonial First State Investments Limited. Product Disclosure Statements (PDSs) describing the products are available from Colonial First State. The relevant PDS should be considered before making a decision about any product. Stocks referred to in this presentation are not a recommendation of any securities.

The information is taken from sources which are believed to be accurate but Colonial First State accepts no liability of any kind to any person who relies on the information contained in the presentation.

This presentation is for adviser training purposes only and must not be made available to any client.

This presentation cannot be used or copied in whole or part without our express written consent.

© Colonial First State Investments Limited 2014.

Disclaimer

What we’ll cover...

Planning implications of…

Redundancy

Divorce

Redundancy

Check employer payment summary - components and taxation

Non - termination payments Annual leave: Maximum tax 32%Long service leave accrued after 15/8/78: Maximum tax 32%

Termination payments Includes golden handshakes, severance pay, unused sick leave, rostered days off, payments in lieu of noticeCalculate tax free component: $9,246 plus $4,624 for every year of completed service

Remainder taxed as an employment termination payment

Redundancy

Check ETP taxationIt’s complicated, need to consider

ETP capWhole of income cap

Important to calculate as amount withheld by employer may not be the final tax payable

Refer to FirstTech “Termination Payment Essentials” or call FirstTech to determine ETP taxation

Redundancy

ETP cap $185,000

Over age 55: 17%

Under age 55: 32%

49%**

*including Medicare Levy**uncertainty over 2% deficit levy

Whole of income cap does not apply to ETPs paid due to genuine redundancy (excluded) Only have to worry about ETP cap

Genuine redundancy = amount paid in addition to the amount payable if left employment voluntarily

Redundancy

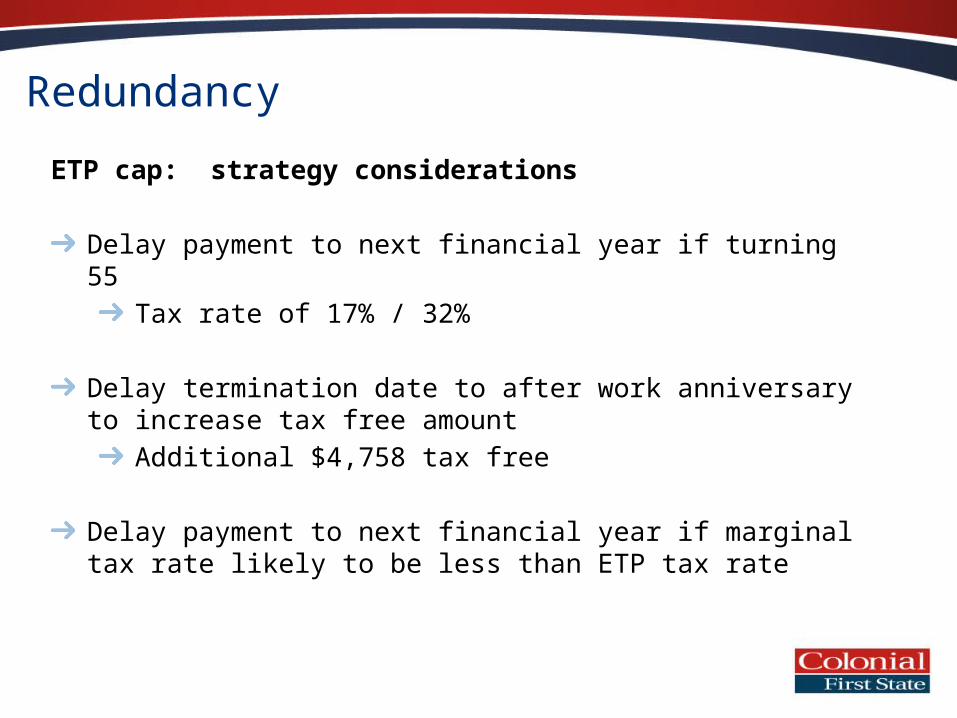

ETP cap: strategy considerations

Delay payment to next financial year if turning 55Tax rate of 17% / 32%

Delay termination date to after work anniversary to increase tax free amount

Additional $4,758 tax free

Delay payment to next financial year if marginal tax rate likely to be less than ETP tax rate

Redundancy

*including Medicare Levy**uncertainty over 2% deficit levy

Need to consider both “whole of income cap” and “ETP cap” where termination payment includes:

Genuine redundancy, and Other ETP amounts

Other ETP amounts include:Amounts that would have been paid if voluntarily terminated employmentEx gratia payments

Non

-exclu

ded

ETP

ETP cap $185,000

17% / 32% 49%

Whole of income cap $180,000

49%

49%

Redundancy

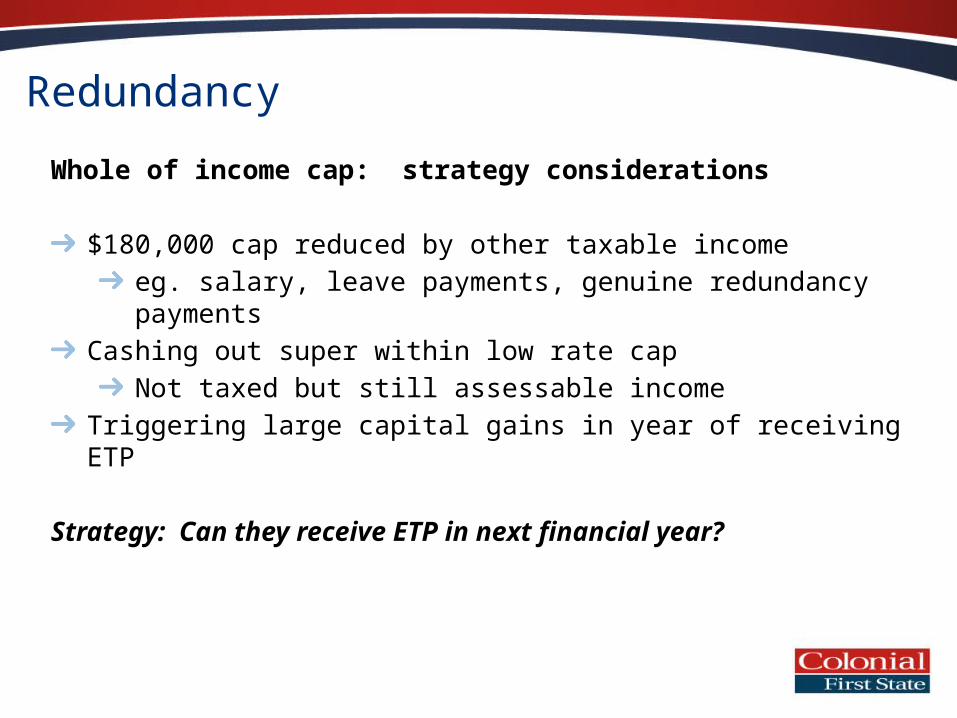

Whole of income cap: strategy considerations

$180,000 cap reduced by other taxable income eg. salary, leave payments, genuine redundancy payments

Cashing out super within low rate capNot taxed but still assessable income

Triggering large capital gains in year of receiving ETP

Strategy: Can they receive ETP in next financial year?

Redundancy

Example: timing receipt for whole of income cap

Chris: aged 40 with 10 years of service

Made redundant on 1 June 2014Genuine redundancy payment of $100,000

$55,486 tax free, $44,514 included in ETPEx Gratia payment of $130,000

Salary in 2013/14: $140,000Salary in 2014/15: $80,000

Redundancy

1. Receive everything in 2013/14$180,000 whole of income cap reduced by:

Salary $140,000Redundancy $44,514

Ex gratia payment of $130,000 above whole of income capTaxed at 49% ($63,700)

2. Receive ex-gratia in 2014/15$180,000 whole of income cap reduced by:

Salary $80,000Ex gratia payment of $130,000 received when $100,000 remaining cap $100,000 taxed at 32%, $30,000 taxed at 49%$46,700 tax overall ($15,000 saving)

Redundancy

Leave payments, ongoing or lump sum

Compare taking leave payments where redundancy: ongoing versus lump sum

Strategy: Receiving payments ongoing can assist in delaying termination payments to next financial year

Ongoing leave Lump sum leave

SG payable Maximum tax 32%

Accrues further leave

Taxed at MTR

Potentially salary sacrifice

Redundancy

Should they contribute to super?

Accessibility. Will they be able to access their funds if required?TTR?

Are they a member of an employer super fund and have to rollover as they have left employment?

If yes, review insurance cover

Strategy: contributing to super reduces assessable income & assets under pension age for Centrelink

Redundancy

Watch out for Div 293 tax

Additional 15% tax on concessional contributions by high income earners (income over $300,000)

Employer ETPs and leave payments included in income calculation

Tax bill won’t be received until after lodge tax returnMaximum additional tax 15% x $35,000 = $5,250

Strategy: Division 293 tax may be reduced by receiving payments over 2 financial years

Redundancy

Should client repay debt?

General rule is to pay off non-deductible debt first

Be careful not to close credit cards as may have trouble accessing credit in future if does not find employment

Accessibility – can they get access to funds if used to repay debt?

Strategy: Certain debt repayment may assist with Centrelink income and assets tests

Redundancy

Debt repayment example

Michael is 49yo and received a redundancy paymentHe has outstanding debt against his home and is considering reducing the debt by $50,000

If Michael places the funds in a mortgage offset account$50,000 will be an assessable asset and deemed

If Michael repays his outstanding line of credit against his home

$50,000 is not assessable as reduces debt against an exempt asset

Redundancy

Centrelink liquid assets waiting periodApplies to Newstart, Austudy and Sickness AllowanceLiquid assets exceeding $10,000 for couples or $5,000 for singlesDivisor $500 for singles or $1,000 for couplesMaximum 13 weeksLiquid assets include cash, bank accounts, shares and managed funds

Strategy: LAWP can be reduced by making one voluntary payment on a debt since becoming unemployed. Debt cannot be related to the principal home and must be voluntary (ie. more than minimum payment)

Redundancy

Example: voluntary non-housing debt repayment

Paula (single) has liquid assets of $10,000Credit card debt $3,000

Effect of Paula paying off her credit cardLiquid assets reduce to $7,000LAWP = $7,000 - $5,000 / $500 = 4 weeks

Liquid assets waiting period reduces from 10 weeks to 4 weeks

Redundancy

Centrelink income maintenance period

Applies to Newstart, widow allowance, sickness allowance, parenting payment and DSPIncludes lump sum leave payments such as annual, long service and redundancy paymentsDuration: number of weeks of leave payments + number of weeks of redundancy (eg. 2 weeks for every year of service) + number of weeks golden handshake represents (divide payment by weekly wage)

Strategy: If leave is taken as a lump sum prior to redundancy, it will not be assessable income once employment ceases for Centrelink.

Redundancy

Example: how income maintenance period works

Laura terminates employment and receives3 weeks unused annual leave6 weeks unused long service leave8 weeks redundancy (2 weeks pa over 4 years)$10,000 ex gratia payment

Gross weekly income while working was $1,200

Redundancy

Example: how income maintenance period works

Calculation of IMP3 weeks unused annual leave +6 weeks unused long service leave +8 weeks redundancy payment + 8 weeks ex gratia payment

$10,000 / $1,200

Laura would have $1,200 per week counted as income for 27 weeks from the date her termination payment is paid.

Divorce

Step 1: separation

Close joint accountsGet a copy of all financial statementsCreate a new budget

Rent on new residence (if applicable)Change name on utility billsReview debts

Are any debts in joint names?Be careful not to close credit cards as non-working spouse may have difficulty accessing credit

Divorce

Centrelink assessment on separation

Partner who moves out of principal residence - non-homeowner

If home jointly owned, 50% of market value assessableNon-homeowner allowance asset threshold $348,500If they subsequently buy a house may assist but this may not be possible until property settlement

Partner who remains in the principal residence - homeownerAdvantaged for Centrelink purposes where home value exceeds $146,500

Other income and assets assessable depending on whose name its in

50% for jointly held assets

Divorce

Centrelink: Widow allowancewoman born on or before 1 July 1955widowed, divorced, or separated since turning 40no recent workforce experience

employment of 20 hours or more a week for 13 weeks during the last 12 months.

allowance income and assets testincome must be less than $999.00pfassets must be less than $202,000 homeowners or $348,500 non homeowners

Maximum $515.60pf

Divorce

Case studyJohn and Glenda separated 2 months agoJohn is 58 and working fulltime whereas Glenda age 57 ceased work 18 months ago

Assets Glenda’s shareHome (jointly owned) $700,000 $350,000Contents (jointly owned) $ 10,000 $5,0002 cars (jointly owned) $25,000 $12,500Savings account (Glenda) $12,000 $12,000Savings account (John) $16,000 -TOTAL $379,500

Divorce

Case studyGlenda’s assets of $379,500 exceed the non-homeowner asset limit of $348,500

not eligible for an allowanceOnce the property settlement is finalised and Glenda receives cash of $350,000 she can either

purchase a home or contribute to superannuation

Divorce

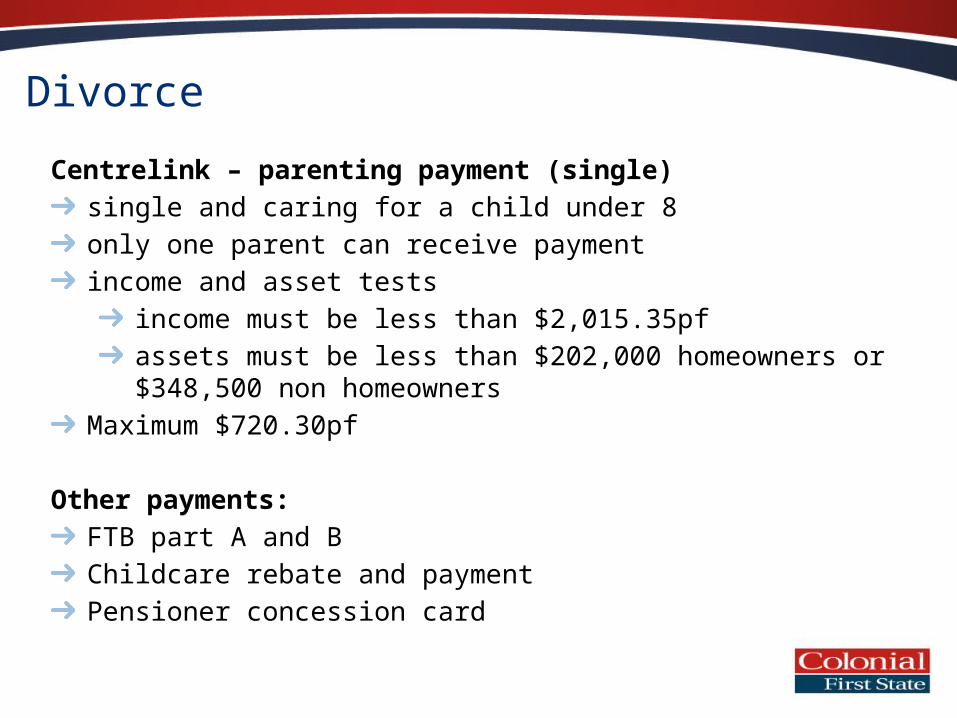

Centrelink – parenting payment (single)single and caring for a child under 8only one parent can receive paymentincome and asset tests

income must be less than $2,015.35pf assets must be less than $202,000 homeowners or $348,500 non homeowners

Maximum $720.30pf

Other payments:FTB part A and BChildcare rebate and paymentPensioner concession card

Divorce

Child supportMust obtain child support agreement if receive more than base rate FTB part AChild support reduces FTB part A by 50c in the dollar above the maintenance free area $1,522.05 plus $507.35 for each additional child

Child support formula:both parents' incomes are considered a self-support amount is deducted from each parent's income the percentage of care each parent provides is taken into accountchildren from first and subsequent families are treated in a similar way

Divorce

Child support – children aged 12 and younger

Parents' combined child support income 1 child 2 children

$0 to $35,285 17c for each $1 24c for each $1

$35,286 to $70,569 $5,998 plus 15c for each $1 over $35,285

$8,468 plus 23c for each $1 over $35,285

$70,570 to $105,854 $11,291 plus 12c for each $1 over $70,569

$16,583 plus 20c for each $1 over $70,569

$105,855 to $141,138 $15,525 plus 10c for each $1 over $105,854

$23,640 plus 18c for each $1 over $105,854

$141,139 to $176,423 $19,053 plus 7c for each $1 over $141,138

$29,991 plus 10c for each $1 over $141,138

$176,423 and over $21,523 $33,520

Divorce

Binding financial agreementWritten agreement for splitting assets if relationship ends

Legally binding on the spouses if:both have a copyboth have received independent legal advice (rights, advantages/disadvantages)both have signedhas not been terminatedhas not been set aside by the Court

Can only be set aside by the Court due to fraud, non-disclosure or unconscionable conduct

Divorce

Court ordersRequire leave of court if not brought about within:

12 months from divorce2 years from the end of a de facto relationship

Consent orderAgreement between spouses, then approved by CourtMust be just and equitable

Financial orderContested settlement where court makes a decisionMust be just and equitable

Court orders are binding on the couple

Divorce

Superannuation

Determine income needs now and in retirementDetermine lump sum required to meet income needsDetermine lump sum tax and preservationAdvise on appropriate superannuation fund for non-member spouseReview binding nominations – nomination to spouse still valid when separated but not divorced

Divorce

Superannuation

Legal process

Method

Court Order

FlaggingSplitting

Interest SplitPayment Split

Pension paymentsLump sum payments

Puts ‘stop’ on withdrawals and rollovers prior to

condition of release

New account for non-member

spouse

Each payment is split as it is made

Superannuation Agreement

Divorce

Splitting for non-member spouse

Adviser role – advise on most appropriate new superannuation arrangement

Create new interest

Payment of lump sum If UNPB or condition of release

Transfer to other fundSpouse

Non-member spouse

Non-memberspouse

Divorce

Superannuation: tax and preservation

Member benefits reduced by splitting payment

Everything is proportionaltax componentspreservation

Any preserved amount transferred would remain so until the receiving spouse satisfies a condition of release

If access to super is an issue for one spouse (eg, because of a difference in ages), this could be dealt with through a binding financial agreement

Divorce

Example: Duncan is splitting 30% of his super balance to Julia

Tax components Duncan (existing) Julia (new) Duncan (new)

Tax free component

$100,000 $33,333 $66,667

Taxable component

$200,000 $66,667 $133,333

Preservation Duncan (existing) Julia (new) Duncan (new)

UNP $20,000 $6,667 $13,333

RNP $5,000 $1,667 $3,333

Preserved $275,000 $91,667 $183,333

Divorce

Property settlement - transferring assets CGT relief

CGT rollover relief applies where an asset is transferred due to a binding financial agreementMust be transferred as a result of the relationship breakdownReceiving spouse inherits the original cost baseCGT on eventual sale should be taken into account when determining the property settlement