Embed Size (px)

Citation preview

4/12/2016

1

Patti Schroeder, Finance Support Director at

Iowa Association of School Boards (IASB)

and Iowa ASBO member

Information you can use to address Internal Control within your school district.

Introduction to Iowa’s booklet: Segregation of Financial Duties in the Smaller Public School to Improve Financial Internal Controls. (Iowa’s story)

SBO/CFO/Entity requests

DOE/Federal Government

Audit Reports

Insurance

Fraud cases

4/12/2016

2

Many, many audits have segregation of duties comments:

Cash Wire Transfers Receipts Disbursements Payroll School Lunch Program Financial Reporting

When segregation of duties cited, it is always labeled as a:

Material weakness

That is, internal control is weak, misstatements could occur and not be detected and corrected in a timely basis

Insurance companies have had a huge amount of bond losses, due in large part to lack of proper segregation of duties.

As a result, Iowa insurers will not increase any bond limits on any Iowa school until proper segregation of duties has occurred.

Proper segregation of duties will only be increased

once improper segregation of duties no longer appears as a material or significant finding on a school district’s audit.

4/12/2016

3

School District: Two losses from same occurrence, one an employee theft loss for $510,000 and the other a faithful performance loss for $500,000. Business office supervisor deposited checks received into an unapproved checking account and numerous unapproved CD’s that were opened by and controlled by the thief. District officials had no knowledge of the checking account or CD’s. Insured suffered total loss of more than $1,200,000.

Insurance Carrier said:

This loss largely caused by inadequate segregation of duties, little internal controls, poor documentation of checks received by the district, and inadequate supervision by supervisor (District Treasurer).

Setting An Employee Dishonesty Limit

The Surety Association of America, an organization which compiles

employee dishonesty premium and loss data, has published a guide to help

select minimum bond limits. It is worth using this as a guide when your

district is selecting an employee dishonesty limit.

“Exposure factor = 20% of current assets plus 10% of annual revenue.

The principal current asset of a school district is cash.

Example: $ 2,000,000 cash in the bank

$25,000,000 in annual revenues

Exposure factor = (.2 x 2,000,000) + (.10 x 25,000,000) = $2,900,000.

An exposure factor of $2,900,000 results in a minimum bond limit in the

$200,000 to $300,000 range.

8

9

4/12/2016

4

Undeposited collections

Unauthorized cash withdrawals

Set up separate bank account, diverted district funds: • From summer softball camps • From the football program

Made personal expenditures from bank account

Charged personal purchases to district issued procurement card

Paid out unauthorized (perhaps unincurred) overtime

“Her bosses made it easy.”

“Maybe we were naïve in counting on one person to look after the accounts.”

Without that documentation, you can’t tell specifically what was purchased.”

61% - undeposited collections

55% - improper purchases from vendors

37% - payroll / extra pay

31% - improper reimbursements

21% - improper credit card payments or

purchases

14% - cash withdrawals

Mary Mosiman, CPA, Iowa Auditor of State

4/12/2016

5

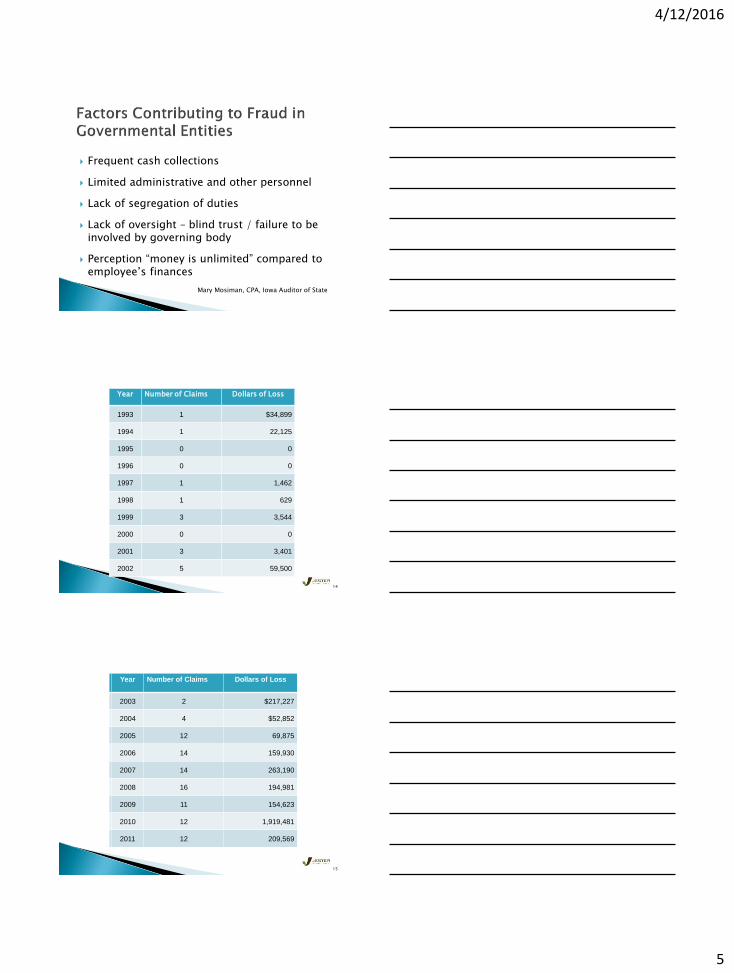

Frequent cash collections

Limited administrative and other personnel

Lack of segregation of duties

Lack of oversight – blind trust / failure to be involved by governing body

Perception “money is unlimited” compared to employee’s finances

Mary Mosiman, CPA, Iowa Auditor of State

Year Number of Claims Dollars of Loss

1993 1 $34,899

1994 1 22,125

1995 0 0

1996 0 0

1997 1 1,462

1998 1 629

1999 3 3,544

2000 0 0

2001 3 3,401

2002 5 59,500

14

Year Number of Claims Dollars of Loss

2003 2 $217,227

2004 4 $52,852

2005 12 69,875

2006 14 159,930

2007 14 263,190

2008 16 194,981

2009 11 154,623

2010 12 1,919,481

2011 12 209,569

15

Year Number of Claims Dollars of Loss

2003 2 $217,227

2004 4 $52,852

2005 12 69,875

2006 14 159,930

2007 14 263,190

2008 16 194,981

2009 11 154,623

2010 12 1,919,481

2011 12 209,569

4/12/2016

6

Year Number of Claims Dollars of Loss

2012 9 $183,820

2013 16 $107,459

2014 15

$ 96,622

2015 7 $ 24,669

16

No single person should have control over two or more phases of

a task, process or transaction

OR another way to say that is…

More than one person should be required to complete any task

17

Greater accuracy

Find errors quickly

Deter mismanagement/fraud

Provide checks & balances

Protect DISTRICT and SBO/CFO!

4/12/2016

7

Access

(to Assets)

Custody, control or handling of asset : • Cash; checks; receipts; deposits; credit cards; safes;

lock boxes • Equipment; receipt of new purchases; inventories • Paychecks /vendor checks - printing or distribution

Authorization

Reviewing and approval of task or transaction or operation such as approval of:

• Bank account adjustments or transfers; • purchase orders or requisitions; • use or disposition of an assets; • changes in pay or benefits; • timesheets or leave requests; • change orders; • IT programming changes; • adjusting journal entries

Accounting • Creating or maintaining records, such as cash

receipts, requisitions • Maintaining inventory records

19

RECONCILIATION RECONCILIATION RECONCILIATION RECONCILIATION

Comparison or review of transactions:

• Timely bank reconciliations

• Surprise petty cash counts

• Timely review of IT edits – new employees; benefits; new vendors

• Comparison of goods received to what was ordered

• Payroll and benefit reconciliations

• Physical inventory and reconciliation

• Comparison of accounting records to reports

• Analytical review 20

1. Drafted “best practice” templates on segregation of duties for a:

One person Business Office Two person Office Three person Office

2. Then asked Committee of “Auditor-types” to review, provide suggestions… but not bless.

4/12/2016

8

Member School District

Johna Clancy Gilbert (now Indianola)

Jill Gavin Martensdale-St. Marys

Sue Huls Sigourney

Patti Schroeder Iowa Assn. of School Boards

Shonna Trudo Van Meter

Member

Organization/School District

Pam Bormann Andy Nielsen

Iowa State Auditor’s Office

Mary Babinet Nolte, Cornman & Johnson, PC

Kevin Baccam Southeast Polk Schools

Ryan Eidahl Saydel Schools

Kristy Weiss Northeast Schools

Access

Authorization Accounting

(Reconciliation)

Duty/

Transaction Step

Person(s)

Responsible for Duty/Step

4/12/2016

9

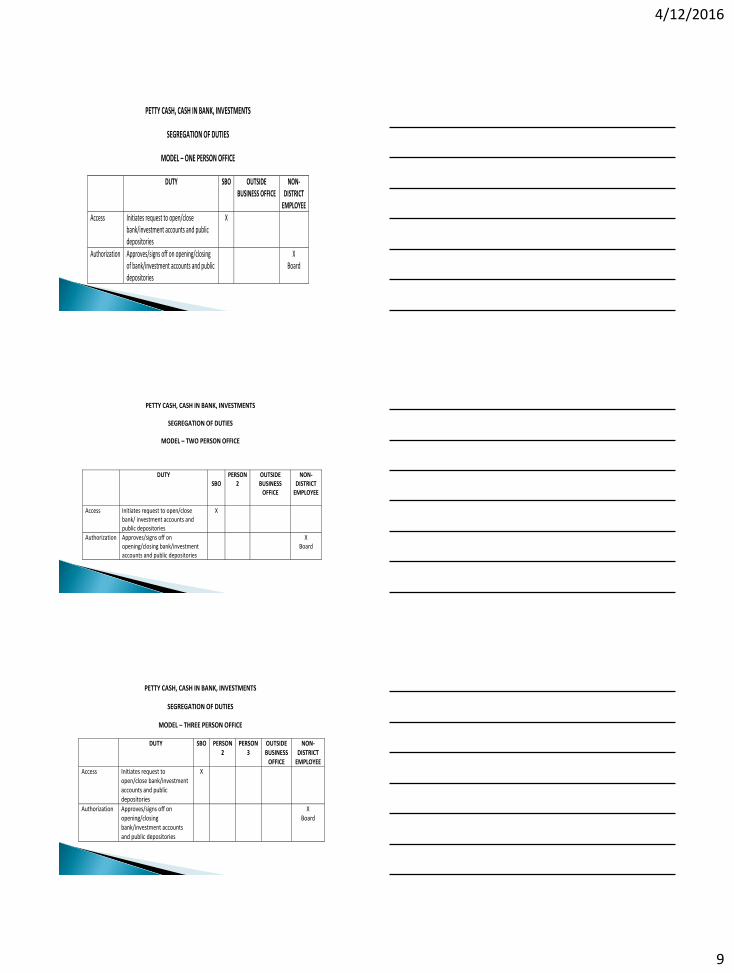

PETTY CASH, CASH IN BANK, INVESTMENTS

SEGREGATION OF DUTIES

MODEL – ONE PERSON OFFICE

DUTY SBO OUTSIDE BUSINESS OFFICE

NON-DISTRICT

EMPLOYEE

Access Initiates request to open/close bank/investment accounts and public depositories

X

Authorization Approves/signs off on opening/closing of bank/investment accounts and public depositories

X Board

PETTY CASH, CASH IN BANK, INVESTMENTS

SEGREGATION OF DUTIES

MODEL – TWO PERSON OFFICE

DUTY SBO

PERSON 2

OUTSIDE BUSINESS

OFFICE

NON-DISTRICT

EMPLOYEE

Access Initiates request to open/close bank/ investment accounts and public depositories

X

Authorization Approves/signs off on opening/closing bank/investment accounts and public depositories

X Board

PETTY CASH, CASH IN BANK, INVESTMENTS

SEGREGATION OF DUTIES

MODEL – THREE PERSON OFFICE

DUTY SBO PERSON 2

PERSON 3

OUTSIDE BUSINESS

OFFICE

NON-DISTRICT

EMPLOYEE

Access Initiates request to open/close bank/investment accounts and public depositories

X

Authorization Approves/signs off on opening/closing bank/investment accounts and public depositories

X Board

4/12/2016

10

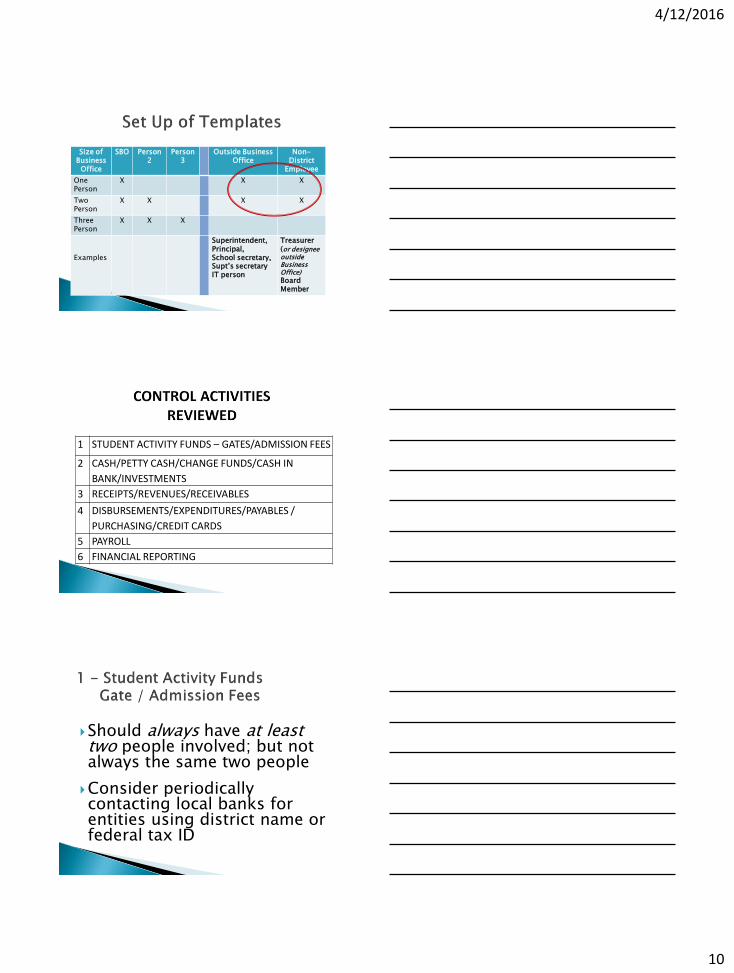

Size of Business

Office

SBO Person 2

Person 3

Outside Business Office

Non-District

Employee

One Person

X X X

Two Person

X X X X

Three Person

X X X

Examples

Superintendent, Principal, School secretary, Supt’s secretary IT person

Treasurer (or designee outside Business Office) Board Member

1 STUDENT ACTIVITY FUNDS – GATES/ADMISSION FEES

2 CASH/PETTY CASH/CHANGE FUNDS/CASH IN

BANK/INVESTMENTS

3 RECEIPTS/REVENUES/RECEIVABLES

4 DISBURSEMENTS/EXPENDITURES/PAYABLES /

PURCHASING/CREDIT CARDS

5 PAYROLL

6 FINANCIAL REPORTING

Should always have at least two people involved; but not always the same two people

Consider periodically contacting local banks for entities using district name or federal tax ID

4/12/2016

11

Who receives bank statements and performs bank reconciliation is crucial!

Let bank(s) know who is authorized to do what – insist on dual authorization of all bank/wire transfers

Consider “citizen” Treasurer

All checks should be stamped immediately “For Deposit Only”

Initial listings of receipts should be made before cash/check is handed off to another person and matched to deposit

Limit the number of staff with ability to authorize purchases and/or credit card charges.

Authorization should be separate from ordering and receipt of goods and services.

Limit access to credit cards to only the authorized holder/user of the credit card.

Who receives bank statements and performs bank reconciliation is crucial!

4/12/2016

12

Should have a clear segregation of HR (hiring, salary rate setting, benefit changes) and Payroll functions.

Let bank know who is authorized to do what – insist on dual authorization of all bank/wire transfers

Have someone who is not involved in HR or Payroll receive, distribute and/or mail all payroll checks.

Better yet, insist on direct deposit for all employees!

Access to assets should not be necessary when preparing financial reports.

Reports should be prepared by someone who does not have access to assets, nor does the daily accounting.

AND/OR

Critical analytical review should be done by someone who did not prepare the reports.

Must look outside Business Office for leverage:

Superintendent

Clerical assistance

IT personnel

School Building personnel

Treasurer (or designee outside the Business Office)

Board members

Others

4/12/2016

13

Maximize use of technology!

On-line fees payment system

Direct deposit for all employees

District only credit cards

Limit access to all accounting, banking, payroll, purchasing and programming to only those with a legitimate need for access

Limit SBO /CFO access as well

Review Insurance coverage

How Will Insurance Coverage Help?

(example) 1) Faithful Performance (or really lack thereof) is a covered

cause of loss

2) Must be able to prove the loss -

i.e. document what is gone, not just illustrate that we

have less than we should have had.

3) It must be a covered cause of loss, not just bad

behavior.

Paying for your daughter’s wedding with the corporate

credit card was covered.

Paying his wife a fee for lavishly decorating his office was

not covered.

4) Money for external costs to establish a proof of loss

is often covered.

EMC pays up to $10,000 based on the size of the loss.

38

Investigate every anomaly:

◦ “We bought a DVD and my check never got cashed…”

◦ “My daughter paid for a shirt - never got a shirt..”

Ask your auditor for advice!

◦ “Specifically, how can we change how we are doing a certain transaction cycle to make it even stronger?” “Will it erase the comment in our audit?”

◦ “Can you review all expenses related to… Superintendent, SBO, HR Director…”

4/12/2016

14

Contact IASBO Assistant Director, Nancy Blow at:

[email protected] to purchase and mail you a booklet ($10) or to PDF you a copy at no cost!

Thanks!!