Embed Size (px)

Citation preview

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Perfect Competition

Econ 102: Introduction to Microeconomics

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Goals of today’s class

Goals of today’s class 2/ 14

Learn different types of market structures.

Learn how perfectly competitive firms make productiondecisions.

Learn about the long-run outcome of perfectly competitivefirms.

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Types of MarketsCharacteristics

Types of Markets 3/ 14

Perfect Competition (Chapter 11): many firms producingidentical products, no barriers to enter industry.

Monopoly (Chapter 12): one firm with control over itsprice, barriers to other firms entering.

Monopolistic Competition (Chapter 13): many firms withdifferentiated products, no barriers to entry.

Oligopoly (Chapter 13): only a small number of large firmsdominate the industry - one firm’s actions affect the decisionsof others.

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Types of MarketsCharacteristics

Types of Markets 3/ 14

Perfect Competition (Chapter 11): many firms producingidentical products, no barriers to enter industry.

Monopoly (Chapter 12): one firm with control over itsprice, barriers to other firms entering.

Monopolistic Competition (Chapter 13): many firms withdifferentiated products, no barriers to entry.

Oligopoly (Chapter 13): only a small number of large firmsdominate the industry - one firm’s actions affect the decisionsof others.

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Types of MarketsCharacteristics

Types of Markets 3/ 14

Perfect Competition (Chapter 11): many firms producingidentical products, no barriers to enter industry.

Monopoly (Chapter 12): one firm with control over itsprice, barriers to other firms entering.

Monopolistic Competition (Chapter 13): many firms withdifferentiated products, no barriers to entry.

Oligopoly (Chapter 13): only a small number of large firmsdominate the industry - one firm’s actions affect the decisionsof others.

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Types of MarketsCharacteristics

Types of Markets 3/ 14

Perfect Competition (Chapter 11): many firms producingidentical products, no barriers to enter industry.

Monopoly (Chapter 12): one firm with control over itsprice, barriers to other firms entering.

Monopolistic Competition (Chapter 13): many firms withdifferentiated products, no barriers to entry.

Oligopoly (Chapter 13): only a small number of large firmsdominate the industry - one firm’s actions affect the decisionsof others.

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Types of MarketsCharacteristics

Perfect Competition 4/ 14

Characteristics of Perfect Competition:

Many small firms, each is very small compared to the entiremarket.Firms all sell identical products.All firms and customers are well informed about prices.No barriers to entering the industry.

Very few “perfect” examples of perfect competition. Someclose examples:

Agricultural products: wheat, soybeans, corn, etc.Secondary sellers - eg: textbook stores.Unskilled labor.

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Types of MarketsCharacteristics

Perfect Competition 4/ 14

Characteristics of Perfect Competition:

Many small firms, each is very small compared to the entiremarket.Firms all sell identical products.All firms and customers are well informed about prices.No barriers to entering the industry.

Very few “perfect” examples of perfect competition. Someclose examples:

Agricultural products: wheat, soybeans, corn, etc.Secondary sellers - eg: textbook stores.Unskilled labor.

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Types of MarketsCharacteristics

Perfect Competition 4/ 14

Characteristics of Perfect Competition:

Many small firms, each is very small compared to the entiremarket.Firms all sell identical products.All firms and customers are well informed about prices.No barriers to entering the industry.

Very few “perfect” examples of perfect competition. Someclose examples:

Agricultural products: wheat, soybeans, corn, etc.Secondary sellers - eg: textbook stores.Unskilled labor.

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Types of MarketsCharacteristics

Perfect Competition 4/ 14

Characteristics of Perfect Competition:

Many small firms, each is very small compared to the entiremarket.Firms all sell identical products.All firms and customers are well informed about prices.No barriers to entering the industry.

Very few “perfect” examples of perfect competition. Someclose examples:

Agricultural products: wheat, soybeans, corn, etc.Secondary sellers - eg: textbook stores.Unskilled labor.

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Types of MarketsCharacteristics

Perfect Competition 4/ 14

Characteristics of Perfect Competition:

Many small firms, each is very small compared to the entiremarket.Firms all sell identical products.All firms and customers are well informed about prices.No barriers to entering the industry.

Very few “perfect” examples of perfect competition. Someclose examples:

Agricultural products: wheat, soybeans, corn, etc.Secondary sellers - eg: textbook stores.Unskilled labor.

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Types of MarketsCharacteristics

Perfect Competition 4/ 14

Characteristics of Perfect Competition:

Many small firms, each is very small compared to the entiremarket.Firms all sell identical products.All firms and customers are well informed about prices.No barriers to entering the industry.

Very few “perfect” examples of perfect competition. Someclose examples:

Agricultural products: wheat, soybeans, corn, etc.Secondary sellers - eg: textbook stores.Unskilled labor.

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Types of MarketsCharacteristics

Perfect Competition 4/ 14

Characteristics of Perfect Competition:

Many small firms, each is very small compared to the entiremarket.Firms all sell identical products.All firms and customers are well informed about prices.No barriers to entering the industry.

Very few “perfect” examples of perfect competition. Someclose examples:

Agricultural products: wheat, soybeans, corn, etc.Secondary sellers - eg: textbook stores.Unskilled labor.

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Types of MarketsCharacteristics

Perfect Competition 4/ 14

Characteristics of Perfect Competition:

Many small firms, each is very small compared to the entiremarket.Firms all sell identical products.All firms and customers are well informed about prices.No barriers to entering the industry.

Very few “perfect” examples of perfect competition. Someclose examples:

Agricultural products: wheat, soybeans, corn, etc.Secondary sellers - eg: textbook stores.Unskilled labor.

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Types of MarketsCharacteristics

Perfect Competition 4/ 14

Characteristics of Perfect Competition:

Many small firms, each is very small compared to the entiremarket.Firms all sell identical products.All firms and customers are well informed about prices.No barriers to entering the industry.

Very few “perfect” examples of perfect competition. Someclose examples:

Agricultural products: wheat, soybeans, corn, etc.Secondary sellers - eg: textbook stores.Unskilled labor.

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Demand Facing Individual FirmsProfit MaximizationIndividual Firm’s Supply Curve

Demand Facing Individual Firm 5/ 14

Entire market demand curve may be downward sloping.

Conditions facing individual firm.

Because product is identical to many competitors → cannotcharge higher prices than competitors.Because firm is small → no incentive to charge lower pricesthan competitors.Perfectly competitive firms are referred to as price takers.

Price taking → P = MR.

What will demand curve facing the firm look like?

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Demand Facing Individual FirmsProfit MaximizationIndividual Firm’s Supply Curve

Demand Facing Individual Firm 5/ 14

Entire market demand curve may be downward sloping.

Conditions facing individual firm.

Because product is identical to many competitors → cannotcharge higher prices than competitors.Because firm is small → no incentive to charge lower pricesthan competitors.Perfectly competitive firms are referred to as price takers.

Price taking → P = MR.

What will demand curve facing the firm look like?

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Demand Facing Individual FirmsProfit MaximizationIndividual Firm’s Supply Curve

Demand Facing Individual Firm 5/ 14

Entire market demand curve may be downward sloping.

Conditions facing individual firm.

Because product is identical to many competitors → cannotcharge higher prices than competitors.Because firm is small → no incentive to charge lower pricesthan competitors.Perfectly competitive firms are referred to as price takers.

Price taking → P = MR.

What will demand curve facing the firm look like?

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Demand Facing Individual FirmsProfit MaximizationIndividual Firm’s Supply Curve

Demand Facing Individual Firm 5/ 14

Entire market demand curve may be downward sloping.

Conditions facing individual firm.

Because product is identical to many competitors → cannotcharge higher prices than competitors.Because firm is small → no incentive to charge lower pricesthan competitors.Perfectly competitive firms are referred to as price takers.

Price taking → P = MR.

What will demand curve facing the firm look like?

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Demand Facing Individual FirmsProfit MaximizationIndividual Firm’s Supply Curve

Demand Facing Individual Firm 5/ 14

Entire market demand curve may be downward sloping.

Conditions facing individual firm.

Because product is identical to many competitors → cannotcharge higher prices than competitors.Because firm is small → no incentive to charge lower pricesthan competitors.Perfectly competitive firms are referred to as price takers.

Price taking → P = MR.

What will demand curve facing the firm look like?

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Demand Facing Individual FirmsProfit MaximizationIndividual Firm’s Supply Curve

Demand Facing Individual Firm 5/ 14

Entire market demand curve may be downward sloping.

Conditions facing individual firm.

Because product is identical to many competitors → cannotcharge higher prices than competitors.Because firm is small → no incentive to charge lower pricesthan competitors.Perfectly competitive firms are referred to as price takers.

Price taking → P = MR.

What will demand curve facing the firm look like?

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Demand Facing Individual FirmsProfit MaximizationIndividual Firm’s Supply Curve

Demand Facing Individual Firm 5/ 14

Entire market demand curve may be downward sloping.

Conditions facing individual firm.

Because product is identical to many competitors → cannotcharge higher prices than competitors.Because firm is small → no incentive to charge lower pricesthan competitors.Perfectly competitive firms are referred to as price takers.

Price taking → P = MR.

What will demand curve facing the firm look like?

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Demand Facing Individual FirmsProfit MaximizationIndividual Firm’s Supply Curve

Firm’s Decisions 6/ 14

Short-run decision: how much to produce to maximize profits.

Can only change variable factor of production (usually labor),all other decisions are pre-determined.

Long-run decisions:

New firms can enter the industry.Existing firms can leave the industry.Firms can change their scale (eg: increase plant size).

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Demand Facing Individual FirmsProfit MaximizationIndividual Firm’s Supply Curve

Firm’s Decisions 6/ 14

Short-run decision: how much to produce to maximize profits.

Can only change variable factor of production (usually labor),all other decisions are pre-determined.

Long-run decisions:

New firms can enter the industry.Existing firms can leave the industry.Firms can change their scale (eg: increase plant size).

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Demand Facing Individual FirmsProfit MaximizationIndividual Firm’s Supply Curve

Firm’s Decisions 6/ 14

Short-run decision: how much to produce to maximize profits.

Can only change variable factor of production (usually labor),all other decisions are pre-determined.

Long-run decisions:

New firms can enter the industry.Existing firms can leave the industry.Firms can change their scale (eg: increase plant size).

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Demand Facing Individual FirmsProfit MaximizationIndividual Firm’s Supply Curve

Firm’s Decisions 6/ 14

Short-run decision: how much to produce to maximize profits.

Can only change variable factor of production (usually labor),all other decisions are pre-determined.

Long-run decisions:

New firms can enter the industry.Existing firms can leave the industry.Firms can change their scale (eg: increase plant size).

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Demand Facing Individual FirmsProfit MaximizationIndividual Firm’s Supply Curve

Firm’s Decisions 6/ 14

Short-run decision: how much to produce to maximize profits.

Can only change variable factor of production (usually labor),all other decisions are pre-determined.

Long-run decisions:

New firms can enter the industry.Existing firms can leave the industry.Firms can change their scale (eg: increase plant size).

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Demand Facing Individual FirmsProfit MaximizationIndividual Firm’s Supply Curve

Firm’s Decisions 6/ 14

Short-run decision: how much to produce to maximize profits.

Can only change variable factor of production (usually labor),all other decisions are pre-determined.

Long-run decisions:

New firms can enter the industry.Existing firms can leave the industry.Firms can change their scale (eg: increase plant size).

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Demand Facing Individual FirmsProfit MaximizationIndividual Firm’s Supply Curve

Profit Maximization 7/ 14

Suppose MR > MC . What does this mean?

If this is the case, should you decide to...

... produce more?

... produce less?

... not change production decisions (already maximizingprofits)?

What impact does this have on MR −MC?

What is the profit maximization rule?

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Demand Facing Individual FirmsProfit MaximizationIndividual Firm’s Supply Curve

Profit Maximization 7/ 14

Suppose MR > MC . What does this mean?

If this is the case, should you decide to...

... produce more?

... produce less?

... not change production decisions (already maximizingprofits)?

What impact does this have on MR −MC?

What is the profit maximization rule?

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Demand Facing Individual FirmsProfit MaximizationIndividual Firm’s Supply Curve

Profit Maximization 7/ 14

Suppose MR > MC . What does this mean?

If this is the case, should you decide to...

... produce more?

... produce less?

... not change production decisions (already maximizingprofits)?

What impact does this have on MR −MC?

What is the profit maximization rule?

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Demand Facing Individual FirmsProfit MaximizationIndividual Firm’s Supply Curve

Profit Maximization 7/ 14

Suppose MR > MC . What does this mean?

If this is the case, should you decide to...

... produce more?

... produce less?

... not change production decisions (already maximizingprofits)?

What impact does this have on MR −MC?

What is the profit maximization rule?

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Demand Facing Individual FirmsProfit MaximizationIndividual Firm’s Supply Curve

Profit Maximization 7/ 14

Suppose MR > MC . What does this mean?

If this is the case, should you decide to...

... produce more?

... produce less?

... not change production decisions (already maximizingprofits)?

What impact does this have on MR −MC?

What is the profit maximization rule?

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Demand Facing Individual FirmsProfit MaximizationIndividual Firm’s Supply Curve

Profit Maximization 8/ 14

Set MR=MC.

Total Revenue = Price xQuantity

Total Cost = ATC xQuantity

Profit = Total Revenue -Total Cost

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Demand Facing Individual FirmsProfit MaximizationIndividual Firm’s Supply Curve

Profit Maximization 8/ 14

Set MR=MC.

Total Revenue = Price xQuantity

Total Cost = ATC xQuantity

Profit = Total Revenue -Total Cost

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Demand Facing Individual FirmsProfit MaximizationIndividual Firm’s Supply Curve

Profit Maximization 8/ 14

Set MR=MC.

Total Revenue = Price xQuantity

Total Cost = ATC xQuantity

Profit = Total Revenue -Total Cost

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Demand Facing Individual FirmsProfit MaximizationIndividual Firm’s Supply Curve

Profit Maximization 8/ 14

Set MR=MC.

Total Revenue = Price xQuantity

Total Cost = ATC xQuantity

Profit = Total Revenue -Total Cost

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Demand Facing Individual FirmsProfit MaximizationIndividual Firm’s Supply Curve

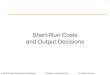

Minimizing Losses 9/ 14

Sometimes the “profitmaximizing” quantity endsin a loss.

Happens when price is lessthan ATC.

The loss is still less thantotal fixed cost = AFC xQ.

In this case it is better toproduce and make a lossthan shut down.

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Demand Facing Individual FirmsProfit MaximizationIndividual Firm’s Supply Curve

Minimizing Losses 9/ 14

Sometimes the “profitmaximizing” quantity endsin a loss.

Happens when price is lessthan ATC.

The loss is still less thantotal fixed cost = AFC xQ.

In this case it is better toproduce and make a lossthan shut down.

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Demand Facing Individual FirmsProfit MaximizationIndividual Firm’s Supply Curve

Minimizing Losses 9/ 14

Sometimes the “profitmaximizing” quantity endsin a loss.

Happens when price is lessthan ATC.

The loss is still less thantotal fixed cost = AFC xQ.

In this case it is better toproduce and make a lossthan shut down.

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Demand Facing Individual FirmsProfit MaximizationIndividual Firm’s Supply Curve

Minimizing Losses 9/ 14

Sometimes the “profitmaximizing” quantity endsin a loss.

Happens when price is lessthan ATC.

The loss is still less thantotal fixed cost = AFC xQ.

In this case it is better toproduce and make a lossthan shut down.

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Demand Facing Individual FirmsProfit MaximizationIndividual Firm’s Supply Curve

Individual Firm’s Supply Curve 10/ 14

When the price is less thanminimum AVC, the loss islarger than fixed cost →Better to shut down.

When the price is betweenATC and AVC, the firm ismaking a loss, but loss issmaller than fixed cost.

When the price is abovethe minimum ATC, firmmakes profits.

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Demand Facing Individual FirmsProfit MaximizationIndividual Firm’s Supply Curve

Individual Firm’s Supply Curve 10/ 14

When the price is less thanminimum AVC, the loss islarger than fixed cost →Better to shut down.

When the price is betweenATC and AVC, the firm ismaking a loss, but loss issmaller than fixed cost.

When the price is abovethe minimum ATC, firmmakes profits.

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Demand Facing Individual FirmsProfit MaximizationIndividual Firm’s Supply Curve

Individual Firm’s Supply Curve 10/ 14

When the price is less thanminimum AVC, the loss islarger than fixed cost →Better to shut down.

When the price is betweenATC and AVC, the firm ismaking a loss, but loss issmaller than fixed cost.

When the price is abovethe minimum ATC, firmmakes profits.

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Firm EntryDisappearing ProfitsLong-run Efficiency

Long-run Outcome 11/ 14

In the long run, firms decide to enter or exit the industry.

Perfect competition: no barriers to entry.

What happens over long run if firms in industry are makingprofits?

What happens over long run if firms in industry are makinglosses?

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Firm EntryDisappearing ProfitsLong-run Efficiency

Long-run Outcome 11/ 14

In the long run, firms decide to enter or exit the industry.

Perfect competition: no barriers to entry.

What happens over long run if firms in industry are makingprofits?

What happens over long run if firms in industry are makinglosses?

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Firm EntryDisappearing ProfitsLong-run Efficiency

Long-run Outcome 11/ 14

In the long run, firms decide to enter or exit the industry.

Perfect competition: no barriers to entry.

What happens over long run if firms in industry are makingprofits?

What happens over long run if firms in industry are makinglosses?

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Firm EntryDisappearing ProfitsLong-run Efficiency

Long-run Outcome 11/ 14

In the long run, firms decide to enter or exit the industry.

Perfect competition: no barriers to entry.

What happens over long run if firms in industry are makingprofits?

What happens over long run if firms in industry are makinglosses?

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Firm EntryDisappearing ProfitsLong-run Efficiency

Long-run Disappearing Profits 12/ 14

Firms are making profits.

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Firm EntryDisappearing ProfitsLong-run Efficiency

Long-run Disappearing Profits 12/ 14

New firms enter industry.

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Firm EntryDisappearing ProfitsLong-run Efficiency

Long-run Disappearing Profits 12/ 14

Market supply shifts left → Price decreases.

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Firm EntryDisappearing ProfitsLong-run Efficiency

Long-run Disappearing Profits 12/ 14

Price decreases → Profits decrease.

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Firm EntryDisappearing ProfitsLong-run Efficiency

Long-run Disappearing Profits 12/ 14

Process continues until profits disappear

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Firm EntryDisappearing ProfitsLong-run Efficiency

Economic Profit 13/ 14

Economic profit: Total Revenue minus Total Cost.

Economists consider opportunity costs part of total costs.

What is the opportunity cost of putting your money/resourcesinto a business.

Zero economic profit implies making a “normal” level of profit.

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Firm EntryDisappearing ProfitsLong-run Efficiency

Economic Profit 13/ 14

Economic profit: Total Revenue minus Total Cost.

Economists consider opportunity costs part of total costs.

What is the opportunity cost of putting your money/resourcesinto a business.

Zero economic profit implies making a “normal” level of profit.

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Firm EntryDisappearing ProfitsLong-run Efficiency

Economic Profit 13/ 14

Economic profit: Total Revenue minus Total Cost.

Economists consider opportunity costs part of total costs.

What is the opportunity cost of putting your money/resourcesinto a business.

Zero economic profit implies making a “normal” level of profit.

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Firm EntryDisappearing ProfitsLong-run Efficiency

Economic Profit 13/ 14

Economic profit: Total Revenue minus Total Cost.

Economists consider opportunity costs part of total costs.

What is the opportunity cost of putting your money/resourcesinto a business.

Zero economic profit implies making a “normal” level of profit.

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Firm EntryDisappearing ProfitsLong-run Efficiency

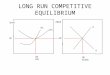

Long-run Outcome 14/ 14

Free-entry caused long-run profits to drive to zero.

In the long run, firms produce at a point where average totalcosts are as small as possible.

In the long run, the amount consumers pay (price) is equal tothe average total cost of producing the good.

Long run outcome is both efficient and fair to consumers.

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Firm EntryDisappearing ProfitsLong-run Efficiency

Long-run Outcome 14/ 14

Free-entry caused long-run profits to drive to zero.

In the long run, firms produce at a point where average totalcosts are as small as possible.

In the long run, the amount consumers pay (price) is equal tothe average total cost of producing the good.

Long run outcome is both efficient and fair to consumers.

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Firm EntryDisappearing ProfitsLong-run Efficiency

Long-run Outcome 14/ 14

Free-entry caused long-run profits to drive to zero.

In the long run, firms produce at a point where average totalcosts are as small as possible.

In the long run, the amount consumers pay (price) is equal tothe average total cost of producing the good.

Long run outcome is both efficient and fair to consumers.

Econ 102: Introduction to Microeconomics Perfect Competition

What is Perfect CompetitionShort-run DecisionsLong-run Outcome

Firm EntryDisappearing ProfitsLong-run Efficiency

Long-run Outcome 14/ 14

Free-entry caused long-run profits to drive to zero.

In the long run, firms produce at a point where average totalcosts are as small as possible.

In the long run, the amount consumers pay (price) is equal tothe average total cost of producing the good.

Long run outcome is both efficient and fair to consumers.

Econ 102: Introduction to Microeconomics Perfect Competition