Embed Size (px)

Citation preview

Prepared for:Dr Andrew Barber, SARDI

Prepared by:

Dr Hervé Remaud and Dr Nick DanenbergSenior Research Associates

T. +33 6 76 55 58 60 and (08) 8302 9167

and Kimberley Peters, Research Associate

Date of Issue: 8th of April 2010

What Influences Consumer Choice in a Restaurant Context?

EXECUTIVE SUMMARYThis report presents the results of the research “What influences Consumer Choice in a Restaurant Context”, conducted by the Ehrenberg-Bass Institute on behalf of Marine innovation South Australia (MISA) for the South Australian seafood industry.

The project surveyed 1208 Australian restaurant patrons regarding the factors that influence their food and seafood purchase behaviour in the contexts of both casual and fine-dining restaurants (places where people can sit in and order lunch/dinner from a menu). Focus groups were conducted in August 2009, followed by an online quantitative survey distributed for a period of one week during September 2009.

The ultimate aim of the project was to explore the decision-making processes underlying restaurant patrons’ menu item choices, in order to identify barriers and determine potential opportunities to direct consumers’ attention towards the purchase of seafood products when patronising a full-service restaurant.

There were 5 objectives in this research.

Objective 1

The first objective aimed to describe the Consumers’ restaurant experience at casual and fine-dining restaurants during the past 4 and 8 weeks respectively.

Specifically this section investigated:

• Consumers’ restaurant experience in the last 4 weeks, for people who visited a casual restaurant, and in the last 2 months for people who visited a fine-dining restaurant: number of casual and fine-dining restaurants visited; what was purchased and average expenditure for a meal; barriers preventing the increased consumption of fish and shellfish in casual and fine-dining restaurants.

• Where they consumed seafood during the last four weeks.

• Consumers’ perception of various menu items in each restaurant context (casual and fine-dining).

The key findings are outlined below:

• Generally, there is a very low percentage of restaurant patrons who are exclusively loyal to one establishment type (i.e. casual or fine-dining restaurant).

• Majority of casual-dining restaurant patrons had also visited a fine-dining restaurant (at least once) during the last 8 weeks.

• Casual-dining restaurant patrons spend an average of $22.50 on a fish dish in

comparison to fine-dining restaurant patrons who spend an average of $27.00.

• Casual-dining restaurant patrons spend an average of $25.50 on a shellfish dish in comparison to fine-dining restaurant patrons who spend an average of $32.00.

• Regardless of the species both casual and fine-dining restaurant patrons are generally light buyers of seafood.

• Fine-dining patrons visited on average about twice a fine-dining restaurant during a 2 month-period. The chances for these clients to order seafood when visiting such a restaurant are low, less than 0.5 time out of these two visits.

• Prawns are the most frequently ordered seafood species at both casual and fine-dining restaurants.

• There is a clear distinction in relation to consumers’ perception of seafood and meat in a restaurant context.

• Consumers perceive seafood as being less versatile and considered to be a “special occasion food” in comparison to meat dishes.

• In comparison to meat, seafood is considered as being more healthy and lower in fat.

• There is no particular perceptual barrier that needs to be overcome to increase consumers’ consumption of seafood at casual and fine-dining restaurants.

• The proportion of respondents’ total seafood consumption increases slightly with respondents’ income level.

• Respondents with an undergraduate and/or postgraduate qualification consume a larger proportion of seafood at restaurants than other locations (i.e., at home, fish and chip outlets etc) and visit restaurants more frequently on average.

• Most seafood is consumed at home (about 47%) and then in a restaurant (33%). Fish and Chips outlets represent about 16% of the total seafood consumption in Australia. And only about 6.5% of seafood is finally consumed at a friends / relatives’ home.

Objective 2

The second objective was to explore the primary influencing factors that determine consumers' choice on restaurant menus, and the relative importance of (seafood) menu item attributes at the point of selection. Specifically, this objective investigated the factors that (most and least) influence consumers’ menu item choice in a restaurant context.

The key findings are outlined below:

• Both segments of consumers (casual and fine-dining) consider “the combination of ingredients” and ordering “a dish that I could not / would not want to prepare at home” as the most important attributes influencing menu item selection in a restaurant context.

• Both segments of consumers (casual and fine-dining) consider “the core ingredient of the dish is sustainably produced” to be the least important attribute influencing menu item selection in a restaurant context.

• The inclusion of “local produce” and “a dish representing a healthy option” were more important for fine-dining patrons than casual-dining restaurant patrons.

• The price of a dish and “the method of preparation” were considerd more important for casual-dining restaurant patrons than fine-dining restaurant patrons.

• The relative importance of menu item attributes is not significantly different between casual and fine-dining restaurant patrons.

• Many more attributes are considered important when selecting a seafood dish from a restaurant menu in comparison to the selection of a dish not containing seafood when dining-out at a restaurant.

Objective 3

Section 3 explored the factors that may affect or moderate consumers’ choice of (sea)food items from a restaurant menu according to a patron’s level of involvement and social context. These factors included:

• Consumers’ involvement with regards to food;

• The effect of social context on consumers’ choice of (sea)food items from a menu.

The key findings are outlined below:

• The relative importance of menu item attributes differ significantly among restaurant patrons with a low and high level of involvement with food.

• The main attributes that most strongly influence the menu item choices of consumers with a low level of food involvement are associated with the concept of value.

• Restaurant patrons with a high level of involvement with food place a greater emphasis on hedonic ‘pleasure-seeking’ and sensory evaluations stemming from the dining experience.

• A dish ‘representing a healthy option’ exerts a much greater influence on the menu item choice of consumers with a low level of involvement with food

• Contrary to much current anecdotal information, the reference to local and sustainable produce are relatively unimportant attributes influencing casual and fine-dining restaurant patrons menu item choices, whatever their involvement for food or the effect of the social context.

• Consumers who are rather highly influenced by the social context effect when dining at a restaurant do place greater importance on all attributes in the dining environment when selecting a menu item compared to consumers with a low social influence.

Objective 4

This section investigated consumers’ likely purchase behaviour with regards to prawns, and the likelihood of consumers ordering prawns in a restaurant context depending on various situations.

In the first instance, consumers were asked their likelihood of purchasing prawns in the next 4 weeks at a restaurant. Then, introducing various claims associated with the consumption of prawns, we sought to estimate the extent consumers would be less or more likely to purchase prawns compared to the base line situation.

The key findings are outlined below:

• Whatever the scenario, there was no significant difference in the responses provided between the casual and fine-dining restaurant contexts nor between prawns for an entrée and prawns for a main plate.

• The chances for casual and fine-dining patrons of ordering prawns at a restaurant in the next 4 weeks are about 1 chance out of 2 (score of 5 out of 10).

• Two situations would slightly increase the chances of ordering prawns: if there was a greater variety of dishes including prawns (new recipes / innovative way to have prawns in the dish) (score of 5.6); and if the prawns were local (score of 5.5).

• Knowing that the prawns are frozen on the boat (score 3.7) and knowing that prawns are imported (score of 3) would clearly decrease the chances of a consumer ordering prawns for an entrée in the next 4 weeks in a restaurant.

• Overall, females gave slightly higher scores to almost all questions (in general, females are more likely to order prawns at a restaurant).

• People in NSW have the highest likelihood of ordering prawns in a restaurant in the next 4 weeks and would also have the highest chance of ordering prawns whatever the scenario (except for Spencer Gulf prawns in SA).

• The older the respondent, the greater the likelihood of ordering prawns whatever the scenario.

Objective 5

The final objective sought to determine consumers’ (stated) willingness to pay for (sea)food dishes, taking into consideration various claims and descriptors that would typically generate a price premium for consumers in a restaurant context. The descriptors were chosen arbitrarily, through discussions with MISA and the Institute. The items were selected to represent a broad range of the types of menu item descriptions that are found on restaurant menus—from the simple addition of a species name, up to a preparation described using fancy, French terms. Respondents were presented a baseline situation including a seafood dish that could be available in a restaurant as well as its price. Then, using various claims or descriptors for the dish, we asked consumers how much they would be willing to pay for the dish, and lastly, which one(s) they would consider ordering at a restaurant.

The key findings are outlined below:

• For a Fish and Chips (served with green salad) dish priced at $15, people would pay an extra price premium of $1.80 if the dish is presented as ‘Cooper’s beer battered fish and chips (served with green salad)’, and about $1.40 more if the dish is presented as ‘Grilled fish and baked potatoes (served with green salad and low fat sour cream)’.

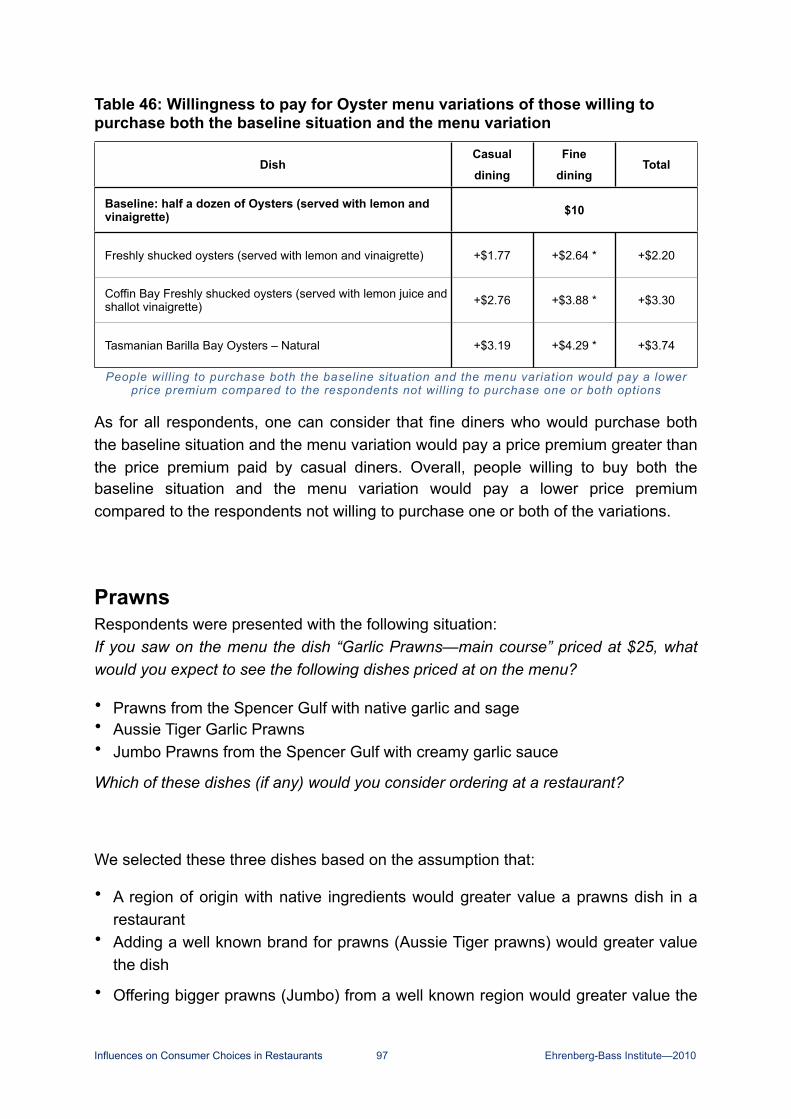

• For a dish of “half a dozen of Oysters (served with lemon and vinaigrette)” priced at $10, people would pay a price premium of about $4.20 if the dish is presented as ‘Tasmanian Barilla Bay Oysters – Natural’, and of about $3.70 more if the dish is presented as ‘Coffin Bay Freshly shucked oysters (served with lemon juice and shallot vinaigrette)’. For ‘Freshly shucked oysters', the extra price premium is about $2.70.

• For a dish of “Garlic Prawns - main course” priced at $25, people would pay a price premium of about $1.40 more if the dish is presented as ‘Prawns from the Spencer Gulf with native garlic and sage’, and $1.10 more if the dish is presented as ‘Jumbo Prawns from the Spencer Gulf with garlic’.

• For a dish of “Blue Eye Trevalla with a julienne of vegetables” priced at $25, people would pay about $1.70 extra if the dish is presented as ‘Trevalla en papillotte served with potato dauphinoise and a beurre blanc sauce’, and about $1.30 more if the dish is presented as ‘South Australian line-caught blue eye trevalla on a bed of risotto’. If presented as ‘Fresh deep sea blue eye trevalla with a sauce of native green olive and vernaccia’, the price premium is about $1.20.

• For a dish of “Yellowtail Kingfish with roasted capsicum and mashed potatoes” priced at $25, people would pay very little more (only up to $0.60 cents) for any other descriptions that were suggested.

There is a fine-dining effect—in a fine-dining scenario, people generally expect to pay more for a given dish and to pay incrementally more for variations to the dish. In a fine-dining scenario, basic offerings are also generally less favoured than they are in a casual dining context. This implies that at a fine-dining restaurant, to some extent diners do expect to be and want to be ‘wowed’ by the meals on offer.

Fine and casual diners who would purchase both the baseline situation and one of the menu variations would pay (in most cases) a greater price premium compared to the respondents not willing to purchase one of the variations. Fine diners willing to buy both the baseline situation and one of the menu variations would pay a greater price premium compared to casual diners.

CONTENTS............................................................................................................................................Introduction 3

.................................................................................................................................Research objectives 5................................................................................................................Objective 1: Consumers’ restaurant experiences 5

..........................Objective 2: The primary influencing factors that determine consumers’ choices from restaurant menus 5

Objective 3: The relative importance of menu item attributes according to consumers’ level of food involvement, social .......................................................................................................context and establishment type (casual vs. fine-dining) 6

..................................Objective 4: Consumers’ future behaviour with regards to prawns depending on various situations 6................................................................Objective 5: Consumers’ (stated) willingness to pay for various seafood dishes 6

............................................................................................................................................Methodology 7..........................................................................................................Differences between sub-samples 9

..............................................................................................................................Sample description 10................................................................................Objective 1: Consumers’ restaurant experience 11

...........................................................................................................Duplication of restaurants visit 11..........................................................................................................................Dining-out frequency 13

..........................................Seafood consumption frequency when dining-out in a casual restaurant 16..............................................................................................................................................................Loyalty varies little 18

....................................Seafood consumption frequency when dining-out at a fine-dining restaurant 19..............................................................................................................................................................Loyalty varies little 22

........................................................................................................................Money spent for a dish 23Number of red/white meat, shellfish, fish and vegetarian dishes ordered at a casual-dining

............................................................................................................................................restaurant 29Number of red/white meat, shellfish, fish and vegetarian dishes ordered at a fine-dining restaurant............................................................................................................................................................. 34

...........Reasons for people to stop ordering fish and shellfish in casual and fine-dining restaurants 39.........................................................................................................................................Reasons for not eating shellfish 39

................................................................................................................................................Reasons for not eating fish 41

.....................................Shellfish and fish consumption trends in casual and fine-dining restaurants 43.................................................................................Seafood consumption in-home and out of home 44

............................................................................................Food perceptions in a restaurant context 48...............................................................................................................Guidelines for interpretation of Perceptual Maps 49

.........................................................................................................................Guidelines for interpretation of Deviations 50

.......................................................................................Perceptual map – casual restaurant context 50.................................................................................Deviations analysis—casual restaurant context 52.................................................................................Meats key perceptual strengths and weaknesses 53

....................................................................................................................................................Core Meats comparison: 53

............................................................................Seafoods key perceptual strengths and weaknesses 54..................................................................................................................................Core Seafood products comparison: 56

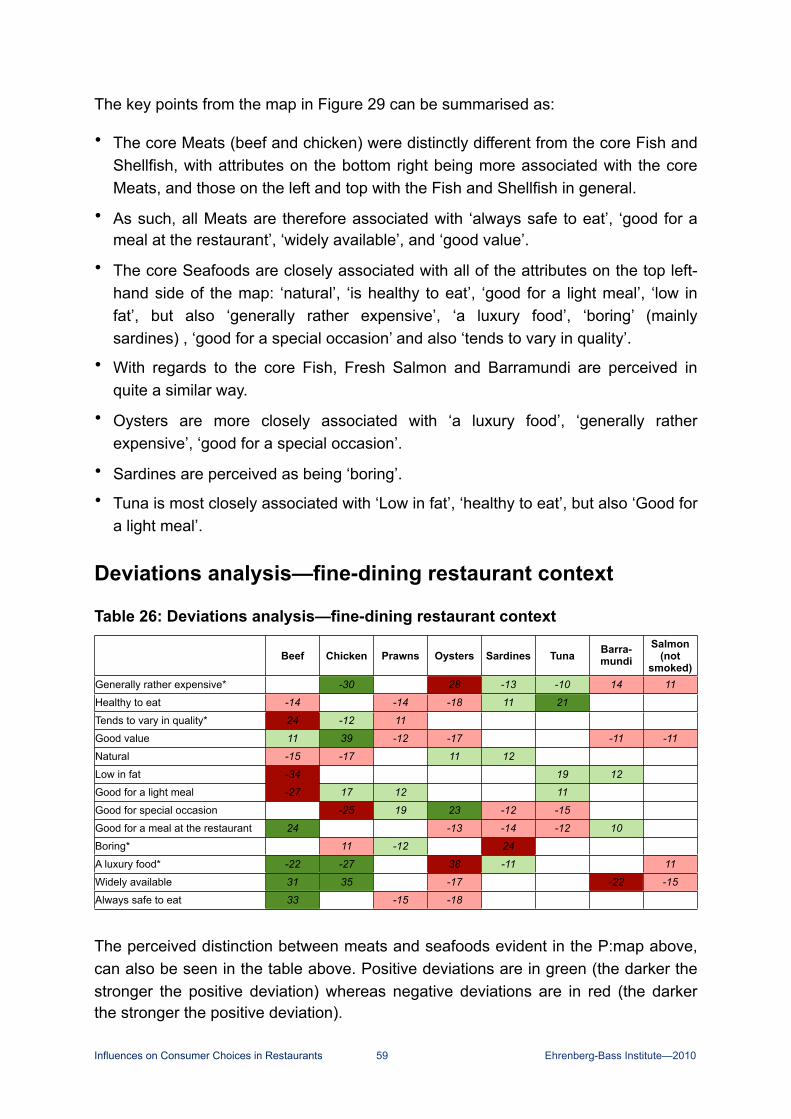

................................................................................Perceptual map – fine-dining restaurant context 58..........................................................................Deviations analysis—fine-dining restaurant context 59

.................................................................................Meats key perceptual strengths and weaknesses 60....................................................................................................................................................Core Meats comparison: 60

............................................................................Seafoods key perceptual strengths and weaknesses 61..................................................................................................................................Core Seafood products comparison: 63

...........................................................................................Perceptual maps – casual vs. fine-dining restaurant contexts 64

Objective 2: The primary influencing factors that determine consumers' choice on restaurant .....................................................................................................................................................menus 65

The primary influencing factors that determine consumers’ choice on casual vs. fine-dining ................................................................................................................................restaurant menu’s 66

......................................................................................................................................................................Sustainability 67

................................................................................................Choice variety, difference between casual and fine diners 67........................................................................................Importance of price, difference between casual and fine diners 68

Influences on Consumer Choices in Restaurants 1 Ehrenberg-Bass Institute—2010

............................................................................................................................................................................Summary 68

The primary influencing factors that determine consumers’ choices of a regular dish vs. seafood .................................................................................................................dish from restaurant menus 69

The primary influencing factors that determine consumers’ choice of a dish vs. seafood dish from a ...............................................................................................casual vs. fine-dining restaurant menu 70

............................................................................................................................................Seafood dish at casual dining 71

............................................................................................................................................Regular Dish at casual dining 72

................................................................Comparison of a regular dish vs a seafood dish in a casual restaurant context 72.................................................................................................................................................Seafood dish at fine-dining 72

..................................................................................................................................................Regular dish at fine-dining 73..........................................................Comparison of a regular dish vs a seafood dish in a fine-dining restaurant context 73

Objective 3: the relative importance of menu item attributes according to consumers’ level of ...................................................................................................food involvement and social context 74

The relative importance of menu item attributes for consumers with a low vs. high level of food .........................................................................................................................................involvement 74

.....................................................................................................................................................Food involvement scale 74.................The relative importance of menu item attributes for consumers with a low vs. high level of food involvement 75

The relative importance of menu item attributes for consumers with a low vs. high effect of social .................................................................................................................................................context 79

...............................................................................................................................Social context (opinion-seeking) scale 79......................The relative importance of menu item attributes for consumers with a low vs. high effect of social context 81

................................................Objective 4: Consumers’ future behaviour with regards to prawns 82.......................................Chances to order prawns for an entrée at a restaurant in the next 4 weeks 84

...............................Chances to order prawns for a main course at a restaurant in the next 4 weeks 85...........................................Chances to order prawns for a meal at a restaurant in the next 4 weeks 86

............................Objective 5: Consumers’ (stated) willingness to pay for various seafood dishes 90....................................................................................................................................Fish and Chips 90

.................................................................................................................................................Oysters 94

.................................................................................................................................................Prawns 97.............................................................................................................................................Trevalla 101

............................................................................................................................Yellowtail Kingfish 104..........................................................................................................................Summary of findings 108

...........................................................................................................................................Conclusion 110........................................................................................................................................Objective 1 110........................................................................................................................................Objective 2 111........................................................................................................................................Objective 3 112........................................................................................................................................Objective 4 113........................................................................................................................................Objective 5 113

................................................................................................Appendix 1: Focus group transcripts 116....................................................................................................................................Casual-dining 116

........................................................................................................................................Fine-dining 125........................................................................................................Appendix 2: Best-Worst Scaling 133

................................................................................................................Appendix 3: Questionnaire 134

Influences on Consumer Choices in Restaurants 2 Ehrenberg-Bass Institute—2010

INTRODUCTIONThis report presents the results of research conducted with the broad objective of identifying “what influences consumer choices in a restaurant context?”, conducted by the Ehrenberg-Bass Institute for Marketing Science on behalf of Marine Innovation South Australia (MISA). The overall objective of the research was to better understand what influences consumers’ menu item choices when dining at a casual or fine-dining restaurant. Given that a significant quantity of shellfish and seafood products are sold to the food-service sector, we believe that the seafood industry would benefit from a greater understanding of consumer behaviour in the restaurant context.

A restaurant is defined as a place where people can sit and have lunch or dinner. A restaurant can be Premium Class (5 stars), High Class or a Standard Restaurant (2-4 stars), and also include Bistros, Cafes, Pubs, and dine-in Fish & Chips. To date, very little research has been carried out (or, at least published in the public domain) to systematically understand consumers’ purchase decisions regarding food in general and seafood products in particular in the food service sector. This report follows on from research conducted in 2009 by the Institute on behalf of MISA, that surveyed key food purchase decision makers in the South Australian food service sector about their seafood purchase behaviour (in order to increase the Australian food service sector’s purchase of SA seafood products).

For the purpose of this research, we focus on casual and fine-dining restaurants only, excluding fish and chips and take-away outlets.

Casual and fine-dining restaurants are classified under the umbrella of full-service restaurants. A full-service restaurant includes, “all sit-down establishments where the focus is on food rather than on drink…characterised by table service and a relatively higher quality of food offering to quick-service units” (Euromonitor, 2009). For the purpose of this report, fine-dining patrons were defined as individuals who purchased a main course between AU$30.00 and AU$50.00 at a fine-dining restaurant (at least once) within the last 8 weeks. Casual-diners were classified as individual’s who purchased a main course between AU$15.00 and AU$30.00 at a casual-dining restaurant (at least once) within the last four weeks.

This research investigated:

• Consumers’ stated behaviour when selecting menu items at a casual/fine-dining restaurant, as well as their perception of various protein products in this restaurant dining context.

• The factors that determine consumers’ menu item choices at casual/fine-dining

Influences on Consumer Choices in Restaurants 3 Ehrenberg-Bass Institute—2010

restaurants, including a particular emphasis on menu item choices involving seafood.

• The relative importance of (seafood) menu item attributes at the point of selection.

• The relative importance of menu item attributes and differences (if any) that exist according to the type of restaurant (casual vs. fine-dining), as well as between restaurant patrons’ level of involvement with food and social contexts.

• Consumers’ future purchase behaviour with regards to prawns depending on various situations.

• Consumers’ (stated) willingness to pay for various seafood dishes.

The main methodology used for this research was a quantitative survey conducted online with 1,208 respondents across all regions of Australia. Prior to the conduct of the quantitative survey, two focus groups were conducted in Adelaide in order to better understand (from a qualitative perspective) how consumers select an item from a menu. The two focus groups were conducted on the 26th of August 2009. The quantitative survey was conducted between the 23rd and the 30th of September 2009.

Influences on Consumer Choices in Restaurants 4 Ehrenberg-Bass Institute—2010

RESEARCH OBJECTIVESIn June 2009, we reported on chefs’ seafood purchase behaviour, with the aim of better understanding their requirements in order to increase the Australian food service sector’s purchase and consumption of SA seafood products. Interestingly, SA chefs highlighted the importance and potential benefits associated with exploring the factors that influence consumers’ menu item choice when dining-out at a restaurant. A comprehensive understanding of how such factors impact the choices and selection of menu items in the restaurant would help the food service sector and the seafood industry to better satisfy consumers’ expectations from a restaurant dining occasion.

The objectives of this research include:

Objective 1: Consumersʼ restaurant experiences This section describes how consumers behave in a restaurant context. The research investigates:

• Consumers’ restaurant experience in the last 4 weeks, for people who visited a casual restaurant, and in the last 2 months for people who visited a fine-dining restaurant:

• Number of casual and fine-dining restaurants visited;

• What was purchased and the average expenditure for a meal;

• Barriers preventing the increased consumption of fish and shellfish in the restaurant industry;

• Location where seafood was consumed during the last four weeks;

• Consumers’ perceptions of various food items in each restaurant context (casual and fine-dining).

Objective 2: The primary influencing factors that determine consumersʼ choices from restaurant menusSection 2 explores the primary influencing factors that determine consumers’ choices from restaurant menus, and the relative importance of (seafood) menu item attributes at the point of selection. Specifically, this section investigates:

• The factors that (most) influence consumers’ menu item choice in a restaurant context;

• The factors that (least) influence consumers’ menu item in a restaurant context.

Influences on Consumer Choices in Restaurants 5 Ehrenberg-Bass Institute—2010

Objective 3: The relative importance of menu item attributes according to consumersʼ level of food involvement, social context and establishment type (casual vs. fine-dining)Section 3 investigates the extent to which potential factors may affect or moderate consumers’ choice of items from a restaurant menu. These factors include:

• Consumers’ involvement with regards to food;

• The effect of social context on consumers’ choice of (sea)food items from a menu.

Objective 4: Consumersʼ future behaviour with regards to prawns depending on various situationsThis section investigates consumers’ likely purchase behaviour with regards to prawns, and the likelihood of consumers ordering prawns in a restaurant context depending on various situations. In the first instance, consumers were asked their likelihood of purchasing prawns in the next 4 weeks at a restaurant. Then, introducing various claims associated with the consumption of prawns, we sought to estimate the extent to which consumers would be more or less likely to purchase prawns compared to the base-line condition.

Objective 5: Consumersʼ (stated) willingness to pay for various seafood dishesThe final section looks at the impact that various claims and descriptors of food items would have in generating a price premium among consumers in a restaurant context. Again, respondents were presented a baseline situation of a seafood dish that can be available in a restaurant as well as its price. Then, using various claims or descriptors for the dish, we asked consumers how much they would be willing to pay for the dish, and lastly, which one(s) they would actually consider ordering at a restaurant.

Influences on Consumer Choices in Restaurants 6 Ehrenberg-Bass Institute—2010

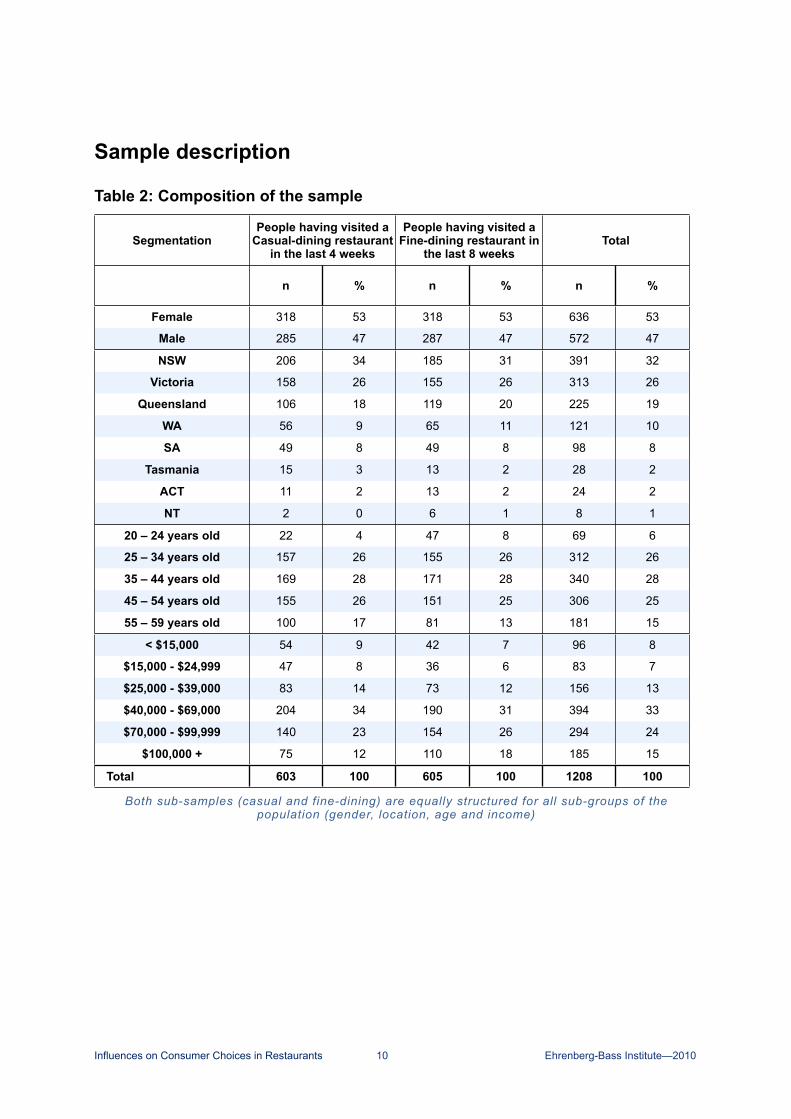

METHODOLOGYThe predominant approach to this research was a quantitative survey involving 1,208 respondents. The quantitative approach was selected to gain a realistic view and understanding of consumers’ behaviour in a restaurant context, and to be able to quantify the likely impact of various scenarios and factors. Prior to the quantitative survey, a literature review was conducted to identify any relevant prior work that had been conducted on the topic of interest. The study most similar to this research is a PhD thesis conducted in the United States by Jones1 (2007). In Australia, no extensive survey has been conducted on these topics and therefore, almost nothing is known about consumers’ food-choice behaviour in the restaurant context, especially in relation to the purchase of seafood. The most recent survey conducted was that by Ruello in 2004.

Following the literature review, more than 30 attributes or factors that have the potential to influence consumers’ choice on a restaurant menu were identified. The list was narrowed down after interviewing six colleagues of the Ehrenberg-Bass Institute for Marketing Science. This new list of factors was then discussed in two focus groups conducted in Adelaide at the end of August 2009. A detailed summary of the findings of the focus groups discussions are contained in Appendix 1. Following these focus groups, a final list of 13 primary factors was selected for inclusion in the quantitative survey.

The quantitative study involved 1,208 on-line interviews with consumers who had dined out at a casual or fine-dining restaurant in the last 4 or 8 weeks respectively. Half of the sample included people who had visited a casual-dining restaurant in the last four weeks, and most of the questions to this group referred to the selection of menu items specifically in the context of a casual-dining restaurant. The other half of the sample included people who had visited a fine-dining restaurant in the last 8-weeks, and most of the questions to this group referred to the selection of menu items specifically in the context of a fine-dining restaurant. Given the consideration that most consumers patronise fine-dining restaurants less frequently than they do casual-dining restaurants, we increased the period of time from within 4 weeks to within 8 weeks in order to effectively facilitate the recruitment of fine-dining restaurant patrons. Following the segmentation of the population of restaurant patrons, each sub-sample was then divided again in two, as described in the following table:

Influences on Consumer Choices in Restaurants 7 Ehrenberg-Bass Institute—2010

1 Jones C., S., (2007), Exploring the Factors Affecting Food Choice at Restaurants with Special Emphasis on the Roles Played by Menus, Health Information, and Health Icons. Robert Morris University

Table 1: Structure of the sample

People having visited a Casual restaurant in

the last 4 weeks

People having visited a Fine-dining restaurant

in the last 8 weeks

Total

Primary factors influencing your choice of a dish on the menu

&Scenarios for Prawns as a main course

301 300 601

Primary factors influencing your choice of a seafood dish on the menu

&Scenarios for Prawns as an entrée

302 305 607

Total 603 605 1208

With regards to Objective 2, we wanted to investigate the primary influencing factors that determine consumers’ choices on restaurant menus and whether this differed for dishes containing seafood and dishes that do not. Therefore, for each sub-sample of casual and fine-dining respondents, we split each sample in two, resulting in approximately 300 participants in each group. The first group responded to the following question: “Imagine that you are in a casual/fine-dining restaurant for dinner with other people…What attribute would most influence and which would least influence your choice when selecting a dish from the menu?”. Those in the second group responded to the following question: “Imagine that you are in a casual/fine-dining restaurant for dinner with other people…What attribute would most influence and which would least influence your choice when selecting a seafood dish from the menu?”.

With regards to Objective 4, we wanted to investigate consumers’ likely purchase behaviour with regards to prawns as an entrée dish versus as a main course dish (and whether there were differences between the two); and how likely consumers would be to order prawns in a restaurant context depending on various claims associated with the consumption of prawns. Therefore, for each sub-sample of casual and fine-dining respondents, we split each sample in two with approximately 300 participants in each group. The first group responded to the question: “What are the chances that you will order prawns for an entrée at a casual/fine-dining restaurant in the next 4 weeks?” While those in the second group responded to the question: “What are the chances that you will order prawns for a main course at a casual/fine-dining restaurant in the next 4 weeks?”.

Influences on Consumer Choices in Restaurants 8 Ehrenberg-Bass Institute—2010

The primary influencing factors that determine consumers’ menu item choices were measured using a method called Best-Worst Scaling (also known as Max-Diff Scaling). A full description of the approach is presented in Appendix 2. Briefly, the key advantage of this approach against other approaches such as with Likert Scale measurement is the fact that respondents are forced to make a trade off between what is perceived as most important in regards to a specific question and what is perceived as least important. This results in a realistic comparison of the factors that are most (and least) likely to influence consumers’ menu item choice in a restaurant context.

The focus groups were moderated by Dr Hervé Remaud and Kimberley Peters of the Institute.

For the quantitative research, a questionnaire was developed (which is reproduced in Appendix 3) for administration via an online survey. The survey was conducted between 23rd and the 30th of September 2009.

Respondents were randomly selected from all Australian states and territories, ensuring a good representation of Australian casual and fine-dining restaurant patrons. The sample is further described hereafter. The results were analysed using a range of statistical techniques using the data analysis application SPSS 17 and Excel.

The average questionnaire length over all interviews was approximately 20 minutes.

Differences between sub-samplesBy default, all findings are presented split between the ‘Casual’, ‘Fine-dining’ and ‘Total’ groups. When the differences that exist between the dining groups in respect of the factors that influence their menu item choices are statistically significant, the results are indicated by an ‘*’. When comparing scale data, an analysis of variance (ANOVA) was performed. When comparing nominal data, a Chi-Square test was conducted.

Influences on Consumer Choices in Restaurants 9 Ehrenberg-Bass Institute—2010

Sample description

Table 2: Composition of the sample

SegmentationPeople having visited a

Casual-dining restaurant in the last 4 weeks

People having visited a Casual-dining restaurant

in the last 4 weeks

People having visited a Fine-dining restaurant in

the last 8 weeks

People having visited a Fine-dining restaurant in

the last 8 weeksTotalTotal

n % n % n %

Female 318 53 318 53 636 53

Male 285 47 287 47 572 47

NSW 206 34 185 31 391 32

Victoria 158 26 155 26 313 26

Queensland 106 18 119 20 225 19

WA 56 9 65 11 121 10

SA 49 8 49 8 98 8

Tasmania 15 3 13 2 28 2

ACT 11 2 13 2 24 2

NT 2 0 6 1 8 1

20 – 24 years old 22 4 47 8 69 6

25 – 34 years old 157 26 155 26 312 26

35 – 44 years old 169 28 171 28 340 28

45 – 54 years old 155 26 151 25 306 25

55 – 59 years old 100 17 81 13 181 15

< $15,000 54 9 42 7 96 8

$15,000 - $24,999 47 8 36 6 83 7

$25,000 - $39,000 83 14 73 12 156 13

$40,000 - $69,000 204 34 190 31 394 33

$70,000 - $99,999 140 23 154 26 294 24

$100,000 + 75 12 110 18 185 15

Total 603 100 605 100 1208 100

Both sub-samples (casual and fine-dining) are equally structured for all sub-groups of the population (gender, location, age and income)

Influences on Consumer Choices in Restaurants 10 Ehrenberg-Bass Institute—2010

OBJECTIVE 1: CONSUMERS’ RESTAURANT EXPERIENCEThis section describes consumers’ restaurant patronage behaviour in a restaurant context within the time period of the last 4-weeks for the casual restaurant patrons and of the last 8-weeks for fine-dining restaurant patrons.

Table 3: Penetration of restaurants visit

Food service outlet

PenetrationPenetrationFood service outlet n %

Casual 1126 93

Fast food 965 80

Take-away 939 78

Fine-dining* 848 70

Average 80

Casual-dining has a higher penetration rate than fine-dining restaurants

* Penetration measured over 8-weeks

Casual-dining has a higher penetration rate (93% of the respondents visited a casual-dining restaurant in the last 4 weeks) than fine-dining restaurants—70% of the sample respondents reported to have visited such an outlet during the last 8 weeks.

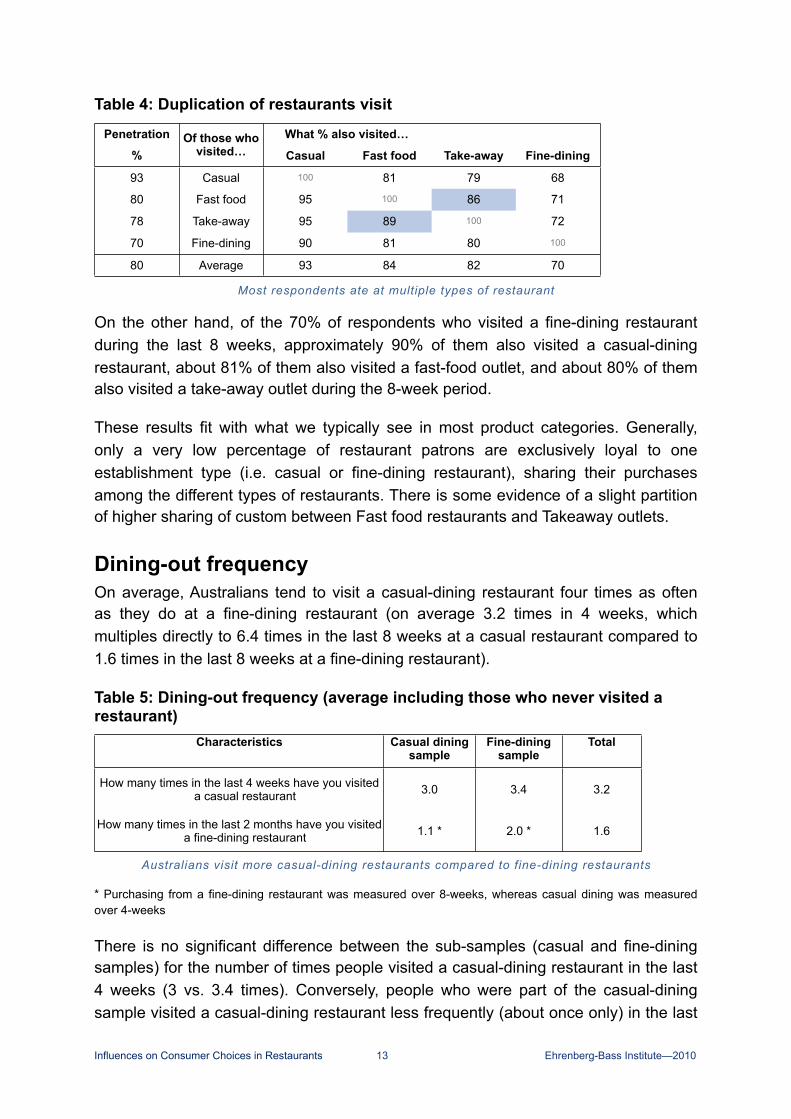

Duplication of restaurants visitIn this section, we examine the sharing of customers between the main categories of restaurants and eateries. We examine this by cross-tabulating the customers of each eatery type (i.e., casual restaurant) with the customers of every other eatery type (i.e., fast food) and examine the overlaps, or duplications; that is the proportion of people who bought both. Each category is listed in the first column, followed by a percentage which indicates the penetration of that category amongst the total sample.

The table can be interpreted as follows: Of the 93% of people who ate at a casual restaurant in the last month, 81% also ate at a fast food restaurant. Of the 80% of people who ate at a fast food restaurant in the last month, 95% also ate at a casual restaurant and so on. Of course, the diagonals total 100% (those who ate at a casual restaurant who ate at a casual restaurant), and thus these figures are shown in the table in a way so as to detract attention from these figures.

The key observation from duplication of purchase tables such as these is the comparison of figures down each column. In markets where customers divide their purchases among competing ‘brands’ (or, restaurant types in this example) freely,

Influences on Consumer Choices in Restaurants 11 Ehrenberg-Bass Institute—2010

that is, treating each brand as a substitute for every other, then the column figures will be extremely similar, or the same. And furthermore, the figures in each column will reflect the penetration of the brand, which are the figures in the first column from left.

This then means that the same proportion of each brand’s customers are dividing their purchases with each competitive brand, solely in line with the overall popularity of those competitive brands in each case. The implication of this then is that each brand is perfectly substitutable with each other, and the sharing is based only on the popularity (penetrations) of the brands.

Almost every product market or category exhibits this pattern of duplication of purchase. When there are discrepancies away from this overall pattern of equal figures within each column, this is an indication that sharing between two or more restaurant types might be higher (or, conversely lower), thus indicating that these restaurant types are closer (or more distant) competitors than they are with other eateries in the same market. Indeed, in certain of these situations, this can provide evidence that the market is not just one holistic market, but are in fact a number of somewhat separate markets.

The table below presents this information for the main restaurant types in the market. Inspecting them in this way therefore implies that we are initially treating them as if they are directly substitutable products with one another. Adherence to (or deviation from) this pattern will give us some evidence to say one way or the other whether this is a justified assumption.

The duplication of restaurant visits by casual and fine-dining patrons (shown in the Table below) indicates that of the respondents who visited a casual-dining restaurant during the last 4 weeks (93%), approximately 81% of those respondents also visited a fast-food outlet, approximately 79% of them also visited a Take-away outlet, and 68% of them also visited a fine-dining restaurant during the 4-week period. These results are very much in line with the average penetration rate of patrons visiting casual and fine-dining restaurants.

Influences on Consumer Choices in Restaurants 12 Ehrenberg-Bass Institute—2010

Table 4: Duplication of restaurants visit

Penetration

%Of those who

visited…What % also visited…What % also visited…What % also visited…What % also visited…Penetration

%Of those who

visited… Casual Fast food Take-away Fine-dining

93 Casual 100 81 79 68

80 Fast food 95 100 86 71

78 Take-away 95 89 100 72

70 Fine-dining 90 81 80 100

80 Average 93 84 82 70

Most respondents ate at multiple types of restaurant

On the other hand, of the 70% of respondents who visited a fine-dining restaurant during the last 8 weeks, approximately 90% of them also visited a casual-dining restaurant, about 81% of them also visited a fast-food outlet, and about 80% of them also visited a take-away outlet during the 8-week period.

These results fit with what we typically see in most product categories. Generally, only a very low percentage of restaurant patrons are exclusively loyal to one establishment type (i.e. casual or fine-dining restaurant), sharing their purchases among the different types of restaurants. There is some evidence of a slight partition of higher sharing of custom between Fast food restaurants and Takeaway outlets.

Dining-out frequencyOn average, Australians tend to visit a casual-dining restaurant four times as often as they do at a fine-dining restaurant (on average 3.2 times in 4 weeks, which multiples directly to 6.4 times in the last 8 weeks at a casual restaurant compared to 1.6 times in the last 8 weeks at a fine-dining restaurant).

Table 5: Dining-out frequency (average including those who never visited a restaurant)

Characteristics Casual dining sample

Fine-dining sample

Total

How many times in the last 4 weeks have you visited a casual restaurant 3.0 3.4 3.2

How many times in the last 2 months have you visited a fine-dining restaurant 1.1 * 2.0 * 1.6

Australians visit more casual-dining restaurants compared to fine-dining restaurants

* Purchasing from a fine-dining restaurant was measured over 8-weeks, whereas casual dining was measured over 4-weeks

There is no significant difference between the sub-samples (casual and fine-dining samples) for the number of times people visited a casual-dining restaurant in the last 4 weeks (3 vs. 3.4 times). Conversely, people who were part of the casual-dining sample visited a casual-dining restaurant less frequently (about once only) in the last

Influences on Consumer Choices in Restaurants 13 Ehrenberg-Bass Institute—2010

8 weeks compared to the people who comprised the fine-dining sample (twice in the last 8 weeks).

When thinking of the frequency of consumers’ casual-dining restaurant patronage (approximately 3 times in the last 4 weeks), it is logical to estimate that the average is comprised of people with a range of different frequencies of eating out: some people might not eat out at all in the 4 weeks; some eating out once; others twice; and so on. Plotting a histogram of the frequency of each eating occasion results in a distribution—the distribution of such purchase frequencies is typically the Negative Binomial Distribution (the NBD), rather than the Normal Distribution (a bell-shaped curve). The most obvious characteristic of the NBD is the bunching up of responses towards the left-hand end of the chart—the high proportion of people making low numbers of visits, 0, 1 or 2 purchases—and the corresponding long tail of small numbers of people making a higher number of purchases.

The majority of respondents reported visiting a casual-dining restaurant less than 3 times each month (see Figure 1). Similarly, most of the respondents who visited a fine-dining restaurant did so less frequently than the average (between once or twice depending of the subsample).

Figure 1: Distribution of casual-restaurant visits in the last 4 weeks

0%

23%

34%

14% 13%

5% 4% 1% 2%

0% 1% 0% 1% 0% 0% 1% 0% 0% 0%

5%

19%

26%

15% 16%

6% 5%

1%

4%

0% 1% 0% 0% 0% 0% 1% 0% 0% 0%

0% 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 18 20 30

Num

ber o

f res

pond

ent

Number of visit done in a casual restaurant in the last 4 weeks

How many times in the last 4 weeks have you visited a casual restaurant (excluding food court and fish & chips outlets)?

Casual Dining Sample

Fine Dining sample

Influences on Consumer Choices in Restaurants 14 Ehrenberg-Bass Institute—2010

Because a requirement to participate in the survey was to have visited a casual-dining restaurant at least once (for the casual dining sample) and a fine-dining restaurant at least once (for the fine-dining sample), the penetration rates for both are rather high; higher than we would expect in the population as a whole—only a few respondents had not visited one or the other type of restaurant in each sub-sample (casual vs. fine-dining).

The distribution (bunching up on the left, declining to a long tail on the right) is very similar in comparison to the frequency of patrons reporting to have visited a fine-dining restaurant (Figure 2), but even more pronounced, due to the lower penetration and purchase frequency of fine dining.

Figure 2: Distribution of fine-dining restaurant visits in the last 8 weeks

48%

28%

14%

4% 2% 1% 1% 0% 1% 1% 0% 0%

56%

26%

8% 5%

1% 1% 0%

2% 0% 1% 0%

0 1 2 3 4 5 6 7 8 10 20+

Num

ber o

f res

pond

ent

Number of visit done in a fine-dining restaurant in the last 8 weeks

How many times in the last 2 months have you visited a fine-dining restaurant?

Casual Dining Sample

Fine Dining sample

Most people dine at a fine dining restaurant very infrequently

Influences on Consumer Choices in Restaurants 15 Ehrenberg-Bass Institute—2010

Seafood consumption frequency when dining-out in a casual restaurantRespondents who reported visiting a casual-dining restaurant in the last 4 weeks (1,175 in total) were asked to estimate the number of times they ordered various seafood species in a casual-dining restaurant during the 4-week time period. We start to describe the results of this question with a presentation of the distribution for each species, followed by the presentation of the average number of times those species have been ordered compared to the average number of visits to a casual-dining restaurant.

Table 6: Distribution of purchase frequencies for seafood species within the last 4 weeks at a casual restaurant (excluding food court and fish & chip outlets)

Frequency Prawn Calamari Squid

Fresh Salmon

Barra mundi Scallop Oyster Snapper Fresh

Tuna Lobster Sardine

0 461 620 851 890 910 939 970 1022 1082 1127

1 521 413 249 244 210 182 176 113 78 33

2 133 92 47 28 38 38 23 24 14 11

3 28 26 13 6 7 7 3 7 1 2

4 18 14 7 4 6 4 2 2 0 0

5 8 6 7 1 2 3 1 5 0 0

6 3 2 1 1 1 1 0 1 0 0

7 0 0 0 0 0 0 0 0 0 1

8 0 0 0 0 0 0 0 0 0 0

9 1 0 0 0 0 0 0 0 0 1

10 2 2 0 1 1 1 0 1 0 0Penetration

(%)61 47 28 24 23 20 17 13 8 4

Based on these figures, one can calculate the penetration (i.e. the number of times each species was ordered at least once during the time period) of each species in the casual restaurant context for the last 4 weeks. Prawns appear to be by far the most popular seafood species to be ordered at a casual-dining restaurant with a penetration of 61%. On the other hand, sardines have the lowest penetration, with approximately only 4% of respondents who visited a casual-dining restaurant in the last 4 weeks having ordered them.

Based on the number of people who visited a casual-dining restaurant in the last 4 weeks, we can estimate the average number of visits and compare that figure with the average number of times a species was ordered (Figure 3). People visited a

Influences on Consumer Choices in Restaurants 16 Ehrenberg-Bass Institute—2010

casual-dining restaurant an average 3 times in the last 4 weeks. In line with the penetration rate of each species, the average number of times each species was ordered decreased from the penetration rate of prawns (ordered on average just under once in the last 4 weeks) to lobster and sardines with an average order of only 0.1 in the last 4 weeks. The average number of orders for each species does include people who never order the species as well as those who ordered a particular species at least once.

Figure 3: Average number of times a seafood species was ordered in a casual restaurant in the last 4 weeks

3.3

0.9

0.7

0.4 0.3 0.3 0.3 0.2 0.2 0.1 0.1

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

# of visit Prawn Calamari/Squid Fresh Salmon Barramundi Scallop Oyster Snapper Fresh Tuna Lobster Sardine

Mea

n

Visit and species

Average number of order of seafood species in a casual restaurant in the last 4 weeks (of those who consumed or not the species and visited at least once a casual restaurant)

Prawns and Squid are the most popularly ordered species at casual restaurants.

The previous chart shows the average number of purchases across all respondents, including the people who did not buy the species at all in the previous 4 weeks (their purchase rate was 0). Therefore, much of the difference between species is likely to be due to the high number of non-purchasers, especially for those species that had a low penetration.

Therefore, in order to separate the effect of the non-purchasers, we can analyse the average purchase rate for each species but only for those people who had bought the species in the previous 4 weeks; therefore, omitting in each case the non-purchasers. This is shown in the following table.

Influences on Consumer Choices in Restaurants 17 Ehrenberg-Bass Institute—2010

Table 7: Average number of orders of each species in last 4 weeks, of those who ordered each species at least once (at a casual restaurant)

Species Penetration%

Average number of

ordersPrawns 61 1.4

Calamari Squid 47 1.4

Fresh Salmon 28 1.4

Barra mundi 24 1.3

Scallops 23 1.4

Oysters 20 1.4

Snapper 17 1.2

Fresh Tuna 13 1.5

Lobster 8 1.2

Sardines 4 1.6

AverageAverage 1.4

Loyalty varies little: penetration matters most, as there’s not much difference between the purchase rates of species

On average, restaurant patrons who ordered prawns at least once, ordered prawns approximately 1.4 times during a 4-week period. The highest score is obtained for sardines, but which was only slightly higher, with an average number of times of only 1.6 times. This indicates that despite having a very low penetration rate (only 4 percent of people bought sardines in the 4-week period), those who did so ordered them about the same number of times as did buyers of other seafood species.

Loyalty varies littleWhen considering the responses of people who consumed each of the species at least once, the average number of times each was ordered now is very similar across all species—all are about 1.4 times. Despite the very large difference in penetration rates—about 15-fold, from 60% down to 4%—the average number of purchases (or, orders at the restaurant) of each species made by those people who bought the species at all hardly varied at all—a maximum of 1.6 to a minimum of 1.2.

This pattern—where the number of buyers varies a great deal, while purchase rates hardly vary at all—is not at all unique. In fact, this pattern holds in every competitive market where there’s repeat purchasing, wherever it has been examined. What this means is that loyalty (or, purchase rates in this instance) does not differ appreciably between brands (or, species in this instance), whereas the number of people who buy each species at all is the biggest difference between species—only 40% of people did not buy a restaurant meal including prawns in the last 4 weeks, compared to 96% of people who did not buy any sardines.

Influences on Consumer Choices in Restaurants 18 Ehrenberg-Bass Institute—2010

As is the case with all products in any industry around the world, the biggest marketing challenge facing the industry (collectively, but also individually within species industry groups) is how to build penetration. In order to grow, it is penetration that must move the most, and therefore getting more people to buy the species is a much bigger challenge than trying to get existing buyers to buy more or at a higher rate. But also, lifting the consumption of seafood in total, will lift the consumption of all species—‘a rising tide will lift all boats’.

Seafood consumption frequency when dining-out at a fine-dining restaurantRespondents who reported visiting a fine-dining restaurant during the prior 8 weeks (919 in total) were asked to estimate the number of times they ordered various seafood species in a fine-dining restaurant during that period of time. We start to describe the results of this question with a presentation of the distribution for each seafood species, and then present the average number of times those species had been ordered compared to the average number of visits to a fine-dining restaurant during the 8-week time period.

Table 8: Distribution of purchase frequencies for seafood species within the last 8 weeks at a fine-dining restaurant

Frequency Prawn Calamari Squid

Fresh Salmon

Scallop Oyster Barra mundi

Lobster Snapper Fresh Tuna

Sardine

0 479 666 686 706 711 729 785 810 838 897

1 349 200 199 178 173 172 120 90 60 16

2 62 31 18 24 17 11 5 11 13 1

3 16 1 6 4 9 1 7 4 4 2

4 4 6 5 3 3 3 1 0 2 0

5 4 1 2 2 3 1 0 1 1 2

6 3 1 1 0 2 1 0 1 0 0

7 0 0 0 0 0 0 0 0 0 0

8 0 0 0 0 0 0 0 0 0 0

9 0 0 0 0 0 0 0 0 0 0

10+ 2 3 2 2 2 1 1 2 1 1Penetration

(%)48 28 25 23 23 21 15 12 9 2

Prawns are (still) the most popular seafood species ordered at fine-dining restaurants with a penetration of 48%, followed again by squid (28%). Conversely, sardines has the lowest level of penetration, with approximately 2% of respondents who visited a fine-dining restaurant ordering sardines in the last 8 weeks.

Influences on Consumer Choices in Restaurants 19 Ehrenberg-Bass Institute—2010

Table 9: Comparison of penetrations of species between casual and fine-dining restaurants

Species Penetration%

Casual

Penetration%

Fine-diningPrawns 61 48↓

Calamari Squid 47 28↓

Fresh Salmon 28 25

Barramundi 24 21

Scallops 23 23

Oysters 20 23

Snapper 17 12↓

Fresh Tuna 13 9↓

Lobster 8 15↑

Sardines 4 2

Except for lobster, penetration is generally lower in fine-dining than in casual restaurants

Despite the longer period of time investigated (8 weeks for fine-dining versus 4 weeks for casual), the penetration rate of each species in fine-dining is generally lower in comparison to its penetration at casual–dining restaurants. Lobster is the biggest exception to this, where its penetration doubles for fine-dining; an issue primarily of availability, where lobster is typically unavailable in casual restaurants. However, oysters and scallops also have high penetrations in fine-dining restaurants; and are both higher than for Barramundi.

This general lower level of penetration of each species is mainly just a reflection of the lower penetration of fine dining compared to the penetration of casual dining: penetration of casual dining was 3.2 times in 4 weeks, c.f. 1.6 times for fine dining in 8 weeks.

As for the casual-dining restaurant patrons, the penetration rate for consumption of all seafood species should be interpreted keeping in mind the physical availability of particular species in casual-dining restaurants. In other words, sardines have the lowest penetration rate because they are not very popular from a consumer perspective but also because they are not widely available in a restaurant context. Therefore, if the species is not available on the menu, consumers cannot purchase it.

Based on the number of people who visited a fine-dining restaurant during the last 8 weeks (919), it is possible to estimate the average patronage of fine-dining restaurant patrons and compare that figure with the average number of times a particular seafood species was ordered (Figure 5). The sample of restaurant patrons visited a fine-dining restaurant an average of just over 2 times during the last 8 weeks.

Influences on Consumer Choices in Restaurants 20 Ehrenberg-Bass Institute—2010

Again for fine-dining restaurants, in line with the penetration rate for each seafood species, the average number of times that each species was ordered decreased from the most popular species, prawns (ordered on average just under once during the last 8 weeks), to fresh tuna and sardines with an average order of 0.1 during the last 8 weeks. The average number of orders shown below in figure 5 again includes non-purchasers.

Figure 4: Average number of times seafood species were ordered at a fine-dining restaurant during the last 8 weeks

2.1

0.7

0.4 0.4 0.3 0.3 0.3 0.2 0.2 0.1

0.1 0.0

0.5

1.0

1.5

2.0

2.5

# of visit Prawn Calamari/Squid

Fresh Salmon

Scallop Oyster Barramundi Lobster Snapper Fresh Tuna Sardine

Mea

n

Visit and species

Average number of order of seafood species in a fine-dining restaurant in the last 8 weeks

(of those who consumed or not the species and visited at least once a fine-dining restaurant)

However, when we consider only the responses of restaurant patrons who consumed each of the seafood species at least once during the 8-week period, the average number of times a particular species was ordered again becomes very similar across all species.

Influences on Consumer Choices in Restaurants 21 Ehrenberg-Bass Institute—2010

Table 10: Average number of orders of each species in last 8 weeks, of those who ordered each species at least once (at a fine-dining restaurant)

Species Penetration%

Average number of

ordersPrawns 48 1.4

Calamari/Squid 28 1.5

Fresh Salmon 25 1.5

Scallops 23 1.4

Oysters 23 1.4

Barramundi 21 1.2

Lobster 15 1.3

Snapper 12 1.9

Fresh Tuna 9 1.5

Sardines 2 2.2

AverageAverage 1.5

Again, penetration matters most. There is not much difference in purchase rates of species.Snapper and Sardines have higher rates of purchase than other species

On average, patrons who ordered prawns at least once at a fine-dining restaurant, ordered prawns approximately 1.4 times during an 8-week period (the same as for casual-dining restaurant patrons during the last 4 weeks). As can be seen in the table above, sardines again were ordered at a high rate by the few people who did order it at all in fine-dining restaurants. Similarly, Snapper has a low level of penetration, but a higher average purchase rate among those consumers who purchased Snapper at least once during the 8-week period. Furthermore, whereas Snapper was purchased below the average of other species in casual restaurants, in fine-dining restaurants, it was purchased above the average of other species; indicating that it is more popular as a meal in fine-dining restaurants than in casual restaurants.

Loyalty varies littleAgain, just as was the case with casual dining, the average number of times each was ordered now is very similar across all species—all are about 1.5 times. Despite the very large difference in penetration rates—over 20-fold, from 48% down to 2%—the average number of purchases of each species made by those people who bought the species at all varied very little—from a maximum of 2.2 to a minimum of 1.2. Clearly, sardines, and to a lesser extent snapper, are exceptions to this. Perhaps it is the small size of sardines that results in the species having such a high average order rate; or it could be due to the unique preparation or taste of sardines in comparison to other seafood.

Again, this pattern—where the number of buyers varies a great deal, while purchase rates hardly vary at all—is common to every competitive market where there’s repeat purchasing. And what this means is that loyalty does not differ appreciably between

Influences on Consumer Choices in Restaurants 22 Ehrenberg-Bass Institute—2010

species, whereas the number of people who buy each species at all is the biggest difference between species—only 52% of people did not buy a prawns meal at a fine-dining restaurant in the last 8 weeks, compared to 98% of people who did not buy any sardines meals.

Therefore, the biggest marketing challenge facing the industry remains the necessity of building penetration. In order to grow, it is penetration that must move the most, and therefore getting more people to buy seafood is a much bigger challenge than trying to get existing buyers to buy more or at a higher rate.

Money spent for a dishRespondents were asked to indicate the amount of money that they would usually spend on various dishes (a red meat dish; a white meat dish; a shellfish dish; a fish dish and a vegetarian dish) at a restaurant. Respondents were asked to consider the context of eating at either a casual restaurant or at a fine-dining restaurant.

Figure 5: Money spent for a red meat dish in a casual vs. fine-dining restaurant

3% 2%

10%

31% 30%

18%

4%

1% 1%

3%

1%

4%

12%

25%

31%

11%

8%

4%

0%

5%

10%

15%

20%

25%

30%

35%

0 $10 or less $11-$15 $16-$20 $21-$25 $26-$30 $31-$35 $36-$40 >$40

% re

spon

dent

s

Price tiers

How much would you usually spend for a Red Meat dish (for yourself and excluding beverages)?

Casual Dining Sample

Fine Dining Sample

Most people will usually pay $16-25 for a red meat dish at a casual restaurant; $26-30 from a fine-dining restaurant

The distributions for the usual expenditure on a red meat dish from casual and fine-dining restaurants are both normally distributed (bell-shaped). The majority of the casual-dining sub-sample would usually spend between $16 and $25 on a red-meat dish. On the other hand, most respondents of the fine-dining sub-sample would usually spend between $26 and $30 for a red meat dish.

Influences on Consumer Choices in Restaurants 23 Ehrenberg-Bass Institute—2010

In looking at those respondents who spent $15 or more for a main meal in both types of restaurant, on average casual-dining patrons usually spend $24 on a red meat dish, compared to $29 form a fine-dining restaurant.

Figure 6: Money spent for a white meat dish in a casual vs. fine-dining restaurant

2% 3%

19%

42%

21%

9%

2% 0% 1% 1% 1%

8%

25% 27%

25%

7%

4%

2%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

0 $10 or less $11-$15 $16-$20 $21-$25 $26-$30 $31-$35 $36-$40 >$40

% o

f res

pond

ents

Price tiers

How much would you usually spend for a White Meat dish (for yourself and excluding beverages)?

Casual Dining Sample

Fine Dining Sample

Again, the distributions of the usual expenditures on white meat dishes from both casual-dining and fine-dining restaurants were approximately normally distributed. Most respondents usually spending $16-20 on a white meat dish in a casual restaurant and $21-25 from a fine-dining restaurant. However, there was larger variation around this average expenditure in fine-dining restaurants than for red-meat.

In looking at those respondents who spent $15 or more for a main meal2 in both types of restaurant, on average casual-dining patrons usually spend $22 on a red meat dish, compared to $25 from a fine-dining restaurant.

Influences on Consumer Choices in Restaurants 24 Ehrenberg-Bass Institute—2010

2 Because we stated during the interview that a main plate in a casual restaurant would cost about $15 to $30 and about $30 to $50 in a fine dining restaurant, we focus the analysis on the responses above $15.

Figure 7: Money spent for a shellfish dish in a casual vs. fine-dining restaurant

9%

1%

8%

25%

28%

19%

5% 3%

6%

11%

1%

4%

8%

18%

24%

13%

11%

20%

0%

5%

10%

15%

20%

25%

30%

0 $10 or less $11-$15 $16-$20 $21-$25 $26-$30 $31-$35 $36-$40 >$40

% o

f res

pond

ents

Price tiers

How much would you usually spend for a Shellfish dish (for yourself and excluding beverages)?

Casual Dining Sample (n=603) Fine Dining Sample (n=605)

‘Lobster effect’: a large number of people are willing to pay high amounts on shellfish (presumably lobster) at fine dining restaurants. There’s also a number not willing to buy any shellfish.

While the dominant feature of the distributions of expenditures on shellfish is the normal distribution, there are some unique characteristics in comparison to what was seen in red and white meats. In both the casual and fine-dining contexts, we see a group of people who will not buy any shellfish at all—some of this will be due to people having an allergy to shellfish. However, we also see a pronounced ‘kick-up’ in the tail at the right hand of the chart, indicating a group of people willing to pay more than $40 for a meal with shellfish. This is much more pronounced in the case of fine-dining restaurants than in casual restaurants—the ‘lobster effect’.

The average expenditures that people would usually make for shellfish from both casual and fine-dining restaurants were higher than for either of the meats. On average, among those who spent $15 or more for a main meal in both types of restaurant, we found that casual-dining patrons usually spend $26 for a shellfish dish, c.f., $32 for fine-dining patrons.

Influences on Consumer Choices in Restaurants 25 Ehrenberg-Bass Institute—2010

Figure 8: Money spent for a fish dish in a casual vs. fine-dining restaurant

2% 3%

17%

37%

25%

11%

2% 1% 1% 3%

1%

6%

18%

24%

29%

10%

5%

8%

0%

5%

10%

15%

20%

25%

30%

35%

40%

0 $10 or less $11-$15 $16-$20 $21-$25 $26-$30 $31-$35 $36-$40 >$40

% o

f res

pond

ents

Price tiers

How much would you usually spend for a Fish dish (for yourself and excluding beverages)?

Casual Dining Sample (n=603) Fine Dining Sample (n=605)

Fish has broader appeal than does shellfish

In comparison to shellfish, there are fewer people with an aversion to fish; most are willing to buy fish at the restaurant as the number of people who do not order fish at all is quite low. The difference between the usual expenditures from casual to fine-dining restaurants is more pronounced for fish dishes than for meats and for shellfish; with most casual diners paying $16-20 versus $26-30 for fine-dining patrons. Furthermore, whereas there is a pronounced ‘kick-up’ in the tail among the fine-dining patrons here in relation to fish, as there was for shellfish previously, this is not evident among the casual diners—casual diners don’t usually pay more than $30 for a fish meal.

On average, among those who spent $15 or more for a main meal in both types of restaurant, casual-dining patrons usually spend $22 for a fish dish, c.f., $27 for fine-dining patrons.

Influences on Consumer Choices in Restaurants 26 Ehrenberg-Bass Institute—2010

Figure 9: Money spent for a vegetarian dish in a casual vs. fine-dining restaurant

24%

12%

30%

27%

5%

1% 1% 0% 0%

24%

6%

20%

26%

14%

7%

1% 1% 0%

0%

5%

10%

15%

20%

25%

30%

35%

0 $10 or less $11-$15 $16-$20 $21-$25 $26-$30 $31-$35 $36-$40 >$40

% o

f res

pond

ents

Price tiers

How much would you usually spend for a Vegetarian dish (for yourself and excluding beverages)?

Casual Dining Sample (n=603) Fine Dining Sample (n=605)

Many people are unwilling to buy a vegetarian meal

Given the large proportion of respondents who reported an unwillingness to spend their money on a vegetarian dish, there is evidence to suggest that a large majority of both casual and fine-dining restaurant patrons avoid the consumption of vegetarian dishes when dining out. We again see that fine-dining sample respondents spend more on average in comparison to casual-dining restaurant patrons. However, both groups usually expect to spend less for vegetarian meals than for meals with other proteins. The majority of the casual-dining sample respondents spend approximately $11 to $20 on a vegetarian dish, whereas fine-dining restaurant patrons spent $16 to $20 on average.

On average, among those who spent $15 or more for a main meal in both types of restaurant, casual-dining patrons usually expect to spend $19 for a vegetarian dish, c.f., $21 for fine-dining patrons.

Influences on Consumer Choices in Restaurants 27 Ehrenberg-Bass Institute—2010

Figure 10: Average expenditure for a dish in a casual vs. fine-dining restaurant (for a dish valued $15 or more)

24

21.5

25.5

22.5

18.6

29

25.3

32

27

21

0

5

10

15

20

25

30

35

Red meat White meat Shellfish Fish Vegetarian

$

Main ingedient of meal

Average expenditure for a dish in casual vs. fine-dining restaurant Casual Dining Sample (n=603)

Fine Dining Sample (n=605)

People expect to pay more at fine-dining than casual restaurants.People expect to pay most for shellfish dishes.

Overall, one can assume that when dining out, people are only willing to spend slightly more for a shellfish dish compared to all other dishes (Figure 12). And people would spend slightly more for a red meat dish than for a fish dish.

Influences on Consumer Choices in Restaurants 28 Ehrenberg-Bass Institute—2010

Number of red/white meat, shellfish, fish and vegetarian dishes ordered at a casual-dining restaurantThis section describes the number of red/white meat, shellfish, fish and vegetarian dishes that casual-dining restaurant patrons ordered during a 4-week period.

Figure 11: Number of red meat dishes ordered at a casual restaurant during the last 4 weeks

75

65

17 11 3

1 1 1 2

54

92

41

29

9

7

0

5

1

5

41

17

24

11

8

3

1

4

3 4

7

7 3

2

4

0

3

1 1 2

6 3

3 0

4

1

0 0 0 0 0

2

0 1

1

1 1 2 3 0 0

1 1

8

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1 2 3 4 5 6 7 8 9+

# an

d %

of r

espo

nden

ts

Number of visit to a casual restaurant in the last 4 weeks

Number of people having ordered a red meat meal * Number of time they visited a casual restaurant in the last 4 weeks

6+ orders

5 orders

4 orders

3 orders

2 orders

1 order