Embed Size (px)

Citation preview

ALSO IN THIS ISSUE> Shop View: Making the Journey to a Lean Shop

> A Look into Future Technology:

Electric Vehicles and License-Plate Scanning

> Much More

AudatexDirectionsNews from Audatex North America, Inc. Vol 04

What DrivesHybrid Repair Costs?Industry professionals are already aware that hybrids generally cost more to repair than their gasoline counterparts. The question is, “How much more?”

Audatex Directions is a quarterly newsletter that provides in-depth trends and industry analysis on the auto physicaldamage market. It is published by AudatexNorth America, Inc., a Solera Company.

EditorKate LosCorporate Communications Manager

Contributing WritersMichael T. AndersonSr. Director of Data Analytics, Audatex

Tanya ElkinsProduct Manager, Autosource, Audatex

Diane KlundRegulatory Compliance Manager, Audatex

Charles LukensCEO, APU Solutions

Krishna MasurLean Six Sigma Black Belt, Audatex

Dave TrisselAssociate VP of Process Excellence,Audatex

Brian VannoniSr. Director, Product Management, Audatex

Request CopiesTo request a printed copy of this publication,please email: [email protected]

To download the pdf, please visit ourWeb site: http://audatex.us/thinktank.aspx

Local focus. Global knowledge.

Audatex is the leading global claimssolutions provider. As part of the Soleragroup of companies, we draw on our broadglobal claims market experience to identifyand implement the best-practice processesthat drive continuous improvement for ourlocal customers and their trading partners.Solera companies serve the automotiveindustry in more than 50 countries acrosssix continents.

© 2009 Audatex North America, Inc. All rights reserved.Audatex, AudaInsight, Autosource, Audatex Estimating,Audatex Win-EMR, PenPro and Shoplink are trademarks orregistered trademarks of Audatex. All other companyand/or product names may be trademarks or registeredtrademarks of their respective owners in the United Statesand other countries.

ContentsManaging Director’s Message

Feature Article–What Drives Hybrid Repair Costs?

Industry Trends

–Are Electric Vehicles the Answer?

–Vehicle Sales and Actual Cash Values

–Staying On Top of Vehicle-Value

Fluctuations

Shop View–Making the Journey to a Lean Shop.

Part 1: Why Lean? Why Now?

A Look into Future Technology–Auto Thieves’ Newest Opponents:

License-Plate Scanners

Regulatory Highlights–Total Loss Changes on the Horizon

in the Northwest U.S.–New York Kicks Off 2009 with a

New Flex-Rating Program

Industry Collaboration–Audatex and APU to Launch

Integrated Recycled-PartsProcurement Solution

–Repairers and Insurers GuideInaugural Meeting of AudatexTechnical Advisory Council

Audatex News and Events–Audatex’s Parent Company

Strengthens Its Global LeadershipThrough the Acquisition of Two NewCompanies

–Revamped Online Training CenterWill Help Users Unleash the Power of Their Audatex Solutions

– In Memoriam:Wadine Traylor-Freeman

–Upcoming Events

34

15

17

18

21

23

Audatex Directions

9

Positioning Yourself for Success in 2009

While 2009 holds the promise of a new year, it also brings about some uncertainty ofwhat’s to come. But, one thing is clear—2009 will demand that you approach business inan informed, strategic and disciplined manner.

With this edition of Audatex Directions, we aim to provide insight that will help you preparefor success in 2009. We do so by first digging deeper into key industry trends that mayimpact your business. In our feature story, we look at the factors influencing hybrid repaircosts and what this can mean for your bottom-line. We then examine how a changingeconomy can influence vehicle sales and values and how you can stay on top of thesefluctuations. Looking ahead, we explore how up-and-coming innovations like electricvehicles and license plate-scanners may impact your business in the future.

Recognizing that in 2009 efficient business processes will be more important than ever, weare introducing a series of articles that explore how proven Lean Six Sigma methodologiescan be applied to collision repair, ultimately helping to improve shop productivity,customer satisfaction, and business-growth potential.

As the year 2009 commenced, so did changes on the regulatory front. To help you stay ontop of these changes, we’ve included details around total loss regulation in the NorthwestU.S. and a new flex-rating program in New York.

On the Audatex news front, we report on initiatives that will help us best serve you in yourquest for success. Read about our parent company’s strategic acquisition of companieswhose solutions could potentially aid in additional markets. Learn how we’re teaming upwith APU Solutions to deliver a powerful search and procurement solution that will helpyou maximize the use of recycled parts. See how our collaboration with users in the newAudatex Technical Advisory Council will help us deliver solutions that best meet industryneeds. And, learn how you can ensure you’re getting the most from your investment inAudatex solutions by leveraging the newly revamped Audatex online training center, whichis coming this month.

Finally, please take a moment to read the tribute to Wadine Traylor-Freeman, our colleaguewho passed away last fall after a brave battle with cancer. Wadine has left a lastingimpression on her colleagues, not only because of her 25 years of impressive work, butmore importantly because of her warm personality and genuine care for others. She will not be forgotten.

Regards,

John Kotsopoulos,Managing DirectorAudatex North America, Inc.

3www.audatex.us

‘‘’’

With this edition of

Audatex Directions,

we aim to provide

insight that will help

you prepare for

success in 2009.

Managing Director’s Message

4 Audatex Directions Vol 4

When comparing hybrids to gasoline-poweredvehicles, many look very much the same.However, hybrids are much more complex andhave traditionally cost more to repair. Becausehybrid sales represent a growing percentage ofnew vehicles sales, these increased costs havebeen a concern for many. And, although recentreductions in fuel costs and a lagging economycaused hybrid sales to drop 10 percent in late2008 compared to 2007, they still represented2.6 percent of new car sales in October 2008.As a result, companies must take a closer lookat the underlying factors driving hybrid repaircosts, such as their unique qualities, the limitedavailability of alternative parts, and theopportunity for more consistent appraisalpractices.

Hybrid Claim DistributionAs fuel prices reached record levels in recentyears, the need for more fuel efficient vehiclesforced manufacturers to develop new hybridvehicles or create hybrid cross-over versions ofexisting gasoline models. Since its introductionto the U.S. market in 2000, the Toyota Prius hasled all hybrid car sales, and in 2008 it enteredinto the top 10 of all vehicles sold. Notsurprisingly, during 2008, the Prius alsorepresented the majority of hybrid insuranceclaims (figure 1).

What Drives HybridRepair Costs?Industry profess ionals are a l ready awarethat hybr ids genera l ly cost more torepai r than the i r gasol ine counterparts .The quest ion is , “How much more?”

By Michael T. Anderson

Feature Article

Continued next page

Figure 1: Hybrid claim distribution in 2008 bymodel type as a percentage of all hybrid claims.(Source: Audatex® Insight™)

Claim Distribution by Hybrid Model in 2008

4%4%6%7%

11%

15%

51%

3%

Toyota Prius

Lexus RX 400h

Honda Civic

Ford Escape

Toyota Camry

Honda Accord

Toyota Highlander

Other (17 models)

Hybrid vehicles that have a gasoline counterpartaveraged 3.8 percent more to repair on a weightedbasis than their comparable gasoline-only models(figure 3).

A review of repair costs over time suggests thatgreater differences exist in early model years,while the repair costs for newer model years arenearly identical. As discussed in the followingsection, specific factors are driving these trends.

Part-Dollar DistributionTo explore the underlying factors influencinghigher hybrid repair costs, we reviewed the part-dollar percentage for each of the four standard

part classifications (OEM, aftermarket,recycled and other) represented in terms oftotal part dollars.

Part-Dollar Distribution: Toyota Prius versus Gasoline-PoweredEconomy ImportsTo begin, we examined the Toyota Priusversus gasoline-powered economyimports. As shown in figure 4 (on the nextpage) OEM part utilization is much higheron the Prius.

Why is OEM part utilization so muchhigher in the Prius? Consider this—the

Prius was introduced to the U.S. market in 2000,and it took nearly five years to reach 330,000 unitssold. It wasn’t until 2005 that Toyota sold morethan 100,000 units in a single year. The limitednumber of unit sales during these early modelyears now directly impacts aftermarket andrecycled part availability.

5www.audatex.us

As the prevalence of hybrid vehicles increases interms of both numbers produced and modelsoffered, claim and underwriting professionals willneed a better understanding of repair costs andinfluencing factors.

Average Repair CostsIndustry professionals are already aware thathybrids generally cost more to repair than theirgasoline counterparts. The question is, “Howmuch more?” To better answer this question,we performed two separate analyses.

• In the first analysis, we examined averagerepair costs for the Toyota Prius relative tothe gasoline-powered economy-import class.Sixty-eight percent of this class is comprisedof the Honda Accord, Honda Civic, ToyotaCorolla, Nissan Sentra, and Hyundai Elantra.

• The second analysis isolated hybrid cross-over vehicles that have a gasoline counterpart.The comparisons for this hybrid populationwere made directly to their gasolinecounterparts.

In our first set of analyses, we found that onaverage in 2008, the Toyota Prius cost 8.4 percent more to repair than the gasoline-powered economy imports (figure 2).

Figure 2: Average repair costs by model yearfor the Toyota Prius versus gasoline-poweredeconomy imports. (Source: Audatex Insight)

Feature ArticleCont inued f rom prev ious page

Continued next page

$2,300

$2,500

$2,700

$2,900

$2,100$1,900$1,700$1,500

2001 2002 2003 2004 2005 2006 2007 2008

Prius Average Repair CostEconomy Import Average Repair Cost

Repair Costs by Model Year:Toyota Prius vs. Gasoline-Powered Economy Imports

$2,300

$2,500

$2,700

$2,900

$2,100$1,900$1,700$1,500

2003 2004 2005 2006 2007 2008

Hybrid Gas Equivalent

Repair Costs by Model Year:Hybrids versus Gasoline Equivalents

Figure 3: Averagerepair costs by modelyear for hybrid vehiclesversus their gasolinecounterparts. (Source: Audatex Insight)

6 Audatex Directions Vol 4

because in the 2003, 2004 and 2005 modelyears, the majority of hybrid claims were for theHonda Civic Hybrid, which has manyinterchangeable parts with its gasoline-poweredcounterpart and therefore allows for greaterusage of alternative parts in the repair process.

Overall, the ability to identify, locate andsubsequently provide alternative parts that areunique to a hybrid cross-over (i.e., not shared bythe gasoline counterpart) requires a precise part-interchange process, accurate inventory recordsby the recycler and, frequently, extended partsearches by appraisers.

OEM Part Costs

We examined some commonly replaced partsand compared the OEM price for hybrid partsversus gasoline parts based upon year, make,model and specific part. While many of thehybrid parts cost the same as their gasoline

counterparts, some significant differences existat the part level that impact alternative-partavailability and overall repair costs (figure 6).

For the majority of parts with significant OEMprice differences, the discrepancy can be traceddirectly to new (and frequent) design changesthat are made by manufacturers in efforts to

As fuel prices rose during 2006 through 2008,Prius sales exploded, doubling the previousfive-year total. Cumulative sales now exceedone million vehicles. Not surprisingly, claimfrequencies are also skewed towards thesenewer model years. In 2008, 66 percent ofall Prius claims were for model year 2006 orhigher. In contrast, only 44 percent of allgasoline-poweredeconomy importsfell into this range.This skew towardnewer Priusmodels, alongwith insurer partpolicies andlimited alternative-part availability, allimpact OEM partpercentages.

Part-DollarDistribution: Hybrids versus their Gasoline-PoweredCounterpartsIn our second set of analyses, we looked atpart-dollar distribution for hybrids versus theirgasoline-powered counterparts. As seen infigure 5, hybrids also have higher OEM partpercentages than their gasoline counterparts,but the difference is notably less than that seenwith the Prius (as seen in figure 4).

There is a specific reason why the differencesbetween OEM part usage for these hybridsversus their counterparts are not as great asthose for the Prius versus economy imports. It is

Part-Dollar Distribution: Prius versus Gasoline-PoweredEconomy Imports (as percentage of total dollars spent)

20012002200320042005200620072008

OEM Aftermarket Recycled Other

Prius Prius Prius PriusEconomyImport

EconomyImport

EconomyImport

EconomyImport

7576818184868995

5255596366738393

44377654

17161414131074

1414885430

26232017161262

76844431

56765541

Feature ArticleCont inued f rom prev ious page

Figure 4: A comparison ofpart-dollar distribution showsa significantly higherutilization of OEM parts inearly-year Prius modelscompared to gasoline-powered economy imports(highlighted in orange).(Source: Audatex Insight)

Part-Dollar Distribution: Hybrids versus Gasoline Counterparts(as percentage of total dollars spent)

200320042005200620072008

OEM Aftermarket Recycled Other

Hybrids Hybrids Hybrids HybridsGasoline Gasoline Gasoline Gasoline

637074848994

565966738493

151612754

1617141174

1599431

2218141061

765541

566642

Figure 5: A comparison of part-dollar distributionshows a higher utilization of OEM parts in early-year hybrids versus their gasoline counterparts(highlighted in orange), but the difference is not asgreat as seen with the Prius (as seen in figure 4).(Source: Audatex Insight)

Continued next page

7www.audatex.us

reduce hybrid vehicle weight or betteraccommodate the hybrid system. For example,many manufacturers developed variations of adual-scroll air-conditioning compressor thatutilizes two compressors in one—aconventional, belt-driven scroll compressor forwhen the vehicle is running on gasoline powerand a smaller, electric compressor for when thevehicle is running on battery power. The newhybrid compressor technology represents a$200 part-price difference compared to the costfor a compressor used in gasoline only models.Depending on the model year and vehicle, othercostly modifications (i.e., modificationsrepresenting a greater than $100 per-partdifference) include incorporating aluminumhoods and fenders, aluminum bumper rails,modified airbag control modules, redesignedgrills and head lamp/tail lamp assemblies andradiators to support the hybrid system. Thesesubtle design differences can result in higherpart prices, repair costs and limited alternative-part availability.

Labor Rates and Labor HoursLabor ratios and rate variances also impactrepair costs for hybrids. As seen in figure 7,when comparing the weighted-average laborcost for hybrids versus their gasolinecounterparts and gasoline-powered economy

Continued next page

Feature ArticleCont inued f rom prev ious page

imports, hybrid claims yield both higher laborhours and rates.

The variance in sheet metal labor hours isexplained, in part, by the repair versus replaceratio. Hybridvehicles have anaverage sheet-metal-repair ratioof 42.7 percent,while theirgasolinecounterparts andgasoline-poweredeconomy importshave an averagerepair ratio of40.6 percent.Repairpercentages andlabor hours forhybrids werehigher duringmodel years 2001through 2005, and these figures subsequentlydeclined in 2006 through 2008, at which pointthey reflected nearly identical results tocomparable gasoline vehicles.

Compared to non-hybrids, hybrid labor rateswere on average $1.74 per hour higher forrefinish work, $1.71 per hour higher for sheetmetal, $6.42 per hour higher formechanical/electrical and $2.12 per hour higherfor frame work. A portion of these results isreflective of the geographic distribution ofhybrid vehicles in the U.S. (figure 8 on nextpage), and the higher costs of repairs in thoseareas, as well as the higher percentage ofdealership repairs, and increased insurer-applied electrical labor rates on hybridestimates.

As illustrated in figure 7, the biggest differenceis seen for the shift in mechanical/electricallabor hours. Data suggests this increase may bedue to several contributing factors, including theincreased frequency and hours needed todisconnect and reconnect a hybrid battery, aswell as the increased hours and other itemssuch as the rates that are applied to reset

$80

$100

$120

$140

$60$40$20$0

2003 2004 2005 2006 2007 2008

Hybrid Gas Equivalent

Average OEM Part Cost by Model Year:Hybrids vs. Gasoline Equivalents

Figure 7: Percentvariance of labor ratesand hours for hybridsversus the baseline seenfor their gasolinecounterparts andgasoline-poweredeconomy imports.(Source: Audatex Insight)

Figure 6: Average OEM part cost by modelyear for hybrids and their gasoline equivalents.(Source: Audatex Insight)

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

0.0%-2.0%-4.0%-8.0%

Refinish Sheet Metal Mech/Elec Frame

Percent of Change - Rates Percent of Change - Hours

Percent Variance in Labor Ratesand Hours for Hybrids

4.0% 4.4%

-4.1%

3.9%

1.4%

5.1%

10.1%

14.6%

Feature ArticleCont inued f rom prev ious page

electrical components in hybrid vehicles. Thetime allowed to reset electrical components inhybrids takes on average .52 hours versus.46 hours for gasoline vehicles, or $7.00 moreper claim. A review of electrical-related,manually-entered line-item entries shows thereare opportunities for insurers and repairers tobetter leverage their estimating system’sautomatic entries versus manual entries, as wellas for more consistent definition and applicationof hours and rates for hybrid-specific electricoperations.

Hybrid Trends, Moving ForwardDespite the recent decline in sales, automakersare more committed to hybrids than ever.Toyota, Honda, General Motors, Ford andChrysler all announced continued plans toaggressively expand their hybrid-vehiclemarkets. In fact, General Motors announcedplans to have 15 hybrid models by 2012 andother manufacturers are investing heavily in theelectric-vehicle market.

As such, the following factors that driveincreased hybrid repair costs should be keptin mind.

• Until a more significant market share isobtained by hybrid vehicles, a higherpercentage of hybrid-vehicle-only claims(versus cross-over-vehicle claims) may limitalternative-part availability for several years tocome.

• Subtle, yet costly, design changes on cross-over vehicles increase part prices andnegatively impact the availability of hybrid-specific parts.

• Labor rates on electrical-related procedurestend to be higher and inconsistently appliedfor hybrid vehicles.

• Use of aluminum (light weight) panels onhybrids changes the repair process.Traditional steel panels have “memory”allowing for standard repair versus replacedecisions. Aluminum is a softer metal anddoes not have the repairability characteristicsthat steel offers.

As additional cross-over vehicles enter themarket and more alternative parts becomeavailable for hybrid-only models, insurers shouldsee hybrid repair costs fall more in line with theirgasoline counterparts. However, it remainsimportant for insurers to understand howvehicle-specific design differences can impactloss costs. This requires insight to part-leveldata and an effective alternative-parts strategy.The parts analytics module in the AudatexInsight business intelligence tool can greatlyassist your organization in understanding line-item, part-level and behavioral trends andvariances. For more information on AudatexInsight, visithttp://audatex.us/insurance_solutions/reporting_solutions.aspx. n

States with the Most Hybrid Sales

Rank State New Hybrids*1

2

3

4

5

California

New York

Texas

Florida

Illinois

67,92315,435

14,43014,387

11,252

*Year to date - October 2008. (Source: Hybridcars.com)

Figure 8: States with the mosthybrid sales as of October 2008.

The parts analytics

module in the

Audatex Insight

business

intelligence tool can

greatly assist your

organization in

understanding line-

item, part-level and

behavioral trends

and variances.

Audatex Directions Vol 48

It is estimated that in 2007 vehicles on U.S.roads consumed in excess of 140 billion gallonsof gasoline. Although hybrids offered vehicleowners some relief from the record-highgasoline prices seen in 2008, manufacturersand venture capitalists across the globerecognize the severity of the situation andcontinue to search for true fossil-fuelreplacements. Thus, the crucial question for allthose involved in the automotive industryremains—“What will power vehicles in the nexttwo to five years?”

The answer is that we will likely see acombination of combustion, hybrid, hybridcross-over and extended-range electric vehicles(EVs) in the near future. This diversity will surelycreate new challenges for manufacturers,insurers and repairers alike. Consider, forinstance, that only now—10 years after theHonda Insight became the first mass-producedhybrid car introduced to the North Americanmarket—do we see the true extent to whichhybrids impact claim costs, traditional repairprocesses and even underwriting assumptions.And that’s just one type of alternative vehicle.

Today’s HybridsToday’s hybrids combine the power from agasoline-based internal-combustion engine withelectricity derived from batteries in an electricmotor. So, for all intents and purposes, they aregasoline-powered vehicles that run on batterypower for very short periods of time. And whilehybrids deliver much promise to the automotivemarket, many studies show that their increasedcosts are often disproportionate to theirassociated fuel savings. This paradigmmotivates manufacturers to continue pursuingextended-range EVs, especially when the priceof oil falls.

Electric Vehicle ChallengesGeneral Motors, Mazda, Nissan, Toyota, Mini,Subaru, Hyundai and Volkswagen have allannounced their intent to deliver several EVmodels in the next few years. So consumersmay soon have several EVs available at theirlocal dealerships. Extended-range EVs, such asthe Chevrolet Volt, will be propelled primarily byan electric motor powered by rechargeablelithium-ion battery packs, with a gasolineinternal-combustion engine as a backup powersource.

Continued next page

Are Electric Vehiclesthe Answer?By Michael T. Anderson

www.audatex.us 9

Industry Trends

While promising, four significant challengesremain for manufacturers:

• weight

• distance

• longevity

• cost

The lithium-ion “T” battery pack that will powerthe Chevrolet Volt weighs 400 pounds and is oneof the most advanced battery packs everdesigned; however, it will only enable the Volt totravel a distance of 40 miles. This is becauselithium-ion batteries generate only about one-twenty-fifth of the energy produced by gasoline.As a result, manufacturers must discover newways to generate more energy from the lithium-ion batteries.

Researchers have tried—with limited success—to improve lithium-ion energy output through avariety of approaches, such as alternative latticeconfigurations, chemical and structural changes,and creation of multiple storage systems withvarying power densities.

The uncertain longevity of lithium-ion batteries isof equal concern and also creates potentialliability and warranty risks to manufacturers.Batteries are highly complex, containing billionsof molecules, ions and electrons within asophisticated, and sometimes volatile, system.To minimize risk, highly complicated cell-

management systems have been developed, butthese systems add considerable costs to thevehicle. Some experts say if a battery needs tobe replaced, costs could be as high as $10,000for today’s short-range lithium-ion batteries andfuture batteries with a potential range of up to200 miles may cost in excess of $15,000.

Managing ChangeEVs are highly complex vehicles, and theirintricacy continues to grow as numerousmanufacturers design unique power systems toreduce weight, increase distance, improvelongevity and manage costs. As EVspecifications are altered in attempts to bridgethe gap between technical feasibility andcommercial viability, manufacturers will introduceincreasingly complex and varied vehicles intotest markets throughout the world. As thishappens, some certainties exist. To begin, bothinsurers and repairers will need a greaterunderstanding of how these vehicles impactrepair procedures, equipment needs, engineeringrisks, repair costs, and standard repairguidelines. As these vehicles enter the market atgreater rates, insurers will likely see increasedrepair costs for many of the same reasons seenwith early-model hybrids (see the article “WhatDrives Hybrid Repairs Costs?” in this edition ofAudatex Directions). For example, newtechnology, greater use of alternative metals,increased electrical procedures and a lack ofalternative parts will all impact costs.

As the only global service provider currentlyserving more than 50 countries, Audatex is wellpositioned to provide best practice techniquesfor EV damageability and repair, regardless ofwhere these new vehicles are launched. n

Audatex Directions Vol 410

Industry TrendsCont inued f rom prev ious page Figure 1. The figure shown here is based on a map

developed by Venkat Srinivasan – a researcher atthe Lawrence Berkeley National Laboratory'sEnvironmental Energy Technologies Division. Itcompares the specific energy (in watt-hours perkilogram) of vehicle power sources, an indicator oftheir range, with their specific power (in watts perkilogram) an indicator of acceleration. Dotted linesindicate acceleration and cruise times, while bluestars show the Department of Energy’s energy andpower goals for electric vehicles and hybrids.Internal combustion engines still out-perform allother power sources, but battery researchers areconfident that they can improve the profile oflithium-ion batteries substantially. (Image and caption source: Environment Energy TechnologiesDivision News Report from the Lawrence Berkeley NationalLaboratory, Fall Newsletter, Volume 7, Number 4).

Some experts say

if a battery needs

to be replaced,

costs could be as

high as $10,000 for

today’s short-range

lithium-ion batteries

and future batteries

with a potential

range of up to

200 miles may

cost in excess of

$15,000.

11www.audatex.us

target for the federal funds interest rate to nearlyzero percent in mid-December 2008. Manyanalysts anticipate that this move will stimulatenew home and car sales during 2009, despitenearly half a million workers having lost theirjobs in November 2008.

So why do new car sales impact the insuranceand repair industry? A major determinant as towhether an insurer decides to repair a vehicle,versus declare it a total loss, is the percent ofdamages relative to the vehicle’s Actual Cash

Value (ACV). As consumer confidence weakens,unemployment rises and the financial marketsremain uncertain, would-be car buyers havedeferred their purchasing decisions. As a resultthere are fewer new (and higher-valued) cars onthe road. As forecasted in Volume 2 of AudatexDirections, the percentage of estimates identifiedas potential total losses continued to slowlyincrease through the second half of 2008, afterprior months of decline (figure 1). This is primarilydue to declining trends in ACVs relative to grossappraisal values (figure 2), an older vehiclepopulation and, to a lesser extent, seasonality andslight increases in repair costs.

In October 2008, the ManheimIndex—a key indicator ofpricing trends in the used-vehicle market—showed thelargest month-to-month andyear-over-year decrease in its14-year history. Whileinsurance claims may deviatefrom the Index due togeography and vehicle mix, itis a widely-accepted measure.Audatex’s ACV trends areconsistent with the Index.According to Audatex data,from September to November2008 ACVs declined by 7.3 percent in two months to

a level that was down 5.9 percent as comparedto the ACV in November 2007 (figure 3 on nextpage).

Vehicle Sales andActual Cash Values By Michael T. Anderson

Industry TrendsCont inued f rom prev ious page

12%

13%

14%

15%

16%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov

Total Loss Estimates

2007 Total Loss Percentage

2008 Total Loss Percentage

Actual Cash Value versusGross Appraisal Value in 2008

$2,000

$2,100

$2,200

$2,300

$2,400

$2,500

$2,600

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov$6,000

$6,200

$6,400

$6,600

$6,800

$7,000

$7,200

$7,400

$7,600

$7,800

Industry GAV Industry ACV

Figure 1: Through the second half of 2008, thepercentage of estimates identified as potential totallosses continued to slowly increase, after proirmonths of decline.

Figure 2: In late 2008,ACVs declined fromSeptember’s high asrepair costs incresed,narrowing the repairabilitywindow.

Continued next page

As consumer credit remains tight, 2009 new-car-sales forecasts remain grim. Despite significantincentive programs, sales at many of the topautomakers fell significantly in November 2008,as demand fell to a 25-year low. According tosome reports, conservative loan underwritingrestrictions instituted in October 2008 may denyas many as one out of four car-loan applicants.In efforts to open up the consumer creditmarkets, the U.S. Federal Reserve Board cut the

Vehicle Class (Q1 to Q2) (Q2 to Q3)Q3 to Q4

(through Nov. 2008)

Economy ImportsEconomy Domestic

Midsize Foreign

Midsize DomesticFull size

Luxury

Luxury SupremeSport

Sport Luxury

Mini VanFull size Vans

Small Pick-Up Trucks

Full size Pick-Up TrucksSmall SUVs

Large SUVs

-1.5 %-1.1 %

-2.9 %-1.4 %

-2.4 %-3.3 %

0.2 %-1.9 %

0.2 %-3.7 %

-9.1 %-9.3 %

-8.4 %

-2.3 %-2.9 %

3.0 %0.0 %

0.7 %0.8 %

0.9 %-0.9 %

9.6 %1.8 %

6.3 %-1.0 %

-0.1 %3.4 %

1.0 %

0.9 %-3.1 %

-2.2 %-3.7 %

-2.6 %-0.5 %

-3.2 %-2.6 %

-12.6 %-2.0 %

-3.7 %-5.6 %

-5.0 %-3.6 %

-8.1 %

-8.5 %-11.0 %

Percent of Change in Audatex ACVs during 2008

Hardest-Hit Vehicle TypesIn tough economic times, logic would indicatethat the used-car market would improve versusdeteriorate. However, only time will tell becausethe industry has never before experienced suchdire economic conditions. The lack of creditavailable to dealers and consumers is having aprofound impact on used-vehicle sales, valuesand inventories. Despite the U.S. Federal

12 Audatex Directions Vol 4

$6,500

$6,700

$6,900

$7,100

$7,300

$7,500

$7,700

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov90

95

100

105

110

115

Audatex Actual Cash Values versus Manheim Used-Vehicle Value Index

Audatex ACV’s Manheim Used Vehicle Value Index

Industry TrendsCont inued f rom prev ious page

Reserve Board taking aggressive actions to freeup the frozen credit markets, consumerconfidence and concerns over unemploymentwill continue to restrict many buyers topurchasing vehicles only out of necessity. Whileno vehicles are immune to the recent decline invalues, luxury supreme vehicles comprisedmostly of higher-end European models, largeSUVs and pick-up trucks have shown thegreatest declines in value (figure 4).

What’s to Come?Higher-value vehicles are taking the largest hiton ACVs, which seems reflective of the tightercredit and consumer financing markets. Onlywhen consumer credit eases, confidenceimproves and the backlog of inventories hassold will the value of these vehicles rise tonormal levels. However, this readjustment willlikely take several months to achieve, dependingon a multitude of economic variables. Economyand midsize vehicles, while down, remain moreaffordable to most consumers, seem to be lessinfluenced by the limited availability of creditoffered to buyers (on average, $4,500 to $8,000)and should remain stable in the next fewmonths. Experts in the wholesale industryforecast a soft year for most of 2009, with thelikelihood of the typical spring increase.

In the interim, insurers may need to re-examinetheir books of business at a more detailed levelin order to understand how this will impact theirpercentage of repairable vehicles. Access tovehicle-specific appraisal and ACV data is thefirst critical step in such analysis.

Insurers may also want to consider taking acloser look at their current total-loss thresholds,the impact these thresholds have on their total-loss percentages, and how a slight adjustmentwould affect not only their overall loss costs, butalso the satisfaction levels of customers whomay not be in a position to purchasereplacement vehicles. n

Figure 3: Audatex Actual Cash Values areconsistent with those seen in Manheim Index of used-vehicle values.

Figure 4: Audatex ACVs showthat luxury supreme vehiclescomprised mostly of higher-endEuropean models, large SUVsand pick-up trucks have sufferedthe greatest declines in value.

13www.audatex.us

Industry TrendsCont inued f rom prev ious page

Continued next page

Over 40 million used vehicles exchanged handsduring 2008 in the U.S. and Canada. Marketfluctuations and price swings in 2008 had amaterial impact on vehicle valuations, therebyinfluencing the total-loss-settlement process. In a highly volatile used-car market, the ability toprovide accurate and timely vehicle values thatare reflective of current market conditionsbecomes increasingly important. With theaverage Actual Cash Value of used vehiclesdeclining by $600 between October andNovember 2008, the use of fresh data becomesincreasingly important during the settlement oftotal-loss claims.

The ability to attain vehicle valuations that arereflective of current local conditions can beinfluenced by several factors, including the:

• frequency of vehicle updates

• method of vehicle updates

• timeliness of the data

• database size

Frequency of UpdatesAs seen in October and November of 2008, thefinancial markets, consumer confidence and theoverall state of the economy can cause rapid

changes in vehicle values. In just 60 days, theindustry experienced unprecedented declinesthat impacted some market segments by asmuch as $800, with an average decline of $600.With insurers settling thousands of total-lossclaims each month, access to timely marketdata from the onset of the settlement processcan impact both loss costs and loss-adjustmentexpenses. With frequent fluctuations in today’smarket, access to data that is updated on a dailybasis becomes increasingly important.

Method of UpdatesVehicle information is obtained from numeroussources, including dealerships, industrypublications and several other sources. Themethod through which this information isupdated is just as important as the frequency ofthe updates. For example, manually-enteredrecords can take more time to update and canbe more error prone than electronic updates thattend to be more timely and accurate.

Timeliness of DataMost states have regulatory governance thatlimits the age of data used in establishing totalloss valuations. This is because external markettrends can influence the prices being asked for

Staying On Top of Vehicle-Value Fluctuations By Tanya Elkins and Michael T. Anderson

14 Audatex Directions Vol 4

vehicles. In valuing total loss vehicles, thefresher the data, the more accurately it reflectscurrent market conditions. So, the faster newdata gets into a data source, the better.

Database SizeDatabase size also becomes increasinglyimportant in volatile markets. This is especiallytrue for rural markets and less common vehicles,which are both cases where some data sourcesmay contain fewer comparative vehicles andmay not reflect local market conditions. If limitedvehicle records exist, this impacts the timeneeded to attain a sufficient number of recordsthat reflect current market conditions and thiscan also impact the amount of time spent ontasks such as obtaining dealer quotes.

Staying on TopStatistically-valid vehicle valuations that reflectcurrent market conditions can materially impactloss costs, settlement expenses and customersatisfaction. The size of a vehicle-valuationdatabase (especially for rural markets and lesscommon vehicles), the frequency and method ofvehicle updates, and the timeliness of data areall important factors in a rapidly changing used-

vehicle market. In such conditions, outdatedvehicle information not only impacts vehiclevalues, but it can ultimately result in higherexpenses incurred from the process of reachingfair and accurate settlements with customers.

The Audatex Autosource® total loss valuationsolution helps users address these concerns byproviding:

• Frequent data updates: Each week, more than3 million new and updated vehicle records areadded to the system.

• Electronic updates: 98 percent of the recordswithin the Autosource total loss valuationsolution are updated electronically.

• Timely data: On average, just two days passfrom the time vehicle data is first published toits inclusion within Autosource.

• A vast amount of data: Each year, millions ofvehicle records are entered into the system,ensuring broad coverage.

For more information on Autosource, visit theAudatex Web site athttp://audatex.us/insurance_solutions/total_loss_valuation.aspx. n

The Autosource

total loss valuation

solution can help

you stay on top of

vehicle-value

fluctuations.

Industry TrendsCont inued f rom prev ious page

15www.audatex.us

owned businesses and don’t have a lot ofeconomic wiggle room. According toBodyShop Business:

• 75 percent of shop owners run a small,independent, family-owned collision repairshop.

• Shop owners are not novices. The averagenumber of years in the collision industry is27.2 years.

• One-third of shop owners have annual grosssales of up to $249,000, while 26 percentreach over $1 million in sales.

• Most business comes from word of mouth,meaning a lot hinges on customer satisfaction.

Do you see yourself reflected in these statistics?With shop and insurance profits shrinking, shopowners need to rethink how they run theirbusinesses. They have to find ways to repairmore cars, faster and without sacrificing quality.They’ve got to identify ways to reduce waste, inother words, ways to cut out anything that addscosts but not value.

The number-one topic everywhere these days is,of course, the economy, and naturally the topconcern of any business person is the future.How robust will my business be? How will myprofits compare to previous years? Can I stillexpect to grow my profits and my customerbase?

As we address the overall health of theeconomy, we must also examine the state of thebody shop industry itself. More and more, it hasbecome apparent that insurers expect shops toassist in managing loss costs and ensuringcustomer retention during the collision repairprocess. In fact, for some insurers, customersatisfaction trumps costs and is the single mostimportant factor in handling a claim. Andcustomers? Well, they want their vehiclesrepaired quickly and correctly—the first time.

In short, body shops are under immensepressure to perform. The pinch is being felt byeven the most experienced shop owners,especially those who operate small, family-

Shop View

Making the Journey to a Lean ShopPart 1: Why Lean? Why Now?By Dave Trissel and Krishna Masur

Continued next page

16 Audatex Directions Vol 4

‘‘

’’

Shop ViewCont inued f rom prev ious page

The way to reach these goals is to adopt andapply Lean principles. Lean isn’t about tellingyou how to run your business. Even the best-runbody shops can benefit from Lean principles,which simply give you the basis from which tomake the most effective decisions for yourbusiness.

What is Lean?To answer this question, one must firstunderstand what Lean is not. Lean is not cuttingfor the sake of cutting, whether it is employees,costs or anything else you can think of in yourshop. It’s not a management system. It’s notsomething you can buy off the shelf and installlike software. It’s not something you learn aboutand then check off the to-do list.

Lean is a philosophy. In essence, it’s anapproach to running a business that focuseson value, waste elimination and increasedspeed. As stated by John Sweigart, co-developer of a lean auto-body-repairworkflow-management process and one ofprincipals at The Body Shop @, “Lean is ajourney, not a destination.”

The term ‘Lean’ was coined by Jim Womack,author of The Machine That Changed the Worldand Lean Thinking. It stemmed from his researchof the famous Toyota Production System, orTPS. Toyota takes a long-term approach tobusiness, making decisions based on thephilosophy that they’ll be around for hundreds ofyears. So, instead of thinking short term andlooking for a quick fix, Lean thinkers, like thoseat Toyota, plan for the future, which naturallyaffects how they treat their employees,customers, community and suppliers.

When you think long term, your focus changes.You tend to look at solutions that can evolveover time to improve value, decrease waste andincrease speed. You look at how to utterlytransform your organization, not just how tosolve one specific problem. And, if you’re truly aLean organization, you look for others to workwith who have the same philosophy. In fact,Lean works best when all entities in a supplychain are Lean. Many top insurance companieshave adopted Lean principles and are looking totheir shop partners to adopt the samephilosophy because it has routinely led to cycle-time reductions of 25 to 50 percent.

Coming in Part 2Look out for part 2 of this series of articles onLean collision repair in the next edition ofAudatex Directions. Part 2 will examine the basicprinciples and concepts associated with Lean. Itwill focus on the idea that Lean is a long-termcommitment that has the potential to send youand your employees on a journey that willpositively transform your business, making itmore profitable by positioning you to be a betterpartner to your customers and suppliers.

The only way to have a truly Lean organizationis to train all the employees in your shop.Audatex provides an online Lean Shopcertification course that doesn’t just cover thebasics of Lean, it applies the principlesspecifically to collision repair. If you’d like moreinformation about Audatex Lean Six Sigma for Collision Repair™, contact Audatex at 1-888-776-5372 extension 1964. n

It opened my eyes,

We anticipate a

35 percent

increase in

efficiency and

throughput in all

areas, including

average length of

jobs, parts and

supplies

procurement and

cycle times.

Vartan GhazarianAssistant ManagerSupreme Collision Centre

17www.audatex.us

According to the Insurance Information Institute,about one-third of a typical comprehensive auto-insurance premium goes to paying for auto-theftclaims. It is estimated that a vehicle is stolenevery 26 seconds in the U.S., which equates toapproximately 1.2 million stolen vehicles a year.Although data from the National Insurance CrimeBureau has shown a downward trend in U.S.vehicle theft over the past several years,conservative estimates project that these lossescost the industry approximately $8 billion a year.Overall, the recovery rate for stolen vehiclesaverages 62 percent, but rates can vary widelyby state and region. For example, border statestend to have lower than average recovery rates,especially among pick-up trucks and SUVs,because a higher percentage of vehicles stolennear the border are taken outside the U.S. fordisassembly and resale of parts.

In an attempt to capture criminals and recoverstolen vehicles, law enforcement agencies inseveral U.S. states and Canada have institutednew infrared tag-reading technology. Theseautomated-license-plate-recognition (ALPR)systems can be mounted to patrol cars or fixeddevices such as toll booths, overhead highwaystructures, or border signs and structures. At acost of approximately $25,000 per unit, thesedevices have the ability to scan thousands oflicense plates per hour. Within seconds, lawenforcement can identify stolen vehiclestraveling on interstates, local streets and evenparking lots. Such immediate notification hashelped U.S. and Canadian law enforcementagencies detect and recover stolen vehiclesfaster than ever.

ALPR systems can automatically recognize over3,000 license plates per hour, even in poorweather conditions or complete darkness.Scanned plates are automatically compared tostolen-vehicle databases. When a match isdetected, an alarm is triggered within seconds,giving law enforcement notification to react.

As reported in TheWashington Post, inMaryland’s Prince George’sCounty, approximately 400stolen vehicles weredetected using ALPRtechnology in 2007. Infinancial terms, this equatesto $3.7 million in recoveredassets. In neighboringCharles County, police haverecovered 69 stolen vehiclesin 18 months. Otherjurisdictions that are proneto auto theft report similarresults from theirimplementation of ALPRsystems.

The use of ALPR systemsprovides many benefits toinsurers as well. Lawenforcement agenciesreport that the use of suchsystems significantlyincreases stolen-vehiclerecovery rates, decreasestime frames from theft torecovery, and also acts as a theft deterrent, asevidenced bydisproportionate declines inoverall theft rates in ALPR-active areas. For insurers,improving recovery ratesand time from initial loss to recovery can mean thedifference between vehicles being declaredrepairable versus total losses.

Also good news for insurers is the rapid rate atwhich ALPR technology is being adopted. In thegreater Washington D.C. area, for example,funding in excess of $4.5 million was approved toinstall 200 additional readers in the Maryland,Virginia and the District of Columbia. Several otherstates are also adopting this technology. WhileALPR technology may be new, its implications forthe future are very promising. Over the next fewyears, it could significantly impact insurers’ overalltheft and recovery percentages. n

Auto Thieves’ NewestOpponent: License-PlateScanners By Michael T. Anderson

A Look into Future Technology

Source: The Arizona Republic

(Republic Research, Platescan)

References:

Zapotosky, Matt. “Cruiser-TopCameras Make Police Work a Snap,”The Washington Post.August 2, 2008.

Sheridan, Mary Beth. “License PlateReaders To Be Used In D.C. Area,”The Washington Post.August 17, 2008.

18 Audatex Directions Vol 4

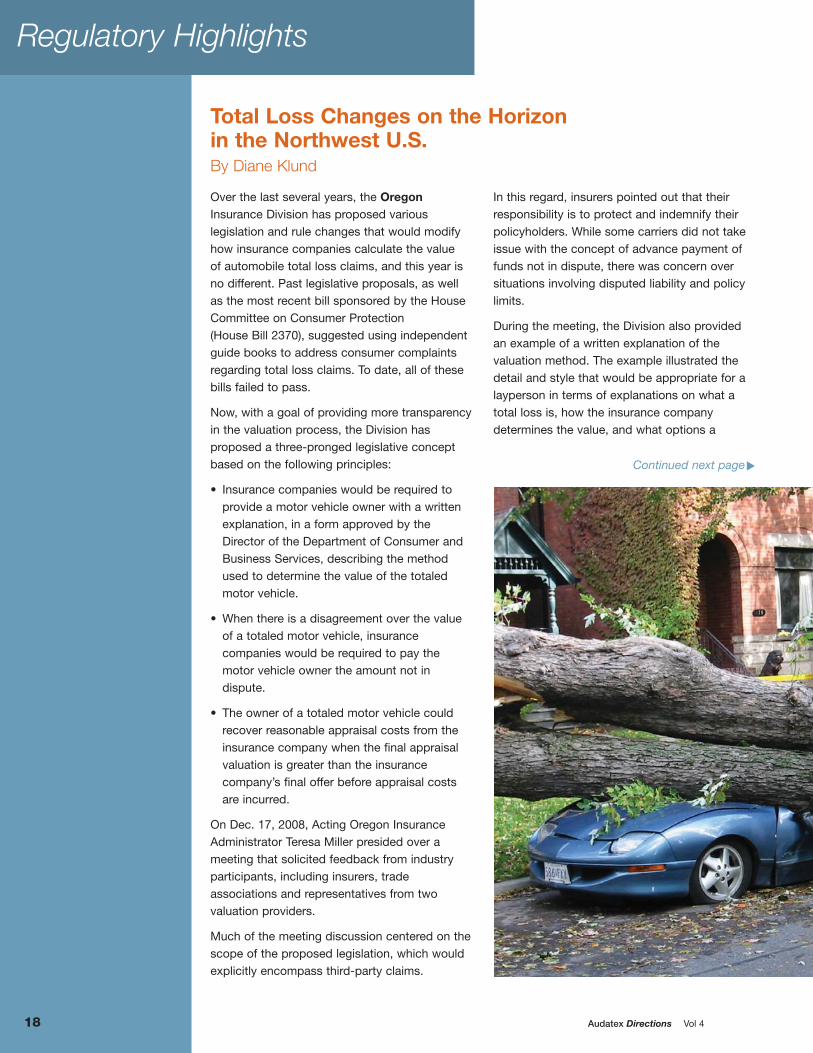

Regulatory Highlights

Over the last several years, the OregonInsurance Division has proposed variouslegislation and rule changes that would modifyhow insurance companies calculate the value of automobile total loss claims, and this year isno different. Past legislative proposals, as wellas the most recent bill sponsored by the HouseCommittee on Consumer Protection (House Bill 2370), suggested using independentguide books to address consumer complaintsregarding total loss claims. To date, all of thesebills failed to pass.

Now, with a goal of providing more transparencyin the valuation process, the Division hasproposed a three-pronged legislative conceptbased on the following principles:

• Insurance companies would be required toprovide a motor vehicle owner with a writtenexplanation, in a form approved by theDirector of the Department of Consumer andBusiness Services, describing the methodused to determine the value of the totaledmotor vehicle.

• When there is a disagreement over the valueof a totaled motor vehicle, insurancecompanies would be required to pay themotor vehicle owner the amount not indispute.

• The owner of a totaled motor vehicle couldrecover reasonable appraisal costs from theinsurance company when the final appraisalvaluation is greater than the insurancecompany’s final offer before appraisal costsare incurred.

On Dec. 17, 2008, Acting Oregon InsuranceAdministrator Teresa Miller presided over ameeting that solicited feedback from industryparticipants, including insurers, tradeassociations and representatives from twovaluation providers.

Much of the meeting discussion centered on thescope of the proposed legislation, which wouldexplicitly encompass third-party claims.

In this regard, insurers pointed out that theirresponsibility is to protect and indemnify theirpolicyholders. While some carriers did not takeissue with the concept of advance payment offunds not in dispute, there was concern oversituations involving disputed liability and policylimits.

During the meeting, the Division also providedan example of a written explanation of thevaluation method. The example illustrated thedetail and style that would be appropriate for alayperson in terms of explanations on what atotal loss is, how the insurance companydetermines the value, and what options a

Total Loss Changes on the Horizon in the Northwest U.S.By Diane Klund

Continued next page

19www.audatex.us

Regulatory HighlightsCont inued f rom prev ious page

consumer has when there is a dispute with theinsurer over the value. The meeting participantsstarted to dive into this document, but thediscussion was tabled pending the outcome ofthe bill.

The final issuediscussed at

the meetingwas the

Division’sconcern that

consumers maybe at a disadvantage

in the dispute process because they may needto pay out-of-pocket expenses for an appraisal.This concern is the basis for the proposedrequirement that an insurer reimburse theinsured for reasonable appraisal costs if the finalappraisal value (umpire decision) is greater thanthe insurer’s last offer before the final appraisal.Other concerns regarding this matter includedthe potential for a dramatic increase in appraisaldemands, as well as potential costs that mayarise if the policy brought forth were to beamended.

While not committing to any amendments,Acting Administrator Miller thanked the industryparticipants and said their feedback would betaken into consideration. At the time of thispublication, no further meetings were plannedand the industry was awaiting news of acommittee hearing.

Elsewhere in the Northwest U.S., WashingtonState’s Office of the Insurance Commissioner(OIC) has been holding stakeholder meetings todiscuss proposed amendments to the UnfairClaims Practices Act. After two lengthy meetingsin which insurers, trade associations and

valuation providers provided their input, the OIChas made significant changes to the draft. Themost recent draft can be viewed on the office’sWeb site athttp://www.insurance.wa.gov/oicfiles/rules/proposed/drafttext2.pdf.

Although the OIC has loosened its limitations onthe geographic area allowed for comparable-vehicle and dealer-quotation searches, input atthe third stakeholder meeting on Nov. 18, 2008continued to center around this topic.

Specifically at issue was the needto differentiate between

requirements that areappropriate whenactually replacing a

lost vehicle (in which case a very similar andgeographically-close comparable vehicle mightbe warranted) versus the requirementsappropriate when determining an Actual CashValue settlement (in which case adjustments areeasily made for differences in comparability).Other points highlighted by industry participantswere that the market should not be artificiallyrestricted geographically, and in fact, consumerbuying habits have expanded significantly withthe availability of online vehicle-shoppingWeb sites. For now, the industry awaits the nextdraft or the notice of a formal hearing on theamendments. n

20 Audatex Directions Vol 4

Regulatory HighlightsCont inued f rom prev ious page

Insurers operating in the state of New Yorkkicked off the new year by regaining the abilityto adjust annual private-passenger automobileinsurance rates under a new flex-rating program.Insurers can now adjust rates within a 5 percentflex-band, without prior approval from the state’sInsurance Department. The new program, whichwas signed into law in July 2008 as InsuranceRegulation Number 153, is designed to enhancecompetition in the state’s automobile and home-owners insurance markets. In order to allow thestate’s Insurance Department time to formallypublish this new regulation, it was adopted onan emergency basis beginning in late December2008. This temporary regulation will expire after90 days, or sooner if the Department formallypublishes the regulation before then. At the timethis newsletter was printed, the formal regulationhad not yet been published.

“For the last seven years the government hasemployed a system of price fixing for autoinsurance,” said New York Insurance AssociationPresident, Ellen Melchionni. “The reinstatementof flex-rating will allow for a more nimble andcompetitive market.”

New York State previously had a seven-percentflex-band rating structure, which expired in2001. Under that program, automobile insurancepremiums were lower and there was increasedcompetition among insurers operating in thestate. After the statute expired, some insurersleft the state and prices subsequently increased.The new law is intended to ensure the availabilityand affordability of property and casualtyinsurance, as well as to stabilize the marketthroughout the state.

While several groups, including the PropertyCasualty Insurers Association (PCI), havesupported the regulation, some questions stillremain. For example, in November 2008, PCI,whose members represent 65.3 percent of allpersonal-lines insurance business in New York,asked the state’s Insurance Department to clarify the precise effective date from which the

5 percent cumulative rate change will bemeasured. PCI maintains that the law is intendedto limit the number and cumulative effect of rateincreases applied during the 12-month periodfollowing the law’s effective date, and that“looking back” at increases approved prior tothe effective date is not the true intention of thelaw.

Several other outstanding questions pertainingto this new regulation include, but are not limitedto, those asking for clarification regarding the:

• definition of “non-business automobileinsurance policy”

• use of the term “premium”

• frequency of rate reduction file-and-use filingsin a twelve month period

• precise date range for measuring the five-percent cumulative rate change

For further updates on this regulation, you cancontact the New York Insurance Department byvisiting their Web site athttp://www.ins.state.ny.us.

The emergency regulation can be found at:http://www.ins.state.ny.us/r_emergy/remgindx.htm. n

New York Kicks Off 2009 with a New Flex-Rating Program By Michael T. Anderson

21www.audatex.us

Industry Collaboration

In 2009, two trends will continue to evolve intobusiness standards—efficient supply-chainsolutions and ‘green’ corporate citizenship. For the collision repair industry, maximizingrecycled-part use achieves both.

Smart part choice enabled by Web-based partssourcing and procurement represents the mostpromising opportunity for insurers to impactvehicle-repair costs. Under the traditionalparadigm of using new parts, replacement-partcosts represent an average of 42 percent of acollision repair estimate. As such, carriers canimprove loss costs by switching to quality,recycled OE part assemblies. At the same time,recycled OE parts represent significantenvironmental benefits because they savematerials and energy used in the manufacturingprocess.

Despite these benefits, wide-spread adoption ofrecycled-part use has been slow to increasebecause, until recently, it’s been much easier totalk about recycled OE parts than to actually findand procure them. The challenge many insurersand repairers faced was the ability to sourceinsurance-quality parts quickly and accurately. In the past, the process of locating recycled OE parts demanded that appraisers andcollision-repair estimators make multiple phonecalls to local recyclers or conduct multiplesearches, thereby adding unnecessary expenseto the process. As a result of these challenges,over the past several years, costs attributed torecycled parts have consistently representedonly about 14 percent of the total part dollars.

A major milestone in the move towards recycled-parts utilization was achieved with the launch of

the Real Steel Download add-on module forAudatex Estimating™. The solution enables anestimate preparer to directly search for specificparts within a vast database of insurance-qualityparts available from leading recyclers. While thissolution makes it easier than ever to locateparts, phone calls are still needed to verifyavailability and procure parts. To build upon thestrengths of this existing process, and to expandthe parts database, Audatex and APU haveannounced plans to work together to deliverreal-time parts sourcing and procurementfunctionality that is fully integrated withinAudatex Estimating. Powered by APU’sPartsNetwork®, this integrated solution willprovide appraisers and repairers with real-timeaccess to part inventories representing millionsof alternative parts from suppliers nationwide, aswell as online procurement functionality. A search engine will return data on partavailability, description, quality, pricing andonline procurement options—all within theestimating system. The resulting solution willreduce time previously needed for phone calls,inquiries and supplements due to part availabilityor condition.

An equally exciting feature of the new solutionwill be the availability of actionable reportingmetrics surrounding alternative-parts utilization.The new solution will capture critical behavior-based metrics, such as compliance withalternative-parts rules, part-related supplementactivity, and the influence of appraiser decisionson potential versus actual outcomes.

The new solution will make it easier than ever to leverage used parts and make greenchoices. n

Audatex and APU to Launch IntegratedRecycled-Parts Procurement SolutionBy Charles Lukens and Brian Vannoni

...this integrated

solution will

provide appraisers

and repairers with

real-time access to

part inventories

representing

millions of

alternative parts

from suppliers

nationwide, as well

as online

procurement

functionality.

22 Audatex Directions Vol 4

Industry CollaborationCont inued f rom prev ious page

Repairers and Insurers Guide Inaugural Meeting ofAudatex Technical Advisory Council

‘‘

’’

I was very

impressed with the

participants,

their varied

backgrounds, and

the direction of the

discussion.

Everyone was

sincere in seeking

better estimating

products and

solutions, not

simply seeking an

advantage for their

personal business.

Darrel AmbersonPresident of Lehman’sGarage and two-termNACE Chairman

Technical and database questions, userexperiences, and industry trends were just someof the issues explored at the inaugural meetingof the Audatex Technical Advisory Council,which kicked off during NACE 2008. This newlyformed group of repairers and insurers willcommunicate closely with Audatex to provideend-user input for consideration in thedevelopment of the Audatex database, as wellas specific product features and functionality.

“Audatex is very serious about listening to thevoice of our clients and responding to industryneeds. Earlier this year, we formed an inter-industry Strategic Advisory Council to gatherinput at the strategic level,” said Rick Tuuri,Associate VP of Industry Relations for Audatex.“The Technical Advisory Council is the nextlogical step in this process because it provides aregular venue for collecting input directly fromend users and exploring how Audatex can bestmeet their needs through product development,training, and customer communications.”

“We invited Council members with the goal ofhaving balanced participation from allstakeholders and industry constituents,”

continued Tuuri. “Therefore, we invited bothinsurers and repairers. Several national andregional insurers have joined the Council, andwithin the repairer segment, there isrepresentation from the CIC Database TaskForce, as well as the Database EnhancementGateway Joint Operating Committee, includingindustry leaders from the AASP, ASA andSCRS.”

The aim for inclusion seems to be succeeding.After the first meeting, participant DarrelAmberson, President of Lehman’s Garage andtwo-term NACE Chairman, commented, “I wasvery impressed with the participants, their variedbackgrounds, and the direction of thediscussion. Everyone was sincere in seekingbetter estimating products and solutions, notsimply seeking an advantage for their personalbusiness.”

The Council plans to meet twice per year, withregular communication between meetings. Thenext meeting is scheduled for July to coordinatewith the I-CAR 30th Anniversary Meeting inWashington, DC. n

23www.audatex.us

Audatex News and Events

Last year, Audatex’s parent company, SoleraHoldings, Inc. (NYSE: SLH), strengthened itsposition as the leading global provider ofsoftware and services to the automobileinsurance claims processing industry bycompleting two key acquisitions.

In November 2008, Solera acquired the Braziliancompany Inpart Servicos Ltda. Inpart is aleading provider of electronic-exchangesolutions used for the purchase and sale ofvehicle replacement parts. The company has anextensive network of parts suppliers, as well asan impressive customer list that includes someof Brazil’s leading insurance companies andcollision repair facilities. Solera’s Founder,Chairman and Chief Executive Officer, TonyAquila, commented, “We are very excited aboutthe accomplishments already achieved by theInpart team in the Brazilian market and we willbe exploring the opportunity to expand theInpart offering to other Latin American marketsthat we already serve.”

In December 2008, Solera acquired HPI Ltd., theleading provider of used-vehicle history and data

validation services in the United Kingdom. Inaddition to confirming whether a vehicle hasoutstanding car financing, is recorded as stolen,or has previously been declared a total loss, HPIsolutions can also confirm details such asspecific make, model, color, door plan andengine size. When speaking about thisacquisition, Aquila remarked, “The HPI suite ofproducts and services will enhance our deliveryof decision-support data and softwareapplications to our insurer, car manufacturer,auto dealer, and finance company customers.The acquisition will help us meet some of theincreased demand from our clients for access tointegrated historical information on specificvehicles involved in potential transactions.”Aquila also noted that Solera will explore thepossibility of expanding the HPI model, bothregionally and internationally.

With plans to consider delivering the solutions ofthese newly acquired companies into additionalmarkets, Solera continues its quest to best servelocal customers by leveraging its globalknowledge. n

Audatex’s Parent Company StrengthensIts Global Leadership through theAcquisition of Two New Companies

24 Audatex Directions Vol 4

Wadine Traylor-FreemanNov. 26, 1947 - Nov, 24, 2008

On Nov. 24, 2008, long-time Audatex employeeWadine Traylor-Freeman passed away after abrave battle against cancer. She was just twodays shy of her 61st birthday.

Throughout her career, Wadine made a lastingimpression on all her colleagues—not onlybecause of her admirable work ethic andattention to detail, but more importantly, becauseof her warm personality and genuine care forothers.

Wadine first joined Audatex (then ADP) in 1983,at which time she managed the Dublin, Californiahardware facility, a precursor to the technical-logistics asset-management company Integron.Under Wadine’s leadership, an impressivehardware-workflow and repair process wascreated to support clients who leased equipment.

In fact, Wadine did such a great job that part of theprocess she developed is still in place today, over 25years later. In 1995, Wadine transferred to Audatex’sAnn Arbor, Michigan location, where she led thehardware team and acted as corporate liaison toIntegron, as well as to several of the industry’s toplaptop manufacturers.

The accolades Wadine received for her work were asgreat as the impact she had on her colleagues, whodescribed her not only as a “mentor” and “role-model,” but also as a “wonderful person who was afriend to many.”

For everyone who was lucky enough to have knownWadine, the impression she left will surely never fade.

Wadine is survived by her son Mark, daughter Nikkiand six grandchildren. n

In Memoriam: Wadine Traylor-Freeman A Colleague Who Left a Lasting Impression

Audatex News and EventsCont inued f rom prev ious page

Revamped OnlineTraining Center Will HelpUsers Unleash thePower of TheirAudatex Solutions

In today’s demanding workplace, it’s moreimportant than ever to leverage all the tools atyour disposal. The newly revamped AudatexOnline Training Center will help ensure you’regetting the most from your investment inAudatex solutions.

Last year, the Audatex Online Training Centerwas accessed over 300,000 times by userslooking to gain an edge through obtaininginformation on Audatex products, receiving on-demand training or attending live virtual classes.Were you one of those users?

Later this month, new and enhanced features ofthe Online Training Center will make it easierthan ever to put this resource to work for you. Some of the features you’ll see include:

• Popular Document Tracking – See whatdocuments have helped other users bychecking out the most popular recently

accessed documents, which will be highlighted onproduct pages.

• Enhanced Document Classifications – Enjoyfaster page loading and easier document navigationwith the help of new classification methods on theproduct pages.

• Pop-Up Calendar, Multiple-Class Registration,Faster Access – Save time by viewing upcomingclasses in a new pop-up calendar, registering formultiple live online classes at the same time andjoining live online classes via a new, and faster,access method.

• Master Proficiency Certificate (MPC) – Earn anMPC by successfully completing a programcomprised of several different training components,such as multiple classroom or virtual instructor-ledclasses, or a mixture of classroom and virtualclasses, webinars, or computer-based training. In addition to the MPC, you’ll also earn certificatesor accreditation typically associated withcompletion of the individual course components.

• Enhanced Support for French- and Spanish-Speaking Clients – If your preferred language fortraining is French or Spanish, learn in yourlanguage-of-choice by accessing new language-specific training pages. n

Did You Know You Can:

• Attend award-winningAudatex onlinetraining for free

• Earn I-CAR points andContinuing EducationUnits by attendingselect Audatex trainingclasses

Check It Out Today!www.training.audatex.us

25www.audatex.us

“Leadership: The Business-IT Imperative”2009 P&C Insurance Technology ConferenceTotonto, Canada

Audatex Strategic Advisory Council - By Invitation OnlyMiami, Florida

Northeast Tradeshow (AASP)Secaucus, New Jersey

Property Loss Research Bureau (PLRB) / Liability InsuranceResearch Bureau (LIRB) Claims ConferenceSeattle, Washington

Insurance Data Management Association’s Annual Seminar,“Insurance Business Intelligence– How Smart Are You?”Philadelphia, Pennsylvania

Canadian Collision Industry Forum (CCIF) MeetingEdmonton, Alberta

Risk and Insurance Management Society (RIMS) 2009 Annual Conference and ExhibitionOrlando, Florida

Collision Industry Conference (CIC) MeetingHartford, Connecticut

The Brian Sullivan 2009 Auto Insurance Report National ConferenceNaples, Florida

IT TradeshowAuto Recyclers Reunion and ReviewSouthington, Connecticut

CIC Meeting in conjunction with I-CAR Annual MeetingWashington D.C.

Feb 23

Feb 24-26

Mar 20-22

Apr 6-7

Apr 18Apr 19-23

Apr 22-23

May 15-16

July 29-30

Catch Audatex at the next industry event or trade show.

Audatex News and EventsCont inued f rom prev ious page

www.audatex.us

Apr 26-28

Mar 22-25

© 2009 Audatex North America, Inc. All rights reserved. All other registered trademarks are the property of their respective owners.

15030 Avenue of Science, Suite 100, San Diego, CA 92128Tel: (800) 237-4968 Fax: (858) 946-1073

www.audatex.us www.solerainc.com

Want more frequent industry updates?

ThinkTank is the answer.

This new web information hub from Audatex helps you top off your tank by staying current on trends and news in the automotive industry.

• Stay informed of the latest industry trends and news

• Receive tips on how to better use Audatex solutions

• Preview the latest Audatex developments

• Give Audatex feedback on what’s important to you

Check out the latest edition of ThinkTank at http://audatex.us/thinktank.aspx

Sign up for weekly ThinkTank updates!

Get ThinkTank delivered directly to your inbox each week.

To subscribe, fill out our online web form, noting in the comments field, “Sign me up for ThinkTank.”

http://audatex.us/contact/web_contact_form.aspx

Intelligence. Built In. © Audatex North America, Inc. All Rights Reserved.

Proceed with Intelligence.

Intelligence. Built In.

Customers look to you for more than an insurance policy. They want safety and peace of mind.

You ask no less of your information provider. You want a partner who will be there as your business needs

change. You demand stablility, vision, and intelligence. Audatex North America builds automotive claims

solutions that provide insurers with smart information. We develop software that runs on the world’s most

comprehensive vehicle database so you can delight policyholders. We’re constantly driving improvement.

From a new dispatch solution that can power your appraiser teams to higher performance to new

business analytics that deliver unparalleled insight, Audatex builds intelligence into every product.

Audatex associates stand ready to help get you through any obstacles ahead. For more than 40 years,

we’ve done business this way. And we have no plans to change. You can count on it.

800.237.4968 | www.audatex.us