Embed Size (px)

Citation preview

What are PSAS and IFRS® Standards ? Why are these Accounting Standards Important to Understand? Linda Mezon, Chair, AcSB Michael Puskaric, Director, PSAB October 3, 2017

The views expressed in this presentation are those of the presenter, not necessarily those of the AcSB and the PSAB.

2

Agenda

• Standard setting in Canada – How the PSAB and the AcSB are working on behalf

of Canadians

• Developments in PSAS – PSAB 2017-2020 Strategic Plan – New Standards

• Developments in IFRS – Use around the World and in Canada – New Standards

Links provided throughout

3

Where We Fit

4

PSAB’s Mission

• Public Sector Accounting Board (PSAB) • Serves the public interest by establishing

standards and other guidance for financial reporting by all Canadian entities in the public sector

• Supporting informed decision making and accountability for Canadian public sector entities

5

AcSB’s Mission

• Support informed economic decision-making

• Serving the public interest – Establishing high-quality accounting

standards – Being accountable to stakeholders – Contributing to global best practices

6

Due Process • AcSB and PSAB follow

– Rigorous consultative procedures – Develop and issue of accounting standards and

statements of recommended practices

• Key principles – Transparency – Consultation – Accountability

7

Public Sector Accounting Standards (PSAS) • The objectives of financial reporting for

governments and businesses are not the same

• Governments have unique characteristics – therefore financial statements do not look the same

8

PSA Overview - Roadmap

• Gov’t and components

GBEs

OGOs and Partnerships

PS-NFPs*

PSA Handbook

IFRS

IFRS

PSA Handbook

PSA Handbook +/-

* NFPs in the public sector

9

2017-2020 Strategic Plan

OUR JOURNEY FORWARD 2017-2020 Strategic Plan (effective April 1, 2017)

10

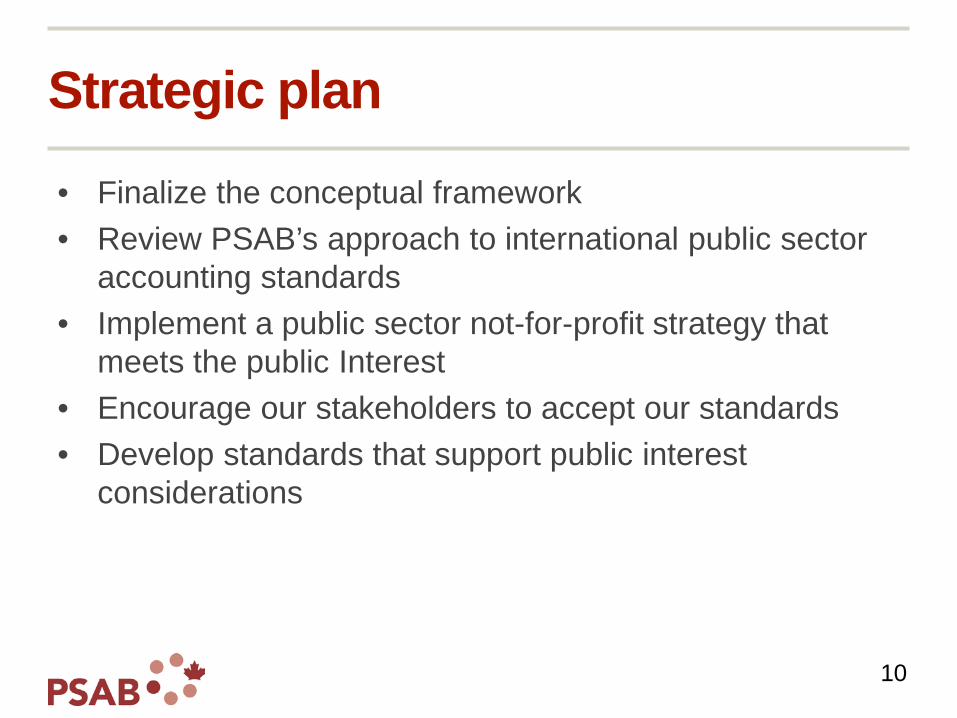

Strategic plan

• Finalize the conceptual framework • Review PSAB’s approach to international public sector

accounting standards • Implement a public sector not-for-profit strategy that

meets the public Interest • Encourage our stakeholders to accept our standards • Develop standards that support public interest

considerations

11

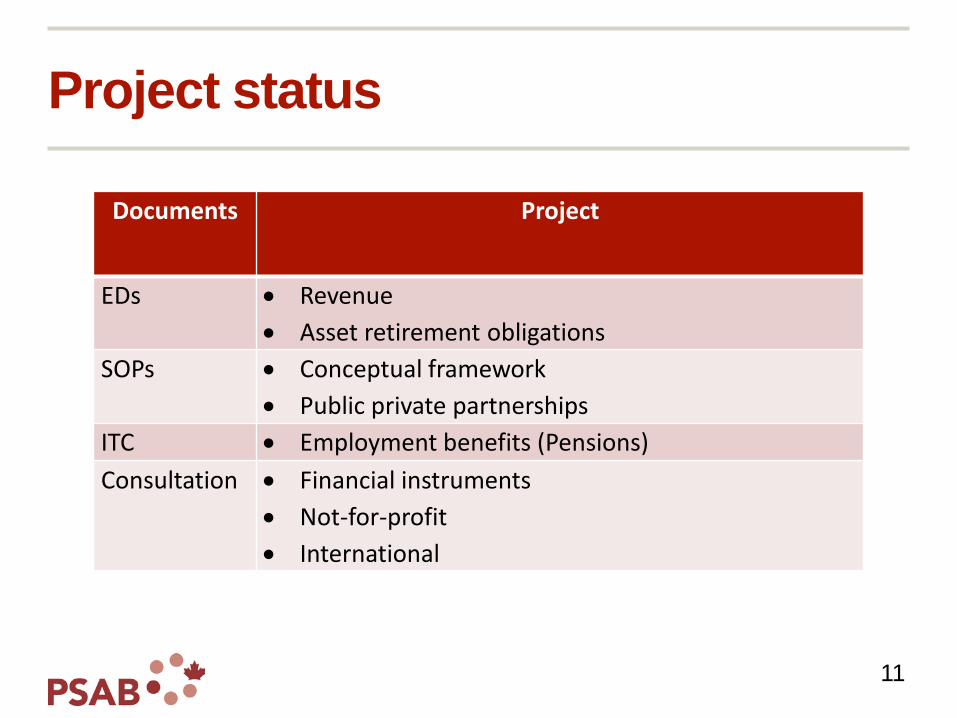

Project status

Documents Project

EDs • Revenue • Asset retirement obligations

SOPs • Conceptual framework • Public private partnerships

ITC • Employment benefits (Pensions) Consultation • Financial instruments

• Not-for-profit • International

Effective dates

12

Date Topic

January 1, 2017 Governments and government organizations - Introduction (components, NFPs and partnerships)

April 1, 2017 Governments and government organizations - Related Party Disclosures - Inter-entity Transactions

April 1, 2017 Governments and government organizations - Assets PS 3210 - Contingent Assets PS 3320 - Contractual Rights PS 3380

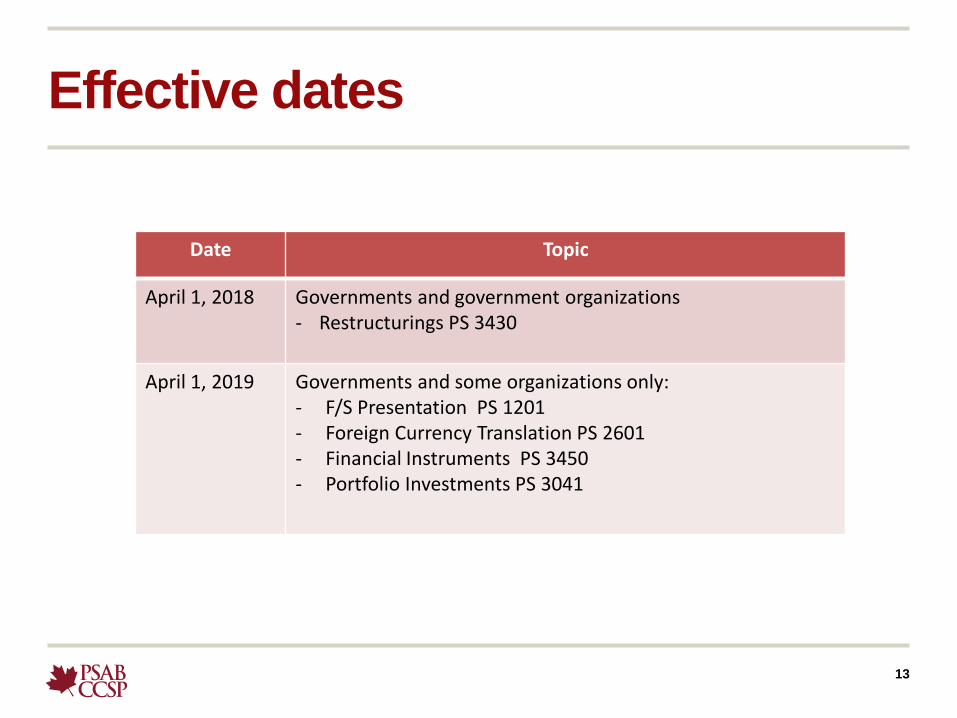

Effective dates

13

Date Topic

April 1, 2018 Governments and government organizations - Restructurings PS 3430

April 1, 2019 Governments and some organizations only: - F/S Presentation PS 1201 - Foreign Currency Translation PS 2601 - Financial Instruments PS 3450 - Portfolio Investments PS 3041

14

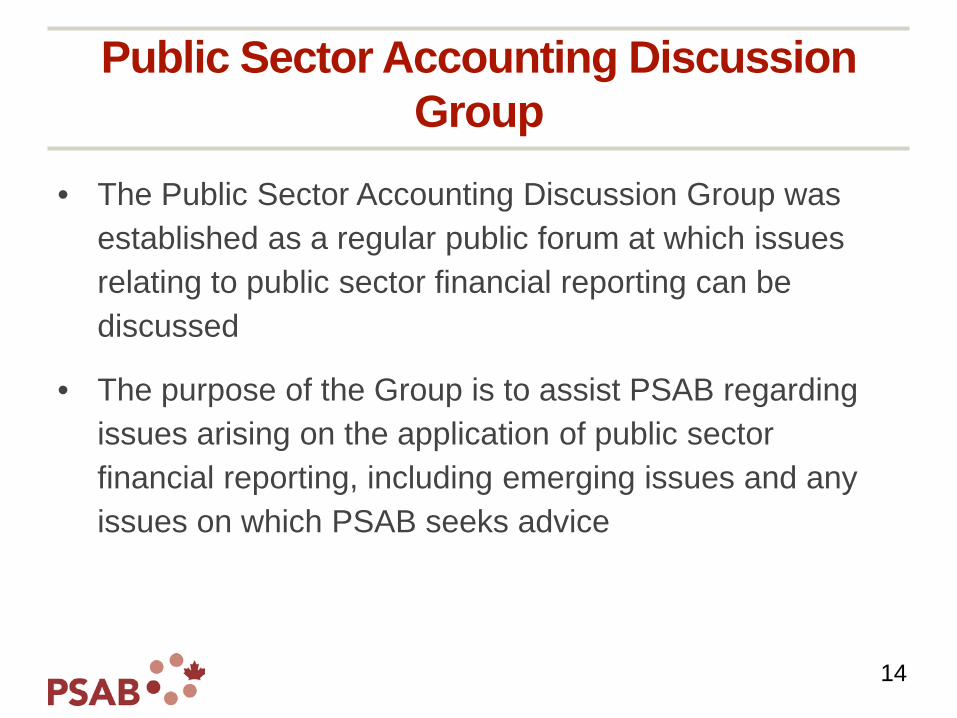

Public Sector Accounting Discussion Group

• The Public Sector Accounting Discussion Group was

established as a regular public forum at which issues relating to public sector financial reporting can be discussed

• The purpose of the Group is to assist PSAB regarding issues arising on the application of public sector financial reporting, including emerging issues and any issues on which PSAB seeks advice

15

AcSB’s 2016-2021 Strategic Plan • Sets out strategic objectives to

– Develop a research program

– Support application of IFRS in Canada for publicly accountable enterprises

– Retain and improve standards for private enterprises and not-for-profit organizations

– Monitor developments for pension plans

16

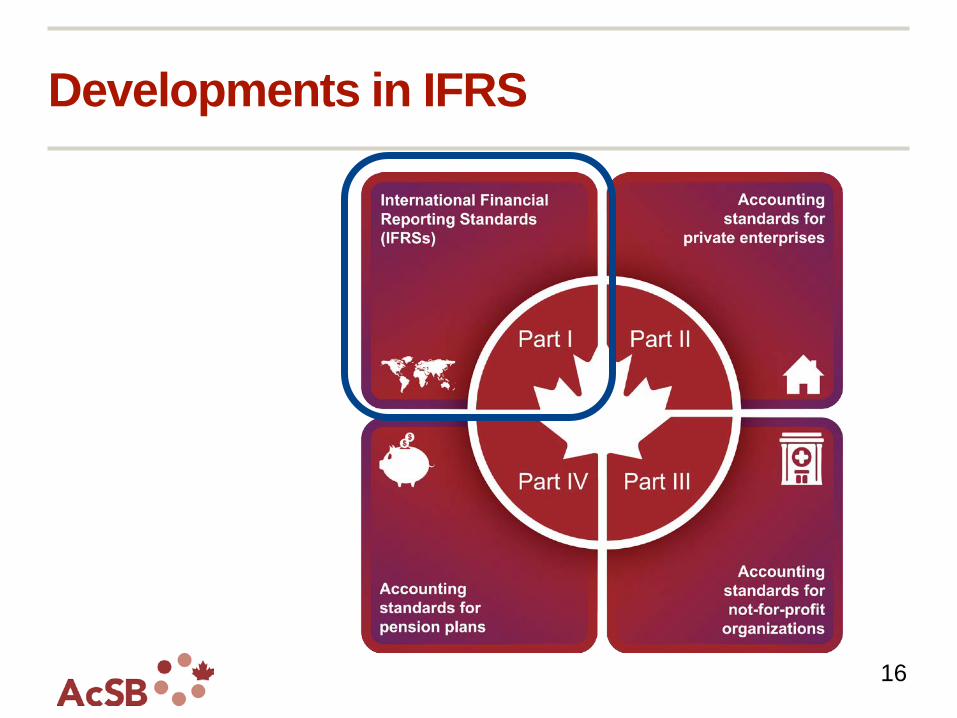

Developments in IFRS

17

IFRS® Standards: Global Use

• Over 47% Total World GDP require publically accountable enterprises to apply IFRS*

• Others apply IFRS-based frameworks tailored for public sector entities, e.g. IPSASs

* IFRS Foundation, GDP of profiled information

18

2004 Begin strategic review of

accounting standards used in Canada

2005 Invitation to comment on new

Strategic Plan – “one size does not fit all”

2005 Issue Financial Instruments

standard (Section 3855) – moves accounting closer to IAS 39/FAS

133

2005 Public consultations/

roundtables

2006 Decision made to go to

IFRS – new standards for private/NFPO

2007 Issued implementation plan for

incorporating IFRS into Canadian GAAP

2008 Status reviewed and decision confirmed

2008/2009 Exposure drafts of all IFRSs –

due process to put into Canadian Handbook

Dec 2008 Global financial crisis – changes

to Canadian GAAP to mirror reclassification changes in

IFRS/US GAAP

Dec 2008 Issue new Business Combinations standard (Section 1581 – converged with IFRS 3) – to

allow preparers to account for business combinations without requiring transition adjustments upon changeover to IFRS

2010 IFRSs in Canadian

Handbook and preparers start to disclose status of

IFRS conversion in MD&A

2011 Changeover to IFRS

Canada’s journey to IFRS

19

Canada’s transition to IFRS

Key elements • Converged standards • Provided 5-years • Incorporated IFRS into

Canadian GAAP • Helped stakeholders • Monitored

The results • Acceptance • Costs • Readiness • No surprises • Benefits

20

Implementing New IFRS Standards

• Effective dates for new standards November 1, 2017 IFRS 9

Financial Instruments

(large Canadian Banks)

January 1, 2018 IFRS 9

Financial Instruments (all other entities)

January 1, 2019 IFRS 16

Leases

January 1, 2018

IFRS 15 Revenue from Contracts with

Customers

2017 is the

comparative year for IFRS 9

and 15!

2017 2018 2019

January 1, 2021 IFRS 17

Insurance

2020 2021

See Appendix for overview and resources on new

IFRS Standards

21

IFRS 9 – Effective in 2018

• Major impact for financial institutions, but can affect all entities

• What changes? − New impairment model

− Some changes to classification and measurement

o Classification based on business model

o Measurement principles similar to current standard

• Refer to Project Page

• Refer to Implementation page

22

IFRS 15 – Effective in 2018 • Major impact expected for certain sectors – telecoms, software, real

estate • All entities will have significant new disclosures – for example:

− Additional information about disaggregated revenue − Assets recognised from the cost to obtain or fulfill a contract (balances

and amortization)

• What changes? − New criteria for when revenue is recognized

o When customer has control of goods or services

• IASB indicated no further amendments to IFRS 15 before effective date

• Refer to Project Page • Refer to Implementation page

23

IFRS 16 – Effective in 2019 • Affects all entities who are lessees

• What changes? − Eliminates classification of leases as operating or finance

− Recognize a lease asset and lease liability for most leases

− Some exemptions for certain leases (for example, short-term or low dollar-value leases)

• Refer to Project Page

• Refer to Implementation page

Key IFRS 16 Implementation Consideration - System requirements

Can your current systems track and produce required information?

24

Implementation Resources AcSB implementation activities: • AcSB’s IFRS Discussion Group (IDG)

− Discussing implementation issues on IFRS 9, IFRS 15 and IFRS 16 – use the searchable database to find details on issues

− Submit issues for discussion by IDG confidentially

• Translation of non-authoritative IFRS material for use by all Canadians − IFRS 9 (Illustrative Examples and Implementation Guidance), IFRS 15 and IFRS 16

non-authoritative material available in Knotia now − IFRS 9 Basis for Conclusions in progress – will be available by November 1 − IFRS 17 non-authoritative material will be next

• IFRS 15 Panel Discussion from October 2016 IASB implementation activities: • IFRS Interpretations Committee • Transition resource groups

25

Disclosing the Impact of New Standards

• IFRS requires entities to disclose the possible impact of the new standard in future years

• IFRS 9 and 15 – effective next year, and therefore entities should be aware of and disclosing impact

• Important information to communicate to financial statement users – Need to know if material changes are coming!

• AcSB’s IDG will be discussing nature and extent of disclosures of new standards at October IDG Meeting in Halifax

Have you provided sufficient disclosure of the expected

impact of the new standards?

26

• Hosted by CPA Canada & the IFRS Foundation

• November 1-2, 2017 in Toronto

• Register at cpacanada.ca/2017IFRS

27

Q&A

28

Get involved

• Respond to proposals • Participate in roundtable discussions • Visit www.frascanada.ca • Volunteer

29

Stay Up-to-Date

Email updates – www.frascanada.ca/subscribe • Tailor your subscription

For more information, visit www.frascanada.ca

Contact Michael A. Puskaric

Director, Public Sector Accounting Board Phone: +1 (416) 204-3451

Email: [email protected]

Contact Linda Mezon, FCPA, FCA

CPA (MI) Chair, Accounting Standards Board

Phone: +1 (416) 204-3490 Email: [email protected]

For more information, visit www.frascanada.ca

33

Appendix

New IFRS Standards • IFRS 9 • IFRS 15 • IFRS 16 • IFRS 17

34

IFRS 9 – Recent Developments • IASB making amendments to address issues raised by

stakeholders during implementation – AcSB working to get amendments in Handbook for banks applying

IFRS 9 on November 1

Possible changes

in practice

Prepayment Features with Negative Compensation • Narrow exception for particular financial instruments with options to prepay the instrument at

an amount that is less than the unpaid amounts of principal and interest (‘negative compensation’)

• Amendment would allow such instruments to be measured at amortized cost

Modifications or exchanges of financial liabilities do not result in derecognition • Adjustment to amortized cost recognised in profit or loss at the date of

modification/exchange • IASB concluded further standard setting not required. • Will be clarified in the Basis for Conclusions accompanying the Prepayment Features with

Negative Compensation amendments. • This will likely change current practice in Canada

35

IFRS 15 Revenue • IFRS 15 Revenue from Contracts with Customers issued

by IASB May 2014

• Modifications issued by IASB – Defer effective date by 1 year (Sept 2015)

– Narrow-scope clarifications (April 2016)

• Now effective January 1, 2018

• Replaces IAS 11, IAS 18 and related interpretative guidance

• Incorporated into Part I of CPA Canada Handbook – Accounting

36

IFRS 15: Framework

• Establishes a comprehensive framework for recognition, measurement and disclosure of revenue

• Improves comparability across entities (e.g. publicly accountable enterprises, government business enterprises), industries, jurisdictions

• Applies to contracts with customers

• Covers when and how much revenue to recognize

37

IFRS 15: Framework • Excludes leases, insurance contracts, financial

instruments and other contractual rights or obligations, non-monetary exchanges

• Includes guidance for transactions not previously addressed comprehensively – Contracts with multiple deliverables, contract modifications

• Establishes core principle – Reduces need for interpretative guidance

• Provides improved disclosure requirements

38

IFRS 15: Core principle

Step 1: Identify

the contract(s)

with a customer

Step 2: Identify

the performance obligations

in the contract

Step 3: Determine

the transaction

price

Step 4: Allocate

the transaction

price to performance obligations

Step 5: Recognize revenue when (or as) the entity

satisfies a performance obligation

39

IFRS 15: Principal vs Agent • Another party involved in providing a good or service • Focus on control – use significant judgement • Entity is a principal

– Provider of a good or service

– Controls good or service before transferred to customer

– Recognize revenue = Gross amount of consideration

• Entity is an agent – Arranges for good or service to be provided

– Does not control good or service before transferred to customer

– Recognize revenue = Amount of any fee or commission

40

IFRS 15: Disclosure • Disaggregate revenue into categories

– Depict how nature, amount, timing and uncertainty of revenue and cash

flows are affected by economic factors (¶114)

– Application guidance on selection of categories including examples that

might be appropriate (¶B87-B89)

○ Type of good or service (eg major product lines)

○ Geographic region (eg province)

○ Market or type of customer (eg government and non-government customer)

• Disclose sufficient information to enable an understanding of relationship between IFRS 15 and IFRS 8 Operating Segments

41

IFRS 15: Transition

• Optional relief – Completed contracts – Modified contracts

42

IFRS 16 Leases

• IFRS 16 Leases issued by IASB January 2016

• Effective January 1, 2019 – Earlier application permitted if IFRS 15 applied

• Replaces IAS 17 and related interpretative guidance

• Incorporated into Part I of CPA Canada Handbook – Accounting

43

IFRS 16: The Need for Change

• Leases an important and flexible source of financing

• Difficult for investors and others to estimate amount of off-balance sheet obligations

• IAS 17 lessor model substantially remains

• Significant change for lessees – Recognize lease assets and liabilities instead

– Recognition of right-of-use asset by lessee

44

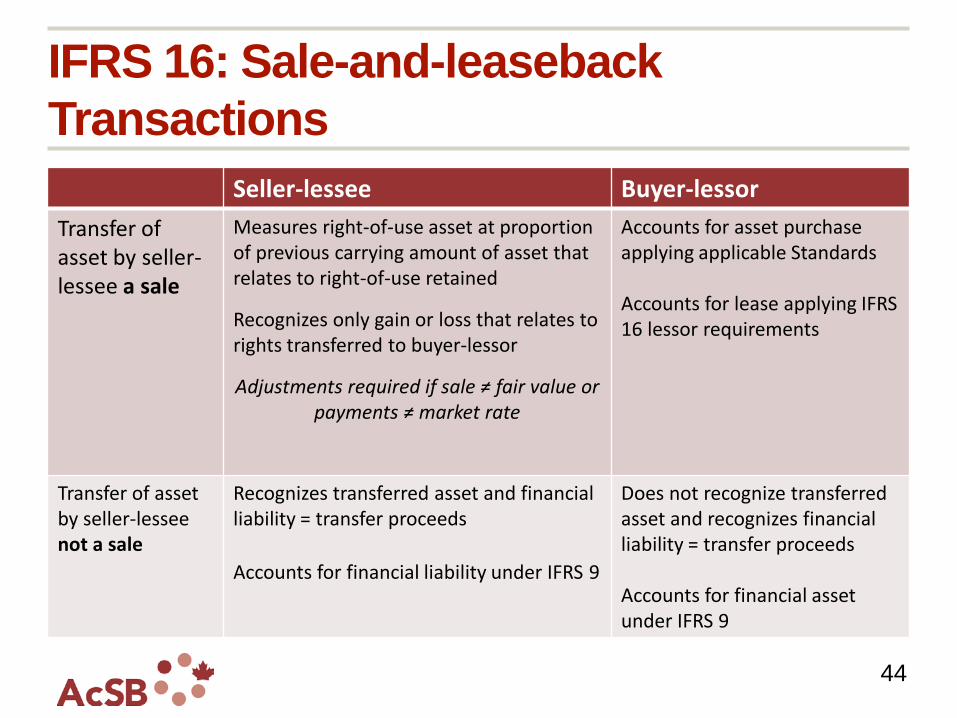

IFRS 16: Sale-and-leaseback Transactions

Seller-lessee Buyer-lessor Transfer of asset by seller-lessee a sale

Measures right-of-use asset at proportion of previous carrying amount of asset that relates to right-of-use retained

Recognizes only gain or loss that relates to rights transferred to buyer-lessor

Adjustments required if sale ≠ fair value or payments ≠ market rate

Accounts for asset purchase applying applicable Standards Accounts for lease applying IFRS 16 lessor requirements

Transfer of asset by seller-lessee not a sale

Recognizes transferred asset and financial liability = transfer proceeds Accounts for financial liability under IFRS 9

Does not recognize transferred asset and recognizes financial liability = transfer proceeds Accounts for financial asset under IFRS 9

45

IFRS 16: Implementation

• Other considerations – Lease contract identification – Volume of contracts – Contract structure – Discount rate for former operating leases a

challenge

46

IFRS 16: Implementation

• Consider choices – potential benefits – Early adopt with IFRS 15?

○ Significant interrelationship between IFRS 15 and IFRS 16

○ E.g., sale/leaseback transactions (IFRS 16.98-103)

» This interrelationship requires the standards to be applied together

47

IFRS 16: Implementation

• Full/modified retrospective ○ Full retrospective may necessitate parallel

systems ○ Modified retrospective with practical

expedients potentially beneficial » Consider availability of information needed to

meet enhanced disclosure requirements » Consider impact of setting right of use asset

equal to liability in year of adoption and subsequently on asset, depreciation, profit etc.

48

IFRS 15 and IFRS 16: Implementation

• Time needed to consider implications • Need to assess extent of change

○ Significant undertaking ○ At same time as other standards ○ Ability to capture information ○ Availability of historical information ○ Consultations/discussions

» Internally with business units » Externally with auditors, investors (e.g. government),

competitors (US GAAP differences)

Processes IT systems

Internal controls

49

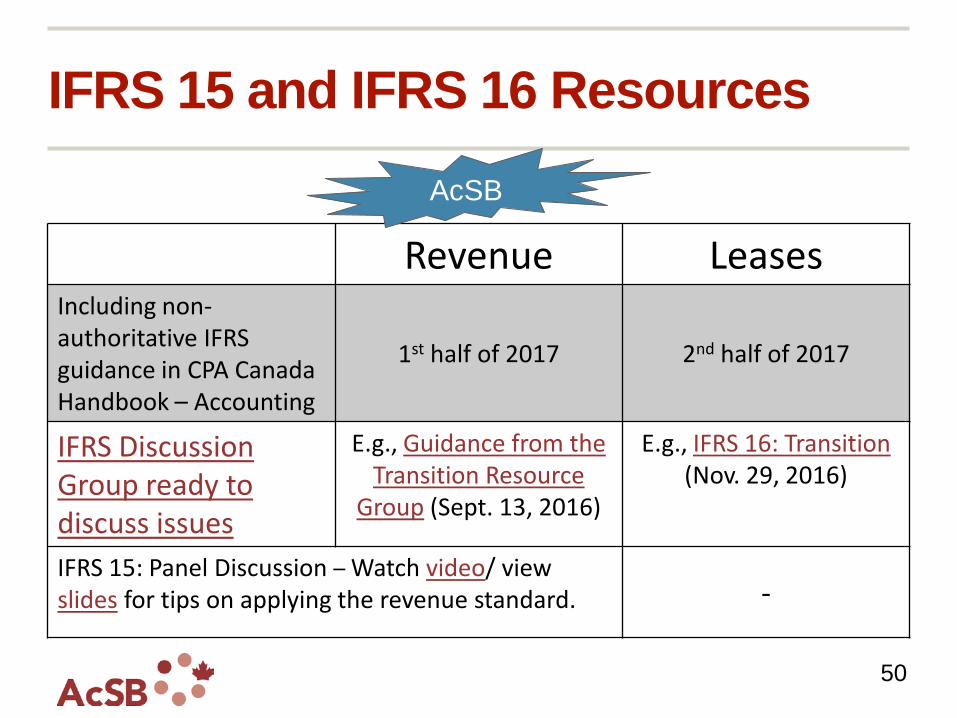

IFRS 15 and IFRS 16 Resources

Implementation page includes:

• Project Summary and Feedback Statement

• Webcasts, e.g., Transition to IFRS 16 (March 2016)

• IASB member articles, e.g., Leases one year on – putting IFRS 16 into practice (Jan 2017)

Implementation page includes:

• Project Summary and Feedback Statement

• Webcast – Implementation update on IFRS 15 (September 2016)

• Transition Resource Group material, e.g., submissions log

IASB Revenue Leases

50

IFRS 15 and IFRS 16 Resources

Revenue Leases Including non-authoritative IFRS guidance in CPA Canada Handbook – Accounting

1st half of 2017 2nd half of 2017

IFRS Discussion Group ready to discuss issues

E.g., Guidance from the Transition Resource

Group (Sept. 13, 2016)

E.g., IFRS 16: Transition (Nov. 29, 2016)

IFRS 15: Panel Discussion – Watch video/ view slides for tips on applying the revenue standard. -

AcSB

51

IFRS 16 – Implementation

• Emerging issue – Easements – Issue is whether easements and right-of-way

agreements are in the scope of IFRS 16

– Issue was discussed by the AcSB’s IFRS Discussion Group – see meeting report and audio

– Financial Accounting Standards Board in U.S. is considering whether standard-setting action is required on this issue.

52

IFRS 17 – Effective in 2021 • Final standard issued in May 2017 • Creates one comprehensive IFRS standard on insurance

− Historically IFRS 4 allowed insurers to maintain previous accounting on transition to IFRS – practice around the world varied

− New standard aims to improve global comparability

• IASB held education sessions for investors on new standard − Session works through example applying new insurance accounting model

• AcSB and IASB each establishing transition support groups − Applications deadline for AcSB group closed September 14 – currently

considering applicants

• Refer to Implementation page