Embed Size (px)

Citation preview

Investment Update AUMCPBO Annual Meeting September 2015

David Zellner Chief Investment Officer

© Wespath, a division of the General Board of Pension and Health Benefits of The United Methodist Church

2

Agenda

• Investment World View

• U.S. Economic Update

• Investment Market Performance Update

• 2015 Top 10 List Update

3

Investment World View

The world will continue to experience modest and

sustainable long-term growth driven by the emerging economies

of Asia, Latin America, Africa and Eastern Europe.

4

U.S. Economic Update

5

Employment Picture

6

2

4

6

8

10

12

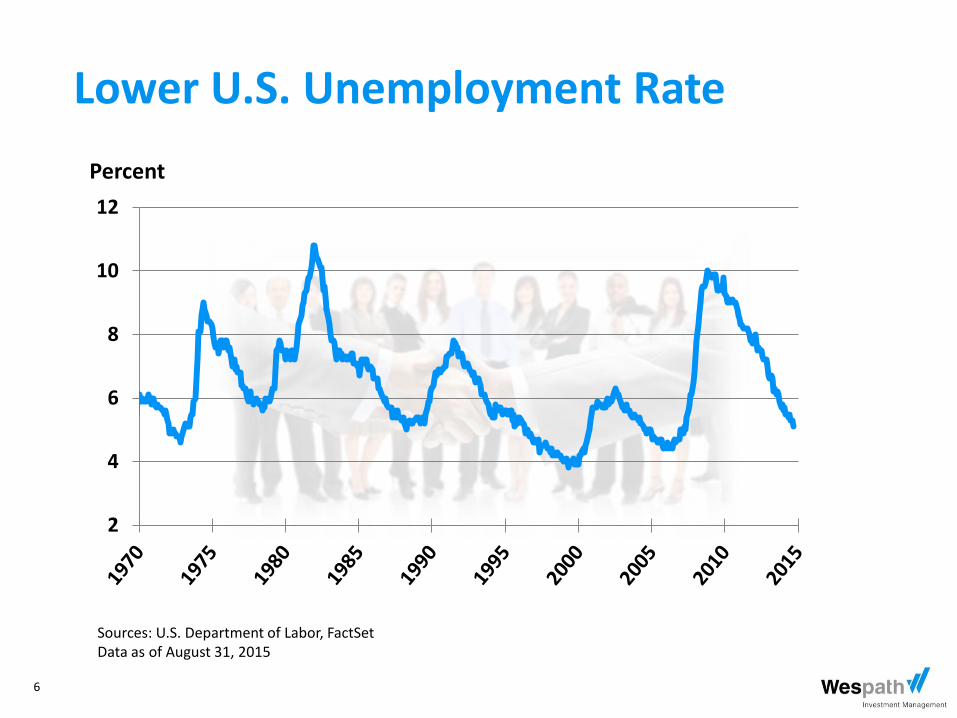

Lower U.S. Unemployment Rate

Sources: U.S. Department of Labor, FactSet Data as of August 31, 2015

Percent

7

100

200

300

400

500

600

700

Sources: U.S. Department of Labor, FactSet Data as of September 4, 2015

Fewer Unemployment Claims

Thousands

8

1,500

2,500

3,500

4,500

5,500

6,500

Job Openings Continue to Increase

Sources: Bureau of Labor Statistics, FactSet Data as of July 31, 2015

Thousands

9

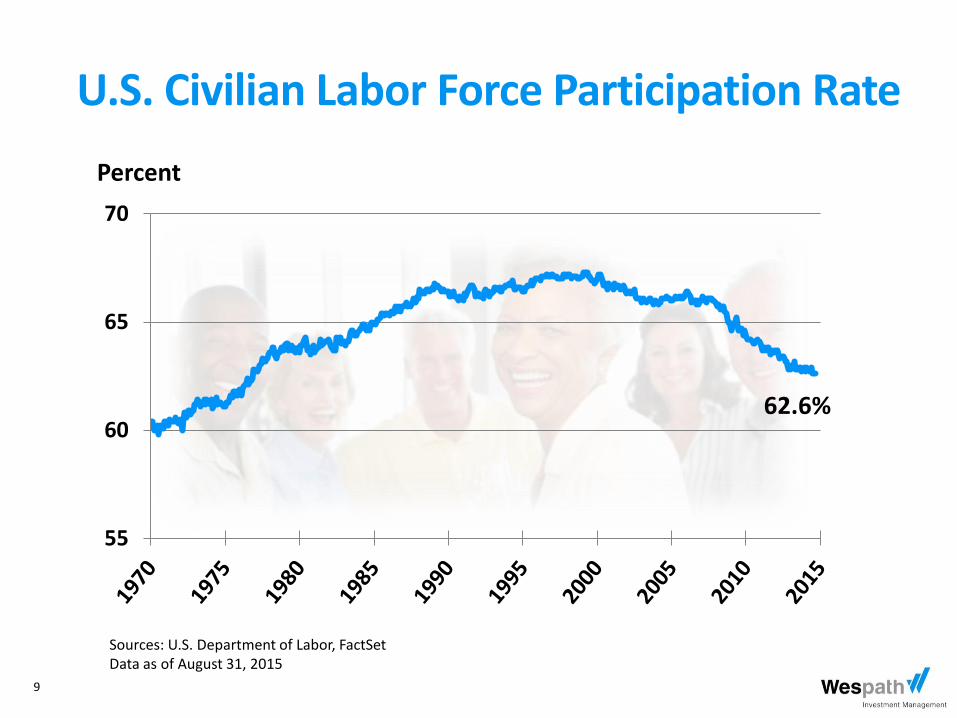

55

60

65

70

62.6%

U.S. Civilian Labor Force Participation Rate

Sources: U.S. Department of Labor, FactSet Data as of August 31, 2015

Percent

10

Consumer Health

11

Consumer Credit Ratings Have Improved

680

685

690

695

700

Source: Fair Isaac Corporation Data as of April 2015

Average FICO Scores

12

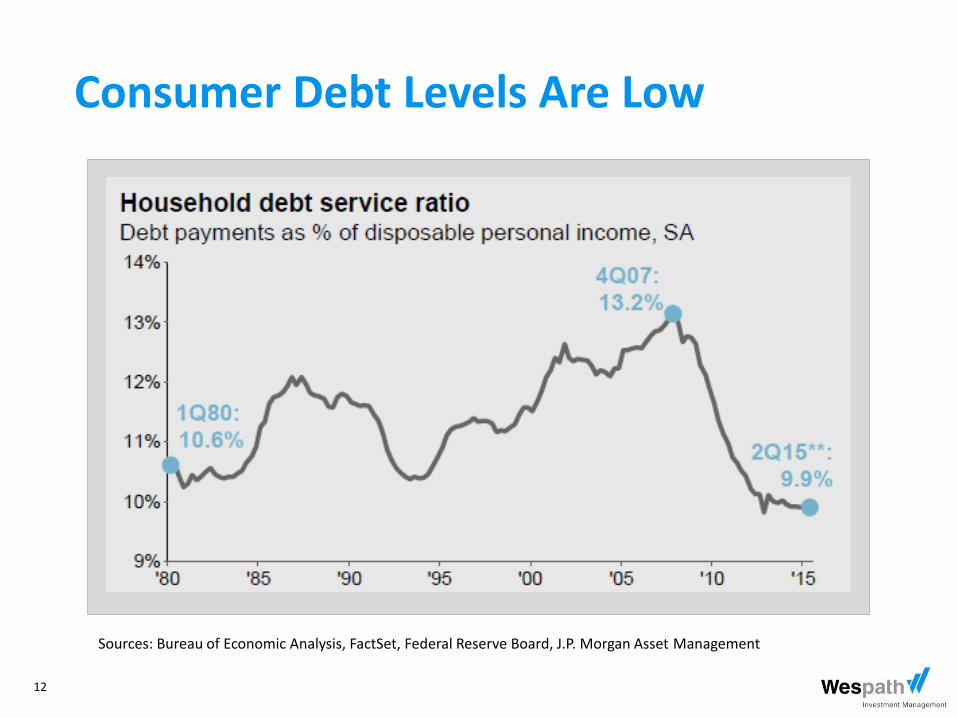

Sources: Bureau of Economic Analysis, FactSet, Federal Reserve Board, J.P. Morgan Asset Management

Consumer Debt Levels Are Low

13

Sources: Bureau of Economic Analysis, FactSet, Federal Reserve Board, J.P. Morgan Asset Management

Consumers Feel More Wealthy

14

S&P/Case-Shiller National Home Price Index

50

100

150

200

-27.3%

+29.6%

6.2% rise returns to July ’06 Levels

Source: S&P Dow Jones Indices; FactSet Data as of June 30, 2015

15

Sources: Census Bureau, J.P. Morgan Asset Management Data as of May 31, 2015.

Housing Remains Affordable

16

Sources: Bureau of Economic Analysis, FactSet; Census Bureau, J.P. Morgan Asset Management. U.S. Data as of June 30, 2015.

Auto Sales Have Improved

17

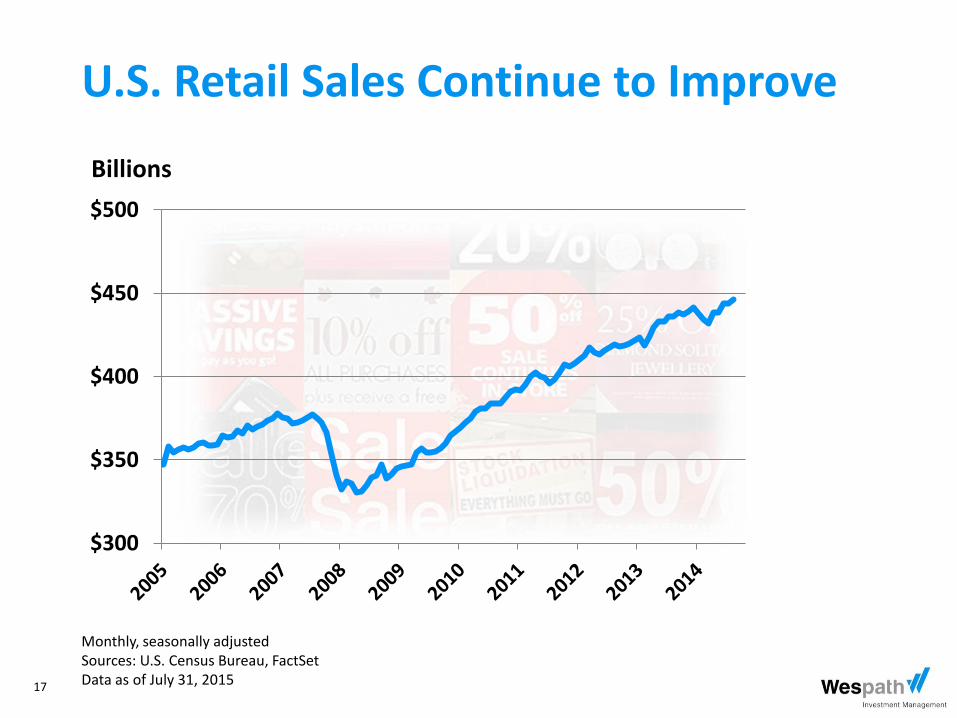

U.S. Retail Sales Continue to Improve

$300

$350

$400

$450

$500

Monthly, seasonally adjusted Sources: U.S. Census Bureau, FactSet Data as of July 31, 2015

Billions

18

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

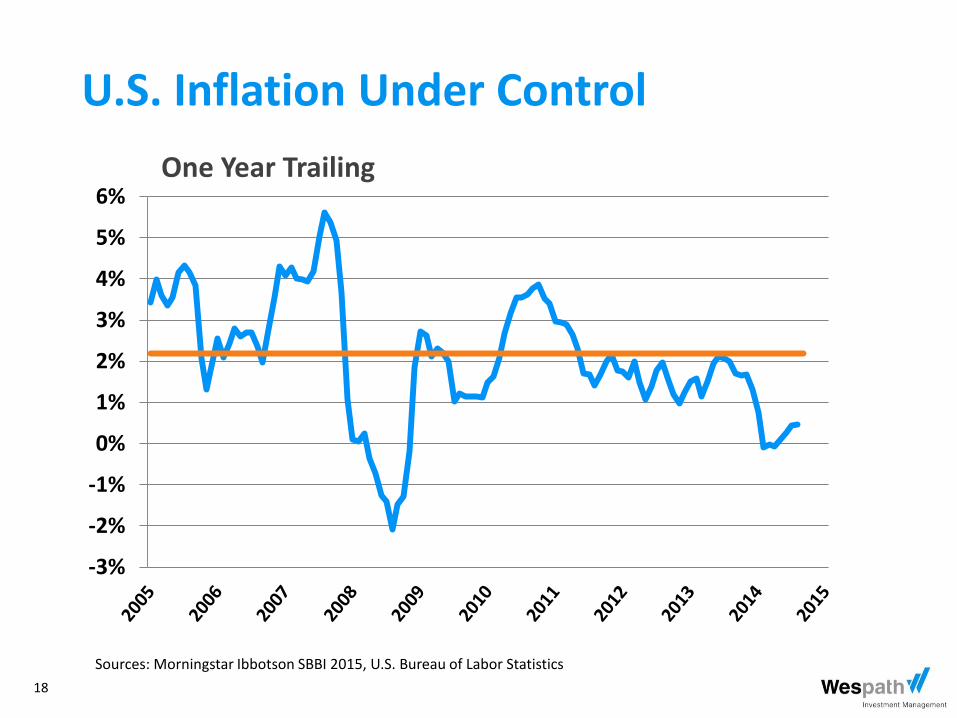

6%One Year Trailing

U.S. Inflation Under Control

Sources: Morningstar Ibbotson SBBI 2015, U.S. Bureau of Labor Statistics

19

U.S. Inflation

-6%

-4%

-2%

0%

2%

4%

6%

8%

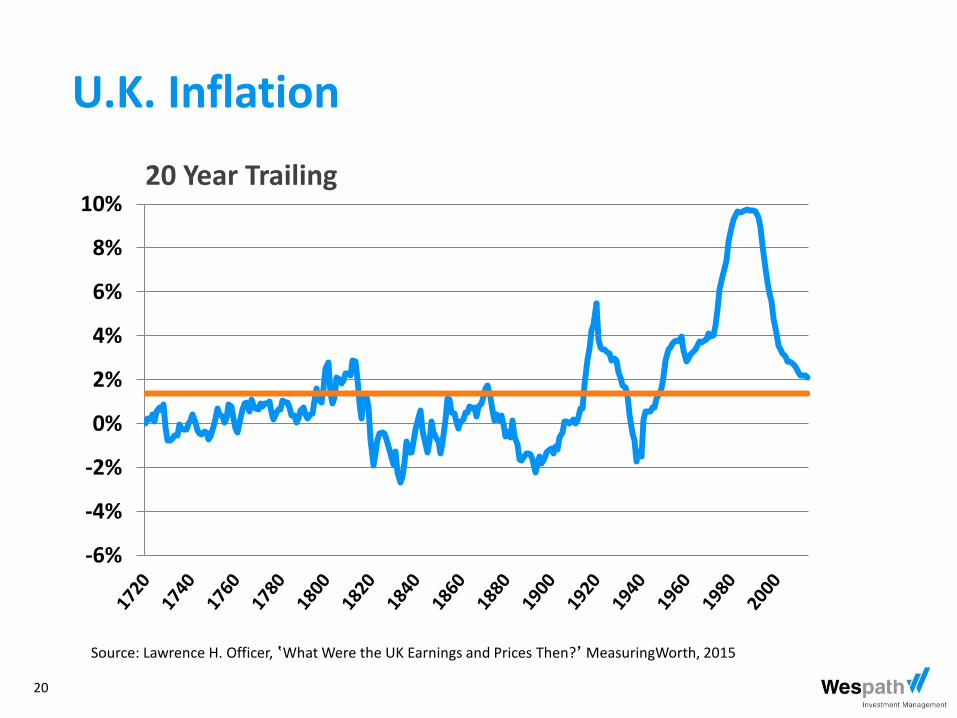

20 Year Trailing

Citation: Lawrence H. Officer and Samuel H. Williamson, ‛The Annual Consumer Price Index for the United States, 1774-2014,’ MeasuringWorth, 2015

20

U.K. Inflation

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

Source: Lawrence H. Officer, ‛What Were the UK Earnings and Prices Then?’ MeasuringWorth, 2015

20 Year Trailing

21

-1

0

1

2

3

4

5

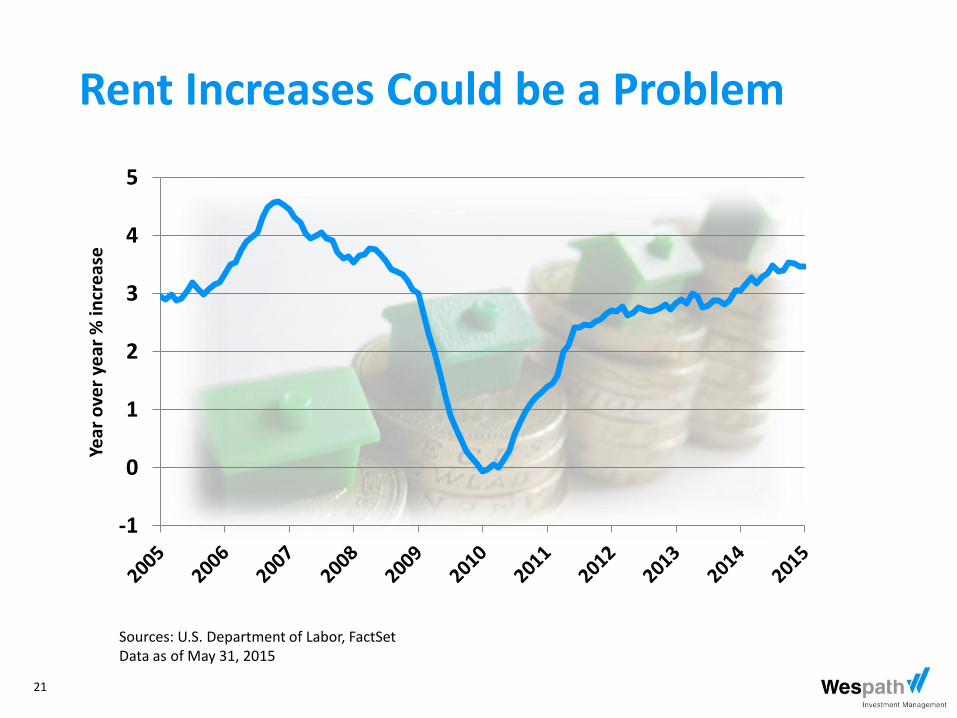

Sources: U.S. Department of Labor, FactSet Data as of May 31, 2015

Rent Increases Could be a Problem Ye

ar o

ver

year

% in

cre

ase

22

Growth

23

U.S. Real Gross Domestic Product (GDP) Growth

-9%

-6%

-3%

0%

3%

6%

9%

Seasonally Adjusted Annual Rate Sources: Bureau of Economic Analysis, FactSet Data as of June 30, 2015

24

U.S. Dollar Index 2012 – 2015

70

80

90

100

110

Data as of September 14, 2015 Source: FactSet

25

70

80

90

100

110

120

130

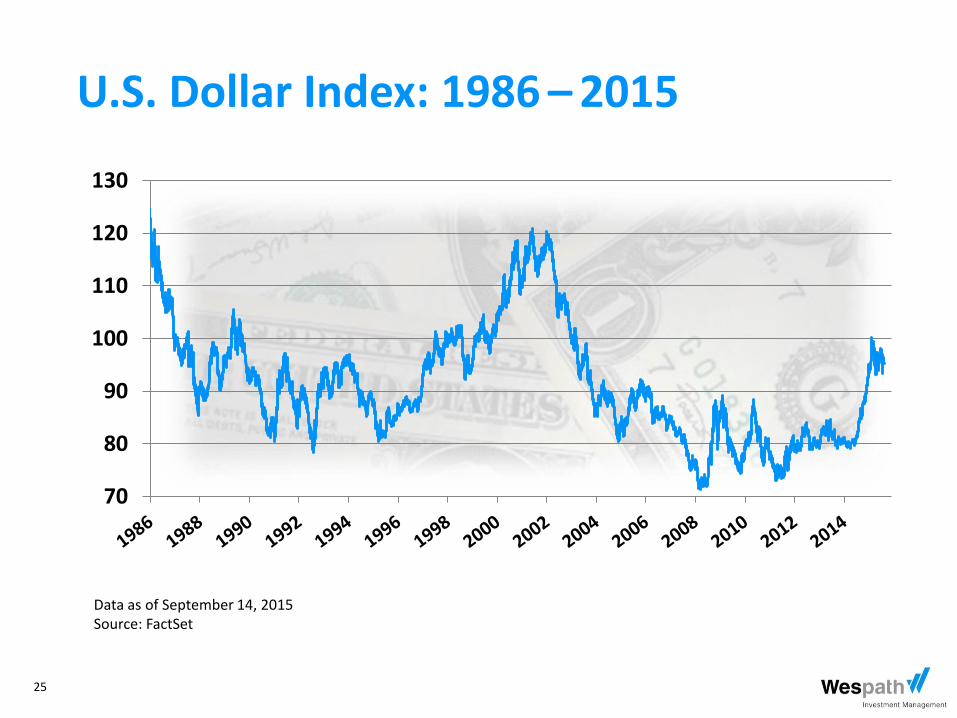

U.S. Dollar Index: 1986 – 2015

Data as of September 14, 2015 Source: FactSet

26

Investment Market Performance Update

27

S&P 500 Index

1,800

1,900

2,000

2,100

2,200

Sources: Standard & Poor’s, FactSet Data as of September 14, 2015

-12%

28

MSCI EAFE Index— Developed Countries (ex USA)

900

1,000

1,100

1,200

Sources: MSCI, FactSet Data as of September 14, 2015

-21%

29

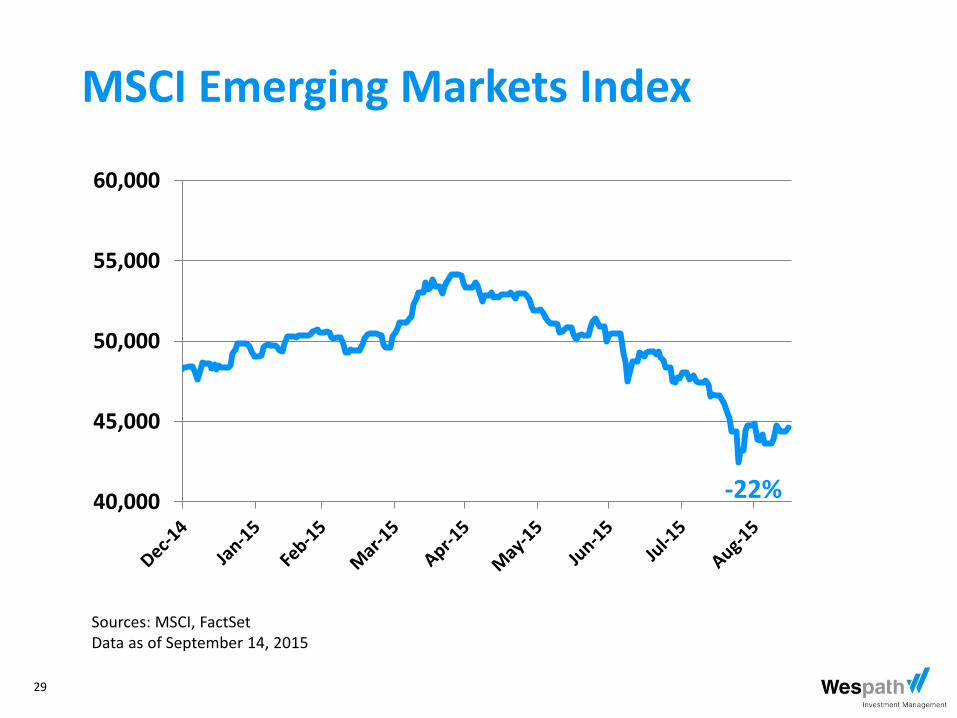

MSCI Emerging Markets Index

40,000

45,000

50,000

55,000

60,000

-22%

Sources: MSCI, FactSet Data as of September 14, 2015

30

Current U.S. Stock Valuations Are Reasonable

Sources: FactSet, FRB, Robert Shiller, Standard & Poor’s, J.P. Morgan Asset Management

31

U.S. Stock Market—Returns by Decade As of September 10, 2015

5.5%

3.1%

5.3%

4.1%

7.6%

-0.2%

15.4%

8.6%

2.3%

8.3% 7.2%

3.0%

13.7%

1.8%

13.4%

16.2%

8.2% 8.5%

13.9%

17.5%

1.4%

11.4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Compounded annual return for 10-year period ending specified year

Mean nominal compounded return = 7.8% (1801-2013)

Sources: Ibbotson Associates, Global Financial Data

32

1,000

2,000

3,000

4,000

5,000

6,000

Source: FactSet Data as of September 14, 2015

Shanghai Stock Exchange Composite Index

33

Shanghai Stock Exchange Composite Index

1,000

2,000

3,000

4,000

5,000

6,000

Source: FactSet Data as of September 14, 2015

June 2010 to Present

34

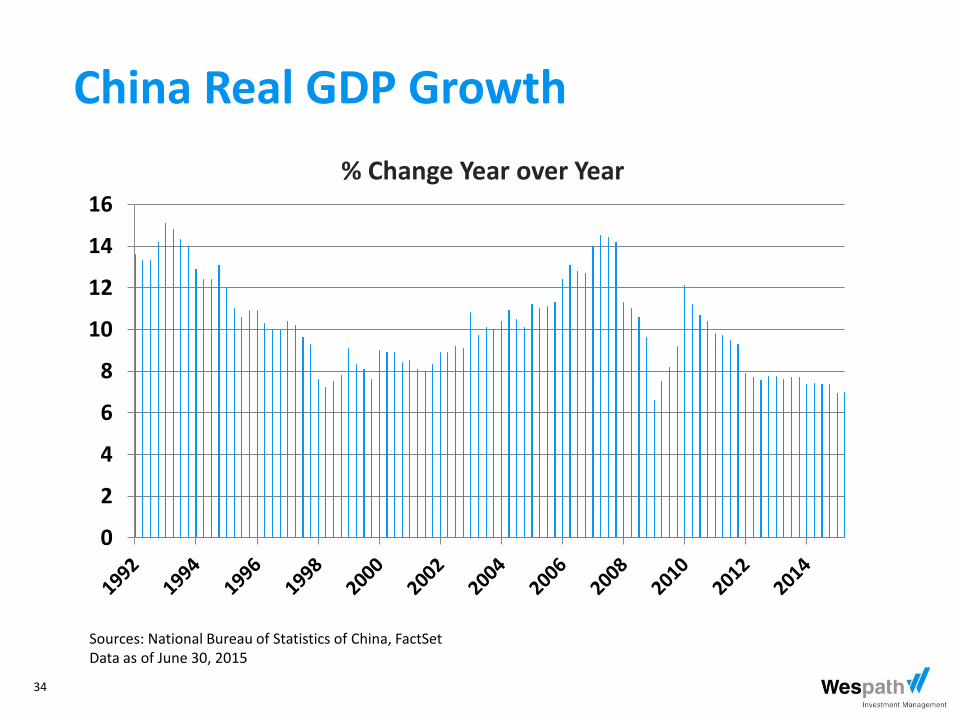

China Real GDP Growth

0

2

4

6

8

10

12

14

16

Sources: National Bureau of Statistics of China, FactSet Data as of June 30, 2015

% Change Year over Year

35

Update on World Economic Issues and Concerns for 2015

35

36

U.S. Public Pension Funding Crisis

37

88%

97%

70%

69%

72%

85%

77%

67%

73%

60%

61%

80% 100%

80%

79%

60%

66% 75%

58%

77%

81%

75% 100%

39%

58%

48%

65%

60%

66% 79%

85%

73%

63%

96%

66%

52%

60%

88%

Source: National Conference of State Legislatures, S&P, Pension and Investments, July 2015

VT 67%

NH 57%

MA 61%

RI 59%

CT 49%

NJ 64%

DE 88%

MD 65%

WV 67%

State Pension Funded Status

38

U.S. Debt Burden

39

Sources: U.S. Treasury, BEA, CBO, St. Louis Fed, J.P. Morgan Asset Management

January 2012 Forecast

40

Sources: U.S. Treasury, BEA, CBO, St. Louis Fed, J.P. Morgan Asset Management

June 2015 Forecast

41

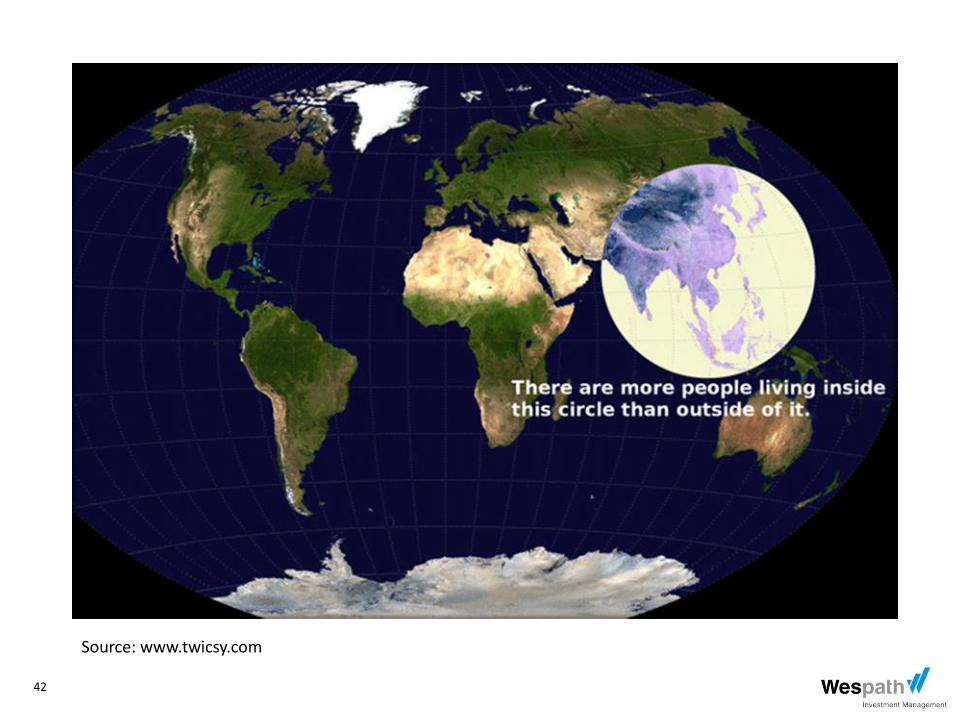

Economic Growth in the Developing World

42

Source: www.twicsy.com

43

Sources: The Brookings Institution, World Bank, United Nations, J.P. Morgan Asset Management

Strong Long-Term Case for Developing Markets

44

U.S. Energy Renaissance

45

Oil Prices Remain Low

$35

$45

$55

$65

$75

$85

$95

$105

$115

Dec-13 Mar-14 Jun-14 Sep-14 Dec-14 Mar-15 Jun-15

Source: FactSet Data as of September 14, 2015

46

World’s Response to Climate Change

47

Paris U.N. Climate Change Conference November 30 – December 11, 2015

48

Eurozone Recovery and Threat of Deflation

49

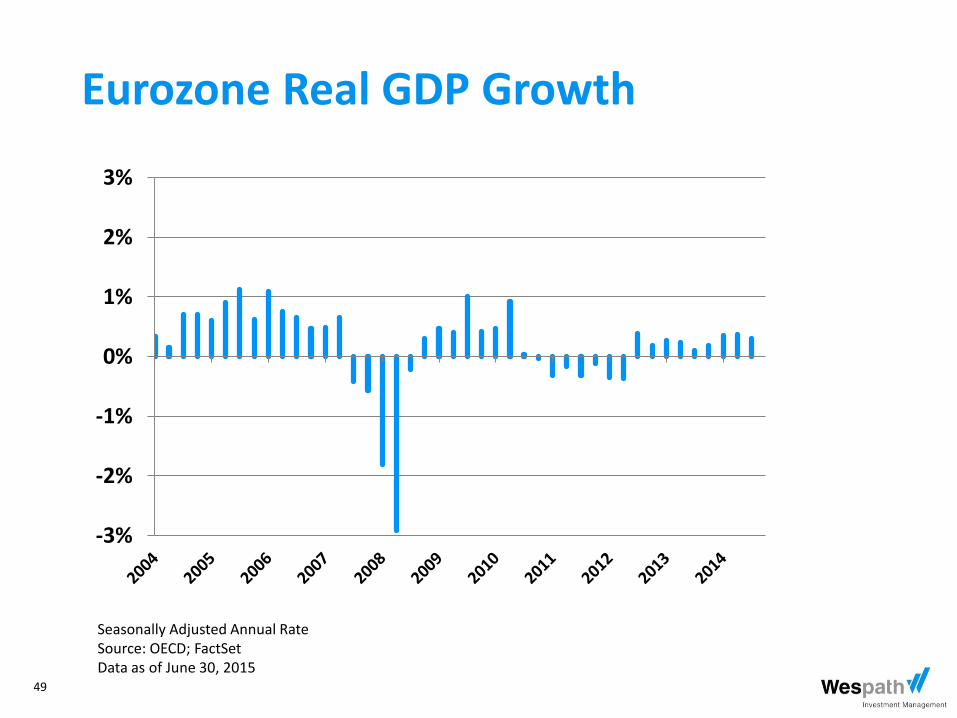

Eurozone Real GDP Growth

-3%

-2%

-1%

0%

1%

2%

3%

Seasonally Adjusted Annual Rate Source: OECD; FactSet Data as of June 30, 2015

50

Eurozone Inflation

-1%

0%

1%

2%

3%

4%

5%

Sources: Eurostat, FactSet Data as of August 31, 2015

51

Geopolitical Crises

52

wespath.com