Embed Size (px)

Citation preview

March 10, 2016

INITIATION Vocus Communications Ltd. (VOC.AX)

Neutral Equity Research

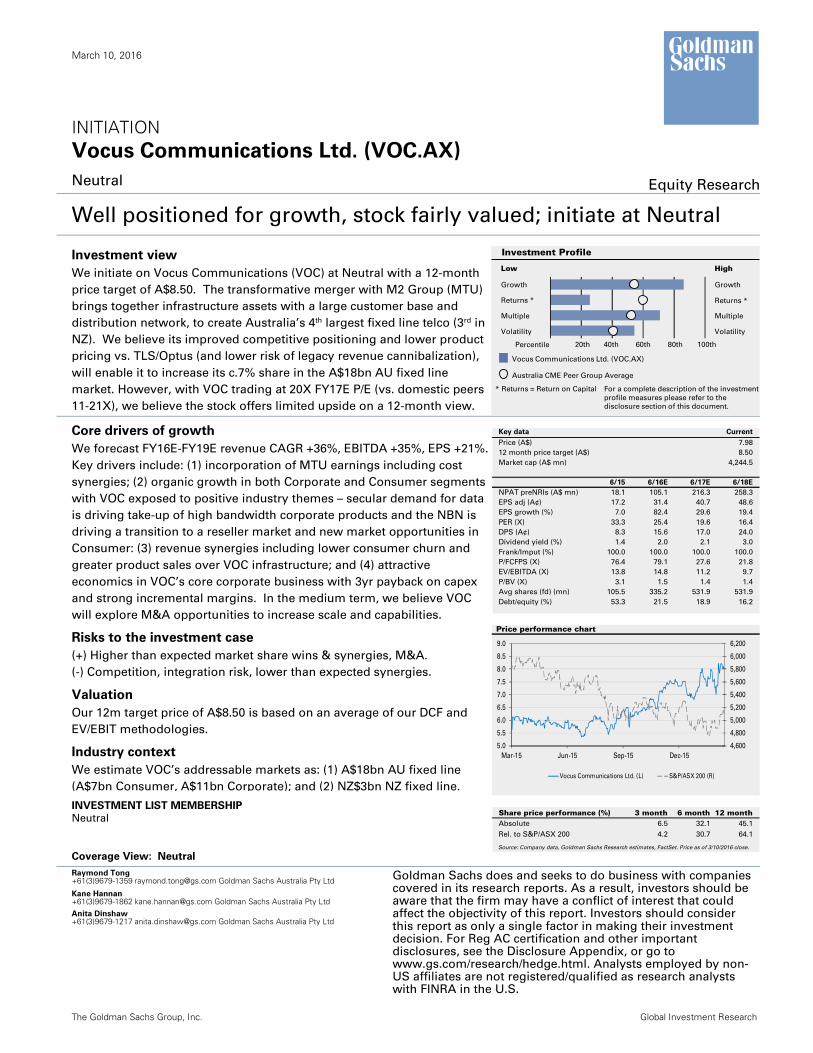

Well positioned for growth, stock fairly valued; initiate at Neutral

Investment view

We initiate on Vocus Communications (VOC) at Neutral with a 12-month

price target of A$8.50. The transformative merger with M2 Group (MTU)

brings together infrastructure assets with a large customer base and

distribution network, to create Australia’s 4th largest fixed line telco (3rd in

NZ). We believe its improved competitive positioning and lower product

pricing vs. TLS/Optus (and lower risk of legacy revenue cannibalization),

will enable it to increase its c.7% share in the A$18bn AU fixed line

market. However, with VOC trading at 20X FY17E P/E (vs. domestic peers

11-21X), we believe the stock offers limited upside on a 12-month view.

Core drivers of growth

We forecast FY16E-FY19E revenue CAGR +36%, EBITDA +35%, EPS +21%.

Key drivers include: (1) incorporation of MTU earnings including cost

synergies; (2) organic growth in both Corporate and Consumer segments

with VOC exposed to positive industry themes – secular demand for data

is driving take-up of high bandwidth corporate products and the NBN is

driving a transition to a reseller market and new market opportunities in

Consumer: (3) revenue synergies including lower consumer churn and

greater product sales over VOC infrastructure; and (4) attractive

economics in VOC’s core corporate business with 3yr payback on capex

and strong incremental margins. In the medium term, we believe VOC

will explore M&A opportunities to increase scale and capabilities.

Risks to the investment case

(+) Higher than expected market share wins & synergies, M&A.

(-) Competition, integration risk, lower than expected synergies.

Valuation

Our 12m target price of A$8.50 is based on an average of our DCF and

EV/EBIT methodologies.

Industry context

We estimate VOC’s addressable markets as: (1) A$18bn AU fixed line

(A$7bn Consumer, A$11bn Corporate); and (2) NZ$3bn NZ fixed line.

INVESTMENT LIST MEMBERSHIP

Neutral

Coverage View: Neutral

Raymond Tong +61(3)9679-1359 [email protected] Goldman Sachs Australia Pty Ltd Goldman Sachs does and seeks to do business with companies

covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. For Reg AC certification and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html. Analysts employed by non-US affiliates are not registered/qualified as research analysts with FINRA in the U.S.

Kane Hannan +61(3)9679-1862 [email protected] Goldman Sachs Australia Pty LtdAnita Dinshaw +61(3)9679-1217 [email protected] Goldman Sachs Australia Pty Ltd

The Goldman Sachs Group, Inc. Global Investment Research

Growth

Returns *

Multiple

Volatility Volatility

Multiple

Returns *

Growth

Investment Profile

Low High

Percentile 20th 40th 60th 80th 100th

* Returns = Return on Capital For a complete description of the investment

profile measures please refer to the

disclosure section of this document.

Vocus Communications Ltd. (VOC.AX)

Australia CME Peer Group Average

Key data Current

Price (A$) 7.98

12 month price target (A$) 8.50

Market cap (A$ mn) 4,244.5

6/15 6/16E 6/17E 6/18E

NPAT preNRIs (A$ mn) 18.1 105.1 216.3 258.3

EPS adj (A¢) 17.2 31.4 40.7 48.6

EPS growth (%) 7.0 82.4 29.6 19.4

PER (X) 33.3 25.4 19.6 16.4

DPS (A¢) 8.3 15.6 17.0 24.0

Dividend yield (%) 1.4 2.0 2.1 3.0

Frank/Imput (%) 100.0 100.0 100.0 100.0

P/FCFPS (X) 76.4 79.1 27.6 21.8

EV/EBITDA (X) 13.8 14.8 11.2 9.7

P/BV (X) 3.1 1.5 1.4 1.4

Avg shares (fd) (mn) 105.5 335.2 531.9 531.9

Debt/equity (%) 53.3 21.5 18.9 16.2

Price performance chart

4,600

4,800

5,000

5,200

5,400

5,600

5,800

6,000

6,200

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0

Mar-15 Jun-15 Sep-15 Dec-15

Vocus Communications Ltd. (L) S&P/ASX 200 (R)

Share price performance (%) 3 month 6 month 12 monthAbsolute 6.5 32.1 45.1

Rel. to S&P/ASX 200 4.2 30.7 64.1

Source: Company data, Goldman Sachs Research estimates, FactSet. Price as of 3/10/2016 close.

March 10, 2016 Vocus Communications Ltd. (VOC.AX)

Goldman Sachs Global Investment Research 2

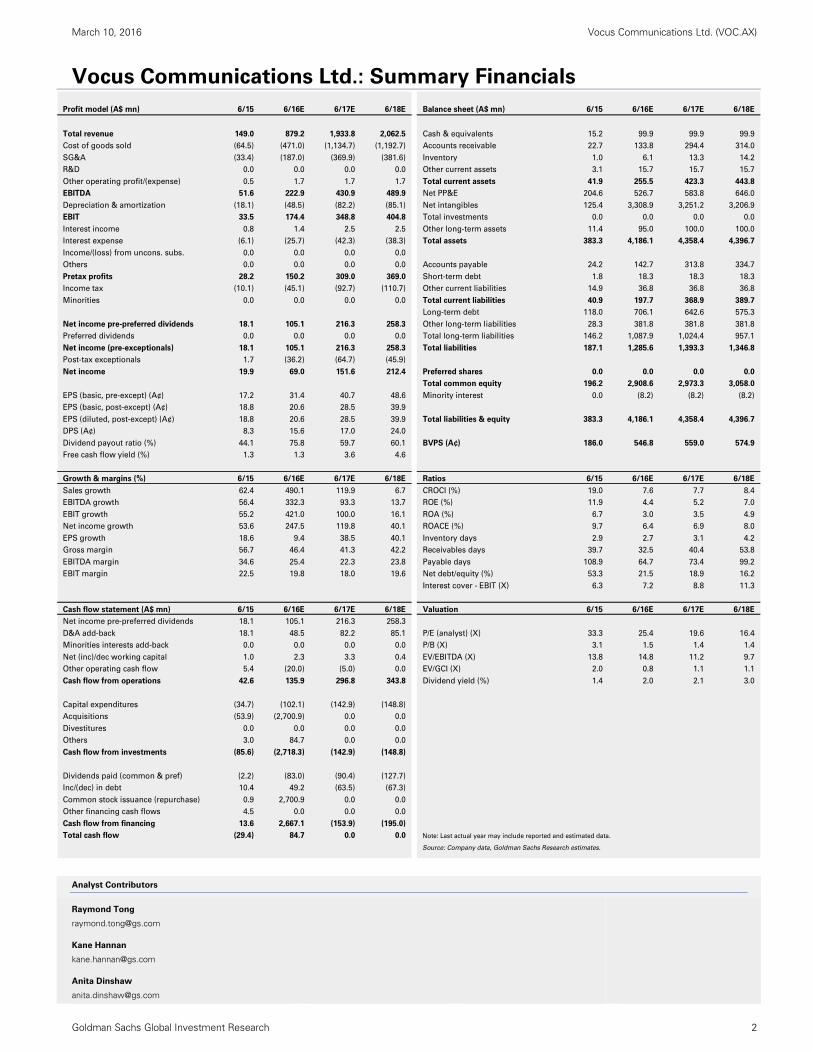

Vocus Communications Ltd.: Summary Financials

Analyst Contributors

Raymond Tong

Kane Hannan

Anita Dinshaw

Profit model (A$ mn) 6/15 6/16E 6/17E 6/18E Balance sheet (A$ mn) 6/15 6/16E 6/17E 6/18E

Total revenue 149.0 879.2 1,933.8 2,062.5 Cash & equivalents 15.2 99.9 99.9 99.9

Cost of goods sold (64.5) (471.0) (1,134.7) (1,192.7) Accounts receivable 22.7 133.8 294.4 314.0

SG&A (33.4) (187.0) (369.9) (381.6) Inventory 1.0 6.1 13.3 14.2

R&D 0.0 0.0 0.0 0.0 Other current assets 3.1 15.7 15.7 15.7

Other operating profit/(expense) 0.5 1.7 1.7 1.7 Total current assets 41.9 255.5 423.3 443.8

EBITDA 51.6 222.9 430.9 489.9 Net PP&E 204.6 526.7 583.8 646.0

Depreciation & amortization (18.1) (48.5) (82.2) (85.1) Net intangibles 125.4 3,308.9 3,251.2 3,206.9

EBIT 33.5 174.4 348.8 404.8 Total investments 0.0 0.0 0.0 0.0

Interest income 0.8 1.4 2.5 2.5 Other long-term assets 11.4 95.0 100.0 100.0

Interest expense (6.1) (25.7) (42.3) (38.3) Total assets 383.3 4,186.1 4,358.4 4,396.7

Income/(loss) from uncons. subs. 0.0 0.0 0.0 0.0

Others 0.0 0.0 0.0 0.0 Accounts payable 24.2 142.7 313.8 334.7

Pretax profits 28.2 150.2 309.0 369.0 Short-term debt 1.8 18.3 18.3 18.3

Income tax (10.1) (45.1) (92.7) (110.7) Other current liabilities 14.9 36.8 36.8 36.8

Minorities 0.0 0.0 0.0 0.0 Total current liabilities 40.9 197.7 368.9 389.7

Long-term debt 118.0 706.1 642.6 575.3

Net income pre-preferred dividends 18.1 105.1 216.3 258.3 Other long-term liabilities 28.3 381.8 381.8 381.8

Preferred dividends 0.0 0.0 0.0 0.0 Total long-term liabilities 146.2 1,087.9 1,024.4 957.1

Net income (pre-exceptionals) 18.1 105.1 216.3 258.3 Total liabilities 187.1 1,285.6 1,393.3 1,346.8

Post-tax exceptionals 1.7 (36.2) (64.7) (45.9)

Net income 19.9 69.0 151.6 212.4 Preferred shares 0.0 0.0 0.0 0.0

Total common equity 196.2 2,908.6 2,973.3 3,058.0

EPS (basic, pre-except) (A¢) 17.2 31.4 40.7 48.6 Minority interest 0.0 (8.2) (8.2) (8.2)

EPS (basic, post-except) (A¢) 18.8 20.6 28.5 39.9

EPS (diluted, post-except) (A¢) 18.8 20.6 28.5 39.9 Total liabilities & equity 383.3 4,186.1 4,358.4 4,396.7

DPS (A¢) 8.3 15.6 17.0 24.0

Dividend payout ratio (%) 44.1 75.8 59.7 60.1 BVPS (A¢) 186.0 546.8 559.0 574.9

Free cash flow yield (%) 1.3 1.3 3.6 4.6

Growth & margins (%) 6/15 6/16E 6/17E 6/18E Ratios 6/15 6/16E 6/17E 6/18E

Sales growth 62.4 490.1 119.9 6.7 CROCI (%) 19.0 7.6 7.7 8.4

EBITDA growth 56.4 332.3 93.3 13.7 ROE (%) 11.9 4.4 5.2 7.0

EBIT growth 55.2 421.0 100.0 16.1 ROA (%) 6.7 3.0 3.5 4.9

Net income growth 53.6 247.5 119.8 40.1 ROACE (%) 9.7 6.4 6.9 8.0

EPS growth 18.6 9.4 38.5 40.1 Inventory days 2.9 2.7 3.1 4.2

Gross margin 56.7 46.4 41.3 42.2 Receivables days 39.7 32.5 40.4 53.8

EBITDA margin 34.6 25.4 22.3 23.8 Payable days 108.9 64.7 73.4 99.2

EBIT margin 22.5 19.8 18.0 19.6 Net debt/equity (%) 53.3 21.5 18.9 16.2

Interest cover - EBIT (X) 6.3 7.2 8.8 11.3

Cash flow statement (A$ mn) 6/15 6/16E 6/17E 6/18E Valuation 6/15 6/16E 6/17E 6/18E

Net income pre-preferred dividends 18.1 105.1 216.3 258.3

D&A add-back 18.1 48.5 82.2 85.1 P/E (analyst) (X) 33.3 25.4 19.6 16.4

Minorities interests add-back 0.0 0.0 0.0 0.0 P/B (X) 3.1 1.5 1.4 1.4

Net (inc)/dec working capital 1.0 2.3 3.3 0.4 EV/EBITDA (X) 13.8 14.8 11.2 9.7

Other operating cash flow 5.4 (20.0) (5.0) 0.0 EV/GCI (X) 2.0 0.8 1.1 1.1

Cash flow from operations 42.6 135.9 296.8 343.8 Dividend yield (%) 1.4 2.0 2.1 3.0

Capital expenditures (34.7) (102.1) (142.9) (148.8)

Acquisitions (53.9) (2,700.9) 0.0 0.0

Divestitures 0.0 0.0 0.0 0.0

Others 3.0 84.7 0.0 0.0

Cash flow from investments (85.6) (2,718.3) (142.9) (148.8)

Dividends paid (common & pref) (2.2) (83.0) (90.4) (127.7)

Inc/(dec) in debt 10.4 49.2 (63.5) (67.3)

Common stock issuance (repurchase) 0.9 2,700.9 0.0 0.0

Other financing cash flows 4.5 0.0 0.0 0.0

Cash flow from financing 13.6 2,667.1 (153.9) (195.0)

Total cash flow (29.4) 84.7 0.0 0.0 Note: Last actual year may include reported and estimated data.

Source: Company data, Goldman Sachs Research estimates.

March 10, 2016 Vocus Communications Ltd. (VOC.AX)

Goldman Sachs Global Investment Research 3

Contents

Executive Summary 4

Company strategy and profile 6

Outlook and key stock drivers 12

Building blocks in place to win share across Consumer & Corporate 12

Corporate: Infrastructure ownership, secular demand for data, strong economics 12

Consumer: Strong industry growth, NBN opportunity 14

Synergies: We see upside from potential revenue synergies 16

We expect VOC will continue to pursue M&A opportunities 18

Industry overview 20

Financial forecasts 25

Valuation 27

Key risks 29

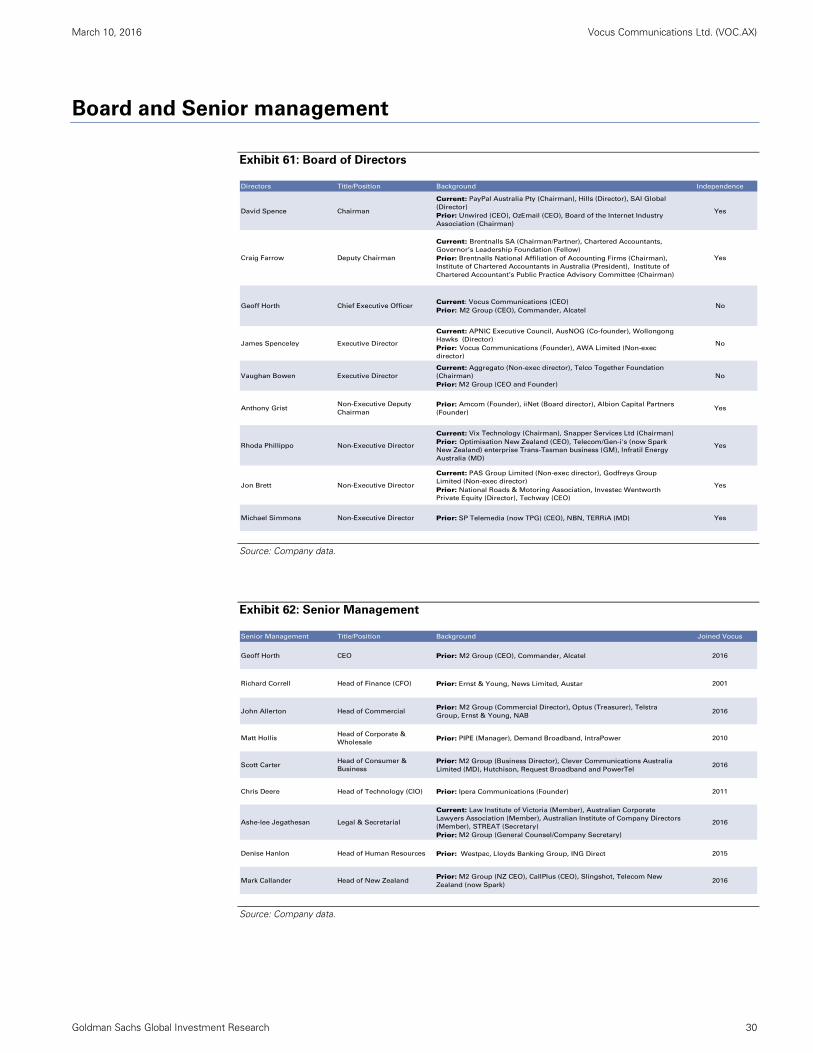

Board and Senior management 30

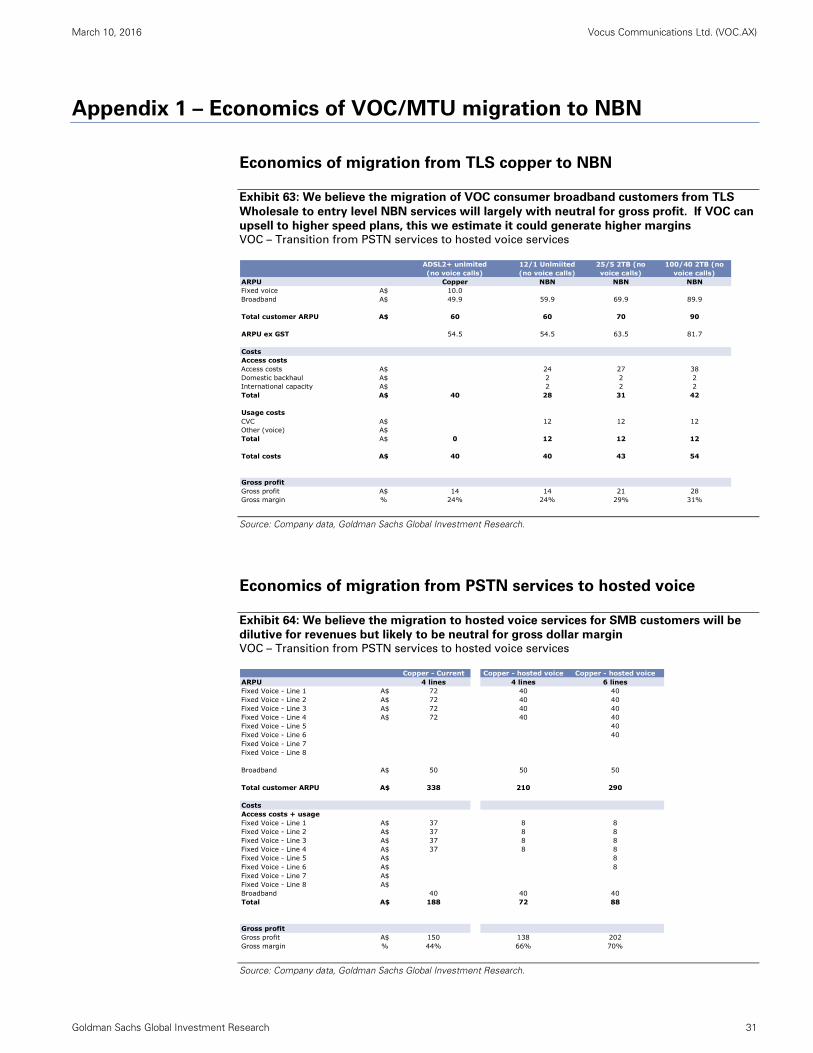

Appendix 1 – Economics of VOC/MTU migration to NBN 31

Economics of migration from TLS copper to NBN 31

Economics of migration from PSTN services to hosted voice 31

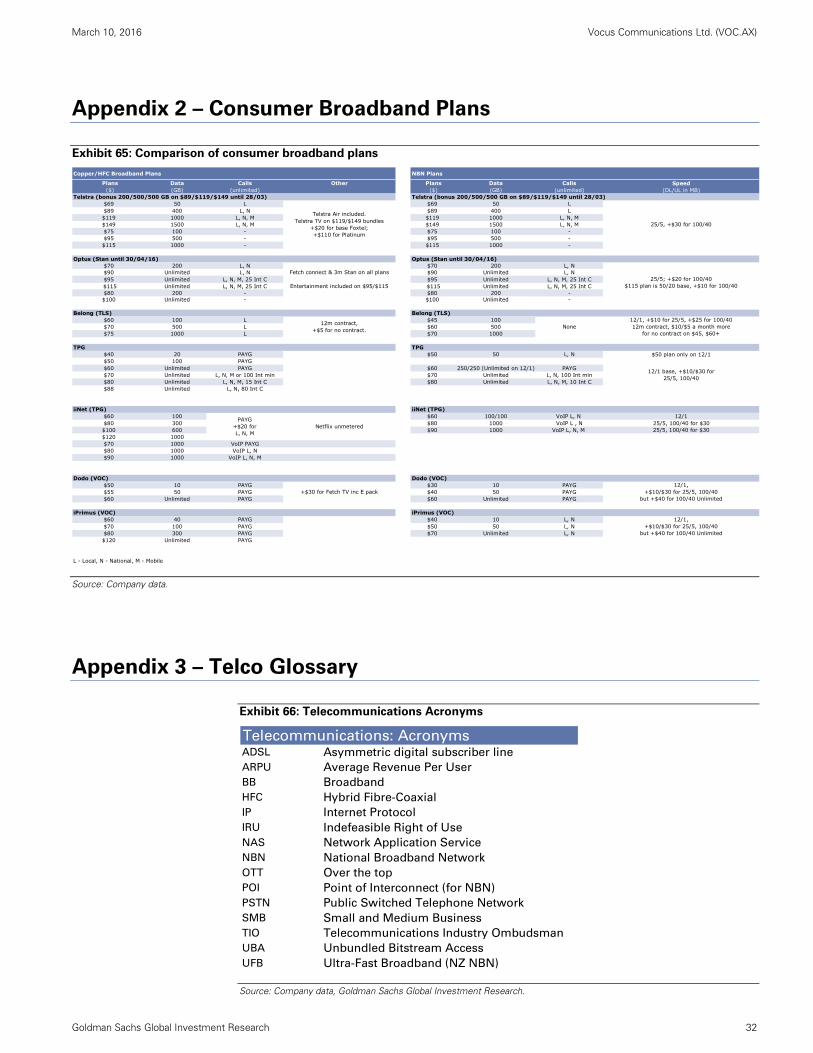

Appendix 2 – Consumer Broadband Plans 32

Appendix 3 – Telco Glossary 32

Disclosure Appendix 33

March 10, 2016 Vocus Communications Ltd. (VOC.AX)

Goldman Sachs Global Investment Research 4

Executive Summary

Well positioned for growth; stock fairly valued; initiate at Neutral

We initiate coverage on Vocus Communications (VOC) with a Neutral rating and 12-month

price target of A$8.50. The transformative merger with M2 Group (MTU) brings together

infrastructure assets with a large customer base and distribution network, to create

Australia’s 4th largest fixed line telco (and 3rd in NZ). We believe its improved competitive

positioning and lower product pricing vs. TLS/Optus (and lower risk of legacy revenue

cannibalization), will enable it to increase its c.7% share of the A$18bn AU fixed line market.

However, with the stock trading at 20X FY17E P/E (vs. domestic peers 11-21X) we believe

the stock offers limited upside on a 12-month view.

Key drivers of growth

We forecast FY16E-FY19E revenue CAGR +36%, EBITDA +35%, EPS +21%. Key drivers

include: (1) incorporation of MTU earnings including cost synergies; (2) organic growth in

both the Corporate and Consumer segments; (3) revenue synergies including lower

consumer churn and greater product sales over VOC infrastructure; and (4) attractive

economics in VOC’s core infrastructure based corporate business.

We believe VOC is well positioned to drive growth:

Positioned to increase market share:

Low market share in a large addressable market: We estimate VOC/MTU has low

market share: (1) 6% of the A$7bn Australian fixed line Consumer market; (2) 7% in

A$11bn fixed line Corporate market; and (3) c.9% share of NZ$3bn NZ fixed line market.

Improved competitive positioning following consolidation: We believe VOC has a

stronger competitive positioning following its transformative M&A with MTU,

combining: (1) national fibre network; (2) national distribution assets; and (3) increased

scale.

Lower pricing vs. incumbents: (1) in Corporate, VOC seeks to price its products

c.15% below TLS; (2) in Consumer, we estimate MTU through the Dodo brand prices

broadband products at c.20-40% discount to incumbents TLS/Optus, while at largely

similar levels to TPM.

Exposure to positive industry themes:

Corporate: We believe VOC will continue to benefit from secular demand for data that

is driving demand for high bandwidth products. We believe: (1) the economics are

positive in the Corporate segment with 3-year payback for capex investments and

strong incremental margins; and (2) VOC does not have significant exposure to the

risks of cannibalization of legacy products unlike its larger competitors TLS and Optus.

Consumer: We believe VOC, given its low market share, stands to benefit from the

rollout of the National Broadband Network (NBN) in Australia and Ultra-Fast

Broadband (UFB) in NZ. This could potentially be an opportunity for VOC to win

market share as customers migrate from copper to the NBN/UFB and the industry

transitions to a reseller model in Australia.

March 10, 2016 Vocus Communications Ltd. (VOC.AX)

Goldman Sachs Global Investment Research 5

Synergies from consolidation:

Costs: VOC is targeting c.A$40mn of cost synergies by FY18E. We note this

represents c.4% of VOC/MTU combined cost base, which looks conservative compared

with recent transactions.

Revenues: We believe the key areas of revenue synergies include: (1) lowering

Consumer broadband churn from high levels of c.2.8%/month by increasing use of

VOC infrastructure to improve bandwidth capacity; and (2) leveraging MTU’s sales

force and distribution assets to increase product sales to SMB segments in VOC on-net

buildings.

We expect VOC to continue to explore M&A opportunities

While the Australian telco market has consolidated, we expect VOC to continue to explore

M&A opportunities across Australia and New Zealand (ANZ) to increase its network

footprint, scale and capabilities, consistent with management’s stated strategy.

We assume VOC will deleverage from its proforma 1H16 Net Debt/EBITDA 2.0X to 1.0X by

FY18E. While its dividend policy is yet to be determined, we have assumed a dividend

payout ratio of 50-60% which is lower than MTU’s prior dividend payout ratio of 70% given

the higher capital intensity of the combined entity.

Key risks: Competition, integration, forecast

Competition: VOC faces competition from larger operators Telstra (TLS), Optus and TPG

Telecom (TPM) (and Spark New Zealand (SPK), Vodafone NZ in NZ) who we believe have

stronger competitive positions given greater scale and ability to leverage mobile

infrastructure ownership (apart from TPM). Over time, it will likely face increased

competition in the Consumer segment from new entrants as the NBN rollout reaches

greater scale. However we note that VOC: (1) has the lowest market share among its key

competitors; and (2) is not facing a material increase in wholesale input costs (vs.

competitors) with the migration to the NBN.

M&A integration/execution risk: While both have a strong track record of integrating

acquisitions, combining VOC/MTU soon after VOC’s acquisition of AMM will likely to be

challenging. There is a risk that synergies from the merger may not be achieved.

Valuation: 12-month target price of A$8.50

Our 12-month target price of A$8.50 is based on a blended average of:

DCF valuation: Our DCF of A$8.30 is based on: (1) WACC 9.0%; and (2) terminal growth

rate (TGR) 2.5%.

EV/EBIT valuation: Our EV/EBIT based valuation is A$8.65 is based on an EV/EBIT

multiple of 15X on FY17E earnings. Our multiple of 15X compares with the average of 13X

for domestic peers and 16X for high growth international challengers.

Our 12-month target price of A$8.50 implies a FY16E/FY17E/FY18E P/E of 27X/21X/18X and

dividend yield of 1.8%/2.0%/2.8%.

March 10, 2016 Vocus Communications Ltd. (VOC.AX)

Goldman Sachs Global Investment Research 6

Company strategy and profile

Company background

Vocus Communications

Vocus is a telecommunications company offering fibre, ethernet and internet services

across ANZ. Founded in Australia in 2008 by James Spenceley as a voice and internet

services provider, it has since expanded its range of products and acquired a number of

data centres and fibre assets in ANZ, now owning national intracity infrastructure in

Australia. Vocus has also invested in international submarine cable capacity that connects

ANZ with Asia and the USA. It listed on the ASX in December 2014.

M2 Group

The M2 Group (MTU) is a retail and wholesale provider of telco (broadband, voice, and

mobile), utility and insurance services to Consumer and SMB customers. MTU was

founded in 1999 by Vaughan Bowen and listed on the ASX in October 2004. Like VOC,

MTU has also grown its business acquisitively, investing in a range of challenger brands to

expand its services; notable acquisitions include Commander, Primus, Dodo and CallPlus.

MTU delivers its fixed line and mobile products through reseller agreements with TLS and

Optus. Both wholesale contracts are due for renewal in July 2016.

Merged group

The combination of Vocus Communications and M2 Group (VOC) creates a full-service,

vertically integrated ANZ telco provider. VOC offers full internet coverage across all Points

of Interconnect (POI) in Australia’s NBN and NZ’s UFB and owns 1,791km of metro fibre,

more than 3,647 on-net buildings in Australia, as well as 4,500km of NZ fibre.

Exhibit 1: The Vocus brand will operate in the Corporate & Government and Wholesale

segments, while MTU’s brands will operate in the Consumer & SMB segments. VOC combined trans-Tasman portfolio of brands

Source: Company data.

March 10, 2016 Vocus Communications Ltd. (VOC.AX)

Goldman Sachs Global Investment Research 7

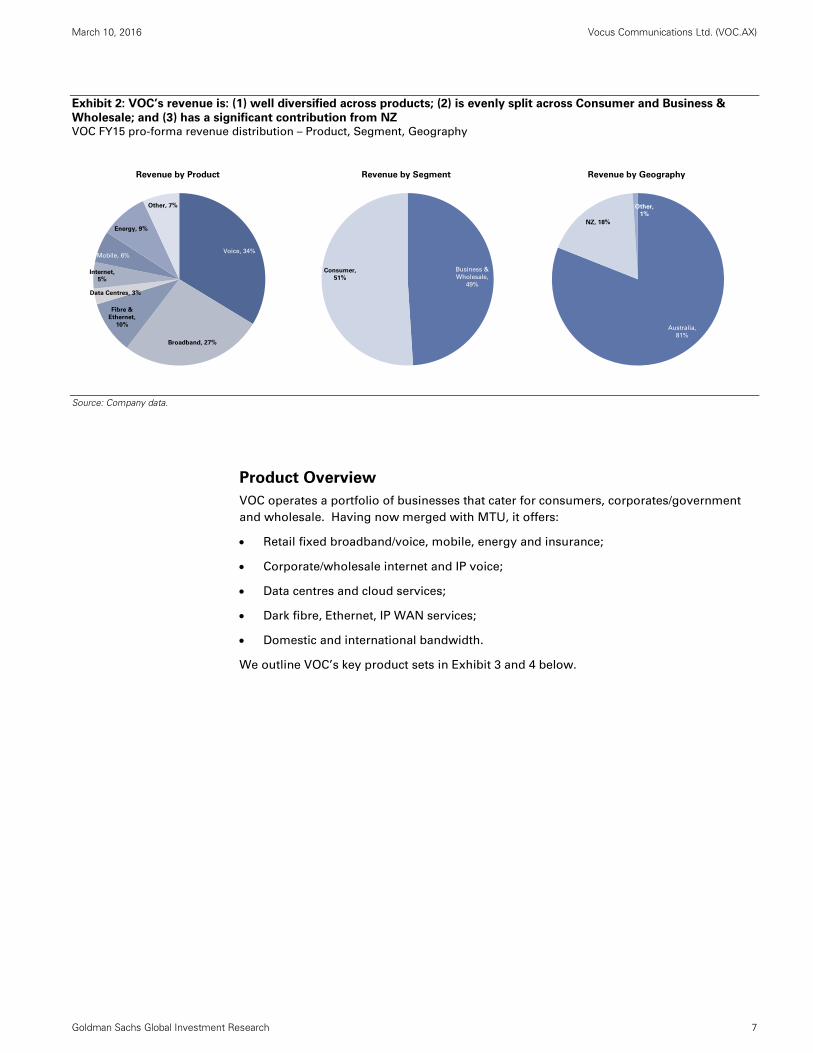

Exhibit 2: VOC’s revenue is: (1) well diversified across products; (2) is evenly split across Consumer and Business &

Wholesale; and (3) has a significant contribution from NZ VOC FY15 pro-forma revenue distribution – Product, Segment, Geography

Source: Company data.

Product Overview

VOC operates a portfolio of businesses that cater for consumers, corporates/government

and wholesale. Having now merged with MTU, it offers:

Retail fixed broadband/voice, mobile, energy and insurance;

Corporate/wholesale internet and IP voice;

Data centres and cloud services;

Dark fibre, Ethernet, IP WAN services;

Domestic and international bandwidth.

We outline VOC’s key product sets in Exhibit 3 and 4 below.

Voice, 34%

Fibre &

Ethernet,

10%

Internet,

5%

Mobile, 6%

Energy, 9%

Other, 7%

Data Centres, 3%

Broadband, 27%

Revenue by Product

Business &

Wholesale,

49%

Consumer,

51%

Revenue by Segment

Australia,

81%

NZ, 18%

Revenue by Geography

Other,

1%

March 10, 2016 Vocus Communications Ltd. (VOC.AX)

Goldman Sachs Global Investment Research 8

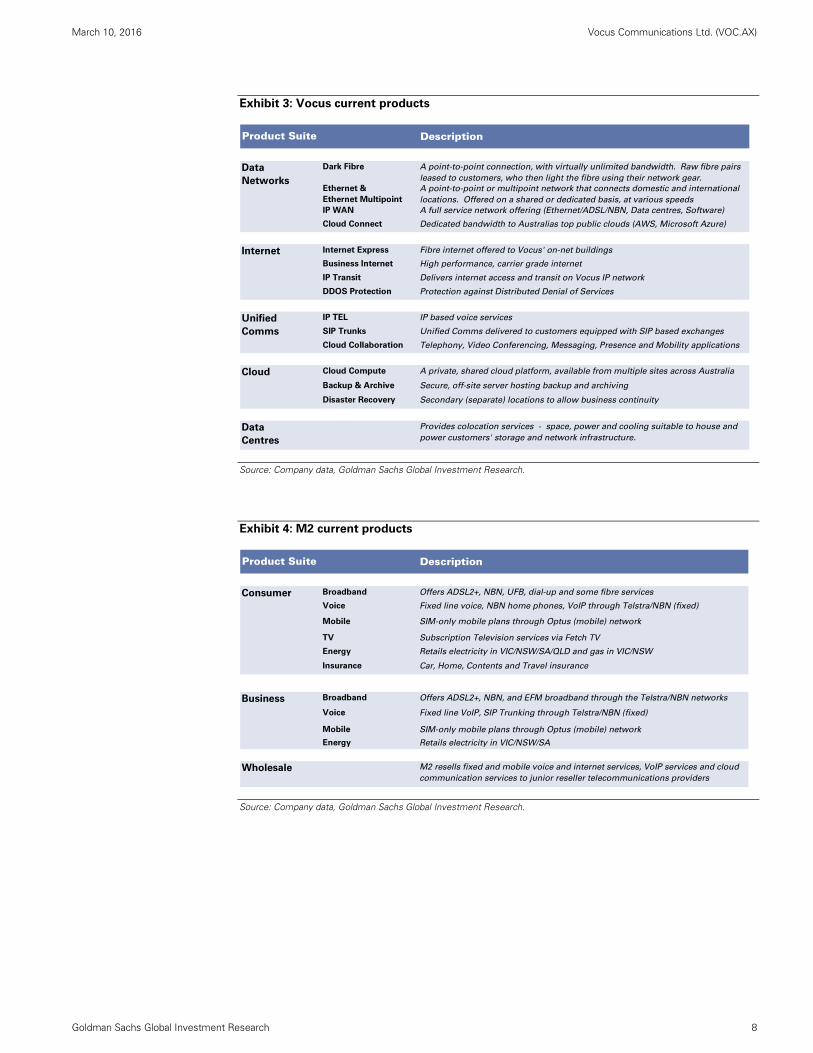

Exhibit 3: Vocus current products

Source: Company data, Goldman Sachs Global Investment Research.

Exhibit 4: M2 current products

Source: Company data, Goldman Sachs Global Investment Research.

Description

Dark Fibre A point-to-point connection, with virtually unlimited bandwidth. Raw fibre pairs

leased to customers, who then light the fibre using their network gear.

Ethernet &

Ethernet Multipoint

A point-to-point or multipoint network that connects domestic and international

locations. Offered on a shared or dedicated basis, at various speeds

IP WAN A full service network offering (Ethernet/ADSL/NBN, Data centres, Software)

Cloud Connect Dedicated bandwidth to Australias top public clouds (AWS, Microsoft Azure)

Internet Express Fibre internet offered to Vocus' on-net buildings

Business Internet High performance, carrier grade internet

IP Transit Delivers internet access and transit on Vocus IP network

DDOS Protection Protection against Distributed Denial of Services

IP TEL IP based voice services

SIP Trunks Unified Comms delivered to customers equipped with SIP based exchanges

Cloud Collaboration Telephony, Video Conferencing, Messaging, Presence and Mobility applications

Cloud Compute A private, shared cloud platform, available from multiple sites across Australia

Backup & Archive Secure, off-site server hosting backup and archiving

Disaster Recovery Secondary (separate) locations to allow business continuity

Data

Centres

Provides colocation services - space, power and cooling suitable to house and

power customers' storage and network infrastructure.

Data

Networks

Internet

Unified

Comms

Cloud

Product Suite

Description

Broadband Offers ADSL2+, NBN, UFB, dial-up and some fibre services

Voice Fixed line voice, NBN home phones, VoIP through Telstra/NBN (fixed)

Mobile SIM-only mobile plans through Optus (mobile) network

TV Subscription Television services via Fetch TV

Energy Retails electricity in VIC/NSW/SA/QLD and gas in VIC/NSW

Insurance Car, Home, Contents and Travel insurance

Broadband Offers ADSL2+, NBN, and EFM broadband through the Telstra/NBN networks

Voice Fixed line VoIP, SIP Trunking through Telstra/NBN (fixed)

Mobile SIM-only mobile plans through Optus (mobile) network

Energy Retails electricity in VIC/NSW/SA

Wholesale M2 resells fixed and mobile voice and internet services, VoIP services and cloud

communication services to junior reseller telecommunications providers

Product Suite

Business

Consumer

March 10, 2016

Vocus Com

munications Ltd. (VO

C.A

X)

Goldm

an Sachs Global Investm

ent Research

9

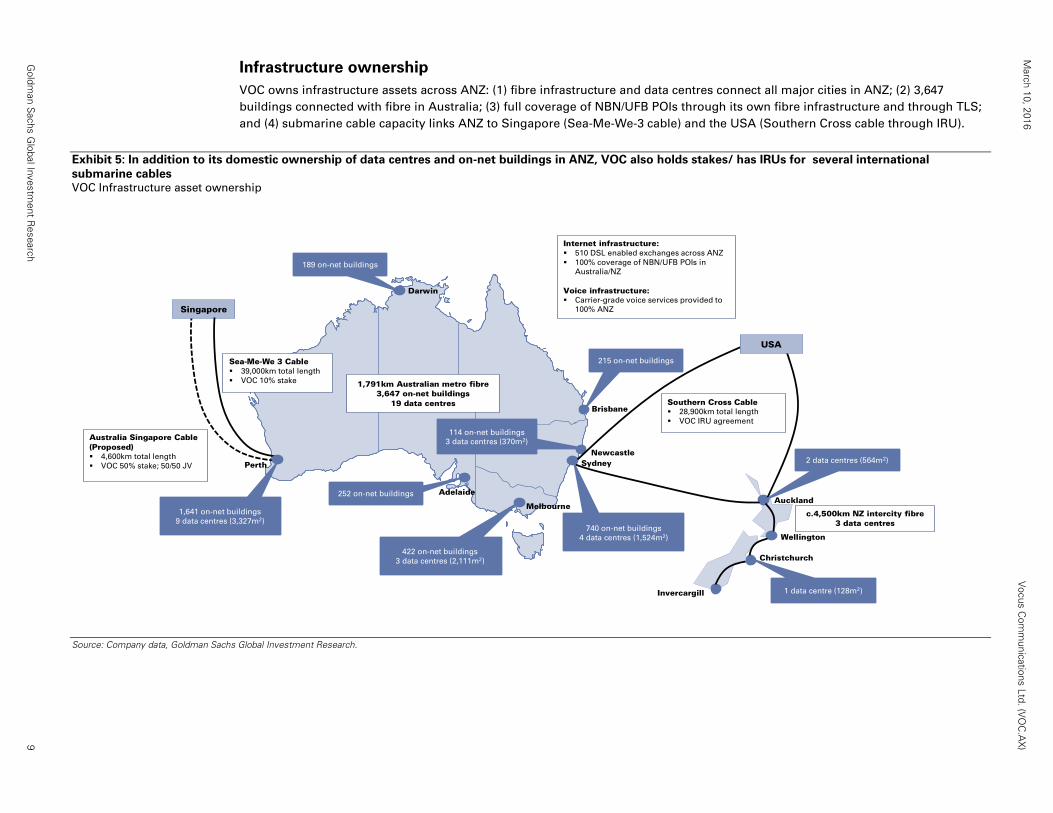

Infrastructure ownership

VOC owns infrastructure assets across ANZ: (1) fibre infrastructure and data centres connect all major cities in ANZ; (2) 3,647

buildings connected with fibre in Australia; (3) full coverage of NBN/UFB POIs through its own fibre infrastructure and through TLS;

and (4) submarine cable capacity links ANZ to Singapore (Sea-Me-We-3 cable) and the USA (Southern Cross cable through IRU).

Exhibit 5: In addition to its domestic ownership of data centres and on-net buildings in ANZ, VOC also holds stakes/ has IRUs for several international

submarine cables VOC Infrastructure asset ownership

Source: Company data, Goldman Sachs Global Investment Research.

Brisbane

NewcastleSydney

Melbourne

Adelaide

Darwin

Perth

Auckland

Wellington

Christchurch

Invercargill

USA

Singapore

c.4,500km NZ intercity fibre3 data centres

1,791km Australian metro fibre3,647 on-net buildings

19 data centres

189 on-net buildings

114 on-net buildings

3 data centres (370m2)

252 on-net buildings

2 data centres (564m2)

1 data centre (128m2)

Internet infrastructure: 510 DSL enabled exchanges across ANZ

100% coverage of NBN/UFB POIs in

Australia/NZ

Voice infrastructure: Carrier-grade voice services provided to

100% ANZ

Sea-Me-We 3 Cable 39,000km total length

VOC 10% stake

Australia Singapore Cable (Proposed) 4,600km total length

VOC 50% stake; 50/50 JV

Southern Cross Cable 28,900km total length

VOC IRU agreement

740 on-net buildings

4 data centres (1,524m2)

422 on-net buildings

3 data centres (2,111m2)

215 on-net buildings

1,641 on-net buildings

9 data centres (3,327m2)

March 10, 2016 Vocus Communications Ltd. (VOC.AX)

Goldman Sachs Global Investment Research 10

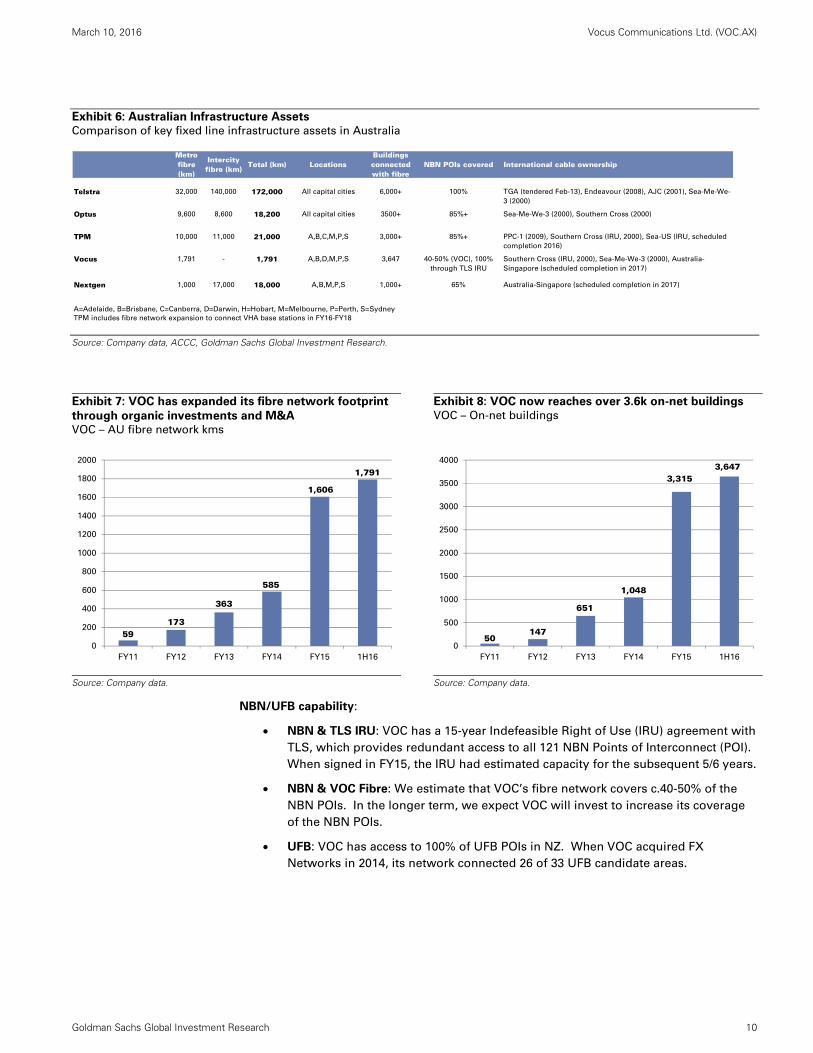

Exhibit 6: Australian Infrastructure Assets

Comparison of key fixed line infrastructure assets in Australia

Source: Company data, ACCC, Goldman Sachs Global Investment Research.

Exhibit 7: VOC has expanded its fibre network footprint

through organic investments and M&A VOC – AU fibre network kms

Exhibit 8: VOC now reaches over 3.6k on-net buildings

VOC – On-net buildings

Source: Company data.

Source: Company data.

NBN/UFB capability:

NBN & TLS IRU: VOC has a 15-year Indefeasible Right of Use (IRU) agreement with

TLS, which provides redundant access to all 121 NBN Points of Interconnect (POI).

When signed in FY15, the IRU had estimated capacity for the subsequent 5/6 years.

NBN & VOC Fibre: We estimate that VOC’s fibre network covers c.40-50% of the

NBN POIs. In the longer term, we expect VOC will invest to increase its coverage

of the NBN POIs.

UFB: VOC has access to 100% of UFB POIs in NZ. When VOC acquired FX

Networks in 2014, its network connected 26 of 33 UFB candidate areas.

Metro fibre (km)

Intercity fibre (km)

Total (km) LocationsBuildings connected with fibre

NBN POIs covered International cable ownership

Telstra 32,000 140,000 172,000 All capital cities 6,000+ 100% TGA (tendered Feb-13), Endeavour (2008), AJC (2001), Sea-Me-We-

3 (2000)

Optus 9,600 8,600 18,200 All capital cities 3500+ 85%+ Sea-Me-We-3 (2000), Southern Cross (2000)

TPM 10,000 11,000 21,000 A,B,C,M,P,S 3,000+ 85%+ PPC-1 (2009), Southern Cross (IRU, 2000), Sea-US (IRU, scheduled

completion 2016)

Vocus 1,791 - 1,791 A,B,D,M,P,S 3,647 40-50% (VOC), 100%

through TLS IRU

Southern Cross (IRU, 2000), Sea-Me-We-3 (2000), Australia-

Singapore (scheduled completion in 2017)

Nextgen 1,000 17,000 18,000 A,B,M,P,S 1,000+ 65% Australia-Singapore (scheduled completion in 2017)

A=Adelaide, B=Brisbane, C=Canberra, D=Darwin, H=Hobart, M=Melbourne, P=Perth, S=Sydney

TPM includes fibre network expansion to connect VHA base stations in FY16-FY18

59173

363

585

1,606

1,791

0

200

400

600

800

1000

1200

1400

1600

1800

2000

FY11 FY12 FY13 FY14 FY15 1H16

50147

651

1,048

3,3153,647

0

500

1000

1500

2000

2500

3000

3500

4000

FY11 FY12 FY13 FY14 FY15 1H16

March 10, 2016 Vocus Communications Ltd. (VOC.AX)

Goldman Sachs Global Investment Research 11

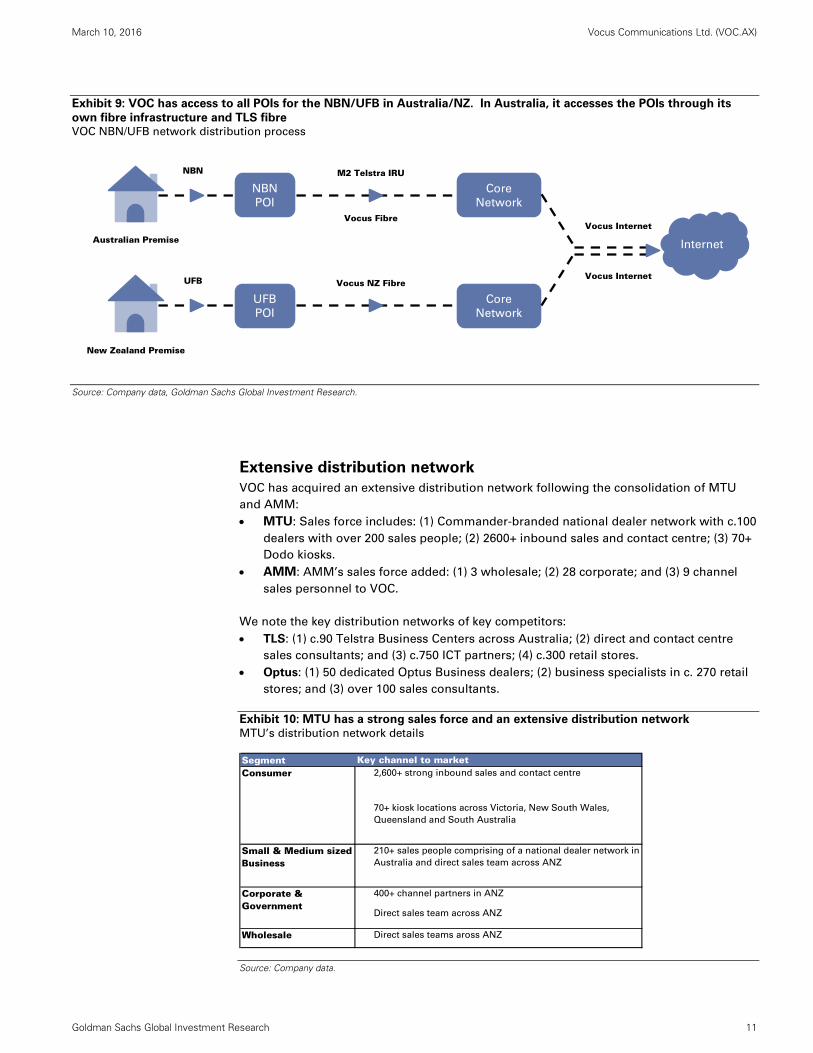

Exhibit 9: VOC has access to all POIs for the NBN/UFB in Australia/NZ. In Australia, it accesses the POIs through its

own fibre infrastructure and TLS fibre VOC NBN/UFB network distribution process

Source: Company data, Goldman Sachs Global Investment Research.

Extensive distribution network

VOC has acquired an extensive distribution network following the consolidation of MTU

and AMM:

MTU: Sales force includes: (1) Commander-branded national dealer network with c.100

dealers with over 200 sales people; (2) 2600+ inbound sales and contact centre; (3) 70+

Dodo kiosks.

AMM: AMM’s sales force added: (1) 3 wholesale; (2) 28 corporate; and (3) 9 channel

sales personnel to VOC.

We note the key distribution networks of key competitors:

TLS: (1) c.90 Telstra Business Centers across Australia; (2) direct and contact centre

sales consultants; and (3) c.750 ICT partners; (4) c.300 retail stores.

Optus: (1) 50 dedicated Optus Business dealers; (2) business specialists in c. 270 retail

stores; and (3) over 100 sales consultants.

Exhibit 10: MTU has a strong sales force and an extensive distribution network

MTU’s distribution network details

Source: Company data.

Internet

NBN

POI

UFB

POI

Core

Network

Core

Network

Australian Premise

New Zealand Premise

Vocus Internet

Vocus Internet

M2 Telstra IRU

Vocus Fibre

Vocus NZ Fibre

NBN

UFB

SegmentConsumer 2,600+ strong inbound sales and contact centre

70+ kiosk locations across Victoria, New South Wales,

Queensland and South Australia

Small & Medium sized Business

210+ sales people comprising of a national dealer network in

Australia and direct sales team across ANZ

400+ channel partners in ANZ

Direct sales team across ANZ

Wholesale Direct sales teams aross ANZ

Corporate & Government

Key channel to market

March 10, 2016 Vocus Communications Ltd. (VOC.AX)

Goldman Sachs Global Investment Research 12

Outlook and key stock drivers

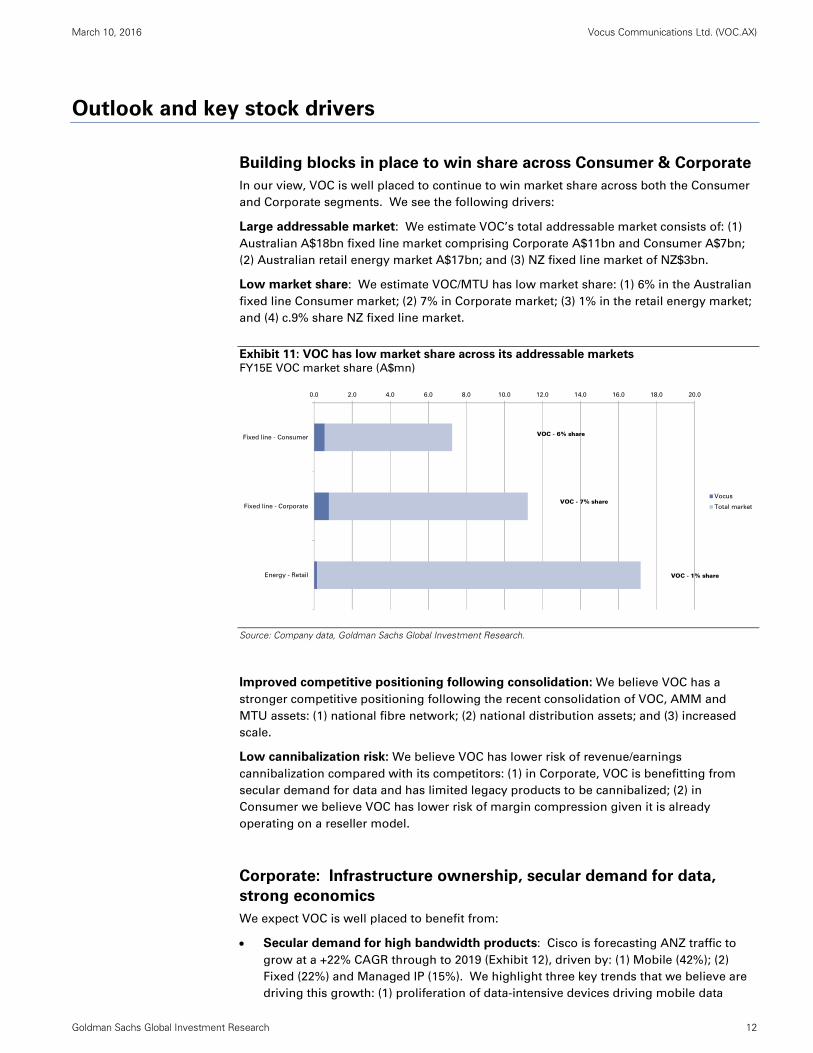

Building blocks in place to win share across Consumer & Corporate

In our view, VOC is well placed to continue to win market share across both the Consumer

and Corporate segments. We see the following drivers:

Large addressable market: We estimate VOC’s total addressable market consists of: (1)

Australian A$18bn fixed line market comprising Corporate A$11bn and Consumer A$7bn;

(2) Australian retail energy market A$17bn; and (3) NZ fixed line market of NZ$3bn.

Low market share: We estimate VOC/MTU has low market share: (1) 6% in the Australian

fixed line Consumer market; (2) 7% in Corporate market; (3) 1% in the retail energy market;

and (4) c.9% share NZ fixed line market.

Exhibit 11: VOC has low market share across its addressable markets FY15E VOC market share (A$mn)

Source: Company data, Goldman Sachs Global Investment Research.

Improved competitive positioning following consolidation: We believe VOC has a

stronger competitive positioning following the recent consolidation of VOC, AMM and

MTU assets: (1) national fibre network; (2) national distribution assets; and (3) increased

scale.

Low cannibalization risk: We believe VOC has lower risk of revenue/earnings

cannibalization compared with its competitors: (1) in Corporate, VOC is benefitting from

secular demand for data and has limited legacy products to be cannibalized; (2) in

Consumer we believe VOC has lower risk of margin compression given it is already

operating on a reseller model.

Corporate: Infrastructure ownership, secular demand for data,

strong economics

We expect VOC is well placed to benefit from:

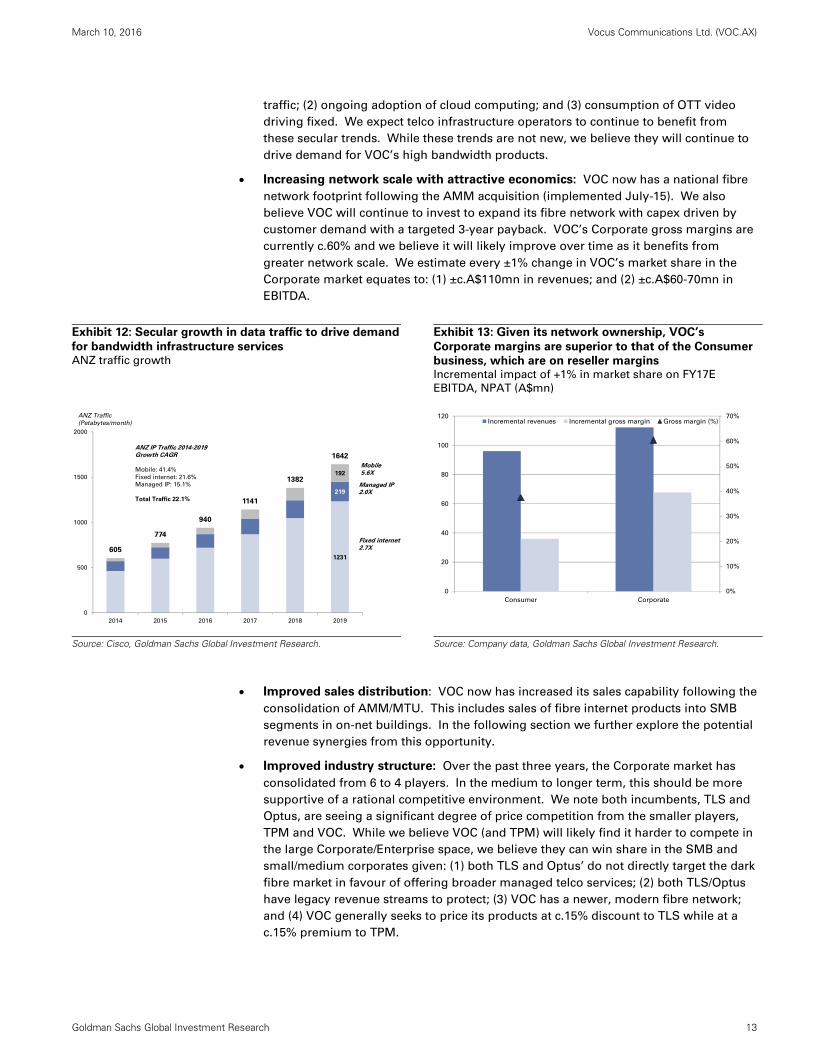

Secular demand for high bandwidth products: Cisco is forecasting ANZ traffic to

grow at a +22% CAGR through to 2019 (Exhibit 12), driven by: (1) Mobile (42%); (2)

Fixed (22%) and Managed IP (15%). We highlight three key trends that we believe are

driving this growth: (1) proliferation of data-intensive devices driving mobile data

0.0 2.0 4.0 6.0 8.0 10.0 12.0 14.0 16.0 18.0 20.0

Fixed line - Consumer

Fixed line - Corporate

Energy - Retail

Vocus

Total market

VOC - 6% share

VOC - 7% share

VOC - 1% share

March 10, 2016 Vocus Communications Ltd. (VOC.AX)

Goldman Sachs Global Investment Research 13

traffic; (2) ongoing adoption of cloud computing; and (3) consumption of OTT video

driving fixed. We expect telco infrastructure operators to continue to benefit from

these secular trends. While these trends are not new, we believe they will continue to

drive demand for VOC’s high bandwidth products.

Increasing network scale with attractive economics: VOC now has a national fibre

network footprint following the AMM acquisition (implemented July-15). We also

believe VOC will continue to invest to expand its fibre network with capex driven by

customer demand with a targeted 3-year payback. VOC’s Corporate gross margins are

currently c.60% and we believe it will likely improve over time as it benefits from

greater network scale. We estimate every ±1% change in VOC’s market share in the

Corporate market equates to: (1) ±c.A$110mn in revenues; and (2) ±c.A$60-70mn in

EBITDA.

Exhibit 12: Secular growth in data traffic to drive demand

for bandwidth infrastructure services ANZ traffic growth

Exhibit 13: Given its network ownership, VOC’s

Corporate margins are superior to that of the Consumer

business, which are on reseller margins Incremental impact of +1% in market share on FY17E

EBITDA, NPAT (A$mn)

Source: Cisco, Goldman Sachs Global Investment Research.

Source: Company data, Goldman Sachs Global Investment Research.

Improved sales distribution: VOC now has increased its sales capability following the

consolidation of AMM/MTU. This includes sales of fibre internet products into SMB

segments in on-net buildings. In the following section we further explore the potential

revenue synergies from this opportunity.

Improved industry structure: Over the past three years, the Corporate market has

consolidated from 6 to 4 players. In the medium to longer term, this should be more

supportive of a rational competitive environment. We note both incumbents, TLS and

Optus, are seeing a significant degree of price competition from the smaller players,

TPM and VOC. While we believe VOC (and TPM) will likely find it harder to compete in

the large Corporate/Enterprise space, we believe they can win share in the SMB and

small/medium corporates given: (1) both TLS and Optus’ do not directly target the dark

fibre market in favour of offering broader managed telco services; (2) both TLS/Optus

have legacy revenue streams to protect; (3) VOC has a newer, modern fibre network;

and (4) VOC generally seeks to price its products at c.15% discount to TLS while at a

c.15% premium to TPM.

1231

219

192

605

774

940

1141

1382

1642

0

500

1000

1500

2000

2014 2015 2016 2017 2018 2019

ANZ Traffic

(Petabytes/month)

Mobile5.6X

Fixed internet 2.7X

Managed IP 2.0X

ANZ IP Traffic 2014-2019 Growth CAGR

Mobile: 41.4%

Fixed internet: 21.6%

Managed IP: 15.1%

Total Traffic 22.1%

0%

10%

20%

30%

40%

50%

60%

70%

0

20

40

60

80

100

120

Consumer Corporate

Incremental revenues Incremental gross margin Gross margin (%)

March 10, 2016 Vocus Communications Ltd. (VOC.AX)

Goldman Sachs Global Investment Research 14

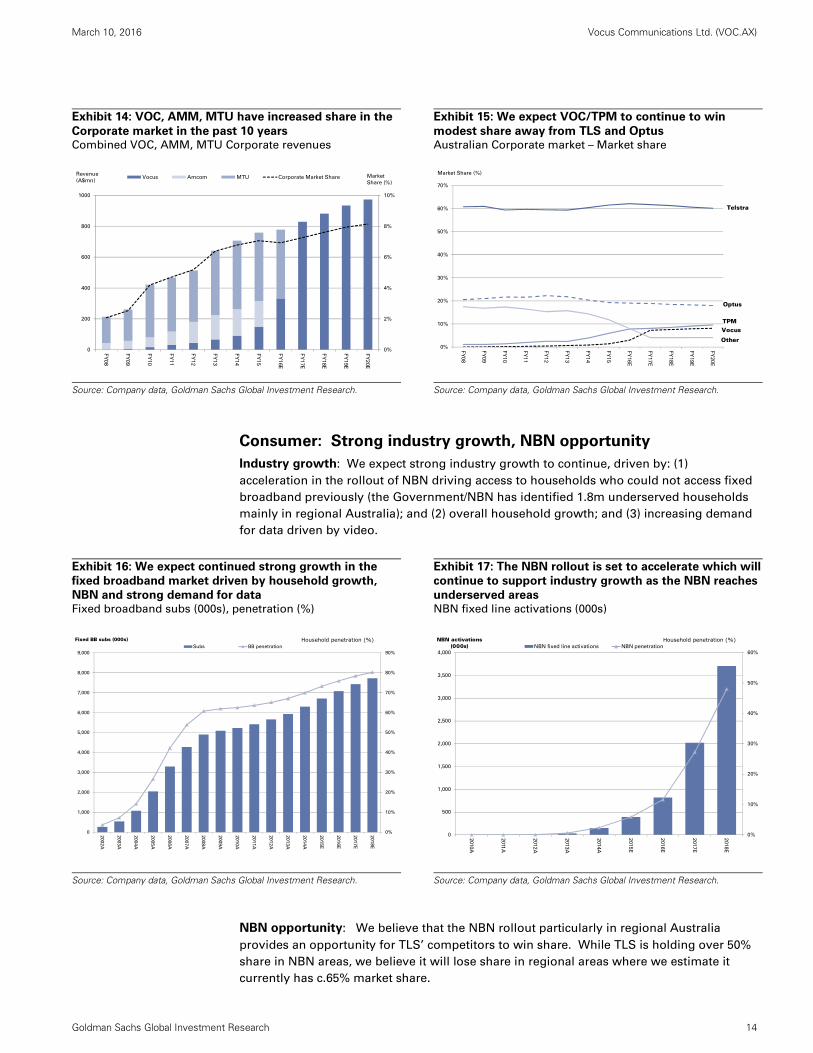

Exhibit 14: VOC, AMM, MTU have increased share in the

Corporate market in the past 10 years Combined VOC, AMM, MTU Corporate revenues

Exhibit 15: We expect VOC/TPM to continue to win

modest share away from TLS and Optus Australian Corporate market – Market share

Source: Company data, Goldman Sachs Global Investment Research.

Source: Company data, Goldman Sachs Global Investment Research.

Consumer: Strong industry growth, NBN opportunity

Industry growth: We expect strong industry growth to continue, driven by: (1)

acceleration in the rollout of NBN driving access to households who could not access fixed

broadband previously (the Government/NBN has identified 1.8m underserved households

mainly in regional Australia); and (2) overall household growth; and (3) increasing demand

for data driven by video.

Exhibit 16: We expect continued strong growth in the

fixed broadband market driven by household growth,

NBN and strong demand for data Fixed broadband subs (000s), penetration (%)

Exhibit 17: The NBN rollout is set to accelerate which will

continue to support industry growth as the NBN reaches

underserved areas NBN fixed line activations (000s)

Source: Company data, Goldman Sachs Global Investment Research.

Source: Company data, Goldman Sachs Global Investment Research.

NBN opportunity: We believe that the NBN rollout particularly in regional Australia

provides an opportunity for TLS’ competitors to win share. While TLS is holding over 50%

share in NBN areas, we believe it will lose share in regional areas where we estimate it

currently has c.65% market share.

0%

2%

4%

6%

8%

10%

0

200

400

600

800

1000

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16E

FY

17E

FY

18E

FY

19E

FY

20E

Vocus Amcom MTU Corporate Market ShareRevenue

(A$mn)Market

Share (%)

0%

10%

20%

30%

40%

50%

60%

70%

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

E

FY

17

E

FY

18

E

FY

19

E

FY

20

E

Market Share (%)

Telstra

Optus

Other

VocusTPM

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

200

2A

200

3A

200

4A

200

5A

200

6A

200

7A

200

8A

200

9A

201

0A

201

1A

201

2A

201

3A

201

4A

201

5E

201

6E

201

7E

201

8E

Fixed BB subs (000s)Subs BB penetration

Household penetration (%)

0%

10%

20%

30%

40%

50%

60%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2010A

2011

A

2012

A

2013

A

2014A

2015

E

2016

E

2017

E

2018

E

NBN activations (000s) NBN fixed line activations NBN penetration

Household penetration (%)

March 10, 2016 Vocus Communications Ltd. (VOC.AX)

Goldman Sachs Global Investment Research 15

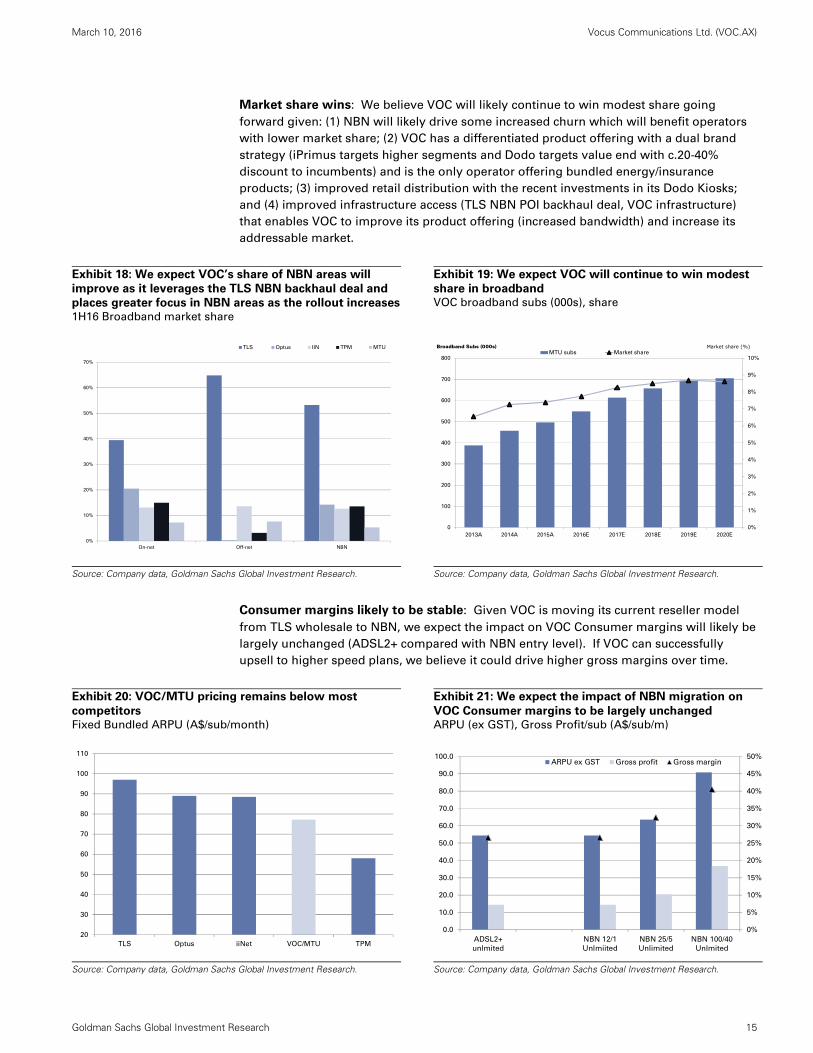

Market share wins: We believe VOC will likely continue to win modest share going

forward given: (1) NBN will likely drive some increased churn which will benefit operators

with lower market share; (2) VOC has a differentiated product offering with a dual brand

strategy (iPrimus targets higher segments and Dodo targets value end with c.20-40%

discount to incumbents) and is the only operator offering bundled energy/insurance

products; (3) improved retail distribution with the recent investments in its Dodo Kiosks;

and (4) improved infrastructure access (TLS NBN POI backhaul deal, VOC infrastructure)

that enables VOC to improve its product offering (increased bandwidth) and increase its

addressable market.

Exhibit 18: We expect VOC’s share of NBN areas will

improve as it leverages the TLS NBN backhaul deal and

places greater focus in NBN areas as the rollout increases 1H16 Broadband market share

Exhibit 19: We expect VOC will continue to win modest

share in broadband VOC broadband subs (000s), share

Source: Company data, Goldman Sachs Global Investment Research.

Source: Company data, Goldman Sachs Global Investment Research.

Consumer margins likely to be stable: Given VOC is moving its current reseller model

from TLS wholesale to NBN, we expect the impact on VOC Consumer margins will likely be

largely unchanged (ADSL2+ compared with NBN entry level). If VOC can successfully

upsell to higher speed plans, we believe it could drive higher gross margins over time.

Exhibit 20: VOC/MTU pricing remains below most

competitors Fixed Bundled ARPU (A$/sub/month)

Exhibit 21: We expect the impact of NBN migration on

VOC Consumer margins to be largely unchanged ARPU (ex GST), Gross Profit/sub (A$/sub/m)

Source: Company data, Goldman Sachs Global Investment Research.

Source: Company data, Goldman Sachs Global Investment Research.

0%

10%

20%

30%

40%

50%

60%

70%

On-net Off-net NBN

TLS Optus IIN TPM MTU

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0

100

200

300

400

500

600

700

800

2013A 2014A 2015A 2016E 2017E 2018E 2019E 2020E

Broadband Subs (000s)MTU subs Market share

Market share (%)

20

30

40

50

60

70

80

90

100

110

TLS Optus iiNet VOC/MTU TPM

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

ADSL2+

unlmited

NBN 12/1

Unlmiited

NBN 25/5

Unlimited

NBN 100/40

Unlmited

ARPU ex GST Gross profit Gross margin

March 10, 2016 Vocus Communications Ltd. (VOC.AX)

Goldman Sachs Global Investment Research 16

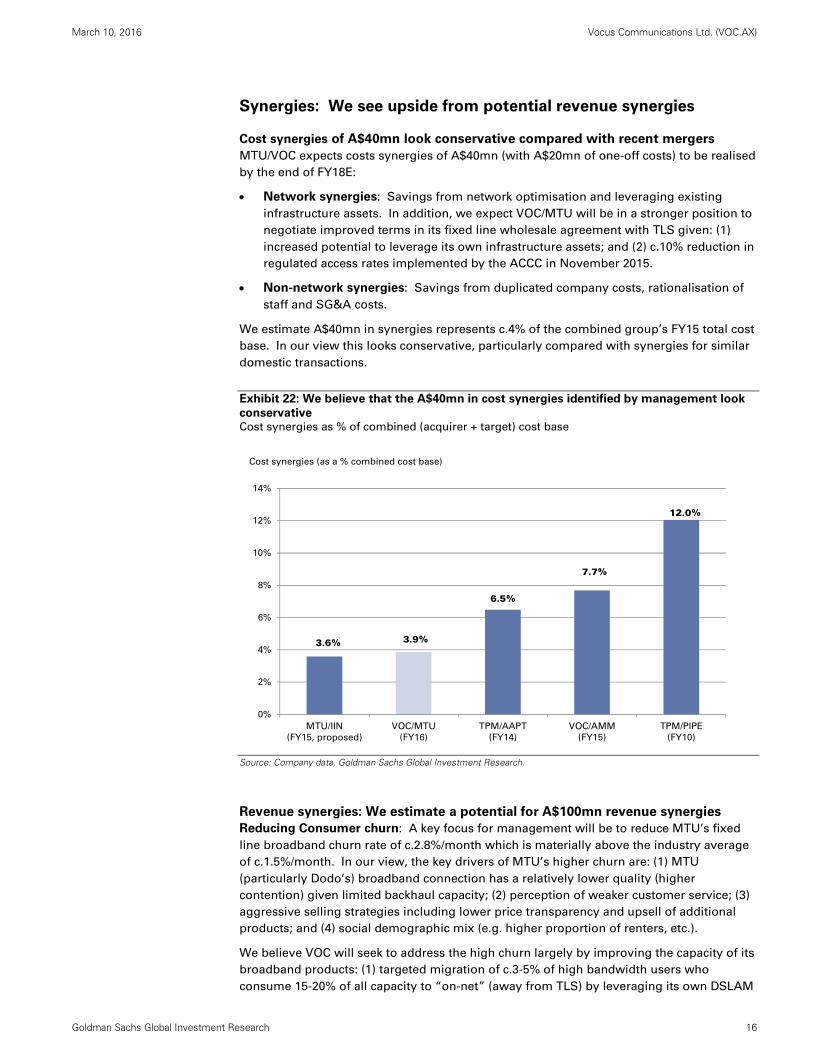

Synergies: We see upside from potential revenue synergies

Cost synergies of A$40mn look conservative compared with recent mergers

MTU/VOC expects costs synergies of A$40mn (with A$20mn of one-off costs) to be realised

by the end of FY18E:

Network synergies: Savings from network optimisation and leveraging existing

infrastructure assets. In addition, we expect VOC/MTU will be in a stronger position to

negotiate improved terms in its fixed line wholesale agreement with TLS given: (1)

increased potential to leverage its own infrastructure assets; and (2) c.10% reduction in

regulated access rates implemented by the ACCC in November 2015.

Non-network synergies: Savings from duplicated company costs, rationalisation of

staff and SG&A costs.

We estimate A$40mn in synergies represents c.4% of the combined group’s FY15 total cost

base. In our view this looks conservative, particularly compared with synergies for similar

domestic transactions.

Exhibit 22: We believe that the A$40mn in cost synergies identified by management look

conservative Cost synergies as % of combined (acquirer + target) cost base

Source: Company data, Goldman Sachs Global Investment Research.

Revenue synergies: We estimate a potential for A$100mn revenue synergies

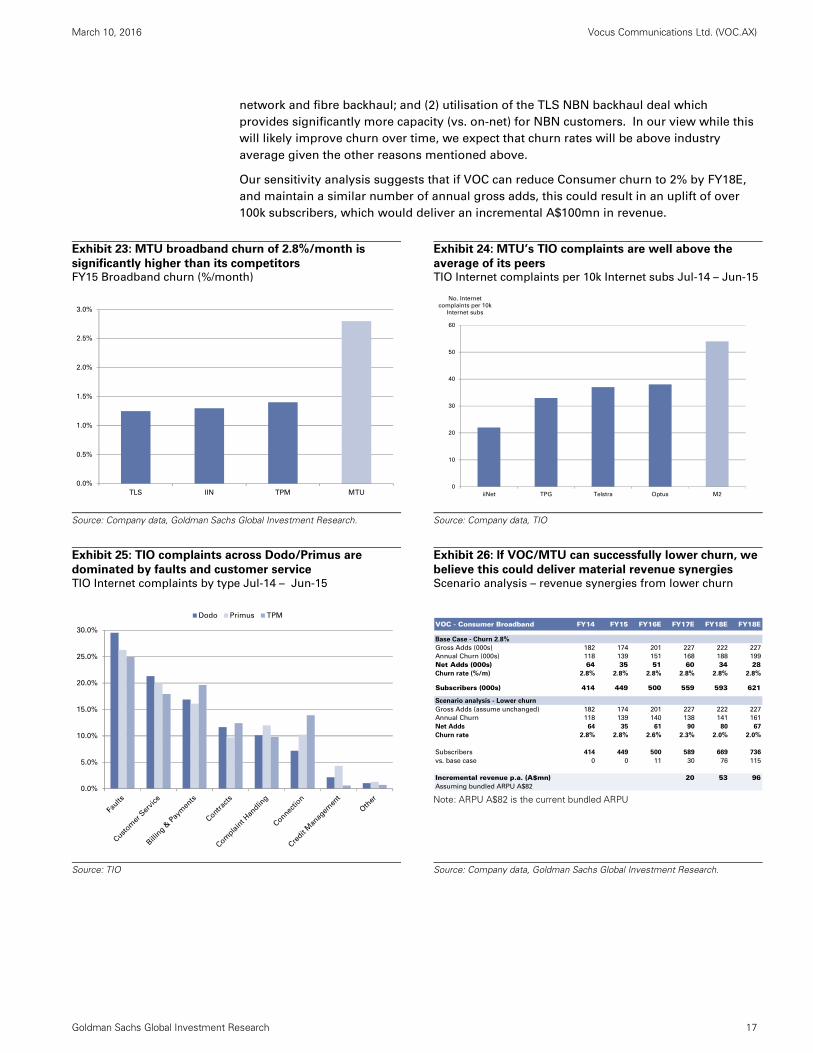

Reducing Consumer churn: A key focus for management will be to reduce MTU’s fixed

line broadband churn rate of c.2.8%/month which is materially above the industry average

of c.1.5%/month. In our view, the key drivers of MTU’s higher churn are: (1) MTU

(particularly Dodo’s) broadband connection has a relatively lower quality (higher

contention) given limited backhaul capacity; (2) perception of weaker customer service; (3)

aggressive selling strategies including lower price transparency and upsell of additional

products; and (4) social demographic mix (e.g. higher proportion of renters, etc.).

We believe VOC will seek to address the high churn largely by improving the capacity of its

broadband products: (1) targeted migration of c.3-5% of high bandwidth users who

consume 15-20% of all capacity to “on-net” (away from TLS) by leveraging its own DSLAM

3.6% 3.9%

6.5%

7.7%

12.0%

0%

2%

4%

6%

8%

10%

12%

14%

MTU/IIN

(FY15, proposed)

VOC/MTU

(FY16)

TPM/AAPT

(FY14)

VOC/AMM

(FY15)

TPM/PIPE

(FY10)

Cost synergies (as a % combined cost base)

March 10, 2016 Vocus Communications Ltd. (VOC.AX)

Goldman Sachs Global Investment Research 17

network and fibre backhaul; and (2) utilisation of the TLS NBN backhaul deal which

provides significantly more capacity (vs. on-net) for NBN customers. In our view while this

will likely improve churn over time, we expect that churn rates will be above industry

average given the other reasons mentioned above.

Our sensitivity analysis suggests that if VOC can reduce Consumer churn to 2% by FY18E,

and maintain a similar number of annual gross adds, this could result in an uplift of over

100k subscribers, which would deliver an incremental A$100mn in revenue.

Exhibit 23: MTU broadband churn of 2.8%/month is

significantly higher than its competitors FY15 Broadband churn (%/month)

Exhibit 24: MTU’s TIO complaints are well above the

average of its peers TIO Internet complaints per 10k Internet subs Jul-14 – Jun-15

Source: Company data, Goldman Sachs Global Investment Research.

Source: Company data, TIO

Exhibit 25: TIO complaints across Dodo/Primus are

dominated by faults and customer service TIO Internet complaints by type Jul-14 – Jun-15

Exhibit 26: If VOC/MTU can successfully lower churn, we

believe this could deliver material revenue synergies Scenario analysis – revenue synergies from lower churn

Note: ARPU A$82 is the current bundled ARPU

Source: TIO

Source: Company data, Goldman Sachs Global Investment Research.

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

TLS IIN TPM MTU0

10

20

30

40

50

60

iiNet TPG Telstra Optus M2

No. Internet

complaints per 10k

Internet subs

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

Dodo Primus TPM

VOC - Consumer Broadband FY14 FY15 FY16E FY17E FY18E FY18E

Base Case - Churn 2.8%

Gross Adds (000s) 182 174 201 227 222 227

Annual Churn (000s) 118 139 151 168 188 199

Net Adds (000s) 64 35 51 60 34 28Churn rate (%/m) 2.8% 2.8% 2.8% 2.8% 2.8% 2.8%

Subscribers (000s) 414 449 500 559 593 621

Scenario analysis - Lower churn

Gross Adds (assume unchanged) 182 174 201 227 222 227

Annual Churn 118 139 140 138 141 161

Net Adds 64 35 61 90 80 67

Churn rate 2.8% 2.8% 2.6% 2.3% 2.0% 2.0%

Subscribers 414 449 500 589 669 736

vs. base case 0 0 11 30 76 115

Incremental revenue p.a. (A$mn) 20 53 96Assuming bundled ARPU A$82

March 10, 2016 Vocus Communications Ltd. (VOC.AX)

Goldman Sachs Global Investment Research 18

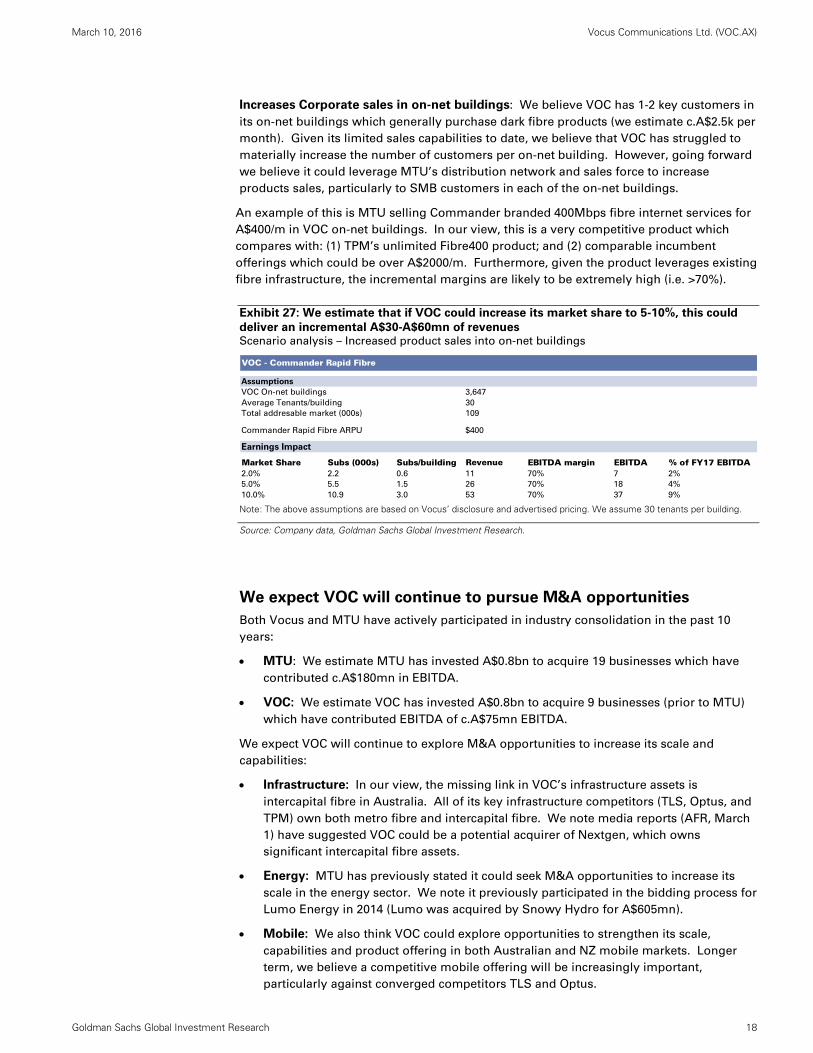

Increases Corporate sales in on-net buildings: We believe VOC has 1-2 key customers in

its on-net buildings which generally purchase dark fibre products (we estimate c.A$2.5k per

month). Given its limited sales capabilities to date, we believe that VOC has struggled to

materially increase the number of customers per on-net building. However, going forward

we believe it could leverage MTU’s distribution network and sales force to increase

products sales, particularly to SMB customers in each of the on-net buildings.

An example of this is MTU selling Commander branded 400Mbps fibre internet services for

A$400/m in VOC on-net buildings. In our view, this is a very competitive product which

compares with: (1) TPM’s unlimited Fibre400 product; and (2) comparable incumbent

offerings which could be over A$2000/m. Furthermore, given the product leverages existing

fibre infrastructure, the incremental margins are likely to be extremely high (i.e. >70%).

Exhibit 27: We estimate that if VOC could increase its market share to 5-10%, this could

deliver an incremental A$30-A$60mn of revenues Scenario analysis – Increased product sales into on-net buildings

Note: The above assumptions are based on Vocus’ disclosure and advertised pricing. We assume 30 tenants per building.

Source: Company data, Goldman Sachs Global Investment Research.

We expect VOC will continue to pursue M&A opportunities

Both Vocus and MTU have actively participated in industry consolidation in the past 10

years:

MTU: We estimate MTU has invested A$0.8bn to acquire 19 businesses which have

contributed c.A$180mn in EBITDA.

VOC: We estimate VOC has invested A$0.8bn to acquire 9 businesses (prior to MTU)

which have contributed EBITDA of c.A$75mn EBITDA.

We expect VOC will continue to explore M&A opportunities to increase its scale and

capabilities:

Infrastructure: In our view, the missing link in VOC’s infrastructure assets is

intercapital fibre in Australia. All of its key infrastructure competitors (TLS, Optus, and

TPM) own both metro fibre and intercapital fibre. We note media reports (AFR, March

1) have suggested VOC could be a potential acquirer of Nextgen, which owns

significant intercapital fibre assets.

Energy: MTU has previously stated it could seek M&A opportunities to increase its

scale in the energy sector. We note it previously participated in the bidding process for

Lumo Energy in 2014 (Lumo was acquired by Snowy Hydro for A$605mn).

Mobile: We also think VOC could explore opportunities to strengthen its scale,

capabilities and product offering in both Australian and NZ mobile markets. Longer

term, we believe a competitive mobile offering will be increasingly important,

particularly against converged competitors TLS and Optus.

VOC - Commander Rapid Fibre

Assumptions

VOC On-net buildings 3,647

Average Tenants/building 30

Total addresable market (000s) 109

Commander Rapid Fibre ARPU $400

Earnings Impact

Market Share Subs (000s) Subs/building Revenue EBITDA margin EBITDA % of FY17 EBITDA2.0% 2.2 0.6 11 70% 7 2%

5.0% 5.5 1.5 26 70% 18 4%

10.0% 10.9 3.0 53 70% 37 9%

March 10, 2016 Vocus Communications Ltd. (VOC.AX)

Goldman Sachs Global Investment Research 19

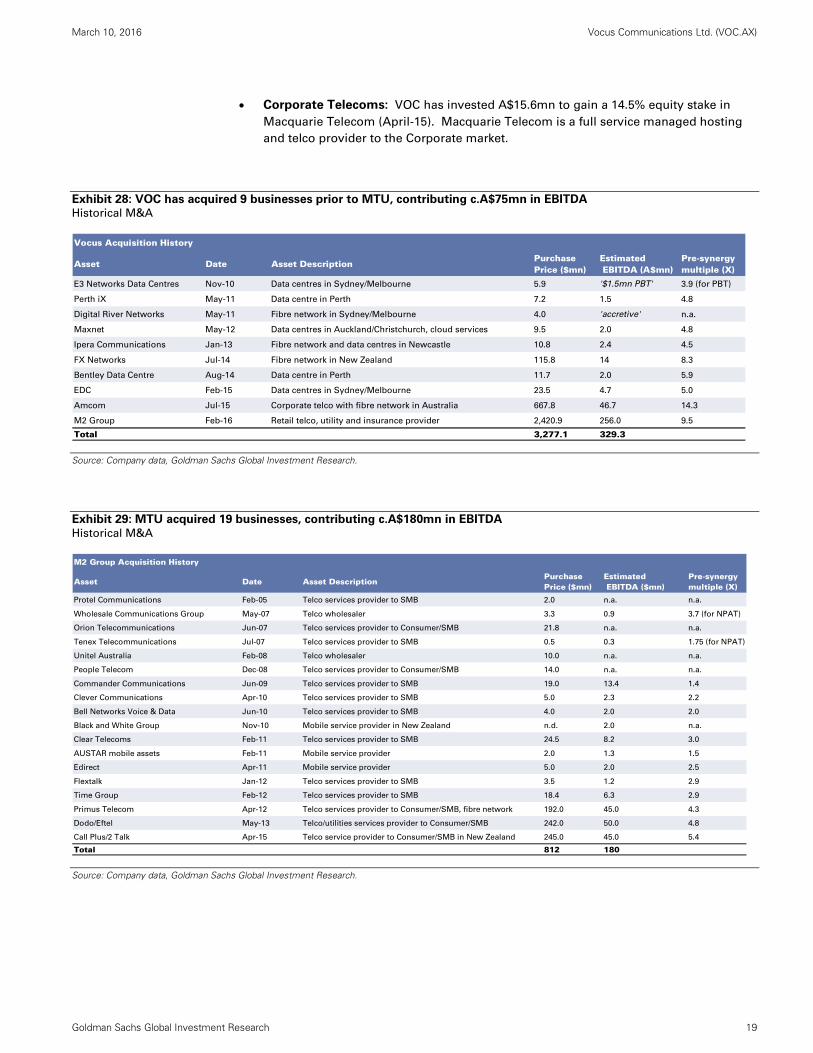

Corporate Telecoms: VOC has invested A$15.6mn to gain a 14.5% equity stake in

Macquarie Telecom (April-15). Macquarie Telecom is a full service managed hosting

and telco provider to the Corporate market.

Exhibit 28: VOC has acquired 9 businesses prior to MTU, contributing c.A$75mn in EBITDA Historical M&A

Source: Company data, Goldman Sachs Global Investment Research.

Exhibit 29: MTU acquired 19 businesses, contributing c.A$180mn in EBITDA

Historical M&A

Source: Company data, Goldman Sachs Global Investment Research.

Vocus Acquisition History

Asset Date Asset DescriptionPurchasePrice ($mn)

Estimated EBITDA (A$mn)

Pre-synergymultiple (X)

E3 Networks Data Centres Nov-10 Data centres in Sydney/Melbourne 5.9 '$1.5mn PBT' 3.9 (for PBT)

Perth iX May-11 Data centre in Perth 7.2 1.5 4.8

Digital River Networks May-11 Fibre network in Sydney/Melbourne 4.0 'accretive' n.a.

Maxnet May-12 Data centres in Auckland/Christchurch, cloud services 9.5 2.0 4.8

Ipera Communications Jan-13 Fibre network and data centres in Newcastle 10.8 2.4 4.5

FX Networks Jul-14 Fibre network in New Zealand 115.8 14 8.3

Bentley Data Centre Aug-14 Data centre in Perth 11.7 2.0 5.9

EDC Feb-15 Data centres in Sydney/Melbourne 23.5 4.7 5.0

Amcom Jul-15 Corporate telco with fibre network in Australia 667.8 46.7 14.3

M2 Group Feb-16 Retail telco, utility and insurance provider 2,420.9 256.0 9.5

Total 3,277.1 329.3

M2 Group Acquisition History

Asset Date Asset DescriptionPurchasePrice ($mn)

Estimated EBITDA ($mn)

Pre-synergymultiple (X)

Protel Communications Feb-05 Telco services provider to SMB 2.0 n.a. n.a.

Wholesale Communications Group May-07 Telco wholesaler 3.3 0.9 3.7 (for NPAT)

Orion Telecommunications Jun-07 Telco services provider to Consumer/SMB 21.8 n.a. n.a.

Tenex Telecommunications Jul-07 Telco services provider to SMB 0.5 0.3 1.75 (for NPAT)

Unitel Australia Feb-08 Telco wholesaler 10.0 n.a. n.a.

People Telecom Dec-08 Telco services provider to Consumer/SMB 14.0 n.a. n.a.

Commander Communications Jun-09 Telco services provider to SMB 19.0 13.4 1.4

Clever Communications Apr-10 Telco services provider to SMB 5.0 2.3 2.2

Bell Networks Voice & Data Jun-10 Telco services provider to SMB 4.0 2.0 2.0

Black and White Group Nov-10 Mobile service provider in New Zealand n.d. 2.0 n.a.

Clear Telecoms Feb-11 Telco services provider to SMB 24.5 8.2 3.0

AUSTAR mobile assets Feb-11 Mobile service provider 2.0 1.3 1.5

Edirect Apr-11 Mobile service provider 5.0 2.0 2.5

Flextalk Jan-12 Telco services provider to SMB 3.5 1.2 2.9

Time Group Feb-12 Telco services provider to SMB 18.4 6.3 2.9

Primus Telecom Apr-12 Telco services provider to Consumer/SMB, fibre network 192.0 45.0 4.3

Dodo/Eftel May-13 Telco/utilities services provider to Consumer/SMB 242.0 50.0 4.8

Call Plus/2 Talk Apr-15 Telco service provider to Consumer/SMB in New Zealand 245.0 45.0 5.4

Total 812 180

March 10, 2016 Vocus Communications Ltd. (VOC.AX)

Goldman Sachs Global Investment Research 20

Industry overview

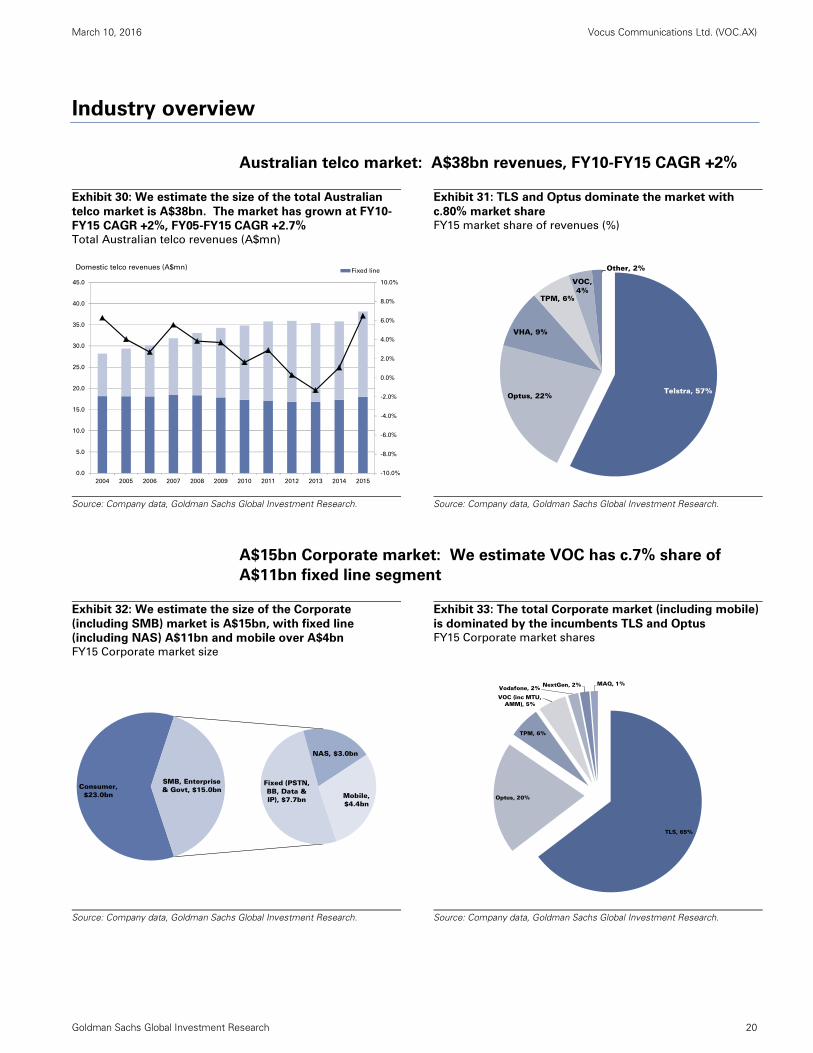

Australian telco market: A$38bn revenues, FY10-FY15 CAGR +2%

Exhibit 30: We estimate the size of the total Australian

telco market is A$38bn. The market has grown at FY10-

FY15 CAGR +2%, FY05-FY15 CAGR +2.7% Total Australian telco revenues (A$mn)

Exhibit 31: TLS and Optus dominate the market with

c.80% market share FY15 market share of revenues (%)

Source: Company data, Goldman Sachs Global Investment Research.

Source: Company data, Goldman Sachs Global Investment Research.

A$15bn Corporate market: We estimate VOC has c.7% share of

A$11bn fixed line segment

Exhibit 32: We estimate the size of the Corporate

(including SMB) market is A$15bn, with fixed line

(including NAS) A$11bn and mobile over A$4bn FY15 Corporate market size

Exhibit 33: The total Corporate market (including mobile)

is dominated by the incumbents TLS and Optus FY15 Corporate market shares

Source: Company data, Goldman Sachs Global Investment Research.

Source: Company data, Goldman Sachs Global Investment Research.

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Fixed lineDomestic telco revenues (A$mn)

Telstra, 57%Optus, 22%

VHA, 9%

TPM, 6%

VOC, 4%

Other, 2%

Consumer, $23.0bn

Fixed (PSTN, BB, Data & IP), $7.7bn

NAS, $3.0bn

Mobile, $4.4bn

SMB, Enterprise & Govt, $15.0bn

TLS, 65%

Optus, 20%

TPM, 6%

VOC (inc MTU, AMM), 5%

Vodafone, 2% NextGen, 2% MAQ, 1%

March 10, 2016 Vocus Communications Ltd. (VOC.AX)

Goldman Sachs Global Investment Research 21

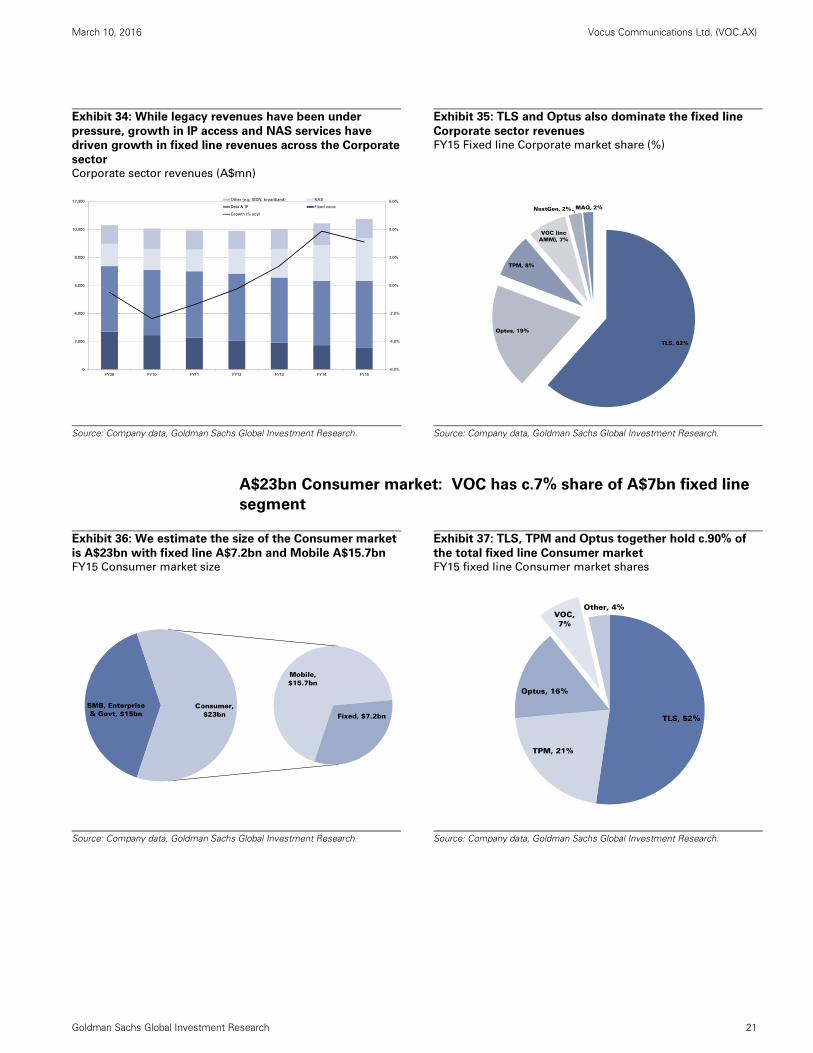

Exhibit 34: While legacy revenues have been under

pressure, growth in IP access and NAS services have

driven growth in fixed line revenues across the Corporate

sector Corporate sector revenues (A$mn)

Exhibit 35: TLS and Optus also dominate the fixed line

Corporate sector revenues FY15 Fixed line Corporate market share (%)

Source: Company data, Goldman Sachs Global Investment Research.

Source: Company data, Goldman Sachs Global Investment Research.

A$23bn Consumer market: VOC has c.7% share of A$7bn fixed line

segment

Exhibit 36: We estimate the size of the Consumer market

is A$23bn with fixed line A$7.2bn and Mobile A$15.7bn FY15 Consumer market size

Exhibit 37: TLS, TPM and Optus together hold c.90% of

the total fixed line Consumer market FY15 fixed line Consumer market shares

Source: Company data, Goldman Sachs Global Investment Research.

Source: Company data, Goldman Sachs Global Investment Research.

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

0

2,000

4,000

6,000

8,000

10,000

12,000

FY09 FY10 FY11 FY12 FY13 FY14 FY15

Other (e.g. ISDN, broadband) NAS

Data & IP Fixed voice

Growth (% yoy)

TLS, 62%

Optus, 19%

TPM, 8%

VOC (inc AMM), 7%

NextGen, 2% MAQ, 2%

SMB, Enterprise & Govt, $15bn

Mobile, $15.7bn

Fixed, $7.2bnConsumer,

$23bn TLS, 52%

TPM, 21%

Optus, 16%

VOC, 7%

Other, 4%

March 10, 2016 Vocus Communications Ltd. (VOC.AX)

Goldman Sachs Global Investment Research 22

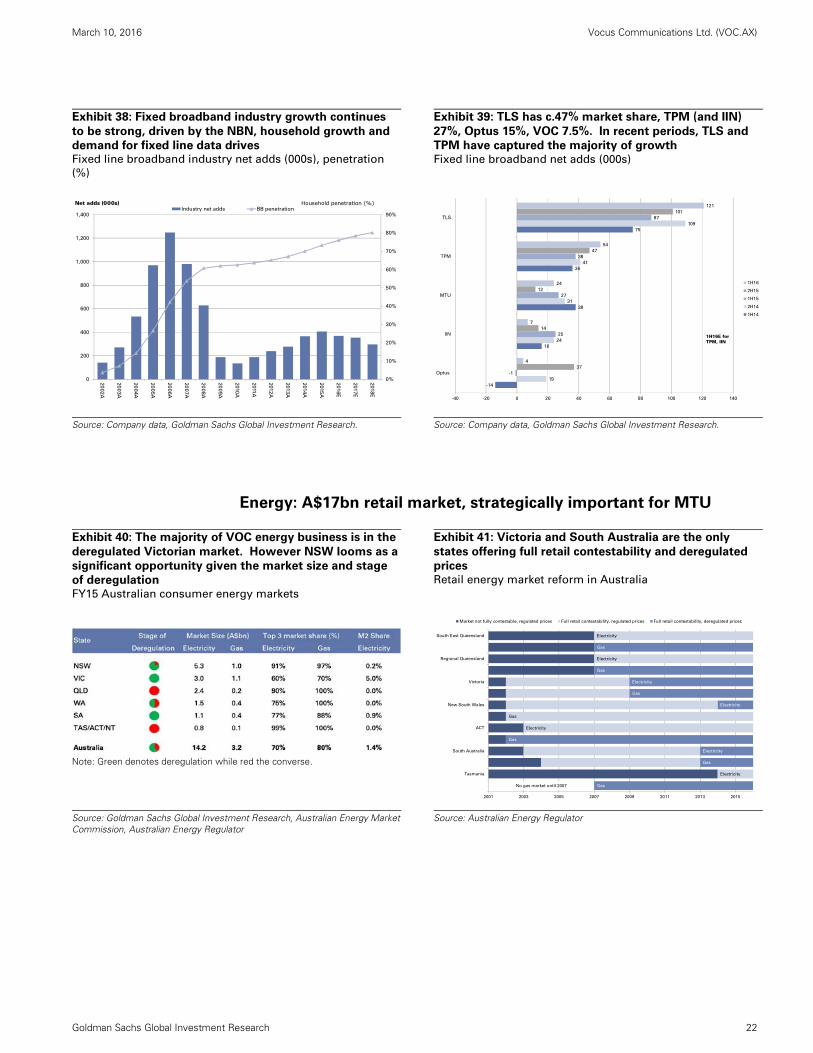

Exhibit 38: Fixed broadband industry growth continues

to be strong, driven by the NBN, household growth and

demand for fixed line data drives Fixed line broadband industry net adds (000s), penetration

(%)

Exhibit 39: TLS has c.47% market share, TPM (and IIN)

27%, Optus 15%, VOC 7.5%. In recent periods, TLS and

TPM have captured the majority of growth Fixed line broadband net adds (000s)

Source: Company data, Goldman Sachs Global Investment Research.

Source: Company data, Goldman Sachs Global Investment Research.

Energy: A$17bn retail market, strategically important for MTU

Exhibit 40: The majority of VOC energy business is in the

deregulated Victorian market. However NSW looms as a

significant opportunity given the market size and stage

of deregulation FY15 Australian consumer energy markets

Exhibit 41: Victoria and South Australia are the only

states offering full retail contestability and deregulated

prices Retail energy market reform in Australia

Note: Green denotes deregulation while red the converse.

Source: Goldman Sachs Global Investment Research, Australian Energy Market Commission, Australian Energy Regulator

Source: Australian Energy Regulator

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0

200

400

600

800

1,000

1,200

1,400

20

02A

20

03A

20

04A

20

05A

20

06A

20

07A

20

08A

20

09A

2010

A

2011

A

2012

A

2013

A

2014A

2015

A

201

6E

201

7E

201

8E

Net adds (000s)Industry net adds BB penetration

Household penetration (%)

-14

16

38

36

75

19

24

31

41

109

-1

25

27

38

87

37

14

12

47

101

4

7

24

54

121

-40 -20 0 20 40 60 80 100 120 140

Optus

IIN

MTU

TPM

TLS

1H16

2H15

1H15

2H14

1H14

1H16E for TPM, IIN

No gas market until 2007 Gas

Electricity

Gas

Electricity

Gas

Gas

Electricity

Gas

Electricity

Gas

Electricity

Electricity

Gas

Electricity

2001 2003 2005 2007 2009 2011 2013 2015

Tasmania

South Australia

ACT

New South Wales

Victoria

Regional Queensland

South East Queensland

Market not fully contestable, regulated prices Full retail contestability, regulated prices Full retail contestability, deregulated prices

March 10, 2016 Vocus Communications Ltd. (VOC.AX)

Goldman Sachs Global Investment Research 23

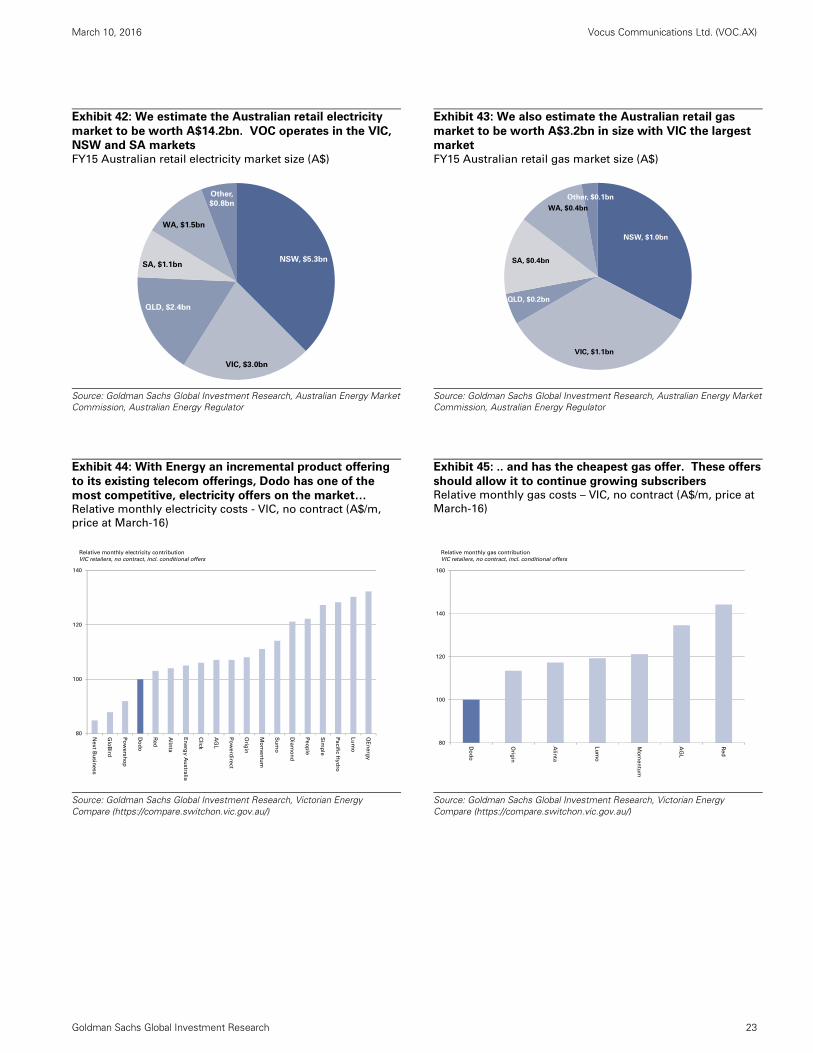

Exhibit 42: We estimate the Australian retail electricity

market to be worth A$14.2bn. VOC operates in the VIC,

NSW and SA markets FY15 Australian retail electricity market size (A$)

Exhibit 43: We also estimate the Australian retail gas

market to be worth A$3.2bn in size with VIC the largest

market FY15 Australian retail gas market size (A$)

Source: Goldman Sachs Global Investment Research, Australian Energy Market Commission, Australian Energy Regulator

Source: Goldman Sachs Global Investment Research, Australian Energy Market Commission, Australian Energy Regulator

Exhibit 44: With Energy an incremental product offering

to its existing telecom offerings, Dodo has one of the

most competitive, electricity offers on the market… Relative monthly electricity costs - VIC, no contract (A$/m,

price at March-16)

Exhibit 45: .. and has the cheapest gas offer. These offers

should allow it to continue growing subscribers Relative monthly gas costs – VIC, no contract (A$/m, price at

March-16)

Source: Goldman Sachs Global Investment Research, Victorian Energy Compare (https://compare.switchon.vic.gov.au/)

Source: Goldman Sachs Global Investment Research, Victorian Energy Compare (https://compare.switchon.vic.gov.au/)

NSW, $5.3bn

VIC, $3.0bn

QLD, $2.4bn

SA, $1.1bn

WA, $1.5bn

Other,

$0.8bn

NSW, $1.0bn

VIC, $1.1bn

QLD, $0.2bn

SA, $0.4bn

WA, $0.4bn

Other, $0.1bn

80

100

120

140

Nex

t Bu

sin

ess

Glo

Bird

Po

wers

ho

p

Do

do

Red

Alin

ta

En

erg

y A

ustra

lia

Clic

k

AG

L

Po

we

rdire

ct

Orig

in

Mo

men

tum

Su

mo

Dia

mo

nd

Pe

op

le

Sim

ple

Pa

cific

Hy

dro

Lu

mo

QE

nerg

y

Relative monthly electricity contribution

VIC retailers, no contract, incl. conditional offers

80

100

120

140

160

Do

do

Orig

in

Alin

ta

Lu

mo

Mo

men

tum

AG

L

Red

Relative monthly gas contribution

VIC retailers, no contract, incl. conditional offers

March 10, 2016 Vocus Communications Ltd. (VOC.AX)

Goldman Sachs Global Investment Research 24

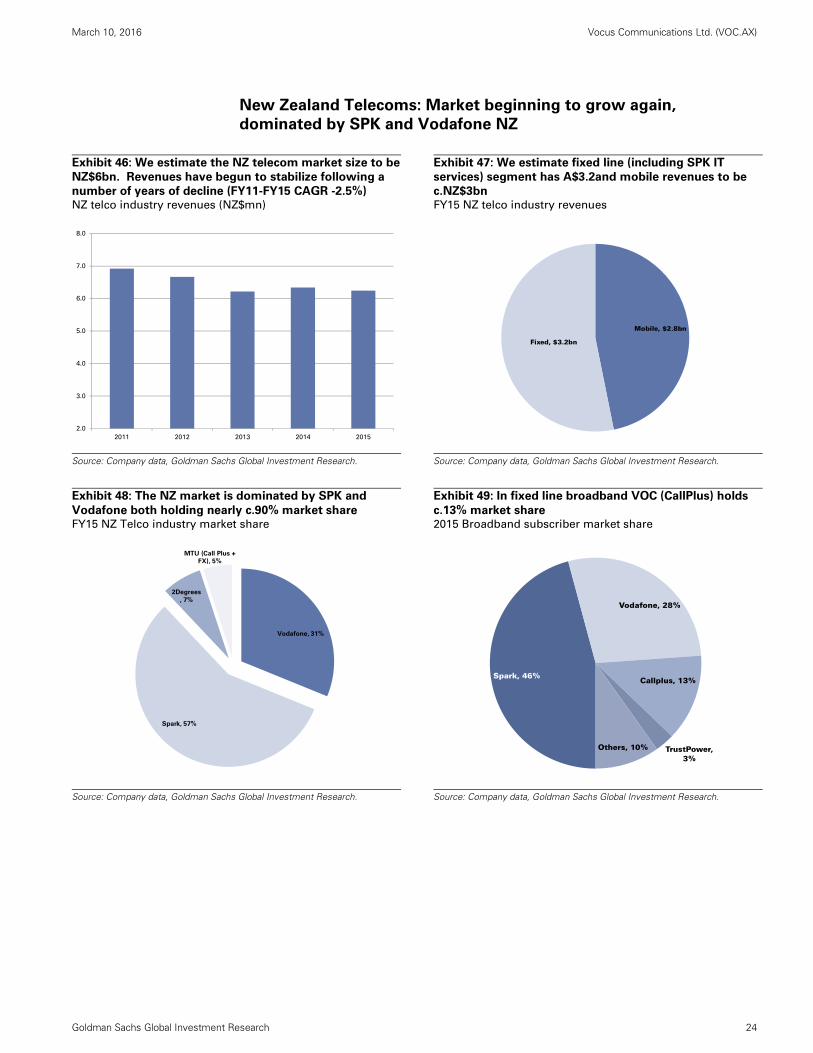

New Zealand Telecoms: Market beginning to grow again,

dominated by SPK and Vodafone NZ

Exhibit 46: We estimate the NZ telecom market size to be

NZ$6bn. Revenues have begun to stabilize following a

number of years of decline (FY11-FY15 CAGR -2.5%) NZ telco industry revenues (NZ$mn)

Exhibit 47: We estimate fixed line (including SPK IT

services) segment has A$3.2and mobile revenues to be

c.NZ$3bn FY15 NZ telco industry revenues

Source: Company data, Goldman Sachs Global Investment Research.

Source: Company data, Goldman Sachs Global Investment Research.

Exhibit 48: The NZ market is dominated by SPK and

Vodafone both holding nearly c.90% market share FY15 NZ Telco industry market share

Exhibit 49: In fixed line broadband VOC (CallPlus) holds

c.13% market share 2015 Broadband subscriber market share

Source: Company data, Goldman Sachs Global Investment Research.

Source: Company data, Goldman Sachs Global Investment Research.

2.0

3.0

4.0

5.0

6.0

7.0

8.0

2011 2012 2013 2014 2015

Mobile, $2.8bn

Fixed, $3.2bn

Vodafone, 31%

Spark, 57%

2Degrees

, 7%

MTU (Call Plus +

FX), 5%

Spark, 46%

Vodafone, 28%

Callplus, 13%

TrustPower, 3%

Others, 10%

March 10, 2016 Vocus Communications Ltd. (VOC.AX)

Goldman Sachs Global Investment Research 25

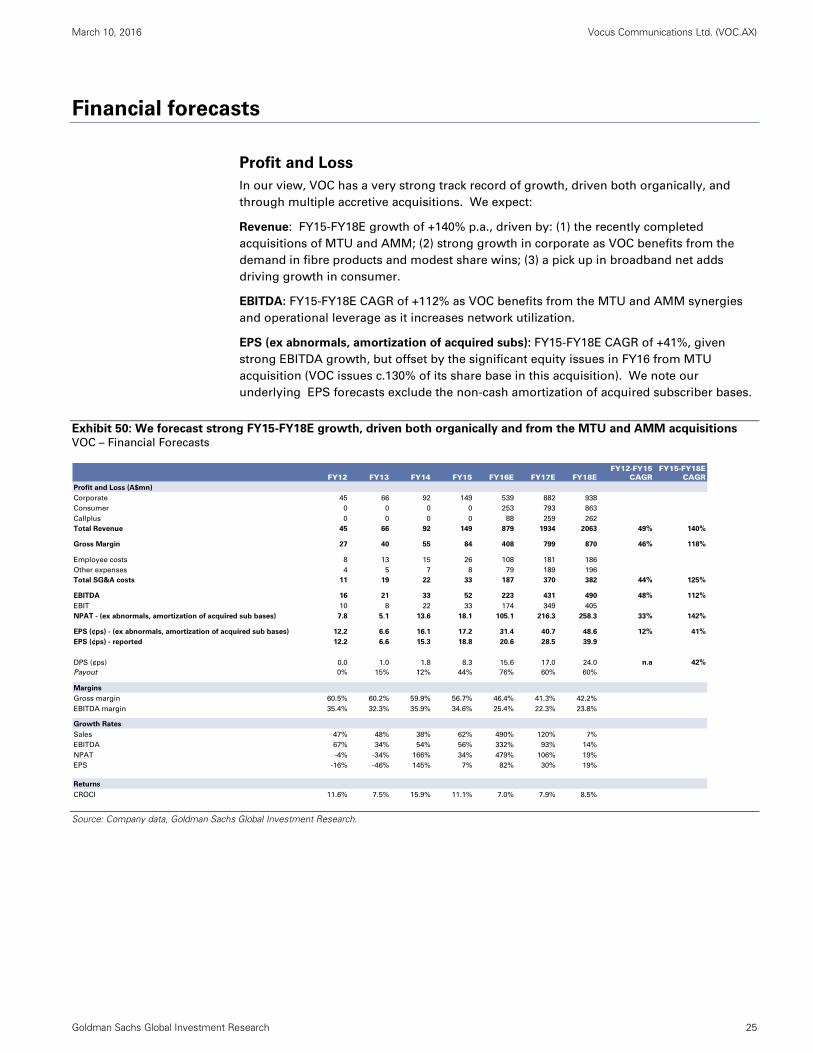

Financial forecasts

Profit and Loss

In our view, VOC has a very strong track record of growth, driven both organically, and

through multiple accretive acquisitions. We expect:

Revenue: FY15-FY18E growth of +140% p.a., driven by: (1) the recently completed

acquisitions of MTU and AMM; (2) strong growth in corporate as VOC benefits from the

demand in fibre products and modest share wins; (3) a pick up in broadband net adds

driving growth in consumer.

EBITDA: FY15-FY18E CAGR of +112% as VOC benefits from the MTU and AMM synergies

and operational leverage as it increases network utilization.

EPS (ex abnormals, amortization of acquired subs): FY15-FY18E CAGR of +41%, given

strong EBITDA growth, but offset by the significant equity issues in FY16 from MTU

acquisition (VOC issues c.130% of its share base in this acquisition). We note our

underlying EPS forecasts exclude the non-cash amortization of acquired subscriber bases.

Exhibit 50: We forecast strong FY15-FY18E growth, driven both organically and from the MTU and AMM acquisitions

VOC – Financial Forecasts

Source: Company data, Goldman Sachs Global Investment Research.

FY12-FY15 FY15-FY18EFY12 FY13 FY14 FY15 FY16E FY17E FY18E CAGR CAGR

Profit and Loss (A$mn)

Corporate 45 66 92 149 539 882 938

Consumer 0 0 0 0 253 793 863

Callplus 0 0 0 0 88 259 262

Total Revenue 45 66 92 149 879 1934 2063 49% 140%

Gross Margin 27 40 55 84 408 799 870 46% 118%

Employee costs 8 13 15 26 108 181 186

Other expenses 4 5 7 8 79 189 196

Total SG&A costs 11 19 22 33 187 370 382 44% 125%

EBITDA 16 21 33 52 223 431 490 48% 112%

EBIT 10 8 22 33 174 349 405

NPAT - (ex abnormals, amortization of acquired sub bases) 7.8 5.1 13.6 18.1 105.1 216.3 258.3 33% 142%

EPS (¢ps) - (ex abnormals, amortization of acquired sub bases) 12.2 6.6 16.1 17.2 31.4 40.7 48.6 12% 41%

EPS (¢ps) - reported 12.2 6.6 15.3 18.8 20.6 28.5 39.9

DPS (¢ps) 0.0 1.0 1.8 8.3 15.6 17.0 24.0 n.a 42%

Payout 0% 15% 12% 44% 76% 60% 60%

Margins

Gross margin 60.5% 60.2% 59.9% 56.7% 46.4% 41.3% 42.2%

EBITDA margin 35.4% 32.3% 35.9% 34.6% 25.4% 22.3% 23.8%

Growth Rates

Sales 47% 48% 38% 62% 490% 120% 7%

EBITDA 67% 34% 54% 56% 332% 93% 14%

NPAT -4% -34% 166% 34% 479% 106% 19%

EPS -16% -46% 145% 7% 82% 30% 19%

Returns

CROCI 11.6% 7.5% 15.9% 11.1% 7.0% 7.9% 8.5%

March 10, 2016 Vocus Communications Ltd. (VOC.AX)

Goldman Sachs Global Investment Research 26

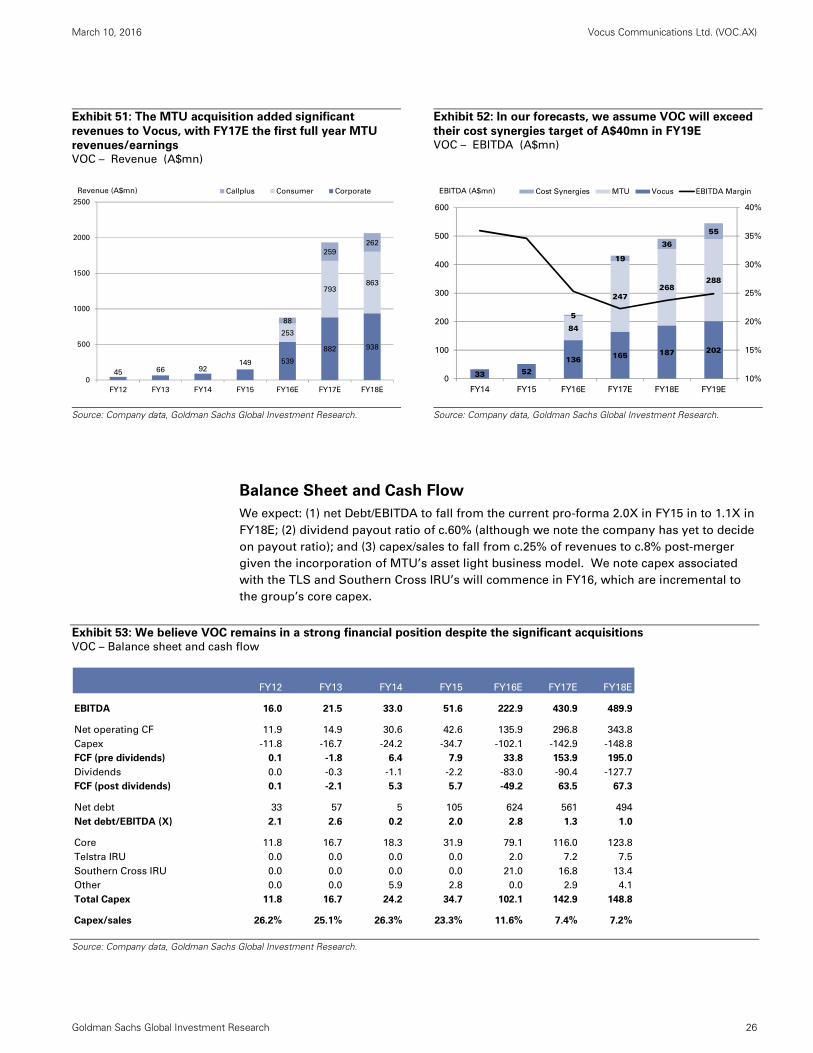

Exhibit 51: The MTU acquisition added significant

revenues to Vocus, with FY17E the first full year MTU

revenues/earnings VOC – Revenue (A$mn)

Exhibit 52: In our forecasts, we assume VOC will exceed

their cost synergies target of A$40mn in FY19E VOC – EBITDA (A$mn)

Source: Company data, Goldman Sachs Global Investment Research.

Source: Company data, Goldman Sachs Global Investment Research.

Balance Sheet and Cash Flow

We expect: (1) net Debt/EBITDA to fall from the current pro-forma 2.0X in FY15 in to 1.1X in

FY18E; (2) dividend payout ratio of c.60% (although we note the company has yet to decide

on payout ratio); and (3) capex/sales to fall from c.25% of revenues to c.8% post-merger

given the incorporation of MTU’s asset light business model. We note capex associated

with the TLS and Southern Cross IRU’s will commence in FY16, which are incremental to

the group’s core capex.

Exhibit 53: We believe VOC remains in a strong financial position despite the significant acquisitions

VOC – Balance sheet and cash flow

Source: Company data, Goldman Sachs Global Investment Research.

45 66 92149 539

882 938

253

793863

88

259

262

0

500

1000

1500

2000

2500

FY12 FY13 FY14 FY15 FY16E FY17E FY18E

Callplus Consumer CorporateRevenue (A$mn)

33 52

136 165 187 202

84

247268

288

5

19

36

55

10%

15%

20%

25%

30%

35%

40%

0

100

200

300

400

500

600

FY14 FY15 FY16E FY17E FY18E FY19E

Cost Synergies MTU Vocus EBITDA MarginEBITDA (A$mn)

FY12 FY13 FY14 FY15 FY16E FY17E FY18E

EBITDA 16.0 21.5 33.0 51.6 222.9 430.9 489.9

Net operating CF 11.9 14.9 30.6 42.6 135.9 296.8 343.8

Capex -11.8 -16.7 -24.2 -34.7 -102.1 -142.9 -148.8

FCF (pre dividends) 0.1 -1.8 6.4 7.9 33.8 153.9 195.0

Dividends 0.0 -0.3 -1.1 -2.2 -83.0 -90.4 -127.7

FCF (post dividends) 0.1 -2.1 5.3 5.7 -49.2 63.5 67.3

Net debt 33 57 5 105 624 561 494

Net debt/EBITDA (X) 2.1 2.6 0.2 2.0 2.8 1.3 1.0

Core 11.8 16.7 18.3 31.9 79.1 116.0 123.8

Telstra IRU 0.0 0.0 0.0 0.0 2.0 7.2 7.5

Southern Cross IRU 0.0 0.0 0.0 0.0 21.0 16.8 13.4

Other 0.0 0.0 5.9 2.8 0.0 2.9 4.1

Total Capex 11.8 16.7 24.2 34.7 102.1 142.9 148.8

Capex/sales 26.2% 25.1% 26.3% 23.3% 11.6% 7.4% 7.2%

March 10, 2016 Vocus Communications Ltd. (VOC.AX)

Goldman Sachs Global Investment Research 27

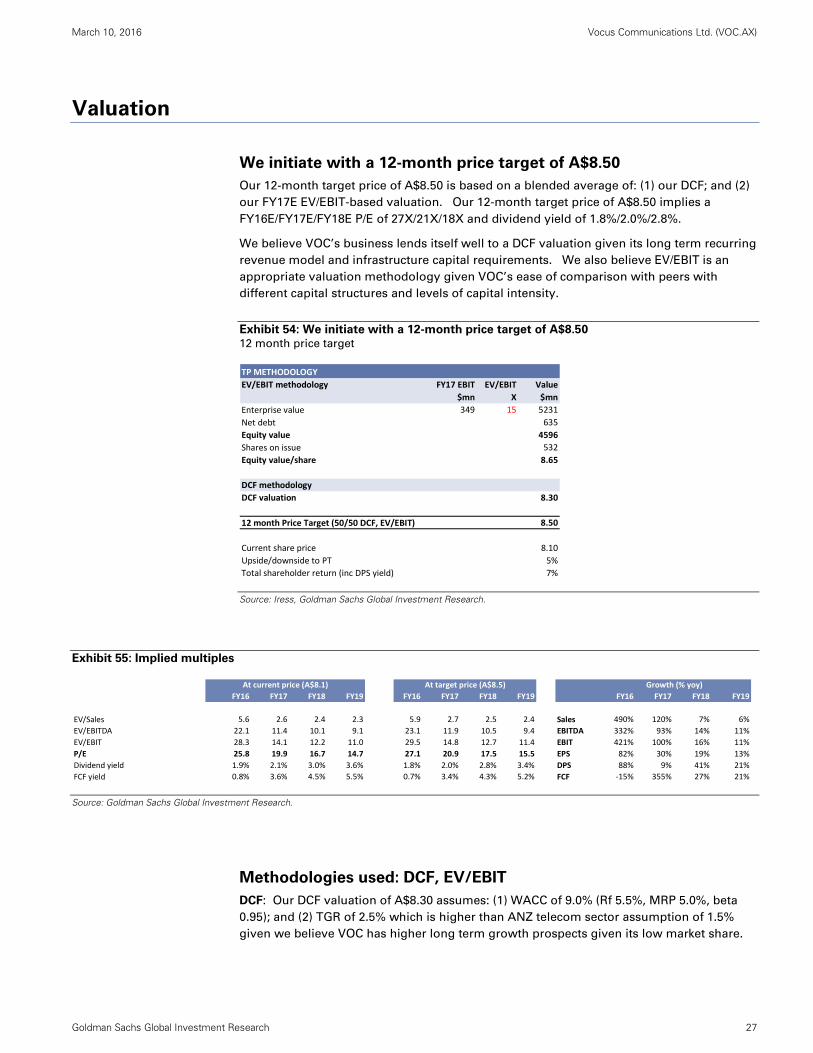

Valuation

We initiate with a 12-month price target of A$8.50

Our 12-month target price of A$8.50 is based on a blended average of: (1) our DCF; and (2)

our FY17E EV/EBIT-based valuation. Our 12-month target price of A$8.50 implies a

FY16E/FY17E/FY18E P/E of 27X/21X/18X and dividend yield of 1.8%/2.0%/2.8%.

We believe VOC’s business lends itself well to a DCF valuation given its long term recurring

revenue model and infrastructure capital requirements. We also believe EV/EBIT is an

appropriate valuation methodology given VOC’s ease of comparison with peers with

different capital structures and levels of capital intensity.

Exhibit 54: We initiate with a 12-month price target of A$8.50

12 month price target

Source: Iress, Goldman Sachs Global Investment Research.

Exhibit 55: Implied multiples

Source: Goldman Sachs Global Investment Research.

Methodologies used: DCF, EV/EBIT

DCF: Our DCF valuation of A$8.30 assumes: (1) WACC of 9.0% (Rf 5.5%, MRP 5.0%, beta

0.95); and (2) TGR of 2.5% which is higher than ANZ telecom sector assumption of 1.5%

given we believe VOC has higher long term growth prospects given its low market share.

TP METHODOLOGY

EV/EBIT methodology FY17 EBIT EV/EBIT Value

$mn X $mn

Enterprise value 349 15 5231

Net debt 635

Equity value 4596

Shares on issue 532

Equity value/share 8.65

DCF methodology

DCF valuation 8.30

12 month Price Target (50/50 DCF, EV/EBIT) 8.50

Current share price 8.10

Upside/downside to PT 5%

Total shareholder return (inc DPS yield) 7%

FY16 FY17 FY18 FY19 FY16 FY17 FY18 FY19 FY16 FY17 FY18 FY19

EV/Sales 5.6 2.6 2.4 2.3 5.9 2.7 2.5 2.4 Sales 490% 120% 7% 6%

EV/EBITDA 22.1 11.4 10.1 9.1 23.1 11.9 10.5 9.4 EBITDA 332% 93% 14% 11%

EV/EBIT 28.3 14.1 12.2 11.0 29.5 14.8 12.7 11.4 EBIT 421% 100% 16% 11%

P/E 25.8 19.9 16.7 14.7 27.1 20.9 17.5 15.5 EPS 82% 30% 19% 13%

Dividend yield 1.9% 2.1% 3.0% 3.6% 1.8% 2.0% 2.8% 3.4% DPS 88% 9% 41% 21%

FCF yield 0.8% 3.6% 4.5% 5.5% 0.7% 3.4% 4.3% 5.2% FCF ‐15% 355% 27% 21%

At current price (A$8.1) At target price (A$8.5) Growth (% yoy)

March 10, 2016 Vocus Communications Ltd. (VOC.AX)

Goldman Sachs Global Investment Research 28

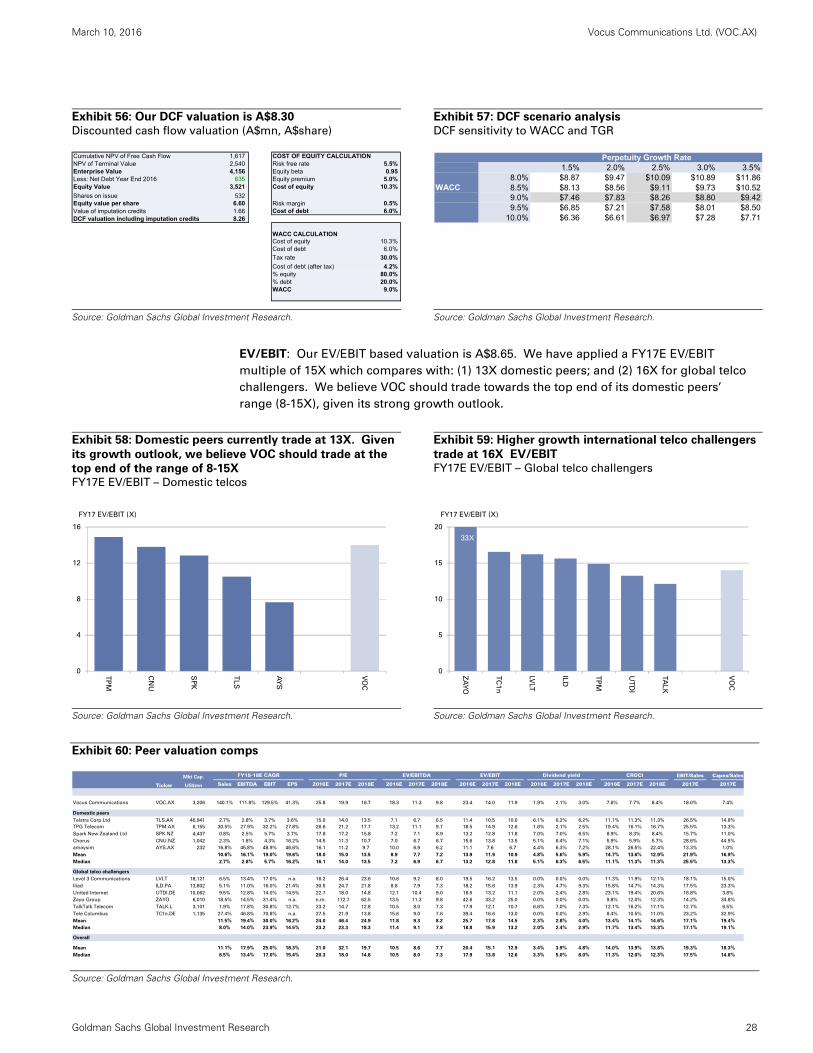

Exhibit 56: Our DCF valuation is A$8.30

Discounted cash flow valuation (A$mn, A$share)

Exhibit 57: DCF scenario analysis

DCF sensitivity to WACC and TGR

Source: Goldman Sachs Global Investment Research.

Source: Goldman Sachs Global Investment Research.

EV/EBIT: Our EV/EBIT based valuation is A$8.65. We have applied a FY17E EV/EBIT

multiple of 15X which compares with: (1) 13X domestic peers; and (2) 16X for global telco

challengers. We believe VOC should trade towards the top end of its domestic peers’

range (8-15X), given its strong growth outlook.

Exhibit 58: Domestic peers currently trade at 13X. Given

its growth outlook, we believe VOC should trade at the

top end of the range of 8-15X FY17E EV/EBIT – Domestic telcos

Exhibit 59: Higher growth international telco challengers

trade at 16X EV/EBIT FY17E EV/EBIT – Global telco challengers

Source: Goldman Sachs Global Investment Research.

Source: Goldman Sachs Global Investment Research.

Exhibit 60: Peer valuation comps

Source: Goldman Sachs Global Investment Research.

Cumulative NPV of Free Cash Flow 1,617 COST OF EQUITY CALCULATIONNPV of Terminal Value 2,540 Risk free rate 5.5% Enterprise Value 4,156 Equity beta 0.95 Less: Net Debt Year End 2016 635 Equity premium 5.0% Equity Value 3,521 Cost of equity 10.3%

Shares on issue 532 Equity value per share 6.60 Risk margin 0.5% Value of imputation credits 1.66 Cost of debt 6.0% DCF valuation including imputation credits 8.26

WACC CALCULATIONCost of equity 10.3% Cost of debt 6.0%

Tax rate 30.0%

Cost of debt (after tax) 4.2% % equity 80.0% % debt 20.0% WACC 9.0%

Perpetuity Growth Rate8 1.5% 2.0% 2.5% 3.0% 3.5%

8.0% $8.87 $9.47 $10.09 $10.89 $11.86WACC 8.5% $8.13 $8.56 $9.11 $9.73 $10.52

9.0% $7.46 $7.83 $8.26 $8.80 $9.429.5% $6.85 $7.21 $7.58 $8.01 $8.50

10.0% $6.36 $6.61 $6.97 $7.28 $7.71

0

4

8

12

16

TP

M

CN

U

SP

K

TL

S

AY

S

VO

C

FY17 EV/EBIT (X)

0

5

10

15

20

ZA

YO

TC

1n

LVLT

ILD

TP

M

UT

DI

TA

LK

VO

C

FY17 EV/EBIT (X)

33X

Mkt Cap. EBIT/Sales Capex/Sales

Ticker US$mn Sales EBITDA EBIT EPS 2016E 2017E 2018E 2016E 2017E 2018E 2016E 2017E 2018E 2016E 2017E 2018E 2016E 2017E 2018E 2017E 2017E

Vocus Communications VOC.AX 3,206 140.1% 111.8% 129.5% 41.3% 25.8 19.9 16.7 18.3 11.3 9.8 23.4 14.0 11.9 1.9% 2.1% 3.0% 7.6% 7.7% 8.4% 18.0% 7.4%

Domestic peers

Telstra Corp Ltd TLS.AX 46,941 2.7% 2.8% 3.7% 3.6% 15.0 14.0 13.5 7.1 6.7 6.5 11.4 10.5 10.0 6.1% 6.2% 6.2% 11.1% 11.3% 11.3% 26.5% 14.8%

TPG Telecom TPM.AX 6,155 30.5% 27.9% 32.2% 27.8% 26.6 21.2 17.7 13.2 11.1 9.7 18.5 14.9 12.6 1.6% 2.1% 2.5% 19.4% 16.1% 16.7% 25.5% 13.3%

Spark New Zealand Ltd SPK.NZ 4,437 0.8% 2.5% 5.7% 3.7% 17.8 17.2 15.8 7.2 7.1 6.9 13.2 12.8 11.8 7.0% 7.0% 6.5% 8.9% 8.3% 8.4% 15.7% 11.0%

Chorus CNU.NZ 1,042 2.3% 1.8% 4.3% 16.2% 14.5 11.3 10.7 7.0 6.7 6.7 15.6 13.8 13.5 5.1% 6.4% 7.1% 5.9% 5.9% 5.7% 28.6% 44.5%

amaysim AYS.AX 232 16.8% 45.8% 48.9% 46.6% 16.1 11.2 9.7 10.0 6.9 6.2 11.1 7.6 6.7 4.4% 6.3% 7.2% 28.1% 26.5% 22.4% 13.3% 1.0%

Mean 10.6% 16.1% 19.0% 19.6% 18.0 15.0 13.5 8.9 7.7 7.2 13.9 11.9 10.9 4.8% 5.6% 5.9% 14.7% 13.6% 12.9% 21.9% 16.9%

Median 2.7% 2.8% 5.7% 16.2% 16.1 14.0 13.5 7.2 6.9 6.7 13.2 12.8 11.8 5.1% 6.3% 6.5% 11.1% 11.3% 11.3% 25.5% 13.3%

Global telco challengers

Level 3 Communications LVLT 18,121 6.5% 13.4% 17.0% n.a. 16.2 26.4 23.6 10.6 9.2 8.0 19.5 16.2 13.5 0.0% 0.0% 0.0% 11.3% 11.9% 12.1% 18.1% 15.0%

Iliad ILD.PA 13,802 5.1% 11.0% 16.0% 21.4% 30.5 24.7 21.8 8.8 7.9 7.3 18.2 15.6 13.9 2.3% 4.7% 9.3% 15.8% 14.7% 14.3% 17.5% 23.3%

United Internet UTDI.DE 10,062 9.5% 12.8% 14.0% 14.5% 22.7 18.0 14.8 12.1 10.4 9.0 16.5 13.2 11.1 2.0% 2.4% 2.8% 23.1% 19.4% 20.6% 16.8% 3.8%

Zayo Group ZAYO 6,010 18.5% 14.5% 31.4% n.a. n.m. 172.7 62.5 13.5 11.3 9.8 42.6 33.2 25.0 0.0% 0.0% 0.0% 9.8% 12.0% 12.3% 14.2% 34.8%

TalkTalk Telecom TALK.L 3,101 1.9% 17.8% 30.8% 12.7% 23.2 14.7 12.8 10.5 8.0 7.3 17.9 12.1 10.7 6.6% 7.0% 7.3% 12.1% 16.2% 17.1% 12.7% 6.5%

Tele Columbus TC1n.DE 1,135 27.4% 46.8% 70.8% n.a. 27.5 21.9 13.8 15.6 9.0 7.6 39.4 16.6 13.0 0.0% 0.0% 2.9% 8.4% 10.5% 11.0% 23.2% 32.9%

Mean 11.5% 19.4% 30.0% 16.2% 24.0 46.4 24.9 11.8 9.3 8.2 25.7 17.8 14.5 2.3% 2.8% 4.0% 13.4% 14.1% 14.6% 17.1% 19.4%

Median 8.0% 14.0% 23.9% 14.5% 23.2 23.3 18.3 11.4 9.1 7.8 18.8 15.9 13.2 2.0% 2.4% 2.9% 11.7% 13.4% 13.3% 17.1% 19.1%

Overall

Mean 11.1% 17.9% 25.0% 18.3% 21.0 32.1 19.7 10.5 8.6 7.7 20.4 15.1 12.9 3.4% 3.9% 4.8% 14.0% 13.9% 13.8% 19.3% 18.3%

Median 6.5% 13.4% 17.0% 15.4% 20.3 18.0 14.8 10.5 8.0 7.3 17.9 13.8 12.6 3.3% 5.0% 6.0% 11.3% 12.0% 12.3% 17.5% 14.8%

CROCIFY15-18E CAGR P/E EV/EBITDA EV/EBIT Dividend yield

March 10, 2016 Vocus Communications Ltd. (VOC.AX)

Goldman Sachs Global Investment Research 29

Key risks

Competition: VOC faces competition from larger operators TLS, Optus and TPM (and SPK,

Vodafone in NZ) with stronger competitive positioning (e.g. greater ability to bundle,

infrastructure ownership) and greater scale. Over time it will likely face increased

competition in the Consumer segment from new entrants as the NBN rollout reaches

greater scale. However we note that VOC: (1) has the lowest market share among its key

competitors; and (2) is not facing a material increase in wholesale input costs (vs.

competitors) with the migration to the NBN.

M&A integration/execution risk: While both have a strong track record of integrating

acquisitions, combining VOC/MTU soon after VOC’s acquisition of AMM, will likely to be

challenging. There is a risk that cost and revenue synergies from the merger could be

lower/higher than our expectations.

Technology risk: We expect the NBN to accelerate the decline in legacy products such as

PSTN. The key issue for MTU is that an average SMB customer (3 PSTN lines, 1 broadband

line) spends 65%-75% of its monthly bill on PSTN products. One of the key challenges

facing MTU will be growing other revenue streams to replace these legacy products.

Supplier risk: VOC’s two main suppliers of telecom services are TLS and Optus. As a