Embed Size (px)

Citation preview

8/3/2019 Weekly Market Update for Sunday January 22nd 2012

http://slidepdf.com/reader/full/weekly-market-update-for-sunday-january-22nd-2012 1/6

WeeklyMarketUpdate

22 January 2012

GCC Indices

GCC Indices

The GCC region finished the week mixed after three indices increased and

four declined. The DSM lost 2.73% due to across-the-board selling, while

the MSM 30 dropped 1.91% as all three sectors ended lower. The TASI fell

1.67% depressed by the Cement and Banks & Financial Services sectors,

while the ADX closed down 1.00% impacted by Investment & Financial

Services and Services sector selling. Winners included the KSE which rose

0.90% following strong performances by the Real Estate and Banking

sectors, and the BSE which gained 0.79% on positive Investment and

Commercial Bank sector sentiment. The DFM ended the week up 0.02%.

World Indices The NASDAQ, Dow Jones, and S&P 500 increased 2.80%, 2.40%, and

2.04%, respectively, as better-than-expected economic data and company

earnings boosted confidence in US growth. The Hang Seng and Nikkei

jumped 4.72% and 3.13%, respectively, in response to lower US initial

jobless claims and European borrowing costs. Similarly, the Sensex added

3.62% as concerns over global economic growth eased and several Indian

companies posted earnings ahead of estimates. The FTSE finished the

week 1.63% higher led by a rally in lenders, after Spain and France sold

bonds at lower yields, and following results from financials including Bank

of America Corp. and Morgan Stanley which exceeded estimates.

Asset Management | [email protected] 1

Global Commodities and CurrenciesCommodit Latest 1W YTDICE Brent USD/bbl 109.90 (0.45% 2.33%

Nymex WTI 98.46 (0.24% (0.37%

OPEC Bas. 111.59 (1.19% 4.53%

Nat. Gas 2.34 (12.25 (21.61

Gold 100 oz USD/t 1,663.7 2.04% 6.25%

Platinum USD/t oz 1,530.3 2.93% 9.33%

Copper USD/MT 8,350.5 5.09% 13.27%

Zinc USD/MT 2,011.5 3.42% 11.87%

Aluminium 2,181.0 1.09% 10.37%

Su ar USD/lb 24.89 4.40% 6.82%Soybean USD/bu 1,187.0 2.33% (0.95%

Corn USD/bu 611.40 2.00% (5.41%

Wheat USD/bu 610.40 1.36% (6.47%

Rice USD/cwt 14.54 1.04% (0.48%

EUR 1.2941 2.01% (0.27%

GBP 1.5536 1.53% (0.00%

PY 76.99 0.12% 0.01%

Index Sna shot World IndicesIndex Latest 1W YTDS&P 500 1,315.38 2.04% 4.59%

Dow Jones 12,720.4 2.40% 4.12%

Nasda 2,786.70 2.80% 6.97%

Hang Seng 20,110.3 4.72% 9.09%

Nikkei 225 8,766.36 3.13% 3.68%

FTSE 100 5,728.55 1.63% 2.80%

Sensex 30 16,739.0 3.62% 8.31%

Interest Rates

Int. Rates Lates 1W YTD

1M US Libor (%) 0.28 (0.01) (0.02)3M US Libor (%) 0.56 (0.01) (0.02)

6M US Libor (%) 0.79 - (0.02)

1M Eibor (%) 0.98 0.01 0.01

3M Eibor (%) 1.53 0.01 0.01

6M Eibor (%) 1.71 - -

2-yr US Treasury 0.26 0.02 0.01

10- r US Treasur 2.05 0.16 0.16

Sources: Bloomberg, LME, US treasury, CME Group, OPEC, Live charts, UAE Central Bank, Erate, and XE

ndex Snapshot (Regionalices)

1W chg (19 Jan. 2011)

-3% -2% -1% 0% 1%

DSM

MSM 30

BSE

KSE

ADSM

DFM

TASI

S&P Pan Arab

DCB Funds

und Curr. NAV*

DCB MSCI UAEndex Fund

AED 3.400

DCB Arabianarkets Fund

USD 5.006

NAV as on 17th Jan, 2012

DCB Arabian Index Fund

The Fund’s investmentbjective is to provide

nvestors with the investmenteturns which correspondosely to the total return of

he S&P Pan Arab Large/Midap Composite Index before

ees and expenses.

ontactsIlias Kakos

hone: +971 2 697 3475mail: [email protected]

8/3/2019 Weekly Market Update for Sunday January 22nd 2012

http://slidepdf.com/reader/full/weekly-market-update-for-sunday-january-22nd-2012 2/6

WeeklyMarketUpdate

22 January 2012

International News

Economic ReleasesThe US reported a much bigger than

expected decline in initial jobless claims in the

week ended January 14th, with claims falling to

352,000 from the previous week's revised figure

of 402,000, Labor Department figures showed.

New US housing starts fell further than

anticipated in December to a seasonally

adjusted annual rate of 657,000, 4.1% below

their November level, according to data released

by the Commerce Department.

US industrial production rose slightly less

than forecast in December, increasing 0.4%

compared with a 0.5% rise projected by

economists, according to a report issued by the

Federal Reserve.

UK retail sales volumes including auto fuel

rose 0.6% m-o-m in December following a

revised 0.5% decrease in November, figurespublished by the Office for National Statistics

showed.

The Greek current account deficit fell 7.3%

in November, to EUR 2.30bn from EUR 2.48bn a

year earlier, according to data released by the

central bank.

Italian industrial new orders declined 0.7%

in November compared to the corresponding

period in 2010, figures published by statisticaloffice Istat data showed.

France's leading economic index decreased

for the fourth time in five months in November

to 112.5 from 112.7 in October, Conference

Board survey data revealed.

German producer price inflation in 2011

accelerated to a post-1982 high of 5.7%

compared with 2010, figures released by the

Federal Statistical Office showed.

Hong Kong's jobless rate fell to 3.3%

between October and December, the Census and

Statistics Department announced.

Taiwanese export orders decreased 0.72%

y-o-y in December, according to figures released

by the Ministry of Economic Affairs.

India's annual food inflation rate for the

week ended January 7 remained close to zero for

the third consecutive week, increasing only

0.42% following sharp falls in prices of onions,

vegetables, potatoes and wheat.

China posted a fiscal deficit of CNY 519bn in

2011, equal to 1.1% of GDP, said reports citing

Finance Ministry data.

The Mauritian merchandise trade deficit

decreased to MUR 7.82bn in November from

MUR 8.0bn in October, figures released by the

Central Statistical Office showed.

Corporate Actions

Talanx AG acquired Poland’s Towarzystwo

Ubezpieczen Reasekuracji Warta SA from KBC

Group NV for EUR 770mn, beating off various

rivals to expand in Eastern Europe’s largest

insurance market.

The Italian government announced plans to

force Eni SpA to sell its EUR 5.9bn stake in

natural gas distribution network Snam Rete Gas

SpA to increase competition.

Geo Political News

Republican presidential candidate Mitt

Romney accused US President Barack Obama of

practicing "crony capitalism" and taking thecountry down a very dangerous path.

Asset Management | [email protected] 2

8/3/2019 Weekly Market Update for Sunday January 22nd 2012

http://slidepdf.com/reader/full/weekly-market-update-for-sunday-january-22nd-2012 3/6

WeeklyMarketUpdate

22 January 2012

Iran's foreign minister warned Arab

neighbours not to put themselves in a dangerous

position by aligning themselves too closely with

the US in the escalating dispute over Tehran's

nuclear activity.

Asset Management | [email protected] 3

8/3/2019 Weekly Market Update for Sunday January 22nd 2012

http://slidepdf.com/reader/full/weekly-market-update-for-sunday-january-22nd-2012 4/6

WeeklyMarketUpdate

22 January 2012

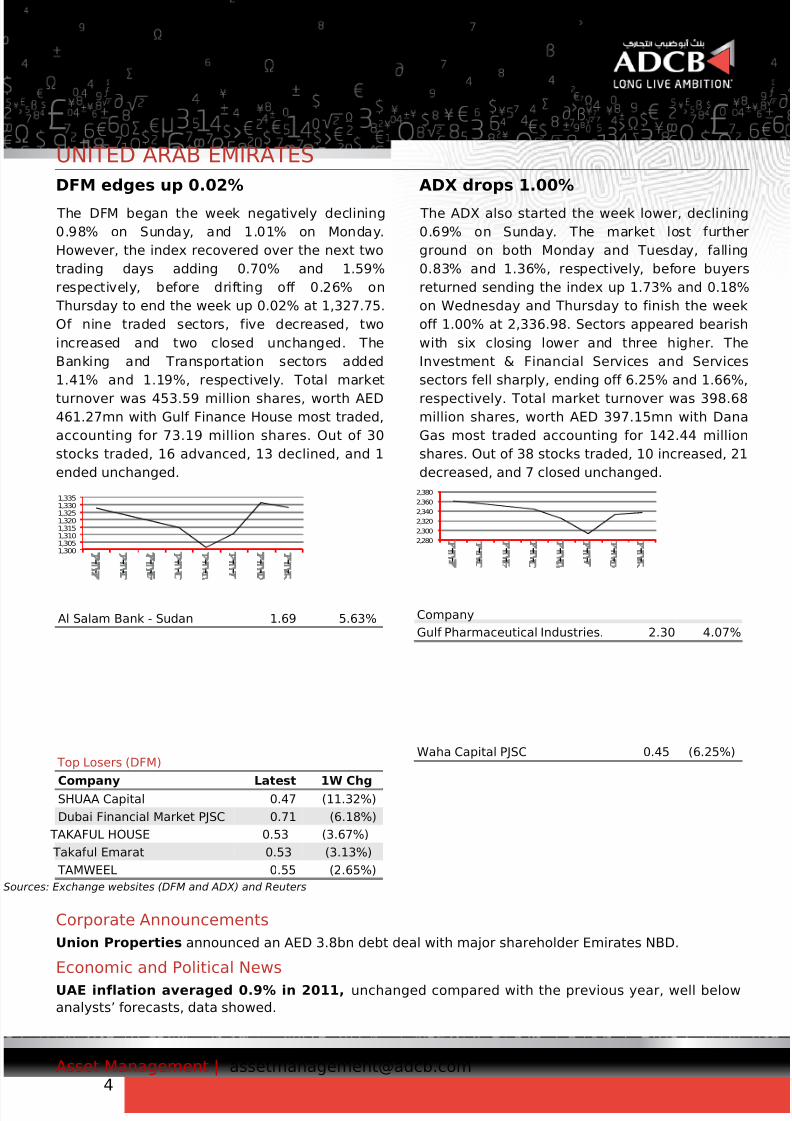

UNITED ARAB EMIRATES

DFM edges up 0.02%

The DFM began the week negatively declining

0.98% on Sunday, and 1.01% on Monday.

However, the index recovered over the next two

trading days adding 0.70% and 1.59%

respectively, before drifting off 0.26% on

Thursday to end the week up 0.02% at 1,327.75.

Of nine traded sectors, five decreased, two

increased and two closed unchanged. The

Banking and Transportation sectors added

1.41% and 1.19%, respectively. Total market

turnover was 453.59 million shares, worth AED

461.27mn with Gulf Finance House most traded,

accounting for 73.19 million shares. Out of 30

stocks traded, 16 advanced, 13 declined, and 1

ended unchanged.

ADX drops 1.00%

The ADX also started the week lower, declining

0.69% on Sunday. The market lost further

ground on both Monday and Tuesday, falling

0.83% and 1.36%, respectively, before buyers

returned sending the index up 1.73% and 0.18%

on Wednesday and Thursday to finish the week

off 1.00% at 2,336.98. Sectors appeared bearish

with six closing lower and three higher. The

Investment & Financial Services and Services

sectors fell sharply, ending off 6.25% and 1.66%,

respectively. Total market turnover was 398.68

million shares, worth AED 397.15mn with Dana

Gas most traded accounting for 142.44 million

shares. Out of 38 stocks traded, 10 increased, 21

decreased, and 7 closed unchanged.

1,300

1,305

1,310

1,315

1,320

1,325

1,330

1,335

- -

- -

- -

- -

- -

- -

- -

- -

2,280

2,300

2,320

2,340

2,360

2,380

- -

- -

- -

- -

- -

- -

- -

- -

Al Salam Bank - Sudan 1.69 5.63% Company

Gulf Pharmaceutical Industries. 2.30 4.07%

Top Losers (DFM)

Company Latest 1W ChgSHUAA Capital 0.47 (11.32%)

Dubai Financial Market PJSC 0.71 (6.18%)

TAKAFUL HOUSE 0.53 (3.67%)

Takaful Emarat 0.53 (3.13%)

TAMWEEL 0.55 (2.65%)

Waha Capital PJSC 0.45 (6.25%)

Corporate Announcements

Union Properties announced an AED 3.8bn debt deal with major shareholder Emirates NBD.

Economic and Political News

UAE inflation averaged 0.9% in 2011, unchanged compared with the previous year, well below

analysts’ forecasts, data showed.

Asset Management | [email protected] 4

rces: Exchange websites (DFM and ADX) and Reuters

8/3/2019 Weekly Market Update for Sunday January 22nd 2012

http://slidepdf.com/reader/full/weekly-market-update-for-sunday-january-22nd-2012 5/6

WeeklyMarketUpdate

22 January 2012

Asset Management | [email protected] 5

8/3/2019 Weekly Market Update for Sunday January 22nd 2012

http://slidepdf.com/reader/full/weekly-market-update-for-sunday-january-22nd-2012 6/6

WeeklyMarketUpdate

22 January 2012

Sources

All information in this report has been obtained from the following sources except were indicatedotherwise:

1. Bloomberg

2. Wall Street Journal

3. Rttnews

4. Reuters

5. Gulfbase

6. Zawya

7. Indian Express

Disclosures This document is for information and illustrative purposes only; it is in no way a recommendation, or

an offer or solicitation to buy or sell any investment products, but only factual information being

provided. ADCB will not be held liable for any information provided in this document which is stated to

have been obtained from third party sources, this information may be based on assumptions or

market conditions and may change without notice.

The information in this report was prepared by employees of ADCB and is current as of the date of

the report. The information contained herein has been obtained from sources that ADCB believes to

be reliable, but ADCB does not guarantee its accuracy, adequacy, completeness, reliability, or

timeliness, and will not be held liable for any investment decisions made based on this information.Moreover, ADCB is not responsible for any errors or omissions or for the results obtained from the use

of such information. All information and estimates included in this report are subject to change

without notice. This report is intended for qualified customers of ADCB.

Past performance does not guarantee future results. Investment products are not bank deposits and

are not guaranteed by ADCB. They are subject to investment risks, including possible loss of principal

amount invested. Please refer to ADCB Terms and Conditions for Investment Services.

You may not redistribute this report without explicit permission from ADCB.

Asset Management | [email protected] 6