Embed Size (px)

Citation preview

1

Weekly Market CommuniquWeekly Market CommuniquWeekly Market CommuniquWeekly Market Communiquéééé

NovemberNovemberNovemberNovember 25, 201125, 201125, 201125, 2011

Mutual Fund Investments are subject to market risks. Please readMutual Fund Investments are subject to market risks. Please readMutual Fund Investments are subject to market risks. Please readMutual Fund Investments are subject to market risks. Please read Scheme Information Document & Statement of Additional InformatiScheme Information Document & Statement of Additional InformatiScheme Information Document & Statement of Additional InformatiScheme Information Document & Statement of Additional Information carefully before on carefully before on carefully before on carefully before investing..investing..investing..investing.. All data/information used in the preparation of this material and the outlook on Markets is dated November 25, 2011 and may or may not be relevant any time after the issuance of this material. The AMC takes no responsibility of updating any data/information in this material from time to time. The recipient of this material is solely responsible for any action taken based on this material. All data source: Crisil except as mentioned specifically. The information contained herein are meant solely for the benefit of the addressee and shall not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent of ICICI Prudential Asset Management Company Limited. Further, the information contained herein should not be construed as forecast or promise. The recipient of this material is solely responsible for any action taken based on this material. Please refer slide no. 42 to 47 for risk factors.

2

Global EconomyGlobal EconomyGlobal EconomyGlobal Economy

Global Economy Global Economy Global Economy Global Economy ---- USUSUSUS

A US Congressional committee fails to reach a deal to cut the federal budget deficit.

US third quarter GDP growth rate was revised down to 2% from previous estimate of 2.5%.

US Federal Reserve to conduct a third round of stress tests to determine if major US banks can withstand a downturn in the economy.

US Fed’s meeting minutes showed that the policymakers this month discussed how they could give businesses and investors more information about what might trigger an increase in interest rates.

US personal income rose 0.4% or $48.1bn in October, while personal spending edged up by just 0.1% as compared to a 0.7% increase in consumer spending in September.

US orders for durable goods fell 0.7% in October, following a decline of 1.5% in September.

S&P says it will not cut US credit rating based on failure of super committee to reach deal.

Moody's warns that its top credit rating for the US could be in trouble if lawmakers backtrack on $1.2 trillion in deficit cuts planned over 10 years.

US index of leading economic indicators rose 0.9% in October, compared with a 0.1% increase in September.

US existing-home sales increased by 1.4% in October from a month earlier to a seasonally adjusted annual rate of 4.97mn.

US Initial Jobless Claims rose by 2000 to 393000 in the week ended November 19.

Global Economy Global Economy Global Economy Global Economy ---- EuropeEuropeEuropeEurope

IMF enhances its lending facility and introduces a new six-month liquidity line to encourage countries at risk from the euro-zone crisis to turn to the fund for help.

European Union agrees to a 2% rise in the bloc's budget for next year to 129bn euros.

European Central Bank (ECB) chief urge Eurozone governments to act fast to get their rescue fund up and running.

Eurozone posts current-account surplus of 500 mn euro in September, the first surplus since January 2010, after an August deficit of 5.9 bn euro.

European consumer confidence drops to the lowest in more than two years at -20.4 points in November from -19.9 in October.

Euro zone industrial new orders fell 6.4% in September from August, the deepest fall since December 2008 and compared with a 1.4% gain in August; on an annual basis, industrial new orders in the euro zone rose 1.6% in September compared with 5.9% gain in August.

Euro-Zone Purchasing Manager Index Composite index rose to 47.2 in November from 46.5 in October.

UK GDP rose 0.2% in the third quarter following 0.1% growth in second quarter as per the second estimate from Britain’s official statistics agency ONS.

Minutes of the Bank of England's November meeting showed that members voted unanimously to hold interest rates and increase the asset borrowing limit by 75bn pounds, some members also said more quantitative easing might well become warranted in due course.

UK public sector borrowing fell to 6.5bn pounds in October as compared with 7.7 bn pounds a year ago.

Global Economy Global Economy Global Economy Global Economy ---- EuropeEuropeEuropeEurope

Moody's Investors Services says that if yields on France's AAA-rated sovereign bonds stay high, it might have a negative impact on the country's credit rating and increase its fiscal challenges.

Fitch Ratings says France's AAA rating would be at risk if the euro-zone debt crisis intensifies; also downgrades Portugal's rating to junk status to BB+ from BBB-.

Global Economy Global Economy Global Economy Global Economy ---- AsiaAsiaAsiaAsia

Japan’s exports declined 3.7% from a year earlier to 5.51 trillion yen in October, while imports rose almost 18% to 5.79 trillion yen, resulting in a trade deficit of 273.8bn yen.

Japan's parliament passes a $157bn extra budget including the issuance of new bonds to pay for the bulk of rebuilding from the March earthquake.

Japan's consumer price index fell 0.1% in October from a year earlier.

S&P warns that Japan could face a downgrade over its inability to reduce its debt pile.

China’s HSBC purchasing managers' index dropped to 48 in November, the lowest since March 2009, compared with 51 in the previous month.

Chinese officials sign $6bn in new loans to Venezuela aiming to boost latter’s oil industry.

People's Bank of China cuts the reserve ratio for more than 20 rural credit cooperatives nationwide by 0.5%.

Singapore warns that its economy will likely suffer a sharp slowdown next year as export demand from developed countries reduces; also says that GDP growth will probably drop to between 1-3% in 2012 from 5% this year.

According to statistics by International Enterprise (IE) Singapore's total trade grew by 5.4 % on-year in the third quarter, down from the previous quarter's 7.5 % expansion.

Singapore's wholesale trade index increased on-year with domestic trade growing 18.0 % and foreign trade increasing by 17.8 % in the third quarter this year.

S&P cuts Egypt’s long-term foreign and local currency sovereign ratings to B+ from BB-, citing the country's dire political and economic situation and the increased risk of civil strife.

Global Economy Global Economy Global Economy Global Economy –––– CorporateCorporateCorporateCorporate

S&P's plans to update its credit ratings for the world's 30 biggest banks within three weeks.

Starr International sues the US government for $25bn, accusing the latter of using the bailout of AIG to channel funds to AIG’s trading partners.

Statoil ASA signs two deals with UK’s Centrica to sell gas for ten years and divest five assets on the Norwegian continental shelf for a combined value of $18.8bn.

Gilead Sciences agrees to buy hepatitis C drug developer Pharmasset for $11bn.

Australia's government approves SABMiller's $11.2bn deal to acquire Foster's Group.

Lockheed Martin wins US Air Force contract worth $7.4bn to upgrade systems on F-22.

KKR & Co to acquire Samson Investment Co for $7.2bn.

Tokyo Stock Exchange to takeover its smaller rival in Osaka in 2013 to create the world's third-biggest bourse with listed stocks worth $3.6 trillion.

Brazil's Vale approves a $6bn expansion of its Moatize coal project in Mozambique.

Suzuki Motor Corp terminates its agreement with Volkswagen AG alleging that the German carmaker denied it access to core technology as was agreed.

8

Global MarketsGlobal MarketsGlobal MarketsGlobal Markets

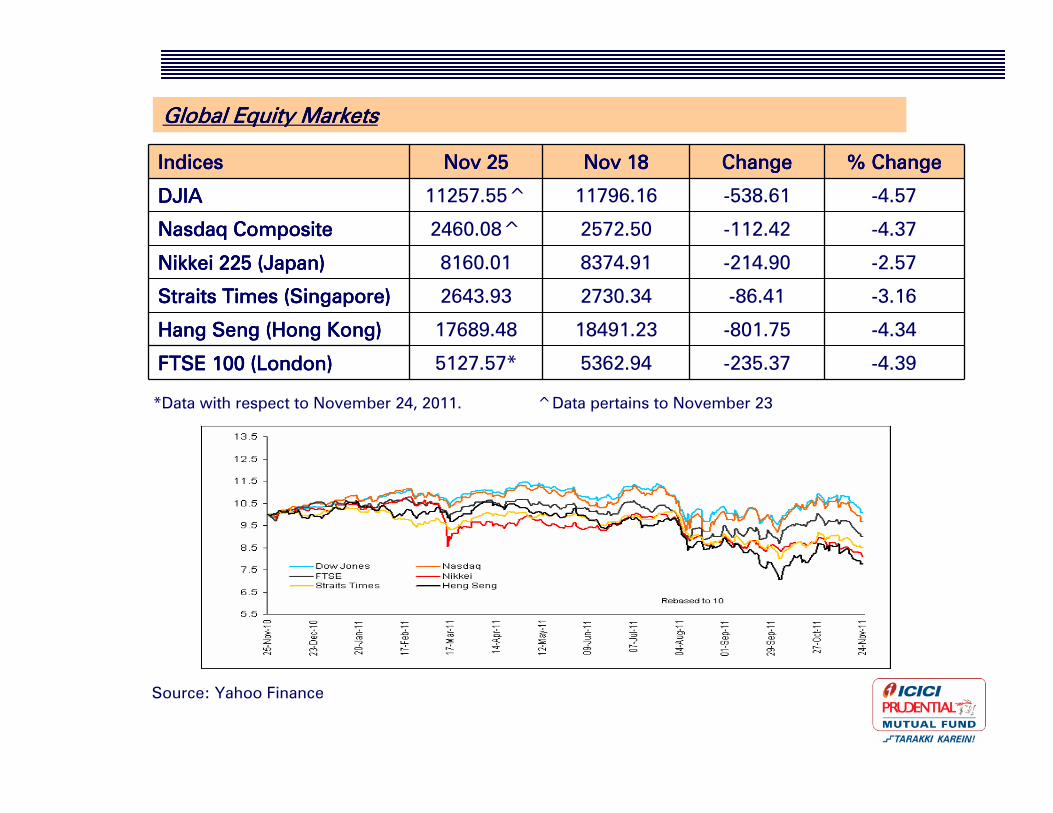

Global Equity MarketsGlobal Equity MarketsGlobal Equity MarketsGlobal Equity Markets

IndicesIndicesIndicesIndices Nov 25Nov 25Nov 25Nov 25 Nov 18Nov 18Nov 18Nov 18 ChangeChangeChangeChange % Change% Change% Change% Change

DJIADJIADJIADJIA 11257.55^ 11796.16 -538.61 -4.57

Nasdaq CompositeNasdaq CompositeNasdaq CompositeNasdaq Composite 2460.08^ 2572.50 -112.42 -4.37

Nikkei 225 (Japan)Nikkei 225 (Japan)Nikkei 225 (Japan)Nikkei 225 (Japan) 8160.01 8374.91 -214.90 -2.57

Straits Times (Singapore)Straits Times (Singapore)Straits Times (Singapore)Straits Times (Singapore) 2643.93 2730.34 -86.41 -3.16

Hang Seng (Hong Kong)Hang Seng (Hong Kong)Hang Seng (Hong Kong)Hang Seng (Hong Kong) 17689.48 18491.23 -801.75 -4.34

FTSE 100 (London)FTSE 100 (London)FTSE 100 (London)FTSE 100 (London) 5127.57* 5362.94 -235.37 -4.39

*Data with respect to November 24, 2011. ^Data pertains to November 23

Source: Yahoo Finance

Key global indices plunge on continuing eurozone debt worriesKey global indices plunge on continuing eurozone debt worriesKey global indices plunge on continuing eurozone debt worriesKey global indices plunge on continuing eurozone debt worries

Wall Street benchmark indices plunged in the week, primarily weighed down by continuing eurozone debt worries, and after a US congressional committee failed to agree on deficit cuts.

Higher borrowing costs for Spain, and weak German bond sale dented investors’sentiments further.

Britain’s FTSE index fell 4.4% in the week weighed down by negative global cues, especially from the Eurozone.

The benchmark was plagued by mounting worries over the health of the global economy as the US and Europe were plagued with their respective debt problems.

Japan's Nikkei fell 2.6% in the holiday curtailed week rising global economic concerns.

Market was affected by US congressional committee’s failed to agree on deficit cuts and a worrying German bond sale.

Hong Kong’s Hang Seng index fell 4.3% in the week amid weak domestic and global cues.

Lingering worries over sovereign debt problems and a sell off in Chinese developers amid concerns of slowing property sales, weighed on the market further.

Singapore’s Straits Times index retreated 3.2% in the week primarily affected by the US congressional committee’s failure to agree on deficit cuts and persisting eurozone debt problems.

US markets decline US markets decline US markets decline US markets decline

Wall Street Wall Street Wall Street Wall Street benchmark indices fell sharply in the week, with the Dow Jones falling 4.6% and Nasdaq ending 4.4% lower.

Markets started negatively after the co-chairs of a US congressional committee said that they have failed to reach a deal on reducing federal government deficits.

Higher borrowing costs for Spain, and weak German bond sale dented investors’sentiments further.

A downward revision of US economic growth in the third quarter pulled down the markets further.

• The Commerce Department said that the US economy grew at a 2% annual rate from July through September, down from its initial estimate of 2.5%.

Persisting worries about the euro zone's debt crisis, coupled with weak Chinese factory data inflicted more losses to the markets.

Some losses were however capped after US index of leading economic indicators rose 0.9% in October, compared with a 0.1% increase in September.

Among other developments and indicators in the week,

• US Federal Reserve decided to conduct a third round of stress tests to determine if major US banks can withstand a downturn in the economy.

• US Fed’s meeting minutes showed that the policymakers this month discussed how they could give businesses and investors more information about what might trigger an increase in interest rates.

BritainBritainBritainBritain’’’’s FTSE fall on negative global cuess FTSE fall on negative global cuess FTSE fall on negative global cuess FTSE fall on negative global cues

BritainBritainBritainBritain’’’’s FTSE s FTSE s FTSE s FTSE index fell 4.4% in the week ended November 24 weighed down by negative global cues, especially from the Eurozone.

Market sentiments were dim earlier amid worries about a lack of unity among European Union politicians on how to deal with the debt crisis.

The benchmark plummeted further on mounting worries over the health of the global economy as the US and Europe were plagued with their respective debt problems.

A weaker than expected US third quarter economic growth dampened investors’ mood further.

Downbeat domestic corporate outlook also contributed to pull the market down.

More losses were seen on the back of downbeat data from China, Europe and the US.

Germany’s opposition to the use of euro bonds or monetary tools to help solve the euro zone's debt crisis, also added to the negativity in the market.

Among major developments and indicators released in the week,

• UK GDP rose 0.2% in the third quarter following 0.1% growth in second quarter as per the second estimate from Britain’s official statistics agency ONS.

Minutes of the Bank of England's November meeting showed that members voted unanimously to hold interest rates and increase the asset borrowing limit by 75bn pounds, some members also said more quantitative easing might well become warranted in due course.

Asian indices also nosediveAsian indices also nosediveAsian indices also nosediveAsian indices also nosedive

SingaporeSingaporeSingaporeSingapore’’’’s Straits Times s Straits Times s Straits Times s Straits Times index retreated 3.2% in the week ended November 25 amid weak global cues, especially from the US and Europe.

The benchmark fell earlier after a US congressional committee failed to agree on deficit cuts.

Persisting worries over sovereign-debt problems in Europe along with a fall in manufacturing activity in China marred investors’ sentiments further.

More losses were seen after the local government said that the economic growth in 2012 would slow amid deteriorating external macroeconomic conditions.

• Singapore warned that its economy would likely suffer a sharp slowdown next year as export demand from developed countries reduces; also said that GDP growth would probably drop to between 1-3% in 2012 from 5% this year.

Market received some respite later in the week after investors shrugged off a poor bond auction in Germany to cover their short positions.

Japan's Nikkei Japan's Nikkei Japan's Nikkei Japan's Nikkei fell 2.6% in the holiday curtailed week ended November 25 on rising global economic concerns.

Market started on a weak note after a US congressional committee failed to agree on deficit cuts.

The benchmark plummeted to a two-and-a-half-year low earlier weighed down by a worrying German bond sale and growing concerns about the European debt crisis.

Asian indices also nosediveAsian indices also nosediveAsian indices also nosediveAsian indices also nosedive

An unexpected fall in Japanese exports in October also affected the market,

• Japan’s exports declined 3.7% from a year earlier to 5.51 trillion yen in October, while imports rose almost 18% to 5.79 trillion yen, resulting in a trade deficit of 273.8bn yen

Among other major developments and indicators released in the week,

• Japan's parliament passed a $157bn extra budget including the issuance of new bonds to pay for the bulk of rebuilding from the March earthquake.

• Japan's consumer price index fell 0.1% in October from a year earlier.

• S&P warned that Japan could face a downgrade over its inability to reduce its debt pile.

• Tokyo Stock Exchange to takeover its smaller rival in Osaka in 2013 to create the world's third-biggest bourse with listed stocks worth $3.6 trillion.

Hong KongHong KongHong KongHong Kong’’’’s Hang Seng index s Hang Seng index s Hang Seng index s Hang Seng index ended 4.3% lower in the week ended November 25 amid weak domestic and global cues.

Investors’ sentiments were hit earlier after Chinese Vice-Premier cautioned that the global economy is in a dismal state.

Lingering worries over sovereign debt problems and a sell off in Chinese developers amid concerns of slowing property sales, weighed on the market further.

Asian indices also nosediveAsian indices also nosediveAsian indices also nosediveAsian indices also nosedive

Chinese Market tumbled further after domestic manufacturing data fell to a 32-month low in November,

• China’s HSBC purchasing managers' index dropped to 48 in November, the lowest since March 2009, compared with 51 in the previous month.

Some losses were however cut short on the back of bargain buying, and on China’s decision to cut the reserve ratio for rural cooperative banks.

• People's Bank of China cut the reserve ratio for more than 20 rural credit cooperatives nationwide by 0.5%.

US debt prices continued to rise in the weekUS debt prices continued to rise in the weekUS debt prices continued to rise in the weekUS debt prices continued to rise in the week

• US Treasury prices rose in the week ended November 23 as worries over the outcome of the euro zone debt crisis underpinned the safe-haven appeal of U.S. government debt.

• The yield on 10 year benchmark bond fell to 1.88% on November 23 as compared to 1.96% on November 17.

• Germany's worst bond auction in the euro era raised concerns the debt crisis was beginning to threaten even the region's benchmark debt issuer.

• Concern got further aggravated after Spain paid a euro-era record of 5.11% to sell three-month bills, more than double the rate it paid at an auction in October.

• Bond prices got support after a congressional panel appeared ready to declare failure in its mission to cut the budget deficit by $1.2 trillion.

• Moody's warning to France of a ratings downgrade also added to the fears of debt contagion.

• Further fall in yields was restricted however after new claims for U.S. unemployment benefits held below 400,000 for the third straight week, suggesting the labor market was gaining some traction.

• Concern over increasing supply due the auction of $29 billion of 7-year notes & $35 billion of the 2-year notes further pulled down the bond prices.

17

Domestic Economic NewsDomestic Economic NewsDomestic Economic NewsDomestic Economic News

EconomyEconomyEconomyEconomy

Prime Minister's Economic Advisory Council Chairman projects a GDP growth rate of 7.5-8% in the 2011-12 financial year.

Planning Commission deputy chairman says that fiscal deficit in the current financial year will exceed 4.6% of the GDP target, though the final figures would depend on the actual expenditure.

India's annual inflation rate based on the CPI for agricultural labourers marginally slipped to 9.36% in October from 9.43% in the previous month and CPI inflation rate for rural labourers rose to 9.73% in October, compared with 9.25% in September.

India's National Consumer Price Index rose to 114.2 in October from 113.1 a month ago.

India's primary articles inflation for week to Nov 12 slipped to an over two-year low of 9.08% from 10.39% a week ago while food articles inflation fell to a 16-week low of 9.01% from 10.63% a week ago.

FM says that inflation may come down to 6-7% by March-end adds that monetary measures taken by RBI have helped curb inflation and inflationary expectations.

RBI Governor says that a sustained increase in the inflation rate undoubtedly warrants a monetary policy response from the central bank.

RBI says demand side inflationary pressures are starting to moderate, but medium-term risks to inflation is still significant.

RBI Governor said that he will not confirm reports that the central bank intervened in the foreign exchange market to arrest the rupee's fall against the dollar.

EconomyEconomyEconomyEconomy

FDI in India rose 41% to $22.5bn during the January-September period this year.

Fitch says India is less prone to global growth shocks but it also has less scope for policy stimulus. S&P says India needs to reform policies concerning project execution and long-term funding to fix its infrastructure, which is a major roadblock to its target of achieving a 9-9.5% annual growth during 2012-2017.

India’s forex reserves fell by $5.72 bn to $308.62 bn as on week ended Nov 18.

GovernmentGovernmentGovernmentGovernment

Union Cabinet allows 51% FDI in multi-brand retail and 100% in single-brand retail operations, up from the current 51%.

Union Cabinet approves the Companies Bill that will completely recast the key provisions of the Companies Act 1956.

Government says it will stick to its disinvestment target of Rs 40,000 cr for the 2011-12 financial year, but achieving this goal will hinge on many other factors.

Disinvestment Ministry says it has received in-principle clearance from Petroleum Ministry and is going ahead with the sale of government equity in Oil India Ltd (OIL).

Department of Industrial Policy and Promotion recommends that overseas airlines be allowed to acquire up to 26% of domestic carriers.

India to launch its maiden bid round for exploration of shale gas during the 12th Plan Period.

Petroleum Ministry seeks Rs 56,600 cr additional cash subsidy to partially compensate the state-owned oil firms for losses they incur on selling fuel below cost.

Petroleum Minister hints that the government will not rush into raising retail fuel prices just yet, even though a falling rupee has increased cost of oil imports.

Government gives clearances to three mega infrastructure projects involving an investment of Rs 25,000 cr.

Finance ministry and RBI are planning to put stringent curbs on financial entities taking on too many risks with their own funds.

GovernmentGovernmentGovernmentGovernment

Finance ministry asks SEBI to take a second look at its decision to introduce transaction charges for mutual fund agents.

Finance ministry is in talks with financial regulators to relax the entry norms for foreign retail investors into India’s MF industry.

Government says Policy responses have "succeeded" in moderating inflation expectations below double digits.

Government says it is not considering bringing a Voluntary Disclosure Scheme for declaration of unaccounted money stashed abroad.

Government says it is not considering lowering the Securities Transaction Tax in the country.

Government says gross collections under various small savings schemes of the Indian Post increased by about 9% to Rs.2.75 lakh cr in 2010-11 in comparison to the previous year.

Power Ministry asks for a Rs 40,000 cr fund allocation from the Planning Commission for green energy sector.

Government asks the accounting regulator ICAI to remind companies that they have only a week left for switchover to the new financial reporting format.

Government plans to set up a Rs 2,500 cr development fund for auto component sector.

FM says that RBI intervention in the forex market will not arrest the slide as FIIs' pullout and global reasons were behind the depreciation.

Economic Affairs Secretary says that the ability to intervene in the foreign exchange market is limited.

GovernmentGovernmentGovernmentGovernment

Finance Ministry rejects a policy drafted by the Planning Commission to attract new investment in the urea sector, saying the proposals are unrealistic, unviable and will lead to high subsidy outgo.

World Bank plans to invest about $1.5bn in India’s energy sector over the next two years.

Government plans to devise a new index of industrial output that will also measure the growth in the value of goods.

Finance Ministry sanctions an additional Rs 15,000 cr to partially compensate state-owned oil firms for losses they incur on selling fuel below cost.

Petroleum Ministry to decide on taking action against RIL for falling gas output from the D6 gas fields in the KG-Basin in the next three-four weeks.

Ministry of Road Transport and Highways has asked NHAI and states to strictly adopt e-tendering system for better transparency in highways projects.

Government decides to ask the LIC to consider picking up 10% stake in Kingfisher Airlines.

Government invites proposals from bankers and financial institutions to advise on the outright stake sale in Tyre Corp of India.

Cabinet likely to decide by end of November the price of ethanol to be sold to state-owned oil marketing companies for blending with petrol.

Government plans to bring IFCI Ltd under its direct control by converting its loans into equity.

CBEC serves a Rs 2,075 cr tax notice on Deposit Insurance and Credit Guarantee Corp towards payment of service tax for the last five years.

GovernmentGovernmentGovernmentGovernment

Coal Ministry will notify revised royalty rates on coal and lignite production early next year.

Government refuses to recognize six discoveries by RIL in its KG-D 6 block.

Government finalizes radiation emission guidelines for cellphones and towers.

Oil Ministry sanctions taking scrupulous action against RIL over natural gas output from its KG-D6 fields having fallen below the target.

Government says it is looking into complaints over alleged misuse of the Universal Service Obligation Fund by Tata Teleservices and Reliance Communications.

RegulatoryRegulatoryRegulatoryRegulatory

RBI Governor attributes the Indian rupee's sharp fall to global factors and said that the currency would reverse its course once the debt crisis in the Eurozone is resolved.

RBI eases the norms for investments by foreign institutional investors and non-resident Indians into infrastructure debt funds.

RBI issues guidelines to allow banks and NBFCs to sponsor infrastructure debt funds (IDFs); NBFCs trying to set up IDFs should have been operational for at least five years, should have minimum net owned funds of Rs.300cr and a capital adequacy ratio of 15%.

RBI withdraws the $100 mn limit on net foreign exchange supply arising out of rupee swap transactions that banks undertake on behalf of customers.

RBI hiked the limit on the all-in-cost rate on external commercial borrowings of companies by 50 bps and said the proceeds of the loan should be credited in local bank accounts immediately for rupee expenditure.

RBI notified deregulation of savings bank deposit rates but said that the deregulation was applicable only on deposits held by Indian residents; the non-resident (external) accounts schemes and ordinary non-resident deposits will continue to be regulated till further review.

RBI deregulates interest rate on savings accounts in Regional Rural Banks.

RBI allows direct access of the NDS- OM platform to urban co-operative banks to widen participation in the government bond market.

RBI reiterates that all state and central co-operative banks are barred from crediting "account payee" cheques to the account of any person other than the payee named therein.

RegulatoryRegulatoryRegulatoryRegulatory

RBI approves extension of the tenure of loans to troubled state-run carrier Air India to 15 years from 10 years.

Security Appellate Tribunal sets aside a SEBI order to penalise the promoters of Gujarat NRE Coke in an insider trading case.

SEBI says private equity and venture capital funds will not be clubbed with promoters; a move which will lend greater flexibility to these financial investors as well as companies planning to mop-up funds.

SEBI specifies a maximum tenure of 12 months for warrants issued along with public issues or rights issue of securities, to prevent any misuse of such instruments.

SEBI set a minimum allotment size of Rs 5 cr for issuing shares in an initial public offer to "anchor" or cornerstone investors.

SEBI increase the net worth requirement of debenture trustees from existing Rs 1 cr to Rs 2 cr.

SEBI will allocate the enhanced foreign institutional investor limits in government and corporate debt via auction on Nov 30.

IRDA proposes to open up a bancassurance distribution channel, where banks would be allowed to tie up with one set of insurance companies, in one state.

IRDA tightens rules for web portals selling insurance products; says websites can’t display ratings, rankings, endorsements or bestsellers of insurance products.

RegulatoryRegulatoryRegulatoryRegulatory

IRDA says users of mobile phones with internet connectivity can now compare insurance products and premium rates on their devices.

An interim order by the Delhi High Court forces SEBI to put on hold its practice of issuing consent orders to settle securities market violations.

TDSAT directs Vodafone to deposit half of the Rs.50cr penalty imposed on it by the telecom department regarding a case of issuing bulk SIM cards without proper verification.

DoT rejects TRAI’s proposal for liberal M&A rules to make consolidation easier in the ultracompetitive market.

Income Tax department has doubts over the authenticity of the list of Swiss bank account holders it obtained from the French government three months ago.

CBI conducts searches at Vodafone's Indian unit and Bharti Airtel's offices seeking details on spectrum allocation by the government to operators between 2001-02.

CommoditiesCommoditiesCommoditiesCommodities

Crude oil prices fell in the week primarily on the back of weak economic data from Europe, China and the US and concerns that Middle East trouble could disrupt supplies; prices ended at $96.96 a barrel on the NYMEX on November 24 as compared to $98.82 a barrel on November 17.

US crude oil inventories fell 6.2mn barrels to 330.8mn barrels for the week ended Nov 18.

Indian gold prices gave up its earlier gains and ended lower at Rs 28,414 per 10 gm in the week ended November 25 due to profit taking and on sustained selling by stockists driven by a weakening global trend.

Silver prices too fell at Rs 55,200 per kg in domestic market during the week ended November 25 due to speculative sell-off following reduced industrial offtake.

The government likely to scrap its plan to announce a bonus of Rs. 80 per 100 kg on paddy procurement as it is robust so far and exports are ensuring good price to farmers.

Trade secretary says that government is considering cut in basmati export floor price.

MCX to launch gold petal futures on November 23.

28

Indian EquityIndian EquityIndian EquityIndian Equity

2929

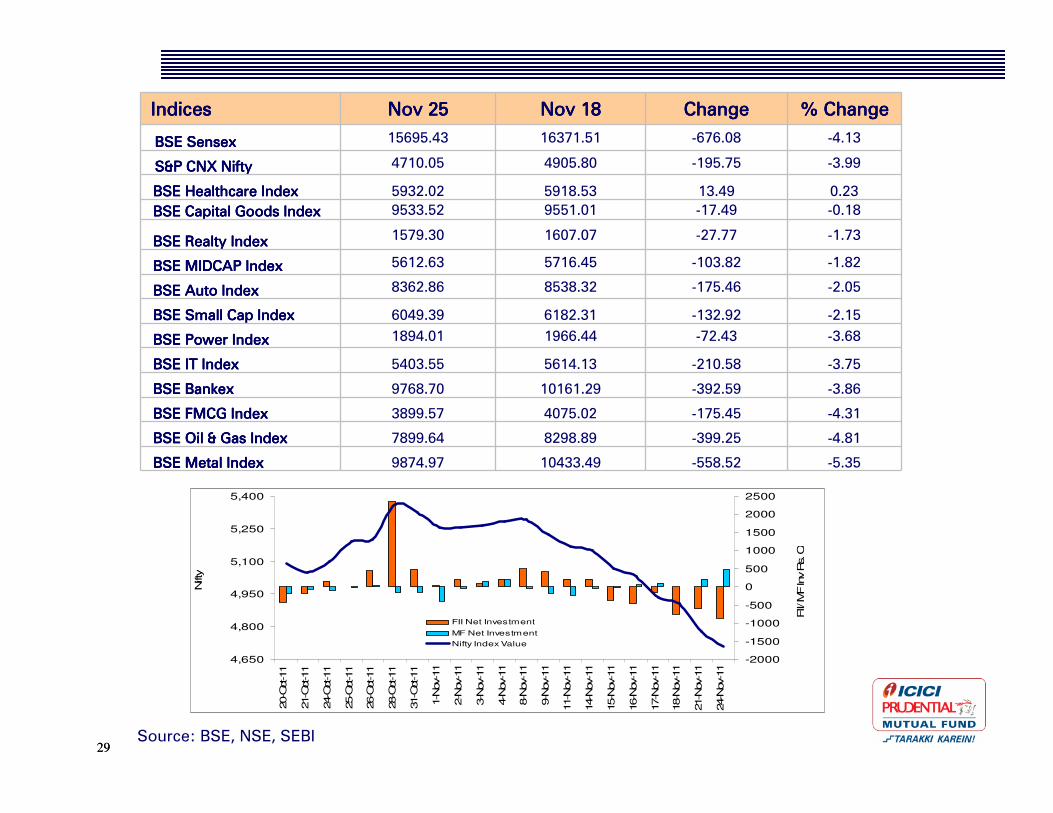

IndicesIndicesIndicesIndices Nov 25Nov 25Nov 25Nov 25 Nov 18Nov 18Nov 18Nov 18 ChangeChangeChangeChange % Change% Change% Change% Change

BSE SensexBSE SensexBSE SensexBSE Sensex 15695.43 16371.51 -676.08 -4.13

S&P CNX NiftyS&P CNX NiftyS&P CNX NiftyS&P CNX Nifty 4710.05 4905.80 -195.75 -3.99

BSE Healthcare IndexBSE Healthcare IndexBSE Healthcare IndexBSE Healthcare Index 5932.02 5918.53 13.49 0.23

BSE Capital Goods IndexBSE Capital Goods IndexBSE Capital Goods IndexBSE Capital Goods Index 9533.52 9551.01 -17.49 -0.18

BSE Realty IndexBSE Realty IndexBSE Realty IndexBSE Realty Index 1579.30 1607.07 -27.77 -1.73

BSE MIDCAP IndexBSE MIDCAP IndexBSE MIDCAP IndexBSE MIDCAP Index 5612.63 5716.45 -103.82 -1.82

BSE Auto IndexBSE Auto IndexBSE Auto IndexBSE Auto Index 8362.86 8538.32 -175.46 -2.05

BSE Small Cap IndexBSE Small Cap IndexBSE Small Cap IndexBSE Small Cap Index 6049.39 6182.31 -132.92 -2.15

BSE Power IndexBSE Power IndexBSE Power IndexBSE Power Index 1894.01 1966.44 -72.43 -3.68

BSE IT IndexBSE IT IndexBSE IT IndexBSE IT Index 5403.55 5614.13 -210.58 -3.75

BSE BankexBSE BankexBSE BankexBSE Bankex 9768.70 10161.29 -392.59 -3.86

BSE FMCG IndexBSE FMCG IndexBSE FMCG IndexBSE FMCG Index 3899.57 4075.02 -175.45 -4.31

BSE Oil & Gas IndexBSE Oil & Gas IndexBSE Oil & Gas IndexBSE Oil & Gas Index 7899.64 8298.89 -399.25 -4.81

BSE Metal IndexBSE Metal IndexBSE Metal IndexBSE Metal Index 9874.97 10433.49 -558.52 -5.35

Source: BSE, NSE, SEBI

4,650

4,800

4,950

5,100

5,250

5,400

20-O

ct-11

21-O

ct-11

24-O

ct-11

25-O

ct-11

26-O

ct-11

28-O

ct-11

31-O

ct-11

1-N

ov-1

1

2-N

ov-1

1

3-N

ov-1

1

4-N

ov-1

1

8-N

ov-1

1

9-N

ov-1

1

11-N

ov-1

1

14-N

ov-1

1

15-N

ov-1

1

16-N

ov-1

1

17-N

ov-1

1

18-N

ov-1

1

21-N

ov-1

1

24-N

ov-1

1

Nifty

-2000

-1500

-1000

-500

0

500

1000

1500

2000

2500

FII/ M

F Inv R

s. Cr

FII Net Investment

MF Net Investment

Nifty Index Value

3030

Indian EquityIndian EquityIndian EquityIndian Equity

Indian benchmark indices fell over 4% in the week, weighed down mainly by weak global sentiments.

Weak global cues came in the form of dip in overseas equities due to persisting Eurozone crisis as well as a downward revision in the US GDP growth in the third quarter.

Concerns over high domestic inflation, depreciating rupee, slowing domestic growth and lack of policy reforms also dragged down the markets.

Market fell further later, mirroring weak Asian markets, after Fitch ratings cut Portugal's credit rating to junk status.

More losses were witnessed after investors pared their positions ahead of the November futures contract expiry; though some losses were recovered after some investors covered their short positions.

All the BSE sectoral indices, except BSE Healthcare Index, ended in the red in the week.

BSE healthcare Index ended marginally higher as investors took some defensive bets amid current market volatility.

BSE Metal Index was the biggest decliner, down 5.4%, as traders dumped shares of companies in the sector after metal prices slumped on the London Metal Exchange due to weak economic data from China; Jindal Steel and SAIL emerged among the topmost individual decliners, down 9-12%.

31

Domestic F&O UpdateDomestic F&O UpdateDomestic F&O UpdateDomestic F&O Update

3232

Domestic F&O Update

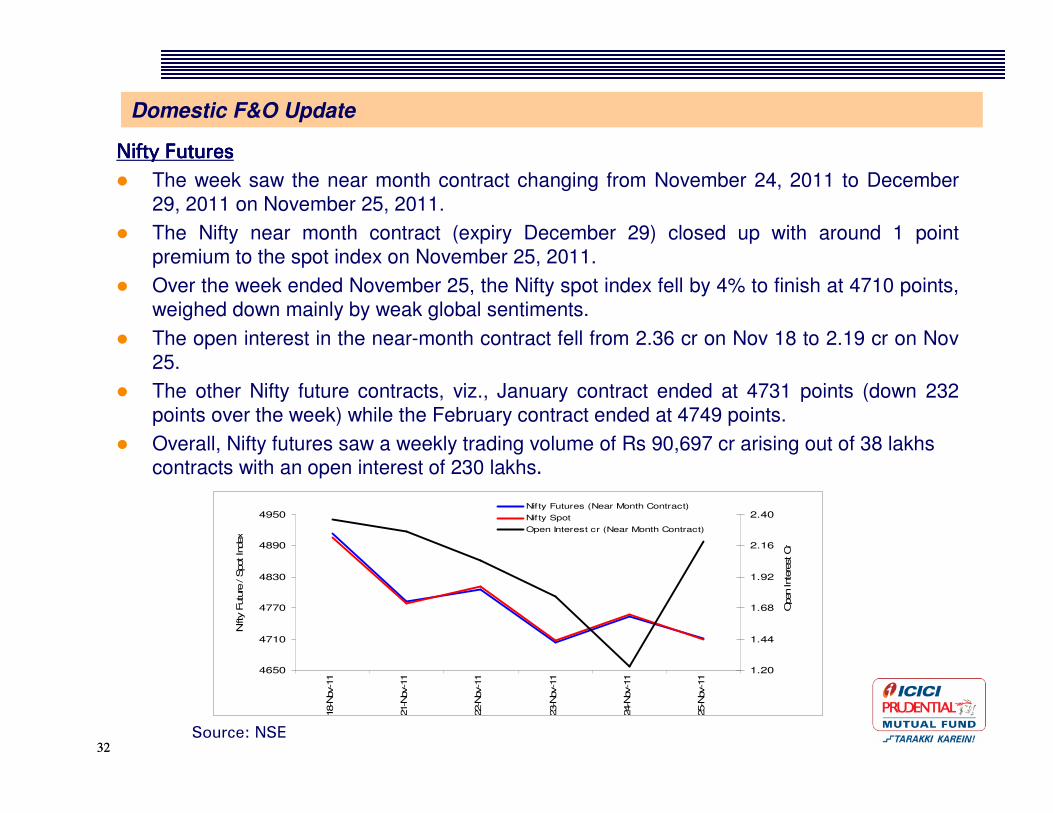

Nifty FuturesNifty FuturesNifty FuturesNifty Futures

The week saw the near month contract changing from November 24, 2011 to December

29, 2011 on November 25, 2011.

The Nifty near month contract (expiry December 29) closed up with around 1 point

premium to the spot index on November 25, 2011.

Over the week ended November 25, the Nifty spot index fell by 4% to finish at 4710 points,

weighed down mainly by weak global sentiments.

The open interest in the near-month contract fell from 2.36 cr on Nov 18 to 2.19 cr on Nov

25.

The other Nifty future contracts, viz., January contract ended at 4731 points (down 232

points over the week) while the February contract ended at 4749 points.

Overall, Nifty futures saw a weekly trading volume of Rs 90,697 cr arising out of 38 lakhs contracts with an open interest of 230 lakhs.

Source: NSE

4650

4710

4770

4830

4890

4950

18-N

ov-1

1

21-N

ov-1

1

22-N

ov-1

1

23-N

ov-1

1

24-N

ov-1

1

25-N

ov-1

1

Nifty

Futu

re / S

pot In

dex

1.20

1.44

1.68

1.92

2.16

2.40

Open Inte

rest Cr

Nifty Futures (Near Month Contract)

Nifty Spot

Open Interest cr (Near Month Contract)

3333

Domestic F&O Update

Nifty Options Nifty Options Nifty Options Nifty Options

Nifty 5000 call witnessed the highest open interest of 69 lakhs on November 25; while Nifty

4700 call witnessed the highest increase in open interest of over 25 lakhs over the week

Nifty 4800 garnered the highest number of contracts over the week at 37 lakhs.

For put options, Nifty 4500 put witnessed the highest open interest of over 95 lakhs on

November 25; it also witnessed the highest increase in open interest of 21 lakhs over the

week.

Nifty 4700 put garnered the highest number of contracts over the week at over 40 lakhs.

Overall, options saw 291 lakh contracts getting traded at a notional value of Rs 7,06,120 cr during the week.

3434

Domestic F&O Update

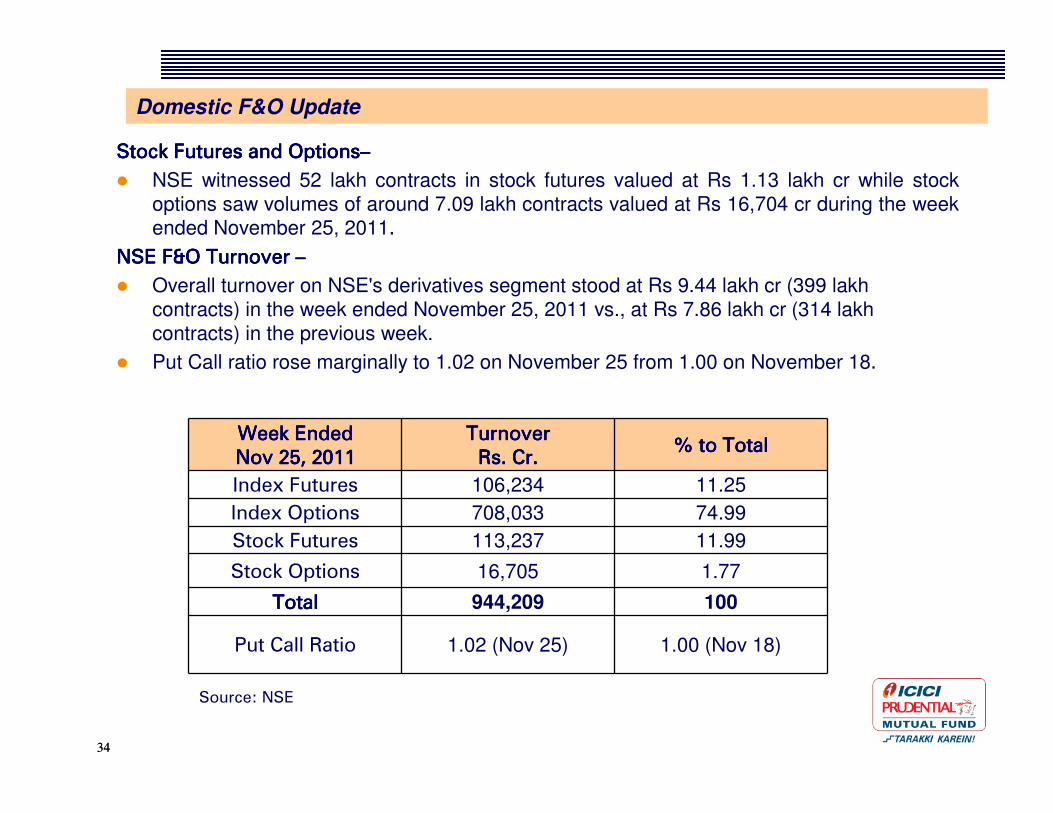

Stock Futures and OptionsStock Futures and OptionsStock Futures and OptionsStock Futures and Options––––

NSE witnessed 52 lakh contracts in stock futures valued at Rs 1.13 lakh cr while stock

options saw volumes of around 7.09 lakh contracts valued at Rs 16,704 cr during the week ended November 25, 2011.

NSE F&O Turnover NSE F&O Turnover NSE F&O Turnover NSE F&O Turnover ––––

Overall turnover on NSE's derivatives segment stood at Rs 9.44 lakh cr (399 lakh

contracts) in the week ended November 25, 2011 vs., at Rs 7.86 lakh cr (314 lakh

contracts) in the previous week.

Put Call ratio rose marginally to 1.02 on November 25 from 1.00 on November 18.

Week Ended Week Ended Week Ended Week Ended Nov 25, 2011Nov 25, 2011Nov 25, 2011Nov 25, 2011

TurnoverTurnoverTurnoverTurnoverRs. Cr.Rs. Cr.Rs. Cr.Rs. Cr.

% to Total% to Total% to Total% to Total

Index Futures 106,234 11.25

Index Options 708,033 74.99

Stock Futures 113,237 11.99

Stock Options 16,705 1.77

TotalTotalTotalTotal 944,209 100

Put Call Ratio 1.02 (Nov 25) 1.00 (Nov 18)

Source: NSE

3535

Domestic F&O Update

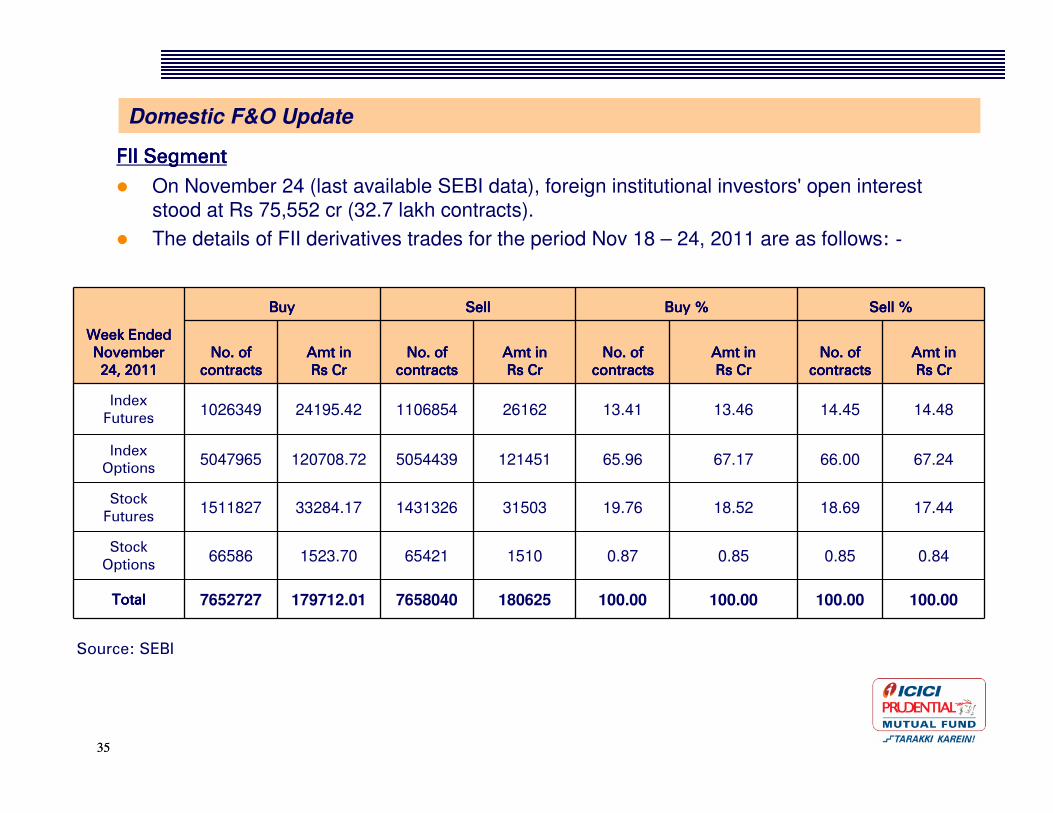

FII Segment FII Segment FII Segment FII Segment

On November 24 (last available SEBI data), foreign institutional investors' open interest

stood at Rs 75,552 cr (32.7 lakh contracts).

The details of FII derivatives trades for the period Nov 18 – 24, 2011 are as follows: -

Week Ended Week Ended Week Ended Week Ended November November November November 24, 201124, 201124, 201124, 2011

BuyBuyBuyBuy SellSellSellSell Buy %Buy %Buy %Buy % Sell %Sell %Sell %Sell %

No. of No. of No. of No. of contractscontractscontractscontracts

Amt in Amt in Amt in Amt in Rs CrRs CrRs CrRs Cr

No. of No. of No. of No. of contractscontractscontractscontracts

Amt in Amt in Amt in Amt in Rs CrRs CrRs CrRs Cr

No. of No. of No. of No. of contractscontractscontractscontracts

Amt in Amt in Amt in Amt in Rs CrRs CrRs CrRs Cr

No. of No. of No. of No. of contractscontractscontractscontracts

Amt in Amt in Amt in Amt in Rs CrRs CrRs CrRs Cr

Index Futures

1026349 24195.42 1106854 26162 13.41 13.46 14.45 14.48

Index Options

5047965 120708.72 5054439 121451 65.96 67.17 66.00 67.24

Stock Futures

1511827 33284.17 1431326 31503 19.76 18.52 18.69 17.44

Stock Options

66586 1523.70 65421 1510 0.87 0.85 0.85 0.84

TotalTotalTotalTotal 7652727 179712.01 7658040 180625 100.00 100.00 100.00 100.00

Source: SEBI

36

Indian DebtIndian DebtIndian DebtIndian Debt

Indian Debt

Indian call money rates fell in the week as high rates prompted banks to meet their reserve requirements from the RBI repo tender and CBLO markets.

The interbank rates finished the week at 8.60-8.65% on November 25 versus 8.85-8.90% on November 18; however rates were under pressure due to the start of the reporting fortnight amid tight liquidity condition in the system.

Indian gilts ended higher in the week on the backdrop of easing domestic inflationary worries, better than expected demand at weekly bond auctions and falling risk appetite due to weaker cues from US and Europe.

Major fillip for the bonds was provided after worries over the interest rate hike eased due to a fall in the weekly food inflation.

Reports in the media that India's fiscal deficit for 2011-12 is expected to be below 5.0% also supported gilt prices.

Gilts gained further due to better-than- expected demand at weekly Rs 13,000 cr bond auction.

The current 10-year benchmark 8.79% 2021 paper also rose in the week due to absence of fresh supply in the stock this week; yield on the benchmark fell to 8.81% on November 25 as compared with 8.83% on November 18

Sharp rise in gilt prices were however capped as sharp fall in the Indian rupee stoked inflationary concerns.

Further fall was also witnessed on fear that the government may have to further increase its market borrowing for current fiscal to fulfill second supplementary demand for grants.

After market hours on November 25, RBI announced auction of T-bills worth Rs 8,000 cr on November 30.

38

Forthcoming Economic IndicatorsForthcoming Economic IndicatorsForthcoming Economic IndicatorsForthcoming Economic Indicators

Forthcoming Economic Indicators

DayDayDayDay EventEventEventEvent

Monday, Nov 28Monday, Nov 28Monday, Nov 28Monday, Nov 28 • US New Home Sales, October

• Japan’s Jobless Rate, October

• Japan’s Retail Trade, October

Tuesday, Nov 29Tuesday, Nov 29Tuesday, Nov 29Tuesday, Nov 29 • US Consumer Confidence, November

• S&P Case Shiller Home Price Index, September

• US Nationwide House Prices, November

• Euro-Zone Consumer / Economic Confidence, November

• UK Net Consumer Credit, October

• Japan’s Industrial Production, October

• Japan’s Nomura/JMMA Manufacturing Purchasing Manager Index, November

Wednesday, Nov 30Wednesday, Nov 30Wednesday, Nov 30Wednesday, Nov 30 • ADP Employment Report, November

• US Fed's Beige Book, November

• US Productivity/costs data, Q3

• Chicago Purchasing Managers Index, November

• US Pending Home Sales, September

• US Crude Oil Inventories, November 25

• Euro-Zone Consumer Price Index Estimate, November

• Euro-Zone Unemployment Rate, October

• UK GfK Consumer Confidence Survey, November

• India’s GDP growth estimate for Jul-Sep

• India’s Core sector growth, October

• India’s Government finances, October

• India’s CPI for industrial workers, October

Thursday, Dec 1Thursday, Dec 1Thursday, Dec 1Thursday, Dec 1 • US Institute of Supply Management Mfg Index, November

• US Auto Sales, December

• US Construction Spending, October

• US Initial Jobless Claims, November 26

• Euro-Zone Purchasing Manager Index Manufacturing, November

• UK Purchasing Manager Index Manufacturing, November

• China’s Manufacturing PMI, November

• China’s HSBC Manufacturing PMI, November

• India’s Trade data, October

• India’s HSBC Manufacturing PMI, November

• India’s primary articles inflation, week ended November 19

Friday, Dec 2Friday, Dec 2Friday, Dec 2Friday, Dec 2 • US Nonfarm Payrolls, November

• US Unemployment Rate, November

• Euro-Zone Producer Price Index, October

• UK Purchasing Manager Index Construction, November

• India’s Forex Reserves, week ended November 25

40

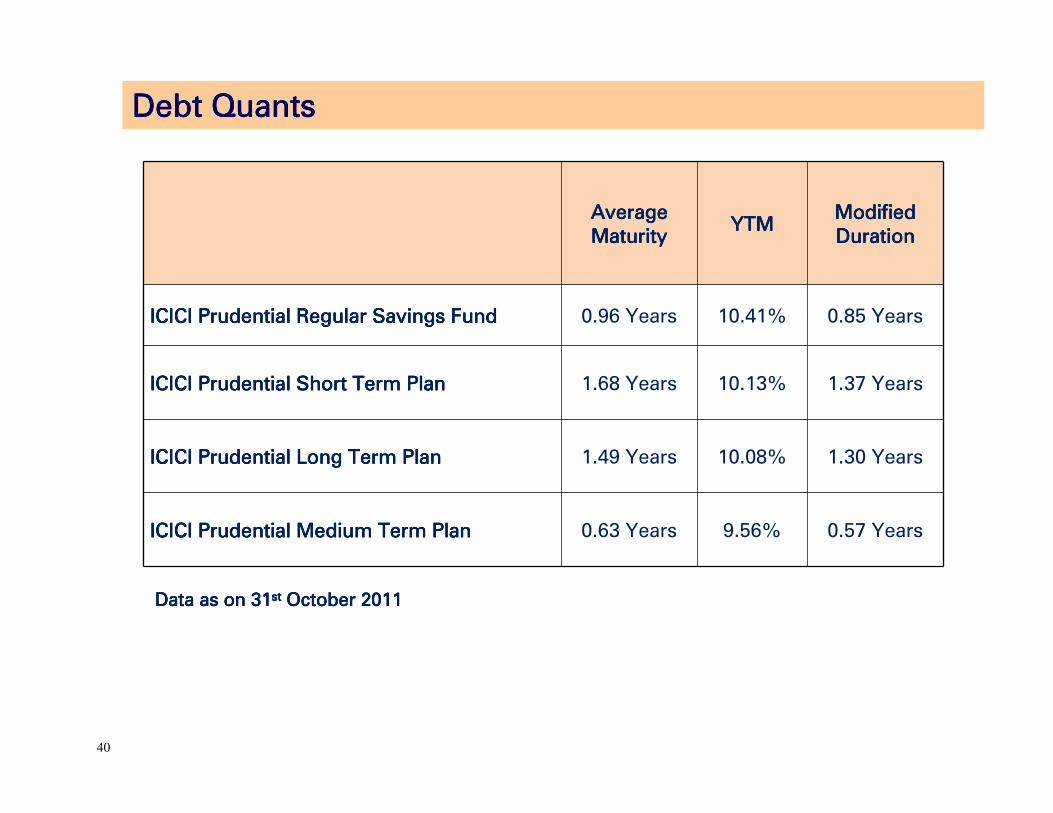

Debt QuantsDebt QuantsDebt QuantsDebt Quants

Average Average Average Average MaturityMaturityMaturityMaturity

YTMYTMYTMYTMModified Modified Modified Modified DurationDurationDurationDuration

ICICI Prudential Regular Savings FundICICI Prudential Regular Savings FundICICI Prudential Regular Savings FundICICI Prudential Regular Savings Fund 0.96 Years 10.41% 0.85 Years

ICICI Prudential Short Term PlanICICI Prudential Short Term PlanICICI Prudential Short Term PlanICICI Prudential Short Term Plan 1.68 Years 10.13% 1.37 Years

ICICI Prudential Long Term PlanICICI Prudential Long Term PlanICICI Prudential Long Term PlanICICI Prudential Long Term Plan 1.49 Years 10.08% 1.30 Years

ICICI Prudential Medium Term PlanICICI Prudential Medium Term PlanICICI Prudential Medium Term PlanICICI Prudential Medium Term Plan 0.63 Years 9.56% 0.57 Years

Data as on 31Data as on 31Data as on 31Data as on 31stststst October 2011October 2011October 2011October 2011

41

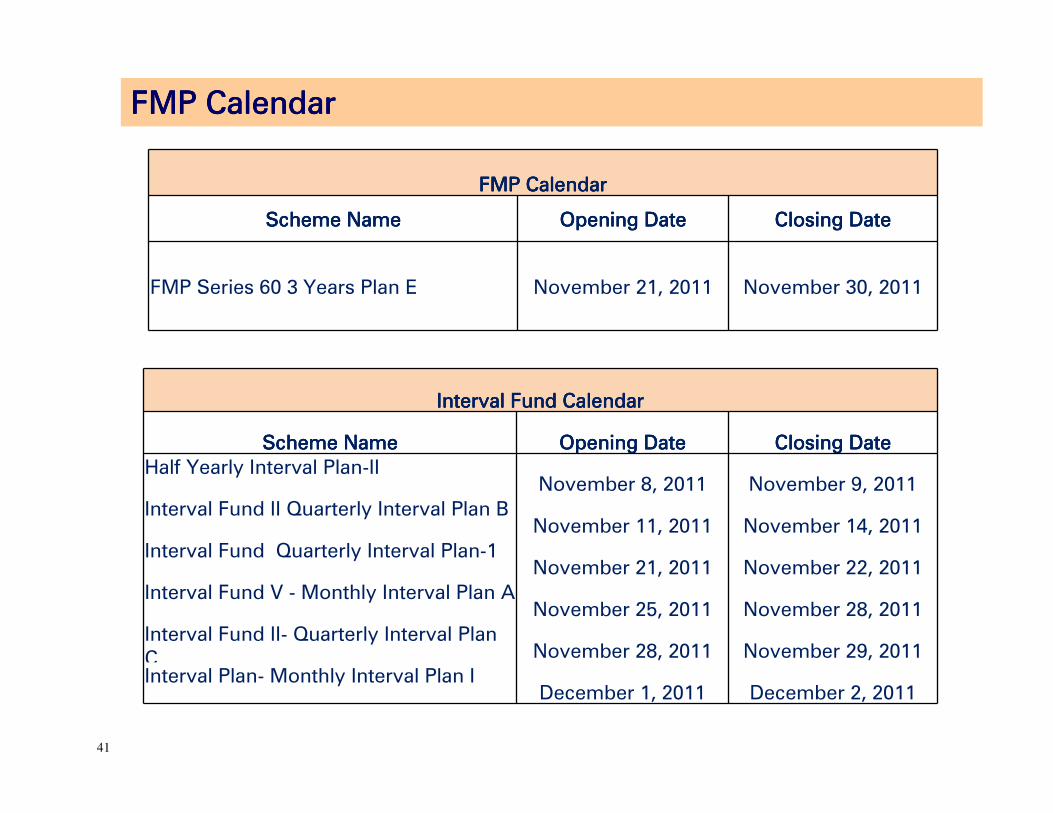

FMP CalendarFMP CalendarFMP CalendarFMP Calendar

FMP CalendarFMP CalendarFMP CalendarFMP Calendar

Scheme NameScheme NameScheme NameScheme Name Opening DateOpening DateOpening DateOpening Date Closing DateClosing DateClosing DateClosing Date

FMP Series 60 3 Years Plan E November 21, 2011 November 30, 2011

Interval Fund CalendarInterval Fund CalendarInterval Fund CalendarInterval Fund Calendar

Scheme NameScheme NameScheme NameScheme Name Opening DateOpening DateOpening DateOpening Date Closing DateClosing DateClosing DateClosing Date

Half Yearly Interval Plan-IINovember 8, 2011 November 9, 2011

Interval Fund II Quarterly Interval Plan BNovember 11, 2011 November 14, 2011

Interval Fund Quarterly Interval Plan-1November 21, 2011 November 22, 2011

Interval Fund V - Monthly Interval Plan ANovember 25, 2011 November 28, 2011

Interval Fund II- Quarterly Interval Plan C November 28, 2011 November 29, 2011

Interval Plan- Monthly Interval Plan IDecember 1, 2011 December 2, 2011

42

Statutory Disclaimers and Risk FactorsStatutory Disclaimers and Risk FactorsStatutory Disclaimers and Risk FactorsStatutory Disclaimers and Risk Factors

Statutory Details: Statutory Details: Statutory Details: Statutory Details: Settlor of ICICI Prudential Mutual Fund (IPMF): ICICI Bank Ltd. and Prudential plc; IPMF was set up as a Trust sponsored by the settlor in accordance with the provisions of Indian Trust Act, 1882. Trustee:Trustee:Trustee:Trustee: ICICI Prudential Trust Ltd. (IPTL); Investment Manager: Investment Manager: Investment Manager: Investment Manager: ICICI Prudential Asset Management Co. Ltd. (IPAMCL); IPTL & IPAMCL are incorporated under Companies Act, 1956. Liability:Liability:Liability:Liability: Liability of IPMF/Sponsors/IPTL/IPAMCL is limited to Rs. 22.2 lacs collectively. Past performance of the Sponsors, AMC, Fund, and Trustee has no bearing on the expected performance of the mutual fund or any of its schemes. Risk Factors: All investments in Risk Factors: All investments in Risk Factors: All investments in Risk Factors: All investments in Mutual Fund and securities are subject to market risks and the NMutual Fund and securities are subject to market risks and the NMutual Fund and securities are subject to market risks and the NMutual Fund and securities are subject to market risks and the NAV of the Schemes may go up or AV of the Schemes may go up or AV of the Schemes may go up or AV of the Schemes may go up or down, depending upon the factors and forces affecting the securidown, depending upon the factors and forces affecting the securidown, depending upon the factors and forces affecting the securidown, depending upon the factors and forces affecting the securities markets and there can be no ties markets and there can be no ties markets and there can be no ties markets and there can be no assurance that the fundassurance that the fundassurance that the fundassurance that the fund’’’’s objectives will be achieved. s objectives will be achieved. s objectives will be achieved. s objectives will be achieved.

ICICI Prudential Medium Term Plan ICICI Prudential Medium Term Plan ICICI Prudential Medium Term Plan ICICI Prudential Medium Term Plan (An open-ended income fund that intends to generate regular income through investments in debt and money market instruments with a view to provide regular dividend payments and a secondary objective of growth of capital. Exit load : Upto Mar 15,2012 from allotment - 0.50% of applicable NAV, After Mar 15,2012 – Nil

ICICI Prudential Short Term Plan ICICI Prudential Short Term Plan ICICI Prudential Short Term Plan ICICI Prudential Short Term Plan (An open-ended Income Fund. is an additional Plan under the existing ICICI Prudential Income Plan with characteristics similar to ICICI Prudential Income Plan. The objective of the Plan is to generate income through investments in a range of debt and money market instruments of various maturities with a view to maximizing income while maintaining the optimum balance of yield, safety and liquidity, Exit Load: (i) If the amount, sought to be redeemed or switched out is invested for a period of upto 6 month from the date of allotment – 0.5% of applicable Net Asset Value; (ii) If the amount, sought to be redeemed or switched out is invested for a period of more than 6 months from the date of allotment – Nil

Statutory Disclaimers and Risk FactorsStatutory Disclaimers and Risk FactorsStatutory Disclaimers and Risk FactorsStatutory Disclaimers and Risk Factors

ICICI Prudential Long Term Plan ICICI Prudential Long Term Plan ICICI Prudential Long Term Plan ICICI Prudential Long Term Plan (An open-ended Income Fund. Objective is to generate income through investments in a range of debt and money market instruments of various maturities with a view to maximising income while maintaining the optimum balance of yield, safety and liquidity. Exit load: (i) If the amount, sought to be redeemed or switched out is invested for a period of upto one year from the date of allotment – 0.75% of applicable Net Asset Value; (ii) If the amount, sought to be redeemed or switched out is invested for a period of more than one year from the date of allotment – Nil.

ICICI Prudential Regular Savings Fund ICICI Prudential Regular Savings Fund ICICI Prudential Regular Savings Fund ICICI Prudential Regular Savings Fund (IPRSF) is an open-ended income fund that intends to provide reasonable returns, by maintaining an optimum balance of safety, liquidity and yield, through investments in a basket of debt and money market instruments with a view to delivering consistent performance. However, there can be no assurance that the investment objective of the Scheme will be realized. Exit load: (i) If the amount, sought to be redeemed or switched out is invested for a period of upto 15 months from the date of allotment – 2% of applicable Net Asset Value; (ii) If the amount, sought to be redeemed or switched out is invested for a period of more than 1 Year from the date of allotment – Nil.

ICICI Prudential Interval Fund ICICI Prudential Interval Fund ICICI Prudential Interval Fund ICICI Prudential Interval Fund ---- ICICI Prudential Interval Fund ICICI Prudential Interval Fund ICICI Prudential Interval Fund ICICI Prudential Interval Fund ---- Half Yearly Interval PlanHalf Yearly Interval PlanHalf Yearly Interval PlanHalf Yearly Interval Plan----II; ICICI II; ICICI II; ICICI II; ICICI Prudential Interval Fund Prudential Interval Fund Prudential Interval Fund Prudential Interval Fund ---- Monthly lnterval PlanMonthly lnterval PlanMonthly lnterval PlanMonthly lnterval Plan----I; ICICI Prudential Interval Fund I; ICICI Prudential Interval Fund I; ICICI Prudential Interval Fund I; ICICI Prudential Interval Fund ---- Quarterly Quarterly Quarterly Quarterly lnterval Planlnterval Planlnterval Planlnterval Plan----I; ICICI Prudential Interval Fund II I; ICICI Prudential Interval Fund II I; ICICI Prudential Interval Fund II I; ICICI Prudential Interval Fund II ---- Quarterly lnterval PlanQuarterly lnterval PlanQuarterly lnterval PlanQuarterly lnterval Plan B, Quarterly lnterval B, Quarterly lnterval B, Quarterly lnterval B, Quarterly lnterval PlanPlanPlanPlan C; ICICI Prudential Interval Fund V C; ICICI Prudential Interval Fund V C; ICICI Prudential Interval Fund V C; ICICI Prudential Interval Fund V ---- Monthly lnterval Plan A: (A Debt Oriented Interval Monthly lnterval Plan A: (A Debt Oriented Interval Monthly lnterval Plan A: (A Debt Oriented Interval Monthly lnterval Plan A: (A Debt Oriented Interval Scheme.Scheme.Scheme.Scheme. The investment objective of the Scheme is to generate optimal returns consistent with moderate levels of risk and liquidity by investing in debt securities and money market securities.

43

Statutory Disclaimers and Risk FactorsStatutory Disclaimers and Risk FactorsStatutory Disclaimers and Risk FactorsStatutory Disclaimers and Risk Factors

ICICI Prudential Fixed Maturity Plan ICICI Prudential Fixed Maturity Plan ICICI Prudential Fixed Maturity Plan ICICI Prudential Fixed Maturity Plan ---- ICICI Prudential Fixed Maturity Plan ICICI Prudential Fixed Maturity Plan ICICI Prudential Fixed Maturity Plan ICICI Prudential Fixed Maturity Plan ---- Series 60 Series 60 Series 60 Series 60 –––– 3 Years Plan E: (Close3 Years Plan E: (Close3 Years Plan E: (Close3 Years Plan E: (Close----

ended Debt Fund) ended Debt Fund) ended Debt Fund) ended Debt Fund) The investment objective of the Plans under the Scheme is to seek to generate regular returns by investing in a portfolio of fixed income securities/ debt instruments which mature on or before the date of maturity of the Plan/Scheme. Entry Load: Entry Load: Entry Load: Entry Load: Not Applicable; Exit Load: Exit Load: Exit Load: Exit Load: Since the Plan will be listed on the stock exchange, load will not be applicable. Terms of Issue: Terms of Issue: Terms of Issue: Terms of Issue: Offer of Units of Rs. 10 each during the New Fund Offer (NFO) period. Units can be purchased during NFO period only Repurchase facility: Repurchase facility: Repurchase facility: Repurchase facility: No redemption/repurchase of units shall be allowed prior to the maturity of this close ended scheme. Investors wishing to exit may do so, only in demat mode, by selling through Bombay Stock Exchange of India Ltd. or any of the stock exchange(s) where the scheme will be listed as the Trustee may decide from time to time. Investments in the Plans under the Scheme may be affected by risInvestments in the Plans under the Scheme may be affected by risInvestments in the Plans under the Scheme may be affected by risInvestments in the Plans under the Scheme may be affected by risks relating to trading volumes, settlement ks relating to trading volumes, settlement ks relating to trading volumes, settlement ks relating to trading volumes, settlement periods, interest rate, liquidity or marketability, credit, reinperiods, interest rate, liquidity or marketability, credit, reinperiods, interest rate, liquidity or marketability, credit, reinperiods, interest rate, liquidity or marketability, credit, reinvestment, regulatory, investment in unlisted vestment, regulatory, investment in unlisted vestment, regulatory, investment in unlisted vestment, regulatory, investment in unlisted securities, default risk including the possible loss of principasecurities, default risk including the possible loss of principasecurities, default risk including the possible loss of principasecurities, default risk including the possible loss of principal, investment in securitised instruments and risk l, investment in securitised instruments and risk l, investment in securitised instruments and risk l, investment in securitised instruments and risk of coof coof coof co----mingling etc. Unitholder Information & General Services:mingling etc. Unitholder Information & General Services:mingling etc. Unitholder Information & General Services:mingling etc. Unitholder Information & General Services: IPAMCL shall as per the Regulations from the closure of the NFO Period will - (a) send account statement, indicating the number of unit allotted, (by ordinary post or by email, wherever the email id is provided) to the unit holder (b) calculate and disclose the first and subsequent NAV at the close of every Business Day. NAV shall be published in at least in 2 daily newspapers on daily basis. Application forms can be submitted at customer service centers, during NFO. In the event of inordinately large number of redemption requests or of restructuring of the Scheme’s investment portfolio, the trustees reserve the right in their sole discretion to limit the redemptions (including suspending redemptions) under certain circumstances. The Scheme (at the portfolio level) should have atleast 20 investors and no investor on the date of allotment should account for more than 25% of the corpus of the Scheme; or IPAMCL shall comply with the specified SEBI guidelines in this regard. For application form and copies of SID, SAI and Key Information Memorandum, contact your financial advisor or log onto www.icicipruamc.com or visit any of the branches of IPAMCL

44

45

Statutory Disclaimers and Risk FactorsStatutory Disclaimers and Risk FactorsStatutory Disclaimers and Risk FactorsStatutory Disclaimers and Risk Factors

BSE Disclaimer:BSE Disclaimer:BSE Disclaimer:BSE Disclaimer: It is to be distinctly understood that the permission given by BSE should not in any way be deemed or construed that the SID has been cleared or approved by BSE nor does it certify the correctness or completeness of any of the contents of the Draft SID. Investors are advised to refer to the SID for the full text of the Disclaimer clause of the BSE.

However, there is no assurance or guarantee that the objectives However, there is no assurance or guarantee that the objectives However, there is no assurance or guarantee that the objectives However, there is no assurance or guarantee that the objectives of the abovementioned of the abovementioned of the abovementioned of the abovementioned Schemes will be achieved.Schemes will be achieved.Schemes will be achieved.Schemes will be achieved.

Scheme specific risk factors for Debt Scheme specific risk factors for Debt Scheme specific risk factors for Debt Scheme specific risk factors for Debt ---- Investments in the schemes may be affected by trading Investments in the schemes may be affected by trading Investments in the schemes may be affected by trading Investments in the schemes may be affected by trading volumes, settlement periods, volatility, price fluctuations, liqvolumes, settlement periods, volatility, price fluctuations, liqvolumes, settlement periods, volatility, price fluctuations, liqvolumes, settlement periods, volatility, price fluctuations, liquidity risks, derivative risk, market uidity risks, derivative risk, market uidity risks, derivative risk, market uidity risks, derivative risk, market risk, risk relating to fluctuations in foreign exchange for inverisk, risk relating to fluctuations in foreign exchange for inverisk, risk relating to fluctuations in foreign exchange for inverisk, risk relating to fluctuations in foreign exchange for investments in foreign securities, stments in foreign securities, stments in foreign securities, stments in foreign securities, lending & borrowing risks, credit & interest rate risks relatinglending & borrowing risks, credit & interest rate risks relatinglending & borrowing risks, credit & interest rate risks relatinglending & borrowing risks, credit & interest rate risks relating to debt investment. to debt investment. to debt investment. to debt investment.

The aforesaid are only the names of the schemes and do not in anThe aforesaid are only the names of the schemes and do not in anThe aforesaid are only the names of the schemes and do not in anThe aforesaid are only the names of the schemes and do not in any manner indicate either the y manner indicate either the y manner indicate either the y manner indicate either the quality of the Schemes or their future prospects and returns. Muquality of the Schemes or their future prospects and returns. Muquality of the Schemes or their future prospects and returns. Muquality of the Schemes or their future prospects and returns. Mutual Fund investments are tual Fund investments are tual Fund investments are tual Fund investments are subject to market risks. Please read the Statement of Additionalsubject to market risks. Please read the Statement of Additionalsubject to market risks. Please read the Statement of Additionalsubject to market risks. Please read the Statement of Additional Information and Scheme Information and Scheme Information and Scheme Information and Scheme Information Document carefully before investingInformation Document carefully before investingInformation Document carefully before investingInformation Document carefully before investing

The stock (s)/sectors mentioned in this presentation do not constitute any recommendation of the same and the schemes of the Fund may or may not have any future position in these stock's)/sectors. In the preparation of the material contained in this document. All figures, indicative yields, tax rates, returns, indexation cost and other data assumed in the preparation of this document is dated. The same may or may not be relevant at a future date Prospective investors are therefore advised to consult their own legal, tax and financial advisors to determine possible tax, legal and other financial implication or consequence of subscribing to the units of the schemes of the Fund.

Statutory Disclaimers and Risk FactorsStatutory Disclaimers and Risk FactorsStatutory Disclaimers and Risk FactorsStatutory Disclaimers and Risk Factors

Source of the data in this presentation is CRISIL: Source of the data in this presentation is CRISIL: Source of the data in this presentation is CRISIL: Source of the data in this presentation is CRISIL: CRISIL Research, a division of CRISIL Limited

(CRISIL) has taken due care and caution in preparing this Report based on the information obtained by CRISIL from sources which it considers reliable (Data). However, CRISIL does not guarantee the accuracy, adequacy or completeness of the Data / Report and is not responsible for any errors or omissions or for the results obtained from the use of Data / Report. This Report is not a recommendation to invest / disinvest in any company covered in the Report. CRISIL especially states that it has no financial liability whatsoever to the subscribers/ users/ transmitters/ distributors of this Report. CRISIL Research operates independently of, and does not have access to information obtained by CRISIL’s Ratings Division / CRISIL Risk and Infrastructure Solutions Limited (CRIS), which may, in their regular operations, obtain information of a confidential nature. The views expressed in this Report are that of CRISIL Research and not of CRISIL’s Ratings Division / CRIS. No part of this Report may be published / reproduced in any form without CRISIL’s prior written approval.

46

Statutory Disclaimers and Risk FactorsStatutory Disclaimers and Risk FactorsStatutory Disclaimers and Risk FactorsStatutory Disclaimers and Risk Factors

Disclaimer:Disclaimer:Disclaimer:Disclaimer: ICICI Prudential Mutual Fund (the Fund) has used information that is publicly available, including information developed in-house. Some of the material used in the document may have been obtained from members/persons other than the Fund and/or its affiliates and which may have been made available to the Fund and/or to its affiliates. Information gathered and material used in this document is believed to be from reliable sources. The Fund however does not warrant the accuracy, reasonableness and/or completeness of any information. For data reference to any third party in this material no such party will assume any liability for the same. All recipients of this material should before dealing and or transacting in any of the products referred to in this material make their own investigation, seek appropriate professional advice and carefully read the scheme information document. We have included statements/opinions/recommendations in this document, which contain words, or phrases such as “will”, “expect”, “should”, “believe” and similar expressions or variations of such expressions, that are “forward looking statements”. Actual results may differ materially from those suggested by the forward looking statements due to risk or uncertainties associated with our expectations with respect to, but not limited to, exposure to market risks, general economic and political conditions in India and other countries globally, which have an impact on our services and / or investments, the monitory and interest policies of India, inflation, deflation, unanticipated turbulence in interest rates, foreign exchange rates, equity prices or other rates or prices, the performance of the financial markets in India and globally, changes in domestic and foreign laws, regulations and taxes and changes in competition in the industry. All data/information used in the preparation of this material is dated and may or may not be relevant any time after the issuance of this material. The AMC takes no responsibility of updating any data/information in this material from time to time. For Scheme Information Document and Key Information Memorandum, contact your financial advisor or log onto www.icicipruamc.com or visit any of the branches of the AMC.

The AMC (including its affiliates), the Fund and any of its officers directors, personnel and employees, shall not liable for any loss, damage of any nature, including but not limited to direct, indirect, punitive, special, exemplary, consequential, as also any loss of profit in any way arising from the use of this material in any manner. The recipient alone shall be fully responsible/are liable for any decision taken on the basis of this material

47

48

Thank youThank youThank youThank you