Embed Size (px)

Citation preview

WEBINAR: “How to Create a Robust and Credible Materiality Analysis?”

10 April 2014, 15:00 -16:00 CET

The webinar will start shortly. We are waiting for all the participants to join…

Technical information

• During the webinar, you will be on mute to minimize audio noise.

• If you have trouble hearing or have any technical problems it often helps to refresh the link or to log in again

• During the presentation, if you have any questions/feedback, please use the “chat” function or email Erika Eriksson at [email protected]

Further information can be found in the webinar login guide

Webinar Objectives

To provide first hand information on:

- How to start a materiality analysis process

- What are main challenges to anticipate

- What are opportunities to grab

- What could be tricks to make it all work

Agenda Time Agenda point Speaker

10 min 1. Welcome and Introduction Aron Horvath Project manager, CSR Europe

15 min 2. How to Create a Robust and Credible Materiality Analysis framework? – the AA1000 experience

David Pritchett Head of Europe, AccountAbility

20 min 3. What are main challenges, opportunities and tricks in materiality analysis? - view from the practice

Rebecca Wilkinson CR Report Manager, State Street Cora Olsen ESG Data manager Global TBL Management, Novo Nordisk

15 min Discussion Round, Q&A and closing Aron Horvath Project manager, CSR Europe

1.Welcome and Introduction Aron Horvath Project manager, CSR Europe

6

CSR Europe`s flagship initiative, Enterprise

2020 is the only business-driven initiative

supporting the EU`s CSR Strategy

Materiality Analysis: Key Starting Point of True Value Creation for Future Market Value

Virtuous cycle of an integrated approach

2013 marks the convergence of guidelines and legislation on fostering and mainstreaming more integrated thinking and reporting

True market value of a company is expressed in both financial and non-financial performance

Management

Performance & Reporting

Materiality Analysis / due diligence on

risks & opportunities

Strategy

Re-evaluation & Stakeholder Engagement

Scaling up solutions

Generic Materiality Analysis Process

Stakeholder expectations

2) Capturing stakeholder expectations

A) Stakeholder mapping

B) Issue identification

First draft of matrix by company management

3) Management agreement on first

draft matrix

C) Internal issue prioritization

D) Materiality matrix preparation

External validation

4) Check with key stakeholders

E) Stakeholder dialogue

5) M

ateriality m

atrix &

use

of it

1)

Pu

rpo

se a

nd

Sco

pe

of

Mat

eri

alit

y A

sse

ssm

en

t

1) Define purpose (informing sustainability strategy or reporting) and scope (local, regional, group level)

2) Capture the expectations of a well-defined group of stakeholders through stakeholder consultation

3) Boil down issues identified into a draft materiality matrix or other 4) Validate it through preferably external stakeholder dialogues 5) Update matrix or other with validated material issues

2. How to Create a Robust and Credible Materiality Analysis framework? David Pritchett Head of Europe, AccountAbility

Dubai London New York Riyadh Zurich

Create a Robust and Credible

Materiality Analysis Framework

April 2014

Leading Actors

11

GRI: 4th generation of

Sustainability Reporting

Guidelines, “G4”

IIRC: Consultation draft on the

Integrated Reporting Framework

SASB: Industry-based materiality

standards

GISR: Global sustainability

ratings standard

Public policy initiatives:

European Commission

Stock exchanges / listing

standards: Sustainable Stock

Exchange Initiative

Recent AccountAbility research questions

12

How engaged is your

organization in the following

global reporting and non-

financial materiality

initiatives?

How engaged are leaders

from the following levels at

your organization with non-

financial material issues?

AccountAbility’s Pioneering Materiality Framework

13

AccountAbility has worked in the area of Materiality since its inception in 1995, doing in depth analysis

and extensive research on the topic and creating the Materiality Framework below helping many

companies better understand and successfully integrate their ESG issues into their business strategy and

performance:

Source: The Materiality Report: Aligning Strategy,

Performance, and Reporting, AccountAbility, 2006.

AccountAbility’s Materiality Approach - and some questions

14

Plan •How do we ensure we are engaging with a fair and representative selection of stakeholders?

•How do we effectively manage the expectations from stakeholders of what will be delivered

during the engagement process?

•How do we integrate existing processes and meet the needs of different business units?

Identify

Prioritize

Review

Embed

•How do we decide on the granularity or time horizons of the issues?

•What sources should we best use to identify the material issues?

•What internal and external criteria should we use to determine material issues?

•What thresholds should we set in order to generate valuable results?

•Who should be involved in the review process, and how often does the whole determination

approach need to be reviewed?

•How do we manage conflicting internal and external views?

•How do we effectively align and integrate materiality determination into our existing core

business and decision-making processes?

•What is the value of obtaining external assurance over the process?

AccountAbility’s approach to materiality discovers and validates issues that are most relevant to the business,

important to internal and external stakeholders, and that the company can have the greatest impact on. Our

tested methodology addresses the following questions:

AccountAbility

Standards – we provide

the secretariat for the

AA1000 AccountAbility

Principles Standard,

AA1000 Assurance

Standard & AA1000

Stakeholder

Engagement Standard

Redefining

Materiality II: Why it

Matters, Who’s

Involved, and What It

Means for Corporate

Leaders and Boards

describes the

landscape of various

global materiality

initiatives and provides

a framework for

corporate leaders and

boards to enhance the

definition and

management of non-

financial materiality.

Critical Friends

examines the

experience of

businesses convening

stakeholder panels

made up of external

experts or stakeholder

representatives, to help

strengthen their

strategy, performance

and accountability in

relation to sustainability.

The Stakeholder

Engagement Manual

Volume I and II – The

Practitioners'

Handbook on

Stakeholder

Engagement forms a

best practice guide to

stakeholder engagement

developed in

collaboration with UNEP,

providing guidance to

corporate and non-

corporate users on how

to practice effective

stakeholder engagement.

Our Thought Leadership

The Materiality Report:

Aligning Strategy,

Performance and

Reporting explores the

concept of materiality, reviews how various

companies have tackled

it and proposes a

Materiality Framework

that everyone can use to

inform a CR report.

David Pritchett

Senior Manager, Head of Europe

Tel. +41 79 366 9582 www.accountability.org

Contact

3. View from the practice: State Street Rebecca Wilkinson CR Report Manager, State Street

LIMITED ACCESS

GLOBAL MARKETING

State Street Corporation:

Materiality Approach

Rebecca Wilkinson

CR Report Manager

April 10, 2014

www.statestreet.com

LIMITED ACCESS

GLOBAL MARKETING

CORPORATE CITIZENSHIP

Materiality Agenda

19

About Us

CR Reporting Trends

Our Approach

Roadmap

Lessons Learned

LIMITED ACCESS

GLOBAL MARKETING

CORPORATE CITIZENSHIP

State Street Corporation Highlights

20

• $27.4 trillion in assets under custody and administration

• $2.3 trillion in assets under management

• Revenue of $9.88 billion in full-year 2013

• Strong securities lending program, with more than $2.95 trillion in average lendable assets as of

December 31, 2013

• Founded in 1792

• Ticker Symbol: STT

• More than 29,000 employees

• Offices in 29 countries serving more than 100 markets

Profile

LIMITED ACCESS

GLOBAL MARKETING

CORPORATE CITIZENSHIP

CR Reporting Trends Evolution of CR Reporting

21

Past Present Future

Summary Helping raise awareness

internally and externally

for the positive work a

company is undertaking to

benefit society at large

Focusing on a few key

issues where the

company can have

the biggest positive

impact

Linking performance on

CSR issues to business

performance—potentially

producing an integrated

financial/ non-financial

report

Content • Narratives

• Pictures

• Material issue

focus

• KPIs

• Sustainability context

and performance

Process • Anecdotes

• Ad hoc

• Stakeholder

inclusion

• Assurance

verification

• Advisory panel

• Consultancy expertise

Structure • Dis-integrated • Multi comms/

engagement

channels

• Integrated reporting

LIMITED ACCESS

GLOBAL MARKETING

CORPORATE CITIZENSHIP

22

Rise of ESG Disclosure

Source: Business for Social Responsibility

LIMITED ACCESS

GLOBAL MARKETING

CORPORATE CITIZENSHIP

23

Step 1: Landscape Assessment Key Comparisons

• A landscape assessment was conducted through which a

select group of peers and competitors were examined as a

benchmarking exercise

• Companies assessed include:

o Citigroup, Barclays, Credit Suisse, Citigroup, Westpac,

Northern Trust, BNY Mellon, Mizuho

• Economic Value Generated and Wealth

and Income Generation in Society: we

belong to a group of companies that

gives significant value to the core

business-related topics within CR

considerations, and thus demonstrate an

integrated approach

• Environment: we put more emphasis on

Impacts from Business Travel than peers

and competitors, which seems an

opportunity for positive differentiation

• Social: Employee Incentives and

Compensation highly ranked, Gender

Compensation Equality receives

unusually high emphasis, Public Policy is

also ranked notably high, Responsible

Marketing is also emphasized rather

strongly, Human Rights Risk

Management higher than Human Rights

Policy and Training, this is reversed in

our case

Our Approach Materiality

Step 2: Materiality Workshop

• A series of cross-regional workshops and interviews were

scheduled for conducting a materiality assessment

• In preparation a comprehensive list of sustainability topics to

be used was generated that are highly relevant to State Street

and its value chain

• Topics were generated by reporting standards such as: GRI

G4 reporting framework and Financial Sector Supplement,

SASB (Sustainability Accounting Standards Board) topics, and

ISO 26000 (guidance social responsibility) topics

LIMITED ACCESS

GLOBAL MARKETING

CORPORATE CITIZENSHIP

Our Approach

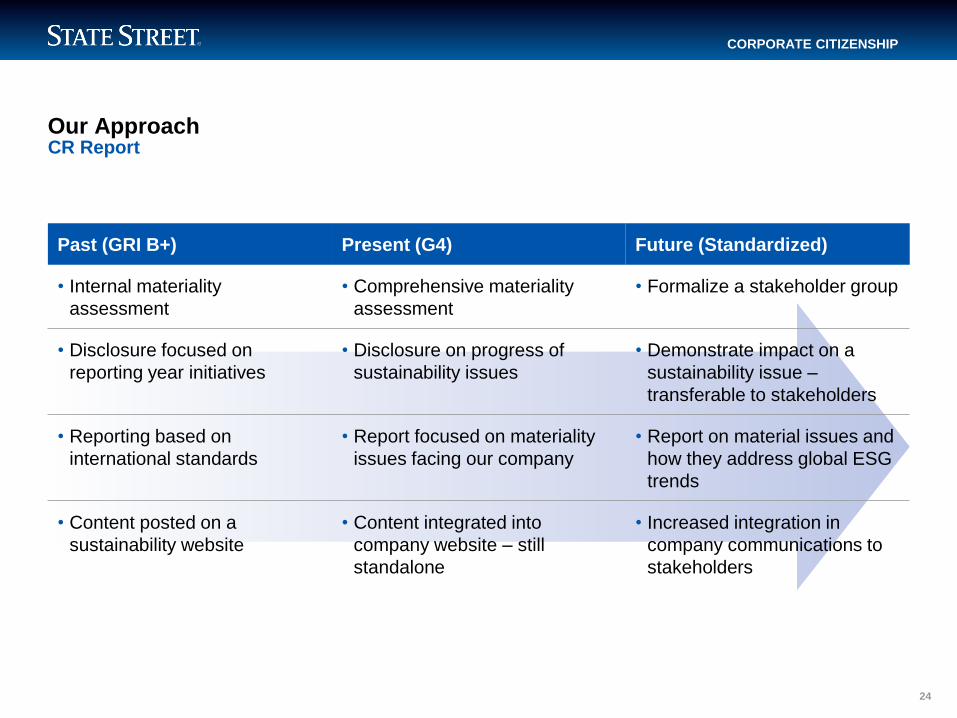

Past (GRI B+) Present (G4) Future (Standardized)

• Internal materiality

assessment

• Comprehensive materiality

assessment

• Formalize a stakeholder group

• Disclosure focused on

reporting year initiatives

• Disclosure on progress of

sustainability issues

• Demonstrate impact on a

sustainability issue –

transferable to stakeholders

• Reporting based on

international standards

• Report focused on materiality

issues facing our company

• Report on material issues and

how they address global ESG

trends

• Content posted on a

sustainability website

• Content integrated into

company website – still

standalone

• Increased integration in

company communications to

stakeholders

24

CR Report

LIMITED ACCESS

GLOBAL MARKETING

CORPORATE CITIZENSHIP

Roadmap Materiality Informs CR Strategy

25

• A gap analysis of the material subjects assessed against current CR programs and the latest GRI CR

report at State Street, in alignment with the GRI G4 guidelines;

• An assessment of current CR management systems and processes, considering newly identified material

subjects;

• Suggestions for improving the content of State Street’s data and information about its CR programs;

• Identification of gaps in current data collection methodologies that will hinder the quality and/or timeliness

of data collection regarding material subjects;

• Prioritization of requirements for management systems, processes, and policies for material subjects;

• Recommendations for how material subjects can be better communicated internally and externally;

• Evaluation of material subjects against international trends and important issues (e.g. Scope 3 reporting,

supply chain sustainability, integrated reporting, external assurance such as AA1000).

LIMITED ACCESS

GLOBAL MARKETING

CORPORATE CITIZENSHIP

Lessons Learned Challenges and Recommendations

26

• Consult more stakeholders for the external verification (difficult due to availability issues)

• Do materiality analysis in August, September – before report data collection and drafting.

• Have a goal in mind for reporting right from the start of materiality analysis (e.g. whether to use G4

or not)

• Short deadline

• Parallel work on CR report and materiality analysis rather than materiality analysis preceding

collection of internal performance data and drafting CR report

• Translated materiality guidelines into practical steps suited to our company

• Provided outside perspective and helped participants understand the process

• Productive division roles:

• Provided balanced guidance, process and moderation

• Guided our approach to make informed decisions

Benefits of an External Partner

Sustainserv’s support was based on 13-years experience helping companies design and implement

sustainability strategies and having produced over 100 GRI reports. Sustainserv is a GRI Certified

Training Partner in Switzerland.

4. View from the practice: Novo Nordisk Cora Olsen ESG Data manager Global TBL Management, Novo Nordisk

Materiality assessment at

Novo Nordisk – annual

reporting

In search of the holy grail

28

Integrated strategic management A solid governance structure is in place

Stakeholders

Governance

Aspirations & goals

Integrated thinking in

business processes

Performance

- Articles of Association

- Novo Nordisk Way

- Policies and strategies

- Boards and Committee

- Annual strategy review by the Board of Directors

- Strategic long-term targets and 2020 aspirations

- Specific short-term targets

- Trend spotting

- Stakeholder engagement

- Partnerships

- Balanced Scorecard

- Personal performance goals

- Long-term incentive programme

- Quarterly management reporting

- Annual reporting

29

Developing a pragmatic approach

30

Evidence of interest

Evidence of financial impact

Evidence of reputational impact

Forward looking adjustment

1. Financial disclosures

6. Revenue and costs

9. Reputation 10. High/systematic impact with low probability

2. Legal drivers 7. Assets and liabilities

11. Externality

3. Industry norms 8. Risk profile

4. Stakeholder concerns

5. Innovation opportunity

Material issues – determining relevance

31

Discussion round, Q&A

Important note:

• To ask a question, please use the raise hand function or chat function or email Aron Horvath ([email protected])

• You will be called out and un-muted if you wish to take the floor.

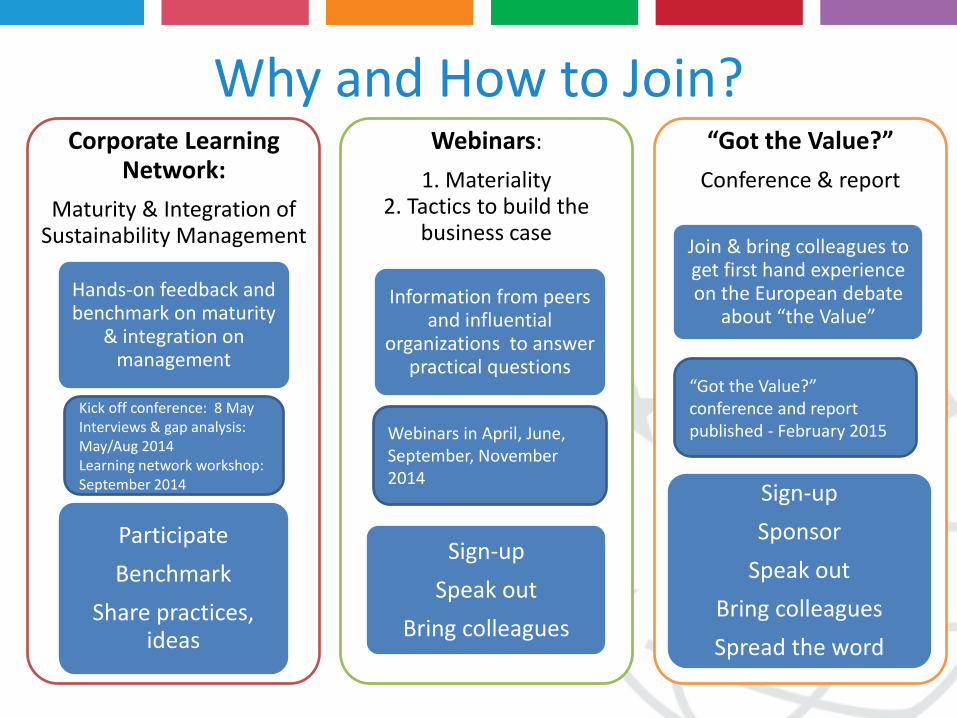

5. Closing: work with us on next steps Aron Horvath Project manager, CSR Europe

European Stakeholder Consultations

• A proven methodology to receive constructive feedback and provide follow-up to stakeholders

• Full service from conceptualizing through moderating the session to following up with stakeholders 6 months after

CSR Europe helps you engage with stakeholders in your materiality analysis process through:

Valuing & Improving

Sustainability Management

series

Corporate Learning Network:

Maturity & Integration of Sustainability Management

(MIA)

Webinars:

1. Materiality in April and September

2. Tactics to build the business case

in June and November

“Got the Value?”

Conference & report

Learning network: Valuing & Improving Sustainability Management - answering challenges

CEOs: “I need numbers,

objectives and targets”

CFOs: “Nice, but why does it matter for our business?”

CEOs: “We cannot do everything, tell me what

really matters!”

Corporate Learning Network:

Maturity & Integration of Sustainability Management

Hands-on feedback and benchmark on maturity

& integration on management

Participate

Benchmark

Share practices, ideas

Webinars:

1. Materiality 2. Tactics to build the

business case

Information from peers and influential

organizations to answer practical questions

Sign-up

Speak out

Bring colleagues

“Got the Value?”

Conference & report

Join & bring colleagues to get first hand experience on the European debate

about “the Value”

Sign-up

Sponsor

Speak out

Bring colleagues

Spread the word

Why and How to Join?

Kick off conference: 8 May Interviews & gap analysis: May/Aug 2014 Learning network workshop: September 2014

Webinars in April, June, September, November 2014

“Got the Value?” conference and report published - February 2015

“Get Your Company Ready for a New Era of European Non-Financial Reporting and Integrated Performance”

Conference, 8 May, Brussels Purpose • Gain insight to global and European context of non-financial reporting • Get inspired of how better sustainability management and reporting can add to your

company`s organization’s value • Get equipped with tools and frameworks

Confirmed speakers • Didier Millerot, DG Internal Market and Services European Commission • Wim Bartels, Partner, KPMG Sustainability Global Head Sustainability Assurance • Michel Bande, Vice President Sustainability, Solvay • Marina Migliorato, Head of Sustainability, Enel • Maria Alexiou, CSR Director, Titan • Lois Guthrie, Director, Climate Disclosure Standards Board • Pietro Bertazzi, Senior Manager - Policy and Government Affairs, Global Reporting Initiative • Joan Geerts, Senior Manager Operations, DSM – on natural and social capital • Carola Wijdoogen, CSR Director, Dutch Railway Organization – on E P&L • Eduardo Puig Aznar, Director Stakeholder Engagement, Telefónica – on stakeholder

engagement 4.0

We value your feedback

Thank you for participating in this webinar!

We kindly ask you to take 3 minutes of your time to share with us how you experienced the webinar in terms of quality

and relevance.

Your feedback is invaluable to us and will help us to improve our service to match your ongoing needs.

Access the evaluation survey at:

CSR Europe Webinar Evaluation 2014

Thank you for your attention!

For more information: www.csreurope.org Contact: Aron Horvath ([email protected])