Embed Size (px)

Citation preview

7/28/2019 weather derivatives .docx

http://slidepdf.com/reader/full/weather-derivatives-docx 1/19

Introduction (Priyanka)

Weather derivatives are financial instruments that can be used by organizations or individuals as part of a risk management strategy to reduce risk associated with adverse or unexpected weather conditions. The differencefrom other derivatives is that the underlying asset (rain/temperature/snow) has no direct value to price the

weather derivative

A weather derivative is defined by several elements, explained below:

Reference Weather StationAll weather contracts are based on the actual observations of weather at one or more specific weather stations.Most transactions are based on a single station, although some contracts are based on a weighted combination ofreadings from multiple stations and others on the difference in observations at two stations.

IndexThe underlying index of a weather derivative defines the measure of weather which governs when and how

payouts on the contract will occur. The most common indexes in the market are Heating Degree Days (HDDs)and Cooling Degree Days (CDDs) - these measure the cumulative variation of average daily temperature from65oF or 18oC over a season and are standard indexes in the energy industry that correlate well with energyconsumption. A wide range of other indexes are also used to structure transactions that provide the mostappropriate hedging mechanisms for end-users in various industries. Average temperature is another commonindex for non-energy applications, and some transactions are based on so-called event indexes which count thenumber of times that temperature exceeds or falls below a defined threshold over the contract period. Similar indexes are also used for other variables; for example cumulative rainfall or the number of days on whichsnowfall exceeds a defined level.

Term

All contracts have a defined start date and end date that constrain the period over which the underlying index iscalculated. The most common terms in the market are November 1 through March 31 for winter seasoncontracts and May 1 through September 30 for summer contracts, however there have been an increasingvolume of trading in one month and one week contracts as the market has grown. Some contracts also specifyvariable index calculation procedures within the overall term - such as exclusion of weekends or doubleweighting on specific days - to address individual end-user business exposures.

StructureWeather derivatives are based on standard derivative structures such as puts, calls, swaps, collars, straddles, andstrangles. Key attributes of these structures are the strike (the value of the underlying index at which thecontract starts to pay out), the tick size (the payout amount per unit increment in the index beyond the strike),

and the limit (the maximum financial payout of the contract).

PremiumThe buyer of a weather option pays a premium to the seller that is typically between 10 and 20% of the notionalamount of the contract, however this can vary significantly depending on the risk profile of the contract. Thereis typically no upfront premium associated with swaps.

7/28/2019 weather derivatives .docx

http://slidepdf.com/reader/full/weather-derivatives-docx 2/19

History

The first weather derivative deal was in July 1996 when Aquila Energy structured a dual-commodity hedge for Consolidated Edison Co.[1] The transaction involved ConEd's purchase of electric power from Aquila for themonth of August. The price of the power was agreed to, but a weather clause was embedded into the contract.

This clause stipulated that Aquila would pay ConEd a rebate if August turned out to be cooler than expected.The measurement of this was referenced to Cooling Degree Days measured at New York City's Central Park weather station. If total CDDs were from 0 to 10% below the expected 320, the company received no discountto the power price, but if total CDDs were 11 to 20% below normal, Con Ed would receive a $16,000 discount.Other discounted levels were worked in for even greater departures from normal.

After that humble beginning, weather derivatives slowly began trading over-the-counter in 1997. As the marketfor these products grew, the Chicago Mercantile Exchange introduced the first exchange-traded weather futurescontracts (and corresponding options), in 1999. The CME currently trades weather derivative contracts for 18cities in the United States, nine in Europe, six in Canada and two in Japan. Most of these contracts track coolingdegree days or heating degree days, but recent additions track frost days in the Netherlands and

monthly/seasonal snowfall in Boston and New York. A major early pioneer in weather derivatives was Enron Corporation, through its EnronOnline unit.

In an Opalesque video interview, Nephila Capital's Barney Schauble discusses how some hedge funds have now begun focusing on weather derivatives as an investment class. Counterparties such as utilities, farmingconglomerates, individual companies and insurance companies are essentially looking to hedge their exposurethrough weather derivatives, and funds have become a sophisticated partner in providing this protection. Therehas also been a shift over the last few years from primarily fund of funds investment in weather risk, to moredirect investment for investors looking for non-correlated items for their portfolio. Weather derivatives providea pure non-correlated alternative to traditional financial markets.

It is estimated that nearly 20% of the U.S. economy is directly affected by the weather, and that the profitabilityand revenues of virtually every industry - agriculture, energy, entertainment, construction, travel and others -depend to a great extent on the vagaries of temperature. In a 1998 testimony to Congress, former commercesecretary William Daley stated, "Weather is not just an environmental issue; it is a major economic factor. Atleast $1 trillion of our economy is weather-sensitive."

The risks businesses face due to weather are somewhat unique. Weather conditions tend to affect volume andusage more than they directly affect price. An exceptionally warm winter, for example, can leave utility andenergy companies with excess supplies of oil or natural gas (because people need less to heat their homes). Or,an exceptionally cold summer can leave hotel and airline seats empty. Although the prices may changesomewhat as a consequence of unusually high or low demand, price adjustments don't necessarily compensate

for lost revenues resulting from unseasonable temperatures.

Finally, weather risk is also unique in that it is highly localized, cannot be controlled and despite great advancesin meteorological science, still cannot be predicted precisely and consistently.

7/28/2019 weather derivatives .docx

http://slidepdf.com/reader/full/weather-derivatives-docx 3/19

Temperature as a Commodity ( Anchita)

Until recently, insurance has been the main tool used by companies' for protection against unexpected weather conditions. But insurance provides protection only against catastrophic damage. Insurance does nothing to

protect against the reduced demand that businesses experience as a result of weather that is warmer or colder than expected.

In the late 1990s, people began to realize that if they quantified and indexed weather in terms of monthly or seasonal average temperatures, and attached a dollar amount to each index value, they could in a sense"package" and trade weather. In fact, this sort of trading would be comparable to trading the varying values of stock indices, currencies, interest rates and agricultural commodities. The concept of weather as a tradeablecommodity, therefore, began to take shape.

"In contrast to the various outlooks provided by government and independent forecasts, weather derivativestrading gave market participants a quantifiable view of those outlooks," noted Agbeli Ameko, managing partner

of energy and forecasting firm EnerCast.

In 1997 the first over-the-counter (OTC) weather derivative trade took place, and the field of weather risk management was born. According to Valerie Cooper, former executive director of the Weather Risk Management Association, an $8 billion weather-derivatives industry developed within a few years of itsinception.

In Contrast to Weather Insurance In general, weather derivatives cover low-risk, high-probability events. Weather insurance, on the other hand,typically covers high-risk, low-probability events, as defined in a highly tailored, or customized, policy. For example, a company might use a weather derivative to hedge against a winter that forecasters think will be 5° F

warmer than the historical average (a low-risk, high-probability event). In this case, the company knows itsrevenues would be affected by that kind of weather. But the same company would most likely purchase aninsurance policy for protection against damages caused by a flood or hurricane (high-risk, low-probabilityevents).

Insurance contracts cover high risk, low probability scenarios whereas weather derivatives cover lowrisk, high probability scenarios.

With weather derivatives the payout is designed to be in proportion to the magnitude of the phenomenonwhereas insurance pays a one off lump sum which may or may not be proportional and hence lacksflexibility.

Insurance normally will payout if there has been damage or loss. Weather derivatives require only that

the index has passed on a certain point. Weather derivatives are index-based securities, which allow many players to participate in the market.

This increases liquidity. It is possible to monitor the performance of the hedged weather derivatives during the life of the

contract.

Additional shorter term forecasting towards the end of the contract might mean that one can remove himself from the weather derivative. Because it is a traded security there will always be a price at which one can sell or buyback the contract.

7/28/2019 weather derivatives .docx

http://slidepdf.com/reader/full/weather-derivatives-docx 4/19

Weather Events

The weather futures markets are based upon weather information and specific weather events, such as thefollowing:

Heating Degree Days

HDD is the baseline temperature of 65°F less the average temperature for a given day. For example, if the average temp is 55°F, there are 10 HDDs for that day [65°F-55°F = 10 HDD].

Cooling Degree Days

CDD is the average temperature for a given day less the baseline of 65°F. For example, if the averagetemp is 75°F, there are 10 CDDs for that day [75°F-65°F = 10 CDD].

Cumulative Average Temperature Average Temperature Frost Snowfall Hurricanes

Locations

The weather futures markets cover the above weather events in three different regions (North America, Europe,and Asia), and cover many locations throughout the world, including the following:

North America

Atlanta Des Moines New York Baltimore Detroit Philadelphia Boston Houston Portland Chicago Kansas City Sacramento Cincinnati Las Vegas Salt Lake City Dallas Minneapolis Tucson Calgary

7/28/2019 weather derivatives .docx

http://slidepdf.com/reader/full/weather-derivatives-docx 5/19

Edmonton Montreal Toronto Vancouver Winnipeg

Europe

Amsterdam Essen Paris Barcelona London Rome Berlin Madrid Stockholm

Asia

Sydney Melbourne Tokyo Osaka

Types of Weather Derivatives ( Harnish) Various brokerage and trading firms customize the weather derivatives to the client‟s needs. Only certain partiesmay be interested in trading a specific type of weather commodity based on their business structure. Some of the common weather derivative products include

1. Swaps Swaps are contracts where two parties agree to exchange their risks. This will produce a more stable cash flowwhen weather conditions are volatile. In simple terms one party agrees to pay the other if the contracted indexsettles above a certain level while the other agrees to pay if the index settles below that level.

Swaps have no premium but provide protection from adverse weather in return for giving up some of the upsideof a favorable season. For example, a swimsuit manufacturer may buy a swap to protect against the averagetemperature over the summer period being cool in return for sacrificing some of the extra revenues earnedduring a hot summer.

2. Collars Collar is similar to swap in that protection against adverse weather is provided in return for giving up some of the returns generated in favorable conditions. The difference is that the payments to and from the parties‟ takes

7/28/2019 weather derivatives .docx

http://slidepdf.com/reader/full/weather-derivatives-docx 6/19

place outside an upper and lower level. This allows revenues to fluctuate within a normal range of weather conditions but protects either party against extreme weather.

3. Puts (Floors) Put options or floors are contracts that compensate a buyer if a weather variable falls below a predeterminedlevel. This type of protection involves a premium being paid upfront. It provides protection against adverse

weather whilst allowing profits to be retained in a favourable period. For instance, a ski resort may buy a Put onthe level of snowfall over a skiing period. This would then compensate the resort if the level of snowfall is lowdeterring a large number of skiers. If the level of snowfall is high, the resort loses only the premium paid.

4. Calls (Caps) Call option or Caps are contracts that compensate a buyer if a weather variable falls above a predeterminedlevel. This type of protection also involves a premium being paid upfront. It provides protection against adverseweather whilst allowing profits to be retained in a favorable period. To illustrate, a commercial airfield might buy a call option when the number of days that the average wind speed exceeds a certain level. This wouldcompensate the airfield for the loss of revenue during days when they had to stop flying.

Two of the non-standard weather contracts, which are gaining popularity, are:

Compounds is a structure that provides the buyer with the option to purchase or sell a weather contract on anagreed date in the future. This future date must be prior to the start date of the underlying weather contract. Thisrequires a premium payment. If the buyer exercises the compound at the later date, a second premium paymentwould be required.

It provides the buyer an option to cancel the purchase of the contract if he feels weather protection is notrequired. Digital is a contract that has linear payouts. In other words it provides a fixed amount of payout if a particular weather event occurs. If the event does not occur there is no payout, only the premium stands lost.

Valuation ( Hardik) Plz search more info on this

There is no standard model for valuing weather derivatives similar to the Black-Scholes formula for pricingEuropean style equity option and similar derivatives. That is due to the fact that underlying asset of the weather derivative is non-tradeable which violates a number of key assumptions of the BS Model. Typically weather derivatives are priced in a number of ways:

[edit] Business pricing

Business pricing requires the company utilizing weather derivative instruments to understand how its financial performance is affected by adverse weather conditions across variety of outcomes (i.e. obtain a utility curvewith respect to particular weather variables). Then the user can determine how much he is willing to pay inorder to protect his/her business from those conditions in case they occurred based on his/her cost-benefitanalysis and appetite for risk. In this way a business can obtain a 'guaranteed weather' for the period in question,

7/28/2019 weather derivatives .docx

http://slidepdf.com/reader/full/weather-derivatives-docx 7/19

largely reducing the expenses/revenue variations due to weather. Alternatively, an investor seeking certain levelor return for certain level of risk can determine what price he is willing to pay for bearing particular outcomerisk related to a particular weather instrument.

[edit] Historical pricing (Burn analysis)

The historical payout of the derivative is computed to find the expectation. The method is very quick andsimple, but does not produce reliable estimates and could be used only as a rough guideline. It does not

incorporate variety of statistical and physical features characteristic of the weather system.

[edit] Index modelling

This approach requires building a model of the underlying index, i.e. the one upon which the derivative value isdetermined (for example monthly/seasonal cummulative heating degree days). The simplest way to model theindex is just to model the distribution of historical index outcomes. We can adopt parametric or non-parametricdistributions. For monthly cooling and heating degree days assuming a normal distribution is usually warranted.The predictive power of such model is rather limited. A better result can be obtained by modelling the indexgenerating process on a finer scale. In the case of temperature contracts a model of the daily average (or minand max) temperature time series can be built. The daily temperature (or rain, snow, wind, etc.) model can be

built using common statistical time series models (i.e. ARMA or Fourier transform in the frequency domain) purely based only on the features displayed in the historical time series of the index. A more sophisticatedapproach is to incorporate some physical intuition/relationships into our statistical models based on spatial andtemporal correlation between weather occurring in various parts of the ocean-atmosphere system around theworld (for example we can incorporate the effects of El Niño on temperatures and rainfall).

Physical models of the weather

We can utilize the output of numerical weather prediction models based on physical equation describingrelationships in the weather system. Their predictive power tends to be less or similar to purely statisticalmodels beyond time horizons of 10 – 15 days. Ensemble forecasts are especially appropriate for weather derivative pricing within the contract period of a monthly temperature derivative. However, individualsmembers of the ensemble need to be 'dressed' (for example with gaussian kernels estimated from historical performance) before a reasonable probabilistic forecast can be obtained.

Mixture of statistical and physical models

A superior approach for modelling daily or monthly weather variable time series is to combine statistical and physical weather models using time-horizon varying weight which are obtained after optimization of those based on historical out-of-sample evaluation of the combined model scheme performance.

7/28/2019 weather derivatives .docx

http://slidepdf.com/reader/full/weather-derivatives-docx 8/19

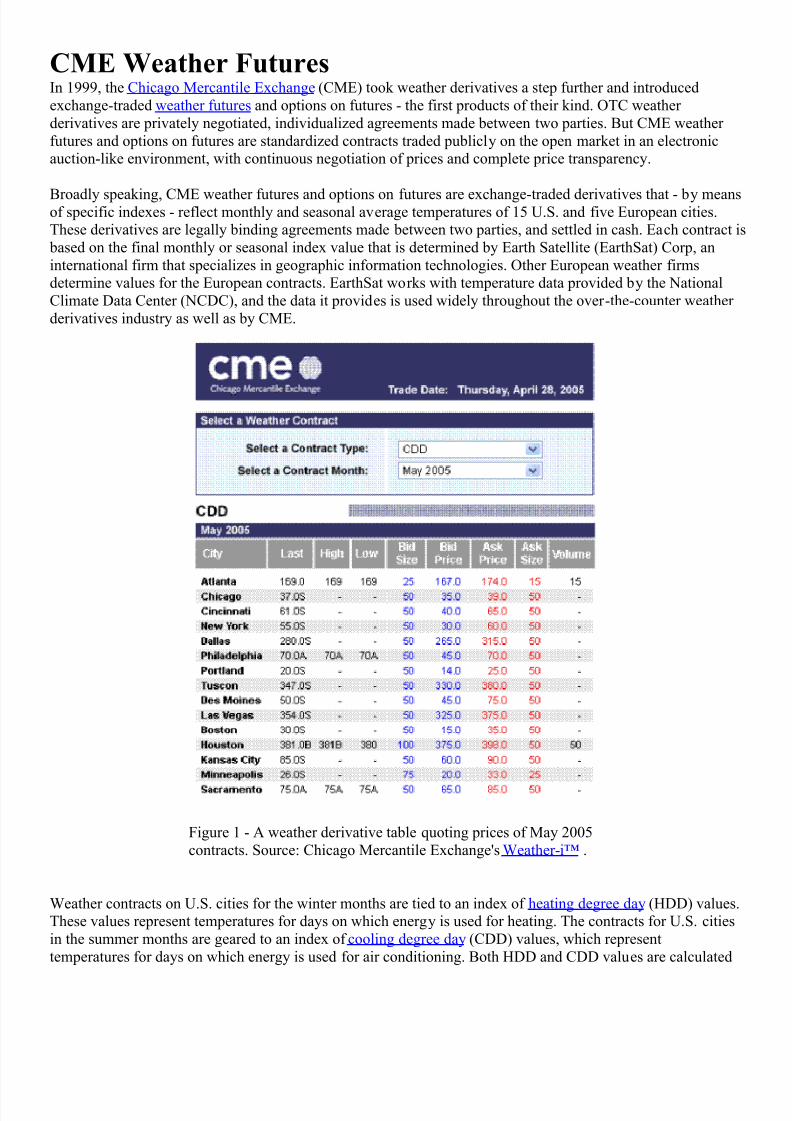

CME Weather FuturesIn 1999, the Chicago Mercantile Exchange (CME) took weather derivatives a step further and introducedexchange-traded weather futures and options on futures - the first products of their kind. OTC weather derivatives are privately negotiated, individualized agreements made between two parties. But CME weather futures and options on futures are standardized contracts traded publicly on the open market in an electronicauction-like environment, with continuous negotiation of prices and complete price transparency.

Broadly speaking, CME weather futures and options on futures are exchange-traded derivatives that - by meansof specific indexes - reflect monthly and seasonal average temperatures of 15 U.S. and five European cities.These derivatives are legally binding agreements made between two parties, and settled in cash. Each contract is based on the final monthly or seasonal index value that is determined by Earth Satellite (EarthSat) Corp, aninternational firm that specializes in geographic information technologies. Other European weather firmsdetermine values for the European contracts. EarthSat works with temperature data provided by the NationalClimate Data Center (NCDC), and the data it provides is used widely throughout the over-the-counter weather derivatives industry as well as by CME.

Figure 1 - A weather derivative table quoting prices of May 2005contracts. Source: Chicago Mercantile Exchange's Weather-i™ .

Weather contracts on U.S. cities for the winter months are tied to an index of heating degree day (HDD) values.These values represent temperatures for days on which energy is used for heating. The contracts for U.S. citiesin the summer months are geared to an index of cooling degree day (CDD) values, which representtemperatures for days on which energy is used for air conditioning. Both HDD and CDD values are calculated

7/28/2019 weather derivatives .docx

http://slidepdf.com/reader/full/weather-derivatives-docx 9/19

according to how many degrees a day's average temperature varies from a baseline of 65° Fahrenheit. (Theday's average temperature is based on the maximum and minimum temperature from midnight to midnight.)

Measuring Daily Index Values An HDD value equals the number of degrees the day's average temperature is lower than 65° F. For example, aday's average temperature of 40° F would give you an HDD value of 25 (65 - 40). If the temperature exceeded65° F, the value of the HDD would be zero. This is because in theory there typically would be no need for heating on a day warmer than 65°.

Figure 2 - Table summarizing daily averagetemperatures and the corresponding HDD and itsimpact on the relevant contract.

A CDD value equals the number of degrees an average daily temperature exceeds 65° F. For example, a day'saverage temperature of 80° F would give you a daily CDD value of 15 (80 - 65). If the temperature were lower

than 65° F, the value of the CDD would be zero. Again, remember that in theory there typically would be noneed for air conditioning if the temperature were less than 65°F.

For European cities, CME's weather futures for the HDD months are calculated according to how much theday's average temperature is lower than 18° Celsius. However CME weather futures for the summer months inEuropean cities are based not on the CDD index but on an index of accumulated temperatures, the CumulativeAverage Temperature (CAT).

7/28/2019 weather derivatives .docx

http://slidepdf.com/reader/full/weather-derivatives-docx 10/19

Measuring Monthly Index Values A monthly HDD or CDD index value is simply the sum of all daily HDD or CDD value recorded that month.And seasonal HDD and CDD values, accordingly, are simply accumulated values for the winter or summer months. For example, if there were 10 HDD daily values recorded in Nov 2004 in Chicago, the Nov 2004 HDDindex would be the sum of the 10 daily values. Thus, if the HDD values for the month were 25, 15, 20, 25, 18,22, 20, 19, 21 and 23 the monthly HDD index value would be 208.

The value of a CME weather futures contract is determined by multiplying the monthly HDD or CDD value by

$20. In the example above, the CME November weather contract would settle at $4,160 ($20 x 208 = $4,160).

Major Players and Beneficiaries ( Krupali)

Major Players:

ICICI-Lombard , IFFCO-Tokio, Agricultural Insurance Company of India, Swiss Reinsurance , World Bank ,

Government of India , Rabobank, ABN Amro, NCDEX, MCX

Weather derivatives can be used in a variety of ways by diverse industries:

Construction, Energy, Tourism, Food, Event Management, Retail, Transport

Risk Holder Weather Type Risk

Energy Industry Temperature Lower sales during warmwinters or cool summers

Energy Consumers Temperature Higher heating/cooling costsduring cold winters and hotsummers

Beverage Producers Temperature Lower sales during coolsummers

Building Material

Companies

Temperature/Snowfall Lower sales during severewinters (construction sites shutdown)

Construction

Companies

Temperature/Snowfall Delays in meeting schedulesduring periods of poor weather

Ski Resorts Snowfall Lower revenue during winters

with below-average snowfallAgricultural Industry Temperature/Snowfall Significant crop losses due to

extreme temperatures or rainfall

Municipal Governments Snowfall Higher snow removal costsduring winters with above-average snowfall

Road Salt Companies Snowfall Lower revenues during lowsnowfall winters

Hydro-electric power

generation

Precipitation Lower revenue during periods of drought

7/28/2019 weather derivatives .docx

http://slidepdf.com/reader/full/weather-derivatives-docx 11/19

A wide variety of companies are turning to weather derivatives for risk management. Below is an overview of avariety of industries, how they are exposed to weather risk, and how they are hedging this risk with weather derivatives:

Local Distribution Companies (LDC)One of the largest factors in natural gas consumption is the severity and duration of the winter. LDC's are

naturally exposed to warm winters because their sales revenue is largely based on the volume of natural gas that

is consumed during the winter season.Electric Utilities

One of the largest factors in the consumption of electricity is the severity and duration of the summer. Electricutilities are naturally exposed to cool summers because their sales revenue is largely based on the volume of electricity that is consumed during the summer season. Weather derivatives provide electric utilities with a toolto hedge their volumes.

> Download Case Study

Propane / Heating Oil Distributors

Similar to the LDC's, this group is exposed to warm winters because their sales revenue is based on the volumeof Propane/Heating Oil that is consumed during a winter season.Agriculture / Livestock Agribusiness is perhaps the most reliant on weather factors. It can be exposed to a number of different elementsdepending on the crop/livestock. The yield of a given crop is subject to a combination of weather conditions;livestock yield is susceptible to extreme summer heat or winter cold. Mainly, this group is exposed to rain,temperature, frost and any combination.ConstructionThe construction industry is exposed to weather related delays in projects. These delays cost money not only inlabor and inventory cost but also in potential penalties levied by customers for delays. Weather derivatives tohedge these risks can be included in the original quote to a customer and can hedge against adverse weather at aconstruction site.

> Download Case Study Offshore OperationsWeather conditions on offshore rigs are not only dangerous but also costly. Besides actual damage to anoffshore operation, there are other costs associated with inclement weather such as removal of crews and halt of production during major weather events.Beverage

Beverage sales are very sensitive to the weather. On hot summer days, customers drink more soft drinks - on

cool days they drink less. It is this fact, which exposes the beverage industry to the weather.

> Download Case Study HospitalityVacation destinations rely on favorable climates, whether it is snowfall at ski resorts or sunshine as beachresorts. The industry is increasingly turning to weather derivative markets to hedge the risk that inclementweather will keep away customers and decrease revenue.

> Download Case Study

7/28/2019 weather derivatives .docx

http://slidepdf.com/reader/full/weather-derivatives-docx 12/19

RetailingRetailers can be categorized into two groups: seasonal and situational. Retailers of seasonal products are subjectto weather risk within that specific season. Examples of this are retailers of swimsuits for the summer or coats

for the winter. Some retailers have "situational" risk; they need certain weather events to happen in order to sell products. Examples include umbrella manufacturers with sales based on the amount of rain or snow shovelmanufacturers with sales based on snowfall.Municipal Government PlanningWeather volatility can wreak havoc on a municipality's budget. A snowy winter can increase costs of snow

removal or a hot summer can delay much-needed maintenance. Due to municipal budget constraints risk management tools help stabilize weather-related expenses, keeping budgets in balance and appeasing taxpayers.TransportationWhether transporting people or goods, the transportation industry has exposure to inclement weather. Theairline industry has to battle weather-related delays that cost millions of dollars. Increasingly, customers' just-in-time inventory demands are making logistics companies and in-house logistics departments vary aware of thedelays caused by weather.Manufacturing

Many companies' revenues vary given the amount of specific weather events. Examples of this are a sunglassmanufacturer or ski equipment maker whose sales are sensitive to weather trends.

Weather Derivatives: A Futuristic Concept in India

( prajakta)

Weather Derivative still has not been introduced in the Indian Market. Weather derivatives listed as a tradableinstrument on the commodity exchanges of India back in September last year when the Indian government

approved laws to allow commodity options and futures to be traded in the country. It was hoped that the newlaw would lead to other instruments such as weather derivatives being listed and traded but so far it hasn‟thappened.

Now, the Associated Chambers of Commerce and Industry of India (ASSOCHAM), have called for yet another amendment in the countries Forward Contracts (Regulation) Act, 1952 (FCRA) to allow for the trading of weather derivatives, futures and options on exchanges.

Commodity trading regulation has been hard-won in India but ASSOCHAM see enormous potential and saythat trading in commodities is likely to grow two to three times in volume over the next five years due to anincreasing population and rapid economic growth.

They see weather trading as a necessity given how exposed certain industries and farmers are to the extremes of India‟s weather. The agriculture market in India is estimated at a size of $281 billion and they say that withoutthe ability to trade in commodities such as weather it will be difficult for farmers to manage price risks.

Implementational Issues

The effectiveness and success of weather derivatives would depend on its successful implementation which, in

turn depends on:

7/28/2019 weather derivatives .docx

http://slidepdf.com/reader/full/weather-derivatives-docx 13/19

Institutional infrastructure;

Regulatory mechanism; and

. Education and awareness among market participants

Institutional infrastructure

An institutional set-up comprising of derivative exchanges, brokers, consumer

associations and weather observatories, is one of the most essential prerequisite for

implementing trading in weather derivatives. Securities and commodities derivative

trading already exist in many Indian exchanges and the same exchanges may be used

for trading derivative contracts on underlying weather parameters. Small farmers and

power consumers can access the weather derivative market through the consumer

associations or cooperatives. Most of all, institutional arrangements must be made to

provide the timely, reliable data (on weather parameters, crop yields and power

production and consumption) to all concerned parties.

Regulatory mechanism

A strong regulatory mechanism must be in place before the introduction of weather

based derivative contracts. The Forward Contract (Regulation) Act, at present covers

forward trading (derivative) in “goods” only. Necessary amendments are required to

broad base the scope of the act so as to permit derivatives trading on underlying “intangibles” like weather

parameters, electricity, etc. The Forward Contract

(Regulation) Amendment Bill 2006 is pending with the parliament which aims to

introduce such amendments and further seeks to transform the role of the Forward

7/28/2019 weather derivatives .docx

http://slidepdf.com/reader/full/weather-derivatives-docx 14/19

Markets Commission (FMC) from a government department to an independent

regulator like Securities and Exchange Board of India (SEBI).

Presently, SEBI regulates spot and derivative trading on exchanges of all securities

(i.e. stocks and bonds). Commodity forwards and futures are regulated by the Forward

Market Commission (FMC) which continues to be a subordinate office of the

government department and has no autonomy to garner resources. More over, Ministry

of Agriculture, Ministry of Company Affairs and the Reserve Bank of India also

exercise direct or indirect regulation over securities and commodity trading. This

overlapping regulatory jurisdiction and multiplicity of regulators may pose regulatory

challenges. Establishment of an independent regulator with adequate resources and

empowerment is essential for regulating the markets for weather derivative.

Education and awareness among market participants

Various market participants need to be educated and trained for understanding the

benefits and risks associated with weather derivatives. Farmers, consumers, financial

intermediaries, etc. can be benefited from weather derivatives only if they are well

educated about the various derivatives products and their effectiveness.

Other requirements like developing appropriate weather-based indices and

designing pricing mechanism for weather derivative contracts may be easily fulfilled once a strong institutional

and regulatory infrastructure is in place.

7/28/2019 weather derivatives .docx

http://slidepdf.com/reader/full/weather-derivatives-docx 15/19

Weather derivatives – A boon to Indian Farmer

( Nitiesh)

Farmers use old fashioned and traditional ways to ward off risks. Generally they end up mortgaging, leveraging

from the moneylenders or leasing land and farming. Rich farmers try to rope in more modern and heavy

machines such as automatic reapers, cutters, planters and try to make optimal utilization of the favorable

weather. They still follow the old diction of „Making hay while the sun shines‟. But this methods are only

helpful to those who can afford them .Most of the farmers have small pieces of lands and still use manual

methods of planting seeds, reaping, and sowing. Government is trying to support by improving the

infrastructure for irrigation by building canals and trying to free the farmers from the clutches of the evil money

lenders. But they still have a long way to go. The five year plans always have wonderful plans for the benefit

and uplift agriculture in India. The Finance ministers tend to give incentives and waiver huge loans but still

farmers are facing huge problems in spite of the government efforts. Agriculture credit off-take in ninth plan

grew @ 20% pa to Rs. 2,31,798 crores. Target for tenth plan was Rs. 7,36,570 crores. Eleventh five year plan

also incorporates to help the growth of agriculture.

The only way for mitigating the risk from inclement weather has been crop insurance. The insurance policies

and markets are unable to cope with the certain disasters dub to non availability of monsoon or sudden increase

in the rain. As the government waivers of loans and provides subsidies to farmers being effected by natural

calamities, people tend to take advantage and the risk of moral hazard plays an important part in dampening the

spirit of insurance. Also all crops do not classify to fall under the insurance schemes. Though a variety of crops

are grown in India most of the insurance schemes cover the staple food crops and the crops which are traded in

the commodities market. Less than two percent of the income generated by agriculture is covered by crop

insurance. Generally the amount of payout is far larger than the amount of premium collected hence private

companies are afraid to venture into the field of agro insurance and government has to carry a huge burden.

Settlement of claims also takes a long time due to informatics and operational problems and the farmers are

forced to take loans from money lenders again. The various national insurance scheme launched by government

have not passed with flying colors. As a result of this farmers participating in the insurance schemes have

dropped sharply.

Weather derivatives can play a very important part in removing these bottlenecks. They can be an alternate way

to hedge the weather risks. For an indemnity or claim a loss has to occur and only upon proof of that loss is the

claim passed. But in the case of a derivative it does not require a loss to occur. A farmer can buy an option and

7/28/2019 weather derivatives .docx

http://slidepdf.com/reader/full/weather-derivatives-docx 16/19

decide the strike price on a derivative and pay or receive the difference within a matter of days. The underlying

for weather derivatives may be anything related to weather. It may be rainfall, temperature, wind velocity, snow

fall, or for that matter the occurrence of a hurricane.

“A financial weather derivative contract may be termed as a weather contingent contract whose payoff will be

in an amount of cash determined by future weather events. The settlement value of these weather events is

determined from a weather index, expressed as values of a weather variable measured at a stated location”.

Dischel and Barrieu.

Rather than paying huge premium for multi calamity insurances farmers can pay less premium and invest in

derivatives and hedge off their risks. With a bit of innovation and high finance wizardry it is possible to make

structured product which will help the farmers in case of natural disasters and make it profitable for them if

everything is alrite.Also as the transactions will occur in the exchange their will be less operational and

administrational overhead. Moral hazard risk also will be reduced because of the transparency in the market. As

the derivatives can be individually bought and sold by each farmer he can hedge his own risk unlike proving

individual loss for getting individual claims. Also as these options will be traded on the exchange it shall have a

larger market to cater. Many developing countries are slowly trying to incorporate weather derivatives into their

systems. Romania, Mexico, Morocco, Mangolia, Ukraine are some of the fore runners who have opened up

after realizing the numerous advantages of Weather derivatives.

Conclusion

Weather trading in India has a long way to go. First and foremost until and unless the bill is passed and trading

is allowed on intangibles such as rain, weather trading will be a dream. Even if the bill is passed and weather is

traded on the exchange a very strong infrastructure should be created so as to have a far reaching effect.

Farmers from every nook and cranny of the country should be able to hedge of their risks. This can be done

with the help of the local Gram Panchayats and e-choupals. Farmers and traders should be given exposure and

educated about the benefits of weather trading. They should be taught that how by using weather derivatives

they can hedge their risks in an easier fashion rather than falling in the clutches of a money lender or waiting for

an unknown period of time for settlement of claims. Technology should be the driver for collecting real time

and accurate data. Historical data from different agencies should be taken and cleaned before creating the

rainfall index. The huge loopholes created by the insurance companies can be reduced by the creation of

derivatives. Weather derivatives like any other exchange traded instrument can serve the purpose of its creation

only if it increases in volume and is in demand. Instruments which work in one country may pass or fail in

7/28/2019 weather derivatives .docx

http://slidepdf.com/reader/full/weather-derivatives-docx 17/19

another region. But from the empirical studies conducted in other developing countries and with the success of

weather derivatives their, India seems to have the potential to have a weather derivatives market. Theoretically

weather derivatives seem a good hedge against the vagaries of nature which affect India and lead to a huge loss

every year. In view of the significance of agriculture and power sectors in the Indian economy and

their vulnerability to weather factors, the need for evolving an adequate, sustainable

weather risk management system should be duly recognized. In agriculture sector the

traditional crop insurance system has failed due to associated deficiencies. As an

alternative, weather derivative contracts are free from these deficiencies. These

contracts offer prospects of a low-cost, flexible and sustainable approach to weather

risk management. Weather derivatives, like any other risk-hedging instrument,

operate strictly on the basic insurance principles of law of large numbers,

estimatability of probability and diversity in individual expectations. As such, the

relevance of the concept is not country-specific. Its success elsewhere as revealed by

various empirical studies only make a case for its adoption in any country, more

particularly a country whose performance is severely constrained by highly

unpredictable, erratic weather conditions. The conditions necessary for the success

of weather derivative market may not be equally present in all countries. But as far as

the Indian economy is concerned; it appears to be, by and large, a substantially fit case

for the adoption of weather derivatives. It has an immensely weather-based and

predominant agricultural sector. The huge energy sector is mostly hydro-based and

occupies a pivotal position in the economic infrastructure. The extreme climatic

conditions during winter and summer in most parts of the country increase the

7/28/2019 weather derivatives .docx

http://slidepdf.com/reader/full/weather-derivatives-docx 18/19

dependence of people on electricity substantially. Besides the present trend of

integrating the Indian financial sector with the global market may be expected to

contribute to the growth and success of the derivatives market in terms of participation of foreign players and

raising the level of competition. Above all, the country‟s fiscal

health does not warrant continuation of subsidizing the traditional crop-insurance

system, any longer. The policy-makers need to make a choice between yielding to

populist approach and disciplining the fiscal system.

There are some limitations of weather derivative contracts. They suffer from what

is known as “basis risk” (Quiggin et al., 1994). Also, the non-availability of accurate

weather data to the parties concerned seriously hampers the smooth functioning of

these contracts. But these limitations are not insurmountable. Despite these limitations,

weather derivatives continue to capture increasing attention of risk managers, all over

the world. Weather derivatives are undoubtedly a low-cost, flexible and sustainable

option. It deserves to be tried. Weather derivatives too have its disadvantages. It may not be understood by the

major chunk of illiterate farmers, it may be too complex for them. The infrastructure needed to trade weather

derivatives effectively may be high. Everything has its limitations. But we won‟t know whether we can succeed

or not until we try. The potential is their in India for weather derivatives. We have to wait and see how the

weather derivative saga unfolds once the Government passes the bill.

7/28/2019 weather derivatives .docx

http://slidepdf.com/reader/full/weather-derivatives-docx 19/19