Embed Size (px)

Citation preview

BASF Capital Market Story__June 2012

We add value as one company

Group Visit Morgan Stanley Ludwigshafen June 29, 2012

BASF Presentation June 2012

BASF Performance Products Growth. Value. Sustainability

Michael Heinz Member of the Board of Executive Directors Ludwigshafen June 29, 2012

BASF Presentation June 2012 2

Distinct customer interaction models allow to generate and fairly share additional value by serving differentiated customer needs

Industry leader in managing complexity and cost efficiency

Globally leading market positions serving a broad portfolio of industries

Leading the industry in innovations developed in close cooperation with customers for both developed and emerging markets

Growth

Value

Sustainability

Value generation throughout economic cycles

Outstanding contribution to consumers‘ need for sustainable well-being as well as resource and energy efficiency

Performance Products: Positioned to outperform

BASF Presentation June 2012 3

Performance Products segment in 2011: Net Sales of €15.7 billion

Dispersions & Pigments Sales: € 3.5bn

Care Chemicals Sales: € 5.2bn

Paper Chemicals Sales: € 1.6bn

Performance Chemicals Sales: € 3.5bn

Nutrition & Health

Sales: € 1.9bn

Pigments, Resins and Additives for - Paints &

Coatings - Printing &

Packaging Dispersions for

- Construction - Adhesives

Home Care

Personal Care - Cosmetics

Hygiene

Paper coating chemicals

Paper production chemicals

Kaolin

Plastics processing

Oilfield & Mining

Water

Automotive & Refineries

Textile & Leather

Human Nutrition

Animal Nutrition

Pharma

Aroma Ingredients

Five divisions serving a distinct portfolio of industries

BASF Presentation June 2012 4

Paints & Coatings | Plastics Processing | Fuel and Lubricants | Hygiene

10 – 15 %

5 – 10 %

< 5 % Printing & Packaging | Construction | Adhesives | Water | Oilfield & Mining | Textile & Leather

Personal Care | Home Care | Nutrition & Health | Paper

No dependency on single industry cycle

Performance Products sales by industry* - % of sales in 2011

* Distribution by direct customers of BASF

Broad array of end markets

BASF Presentation June 2012 5

Sales development (in billion €)* Sustainable growth

Steady sales increase since 2005

Acceleration in 2009 through Ciba acquisition

2010 sales increase reflects strong demand

In 2011 sales growth was especially supported by the inclusion of Cognis

Dispersions & Pigments Paper Chemicals

Care Chemicals Performance Chemicals

* All data restated for 2009 segment portfolio

Performance Products: Steady sales growth

Nutrition & Health

7.0 7.7 8.1 8.1 9.4

12.3

15.7

BASF Presentation June 2012 6

Sales development of Performance Products by region* (in million €) 2011 vs. 2010

25%

Europe - our home market with well established market position

North America – position significantly strengthened by additional Cognis businesses

Asia - strongly positioned for further growth with investments in assets and R&D

Excellent basis for growth in South America, Middle East due to in-depth knowledge of industries and consumer requirements

Global reach and excellent basis for growth in emerging markets

North America 3,560 (+23%)

Europe 7,247 (+34%)

Asia Pacific 3,416 (+23%)

South America, Africa, Middle East 1,474 (+23%)

46%

22% 9%

23%

* By location of customer

15,697 (+27%)

BASF Presentation June 2012 7

Development of EBITDA before special items (in million €)

Performance Products: Business portfolio shaped to optimize cash generation

EBITDA bSI continuously improving even in crisis years 2008 and 2009

EBITDA bSI 2010 substantially increasing due to higher sales volumes, successful measures to Ciba integration and repositioning of the combined businesses

EBITDA bSI 2011 benefitting from Cognis inclusion and lower integration expenses

Strategic portfolio development paying off

Improved value generation through repositioning of businesses

0

500

1.000

1.500

2.000

2005 2006 2007 2008 2009 2010 2011

BASF Presentation June 2012 8

Customers need certain breadth of product/service offering but not complete customization

Customers can configure own packages

Numerous anonymous or shallow buyer-supplier relationships

Spot market behavior

Customers willing to partner with supplier to jointly develop solutions

Customers ask for customization of product/service to fulfill their specific needs

Customer prepared to share value jointly created

Achieve benchmark leading cost position Supply reliability is important buying factor Customers see differentiation in sustainability

Distinct customer interaction models help managing complexity

Trader/transactional supplier

Standard package provider

Customized solution provider

Lean/reliable basics supplier

Customers open to shift parts of their own value chain

Substantial transaction cost and risk reduction seen by customer

Value chain integrator

Customer interested in superior performance of products/services

High spending in R&D required to capture market needs

Customer pays for value created in innovation

Product/process innovator

Differentiated BASF Customer Interaction Models matched to customer needs

BASF Presentation June 2012 9

Lean/reliable basics supplier

Standard package provider

Product/process innovator

Customized solution provider

2011 % of the business

~40 ~30 ~25 ~5

BASF

Reliable quality supplier

Sustainable product offering

Benchmark cost leader

Broader portfolio of products & services for differentiation in the market place

Continuous stream of new products, systems and business models

Customer-specific cooperations to fulfill unmet consumer needs

Customer

Leverages market opportunities

Values quality, sustainability and reliability of offering

Values industry specific synergies & support

Values innovation contribution

Fairly shares value jointly created

Pricing Cost leader defines lowest price limit Supply / demand balance defines market price Mitigating volatility essential

Value created along the value chain compared to market standard defines price level

Product life cycle management essential

Differentiated Customer Interaction Models at BASF Performance Products

BASF Presentation June 2012 10

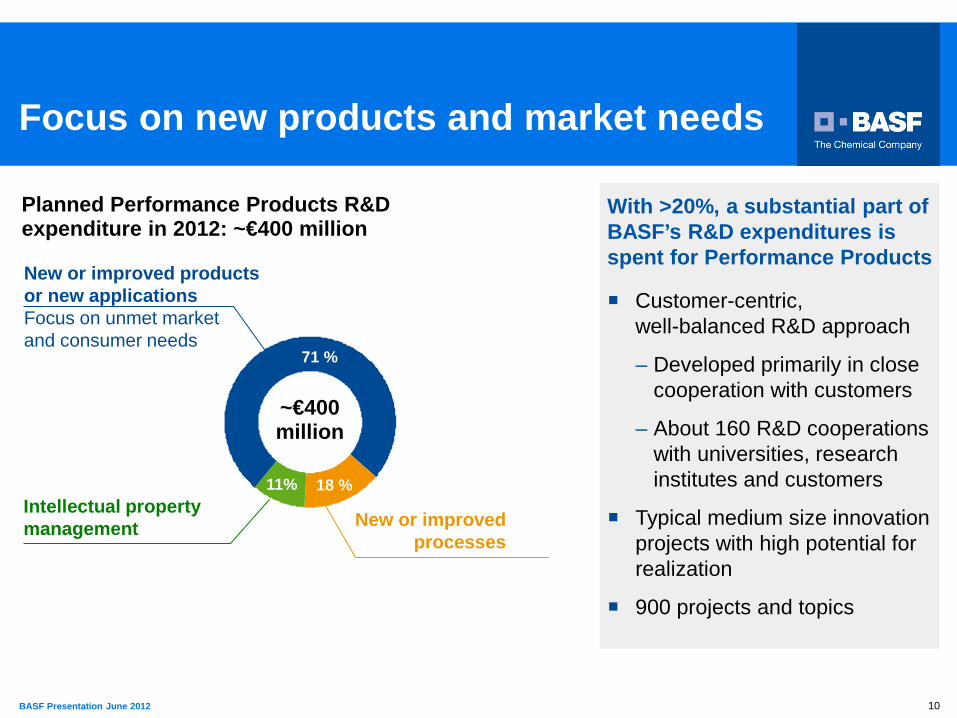

New or improved products or new applications Focus on unmet market and consumer needs

New or improved processes

71 %

18 %

Customer-centric, well-balanced R&D approach

– Developed primarily in close cooperation with customers

– About 160 R&D cooperations with universities, research institutes and customers

Typical medium size innovation projects with high potential for realization

900 projects and topics

With >20%, a substantial part of BASF’s R&D expenditures is spent for Performance Products

Focus on new products and market needs

Intellectual property management

11%

~€400 million

Planned Performance Products R&D expenditure in 2012: ~€400 million

BASF Presentation June 2012 11

Cetiol® RLF Light emollient for sensitive skin produced via an enzymatic process and solely derived from renewable feedstocks

L-Menthol New cost-effective and efficient production process for synthetic menthol used as an aroma ingredient Ecovio® FS Paper Biopolymer based on renewable resources to produce e.g. fully compostable drinking cups for hot and cold beverages

Irgaphor Red S 3620 CF High-performance organic pigment for an optimum contrast ratio in display applications

Rich R&D pipeline

Tinuvin® 1600 UV absorber for extremely demanding transparent outdoor plastic sheets, films and other thin-section applications

Multibore® Membrane Small-pore ultrafiltration membranes reliably remove suspended solids, bacteria, germs, viruses from polluted water

BASF Presentation June 2012

2

Formulation Additives

Further growth by capturing the full potential of our previous acquisitions

Market position

>10 5 Broad spectrum of

technologies with excellent market access to the coatings industry

Innovation power, deep formulation know-how, global production network & supply capability

Lubricant Solutions Mining Solutions Water Solutions

Market position

Leading provider of innovative chemical solutions to the Water industry worldwide

Bundling of membrane technology and chemical expertise

Market position Market position

n.a. >10 3 3 2 Unique position with

backwards integration, broad product portfolio and customer access

Synergies with fuel additives business to deliver superior fuel economy solutions

Globally strong position, esp. in Solid- Liquid Separation and Hydrometallurgy

Customer proximity with technical service

Promising R&D pipeline

2

BASF Presentation June 2012 13

BASF Performance Products: Today and into the future

Vision 2020 2011

13

Chemical industry leader to improve quality of life

Preferred partner for all performance & innovation driven customers

Comprehensive portfolio of value-adding and sustainable products and services

Earning a substantial premium on cost of capital every year in each division

Sales to 3rd parties € 15.7 billion

EBITDA bSI margin of 16.2%

Cognis integration cost of € 298 million

EBIT after cost of capital € - 119 million

BASF Presentation June 2012 14

This presentation includes forward-looking statements that are subject to risks and uncertainties, including those pertaining to the anticipated benefits to be realized from the proposals described herein. This presentation contains a number of forward-looking statements including, in particular, statements about future events, future financial performance, plans, strategies, expectations, prospects, competitive environment, regulation and supply and demand. BASF has based these forward-looking statements on its views with respect to future events and financial performance. Actual financial performance of the entities described herein could differ materially from that projected in the forward-looking statements due to the inherent uncertainty of estimates, forecasts and projections, and financial performance may be better or worse than anticipated. Given these uncertainties, readers should not put undue reliance on any forward-looking statements.

Forward-looking statements represent estimates and assumptions only as of the date that they were made. The information contained in this presentation is subject to change without notice and BASF does not undertake any duty to update the forward-looking statements, and the estimates and assumptions associated with them, except to the extent required by applicable laws and regulations.

Forward-looking statements

BASF Presentation June 2012 15

BASF Presentation June 2012 16

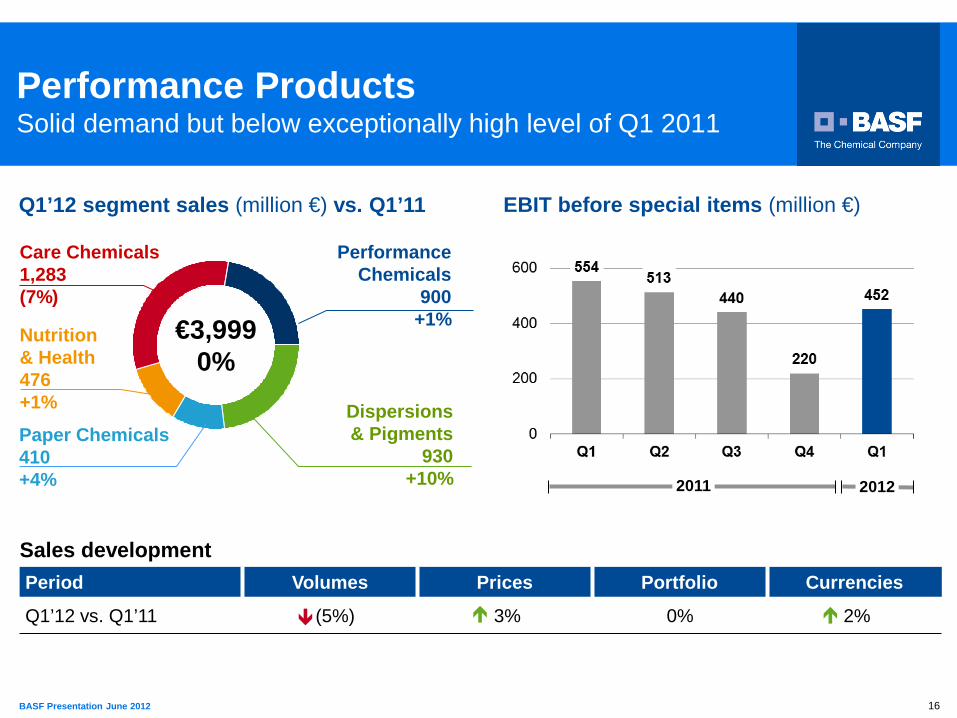

Performance Products Solid demand but below exceptionally high level of Q1 2011

Performance Chemicals

900 +1%

Care Chemicals 1,283 (7%)

€3,999 0%

Paper Chemicals 410 +4%

Q1’12 segment sales (million €) vs. Q1’11

Nutrition & Health 476 +1% Dispersions

& Pigments 930

+10%

EBIT before special items (million €)

2012 2011

Sales development Period Volumes Prices Portfolio Currencies

Q1’12 vs. Q1’11 (5%) 3% 0% 2%