Embed Size (px)

DESCRIPTION

Warsaw Business Journal, vol. 19, #13, 2013

Citation preview

VOLUME 19, NUMBER 13 • APRIL 8-14, 2013 . z∏.12.50 (VAT 8% included) . ISSN 1233 7889 INDEX-RUCH-332-127 Since 1994 . Poland’s only business weekly in English

WW

W.W

BJ.P

L

2, 4

Pass the gasConfusion erupts after Vladimir Putinorders Gazprom to build a gas pipelinethrough Poland 10-11

PPeennssiioonn ggrraabb??The government is reviewingPoland’s pension system, andis considering nationalizing theassets of some private funds 5

Will Germany lead?In an exclusive interview,Germany’s former foreignminister, Joschka Fischer,explains why his countryhas not provided theleadership needed to heal the EU’s woes 12-13

EEnnddlleessss wwiinntteerrPoland’s wintry spring weatherhas taken its toll on businessesand infrastructure, and couldmean floods in the near future 4

EA

ST

NE

WS

News . . . . . . . . . . . . . . . . . . . . . . .2-4

Business . . . . . . . . . . . . . . . . . . . .5-6

Finance & Economics . . . . . . . . . . .7

Exports in Focus . . . . . . . . . . . . . . .8

Interview . . . . . . . . . . . . . . . . .10-11

Cover Story . . . . . . . . . . . . . . .12-13

Opinion & Analysis . . . . . . . . . . . .14

Lokale Immobilia . . . . . . . . . .15-17

The List . . . . . . . . . . . . . . . . . . . . . .19

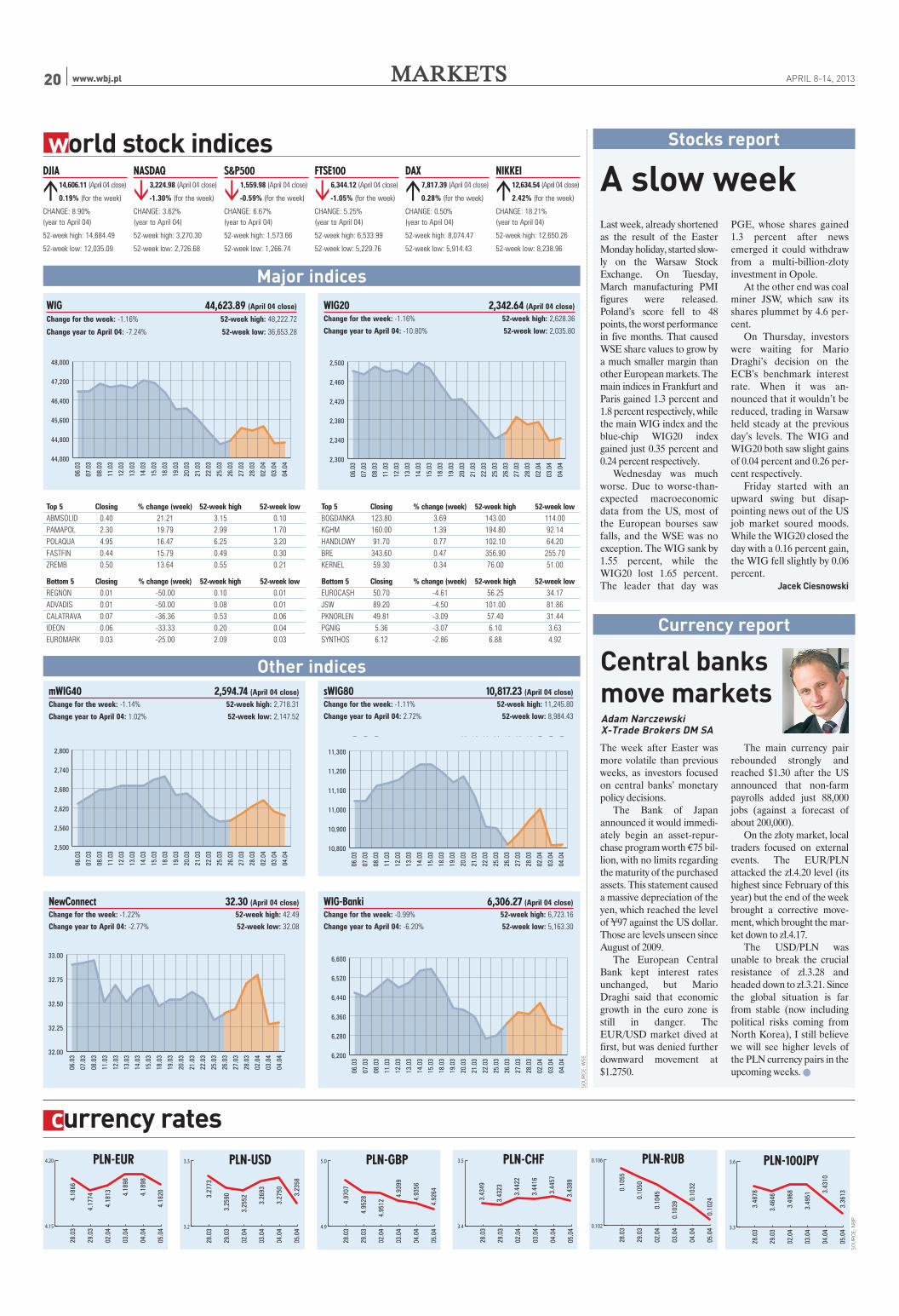

Markets . . . . . . . . . . . . . . . . . . . . .20

Sports . . . . . . . . . . . . . . . . . . . . . . .21

Lifestyle . . . . . . . . . . . . . . . . . . . . .22

Last Word . . . . . . . . . . . . . . . . . . . .23

In this issue

• Griffin in Powsin

• Qualia’s skyscraper

• Retail in small cities15-17

Made inPoland2013The latest

edition of

WBJ ’s

annual analysis

of Poland’s export

markets launches this

week 8

CO

UR

TE

SY O

F G

RIF

FIN

LLOOKKAALLEEIIMMMMOOBBIILLIIAARREEAALL EESSTTAATTEE

A new center-leftWBJ sat down with Marek Siwiec, co-leaderof Europe Plus, a new center-left politicalinitiative, to discuss its plans for the future

0

30,000

60,000

90,000

120,000

150,000

Lithuan

ia**

Czech R

epublic

Swede

nFra

nce

Poland

Germany

Ireland

United K

ingdom

Netherla

ndsMalta

*

* Highest in EU** Lowest in EU

APRIL 8-14, 2013NNEEWWSS2 www.wbj.pl

Transport

Minister

survives vote

of no-confi-

dence

Transport Minister

S∏awomir Nowak

survived a vote of no

confidence last Friday. A

motion suggesting his

dismissal had been filed

by opposition party

Solidarna Polska, and

supported by Palikot’s

Movement and the

Democratic Left

Alliance, who argued

that he is responsible

for the poor condition of

roads and railways.

Billionaire

Barbara

Piasecka-

Johnson dies

Polish-born Barbara

Piasecka-Johnson, one

of the world’s richest

women, died on April 1.

She was 76. Ms

Piasecka-Johnson was

the third wife of John

Seward Johnson, the

son of the founder of

Johnson & Johnson, and

inherited a large part of

his fortune after his

death. Her assets were

recently valued by

Forbes at $3.6 billion.

Horse

painkiller

found in meat

from Poland

Czech veterinary

inspectors confirmed

that they found traces of

a horse painkiller in

Polish horse meat sold

in the country. The drug,

phenylbutazone, which

may be harmful to

humans, was found in

meat which came from

the Polish supplier.

PGE

withdraws

from Opole

project

Poland’s largest utility

PGE has decided to

withdraw from its plan

to build new units at its

Opole power plant. The

company said that

changes in the energy

market and

macroeconomic

conditions have limited

the profitability of the

project and that

continuing it would not

create value for PGE’s

shareholders. The

contract was worth

z∏.9.4 billion. ●

Air France ..........................5

Albright Stonebridge Group..13

Allianz ..............................15

Asseco ................................8

Automatic Labs ................23

B+R Studio ..........................8

Bank Millennium ................6

Bank Pekao ......................16

BBI Development..............15

Biedronka..........................16

Blackstone ........................15

British Airways ..................5

Castorama ........................16

CCC ....................................4

CEPD Management ..........16

Colliers........................16, 17

Comarch ............................8

Cushman & Wakefield......15

Cyfra+..................................6

Cyfrowy Polsat ....................6

Elektrim ............................15

Enea ....................................6

Eurolot ................................5

EuRoPol Gaz ......................4

Gaz-System ........................4

Gazprom..............................4

GLL....................................15

Google ................................8

Griffin Group ....................16

Grupa Capital Park ..........16

GTC....................................17

H&M..................................17

Hannover Real Estate ......15

Hines ................................15

HSBC ..............................7, 8

IBM......................................8

Imtech Polska ..................16

Inglot ..................................8

Invesco ..............................15

Johnson & Johnson ..........2

Jones Lang LaSalle..........15

JSW ..................................20

KGHM..................................6

Kulczyk Silverstein

Properties ........................15

Kury∏owicz & Associates..15

Lidl ....................................16

LOT ......................................5

Lufthansa............................5

Macro Cash & Carry ........16

Marriott ............................15

Media Expert ....................16

Microsoft ............................8

“n” ......................................6

NAC ..................................21

nc+ ......................................6

NEPI ..................................15

Nordea Bank ......................6

Norges ..............................15

Parrot ................................23

PGE ..........................2, 6, 20

PKO BP ........................6, 15

Polpharma ..........................8

PRC Architekci..................16

Prologis ............................15

PZL Mielec..........................8

PZL-Âwidnik ......................8

PZU ..................................15

Qualia Development ........15

Qumak ..............................16

Randstad Polska ..............16

Skanska ............................15

Tauron ................................6

Tebodin..............................16

The Hines Global Reit ......15

Transport Consultants

Group TOR ..........................5

Warsaw Stock Exchange2, 20

X-Trade Brokers ..............20

April 10, 2013 will mark thethird anniversary of the cata-strophic plane crash inSmolensk, Russia whichclaimed the lives of PresidentLech Kaczyƒski and 95 others,including Poland’s militarychiefs and many top politi-cians. But after briefly unitingthe nation in grief, the disasterhas since turned into one ofthe most significant wedgeissues in Polish politics.

Jaros∏aw Kaczyƒski, twinbrother of the late presidentand leader of Poland’s biggestopposition party, Law and Jus-tice, has accused Prime Minis-ter Donald Tusk of complicityin Lech Kaczyƒski’s death,openly suggesting that therehad been a conspiracy toassassinate his brother involv-ing Mr Tusk and Russia’s pres-

ident Vladimir Putin. A Polish investigative com-

mission found the causes ofthe crash to have been piloterror and negligence on thepart of the Russian air-con-trollers in Smolensk.

This year’s commemora-tions are set to provide furtherevidence of the rift theSmolensk catastrophe has cre-ated in Poland.

When Donald Tuskannounced that he would bemaking an official trip to Nige-ria on April 10, many Law andJustice politicians reactedangrily, accusing the primeminister of everything fromcowardice to malice. JoachimBrudziƒski, an MP from theconservative opposition party,said Donald Tusk, “most prob-ably has a guilty conscience

and the fact that he is runningoff with his tail between hislegs is typical.”

However, Mr Tusk is expect-ed to lay a wreath at the monu-ment to the Smolensk planecrash victims in Warsaw’sPowàzki cemetery early in themorning on April 10, justbefore his flight. MeanwhileLaw and Justice plans to holddemonstrations and prayermeetings, as well as attend spe-cial commemorative masses onApril 10.

Government ministers andMPs from all parties will beattending some of those mass-es. Asked who had decided onApril 10 for his visit to Nigeria,Mr Tusk said it had been theNigerian side, adding that thedate was “unfortunate.”

RReemmii AAddeekkooyyaa

48.0was the value of Poland’s manufacturing PMI index in

March 2013, its lowest level in five months.

450%is by how much trade on the natural gas market of thePolish Power Exchange increased in March, compared

to February.

211were the number of bankruptcies of Polish companiesin the first quarter of 2013, the highest number since

the first quarter of 2005, according to data fromCoface.

5:05 pmwill be the new time for the close of trade on the

Warsaw Stock Exchange, starting April 15. Currently,trade closes at 5:35 pm.

“We should just say: ‘We’re not entering ERM II.If you want us in, invite us without that

requirement.’ Is that chutzpah? You bet it is.”National Bank of Poland head Marek Belka, during a debate last week on theterms of Poland’s eventual entry into the euro zone.

Quote of the Week

The politics of gasRussia’s Vladimir Putin has proposed building a new naturalgas pipeline through Poland. How could this affect Poland’srelationship with Russia and what would be the geopoliticalconsequences of such a project, if the Polish governmentagrees to come on board? Long on to WBJ.pl to read geopo-litical analysis firm Stratfor’s take on the issue.

On WBJ.pl

Numbers in the News

Company index

SH

UT

TE

RS

TO

CK

9-10 OFFICEDAYSEvent: This fair is designed for four main groups of

attendees: office managers and personsresponsible for ordering equipment andoffice services; developers, owners andmanagers of office buildings; architects andinterior designers; and IT specialists respon-sible for company hardware.

Location: WARSAW EXPO XXI Centre, ul. Pràdzyƒskiego 12/14, Warsaw

Web: www.officedays.pl

10 MADE IN POLAND CONFERENCEEvent: Journalists, entrepreneurs and officials will

discuss Polish exports – their successes,challenges and impact on the Polish economy.

Location: National Stadium, Al. Poniatowskiego 1, Warsaw

17-21 FASHIONPHILOSOPHY FASHION WEEK POLAND

Event: The spring edition of the biggest fashion eventin Central and Eastern Europe. This timedesigners from the region will present theirideas for their autumn/winter collections.

Location: ¸ódê Special Economic Zone, ul. Tymienieckiego 22/24, ¸ódê

APRIL 30-MAY 2ANNUAL INVESTMENT MEETING

Event: AIM is the Middle East’s first Emerging Mar-kets FDI-focused event to offer a perfectblend of trade fair and intellectual featuresaimed at enriching institutional, corporateand individual investors attending with acomprehensive set of guidelines for theirfuture investment decisions in high-growthregions.

Location: Dubai International Convention and Exhibition Center, Dubai, UAE

Web: www.aimcongress.com

April

Calendar

The third anniversary of

the Smolensk disaster

IN THE SPOTLIGHT

Figures in focusLand of milk and honeyHow much a hectare of agricultural land costs in selected EUstates (in €)

Sources: Eurostat, ARiMR

APRIL 8-14, 2013NNEEWWSS4 www.wbj.pl

Weather

CCoouulldd AApprriill ssnnooww sshhoowweerrss bbrriinngg MMaayy ffllooooddss??

The threat of floods in thefirst weeks of May is loomingover southeastern Poland.Flood warnings have alreadybeen issued in towns and vil-lages along the Bug River.The southeastern voivod-ships Podkarpackie, Âwi´-tokrzyskie and Lubelskiemay experience some flood-ing in the near future, whenthe snow begins to melt. Andthaw is indeed coming, withweather forecasts putting thisweek’s temperatures in thevicinity of 10 degrees Celsius.

Experts say, however, thatthere is no reason for worry.“The winter is indeed snowy,but not frosty. This meansthere is not much ice onrivers making it difficult forthe water to flow,” ArturMagnuszewski, a hydrologyprofessor at the University ofWarsaw told TVN24. MrMagnuszewski also said thatneither a sudden warming orintense rainfall are expected

in the coming weeks, whichare the biggest threats whenit comes to floods.

Transport and infrastructure snowed under The unseasonable weather isalso taking its toll onPoland’s infrastructure. Dur-ing the Easter weekend, theexceptionally wet, heavysnow left some 100,000 Poleswithout power, when treebranches snapped under theweight and broke severalpower lines in centralPoland.

Hundreds of flights havebeen canceled or delayed dueto poor weather conditions.Despite deploying 1,100snowplows, driving condi-tions in Poland remained dif-ficult. During the Easterweekend, accidents claimedthe lives of 16 people and left232 injured. Local authori-ties are worried about the

strain the continuing effortsto clear roads is putting ontheir budgets.

Winter is a dangerous sea-son in Poland, and not onlyfor drivers. According to theMinistry of Internal Affairs,29 people froze to death inMarch alone. Since thebeginning of the winter sea-son 180 have died ofhypothermia and 88 of car-bon monoxide poisoningcaused by faulty heatinginstallations.

Heavy snow, heavy losses The financial repercussionsof the snowy spring gobeyond costly road mainte-nance, though. Clothes andfootwear manufacturers arestruggling as a result of thelong-lasting winter weather.At a time when they usuallyearn more on new spring col-lections, they now have lowerturnover and lower margins.Piotr Nowjalis, deputy CEOat shoe retailer CCC, toldbusiness daily Parkiet thatthis year’s March sales valuewas 20 percent lower than

last year’s.The entire economy is

experiencing a protractedslowdown due to the unfa-vorable and harsh weatherconditions. With seasonalwork delayed, one should notexpect unemployment to fallin March, as it usually does.

The jobless rate is expectedto start declining in April,though, deputy Labor Minis-ter Jacek M´cina said.

The unseasonably wintryweather in the beginning ofApril is highly unusual, butnevertheless has frustratedPoles who are anxious for

spring to begin. “Our climate and our

weather are very varied,” MrMagnuszewski told TVN24,adding that there is no rea-son to expect that this kind ofweather will become com-monplace in the future.

BBeeaattaa SSoocchhaa

The unusually long and snowy winter hasalready wreaked havoc, causing power outages,road collisions and incurring heavy losses forthe Polish economy

SH

UT

TE

RS

TO

CK

The wintry conditions made holiday driving especially treacherous

Pipelines

Russia moots new gasline through PolandThe Polishgovernment says itwon’t play Russia’s“political games”

Confusion arose last Wednes-day after media reported thatRussian President VladimirPutin had ordered state-owned gas distributor Gaz-prom to consider buildinganother section of the Yamalnatural gas pipeline that wouldgo through Polish territory,bypassing Ukraine. Gazprom’sCEO Alexei Miller said thatthe new part of the pipelinecould be in operation by asearly as 2018.

The Polish governmentseemed taken aback by thenews. Treasury MinisterMiko∏aj Budzanowski criticizedthe proposal, and stressed thatany decision on whether a newpipeline would go throughPoland was solely the purviewof the Polish government.

“No one, except for thePolish company and the Polishgovernment, is entitled tomake decisions about transitvia Polish territory,” he said.

However, Deputy PrimeMinister and Economy Minis-

ter Janusz Piechociƒski toldPolish Radio on Thursday thatPoland could benefit fromsuch a deal.

Then on Friday, before thegovernment could articulate acoherent position, Mr Millerand the Polish CEO of Russ-ian-Polish pipeline operatorEuRoPol Gaz, Miros∏awDobrut, signed a memoran-dum stating that the two partieswould jointly asses whether anew gas line running throughPoland’s territory was techni-cally and economically feasible.

Polish politicians wereunwilling to make any publicstatements until the situationhad been clarified, with evenPrime Minister Tusk refusingto address the issue. It tookgovernment representativesthe better part of Friday to gettheir story straight.

Polish Treasury MinisterMiko∏aj Budzanowski said at along-awaited press conferencethat no formal agreement hadbeen entered into and addedthat the memorandum be-tween EuRoPol Gaz andGazprom “is clearly technicalin nature and only pertains toa transfer of information.”

Just a pawn?The announcement of thenew pipeline came only twodays after Ukrainian Energyand Coal Industry Ministrystated that Ukraine had notbroken any laws by progres-sively decreasing its gas pur-chases from Russia whileincreasing them from Hun-gary. That issue is only one ofseveral bones of contentionin a lengthy Russian-Ukrain-ian dispute over gas quotasand payments. Analystsbelieve that Mr Putin’s pro-posal was a veiled threat toKiev that Moscow could stilldeliver gas to customers whilecutting off the taps inUkraine.

But the Polish governmentwas reluctant to cooperatewith Russia’s apparent strong-arm tactics. “Poland will notparticipate in such politicalgames, for us gas is not a polit-ical instrument and we reallywant, as per EU regulations,to keep gas issues free frompoliticking,” Polish PrimeMinister Donald Tusk said Fri-day afternoon.

BBeeaattaa SSoocchhaa,,KKaammiillaa WWaajjsszzcczzuukk

International

Idle threats of an idle dictator?As Pyongyang rattlesits sabers, Polandencourages NorthKorea to “abstainfrom provocativemoves”

Last week’s news was domi-nated by reports of NorthKorean saber-rattling and thecountry’s preparations to go towar with its southern neigh-bor. And while the US contin-ues to send troops and equip-ment to the Korean peninsula,experts agree that Pyongyang’smoves are little more thanpropaganda.

Nevertheless, the risingtensions have sparked fears ofa war on the Korean peninsu-la, or an even wider conflict.And the rhetoric coming outof North Korea is at its mostbellicose in years.

A statement posted on thewebsite of the North Koreanembassy in Poland reads,“Kim Jong-un has made adecision to declare a life-and-death battle that will ensure anepoch-making opportunity toput an end to an ongoing clashwith the US, and to start a newera. This is the final warning tothe US and South Korea.”

When asked by a reporter

from TVN24 to comment onthe statement, one of theemployees of the embassy saidthat Pyongyang was onlyresponding to “aggressiveattacks” from the “other side.”

“We haven’t declared war,our actions are merely pre-emptive,” the unnamed sourceform the embassy said. Thesource concluded the state-ment, however, with the omi-nous: “We’re ready to counter-attack.”

Polish diplomats to stayin Pyongyang, for nowThe Polish Ministry of ForeignAffairs claims there is no needto evacuate Poland’s embassyin North Korea. The ministry’s

press officer, Marcin Bosacki,said that evacuation may beconsidered if the situation getsworse, though.

Mr Bosacki also confirmedthat there are currently no Pol-ish citizens in North Koreaapart from the embassy staff.Only one other Pole lives inthe country, but he is currentlystaying in Poland, Mr Bosackiexplained.

Mr Bosacki also added that“the Ministry of ForeignAffairs appeals to Pyongyangto abstain from drastic andprovocative moves. We ask[North Korea] to return topeace talks and comply withbinding UN resolutions.”

JJaacceekk CCiieessnnoowwsskkii

SH

UT

TE

RS

TO

CK

The increasingly bellicose rhetoric coming out of North

Korea has the world on edge

Warsaw Business Journal PDF version and a link to view WBJ in e-zine format delivered to your e-mail address each week for 12 months.

Choose one option by checking the box

OPTION 1

Warsaw Business Journal print edition delivered each week to your address for 12 months, plus receive Investing in Poland 2012 (zł.78 value) and Book of Lists 2012 (zł.100 value).

Warsaw Business Journal print edition delivered each week to your address for 12 months, plus WBJ PDF version and a link to view WBJ in e-zine format delivered to your e-mail address each week. Also receive Investing in Poland 2012 (zł.78 value) and Book of Lists 2012 (zł.100 value).

CLIENT DETAILS

Name......................................................................................................................Company......................................................................................................................Address......................................................................................................................Postal code......................................................................................................................City......................................................................................................................Country......................................................................................................................Telephone/Fax......................................................................................................................e-mail......................................................................................................................NIP (Poland)/EU VAT number (EU countries)......................................................................................................................

Please fax this form to: +48 22 639 85 69 or mail it to our office: Subscriptions Warsaw Business Journal Valkea Media S.A. ul. Elblàska 15/17, 01-747 Warsaw, Poland

PAYMENT OPTIONS (please check one)

❏ Pre-payment by bank transfer upon receipt of a pro-forma invoice. The pro-forma invoice will be sent to you immediately upon receipt of your order. Your subscription will start within one week of payment.

❏ Credit card: ❏ American Express ❏ Visa ❏ Mastercard

Cardholder name

......................................................................................................................Number

......................................................................................................................

CVV2/CVC2/CID Expiration date

....................................................... ............................................................

Signature

......................................................................................................................

SUBSCRIBE FOR 1 YEAR AND SAVE UP TO 50% OFF THE COVER PRICE

Wafor

[email protected], OR CALL +48 (22) 678-9912

Everywhere: zł.424

In Poland: zł.550 In Europe: €297 Outside Europe: €374

In Poland: zł.691 In Europe: €330 Outside Europe: €407

WBJ IS NOW AVAILABLE IN DIGITAL FORMAT.READ WBJ AS A PDF OR E-ZINE.

❏

OPTION 2❏ WBJ Print

OPTION 3❏ WBJ PremiumWBJ Electronic

One expert saysBritish Airways couldbe the frontrunner toacquire the troubledPolish airline

Poland’s government hasadopted a draft law that ismeant to pave the way for theprivatization of the country’snational air carrier, LOT Pol-ish Airlines. The new regula-tion will enable the State Trea-sury to sell a majority stake,while under current legislationit is obliged to keep a 51 per-cent share in the airline.

LOT’s privatization is partof a deep restructuring processin the company, Treasury Min-ister Miko∏aj Budzanowskisaid last week. Offering amajority stake will give theTreasury the option of sellingLOT to a stable, strategicinvestor, he added.

Polish law is not the onlyobstacle to selling the nationalair carrier. According to EUlaw, at least 50 percent of anyEuropean airline must beowned by an EU memberstate, or a citizen thereof.

That, however, likely won’tbe a problem. “I expect thatone of the big three Europeanairlines (British Airways,Lufthansa and Air France) will

buy LOT. This would makemore sense from an economicstandpoint,” Adrian Furgalski,from Transport ConsultantsGroup TOR, told WBJ.

He added that in his view,British Airways is the fron-trunner. “They were alreadyconsidering buying LOT twoyears ago, and now finally theywill have a legal framework inplace to do so.”

First the sale,and then what?The sale will be possible aftera drastic rescue plan for LOTis implemented, cutting hun-dreds of jobs and offloadingsome of the airline’s planes.

“Only when the company isin better shape will there beany potential buyer interestedin the acquisition,” explainedMr Furgalski.

“But even when we do sell,we have to realize that theTreasury won’t be able to gettoo much money from thesale. We really should behappy that the brand LOTwill continue to exist after thesale,” Mr Furgalski contin-ued.

If another airline buysLOT, experts assume it willincorporate internationalroutes operated by LOT intoits own flight network, whiledomestic flights will still becarried out by a smaller Polishcarrier, Eurolot, owned byLOT and the Treasury.

The Treasury wants to buyout LOT’s stake in Eurolot,which would help secure thenecessary funds to keep LOTafloat, and then sell it in apackage deal along with LOT.

JJaacceekk CCiieessnnoowwsskkii

Airlines

Treasury prepares to sell LOT

APRIL 8-14, 2013 BBUUSSIINNEESSSS www.wbj.pl 5

The government isreviewing a revamp ofPoland’s pensionsystem that couldeventually see privatepension fundsnationalized

Media reports suggestingthat the government is con-sidering shifting roughlyz∏.125 billion in treasurybonds held by private pen-sion funds (OFEs) to thestate budget has sparked anoutcry and speculation thatthe government may be con-sidering getting rid of OFEsaltogether. Poland’s pensionsystem combines a state-con-trolled pay-as-you-go compo-nent with state-guaranteedOFEs that receive part ofemployees’ pension contribu-tions each month.

The government hastaken aim at OFEs to shoreup the budget before. In2011, it cut the share ofemployees’ contributions toOFEs to 2.3 percent of grosswages from 7.3 percent. Thisyear, the transfers rose to 2.8percent of wages, but this isstill less than half the previ-

ous share.Diverting the treasury-

bond holdings into the budg-et would reduce public debtand lower Poland’s annualdebt-servicing costs. FinanceMinister Jacek Rostowski haspledged that by 2015 Polandwill bring down its publicdebt to 50 percent of GDP.After the third quarter of2012, that figure stood at 55.9percent, according to Euro-stat.

No doctrineDaily Gazeta Wyborcza, quot-ing an anonymous governmentofficial, said Prime MinisterDonald Tusk’s government iscurrently considering furthercutting the share of salariestransferred to OFEs.

Moreover, in the future,OFEs might be restricted toinvesting their funds solely instocks, according to thereports. In response, theprime minister acknowl-edged that the pension sys-tem is being “reviewed” atthe moment.

“We will analyze the con-clusions drawn from thatreview, as well as the propos-als of experts and politicians

regarding the future ofOFEs,” said Mr Tusk. “Wehave no doctrine. There is nosecret plan to liquidateOFEs, nor is there a doctrinethat says OFEs must remainat all costs,” he added.

The PM said that the gov-ernment would present itsproposals on the future ofPoland’s pension system inMay.

A misunderstandingCommenting on the issue,Deputy PM and Finance Min-ister Jacek Rostowski insistedthe government does not haveplans to do away with privatepension funds. However, healso responded angrily to arecent proposal from OFErepresentatives suggesting thepension-payment period bereduced to 10 years, insteadof for the remainder of a pen-sioner’s lifetime, as is the casecurrently.

“Life-long pensions willbe paid from the funds thatOFEs have accumulated intheir accounts over the last15 years,” said Mr Rostowski,calling the proposal a “mis-understanding.”

RReemmii AAddeekkooyyaa

Pension funds

Government consideringpension-fund asset-grab

CO

UR

TE

SY O

F L

OT

Soon to be sold?

APRIL 8-14, 2013BBUUSSIINNEESSSS6 www.wbj.pl

Nuclear energy

The wait continues on Poland’snuclear power programAnother deadline –this one for agreeingon terms for aconsortium to fundconstruction – haspassed with noprogress

Over six months have passedsince the state-run energyfirms PGE, Tauron and Enea,as well as state-owned mininggiant KGHM, signed a letterof intent to buy into PGE EJ 1,a company established for thepurpose of building a nuclearfacility in Poland. The date forthe signing of an agreement –

the second after the first dead-line was missed – passed againin March, with no deal. As ofpress time, no new deadlinehad been set.

While it is known thatPGE, Poland’s largest electric-ity producer, will hold themajority share, how mucheach of the other state-ownedgiants will own is stillunknown.

Poland’s nuclear power-plant project has faced diffi-culties from its outset. Origi-nally planned to come onlinefully in 2020, the date that hasnow been officially set for thefirst of two plants to begin

operations is 2023. That plantis set to come fully online in2025, with a generation capac-ity of 3,000 megawatts. A sec-ond plant of roughly the samecapacity is planned to comeonline by 2029.

The biggest issue holdingup the program is its cost. Lastyear PGE chief executiveKrzysztof Kilian said publiclythat Poland would have tochoose between investing innuclear power or in shale gas.In February, Treasury MinisterMiko∏aj Budzanowski saidthat constructing a nuclearplant might be too costly forPoland, especially in view of

the economic slowdown. Thereafter, Prime Minister

Tusk held a meeting with MrKilian to discuss the future ofthe program. “Poland is by nomeans abandoning plans tobuild a nuclear power plant,”said Mr Tusk after the meet-ing, rebutting rumors that theprogram might be suspended.

“We expect governmentagencies and PGE to come upwith a responsible solutionthat will allow Poland to takeadvantage of the safest andmost cutting-edge nucleartechnology,” he added.

But precisely how much theprogram will cost is an openquestion. Estimates for thefirst plant vary between z∏.35billion and z∏.60 billion (about€9 billion-€15 billion).

PGE was due to hold a ten-der for the construction anddelivery of the plant by the endof March as well. That was adeadline that had also beenpushed back, originally fromthe first quarter of 2012. It isnot known when PGE willhold the tender, but it will like-ly have to sign the consortiumagreement with the otherstate-owned firms first.

JJaacceekk CCiieessnnoowwsskkii

Media

New satellite platformearns ire of subscribersA merger of twosatellite TV operatorswas supposed tobring viewers the bestprogramming fromboth. Instead, itsparked an outcryfrom subscribers

When the merger of satelliteplatforms Cyfra+ and “n”was announced back inNovember 2011, officialshailed the expanded offer ofsports and movies that thenew platform would provide.Eighteen months later, afterwaiting for regulators toapprove the deal and discus-sions on how it would oper-ate, the new platform –dubbed “nc+” – waslaunched.

But the claims of “the bestsport and cinema on Polishmarket,” haven’t convinced alarge number of subscribersfrom both platforms. Manywere unimpressed, and evenangry, at the new channeloffer and pricing policy. Inboth the Cyfra+ and “n”platforms, viewers were ableto buy special packages withpremium channels for z∏.20-

40 per month. But in nc+, acomparable package costsmore than double that. The“CANAL+ Silver” package,for example, comes to a totalof z∏.109 monthly.

The vociferous protestsforced nc+ officials intodamage-control mode, but itwas too little too late. A Face-book page protesting thechanges (“Anty NC+”)quickly gathered nearly70,000 likes. The president ofnc+, Julien Verley, invitedthe creator of the page,Dawid Zieliƒski, to discussthe issues protesters havewith the new platform. MrZieliƒski declined the offer,but sent a long list of ques-tions, demands and sugges-tions.

A few top nc+ executiveseven lost their jobs over thefuror. Some of these appar-ently left of their own volition,in protest against the compa-ny’s “aggressive approach”towards existing customers,several Polish media reportedunnamed sources inside thecompany as saying.

This “aggressive appr-oach” got the attention ofPoland’s consumer and com-

petition regulator, UOKIK,which has said it will investi-gate the matter.

“After preliminary analysiswe are concerned withactions to change existingagreements in a one-sidedfashion, and automaticallyreplacing existing Cyfra+ and‘n’ contracts with new ones,”the regulator said in a state-ment. If found in violation ofconsumer protection laws,the company could be finedas much as 10 percent of lastyear’s revenue.

Cyfra+ and “n” togetherhave 2.5 million subscribers.Market leader Cyfrowy Pol-sat has over 3.5 million sub-scribers.

JJaacceekk CCiieessnnoowwsskkii

PKO BP eyestakeovers inCentral Europe

Poland’s largest bank PKO BPis looking for takeovers, if notin Poland then within theregion, the bank’s CEO, Zbig-niew Jagie∏∏o, said at a pressconference last week.

“There are several foreignentities that will be interestedin exiting, or will be forced toexit, the market,” he said.

The bank listed acquisi-tions as one of the goals of itsdevelopment strategy for2013-2015. It plans to reservecapital and monitor the mar-ket for potential targets. PKOis interested in buying small

and medium-sized banks, andhas reportedly been in the run-ning to buy Nordea Bank’sPolish arm, and Bank Millen-nium, the Polish outfit of Por-tuguese bank Millennium bcp.

Much of the lender’s strate-gy is also focused on organicgrowth and improving cus-tomer service. The lenderwants its assets to grow by 4-5percent annually. PKO alsosaid its targeted return-on-equity is above 15 percent andcost-to-income ratio below 45percent.

KKWW,, AAKK

CO

UR

TE

SY O

F F

AC

EB

OO

K.C

OM

/AN

TYN

CP

LU

S

The “Anty NC+” page on

Facebook quickly gath-

ered 70,000 likes

CO

UR

TE

SY O

F P

KO

BP

PKO BP headquarters in Warsaw

Support for nuclear?It’s unclear how much support the project hasamong the Polish populace. While Poles cer-tainly favor nuclear power more than some oftheir Western European counterparts, anApril 2011 poll (just after Japan’s Fukushimadisaster) found 53 percent of Poles wereopposed. However, in December last year, agovernment-funded poll during a nuclearpower promotion campaign found that 56percent of Poles were in favor.

The residents of Mielno, which is locatedclose to the Baltic coast town of Gàski, one ofthe proposed sites for the first nuclear power

plant, held a referendum on the subject.Ninety-four percent of residents voted againsthosting the plant.

˚arnowiec and Choczewo, also on theBaltic Sea, are the other two shortlisted loca-tions. Support for construction is said to behigher in these towns, especially in˚arnowiec, where another nuclear powerplant was due to be built under the commu-nist regime. Those plans were discarded afterthe Chernobyl disaster.

A decision on where the plant will be builtcould take as long as two years. ●

DAILY EXECUTIVE DIGEST

S i g n u p f o r a 2 - w e e k f r e e - t r i a l ! w w w. p o l a n d a m . p lG e r m a n v e r s i o n : w w w. p o l e n a mm o r g e n . p l

Poland A.M. gives you the biggest Polish stories of the day.

Have the most valuable news delivered to your inbox each weekday morning.

APRIL 8-14, 2013 FFIINNAANNCCEE && EECCOONNOOMMIICCSS www.wbj.pl 7

Euro zone

Belka suggests Poland shouldadopt euro without ERM IIThe NBP presidentsaid Poland needs the“chutzpah” to demandit be allowed inwithout the criterion

President of the NationalBank of Poland Marek Belkasaid last week that Polandshould try to convince EUleaders to allow it to join theeuro zone without the

required two-year member-ship in the ERM II.

“I think we should publiclyspeak about this being a veryserious barrier that could pre-vent a country such as Polandfrom joining the euro zone,”he said.

Poland has a large curren-cy market, he explained, so itshould be able to say it doesnot want to join the exchange-rate mechanism.

“We have a big currencymarket and we should justsay: ‘We’re not entering ERMII. If you want us in, invite uswithout that requirement.’ Isthat chutzpah? You bet it is.”Mr Belka said.

Mr Belka added that theERM II is unfavorable forPoland, since it paves the wayfor currency “speculation.”He said that he understandsthat the criteria are part of a

treaty but that he believesthere could be some flexibili-ty.

The ERM II is known asthe euro’s “waiting room.” Itis a mechanism by which acountry’s currency is moni-tored for two years duringwhich it is not allowed tobreak certain thresholds, withthe aim of ensuring a stableexchange rate.

KKWW

PMIlowestin fivemonthsThe Purchasing Managers’Index (PMI) for Poland’s man-ufacturing sector fell to 48points from 48.9 points inFebruary, reaching its lowestlevel in five months, HSBCsaid in a statement on Tuesday.The decline in PMI is an indi-cation of a prolonged down-turn in the Polish industry.

HSBC economist AgataUrbaƒska said that the resultwas disappointing and “high-lights that the bottoming outof the 2012 slowdown contin-ues to be questionable notmentioning that it under-mines chances for a firmrecovery through 2013.”

“The number of neworders received by Polishmanufacturers fell for thefourteenth consecutive monthin March. ... The pace ofdecline in new export orderswas the fastest since Novem-ber,” HSBC said in thereport.

The volume of productionslid for the 11th month in arow and at the fastest pacesince November amidreduced orders, with the paceof price reduction accelerat-ing to a historic high.

Production costs fell forthe seventh time in the lastnine months, at the fastestpace since June 2009, thereport authors added.

“The level of employmentin the production sector con-tracted for the seventh monthin a row in March, making itthe longest decline period inover three years. Producersreduced the purchases capitalgoods at the fastest pace sinceSeptember 2012,” HSBC said.

A PMI reading above 50indicates expansion in the sec-tor, while one below 50 sig-nals contraction.

AASS,, KKWW

CO

UR

TE

SY O

F T

HE

NB

P

Mr Belka said that the ERM II could invite “speculation”

APRIL 8-14, 20138 www.wbj.pl EEXXPPOORRTTSS IINN FFOOCCUUSS

Trade

Poland driven by exportsThough painful and costly, theglobal economic crisis mayhave been a blessing in dis-guise for Polish exporters. Inthe period between 2008-2012,the value of Polish exportsincreased by 22 percent, or€25.7 billion. Last year alonePoland exported nearly €142billion worth of products,according to preliminary datacompiled by Poland’s statisticsoffice, a record high and anincrease of 6.9 percent y/y.

Poland’s most popularexport sectors include: food(exports of which rose by 14.8percent y/y), ceramics (12.4percent), minerals (5.4 per-cent) and chemicals (4.9 per-cent), although when it comesto value, the electrical machin-ery sector is by far the leader,with some €55 billion worth ofproducts exported in 2012.That leaves chemicals (€19.8billion), foodstuffs (€17.5 bil-lion) and metallurgy (€16.6billion) far behind.

Looking in a differentdirectionThe euro zone crisis hasforced Polish exporters to findalternative markets. The valueof goods sold to the EU has

decreased by 0.9 percent,although it’s still by far thebiggest export destination with€107.5 billion worth of prod-ucts being sold there in 2012.Nevertheless, Polish exportersare hoping new markets canhelp make up the difference.

Exports to developing andless-developed countries,while still small compared toexports to developed markets,rose by 19 percent andreached €25.5 billion. Russia isthe driving force among thesecountries, with €8 billionworth of Polish goods export-ed there.

Additionally, Poland’s Min-istry of Economy has selectedfive potential destination mar-kets for Polish products: Cana-da, Brazil, Algeria, Kaza-khstan and Turkey.

“Right now, these coun-tries account for 2 percent ofPolish exports, and with theirbig potential, macroeconomicstability and huge markets,they can become major desti-nations for Polish export,” theministry wrote in a statement.

According to forecasts byHSBC and Oxford Econom-ics, Asia will see an increase inPolish products. In 2013-2015exports to India, Vietnam andSouth Korea should increaseannually by 21, 18 and 17 per-cent respectively, and will con-tinue to grow even further inlater years.

But despite all the changein economies worldwide, andin the EU in particular, Ger-many remains the country thatimports the most from Poland– €35.7 billion of goods wasexported there (the samevalue as the year before),while the United Kingdom(€9.6 billion) overtook theCzech Republic (€ 8.9 billion)for second place on the list.

Price to quality ratioWhat’s behind the success ofPolish exports? Buyers taketwo factors into account whenmaking a purchase: price andquality. And Polish products

can boast excellent value formoney, thus winning a sizablechunk of global demand.

Undercutting competitionwith lower prices is a double-edged sword, though. Polishexporters have a clear com-petitive advantage in the formof lower labor costs (an hourof labor in Poland costs onaverage €7.20, while the EUaverage is €23.20, accordingto the EU’s statistics agencyEurostat), and can offer lowerprices, thus selling a fargreater volume of products.But this does not translateinto an equal increase in thetotal value of exports.

The furniture sector is agood example here. In termsof volume, Poland is the sec-ond-largest exporter in the

world, selling 2.7 million met-ric tons of its furniture abroad(China is the undisputedleader with nearly 15 milliontons), but in terms of value, itfalls behind Germany andItaly.

The reason is simple: forevery 100 kilograms of furni-ture exported, German andItalian companies receive€500-600 while Polishexporters only receive halfthat, according to estimatesprepared by market researchfirm B+R Studio.

The Ministry of Economyprojects that in 2013, the valueof Polish exports will rise by 2percent (to €144.8 billion),although other experts aremore optimistic in their fore-casts. HSBC predicts a 5.8 per-cent increase, while the ExportCredit Insurance Corporationexpects an 8 percent spike.

JJaacceekk CCiieessnnoowwsskkii

Polish exports brokeanother record in2012. What makes thecountry’s products sosuccessful abroad?

SH

UT

TE

RS

TO

CK

Polish food is becoming increasingly popular abroad

Big five customersPoland’s top five export destinations, by value of exported goods(in € billions)

Country 2012 Change y/y

1. Germany 35.7 0%

2. United Kingdom 9.6 8.5%

3. Czech Republic 8.9 4.4%

4. France 8.3 -1.2%

5. Russia 7.7 25.2%

Source: Central Statistical Office

Exports

Made in Poland focuses on innovative exportersPoland’s exporters aregrowing in bothstrength andsophistication

The phrases “hi-tech,” “inno-vative” and “state-of-the-art”weren’t often mentioned inthe same breath as “Polisheconomy” until recently. Butthat is changing, and rapidly.

For years now Poland hashad a strong stable of young,world-leading programmersand computer specialists, butit was understood that theywere being hired off by thelikes of huge global tech com-panies that were investing inPoland, such as Google,Microsoft or IBM. Perhapssome went to large Polish ITfirms like Asseco or Comarch.They were something to beproud of, but few predictedthat they would become thefoundation for an entrepre-neurial explosion.

To be fair, Poland stillplaces low in innovation rank-ings. the European Commis-sion has just released a reportputting Poland fourth-lowest

in the European Union interms of innovativeness.

But that belies a small butgrowing group of hi-tech firmsthat Poles are starting up.Poland’s growing strength inthis field was on full display atCeBIT 2013 in Germany,where Poland was the “PartnerCountry.” From ERP software

to video games tocloud computing,Polish firms made –and are making –their mark.

The trend isspilling over intoPoland’s export sec-tors as well, which iswhy in our thirdannual edition ofMade in Poland,which launches at aspecial conferencededicated to exportsthis week, we have aspecial report onresearch and devel-opment in Poland.Poles have come upwith some innova-tions that will haveglobal applications

– and money being spent onR&D is on the rise too, a wel-come development.

Poland’s export sectors areleaders in R&D – from devel-opments in cosmetics to min-ing machinery to pharmaceuti-cals to aviation, Polish firmsare producing state-of-the-artproducts at lower prices than

their Western counterparts,putting them in prime positionto find new markets andincrease market share in thosein which they are already pres-ent.

Take cosmetics producerInglot, for example. Thehome-grown firm recentlydeveloped a type of nail polishthat “breathes,” allowingwater underneath while main-taining its color. While somemight not find that particularlyremarkable, it was a boon toMuslim women, who arerequired to wash their armsand hands – including theirnails – before daily prayers.Muslim scholars have sinceendorsed Inglot’s nail polish aspermissible.

Then there is Polpharma,which recently won the awardfor “Most Innovative Product”from the Polish Academy ofSciences for its innovativetechnologies used in produc-ing osteoporosis drugs. Notonly do the innovations makethe drugs cheaper to produceand safer for the patient, theyalso allow for significantly

more environmentally friendlyproduction.

In Aviation, PZL-Âwidnikand PZL Mielec produce cut-ting-edge helicopters thatserve the most demandingcivilian and military cus-tomers. The list goes on, butyou can read more about howPolish exports are becomingmore hi-tech and sophisticatedin the sector analyses found inthe pages of Made in Poland.

For foreign firms consider-ing importing Polish productsor cooperating with Polishfirms, Made in Poland providessome other resources: a list ofPoland’s largest exporters andcontact details to governmentagencies that aid importersand foreign businesses.

There’s also a bevy ofanalysis from our partners atPoland’s various chambers ofcommerce and institutionsthat work with exporters,including patent attorneysoffices and development agen-cies. We hope that these serveforeign firms well in theirsearch for a Polish businesspartner.

As part of its mission, theWarsaw Business JournalGroup – which comprisesMade in Poland, the flagshipweekly Warsaw Business Jour-nal and several other publica-tions – supports Polish exports.For that reason, we continueto publish Made in Poland,which has been welcomed inthe market to no little success.Exporters and governmentagencies alike have found thepublication useful in their pro-motion activities. We also con-tinue to hold a conferenceeach year dedicated to explor-ing the issues facing Polishexporters.

Bigger, stronger, but alsomore sophisticated andresearch-oriented – Polishexporters continue to provetheir value to the Polish econ-omy.

Pick up your own copy ofMade in Poland, or visitWBJ.pl to download the PDF;we’re sure it will prove theirvalue to your business as well.

AAnnddrreeww KKuurreetthhEEddiittoorr--iinn--CChhiieeff

WWaarrssaaww BBuussiinneessss JJoouurrnnaall

APRIL 8-14, 201310 www.wbj.pl IINNTTEERRVVIIEEWW

Ewa Boniecka: What madeAleksander KwaÊniewskireturn to active politics andannounce he will be establish-ing Europe Plus with you andJanusz Palikot?Marek Siwiec: Our politicalscene is rigid. The ruling Civic

Platform is totally focused onitself and on its confrontationwith the opposition Law andJustice. So Aleksander KwaÊ-niewski decided it was high timeto build a strong center-left for-mation in Poland as the alterna-tive to the governing parliamen-tary majority and the domina-tion of right-wing parties.

We both strongly believethat there is room for a mod-ern, center-left party in Polandbut until now that potentialhas not been exploited. Thefirst step in building coopera-tion between existing leftistparties, leftist political groupsand feminist organizations ispreparing a common electorallist of leftist candidates forelections to the European Par-liament in 2014.

But Democratic Left Allianceleader Leszek Miller hasrejected the invitation to suchcooperation because of JanuszPalikot’s involvement. What’syour next move?Poland should send a strongrepresentation of people tothe EP – people who can havea say in decisions made there –and we would like to invitesuch people to join our elec-toral list. The fact is that whenLeszek Miller rejected ourproposal to build one leftistvoting list, it created an obsta-

cle to our plans. But I think that some mem-

bers of his party would like tosee that decision changed. Itwas an unwise one, because it isevident that one leftist electorallist would gain more supportfrom voters than separate lists.

The Democratic LeftAlliance can join Europe Plusat any time and I think thatdiscussions within that partyabout joining us will go on, sothe matter is not closed yet.The party hasn’t enjoyed muchsupport in recent years, while

Palikot’s Movement enteredthe Sejm with over 40 MPs.Some 1.5 million people votedfor Mr Palikot’s party.

It seems that building EuropePlus may prove very difficultconsidering the current war

within the left. Besides, MrKwaÊniewski hasn’t declaredyet that he will be running forthe European Parliamenthimself...I wouldn’t say we have a waron the left. It is in my view aheated confrontation with

WBJ sat down to discuss politics with MarekSiwiec, an MEP who is currently building a newcenter-left political initiative, Europe Plus,under the leadership of AleksanderKwaÊniewski, former president of Poland

CO

UR

TE

SY O

F F

AC

EB

OO

K/M

AR

EK

SIW

IEC

Marek Siwiec believes Poland’s political scene is “too rigid”

“People’sexpectations for acenter-leftformation arebigger than wehad anticipated.”

Politics

BBuuiillddiinngg aa nneeww cceenntteerr--lleefftt

APRIL 8-14, 2013 IINNTTEERRVVIIEEWW www.wbj.pl 11

Leszek Miller’s party, but Iagree that it makes our effortsmore difficult. And the thingthat is most troubling is thatMr Miller does not under-stand that the left needs somefresh air and credibility toattract voters and that by join-ing our project, the Democrat-ic Left Alliance will open up tonew people with leftist and lib-eral views and that togetherwe can offer a real alternativeto right-wing parties. Other-wise, his party will remain stag-nant.

A prominent feminist organi-zation, The Congress ofWomen, has taken offensewith Mr Palikot for his treat-ment of women. They are notsupporting you as of now, sohow do you bring key playerslike that around?We’ve guaranteed women 50percent of the places on ourelectoral list and I am certainthat those female activistslooking for a better future inPoland and Europe will sup-port our initiative, in due time.

Let’s look at leftist partiesin the West. They are chang-ing, they are looking for newideas and proposals, especiallyin a time of crisis and changesin the EU architecture. Theyhave to redefine some of theirapproaches to economic,financial and social matters inorder to deal with unemploy-ment, frustration among EUcitizens and also meet the

expectations of minorities.The same challenges face

Poland’s leftist politicians.Europe Plus is our response tothose challenges, through sup-porting deeper integrationwithin the EU, promotingmore solidarity in fighting withcrises and by making EUmechanisms function moredemocratically. If we send astrong and numerous leftistrepresentation to the Euro-pean Parliament, it willincrease Poland’s role in shap-ing European policies.

But the average Pole is proba-bly more interested in domes-tic problems than in Europe.So what can you offer them,other than the voting list?I have had many meetingswith people all over Polandand I am very often askedabout our position on domes-tic issues. People’s expecta-tions for a center-left forma-tion are bigger than we hadanticipated.

So we have thought aboutcreating a new political party,a “Poland Plus” if you will,akin to Europe Plus and whatit stands for. When the firststep of building a center-leftlist is successful, we will workon establishing a party with anequally comprehensive pro-gram, far from populism.

We are sensitive towardssocial needs, but in order toprovide state support to thosewho need it and to run an

effective social policy, theeconomy has to be effective.Leftist parties acknowledgethat economic results are alsobased on providing favorableconditions for SMEs and notonly for big corporations.

It is still an open questionwhether AleksanderKwaÊniewski will lead such aparty officially, isn’t it?It is for President KwaÊ-niewski to decide about hisfinal political involvement,but it is he who will shape thelist of candidates for theEuropean Parliament. In acouple of weeks we will knowmore about his own plans.Now it is too early to talkabout names on the list or hisdecision concerning his per-sonal involvement in theelections or in building thecenter-left party.

If Europe Plus is established,would Mr Palikot give up hisparty’s name – Palikot’sMovement – and make it partof Europe Plus? Palikot’s Movement is anindependent party that hassignificant representation inparliament and it will be MrPalikot who will have toanswer that question in duetime. The name of his partyand its brand are important,but it has to be treated realisti-cally when it comes to politicalchanges and new circum-stances. Parties in Poland andin Europe have sometimeschanged their names as thepolitical scene changed. Andcertainly when Europe Plus istransformed into a center-leftparty, it will mean significantchanges on our present politi-cal scene.

Do you envisage a situationwhereby Europe Plus couldenter into a coalition with theruling Civic Platform?If, after the 2015 parliamen-tary elections, our party hassignificant political capital,maybe it could be taken intoconsideration. For now all wecan do is speculate. ●

Marek Siwiec

Marek Siwiec was born in1955 in the Silesia voivod-ship. He joined the commu-nist party in 1977 and was amember until communism’scollapse in Poland. From1997 to 2004, he served ashead of the Polish NationalSecurity Bureau under then-President Aleksander KwaÊ-niewski, also a former com-munist party member.

Mr Siwiec was elected anMEP in 2004 and kept his

seat after the 2009 Euro-pean parliamentary elec-tions. From 2011 to 2012, hewas deputy leader of theDemocratic Left Alliance,but has since left the partyto join Europe Plus, a newcenter-left political initia-tive that he is leading inpartnership with MrKwaÊniewski and JanuszPalikot, the leader of theanti-clerical Palikot’s Move-ment party. ●

CO

UR

TE

SY O

F M

AR

EK

SIW

IEC

Mr Siwiec says the new grouping could eventually become a domestic political party

APRIL 8-14, 2013CCOOVVEERR SSTTOORRYY12 www.wbj.pl

Exclusive interview

Fischer: Germany ‘doesn’tknow how’ to lead Europe

Remi Adekoya: What is youropinion on the current situa-tion in Cyprus in view of theGerman role leading up to thewhole mess? What could be theconsequences of the Cypruscase for Europe as a whole?Joschka Fischer: For me, itseemed there was and is a lot ofGerman, Austrian and Finnishdomestic politics involved in theCyprus issue. With its hugefinancial system made up oflargely Russian money and allthose rumors about money-laundering, Cyprus is not allthat popular in those countries Imentioned. It’s extremelyunpopular in the parties of MsMerkel and her center-rightcoalition partner. I think thecurrent Cyprus agreement isdriven by all these factors.

I am concerned there mightbe negative consequences ofthis affair in the whole eurozone, not only in the crisis-hitcountries. Investors and regularfolks with savings could losetrust in the banking and finan-cial system and the conse-quences of such a loss of trustcould be very unpleasant in themedium- to long-term future.

I understand the frustrationof many in Europe regardingCyprus, but the issue at stakehere is the future of the eurozone. Trust is essential to calmthe situation and anything thatcould lead to a re-emergence ofthe crisis should be avoided. Iwas shocked that the Europeanfinancial leadership and thepresident of the World Bankhad failed to foresee the nega-tive reactions of Cypriots to theidea of seizing their bankdeposits. That smacked of ama-teurism.

There are two levels of trust atissue here: one is investors’trust in governments and theother is citizens’ trust in euro-crats. Which are you referringto?But finance ministers are noteurocrats, they are members ofnational governments. Thatshould not be forgotten.

True, but nowadays they areabout as popular as the euro-crats who are regularly bashedfor their perceived excessivebureaucracy and big-spending

ways, aren’t they?That’s true, but that perceptionabout a big-spending Europeanbureaucracy is completely false.EU bureaucracy is smaller thanthe bureaucracy in Munich.

But how can we change theperception of fat-cat eurocratsspending taxpayers’ money? I think in Europe, as in theUnited States, it will always bepart of the reality that peopleblame the center for everythingthat goes wrong. In the US,people blame Washington andthe Beltway for all the problemsAmerica has.

As Europe becomes morepolitically integrated, the blamewill increasingly be placed onBrussels for all that is wrong.“Vote for me and I will clean upthe mess in Brussels,” is alreadya common political pitch. Thesesentiments will not go away.

On the other hand, the con-struct of the present euro zoneis an element which should bereconsidered. Take for exam-ple, the relationship betweennation states and the EU.There is a federalist element inthe construct but it is not well-designed. Member-state gov-ernments are very powerful andpossess veto rights, but nationalparliaments have less of a say.

This increases the convic-tion of EU citizens that Europeis governed by a technocracy,because governments play theblame game. They are the realpower in the EU but at homethey say “Oh, look at crazyEurope.” The Polish govern-ment is guilty of this as well. Iknow they want to avoid theanger and blame of their peopleso they act powerless againstEurope at home and then flextheir veto power in Brussels.This a dangerous game.

So what kind of changes do youpropose to Europe’s construct?Today, the European Parlia-ment plays an important role,but does not have the key pow-ers needed to control the crisis.This remains in the hands ofnational governments. It wouldbe helpful to give national par-liaments, in the context of theirrole within Europe, an institu-tional role. I am strongly infavor of considering a Euro

Chamber with representativesof national parliaments. Itwould have a majority and aminority likewise and could bevery helpful with thorny issuessuch as those regarding budg-ets.

I think it would be helpful ifthe creditors and debtors nego-tiated directly and then pre-pared decisions. This wouldalso get national media outletsand people more interested.People criticize their electednational politicians a lot, butthose same politicians still havemore legitimacy in citizens’ eyesthan bureaucrats in Brussels,for instance. More trust is need-ed in Europe today.

In November 2011 ForeignMinister Rados∏aw Sikorskimade a speech in Berlin wherehe suggested a European feder-ation under German leader-ship. What is your take on thatas a German?No, that won’t work. I agreewith Mr Sikorski that Germanyshould be more in the lead but Idoubt that will happen.

Why not?Because we don’t know how todo it.

Don’t know or are afraid peo-ple will start making WWIIanalogies? That is also an element, but it’seven deeper than that. TheGerman psyche is really struc-tured by the past. We not onlyburned our fingers but wealmost burned ourselves not tomention all the innocent victimsin other countries.

This is deeply rooted in the

German psyche, be it on the leftor on the right. It’s therewhether you like it or not. Imyself am happy it’s not beenforgotten and is defining ouridentity even amongst the newgeneration. The memory is notdisappearing, that’s good. I saythat as a German because it’svery important for us but it’s alsovery important for Europe and Ithink the excellent relations thatwe have, for instance, withPoland today are proof of thepositive elements of keepingthat memory alive. But in a nut-shell, we are reluctant to engage.

And to lead?And to lead because there is a

realistic self-perception that weare not the best at doing that.Henry Kissinger, I was told, saidrecently that if the French hadthe economic power of the Ger-mans, the euro zone crisiswould have been fixed. And Iadd to this that if the Brits werein the euro zone, they wouldhave handled the issues maybe

even better than the French. In our collective psyche, we

Germans are not designed forsuch a role. The Germans areas old as the Poles as a nation,more or less 1,000 years oldnow. But politically, we are apretty young state. It all startedin 1871, before which there wasno one united Germany but 10different Germanys. So it start-ed in 1871 and ended in 1945 inunbelievable disaster. So politi-cally, it’s not an old country.

France and Poland wereunited much earlier and playeda much stronger role in earlierEuropean history. The old Pol-ish state was a European power.But even smaller states like

Sweden, Denmark or theNetherlands have older politi-cal traditions and identitiesthan we do.

Are you saying that even ifAngela Merkel was to arrive atthe conclusion that withoutGerman leadership, Europecannot move forward, she stillwouldn’t be able to effect thatleadership?No, that’s a different scenario. Iwas in the government and wehad to make very tough deci-sions such as getting the con-sent of the majority to sendtroops to Kosovo. You had tomake the case and you had tocreate a majority, which we did.It’s doable, not easy but doable.

I am not telling you that it’simpossible to convince the Ger-mans and make the move inthat direction, but AngelaMerkel doesn’t have thecourage. She is obviously a greattactician but I don’t believe she’sa great strategist. You need acertain vision that you believein, a direction in which you wantto lead. Direction is the mostimportant element.

Angela Merkel said Ger-many would do everything todefend the euro but since thenshe’s not been consistent.

Always, she’s half or a quarterof an hour late and these latesolutions are expensive. She isrisking a very severe crisis oftrust and legitimacy.

Because as long as the solu-tions are delayed, the more youhave to rely on the EuropeanCentral Bank and other backdoors. Rather, she should say tothe German people: “This isthe direction we will go nowand I will fight for this. My des-tiny as a Chancellor depends onwhether I succeed in this ornot.”

That’s the stuff people wantto hear in a democracy andthen they start scratching theirheads and discussing with eachother and you have the oppor-tunity to convince them.

If Ms Merkel lacks vision, whythen is she so popular withGerman voters?Because Germany is economi-cally strong. It’s very simple, it isnot the chancellor who isstrong, but the country which isstrong. There is no crisis in Ger-many today and that helpswhen you are in power. Polandtoo is doing well today.

Yes, but the Polish prime min-ister of six years now, Donald

WBJ sat down with former vice chancellor andforeign minister of Germany, Joschka Fischer,to discuss the German point of view on thecrisis in Europe, the lack of democraticlegitimacy EU institutions are suffering fromtoday and what Europe’s biggest economy needsto do to keep the European dream alive

“Europe is the most importantfactor for the well-being of a

democratic Germany.”

SH

UT

TE

RS

TO

CK

Former German Foreign Minister Joschka Fischer worries that events in Cyprus

could undermine trust in financial institutions across the EU

Tusk, is nowhere near as popu-lar as Angela Merkel. Hisapproval rating is in the mid30s, not in the mid 60s.As you surely know, Poles areusually very skeptical of thepowerful and of their leaders.So that’s probably not a sur-prise.

Returning to ChancellorMerkel, you have said thatmutualizing the euro zone’sdebt is the only solution to theproblem. But is there a Ger-man leader who could get awaywith agreeing to that or wouldit be the end of that person’scareer?It wouldn’t be the end of thatperson’s career. I’ll give you anexample. I’ve had a lot of dis-cussions with very conservativegroups of German businesspeo-ple who run small and medium-sized enterprises. At first, whenI end my speech with calling formutualization, they say, “Areyou crazy? We should pay forBerlusconi, for the Cypriots, theGreeks? Never, we will neverdo that, it would be completemadness.”

Then I start explaining andwe start discussing. Afterroughly an hour and a half, themood is very different. Nobodyis happy. My interlocutors arenow scratching their heads, ask-ing “so you really think we haveto do that or the EU will even-tually collapse?” “Certainly,” Irespond.

“Oh well so we have to thinkabout how to go about it in thatcase then,” they say.

There is an emotional

understanding among Germansthat if things get serious,Europe needs to be helped.Europe is the most importantfactor for the well-being of ademocratic Germany. Our his-tory, as you know, is not alwaysone to be proud of, but we canbe proud about the unificationof Germany and its integrationwith Europe. This is deeplyingrained, so I am not pes-simistic. A courageous leadercould convince the Germanpeople to make the move butthe longer we wait, the biggerthe mess and the deficit of trust,which we spoke about earlier.

There’s been some talk recentlyof a British exit from the EU.What consequences wouldthere be if that happened, or ifthe UK radically limited itsparticipation in the Union? I don’t see how they can limittheir participation in the EUany more than they alreadyhave. They are paying a pricefor this limitation. For example,it was a big mistake to withdrawthe Tories from the EuropeanPeoples’ Party. Cameron haslost influence in the EuropeanParliament and so has the UK.

If the debate over a Brixitgets real, then the majority ofBrits will start to seriously con-sider what it would mean. Ifthey left, it would be a severeblow for the EU but a disasterfor the UK. London’s City isthe financial center for the euroand it depends on the future ofthe euro more than on thefuture of the pound. The poundhas a great history but not a

great future. The UK is toosmall to have its own currencythat could play an importantrole in the 21st century. But weshould be patient with our Bri-tish friends. The EU is strongerwith Britain and I think Britainbelongs in the EU.

Foreign Minister Rados∏awSikorski has said he thinksPoland has a chance to accessthe inner circle of EU decision-makers in the near future. Doyou agree?I am not saying this because Iwant to please your readers, butyes, I agree. The economicdevelopment of Poland hasbeen impressive and so has therise of a new Poland, built bythe young generation. Also,Poland is one of the big-six inthe EU – that shouldn’t be for-gotten. So my answer is yes, def-initely.

According to the World Eco-nomic Forum’s 2012 ranking,six of the 10 most competitiveeconomies in the world areEuropean. However, there is awidespread perception, whichprobably has some truth to it,that Europe needs to improveits competitiveness. How doyou see it? I don’t buy into all the dooms-day prophesies screaming thatEurope is not competitive. Ger-many used to be called the sickman of Europe. We knew thereasons for that. Unificationwas an unexpected miracle butalso one which, in economicand social terms, was a hugechallenge.

We needed more than adecade and millions of euros aswell as Deutschmarks to get usthrough that. One of the rea-sons for the recovery of com-petitiveness by Germany is thatwe did it together. Eighty to 85percent of unification is behindus now. Of course there are stillstrong disparities because youcan’t expect differences createdover five decades to evaporateovernight.

Germany regained competi-tiveness and I am sure Francewill do the same. It’s not easy.It’s painful, but you have toadjust to the new realities.Globalization is not a WallStreet conspiracy or an Anglo-American conspiracy, it is real.The competition the French carindustry has from South Koreaand Japan today, and probablyChina tomorrow, is real.

The crisis must be addressedin a balanced manner. We haveto bring down public debt. Thequestion is when, by how muchand in what time frame. Wehave to increase our competi-tiveness everywhere in Europe,in some places more, in othersless.

But we also have to developa growth strategy because if wedon’t, the other two elementswon’t work. They will lead us

into a depression. The processhas to be balanced, but I am notpessimistic about it. Of course,there is also the issue of divisionof labor. Northern Europe ismore industrialized, SouthernEurope is less so. And theSouth won’t be as industrializedas Northern and CentralEurope, we won’t change that.So the answer must be that they

have to develop their own eco-nomic strengths. But we alsohave to think of a transfermechanism in the EU.

Look at the United States,Greece is better off than WestVirginia if you look at publicdebt. There are strong dispari-ties in the US too, but somehowthings are worked out. We alsohave to think about a transfermechanism here in Europe.

You know the role Russia hasplayed in Poland’s history. Theview here in Warsaw of Moscowis pretty bleak. How do Ger-many’s elites view Russia?Differently from Poland’s forsure. What we have in commonis the understanding of theimportance of Russia forEurope, for the good or for thebad. Therefore, I think bothcountries understand theimportance of the independ-ence of Ukraine for the newpost-Soviet order in Europe.Ukraine is the cornerstone ofthat and if that cornerstonewere broken, we would be in acompletely different geopoliti-cal reality via-a-vis Russia.

Poland, the Scandinaviansand some others understandthat, some others might not. Weboth benefit from economicgrowth in Russia if you look at

German and Polish trade. Wehave an interest in Russia beingmodernized but unfortunately,I don’t think the Putin era nowwill usher in much moderniza-tion. However, there are fasci-nating developments going on.

Yes, Russia is a “guideddemocracy” – whatever thatmeans – but there are also veryimpressive developments in the

young generation. Freedom ofinformation is a reality in Rus-sia because of the internet.Young Russians are lookingtowards the West. Lots of mid-dle and upper-class Russianscome to the West. In Germany,we have a very strong middleand upper-middle class Russianminority and they have goodties with native Germans.

It’s in our common interestto have a realistic picture, to seethe positives and negativesbecause Russia is very impor-tant for all of Europe.

On a personal note, Mr Fisch-er, the world knew you in thepast as a contestant of theestablished order, but in recentyears you have become less ofthat ...You are too kind! (Laughs.) Iam part of the establishmentnow. I am also a 65-year-oldgrandfather today.

So what are the thoughtprocesses that take a man fromwhere you were before to whereyou are now?Life is long and not everythingyou believed in your youth wasthe truth. A lot of illusionsbelong to that period. Gettingolder means thinking moredeeply. For 10 years, I believedin revolution and that was a bigmistake.

So now you believe in evolu-tion?Yes. There was a debate in myparty, the Greens, on whetherwe were betraying our princi-ples by joining the government.I asked them, “Where are theGreens more dangerous for thenuclear industry, protesting infront of a power plant or in thegovernment making the lawsthat govern that power plant?”

The answer was, of course,the latter. But being in the gov-ernment and making the lawsmeans you cannot be anti-establishment anymore. So youhave to make a choice. ●

APRIL 8-14, 2013 CCOOVVEERR SSTTOORRYY www.wbj.pl 13

“The pound has a great history butnot a great future. The UK is too small

to have its own currency that couldplay an important role in the

21st century.”

SH

UT

TE

RS

TO

CK

Despite differences in their approach to Russia, both Germany and Poland realize

that the independence of Ukraine is the “cornerstone for the new post-Soviet order

in Europe,” says Mr Fischer

Joschka Fischer

Joschka Fischer was born in Baden-Würt-temberg, southwestern Germany, in 1948.The third child of a butcher, he never com-pleted secondary school nor attended uni-versity. However, by 1967, he had becomeactive in German student and leftist move-ments, joining the militant group, Revolu-tionärer Kampf (Revolutionary Struggle).

Mr Fischer was a leader in several streetbattles against police officers. But after aspate of leftist terror attacks in 1977, herenounced violence as a means for politicalchange and became involved in the GreenParty.

In 1998, the Greens formed a coalitiongovernment with Gerhard Schröder’s SocialDemocratic Party and Joschka Fischerbecame vice chancellor and foreign ministerof Germany. As foreign minister, he apolo-gized for the violence of his activist days.

Mr Fischer left office in 2005 as the sec-ond longest-serving foreign minister in Ger-man postwar history. Since 2008, he hasbeen employed with the Albright Stone-bridge Group, a consulting firm led by for-mer US Secretary of State MadeleineAlbright and former US National SecurityAdvisor Samuel Berger. ●

APRIL 8-14, 201314 www.wbj.pl OOPPIINNIIOONN && AANNAALLYYSSIISS

Jan-Werner Mueller

In recent years, the European Union– or, more accurately, the powerfulcountries of northern Europe – has

been subjecting its weaker members tosocial and political “stress tests” in thename of fiscal rectitude. As a result,southern Europe and parts of EasternEurope have become a kind of politi-cal laboratory, with experiments pro-ducing strikingly varied – and increas-ingly unpredictable – outcomes in dif-ferent countries. At the last EU sum-mit, Luxembourg’s prime minister,Jean-Claude Juncker, even suggestedthat the risk of a “social revolution”should not be excluded.

While that outcome remainsunlikely, it is increasingly clear thatmany European countries – and theEU as a whole – need to renegotiatetheir basic social contracts. But Euro-pean elites, preoccupied with short-term fixes, have not considered thelong-term need for such revisions – totheir own detriment.

Indeed, despite significant varia-tions by country, one trend is becom-ing increasingly apparent across theEU: voters, regardless of their politicalorientation, are ejecting at the first

opportunityleaders whoimplement aus-terity. But, beyond this overwhelmingopposition to austerity, countries’experiences vary widely.

Country-by-countryGreece has seen the rise of an overtlyfascist party, Golden Dawn, which

proudly celebrates the legacy of for-mer dictator Ioannis Metaxas.Although Golden Dawn has existedfor roughly two decades, only in thelast year did it gain enough support toenter parliament. Moreover, its pollnumbers continue to climb.

Golden Dawn’s success does notreflect a deep-seated desire amongGreeks to return to authoritarianism.The party has simply stepped in wherethe Greek state – long plagued by inef-ficiency and corruption – has retreat-ed, providing basic welfare and otherservices to desperate citizens, whileengaging in unprecedented violenceagainst people who are or look likeimmigrants. One way that GoldenDawn attempts to embody the state isby having party members out on thestreets as vigilantes.

Austerity has similarly sharpened along-standing crisis of statehood andpolitical legitimacy in Italy, reflectedin the rise

of a newanti-establishment party, the

Five Star Movement, which claims totranscend the traditional left-rightpolitical spectrum. Indeed, the move-ment lacks clear policy objectives,instead capitalizing on popular disgustwith Italy’s political elites – a senti-ment that led directly to the last elec-