Embed Size (px)

Citation preview

Michael L. Stevens, CEIC

Senior Executive Vice President

Conference of State Bank Supervisors

WASHINGTON VIEWS

AND COMMUNITY BANKING

Washington Views

& Community Banking

The Federal Policy Landscape

Congress

The Agencies

• Federal Reserve

• FDIC

• OCC

• CFPB

What regulatory relief?

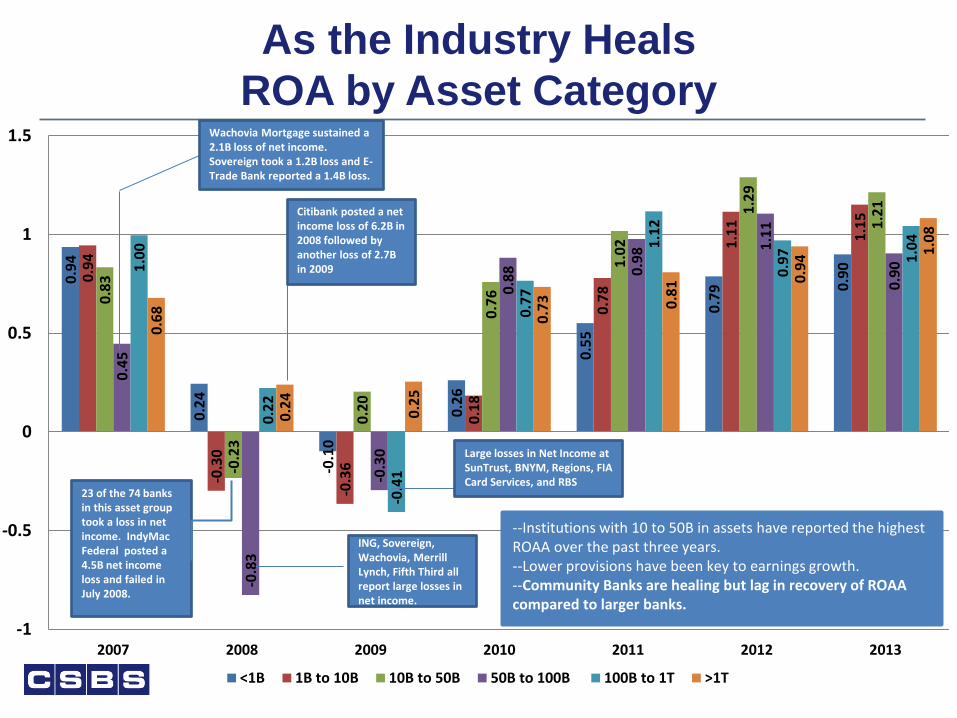

0.9

4

0.2

4

-0.1

0

0.2

6

0.5

5

0.7

9 0.9

0

0.9

4

-0.3

0

-0.3

6

0.1

8

0.7

8

1.1

1

1.1

5

0.8

3

-0.2

3

0.2

0

0.7

6

1.0

2

1.2

9

1.2

1

0.4

5

-0.8

3

-0.3

0

0.8

8

0.9

8 1.1

1

0.9

0

1.0

0

0.2

2

-0.4

1

0.7

7

1.1

2

0.9

7

1.0

4

0.6

8

0.2

4

0.2

5

0.7

3

0.8

1 0.9

4 1

.08

-1

-0.5

0

0.5

1

1.5

2007 2008 2009 2010 2011 2012 2013

<1B 1B to 10B 10B to 50B 50B to 100B 100B to 1T >1T

Citibank posted a net income loss of 6.2B in 2008 followed by another loss of 2.7B in 2009

Large losses in Net Income at SunTrust, BNYM, Regions, FIA Card Services, and RBS

23 of the 74 banks in this asset group took a loss in net income. IndyMac Federal posted a 4.5B net income loss and failed in July 2008.

Wachovia Mortgage sustained a 2.1B loss of net income. Sovereign took a 1.2B loss and E-Trade Bank reported a 1.4B loss.

--Institutions with 10 to 50B in assets have reported the highest ROAA over the past three years. --Lower provisions have been key to earnings growth. --Community Banks are healing but lag in recovery of ROAA compared to larger banks.

ING, Sovereign, Wachovia, Merrill Lynch, Fifth Third all report large losses in net income.

As the Industry Heals

ROA by Asset Category

Driving a Better Policy Outcome

Community Banking

in the 21st Century

Opportunities, Challenges and Perspectives

Conference Objectives

• Improved understanding about how financial policy and

regulation shapes and impacts all aspects of the financial

system.

• Appreciation for the important role community banks in

serving small business and the financial and service needs of

local communities.

• Public policy that better reflects how the various components

of our financial system contribute to the economic life and

financial well-being of market participants.

• Public policy that accommodates a community banking

system and, in turn, further empowers local communities.

Public policy has many drivers…

Politics

Domestic Issues

International Issues

Public policy must accommodate the

community banking business model

To achieve this objective:

• Industry engagement on its issues, opportunities, and

challenges is key

• High quality, independent research focused on

community banking

– Contribution to the economy

– Role in local economic development

– Support of small business & individuals, especially customized

credit

– Consistent venues to present and publish

• Clear policy objectives and initiatives for advocacy -

CSBS and others

Current state of the initiative and its

influence on policy

Politics

International Issues

Accommodative Public Policy

Domestic Issues

The dominant

activity in the

process is

currently

industry

engagement.

However, the

research

conference

demonstrated

that research

does exist…

The proportions in the outer band are illustrative and not specific measurements.

2013 Town Hall Profile

• 28 States

• 54 Events

• 1,700 Bankers

Areas of Inquiry

• Challenges

• Opportunities

• Size and Scale

• Characteristics of Management and Directors

• Financial services in declining areas

• Areas of Future Research

What we should take-away

1. The challenges of the industry are real and will likely

lead to significant changes in how community banks

operate.

2. This industry has changed and survived through

multiple transitions.

3. This phase is in the early stages with an uncertain

outcome, but considered to be significant.

4. There are scores of bankers who are thinking and

planning for the future. They see opportunities. They

know what they do is important.

What fun would it be without a challenge?

• One size fits all approach to regulation, removes one of

the strongest advantages of community banks: tailoring

products to fit specific needs

• Competitors

– “too big to fail” banks

– Farm Credit Banks

– Credit Unions

– Non bank providers of payment services

What fun would it be without a challenge?

• Rapidly changing technology and related consumer

demand

• Access to capital

• Attracting and retaining qualified employees

Opportunities Abound

• Differentiating from larger banks

– Customer service

– Customization

– Fees

• Lending opportunities

– Improving economy

– Serving void left by mortgage companies

– SBA loans

• Wealth management

• Return to a “normal” banking market

Must be bigger unless

it is better to be smaller

• Compliance cost is more challenging for smaller banks

• Compliance cost and burden increases with size

• Smaller banks can be profitable

The size must be related to the community the bank serves

and give it the capacity to serve that community.

Serving Areas in Decline

• Larger banks are not interested in these areas

• It takes a connection and interest in these areas to want

to serve them

• Community banks need to collaborate to serve these

areas

• Need better cooperation, less competition, from state

agencies designed to promote economic development

• Regulation needs to allow tailoring of products and

services to serve these areas

2014 Industry Engagement Plan

National survey sponsored by each state regulator

Topics:

1. Mortgage Lending

2. Changing competition

3. Cost of compliance & technology

4. Buy & Sell

Roundtable / Town Hall meetings to supplement with

qualitative information

Research Demonstrates Value of

Community Banks…

• Community bank failure leads to measurable economic

underperformance in local markets. High competition

markets are even more affected by bank failures. (Kandrac)

• Community banks enhance the chances for the survival

of start-up companies. The closer a customer is to a

community bank, the more likely the start-up borrower is to

receive a loan. (Williams & Lee)

• Community banks have a key advantage through “social

capital,” which supports well-informed financial

transactions. This is especially true in rural areas, where

community banks have lower default rates on SBA loans than

their urban counterparts. (DeYoung, et. al.)

Improved proportion is needed to

achieve the objectives

Politics

Domestic Issues

International Issues

The optimal outcome,

achieved over time,

maintains the level of

engagement while

increasing the

volume and quality of

research and leading

to more

accommodative

public policy.

There have been public policy successes

• Significant changes to Basel III

• Significant changes to the Volcker Rule plus expedited

changes to address the issue with TruPS CDO issue

• Small creditor QM included in CFPB rule

• House and Senate bills to provide a petition process for

rural designation under the CFPB qualified mortgage

rule