Embed Size (px)

DESCRIPTION

Gas power generation is so big and growing, gloriously making the more market from all global.

Citation preview

POWER PLANTS’ FOCUS ON GAS VESA RIIHIMÄKI

President, Power Plants & Executive Vice President

© Wärtsilä 1 14 November 2013 VESA RIIHIMÄKI

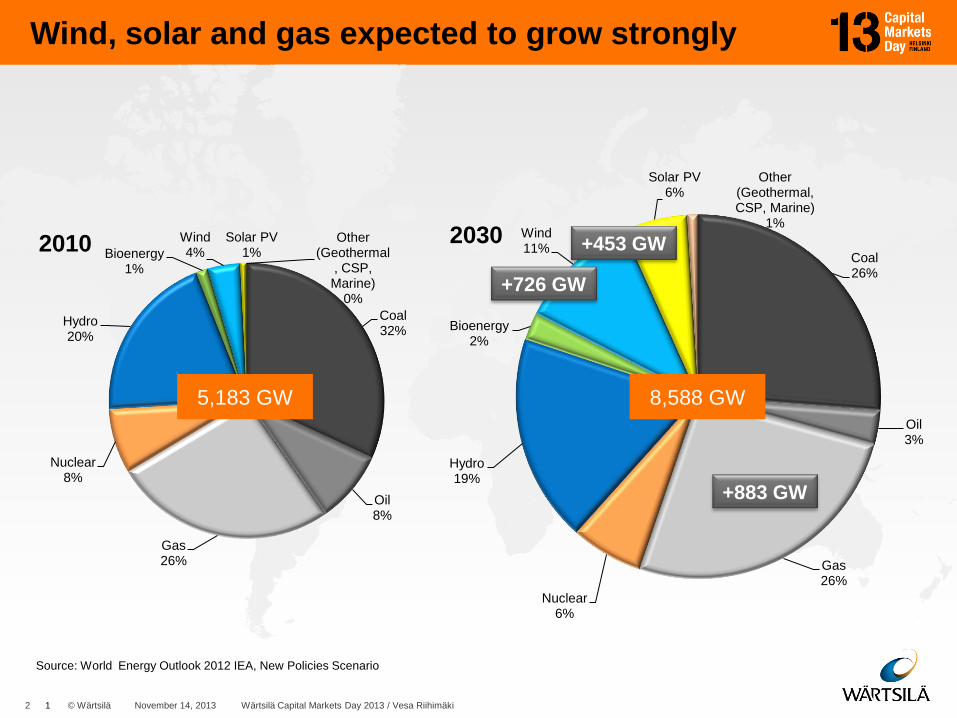

Wind, solar and gas expected to grow strongly

Source: World Energy Outlook 2012 IEA, New Policies Scenario

Coal 32%

Oil 8%

Gas 26%

Nuclear 8%

Hydro 20%

Bioenergy 1%

Wind 4%

Solar PV 1%

Other (Geothermal

, CSP, Marine)

0%

2010 Coal 26%

Oil 3%

Gas 26%

Nuclear 6%

Hydro 19%

Bioenergy 2%

Wind 11%

Solar PV 6%

Other (Geothermal, CSP, Marine)

1%

2030

5,183 GW 8,588 GW

+453 GW

+726 GW

+883 GW

2 © Wärtsilä 1 Wärtsilä Capital Markets Day 2013 / Vesa Riihimäki November 14, 2013

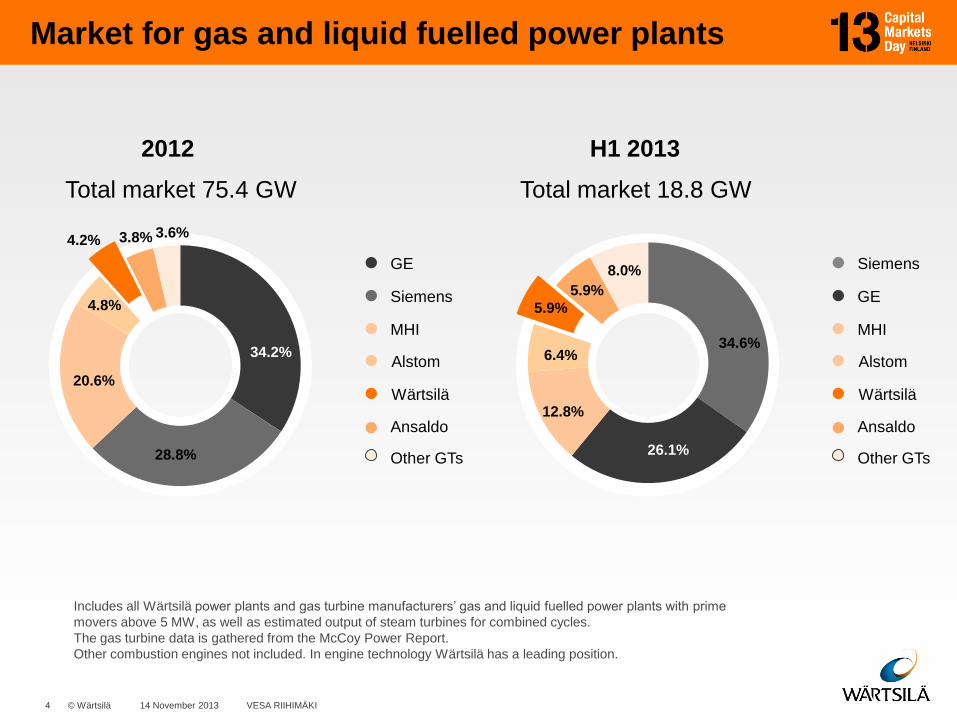

Market for gas and liquid fuelled power plants

0

20

40

60

80

100

120

140

H1 H2

Includes all Wärtsilä power plants and gas turbine manufacturers’ gas and liquid fuelled power plants with prime movers

above 5 MW, as well as estimated output of steam turbines for combined cycles.

The gas turbine data is gathered from the McCoy Power Report.

Other combustion engines not included. In engine technology Wärtsilä has a leading position.

Overall market size

GW

H1 2013 Top 15 countries

Total 18.8 GW

China

USA

Algeria

Malaysia

Thailand

Kuwait

Japan

Bangladesh

Egypt

Saudi Arabia

Uruguay

Tunisia

Russia

Australia

UAE

Other

© Wärtsilä 3 14 November 2013 VESA RIIHIMÄKI

Market for gas and liquid fuelled power plants

6.4%

H1 2013

34.6%

26.1%

5.9%

12.8%

Total market 18.8 GW

5.9%

8.0%

Includes all Wärtsilä power plants and gas turbine manufacturers’ gas and liquid fuelled power plants with prime

movers above 5 MW, as well as estimated output of steam turbines for combined cycles.

The gas turbine data is gathered from the McCoy Power Report.

Other combustion engines not included. In engine technology Wärtsilä has a leading position.

GE

Siemens

MHI

Wärtsilä

Alstom

4.8%

2012

28.8%

34.2%

3.8%

20.6%

Total market 75.4 GW

4.2% 3.6%

Other GTs

Ansaldo

Siemens

GE

MHI

Wärtsilä

Alstom

Other GTs

Ansaldo

© Wärtsilä 4 14 November 2013 VESA RIIHIMÄKI

Other manufacturers

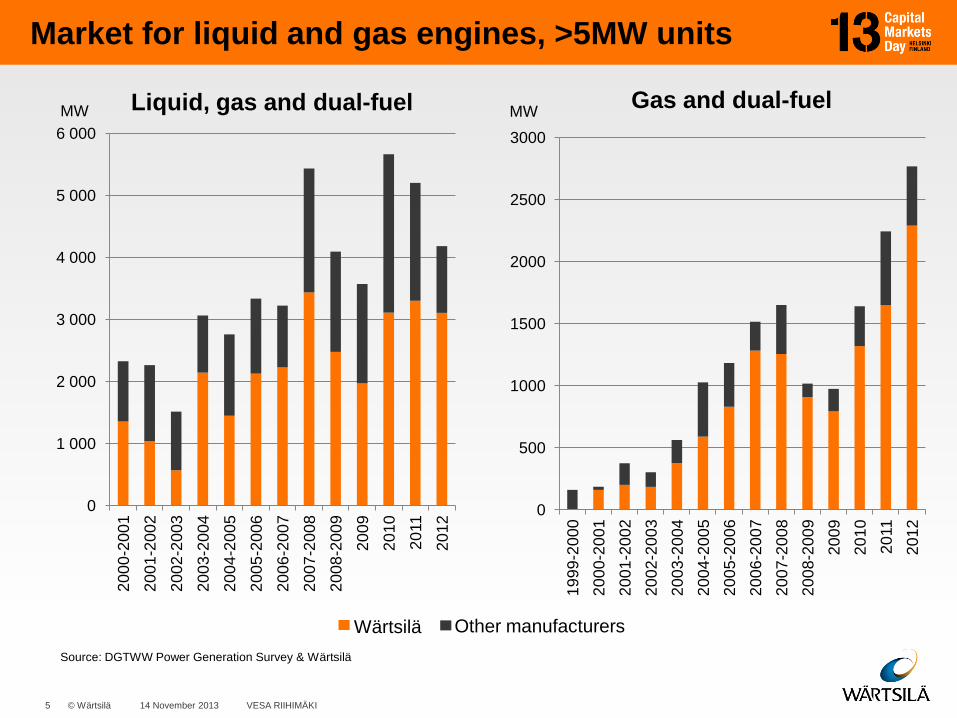

Market for liquid and gas engines, >5MW units

Source: DGTWW Power Generation Survey & Wärtsilä

Gas and dual-fuel Liquid, gas and dual-fuel MW

Wärtsilä

MW

0

1 000

2 000

3 000

4 000

5 000

6 000 2

00

0-2

00

1

20

01

-20

02

20

02

-20

03

20

03

-20

04

20

04

-20

05

20

05

-20

06

20

06

-20

07

20

07

-20

08

20

08

-20

09

20

09

20

10

20

11

20

12

0

500

1000

1500

2000

2500

3000

19

99

-20

00

20

00

-20

01

20

01

-20

02

20

02

-20

03

20

03

-20

04

20

04

-20

05

20

05

-20

06

20

06

-20

07

20

07

-20

08

20

08

-20

09

20

09

20

10

20

11

20

12

© Wärtsilä 5 14 November 2013 VESA RIIHIMÄKI

Power Plants strategy

• Maintain our leading position in HFO & dual-fuel power plants by

enhancing our value proposition

• Grow strongly in large utility gas power plants by capturing market share

from combustion turbines

• Grow in biofuel power plants by enabling a wide fuel range

• Grow in special applications - nuclear emergency power, CHP, oil & gas

and LNG infrastructure - by introducing our value proposition to the

selected customer segments

Strong growth focus on large gas plants in broad utility markets

© Wärtsilä 6 14 November 2013 VESA RIIHIMÄKI

Our customer segments

Industrial Customers

Industries such as mining, cement

and oil & gas investing in captive

power plants.

Utilities

Entities supplying electricity to

residential, commercial & industrial

end users

IPPs*

Financial investors investing in

power plants and selling power to

utilities

Azerenerji, Azerbaijan Cakmaktepe Energy, Turkey Sasol New Energy Holdings, South Africa

South Texas Electric Cooperative, USA GERA, Brazil Barrick Gold Corporation, Canada

*) Independent Power Producers

© Wärtsilä 7 14 November 2013 VESA RIIHIMÄKI

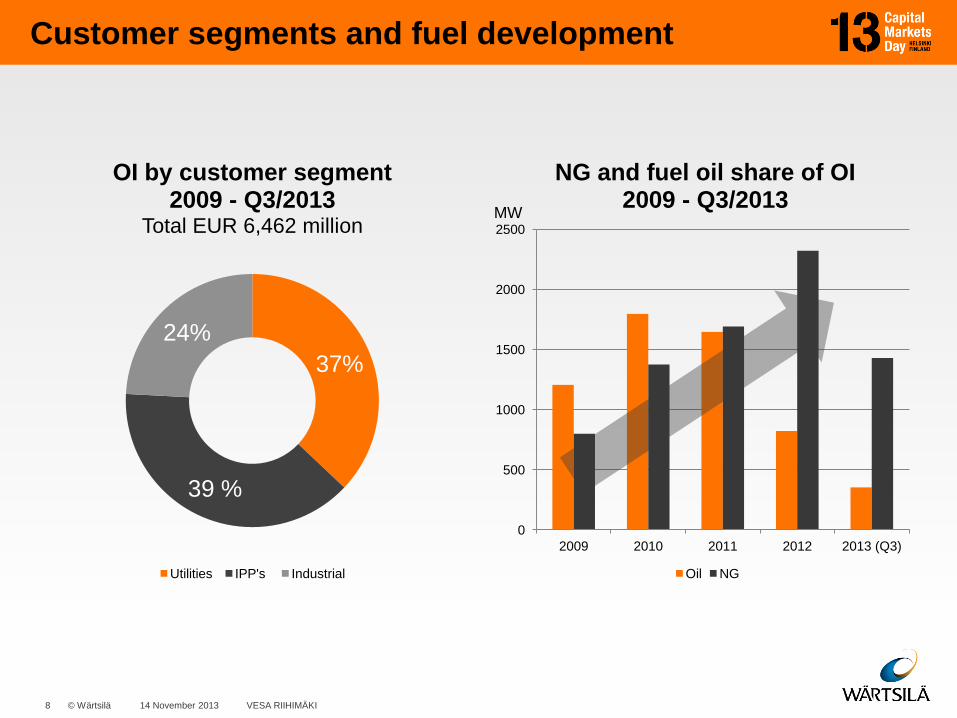

Customer segments and fuel development

37%

39 %

24%

OI by customer segment 2009 - Q3/2013

Total EUR 6,462 million

Utilities IPP's Industrial

0

500

1000

1500

2000

2500

2009 2010 2011 2012 2013 (Q3)

NG and fuel oil share of OI 2009 - Q3/2013

Oil NG

MW

© Wärtsilä 8 14 November 2013 VESA RIIHIMÄKI

Energy

efficiency

Operational

flexibility

Fuel

flexibility

Smart

Power

Generation

Approach markets with Smart Power Generation

All in one!

Smart Power Generation is a new concept which enables an existing power

system to operate at its maximum efficiency by most effectively absorbing

current and future system load variations, hence providing dramatic savings.

© Wärtsilä 9 14 November 2013 VESA RIIHIMÄKI

SPG supports most energy infrastructure types

Liquid fuel

infrastructure

only

Transition to

NG (LNG

infrastructure)

NG as

mainstream

energy

NG as

balancer for

renewable

energy

© Wärtsilä 10 14 November 2013 VESA RIIHIMÄKI

Transition to NG: Smart Power Generation meets LNG

Dual-fuel power plant Medium scale LNG terminal

• Initial operation using HFO

15-16$/MMBtu

• Provides base gas consumption for NG,

enabling investment for the LNG terminal

• NG cost using LNG 11-17 $/MMBtu

• Plant feasibility typically improves with

NG, which is a strong driver for investment

• Economic feasibility depends on scale

• larger terminals can receive larger

tankers which lowers LNG price

• ship size is a key factor

• 50-1,000MWth flow is typically

considered Medium size

• 10,000-160,000 m3 tank sizes

• Tank size to match ship size

© Wärtsilä 11 14 November 2013 VESA RIIHIMÄKI

Transition to NG: Smart Power Generation meets LNG

• Wärtsilä Power Plants has developed

capabilities to become an EPC supplier

for medium scale LNG storage and

regasification terminals

• Wärtsilä can support and enable transition

to gas infrastructure by providing a one

stop shop for the investments related to

power generation and LNG infrastructure

• Wärtsilä’s offering is based on strong EPC

capability for power plants combined with

regasification solution from Wärtsilä

Flow & Gas

© Wärtsilä 12 14 November 2013 VESA RIIHIMÄKI

NG as balancer: changing business model

Traditional world

• Fossil fuels provide baseload energy

• Business model is based on

producing energy (MWh) and getting

a small margin sale

• Solution parameters:

– Electrical efficiency

– Investment cost

– Long-term power purchase

agreement

• Static world

World of renewable energy

• Wind and solar provide increasing

share of energy

• Business model for fossil fuels is to

generate power when renewable

energy is not available

• Solution parameters:

– Operational flexibility

– Energy efficiency

– Remuneration based on

balancing services

• Dynamic world

© Wärtsilä 13 14 November 2013 VESA RIIHIMÄKI

Energy Infrastructure Package:

Implementation progress and expected outcome

Catharina Sikow-Magny

European Commission, Director General for Energy

23-24 May,2013

• Large scale deployment of solar and

wind truncates thermal plants to a

narrow operating window

• CCGT load factors are consistently

going down, but the day vs. night gap

is increasing, causing technology to

operate at its most suboptimal

conditions, low load and cyclic

operation

• System needs SPG – OFF at night,

ON at peaks

• Energy only market does not support

investment for balancing power

• EU is striving towards harmonic

capacity/flexibility markets to support

investment for balancing power

NG as balancer: a need for balancing in the EU

© Wärtsilä 14 14 November 2013 VESA RIIHIMÄKI

California: Net load patterns changing rapidly due to wind & solar

– 2020 expectation is 14GW in 4 hours during non summer months

NET LOAD = LOAD – wind & solar generation

Source: California ISO, Karl Meeusen

California: Solar generation is effectively

turning the daily peak to a daily low

Massive up/down ramps expected,

up to 14GW in 4 hours in 2020

• Fossil generation more than doubled

in 4 hours

• 14GW is the approximate peak load of

Finland

Market opportunity is emerging as ISO’s

are recognizing the value of flexibility

• STEC & Portland projects

NG as balancer: system changes are a reality

© Wärtsilä 15 14 November 2013 VESA RIIHIMÄKI

Wärtsilä is the leader in Smart Power Generation

TECHNOLOGY SOLUTIONS REFERENCES

© Wärtsilä 16 14 November 2013 VESA RIIHIMÄKI

Wärtsilä Power Plants as EPC supplier

• Wärtsilä Power Plants has extensive

experience in turnkey power

solutions since early 90’s

• Approximately 25% of the projects

are executed on an EPC basis

• The turnkey supplier role provides

visibility on the overall economics of

investments and the potential

challenges that our customers have

– key knowledge for solution

development

Basic EEQ

Site Preparation/Soil improvement

Site Investigations Package

EPCM (Construction Mgmt Service )

Extended EEQ

Delivery Value proposition

Basic Eq and Process engineering /Power

Generation

BOP Eq and Materials, Detailed Plant

Engineering

Installation /Power Generation

Foundations &Site Infra

Admin and Service buildings

Substation/El. Interconnection

Full HRC / CC

Emission Control

Options for

all scopes

EPC

Option

s

Scope

Process EPC

EPC

EPC above 0-level

© Wärtsilä 17 14 November 2013 VESA RIIHIMÄKI

Quisqueya I&II 430MW, dual-fuel flexicycle

May 2012 February 2012 November 2011

August 2012 November 2012 March 2013

Quisqueya I&II, Dominican Republic 430MW / dual-fuel flexicycle

Power supply to a gold mine and peaking power to the utility

Wärtsilä EPC delivery

© Wärtsilä 18 14 November 2013 VESA RIIHIMÄKI

Quisqueya I&II 430MW, dual-fuel flexicycle

September 2013

© Wärtsilä 19 14 November 2013 VESA RIIHIMÄKI