Embed Size (px)

Citation preview

Voluntary Early Retirement

Incentive ProgramJanuary 27, 2015

Linda Byron, Partner, Aon HewittSusan Diep, Manager Compensation & Benefits

Today’s agenda Program overview Incentive options What you need to consider Online modelling tool demonstration Questions

Program overview• Monetary incentive to retire = 1 year reference

salary• Retire between July 1, 2015 and July 1, 2017• Does not change pension formula• University must approve application• Designed to help achieve budget reductions

Eligibility to apply By July 1, 2017 will you be…

A full-time Laurier continuing employee in an applicable group (WLUSA/OSSTF, CPAG, PAG, Special Constables), Management?

Yes

At least age 60? Yes

A pension plan member with a combined age and years of pensionable service at the University of at least 80?

Yes

Already participating in a phased in retirement or SVEP or on LTD benefits for more than 2 years?

No

Application and approval process

February 1, 2015 February 28, 2015 March 31, 2015

Fill out online “intent to apply” notification form

Complete and return the paper application form

University reviews applications and

sends notification

Important!Applications are subject to

University approval.Approved applications are

irrevocable.

Your incentive options

Choose one of three incentive options

Lump sum paid on your last pay at retirement

date

Salary continuance beginning up to one year before your retirement

date

Combination of salary

continuance and lump sum amount

or or

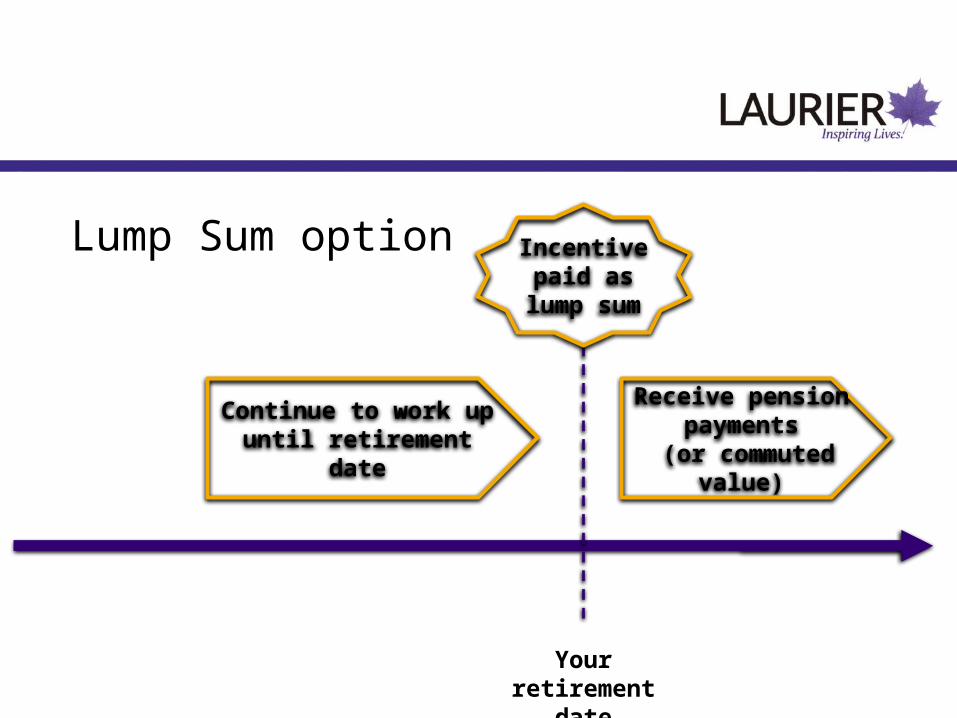

Lump Sum option

Continue to work up until retirement date

Receive pension payments

(or commuted value)

Your retirement date

Incentive paid as lump

sum

Lump sum optionPayments Single amount paid at retirement date - qualifies as

Retirement AllowanceIncome tax Deducted after applicable RRSP transfer, at lump sum rates

(10 to 30%)CPP and EI deductions,Union Dues

None

Transfer to RRSP Transfer eligible portion without affecting contribution room, transfer non-eligible portion if RRSP room available

Benefits Post-retirement benefits (capped at $30,000 per year)

Pension No further contributions or service accrual

Salary Continuance

Your program start date

Receive salary continuance for 12 months

Receive pension payments

(or commuted value)

Your retirement date

Stop working

Salary continuance optionPayments Up to 12 months of regular pay until retirement date

Salary frozen during this periodIncome tax Calculated and deducted as normal earnings

CPP and EI deductions,Union Dues

Calculated and deducted as normal earnings

Benefits Health, dental and basic life insurance benefits continue under active plan until retirement date. Employee-paid

benefits (LTD, AD&D, Optional Life) will cease.Pension Contributions and pensionable service accrual continue

until retirement dateVacation and Sick Leave Vacation and sick leave accrual ends. Unused vacation will

be paid out.

Combination option

Your program start date

Receive salary continuance for less than 12 months

Receive pension payments

(or commuted value)

Your retirement date

Balance of incentive

paid as lump sum

Stop working

What you need to consider

1. How does your age and pensionable service affect:• when you can start the program• what options are available for you

Example 1 – Meets requirements in 2015Alex

Turns age 60 Feb 12, 2014

Reaches “80” factor Mar 6, 2012

Earliest program start date July 1, 2015

Latest retirement date July 1, 2017

Salary continuance option 12 months max

Lump sum option Yes

Example 2 – Meets requirements in 2016Alex Pat

Turns age 60 Feb 12, 2014 Nov 25, 2016

Reaches “80” factor Mar 6, 2012 May 5, 2014

Earliest program start date July 1, 2015 Dec 1, 2016

Latest retirement date July 1, 2017 July 1, 2017

Salary continuance option 12 months max 7 months max

Lump sum option Yes Yes

Example 3 – Meets requirements in 2017Alex Pat Terry

Turns age 60 Feb 12, 2014 Nov 25, 2016 Sept 6, 2015

Reaches “80” factor Mar 6, 2012 May 5, 2014 June 23, 2017

Earliest program start date July 1, 2015 Dec 1, 2016 July 1, 2017

Latest retirement date July 1, 2017 July 1, 2017 July 1, 2017

Salary continuance option 12 months max 7 months max No

Lump sum option Yes Yes Yes

2. Does your normal retirement date fall within the incentive window? Do you want to retire on your normal retirement date?

You can keep working and retire at your normal retirement date

Continue working until you reach age 65 (or later)

Receive unreduced pension payments

(or commuted value)

Your normal retirement date

Receive lump sum

Today

Or take salary continuance for up to a year before retirement

With salary continuance you continue to accrue pension

benefits

Receive unreduced pension payments

(or commuted value)

Your normal retirement date

Full pension

Your program start date

Stop working

3. Are you thinking of retiring before your normal retirement date?

If you retire early, your pension benefit will be reduced:Pension Reduction formulas for retirement age 60-65

Money Purchase Annuity conversion factor rate is based on your age at retirement. Lower age = lower annuity

Minimum Guarantee For each year prior to age 65, benefit is reduced:

1.5% for service prior to January 1, 2013and

3% for service on and after January 1, 2013

Let’s look at an example for a member with final average earnings of $60,000.

What difference will it make if the member retires immediately (takes the lump sum) or retires one year later (takes salary continuance)?

• The reduction is blended based on the split between pre-2013 and post-2012 service

• The reduction is much less than the true actuarial “value” of the additional years of pension

Takes lump sum and retires on July 1, 2016

Age 60

Takes salary continuance and retires on July 1, 2017

Age 61Years of service 25 26

Estimated earned pension $22,100 $22,800

Reduction applied 8.6% 7.0%

Reduced annual pension $20,200 $21,200

Difference - $1,000

4. What other sources of retirement income do you have?

Pension from former employer(s) CPP & OAS benefits RRSP

Non-registered savings Real estate Inheritance

5. What about health, dental and insurance benefits?

With salary continuance, your health, dental and basic life insurance benefits continue

under the active plan

After retirement you receive retiree health &

dental benefits ($30,000 cap on health )

Your retirement date

Full or reduced pension

Your program start date

Keep upcoming changes in mind

January 1, 2016 January 1, 2017

University-paid Retiree benefits

regardless of pension choice

Receive Retiree benefits only if receiving monthly pension

Retiree pays 15% of benefit premiums

6. Have you consulted your financial advisor?

This is an important decision.You should review how it fits into your overall financial situation with your personal financial

advisor.

Resources:Employee & Family Assistance Program• E-courses and materials on retirement planning• Plan Smart Lifestyle Counselling Services

www.homewoodhumansolutions.com/MSA1-800-663-1142

Online Pension Information Portal• View your personalized pension information• Run pension estimates for different retirement dates

https://wlu.penproplus.com

Resources:Human Resources• Questions regarding voluntary retirement incentive program• Susan Diep – [email protected] ext 4487• Mary Jo DaSilva – [email protected] ext 4368

Laurier Pension Contact Centre• Questions regarding pension estimate and options• Trouble accessing online portal• Toll-free at 1-844-342-3624

Questions?