Embed Size (px)

Citation preview

Executive MonitorHealthcare and Life Sciences

Volume 2 : Issue 1 : 2015

2

Executive MonitorHealthcare and Life Sciences

Key Trends Various factors are converging to change the landscape of the traditional Healthcare and Life Sciences sector. For one, the global healthcare industry is characterized by innovation and advancements in practices, treatments, and general business strategy across subsectors. This is illustrated by an increase in patent applications and overall investment and spending. Certain geographies and therapies outperform others. For example, North America and Europe are leaders with respect to the number of patent applications per year, primarily because the focus in developed countries has shifted to using “specific, personalized biologics and care” to treat complex and serious diseases. Specifically, oncology has become a major area in drug development and spending. Though not quite on the same par, Asia, Latin America and the

Executive Summary

Globally, the Healthcare and Life Sciences sector is facing many challenges that are resulting in disruption along management, technological, and regulatory lines. While the quality and access of healthcare remains uneven among regions, there are more opportunities than ever to provide better value to patients while being more cost-effective.

Many countries are under increasing pressure to stretch their dollars as a greater proportion of the populace ages and is diagnosed with chronic diseases. Consequently, governments, pharmaceutical and medical technology companies, and healthcare providers are breaking down traditional methods of treating patients. Thus far there has been measurable success in technological and supply-chain innovation, especially with the increased use of big data and evaluation of hospital efficiency based on patient outcomes, as opposed to traditional metrics such as the cost of each department, patient surveys, and wait times.

Executives in the sector will continue to face financial and regulatory challenges; at the same time they must look for enhanced ways to meaningfully connect with patients and improve operational effectiveness.

“The healthcare industry has shifted and is putting great emphasis on talent acquisition from fast moving consumer goods companies such as Procter & Gamble, Unilever and Reckitt Benckiser. These executives bring strong experience in change management, brand development and other areas important for mass marketing on a larger scale.” Kerstin Roubin, Global Leader of Boyden’s Healthcare & Life Sciences Practice and Managing Partner, Boyden Austria

3

Executive MonitorHealthcare and Life Sciences

Caribbean are also increasing their patent applications. However, instead of concentrating on specialized treatments, these developing countries or “pharmerging” markets are turning to “broad, chronic diseases” and more traditional therapy areas, like antibiotics and pain management.1 2 3

4

Source: http://bit.ly/1McDhst

An aging population has posed interesting challenges for the industry in two distinct ways, with both consumers and employees fuelling an important transformation. On the consumer side, an increasingly elderly patient base has strained service providers operationally and financially. It has also, however, been the impetus for transforming the industry, by pushing the sector to find innovative therapies and treatments, as well as to rethink operations and business models. On the employer facet, hiring managers face difficulty in filling positions because the talent base has gradually aged itself out of the industry: “Between 1993 and 2010, the percentage of the scientific and engineering workforce over the age of 50 increased from 20% to 33%.”

In five years, approximately two million jobs in engineering and life sciences will be newly vacant, primarily due to an exodus of retirees. In addition to a dearth of younger employees, women are underrepresented in the industry. It is expected that the increasing popularity and promotion of STEM initiatives and programs, especially in the United States, will provide employers with an equally skilled but younger and more diverse talent base.5

The legal sphere also plays a role in the future of healthcare. Regulations, especially in the United States and Japan, are burdensome realities for the industry. Consequently, a number of firms recently relocated or began the purchase of other companies that are headquartered

1 http://www.forbes.com/sites/nicolefisher/2014/11/21/7-trends-driving-global-health-and-life-science-in-2015/2 http://www.imshealth.com/deployedfiles/imshealth/Global/Content/Corporate/IMS%20Health%20Institute/Reports/Global_Use_of_ Meds_Outlook_2017/IIHI_Global_Use_of_Meds_Report_2013.pdf 3 Further data analysis and summaries by FTI Consulting, presented at FTI Healthcare Summit, Fall 2014 4 Further data analysis and summaries by FTI Consulting, presented at FTI Healthcare Summit, Fall 20145 http://www.forbes.com/sites/nicolefisher/2014/11/21/7-trends-driving-global-health-and-life-science-in-2015/

4

Executive MonitorHealthcare and Life Sciences

Source: Healthcare Summit presentation deck http://bit.ly/1McDhst

in areas abroad thought to be more tax friendly and offering greater long-term stability. According to Roger Humphrey, Executive Director of private equity firm JLL’s Life Sciences group, “Federal policy, such as corporate tax structures and regulatory frameworks, directly impacts life sciences companies’ ability to establish roots and flourish over time.” While many believe that regulation has contributed to the successes of the industry in the past, companies are now actively looking for ways around legal and regulatory limitations.6

Products, too, are changing the landscape. Generic drugs will become more prevalent in the years to come, especially in emerging countries, where generics will represent 63% of the market. While branded drugs will continue to dominate in developed countries, generics will slowly realize a larger market share. This is partly due to the number of patents expiring in the near future. Spending in pharmerging markets will increase drastically as well and reach nearly $400 billion by 2017. Spending on traditional pharmaceuticals is also expected to increase drastically in pharmerging markets, reaching $336 billion by 2017, a 69% increase from 2012. 7

6 http://www.forbes.com/sites/nicolefisher/2014/11/21/7-trends-driving-global-health-and-life-science-in-2015/ 7 http://www.imshealth.com/deployedfiles/imshealth/Global/Content/Corporate/IMS%20Health%20Institute/Reports/Global_Use_ of_Meds_Outlook_2017/IIHI_Global_Use_of_Meds_Report_2013.pdf

Pharmaceuticals In 2015 the pharmaceutical sector will be challenged to find new growth opportunities, decrease risk, and increase efficiency, especially as it is impacted by “new regulations, advances in technology and tighter revenues.” Five trends are expected to come to fruition this year:

(1) Serialization; companies are examining supply chains to “facilitate visibility and collaboration from end-to-end” in order to “track, trace, and validate the origin of ‘medicinal products for human use.’” (2) Patents are about to expire on many blockbuster drugs. Accordingly, firms will have to find new sources of revenue and cut costs to increase profitability. Two critical components for success will include developing top marketing strategies for new products and delivering these products to the developing world. These shifts are impacted by the rise of generic drugs, imminent not only because of expiring patents but also due to their lower cost of production.

5

Executive MonitorHealthcare and Life Sciences

(3) The effect of these trends in available and affordable drugs especially benefits developing countries. (4) Big data will play a larger role, as companies embrace digitization. This can help traceability of products, areas of risk or growth, and promote intelligent forecasting. (5) Finally, pharmaceutical companies will begin to adopt a mind-set more similar to retailers, especially in terms of supply chain flexibility. Retailers often have many suppliers and markets with very different needs, as well as low margins. As a result, “They have to channel products to different markets and can’t afford to leave things on the shelf.”8

Source: http://bit.ly/1yg7JaK

Larger conglomerates still dominate the sector. Novartis, headquartered in Switzerland, stands out as the top pharma company; Pfizer, headquartered in the United States, closely follows. While “big pharma” is still the key force and leads the sector in drug sales, small biotechs are on the rise and driving innovation with unique products.9 Despite their increasing presence, the high costs and barriers to entry in the pharmaceutical industry make it difficult for small biotechs to compete with big pharma. Because of this, small biotechs tend to be acquired by big companies that want to expand their portfolios.10 CEOs and top executives from both big pharma and small biotechs must be able to think critically and make strategic decisions about such acquisitions going forward. Small biotechs also tend to have limited R&D budgets; some of these companies have received financing from big pharma, through deals and licensing, whereas others have created partnerships with academic institutions.11

8 http://www.pharmamanufacturing.com/articles/2014/five-trends-to-watch-in-2015/ 9 http://images.alfresco.advanstar.com/alfresco_images/pharma/2014/11/25/6b62704d-511b-4b8b-8d26-406a753f1e0a/article-856395.pdf 10 http://www.pharmpro.com/blogs/2014/12/biotech-and-generic-drugs-2015-trends-and-predictions 11 http://www2.deloitte.com/content/dam/Deloitte/global/Documents/Life-Sciences-Health-Care/gx-lshc-2015-life-sciences-report.pdf

6

Executive MonitorHealthcare and Life Sciences

Healthcare Information/Medical Technology As in many other industries, technology is being utilized in the healthcare and medical fields to a greater extent than any time in the past, changing products, services, and the manner in which the industry operates. To name some examples, portable and battery-powered devices are on the rise, and as such, “smarter and more intricate components are increasingly in demand.” In addition, advances in data management “can help facilitate new diagnostic and treatment options.” With the rise of technology, unfortunately, costs also rise; efficient use of resources is therefore critical. 12 13

Not unlike the healthcare industry overall, professionals and executives in the medical technology subsector require a highly technical skillset. Given the shortage of qualified professionals in other sectors, it is important for the information technology sector to attract and retain skilled employees and executives.

Big Data Big data in the healthcare industry is transforming the way the system currently operates. Increases in transparency, better patient outcomes, and accessible care are just a few of the results of big data implementations. Dwayne Spradlin, CEO of Health Data Consortium, elaborates, saying that “the power to access and analyse enormous data sets can improve our ability to anticipate and treat illnesses. This data can help recognize individuals who are at risk for serious health problems.” 14

There is still a long way to go and a number of challenges to overcome. Notably, while big data has made a great deal of information available, an overwhelming amount of data has not yet been consolidated and remains scattered. Aggregating all of this information will be a monumental undertaking, as will maintaining patient privacy throughout the process. However, opportunities exist, and experts see the potential of big data; in the first quarter of 2013, “venture capitalists invested nearly $700 million into digital health start-ups.” 15

A promising area in the field which presents exciting opportunities for both technical and management professionals is DNA sequencing. DNA (or gene) sequencing is the process of “finding a single gene amid the vast stretches of DNA that make up the human genome.”16

This innovative method has led scientists to medical discoveries and prompted new research in the field. In addition, scientists involved in big data are attempting to utilize DNA sequencing as a means of storing data.

Researchers at Harvard University have stated that it will “soon be possible to store the entire content of the entire World Wide Web within just 75 grams of DNA material.” This is still not a cost-effective approach, but scientists expect it will not be long before this theory becomes reality.17 Professionals with an eye toward innovating, especially, will be in high demand as companies specializing in this nascent field advance the science.

12 http://www.mdtmag.com/blogs/2014/12/5-trends-medical-technology-2015 13 https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Life-Sciences-Health-Care/dttl-lshc-2014-global-health-care- sector-report.pdf 14 http://www.forbes.com/sites/castlight/2014/11/10/how-big-data-will-help-save-healthcare/ 15 http://www.forbes.com/sites/castlight/2014/11/10/how-big-data-will-help-save-healthcare/16 http://www.genome.gov/1000117717 http://siliconangle.com/blog/2013/11/25/inside-the-dna-of-big-data-the-future-of-medicine-storage/

7

Executive MonitorHealthcare and Life Sciences

Medical Products and Devices Funding for projects will be an issue for entrepreneurial device developers, though there are a number of astonishing advancements being made in this subsector. The most notable provide ample opportunities for specialists, investors and executives alike. A few noteworthy trends include:

(1) 3D printing, which will allow customization for each patient, as well as the “ability to individualize a therapeutic or surgical device.” Manufacturers must find ways to assess the safety and effectiveness of each product; until then the future of 3D printing in the healthcare industry remains ambiguous.

(2) The natural expansion in the implants market due to a growing aging population will also create new opportunities for devices and the communications and technologies that support them.

(3) There will be an increased demand for immunoassays to address the development and use of biologic therapeutics.

(4) Molecular diagnostics will play a greater role in screening, diagnosis, and even treatment of many diseases by identifying associated genetic variants. The emergence of microRNA (miRNA) diagnostics is expected this year.

(5) Device developers will have to provide greater transparency in order to secure reimbursement from payers. It is projected that this “may also lead to more realistic assessments of the market value of novel devices earlier in the development cycle”, which in turn could lead to greater investments and potential venture partnerships.

(6) The improvement of diagnostics and treatments for infectious diseases will provide greater opportunities for growth in both developed and emerging countries.

In general “increasing efficiency in clinical development through excellence in operations and innovative study design” will be of critical importance through 2015. Recovering R&D costs and maintaining profit margins will be necessary, especially given payer resistance to pricing for new products. Strategies that aim to reduce costs and timelines will be essential. And, developing partnerships with experienced counterparts who can achieve higher operational efficiency will be important.18

Healthcare Providers and Services

Globally, providers are reacting to market-driven changes that render traditional approaches to healthcare obsolete. The global population is increasing and aging, resulting in a greater demand for medical staff.19 However, the industry faces a shortage, especially of physicians.20 The number of doctors per 1,000 people is expected to remain the same through 2015. In Europe and Asia, the shortage is expected to become more problematic over the next few years, which could affect the delivery of even the most basic forms of medical care. Asia overall seems to be faring better than Europe, although coverage across the continent is still uneven, with countries such as China, Indonesia, Vietnam and India struggling to keep up with the needs of patients.

In the United States, experts estimate that by 2025, there could be a shortfall of as many of 150,000 physicians. 21

18 http://www.healthdec.com/blog/white-paper-heralding-2015-medical-device-trends/ 19 https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Life-Sciences-Health-Care/dttl-lshc-2014-global-health-care- sector-report.pdf 20 https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Life-Sciences-Health-Care/dttl-lshc-2014-global-health-care- sector-report.pdf 21 http://www.maastary.com/healthcare-provider-industry-trends/

8

Executive MonitorHealthcare and Life Sciences

To prevent this deficiency, some universities have attempted to make the medical profession more appealing. Harvard Medical School, for example, has invested in redesigning their curricula so medical residents train in small teams as opposed to alone, since many medical students are reluctant to pursue a career in primary care because it is too solitary. 22

There is also a lack of healthcare infrastructure to keep up with patient needs. Hospitals in both developed and emerging markets around the world cannot provide adequate basic care. For instance, in many nations there is a lack of hospital beds. According to studies by Deloitte, countries such as Brazil lack primary care infrastructure; this results in patients going directly to hospitals, raising both costs and hospitalization rates. Additionally, access to care may be difficult for those in underinvested areas, such as smaller towns and rural enclaves, where residents are also likely to have a high out-of-pocket expenditure. These patients are either unable to access healthcare or pay large amounts for treatment at a more advanced stage of the disease.

2014 Global health care outlook Shared challenges, shared opportunities 5

While facilitating increased health care access is an important and worthy endeavor, more people in the system means more demand for services that numerous health care systems are unable to accommodate due to workforce shortages, patient locations, and infrastructure limitations, in addition to the cost issues identified earlier.

Many countries across the globe are facing a challenge to meet their required number of health care workers, a shortage that directly affects the quality of care. Globally, the number of doctors per 1,000 population is expected to remain virtually the same between 2012 and 2015 (Figure 2).29

More than one billion people worldwide lack access to a health care system,30 both for caregivers and facilities. The United Kingdom, for example, had an estimated shortage of 40,000 nurses in 2012, and has a shortage of other health care professionals, including general practitioners (GPs). According to a European commission, there will be a shortage of 230,000 physicians across the continent in the near future.31 The number of caregivers in 36 countries in Africa is inadequate to deliver even the most basic immunization and maternal health services. Rapid economic development across Asia has led to hugely increased access to health care, yet coverage across the region remains uneven. Developed Asian countries such as Singapore,

South Korea, Japan, and Taiwan offer world-class health systems while poorer neighbors such as Indonesia, Vietnam, and India struggle to provide even the most basic coverage. And, like many countries, China is lacking millions of nursing home employees to care for its growing elderly population.32

Uneven distribution of caregivers is also a problem. The physician and mid-level caregiver supply is increasing significantly in the U.S., due to increased enrollment in existing medical schools and the opening of about a dozen new medical schools. From 1970 to 2010 the U.S. physician-to-population ratio increased by 98 percent (from 161 per 100,000 to 319 per 100,000).33 At the same time, India, Nigeria, and Pakistan have critical health workforce shortages but also are in the top 25 countries for the number of their doctors and nurses that are migrating to other countries. More than 50 percent of foreign-born doctors and 40 percent of foreign-born nurses in the U.S. are from Asia.34 Numerous countries in the Middle East have a significant shortage of local talent; numbers indicate dominance of the expat communities in both the nursing and physician functions. South Africa’s caregiver shortage is so acute that the government has been pursuing bilateral and multilateral agreements aimed at discouraging destination countries from “poaching” key health care workers.35

29 Economic Intelligence Unit Database, Losing Ground: Physician Income, CNN Health, World Bank30 Global Issues: http://www.globalissues.org/issue/587/health-issues, Losing Ground: Physician Income, CNN Health, World Bank31 China Daily: http://usa.chinadaily.com.cn/china/2012-10/23/content_15837603.htm, WHO, CNBC32 Ibid33 Derek R. Smart, Physician Characteristics and Distribution in the US, 2012 Edition (American Medical Association, 2012), as cited in “Physician Sup-

ply and the Affordable Care Act,” Congressional Research Service, January 15, 2013. http://op.bna.com/hl.nsf/id/myon-93zpre/$File/crsdoctor.pdf. Accessed January 6, 2014

34 China Daily, Africa portal, Migration Information: http://www.migrationinformation.org/usfocus/display.cfm?ID=35 South Africa: Healthcare and Pharmaceuticals Report, Economist Intelligence Unit, March 25, 2013

Figure 2: Doctors per 1,000 population vs. world population

6650

6700

6750

6800

6850

6900

6950

7000

7050

7100

0

2

4

6

8

10

2012E 2013E 2014E 2015E

Popu

lati

on in

mill

ions

8.2

8.2

6.9

6.6

World Population

Doctors per 1000

Source: DTTL Global Life Sciences and Health Care Industry Group analysis of Economist Intelligence Unit database

Source: http://deloi.tt/1DEYp77

22 http://www.usnewsuniversitydirectory.com/articles/new-harvard-medical-center-works-to-attract-studen_12314.aspx#.VKquByvF_To

9

Executive MonitorHealthcare and Life Sciences

Source: http://deloi.tt/1DEYp77

Given their limited resources, many hospitals are reconsidering traditional approaches to healthcare. Among providers, there is an influx of M&A activity. Increased horizontal integration is enabling hospitals to cut costs by better collaborating with one another, increasing their purchasing power, and consolidating services. Furthermore, vertical integration is resulting in hospitals buying offerings such as physician practices, ambulatory centres, and home care services. All of these efforts demonstrate a shift toward managing risks and costs “along the entire care continuum.”23

Cost efficiency of treatment is also being assessed in new ways. Traditionally, hospital efficiency has been measured by the separate cost of each department or unit, wait times, and patient surveys. Quality is assessed by surveys and compliance with treatment guidelines. The new “value-based hospital” model, however, measures cost efficiency and quality of service differently. Financial efficiency is measured by evaluating healthcare outcomes and costs and how those outcomes were achieved along the clinical pathway. As a result, the patient is the top priority, and different departments and units must communicate and take joint responsibility in order to deliver high-quality and cost-effective care.24

The novel approach of making the patient the focal point of care is also leading to the personification or “consumerization” of healthcare. Concrete patient needs are increasingly being put ahead of assumptions of those same needs traditionally made by providers.25

Some examples of this include allowing patients to customize their caregiving experience based on their language preference, diet, religion, communication preferences, and even what magazines they like to read.26

6

Bolstering the number of professional medical, nursing, and other health care professionals is not the only staffing challenge facing hospitals and health systems in 2014 and beyond: Organizations will need to source, recruit, and retain staff, such as advanced nurse practitioners and telemedicine technicians, who are trained to meet the needs of new 21st-century health care models.

Workforce shortages are a major contributor to health care access problems around the world; patient location can be another deterrent to care. In India, for example, about 80 percent of the population lives in rural areas. Many of these rural areas lack good hospitals when compared to urban parts of India; some rural areas even lack a dispensary.36 Finding innovative solutions to provide health care outside of the traditional hospital setting is going to be critical for industry stakeholders.

A third constraint on patient access is lack of health care infrastructure in certain countries and outdated facilities in both developed and emerging markets. For example, the number of hospital beds per 1,000 population varies from country to country — ranging between 0.3 per 1,000 in Guinea to 11.1 in Belarus (2011)37 — clearly indicating the difference in access to health care around the globe (Figure 3). Due to the lack of a primary care infrastructure in Brazil, patients go directly to hospitals, raising both costs and hospitalizations rates.

One of the major problems in Mexico’s health care system is the lack of resources allocated for the country’s health infrastructure. According to the Organisation for Economic Co-operation and Development (OECD), Mexico spends 6.2 percent of GDP on health care, more than three percentage points lower than the average of 9.5 percent in OECD countries and the second-lowest share among OECD countries, after Turkey.38 There are also limited public-private partnerships to fund infrastructure projects. This underfunding results in a lack of material resources for constructing and equipping medical care units; e.g., insufficient beds, operating rooms, and specialized equipment.

India’s primary health care infrastructure and physician base remain inadequate despite the Ministry of Health and Family Welfare (MoHFW) expanding access to care into tier 1 and 2 cities through the National Rural Health Mission (NHRM). Also, a high patient out-of-pocket-expenditure (>70 percent of total health care costs) implies that many of those living in underinvested areas (i.e., smaller towns and rural areas) either do not have access to health care or have to pay significantly more for treatment because they travel to larger cities and often get treated at an advanced stage of the disease.

36 Difference between Urban and Rural India, http://www.differencebetween.net/miscellaneous/difference-between-urban-and-rural-india. Accessed December 12, 2013

37 World Bank Database38 OECD Better life index. “Mexico. How is life?” available at http://www.oecdbetterlifeindex.org/countries/mexico/

Figure 3: Access to care: Hospital beds

0.0

1.5

3.0

4.5

6.0

7.5

9.0

Germany France United States United Kingdom

Hospital beds (per 1,000 people)

Brazil Mexico

8.2 8.2 8.3

3.1 3.0 3.0

7.1 6.9 6.6

3.4 3.33.0

2.4 2.4 2.4

1.6 1.6 1.71.3 1.3 1.3

Iraq

2008

2009

2010

Source: DTTL Global Life Sciences and Health Care Industry Group analysis of World Bank database

23 http://www2.deloitte.com/us/en/pages/life-sciences-and-health-care/articles/2014-health-care-providers-outlook.html 24 https://www.bcgperspectives.com/content/articles/health_care_payers_providers_transformation_large_scale_change_value_ based_hospital/ 25 http://www.kpmg.com/Global/en/IssuesAndInsights/ArticlesPublications/whats-next-for-healthcare/Pages/cynthia-ambres- consumerization-healthcare.aspx 26 http://www.theihcc.com/en/communities/health_care_consumerism/the-consumerization-of-healthcare-what-patient-exp_h333dkhj. html

10

Executive MonitorHealthcare and Life Sciences

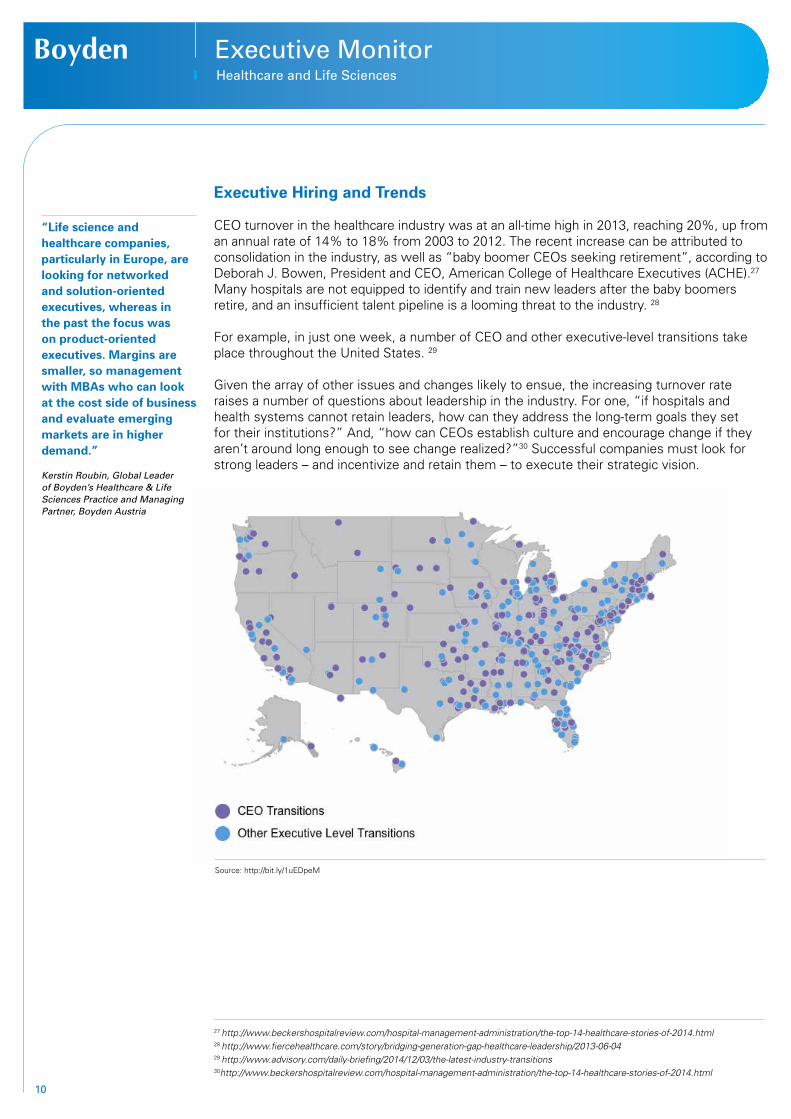

Executive Hiring and Trends CEO turnover in the healthcare industry was at an all-time high in 2013, reaching 20%, up from an annual rate of 14% to 18% from 2003 to 2012. The recent increase can be attributed to consolidation in the industry, as well as “baby boomer CEOs seeking retirement”, according to Deborah J. Bowen, President and CEO, American College of Healthcare Executives (ACHE).27 Many hospitals are not equipped to identify and train new leaders after the baby boomers retire, and an insufficient talent pipeline is a looming threat to the industry. 28

For example, in just one week, a number of CEO and other executive-level transitions take place throughout the United States. 29

Given the array of other issues and changes likely to ensue, the increasing turnover rate raises a number of questions about leadership in the industry. For one, “if hospitals and health systems cannot retain leaders, how can they address the long-term goals they set for their institutions?” And, “how can CEOs establish culture and encourage change if they aren’t around long enough to see change realized?”30 Successful companies must look for strong leaders – and incentivize and retain them – to execute their strategic vision.

Source: http://bit.ly/1uEDpeM

“Life science and healthcare companies, particularly in Europe, are looking for networked and solution-oriented executives, whereas in the past the focus was on product-oriented executives. Margins are smaller, so management with MBAs who can look at the cost side of business and evaluate emerging markets are in higher demand.” Kerstin Roubin, Global Leader of Boyden’s Healthcare & Life Sciences Practice and Managing Partner, Boyden Austria

27 http://www.beckershospitalreview.com/hospital-management-administration/the-top-14-healthcare-stories-of-2014.html 28 http://www.fiercehealthcare.com/story/bridging-generation-gap-healthcare-leadership/2013-06-04 29 http://www.advisory.com/daily-briefing/2014/12/03/the-latest-industry-transitions 30http://www.beckershospitalreview.com/hospital-management-administration/the-top-14-healthcare-stories-of-2014.html

11

Executive MonitorHealthcare and Life Sciences

Succession planning has increased over the past decade. According to a report from ACHE, only 21% of hospitals used formal succession plans for the CEO position in 2004; now, 52% of hospitals have one in place.31

As in many other industries, CEO compensation has come under scrutiny and criticism in recent years. Now, many hospitals will add quality-based metrics to CEO and executive compensation packages. In an effort to incorporate and align physicians with hospital and health systems, executive compensation will be “tied to how well they integrate and collaborate with medical staff.”32

Health systems are expected to add chief marketing officers to their C-suite, as a focus on the patient becomes more important. Patient satisfaction is paramount, and government reimbursements depend on it. In addition, “healthcare companies will be forced to compete for consumer attention”. Patients demand information such as pricing and doctor ratings, similar to what they expect with products, likening the healthcare decision-making process to shopping.33

Healthcare CEOs express confidence in the global economy, according to PwC’s 18th Annual Global CEO Survey (2015). Nearly eight in 10 expect to increase sales in the next year, and almost nine in 10 expect this to happen in the next three years. Despite this confidence, over-regulation and changes in regulation are still a concern, as is the availability of necessary skill sets. Six in 10 express concern over shifting consumer behaviour as well.34

Healthcare CEOs expect headcounts to increase over the next year, at 59% vs. 50% of all CEOs. Asked about their company’s prospects for revenue growth over the next 12 months, a greater portion of healthcare CEOs reported being “very confident” (47% vs. 39% of all CEOs), although compared to CEOs in other industries, they are slightly less confident overall.35

Source: http://pwc.to/1vk6LKn

31 http://www.tldgroupinc.com/2014_CEO_Survey.html 32 http://www.fiercehealthcare.com/story/top-healthcare-ceo-compensation-trends-2014/2014-01-29 33 http://www.bizjournals.com/houston/blog/2015/01/the-next-big-hire-for-health-systems-a-marketing.html 34 http://www.pwc.com/gx/en/ceo-survey/2015/industry/healthcare.jhtml 35 http://www.pwc.com/gx/en/ceo-survey/2015/explore-the-data.jhtml

12

Executive MonitorHealthcare and Life Sciences

Source: http://pwc.to/1vk6LKn

“The healthcare service provider segment continues to grow in Brazil. A larger portion of the population now has access to private services, which increases the need for additional services throughout the business chain. To meet the new demand, hospitals are continuously hiring executives from several industries in an effort to upgrade their management teams and recover margins. In the OTC market, there’s increased demand for well-trained executives, mostly coming from top consumer brands to meet the more dynamic and competitive environment.” Alexandre Sabbag, Partner, Boyden Brazil

Case Studies The following firms epitomize the changes taking place in the evolving healthcare industry.

Sanofi

Sanofi ranks fifth in the world among pharmaceutical companies in revenue.36 In March 2014, it named Dr Anne C. Beal as its first Chief Patient Officer, making Sanofi the first top-10 pharmaceutical company to hire for this position. Prior to joining Sanofi, Dr Beal was Chief Officer for Engagement at the Patient Centered Outcomes Research Institute (PCORI), the United States’ largest research institute focused on patient-centred outcomes research.37 Her appointment indicates a strategic shift with an eye toward value-based healthcare:

“I will use my experience as a physician, researcher, philanthropic leader, and advocate for patient access to high quality care to infuse the patient perspective into Sanofi’s work that will advance our ability to deliver healthcare solutions that matter most to patients and those who care for them.”

Dr Anne C. Beal, Chief Patient Officer, Sanofi

36 http://www.pmlive.com/top_pharma_list/pharma_companies/sanofi 37 http://en.sanofi.com/Images/35990_20140331_cpo_en.pdf

13

Executive MonitorHealthcare and Life Sciences

Johnson & Johnson

In March of last year, Johnson & Johnson hired Ernesto Quinteros to fill the newly created role of Chief Design Officer. The position – the equivalent of a Chief Marketing Officer – was created to generate products that look and work better across the company’s consumer, medical device, and pharmaceutical segments. He previously worked in the technology sector at Belkin International on products such as iPhone and iPad cases. According to the Wall Street Journal, design is a top priority for J&J as it could help the sales of some of the company’s healthcare products by making sure patients take their drugs appropriately and as needed, updating hospital equipment monitors to display information so doctors and nurses can read it more easily, and improving product websites to make them more appealing.38

“I think design thinking has the potential to redefine consumer experiences and fuel innovation inside an organization.”

Ernesto Quinteros, Chief Design Officer, Johnson & Johnson

REGIONAL TRENDS United States Currently, the United States has the largest regional share of the global pharmaceuticals market, at 34%. EMAP (Emerging Markets and Asia Pacific) ranks second with a 31% market share, but is expected to surpass the United States by 2018.39 And, in 2014, U.S. medicine approvals reached the highest level in nearly two decades.40

The biopharmaceutical industry is one of the leading job generators for the United States. It employs over 810,000 people and supports another 3.4 million jobs nationwide. Notably, it invests the most capital for R&D per employee than any other industry, which is thought to drive its huge economic impact. Since 2000, PhRMA (Pharmaceutical Research and Manufacturers of America) members have invested over half a trillion in R&D, with $51.1 billion in 2013 alone. Citing measurements from the Battelle Technology Partnership Practice, PhRMA states that “the overall economic impact of the biopharmaceutical sector on the U.S. economy totals about $790 billion on an annual basis when direct, indirect, and induced effects are considered.”41

The pharmaceutical industry in the United States is extensive, and comprised of four subsectors. First, the innovative pharmaceutical industry is responsible for producing “chemically derived drugs developed as a result of extensive R&D and clinical trials in both humans and animals.” This is the pharma industry in its most traditional sense, and it relies heavily on intellectual property and patent protection. Only a few major global companies produce the majority of products, but they have begun to rely on external groups (partners, smaller manufacturers, etc.) for research.

“In the US, all the life sciences sectors are experiencing a broad upswing after a tough first three years following the recession. This growth, coupled with the renewed strength of the M&A and IPO markets, is resulting in aggressive investing and executive hiring in both larger companies and venture-backed concerns. We expect 2015 to deliver an even stronger growth curve than what we experienced over the last couple of years.” Trevor Pritchard, Partner, Boyden San Francisco

38 http://www.wsj.com/articles/SB10001424052702304256404579449290361956838 39 FTI Consulting, Healthcare Summit 201440http://www.theguardian.com/business/2015/jan/01/us-approvals-new-medicines-rapid-rise 41http://www.phrma.org/economic-impact

14

Executive MonitorHealthcare and Life Sciences

Next, the biopharmaceutical industry “produces medical drugs derived from life forms (biologics)”, including proteins and nucleic acids. This subsector also relies on research from small companies and/or academic institutions. Then there are biologics (including biosimilars), which encompass a wide range of different products including “vaccines, therapeutic proteins, blood and blood components, tissues, etc.” Big pharma companies tend to diversify their portfolio with biologics by acquiring smaller biotech companies, “in-licensing of products, and R&D alliances.”

Finally, the generic pharmaceutical industry makes copies of “innovative pharmaceuticals that contain the same active ingredient, are identical in strength, dosage form, and route of administration.” Pricing is usually lower than the original drug, and manufacturing relies on efficiency of production methods and distribution.42

PwC predicts 10 issues the United States should watch for in 2015:

(1) Do-it-yourself healthcare More than half of clinicians are comfortable with mobile apps/devices monitoring vital

signs.(2) Making the leap from mobile app to medical device A majority (86%) of clinicians feel that mobile apps will become increasingly important

to physicians for patient health management over the next few years.(3) Balancing privacy and convenience Nearly a quarter of U.S. customers said data security trumps convenience when dealing

with doctor’s notes and diagnoses.(4) High-cost patients sparking cost-saving innovations Only 1% of all patients consume 20% of the U.S.’s healthcare spending.

Source: http://onphr.ma/1DFhVjX

42 http://selectusa.commerce.gov/industry-snapshots/pharmaceutical-and-biotech-industries-united-states

15

Executive MonitorHealthcare and Life Sciences

(5) Putting a price on positive outcomes Demand for new evidence is increasing, and definitions of positive health outcomes

are expected.(6) Transparency: Open everything to everyone(7) Getting to know the 10 million newly insured (8) Physician extenders seeing an expanded role in patient care Nurses, nurse practitioners, physician assistants and pharmacists will do more, often

becoming the first line of care for patients.(9) Redefining health and well-being for the millennial generation Employers and insurers must look for fresh ways to engage, retain and attract the millennials, the next generation of healthcare consumers.(10) Partnering to win Joint ventures, open collaboration platforms, and non-traditional partnerships will push healthcare companies out of the traditional model and toward new competitive strategies.43 The Affordable Care Act (ACA) has and will continue to drastically change the industry. Ten million Americans have already signed up for health insurance, and Congress will likely make more decisions regarding changes, implementation and funding.44 A more sizable workforce will be required to meet the new need, and predictions claim that the nation is unprepared to fill this demand.45 Employers face an obstacle as well – under an ACA mandate which went into effect on January 1 of this year, firms with more than 100 employees are required to offer health insurance to their employees.46 More Americans will have to deal with the ACA on an individual level, therefore legislatures and government leaders “will be increasingly pressured to simplify its implementation.”47

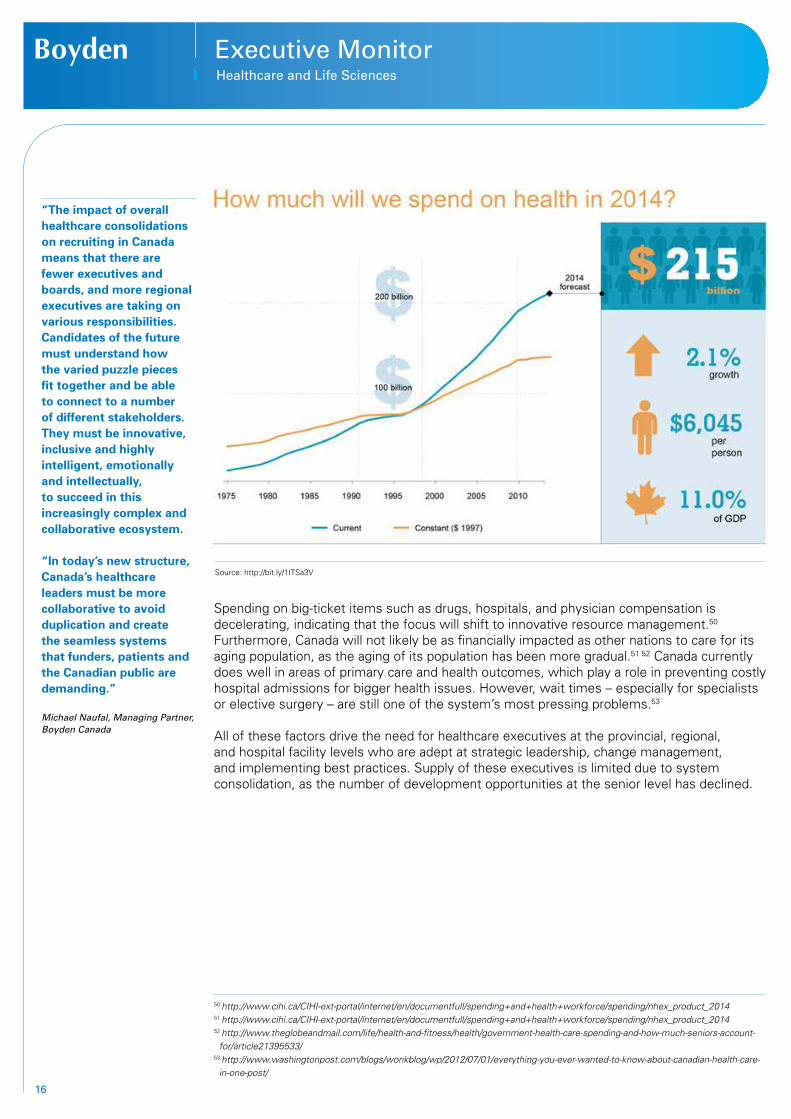

Many U.S.-based companies are now attempting to relocate their headquarters abroad, in order to avoid the strict tax burden at home. This process, called inversion, is discouraged by the U.S. government. In fact, regulations from the Treasury Department will block certain techniques being used to lower corporate tax bills, and make it harder to move overseas by “tightening the ownership requirements (companies) must meet.”48 Critics in the industry insist that a change in U.S. tax structure must take place, as the nation is at risk of losing huge, revenue-generating and job-generating corporations. Canada With its single-payer healthcare system, Canada sees a continuing demand for executives who are successful at leading large, complex healthcare systems. Additionally, healthcare executives must find ways to manage costs and create alternative sources of revenue, since healthcare spending in the country has slowed. Projections for 2013-2014 put it at its slowest growth rate since 1997 at 2.1%. For the period of 2014-2018, spending is forecast to rise slightly, by an average of 4.5% a year.49 The long-term sustainability of publicly funded healthcare is the number one challenge facing governments today; this has resulted in a variety of initiatives, including system consolidation, enhanced use of technology in clinical practice and administration, and discussions regarding scope of practice for healthcare professionals in order to bring about new ways of delivering healthcare services.

“Increasing consolidation of governance and administrative structures for healthcare providers has also decreased the number of ‘training grounds’ for senior level executives in this sector, making it more difficult to recruit and hire individuals who have had experience with a full range of responsibilities at the senior level.” Ken Werker, Managing Partner and Chair, Boyden Canada

44http://www.navigant.com/insights/library/industry-news/2015-healthcare-trends/ 45http://www.heritage.org/research/reports/2014/03/the-impact-of-the-affordable-care-act-on-the-health-care-workforce46http://kff.org/health-reform/poll-finding/kaiser-health-policy-tracking-poll-december-2014/47http://national.deseretnews.com/article/3170/what-to-expect-from-the-affordable-care-act-in-2015.html48http://www.modernhealthcare.com/article/20140923/INFO/309239927 49http://www.cihi.ca/CIHI-ext-portal/internet/en/documentfull/spending+and+health+workforce/spending/nhex_product_2014

16

Executive MonitorHealthcare and Life Sciences

Source: http://bit.ly/1ITSa3V

Spending on big-ticket items such as drugs, hospitals, and physician compensation is decelerating, indicating that the focus will shift to innovative resource management.50 Furthermore, Canada will not likely be as financially impacted as other nations to care for its aging population, as the aging of its population has been more gradual.51 52 Canada currently does well in areas of primary care and health outcomes, which play a role in preventing costly hospital admissions for bigger health issues. However, wait times – especially for specialists or elective surgery – are still one of the system’s most pressing problems.53

All of these factors drive the need for healthcare executives at the provincial, regional, and hospital facility levels who are adept at strategic leadership, change management, and implementing best practices. Supply of these executives is limited due to system consolidation, as the number of development opportunities at the senior level has declined.

“The impact of overall healthcare consolidations on recruiting in Canada means that there are fewer executives and boards, and more regional executives are taking on various responsibilities. Candidates of the future must understand how the varied puzzle pieces fit together and be able to connect to a number of different stakeholders. They must be innovative, inclusive and highly intelligent, emotionally and intellectually, to succeed in this increasingly complex and collaborative ecosystem. “In today’s new structure, Canada’s healthcare leaders must be more collaborative to avoid duplication and create the seamless systems that funders, patients and the Canadian public are demanding.” Michael Naufal, Managing Partner, Boyden Canada

50 http://www.cihi.ca/CIHI-ext-portal/internet/en/documentfull/spending+and+health+workforce/spending/nhex_product_201451 http://www.cihi.ca/CIHI-ext-portal/internet/en/documentfull/spending+and+health+workforce/spending/nhex_product_2014 52 http://www.theglobeandmail.com/life/health-and-fitness/health/government-health-care-spending-and-how-much-seniors-account- for/article21395533/53 http://www.washingtonpost.com/blogs/wonkblog/wp/2012/07/01/everything-you-ever-wanted-to-know-about-canadian-health-care- in-one-post/

17

Executive MonitorHealthcare and Life Sciences

Europe The European healthcare and life sciences sector faces challenging prospects for the near term. At best, experts agree that the future of the sector is undefined. Although the economic environment has stabilized since the 2008 financial meltdown, countries in the region are under extreme pressure to cut costs.54 Even with greater demand for healthcare services due to the aging population and rise in chronic diseases, annual growth in healthcare spending is expected to slow down because of the necessary cost-cutting measures. Currently, Europe has the largest proportion of older individuals (aged 60 or older) in the world and, according to Deloitte, will hold that distinction for the next 50 years.55 Spending, however, is expected to remain flat in the -1 to 2% range through 2016 in the European Union Five (EU5): France, Germany, Italy, Spain, and the United Kingdom.56 Thus far, efforts have been made to cut costs through the greater adoption of generics. While this has made a lot of medicines cheaper and more accessible for the population, the adoption of generics along with more restrictive policies has resulted in the region’s limited access to more innovative medicines.57 While the state of the healthcare sector is uncertain throughout Europe, southern Europe is expected to suffer the most over the next few years. For example, health spending in Portugal is not expected to recover until 2017, and in Greece and Spain, until 2016. In Western Europe, the United Kingdom is also suffering due to constraints on medical spending, which will lead to tighter reimbursement policies, and as a result, higher out-of-pocket costs for patients.

“Efficiency has become even more important with the sharp rise of the Swiss franc. Thus, life science and healthcare companies headquartered in Switzerland are focused on attracting executives from the traditionally lower margin industries such as consumer, high tech and telecoms for finance, marketing, HR and other management roles. “In terms of recruitment from outside healthcare, Boyden partners’ more generalised instead of highly specialised experience has become a benefit for clients. We’re able to think ‘out of the box’ and not focus on the same 10 candidates who are currently in similar roles with other industry competitors.” Sabine Brunthaler, Partner, Boyden Switzerland

• Patent expiries and the impact of low-cost generics will affect spendinggrowth throughout the forecast period,peaking in 2012 and 2013.

• Less impact from expiries will contributeto approximately half of the highermarket growth in 2014, relative to 2013.

• Impact of health insurance reforms willpositively impact growth in 2014; themajority of the impact will be seen in theretail and primary care sectors.

• Patent protected brand volume growth is expected to slow in advance of keypatent expiries.

• Branded price increases above inflation willcontinue, though they are expected to beoffset by off-invoice discounts and rebates,which are not included in the forecasts.

• New brands contribution to spendingwill increase slightly to $10-12Bn peryear as the number of approvals increases.

Source: IMS Market Prognosis, May 2012

Chart notesChart shading indicates forecast, and forecasted growthshows point forecast and high-low ranges.Spendng includes retail pharmacy, mail order, long-termcare and institutional drug spending tracked by IMS audits.

25The Global Use of Medicines: Outlook Through 2016Report by the IMS Institute for Healthcare Informatics

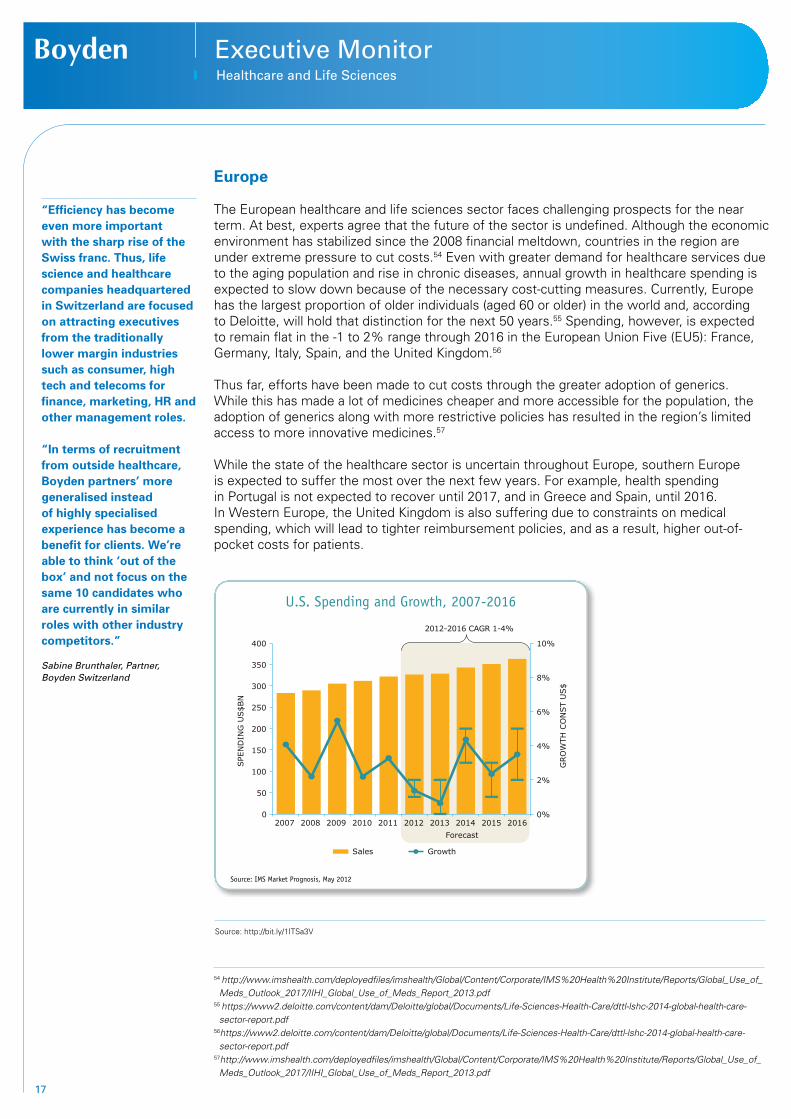

GLOBAL SPENDING GROWTH

U.S. spending growth on medicines will be 1-4% through 2016

U.S. Spending and Growth, 2007-2016

0%

2%

4%

6%

8%

10%

0

50

100

150

200

250

300

350

400

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

GRO

WTH

CO

NST

US$

SPE

ND

ING

US$B

N

Sales Growth

U.S. spending growth recovers after patent cliff in 2012/13

Forecast

2012-2016 CAGR 1-4%

Source: http://bit.ly/1ITSa3V

54 http://www.imshealth.com/deployedfiles/imshealth/Global/Content/Corporate/IMS%20Health%20Institute/Reports/Global_Use_of_ Meds_Outlook_2017/IIHI_Global_Use_of_Meds_Report_2013.pdf 55 https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Life-Sciences-Health-Care/dttl-lshc-2014-global-health-care- sector-report.pdf56https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Life-Sciences-Health-Care/dttl-lshc-2014-global-health-care- sector-report.pdf57http://www.imshealth.com/deployedfiles/imshealth/Global/Content/Corporate/IMS%20Health%20Institute/Reports/Global_Use_of_ Meds_Outlook_2017/IIHI_Global_Use_of_Meds_Report_2013.pdf

18

Executive MonitorHealthcare and Life Sciences

Germany is one of the few exceptions in the entire European region, as the number of doctors remains stable and the nurse to population ratio is high, with healthcare spending expected to rise an average of 2.8% per year.58

India The Indian healthcare industry has seen tremendous growth and become one of the country’s largest sectors. This growth can be attributed to “strengthening coverage, services, and increasing expenditure” from both public and private actors. India’s market value is expected to reach US $280 billion in the next five years. According to PwC, the fastest growing segment of India’s healthcare industry is the diagnostic market. Due to the new availability and affordability of healthcare in this country, services like diagnostics, pharmacies, and equipment are now also in demand. Notably, India has become a base for many clinical trials due to the low cost of procedures. Despite its tremendous growth, there are still some obstacles the country must overcome. For example, “optimal utilization of resources, minimizing operational costs, maximizing performance and efficiency, scaling of business, rapidly evolving technology and globalization of healthcare delivery quality and standards” are all focus areas for India in the near term.59 60

“Clinical services are now a global opportunity for India with a strong competitive edge based on speed and quality of clinical development”. 61

Dr Wolfgang Beier, CEO, Oncology Services Europe Furthermore, India has been scrutinized for its lack of patent protection. According to a report by the U.S. International Trade Commission, “28% of drug makers feel that India doesn’t do enough to protect intellectual property.” The U.S. is pressing India to make a change, and Prime Minister Narendra Modi has agreed to form a working group on intellectual property. On the other side, consumer advocates argue that this change in policy could restrict access to medicine for the Indian people and for other countries that import generic drugs from India.62

“With Indian pharma companies investing heavily in joint collaborative research for new drug discoveries, senior-level professionals with niche skills in the areas of drug discovery, regulatory affairs, quality systems/compliance, clinical research and development and R&D program management are being sought after and well compensated. “There are very strong macro drivers that will ensure growth of the sector in India, despite recent challenges such as stringent government price control mechanisms, compulsory licensing, ambiguous patent laws and regulatory compliance mandates. The sheer size of the population, increasing prevalence of chronic lifestyle diseases, rising disposable incomes along with better penetration of healthcare and access to medical insurance are some of the factors driving pharma growth.” Sushil Gulati, Head of Life Sciences Practice and Partner, Boyden India

Source: http://bit.ly/1hvnlOU

58 http://www.imshealth.com/deployedfiles/ims/Global/Content/Insights/IMS%20Institute%20for%20Healthcare%20Informatics/ Global%20Use%20of%20Meds%202011/Medicines_Outlook_Through_2016_Report.pdf 59 http://www.ibef.org/industry/healthcare-india.aspx 60 http://www.kpmg.com/in/en/industry/pages/healthcare.aspx 61 http://www.ibef.org/industry/healthcare-india.aspx 62 http://blogs.wsj.com/pharmalot/2014/12/29/drug-prices-generics-and-ma-what-to-watch-in-2015/

19

Executive MonitorHealthcare and Life Sciences

China China, the world’s most populated country, has an equally massive healthcare industry. In fact, according to McKinsey & Company, healthcare spending in China will reach $1 trillion in the next five years, from $350 billion in late 2014. The Chinese government itself predicts it will reach $1.3 trillion in the same time. While massive, these figures equate to only around $1,000 per person, considerably less than the United States, which spends approximately $9,000 per person.63

There are two major reasons for this incredible growth trajectory. For one, per capita incomes are rising due to urbanization, leading to conspicuous consumption, among other phenomena. And, consumers are demanding more from the medical field. With a greater consumer culture, more people are affected by cancer, heart disease, diabetes and other chronic illnesses, due to poor diets and pollution.64 China’s growing elderly population is also a concern; however it is driving demand for products and services.65

China is home to 22,000 hospitals, a significant number of which will require major renovations and upgrades in the next few years. Foreign-owned hospitals are being called upon by the Chinese government to help “fill some of the void.” Moreover, the government plans to double the contribution of private hospital services and increase foreign investment in the hospital system.66 China is one of the world’s most attractive markets for foreign investors, but according to McKinsey, companies should still be cautious. Executives and decision-makers should ask the right questions, and decide if they are able to compete in this quickly changing marketplace.67

2014 Global health care outlook Shared challenges, shared opportunities 19

Like many health care systems around the world, funding, provider reimbursement, regulatory uncertainty, and rapid technological change are among the issues facing Australia in 2014. The country also is challenged by workforce shortages; the ratio of doctors to patients was an estimated 2.8 per 1,000 in 2012, fairly low for an industrialized nation.117

To address these challenges, health care providers and payers in Australia should consider changing their care and business models to focus on innovation, efficiency, and safety; regulatory compliance and strategic risk management; personnel recruitment, retention, and development; and technology investments.

China

Market Fact: China’s rapidly rising income level and dramatic increase in Internet and mobile phone usage are increasing patients’ ability to pay for treatment and driving new expectations for quality of care.

Health care spending in China is expected to near $890 billion a year by 2017, growing by an average rate of 13.8

percent annually in local currency terms from 2013-2017. Total spending is forecast to reach the equivalent of 5.9 percent of GDP by 2017, up from an estimated 5.3 percent in 2012.118 The central government spent an additional $125 billion in health care expenses above and beyond its planned expenditures over the past three years.119 To address the huge divides in the quality of health care provision, the percentage of spending in rural areas (e.g., clinics, insurance, equipment and drugs) will rise faster than that in urban areas. However, total urban health care spending will remain far higher than rural expenditure in 2013-2017.120

Looking at demographic trends, China’s population is aging (Figure 5), bringing attendant health conditions and creating demand for health care services and life sciences products. In addition, China is becoming increasingly urbanized — the proportion of urban population has grown from 36 percent in 2010 to 52.6 percent in 2012.121 Urbanization and continued westernization of the population have driven lifestyle changes centered on an increasingly western diet, high prevalence of smoking, and increased pollution, which have materially changed the profile of disease in China.

117 Ibid118 Healthcare Briefing and Forecasts: China: Healthcare and Pharmaceuticals Report, Economist Intelligence Unit, June 7, 2013119 Global life sciences outlook: Resilience and reinvention in a changing marketplace, Deloitte Touche Tohmatsu Limited, 2013 120 Healthcare Briefing and Forecasts: China: Healthcare and Pharmaceuticals Report, Economist Intelligence Unit, June 7, 2013121 Global life sciences outlook: Resilience and reinvention in a changing marketplace, Deloitte Touche Tohmatsu Limited, 2013

Figure 5: China’s aging population vs. global comparison group

2008 2009 2010 2011 2012 2013 2014 2015 2020 China US Japan UK Malaysia S. Korea Germany

107 111 113 118 121 126 129136

171

8.28

120.9

42.4

30.1

10.71.5 6.0

16.9

Aging population in China(2008–2020F)

Comparison of population 65+ Number in Million (2012)

% of population aged 65 and over Population aged 65 and over

Source: Economist Intelligence Unit Monitor Deloitte Analysis

Population aged 65 and over

8.50 8.608.90 9.10 9.40 9.60

12.40

10.10

China’s elderly population exceedsthe combined elderly population in this comparison group.

Source: http://deloi.tt/1kBEayQ

“In Southeast Asia, we expect growth in executive hiring with the increase in developing medical suites in hubs such as Singapore, Bangkok and Phuket. This will also result in the development of new insurance products as well as changes in the medical provisions to account for a surging affluent population.” Roger Wilson, Managing Partner, Boyden Singapore

“Healthcare companies are increasingly focused on executives who have the ability to differentiate products to attract new customers. Organizations are also seeking leaders who are able to navigate government and compliance issues at the highest level of global standards. In addition, in Latin America, clients are increasingly concentrating on C-level executives and country manager level executives who can combine brand name experience with an ability to run generic pharma enterprises.” Antonio Sanchez, Boyden Board Member and Managing Partner, Boyden Colombia

63 http://www.forbes.com/sites/jackperkowski/2014/11/12/health-care-a-trillion-dollar-industry-in-the-making/ 64 http://www.forbes.com/sites/jackperkowski/2014/11/12/health-care-a-trillion-dollar-industry-in-the-making/ 65 https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Life-Sciences-Health-Care/dttl-lshc-2014-global-health-care- sector-report.pdf 66 http://www.forbes.com/sites/jackperkowski/2014/11/12/health-care-a-trillion-dollar-industry-in-the-making/ 67 http://www.mckinsey.com/insights/health_systems_and_services/health_care_in_china_entering_uncharted_waters

20

Executive MonitorHealthcare and Life Sciences

Brazil and Latin America By 2020, the population of Latin America will reach 665 million, with the urban populace accounting for 80% of the total.68 Latin American healthcare spending is expected to rise by an average of 6.8% per year from 2013-2017.69 The healthcare sector in the region must continue to adapt to rising demand resulting from an aging population, high rates of chronic diseases, increased urbanization, and government inefficiencies. These factors pose risks to providing high-quality, affordable healthcare, especially to underserved populations.

According to Americas Market Intelligence, the population of seniors (aged 60 or above) is expected to increase to 83 million by 2020. This is nearly double the senior population in Latin America in the year 2000.70 A larger population, along with high rates of chronic diseases such as diabetes, cancer, and cardiovascular diseases, means that the private and public healthcare sectors must adapt to the consequential increased demand for healthcare services.

Some changes have already taken place to improve access to care in Latin America. In countries such as Brazil and Mexico, for example, the introduction of universal and low-cost insurance has already proved to considerably improve the health of these countries. Since universal healthcare was introduced in Brazil in 1988, infant mortality rates, AIDS and tuberculosis are no longer major threats, and healthcare has become available to a greater extent in remote areas of the country. In Mexico, low-cost health insurance and preventive medicine has led to greater life expectancies. However, these countries, and the rest of Latin America, continue to face challenges to ensuring that care that is both cost-effective and high-quality is accessible to large populations.71 For government-subsidized healthcare to be more effective, long wait times and high out-of-pocket costs must be decreased. Additionally, the process of obtaining government-subsidized medicine in some countries like Brazil must be made shorter and easier to navigate; often patients who need medication immediately must pay the entire out-of-pocket cost to obtain it from a private distributor.

“Overall, healthcare organizations are pursuing executives with a holistic view of business for roles to lead specialty drugs franchises or to serve as general managers of medical device companies. The Brazilian pharmaceutical market has faced a loss of patents, forcing large organizations to downsize their structures. “At the same time, these businesses are developing better strategies to sell to government entities, and companies are focusing on developing specialty drugs. Thus, there’s an increased demand for managers with strong track records in business development with the federal government and marketing and sales professionals who are able to migrate to the OTC market, which is growing at a higher rate.” Áurea Imai, Managing Partner, Boyden Brazil

Source: http://bit.ly/1ITSa3V

68 http://www.pharmaphorum.com/articles/health-technology-trends-in-latin-america-and-brazil69 https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Life-Sciences-Health-Care/dttl-lshc-2014-global-health-care- sector-report.pdf 70 http://www.americasmi.com/en_US/expertise/articles-trends/page/the-latin-american-consumer-of-2020 71 http://www.mckinsey.com.br/LatAm4/Data/Perspectives_on_Healthcare_in_Latin_America.pdf

21

Executive MonitorHealthcare and Life Sciences

Consistent with other parts of the world such as Africa and Asia, Latin America has also had to face challenges arising from rapid urbanization over the last decade. This has led to the creation of more shantytowns and slums lacking proper access to health services, fresh water, and sanitation services.72

To compound matters, in hard-to-reach rural areas, capable physicians are hard to come by. Primary care physicians in these areas often lack the opportunity to continue their education or are simply not motivated to develop their skills due to a lack of performance-based incentive systems. They may also be young and inexperienced doctors who graduated recently and are waiting to find jobs in urban areas. Given that about 120 million people in Latin America reside in rural areas, the aforementioned culminate in serious problems for underserved communities.73

Fortunately telemedicine, the practice of using telecommunications technology to deliver care, could be part of the solution.74 It would enable general practitioners in rural areas to connect with a central hub of experienced medical experts and send patient data, which would then be analysed remotely. Highly qualified physicians at the hub could diagnose the patient, request further examinations, and provide other advice from hundreds of miles away. Brazil, the chief medical market in Latin America, is not only a domestic player, but also a global force. It ranks first in Latin America and is the third-largest pharmaceutical market in the world, behind the United States and Canada.75 Spending is projected to rise to $255.5 billion by 2017. The local generics industry is a booming business as a result of government initiatives to provide low-cost medicines to consumers, and has rapidly captured significant market share since its inception in the early 2000s. Furthermore, the private health insurance industry is rife with opportunities. A quarter of Brazilians can currently afford private health insurance, and this number is expected to increase as more Brazilians become part of the middle class.

Middle East and North Africa Similar to other developing regions, the Middle East and North Africa (MENA) faces new chronic diseases, an aging population, and seismic socioeconomic change. These factors have increased the need for quality and access to healthcare to improve. The Association of Academic Health Centers International identified the following key growth and economic challenges for the region:

• “Educating a skilled and flexible workforce able to adapt to the rapidly changing healthcare environment;

• Building capacity and capability through recruitment, retention, education, and partnership; • Locally relevant research supported by international partnerships; • Driving improved clinical performance through a focus on quality and safety.”76

“Despite some progress, the pharmaceutical industry in the MENA region is still in the emerging phase, with a vast majority of its products being branded and imported. However, we’re seeing an upturn in demand for management as governments are enacting measures to boost local drug manufacturing. Additionally, companies are developing partnerships with Indian and other foreign companies to grow the generic segment.” Athena Tavoulari, Partner, Boyden Middle East

72 http://www.kpmg.com/global/en/issuesandinsights/articlespublications/care-in-a-changing-world/pages/trends-risks-opportunities. aspx 73 http://www.mckinsey.com.br/LatAm4/Data/Perspectives_on_Healthcare_in_Latin_America.pdf 74 http://www.mckinsey.com.br/LatAm4/Data/Perspectives_on_Healthcare_in_Latin_America.pdf75 http://www.gabionline.net/Reports/The-Brazilian-generics-market 76 http://www.thelancet.com/pdfs/journals/lancet/PIIS0140-6736(14)60025-8.pdf

22

Executive MonitorHealthcare and Life Sciences

Despite such challenges, the MENA region has made significant improvements in healthcare in the past few decades. Infant mortality rates and maternal deaths have dropped significantly. Women are actually the largest users of health services, and policymakers should think about addressing “the cultural constraints to women’s reproductive health access.”77 Healthcare IT is also on the rise. As Gartner had predicted, the region saw a huge increase in spending on internal services, software, IT services, data centres, devices, and telecom services in 2014.78 While improvements have been made, MENA still must significantly accelerate development to be on par with its neighbours to the north and west. Executives should be aware of this and work towards establishing a strong foundation and focus on providing the healthcare necessities to a population in need.

77 http://www.prb.org/Publications/Articles/2006/GenderandEquityinAccesstoHealthCareServicesintheMiddleEastandNorthAfrica.aspx 78 http://www.gartner.com/newsroom/id/2935017

23

Executive MonitorHealthcare and Life Sciences

Sources Americas Market Intelligence. (2012). The Latin American Consumer of 2020. Retrieved from http://www.americasmi.com/en_US/expertise/articles-trends/page/the-latin-american-consumer-of-2020.

Anderson, A. (2014). The Impact of the Affordable Care Act on the Health Care Work-force. The Heritage Foundation. Retrieved from http://www.heritage.org/research/re-ports/2014/03/the-impact-of-the-affordable-care-act-on-the-health-care-workforce.

Becker’s Hospital Review. (2014, December 5). The top 14 healthcare stories of 2014. Re-trieved from http://www.beckershospitalreview.com/hospital-management-administration/the-top-14-healthcare-stories-of-2014.html.

Burg, N. (2014, November 10). How Big Data Will Help Save Healthcare. Forbes Magazine. Retrieved January 22, 2015 from http://www.forbes.com/sites/castlight/2014/11/10/how-big-data-will-help-save-healthcare/.

Canadian Institute for Health Information. (2014). National Health Expenditure Trends, 1975 to 2014. Retrieved from http://www.cihi.ca/web/resource/en/nhex_2014_report_en.pdf.

Caramenico, A. (2013, June 4). Bridging the generation gap in healthcare leadership. Fierce Healthcare. Retrieved from http://www.fiercehealthcare.com/story/bridging-generation-gap-healthcare-leadership/2013-06-04.

Dallas, K. (2014). What to expect from the Affordable Care Act in 2015. Deseret News National. Retrieved from http://national.deseretnews.com/article/3170/what-to-expect-from-the-affordable-care-act-in-2015.html.

Deloitte. (2013). 2014 Health Care Providers Outlook: Interview with Mitch Morris, M.D. Retrieved from http://www2.deloitte.com/us/en/pages/life-sciences-and-health-care/articles/2014-health-care-providers-outlook.html.

Deloitte. (2014). 2014 Global Health Care Outlook: Shared challenges, shared opportunities. Retrieved from https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Life-Sciences-Health-Care/dttl-lshc-2014-global-health-care-sector-report.pdf.

Deloitte. (2014). 2015 Global Life Sciences Outlook: Adapting in an era of transformation. Retrieved from http://www2.deloitte.com/content/dam/Deloitte/global/Documents/Life-Sciences-Health-Care/gx-lshc-2015-life-sciences-report.pdf.

DiJulio, B., Firth, J. and Brodie, M. (2014). Kaiser Health Policy Tracking Poll: December 2014. Retrieved from http://kff.org/health-reform/poll-finding/kaiser-health-policy-tracking-poll-december-2014/.

Fisher, N. (2014, November 21). 7 Trends Driving Global Health And Life Sciences In 2015. Forbes Magazine. Retrieved January 22, 2015 from http://www.forbes.com/sites/nicolefisher/2014/11/21/7-trends-driving-global-health-and-life-science-in-2015/. FTI Consulting. (2014). FTI Healthcare Summit.

24

Executive MonitorHealthcare and Life Sciences

GaBI Online. Generics and Biosimilars Initiative. (2014). The Brazilian generics market. Retrieved from http://www.gabionline.net/Reports/The-Brazilian-generics-market.

Gartner. (2014, December 4). Gartner Says Healthcare Providers in Middle East and North Africa to Spend US $3 Billion on IT in 2014 [Press release]. Retrieved from http://www.gartner.com/newsroom/id/2935017.

Grant, K. (2014). Government health care spending, and how much seniors account for. The Globe and Mail. Retrieved from http://www.theglobeandmail.com/life/health-and-fitness/health/government-health-care-spending-and-how-much-seniors-account-for/article21395533/.

Groux, C. (2012). New Harvard Medical Center Works to Attract Student Physicians. U.S. News University Directory. Retrieved from http://www.usnewsuniversitydirectory.com/articles/new-harvard-medical-center-works-to-attract-studen_12314.aspx#.VMFqiUfF-Sp.

Hansson, E., Spencer, B., Kent, J., Clawson, J., Meerkatt, H. & Larsson, S. (2014, September 9). The Value-Based Hospital. BCG Perspectives. Retrieved from https://www.bcgperspectives.com/content/articles/health_care_payers_providers_transformation_large_scale_change_value_based_hospital/.

Healthcare Provider Industry Trends and Technology Business Drivers. (n.d.). Retrieved from http://www.maastary.com/healthcare-provider-industry-trends/.

Hillhouse, E. & Wartman, S. (2014, January 11). Improving health care in the Middle East and North Africa. The Lancelet. Retrieved from http://www.thelancet.com/pdfs/journals/lancet/PIIS0140-6736(14)60025-8.pdf.

HIT Consultant. (2014). PwC: Top 10 Healthcare Industry Issues to Watch in 2015. Retrieved from http://hitconsultant.net/2014/12/04/pwc-top-10-healthcare-industry-issues-to-watch-in-2015/.

IMS Institute for Healthcare Informatics. (2012). The Global Use of Medicines: Outlook Through 2016. Retrieved from http://www.imshealth.com/deployedfiles/ims/Global/Content/Insights/IMS%20Institute%20for%20Healthcare%20Informatics/Global%20Use%20of%20Meds%202011/Medicines_Outlook_Through_2016_Report.pdf.

IMS Institute of Healthcare Informatics. (2013). The Global Use of Medicines: Outlook Through 2017. Retrieved from http://www.imshealth.com/deployedfiles/imshealth/Global/Content/Corporate/IMS%20Health%20Institute/Reports/Global_Use_of_Meds_Outlook_2017/IIHI_Global_Use_of_Meds_Report_2013.pdf.

India Brand Equity Foundation. (2014). Healthcare Industry in India. Retrieved from http://www.ibef.org/industry/healthcare-india.aspx.

Kliff, S. (2012). Everything you ever wanted to know about Canadian health care in one post. The Washington Post. Retrieved from http://www.washingtonpost.com/blogs/wonkblog/wp/2012/07/01/everything-you-ever-wanted-to-know-about-canadian-health-care-in-one-post/.

25

Executive MonitorHealthcare and Life Sciences

KPMG. (2012). Trends, risks and opportunities in healthcare. Retrieved from http://www.kpmg.com/global/en/issuesandinsights/articlespublications/care-in-a-changing-world/pages/trends-risks-opportunities.aspx.

KPMG. (2014). Healthcare India. Retrieved from http://www.kpmg.com/in/en/industry/pages/healthcare.aspx

KPMG. (2014, February 7). What’s next for healthcare: The consumerization of healthcare. Retrieved from http://www.kpmg.com/Global/en/IssuesAndInsights/ArticlesPublications/whats-next-for-healthcare/Pages/cynthia-ambres-consumerization-healthcare.aspx.

Martin, J. (2015, January 7). The next big hire for health systems: a marketing officer. Houston Biz Blog. Retrieved from http://www.bizjournals.com/houston/blog/2015/01/the-next-big-hire-for-health-systems-a-marketing.html.

McKinsey & Company. (2011). Perspectives on healthcare in Latin America. Retrieved from http://www.mckinsey.com.br/LatAm4/Data/Perspectives_on_Healthcare_in_Latin_America.pdf.

McKinsey & Company. (2012). Health care in China: Entering ‘uncharted waters’. Retrieved from http://www.mckinsey.com/insights/health_systems_and_services/health_care_in_china_entering_uncharted_waters.

Modern Healthcare. (2014). U.S. cracks down on companies moving overseas. Retrieved from http://www.modernhealthcare.com/article/20140923/INFO/309239927.

National Human Genome Research Institute. (2011). DNA Sequencing. Retrieved from http://www.genome.gov/10001177.

Navigant. (2014). Navigant Center for Healthcare Research and Policy Analysis Identifies Key Areas to Watch in 2015. Retrieved from http://www.navigant.com/insights/library/industry-news/2015-healthcare-trends/.

New White Paper Heralds 2015 Medical Device Trends (2014, November 18). Retrieved from http://www.healthdec.com/blog/white-paper-heralding-2015-medical-device-trends/.

Palmquist, D. (2014, December 15). Five Trends to Watch in 2015. Pharmaceutical Manufacturing. Retrieved January 10, 2015, from http://www.pharmamanufacturing.com/articles/2014/five-trends-to-watch-in-2015/.

Perkowski, J. (2014). Health Care: A Trillion Dollar Industry In The Making. Forbes. Retrieved from http://www.forbes.com/sites/jackperkowski/2014/11/12/health-care-a-trillion-dollar-industry-in-the-making/.

Pharmaceutical Executive. (2014). 2015 Pharm Science Strategic Outlook: An Industry in Flux: 2014-2015 Market Trends. Retrieved from http://images.alfresco.advanstar.com/alfresco_images/pharma/2014/11/25/6b62704d-511b-4b8b-8d26-406a753f1e0a/article-856395.pdf.

PhRMA (2014). The Biopharmaceutical Industry Helps Strengthen the U.S. Economy. Retrieved from http://www.phrma.org/economic-impact.

26

Executive MonitorHealthcare and Life Sciences

PMLiVE. (2014). Top Pharma List: Sanofi. Surrey, United Kingdom. Retrieved from http://www.pmlive.com/top_pharma_list/pharma_companies/sanofi.

Price, E. (2014, December 9). Biotech and Generic Drugs: 2015 Trends and Predictions. Pharmaceutical Processing. Retrieved from http://www.pharmpro.com/blogs/2014/12/biotech-and-generic-drugs-2015-trends-and-predictions.