Embed Size (px)

Citation preview

NATIONAL CONSUMER DISPUTES REDRESSAL COMMISSIONNEW DELHI CONSUMER COMPLAINT NO. 155 OF 2013 M/s. Shital Fibres Ltd. A-17, Focal Point Extension, Jalandhar, Punjab

… Complainant Versus M/s Bharti Axa General Insurance Co. Ltd. Unit # SFS, 2nd floor, Eminent Mall 261, Lajpant Kunj, Guru Nanak Mission Chowk Jalandhar

… Opposite Party BEFORE:

HON’BLE MR. JUSTICE J. M. MALIK, PRESIDING MEMBER HON’BLE DR. S. M. KANTIKAR, MEMBER For the Complainant : Mr. K.L. Nandwani, Advocate PRONOUNCED ON 4 TH July, 2013 O R D E R

JUSTICE J.M. MALIK

1. The key question involved in this case is “Whether this

Commission can travel outside the Insurance Policy and grant relief to the

complainant, without adhering to the parameters laid down in the policy itself?”.

2. The present complaint has been filed by M/s. Shital Fibres Ltd against M/s. Bharti Axa

General Insurance Co.Ltd., wherein a sum of Rs.4,19,04,368/- towarcds loss & damage,

Rs.25,00,000/- towards punitive losses, Rs.20,00,000/- towards compensation for loss of

business and delay in settling the claim, interest @ 2% or at the bank rate prevalent as on

15.04.2012 as per Regulation No.9 of the Insurance Regulatory and Development Authority

(Protection of Policyholders’ Interest) Regulations, 2002, because the amount was not paid

within 30 days from the appointment of Surveyors and costs of the complaint, were claimed.

3. The facts germane to the present case are these. The complainant got constructed a

building at Plot No.C-81, Focal Point, Jalandhar, Punjab, in December, 2007. The building

was insured with different insurance companies, from time to time, but in the year 2011, the

building was got insured from M/s. Bharati Axa General Insurance Co. Ltd, opposite party,

which was issued seven policy schedules but did not issue the complete policies till date. The

policies issued were Special Peril policies which also included the loss of the building due to

subsidence and landslides. Unfortunately, on 15.04.2012, the building collapsed like a pack of

cards when machines were running and work was going on as the factory used to run for 24

hours.

4. The loss was intimated to the opposite party, which appointed M/s.Puri

Crawford Insurance Surveyors and Loss Assessors, which visited the site for the first time, on

17/18/12/2012. The surveyors called for documents in piece-meal, from time to time, w.e.f.

25.06.2012. All the documents and drawings were immediately furnished whenever the same

were required. A Structural Engineer, was appointed by the Surveyor but he did not have

any interaction with the complainant. No joint meeting was held with the

surveyor. On receipt of the survey report, the complainant again contacted M/s.Gossian &

Associates. They supervised the construction of the building and had issued completion

certificate. The Structural Engineers vide their report reiterated that the sudden collapse of the

entire structure suggested that it could not be a design/material defect and had to do more

with the movement of soil. The opposite party did not pay heed and a legal notice was

served on it to make the payment. The complainant approached Guru Nanak Dev Engineering

College Testing and Consulting Cell, Ludhiana, which vide their report, dated

15.03.2013, gave the opinion that structural design was ‘OK’ and there was no defect in

it. Another opinion from an Expert, namely M/s.ARO Tech Structural Consultants, Jalandhar

City, Punjab, was obtained, which was also of the

opinion that the collapse was due to faulty construction of sewer line by

Punjab Sewerage Board, due to which soil underneath had become bad. The complainant also

met Shri Kunwar Sunil Kumar, Chartered Engineer for

his expert report and he opined that if the total vibration of the machine is taken together, it

cannot cause the collapse of the building.

5. The Opposite party repudiated the claim made by the complainant vide its letter

dated 04.02.2013, wherein it was mentioned :

“…….We reiterate that the claim lodged is not admissible

under the captioned policy due to non-operation of any insured peril

as observed and recommended by surveyors. We thus repudiate our

liability under the claim & close the claim file as “No Claim”.

This report is accompanied by the report given by Er. Surjan Sindh Sidhu, BE (Civil) MIE India,

FIV, Structural Engineer, Formerly Executive Engineer, PB.PWD (B & R), Associate Professor

(Civil) RIET, Abohar. This is a detailed report which runs into five pages. The conclusion

drawn by the Expert is reproduced, as follows:-

“4. CONCLUSION

Keeping in view the above facts and figures, it is reported that the

main cause seems to be the failure at and near joints of R.C.C.

Columns and R.C.C. beams due to shear stresses, as the work was

done without following structural design and may have led to the

collapse. Therefore, structural design defect is the main cause of

collapse of building. Addition to it, there is no reliable

information regarding construction procedure adopted, required

quality control system applied, and qualified Civil Engineers

deputed for construction and supervision,

etc. So, non-compliance of building

construction Codal Rules and

Regulations, Byelaws, Technical Specifications, may have contri

buted to produce a weak structure, which could not resist the

applied loads, continuous vibrations due to operating machinery

and other forces causing ultimate failure of the building”.

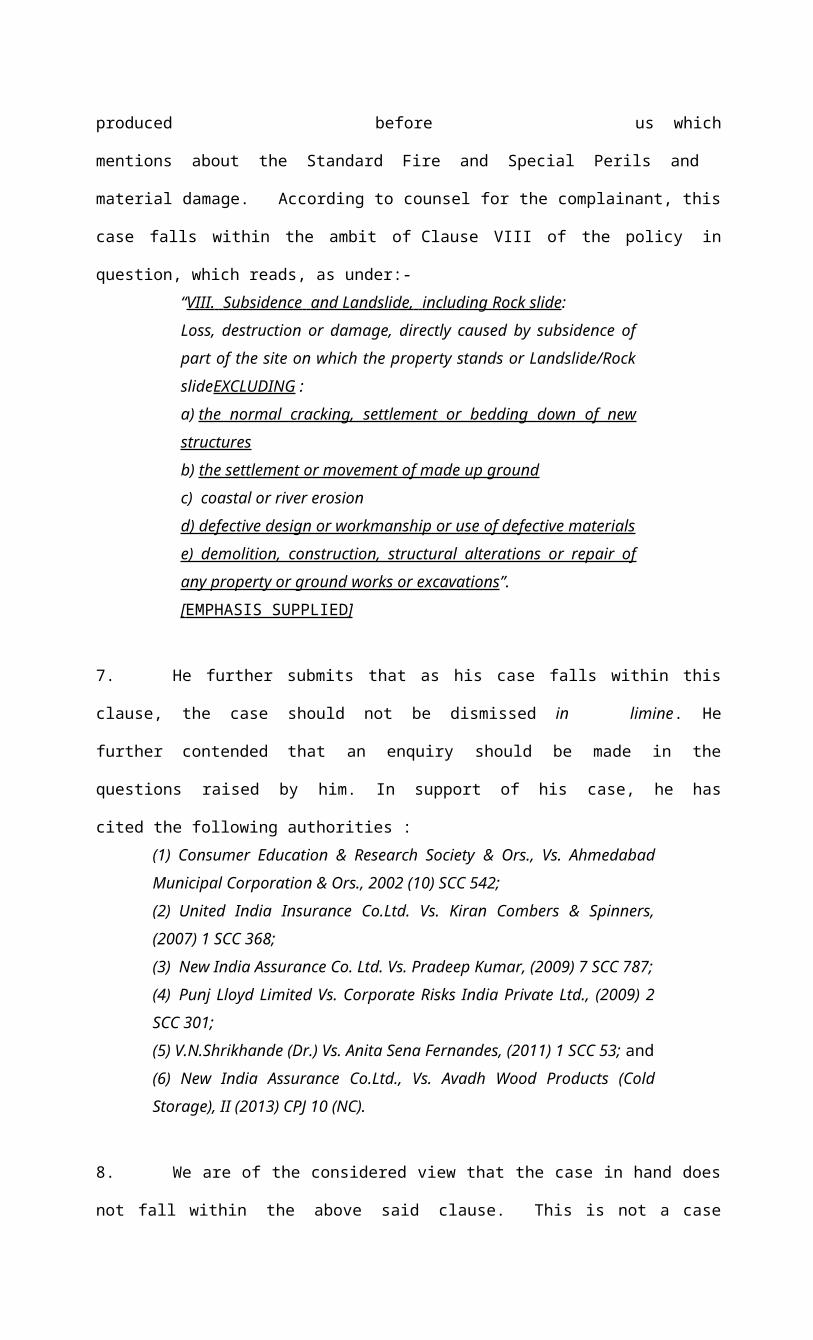

6. We have heard the counsel for the complainant at the time of admission hearing of

this case. The policy in question was produced before us which

mentions about the Standard Fire and Special Perils and material damage. According to

counsel for the complainant, this case falls within the ambit of Clause VIII of the policy in

question, which reads, as under:-

“VIII. Subsidence and Landslide, including Rock slide :

Loss, destruction or damage, directly caused by subsidence of part of

the site on which the property stands or Landslide/Rock

slideEXCLUDING :

a) the normal cracking, settlement or bedding down of new structures

b) the settlement or movement of made up ground

c) coastal or river erosion

d) defective design or workmanship or use of defective materials

e) demolition, construction, structural alterations or repair of any

property or ground works or excavations”.

[ EMPHASIS SUPPLIED ]

7. He further submits that as his case falls within this

clause, the case should not be dismissed in limine. He further contended that an enquiry

should be made in the questions raised by him. In support of his case, he has cited the

following authorities :

(1) Consumer Education & Research Society & Ors., Vs. Ahmedabad

Municipal Corporation & Ors., 2002 (10) SCC 542;

(2) United India Insurance Co.Ltd. Vs. Kiran Combers & Spinners, (2007) 1

SCC 368;

(3) New India Assurance Co. Ltd. Vs. Pradeep Kumar, (2009) 7 SCC 787;

(4) Punj Lloyd Limited Vs. Corporate Risks India Private Ltd., (2009) 2 SCC

301;

(5) V.N.Shrikhande (Dr.) Vs. Anita Sena Fernandes, (2011) 1 SCC 53; and

(6) New India Assurance Co.Ltd., Vs. Avadh Wood Products (Cold Storage),

II (2013) CPJ 10 (NC).

8. We are of the considered view that the case in hand does not fall

within the above said clause. This is not a case of landslide/rock slide. It must be borne in

mind that the policy does not include the normal cracking, settlement or bedding down of new

structures or the settlement or movement of made-up ground. This case clearly falls within the

exceptions (a), (b), (d) and (e), appended with Clause 8, already cited above. There is

hardly any need to make an enquiry. The facts are crystal clear. The report given by the

Expert carries enough value. It is well settled that it will get preponderance over the report

made by the Experts appointed by the private party. There is no allegation

against the Surveyor. He appears to be guileless and there is no reason to discard his

statement/report. The Hon’ble Supreme Court of India has already held that a Surveyor’s

report has significant evidentiary value unless it is proved otherwise, which the complainant has

failed to do so in the instant case. This view was taken in United India Insurance Co. Ltd. Vs.

Roshanlal Oil Mills & Ors., (2000) 10 SCC 19 and also by this Commission in D.N.Badoni

Vs. Oriental Insurance Co.Ltd, 1 (2012) CPJ 272 (NC).

9. Otherwise, too, the reports submitted by the Experts, engaged

by the Complainant have exiguous value. Their reports are vague, evasive and lead us

nowhere. They harp on the same point that structure was quite alright. They have given different

reasons. It is apparent that the complainant is trying to make bricks without straw.

10. The complainant has no bone to pluck with the opposite party. The case is meritless

and, therefore, the same is dismissed at the admission stage. .…..…………………………(J. M. MALIK, J)

PRESIDING MEMBER

.…..…………………………(S. M. KANTIKAR)

MEMBER dd/16

NATIONAL CONSUMER DISPUTES REDRESSAL COMMISSIONNEW DELHI

CONSUMER COMPLAINT NO. 166 OF 2010

M/s K.K.Jewels Impex Z-25, Hauz Khas New Delhi Through its Partner Kailash Chand Jain........ Complainant

Vs.

The Oriental Insurance Company Ltd. Through the Senior Divisional ManagerDivisional Office No.9 1/28, 4th Floor, Asaf Ali Road Near Hamdard Circle, New Delhi-110002

......... Opposite Party

BEFORE:

HON'BLE MR. JUSTICE AJIT BHARIHOKE, PRESIDING MEMBER HON’BLE MR.SURESH CHANDRA, MEMBER

For the Complainant : Mr.S.C.Dhanda and Ms.Sagari Dhanda, Advocates For the Opposite Party : Mr.Kishore Rawat, Advocate

PRONOUNCED ON : 05 th JULY, 2013

ORDER

PER HON’BLE JUSTICE AJIT BHARIHOKE, PRESIDING MEMBER

The complainant – firm is engaged in the business of import and export of jewellery. The

complainant carried jewellery worth US $ 632691.08 to USA for participating in exhibition and

sale of jewellery organized at New York. Before leaving India with the jewellery, the

complainant got the jewellery insured with the OP for Rs.2,96,09,942.67/- vide cover note

number 945271. The insurance cover was for ‘all risks’. The complainant had carried said

jewellery in packed steel containers to USA and the jewellery was declared to the custom

authorities at New Delhi. The complainant participated in the exhibition at New York on 16 th &

17th June 2001. He sold some items of jewellery on both days. On the conclusion of exhibition,

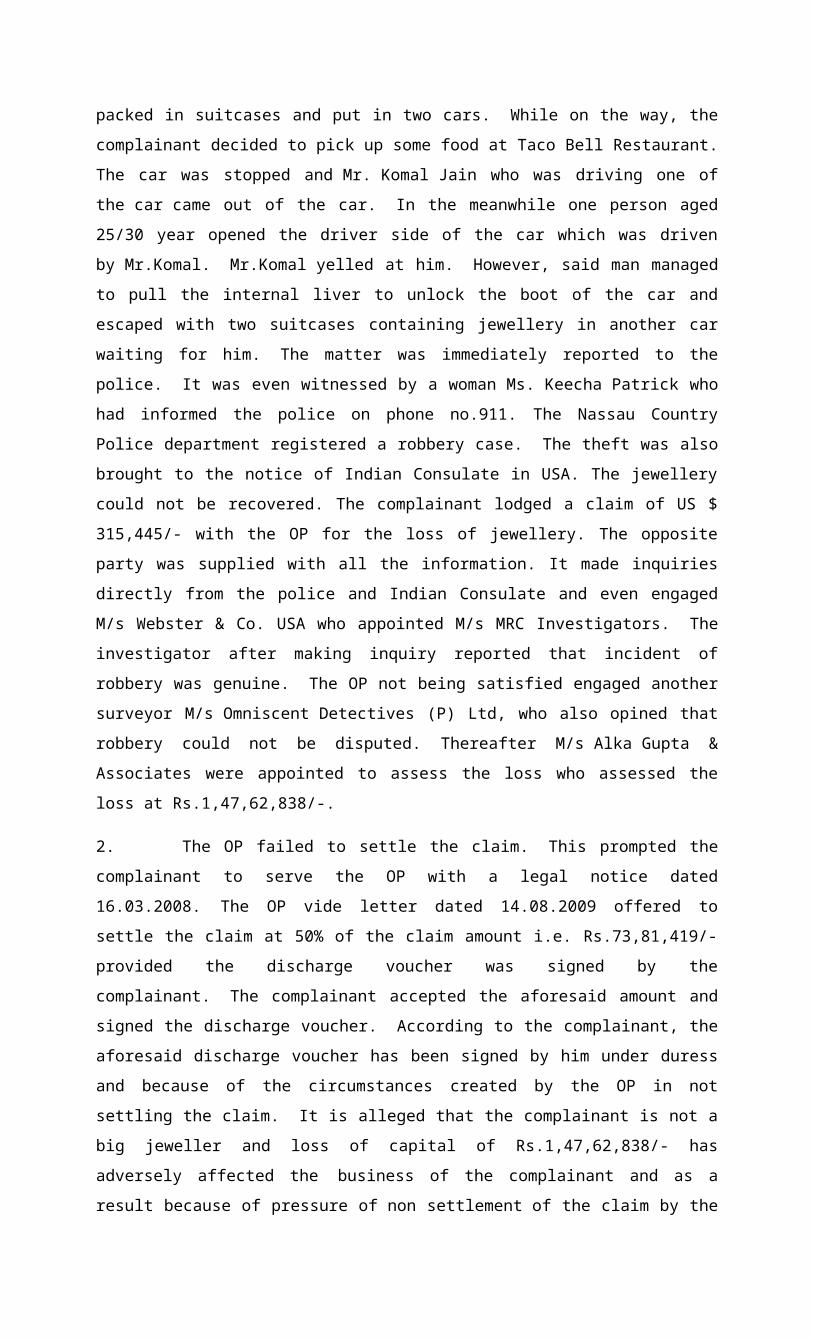

the jewellery was packed in suitcases and put in two cars. While on the way, the complainant

decided to pick up some food at Taco Bell Restaurant. The car was stopped and Mr. Komal Jain

who was driving one of the car came out of the car. In the meanwhile one person aged 25/30

year opened the driver side of the car which was driven by Mr.Komal. Mr.Komal yelled at

him. However, said man managed to pull the internal liver to unlock the boot of the car and

escaped with two suitcases containing jewellery in another car waiting for him. The matter was

immediately reported to the police. It was even witnessed by a woman Ms. Keecha Patrick who

had informed the police on phone no.911. The Nassau Country Police department registered a

robbery case. The theft was also brought to the notice of Indian Consulate in USA. The

jewellery could not be recovered. The complainant lodged a claim of US $ 315,445/- with the OP

for the loss of jewellery. The opposite party was supplied with all the information. It made

inquiries directly from the police and Indian Consulate and even engaged M/s Webster & Co.

USA who appointed M/s MRC Investigators. The investigator after making inquiry reported that

incident of robbery was genuine. The OP not being satisfied engaged another surveyor

M/s Omniscent Detectives (P) Ltd, who also opined that robbery could not be

disputed. Thereafter M/s Alka Gupta & Associates were appointed to assess the loss who

assessed the loss at Rs.1,47,62,838/-.

2. The OP failed to settle the claim. This prompted the complainant to serve the OP with a

legal notice dated 16.03.2008. The OP vide letter dated 14.08.2009 offered to settle the claim at

50% of the claim amount i.e. Rs.73,81,419/- provided the discharge voucher was signed by the

complainant. The complainant accepted the aforesaid amount and signed the discharge

voucher. According to the complainant, the aforesaid discharge voucher has been signed by him

under duress and because of the circumstances created by the OP in not settling the claim. It is

alleged that the complainant is not a big jeweller and loss of capital of Rs.1,47,62,838/- has

adversely affected the business of the complainant and as a result because of pressure of non

settlement of the claim by the OP, he was compelled to accept the offer and signed the settlement

voucher. Claim for the aforesaid settlement is not binding. The complainant has filed this

complaint claiming Rs.2,83,79,458/- including the balance due from the surveryor assessment

report plus interest.

3. The OP has contested the claim by filing the reply. The complaint is also resisted on the

ground that after having settled the matter by receiving a sum of Rs.73,81,419/-, the complainant

is estopped from reagitating the matter by filing a fresh complaint.

4. Undisputedly, the complainant has received a sum of Rs.73,81,419/- in full and final

settlement of the claim by executing a discharge voucher which clearly records that the aforesaid

amount has been received by the complainant in full and final settlement of all his claim. Now

the question is after executing such a discharge voucher, whether the insured complainant could

still pursue the claim for any further amount?

5. This question came up for the consideration of the Supreme Court in the case of United

India InsuranceAjmer Singh Cotton & General Mills and Ors. II (1999) CPJ 10 (SC) =

(1996) 6 SCC 400 , wherein the Supreme Court observed as under:

“The mere execution of discharge voucher would not always deprive the consumer from preferring claim with respect to the deficiency in service or consequential benefits arising out of the amount paid in default of the service rendered. Despite execution of the discharge voucher, the consumer may be in a position to satisfy the Tribunal or the Commission under the Act that such discharge voucher or receipt had been obtained from him under the circumstances which can be termed as fraudulent or exercise of undue influence or by misrepresentation or the like. If in a given case the consumer satisfies the authority under the Act that the discharge voucher was obtained by fraud, misrepresentation, undue influence or the like, coercive bargaining

compelled by circumstances, the authority before whom the complaint is made would be justified in granting appropriate relief”.

6. The above position was reiterated by the Supreme Court in the later decisions in National

Insurance Company Limited Vs. Sehtia Shoes (2008) 5 SCC 400

7. On reading of the above judgments, the legal position which emerges is that the mere

execution of the discharge voucher would not always deprive the consumer for preferring the

claim with respect to deficiency in service despite of execution of discharge voucher. The

consumer can successfully press his claim provided the consumer is able to establish that the

discharge voucher or receipt was obtained from him by fraud, misrepresentation, undue influence

or coercive bargaining.

8. Shri S.C.Dhanda, Advocate, learned counsel for the complainant has submitted that ratio

of the above noted judgments of the Supreme Court are squarely applicable to the facts of the

case. He has contended that admittedly the claim for loss of jewellery due to robbery was

submitted in June 2001. The matter was inquired into by the OP through M/s MRC Investigators

as also M/s Omniscent Detectives (P) Ltd who confirmed the robbery incident. Even the

surveyor assessed the loss suffered due to robbery at Rs.1,47,62,838/- and despite that OP

delayed the settlement of claim which resulted in severe financial constraint on the complainant

and because of this coercive approach of the OP, the complainant was compelled to accept the

offer of 50% of the loss assessed by the surveyor. It is thus contended that complainant was

coerced to sign discharge voucher and as such aforesaid discharge voucher cannot be taken as a

circumstance to deprive the complainant from preferring the claim. Learned counsel further

contended that the intention of the opposite party to pressurise and coerce the complainant to

accept the offer is evident from the office noting dated 21.07.2009 wherein the Chief Manager of

the Opposite Party while recommending settlement of the claim on compromise basis at 50% has

noted that before releasing the payment a letter of compromise towards full and final payment be

obtained by the Regional Office and placed on the file.

9. Learned counsel for the opposite party on the contrary has contended that this is a case of

voluntarily full and final settlement of the claim. In support of this contention, learned counsel

has drawn our attention to copy of letter dated 14.08.2009 addressed by the OP to the

complainant wherein it is clearly mentioned that the cheque of Rs.73,81,419/- is being tendered

in full and final settlement of the claim with a clear warning that if the offer is not acceptable, the

complainant should return the cheque forthwith. Learned counsel contended that the

complainant after having knowledge of the offer given in the letter has accepted the cheque

which clearly indicate that the cheque has been accepted voluntarily without any demur or

protest. Therefore, the complainant is estopped from filing the complaint.

10. We have considered the rival submissions and perused the material on record. The

question for determination is whether or not the complainant has received the offered amount of

Rs.73,81, 419/- and signed the full and final discharge voucher voluntarily under coercion,

misrepresentation or fraud. To find answer to the question it would be useful to have a look on

the content of the letter dated 14.08.2009 vide which the cheque for settlement was sent to the

complainant:

“Sir / Madam,

We are enclosing herewith our cheque no.465772 dated 14.08.2009 for Rs.73,81,419/- (Rupees Seventy Three Lakh Eighty One Thousand Four Hundred Nineteen Only) in full and final settlement of your above claim.

Please note in case the above offer is not acceptable to you, the cheque should be returned forthwith to this office, failing which it will be deemed that you have accepted the offer in full and final satisfaction of your claim. The retention of this cheque and / or encashment thereof will automatically amount to acceptance in full and final satisfaction of your above claim without reason and you will be estopped from claiming any further relief on the subject”.

11. On reading of this letter, it is clear that cheque was offered to the complainant in full and

final settlement of his insurance claim with clear instructions that if the offer was not acceptable,

the cheque should be returned failing which it shall be deemed that the cheque has been accepted

in full and final settlement of claim. Despite that the complainant hasencashed the cheque

without any demur or protest. If the complainant was coerced to sign the discharge voucher

nothing prevented him to record his protest on the discharge voucher, which is not the

case. Therefore, we are unable to accept the contention that discharge voucher has been obtained

by adopting coercive means.

12. Undisputedly the cheque for full and final settlement was received by the complainant on

14.08.2009. The protest notice, however, was signed after six months on 30.03.2010. From this

it can be safely inferred that the complainant accepted the cheque amount in full and final

settlement of his claim voluntarily and signed the discharge voucher. If at all there was a

pressure on the complainant to sign the discharge voucher, the complainant under ordinary

course of circumstances instead of waiting for six months would have protested against the so

called coercive measures adopted by the opposite party. From the conduct of the complainant

also, it appears that the complaint after entering into the settlement has been filed on after-

thought with a view to extract more money from the opposite party. As regards the office noting

dated 21.07.2009, much importance cannot be attached to the same because the noting only

indicate the anxiety of the Chief Manager of the Opposite Party to protect the rights of the

opposite party and this noting by itself cannot be taken as a coercive protest.

13. In view of the discussion above, we find that the complainant received a sum of

Rs.73,81,419/- voluntarily in full and final settlement of his claim and also executed a discharge

voucher in this regard. Thus, the complainant having voluntarily entered into the full and final

settlement is now estopped from re-agitating the claim by filing a complaint. As such, the

complaint is liable to be dismissed as not maintainable.

14. The complaint is, hereby, dismissed as not maintainable.

…..………………………Sd/-…. (AJIT BHARIHOKE, J) ( PRESIDING MEMBER)

…..…………………Sd/-……… (SURESH CHANDRA) MEMBER

NATIONAL CONSUMER DISPUTES REDRESSAL COMMISSION NEW DELHIREVISION PETITION NO. 2945 OF 2012

(Against the order dated 17.05.2012 in First Appeal No. 1518/2009 of the State Commission Haryana, Panchkula)

Rahul Electricals, Shop No.1379, Railway Road Rohtak-124001, Haryana Through its Proprietor Sh.Kulbhushan

........ Petitioner Vs.

1. State Bank of India Hissar Road Branch, Hissar Road, Rohtak Through its Manager 2. The Oriental Insurance Company Ltd. Through its Divisional Manager, Rohtak-124001, Haryana

......... Respondents BEFORE:

HON'BLE MR. JUSTICE AJIT BHARIHOKE, PRESIDING MEMBER

HON’BLE MR.SURESH CHANDRA, MEMBER

For the Petitioner : Mr.Shekhar Raj Sharma, Advocate

For the Respondent No.1 : Mr.U.C.Mittal, Advocate

For the Respondent No.2 : Mr.Manish Pratap, Advocate Alongwith Mr.Ajay Singh, Advocate

PRONOUNCED ON : 05 th JULY, 2013

ORDER

PER JUSTICE AJIT BHARIHOKE, PRESIDING MEMBER

This revision is directed against the order dated 17.05.2012 passed by State Consumer

Disputes Redressal Commission Haryana ( in short, ‘the State Commission’) dismissing the

appeal preferred by the petitioner / complainant against the order of the District Consumer

Forum Rohtak dismissing the complaint.

2. Briefly put relevant facts for the disposal of this revision petition are that M/s Rahul

Electricals filed a complaint under section 12 of the Consumer Protection Act against the

respondents State Bank of India as also the Oriental Insurance Company Limited claiming that

the complainant was engaged in the business of electrical goods. Complainant had obtained a

cash credit limit of Rs.3 lakhs from the respondent / bank against the hypothecation of the

stock. It is the case of the complainant that as per the agreement, the stock of the complainant

was required to be insured and the opposite party / bank had agreed to get the stock insured on

behalf of the complainant and debit the insurance premium to the cash credit account of the

complainant. Pursuant to the agreement, the opposite party / bank had been getting the stock

insured with the insurance company and the last insurance was for the period w.e.f. 25 th May

2006 to 24th May, 2007. It is alleged in the complaint that after 24th May, 2007, the opposite

party / bank failed to renew the insurance. Unfortunately on 30.05.2007 the shop of the

complainant caught fire due to electrical spark and the entire stock was destroyed. The complaint

in this regard was lodged at PS Rohtak City vide DD No.46 dated 31.05.2007. The complainant

approached the opposite party / bank to disclose the name of the insurance company with whom

he had got the stock insured. The opposite party bank after evading the issue for sometime,

ultimately replied that as per the agreement, the insurance was to be got done by the complainant

himself. Claimant alleging the failure of the bank to renew the insurance of the stock as

deficiency in service filed complaint before the District Forum claiming compensation of

Rs.6,27, 870/- on account of loss suffered due to fire accident besides Rs.2,00,000/- on account

of mental pain and agony. The complainant also sought direction to the opposite party bank to

stop charging interest on the over draft w.e.f. 25.05.2007.

3. The opposite party bank contested the complaint and took the plea that stock hypothecated

with the bank were to be insured comprehensively for the market value by the complainant in

joint names of the bank and the complainant. It was alleged that the opposite party bank never

got the goods insured and it was for the complainant to get the goods insured at his own

responsibility. The bank also denied that stock worth Rs.6,27,870/- was destroyed. Thus, it was

pleaded that there was no deficiency on the part of the bank.

4. OP No.2 took the plea that it was neither necessary nor proper party because on the date of

fire accident, the stock of the complainant was not insured with the insurance company.

5. Sole controversy which needs determination in this revision petition is whether or not as

per the terms of agreement between the parties, respondent / bank was under obligation to get the

stock available at the shop of the complainant / petitioner insured?. If answer to this question is

in the affirmative, then of-course, the respondent / bank has been deficient in providing service

to the petitioner / complainant.

6. Shri Shekhar Raj Sharma, Advocate, learned counsel for the complainant/ petitioner has

contended that impugned orders of the fora below are not sustainable as the orders are based

upon incorrect appreciation of the evidence. It is argued that both the foras below have failed to

appreciate that as per the agreement between the parties, opposite party no.1 / bank was under

obligation to get the stock lying in the shop of the petitioner insured on behalf of the petitioner /

complainant and debit the insurance premium amount to his cash credit account. It is contended

that this obligation is admitted by the opposite party / bank in para 2 (c ) and ( e) of their written

statement filed in response to the complaint in the District Forum. Learned counsel for the

petitioner has also drawn our attention to the copies of the statement of accounts pertaining to

cash credit account of the complainant for the periods 01.04.2006 to 31.12.2006 and 21.07.2006

to 31.05.2007 wherein there are debit entries pertaining to the insurance premium for the

insurance of stock lying in the premises of the petitioner. It is contended that impugned orders

have been passed ignoring the aforesaid evidence. Therefore, those are liable to be set aside.

7. On careful perusal of the record, we find both that both the District Forum as well as State

Commission has based their finding on interpretation of Clause V of the hypothecation

agreement which reads thus:

“That the said goods shall be kept by the Borrower (s) in good condition at his / their risk and expense. Further, when required by the Bank all goods the subject of this agreement shall be insured against fire by the Borrower(s) at his / their expense in the joint names of the Borrower(s) and the Bank in some Insurance Office approved by the Bank to the extent of atleast 10 percent in excess of the amount advanced by the Bank against them and that the Insurance Policy (ies) shall be delivered to and held by the Bank, if the Borrower(s) fail(s) to effect such Insurance on being asked in writing to do so, the bank may insure the said goods against fire in such joint names and debit the premium and other charges to such account as aforesaid and in the event of the Bank being at any time apprehensive that the safety of the goods is likely to be endangered owing to not or strike, it shall on failure by the Borrower(s) to do so after request by the Bank at its discretion itself insure the same in such joint names against any damage arising therefrom the cost of such extra insurance being payable by the borrower(s) and being debited to such account as aforesaid, the Borrower(s) expressly agree(s) that the Bank shall be entitled to adjust, settle, compromise or refer to arbitration any dispute between the Company and the insured arising under or in connection with such policy or policies and such adjustment, settlement compromise and any award made on such arbitration shall be valid and binding on the Borrower(s) and also to receive all moneys payable under any such policy or under any claim made there under and to give a valid receipt thereof and that the amount so received shall be credited in the account having reference to the goods in respect of which such amount is received and that the Borrower(s) will not raise any question that a large sum might or ought to have been received or be entitled to dispute his / their liability for the balance remaining due on such account after such credit”.

8. On plain reading of the above said clause, it is evident that as per the agreement between

the parties, the complainant borrower when required by the bank was under obligation to get the

stock in his shop insured at his own expense in the joint names of borrower and the bank and if

the complainant failed to get such insurance on being asked to do so in writing, the bank in its

own discretion was entitled to get the goods insured against fire and debit premium and other

charges to the account of the complainant. There is nothing in this clause which may suggest

that the bank was under any obligation to get the hypothecated goods insured on behalf of the

complainant. Further, the plea of the complainant that there is an admission of obligations to get

the stock insured on the part of the respondent / bank, in para 2 (c) & ( e) of the written

statement is against the record. On perusal of the copy of the written statement of the opposite

party / bank, we find that in para 2 ( c ) & (e ), the bank has categorically denied that it had

any obligation to get hypothecated goods insured on behalf of the complainant. On the contrary

in the aforesaid paragraph, the bank has categorically stated that stock hypothecated with the

bank as per the agreement was to be insured by the complainant at his own expense in the joint

names of the bank and the borrower. Thus, we do not find any merit in the plea of the

complainant.

9. In view of the discussion above, we are of the opinion that both the fora below have rightly

dismissed the complaint in view of the written agreement between the parties. There is no

material irregularity or infirmity in the impugned order which may call for any interference by

this Commission in exercise of its revisional jurisdiction. Accordingly, the revision petition is

dismissed.

………………………Sd/-………. (AJIT BHARIHOKE, J) ( PRESIDING MEMBER)

..…………………Sd/-…………… (SURESH CHANDRA) MEMBER

Am/

NATIONAL CONSUMER DISPUTES REDRESSAL COMMISSION NEW DELHI

REVISION PETITION NO. 4747 OF 2012 (Against order dated 03.10.2012 in First Appeal No. 827 of 2011 of the

Andhra Pradesh State Consumer Disputes Redressal Commission,Hyderabad)

1. The Managing Director Cholamandalam MS. General Insurance Co. Ltd. Venkata Plaza-2, D.No. 6-3-698/3 Ist Floor, Panjagutta Cross Roads, Hyderabad

2. The Managing Director Cholamandalam MS. General Insurance Co. Ltd. Paramount Health Management, Elite House, Ist Floor, 55-A, Vasanji Road, Opp. Andheri Kurla Road Chakala, Andheri, Mumbai- 400 093

…Petitioners

Versus Ms. Borredy Pragahi W/o T. Bharat Reddy R/o D.No. 1/334-3, Opp. RTC Bus Stand, Maruthi Nagar Presently Resident At Flat No.-408, Victory Apartments, Yerramukkapalli Kadapa City, YSR District 526001

…Respondents BEFORE:

HON’BLE MR.JUSTICE J.M.MALIK, PRESIDING MEMBERHON’BLE DR.S.M.KANTIKAR, MEMBER For the Petitioner(s) : Mr.S.M. Tripathi, Advocate For the Respondent(s) : Ms. Radha, Advocate

Pronounced on 5th July, 2013

ORDER

PER DR. S.M. KANTIKAR

1. The Revision Petition is filed against the Impugned Order of Andhra Pradesh State

Commission Disputes Redressal Commission, Hyderabad (in short, State Commission,

AP) in First Appeal Number 827 of 2011 against the Consumer Complaint No. 44/2011

of District Consumer Disputes Redressal Commission, Kadapa (in short District

Consumer Forum).

2. The Facts In Brief are:

The Complainant/Respondent herein was Ms. Borredy Pragahi a medical student of

Nanjing Medical University,China took Overseas Student Travel Insurance Policy from

the respondent for a sum of US $.1,00,000/- covering from 25.02.2007 to 24.02.2009.

She got admitted in Jiang Hospital,Nanjing for treatment of iliac fossa pain, fever and

nausea where she was diagnosed as Right Oopheritis, Menstrual Syndrome and Acute

Appendicitis and treated accordingly.

3. She returned back to India on 16.01.2009 to visit her parents. Thereafter, she suffered

similar attacks of pain as suffered in China for which she was operated on emergency

basis at Pragathi Orthopaedic & General Hospital, Karapa on 10.02.2009. The said

treatment incurred Rs.64,282/- as expenditure. The claim made with the Respondent,

which was repudiated on the ground that said operation was not conducted in China.

Therefore, she was not entitled for the claim amount. Against this repudiation the

Complainant filed a Complaint before District Forum on 25/2/2011 claiming Rs.64,282/-

together with interest 24 per cent per annum, Rs.50,000/- towards mental agony and cost.

4. The respondent resisted the case. While admitting the issuance of policy, it was alleged

that the Complainant having taken treatment at Kadapa was not entitled to the amount

covered under the policy. In fact, she was paid as amount of Rs.25,805/- towards

treatment she underwent in China, which was paid towards full and final settlement of the

claim. The surgeon, who conducted surgery, is none other than her own father. Therefore,

it prayed for dismissal of the Complaint with costs.

5. The District Forum dismissed the Complaint. The Complainant preffered the Appeal in

the State Commission. The State Commission set aside the order of District Forum and

allowed the appeal.

6. Being aggrieved by impugned order of State Commission petitioner herein filed this

revision petition on 14/12/2012.

7. We have heard the learned counsel for both the sides and perused the evidence on

record before District forum and State Commission.

8. It is an undisputed fact that the Opposite party – the Insurance Company had issued an

Overseas Student Travel Insurance Policy, Ex.B.1 for a sum of US $ 1,00,000/- covering

the period from 25.02.2007 to 24.02.2009. It is not in dispute that during the above said

period, she had taken treatment at China and the amount which she incurred towards

treatment was paid. Her case was that after she returned to India,

an emergency Appendicectomy operation was conducted on 10.02.2009,. This is

evident on perusal of discharge summary that the diagnosis was “Acute Recurrent

Appendicitis” and she incurred a sum of Rs.64,282/- towards medical expenses. When

she requested for settlement of claim, the Insurance Company repudiated it by issuing

letter, Ex.B.2 alleging that she would not be entitled to the said amount if the operation

was performed in India.

9. On perusal of the policy condition under section B which is as follows:

“Section B-Cover 1. Medical expenses-

1) Under Medical Evaculation/Transportation: 1) the transportation of the insured

from that overseas country to India or the place of residence where necessary

medical attention can be provided; the coverage for medical treatment will be up

to the limit of indemnity for medical expenses for maximum period of 30 days from

the date of return.” (emphasis supplied)

10.

The Pragathi H

ospital records like In-Patient Case Sheet, Discharge Summery where the Complainant

underwent emergency operation on 10.02.2009 and it’s evident that operation was

within 30 days of her return from China that is on 16.01.2009. Therefore, the Insurance

Company is bound to reimbursement the amount paid by Complainant towards the

hospitalization expenses. The repudiation was unfair and is unjustifiable. Therefore, we

agree with the findings of State Commission in allowing the appeal filed by the

Complainant. Therefore, we upheld the order of State Commission and pass the order-

The Revision Petition is dismissed with a punitive cost of Rs.25,000/- which is to be

paid to Complainant within 45 days otherwise it will carry 9% interest per annum, till its

realization. ..…………………..………

(J.M. MALIK J.) PRESIDING MEMBER

……………….…………… (S.M. KANTIKAR) MEMBER

NATIONAL CONSUMER DISPUTES REDRESSAL COMMISSION NEW DELHI

ORIGINAL PETITION NO. 328 OF 2000

Indian Sugar Exim Corporation Limited Having its registered office at: Block-C, IInd Floor, Ansal Plaza, August Kranti Marg, New Delhi- 110049 Through Mr. V.K. Jain,its Manager (Commercial)

…….Complainant

Versus

1. M/s. United India Insurance Co. Ltd. Having its registered & head office at: 24, Whites Road Chennai- 600014 Through its Divisional Manager Divisional Office No.XXIII 607-608, Devika Tower 6, Nehru Place New Delhi- 110019

2. M/s. J.B. Boda Surveyors Pvt. Ltd. Having its registered office at: Maker Bhavan No.11, Sir Vithal Das Thackersey Marg Mumbai- 400020 Through its Managing Director

........Opposite parties

BEFOREHON’BLE MR. JUSTICE J.M. MALIK, PRESIDING MEMBERHON’BLE MR. VINAY KUMAR, MEMBER For the Complainant : Mr. Buddy Ranganathan, Advocate Mr. Lokesh Bhola, Advocate, Ms. Pankhuri Jain, Advocate Ms. Mansha Anand, Advocate For the Opposite parties : Mr. A.K. De, Advocate Mr. Rajesh Dwivedi, Advocate Ms. Deepa Agarwal, Advocate

PRONOUNCED ON: 5/7/13. ORDER

PER MR.VINAY KUMAR, MEMBER

M/s. Indian Sugar & General Industry Export Import Corporation has filed this complaint

in the year 2000. In the course of the proceedings MA/1428/2009 was filed informing that the

Complainant had changed its name to M/s Indian Sugar Exim Corporation Ltd. The application

was allowed on 15.12.2009 and necessary amendment in the memo of parties permitted. In the

proceeding of 19.11.2012, it was observed that negotiations for compromise between the parties

were in progress. The matter was therefore adjourned to 2.1.2013 directing that in the event of

no compromise being reached, the parties would file their written arguments. The matter was

finally heard on day to day basis and reserved for order on 16.1.2013.

BACKGROUND

2. The consumer dispute arises out of import of 13,800 MT of white sugar by the

Complainant from Switzerland in 1994. The entire consignment was shipped to India and was

received at Mangalore Port. The Complainant had obtained a marine insurance policy to cover

the shipment. It was effective from 13.4.1994, initially for a period of 60 days. Subsequently,

the terms of the policy got extended to 1.11.1994, with three extensions in between.

CASE OF THE COMPLAINANT

3. The Cargo vessel MV Scotian Express left Eemshaven Port in Netherland on 28.4.1994 and

arrived at Mangalore Port on 26.5.1994. Discharge of the entire Cargo of 13,785 (mts) of Sugar

was completed by 3.7.1994. As per para 7 of the complaint petition, “substantial quantity of

sugar bags were found progressively to be partly wet and stained in all hatches of the vessel

apart from bursting of many bags. It would be also evident from perusal of date-wise summary

of discharge as recorded in Annexures-A & B of Annexure-8 herein that; heavy rain was

experienced right from first day of discharge upto the date of final discharge, namely, 3rd July

1994. A copy of Certificate issued by Indian Meteorological Department Station: Panambur

dated 6th December 1994 certifying the recorded rain fall during the months of May, June, July

& August 1994 is annexed herewith and marked as Annexure-9.”

4. In the above background of damaged conditions of the goods, the Complainant appointed

M/s. Superintendence Company of India Pvt. Ltd. (hereinafter referred to SCPL) to inspect the

condition of the Cargo in the vessel and to supervise its discharge therefrom. Simultaneously,

OP-1/ insurance company appointed a Surveyor (OP-2) for the same purpose. The report of OP-

2 (Annexure 12) gives full details of unloading of 13800 (mts) of sugar between 26.5.1994 and

3.7.1994. In this report OP-2 clearly mentions that:-

“During discharging we observed that lots of bags were wet stained/discoloured in-side the holds and the same were discharged alongwith the sound bags since it was difficult to segregate the wet stained/discoloured bags inside the hold.”

The report of the Surveyor (OP-2) has also noted the details of the total discharge of 13800 MTs

(Annexure 12) as follows:-

No. of sound bags 271,266

No. of cut/torn bags 1109

No of wet stained/ discoloured bags 3625

Total no. bags discharged 276,000

The complaint petition states that the Complainant is entitled to compensation on the basis of the

facts contained in the above report of the Surveyor/OP-2.

5. The goods were stored in hired transit godowns of Mangalore Port Trust. The process of

unloading and stacking was completed between 26.5.1994 to 3.7.1994. It is the case of the

complainant that in this period Mangalore received very heavy rain fall. Despite coverage of the

stocks, top and bottom, with tarpaulins sheets, further damage to the stocks occurred from

leakage of the godown roofs. Also, excessive rains continued through the months of June and

July.

6. The Complainant was advised by OP-2 to segregate the damaged cargo, but according to

the Complainant it was not possible as the godowns were packed and there was no space to take

up the segregation exercise of such a huge quantity. Moreover, with incessant rain any such

exercise, involving movement of stocks from one godown to another would have exposed them

to further damage by rain. Allegedly the Complainant also informed the OPs that due to heavy

rain it was not possible to move the stocks to other regions in the country. He was advised to

take action keeping in view Clauses of 16 and 18 of the Policy. The first dealt with

reimbursement of expenditure incurred for averting or minimising loss and protecting the rights

of the underwriter against third parties. The second required the Complainant to act with

‘reasonable despatch’ under all circumstances within its control.

7. The complaint petition states that by 22.10.1994, in all 77414 bags of sugar were

segregated , with re-bagging to the extent necessary and 3870.70 MTs of sound sugar was

despatched. Details of these deliveries made between 10.8.1994 and 22.10.1994 are shown in

Annexure 42 to the complaint. Complaint petition also shows that joint survey of the remaining

stocks—198353 bags-- was done and its report of 22.11.1994, signed by the representatives of

both sides showed that it largely comprised either partly wet or fully wet bags. But, the total

weight of these 198353 is accepted to be 9917.65 MTs in the complaint. This was based on

analysis of 6000 bags as a joint exercise taken by both.

8. The complaint petition also seeks to make out a case that when sugar is damaged by rain it

is not only moisture but also factors like loss of lustre and caking etc. that need to be taken into

consideration. Allegedly, after 198353 bags of sugar were sold @ of Rs.9875 per MT, the

picture of final loss became clear. Therefore on 16.9.1995 a claim under the policy was made for

Rs.707.83 lakhs. In response, OP-1/ United India Insurance Company made an offer of

Rs.44,24,963/- only on 8.5.1998, which was declined by the Complainant. The prayer of the

Complainant is to award an amount of Rs.707.83 lakhs with 24 % interest from the date of the

claim i.e. 16.9.1995.

RESPONSE OF THE OPPOSITE PARTIES

9. Per contra, in the Written Statement filed on behalf of OP-1, it is stated that the entire

unloading operation was personally supervised by the Surveyor/ OP-2 between 26.5.1994 to

3.7.1994. The WS accepts that the cargo has suffered water damage during the voyage and

many bags were found to be wet/stained/discoloured at the time of unloading. Intermittent rains

had continued during the entire period of unloading and the discharged cargo was stored in

godowns with “roofs full of holes”. The written response strikes a note similar to that in the

complaint petition when it comes to effect of continued heavy rain fall and repeated damage to

the godown roofing on the sugar stocks stored therein. Allegedly, the Complainant failed to take

prompt action to save goods from suffering further rain damage in the godowns.

10. It is the case of the Insurance company that while the Surveyor had repeatedly demanded

segregation of sound stocks from the damaged ones in the godown, the Complainant was

unwilling to take up the exercise, on the ground of high cost of the operation and offered to do

the same at the time of delivery. However, the delivery operation itself came to a stop after

23.10.1994 with the despatch of 77414 bags of the sugar to various destinations.

11. As stated in the WS of the OP/United India Insurance Company Ltd., an attempt was made

to settle the claim on non-standard basis, due to failure of the Complainant to segregate the

damaged stocks from the sound ones and failure to take timely action to minimize the loss. The

total loss was quantified by OP-2 to be of the order of 288.127 MTs, for which a total

compensation Rs.44,24,963 was offered to the Complainant on 8.5.1998, against the claim of

Rs.707,83,101.96. Apparently, the offer was declined. According to the OPs, there was no

deficiency of service in rejection of a very large claim of Rs.707,83,101.96.

ARGUMENTS ADVANCED BY THE TWO SIDES

12. Before the National Commission the case of the complainant has been argued by learned

Advocates, Mr Buddy Ranganathan, Advocate and Mr A K De, Advocate has argued the case of

the United India Insurance Co. They have been heard extensively, over several days, with

reference to documents brought on record. We have also considered the written arguments filed

on behalf of the two sides.

13. Coming to the core of their arguments, Mr Ranganathan argued that damage to the stocks

and resultant loss suffered by the complainant are not denied by the insurer. But against a loss of

Rs 707.8 lakhs, the insurance has assessed the loss as Rs 58.99 lakhs only. Even here, OP-1 has

deducted 25% in the name of non-standard settlement of the claim. This was not acceptable to

the complainant. Further, he referred to the joint exercise of November 1994 which segregated

6000 bags for analysis. Learned Counsel argued that the report of the Surveyor/OP-2 itself

mentions that out of 6000 bags 5789 were found to be water stained externally, a fact that by

itself would show that damage to the stocks was extensive. He referred to test results of the

stocks (on parameters of polarisation, moisture, colour etc) at the time of loading for India and

compared them to the results of analysis of samples drawn on 2.12.1994 and claimed that water

had affected the quality (sale value) of the stocks.

14. Reacting sharply to the above, learned counsel for the OP/insurance coy, Mr. A.K.De,

argued that a series of correspondence has taken place between the Surveyor appointed

by the insurance and the insured on precisely the same concern i.e. need to protect the stored

stocks against further damage from continued rain. But, the Complainant did not take action for

speedy repair of the leaking godowns or for segregating damaged stocks from good ones. Nor

was action taken for prompt disposal as a measure against further damaged in continued storage.

The delivery of sugar stocks started only on 10.08.1994 and came to an abrupt stoppage since

23.10.1994. By then only 77414 bags, as against import arrival of 27,0000 bags, had been

delivered to different destinations. It has been strongly argued on behalf of the

respondent/Insurance Company that lab analyses of samples taken from 6000 bags segregated in

November, 1994, showed that despite external damage to the packaging, moisture and sucrose

content as well as colour of sugar were within the stipulated limits. The assessment of total loss

being limited to 288.127 MT against the total quantity of 13800 MT was based on the above

mentioned test results. Mr. A.K.De, argued that the complainant base his case only on the extent

of external damage to the bags and not on actual condition of the sugar within. Therefore, the

claim of the Complainant for Rs.707.83 lakhs is exaggerated, misconceived and untenable. The

insurer cannot be held liable for loss caused by failure of the Complainant to take prompt action

in protection and disposal of the stocks.

THE EVIDENCE ON RECORD

15. Damage during storage at Mangalore Port, caused by continued rains and leaking godown

roofs, is not denied. Para 19 of the affidavit evidence of Mr V K Jain, Manager (Commercial) of

complainant coy accepts it. But it also goes on to add that the godowns were packed and there

was no space to undertake the exercise of stock segregation. But, the claim that OPs had agreed

that it could be done at the time of delivery, is denied by the OPs.

16. The two sides eventually undertook an exercise of segregating 6000 bags in November

1994 and analysed the contents with the help of SGS Goa. (Annexures 54 & 55). The content

analysis of water affected bags showed their moisture content as follows—

Partially stained bags 0.16%

Fully stained bags 0.25%

Further, in December 1994, while the complainant was in the process of moving 1700 MT

(34000 bags) of sugar to Orissa, OP-2 got them analysed. As per his report of 23.5.1995, re-

bagging resulted in 118 bags of water damaged sugar and 33,882 bags of sound quality cargo.

Therefore, his report stated that the condition of sugar was not as bad as to require disposal on

“as is where is” basis. The final assessment of loss was given by the Surveyor in June 1995, as

follows:-

1. Amount of cargo lost due to cut/torn bags

discharged from the vessel 7.950 M.T.

2. Based upon the %age of damages noticed on

the 34,000 bags the loss in respect of the balance

cargo of 1,98,427 bags (9921.350 M tons). 34.433 M.T.

3. Further depreciation allowed on 9,829,766 M.Ts at 2.5% based on

analysis. 245.755 M.T.

4. Total loss of cargo 288.127 M.T.

17. While the OPs have relied on the report of the Insurance Surveyor, the complainant has

relied upon the report of their expert agency, Superintendence Co. of India Pvt. Ltd (SCPL). It

talks about delivery of stocks soon after recession of the monsoon and details segregation and

despatch of 77414 (3870MT) between 17.8.1994 and 22.10.1994. SCPL report of 8.8.1995 states

that on the basis of careful visual examination made on 3.10.1994 and excluding 7185.9 MT of

stocks lying in two Port Sheds, “the entire remaining quantity of 2721.95 MT were completely

damaged/wet/moistured conditioned and contents thereon not free flowing and therefore advised

our client to dispose of the above stock immediately on as is where is condition to avoid to avoid

further losses/damages.” Significantly, this opinion was based on visual examination of

2721.95 MT (corresponding to 54439 bags) stocks. SCPL also relies on segregation of 2000 bags

on 23.10. 1994 and 6000 bags on 22.11.1994, jointly with OP-2. Its conclusion that over 99% of

the remaining stock of 197667 bags (approximately 9883 MT) were damaged, is based on

external appearance of stocks. On the other hand, the Insurance Surveyor has gone further and

based its conclusions on content analyses of sucrose, moisture and polarisation percentages in the

stock of sugar. SCPL report refers to these analyses reports and merely states that moisture

content was above permissible limits. In the affidavit evidence of the complainant it is alleged

that it was the result of selective sampling.

18. Affidavit evidence of Mr S K Sharma, Deputy Manager, has been produced on behalf of

the insurer,OP-1. Its main thrust is on the contention that despite repeated requests and reminders

from the Surveyor, the complainant did not segregate the stocks. Allegedly, this failure of the

complainant “further aggravated the loss and had the soaked bags been separated from the sound

one, the moisture would not have affected the sound bags/or the moisture content in cargo would

have been minimal.” However, 6000 bags were segregated in November 1994, as part of content

evaluation exercise. It also refers to analysis of samples drawn on 2.12.1994 and states that, “It

was noticed that the moisture and sucrose contents were found to be within stipulated limits and

colour of sugar was also within specification.”

19. OBSERVATIONS AND CONCLUSIONS

a. It is not the case of the complainant that it was not aware that the cargo would arrive

into Magalore Port during heavy monsoon season. But when the cargo arrived, the

complainant did nothing more than storing it in unsafe conditions and waiting for the

monsoon season to pass.

b. Some damage had already occurred while in the ship hold itself. But it was only 4734

bags out of 276000 as reported by insurance surveyor and not questioned by the

complainant. Admittedly, (para 9 of the complaint) these 4734 damaged bags were re-

bagged into 3428 standard bags. Thus, the net loss before leaving the ship would come

to 1203 standard bags out of 276000 i.e. 0.43%.

c. Viewed only from external impact on packaging, the above report of the Insurance

Surveyor (preliminary report of 6.10.94 and not followed by a final report) would

show the loss of 65.20 MT out of 236.70 MT i.e. 27.54% of the wet or damaged

bags, which was acceptable to complainant.

d. Complainant has taken conflicting stands by first claiming that there was no space in

the godowns to take up stock segregation and then arguing that its proposal of

25.7.1994 for stock segregation remained pending with OP-2 till 31.10.1994.

e. The results of tests to bring out content analyses of sucrose, polarisation and moisture,

has been dismissed by the complainant as outcome of selective sampling. As per the

affidavit evidence of complainant, fresh sampling was done on 2.12.1994. But, its

results are called ‘patently tainted’, without showing how does it become ‘tainted’,

even if it is somewhat different from another analysis.

f. In Aug-Oct 1994, segregation of 77414 bags with re-bagging, produced 77414 bags of

50 kg sugar. In all 3870.70MTs.Even a subsequent report of 13.12.1994 from the

complainant to OP-2 shows that 33972 bags after rebaging produced 33882 bags of

sugar. Both stocks were moved out for sale. These results would go against

complainant’s claims of extensive damage to the content of externally damaged bags.

g. Admittedly, the complainant wished to undertake stock segregation at the time of their

despatch from Mangalore. But, till December 1994, only about 111,296 bags were

attended to. Another 8000 bags were segregated as part of a joint evaluation exercise.

There is nothing to show that the balance stock, about 170,704 bags, were also

segregated. Clearly, it is a case of action by the complainant which was too little and

too late.

h. In the rejoinder filed on behalf of the Complainant in September, 2009, a reference is

made to segregation and re-bagging of 34000 bags of sugar. Admittedly, re-bagging

produced 33882 standard bags of 50 kg each. But, the stocks were not despatch to

Orissa admittedly for want of a buyer. It is not the case of the Complainant that the

responsibility for disposal of stocks rested with the OP. Therefore, the complainant has

only itself to blame for its resultant predicament.

i. Claim under the policy was lodged on 11.9.1995. The settlement offer from the OPs

came only on 21.5.1998. Even if a reasonable processing time of three months is

allowed, OP’s response was delayed by two years.

j. Correspondence on record shows that high cost involved in segregation of stocks was

one of the reasons why segregation was deferred by the complainant. This cost is

admitted by OP-1 in the settlement offered, which raises a question as to why it was

not agreed earlier.

k. It needs to be observed that the claim of Rs 708.83 lakhs made by the complainant

includes interest claimed at 24%. The interest amount itself comes to Rs 326.4 lakhs.

20. To conclude, details examined above establish that some damage had already been caused

to the consignment before unloading at Mangalore Port. It is also evident that further damage

was caused by improper storage after unloading. For the latter, major part of responsibility must

lie at the door of the complainant itself. Further, the complainant has failed to establish its claim

for a large settlement of Rs 708.83 lakhs. The attempt of the insured to make external condition

of the sugar bags as the basis for determination of loss has rightly been rejected by the insurer.

However, the failure of the insurer to consider reimbursement of the cost of segregation of stocks

is held to be a deficiency of service. It was eventually accepted, though partly, in the proposed

settlement, as re-bagging cost for 197739 bags. Secondly, inordinate delay in proposing the

settlement itself is held to be another deficiency of service on the part of OP-1. We therefore

deem it just and equitable to allow the following, in addition to the settlement of Rs

44,24,963 offered by OP-1 to the complainant on 8.5.1998--

i. Compensation for delay in proposing settlement of the claim Rs eight lakhs.

ii. Compensation for delay in acceptance of the cost of segregation Rs five lakhs.

iii. Litigation cost of Rs two lakhs.

The entire amount of Rs 59,24,963 shall be paid by OP-1 within a period of three months,

computed from 90 days after presentation of the claim to the insurer on 16 th September 1995,

with interest of 8% per annum. Period of delay, if any, shall carry additional interest of 3%

per annum.

.……………Sd/-……………(J. M. MALIK, J.)PRESIDING MEMBER ……………Sd/-……………. (VINAY KUMAR)MEMBER

s./-

NATIONAL CONSUMER DISPUTES REDRESSAL COMMISSION NEW DELHI

CONSUMER COMPLAINT NO. 161 OF 2013

Anand Diamonds Pvt. Ltd. 1980, Ist floor Katra Khushal Rai, Kinari Bazar, Chandni Chowk, Delhi-110006

……Complainant (s)

Versus

1. National Insurance Co. Ltd. (A Govt. of India Undertaking), 808-809, Kailash Building , VIIIth Floor, 26, K.G. Marg, New Delhi.

2. Bank of India New Delhi Mid Corporate Branch, 37, Shahid Bhagat Singh Marg, (Near Shivaji Stadium), New Delhi.

…….Opp. Party (ies)

BEFORE:

HON’BLE MR. JUSTICE J. M. MALIK, PRESIDING MEMBER

HON’BLE DR. S. M. KANTIKAR, MEMBER

For the Complainant (s) : Mr. Rahul Sharma, Advocate

PRONOUNCED ON : 5 th JULY, 2013

ORDER

JUSTICE J. M. MALIK, PRESIDING MEMBER

1. The complainant has made a vain attempt to make bricks without straw. Dacoity/robbery

has to be proved not assumed. Can robbery of goods is a gooddefence to save yourself from

the vigours of the Law under the SARFAESI Act. We have heard the counsel for the

complainant at length.

2. The complainant, Anand Diamonds Pvt. Ltd. is owned by Mr. Rajesh Anand and his wife

Mrs. Chandni Anand. The complainant company is a manufacturer and a wholesaler

of jewellery dealing in both diamonds and gold. The business activities are transacted from their

premises No. 1980, Ist FloorKatra Khushal Rai, Kinari Bazar, Chandni Chowk, Delhi-110006.

3. The complainant approached the Bank of Inida –OP No. 2, which granted credit limits for a

credit amount of 4.5 crores. The complainant mortgaged two immovable properties in favour of

the Bank in February 2008. As agreed and stipulated, hypothecated stocks of jewellery were got

insured with the Respondent No. 1. The insurance amount went on increasing and on

23.03.2010, it was increased to Rs. 12 crores vide insurance policy.

4. On 26.03.2010, 4 unknown persons entered into the business premises of the

complainant. They showed the visiting card of M/s Sri

Ram Jewellers,Sadar Bazar, Gurgaon. When they were being shown the jewellery and other

articles they committed the robbery on gun point after trying the staff present on the side and

ensuring that none was able to raise alarm. They looted gold/gold jewellery &

diamond jewellery lying in the premises which were worth Rs. 11.41crores and its value stands

increased to Rs. 25 crores at the time of filing of this complaint. The police was informed

immediately. FIR was lodged for offences under sections 392/397 read with Section 34 of

IPC. The intimation was furnished to the National Insurance Company Limited-OP-1. The

complainant filed claim in the sum of Rs. 11.41 crores with the OP-1. However, despite several

reminders no claim was granted.

5. However, the OP continued paying the installment/interest to the OP-2 till 31.03.2011 in

the hope of claim being paid. In the meantime Bank of India –OP-2 delcared the account of the

Complainant as N.P.A. on account of non-payment on 29.09.2011. OP-2 issued a noticed dated

21.10.2011 U/S-13(2) ofSecuritisation and Reconstruction of Financial Assets and Enforcement

of Security Interest Act, 2002 (in short, ‘SARFAESI Act) thereby calling the complainant to pay

the entire amount of Rs. 1,49,76,125.03/- alongwith the interest within 60 days.

6. The police filed a closure report as the police could not find any clue about the culprits on

26.02.2011. On 17.10.2011, OP-1 filed an application U/S 173(8) of Cr.P.C. raising doubts

on the police investigation. The said application was dismissed by the learned M.M.

7. The request made by the complainant to the bank that under these circumstances he was

unable in clearing the debts and its claim will be settled when the claim is granted by the

Insurance Company was rejected. On 30.07.2012, the complainant filed a complaint against the

OPs. Notice was issued in that complaint. Thereafter, the OP-1 illegally and arbitrarily vide

letter dated 24.09.2012 repudiated the claim of the complainant, by falsely contended that no

incident of robbery took place in the shop of the complainant. The complainant desired to

withdraw the complaint so as to include the facts mentioned in the repudiation letter. The

complaint was dismissed as withdrawn with the liberty to file another complaint on the same

cause of action. Consequently, this fresh complaint has been filed.

8. We have heard the counsel for the complainant at the time of admission of this

complaint. He contended that the police investigation clearly goes to show that the above said

incident had taken place. He further explained that the investigator was an Ex-Delhi Police

Officer, also supported that the incident had taken place.

9. As a matter of fact, the repudiation letter is very crucial. It is wee bit lengthy one but to

understand this case completely it has become necessary to reproduce it fully. The letter of

repudiation dated 24.09.2012 runs as follows:-

“Kindly refer to your claim under the Jewellers Block Policy No.

354301/46/09/3700000372 regarding the loss on account of alleged robbery on

26.03.2010. The claim has been examined and considered by the competent authority of

the company in detail in terms of the Jewellers Block Insurance Policy terms, conditions

and exceptions. Various observations have been made by Sh. Vinod Sharma,

Surveyor. In his Survey Report indicating that there are many inconsistencies and

contradictions in the alleged material event, as reported by you. To recap, based on the

Surveyor’s observations as well as our own:

1. On enquiring from the other shopkeepers in the same building/ on the ground

floor/neighbourhood, it was found that nobody noticed the said looting nor were

aware of it, till the same was reported in a newspaper. Even the Police visit was

taken as a routine matter.

2. The area in which the Insured location/ establishment is located is a highly and

thickly populated area and to escape with the bags, is very difficult for any

Robber/s. No four wheeler can enter the area from a long distance, and even for

two wheelers also it is very difficult to drive in that locality/area.

3. You, as the Insured and your staff, instead of raising the alarm, went to the Police

post located at some distance on foot.

4. Nearby/neighboring Shopkeepers came to know about the event and the quantum

of loss of Rs. 8-10 Cr. from the Newspaper only, when news was published after 5

days.

5. There was no media reporting of the alleged event from 27th March till 31st March

2010. It came only in a Hindi Newspaper, ‘Nav Bharat Times’.

6. During the Surveyor’s visit to your establishment on 31st March, Mr.

Rajesh Anand was not available and the staff and father of Mr.Rajesh Anand told

that Mr. Rajesh Anand had gone to the Police Station as they wanted him for

some identification. However, when the Surveyor immediately went to the Police

Station and met the SHO and IO, they had to state that they never

called Mr.Rajesh Anand, on that day.

7. There is an increase in the sum insured of Rs.7.5 cr. immediately before the

alleged event and alleged loss. Throughout the year 2009-10, stocks as per stock

statements to Bank was more than Rs.12 Cr. However, you had opted for a sum

insured of only Rs.1.50 crores at inception, increased it by another

Rs.3.00 crores on 24.02.2010, and another Rs.7.5 Cr. on 23.3.2010, which was

suddenly increased to Rs.12 cr on 23.03.2010, just 3 days before loss. There is no

convincing justification for the said increases, particularly of Rs.7.50 crores from

your side.

8. The entire stocks from the shop were reportedly looted/taken away by the alleged

miscreants. Reportedly, not even a single piece was left. As per your statement 4

persons took away the jewellery in 4 bags. The total weight

of jewelleryreportedly stolen is approximately 50.00 Kgs. It does not appear to

be convincing that nobody noticed the 4 persons carrying 4 bags of jewellery,

weighing approx. 50.00 kg each.

9. There is a contradiction in the statement regarding masks used by the

miscreants. At the time of looting, they used mask, in between. Definitely while

escaping they must have taken out the masks. Why these were used in between the

looting is inexplicable, particularly considering the fact that they had not used

masks, while entering the shop.

10.Even in small jewellery shops, CCTV is installed. The CCTV installed by

you was reportedly having no recording facilities. It is only used to have a watch

on the entry from the staircase. At the time of incident, CCTV was not

working. There is contradiction regarding CCTV. You did not

reply/clarify/confirm properly that the CCTV in question, sans the recording

facility was not working at the time of the alleged incident.

11. As per your statement, miscreants/robbers

remained in shop for half-an-hour. However, surprisingly no customer came in

between. And you claim to be one of the leading showrooms in that area?

12. During the Surveyor’s visit, he was told that

due to firing from pistol of miscreant, glass got broken. Subsequently, in all

statements, police report, this information was changed and it is mentioned that

insured, Sh. Rajesh Anand threw the tray on one miscreant, which hit the glass

and same got broken.

13. The Investigator appointed by us (Sh. L.D.

Arora) failed to obtain information regarding stocks in possession of your

employee, Shri Makkan Lal, who was on official duty, outside the office at the

time of alleged incident. Sh. Makkan Lal was having 4 boxes of jewellery with

him, which, he was carrying for Hall Marking.

14. You could not explain why Sh. Makkan Lal, who untied the rope/s of the

person/s tied up, did not call the police from his Mobile.

15. As per the Surveyor, when he went to Police Station and met SHO and

concerned IO, during Internal/Initial investigation, at that time, they, i.e. the

Police were doubtful about the occurrence of event and quantum of loss.

16. There is a contradiction in your reply regarding how the police was

informed. As per one statement of yours, your employee Sh.

S.K. Aggarwal walked to the nearby PCO and informed the Police at

100 No. However, during the Surveyor’s visit, he was told that Sh.

S.K. Aggarwal went on foot, to the Police Station which is at about 10

minutes walking distance. Further, as per the Surveyor, and to which we also

agree, the employee concerned could have immediately gone down and

informed the police from the ground floor shops. In fact, such employee or

Mr. RajeshAnand himself could have raised an alarm, soon after being untied

right from outside the shop, even which was not done. Why such alarm was

not raised, and why the Police was not informed from the ground floor shop/s

itself, is not clear.

17. The nearby shop keepers were not even aware of such an incident, till it

was reported in a Hindi Daily, five days after.

18. Mr. Rajesh Anand did not clearly explain the number of mobile phones he

is/was having. As per the Surveyor’s information, Mr. Rajesh Anand was

having two mobile connections and mobiles.

19. You made a vague reply regarding intimation to the local Market/Traders’

Association.

20. You did not give proper reply regarding loans from Banks by the family

members/close relatives of the Director (Mr.Rajesh Anand). The Police

reportedly verbally informed the Surveyor that the Director and/or his family

members have taken various loans from different Banks and are in default.

The observations made by the Surveyor in his Survey Report, clearly show that

there are many anomalies, inconsistencies and contradictions in

the event ,as purportedly reported by you. Such an event or even attempt of threat

is not remotely possible in a plea like where the Insured

location/premises is located. There is a contradiction with regard to the incident

of gunshot also. There is no mention of the incident of gun shot in the FIR & the

final report. If there was a gunshot, the whole neighbourhood should have been

upon the shop. Even a violent breakage of the glass, should also have brought the

whole neighbourhood, down to your shop.

The absence of a CCTV or it’s non-functioning, if installed, the statement that the

glass/mirror got broken due to the throwing of a plate by an employee at one of

the perpetrators, the role of the Peon, Mr. Makkan Lal, the story about some of

the stocks having been taken for Hall Marking’, the ‘No objection’ statement

given by you, for closure of the case by the P.S. and issuance of the

Final Untrace/Closure Report, all clearly indicate that you were not keen for

proper & further investigation of the case by the Police, even which further

confirms our suspicions that the event of the alleged Robbery was stage-

managed. It is obvious that you were keen to recover the insurance claim amount

from the Insurance Company, as you were in financial distress. It is obvious that

no such alleged robbery ever took place.

The alleged event took place, within 3 days of the SI being

enhanced. Incidentally, you were maintaining stocks of high value, as much as

around, 15 crores even, but had insured only for 1.50 crores, in the previous

year’s policy and also at the inception of the renewal of the policy, which is

material to this claim.

All facts considered, including the circumstantial evidence, the inconsistencies,

the anomalies, the contradictions, we are of the considered opinion that this claim

is based on fraud/fraudulent means. Neither such an event as alleged ever took

place nor have you suffered any such loss, as claimed due to any alleged Robbery.

Condition No. 9 of the Policy contract provides:

“If the claim be fraudulent or if any fraudulent means or devices be used by the

insured or any one, acting on his behalf to obtain any benefit under this policy, or

if any destruction or damage be occasioned by the willful act or with the

connivance of the insured, all benefits under this policy shall be forfeited.”

Besides Condition No. 9, there is breach of Condition no. (ii) and condition no. 10

of the policy of insurance. The said two conditions i.e. no. (ii) and 10, deal with

‘the duty of the Insured to act, as if uninsured” and “due diligence and

reasonable dispatch” respectively.

We accordingly hereby regret our inability in unequivocal and categorical terms

to admit any liability, whatsoever, in respect of this claim of yours, in terms of the

terms and conditions of the governing Policy contract”.

10. It is surprising to note that the counsel for the Complainant could not explain all these

reasons noted in the repudiation letter. He could not deny all these facts. He was asked to

produce the Hindi Newspaper which was allegedly published five days after the incident. He

admitted that he has not attached that Hindi Newspaper with the complaint. He however, argued

that, that paper finds mention in the documents produced by him.

11. Secondly, the police also did not take any effective action. It is difficult to fathom why the

case was sent as untraced. Why the police was not able todetect , even a single clue. The

repudiation letter clearly shows that the case of the complainant is an inchoate mix of

irreconcilable opposites. Such like stories can be created at any time. Arrest of the robbers or

recovery of any article would have done the trick. No evidence was adduced, no proof, from

where these ornaments were purchased, was produced.

12. Last but not the least, it is difficult to fathom as to why Bank of India was made a party in

this case. Bank of India has nothing to do with the Insurance Policy. They have no privity of

contract with the complainant or with the Insurance Policy. It appears that in order to save

themselves from provisions of SARFAESI Act, this false case was instituted. Bank has to do

nothing with the loss. No relief has been claimed against the bank. Attempt was made to punish

them for proceedings against the complainant U/S- 13(2) of the SARFAESI Act. The Complaint

has no merit and the same is dismissed in limine.

.…..…………………………

(J. M. MALIK, J)

PRESIDING MEMBER

.…..…………………………

(S. M. KANTIKAR)

MEMBER

Jr/4

NATIONAL CONSUMER DISPUTES REDRESSAL COMMISSION NEW DELHI

REVISION PETITION NO.3916 OF 2010(From the order dated 25.02.2010 in F.A. No.749/2007 of the A.P. State Consumer Disputes Redressal Commission, Hyderabad)

SMT. P. LAXMI W/O RAMULU R/O 5-1-87/M/C, SIDDARTHNAGAR, SANGAREDDY TOWN, MEDAK DISTRICT, A.P.

.….. PETITIONER Versus

THE BRANCH MANAGER, UNITED INDIAN INSURANCE COMPANY, SANGAREDDY BRANCH, MEDAK DISTRICT, A.P.

....... RESPONDENT

BEFORE:

HON'BLE MR.JUSTICE K.S. CHAUDHARI, PRESIDING MEMBERHON’BLE MR.SURESH CHANDRA, MEMBER

For the Petitioner : Ms.Surekha Raman, Advocate

For the Respondent : Mr.Maiban N. Singh, Advocate

PRONOUNCED ON: JULY, 2013

ORDER