Embed Size (px)

Citation preview

v

Verdipapirisering og forholdet til kapitalkrav

Anders Bruun-Olsen

Nordic CFO

• History

• What are Asset Backed Securities?

• Regulation

According to the EBA, the marked differences in default rates between EU and US Securitisation are mainly due to:

1. Poor assessment and monitoring of the creditworthiness of the underlying mortgage borrowers.

2. Misaligned incentive structures for sponsors and originators (OTD model)

3. Complex securitisation and re-securitisation processes

4. Limited disclosure requirements

5. An overreliance on credit agencies

Securitisation Market Performance pre/post Crisis 2008

European securitisation performance

has demonstrated negligible defaults

pre and post crisis, compared to the

US market 0,2%

46,0%

62,0%Default rates of BBB

Securitisations

during the crisis

Prime & Subprime Prime Subprime

16,0%

0,1%

3,0%

Default rates of AAA

Securitisations

during the crisis

Prime & Subprime Prime Subprime

Source: EBA Discussion Paper on STS securitisations, European Banking Authority, 14 Oct 2014

Despite the superior performance of European ABS, the US market has recovered to pre-2008

issuance levels

Current State of the Securitisation Market

Source: AFME Capital Markets Union Measuring progress and planning for success – Sep 2018

Great difference between the values in the US

and the EU, as the EU value has not exceeded 2%

since 2007

0

100

200

300

400

500

600

700

800

900

2004 2006 2008 2010 2012 2014 2016 20180

500

1.000

3.000

1.500

2.000

2.500

3.500

4.000

4.500

Securitisation and portfolio sales

as % of outstanding loans

considering only instruments

that enable the risk associated

with loans to be transferred to

investors (without covered

bonds or retained

securitisations)10

5

10

15

20

25

2004 2006 2008 2010 2012 2014 2016 2018

%

1.Covered bonds are very rarely issued in the US, and all US securitisation issuance is placed on the public markets.

EU Total securitisation and

covered bond issuance

Strong relationship between securitisation

issuance and bank loan new issuance.

€bn

EU Total Securitisation Issuance (left hand scale)

EU Covered Bond Issuance (left hand scale)

EU Bank Loan New Issuance (right hand scale)

11/11/20196

What are Asset Backed Securities?

Three Different ABS Structures

B

A

B

A

BC

D

A

C

Traditional Traditional with Capital Relief Synthetic Capital Relief

Traditional Securitization

with sale of underlying

contracts.

Pure funding transaction

AAA Rated Class A

Retained all the risk

Traditional Securitization

with sale of underlying

contracts.

Funding and capital relief

transaction

AAA rated Class A, A Rated

Class B

Class D retained for the

economics of the deal

Capital relief obtained due

to the fact that the sold

tranches covers the

Expected (EL) and

Unexpected Losses (UL) in

the pool, which is evidence

that the risk has been sold.

Synthetic securitization

No sale of contracts

No rating

Pure Capital Relief

Class C will be retained for the

economics of the deal

Class B will cover the EL and UL

evidencing that the risk in the

portfolio has been effectively

transferred to the counterpart.

Retained by sellerSold to investors

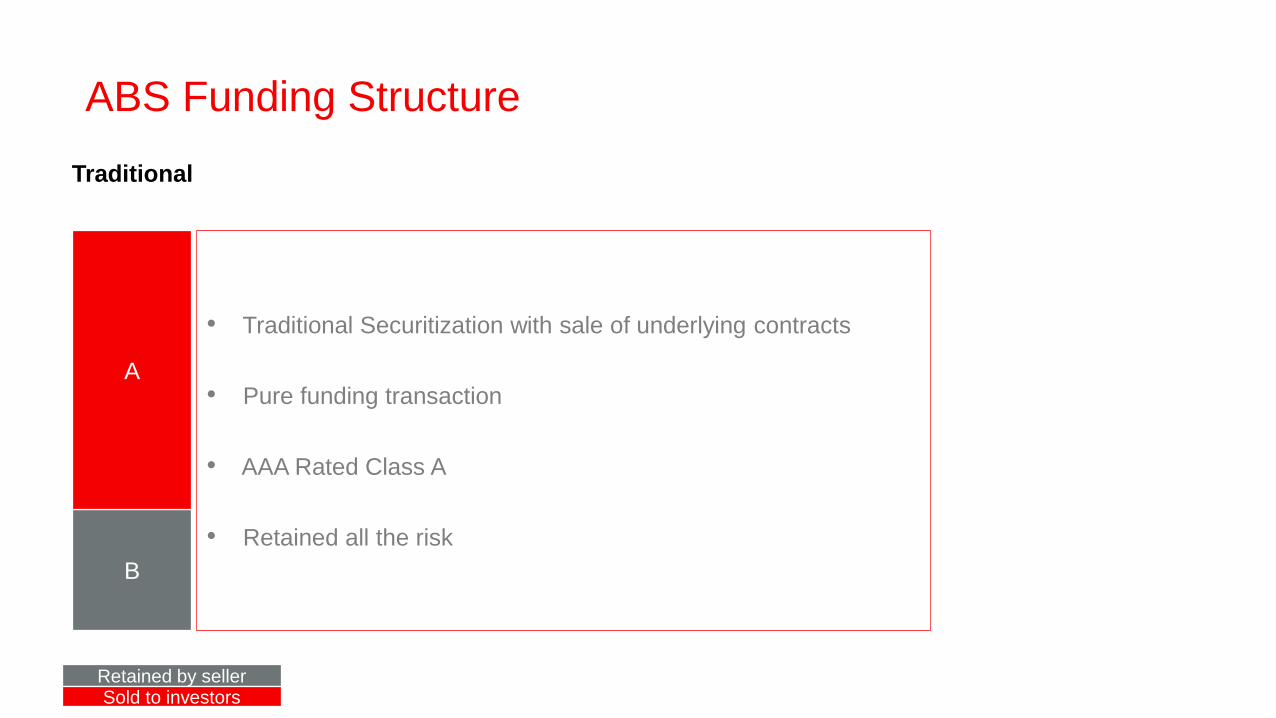

ABS Funding Structure

B

A

Traditional

• Traditional Securitization with sale of underlying contracts

• Pure funding transaction

• AAA Rated Class A

• Retained all the risk

Retained by sellerSold to investors

What are Asset Backed Securities?

9

• Asset backed Securities (ABS) are a way of converting assets with predictable cash flows (for example auto loans, consumer loans , leases, etc.) into marketable securities in order to obtain financing

• The pool of assets are sold to an Special Purpose Vehicle (SPV) which will issue securities (loans) backed by pools of assets (thereby “asset backed securities”)

• The securities are sold to institutional investors

Pool of assets Marketable securitiesIssuer (SPV)Assets Liabilities

Class A Notes

Class B Notes

InvestorsSeller (bank)

Purchase Price

Portfolio

Swap

Transaction

Account Bank

Agreement

Servicing

AgreementCollectionsAuto Loans

Notes

Issue Price

Subordinated

Loan

Servicing

Relationship

SPV

Debtors

Seller

Transaction Account

Bank

Security Trustee

& Note Trustee

Swap CounterpartySubordinated Loan

Provider

Servicer

Noteholders

Potential Parties to a Transaction

10

= bank

Credit enhancement and loss absorption

Structure of the Transaction

11

First loss

Loan portfolio

A Notes

B Notes

Excess

spread

Reserve Fund

1

Second loss2

Third loss3

Fourth loss4

Subordinated Loan

Securitisations are Cash Driven

12

Time

Outstanding loan balance

%/NOK

100%NOK 5,000 mill

20%NOK 1,000 mill

Outstanding Note balance

%/NOK

B Notes

A Notes

• Any principal payments received on the loans are

used to pay down the notes on a 1:1 basis (“pass

through”)

• The A notes are paid down in full before any

principal repayments are made on the B notes

• Consequently the amortisation profile of the loan

portfolio and notes are the same

ABS Structure with Funding and Capital Relief

B

C

D

A

Traditional with Capital Relief

• Traditional Securitization with sale of underlying contracts

• Funding and capital relief transaction

• AAA rated Class A, A Rated Class B

• Class D retained for the economics of the deal

• Capital relief obtained due to the fact that the sold tranches

covers the Expected (EL) and Unexpected Losses (UL) in the

pool, which is evidence that the risk has been sold

Retained by seller

Sold to investors

Approval of Significant Risk Transfer

Significant transaction detail must be provided to the regulator in advance of closing (pre-notification). Following closing, a final

notification must also be delivered confirming the final details of the transaction.

If the SRT tests are passed, an institution may recognise the effect of the transaction in their capital calculations immediately. However,

the regulator retains the right to reject the application of SRT at any time during the life of a transaction.

In 2017, the EBA also released a SRT Discussion Paper, which is being heavily utilised by regulators when analysing current

transactions, despite this not yet being a formal, regulatory text.

Process

Synthetic ABS Structure

A

B

C

Synthetic Capital Relief

• Synthetic securitization

• No sale of contracts

• No rating

• Pure Capital Relief

• Class C will be retained for the economics of the deal

• Class B will cover the EL and UL evidencing that the risk in

the portfolio has been effectively transferred to the

counterpart.Retained by seller

Sold to investors

Synthetic Securitisations

New EU Securitisation Regulation1: “…a securitisation where the transfer of risk is achieved by the use of credit derivatives or

guarantees, and the exposures being securitised remain exposures of the originator”.

The underlying assets are not sold / transferred into a SSPE2 – the assets remain on the balance sheet of the institution issuing the

securitisation.

It is just the credit risk of these assets that is transferred, normally via a credit default swap (CDS) or a financial guarantee.

The CDS / financial guarantee references the underlying assets, with the counterparty(ies) to these instruments incurring the credit risk

related to the assets.

Definition

1 Regulation (EU) 2017/2402 of the European Parliament and of the Council of 12 December 2017. | 2 Securitisation Special Purpose Entity.

Method of transferring risk to end investors, enabling them to share in the relating credit risk of the underlying assets.

Allows investors to gain exposure to real economy assets, such as consumer and corporate loans, without having to develop in-house

origination and servicing capabilities.

Enable issuers to reduce the risk of their balance sheets, being compensated by investors in the event credit risk losses are incurred on

the underlying assets.

As a result of the risk reduction, can also enable banks to reduce their capital requirements.

Purpose

Securitisation for Capital Relief

• Capital relief from RWA reduction.

• Costs compare favourably to cost of capital.

• No dilution of shareholders.

• Preserves client relationship.

• Recycles capital into new lending.

Regulation

State of Securitisations in EU and Santander in a nutshell

19

A post-crisis stigma is

attached to the whole

Securitisation market…

• Lack of investor due diligence

• Resulting in inability to

distinguish “good ABS” from

“bad ABS”

• Despite extremely low

European default experience

Securitisations continue

being an important part of

well-functioning financial

markets…

• Unique role of securitisation to

transfer risk (vs covered

bonds)

• Reduction of encumbrance

ratio

• Transfers risk outside of

banking system

• Allows banks to continue

lending to the real economy.

The European Commission

has taken a positive view

and aims to restart EU

Securitisation market…

• Reviving securitisation at the

centre of its plan for a Capital

Markets Union (CMU)

• The European Commission is

supporting the growth of a:

• Simple

• Transparent

• Standardised

securitisation market

Santander has played over

the last years an active role

in promoting a high quality

securitisation market

• Founding shareholder of

European Data Warehouse, a

data repository promoting

information transparency to

investors

• Founding member of PCS, a

private sector initiative which

awards quality labels to qualifying

ABS

• Active participant in EBA

working groups developing STS

and SRT criteria

• Active member of AFME, EBF

and LeaseEurope which

participated heavily in the

development of STS.

STS Legislation RequirementsSTS “Simple” Criteria

Portfolio ordinary course of business. Stable underwriting standards.

No exposures in default (very wide definition).

Debtor must have made a minimum of one payment before securitisation.

Transaction performance must not be predominantly based on proceeds from sale of the assets.

Assessment of borrowers’ creditworthiness in accordance with CCD.

Portfolio transferred via true sale with no severe claw back provisions.

No discretional active portfolio management.

Homogeneous portfolio, including prepayment characteristics.

Defined portfolio periodic payment streams and proceeds from sale.

No securitization positions in the portfolio.

Regelverk frem til 2016

• Finansieringsvirksomhetsloven hadde egne verdipapiriseringsregler som bl.a. regulerte forholdet mellom kredittinstitusjoner og spesialforetak for verdipapirisering, og unntok spesialforetakene fra krav om konsesjon, kapitaldekning og tilsyn.

• Verdipapiriseringsreglene ble opphevet 1. januar 2016. Det ble ikke vedtatt noe forbud mot verdipapirisering, men uten særlige regler for spesialforetakene anses de for å drive finansieringsvirksomhet og er underlagt alle krav som gjelder for slik virksomhet. Det innebærer i realiteten at en ikke kan drive tradisjonell verdipapirisering gjennom norske spesialforetak, ettersom det ikke er mulig fullt ut å overføre risikoen til investorene.

Forordning (EU) 2017/2402

• Fastsetter et generelt regelverk for verdipapirisering, og gjelder institusjonelle investorer, långivere, spesialforetak for verdipapirisering og kredittinstitusjoner og verdipapirforetak som etablerer verdipapirisering.

• De nye reglene skal gjelde for instrumenter som utstedes i verdipapiriseringer fra 1. januar 2019 i EU. Forordningen antas å være EØS-relevant, men er ennå ikke innlemmet i EØS-avtalen.

• EUs kapitalkravsregelverk for bank og forsikring (CRR og Solvens II) er vedtatt tilpasset verdipapiriseringsforordningen med virkning fra 1. januar 2019.

• Målet med EUs verdipapiriseringsforordning er å harmonisere reguleringen av verdipapirisering i det indre markedet, og gir derfor bare et begrenset rom for nasjonale tilpasninger. Det vil imidlertid være behov for å vurdere nødvendige konsekvenstilpasninger i norsk rett, gitt at forordningen tas inn i EØS-avtalen. Det kan også være behov for å supplere forordningen med nye nasjonale regler.