Embed Size (px)

DESCRIPTION

Vanguard Markets features unbiased, in-depth coverage of corporate and market developments across a wide range of business sectors. Every week, Vanguard Markets delivers essential business analysis and commentary on Nigerian companies, regional economies, and global markets.Vanguard Markets is published by Vanguard Media Limited in association with Customs Street Advisors Limited, a specialist communications consultancy.

Citation preview

HE PAST TWO weeks have been marked by firsts. The

market is hoping they will not be the last. On September 4, Qatar National Bank bought a 12.5 per cent stake in Ecobank Transnational Inc. (ETI) for $290 million from the Asset Management Company of Nigeria in a move that caught many una-wares. The deal is the first in-vestment by the largest Arab lender in sub-Saharan Africa. It is already present in Egypt, Libya, Mauritania, South Su-dan, Sudan and Tunisia.

Before the market could catch its breath, news filtered a few days later that the Invest-ment Company of Dubai,

one of the emirate’s sovereign wealth funds, had signed a deal with Dangote Cement to acquire 243.54m shares, the equivalent of 2.6 per cent in the country’s largest cement producer, for $300 million. It is the first deal on the conti-nent for the fund since it was founded in May 2006.

There are those who see the deals as an indication that the pre-crisis good times are here again. They have raised hopes that a spout of new money is about to be uncorked. Scep-tics, on the other hand, cau-tion that two deals, no matter the size, do not a boom make.

For the two investors, these deals have strategic connota-tions. QNB has an ambitious

plan to become the biggest bank in Africa and the Mid-dle East by 2017. The Ecobank deal fits right into that strategy by giving it exposure to 36 SSA countries in one coup.

With ICD, it signals the emir-ate’s intention to get a foothold in Africa’s biggest economy. Only a few days before the deal, it signed a Memorandum of Understanding with Arik Air ‘to

develop and expand their ex-isting commercial relationship and explore further areas of co-operation.’ Where this cryptic language will lead to is anyone’s guess but an equity investment in liquidity-challenged Arik is not an outlandish thought.

Dangote Cement is targeting to expand its Africa-wide ca-pacity from its current 35 met-ric tonnes per annum (MTA)

to 60 MTA by 2018. It controls 62 per cent of domestic cement production, and operates in 12 other countries with plans to open plants in 4 others by the end of the year. Furthermore, ‘its relatively new & efficient plants coupled with pioneer tax status in Nigeria, have ena-bled Dangote Cement to post net profit margins above 50% for the past few years aided by increasing sales volumes on the back of additional capacity and the rise in demand for ce-ment in Nigeria,’ write analysts at Imara Africa Securities.

There are analysts who in-duce that the flood of Middle Eastern cash is dumb money taken in by the spiel about Ni-geria’s potential in spite of the Boko Haram insurgency in the north-eastern part of the coun-try, and a buffeted middle class strained by the government’s focus on 2015 elections. They are mistaken.

The two companies are listed on the NSE and enjoy a trans-parency in valuation as seasoned stocks. Ecobank is one of the most researched banks on the continent, bar none, with a long record of savvy investors. QNB was advised by Morgan Stanley, a Wall Street bank reputed for its painstaking diligence.

On its side, Dangote Ce-ment’s register parades many A-list shareholders including Fidelity Management (16.3m shares), Morgan Stanley In-vestment Management (9.55m shares), JPMorgan Asset Management (UK) Ltd (6.68m shares), Goldman Sachs As-set Management Intl. Ltd.

Banks picking the macroeconomic agenda’s tab

! page VM2

Vanguard Markets | Monday, September 15, 2014 | Issue 010

FIXED INCOME & FOREX

The high rollers come to town

JAYWALKER

Source: FMDQ

T

‘See that over there on the horizon, Mr. President? Our dreams go further,’ Alhaji Aliko Dangote, chairman of Dangote Cement, says as he takes President Goodluck Jonathan on a tour of the Obajana Cement Plant, Kogi state. The company attracted $300m from the Investment Corporation of Dubai last week.

Its relatively new & efficient plants coupled with pioneer tax status in Nigeria, have enabled Dangote Cement to post net profit margins above 50% for the past few years.

- Imara Africa

Currency Central Rate

SWISS FRANC 166.0854

YEN 1.4472

CFA 0.2959

WAUA 232.0247

RIYAL 41.3885

DANISH KRONA

26.9771

SDR 232.8600

Segun Agbaje, GT Bank CEO, one of banks to have successfully adjusted to regulatory shifts

MoFr25.00

25.10

25.30

25.20

25.40

Tu We Th Fr

CNY/N

MoFr200.0

200.5

201.5

201.0

202.0200.8495

Tu We Th Fr

Euro/N

MoFr250.0

251.0

253.0

252.0

254.0252.0011

Tu We Th Fr

£/N

MoFr155.0

155.1

155.3

155.2

155.4155.24

Tu We Th Fr

$/N

FOREX RATES

InsideThis week Spotlight is on the Onyekachi Onubogu, executive director, Promasidor.

! Page VM6

! Page VM2

FOREIGN INVESTMENT INFLOWS

FGN Bonds & TBills FGN BondsTreasury Bills

29/08

120B

96B

72B

48B

24B

003/09 08/09 11/09

NITTY

29/08

12.00

11.60

11.20

10.80

10.40

10.0003/09 08/09 11/09

1M2M

3M6M

9M12M

NIBOR

29/08

15.00

14.00

13.00

12.00

11.00

10.0003/09 08/09 11/09

O/N1M

3M6M

FX ($/N)

29/08

163.0

162.6

162.2

161.8

161.4

161.003/09 08/09 11/09

BidAsk

Source: Africawatchonline.com

25.304

HEN ANALYSTS at Renaissance Capital, an invest-

ment bank, speak, the market listens. Last week they spoke.

The firm has gained a wide fan base for the relevance of its research reports, and for want of a better word, speed at which its analysts churn them out. They excel in dicing up events and trends into eas-ily digestible and actionable chunks for readers. On Thurs-day, it published a report, Ni-gerian banks: The cost of macro stability that had this as its problem statement: ‘why have Nigerian banks struggled to deliver returns comparable with those of their sub-Saha-ran Africa banking peers over the past few years?’

The answer, in their view, is simple. Taking a sampling of key banking regulations such as capitalization ratios, net open position limits, cash reserve ratios, and liquidity ratios, it will be seen that Ni-gerian banks operate in what is, arguably, the toughest op-

erational and regulatory envi-ronment on the continent.

The paradox is that these measures, introduced during the governorship of Sanusi Lamido Sanusi at the Central Bank of Nigeria, to restore investor confidence, are now eating up returns. This is a classic case of you cannot eat your cake and have it.

Other than this, the CBN’s actions were driven by the dictates of its macroeconomic management mandate. Since the crash, the CBN has been singularly focused ‘on ex-

change rate stability and low inflation using a combination of measures, including hiking the MPR and CRR, tightening banks’ net open position limits and introducing multiple op-erational measures to keep the exchange rate in check,’ writes RenCap.

This has been largely suc-cessful. In comparison with its continental peers, since 2009 the naira has depreci-ated by 9% against the dol-lar, while the Kenyan shilling fell 17 per cent, South African rand dropped 45 per cent, and

the Ghanaian cedi lost 166 per cent.

On the inflation score, the country’s inflation fell from 14.3 per cent in January 2010 to 8.3 per cent in July 2014. In Ghana, inflation climbed from 10 per cent in January 2013 to 15.3 per cent in July 2014, and in Kenya, it leapt from 4.5 per cent in January 2010 to 8.4 per cent by August 2014.

The CBN’s macroeconomic successes have come at a cost for Nigerian banks.

Watching all these big and small regulatory mice nib-bling away at banks’ profits, the casual observer is tempted to agree with Ladi Balo-gun, group chief executive of FCMB that ‘banking will become a utility – very use-ful and helpful to people with stable but thin margins.’ His advice? ‘Non-bank financial services sector is where the

Obiora [email protected]

BUSINESSVM2

JAYWALKER

FOREIGN INVESTMENT INFLOWS

VM | Monday, September 15, 2014 | Issue 010

Banks picking the tab for the CBN’s macroeconomic agenda

W

(4.74m shares), and Black-Rock Fund Advisors (4.33m shares). If you can fool them, you can fool anyone.

Other deals in the offing in-clude an option for Nedbank, a South African lender, to take a 20 per cent stake in ETI by November 25. The potential deal is valued at more than $500 million. Nedbank has an option to convert a $285m loan made in 2011 to ETI into an 11 per cent stake. It can also take up a second subscription right that would give it an additional 9 per cent in the pan-African bank. This would catapult it to ETI’s biggest shareholder.

There is speculation in some quarters that with QNB’s entry into Ecobank’s share register, Nedbank could be reluctant to proceed. This is unlikely. Ned-bank would be pressed to find another lender that would al-

low it grow its footprint on such a scale across Africa. A possible candidate is the United Bank for Africa. It has operations in 19 African countries. But this would be a costly, farfetched and lengthy process fraught with significant risks.

Compared to its SA peers, Nedbank generates only 3 per cent of its income outside South Africa. Standard Bank, Barclays, and FirstRand make 30 per cent, 20 per cent, and 9 per cent of their earnings outside South Africa. ‘If we execute against our

equity with Ecobank that will leapfrog us into a whole new world,’ said Graeme Auret, managing executive of corpo-rate banking at Nedbank.

Moreover, the QNB deal is a vote of confidence in the leadership of Albert Essien, the ETI chief executive, and in consequence, Nedbank’s wis-dom in exercising the option. It is almost impossible to see Nedbank walking away with all these considerations in mind.

One likely entrant to the Ni-gerian deal space is Norges

Bank Investment Manage-ment, Norway’s $893b sov-ereign wealth fund. In June, Yngve Slyngstad, the fund’s chief executive, promised that NBIM will ratchet up its ex-posure to ‘frontier markets’ as it seeks to include ‘quite a few countries where we’re not in-vested in Africa.’ Presently, it has investments in South Af-rica, Egypt, Morocco, and Ken-ya. None is reported in Nigeria.

A recurring presence in both ETI and Dangote Cement is Public Investment Cor-

poration, South Africa’s big-gest pension fund manager. In April 2012, it paid $250 million for 3.125m shares in ETI giving it a stake of 19.58 per cent. It is the bank’s largest shareholder. One year later, in June 2013, it paid $289.3m for 1.5 per cent of Dangote Cement. PIC says that it is ready to invest its war chest of $7 billion in more listed stocks in the consumer, infrastructure, telecommuni-cations and agribusiness sec-tors across the continent, and Nigeria is a prime destination.

This is not to say that the money will keep rushing in. Only last month, Actis, a pan-emerging markets private eq-uity firm, exited its investment in Diamond Bank. The Lon-don-based firm acquired 19.1 per cent of the Nigerian lender for $134 million in 2007. In July, Emerging Capital Partners, a buyout firm that has raised more than $2 bil-

lion for investments on the continent, said that its Africa Fund II was actively ‘exploring’ the sale of C-Re Holding Ltd., which owns about 50.6 percent of the Continental Reinsur-ance, an NSE-listed insurance company. A month earlier, in June, reports surfaced that Mubadala Development Company, an Abu Dhabi sov-ereign wealth fund, is seeking a buyer for its 30 per cent stake in Etisalat Nigeria. Mubadala bought its GSM license for $400 million in 2008.

There is the likelihood that other big rollers are watching on the side lines to see what happens with the Nigerian elec-tions in February next year. If the country gets its presidential election slated for Valentine’s Day next year right the love affair is sealed. The only differ-ence will be that the bride price, read valuations, would have gone way, way up. ;

The high rollers come to townW Continued from Page VM1

The paradox is that these measures, introduced during the governorship of Sanusi Lamido Sanusi at the Central Bank of Nigeria, to restore investor confidence, are now eating up returns.

CRR on public sector deposits increased from 50% to 75%

In line with Pillar I of the Basel II Accords, CBN issues guidance notes specifying how banks should quantify the risk weighted assets for the purpose of determining regulatory capital

Cashless Nigeria policy extended to Abia, Anambra, Kano, Ogun and Rivers States, and Abuja FCT

Banks sign a Trust Fund Deed with CBN to contribute 0.5% of their total assets and a further 0.5% of 33% of their off balance sheet items at the end of each year to an AMCON sinking fund. Previously, they contributed 0.3% on total assets only

Imposition of 50% CRR on public sector deposits to be applied on federal, states’, and local governments’ deposits as well as on those of ministries, departments, and agencies

Gradual phase-out of cost of transfer (COT) applied to customer-induced debit transactions from N3/N1,000 in 2013, N2/N1,000 in 2014, N1//N1,000 in 2015 and free of charge from 2016

CRR increased from 8% to 12%

Introduction of service charges as part of the imple-mentation of a Phase 1 of Cashless Nigeria policy with Cashless Lagos

CRR raised from 4% to 8%

Cash reserve requirement (CRR) increased from 2% to 4%

24 banks sign MoU with CBN to contribute 0.3% of their total assets annually into a Banking Sector Resolution Cost Trust Fund. Each bank’s value of assets is calculated as at the date of their audited financial statement for the immediate preceding financial year

2014

2013

2012

2011

Source: Central Bank of Nigeria

growth will be, although ini-tially at a much smaller scale in areas such as microfinance, asset management, broker-

age, advisory services, capital markets, and insurance,’ he divined. He is not far from the truth. ;

3 Years of Material Regulatory Adjustments

Source: Renaissance Capital

Return on Average Equity (RoAE) for Sub-Saharan Africa banking systems

0%2011 2012 2013 1H14

5%

10%

15%

20%

35%

40%

25%

30%

45%

50%

Data visualisation by Publican Media

NigeriaKenyaGhana

D

J

NOSAJJMAMFJ

DNOSAJJMAMFJ

DNOSAJJMAMFJ

Data visualisation by Publican Media

2012 2013 2014

DANGCEM49B

DANGCEM, 12B

UBN16B

MANSARD12B

Biggest single day trades on the NSE (N)

UBN9B

DANGFLOUR30B

DANGCEM46B

DANGCEM9B ASHAKACEM

41B

ETI35B

Source: Nigerian Stock Exchange

4%

28%

20%

44% 45%47%

29%26% 26%

20%18% 18%

LEGEND

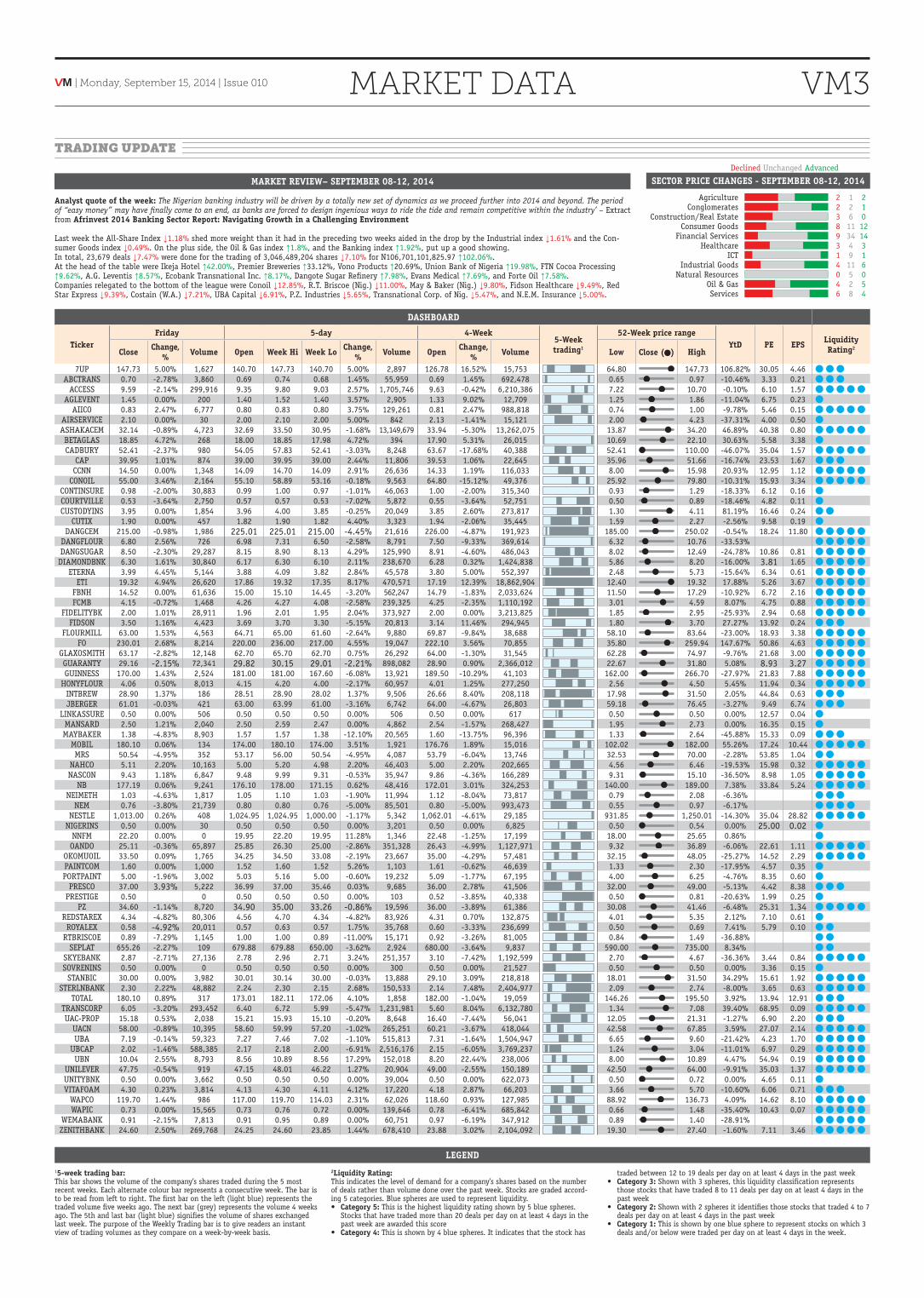

15-week trading bar:This bar shows the volume of the company’s shares traded during the 5 most recent weeks. Each alternate colour bar represents a consecutive week. The bar is to be read from left to right. The first bar on the left (light blue) represents the traded volume five weeks ago. The next bar (grey) represents the volume 4 weeks ago. The 5th and last bar (light blue) signifies the volume of shares exchanged last week. The purpose of the Weekly Trading bar is to give readers an instant view of trading volumes as they compare on a week-by-week basis.

2Liquidity Rating: This indicates the level of demand for a company’s shares based on the number of deals rather than volume done over the past week. Stocks are graded accord-ing 5 categories. Blue spheres are used to represent liquidity. • Category 5: This is the highest liquidity rating shown by 5 blue spheres.

Stocks that have traded more than 20 deals per day on at least 4 days in the past week are awarded this score

• Category 4: This is shown by 4 blue spheres. It indicates that the stock has

traded between 12 to 19 deals per day on at least 4 days in the past week• Category 3: Shown with 3 spheres, this liquidity classification represents

those stocks that have traded 8 to 11 deals per day on at least 4 days in the past week

• Category 2: Shown with 2 spheres it identifies those stocks that traded 4 to 7 deals per day on at least 4 days in the past week

• Category 1: This is shown by one blue sphere to represent stocks on which 3 deals and/or below were traded per day on at least 4 days in the week.

SECTOR PRICE CHANGES - SEPTEMBER 08-12, 2014MARKET REVIEW– SEPTEMBER 08-12, 2014

TRADING UPDATE

DASHBOARD

TickerFriday 5-day 4-Week

5-Week trading1

52-Week price rangeYtD PE EPS Liquidity

Rating2Close Change, % Volume Open Week Hi Week Lo Change,

% Volume Open Change, % Volume Low Close ( ) High

7UP 147.73 5.00% 1,627 140.70 147.73 140.70 5.00% 2,897 126.78 16.52% 15,753 64.80 147.73 106.82% 30.05 4.46 ABCTRANS 0.70 -2.78% 3,860 0.69 0.74 0.68 1.45% 55,959 0.69 1.45% 692,478 0.65 0.97 -10.46% 3.33 0.21

ACCESS 9.59 -2.14% 299,916 9.35 9.80 9.03 2.57% 1,705,746 9.63 -0.42% 6,210,386 7.22 10.70 -0.10% 6.10 1.57 AGLEVENT 1.45 0.00% 200 1.40 1.52 1.40 3.57% 2,905 1.33 9.02% 12,709 1.25 1.86 -11.04% 6.75 0.23

AIICO 0.83 2.47% 6,777 0.80 0.83 0.80 3.75% 129,261 0.81 2.47% 988,818 0.74 1.00 -9.78% 5.46 0.15 AIRSERVICE 2.10 0.00% 30 2.00 2.10 2.00 5.00% 842 2.13 -1.41% 15,121 2.00 4.23 -37.31% 4.00 0.50ASHAKACEM 32.14 -0.89% 4,723 32.69 33.50 30.95 -1.68% 13,149,679 33.94 -5.30% 13,262,075 13.87 34.20 46.89% 40.38 0.80 BETAGLAS 18.85 4.72% 268 18.00 18.85 17.98 4.72% 394 17.90 5.31% 26,015 10.69 22.10 30.63% 5.58 3.38CADBURY 52.41 -2.37% 980 54.05 57.83 52.41 -3.03% 8,248 63.67 -17.68% 40,388 52.41 110.00 -46.07% 35.04 1.57

CAP 39.95 1.01% 874 39.00 39.95 39.00 2.44% 11,806 39.53 1.06% 22,645 35.96 51.66 -16.74% 23.53 1.67 CCNN 14.50 0.00% 1,348 14.09 14.70 14.09 2.91% 26,636 14.33 1.19% 116,033 8.00 15.98 20.93% 12.95 1.12

CONOIL 55.00 3.46% 2,164 55.10 58.89 53.16 -0.18% 9,563 64.80 -15.12% 49,376 25.92 79.80 -10.31% 15.93 3.34 CONTINSURE 0.98 -2.00% 30,883 0.99 1.00 0.97 -1.01% 46,063 1.00 -2.00% 315,340 0.93 1.29 -18.33% 6.12 0.16COURTVILLE 0.53 -3.64% 2,750 0.57 0.57 0.53 -7.02% 5,872 0.55 -3.64% 52,751 0.50 0.89 -18.46% 4.82 0.11CUSTODYINS 3.95 0.00% 1,854 3.96 4.00 3.85 -0.25% 20,049 3.85 2.60% 273,817 1.30 4.11 81.19% 16.46 0.24

CUTIX 1.90 0.00% 457 1.82 1.90 1.82 4.40% 3,323 1.94 -2.06% 35,445 1.59 2.27 -2.56% 9.58 0.19DANGCEM 215.00 -0.98% 1,986 225.01 225.01 215.00 -4.45% 21,616 226.00 -4.87% 191,923 185.00 250.02 -0.54% 18.24 11.80

DANGFLOUR 6.80 2.56% 726 6.98 7.31 6.50 -2.58% 8,791 7.50 -9.33% 369,614 6.32 10.76 -33.53% DANGSUGAR 8.50 -2.30% 29,287 8.15 8.90 8.13 4.29% 125,990 8.91 -4.60% 486,043 8.02 12.49 -24.78% 10.86 0.81 DIAMONDBNK 6.30 1.61% 30,840 6.17 6.30 6.10 2.11% 238,670 6.28 0.32% 1,424,838 5.86 8.20 -16.00% 3.81 1.65

ETERNA 3.99 4.45% 5,144 3.88 4.09 3.82 2.84% 45,578 3.80 5.00% 552,397 2.48 5.73 -15.64% 6.34 0.61 ETI 19.32 4.94% 26,620 17.86 19.32 17.35 8.17% 470,571 17.19 12.39% 18,862,904 12.40 19.32 17.88% 5.26 3.67

FBNH 14.52 0.00% 61,636 15.00 15.10 14.45 -3.20% 562,247 14.79 -1.83% 2,033,624 11.50 17.29 -10.92% 6.72 2.16 FCMB 4.15 -0.72% 1,468 4.26 4.27 4.08 -2.58% 239,325 4.25 -2.35% 1,110,192 3.01 4.59 8.07% 4.75 0.88

FIDELITYBK 2.00 1.01% 28,911 1.96 2.01 1.95 2.04% 373,927 2.00 0.00% 3,213,825 1.85 2.95 -25.93% 2.94 0.68 FIDSON 3.50 1.16% 4,423 3.69 3.70 3.30 -5.15% 20,813 3.14 11.46% 294,945 1.80 3.70 27.27% 13.92 0.24

FLOURMILL 63.00 1.53% 4,563 64.71 65.00 61.60 -2.64% 9,880 69.87 -9.84% 38,688 58.10 83.64 -23.00% 18.93 3.38 FO 230.01 2.68% 8,214 220.00 236.00 217.00 4.55% 19,047 222.10 3.56% 70,855 35.80 259.94 147.67% 50.86 4.63

GLAXOSMITH 63.17 -2.82% 12,148 62.70 65.70 62.70 0.75% 26,292 64.00 -1.30% 31,545 62.28 74.97 -9.76% 21.68 3.00 GUARANTY 29.16 -2.15% 72,341 29.82 30.15 29.01 -2.21% 898,082 28.90 0.90% 2,366,012 22.67 31.80 5.08% 8.93 3.27 GUINNESS 170.00 1.43% 2,524 181.00 181.00 167.60 -6.08% 13,921 189.50 -10.29% 41,103 162.00 266.70 -27.97% 21.83 7.88

HONYFLOUR 4.06 0.50% 8,013 4.15 4.20 4.00 -2.17% 60,957 4.01 1.25% 277,250 2.56 4.50 5.45% 11.94 0.34 INTBREW 28.90 1.37% 186 28.51 28.90 28.02 1.37% 9,506 26.66 8.40% 208,118 17.98 31.50 2.05% 44.84 0.63 JBERGER 61.01 -0.03% 421 63.00 63.99 61.00 -3.16% 6,742 64.00 -4.67% 26,803 59.18 76.45 -3.27% 9.49 6.74

LINKASSURE 0.50 0.00% 506 0.50 0.50 0.50 0.00% 506 0.50 0.00% 617 0.50 0.50 0.00% 12.57 0.04MANSARD 2.50 1.21% 2,040 2.50 2.59 2.47 0.00% 4,862 2.54 -1.57% 268,427 1.95 2.73 0.00% 16.35 0.15MAYBAKER 1.38 -4.83% 8,903 1.57 1.57 1.38 -12.10% 20,565 1.60 -13.75% 96,396 1.33 2.64 -45.88% 15.33 0.09

MOBIL 180.10 0.06% 134 174.00 180.10 174.00 3.51% 1,921 176.76 1.89% 15,016 102.02 182.00 55.26% 17.24 10.44 MRS 50.54 -4.95% 352 53.17 56.00 50.54 -4.95% 4,087 53.79 -6.04% 13,746 32.53 70.00 -2.28% 53.85 1.04

NAHCO 5.11 2.20% 10,163 5.00 5.20 4.98 2.20% 46,403 5.00 2.20% 202,665 4.56 6.46 -19.53% 15.98 0.32 NASCON 9.43 1.18% 6,847 9.48 9.99 9.31 -0.53% 35,947 9.86 -4.36% 166,289 9.31 15.10 -36.50% 8.98 1.05

NB 177.19 0.06% 9,241 176.10 178.00 171.15 0.62% 48,416 172.01 3.01% 324,253 140.00 189.00 7.38% 33.84 5.24 NEIMETH 1.03 -4.63% 1,817 1.05 1.10 1.03 -1.90% 11,994 1.12 -8.04% 73,817 0.79 2.08 -6.36%

NEM 0.76 -3.80% 21,739 0.80 0.80 0.76 -5.00% 85,501 0.80 -5.00% 993,473 0.55 0.97 -6.17% NESTLE 1,013.00 0.26% 408 1,024.95 1,024.95 1,000.00 -1.17% 5,342 1,062.01 -4.61% 29,185 931.85 1,250.01 -14.30% 35.04 28.82

NIGERINS 0.50 0.00% 30 0.50 0.50 0.50 0.00% 3,201 0.50 0.00% 6,825 0.50 0.54 0.00% 25.00 0.02NNFM 22.20 0.00% 0 19.95 22.20 19.95 11.28% 1,346 22.48 -1.25% 17,199 18.00 25.65 0.86%OANDO 25.11 -0.36% 65,897 25.85 26.30 25.00 -2.86% 351,328 26.43 -4.99% 1,127,971 9.32 36.89 -6.06% 22.61 1.11

OKOMUOIL 33.50 0.09% 1,765 34.25 34.50 33.08 -2.19% 23,667 35.00 -4.29% 57,481 32.15 48.05 -25.27% 14.52 2.29 PAINTCOM 1.60 0.00% 1,000 1.52 1.60 1.52 5.26% 1,103 1.61 -0.62% 46,639 1.33 2.30 -17.95% 4.57 0.35PORTPAINT 5.00 -1.96% 3,002 5.03 5.16 5.00 -0.60% 19,232 5.09 -1.77% 67,195 4.00 6.25 -4.76% 8.35 0.60

PRESCO 37.00 3.93% 5,222 36.99 37.00 35.46 0.03% 9,685 36.00 2.78% 41,506 32.00 49.00 -5.13% 4.42 8.38 PRESTIGE 0.50 0 0.50 0.50 0.50 0.00% 103 0.52 -3.85% 40,338 0.50 0.81 -20.63% 1.99 0.25

PZ 34.60 -1.14% 8,720 34.90 35.00 33.26 -0.86% 19,596 36.00 -3.89% 61,386 30.08 41.46 -6.48% 25.31 1.34 REDSTAREX 4.34 -4.82% 80,306 4.56 4.70 4.34 -4.82% 83,926 4.31 0.70% 132,875 4.01 5.35 2.12% 7.10 0.61ROYALEX 0.58 -4.92% 20,011 0.57 0.63 0.57 1.75% 35,768 0.60 -3.33% 236,699 0.50 0.69 7.41% 5.79 0.10

RTBRISCOE 0.89 -7.29% 1,145 1.00 1.00 0.89 -11.00% 15,171 0.92 -3.26% 81,005 0.84 1.49 -36.88% SEPLAT 655.26 -2.27% 109 679.88 679.88 650.00 -3.62% 2,924 680.00 -3.64% 9,837 590.00 735.00 8.34%

SKYEBANK 2.87 -2.71% 27,136 2.78 2.96 2.71 3.24% 251,357 3.10 -7.42% 1,192,599 2.70 4.67 -36.36% 3.44 0.84 SOVRENINS 0.50 0.00% 0 0.50 0.50 0.50 0.00% 300 0.50 0.00% 21,527 0.50 0.50 0.00% 3.36 0.15STANBIC 30.00 0.00% 3,982 30.01 30.14 30.00 -0.03% 13,888 29.10 3.09% 218,818 18.01 31.50 34.29% 15.61 1.92

STERLNBANK 2.30 2.22% 48,882 2.24 2.30 2.15 2.68% 150,533 2.14 7.48% 2,404,977 2.09 2.74 -8.00% 3.65 0.63 TOTAL 180.10 0.89% 317 173.01 182.11 172.06 4.10% 1,858 182.00 -1.04% 19,059 146.26 195.50 3.92% 13.94 12.91

TRANSCORP 6.05 -3.20% 293,452 6.40 6.72 5.99 -5.47% 1,231,981 5.60 8.04% 6,132,780 1.34 7.08 39.40% 68.95 0.09 UAC-PROP 15.18 0.53% 2,038 15.21 15.93 15.10 -0.20% 8,648 16.40 -7.44% 56,041 12.05 21.31 -1.27% 6.90 2.20

UACN 58.00 -0.89% 10,395 58.60 59.99 57.20 -1.02% 265,251 60.21 -3.67% 418,044 42.58 67.85 3.59% 27.07 2.14 UBA 7.19 -0.14% 59,323 7.27 7.46 7.02 -1.10% 515,813 7.31 -1.64% 1,504,947 6.65 9.60 -21.42% 4.23 1.70

UBCAP 2.02 -1.46% 588,385 2.17 2.18 2.00 -6.91% 2,516,176 2.15 -6.05% 3,769,237 1.24 3.04 -11.01% 6.97 0.29 UBN 10.04 2.55% 8,793 8.56 10.89 8.56 17.29% 152,018 8.20 22.44% 238,006 8.00 10.89 4.47% 54.94 0.19

UNILEVER 47.75 -0.54% 919 47.15 48.01 46.22 1.27% 20,904 49.00 -2.55% 150,189 42.50 64.00 -9.91% 35.03 1.37 UNITYBNK 0.50 0.00% 3,662 0.50 0.50 0.50 0.00% 39,004 0.50 0.00% 622,073 0.50 0.72 0.00% 4.65 0.11VITAFOAM 4.30 0.23% 3,814 4.13 4.30 4.11 4.12% 17,220 4.18 2.87% 66,203 3.66 5.70 -10.60% 6.06 0.71

WAPCO 119.70 1.44% 986 117.00 119.70 114.03 2.31% 62,026 118.60 0.93% 127,985 88.92 136.73 4.09% 14.62 8.10 WAPIC 0.73 0.00% 15,565 0.73 0.76 0.72 0.00% 139,646 0.78 -6.41% 685,842 0.66 1.48 -35.40% 10.43 0.07

WEMABANK 0.91 -2.15% 7,813 0.91 0.95 0.89 0.00% 60,751 0.97 -6.19% 347,912 0.89 1.40 -28.91% ZENITHBANK 24.60 2.50% 269,768 24.25 24.60 23.85 1.44% 678,410 23.88 3.02% 2,104,092 19.30 27.40 -1.60% 7.11 3.46

Analyst quote of the week: The Nigerian banking industry will be driven by a totally new set of dynamics as we proceed further into 2014 and beyond. The period of “easy money” may have finally come to an end, as banks are forced to design ingenious ways to ride the tide and remain competitive within the industry’ – Extract from Afrinvest 2014 Banking Sector Report: Navigating Growth in a Challenging Environment

Last week the All-Share Index ↓1.18% shed more weight than it had in the preceding two weeks aided in the drop by the Industrial index ↓1.61% and the Con-sumer Goods index ↓0.49%. On the plus side, the Oil & Gas index ↑1.8%, and the Banking index ↑1.92%, put up a good showing. In total, 23,679 deals ↓7.47% were done for the trading of 3,046,489,204 shares ↓7.10% for N106,701,101,825.97 ↑102.06%.At the head of the table were Ikeja Hotel ↑42.00%, Premier Breweries ↑33.12%, Vono Products ↑20.69%, Union Bank of Nigeria ↑19.98%, FTN Cocoa Processing ↑9.62%, A.G. Leventis ↑8.57%, Ecobank Transnational Inc. ↑8.17%, Dangote Sugar Refinery ↑7.98%, Evans Medical ↑7.69%, and Forte Oil ↑7.58%. Companies relegated to the bottom of the league were Conoil ↓12.85%, R.T. Briscoe (Nig.) ↓11.00%, May & Baker (Nig.) ↓9.80%, Fidson Healthcare ↓9.49%, Red Star Express ↓9.39%, Costain (W.A.) ↓7.21%, UBA Capital ↓6.91%, P.Z. Industries ↓5.65%, Transnational Corp. of Nig. ↓5.47%, and N.E.M. Insurance ↓5.00%.

Agriculture 2 1 2Conglomerates 2 2 1

Construction/Real Estate 3 6 0Consumer Goods 8 11 12

Financial Services 9 34 14Healthcare 3 4 3

ICT 1 9 1Industrial Goods 4 11 6

Natural Resources 0 5 0Oil & Gas 4 2 5Services 6 8 4

MARKET DATA VM3VM | Monday, September 15, 2014 | Issue 010

Declined Unchanged Advanced

MARKET SNAPSHOT

3-MONTH PRICE TREND OF BELLWETHER STOCKS

LEGEND

ACCESS 9.5910.707.22

YtD -0.01-0.10%

-0.21-2.14%

0.242.57%3M 1W

PE 6.100.24

June July August08/09

M T W T F

12/09

ASHAKACEM 32.1434.2013.87

YtD 10.2646.89%

5.1419.04%

-0.55-1.68%3M 1W

PE 40.380.55

June July August08/09

M T W T F

12/09

CADBURY 52.41110.0052.41

YtD -44.77-46.07%

-25.39-32.63%

-1.64-3.03%3M 1W

PE 35.041.64

June July August08/09

M T W T F

12/09

CAP 39.9551.6635.96

YtD -8.03-16.74%

0.962.46%

0.952.44%3M 1W

PE 23.530.95

June July August08/09

M T W T F

12/09

CCNN 14.5015.988.00

YtD 2.5120.93%

3.8035.51%

0.412.91%3M 1W

PE 12.950.41

June July August08/09

M T W T F

12/09

CONTINSURE 0.981.290.93

YtD -0.22-18.33%

-0.05-4.85%

-0.01-1.01%3M 1W

PE 6.130.01

June July August08/09

M T W T F

12/09

FCMB 4.154.593.01

YtD 0.318.07%

0.02 0.48%

-0.11-2.58%3M 1W

PE 4.750.11

June July August08/09

M T W T F

12/09

GUARANTY 29.1631.8022.67

YtD 1.415.08%

-2.11-6.75%

-0.66-2.21%3M 1W

PE 8.930.66

June July August08/09

M T W T F

12/09

MANSARD 2.502.731.95

YtD 0.000.00%

0.000.00%

0.000.00%3M 1W

PE 16.350.00

June July August08/09

M T W T F

12/09

OANDO 25.1136.899.32

YtD -1.62-6.06%

5.1125.55%

-0.74-2.86%3M 1W

PE 22.610.74

June July August08/09

M T W T F

12/09

STANBIC 30.0031.5018.01

YtD 7.6634.29%

3.4512.99%

-0.01-0.03%3M 1W

PE 15.610.01

June July August08/09

M T W T F

12/09

UBA 7.199.606.65

YtD -1.96-21.42%

-0.95-11.67%

-0.08-1.10%3M 1W

PE 4.230.08

June July August08/09

M T W T F

12/09

DANGCEM 215.00250.02185.00

YtD -1.16-0.54%

-9.25-4.12%

-10.01-4.45%3M 1W

PE 18.2410.01

June July August08/09

M T W T F

12/09

FIDELITYBK 2.002.951.85

YtD -0.70-25.93%

-0.06-2.91%

0.042.04%3M 1W

PE 2.940.04

June July August08/09

M T W T F

12/09

GUINNESS 170.00266.70162.00

YtD -66.01-27.97%

-10.73 -5.94%

-11.00-6.08%3M 1W

PE 21.8311.00

June July August08/09

M T W T F

12/09

MOBIL 180.10182.00102.02

YtD 64.1055.26%

53.0441.74%

6.103.51%3M 1W

PE 17.246.10

June July August08/09

M T W T F

12/09

OKOMUOIL 33.5048.0532.15

YtD -11.33-25.27%

-0.33-0.98%

-0.75-2.19%3M 1W

PE 14.520.75

June July August08/09

M T W T F

12/09

TOTAL 180.10195.50146.26

YtD 6.803.92%

8.815.14%

7.094.10%3M 1W

PE 13.947.09

June July August08/09

M T W T F

12/09

UNILEVER 47.7564.0042.50

YtD -5.25-9.91%

-2.74-5.43%

0.601.27%3M 1W

PE 35.030.60

June July August08/09

M T W T F

12/09

DIAMONDBNK 6.308.205.86

YtD -1.20-16.00%

-0.42-6.25%

0.13 2.11%3M 1W

PE 3.810.13

June July August08/09

M T W T F

12/09

FLOURMILL 63.0083.6458.10

YtD -18.82-23.00%

-7.00-10.00%

-1.71-2.64%3M 1W

PE 18.941.71

June July August08/09

M T W T F

12/09

HONYFLOUR 4.064.502.56

YtD 0.215.45%

-0.09-2.17%

-0.09-2.17%3M 1W

PE 11.940.09

June July August08/09

M T W T F

12/09

NASCON 9.4315.109.31

YtD -5.42-36.50%

-2.17-18.71%

-0.05-0.53%3M 1W

PE 8.980.05

June July August08/09

M T W T F

12/09

PRESCO 37.0049.0032.00

YtD -2.00-5.13%

0.431.18%

0.010.03%3M 1W

PE 4.420.01

June July August08/09

M T W T F

12/09

UACN 58.0067.8542.58

YtD 2.013.59%

-2.00-3.33%

-0.60-1.02%3M 1W

PE 27.070.60

June July August08/09

M T W T F

12/09

WAPCO 119.70136.7388.92

YtD 4.70

4.09%9.20

8.33%2.70

2.31%3M 1W

PE 14.622.70

June July August08/09

M T W T F

12/09

ETI 19.3219.3212.40

YtD 2.9317.88%

2.5215.00%

1.468.17%3M 1W

PE 5.261.46

June July August08/09

M T W T F

12/09

FO 230.01259.9435.80

YtD 137.14147.67%

4.371.94%

10.014.55%3M 1W

PE 50.8610.01

June July August08/09

M T W T F

12/09

INTBREW 28.9031.5017.98

YtD 0.582.05%

2.8110.77%

0.391.37%3M 1W

PE 44.840.39

June July August08/09

M T W T F

12/09

NB 177.19189.00140.00

YtD 12.187.38%

2.201.26%

1.090.62%3M 1W

PE 33.841.09

June July August08/09

M T W T F

12/09

PZ 34.6041.4630.08

YtD -2.40-6.48%

-3.90-10.13%

-0.30-0.86%3M 1W

PE 25.310.30

June July August08/09

M T W T F

12/09

UAC-PROP 15.1821.3112.05

YtD -0.20-1.27%

-2.42-13.75%

-0.03-0.20%3M 1W

PE 6.900.03

June July August08/09

M T W T F

12/09

ZENITHBANK 24.6027.4019.30

YtD -0.40-1.60%

-0.70-2.77%

0.351.44%3M 1W

PE 7.110.35

June July August08/09

M T W T F

12/09

TICKER 25.2327.4019.23

1YtD 0.230.92%

2.9012.99%

0.010.04%3M 1W

PE 7.290.01

May June July21/07

M T W T F

25/07

FBNH 14.5217.2911.50

YtD -1.78-10.92%

-0.98-6.32%

-0.48-3.20%3M 1W

PE 6.720.48

June July August08/09

M T W T F

12/09

GLAXOSMITH 63.1774.9762.28

YtD -6.83-9.76%

-5.73-8.32%

0.470.75%3M 1W

PE 21.680.47

June July August08/09

M T W T F

12/09

JBERGER 61.0176.4559.18

YtD -2.06-3.27%

-7.01-10.31%

-1.99-3.16%3M 1W

PE 9.491.99

June July August08/09

M T W T F

12/09

NESTLE 1013.001250.01931.85

YtD -169.00-14.30%

-56.99-5.33%

-11.95-1.17%3M 1W

PE 35.0411.95

June July August08/09

M T W T F

12/09

SEPLAT 655.26735.00590.00

YtD 50.468.34%

5.260.81%

-24.62-3.62%3M 1W

PE 0.0024.62

June July August08/09

M T W T F

12/09

3 4 5

9

13

10 11

12

6

8

14

7

21

1. 52-week low price2. Year low price3. Current price4. Year high price5. 52-week high price6. Current price7. 5-day price change8. PE ratio9. 1-year price change10. 3-months price change11. 1-week price change12. Daily price movement over 3 months.13. 30-day moving average14. Daily price movement over last week

MARKET DATAVM4 VM | Monday, September 15, 2014 | Issue 010

MARKET DATA VM5VM | Monday, September 15, 2014 | Issue 010

MARKET SNAPSHOT

# TICKER WTD YTD

1 DANGCEM -4.45 -0.54

2 NB 0.62 7.38

3 GUARANTY -2.21 5.08

4 NESTLE -1.17 -14.30

5 ZENITHBANK 1.44 -1.60

6 FBNH -3.20 -10.92

7 WAPCO 2.31 4.09

8 ETI 8.17 17.88

9 STANBIC -0.03 34.29

10 GUINNESS -6.08 -27.97

11 FO 4.55 147.67

12 UBA -1.10 -21.42

13 TRANSCORP -5.47 39.40

14 OANDO -2.86 -6.06

15 ACCESS 2.57 -0.10

16 UNILEVER 1.27 -9.91

17 UBN 17.29 4.47

18 FLOURMILL -2.64 -23.00

19 PZ -0.86 -6.48

20 UACN -1.02 3.59

21 DANGSUGAR 4.29 -24.78

22 CADBURY -3.03 -46.07

23 7UP 5.00 106.82

24 INTBREW 1.37 2.05

25 DIAMONDBNK 2.11 -16.00

26 FCMB -2.58 8.07

27 JBERGER -3.16 -3.27

28 ASHAKACEM -1.68 46.89

29 MOBIL 3.51 55.26

30 TOTAL 4.10 3.92

31 GLAXOSMITH 0.75 -9.76

32 FIDELITYBK 2.04 -25.93

33 STERLNBANK 2.68 -8.00

34 CONOIL -0.18 -10.31

35 SKYEBANK 3.24 -36.36

36 PRESCO 0.03 -5.13

37 OKOMUOIL -2.19 -25.27

38 CAP 2.44 -16.74

39 NEIMETH -1.90 -6.36

40 MAYBAKER -12.10 -45.88

WEEK-TO-DATE RETURN-15%

-50%

-20%

-30%

-40%

-10%

0%

+10%

+20%

+30%

+40%

+50%

+60%

+70%

+80%

+100%

+90%

+120%

+140%

+130%

+110%

+150%

0%-10% -5% 5% 10% 15% 20%

YEA

R-TO

-DAT

E RE

TURN

LAGGING

SLIPPING LEADING

IMPROVING

1

23

4

5

6

7

8

9

10

11

12

13

614

15

16

17

18

19

20

21

22

23

24

25

26

1127

28

29

30

1131

32

3334

35

36

37

38

39

40

Bubble size = Market Cap

TRADING BREAKDOWN BY SECTOR

Sector %

Industrial Goods 52

Financial Services 32 \ 84

Conglomerates 5 \ 7

Others 11 \ 6

05/09 11/0909/0913.4

13.6

13.8

14.0

14.2

2960

2970

2980

2990

3000

FGN Bond Index Market Value YTD Return

INDEX PERFORMANCE

Index Week Opening

Week Close Change WtD MtD QtD YtD

1 All Shares Index 41,160.62 40,672.94 -487.68 -1.18 -2.07 -4.26 -1.59

2 NSE 30 Index 1,870.68 1,856.96 -13.72 -0.73 -1.77 -3.87 -2.63

3 NSE Banking Index 426.18 434.35 8.17 1.92 1.33 0.34 -3.01

4 NSE Insurance Index 142.31 142.41 0.1 0.07 -1.49 -3.01 -6.84

5 NSE Consumer Goods Index 1,002.81 997.92 -4.89 -0.49 -2.91 -5.7 -9.3

6 NSE Oil/Gas Index 458.82 467.06 8.24 1.8 -2.79 -0.25 37.42

7 NSE Lotus Islamic Index 2,678.96 2,631.96 -47 -1.75 -3.44 -8.44 -8.07

8 NSE Industrial Index 2,672.58 2,629.45 -43.13 -1.61 -1.86 -1.4 3.25

MARKET SNAPSHOT

Date Deals Turnover Volume Turnover Value Traded Stocks Advanced

StocksDeclined Stocks

Unchanged Stocks

All Shares Index Value

1 08.09.14 4,168 479,791,860 50,706,734,379.59 106 \ 111 29 \ 25 25 \ 30 52 \ 56 41,214.81

2 09.09.14 4,782 1,649,176,997 46,346,888,465.65 121 \ 114 27 \ 20 29 \ 33 65 \ 61 40,868.02

3 10.09.14 5,193 386,565,044 3,788,276,370.17 126 \ 105 20 \ 20 24 \ 33 82 \ 52 40,885.40

4 11.09.14 4,756 267,099,744 3,060,524,239.82 108 \ 109 23 \ 17 24 \ 38 61 \ 54 40,757.20

5 12.09.14 4,780 263,855,559 2,798,678,370.74 115 \ 111 29 \ 36 31 \ 16 55 \ 59 40,672.94

The \ arrow signifies week-on-week change in value. This week’s value is shown on the left of the \ sign, and last week’s value on the right.

GLOBAL INTEREST RATES & INFLATION TARGETSCentral Bank Rate Last Date

Change%

Change Inflation

TargetChina 6.00% 05.07.2012 -0.31 4.00%Japan 0-0.10% 05.10.2010 -0.20 2.00%

UK 0.50% 05.03.2009 -0.50 2.00%USA 0-0.25% 16.12.2008 -0.1 2.00%

Eurozone 0.05% 04.09.2014 -0.10 <2.00%Brazil 11.00% 02.04.201 +0.25 4.5% +/-2.0%Canada 1.00% 20.07.2010 +0.25 2.0% +/-1.0%Egypt 8.25% 05.12.2013 -0.50

India 8.00% 28.01.2014 +0.25Indonesia 7.50% 12.11.2013 +0.25 4.5% +/-1.0%Malaysia 3.25% 10.06.2014 +0.25Mexico 3.00% 06.06.2014 -0.50 3.00% +/-1.0%Morocco 3.00% 28.03.2012 -0.25Nigeria 12.00% 10.10.2011 +2.75 6.00% - 9.00%Qatar 4.50% 10.08.2011 -0.50Russia 8.00% 28.07.2014 +0.50 5%*

Thailand 2.00% 12.03.2014 -0.25 0.5% - 3.0%Turkey 8.75% 24.06.2014 -0.75 5.00%

* +/- 1.5 pct point uncertainty band

Indices

ASI

NSE30

NSEBNK

NSEINS

NSECNSMRGDS

NSEOILGAS

NSELOTUSISLM

NSEINDUSTR

-1.18%-0.21%

-0.73%-0.03%

1.92%0.71%

0.07%-0.11%

-0.49%0.07%

1.80%1.78%

-1.75%-0.46%

-1.61%-0.63%

-1.59%

YtD, % WtD, % DtD, %

-2.63%

-3.01%

-6.84%

-9.30%

37.42%

-8.07%

3.25%

-10% -4%-6%-8% -2% 0% 4%2%

MoFr51,10

51,30

51,70

51,50

51,9051,247.71

Tu We Th Fr

JSE FTSE

FrTh6,700

6,750

6,850

6,800

6,9006,806.96

Tu We Th Fr

FTSE 100

MoFr40,50

40,70

41,10

40,90

41,3040,672.94

Tu We Th Fr

NSEASI

MoFr1,970

1,980

2,000

1,990

2,0101,985.54

Tu We Th Fr

S&P 500

ART AS AN ALTERNATIVE INVESTMENT

EDITOR: MIDENO BAYAGBON

GROUP BUSINESS EDITOR: OMOH GABRIEL

CONTENT DIRECTION: OBIORA TABANSI ONYEASO

DESIGN & ILLUSTRATION: PUBLICAN MEDIA

Vanguard Markets features unbiased, in-depth coverage of corporate and market developments across a wide range of business sectors.Every week, Vanguard Markets delivers essential business analysis and commentary on Nigerian companies, regional economies, and global markets. Vanguard Markets is published by Vanguard Media Limited in associa-tion with Customs Street Advisors Limited, a specialist communications consultancy.

Vanguard Media Limited, Vanguard Avenue, Kirikiri Canal, P.M.B.1007, Apapa.

Website: www.vanguardngr.com

ISSN 0794-652X

Published by

In Association With

ARENAVM6 VM | Monday, September 15, 2014 | Issue 010

T HIS 4OTH birthday celebra-tion in 2013 Kachi

Onubogu’s visibly elated mother shared a story of how her son had always had an entrepreneurial flair. She told the guests seated in the Shell Hall of MUSON Centre that during his National Youth Service orientation he figured that he could start a small ven-ture providing other corpers with the popular ogi pap made

from fermented cornflour. The hall burst into laughter. Until he hit on the idea the raw material was being dis-carded at the camp. Prior to that the budding businessman had had other successful mon-ey-spinning ideas.

Youthful-looking Onubogu honed his management skills at an early age helping his parents manage a successful poultry in Jos, the city where he grew up. His easy man-ner, unassuming nature, and perennial smile mask a highly competitive streak.

Those little beginnings were long ago. In February, Onubogu was named execu-tive director (commercial) at Promasidor Nigeria, makers of Cowbell milk, Loya milk, and Onga seasoning. He is credited with driving the multi-billion naira company’s popularity since he joined in 2010. He was poached from Prosperity Capital Manage-ment, a global fund manage-

ment company, where he was the associate director in its Nairobi office. In a career that has traversed every re-gion in sub-Saharan Africa, a memorable highlight is his conception of the Udeme

campaign for Guinness, when he worked as marketing man-ager in Diageo’s Nigeria op-erations.

Onubogu’s dexterity in the art of selling, and the hard sciences were evident in the course of study he selected at the university. He gradu-ated with flying colours from the physics department of the University of Jos. After

amassing years of practical experience, he went on to earn an MBA from Gordon’s Institute of Business Sci-ences, University of Pretoria in South Africa. He has also participated in the Advanced

Management Program (AMP) at the University of Pennsyl-vania’s prestigious Wharton Business School.

His background in the sci-ences places him at a distinct advantage. Colleagues speak of his obsession with data and identifying causal relation-ships in customer behaviour. He reminds team members that if Promasidor could steal

the milk off the table of more established brands when it entered the market, it knows that the day it grows compla-cent is the day it gives up its crown. Staying on top means staying focused on the mar-keting discipline that helped its brands win mindshare. His marketing savvy paved the way to the engagement of a new generation of en-tertainers and showbiz per-sonalities as embodiments of brands.

He is one of a visible set of young Nigerian executives headhunted from the Dias-pora to assume senior leader-ship positions in companies over the last decade. These men and women were edu-cated here, started their ca-reers here, then went abroad to study, in pursuit of new op-portunities, or were seconded overseas by their employers. Having worked with the best and brightest in world-class companies, they were tempt-

ed to return home to contrib-ute their quota to national development. Their qualifica-tions are not in doubt.

A private crusade he be-gun last year to equip Iyi-Enu Hospital, a missionary hos-pital in his home town, Ogidi in Anambra State, brings him fulfilment. He started a cam-paign to raise N15 million to buy medical equipment for the treatment of cardiovascu-lar diseases at the medical fa-cility after reading that more than thirty million Nigerians suffer from heart related ail-ments linked to hypertension.

Indeed, he told invited guests at his birthday last year to write cheques in support of Iyi-Enu rather than buying him presents.

‘I want to be remembered for one thing, that I was able to bring a change in my en-vironment,’ he said. But this is no ordinary change. It is a change that could save mil-lions of lives. ;

SPOTLIGHT

Onyekachi Onubogu, ED, Promasidor, marketing whiz

A

HIS WEEK, WE will be bringing to you the first in our

book review series. We will start with a review of an in-sightful book, Art as an In-vestment? A Survey of Com-parative Assets, written by art market expert, Melanie Gerlis, an art market expert.

Before her entry into the art market in 2005, she had spent a decade working with investment banks, private equity firms, stock exchanges and hedge funds. Therefore,

it is no surprise that she ini-tially approached the art busi-ness with the mindset that the rules of these financial players could be applied fairly easily to art, to produce a more ef-ficient system of trading.

The author sets out to ques-tion the validity of claims about art’s capacity to gener-ate returns that outweigh its risks.

Over the last decade, there has been considerable debate over the suitability of art as an investment asset. This has pitched financially-minded professionals against the art-dealing community, who spurn their sophisticated models and analytical methods.

These differing opinions set the stage for Gerlis’ dis-cussion on the pros and cons of art as an investment, which she determines in relation to other available investments including stocks, gold, wine, property, private equity and luxury goods.

Aimed at collectors and investors, this 192-page user-friendly guide published by Lund Humphries in Feb-ruary 2014, opens up to an introduction on the risks and returns of high-end art. The author brings to bear her fi-nancial expertise and solid first-hand knowledge of art and its markets. She draws on extensive research and in-terviews with key players in these other markets, as well as her own experience, to clarify the specifics of art as an asset class.

Gerlis kicks off her discus-sion on the premise that all art in the market is an asset, owing to the fact that people are willing to pay money, and that they expect to resell. She argues that art is the source of income for several intermedi-aries including an estimated 23,000 auction houses, as well as 375,000 art dealers, globally.

However, she argues that

most analyses of the art mar-ket concentrate on the relative returns, almost regardless of the risks, including the lack of liquidity and near absence of regulatory structures. She posits that while issues of transparency and regulation continue to be the bane of se-rious investment, by far the biggest problem is valuation. She explains that ‘even in the more opaque financial mar-kets, such as private equity, there are considerably more data points from which to cre-ate indexes, assess risk and at-tempt to gauge returns.’

Next week, in our continu-ing series of this review, we will take a closer look at more of these risks while proffering insightful solutions to those including investors and en-thusiasts who seek to under-stand the nature of the art commodity. ;

Book review: Art as an Investment? A Survey of Comparative Assets, by Melanie Gerlis

Oliver Enwonwuis the director of leading Lagos gallery, Omenka and president of the Society of Nigerian [email protected]

T

Art as an Investment? A Survey of Comparative Assets,

by Melanie Gerlis, published by Lund Humphries in the UK;

ISBN 978-1-84822-134-5, 192pp (hardback); also available as an

e-book.

Onyekachi Onubogu

Onubogu is one of a visible set of young Nigerian executives brought back from the Diaspora to assume senior leadership positions in Nigerian companies in the last decade.

Over the last decade, there has been considerable debate over the suit-ability of art as an investment asset.