Embed Size (px)

DESCRIPTION

VALUATION. Five Categories of Valuation Methods. Discounted cash-flow Market-based Mixed models Asset-based methods Option-based methods. Discounted Cash-Flow Approach. Estimated future cash flows are discounted back to present value based on the investor’s required rate of return - PowerPoint PPT Presentation

Citation preview

VALUATION

Five Categories of Valuation Methods

1. Discounted cash-flow2. Market-based3. Mixed models4. Asset-based methods5. Option-based methods

Discounted Cash-Flow Approach Estimated future cash flows are

discounted back to present value based on the investor’s required rate of return

Discounted dividend valuation Discounted operating cash-flow

models

Discounted Dividend Valuation

Most straightforward approach Explicit cash flows received by

equity investors Dividends Terminal value when shares are sold

Firm is expected to have an infinite life

Discounted Dividend ValuationTheoretical Model

No-growth, constant dividend

Dividends are growing at rate g

r

D0P

gr

g)(D

gr

DP

10

0

1

Discounted Dividend ValuationRequired rate of return (r)

r is the rate of return demanded on a specific investment

Based on investor’s assessment of risk

CAPM )( fmf rrrr

CAPM -- Example rf, Risk-free (30-year Treasury

bond) = 5% rm, Expected stock market return

= 10% Risk premium = (rm – rf)

Beta = 1.5 r = 5% + 1.5(10%-5%) r = 12.5%

Discounted Dividend ValuationRequired rate of return (r)

For nonpublic companies, use a buildup model and historical sources for data Begin with risk-free rate + Equity risk premium + Small company premium + Company specific risk premium = Required rate of return

Discounted Dividend ValuationGrowth rate (g)

Top-Down analysis Begin with growth of economy Adjust for industry, sector and company

factors Sustainable growth = ROE(1-Payout

rate) ROE = Earnings/Average equity Payout rate: proportion of earnings used

to pay dividends or repurchase shares

Company A Annual dividend = $0.16 Beta = 1.35 ROE = 13% Payout ratio = 20%

Economic 20-year Treasury bond = 4.75% Historical market risk premium = 5.4%

Discounted Dividend Valuation- example

r = .0475+1.35(.054) = .120 g = .13(1-.20) = .104 Value = $11.04…

Discounted Dividend Valuation- example

104.120.

)104.1(16.0$

Discounted Dividend Valuation

Assumes a single, constant growth rate (g)

What if growth rates differ? Use a multi-stage model to

calculate future dividends Calculate future stock value based on

future dividend Calculate present value of stock and

dividends

Discounted Operating Cash-Flow Models

Most applicable in the event of a takeover

Free cash flow (FCF) is operating cash flows less necessary investments in working capital and property, plant and equipment

gr

FCFV

1

0

FCFF or FCFEEBITDALess: Depreciation and AmortizationEBITLess: Interest PaidEBTLess: TaxesNet IncomePlus: Depreciation and amortizationLess: Increase in Working CapitalOperating Cash FlowPlus: Interest Expense*(1-tax rate)Less: Increase in Fixed CapitalFree Cash Flows to the Firm (FCFF)Less: Interest Expense*(1-tax rate)Plus: New debt borrowingLess: Debt RepaymentFree Cash Flows to the Equity (FCFE)

Discount Rate FCFF

Weighted Average Cost of Capital FCFE

Cost of Equity (required rate of return)

Discounted Operating Cash-Flow ModelsOther considerations

Growth Can use a multi-stage model to

accommodate rate changes Forecasting cash flows requires

judgment Begin with reported, historical cash flow

and earnings Make company-appropriate adjustments

Special Issues Loss generating firm valuation Closed Firm Valuation Start-up companies

Valuation Of GAP Retail Stores

Revenues 13.763,00 Operating Income 1.851,00 Capital Expenditures 1.650,00 Depreciation 524,00 Total value of Debt 7.460,38 Market value of Equity 28.795,00 Tax rate 35,00%Return on Capital (will be maintained till perpetuity) 13,61%High Growth period-5 years 12,73%Stable Growth 5,00%Beta-high growth 1,20 Beta- stable growth 1,00 Risk free rate 5,40%Market Premium 4,00%Pretax cost of debt 7,20%

Years EBIT(1-t) Reinvestment FCFF Disc. Rate Present Value0 1.203 1.126 1 1.356 1.269 87 9,06% 80 2 1.529 1.431 98 9,06% 82 3 1.723 1.613 110 9,06% 85 4 1.943 1.818 124 9,06% 88 5 2.190 2.050 140 9,06% 91

Total 426

High Growth Stable GrowthDebt Ratio 21% 21%Equity Ratio 79% 79%Beta 1,20 1,00 Risk free rate 5,40% 5%Risk Premium 4,00% 4%Pretax debt rate 7,20% 7%Tax rate 35,00% 35%Cost of debt 4,68% 4,68%Cost of equity 10,20% 9,40%WACC 9,06% 8,43%

FCFF-Stable Growth

Reinvestment Rate =g/ROC 36,74%

FCFF6 EBIT5(1-t)*(1+g)*(1-R) 1.455

Terminal Value FCFF6/(WACC-g) 42.429 1.455/(8,43%-5%)

Disc.terminal value 28.310

Value of Operating Assets 28.736 28.310+426

Value of Equity Value of Operating Assets+Cash and MS-Debt

Market-based Models

Compare subject company to other similar companies for which market prices are available

Simple computations but require a great deal of professional judgment

P/E Model P/B Method P/S Model

P/E Model

Assumes a company is worth a certain multiple of its current earnings

Assumes each share is worth the same multiple of EPS

Derived from the dividend discount models

Requires judgment regarding Peer firms and their prices Historical (average) data

P/E Model

Firms with no internal growth prospects, paying out 100% of earnings Current P/E = 1/r

Constant growth, Leading P/E P0/E1 = (D1/E1)/(r-g) D = annual dividends, E = EPS

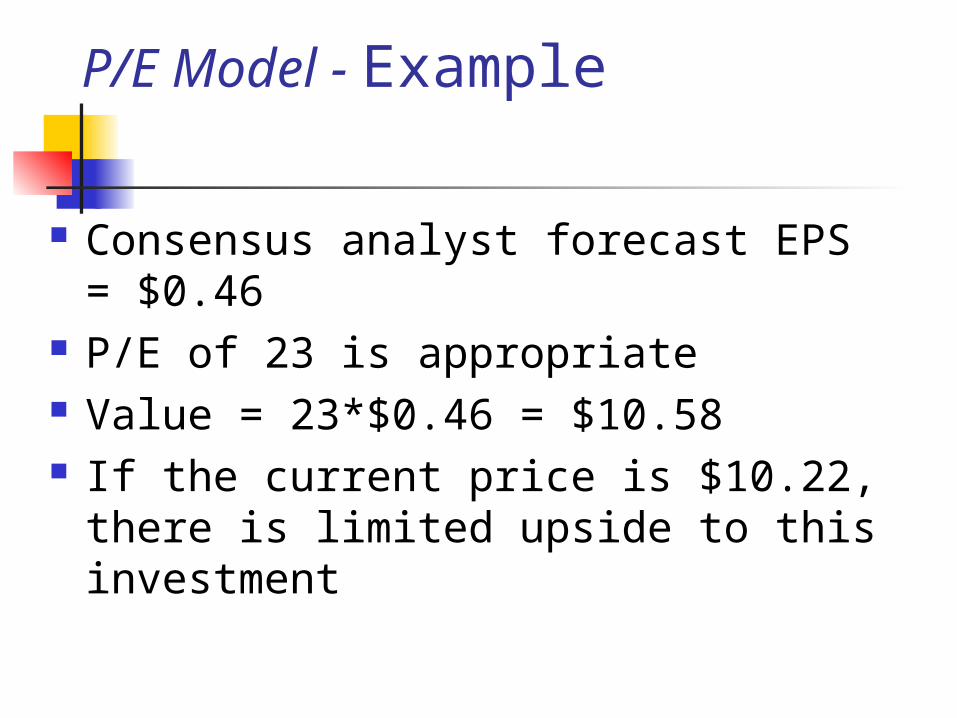

P/E Model - Example

Consensus analyst forecast EPS = $0.46

P/E of 23 is appropriate Value = 23*$0.46 = $10.58 If the current price is $10.22, there is

limited upside to this investment

Mixed Models

Because the previous models are linked (discounted dividend model) a combined approach can be used

May use discounted cash flow approach to forecast cash flows then use market multiple to derive terminal value

Residual income approaches are linked to the dividend discount model

Asset-Based Models Used when a company is going to

be liquidated Valuation is based on underlying

assets Market value of balance sheet items Assets and liabilities

Also called cost or adjusted book value approach

Options-Based Models Theoretically elegant but practical

application is difficult Analyst must have information about

opportunities (and their value) available to a firm

Equity ownership is viewed as an option call on the firm Limited downside, unlimited upside

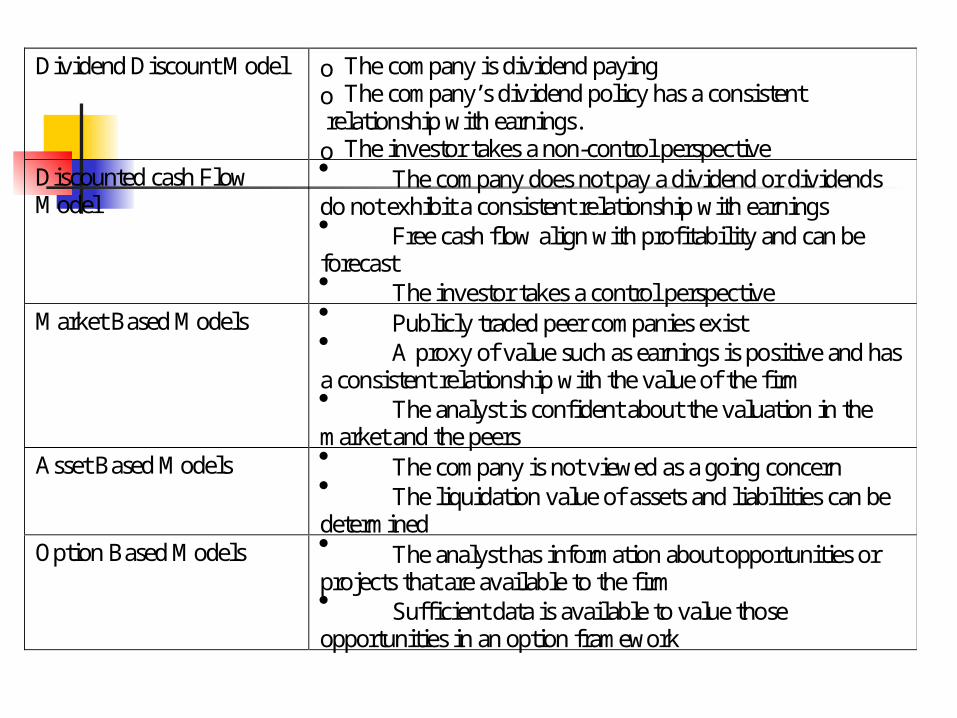

Selecting a Model Consider characteristics of the firm

Dividend paying Growing Likely to be liquidated

Consider data availability of data Publicly available or closely held

Dividend Discount Model o The company is dividend paying o The company’s dividend policy has a consistent relationship with earnings. o The investor takes a non-control perspective

Discounted cash Flow Model

The company does not pay a dividend or dividends do not exhibit a consistent relationship with earnings Free cash flow align with profitability and can be forecast The investor takes a control perspective

Market Based Models Publicly traded peer companies exist A proxy of value such as earnings is positive and has a consistent relationship with the value of the firm The analyst is confident about the valuation in the market and the peers

Asset Based Models The company is not viewed as a going concern The liquidation value of assets and liabilities can be determined

Option Based Models The analyst has information about opportunities or projects that are available to the firm Sufficient data is available to value those opportunities in an option framework