Embed Size (px)

Citation preview

VA Training

VA LOAN APPROVAL REQUIREMENTS

To obtain a VA loan, the law requires that:

the applicant must be an eligible veteran who has available entitlement;

the loan must be for an eligible purpose;

the veteran must occupy the property as a home within a reasonable period of time after closing the loan;

the veteran must be a satisfactory credit risk;

the income for the veteran and spouse, if any, must be shown to be stable and sufficient to meet the mortgage payments, cover the costs of owning a home, taking care of other obligations and expenses and have enough left over for family support.

Note: In community property states information concerning a spouse may be requested and considered in the same manners as for the veteran, even if the spouse will not be contractually obligated on the loan.

How to obtain a Certificate of Eligibility (COE) and Determine Eligibility.

• Automated COE’s are obtained through the VA’s WebLGY system.

• If WebLGY is unable to process an Automated COE, required documents can be scanned and uploaded through the website and the COE will be emailed. The DD-214 will be required for this type of processing.

IS THE VETERAN ELIGIBLE?

REVIEWING THE COE

• Is the veteran a first time or subsequent user?

• Is the veteran exempt from the funding fee?

• Is there sufficient entitlement for your loan amount?

• Are there any special conditions that must be met?

COE CONDITIONS

Condition Condition Description

Active Duty Service Member

Valid unless discharged or released subsequent to date of this certificate. A certification of continuous active duty as of date of note is required.

Subsequent Use Funding Fee

Entitlement code of ‘5’ indicated previously used entitlement has been restored. The veteran must pay a subsequent funding fee on any future loan unless veteran is exempt.

Regular Military No condition description.

Reservist/National Guard Funding Fee

Entitlement is based on service in the Selected Reserve and/or National Guard so increased Funding Fee is required.

One time Restoration Entitlement previously use for 00-00-0-0000000 has bee restored without disposal of the property, under provision of 38 U.S.C. 3702b (4). Any future restoration requires disposal of all property obtained with a VA loan.

Refinance Restoration (Cash out)

The Certificate of Eligibility is valid only for “cash out” refinance loan on the property that secured VA loan number 00-00-0-0000000. VA guaranty on a “cash out” refinance loan is limited to the basic entitlement shown on this certificate.

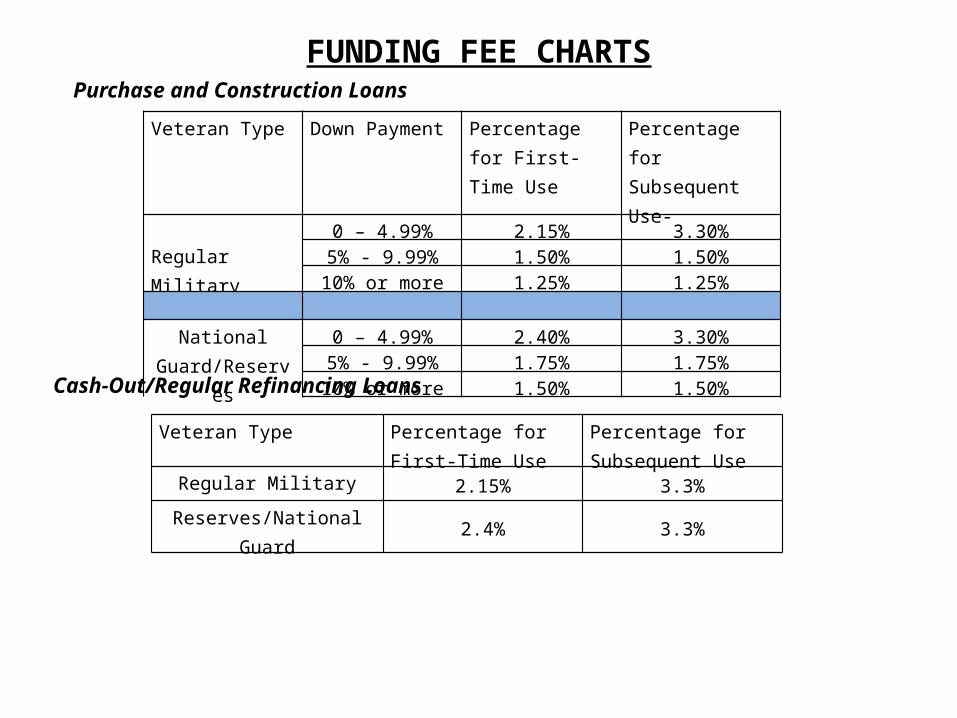

FUNDING FEE CHARTSPurchase and Construction Loans

Veteran Type Down Payment Percentage for First-Time Use

Percentage for Subsequent Use-

Regular Military0 – 4.99% 2.15% 3.30%

5% - 9.99% 1.50% 1.50%10% or more 1.25% 1.25%

National Guard/Reserves

0 – 4.99% 2.40% 3.30%5% - 9.99% 1.75% 1.75%

10% or more 1.50% 1.50%

Cash-Out/Regular Refinancing Loans

Veteran Type Percentage for First-Time Use

Percentage for Subsequent Use

Regular Military 2.15% 3.3%Reserves/National Guard 2.4% 3.3%

Veteran Type Percentage for First-Time Use

Percentage for Subsequent Use

Regular Military .50% .50%%Reserves/National Guard .50% .50%

IRRRL’S

FUNDING FEE CHARTS

Other Types of Loans

Veteran Type Percentage for Type of Veteran Whether First-Time or Subsequent Use

Loan Assumptions .50%

RESIDUAL INCOME REQUIREMENTS

• Residual income is the amount of net income remaining (after deduction of debts and obligations and monthly shelter expenses) to cover family living expenses such as food, health care, clothing, and gasoline. They vary according to loan size, family size, and region of the country.

• Count all members of the household (without regard to the nature of the Relationship) when determining “family size,” including: an applicant’s spouse who is not joining in title or on the note, and any other

individuals who depend on the applicant for support. For example, children from a spouse’s prior marriage who are not the applicant’s legal dependents. Reduce the residual income figure (from the following tables) by a minimum of five percent if:

the applicant or spouse is an active-duty or retired serviceperson, and there is a clear indication that he or she will continue to receive the benefits resulting from use of military-based facilities located near the property.

• Residual income requirement may be reduced by 5% if the applicant or spouse is an active-duty serviceperson.

RESIDUAL INCOME REQUIREMENTSCalculating the Residual Income

Line 19 – Maintenance & Utilities• Calculate M&U costs using 14

cents per square foot (above grade).

For example: A 1500 square foot home would have a M&U cost of $210 (1500 x .14 = $210)

Lines 32-35 – Deductions• Federal and state taxes are based

off the gross income, borrowers filing status and number of exemptions. *See website below for automated calculation of the deductions

• Retirement and Social Security is calculated using 7.65% of the gross income for W-2 borrowers and 15.3% for self-employed borrowers.*Paycheck calculator for calculating federal and state taxes:

http://www.adp.com/tools-and-resources/calculators-and-tools/payroll-calculators/salary-paycheck-calculator.aspx

RESIDUAL INCOME REQUIREMENTS

Table of Residual Income by Region for loan amounts of $79,999 and below

Family Size Northeast Midwest South West1 $390 $382 $382 $4252 $654 $641 $641 $7133 $788 $772 $772 $8594 $888 $868 $868 $9675 $921 $902 $902 $1,004Over 5 Add $75 for each additional member up to a family of seven

Table of Residual Income by Region for loan amounts of $80,000 and above

Family Size Northeast Midwest South West1 $450 $441 $441 $4912 $755 $738 $738 $8233 $909 $889 $889 $9904 $1,025 $1,003 $1,003 $1,1175 $1,062 $1,039 $1,039 $1,158Over 5 Add $75 for each additional member up to a family of seven

KEY TO GEOGRAPHIC REGIONS USED IN THE PRECEDING TABLES

Northeast Connecticut MaineMassachusetts

New Hampshire New JerseyNew York

PennsylvaniaRhode IslandVermont

Midwest Illinois IndianaIowaKansas

MichiganMinnesotaMissouriNebraska

North DakotaOhioSouth DakotaWisconsin

South AlabamaArkansasDelawareDistrict of ColumbiaFloridaGeorgia

KentuckyLouisianaMarylandMississippiNorth CarolinaOklahoma

Puerto Rico South CarolinaTennesseeTexasVirginiaWest Virginia

West AlaskaArizonaCaliforniaColoradoWyoming

HawaiiIdahoMontanaNevada

New MexicoOregonUtahWashington

RESIDUAL INCOME REQUIREMENTS

QUALIFYING REQUIREMENTS

Standard VA DTI ratio of 41% may be exceeded if sufficient residual income and compensating factors are present

Maximum 50% DTI allowed with AUS approval

Ratios between 50.01%-55% allowed wit h AUS approval, second signature¹, and acceptable SNMC

compensating factors listed on Loan Analysis and Ratio Checklist form

VA Jumbo loan amounts > $417,000.00 maximum 50% DTI with AUS approval

Non-traditional credit on government loans has been eliminated. All loans must have at least one occupant borrower with a traditional credit history.

QUALIFYING REQUIREMENTS

FICO Requirements

Purchase

Occupancy Max Loan Amount Units LTV CLTV FICO

Primary ≤$417,000 1-4 100% 100% 620

Primary $417,001 - $700,000 1-4 n/a n/a 680

Cash Out/Regular Refinance

Occupancy Max Loan Amount Units LTV CLTV FICO

Primary ≤$417,000 1-4 90% 90% 620

Primary $417,001 - $700,000 1-4 90% 90% 680

IRRRL

Occupancy Max Loan Amount Units LTV CLTV FICO

Primary ≤$417,000 1-4 100% 100% 660

Credit

• Bankruptcy and Foreclosure – 2 year seasoning• Can be manually underwritten if AUS “Refer”• Borrower must have a least 12 months of clean credit• Unpaid collection accounts are considered current derogatory credit

Additional requirements

• Veteran must complete Child Care Expense Certification. Expense added to debt• Veteran required to give nearest living relative name and address• If Veteran is closing with a Power of Attorney and is Active Duty an Alive and Well Cert is

required• A Termite inspection or Soil Treatment for new construction is required in most States• Builder on new construction must be VA approved• VA has an approved condo list

.

OCCUPANCY

Occupancy requirements are:

• Veterans purchasing a primary residence, refinancing, and or improving their home must certify that they intend to occupy the property.

• If the buyer is on active duty, a spouse may certify occupancy. Single or married service members deployed from their permanent duty station are considered to be in a temporary duty status and are able to certify intent to occupy.

• Non-occupant co-borrowers are not allowed.

Documentation RequirementsVA has certain documentation that lenders must obtain when processing a loan application for a veteran. These requirements can be found in Chapter 4 and 5 of the VA Lender’s Handbook.

Following is a list of the documents required when processing a VA loan.

Certificate of Eligibility (VA Form 26-8320).

VA has certain documentation that lenders must obtain when processing a loan application for a veteran. These requirements can be found in Chapter 4 and 5 of the VA Lender’s Handbook.

Following is a list of the documents required when processing a VA loan.

Certificate of Eligibility (VA Form 26-8320). URLA (Uniform Residential Loan Application).

Documentation Requirements

VA has certain documentation that lenders must obtain when processing a loan application for a veteran. These requirements can be found in Chapter 4 and 5 of the VA Lender’s Handbook.

Following is a list of the documents required when processing a VA loan.

Certificate of Eligibility (VA Form 26-8320). URLA (Uniform Residential Loan Application). HUD/VA Addendum to URLA (VA Form 26-1802-a) pages 1 & 2.

Documentation Requirements

VA has certain documentation that lenders must obtain when processing a loan application for a veteran. These requirements can be found in Chapter 4 and 5 of the VA Lender’s Handbook.

Following is a list of the documents required when processing a VA loan.

Certificate of Eligibility (VA Form 26-8320). URLA (Uniform Residential Loan Application). HUD/VA Addendum to URLA (VA Form 26-1802-a) pages 1 & 2. Residential Mortgage Credit Report or 3 File Merged Credit Report.

Documentation Requirements

VA has certain documentation that lenders must obtain when processing a loan application for a veteran. These requirements can be found in Chapter 4 and 5 of the VA Lender’s Handbook.

Following is a list of the documents required when processing a VA loan.

Certificate of Eligibility (VA Form 26-8320). URLA (Uniform Residential Loan Application). HUD/VA Addendum to URLA (VA Form 26-1802-a) pages 1 & 2. Residential Mortgage Credit Report or 3 File Merged Credit Report. Counseling Checklist for Military Home Buyers (VA Form 26-0592). This form is only required for active duty military.

Documentation Requirements

VA has certain documentation that lenders must obtain when processing a loan application for a veteran. These requirements can be found in Chapter 4 and 5 of the VA Lender’s Handbook.

Following is a list of the documents required when processing a VA loan.

Certificate of Eligibility (VA Form 26-8320). URLA (Uniform Residential Loan Application). HUD/VA Addendum to URLA (VA Form 26-1802-a) pages 1 & 2. Residential Mortgage Credit Report or 3 File Merged Credit Report. Counseling Checklist for Military Home Buyers (VA Form 26-0592). This form is only required for active duty military. Verification of VA Benefits (VA Form 26-8937) if applicable.

Documentation Requirements

VA has certain documentation that lenders must obtain when processing a loan application for a veteran. These requirements can be found in Chapter 4 and 5 of the VA Lender’s Handbook.

Following is a list of the documents required when processing a VA loan.

Certificate of Eligibility (VA Form 26-8320). URLA (Uniform Residential Loan Application). HUD/VA Addendum to URLA (VA Form 26-1802-a) pages 1 & 2. Residential Mortgage Credit Report or 3 File Merged Credit Report. Counseling Checklist for Military Home Buyers (VA Form 26-0592). This form is only required for active duty military. Verification of VA Benefits (VA Form 26-8937) if applicable. Verification of Deposit (VA Form 26-8497) or original or certified true copies of the last two bank statements.

Documentation Requirements

VA has certain documentation that lenders must obtain when processing a loan application for a veteran. These requirements can be found in Chapter 4 and 5 of the VA Lender’s Handbook.

Following is a list of the documents required when processing a VA loan.

Certificate of Eligibility (VA Form 26-8320). URLA (Uniform Residential Loan Application). HUD/VA Addendum to URLA (VA Form 26-1802-a) pages 1 & 2. Residential Mortgage Credit Report or 3 File Merged Credit Report. Counseling Checklist for Military Home Buyers (VA Form 26-0592). This form is only required for active duty military. Verification of VA Benefits (VA Form 26-8937) if applicable. Verification of Deposit (VA Form 26-8497) or original or certified true copies of the last two bank statements. Verification of Employment (VA Form 26-8498) or equivalent. Or alternative documentation as described in Chapter 4, section 2e, of the VA Lender’s Handbook.

Documentation Requirements

VA has certain documentation that lenders must obtain when processing a loan application for a veteran. These requirements can be found in Chapter 4 and 5 of the VA Lender’s Handbook.

Following is a list of the documents required when processing a VA loan.

Certificate of Eligibility (VA Form 26-8320). URLA (Uniform Residential Loan Application). HUD/VA Addendum to URLA (VA Form 26-1802-a) pages 1 & 2. Residential Mortgage Credit Report or 3 File Merged Credit Report. Counseling Checklist for Military Home Buyers (VA Form 26-0592). This form is only required for active duty military. Verification of VA Benefits (VA Form 26-8937) if applicable. Verification of Deposit (VA Form 26-8497) or original or certified true copies of the last two bank statements. Verification of Employment (VA Form 26-8498) or equivalent. Or alternative documentation as described in Chapter 4, section 2e, of the VA Lender’s Handbook. Original or certified copy of pay stubs covering last 30 days income.

Documentation Requirements

VA has certain documentation that lenders must obtain when processing a loan application for a veteran. These requirements can be found in Chapter 4 and 5 of the VA Lender’s Handbook.

Following is a list of the documents required when processing a VA loan.

Certificate of Eligibility (VA Form 26-8320). URLA (Uniform Residential Loan Application). HUD/VA Addendum to URLA (VA Form 26-1802-a) pages 1 & 2. Residential Mortgage Credit Report or 3 File Merged Credit Report. Counseling Checklist for Military Home Buyers (VA Form 26-0592). This form is only required for active duty military. Verification of VA Benefits (VA Form 26-8937) if applicable. Verification of Deposit (VA Form 26-8497) or original or certified true copies of the last two bank statements. Verification of Employment (VA Form 26-8498) or equivalent. Or alternative documentation as described in Chapter 4, section 2e, of the VA Lender’s Handbook. Original or certified copy of pay stubs covering last 30 days income. Sales contract or other purchase agreement.

Documentation Requirements

VA has certain documentation that lenders must obtain when processing a loan application for a veteran. These requirements can be found in Chapter 4 and 5 of the VA Lender’s Handbook.

Following is a list of the documents required when processing a VA loan.

Certificate of Eligibility (VA Form 26-8320). URLA (Uniform Residential Loan Application). HUD/VA Addendum to URLA (VA Form 26-1802-a) pages 1 & 2. Residential Mortgage Credit Report or 3 File Merged Credit Report. Counseling Checklist for Military Home Buyers (VA Form 26-0592). This form is only required for active duty military. Verification of VA Benefits (VA Form 26-8937) if applicable. Verification of Deposit (VA Form 26-8497) or original or certified true copies of the last two bank statements. Verification of Employment (VA Form 26-8498) or equivalent. Or alternative documentation as described in Chapter 4, section 2e, of the VA Lender’s Handbook. Original or certified copy of pay stubs covering last 30 days income. Sales contract or other purchase agreement. Notice of Value (NOV)

Documentation Requirements

VA has certain documentation that lenders must obtain when processing a loan application for a veteran. These requirements can be found in Chapter 4 and 5 of the VA Lender’s Handbook.

Following is a list of the documents required when processing a VA loan.

Certificate of Eligibility (VA Form 26-8320). URLA (Uniform Residential Loan Application). HUD/VA Addendum to URLA (VA Form 26-1802-a) pages 1 & 2. Residential Mortgage Credit Report or 3 File Merged Credit Report. Counseling Checklist for Military Home Buyers (VA Form 26-0592). This form is only required for active duty military. Verification of VA Benefits (VA Form 26-8937) if applicable. Verification of Deposit (VA Form 26-8497) or original or certified true copies of the last two bank statements. Verification of Employment (VA Form 26-8498) or equivalent. Or alternative documentation as described in Chapter 4, section 2e, of the VA Lender’s Handbook. Original or certified copy of pay stubs covering last 30 days income. Sales contract or other purchase agreement. Notice of Value (NOV)Uniform Residential Appraisal Report (Freddie Mac Form/Fannie Mae Form 1004, including all attachments, photos and any document(s) revising or correcting the fee appraiser’s original report.

Documentation Requirements

INCOME

Standard Documentation

Verification of employment Paystubs covering last 30 days income/Active duty veterans Leave and Earnings Statement (LES) Most recent 2 yrs W-2’s Most recent 2 yrs tax returns Most recent 2 yrs tax transcripts

Income claimed by an applicant that is not or cannot be verified should not be given consideration. A minimum of two years employment should be verified (including past employers if needed). An original or certified copy of the applicant’s pay stub, when furnished by the employer, must be provided. The employment verification should be compared with the pay stub for consistency.

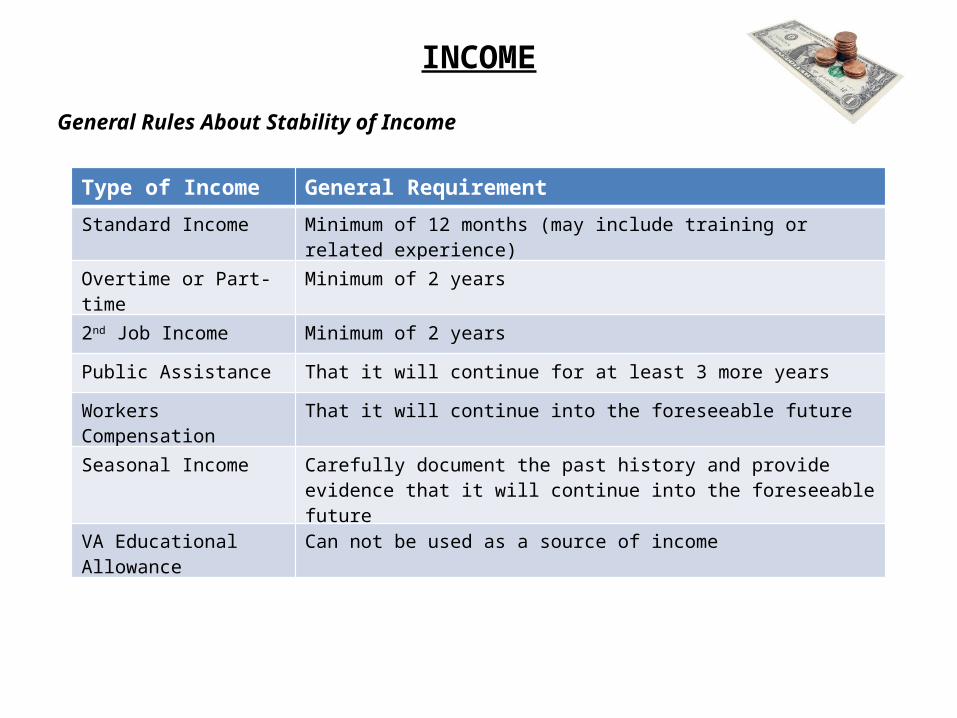

INCOME

General Rules About Stability of Income

Type of Income General Requirement

Standard Income Minimum of 12 months (may include training or related experience)

Overtime or Part-time Minimum of 2 years

2nd Job Income Minimum of 2 years

Public Assistance That it will continue for at least 3 more years

Workers Compensation That it will continue into the foreseeable future

Seasonal Income Carefully document the past history and provide evidence that it will continue into the foreseeable future

VA Educational Allowance Can not be used as a source of income

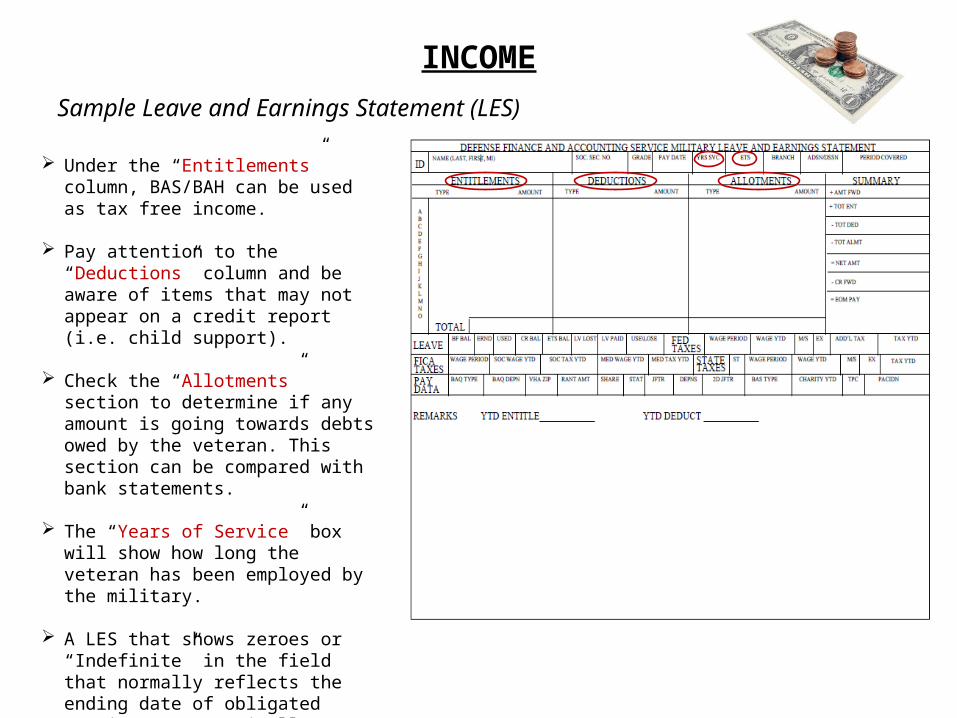

INCOMESample Leave and Earnings Statement (LES)

Under the “Entitlements” column, BAS/BAH can be used as tax free income.

Pay attention to the “Deductions” column and be aware of items that may not appear on a credit report (i.e. child support).

Check the “Allotments” section to determine if any amount is going towards debts owed by the veteran. This section can be compared with bank statements.

The “Years of Service” box will show how long the veteran has been employed by the military.

A LES that shows zeroes or “Indefinite” in the field that normally reflects the ending date of obligated service (ETS) typically means the person is an officer, and not necessarily subject to a specific term of service (i.e. 2 years, 4 years, etc.).

RENTAL INCOME

Multi-Unit Property Securing the VA LoanVerify:• Cash reserves totaling at least 6 months PITI, and • Documentation of the applicant’s prior landlord or property maintenance experience• The amount of rental income used on existing units would be based on 75% of the verified prior rent,

unless a higher percentage can be documented.• If the units are proposed property, then VA would require a letter from the appraiser stating the “fair

rental value” and a vacancy/operating cost reduction of that rental figure

Rental of existing property Existing single-family property may be used to “off-set” the mortgage payment if there is a positive cash-flow, and there is no indication the property will be difficult to rent. A copy of the lease should be furnished (if available) and it is the underwriter’s responsibility to be familiar with the local rental market. On “off-setting” the mortgage payment, the debt should still be listed on the loan analysis, but shown as a “rental offset.”

• If the existing single-family property is located in a weak rental market or has a negative cash flow, the rental income and expenses must be listed separately on the loan analysis.

Other Rental Property If the applicant has other rental property cash reserves equaling three months PITI + previous 2 years tax returns showing rental income generated by the property.

• The strength of the local rental market should be evaluated to determine the property will not be difficult to rent. Depreciation & interest may be added back when tax returns are used to determine effective income.

REFINANCESCash-Out/Regular Refinance vs. IRRRL

What is a VA Cash-Out/Regular Refinancing Loan?A cash-out refinancing loan is a VA-guaranteed loan that refinances any type of lien or liens against the secured property. The liens to be paid off may be:• current and• from any source, such as

– tax or judgment liens, or– VA, FHA, or conventional mortgages.

Loan proceeds beyond the amount needed to pay off the lien(s) may be taken as cash by the borrower for any purpose acceptable to the lender.

The loan must be secured by a first lien on the property.

What is an IRRRL?An IRRRL is a VA-guaranteed loan made to refinance an existing VA-guaranteed loan, generally at a lower interest rate than the existing VA loan, and with lower principal and interest payments than the existing VA loan. Generally, no appraisal, credit information or underwriting is required on an IRRRL, and any lender may close an IRRRL automatically.

CASH-OUT/REGULAR REFINANCES

• Must have an existing lien to pay off. Free and clear properties are not eligible.

• All refinances are considered cash out. VA does not offer a rate and term refinance.

• Borrower must be on title and on current lien to be eligible for cash out refinance.

• VA cash out transactions not allowed in Texas

• Primary Residence Only

IRRRL’S

• Primary Residence only

• Must meet a required Net Tangible Benefit

• The total loan amount (base loan amount including funding fee) cannot exceed 100% LTV

• Maximum loan term is the original loan team of the VA loan being refinanced plus 10 years, but not to exceed 30 years and 32 days

• Minimum Fico of 660, credit report is used to validate credit score and mortgage history only

• No mortgage lates allowed in the last 12 months

• A borrower must have made all mortgage payments within the month due for the preceding 12 months at the time of application

IRRRL’S (continued)

• If current mortgage has less than 12 months, a prior mortgage to equate 12 consecutive payments is required. (Rent rating not acceptable)

• In all cases a borrower must have made at least 6 mortgage payments in the month due for the current mortgage

• Subordinate financing is not allowed

• Employment must be verified at underwriting and again prior to funding. Self-employment can be verified by any third party source such as CPA letter, copy of business license, etc. Income is not required.

• In most cases, a full conventional appraisal must be obtained