Embed Size (px)

Citation preview

UTI Market Outlook Report

February 2020

2

Disclaimers: The information on this document is provided for information purposes only. It does not constitute any offer, recommendation or solicitationto any person to enter into any transaction or adopt any hedging, trading or investment strategy, nor does it constitute any prediction of likely future

movements in rates or prices or any representation that any such future movements will not exceed those shown in any illustration. Users of thisdocument should seek advice regarding the appropriateness of investing in any securities, financial instruments or investment strategies referred to onthis document and should understand that statements regarding future prospects may not be realized. The recipient of this material is solely responsiblefor any action taken based on this material. Opinions, projections and estimates are subject to change without notice.

UTI AMC Ltd is not an investment adviser, and is not purporting to provide you with investment, legal or tax advice. UTI AMC Ltd or UTI Mutual Fund(acting through UTI Trustee Company Pvt. Ltd) accepts no liability and will not be liable for any loss or damage arising directly or indirectly (includingspecial, incidental or consequential loss or damage) from your use of this document, howsoever arising, and including any loss, damage or expensearising from, but not limited to, any defect, error, imperfection, fault, mistake or inaccuracy with this document, its contents or associated services, or dueto any unavailability of the document or any part thereof or any contents or associated services.

The information presented here is not an offer for sale within the United States of any security of UTI Asset Management Company Limited (the"Company"). Securities of the Company, including, but not limited to, its shares, may not be offered or sold in the United States absent registration underU.S. securities laws or unless exempt from registration under such laws.

Market Outlook Flow

Macro Economic View

Fixed Income Outlook

Equity Outlook

IMF projects 2019 global growth at 3.2% (10 bps lower than

Apr projection)

United States growth projection for 2019 raised by 30bps to

2.6% & 2020 retained at 1.9%

India’s GDP projection lowered by 30bps for 2019 & 2020 to

7% & 7.2% respectively

IMF 2020 world GDP growth at 3.5%

- Risks to global growth remain to the downside

Global Macros Growth: Global Growth slowdown

Source: The International Monetary Fund, based on latest IMFdata available till Jan 31, 2020

IMF Growth Projections

3.63.2

3.5

2.21.9 1.7

6.4 6.2 6.2

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2018 2019 2020

World output Advanced economies Emerging & developing Asia

4

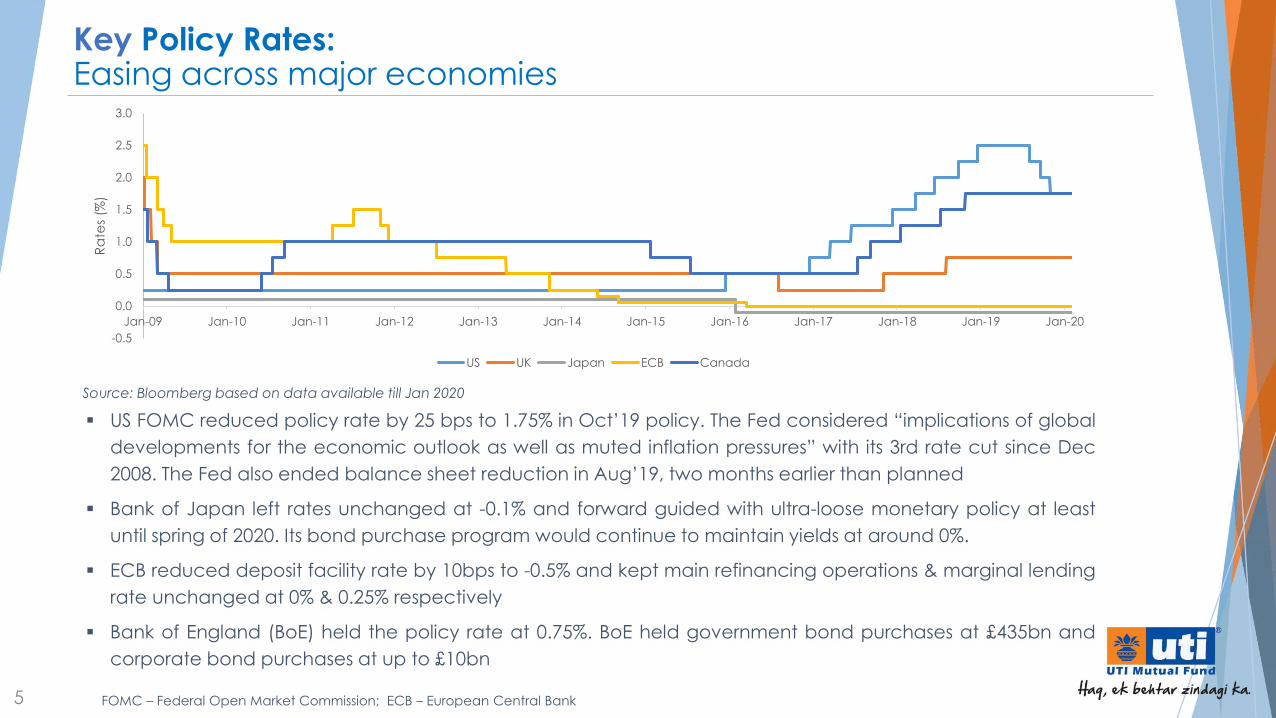

Key Policy Rates:Easing across major economies

US FOMC reduced policy rate by 25 bps to 1.75% in Oct’19 policy. The Fed considered “implications of global

developments for the economic outlook as well as muted inflation pressures” with its 3rd rate cut since Dec

2008. The Fed also ended balance sheet reduction in Aug’19, two months earlier than planned

Bank of Japan left rates unchanged at -0.1% and forward guided with ultra-loose monetary policy at least

until spring of 2020. Its bond purchase program would continue to maintain yields at around 0%.

ECB reduced deposit facility rate by 10bps to -0.5% and kept main refinancing operations & marginal lending

rate unchanged at 0% & 0.25% respectively

Bank of England (BoE) held the policy rate at 0.75%. BoE held government bond purchases at £435bn and

corporate bond purchases at up to £10bn

Source: Bloomberg based on data available till Jan 2020

5 FOMC – Federal Open Market Commission; ECB – European Central Bank

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17 Jan-18 Jan-19 Jan-20

Ra

tes

(%)

US UK Japan ECB Canada

Domestic Macro Growth:

Growth stalled, IIP contracts

Q2FY20 GDP at 4.5% hits a six-year low and IIP at -3.8% for Oct 2019 for third consecutive month

India's GDP growth hit a six-year low of 4.5% in Q2 2019, dragged mainly by deceleration in manufacturingoutput and subdued farm sector activity

The gross value added (GVA) growth in the manufacturing sector contracted by 1% in the Q2 of this fiscalfrom 6.9% expansion a year ago

Index of Industrial Production (IIP) contracted by 3.8% in Nov 2019 for third consecutive time against 4.3% inSep 2019 signalling a persistent slowdown

Negative growth in all the three sectors of manufacturing, mining and electricity pulled down IIP

IIP growth (YoY %)

Source: CSO based on data available till Dec 2019

Real GDP (YoY %)

Source: CSO based on data available till Dec 2019

6

-4.0%

0.0%

4.0%

8.0%

12.0%

Jun

-12

Sep

-12

Dec

-12

Mar

-13

Jun

-13

Sep

-13

Dec

-13

Mar

-14

Jun

-14

Sep

-14

Dec

-14

Mar

-15

Jun

-15

Sep

-15

Dec

-15

Mar

-16

Jun

-16

Sep

-16

Dec

-16

Mar

-17

Jun

-17

Sep

-17

Dec

-17

Mar

-18

Jun

-18

Sep

-18

Dec

-18

Mar

-19

Jun

-19

Sep

-19

GVA Agriculture Industry Services

YoY

%

3.3 3.3 4.0

3.3

4.6 4.4 3.8

0.6

-

1.0

2.0

3.0

4.0

5.0

FY 1

2-1

3

FY 1

3-1

4

FY 1

4-1

5

FY 1

5-1

6

FY 1

6-1

7

FY 1

7-1

8

FY 1

8-1

9

FYTD

19

-20

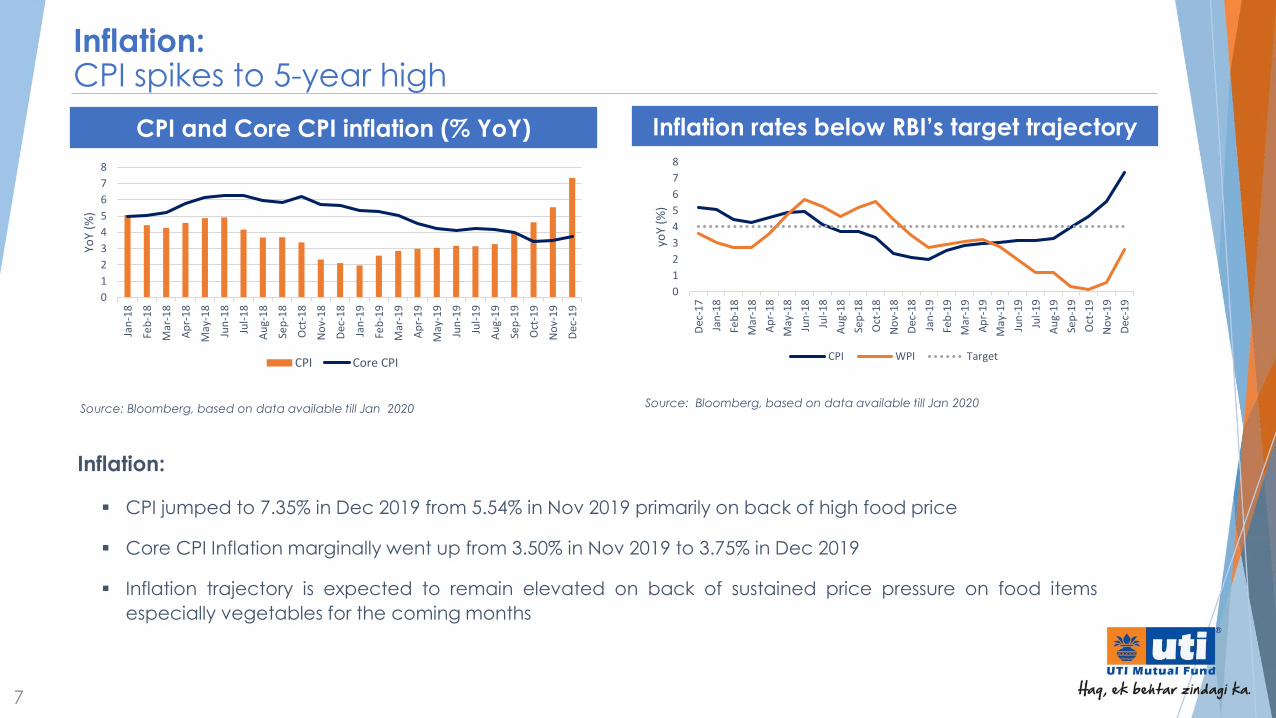

Inflation:CPI spikes to 5-year high

Inflation:

CPI jumped to 7.35% in Dec 2019 from 5.54% in Nov 2019 primarily on back of high food price

Core CPI Inflation marginally went up from 3.50% in Nov 2019 to 3.75% in Dec 2019

Inflation trajectory is expected to remain elevated on back of sustained price pressure on food items

especially vegetables for the coming months

Source: Bloomberg, based on data available till Jan 2020

CPI and Core CPI inflation (% YoY)

Source: Bloomberg, based on data available till Jan 2020

Inflation rates below RBI’s target trajectory

7

0

1

2

3

4

5

6

7

8

Jan

-18

Feb

-18

Mar

-18

Ap

r-1

8

May

-18

Jun

-18

Jul-

18

Au

g-1

8

Sep

-18

Oct

-18

No

v-1

8

Dec

-18

Jan

-19

Feb

-19

Mar

-19

Ap

r-1

9

May

-19

Jun

-19

Jul-

19

Au

g-1

9

Sep

-19

Oct

-19

No

v-1

9

Dec

-19

YoY

(%)

CPI Core CPI

0

1

2

3

4

5

6

7

8

Dec

-17

Jan

-18

Feb

-18

Mar

-18

Ap

r-1

8

May

-18

Jun

-18

Jul-

18

Au

g-1

8

Sep

-18

Oct

-18

No

v-1

8

Dec

-18

Jan

-19

Feb

-19

Mar

-19

Ap

r-1

9

May

-19

Jun

-19

Jul-

19

Au

g-1

9

Sep

-19

Oct

-19

No

v-1

9

Dec

-19

yoY

(%)

CPI WPI Target

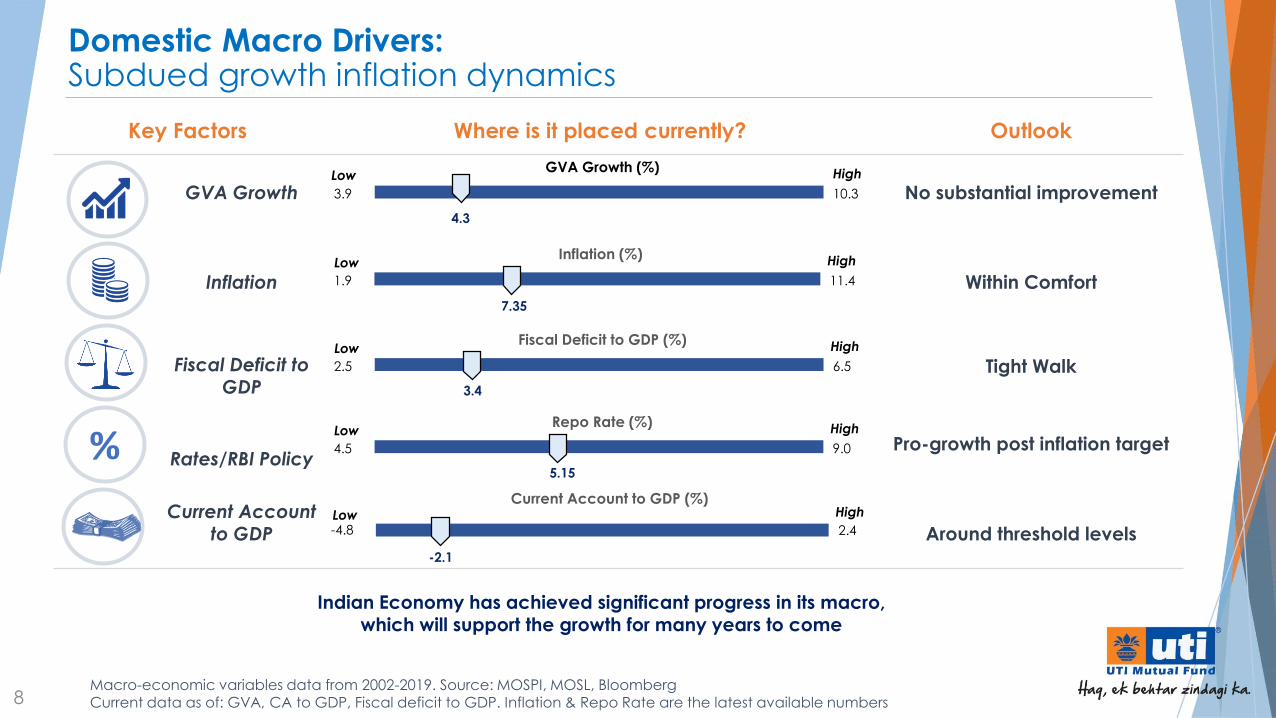

Domestic Macro Drivers:Subdued growth inflation dynamics

Key Factors Where is it placed currently? Outlook

GVA Growth No substantial improvement

Inflation Within Comfort

Fiscal Deficit to GDP

Tight Walk

Rates/RBI PolicyPro-growth post inflation target

Current Account to GDP Around threshold levels

Indian Economy has achieved significant progress in its macro,which will support the growth for many years to come

GVA Growth (%)

4.3

3.9 10.3

Low High

Inflation (%)

7.35

1.9 11.4

Low High

Fiscal Deficit to GDP (%)

3.4

2.5 6.5

Low High

Current Account to GDP (%)

-2.1

-4.8 2.4Low High

Repo Rate (%)

5.15

4.5 9.0

Low High

Macro-economic variables data from 2002-2019. Source: MOSPI, MOSL, Bloomberg Current data as of: GVA, CA to GDP, Fiscal deficit to GDP. Inflation & Repo Rate are the latest available numbers

%

8

Fixed Income Outlook

Indian 10 Year G-Sec:

Hardening of yields

Source: Bloomberg & RBI

The 10 year benchmark G-Sec, the 6.45 2029 GS yields inched up through the month and closed at6.60% (Jan 31, 2020) vis-à-vis 6.56% (Dec 31, 2019)

Factors impacting yields

- Geopolitical tensions between U.S. and Iran

- Uptick in CPI on back of higher food inflation

- Switch/Conversion auction of government securities by RBI

- Fall in crude oil prices on concerns that coronavirus outbreak in China may impact commodity’sdemand outlook

10

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

Jan-15 Jun-15 Nov-15 Apr-16 Sep-16 Feb-17 Jul-17 Dec-17 May-18 Oct-18 Mar-19 Aug-19 Jan-20

10

Yr

Gse

c (%

)

Re

po

(%

)

Repo Rate (LHS) 10 year G-sec Yield (RHS)

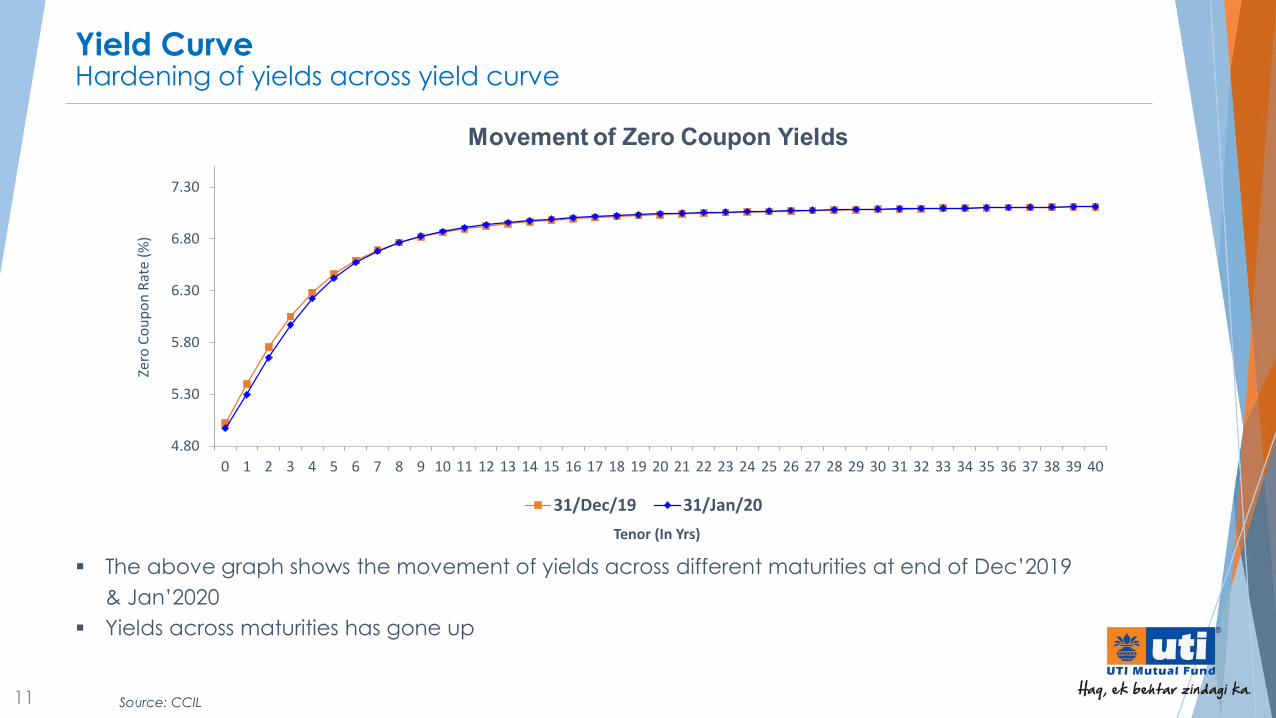

Yield Curve Hardening of yields across yield curve

Source: CCIL

The above graph shows the movement of yields across different maturities at end of Dec’2019

& Jan’2020

Yields across maturities has gone up

11

4.80

5.30

5.80

6.30

6.80

7.30

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40

Zero

Co

up

on

Rat

e (%

)

Tenor (In Yrs)

31/Dec/19 31/Jan/20

12

Domestic Debt Market IndicatorsHardening of yields seen across instruments

Source: Bloomberg, Data as on last day of the above mentioned months

5.11

6.15

6.88

5.19

6.20

6.85

5.27

6.26

6.90

4.00

4.50

5.00

5.50

6.00

6.50

7.00

7.50

Tbill AAA AA

1 Year Rates (%)

Nov-19 Dec-19 Jan-20

5.86

6.65

7.41

6.24

6.95

7.62

6.21

6.83

7.51

5.00

5.50

6.00

6.50

7.00

7.50

8.00

8.50

9.00

G-sec AAA AA

3 Year Rates (%)

Nov-19 Dec-19 Jan-20

6.19

7.14

7.80

6.47

7.17

7.80

6.59

7.15

7.79

5.00

6.00

7.00

8.00

G-sec AAA AA

5 Year Rates (%)

Nov-19 Dec-19 Jan-20

6.47

7.74

8.36

6.56

7.63

8.28

6.60

7.83

8.47

6.00

6.50

7.00

7.50

8.00

8.50

9.00

G-sec AAA AA

10 Year Rates (%)

Nov-19 Dec-19 Jan-20

YTD Data till January 2020Data Source: ICRA MFI Explorer

BnUSD

13

Fund Flows:FPI/ FII Inflow and Debt MF Inflow trend

10.4 7.9 6.4

-8.2

25.0

6.7

-6.2

23.3

-6.8

3.6

-2.0

43.6

55.0

82.876.5

98.5

65.5

46.6

59.5

46.9

74.5

5.5

-20

0

20

40

60

80

100

120

FII/FPI flows Debt MF flows

14

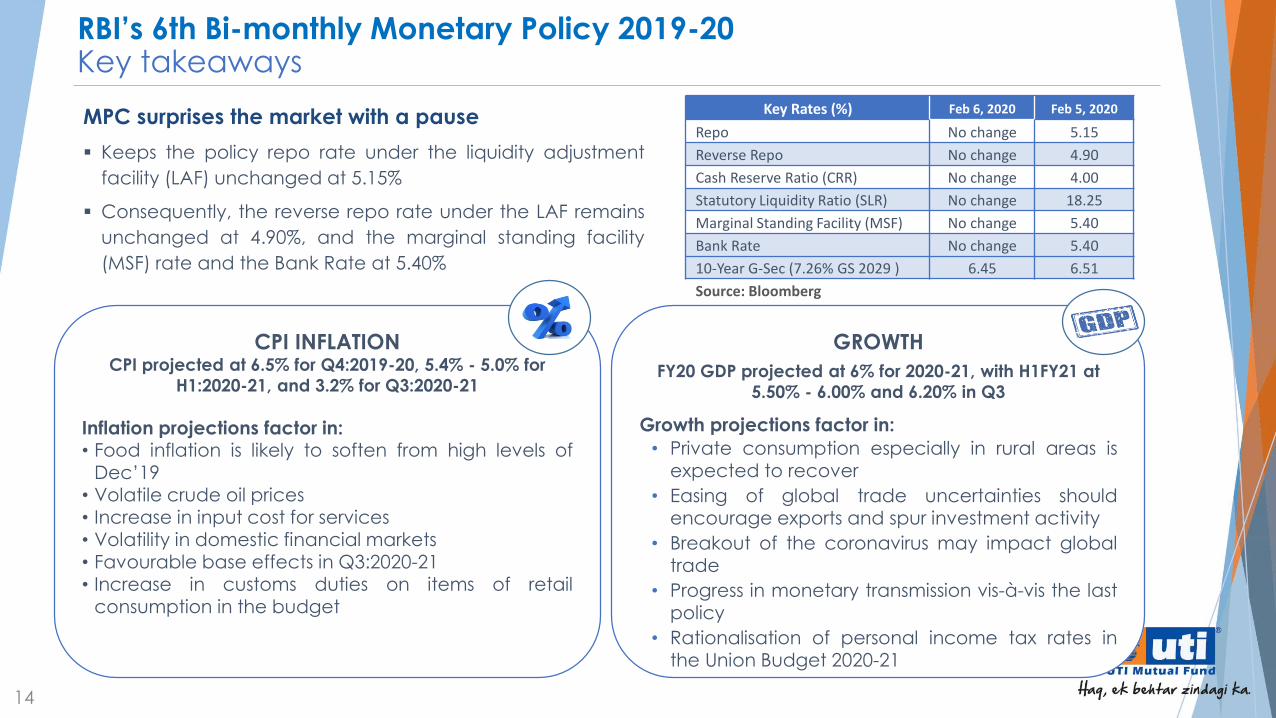

MPC surprises the market with a pause

Keeps the policy repo rate under the liquidity adjustment

facility (LAF) unchanged at 5.15%

Consequently, the reverse repo rate under the LAF remains

unchanged at 4.90%, and the marginal standing facility

(MSF) rate and the Bank Rate at 5.40%

Key Rates (%) Feb 6, 2020 Feb 5, 2020

Repo No change 5.15

Reverse Repo No change 4.90

Cash Reserve Ratio (CRR) No change 4.00

Statutory Liquidity Ratio (SLR) No change 18.25

Marginal Standing Facility (MSF) No change 5.40

Bank Rate No change 5.40

10-Year G-Sec (7.26% GS 2029 ) 6.45 6.51

Source: Bloomberg

CPI INFLATIONCPI projected at 6.5% for Q4:2019-20, 5.4% - 5.0% for

H1:2020-21, and 3.2% for Q3:2020-21

Inflation projections factor in: • Food inflation is likely to soften from high levels of

Dec’19• Volatile crude oil prices• Increase in input cost for services• Volatility in domestic financial markets• Favourable base effects in Q3:2020-21• Increase in customs duties on items of retail

consumption in the budget

GROWTH

FY20 GDP projected at 6% for 2020-21, with H1FY21 at

5.50% - 6.00% and 6.20% in Q3

Growth projections factor in:

• Private consumption especially in rural areas isexpected to recover

• Easing of global trade uncertainties shouldencourage exports and spur investment activity

• Breakout of the coronavirus may impact globaltrade

• Progress in monetary transmission vis-à-vis the lastpolicy

• Rationalisation of personal income tax rates inthe Union Budget 2020-21

RBI’s 6th Bi-monthly Monetary Policy 2019-20Key takeaways

In such a scenario, funds having a combination of income accrual and low to short term

duration would provide a good investment opportunity for the investors

Fixed Income:Current Market Outlook

15

The debt market reacted positively post policy announcement especially on the shorter end of yield curvewith 3 & 5-year g-sec segment saw a rally of 15 to 18 bps, while the 10-year G-Sec benchmark saw a rally of 6bps closing at 6.45%

Going forward, the markets will closely track the growth-inflation dynamics and would look forward to openingup of monetary policy space in the second half of the fiscal as inflation is expected to soften in H2 FY20-21. The10-year benchmark is expected to trade in the range of 6.20% to 6.60% for rest of the calendar year. On theglobal front markets will monitor the impact of corona virus on global growth, movement in crude oil prices,geo-political situation, currency movement, etc

An accommodative stance from RBI with ample and cheap liquidity in the system is expected to support theshorter end of the yield and hence funds with a focus on income accrual and low to shorter duration (up to 3years) are expected to remain attractive for investors

MPC maintained a status quo on rates. RBI announced a slew of developmental & regulatory measures whichincluded providing a revised liquidity management framework, incentivizing credit flow to sectors affected by aslowing economy and introducing long term repo operations for improving the monetary transmission

Measures announced by RBI is likely to provide ample liquidity in the system while kick starting the credit flowtowards the productive sectors of the economy. This is expected to have a multiplier effect and bolster growth.

Equity Outlook

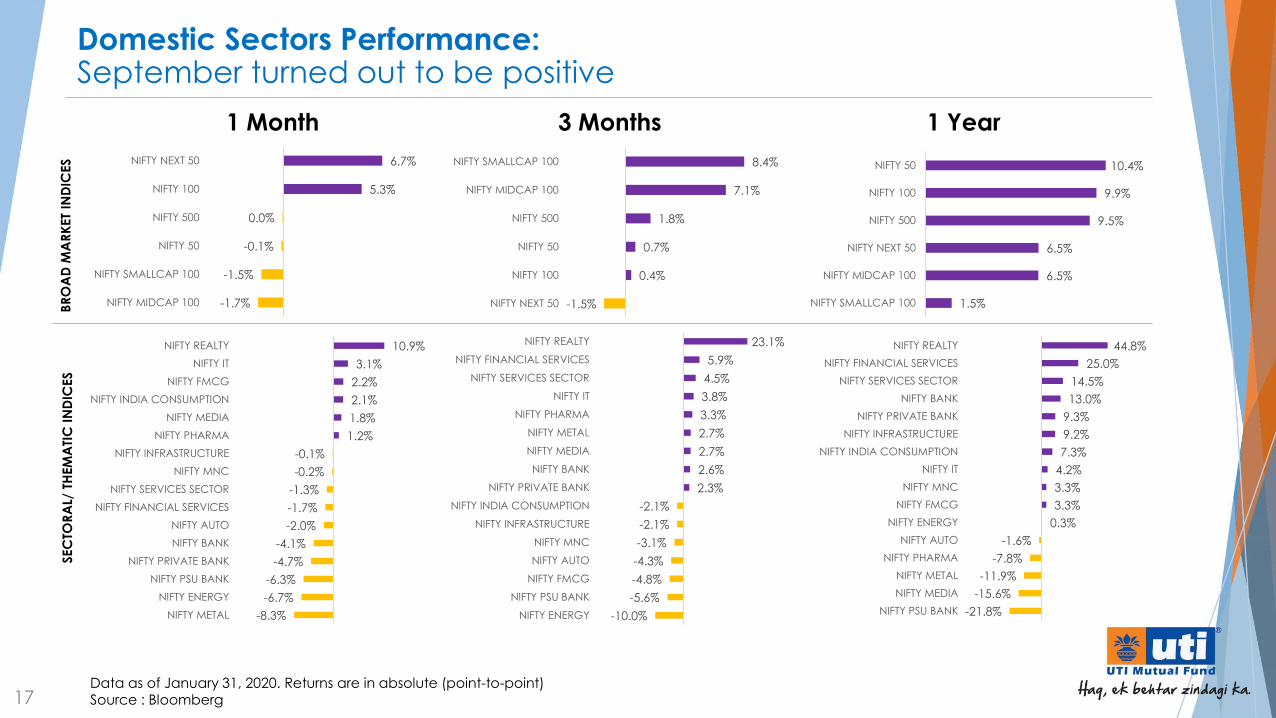

Data as of January 31, 2020. Returns are in absolute (point-to-point)Source : Bloomberg

Domestic Sectors Performance:September turned out to be positive

17

3 Months 1 Year1 Month

-1.5%

0.4%

0.7%

1.8%

7.1%

8.4%

NIFTY NEXT 50

NIFTY 100

NIFTY 50

NIFTY 500

NIFTY MIDCAP 100

NIFTY SMALLCAP 100

1.5%

6.5%

6.5%

9.5%

9.9%

10.4%

NIFTY SMALLCAP 100

NIFTY MIDCAP 100

NIFTY NEXT 50

NIFTY 500

NIFTY 100

NIFTY 50

-10.0%

-5.6%

-4.8%

-4.3%

-3.1%

-2.1%

-2.1%

2.3%

2.6%

2.7%

2.7%

3.3%

3.8%

4.5%

5.9%

23.1%

NIFTY ENERGY

NIFTY PSU BANK

NIFTY FMCG

NIFTY AUTO

NIFTY MNC

NIFTY INFRASTRUCTURE

NIFTY INDIA CONSUMPTION

NIFTY PRIVATE BANK

NIFTY BANK

NIFTY MEDIA

NIFTY METAL

NIFTY PHARMA

NIFTY IT

NIFTY SERVICES SECTOR

NIFTY FINANCIAL SERVICES

NIFTY REALTY

-21.8%

-15.6%

-11.9%

-7.8%

-1.6%

0.3%

3.3%

3.3%

4.2%

7.3%

9.2%

9.3%

13.0%

14.5%

25.0%

44.8%

NIFTY PSU BANK

NIFTY MEDIA

NIFTY METAL

NIFTY PHARMA

NIFTY AUTO

NIFTY ENERGY

NIFTY FMCG

NIFTY MNC

NIFTY IT

NIFTY INDIA CONSUMPTION

NIFTY INFRASTRUCTURE

NIFTY PRIVATE BANK

NIFTY BANK

NIFTY SERVICES SECTOR

NIFTY FINANCIAL SERVICES

NIFTY REALTY

BR

OA

D M

AR

KET

IND

ICES

-1.7%

-1.5%

-0.1%

0.0%

5.3%

6.7%

NIFTY MIDCAP 100

NIFTY SMALLCAP 100

NIFTY 50

NIFTY 500

NIFTY 100

NIFTY NEXT 50

SEC

TOR

AL/

TH

EM

ATI

C I

ND

ICES

-8.3%

-6.7%

-6.3%

-4.7%

-4.1%

-2.0%

-1.7%

-1.3%

-0.2%

-0.1%

1.2%

1.8%

2.1%

2.2%

3.1%

10.9%

NIFTY METAL

NIFTY ENERGY

NIFTY PSU BANK

NIFTY PRIVATE BANK

NIFTY BANK

NIFTY AUTO

NIFTY FINANCIAL SERVICES

NIFTY SERVICES SECTOR

NIFTY MNC

NIFTY INFRASTRUCTURE

NIFTY PHARMA

NIFTY MEDIA

NIFTY INDIA CONSUMPTION

NIFTY FMCG

NIFTY IT

NIFTY REALTY

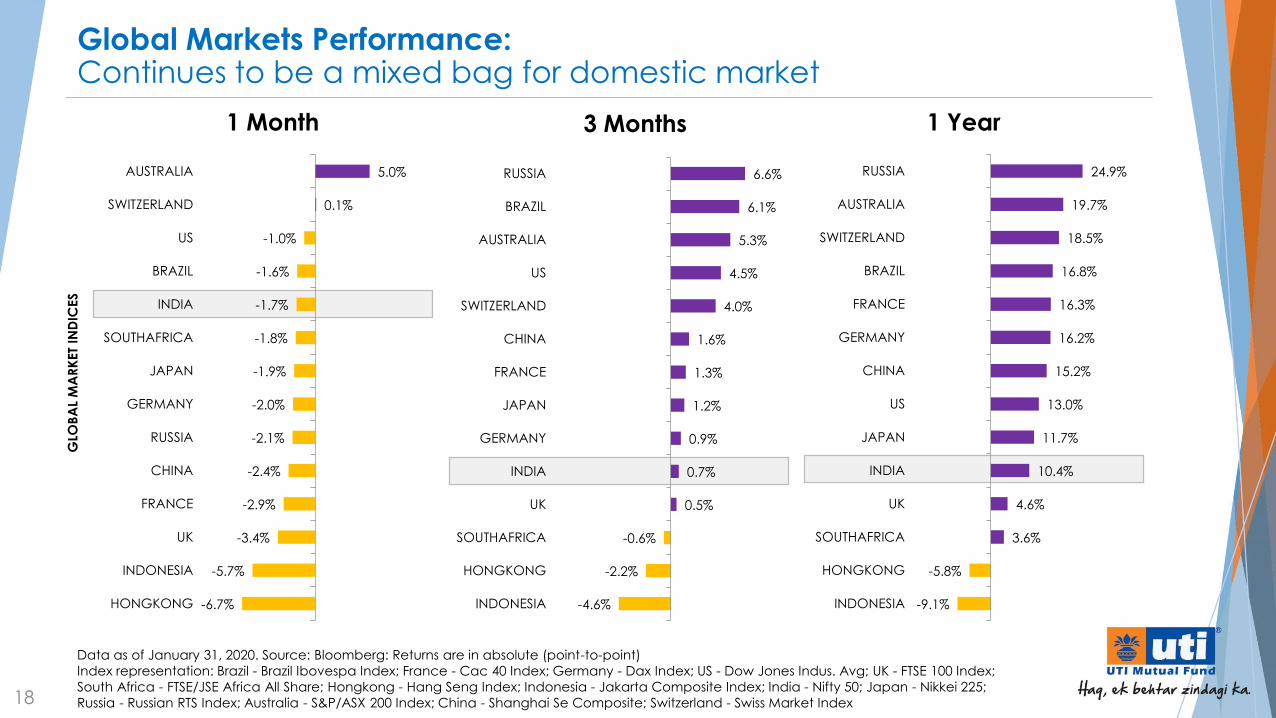

Data as of January 31, 2020. Source: Bloomberg: Returns are in absolute (point-to-point)

Index representation: Brazil - Brazil Ibovespa Index; France - Cac 40 Index; Germany - Dax Index; US - Dow Jones Indus. Avg; UK - FTSE 100 Index;

South Africa - FTSE/JSE Africa All Share; Hongkong - Hang Seng Index; Indonesia - Jakarta Composite Index; India - Nifty 50; Japan - Nikkei 225;

Russia - Russian RTS Index; Australia - S&P/ASX 200 Index; China - Shanghai Se Composite; Switzerland - Swiss Market Index

Global Markets Performance:Continues to be a mixed bag for domestic market

18

3 Months 1 Year1 Month

GLO

BA

L M

AR

KET

IND

ICES

-6.7%

-5.7%

-3.4%

-2.9%

-2.4%

-2.1%

-2.0%

-1.9%

-1.8%

-1.7%

-1.6%

-1.0%

0.1%

5.0%

HONGKONG

INDONESIA

UK

FRANCE

CHINA

RUSSIA

GERMANY

JAPAN

SOUTHAFRICA

INDIA

BRAZIL

US

SWITZERLAND

AUSTRALIA

-4.6%

-2.2%

-0.6%

0.5%

0.7%

0.9%

1.2%

1.3%

1.6%

4.0%

4.5%

5.3%

6.1%

6.6%

INDONESIA

HONGKONG

SOUTHAFRICA

UK

INDIA

GERMANY

JAPAN

FRANCE

CHINA

SWITZERLAND

US

AUSTRALIA

BRAZIL

RUSSIA

-9.1%

-5.8%

3.6%

4.6%

10.4%

11.7%

13.0%

15.2%

16.2%

16.3%

16.8%

18.5%

19.7%

24.9%

INDONESIA

HONGKONG

SOUTHAFRICA

UK

INDIA

JAPAN

US

CHINA

GERMANY

FRANCE

BRAZIL

SWITZERLAND

AUSTRALIA

RUSSIA

Equity Mutual Fund Inflows include Arbitrage Funds, Equity Mutual Fund Inflows in CY 2020 as of Jan-20Data Source: AMFI. Mutual Funds (Equity & ELSS Schemes)FII (Foreign Institutional Investors)

Fund Flows:FPI/ FII Inflow and Equity MF Inflow trend

BnUSD

19

29.3

-0.5

24.5

19.8

16.2

3.3 2.9

8.0

-4.6

14.2

1.4

-3.1

1.6

-2.9-1.8

8.0

13.6

7.8

22.8

19.9

10.1

1.1

-15

-10

-5

0

5

10

15

20

25

30

FPI/ FII Inflow Equity MF Inflow

Source: Bloomberg. Data as of January 09, 2020The vertical axis is on a logarithmic scale Nifty 50, EPS: Earnings per share.CAGR: Compound annual growth rate

Earnings Trend:Forecast suggest Acceleration

20

78 92

131 161

172 225

268

240

251 314

341

356

399

400

389

413

454

486

551 694

Ma

r-92

Ma

r-93

Ma

r-94

Ma

r-95

Ma

r-96

Ma

r-97

Ma

r-98

Ma

r-99

Ma

r-00

Ma

r-01

Ma

r-02

Ma

r-03

Ma

r-04

Ma

r-05

Ma

r-06

Ma

r-07

Ma

r-08

Ma

r-09

Ma

r-10

Ma

r-11

Ma

r-12

Ma

r-13

Ma

r-14

Ma

r-15

Ma

r-16

Ma

r-17

Ma

r-18

Ma

r-19

Ma

r-20

E

Ma

r-21

E

Nifty

50

EP

S

13% 26%7%

S&P BSE Sensex EPS Trend Nifty 50 EPS Trend

Source: Bloomberg. Data as of February 07, 2020

Continued downgrades even after recent tax cuts

21

Nifty

50

EP

STrend in Consensus Nifty 50 EPS

533

500

550

600

650

700

750

800

850

900

Apr-17 Aug-17 Dec-17 Apr-18 Aug-18 Dec-18 Apr-19 Aug-19 Dec-19

FY19 FY20 FY21

551

694

Feb-20

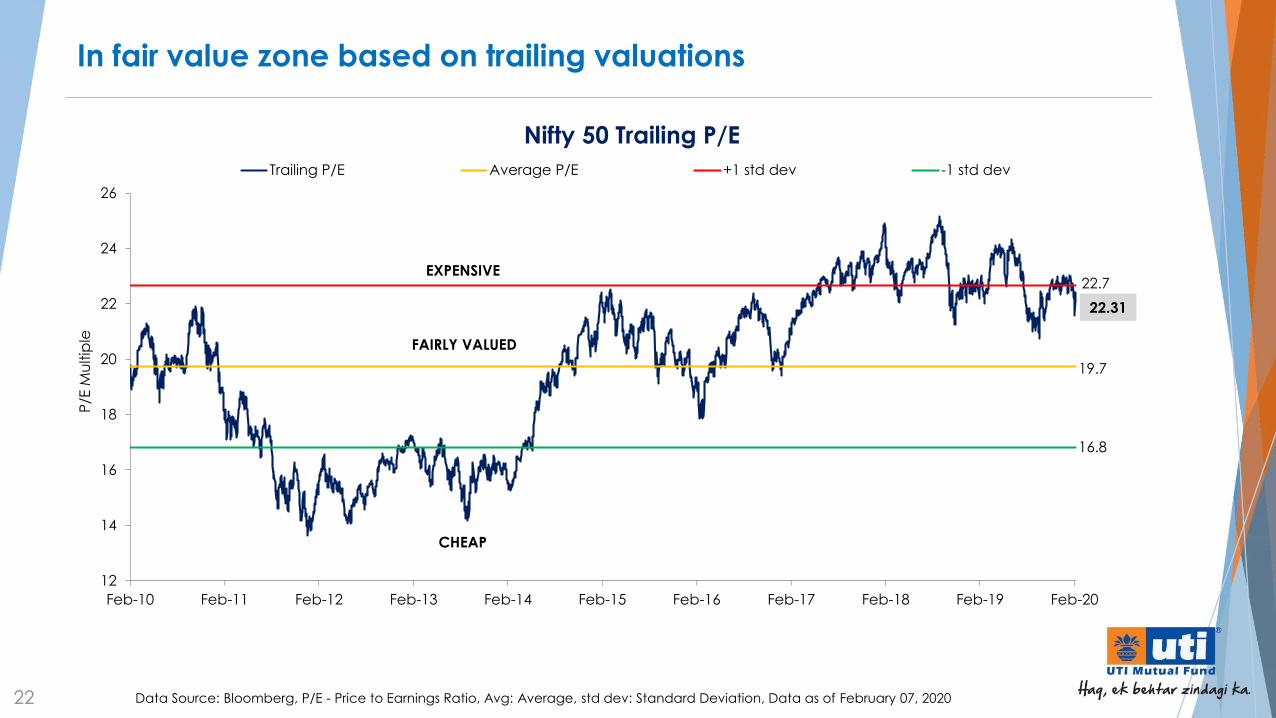

In fair value zone based on trailing valuations

22 Data Source: Bloomberg, P/E - Price to Earnings Ratio, Avg: Average, std dev: Standard Deviation, Data as of February 07, 2020

P/E

Mu

ltip

le

FAIRLY VALUED

EXPENSIVE

CHEAP

Nifty 50 Trailing P/E

12

14

16

18

20

22

24

26

Feb-10 Feb-11 Feb-12 Feb-13 Feb-14 Feb-15 Feb-16 Feb-17 Feb-18 Feb-19 Feb-20

Trailing P/E Average P/E +1 std dev -1 std dev

22.7

19.7

16.8

22.31

23 Data Source: Bloomberg, P/E - Price to Earnings Ratio, Avg: Average, std dev: Standard Deviation, Data as of February 07, 2020

P/E

Mu

ltip

le FAIRLY VALUED

EXPENSIVE

CHEAP

Nifty 50 Forward P/E

Sep-19 rally has moved Nifty forward P/E into expensive zone

10

12

14

16

18

20

Feb-10 Feb-11 Feb-12 Feb-13 Feb-14 Feb-15 Feb-16 Feb-17 Feb-18 Feb-19 Feb-20

Forward P/E Average P/E +1 std dev -1 std dev

17.4

15.6

13.7

17.97

P/B in fair value zone; awaiting mean reversion in RoE

24 Data Source: Bloomberg, P/B - Price to Book Ratio, Avg: Average, std dev: Standard Deviation, Data as of January 09, 2020

Nifty 50 Trailing P/B Nifty 50 Return on Equity (RoE)

CHEAP

12.42

Ro

E

1.5

2.0

2.5

3.0

3.5

4.0

Feb-10 Feb-12 Feb-14 Feb-16 Feb-18 Feb-20

Trailing P/B Average P/B +1 std dev -1 std dev

P/B

Mu

ltip

le

FAIRLY VALUED

EXPENSIVE

3.0

2.7

2.4

2.87

10

11

12

13

14

15

16

17

18

19

20

Feb-10 Feb-12 Feb-14 Feb-16 Feb-18 Feb-20

Return on Equity

Equities are in the attractive zone relative to gilts

25 Data Source: Yield difference is difference of Nifty Yield (1/Forward P/E) and 10 year G-sec yield. Data as of February 07, 2020

Nifty 50 Yield vs 10 Year G-Sec Yield

(5)

(4)

(3)

(2)

(1)

-

1

2

3

4

5

6

Feb-06 Feb-07 Feb-08 Feb-09 Feb-10 Feb-11 Feb-12 Feb-13 Feb-14 Feb-15 Feb-16 Feb-17 Feb-18 Feb-19 Feb-20

Yield Difference Avg. Yield Differnce

Current Yield difference is -0.87%

10 Year Average Yield difference is -1.00%

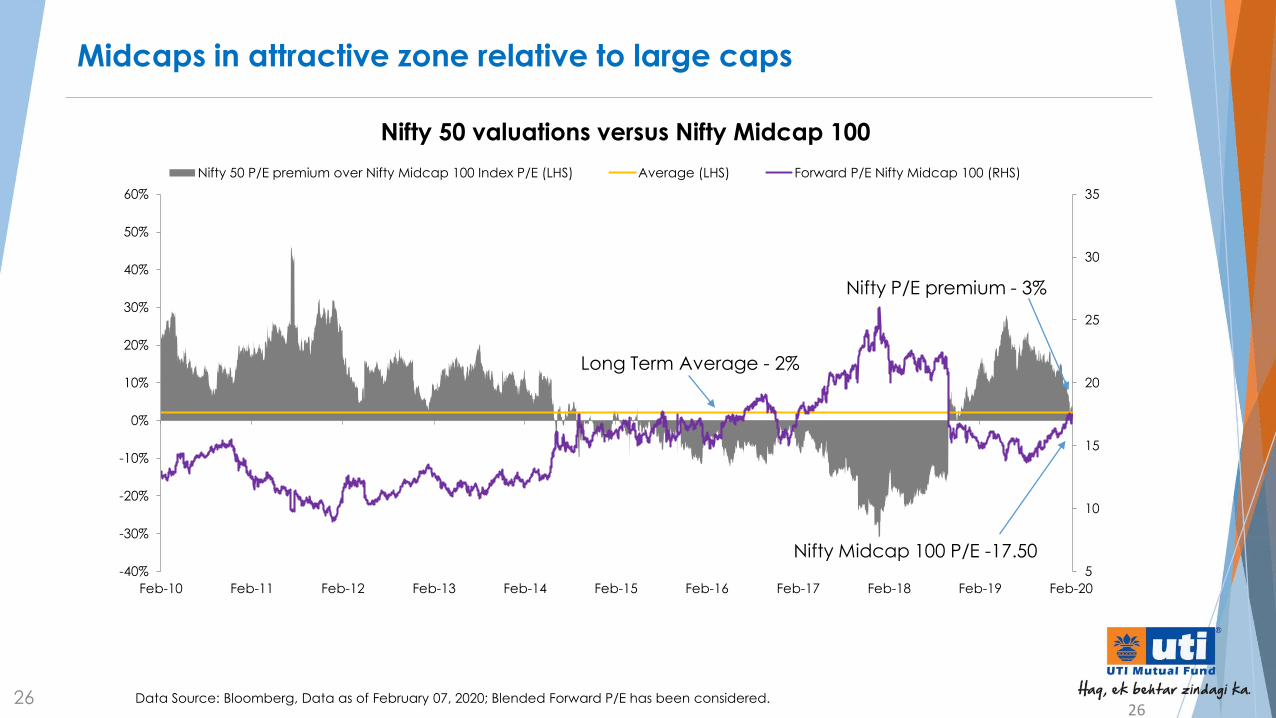

2626 Data Source: Bloomberg, Data as of February 07, 2020; Blended Forward P/E has been considered.

Midcaps in attractive zone relative to large caps

Nifty 50 valuations versus Nifty Midcap 100

5

10

15

20

25

30

35

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

Feb-10 Feb-11 Feb-12 Feb-13 Feb-14 Feb-15 Feb-16 Feb-17 Feb-18 Feb-19 Feb-20

Nifty 50 P/E premium over Nifty Midcap 100 Index P/E (LHS) Average (LHS) Forward P/E Nifty Midcap 100 (RHS)

Nifty P/E premium - 3%

Nifty Midcap 100 P/E -17.50

Long Term Average - 2%

Equity Markets:Current Market Outlook

27 GDP – Gross Domestic Product; CPI – Consumer Price Index; P/E – Price to Earnings

The disruption from Coronavirus Disease 2019 (COVID-19) virus outbreak is threat to Chinese and Global growth

Nifty Midcap 100 index discount to the Nifty 50 index on forward P/E has narrowed through it remains favourable

Despite the uptick in CPI, Monetary policy in India remains accommodative

Growth trends remain weak in India and GDP estimates for FY20 have been cut sharply to 5%

RBI is using other tools in its armoury to improve credit availability

There is significant divergence in valuations and performance in the both the large and midcap space

Bottom up stock-picking remains the key to Alpha

Product Positioning

Eq

uity

& I

nd

ex Diversified Funds

Liq

uid

& D

eb

tH

yb

rid

&So

lutio

ns

Thematic Fund

Sector

Index & ETFs

Large Cap

UTI Mastershare Unit Scheme

Multi Cap

UTI Equity Fund

Large & Mid Cap

UTI Core Equity Fund

Mid Cap

UTI Mid Cap Fund

Infrastructure

UTI Infrastructure Fund

MNC

UTI MNC Fund

Lifestyle

UTI India Consumer Fund

Banking & Financial

UTI B&FS Fund

Healthcare

UTI Healthcare Fund

Transportation & Logistics

UTI T&L Fund

Index – Nifty 50

UTI Nifty Index (Fund & ETF)

Index – Nifty Next 50

UTI Nifty Next 50 (Fund & ETF)

Index – S&P BSE Sensex

UTI Sensex ETF

Index- S&P BSE Sensex Next 50

UTI S&P BSE Sensex Next 50ETF

Dividend Yield

UTI Dividend Yield Fund

Value

UTI Value Opportunities Fund

Accrual

Duration

Credit

Hybrid

Solutions

Product Bouquet: An Overview

Liquid

UTI Liquid Cash Plan

Overnight

UTI Overnight Fund

Money Market

UTI Money Market Fund

Ultra Short Term

UTI Ultra Short Term Fund

Floater Fund

UTI Floater Fund

Banking & PSU Debt

UTI Banking & PSU Debt Fund

Short Term

UTI Short Term Income Fund

Corporate Bond

UTI Corporate Bond Fund

Dynamic Bond

UTI Dynamic Bond Fund

Medium to Long Term

UTI Bond Fund

Gilt

UTI Gilt Fund

Low Duration

UTI Treasury Advantage Fund

Credit Risk

UTI Credit Risk Fund

Medium Term

UTI Medium Term Fund

Conservative Hybrid

UTI Regular Savings Fund

Aggressive Hybrid

UTI Hybrid Equity Fund

Multi Asset Fund

UTI Multi Asset Fund

Arbitrage

UTI Arbitrage Fund

Equity Savings

UTI Equity Savings Fund

Children’s Fund

UTI CCF (Savings & Investment)

Retirement

UTI Retirement Benefit PF UTI ULIP

ELSS

UTI LTEF (Tax Saving)

Gold ETF

UTI Gold ETF

29

Equity – Products

UTI MastershareUnit Scheme

UTI Core Equity Fund

UTI Equity Fund

UTI Value Opportunities Fund

UTI Mid Cap Fund

Market Capitalisation

Large Cap Mid Cap Small Cap Scheme Characteristics

Min. 80% in Large Cap Stocks

Min. 35% in Large & Mid Cap each

Investing across the Market Caps

Following Value investment Strategy

Min. 65% in Mid Cap Stocks

30

Fixed Income – Product Positioning : Duration vis-a-vis Credit Quality

1 day 3 to 4 yrs0 to 3 mths

3 to 6 mths

6 to 12 mths

1 to 3 years

4 to 7 yrs 7+ yrs

CREDIT ORIENTEDAAA/AA+: <=35%

AA/AA-/A : 65% >=

MODERATE QUALITYAAA/AA+: 50% to 70%

AA/ AA-/ A : 30% to 50%

HIGH QUALITYAAA/ AA+ : 80% >= AA/ AA-/ A: <= 20%

HIGHEST QUALITYAAA/AA+ : 95% >=,AA/ AA-/ A : <= 5%

DURATION BUCKET

CREDITQUALITY

UTI

OVERNIGHT

FUND

UTI LIQUID

CASH PLAN

UTI ULTRA

SHORT

TERM FUND

UTI

FLOATER

FUND

UTI TREASURY

ADVTG FUND

UTI MONEY

MKT FUND

UTI B&PSUD

FUND

UTI SHORT TERM

INCOME FUNDUTI BOND

FUND

UTI CREDIT

RISK FUND

UTI GILT FUND

UTI DYNAMIC

BOND FUND

UTI MEDIUM

TERM FUND

31

UTI CORPORATE

BOND FUND

Hybrid - bucketing by Scheme Characteristics

UTI CCF – Savings Plan

UTI RBPF

UTI Regular Savings Fund

Debt : 60% to 100%

Equity : 0% to 40%

Debt : 75% to 90%

Equity : 10% to 25%

Debt : 60% to 100%

Equity : 0% to 40%

UTI Hybrid Equity Fund Equity : 65% to 80%

Debt : 20% to 35%

UTI Arbitrage Fund Equity : 65% to 100%

Derivatives : 65% to 100%

UTI Multi-Asset Fund*Equity : 65% to 100%

Debt : 10%to 25%

Gold : 10% to 25%

UTI CCF – Investment PlanEquity : 70% to 100%

Debt : 0% to 30%

Arbitrage

Multi Asset

Hybrid Aggressive

Solution Children

Solution Retirement

Hybrid Conservative

Solution Children

UTI ULIP@ Dynamic Allocation Debt : 60% to 100%

Equity : 0% to 40%

3

4

1

6

7

8

9

*of which Cash future arbitrage opportunities 20% to 75%, Net long equity position 20% to 50%@ subject to SEBI approval

UTI Equity Savings Fund Equity : 65% to 90%*

Debt : 10% to 35% Equity Savings5

32

2

Name of the Scheme This product is suitable for investors who are seeking* Riskometer

UTI Mastershare Unit Scheme

(Large Cap Fund- An open ended equity scheme

predominantly investing in large cap stocks)

• Long term capital appreciation

• Investment predominantly in equity instruments of large cap

companies

UTI Core Equity Fund

(Large & Mid Cap Fund- An open ended equity scheme

investing in both large cap and mid cap stocks)

• Long term capital appreciation

• Investment predominantly in equity instruments of both large cap

and mid cap companies

UTI Mid Cap Fund

(Mid Cap Fund- An open ended equity scheme

predominantly investing in mid cap stocks)

• Long term capital appreciation

• Investment predominantly in mid cap companies

UTI Value Opportunities Fund

(An open ended equity scheme following a value

investment strategy)

• Long term capital appreciation

• Investment in equity instruments following a value investment

strategy across the market capitalization spectrum

UTI Equity Fund

(Multi Cap Fund- An open ended equity scheme investing

across large cap, mid cap, small cap stocks)

• Long term capital appreciation

• Investment in equity instruments of companies with good growth

prospects across the market capitalization spectrum

UTI Dividend Yield Fund

(An open ended equity scheme predominantly investing in

dividend yielding stocks)

• Long term capital appreciation

• Investment predominantly in dividend yielding equity and equity

related securities

UTI Infrastructure Fund

(An open ended equity scheme following the

Infrastructure theme)

• Long term capital appreciation

• Investment predominantly in equity and equity related securities of

companies forming part of the infrastructure sector

UTI MNC Fund

(An open ended equity following the theme of investing

predominantly in equity and equity related securities of

Multi-National Companies)

• Long term capital appreciation

• Investment predominantly in equity and equity related securities of

Multi-National companies

UTI India Consumer Fund

(An open ended equity scheme following the theme of

changing consumer aspirations, changing lifestyle and

growth of consumption)

• Long term capital growth

• Investment in equity instruments of companies that are expected to

benefit from of the changing consumer aspirations, changing

lifestyle and growth of consumption

Product Label

*Investors should consult their financial advisers if in doubt about whether the product is suitable for them.

33

Name of the Scheme This product is suitable for investors who are seeking* Riskometer

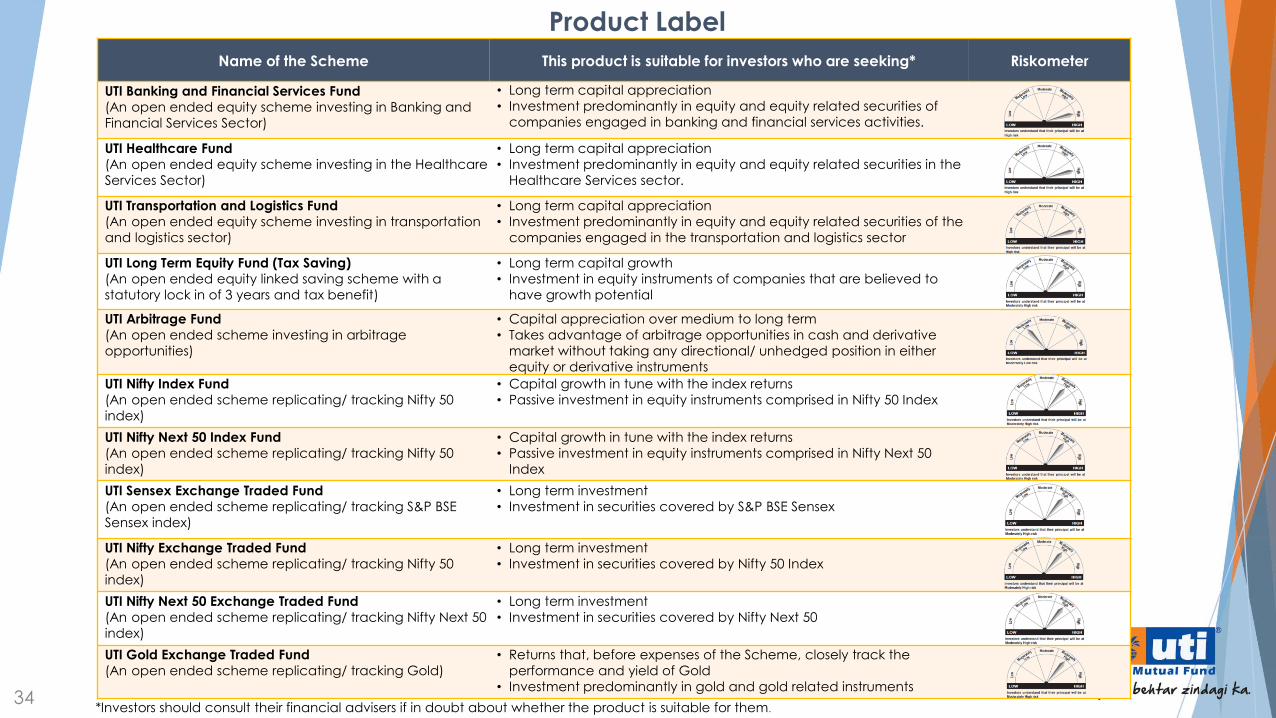

UTI Banking and Financial Services Fund

(An open ended equity scheme investing in Banking and

Financial Services Sector)

• Long term capital appreciation

• Investment predominantly in equity and equity related securities of

companies engaged in banking and financial services activities.

UTI Healthcare Fund

(An open ended equity scheme investing in the Healthcare

Services Sector)

• Long term capital appreciation

• Investment predominantly in equity and equity related securities in the

Healthcare Services sector.

UTI Transportation and Logistics Fund

(An open ended equity scheme investing in transportation

and logistics sector)

• Long term capital appreciation

• Investment predominantly in equity and equity related securities of the

companies engaged in the transportation and logistics sector

UTI Long Term Equity Fund (Tax Saving)

(An open ended equity linked saving scheme with a

statutory lock in of 3 years and tax benefit)

• Long term capital growth

• Investment in equity instruments of companies that are believed to

have growth potential

UTI Arbitrage Fund

(An open ended scheme investing in arbitrage

opportunities)

• Capital appreciation over medium to long term

• Takes advantage of arbitrage opportunities in cash and derivative

market without taking any directional/ unhedged position in either

equity or derivative instruments

UTI Nifty Index Fund

(An open ended scheme replicating/ tracking Nifty 50

index)

• Capital growth in tune with the index returns

• Passive investment in equity instruments comprised in Nifty 50 Index

UTI Nifty Next 50 Index Fund

(An open ended scheme replicating/ tracking Nifty 50

index)

• Capital growth in tune with the index returns

• Passive investment in equity instruments comprised in Nifty Next 50

Index

UTI Sensex Exchange Traded Fund

(An open ended scheme replicating/ tracking S&P BSE

Sensex index)

• Long term investment

• Investment in securities covered by S&P BSE Sensex

UTI Nifty Exchange Traded Fund

(An open ended scheme replicating/ tracking Nifty 50

index)

• Long term investment

• Investment in securities covered by Nifty 50 Index

UTI Nifty Next 50 Exchange Traded Fund

(An open ended scheme replicating/ tracking Nifty Next 50

index)

• Long term investment

• Investment in securities covered by Nifty Next 50

UTI Gold Exchange Traded Fund

(An open ended scheme replicating/ tracking Gold)

• Returns that, before expenses of the Scheme, closely track the

performance and yield of Gold

• Investment predominantly in gold and gold related instruments

Product Label

*Investors should consult their financial advisers if in doubt about whether the product is suitable for them.34

Name of the Scheme This product is suitable for investors who are seeking* Riskometer

UTI Overnight Fund

(An open ended debt scheme investing in overnight securities)

• Reasonable income over one day with capital preservation

• Investment in overnight securities

UTI Liquid Cash Plan

(An open ended liquid scheme)• Steady and reasonable income over short-term with capital

preservation.

• Investment in money market securities & high quality debt

UTI Ultra Short Term Fund

(An open ended ultra-short term debt scheme investing in instruments such

that the Macaulay duration of the portfolio is between 3 months and 6

months)

• Reasonable income with low volatility over short term

• Investment in debt & money market instruments

UTI Treasury Advantage Fund

(An open ended low duration debt scheme investing in instruments such that

the Macaulay duration of the portfolios is between 6 months and 12 months)

• Reasonable income consistent with high liquidity over short term

• Investment in Debt & Money Market instruments

UTI Money Market Fund

(An open ended debt scheme investing in money market

instruments)

• Reasonable income with high level of liquidity over short-term

• Investment in money market securities

UTI Corporate Bond Fund

(An open ended debt scheme predominantly investing in AA+ and

above rated corporate bonds)

• Optimal returns over the medium to long term

• To invest predominantly in AA+ and above rated corporate debt

UTI Short Term Income Fund

(An Open ended Short Term Debt Scheme investing in instruments such that

the Macaulay duration of portfolio is between 1 year and 3 years)

• Reasonable income with low risk and high level of liquidity over

short-term

• Investment in Debt & Money Market instrument

UTI Medium Term Fund

(An open ended medium term debt scheme investing in instruments such

that the Macaulay duration of the portfolio is between 3 years and 4 years)

• Reasonable income over the medium to long term

• Investment in Debt & Money Market Instruments

UTI Bond Fund

(An open ended medium term debt scheme investing in instruments such

that the Macaulay duration of the portfolio is between 4 years and 7 years)

• Optimal returns with adequate liquidity over medium to long term

• Investment in Debt & money market instruments

UTI Dynamic Bond Fund

(An open ended dynamic debt scheme investing across duration)

• Optimal returns with adequate liquidity over medium to long term

• Investment in Debt & Money Market Instruments

UTI Credit Risk Fund

(An open ended debt scheme predominantly investing in AA and below

rated corporate bonds (excluding AA+ rated corporate bonds))

• Reasonable income and capital appreciation over medium to

long term

• Investment in debt and money market instruments

Product Label

*Investors should consult their financial advisers if in doubt about whether the product is suitable for them.35

Name of the Scheme This product is suitable for investors who are seeking* Riskometer

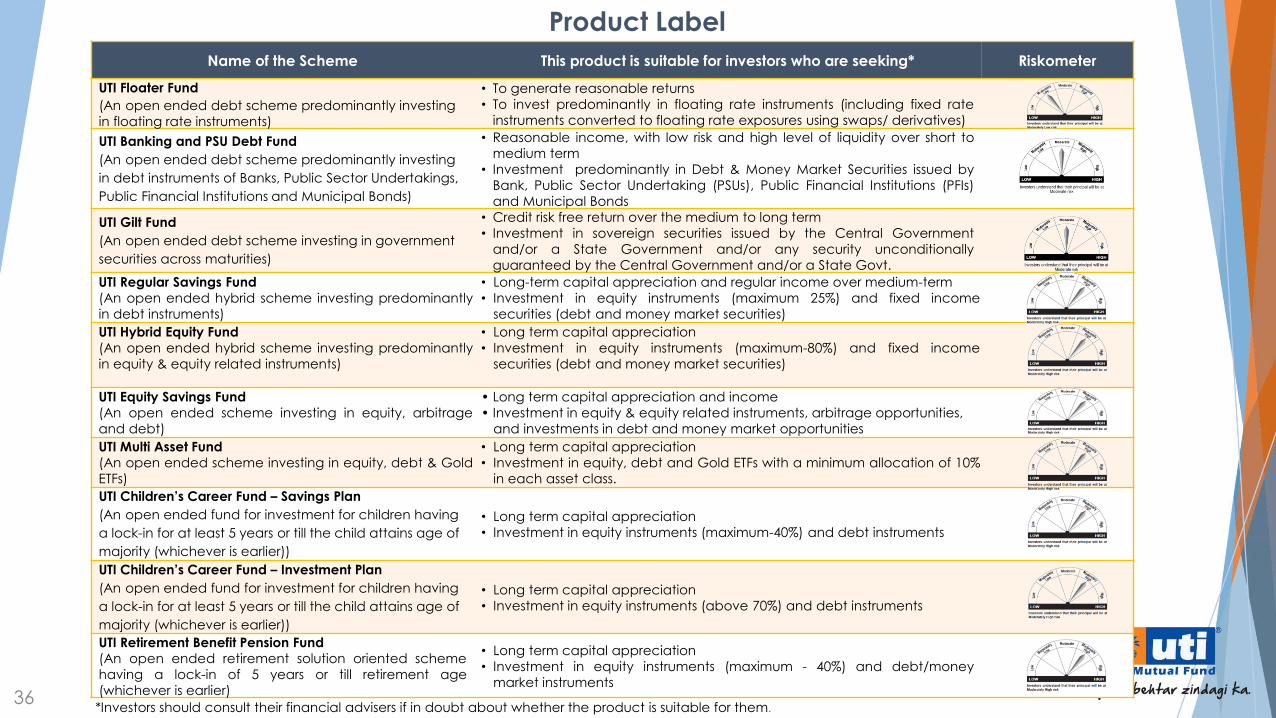

UTI Floater Fund

(An open ended debt scheme predominantly investing

in floating rate instruments)

• To generate reasonable returns

• To invest predominantly in floating rate instruments (including fixed rate

instruments converted to floating rate exposures using swaps/ derivatives)

UTI Banking and PSU Debt Fund

(An open ended debt scheme predominantly investing

in debt instruments of Banks, Public Sector Undertakings,

Public Financial Institutions and Municipal Bonds)

• Reasonable income, with low risk and high level of liquidity over short to

medium term

• Investment predominantly in Debt & Money Market Securities issued by

Bank, Public Sector Undertaking (PSUs), Public Financial Institutions (PFIs)

and Municipal Bonds

UTI Gilt Fund

(An open ended debt scheme investing in government

securities across maturities)

• Credit risk free return over the medium to long term

• Investment in sovereign securities issued by the Central Government

and/or a State Government and/or any security unconditionally

guaranteed by the Central Government and/or a State Govt.

UTI Regular Savings Fund

(An open ended hybrid scheme investing predominantly

in debt instruments)

• Long-term capital appreciation and regular income over medium-term

• Investment in equity instruments (maximum 25%) and fixed income

securities (debt and money market securities)

UTI Hybrid Equity Fund

(An open ended hybrid scheme investing predominantly

in equity & equity related instruments)

• Long term capital appreciation

• Investment in equity instruments (maximum-80%) and fixed income

securities (debt and money market securities)

UTI Equity Savings Fund

(An open ended scheme investing in equity, arbitrage

and debt)

• Long term capital appreciation and income

• Investment in equity & equity related instruments, arbitrage opportunities,

and investments in debt and money market opportunities

UTI Multi Asset Fund

(An open ended scheme investing in equity, debt & Gold

ETFs)

• Long term capital appreciation

• Investment in equity, debt and Gold ETFs with a minimum allocation of 10%

in each asset class.

UTI Children’s Career Fund – Savings Plan

(An open ended fund for investment for children having

a lock-in for at least 5 years or till the child attains age of

majority (whichever is earlier))

• Long term capital appreciation

• Investment in equity instruments (maximum-40%) and debt instruments

UTI Children’s Career Fund – Investment Plan

(An open ended fund for investment for children having

a lock-in for at least 5 years or till the child attains age of

majority (whichever is earlier))

• Long term capital appreciation

• Investment in equity instruments (above 70%) and debt instruments

UTI Retirement Benefit Pension Fund

(An open ended retirement solution oriented scheme

having a lock-in of 5 years or till retirement age

(whichever is earlier)

• Long term capital appreciation

• Investment in equity instruments (maximum - 40%) and debt/money

market instruments

*Investors should consult their financial advisers if in doubt about whether the product is suitable for them.

Product Label

36

AMFI: Association of Mutual Funds of India

Avg. Average

Bn: Billion

BoJ: Bank of Japan

BoP: Balance of Payments

CAD: Current Account Deficit

CAGR: Compounded Annualized Growth Rate

CP: Commercial Papers

CPI(IW): CPI Industrial Workers

CPI: Consumer Price Index

CPOS: Capital Protection Oriented Scheme

CSO: Central Statistical Office

Dual Adv. FTF: Dual Advantage Fixed Term Fund

EBITDA: Earning Before Interest, Tax, Depreciation, Amortization

ECB: External Commercial Borrowing

ELSS: Equity Linked Savings Scheme

EPS: Earnings Per Share

FD: Fiscal Deficit

FMPs: Fixed Maturity Plans

Forex: Foreign exchange

FTIF: Fixed Term Income Fund

FY: Financial Year

GDP: Gross Domestic Product

GVA: Gross Value Added

Abbreviations

GST: Goods & Services Tax

IIP: Index of Industrial Production

INR: Indian Rupee

MF: Mutual Fund

MOSPI: Ministry of Statistics and Programme Implementation

P/E: Price to Earning Multiple

RBI: Reserve Bank of India

SEBI: Securities & Exchange Board of India

US Fed/Fed: US Federal Reserve

USD: US Dollar

vs: Versus

WPI: Wholesale Price Index

YoY: Year on Year

37

Thank You

REGISTERED OFFICE: UTI Tower, ‘Gn’ Block, Bandra Kurla Complex, Bandra (E), Mumbai - 400051. Phone: 022 – 66786666. UTI Asset Management

Company Ltd (Investment Manager for UTI Mutual Fund) Email: [email protected] . (CIN-U65991MH2002PLC137867). For more information, please

contact the nearest UTI Financial Centre or your AMFI/NISM certified UTI Mutual Fund Independent Financial Advisor (IFA) for a copy of the

Statement of Additional Information, Scheme Information Document and Key Information Memorandum cum Application Form.

Mutual Fund Investments are subject to market risks, read all scheme related documents carefully