Embed Size (px)

Citation preview

UTC Investor and Analyst Meeting

March 10, 2016

Note: All results and expectations in this presentation reflect continuing operations unless otherwise noted.

Cautionary Statement:

This presentation includes statements that constitute “forward-looking statements” under the securities laws. Forward-looking statements often contain words such as “believe,” “expect,”

“expectations,” “plans,” “strategy,” “project,” “prospects,” “estimate,” “target,” “anticipate,” “will,” “should,” “see,” “guidance,” “confident” and similar terms. Forward-looking statements may include,

among other things, statements relating to future sales, earnings, cash flow, results of operations, uses of cash, share repurchases and other measures of financial performance or potential future

plans, strategies or transactions. All forward-looking statements involve risks, uncertainties and other factors that may cause actual results to differ materially from those expressed or implied in the

forward-looking statements. Such risks, uncertainties and other factors include, without limitation: the effect of economic conditions in the industries and markets in which we operate in the U.S. and

globally and any changes therein, including financial market conditions, fluctuations in commodity prices, interest rates and foreign currency exchange rates, levels of end market demand in

construction and in both the commercial and defense segments of the aerospace industry, levels of air travel, financial condition of commercial airlines, changes in government procurement priorities

and funding, the impact of weather conditions and natural disasters and the financial condition of our customers and suppliers; challenges in the development, production, delivery, support,

performance and realization of the anticipated benefits of advanced technologies and new products and services; future levels of indebtedness and capital spending and research and development

spending; future availability of credit and factors that may affect such availability, including credit market conditions and our capital structure; delays and disruption in delivery of materials and services

from suppliers; customer- and company-directed cost reduction efforts and restructuring costs and savings and other consequences thereof; the scope, nature, impact or timing of acquisition and

divestiture activity, including among other things integration of acquired businesses into our existing businesses and realization of synergies and opportunities for growth and innovation; new business

opportunities; our ability to realize the intended benefits of organizational changes; the anticipated benefits of diversification and balance of operations across product lines, regions and industries; the

timing and scope of future repurchases of our common stock; the outcome of legal proceedings, investigations and other contingencies; pension plan assumptions and future contributions; the impact

of the negotiation of collective bargaining agreements and labor disputes; the effect of changes in political conditions in the U.S. and other countries in which we operate; and the effect of changes in

tax, environmental, regulatory (including among other things import/export) and other laws and regulations in the U.S. and other countries in which we operate. The forward-looking statements speak

only as of the date of this presentation and we undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as

required by applicable law. Additional information as to factors that may cause actual results to differ materially from those expressed or implied in the forward-looking statements is disclosed from time

to time in our reports on Forms 10-K, 10-Q and 8-K filed with or furnished to the SEC from time to time, including, but not limited to, the information included in UTC's Forms 10-K and 10-Q under the

headings “Business,” “Risk Factors,” “Management's Discussion and Analysis of Financial Condition and Results of Operations” and “Legal Proceedings” and in the notes to the financial statements

included in UTC's Forms 10-K and 10-Q.

United Technologies

Priorities Flawless execution

Innovation for growth

Structural cost reduction

Disciplined capital allocation

2:00 – 2:05 Opening Remarks Hayes

2:05 – 2:20 Financial Overview Johri

2:20 – 2:50 Otis / Q&A Delpech

2:50 – 3:20 CCS / Q&A McDonough

3:20 – 3:35 Break

3:35 – 4:05 UTAS / Q&A Gitlin

4:05 – 4:35 Pratt & Whitney / Q&A Leduc

4:35 – 5:00 Closing Remarks / Q&A Hayes / Johri

5:00 – 6:00 Reception All

United Technologies Agenda

Akhil Johri

March 10, 2016

Chief Financial Officer

Positioned for Growth Mega-trends

Source: United Nations: World Urbanization Prospects, 2014 revision; The Brookings Institution; Airline Monitor

Powerful mega-trends provide significant growth opportunities for UTC core business segments

Urban Population Mega-cities (population >1 million) (billions) (billions)

27%

58%

2010 2015E 2020E 2025E 2030E

~225

~360

~500

~660

1985 2000 2015E 2030E

3.6 4.0

4.3 4.7

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

1970 1980 1990 2000 2010 2020E 2030E

~6% CAGR

Middle class ~6% CAGR

5.1

Revenue Passenger Miles

1

Positioned for Growth Organic Sales Outlook

10%+

5 - 7%

4 - 5%

• ~7,000 engine orders* with industry leading GTF technology

• 30+ systems nose to tail… content per platform up 2x

4 - 5% • Leveraging global scale… with increased innovation spending

• World-class brands… strong replacement demand

See appendix for definition and reconciliation of organic sales *Announced and unannounced firm & option orders

(2016E - 2020E CAGR)

2

Growth / Productivity Achieving Competitive Excellence (ACE)

Operating management system driving continuous improvement

72 74

79

2013 2014 2015

ACE Sites

Supplier Gold

Competency

2013 2014 2015

Performing / Gold

Progressing / Underperforming

(% Gold & Silver)

Customers

SIPOC

Roadmap

Control Tower

0

5

135

Impact/Maturity

D I V E

Turnback Trend

Feedback Comments

3

Productivity

Source: Public company records and internal estimates *Excludes restructuring and other significant items of a non-recurring and/or non-operational nature (referred to as “other significant items”). excludes Sikorsky and years 1996 - 2007 have not been restated for discontinued operations for businesses disposed in 2012 - 2015

Restructuring 2015 – 2018E Cumulative cost ~$1.5B

Annualized savings ~$900M

SG&A Productivity

10.5%

13.0% 13.7%

17.2%

20.4%

23.2%

15.1%

(2015 % of sales)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

(% indexed to 1996*)

Segment profit

Segment sales

Headcount

(Industrial)

4

Productivity

*1995 & 2005 reported operating margins, 1995 & 2005 have not been restated for discontinued operations for businesses disposed of in 2012-2015; 2015 adjusted for restructuring and other significant items. See appendix for reconciliation.

World-class margins — with upside

8%

13%

17%

1995 2005 2015

(% operating margin*)

0 5 10 15 20 25

P&W

UTAS

CCS

Otis

Highest peer (% operating margin*)

2015 Operating Margins UTC Segment Margins

Source: Public company records and internal estimates 5

Cash Generation

Years 1996 - 2007 have not been restated for discontinued operations for businesses disposed in 2012- 2015 See free cash flow definition and reconciliation in appendix

80%

100%

120%

140%

160%

180%

2011 2012 2013 2014 2015

0

2

4

6

8

10

2011 2012 2013 2014 2015

0%

20%

40%

60%

80%

100%

120%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Strong cash generator through the investment cycles

Free Cash Flow to Net Income (%) % Capex / Depreciation

Net Inventory Turns

6

~$8 / share

Capital Allocation

'00 - 02 '03 - 05 '06 - 08 '09 - 11 '12 - 14 '15 - 17E

Dividends Share repurchase

3

10 10

22

($ billions)

*Based on ~7000 firm and option GTF orders to date

5

9

6

16

(~10B)

~7B

P/E view Cash flow view

Disciplined capital deployment

Pratt & Whitney large commercial engines* Value Disconnect Return to Shareholders

~($12) / share

7

Shareholder Value Creation

• Focused portfolio of global franchises

• Resilient business model

• Innovative products and services

• Strong performance culture

• Disciplined capital allocation

8

2016 outlook reaffirmed Sales $56 - $58B (organic growth 1 - 3%)

Adjusted EPS** range $6.30 - $6.60 Free cash flow*** 90 - 100% of net income attributable to common shareowners

See appendix for definition of organic growth *Excludes refrigeration **Adjusted for restructuring and other significant items. See appendix for reconciliation. ***See free cash flow reconciliation and definition in appendix

(% VPY)

2016 Organic Sales Expectations

4 - 6%

1 - 3%

2 - 4%

5 - 7%

0 - 2%

4 - 6%

(7) – (10%)

Americas

Commercial OE

EMEA

Commercial*

Aerospace

China

6%

(5%)

6%

(5%)

1%

5%

(2%)

Asia (ex-China)

Commercial aftermarket

Military

2015 2016E

9

Philippe Delpech

March 10, 2016

President Otis

Note: A, B, C represent industry peers Source: Public company reports & internal estimates *Otis operating profit adjusted for restructuring and other significant items. See appendix for reconciliation.

2015: ~$65 billion

A

B C

All others

18%

Industry Leadership 2015

12.0 9.6 9.1 8.0

1.9 1.4 1.2 1.1

2.4

1.4 1.0 0.9

20% 14% 11% 11%

($ billions) (units, millions) ($ billions) +25% +36%

+6 pts +71%

A B C B C A A C B A B C

($ billions)

Sales Portfolio EBIT ROS

* *

Industry

EBIT

1

6.1

12.0

12%

20%

2000 2005 2010* 2015*

Global scale and balance

Otis

Operating profit % Sales ($ billions)

Industry leader

Large and growing maintenance base

Productivity runway on service

Attractive growth fundamentals

Best-in-class cash flow

*Adjusted for restructuring and other significant items. See appendix for reconciliation.

(@ afx)

2

Challenges

Service Service conversion 15-30 year

lifecycle with retention

Repair

Maintenance

Modernization

New equipment

Source: Internal estimates

100 83

115

2010 20152010 2015

Otis Otis ROW Otis Europe

Service Profit (indexed)

Share of Segment (in units)

3

Accelerate innovation

Service transformation

Operations excellence

New equipment growth

Strategic Initiatives

4

New Equipment Growth – China

ROW

2015: ~$35B Continued urbanization Infrastructure development

Source: Internal estimates

China

Otis position

#1 #2

Global Segment

• Strengthen core brands

• Leverage scale

• Customer segment focus

China Transformation

5

• Expand sales coverage

• Enhance product offering

• Align incentives for profitable growth

53%

24%

15%

MEA Americas Europe Asia(ex. China)

(1%)

Otis ex. China 17%

Asia (ex. China)

Europe

Americas

MEA

(@ cfx)

New Equipment Growth – Rest of World

Growth Strategy

2015: ~$17B

#1

#1

#1

#1

Source: Internal estimates

ROW Segment

Otis position

2015 Orders VPY

6

2010 2015 2020E

(R&D spend, $ millions, @ cfx)

(% of sales)

1.1%

130

Innovation

• Leverage capabilities

• Accelerate programs

• Address product gaps

• Design for service

Priorities

New lead design center in China

Design next generation elevator

7

Service Transformation

Differentiated offerings Field productivity Customer retention

Deploy enhanced digital tools

Value added

Non-value added

Mechanic Time

8

2005 2010 2015

1.0x

5.8x

Service Transformation – China

Service Base (units, indexed 2005 = 1.0)

• Service conversion

• Segmented offering

• Repair and modernization growth

• Portfolio acquisitions

Regulations & enforcement

Higher customer expectations

Industry fragmentation

Priorities

Service Segment

Source: Internal estimates *Independent service providers

Otis portfolio Segment

ISP’s* and OEM agents

Major OEM’s

9

France Rest of Europe

Europe Field Sourcing(% centralized procurement)

China Supply Base(# of suppliers)

Commonacross Otis

Operations Excellence

Factories

Sub-systems

Global Factory Footprint

Highcost

Lowcost

Sourcing

10

2010 2015 2020E

2010 2015 2020E2010 2015 2020E

2010 2015 2020E

(units)

8%

33%

2%

>50%

~3%

2% ~15% China flat ROW ~5%

(5-year CAGR)

Key Metrics (@ cfx)

24%

(@ cfx) New Equipment Growth

(orders)

Service Transformation (maintenance portfolio)

Service Transformation (China service conversion rate)

Accelerate Innovation (R&D investment) (5-year CAGR)

(5-year CAGR)

11

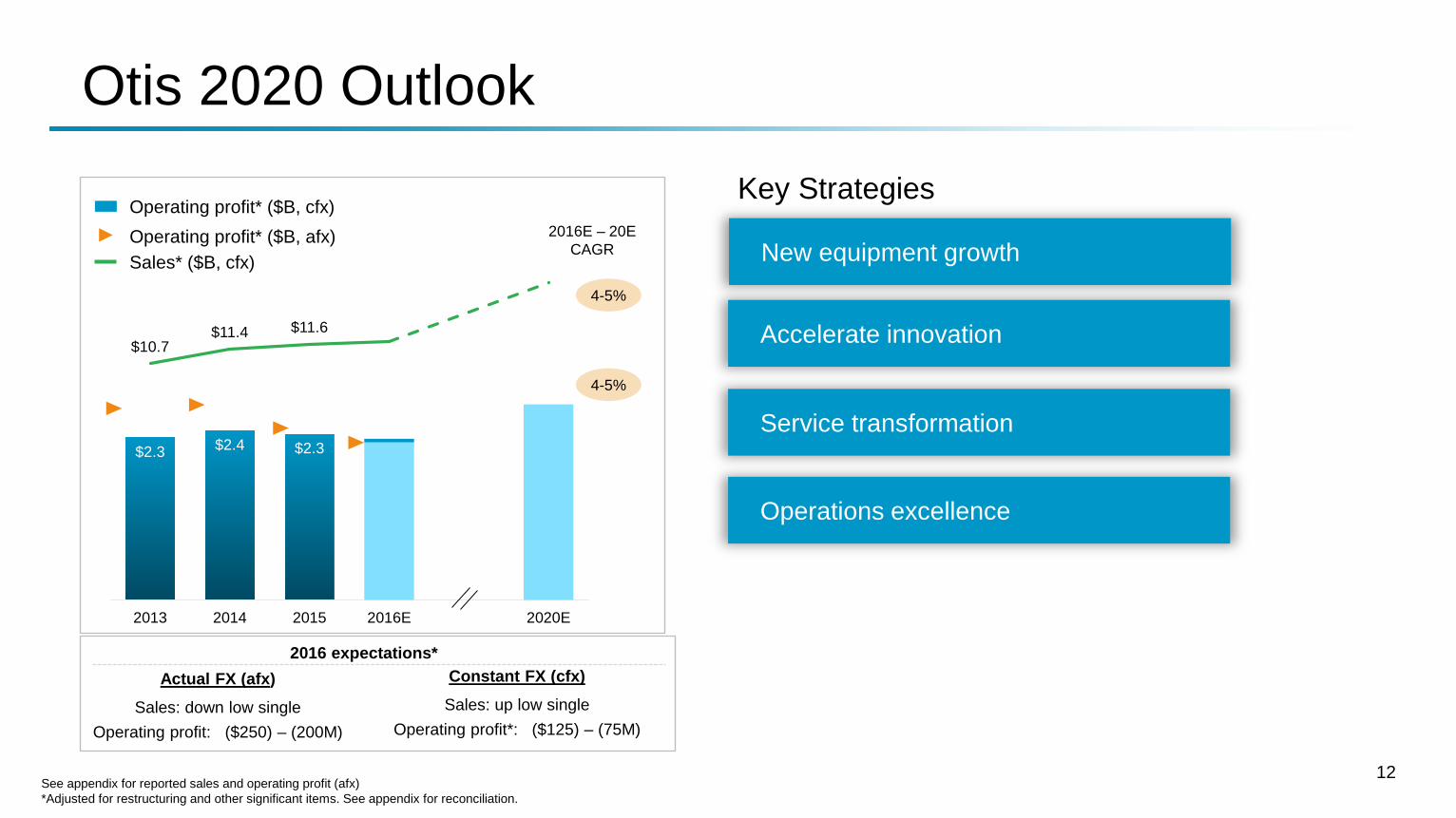

$2.3 $2.4 $2.3

$10.7 $11.4 $11.6

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

2013 2014 2015 2016E 2020E

Operating profit* ($B, cfx)

2016-20 CAGR

4-5%

4-5%

Sales* ($B, cfx)

Otis 2020 Outlook Key Strategies

Accelerate innovation

Service transformation

Operations excellence

New equipment growth 2016E – 20E

CAGR Operating profit* ($B, afx)

See appendix for reported sales and operating profit (afx) *Adjusted for restructuring and other significant items. See appendix for reconciliation.

Actual FX (afx) Sales: down low single

Operating profit: ($250) – (200M)

Constant FX (cfx) Sales: up low single

Operating profit*: ($125) – (75M)

2016 expectations*

12

Bob McDonough

March 10, 2016

President UTC Climate, Controls & Security

Sales $16.7 billion

Operating profit* $2.9 billion

Operating profit* % 17.5%

Employees 55,000

UTC Climate, Controls & Security

Asia

EMEA Americas

New equipment

Field services

• North America Residential HVAC

• Commercial HVAC

• Refrigeration

• Fire & Security

(2015 sales @ afx)

*Adjusted for restructuring and other significant items. See appendix for reconciliation.

F&S products

Transicold

F&S field

Commercial refrigeration

Residential HVAC

Commercial HVAC

1

Operating profit*

Operating profit* (%)

1.9

2.3 2.4 2.6

2.9 2.9 10.8%

12.2%

14.1%

15.7% 17.0%

17.5%

2010 2011 2012 2013 2014 2015 2016E

$175 – 225M @ cfx $100 – 150M @ afx

VPY @ cfx 7% 11% 10% 7% 7% 18%

CAGR ‘10-’15

Organic 3%

Profit* 9%

CCS Priorities

($ billions)

*Adjusted for restructuring and other significant items. See appendix for reconciliation.

Organic growth

Innovation

Cash generation

Cost leadership

2016 profit expectations*

2

up mid single digit

up low single digit

up mid single

up slightly Refrigeration

Americas

EMEA

Asia ex China

China

2016 Outlook

Transport refrigeration

Commercial refrigeration

F&S field

F&S products

Commercial HVAC

NA Residential HVAC up mid single digit

up low single digit

up low single digit

up slightly

up mid single digit

flat

2016 expectations Organic sales: up low single digit

Operating profit* (cfx): $175 – 225M Operating profit* (afx): $100 – 150M

CCS Sales Organic Sales Growth

*Adjusted for restructuring and other significant items. See appendix for reconciliation.

3

Iconic brands Building solutions M&A opportunities Innovation

Value Creation Growth

Cost leadership Operations excellence Cash generation Market fundamentals

Performance

Low cost manufacturing

Lower cost (hours)

Higher cost (hours)

Footprint reduction (2011–15)

R&D centers Factories Branches

28% 23%

15%

2012 2013 2014 2015 2016E

Free cash flow*

~100% of NI

*See free cash flow definition and reconciliation in appendix

4

Source: United Nations: World Urbanization Prospects, 2014 revision; Green Market Size: McGraw Hill Construction Dodge, 2014; internal estimates

2.6 2.9

3.2 3.6

4.0 4.3

4.7

95 00 05 10 15E 20E 25E

0

120

2005 2010 20150

25

50

75

100

75 80 85 90 95 00 05 10 15

U.S. Europe China

Market Growth Fundamentals Urbanization

Replacement (U.S. splits installed base, units in millions)

Energy Efficiency (U.S. green building construction, $ billions)

Adoption (commercial fire detection spend per capita) (global urban population, billions)

5

0.0

0.8

1.6

2.4

00 03 06 09 12 15

0

2

4

6

8

75 80 85 90 95 00 05 10 15

• Industry-leading brands

• Innovation

• Low-cost footprint

• Best-in-class distribution

Source: U.S. Census Bureau; Global Insight; internal estimates

North America Residential HVAC Growth Drivers

Housing Starts (units, millions)

Industry Shipments (U.S. splits, units in millions)

Add-on / replacement New construction

Market Fundamentals

6

Global Green Buildings

Urbanization

2.6 2.9

3.2 3.6

4.0 4.3

4.7

1995 2000 2005 2010 2015E 2020E 2025E

0%

40%

2012 2015 2018E

2X

2X

(respondents with >60% green building projects)

Source: United Nations: World Urbanization Prospects, 2014 revision; World Green Building Trends 2016, Dodge Data & Analytics

Commercial HVAC

• Innovation and efficiency

• Product breadth

• Global footprint

• Automation and controls

(global urban population, billions)

Growth Drivers Market Fundamentals

7

U.S. Europe China India

Refrigeration Spend Per Capita

0

25

50

75

100

125

06 07 08 09 10 11 12 13 14 15

Refrigerated Seaborne Trade (tons, millions)

Source: Global Insight; internal estimates

Refrigeration

• Innovation

• Commercial refrigeration capability

• Product line expansion

Growth Drivers Market Fundamentals

8

U.S. Europe China

U.S. Europe China

(spend per capita) Access Control Adoption

Source: internal estimates

Fire & Security

• High technology products

• Field footprint

• Security product breadth

• Strong brand portfolio

Commercial Fire Control Adoption (spend per capita)

Growth Drivers Market Fundamentals

9

• Consultative selling

• Strategic accounts

• Integrated solutions

Building Solutions Growth Intelligent products Connected systems Integrated buildings

10

$2.4 $2.7

$2.9

$15.3 $15.5 $16.4

-

5.00

10.00

15.00

20.00

-

0.0

0.0

0.0

0.0

0.0

0.0

2013 2014 2015 2016E 2020E

2016E – 20E CAGR

4 - 5%

7 - 8%

CCS 2020 Outlook ($ billions)

Operating profit* (cfx)

Sales* (cfx)

Operating profit* (afx)

Actual FX (afx) Sales: flat

Operating profit: $100 – 150M

Constant FX (cfx) Sales: up low single

Operating profit: $175 – 225M

*Adjusted for restructuring and other significant items. See appendix for reconciliation. See appendix for sales and operating profit at actual FX (afx)

2016 expectations*

Organic growth

Innovation

Cash generation

Cost leadership

M&A actions

Key Strategies

11

Dave Gitlin

March 10, 2016

President UTC Aerospace Systems

UTC Aerospace Systems

1

90 product lines supporting 1,500 operators on 70,000 aircraft

Industry-leading portfolio

Well-positioned on new platforms

Deep customer relationships

Proven track record to drive continued cost reduction

Strategies in place position us for long-term growth

Sales Drivers

2015 sales: $14.3B* Driver Trend

Mili

tary

RPMs

Fuel prices / airline profitability

New program EIS

Surplus availability

Military OEM platforms

ISR

Defense spending

CAGR 2016E – 2020E

Mid to high single digit

Com

m A

M

Mid single digit

Low single digit

Commercial OEM

Commercial aftermarket

Military

Driver Trend

Driver Trend

Com

m O

EM

Large commercial

Regional

Bizjet / rotorcraft

*Adjusted for restructuring and other significant items. See appendix for reconciliation.

2

Program Execution

$240B+ expected life of program sales

A321neo A350-1000

737MAX

A330neo

C919

B777X

KC-46A

787-10

MC-21 CSeries

MRJ

E2

G500/600 KC-390 CH-53K

3

New Program Introduction

2015 2016E 2017E 2018E

Legacy programs

New programs

Large commercial / regional aircraft sales

175

350

500

2016E 2017E 2018E

($ millions)

OEM Mix Cost Reduction Target

4

Productivity Footprint Supply Chain

Cost Reduction

1 25 5 10 15 20 Year

Nac

elle

shi

pset

cos

t (in

dexe

d)

Wroclaw, Poland

• Center of excellence model • Low-cost make

• Localized supply base • Low-cost buy

Poland

New program Legacy program UTAS COE

UTAS supplier

5

Commercial Aftermarket

2015 2016E 2017E 2018E

$4.4B

Provisioning

Repair

Spare parts

Sustained Growth Key Strategies

CAGR

5 - 7%

3 - 5%

2 - 4%

4 - 6% • Expand surplus capability

• Increase operator long-term agreements

• Grow partnerships with independent

service providers (ISPs)

• Provide more comprehensive offerings

6

Growth

$240B+ expected life of program sales

Advanced nacelle

Variable-speed constant frequency generator

Blended night vision goggles

Next-generation ejection seats

Platforms Technology Advancements Military / Retrofits

7

Growth

$1B sales $6B sales $15B sales

Components

15 product lines 40 product lines 90 product lines

Systems Integrated systems

B767 – 2 systems B777 – 6 systems B787 – 26 systems

Hamilton Standard Hamilton Sundstrand UTC Aerospace Systems

What’s next: Continued focus on expanding aerospace systems offerings

8

$2.1 $2.4 $2.4

$13.3 $14.2 $14.3

-

5.00

10.00

15.00

20.00

25.00

0

5E-10

1E-09

1.5E-09

2E-09

2.5E-09

3E-09

3.5E-09

4E-09

4.5E-09

2013 2014 2015 2016E 2020E

UTC Aerospace Systems 2020 Outlook

5 - 7%

7 - 9%

2016E – 20E CAGR

Sales* ($B)

Operating profit* ($B)

*Adjusted for restructuring and other significant items. See appendix for reconciliation.

2016 expectations* Sales: up low single digit

Operating profit: ($50) – 0M

Key Strategies

Industry-leading portfolio

Well-positioned on new platforms

Deep customer relationships

Proven track record to drive continued cost reduction

Strategies in place position us for long-term growth

9

Bob Leduc

March 10, 2016

President Pratt & Whitney

Pratt & Whitney

High quality and diverse backlog

Extensive aftermarket services network

Industry leading technologies

Positioned on leading platforms

1

2

Accomplishments in Last 15 Months

C Series certified

E-Jets E2 roll out ceremony MRJ first flight

First A320neo deliveries to IndiGo and Lufthansa

Large Commercial Engines

F-35B Initial Operational Capability

KC-46A Tanker first refueling flight

Military Engines

Photo: Dassault

Dassault Falcon 8X first flight

Gulfstream G500 first flight

Pratt & Whitney Canada

Photo: Lockheed Martin

Photo: Gulfstream Photo: Airbus Photo: Bombardier

3

18

32

59

2016E 2017E 2018E2008 2009 2010 2011 2012 2013 2014 2015 2016

YTD

High Quality and Diverse Backlog GTF Engine Orders Orders by Platform

*Announced and unannounced firm engine orders, including options

~7,000

~7,000

New customers

Existing customers

A320neo

E-Jets E2

CSeries

MRJ

MC-21

Cumulative Customer Launches

(number of Geared TurbofanTM engines*)

4

P&W legacy

V2500

GP7000

GTF

0

5,000

10,000

15,000

20,000

25,000

2000 2005 2010 2015 2020E 2025E 2030E2015 2016E 2020E

Commercial Engines

GTF

V2500

All other

2015-2020E CAGR ~19%

~650

558

~1,200

Objective Actual engine cost/ engine

Engines

87% learning curve

54%

0 250 500 1250 750

Large Engine Shipments Cost Reduction Installed Base (number of engines)

(number of large commercial engines) (PW1100G-JM engine cost)

5

Pratt & Whitney Canada

Growth platforms

#2

PW800

Cessna Latitude

Gulfstream G500/G600

PW300

#1

AT502XP

ATR72-600 PW100

PT6A

#1

PW210

H135

AW169

PW206

#2

B787

A320ceo family APS3200

APS5000

Position

Business Aviation

Turboprop / General Aviation

Civil Helicopter

Auxiliary Power Unit

Photo: © ATR Photo: Airbus

Photo: Gulfstream Photo: © Air Tractor Photo: Boeing

6

Pratt & Whitney Canada

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

2000 2010 2020E

General aviation

Regional

Business jet

Helicopter

APU

2030E

3,005 ~2,850

~3,500

2015 2016E 2020E

2015-2020E CAGR ~4%

APU Helicopter Business jet Regional General aviation

Engine Shipments Installed Engine Base

7

Long Range Strike Bomber

Pratt & Whitney Military Engines

UAV

Helicopters

F-35 Joint Strike Fighter

F-15 / F-16

F-22 Raptor

C-17 Globemaster

KC-46A Pegasus

KC-390 V-22 Osprey

A400M Atlas

CH-53K King Stallion

Future Opportunities Tactical Mobility / Tanker Auxiliary Power Unit

Photo: Lockheed Martin

Photo: Sikorsky

Photo: Embraer

Photo: Airbus

8

2015 2016E 2020E 0 50 100 150 200 250 300 350 400

Objective Actual engine cost / engine

0

2,000

4,000

6,000

8,000

10,000

2010 2015 2020E

Legacy bomber / special mission / trainers

Tactical

Mobility / tanker

Engines

49%

89% learning curve

Pratt & Whitney Military Engines

2015-2020E CAGR ~17%

*Excludes 8,800 APUs growing to 15,500 in 2020

F100 Tanker F117 F135

Engine Shipments Installed Base Cost Reduction (engines)

(engines*)

(F135 engine cost)

18.8%

~100

~200

96

9

40%

60%

75%

80%

PW4000 V2500 GP7000 GTF

Aftermarket – Growing Engine Services

P&W PROPRIETARY This document/page does not contain any export regulated technical data

Average engine age (years)

new 3 8 17

Shop Visits Global Service Network Service Model (number of shop visits)

2015 2016E 2020E

8,071 ~8,400

GTF

Legacy

V2500 GP7000

Biz

APU

Helo

GA

Regional

2016E-2020E CAGR ~3%

Aftermarket service centers Large commercial engine Pratt & Whitney Canada

~12,400 Operators

~70,000 Engines in

service

(commercial fleet coverage)

10

Q1 Q2 Q3 Q4

~185

Operations – Delivery Assurance

P&W PROPRIETARY This document/page does not contain any export regulated technical data

99%

~1,500 GTF engine part numbers

1%

Strategic buffer in place

Building a buffer

JSF Legacy V2500 GTF

Large Engine Shipments Part Buffer (average % availability)

26% 22% 10%

17% 18%

15%

34% 39% 54%

23% 21% 21%

2014 2015 2016E

Gold

Performing

Under- performing

Suppliers in program 264 413 ~425

~220

~190 ~190

Progressing

(2016E) Supplier Gold

(% of spend in program)

11

Constant FX (cfx) Sales: up low single

Operating profit: ($125) – (75M)

Pratt & Whitney 2020 Outlook

Industrial plan execution

$1.9

$2.1 $1.9

$14.5 $14.5 $14.2

-

5.00

10.00

15.00

20.00

25.00

-

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

2013 2014 2015 2016E 2020E

10+%

6 - 8%

Sales* Operating profit*

($ billions)

2016E - 20E CAGR

Key Strategies

Successful IOC / service entries

Manufacturing cost reduction

E&D stabilization

Aftermarket growth

*Adjusted for restructuring and other significant items. See appendix for reconciliation.

Actual FX (afx) Sales: up low single

Operating profit: ($50) – 0M

2016 expectations*

Appendix

2016 Segment Outlook

1 *Excludes restructuring & certain other items

Organic sales change

Reported sales change

Operating profit change*

(ex FX)

Operating profit change*

Climate, Controls & Security up low single digit flat $175 – 225M $100 – 150M

Otis up low single digit down low single digit ($125) – (75M)

($250) – (200M)

Pratt & Whitney up low single digit up low single digit ($125) – (75M) ($50) – 0M

Aerospace Systems up low single digit up low single digit ($50) – 0M ($50) – 0M

*Adjusted for restructuring and other significant items

up high single digit

up slightly

down low single digit Americas

EMEA

Asia

up low single digit

Asia

EMEA

Americas

Service

Asia*

EMEA

Americas

New equipment flat

~ 10%

up low single digit

down high single digit

up low single digit

up mid single digit

up high single digit

flat

* China down ~10%

(% organic sales change)

2016 Otis Sales Expectations Outlook

Profit Drivers

Operating Profit

Sales

Constant FX ($125) – (75M)

Actual FX ($250) – (200M)

Volume + 25 – 75

Net productivity / restructuring + ~125

Pension + ~25

Price / mix – ~250

R&D / other – ~50

Constant FX – ($125) – (75M)

FX – ~ 125M

Actual FX – ($250) – (200M)

Organic up low single digit

Actual FX down low single digit

Otis 2016 Expectations

Adjusted for restructuring and other significant items

($ millions)

Profit Drivers

Operating Profit

Sales

Constant FX + $175 – 225M

Actual FX + $100 – 150M

Organic volume / mix + 50 – 100

Net productivity / restructuring + ~75

Commodities / price + ~50

Pension + ~50

Non-recurring / other – ~50

Constant FX + $175 – 225M

FX – ~ 75M

Actual FX + $100 – 150M

Organic up low single digit

Actual FX flat

CCS 2016 Expectations

Adjusted for restructuring and other significant items

($ millions)

Operating Profit

down $0 – 50M

Sales

up low-single digit

Pratt & Whitney 2016 Expectations ($ millions)

Pension

E&D

Commercial aftermarket

Commercial OE mix

Military

2016 expectations (@ constant FX)

FX

2016 expectations

+ ~175

+ 0 – 25

+ 0 – 25

– ~225

– ~75

($125) – (75M)

+ 75M

($50) – 0M

Military AM

Military OE

Commercial AM*

Commercial OE*up low

single digits

flat

up high single digits

up double digits

Adjusted for restructuring and other significant items. *Includes large commercial and P&W Canada

– 325 – 300

+ 175 – 200

– ~150 + ~125

+ ~125

Aerospace Systems 2016 Expectations

Military AM

Military OE

Commercial AM

Commercial OE up mid single digit

up low single digit

down low single digit

down high single digit

Adjusted for restructuring and other significant items.

Volume / mix

Product cost reduction

2015 contract / license agreements

R&D / cost actions

Pension

Operating Profit

down $0 – 50M

Sales

up low-single digit

($ millions)

2015 Full Year Sales Change

Total Organic FX Net Acquisitions Other Otis (8%) 1% (9%) 0% 0%

CCS (1%) 3% (6%) 2% 0%

Pratt & Whitney (3%) (1%) (1%) 0% (1%) Aerospace Systems (1%) 3% (2%) (1%) (1%) Total UTC* (3%) 1% (4%) 1% (1%)

Organic sales growth represents the total reported consolidated net sales increase/(decrease) within the Corporation’s ongoing businesses less the impact of foreign currency translation, and acquisitions and divestitures completed in the preceding twelve months and significant items of a non-recurring and/or non-operational nature. Organic growth includes the net impact of transactional foreign exchange hedging. *Reflects consolidated net sales

Free Cash Flow Reconciliation

Free cash flow represents cash flow from operations less capital expenditures. Management believes free cash flow provides a relevant measure of liquidity and a useful basis for assessing the Corporation’s ability to fund its activities, including the financing of acquisitions, debt service, repurchases of the Corporation’s Common Stock and distribution of earnings to shareholders. Others that use the term free cash flow may calculate it differently. The reconciliation of net cash flow provided by operating activities prepared in accordance with Generally Accepted Accounting Principles to free cash flow is above.

FY 15 FY14 Net income attributable to common shareowners from continuing operations

3,996 6,066

Depreciation & amortization 1,863 1,820

Change in working capital (847) (729)

Other 1,686 (163)

Cash flow from operations 6,698 6,994

Capital expenditures (1,652) (1,594)

Free cash flow 5,046 5,400

Free cash flow as a % of net income attributable to common shareowners from continuing operations

126% 89%

($ millions)

UTC Operating Results Reconciliation

2008 2009 2010 2011 2012 2013 2014 2015Segment Sales 1 51,932 44,586 46,004 48,772 51,443 57,141 58,528 56,863Other significant items of a non-recurring/non-operational nature 2 - - - - - - - 352Segment sales - adjusted 51,932 44,586 46,004 48,772 51,443 57,141 58,528 57,215

Segment operating profit 7,230 6,074 6,890 7,653 7,470 9,074 9,777 8,023Other significant items of a non-recurring/non-operational nature 2 (129) (136) 33 (84) (157) (223) (31) 1,182Restructuring 327 718 359 262 518 431 349 375Segment operating profit - adjusted 7,428 6,656 7,282 7,831 7,831 9,282 10,095 9,580

Segment operating margin 13.9% 13.6% 15.0% 15.7% 14.5% 15.9% 16.7% 14.1%Segment operating margin - adjusted 14.3% 14.9% 15.8% 16.1% 15.2% 16.2% 17.2% 16.7%

1 Segment sales for periods prior to 2009 reflect the retrospective adoption of Accounting for Collaborative Arrangements.

2 Details of other significant items of a non-recurring/non-operational nature See Segment operating results reconciliation slides for additional information.

($ millions)

Otis Operating Results Reconciliation 2008 2009 2010 2011 2012 2013 2014 2015

Segment Sales 12,884 11,723 11,579 12,437 12,056 12,484 12,982 11,980Other significant items of a non-recurring/non-operational nature - - - - - - - -Segment sales - adjusted 12,884 11,723 11,579 12,437 12,056 12,484 12,982 11,980

Segment operating profit 2,477 2,447 2,575 2,815 2,512 2,590 2,640 2,338Other significant items of a non-recurring/non-operational nature 1 - (52) - - - - - -Restructuring 21 158 83 73 164 88 87 51Segment operating profit - adjusted 2,498 2,553 2,658 2,888 2,676 2,678 2,727 2,389

Segment operating margin 19.2% 20.9% 22.2% 22.6% 20.8% 20.7% 20.3% 19.5%Segment operating margin - adjusted 19.4% 21.8% 23.0% 23.2% 22.2% 21.5% 21.0% 19.9%

1 Details of other significant items of a non-recurring/non-operational nature 2009: Approximately $52 million non-cash, non-taxable gain recognized on the remeasurement to fair value of a previously held equity interest in a joint venture resulting from the purchase of a controlling interest.

($ millions)

CCS Operating Results Reconciliation 2008 2009 2010 2011 2012 2013 2014 2015

Segment Sales 21,263 16,838 17,876 18,864 17,090 16,809 16,823 16,707Other significant items of a non-recurring/non-operational nature 1 - - - - - - - -Segment sales - adjusted 21,263 16,838 17,876 18,864 17,090 16,809 16,823 16,707

Segment operating profit 1,858 1,233 1,776 2,212 2,425 2,590 2,782 2,936Other significant items of a non-recurring/non-operational nature 1 (67) (84) 5 (43) (157) (55) (30) (121)Restructuring 203 322 153 126 143 97 116 108Segment operating profit - adjusted 1,994 1,471 1,934 2,295 2,411 2,632 2,868 2,923

Segment operating margin 8.7% 7.3% 9.9% 11.7% 14.2% 15.4% 16.5% 17.6%Segment operating margin - adjusted 9.4% 8.7% 10.8% 12.2% 14.1% 15.7% 17.0% 17.5%

1 Details of other significant items of a non-recurring/non-operational nature 2008: Approximately $67 million gain from the contribution of a business into a new venture operating in the Middle East and the Commonwealth of Independent States.

2009: Approximately $57 million gain recognized from the contribution of the majority of Carrier’s U.S. residential sales and distribution business into a new venture formed with Watsco, Inc. and approximately $27 million of gains related to divesiture activity.

2010: Approximately $47 million net charge resulting from dispositions associated with Carrier’s ongoing portfolio transformation. Included in this net charge is an approximately $58 million asset impairment charge associated with the expected disposition of a business, partially offset by an approximately $11 million gain on the sale of another business. Approximately $42 million net gain resulting from dispositions associated with Carrier’s ongoing portfolio transformation.

2011: Approximately $28 million net gain resulting from dispositions associated with Carrier’s ongoing portfolio transformation. Approximately $81 million net gain resulting from Carrier’s ongoing portfolio transformation primarily as a result of the contribution by Carrier's heating, air-conditioning and ventilation operations in Brazil, Argentina and Chile into a new joint venture controlled by Midea Group of China. Approximately $20 million other-than-temporary impairment charge on an equity investment. Approximately $46 million other-than-temporary impairment charge on an equity investment.

2012: Approximately $112 million net gain from UTC Climate, Controls & Security’s ongoing portfolio transformation. This net gain includes approximately $215 million from the sale of a majority interest in a manufacturing and distribution joint venture in Asia, partially offset by $103 million of impairment charges related to planned business dispositions. Approximately $110 million net gain from UTC Climate, Controls & Security’s ongoing portfolio transformation. This net gain includes approximately $142 million from the sale of a controlling interest in its Canadian distribution business, partially offset by $32 million loss on the disposition of its U.S. fire and security branch operations. Approximately $65 million net charge from UTC Climate, Controls & Security’s ongoing portfolio transformation. This net charge includes approximately $24 million of pension settlement charges.

2013: Approximately $38 million net gain from UTC Climate, Controls & Security's ongoing portfolio transformation. This net gain primarily relates to the sale of a business in Hong Kong. Approximately $17 million net gain from UTC Climate, Controls & Security's ongoing portfolio transformation, primarily due to a gain on the sale of a business in Australia.

2014: Approximately $30 million net gain from UTC Climate, Controls & Security's ongoing portfolio transformation, primarily due to a gain on the sale of an interest in a joint venture in North America.

2015: Approximately $126 million gain as a result of a fair value adjustment related to the acquisition of a controlling interest in a UTC Climate, Controls & Security joint venture investment. Approximately $5 million charge related to UTC Climate, Controls & Security acquisitions and integration costs.

($ millions)

Pratt & Whitney Operating Results Reconciliation 2008 2009 2010 2011 2012 2013 2014 2015

Segment Sales 1 13,053 11,584 12,150 12,711 13,964 14,501 14,508 14,082Other significant items of a non-recurring/non-operational nature 2 - - - - - - - 142Segment sales - adjusted 13,053 11,584 12,150 12,711 13,964 14,501 14,508 14,224

Segment operating profit 1 2,047 1,735 1,885 1,867 1,589 1,876 2,000 861Other significant items of a non-recurring/non-operational nature 2 (37) - - (41) - (168) (1) 947Restructuring 94 181 99 52 96 154 64 105Segment operating profit - adjusted 2,104 1,916 1,984 1,878 1,685 1,862 2,063 1,913

Segment operating margin 15.7% 15.0% 15.5% 14.7% 11.4% 12.9% 13.8% 6.1%Segment operating margin - adjusted 16.1% 16.5% 16.3% 14.8% 12.1% 12.8% 14.2% 13.4%

1 Segment sales for periods prior to 2009 reflect the retrospective adoption of Accounting for Collaborative Arrangements.

2 Details of other significant items of a non-recurring/non-operational nature 2008: Approximately $37 million non-cash gain on a partial sale of an investment.

2011: Approximately $41 million gain recognized from the sale of an equity investment.

2013: Approximately $193 million gain from the sale of the Pratt & Whitney Power Systems business. This gain was not reclassified to "Discontinued Operations" due to our expected level of continuing involvement in the business post disposition.

2014: Approximately $83 million net gain, primarily as a result of fair value adjustments related to a business acquisition. Approximately $60 million charge to adjust the fair value of a Pratt & Whitney joint venture investment. Approximately $22 million charge for impairment of assets related to a joint venture.

2015: Approximately $142 million to record in sales and $80 million in losses from Pratt & Whitney customer contract renegotiations. Approximately $867 million charge related to a Pratt & Whitney research and development support agreements with Canadian government agencies.

($ millions)

UTAS Operating Results Reconciliation 2008 2009 2010 2011 2012 2013 2014 2015

Segment Sales 4,732 4,441 4,399 4,760 8,334 13,347 14,215 14,094Other significant items of a non-recurring/non-operational nature 1 - - - - - - - 210Segment sales - adjusted 4,732 4,441 4,399 4,760 8,334 13,347 14,215 14,304

Segment operating profit 848 659 654 759 944 2,018 2,355 1,888Other significant items of a non-recurring/non-operational nature 1 (25) - 28 - - - - 356Restructuring 9 57 24 11 115 92 82 111Segment operating profit - adjusted 832 716 706 770 1,059 2,110 2,437 2,355

Segment operating margin 17.9% 14.8% 14.9% 15.9% 11.3% 15.1% 16.6% 13.4%Segment operating margin - adjusted 17.6% 16.1% 16.0% 16.2% 12.7% 15.8% 17.1% 16.5%

1 Details of other significant items of a non-recurring/non-operational nature 2008: Approximately $25 million gain on the completion of a divestiture of a business.

2010: Approximately $28 million of asset impairment charges related primarily to the expected disposition of an aerospace business as part of Hamilton Sundstrand’s ongoing low cost sourcing initiatives.

2015: Approximately $210 million to record in sales and $295 million in losses from UTC Aerospace Systems customer contract renegotiations. Approximately $61 million charge to UTC Aerospace Systems for impairment of assets held for sale.

($ millions)

2015 Adjusted EPS United Technologies CorporationReconciliation of Diluted Earnings per Share to Adjusted Diluted Earnings per Share

(dollars in millions, except share amounts)

Diluted earnings per share--Net income from continuing operations attributable to common shareowners $ 1.51 $ 1.64 $ 1.61 $ (0.30 ) $ 4.53

Net income from continuing attributable to common shareowners $ 1,364 $ 1,461 $ 1,427 $ (256 ) $ 3,996Adjustments to net income from continuing operations attributable to common shareowners:

Restructuring costsGain on fair value adjustment on acquisition of controlling interest in a joint venture

) )

Acquisition and integration costs related to current period acquisitions - - - 5 5

Charge related to a research and development support agreement with Canadian government agencies

- - - 867 867

Charge resulting from customer contract negotiations - - - 375 375Charge for impairment of assets held for sale -Charge for pending and future asbestos-related claims -Charge (gain) from agreement with a state taxing authority for monetization of tax credits

-

Income tax expense (benefit) on restructuring costs and significant non-recurring and non-operational items

) ) ) ) )

Significant non-recurring and non-operational charges (gains) recorded within income tax expense

- - - 342 342

Total adjustments to net income from continuing operations attributable to common shareowners

)

Adjusted net income from continuing operations attributable to common shareowners $ 1,301 $ 1,485 $ 1,479 $ 1,298 $ 5,563

Less: Impact of total adjustments on diluted earnings per share $ 0.07 $ (0.03 ) $ (0.06 ) $ (1.83 ) $ (1.77 )Adjusted diluted earnings per share--Net income from continuing operations attributable to common shareowners $ 1.44 $ 1.67 $ 1.67 $ 1.53 $ 6.30

(126(126 - - -

61237

27

(617

1,567

27

Full Year 2015

396

(63 24 52 1,554

(30 (15 (21 (551

- - 237

- -

- - 61

93 39 73 191

Q 1 2015 Q 2 2015 Q 3 2015 Q 4 2015

Segment Data SEGMENT DATA - Reported($ Millions except per share amounts)

Q1 Q2 Q3 Q4 2015 YTD Q1 Q2 Q3 Q4 2014 YTDOtis Net Sales 2,745 3,098 3,043 3,094 11,980 2,955 3,365 3,326 3,336 12,982 Operating Profit (a) 527 627 642 542 2,338 570 693 703 674 2,640 Operating Profit % 19.2% 20.2% 21.1% 17.5% 19.5% 19.3% 20.6% 21.1% 20.2% 20.3%

UTC Climate, Controls & Security Net Sales 3,852 4,454 4,279 4,122 16,707 3,851 4,429 4,351 4,192 16,823 Operating Profit (a), (i), (q), (t) 729 823 771 613 2,936 537 815 807 623 2,782 Operating Profit % 18.9% 18.5% 18.0% 14.9% 17.6% 13.9% 18.4% 18.5% 14.9% 16.5%

Pratt & Whitney Net Sales (v) 3,332 3,677 3,234 3,839 14,082 3,329 3,592 3,564 4,023 14,508 Operating Profit (a), (b), (c), (j), (u), (v) 419 487 419 (464) 861 388 432 633 547 2,000 Operating Profit % 12.6% 13.2% 13.0% -12.1% 6.1% 11.7% 12.0% 17.8% 13.6% 13.8%

UTC Aerospace Systems Net Sales (w) 3,548 3,632 3,457 3,457 14,094 3,450 3,636 3,535 3,594 14,215 Operating Profit (a), (w), (x) 569 580 572 167 1,888 590 602 575 588 2,355 Operating Profit % 16.0% 16.0% 16.5% 4.8% 13.4% 17.1% 16.6% 16.3% 16.4% 16.6%

Total Segments Net Sales 13,477 14,861 14,013 14,512 56,863 13,585 15,022 14,776 15,145 58,528 Operating Profit 2,244 2,517 2,404 858 8,023 2,085 2,542 2,718 2,432 9,777 Operating Profit % 16.7% 16.9% 17.2% 5.9% 14.1% 15.3% 16.9% 18.4% 16.1% 16.7%

Corporate, Eliminations, and Other Net Sales: Other (157) (171) (225) (212) (765) (146) (154) (163) (165) (628) Operating Profit: General corporate expenses (110) (120) (101) (133) (464) (112) (119) (124) (133) (488) Eliminations and other (a), (f), (y), (z) 48 18 (1) (333) (268) 48 257 18 (19) 304

Consolidated Net Sales 13,320 14,690 13,788 14,300 56,098 13,439 14,868 14,613 14,980 57,900 Operating Profit 2,182 2,415 2,302 392 7,291 2,021 2,680 2,612 2,280 9,593 Operating Profit % 16.4% 16.4% 16.7% 2.7% 13.0% 15.0% 18.0% 17.9% 15.2% 16.6%

Interest expense, net (g), (k), (m), (n) (217) (217) (184) (206) (824) (224) (206) (185) (266) (881)

Income from continuing operations before income taxes 1,965 2,198 2,118 186 6,467 1,797 2,474 2,427 2,014 8,712

Income tax expense (h), (l), (o), (p), (aa), (bb) (530) (626) (592) (363) (2,111) (549) (486) (575) (634) (2,244)

Income from continuing operations 1,435 1,572 1,526 (177) 4,356 1,248 1,988 1,852 1,380 6,468 Income (loss) from discontinued operations (d), (e), (r), (s) 63 80 (65) 3,532 3,610 58 (198) 100 195 155

Net income 1,498 1,652 1,461 3,355 7,966 1,306 1,790 1,952 1,575 6,623 Less: Noncontrolling interest in subsidiaries' earnings (72) (110) (98) (78) (358) (93) (110) (98) (102) (403)

Net income attributable to common shareowners 1,426 1,542 1,363 3,277 7,608 1,213 1,680 1,854 1,473 6,220

Net income attributable to common shareowners: Income from continuing operations 1,364 1,461 1,427 (256) 3,996 1,155 1,878 1,755 1,278 6,066 Income (loss) from discontinued operations 62 81 (64) 3,533 3,612 58 (198) 99 195 154

Q1 Q2 Q3 Q4 2015 YTD Q1 Q2 Q3 Q4 2014 YTDContinuing Operations Earnings per share - basic 1.53 1.66$ 1.63$ (0.30)$ 4.58 1.28 2.09 1.96 1.43 6.75 Earnings per share - diluted 1.51 1.64 1.61 (0.30)$ 4.53 1.26 2.05 1.93 1.41 6.65

Discontinued Operations Earnings (loss) per share - basic 0.07$ 0.09$ (0.07)$ 4.16$ 4.14 0.07 (0.22) 0.11 0.22 0.17 Earnings (loss) per share - diluted 0.07 0.09 (0.07) 4.16 4.09 0.06 (0.22) 0.11 0.22 0.17

Weighted average number of shares outstanding: (In Millions) Basic shares 890.3 877.3 876.4 849.6 872.7 900.9 900.1 897.7 895.4 898.3 Diluted shares 904.2 889.4 885.0 849.6 883.1776 917.0 914.7 910.3 907.3 911.6

Q1 Q2 Q3 Q4 Total YTD Q1 Q2 Q3 Q4 Total YTDEffective Tax Rate - continuing ops 27.0% 28.5% 28.0% 194.8% 32.6% 30.6% 19.6% 23.7% 31.5% 25.8%

20142015

Segment Data – Notes The earnings release and conference-call discussion adjust 2015 and 2014 segment results for restructuring costs as well as significant items of a non-recurring and/or non-operational nature.

The following items are included in current and prior year results:

(a) Restructuring costs as included in 2015 and 2014 results:2014

Restructuring Costs Restructuring CostsQ1 Q2 Q3 Q4 Total YTD Q1 Q2 Q3 Q4 Total YTD

Operating Profit: Otis 6 8 18 19 51 17 21 15 34 87 UTC Climate, Controls & Security 24 28 15 41 108 43 25 14 34 116 Pratt & Whitney 13 2 22 68 105 42 5 8 9 64 UTC Aerospace Systems 50 - 14 47 111 6 4 26 46 82

Total Segments 93 38 69 175 375 108 55 63 123 349 General corporate expenses - - 4 5 9 - - - 4 4 Eliminations and other - 1 - 11 12 - - - 1 1

Total within continuing operations 93 39 73 191 396 108 55 63 128 354 Total within discontinued operations - 23 116 - 139 17 - - (3) 14

Total UTC 93 62 189 191 535 125 55 63 125 368

(b) Q2 2014: Approximately $60 million charge to adjust the fair value of a Pratt & Whitney joint venture investment.(c) Q2 2014: Approximately $22 million charge for impairment of assets related to a joint venture.

(e) Q2 1014: Approximately $28 million charge for the impairment of a Sikorsky joint venture investment.(f) Q2 2014: Approximately $220 million gain on an agreement with a state taxing authority for the monetization of tax credits.

related to the disposition of the Hamilton Sundstrand Industrials (i) Q3 2014: Approximately $30 million net gain from UTC Climate, Controls & Security's ongoing portfolio transformation, primarily due to a gain on the sale of an interest in a joint venture in North America.

(j) Q3 2014: Approximately $83 million net gain, primarily as a result of fair value adjustments related to a business acquisition.

(p) Q4 2014: Approximately $180 million favorable tax adjustment primarily associated with management’s decision to repatriate additional high taxed dividends in 2014.

(s) Q3 2015: Approximately $68 million of tax provision related to the undistributed earnings of Sikorsky's foreign subsidiaries, which will no longer be permanently reinvested as a result of the announced sale of Sikorsky to Lockheed Martin Corp.

(u) Q4 2015: Approximately $867 million charge related to a Pratt & Whitney research and development support agreements with Canadian government agencies.(v) Q4 2015: Approximately $142 million to record in sales and $80 million in losses from Pratt & Whitney customer contract renegotiations.(w) Q4 2015: Approximately $210 million to record in sales and $295 million in losses from UTC Aerospace Systems customer contract renegotiations.

(d) Q2 2014: A cumulative adjustment to record $830 million in sales and $438 million in losses based upon the change in estimate required for the contractual amendments signed with the Canadian Government on theMaritime Helicopter program.

(o) Q4 2014: Approximately $267 million of unfavorable income tax accruals related to the ongoing dispute with German tax authorities concerning a 1998 reorganization of the corporate structure of Otis operations in Germany.

(r) Q2 2015: Approximately $28 million of transaction and separation costs related to the planned sale or spin-off of Sikorsky.

2015

(aa) Q4 2015: Approximately $274 million of unfavorable income tax accruals related to the repatriation of foreign earnings.(bb) Q4 2015: Approximately $69 million of unfavorable income tax accruals related to a change in tax laws.

(n) Q4 2014: Approximately $88 million of favorable pre-tax interest adjustments, primarily related to conclusion of litigation and the resolution of disputes with the Appeals Division of the IRS regarding Goodrich Corporation’s

(g) Q2 2014: Approximately $21 million of favorable pre-tax interest adjustments, primarily related to the conclusion of the IRS's examination of the Company's 2009 and 2010 tax years.(h) Q2 2014: Approximately $253 million of favorable income tax adjustments related to the conclusion of the IRS's examination of the Company's 2009 and 2010 tax years, as well as the settlement of state income taxes

(k) Q3 2014: Approximately $23 million of favorable pre-tax interest adjustments, primarily related to the resolution of disputes with the Appeals Division of the IRS for the Company's 2006 - 2008 tax years.

(m) Q4 2014: Approximately $143 million of unfavorable pre-tax interest accruals related to the ongoing dispute with German tax authorities concerning a 1998 reorganization of the corporate structure of Otis operations in Germany.

(l) Q3 2014: Approximately $118 million of favorable income tax adjustments, primarily related to the resolution of disputes with the Appeals Division of the IRS for the Company's 2006 - 2008 tax years.

(y) Q4 2015: Approximately $237 million charge for pending and future asbestos-related claims.(z) Q4 2015: Approximately $27 million charge from agreement with a state taxing authority for monetization of tax credits.

(t) Q4 2015: Approximately $5 million charge related to UTC Climate, Controls & Security acquisitions and integration costs.

(x) Q4 2015: Approximately $61 million charge to UTC Aerospace Systems for impairment of assets held for sale.

2000 to 2010 tax years.

(q) Q1 2015: Approximately $126 million gain as a result of a fair value adjustment related to the acquisition of a controlling interest in a UTC Climate, Controls & Security joint venture investment.

Climate, Controls & Security Financials

*afx is at actual FX**cfx is at constant FX

CCS Sales & Operating Profit

2013 2014 2015Sales @ afx* 16.8 16.8 16.7 Op profit @ afx 2.6 2.9 2.9

Sales @ cfx** 15.3 15.5 16.4 Op profit @ cfx 2.4 2.7 2.9

Otis Financials

*afx is at actual FX**cfx is at constant FX

Otis Sales & Operating Profit

2013 2014 2015Sales @ afx* 12.5 13.0 12.0 Op profit @ afx 2.7 2.7 2.4

Sales @ cfx** 10.7 11.4 11.6 Op profit @ cfx 2.3 2.4 2.3