Embed Size (px)

Citation preview

DISPUT E S & INVES TI GATI O N S • ECONOM I C S • F INA N CI A L ADVIS O RY • MANAGE M E N T CONSU LT I NG

©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy.

December 9, 2010

US Natural Gas – A Responsible Choice

National Conference of State Legislatures – Fall Forum

Task Force on Energy Supply

Biltmore Hotel, Phoenix, Arizona

1©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy. E N E R G Y

Important Notice

This presentation was prepared by Navigant Consulting, Inc. exclusively for the benefit and internal use

of the National Conference of State Legislatures (NCSL) at its Fall Forum on December 8-10, 2010. The

presentation is intended for the use of NCSL and its members and no part of it may be circulated,

quoted, or reproduced for distribution outside these organization(s) without prior written approval from

Navigant Consulting, Inc. This presentation is incomplete without reference to, and should be viewed

solely in conjunction with the oral briefing provided by Navigant Consulting, Inc.

December 9, 2010

©2010 Navigant Consulting, Inc. All rights reserved. Navigant Consulting is not a certified public accounting firm and does not provide audit, attest, or public

accounting services. See www.navigantconsulting.com/licensing for a complete listing of private investigator licenses. Investment banking, private placement,

merger, acquisition and divestiture services offered through Navigant Capital Advisors, LLC., Member FINRA/SIPC.

2©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy. E N E R G Y

NCI’s Geographical Presence

SacramentoSan Francisco

Los Angeles

Phoenix

Dallas

Austin

Houston

Nashville

Atlanta

Tampa

Chicago

Toronto Burlington

Boston

Westbury

LawrencevillePhiladelphia

Pittsburgh

ViennaReston

Denver

Detroit

Seattle

Palo Alto

Minneapolis

New York

St. Louis

Fairfield

Ottawa

Irvine

Miami

Rochester

PragueLondon

Hong Kong

ShanghaiBeijing

Washington, DC

Legend

Office includes Energy PracticeOffice includes other practices

Baltimore

Montreal

Quebec City

3©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy. E N E R G Y

2

• Publicly traded since 1996 (NYSE: NCI)

• Over 1,800 consultants in 40 offices globally

• 2007 revenues of $767 million

• 2008 revenues of $810 million

• 2009 revenues of $707 million

• Revenue 6 year CAGR of 21 Percent

North American Dispute & Investigative Services

North American Business Consulting

International Consulting

Economic Consulting

Fraud, Forensic & Accounting Investigations

Commercial Litigation

International Arbitration

Electronic Discovery

Government Contracting

Construction Disputes

Energy

Healthcare

Financial Services

Insurance & Claims

Corporate Finance

Infrastructure Disputes

Financial Services

Public Services

Insurance

International Arbitration

Antitrust

Securities

Labor

Valuation and M&A

Forensic & Accounting Investigations

Commercial Lit / Intellectual Property

Navigant Consulting, Inc. is a Specialized Consulting Firm

4©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy. E N E R G Y

It’s Plain Remarkable – U.S. Natural Gas Production Today is at its Highest Levels Since the 1970’s

0.0

3.0

6.0

9.0

12.0

15.0

18.0

21.0

24.0

1974 1979 1984 1989 1994 1999 2004 2009

Tcf/

year

U.S. Dry Natural Gas Production

Sources: NCI/EIA

1974 - 20.7 Tcf

Dry Gas Production

5©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy. E N E R G Y

» Industry bodies such as the Natural Gas Council (INGAA, AGA, IPAA, NGSA) said major increases in demand could only be served by imports of foreign LNG or by opening up restricted drilling areas.

» Conventional wisdom was ‘we were running out of gas in North America’.

» It was asserted that without expanded drilling access and LNG, prices would surge to new highs on domestic supply deficiencies.

» And prices did increase – for awhile in the Fall of 2008, reaching $13.32 per MMBtujust before hurricanes Gustav and Ike hit in late August and in September 2008.

» But by 2009, even the Energy Information Administration had reported a 24 percent or 6.2 Bcfd average annual adjustment in deliverability of unconventional onshore gas for 2010-2030 in their Annual Energy Outlook 2009 compared to their AEO 2008.

As Recently as 2008 , Some Gas Industry Representatives Believed Supply was Limited and Would be Unable to Respond to New Gas Demand W

6©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy. E N E R G Y

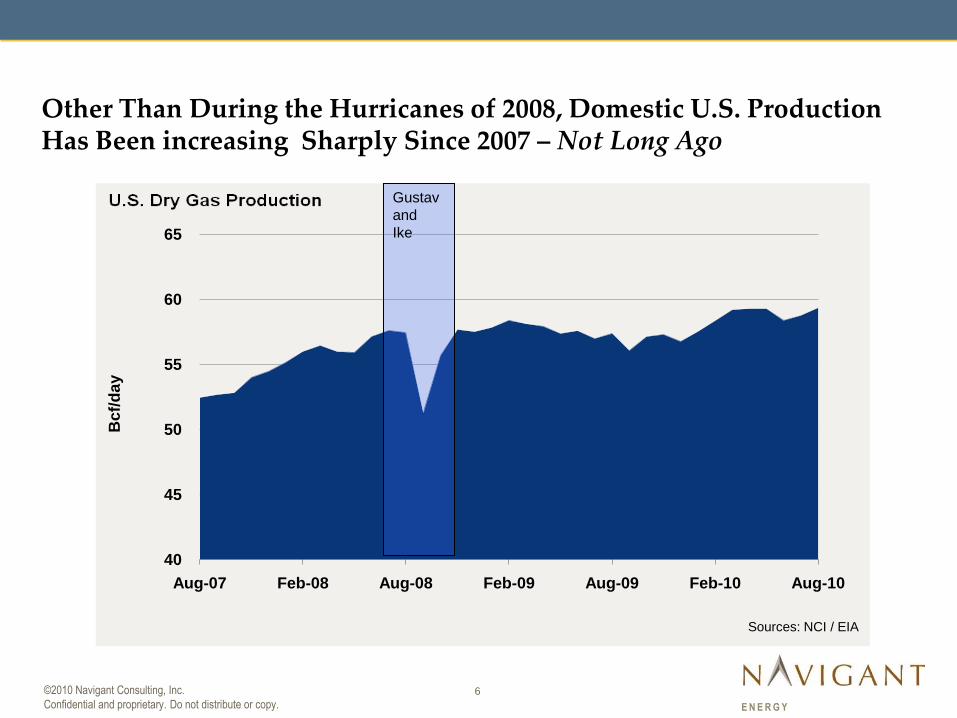

U.S. Dry Gas Production Is Still Increasing

Gustavand Ike

Other Than During the Hurricanes of 2008, Domestic U.S. Production Has Been increasing Sharply Since 2007 – Not Long Ago

40

45

50

55

60

65

Aug-07 Feb-08 Aug-08 Feb-09 Aug-09 Feb-10 Aug-10

Bcf/

da

y

Sources: NCI / EIA

Gustav

and

Ike

7©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy. E N E R G Y

In Navigant’s North American Natural Gas Supply Assessment In 2008, We Indicated What Was to Come

Page 7

8©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy. E N E R G Y

Proved Reserves Plus Assessed Resources—Life of the Gas Resource

» In 2006 the Potential Gas Committee (PGC) gas resource estimate was reported at 1,530 Tcf, inclusiveof about 137 Tcf of shale gas. At that year’s U.S. Production Rate, this was 82 years’ worth of gassupply.

» In 2008, Navigant performed the North American Natural Gas Supply Assessment for the AmericanClean Skies Foundation. This study concentrated on shale gas as evaluated according to producerreports collected by Navigant. The resulting total supply estimate was 2,247 Tcf, including 842 Tcf ofshale gas. This would have been 118 years of production at 2007 levels.

» Then in June 2009, PGC issued its updated study that essentially confirmed the NCI ACSF study.

U.S. Total Gas Supply (Tcf)

82 years at

2006 Prod. Rate

88 years at

2007 Prod. Rate

118 years at

2007 Prod. Rate

-

500

1,000

1,500

2,000

2,500

PGC 2006 Mean

Assessment

NCI 2008 Study

Based on Producer

Reports

PGC 2008 Estimate

Released June 2009

tcf

Shale

Resource

All Other

Technically

Recoverable

Resource

9©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy. E N E R G Y

Production from Six Major Shale Plays

Bcf/day, 1998- 2008

0.00

1.00

2.00

3.00

4.00

5.00

6.00

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Bcf

/Day

Bakken

Haynesville

Antrim

Woodford

Fayetteville

Barnett

As Determined in the Navigant Study in July 2008 – A Paradigm Shift Had Occurred

The Accelerating Run-Up in Shale Production—An Exponential Curve

It’s a 2.9-Power Exponential

Sources: Lippman Consulting, Inc. Production Database, Michigan Public Service Commission,

Arkansas Oil and Gas Commission and NCI Calculations.

10©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy. E N E R G Y

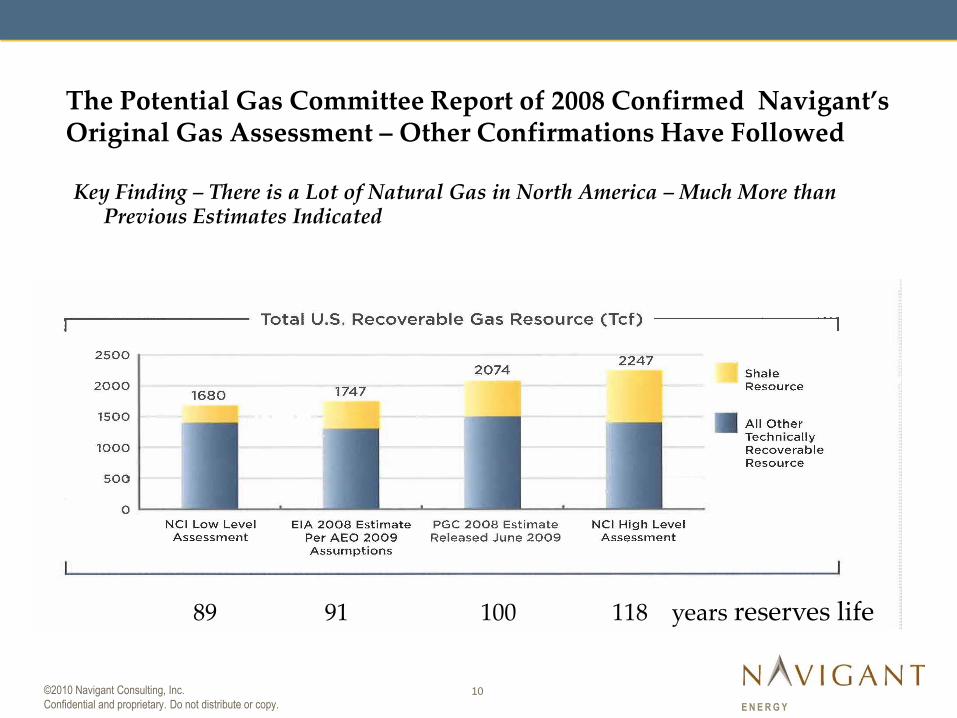

The Potential Gas Committee Report of 2008 Confirmed Navigant’s Original Gas Assessment – Other Confirmations Have Followed

Key Finding – There is a Lot of Natural Gas in North America – Much More than Previous Estimates Indicated

89 91 100 118 years reserves life

11©2010 Navigant Consulting, Inc.

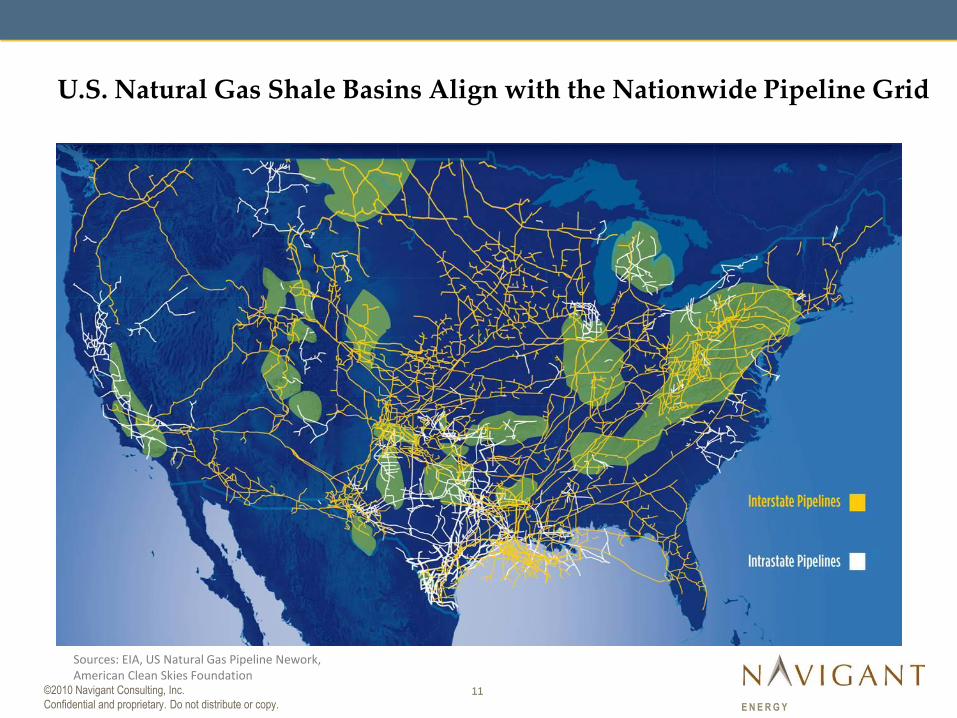

Confidential and proprietary. Do not distribute or copy. E N E R G Y

Sources: EIA, US Natural Gas Pipeline Nework, American Clean Skies Foundation

U.S. Natural Gas Shale Basins Align with the Nationwide Pipeline Grid

12©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy. E N E R G Y

40.00

42.00

44.00

46.00

48.00

50.00

52.00

54.00

56.00

58.00

60.00

Bc

f p

er

Da

y, d

ry

U.S. Dry Gas ProductionSource: EIA Data, Adjusted to Net Dry

KatrinaandRita

GustavandIke

Pre-Katrina Average

July 08

U.S. Gas Supply Increased To Record Levels

Onshore Production By Mid 2008 Was as High as Total Production in 2005

13©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy. E N E R G Y

600

800

1,000

1,200

1,400

1,600

2003 2004 2005 2006 2007 2008 2009 2010

Rigs

Sources: NCI/Baker Hughes

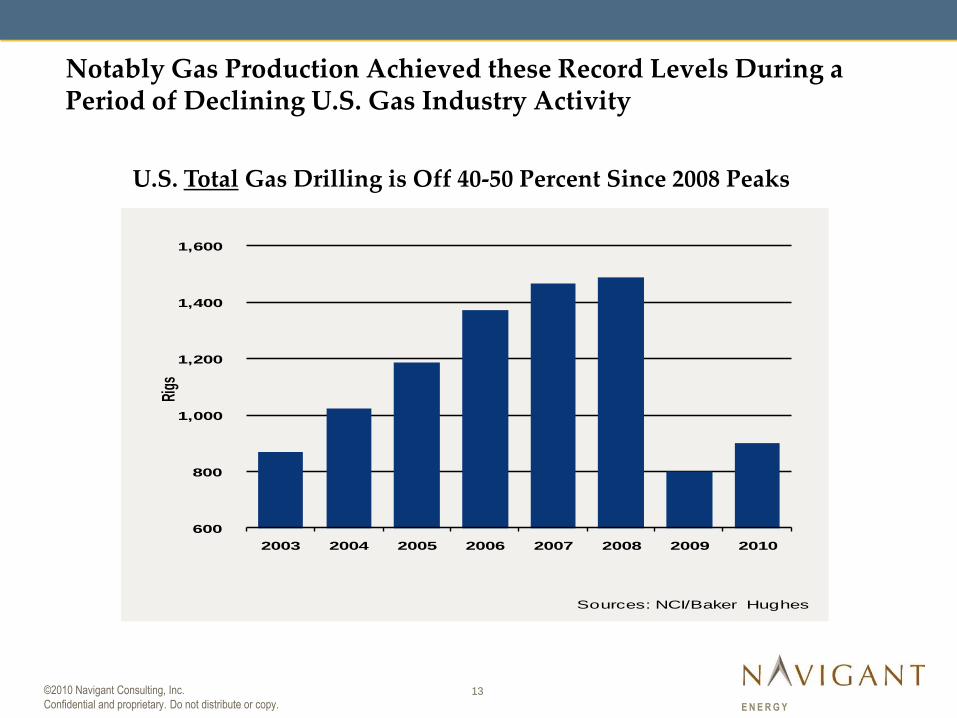

Notably Gas Production Achieved these Record Levels During a Period of Declining U.S. Gas Industry Activity

U.S. Total Gas Drilling is Off 40-50 Percent Since 2008 Peaks

14©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy. E N E R G Y

0

200

400

600

800

Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep

Rig

s

Horizontal Vertical

Sources: NCI / Smith Bits

Horizontal Drilling Activity Has Increased Over Last Year - up 78 Percent YOR

Why Then Hasn’t Production Fallen?

15©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy. E N E R G Y

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

1/4/

2008

3/4/

2008

5/4/

2008

7/4/

2008

9/4/

2008

11/4

/200

8

1/4/

2009

3/4/

2009

5/4/

2009

7/4/

2009

9/4/

2009

11/4

/200

9

1/4/

2010

3/4/

2010

5/4/

2010

7/4/

2010

9/4/

2010

US Gas Rig Count

HORZ. TOTALNCI/Smith Bits

Production is Up As Total Gas Drilling Has Declined –However, Horizontal Drilling has Been Steadily Increasing

16©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy. E N E R G Y

Horizontal Drilling Allowed 4th Q 2009 Shale Avg. Production to Top 10 Bcf Per Day - First Time

620 597 568 561 540 422 407 496 490 482 487 487 492 506 553 588 594 600 696 790 92995 118 221 372 607 839 1,058

1,4132,081

2,7183,174

3,7374,319

4,8435,400

5,9716,529

7,033 7,197 7,0377,355

57

78

77

73

74

77

85

99

137

280

533

9801,549

2,329

51 50 52 5349 56

64

78

86

95

104

100

107

116

132

148

153

164

178

195

204

10 9 7 77 7

5

5

5

7

6

6

6

6

7

7

8

8

7

8

8

0

2,000

4,000

6,000

8,000

10,000

12,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 1st Qtr. 2007

2nd Qtr. 2007

3rd Qtr. 2007

4th Qtr. 2007

1st Qtr. 2008

2nd Qtr. 2008

3rd Qtr. 2008

4th Qtr. 2008

1st Qtr. 2009

2nd Qtr. 2009

3rd Qtr. 2009

4th Qtr. 2009

MM

cf/d

@ 1

4.73

Lower 48 States ShaleRegional Gas Production

Eastern U.S. Mid-Continent Gulf Coast Onshore

Rocky Mountain San Juan Basin

Source: Lippman Consulting

17©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy. E N E R G Y

By August 2010 Shale Production was Up Again to Over 12 Bcf Per Day

By August 2010, Shale Production is Up Again to Over 12 Bcf Per Day

0

2,000

4,000

6,000

8,000

10,000

12,000

14,0001

99

8

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

YT

D 2

01

0

MM

cfd

Lower 48 States Shale Production

Sources:NCI/ LCI

18©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy. E N E R G Y

Source: ‚The Future of Natural Gas, Massachusetts Institute of Technology, 2010

A Recent Study by MIT Shows Shale Production Increasing Through 2030

19©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy. E N E R G Y

Within the Six Largest Shale Plays, the Marcellus and Haynesville Gas Shale Plays are Starting to Come On Strong

0

2

4

6

8

10

12

14

Jul-09 Sep-09 Nov-09 Jan-10 Mar-10 May-10 Jul-10

Bcf/

da

y

Eagleford Woodford Marcellus

Fayetteville Haynesville Barnett Shale Sources: NCI / LCI

US Shale Production

20©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy. E N E R G Y

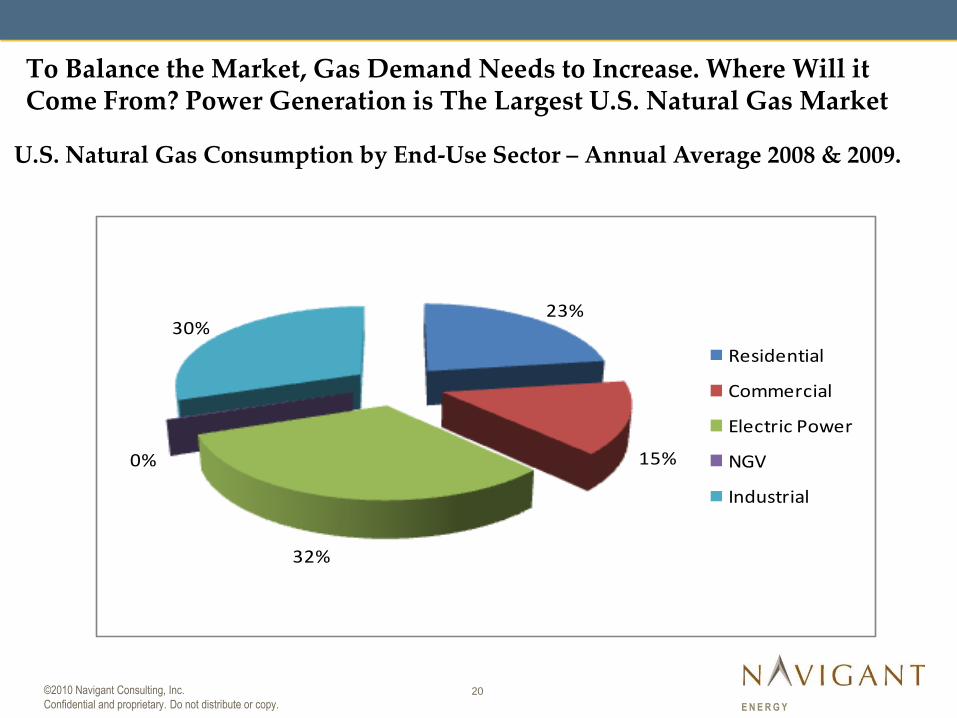

23%

15%

32%

0%

30%

Residential

Commercial

Electric Power

NGV

Industrial

To Balance the Market, Gas Demand Needs to Increase. Where Will it Come From? Power Generation is The Largest U.S. Natural Gas Market

U.S. Natural Gas Consumption by End-Use Sector – Annual Average 2008 & 2009.

21©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy. E N E R G Y

Total United States Electric Nameplate Generation Capacity, 2008

Natural Gas Represents The U.S.’s Largest Source of Generation Capacityat a 41 Percent Market Share – Larger than Coal by 11 Percent

EIA Electric Power Annual 2008, Released Jan 2010.Calculated in MW

Gas 41.16%

Coal 30.54%

Nuclear 9.61%

Wind 2.26%

Hydro 7.04%

Solar 0.02%

Other 9.34%

22©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy. E N E R G Y

Actual Coal Generation is 47 Percent of U.S. Total Generation – Actual Gas Generation is Only 21 Percent of U.S. Total Generation - Though Gas Makes up 41 Percent of Generation Capacity

Gas 20.80%

Coal 46.77%

Nuclear 18.99%

Wind 1.30%

Hydro 6.00%

Solar 0.02%

Other 6.11%

U.S. Actual Generation is Very Different

EIA Electric Power Annual 2008, Released Jan 2010.Net generation in ‘000 MWhr

23©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy. E N E R G Y

The Electric Generation Sector Is a Bit More Complicated

» More than one-half of U.S. Gas fired-electric generation is generated by peaking facilities that operate at extremely low capacity factors and high heat rates.

» Combined cycle generation and coal generation is a more relevant comparison when examining U.S. electric generation and capacity.

2009 U.S. Total Generation and Capacity for Gas, Coal and Other

Capacity Pct. of Total Generation Pct. Of Capacity Heat Rate

MW Capacity 1,000 MWh Total Gen. Factor Btu/kWh

Other Gas 202,335 20% 175,217 4% 10% 10,011

Combined Cycle 196,175 19% 745,161 19% 43% 7,423

Coal Generation 312,887 31% 1,764,486 45% 64% 10,386

Other Generation 302,044 30% 1,268,247 32% 48% -

US Total 2009 1,013,441 100% 3,953,111 100% 45% -

U.S. Generation Deserves Closer Scrutiny

24©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy. E N E R G Y

»Gas market demand— is like a manufacturing business, if the market doesn’t want it, it won’t be produced.

»Price — what will it take? Probably around $5 to $6 with wide variability across basins and operators, although the economics are a moving target – with price levels still trending down on efficiencies.

»Meanwhile, shale development requires hydraulic fracturing of the extremely tight formations.

– Concerns about high-pressure fracturing are causing legal/legislative/public uncertainty at both Federal and State levels.

– The industry must quiet these concerns through a combination of effective communication and embracing of ‘best practices’.

– The more forward-thinking producers are already doing both – such as Range Resources announcing a ‘voluntary disclosure initiative of Marcellus Shale hydraulic fracturing additives’ on a per well basis on July 14, 2010.

»Air-quality issues also have been raised as well around the Barnett development in Texas.

»Then on top of all that there’s tax policy – State and Federal. All jurisdictions want a share!

»In short, full, rapid development of gas supply has to clear some hurdles.

Opportunities in the Midst of Challenges

25©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy. E N E R G Y

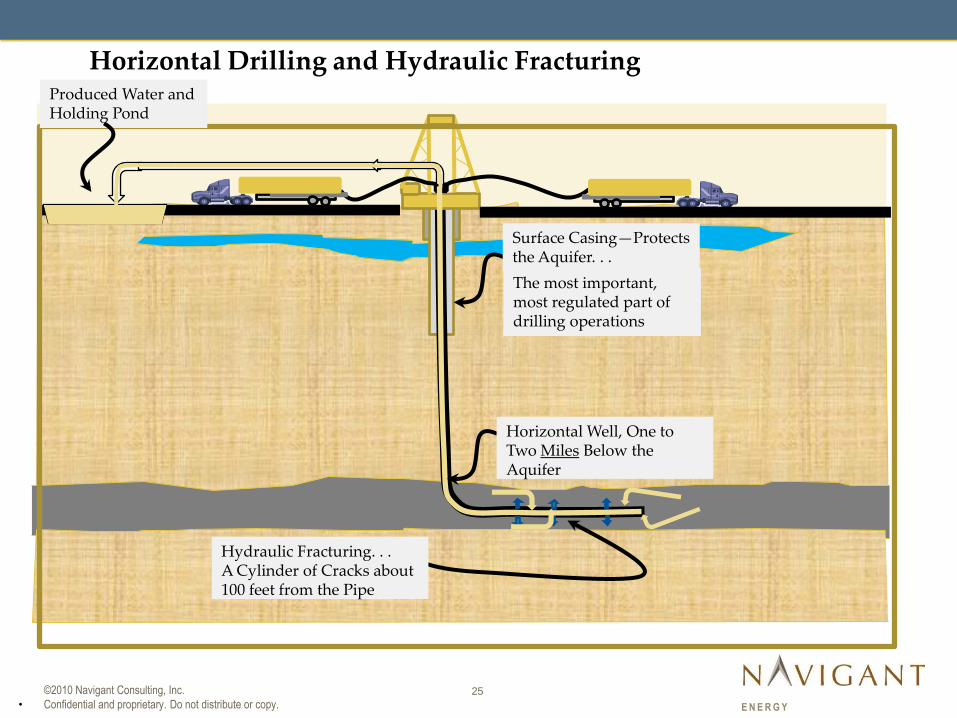

Surface Casing—Protects the Aquifer. . .

The most important, most regulated part of drilling operations

Horizontal Well, One to Two Miles Below the Aquifer

Hydraulic Fracturing. . .A Cylinder of Cracks about 100 feet from the Pipe

.

Produced Water and Holding Pond

Horizontal Drilling and Hydraulic Fracturing

26©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy. E N E R G Y

What New Technology Allows This to Work

» Advanced drilling and completion technologies consist primarily of horizontal drilling and multiple-stage hydraulic fracturing stimulation.

» Horizontal drilling also provides a reduced surface footprint by drilling multiple wells (6-10 sometimes) from a single surface location.

» 90 percent of oil and gas wells now require use of hydraulic fracturing allowing more energy from fewer wells.

» Bridge plugs confine hydraulic fracturing to specific horizontal depths or stages to allow better control of fracturing pressures and patterns.

» Fracturing fluids are at least 98 percent sand and water and other additives - many found in common consumer products.

» Calls for transparency of fracturing fluid content is currently resisted by some industry participants for competitive reasons.

» The compounds are injected into deep shale gas formations and are typically confined by many thousands of feet of rock layers – sometimes two miles or more.

» Industry adoption of ‘best practices’ is becoming more widely accepted in order to prevent against sloppy drilling practices and in seeing the ‘writing on the wall’ otherwise.

27©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy. E N E R G Y

» The development does not take government hand-outs.

» Unlike oil, it does not take expanded land or offshore access.

» And it will provide for less foreign energy dependence - at prices that serve as a economic advantage for the U.S. economy in the world market.

» An important facet of continued development of natural gas is support for natural gas Demand at a stable price and an endorsement through a positive political and policy statement of the role of natural gas can play ‘at least as a bridge‛ in setting the energy standard for electric generation as a means to clean and sustainable energy independence.

» This in recognition of the importance of natural gas in a carbon-constrained world to substantially lower GHG emissions – often at lower costs.

» Without ‘next generation’ gas power plants that have the potential to operate more efficiently with zero emissions and at even lower costs.

In Sum, The Potential for Natural Gas Supply is SubstantialSo, The Potential for Natural Gas Supply is Substantial

28©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy. E N E R G Y

Increased Gas-Fired Electric Generation Can Make a Significant DifferenceAs Shown Facts Say:

» Gas Combined-Cycle generation operating at a 43 percent capacity factor generated 19 percent of U.S. actual electric generation in 2009 (EIA).

» Coal operating at an 64 percent capacity factor generated 45 percent of actual U.S. electric generation in 2009 (EIA).

Which suggest:

» To generate the same amount of power with equal capacity factors, both Gas Combined Cycle and coal would operate at a 56.3 percent capacity factor - shifting 509,662 GWh from coal to gas.

» This shift of generation would require incremental gas demand of 10.3 Bcf per day, 17 percent of existing gas demand of 60.2 Bcfd – a meaningful yet seemingly achievable volume.

-----------------------------------------------------------------

Remember – Gas Combined Cycles emit only 39 percent as much CO2 as coal plants.

» The annual savings in CO2 emissions would be approximately 316 million metric tonnes, or a 15 percent reduction from the 2009 level of CO2 emissions from combined coal and gas fossil fuel electric generation - a significant positive contributor to climate change

All by simply raising Gas Combined-Cycle capacity factors by only 13 percent (43% to 56%)

GOOD NEWS - This shift in generation capacity coal to gas – is already happening!!

29©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy. E N E R G Y

» Low gas prices continue to support coal-to-gas substitution as they have for major portions of the last two years.

» Efficient combined-cycle gas-fired powergen is competitive now with coal in certain areas.

» Gas fired power plants are favored on lower capital costs and shorter lead times and lower emissions.

» Climate change legislation in the future will promote additional gas-fired generation over coal generation.

It Appears Prices have Supported Switching for Some time – 2 Years

History Is Already Telling Us

Appalachian Coal Prices Have Been Higher than Gas PricesSince Mid-2008

30©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy. E N E R G Y

Appalachian Gas vs. Delivered Coal Futures Indicate Gas is Going to be Cheaper than Coal Through 2013

Expectations are that Gas Prices will be Below Coal in the Future

31©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy. E N E R G Y

Summary

» The key impacts of the ‘game changing’ that has occurred in the gas industry over the last few years are hard to ignore:

— A transformation of the country from gas shortage to abundance;

— Provision for less foreign energy dependence;

— Provision for a foundation for a low-carbon and cleaner energy environment of the future; and

— Stage setting for competitive gas prices as a competitive advantage for the US economy in the global market.

» The key now is to overcome challenges – some as to the perception of what gas shale development is and as to its risks.

» As gas shale has become headline making, the need for education and communication becomes critical.

» Regulatory policy will also be important to assure ‘best-practices’ are pursued by the producing industry while at the same time fostering the orderly development of this key energy resource that has crossed over to the center of debate of energy, security and climate issues – in other words for the good of the country!

KeyC O N T A C T S

©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy.

KeyC O N T A C T S

©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy.

KeyC O N T A C T S

©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy.

KeyC O N T A C T S

©2010 Navigant Consulting, Inc.

Confidential and proprietary. Do not distribute or copy.32

E N E R G Y

Gordon PickeringDirector, EnergyRancho Cordova, CA 95670 [email protected]