Embed Size (px)

Citation preview

2

U.S. M&A Quarterly Insights

Executive Summary

This report, created by the BMO Capital Markets Mergers & Acquisitions team, provides an update on selected key trends that we are observing in the public M&A markets.

1. The premium in this document is defined as a five day premium. BMO analyzed one day as well as thirty day volume weighted average prices, both of which yielded similar trends.

2. YTD2018 and ‘18 YTD in this document is defined as through July 31, 2018.

Seth Prostic

Managing DirectorCo-Head of U.S. Mergers & Acquisitions

Are acquisition premiums, which are at a historically low level during this active M&A market, approaching a new normal?

When we visit with clients we frequently hear how surprised

they are at the high EBITDA multiples buyers have continued to

pay for businesses over the past 18 months. While the M&A

market remains robust in terms of transaction multiples, many

are surprised to hear about the dramatic compression of stock

price premiums buyers have been paying recently to acquire

public companies. While stocks of acquired companies, on

average, have consistently traded at roughly 80-85% of their

respective 52-week high prior to acquisition during the stock

market’s bull run over the past nine years, acquisition premiums

continue to decrease. The median five day acquisition premium1

for public companies this year2, at 21%, is the lowest we have

observed since 2004 – and median purchase premiums for

transactions larger than US$500 million are now in the 15% -

20% range. We expect acquisition premiums to remain near

historically low levels as long as the equity markets continue to

trade near all-time highs.

We look forward to your reactions to the BMO M&A team’s

thoughts and analysis of market trends in the enclosed report.

“We expect acquisition

premiums to remain

near historically low

levels as long as the

equity markets continue

to trade near all-time

highs.”

3

U.S. M&A Quarterly Insights

2018 Remains an Active Year

Median acquisition premium for larger than $500MM transactions

‘18 YTD

15-20%

21%Median acquisition premium in ’18 YTD

approaching a 15-year low

26%Median acquisition premium for sub

$500MM transactions

3%Median 3-year historical revenue growth rate of

publicly acquired companies in ‘18 YTD

18%Median NTM EBITDA growth rate of publicly acquired companies in

‘18 YTD

4.9xDifference between

median LTM EBITDA multiple of largest

quartile of transactions (~14x) and smallest

quartile of transactions (~9x)

~40%Median market

premiums during the Great Recession

~3,500 Days

Length of current bull market, longest

in U.S. history

7.3x‘18 YTD bottom

quartile LTM EBITDA multiple of publicly

acquired companies

3.5xIncrease in median LTM

EBITDA multiple paid by sponsors for publicly

acquired companies over the last 3 years

Current median LTM EBITDA transaction

multiple, slightly lower than the median statistic of 13.4x

in ‘17

12.8x

23.3x‘18 YTD top quartile

LTM EBITDA multiple of publicly acquired

companies

4

U.S. M&A Quarterly Insights

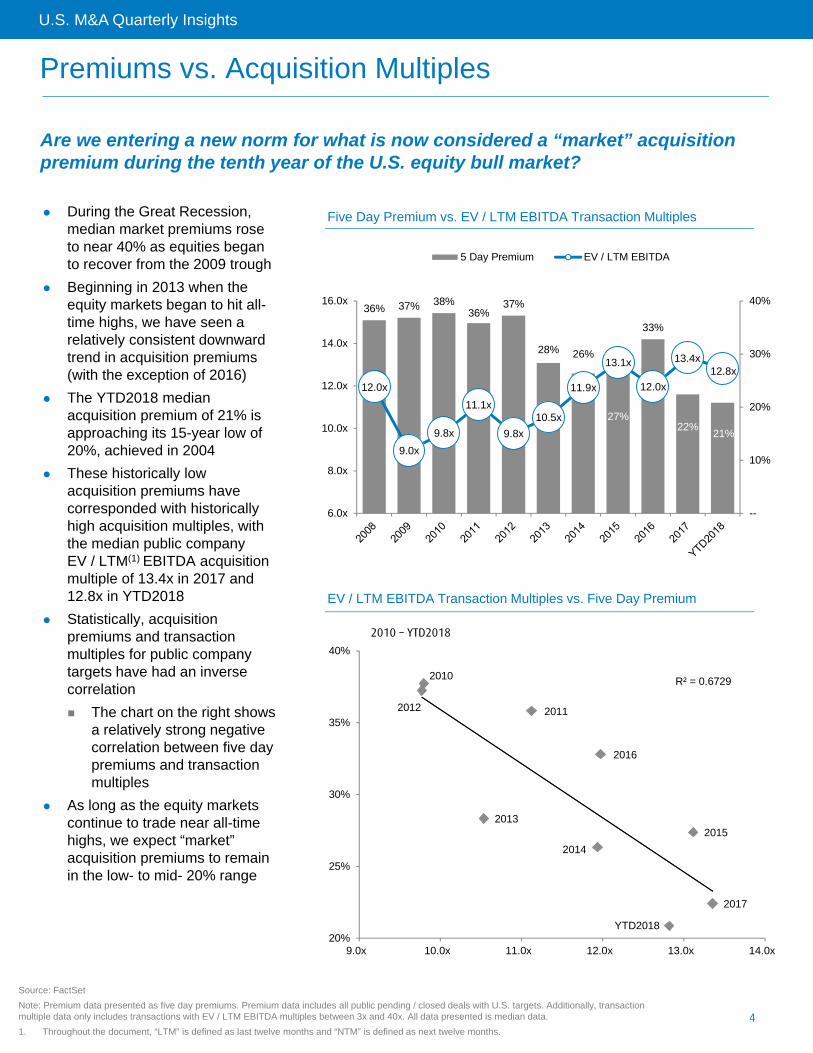

Premiums vs. Acquisition Multiples

During the Great Recession, median market premiums rose to near 40% as equities began to recover from the 2009 trough

Beginning in 2013 when the equity markets began to hit all-time highs, we have seen a relatively consistent downward trend in acquisition premiums (with the exception of 2016)

The YTD2018 median acquisition premium of 21% is approaching its 15-year low of 20%, achieved in 2004

These historically low acquisition premiums have corresponded with historically high acquisition multiples, with the median public company EV / LTM(1) EBITDA acquisition multiple of 13.4x in 2017 and 12.8x in YTD2018

Statistically, acquisition premiums and transaction multiples for public company targets have had an inverse correlation

The chart on the right shows a relatively strong negative correlation between five day premiums and transaction multiples

As long as the equity markets continue to trade near all-time highs, we expect “market” acquisition premiums to remain in the low- to mid- 20% range

2010

20112012

2013

2014

2015

2016

2017

YTD2018

R² = 0.6729

20%

25%

30%

35%

40%

9.0x 10.0x 11.0x 12.0x 13.0x 14.0x

36% 37% 38%36%

37%

28% 26%

27%

33%

22%21%

12.0x

9.0x

9.8x

11.1x

9.8x

10.5x

11.9x

13.1x

12.0x

13.4x 12.8x

--

10%

20%

30%

40%

6.0x

8.0x

10.0x

12.0x

14.0x

16.0x

5 Day Premium EV / LTM EBITDA

2010 – YTD2018

Five Day Premium vs. EV / LTM EBITDA Transaction Multiples

EV / LTM EBITDA Transaction Multiples vs. Five Day Premium

Source: FactSet

Note: Premium data presented as five day premiums. Premium data includes all public pending / closed deals with U.S. targets. Additionally, transaction multiple data only includes transactions with EV / LTM EBITDA multiples between 3x and 40x. All data presented is median data.

1. Throughout the document, “LTM” is defined as last twelve months and “NTM” is defined as next twelve months.

Are we entering a new norm for what is now considered a “market” acquisition premium during the tenth year of the U.S. equity bull market?

5

U.S. M&A Quarterly Insights

Premiums by Size of Acquisition

10%

15%

20%

25%

30%

35%

40%

45%

50%

<$500mm $500mm-$1,000mm

$1,001mm-$5,000mm >$5,000mm

Larger companies ($500mm+ transaction values) have received 15-20% premiums in 2017 – YTD2018

Smaller company (<$500mm transaction values) premiums continue to be meaningfully higher than those of larger deals

At 26%, the smaller company premium is at its lowest level since 2006

Over the past two years, there has been a noticeable convergence of premium percentages for transactions larger than $500mm

Median Premium by Transaction Value

Source: FactSetNote: Premium data presented as five day premiums. Premium data includes all public pending / closed deals with U.S. targets.

6

U.S. M&A Quarterly Insights

Percentage of 52-Week High Analysis

Source: FactSetNote: Premium data presented as five day premiums. Premium data includes all public pending / closed deals with U.S. targets.

83%

88%

62% 64%

83% 81% 79%

88% 87% 83% 80%

87% 85%

24% 24%

36% 37% 38% 36% 37%

28% 26% 27%

33%

22% 21%

--

20%

40%

60%

80%

100%% of 52 Week High 5 Day Premium

Since the onset of the bull market in late 2009, equities of publicly traded acquired companies have consistently been trading around 80-85% of 52-week highs just prior to announcement of acquisition

Although the equity markets have traded near 52-week highs for much of this decade, premiums have continued to compress, as buyers have been less willing to pay fulsome premiums on top of high underlying trading multiples

Target boards and selling shareholders have become more comfortable with accepting lower premiums given the following:

Uncertainty about the duration of the current bull market and economic expansion, which influences confidence in organic growth visibility

Focus on historically strong acquisition EBITDA multiples

Deprioritizing a high acquisition premium given the above as well as the target’s historically strong stock prices

Five Day Premium vs. % of 52-Week High

7

U.S. M&A Quarterly Insights

Historical Transaction Trending Analysis

Source: FactSetNote: Premium data includes all public pending / closed deals with U.S. targets. Additionally, transaction multiple data only includes transactions with EV / LTM EBITDA multiples between 3x and 40x. All data presented is median data.

15% 15% 15%

13%

17%

16%

16%

17%

22%

2%

1%

8%

4% 4% 3% 2% 3% 3%

9% 10%

7%

5%

9%

5% 6%

5% 5%

18%

26%

18%

14%

20%

16%

23%

17%

18%

--

5%

10%

15%

20%

25%

30%

2010 2011 2012 2013 2014 2015 2016 2017 YTD2018

LTM EBITDA Margin 3-Year Historical Revenue Growth

NTM Revenue Growth NTM EBITDA Growth

Although there has been significant multiple expansion in the broader M&A market since the Great Recession, the underlying fundamentals of these public M&A targets have not dramatically improved

As a result, acquirers on average are paying higher transaction multiples in the current M&A market for similar quality businesses as have been available in the past

Clearly, buyers are pricing risk differently in the current M&A market

Median Statistics of Publicly Acquired Companies

8

U.S. M&A Quarterly Insights

Strategic vs. Sponsor Transaction Multiples and Premiums

Source: FactSetNote: Premium data includes all public pending / closed deals with U.S. targets. Additionally, transaction multiple data only includes transactions with EV / LTM EBITDA multiples between 3x and 40x. All data presented is median data.

37

%

40

%

39

%

38

%

40

%

31

%

29

%

28%

33

%

23

%

21

% 2

8%

32

%

33%

29

%

22

%

21

%

13

% 18%

25

%

17

%

21

%

Strategic Sponsor

12.4

x

10

.7x

10

.5x

11.

4x

10

.3x

11.

3x

12

.2x

13

.3x

12

.9x

13

.8x

13.0

x

11

.1x

7.4

x

7.7

x

9.6

x

8.9

x

8.9

x

10.8

x

12

.2x

8.4

x

9.9

x 11

.9x

Strategic Sponsor

Strategic vs. Sponsor LTM Transaction Multiples

Over the past 15 years, the median acquisition multiple and acquisition premium of strategic buyers have exceeded that of sponsor buyers by ~2.5x and ~700bps, respectively

Several interesting underlying trends are apparent when comparing strategic to sponsor buyers over the past several years

YTD2018 median purchase premium is 21% for each of strategic and sponsor buyers – the last time the median sponsor premium exceeded that of the median strategic premium was in 2003

While strategic buyers have historically paid higher multiples than sponsors, they have been acquiring businesses with higher margins and growth profiles (refer to pages 9-10)

While median sponsor acquisition multiples have been increasing, median strategic multiples have remained relatively flat

Strategic vs. Sponsor Five Day Premiums

9

U.S. M&A Quarterly Insights

Financial Sponsor Acquisitions

Over the last three years, there has been a steady increase in the median transaction multiples that sponsors have paid for public company acquisitions

Based on historical analysis since 2010, there appears to be a strong correlation between the EBITDA margin of public companies acquired by financial buyers and the median EV / LTM EBITDA transaction multiple paid

Given the growth profile of the companies acquired by financial sponsors over the last few years has not dramatically changed, improving target EBITDA margins are the largest driver of the observed multiple expansion

With the decrease in sponsor underwritten returns in today’s M&A market, sponsors could be gravitating toward higher margin and more stable businesses as they seek to reduce operating risk

While growth is traditionally thought of as the largest driver of value, sponsor risk profile is changing as buyers are willing to pay premiums for higher EBITDA margin companies

In light of more modest topline growth expectations, the ability to execute on an acquisition strategy is also increasingly important to sponsors as a strategy to drive future growth

--

4%

8%

12%

16%

20%

--

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

EV / LTM EBITDA Multiple LTM EBITDA Margin

15% 16%

11%

12% 14%

18%

11%

14%

17%

2% 1%

5% 3% 3%

4% 4%

3%

4%

7% 6% 6%

3% 4%

7%

10%

5%

2%

--

5%

10%

15%

20%

2010 2011 2012 2013 2014 2015 2016 2017 YTD2018

LTM EBITDA Margin 3-Year Historical Revenue Growth

NTM Revenue Growth

Operating Metrics for Financial Sponsor Acquisitions

Multiples and Margins for Financial Sponsor Acquisitions

Source: FactSet

Note: Premium data includes all public pending / closed deals with U.S. targets. Additionally, transaction multiple data only includes transactions with EV / LTM EBITDA multiples between 3x and 40x. All data presented is median data.

10

U.S. M&A Quarterly Insights

Strategic Buyer Acquisitions

Source: FactSet

Note: Premium data includes all public pending / closed deals with U.S. targets. Additionally, transaction multiple data only includes transactions with EV / LTM EBITDA multiples between 3x and 40x. All data presented is median data.

14% 15% 16%

14%

17%

15%

17% 17%

22%

2% 0%

8%

4% 4%

3% 2% 3% 3%

11% 11%

7%

5%

11%

5% 5% 5% 5%

10.5x

11.4x

10.3x

11.3x12.2x

13.3x12.9x

13.8x13.0x

0.0x

3.0x

6.0x

9.0x

12.0x

15.0x

--

5%

10%

15%

20%

25%

30%

LTM EBITDA Margin 3-Year Historical Revenue Growth

NTM Revenue Growth EV / LTM EBITDA Multiple

Given the relatively consistent target operating profile over the last few years, we are not surprised that the median strategic buyer acquisition multiple has remained relatively constant

The most pronounced change is the rapidly increasing EBITDA margin profile in YTD2018

Interestingly, strategics are buying businesses with higher median LTM EBITDA margin and revenue growth than sponsors

Operating Metrics for Strategic Acquisitions

Operating Metric Premiums for Strategic vs. Sponsor Acquisitions

(0%) (1%)

4%

2%

4%

(3%)

7%

3%

5% 5%

4%

2%

2%

6%

(2%)

(4%)

(0%)

3%

(5%)

--

5%

10%

2010 2011 2012 2013 2014 2015 2016 2017 YTD2018

LTM EBITDA Margin NTM Revenue Growth

11

U.S. M&A Quarterly Insights

Quartile Analysis

Source: FactSet

Note: Premium data includes all public pending / closed deals with U.S. targets. Additionally, transaction multiple data only includes transactions with EV / LTM EBITDA multiples between 3x and 40x. All data presented is median data.

Bottom Quartile represents the 25% of transactions in a given year with the smallest EV / LTM EBITDA transaction multiple.

Top Quartile represents the 25% of transactions in a given year with the largest EV / LTM EBITDA transaction multiple.

12.9x 12.3x

16.4x

13.9x

15.5x 16.1x 15.7x

17.7x

16.0x

8.0x

10.0x

12.0x

14.0x

16.0x

18.0x

20.0x

2010 2011 2012 2013 2014 2015 2016 2017 YTD2018

(5%)

--

5%

10%

15%

20%

25%

2010 2011 2012 2013 2014 2015 2016 2017 YTD2018

--

5%

10%

15%

20%

25%

2010 2011 2012 2013 2014 2015 2016 2017 YTD2018

LTM EBITDA Margin 3-Year Historical Revenue Growth NTM Revenue Growth

6.3x 7.2x 5.5x 6.2x 6.6x 7.3x 6.1x 7.5x 7.3x

19.2x 19.5x 21.9x

20.1x 22.1x 23.3x

21.8x 25.2x

23.3x

--

5.0x

10.0x

15.0x

20.0x

25.0x

30.0x

2010 2011 2012 2013 2014 2015 2016 2017 YTD2018

Bottom Quartile Top Quartile Since the Great Recession, while buyers have been increasingly willing to pay greater EBITDA multiples for higher quality businesses, we’ve observed little multiple expansion in the bottom quartile of transaction multiples

The relative multiple expansion can most easily be observed by comparing the medians of the top and bottom quartiles of EV / LTM EBITDA transaction multiples

The increasing delta between these two metrics shows the divergence that is becoming quite apparent in the market

The current frothy M&A market does not apply to more challenging business profiles, where the market is not seeing an appreciable increase in valuation

While top quartile transaction multiple businesses continue to display higher quality fundamentals, there appears to be little in the historical trends to explain the divergence in transaction multiples that we are observing in the market

EV / LTM EBITDA Transaction Multiple Quartile Medians

Delta Between Top and Bottom Quartiles

Top Quartile Median

Bottom Quartile Median

12

U.S. M&A Quarterly Insights

Quartile Analysis (cont’d)

Source: FactSet

Note: Premium data includes all public pending / closed deals with U.S. targets. Additionally, transaction multiple data only includes transactions with EV / LTM EBITDA multiples between 3x and 40x. All data presented is median data.

Bottom Quartile represents the 25% of transactions in a given year with the smallest EV / LTM EBITDA transaction multiple.

Top Quartile represents the 25% of transactions in a given year with the largest EV / LTM EBITDA transaction multiple.

7%

17%

26%

16% 16% 17%

7%

14%11%

9%

4%

--

5%

10%

15%

20%

25%

30%

--

10%

20%

30%

40%

50%

60%

Bottom Quartile Top Quartile

6.0x

8.0x

10.0x

12.0x

14.0x

16.0x

Bottom Quartile Top Quartile

Buyers are placing a greater value on scaled businesses

Since the Great Recession, buyers have been willing to ascribe increasingly greater multiples to the largest quartile of companies

LTM EBITDA Multiples Based on Target Transaction Value

LTM EBITDA Delta Between Top and Bottom Quartiles

5 Day Premiums Delta Between Bottom and Top Quartiles

5 Day Premiums Based on Target Transaction Value

1.6x

2.9x

0.4x

1.6x

2.4x

1.4x

3.7x

5.2x

3.9x

1.1x

4.9x

--

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

The EBITDA multiple differential between the largest and smallest quartiles has increased to 3.8x EV / LTM EBITDA over the last five years vs. only 1.7x EV / LTM EBITDA over the preceding five year period

The expanding EBITDA multiple premium paid for top vs. bottom quartile sized targets does not translate into stock price purchase premium differential

While historically the smallest quartile businesses were acquired at significantly higher purchase premiums than largest quartile businesses, this spread has compressed to its lowest levels since the onset of the Great Recession

13

U.S. M&A Quarterly Insights

About Us: BMO Capital Markets

• As a member of BMO Financial Group (NYSE, TSX: BMO), we leverage the financial strength and capabilities of one of North America’s leading financial services organizations.

• BMO Capital Markets is a single-stop provider. Depending on your needs, you may use a combination of our capabilities, or only one. Our experience and deep sector knowledge enable us to develop the solution that fits you best.

Access to capital Initial public offerings

Debt financing

Equity financing

Private equity financing

Corporate lending

Structured & project financing

Securitization

Distribution Institutional

Equity sales & trading Fixed income sales & trading

Retail Direct brokerage Private banking

Strategy & growth Strategic advisory

Mergers & acquisitions, including cross-border opportunities

Valuations & fairness opinions

Acquisition & divestitures

Leverage buyouts

Restructurings & recapitalizations

Take-over & activism defense

Share buybacks

Joint ventures and otherpartnership models

Treasury & risk management Commodity products

Money markets

Trade finance

Cash management

Foreign exchange

Research Economics

Commodities

Debt

Corporate

Americas Europe & Middle East

AtlantaBostonCalgaryChicagoDenverHoustonMexico CityMilwaukeeMinneapolisMontrealNew YorkRio de JaneiroSan FranciscoSeattleTorontoVancouverWashington, D.C.

Abu DhabiDublinLondonParisZurich

Asia & Australia

BeijingGuangzhouHong KongMelbourneMumbaiShanghaiSingaporeTaipei

2,500+professionals

30locations

5continents

We offer a complete suite of products and services:

Note: As of July 31, 2018.

14

U.S. M&A Quarterly Insights

BMO M&A Overview and Recent Highlights

Experienced Team

Global M&A practice with ~100 M&A professionals in nine offices around the world, with ~70 M&A professionals in the U.S.

Including over 40 Managing Directors and Directors

Proven Results

US$337 billion of transaction value in 480+ deals since 2011(1)

Approach

Deep sector expertise in close alignment with BMO’s industry groups

M&A professionals partner with industry experts to drive enhanced insights and execution

Full Product Capabilities

Sell-side, buy-side and cross-border advisory

Recapitalizations and restructurings

Fairness opinions

Takeover defense

Activism defense

Leveraged and management buyouts

Strategic alternatives review

Financial Advisor

Sale of Medical Office Building portfolio to

January 2018

US$400 million

US$370 millionSale of the rights to USL261 to

Financial Advisor

June 2018

Financial Advisor

Acquisition of

December 2017

US$500 million

Financial Advisor

Acquisition ofBrocade Communications Systems,

Inc.

November 2017

US$5.9 billion

Financial Advisor

Acquisition of

Americas

May 2018

US$1.3 billion

Financial Advisor

Sale to

May 2018

US$245 million

Special Advisorto Board of Columbus

Sale to

November 2017

US$850 million

Financial Advisor

Sale to

April 2018

US$825 million

Financial Advisor

to

Pending

Financial Advisor

Acquisition of

Merchants’ Choice Payment Solutions

August 2017

US$470 million

Financial Advisor

Sale to

Subsidiary of

October 2017

On its sale of a controllinginterest in

January 2018

Financial Advisor

To a Lovell Minnick Partners – led buyer group

Financial Advisor

Sale of D+H Collateral

Management Services business to

August 2018

Portfolio Company of

Portfolio Company of

Financial Advisor

Sale to

October 2017

C$2.6 billionSale of

1. Bloomberg, completed deals where an acquirer or target is located in North America. Market data as of August 01, 2018.

15

U.S. M&A Quarterly Insights

Contacts

Rob StewartManaging DirectorCo-Head of U.S. Mergers & AcquisitionsNew York, NYTel.: (212) [email protected]

Eric NicholsonManaging DirectorHead of Middle MarketMergers & AcquisitionsMinneapolis, MNTel.: (612) [email protected]

Geoff BarskyManaging DirectorHead of Canadian & International M&AToronto, ONTel.: (416) [email protected]

Seth ProsticManaging DirectorCo-Head of U.S.Mergers & AcquisitionsChicago, IL Tel.: (312) [email protected]

Lyle WilponManaging DirectorHead of Global Advisory New York, NYTel.: (212) [email protected]

These materials are confidential and proprietary to, and may not be reproduced, disseminated or referred to, in whole or in part without the prior consent of BMO Capital Markets (“BMO”). These materials have been prepared exclusively for the BMO client or potential client to which such materials are delivered and may not be used for any purpose other than as authorized in writing by BMO. BMO assumes no responsibility for verification of the information in these materials, and no representation or warranty is made as to the accuracy or completeness of such information. BMO assumes no obligation to correct or update these materials. These materials do not contain all information that may be required to evaluate, and do not constitute a recommendation with respect to, any transaction or matter. Any recipient of these materials should conduct its own independent analysis of the matters referred to herein.

BMO Capital Markets is a trade name used by BMO Financial Group for the wholesale banking businesses of Bank of Montreal, BMO Harris Bank N.A. (member FDIC), Bank of Montreal Ireland p.l.c, and Bank of Montreal (China) Co. Ltd and the institutional broker dealer businesses of BMO Capital Markets Corp. (Member FINRA and SIPC) in the U.S., BMO Nesbitt Burns Inc. (Member Investment Industry Regulatory Organization of Canada and Member Canadian Investor Protection Fund) in Canada and Asia and BMO Capital Markets Limited (authorised and regulated by the Financial Conduct Authority) in Europe and Australia. “BMO Capital Markets” is a trademark of Bank of Montreal, used under license.

® Registered trademark of Bank of Montreal in the United States, Canada and elsewhere.

™ Trademark of Bank of Montreal in the United States and Canada.

BMO does not provide tax or legal advice. Any discussion of tax matters in these materials (i) is not intended to be used, and cannot be used or relied upon, for the purposes of avoiding any tax penalties and (ii) may have been written in connection with the “promotion or marketing” of the transaction or matter described herein. Accordingly, the recipient should seek advice based on its particular circumstances from an independent tax advisor.

18-1696MM